the hygienic laboratory at the university of iowa march 24, 2010

TRANSCRIPT

The Hygienic Laboratory

at The University of Iowa

March 24, 2010

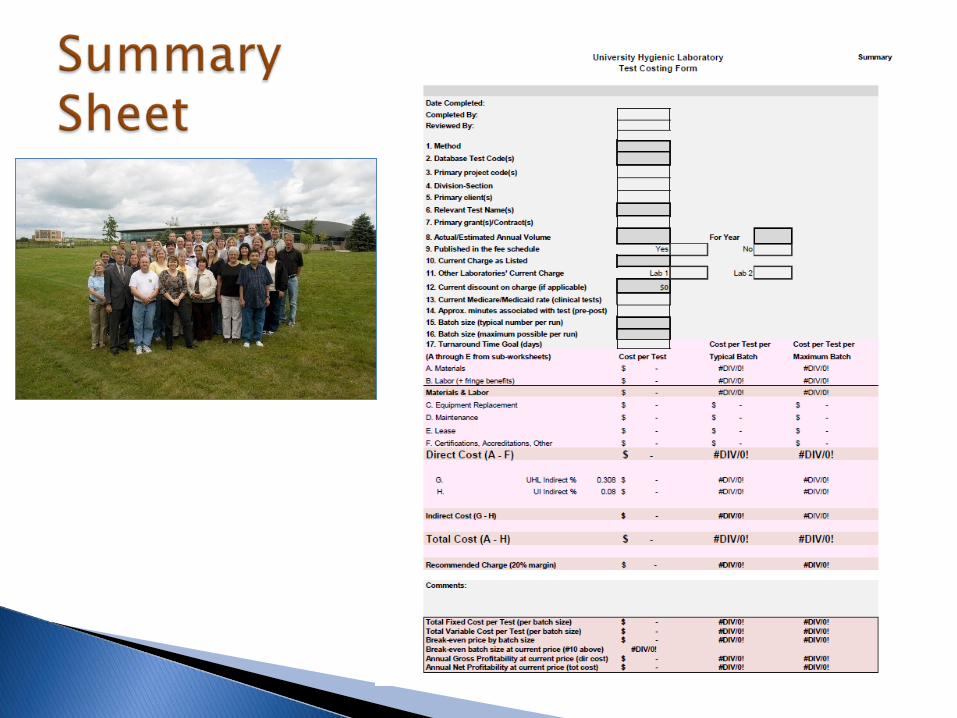

Before the Worksheet: Map the Process Save File As, Instructions for Un-protecting Sheets Summary Sheet Areas to Complete Batch vs. No Batch Advantage Examples of Batch vs. No Batch Advantage Materials Labor Instrument Replacement, Maintenance, Lease Certifications

Per run or sample:

◦ Pre Client orders test and collection kits are sent out Sample collected, received, and prepared Data entry, instrument maintenance

◦ Analytical Run test Analyze results

◦ Post Result entry and communication Client is billed

Occasional:

◦ Performance evaluations◦ Column changes◦ Method development ◦ Certifications◦ Instrument and software acquisition◦ Continuing education◦ What else?

Estimate number of occurrences and divide by approximate number of tests per interval

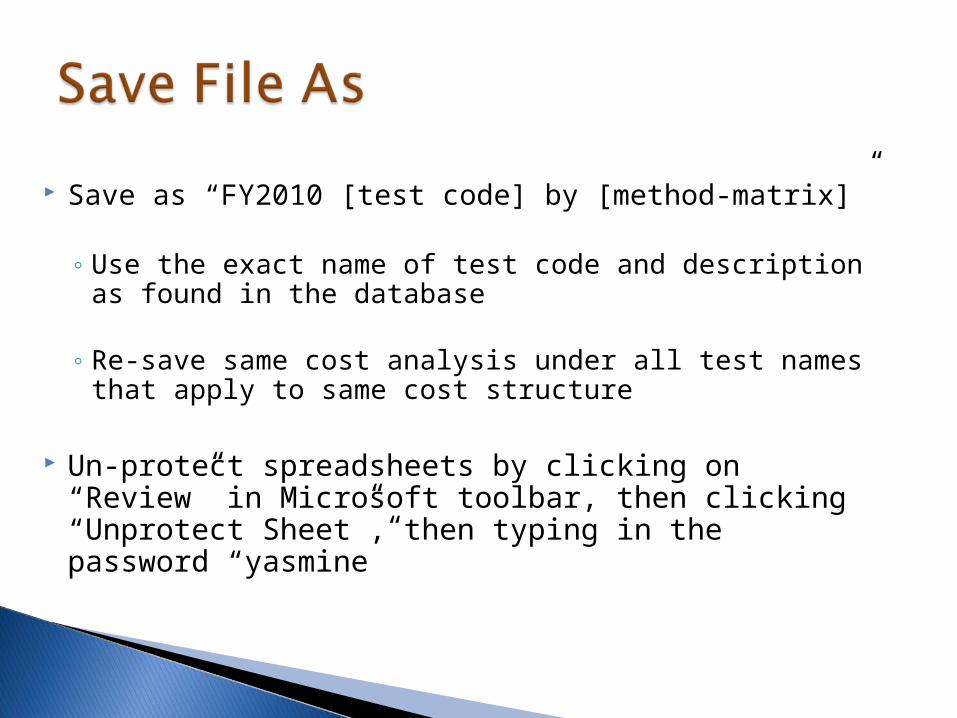

Save as “FY2010 [test code] by [method-matrix]”

◦ Use the exact name of test code and description as found in the database

◦ Re-save same cost analysis under all test names that apply to same cost structure

Un-protect spreadsheets by clicking on “Review” in Microsoft toolbar, then clicking “Unprotect Sheet”, then typing in the password “yasmine”

Fill in the gray areas on every sheet and pink areas will be calculated automatically

If any question takes longer than five minutes to figure out HOW to answer it, make an educated guess and provide comments and assumptions either in the comments sections or the “Notes” sheet at the end of the spreadsheet

The “Materials” and “Labor” sheets are each divided into three sections, that are further divided into a ‘batch advantage’ area and a ‘no batch advantage’ area◦ Pre-analytical

◦ Analytical

Batch Advantage

No Batch Advantage

◦ Post-analytical

Batch Advantage - When a cost is reduced as run size is increased to the point of hitting full capacity per run (ex. Standards)

No Batch Advantage – When a cost is not reduced regardless of the volume of tests in the run (ex. Collection bottles or tubes)

For hard to fit activities, make assumptions and provide notes in ‘Comments’ or ‘Notes’ section

◦ Dilutions

◦ Proficiency Tests or ◦ Performance Evaluations

◦ Reruns

Continuing Calibration of Standards

Materials Batch Advantage

Cost of standards per run is calculated when this area is populated

No Batch Advantage

Labor Batch Advantage

Minutes spent preparing and setting up standards are calculated per run when this area is populated

No Batch Advantage

Rezai Writing Demonstration 3

Pipette tips

Materials Batch Advantage

Use 10 tips for QC No Batch Advantage

Use two more tips per sample in the run

Labor Batch Advantage

Many choose to list minutes in lump form for prep/setup

No Batch Advantage List extra minutes used PER sample to set up with

tips

Sample Bottles

Materials Batch Advantage No Batch Advantage

Sample bottle: $.50

Labor Batch Advantage

Sample bottle to sample for port: 5 minutes per run/batch

No Batch Advantage Sample bottle to sample for port: 2 minutes

Comments: sample bottles - assume it takes 5 minutes to setup for the run no matter how many samples in the run and an extra 2 minutes per extra sample in the run

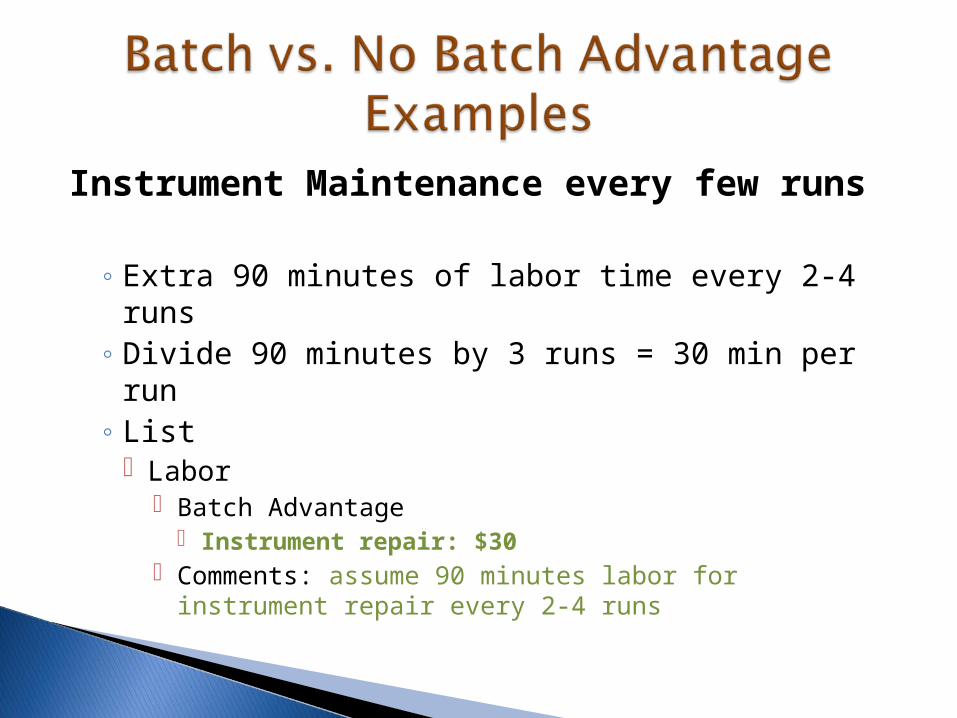

Instrument Maintenance every few runs

◦ Extra 90 minutes of labor time every 2-4 runs◦ Divide 90 minutes by 3 runs = 30 min per run◦ List

Labor Batch Advantage

Instrument repair: $30 Comments: assume 90 minutes labor for instrument

repair every 2-4 runs

List all materials used or consumed in order to run the test

Examples include reagents, kits, shipping, lab coats, gloves, results paper, hazardous waste liners, instruments not listed under ‘Replacement’ sheet such as microscopes, and any other materials that are a direct part of the testing service process

When estimating amounts, include average amounts used for complications such as dilutions and reruns

Can omit overhead materials such as office chairs, regular trash liners, phones and other indirect materials

Materials Bulk Cost Bulk Units Units/Test Cost/Test

Reagent X $2,300 25 1 $92

1. Provide a short description of the test material2. List the amount paid to vendor per package3. List the number of units per package4. List the number of units used per test performed5. Cost per test will automatically be calculated

If a material is used for controls, standards or other batch-fixed activities (at least part of the usage is independent of the number of tests run)a. Batch Advantage: Amount of material used

regardless of batch size b. No Batch Advantage: Extra material used per

extra sample per run

1 2 3 4 5

List every type of labor associated with this test◦ Pre-analytical: Starts with client order and ends just

before running test - can also include PTs, TMDLs here◦ Analytical: Starts with running the test and ends just

before reporting of results◦ Post-analytical: Starts with result reports and ends with

payment for services

Be sure to incorporate all labor time including instrument maintenance, performance testing, and reruns

Labor Category

Minutes/Test

Hours

Avg Wages+

Labor Cost/Test

Sample prep 23 .38 $30 $11.50

1 2 3 4 5

1. List description of labor

2. List the number of minutes this type of labor consumes per test

3. Hours will be automatically calculated

4. List the average hourly wage associated with this labor

a. Use (average annual wage plus fringe)/1880 hours

b. Use1880 hours instead of 2080 since the average cost of vacation and sick days must be incorporated into the hourly labor cost

5. Cost of labor per test will automatically be calculated

If some of the labor can be considered batch advantaged but not all, divide time accordingly (see labor example in batch advantage vs. no batch advantage section)

Allows the user to “play” with different labor rates

Rezai Writing Demonstration 3

Fill in the fields shaded in gray, writing over the numbers found within some of the fields

Fill in the TOTAL number of tests that this instrument services within the referenced time period (annual)

List purchase price if instrument were to be replaced today

If planning to upgrade or innovate methods, then use price of upgrade

Describe the cost

List the amount normally paid

List the number of years paid amount covers

Annual cost will be calculated automatically

List the number of tests per year that pertain to this certification (this may mean combining workload for multiple tests into one number)

Annual cost per test will be automatically calculated

For questions on how to use the tool OR to give us feedback on how we can improve the tool, please contact:

Yasmine Rezai – [email protected] Bonnie Rubin – [email protected]

Also, thanks to Erik Lehmann, UI intern, who has refined and enhanced our test costing initiative

Rezai Writing Demonstration 3