the hartford financial services group principles, or gaap. information regarding these non-gaap and...

TRANSCRIPT

The Hartford Financial Services Group, Inc.

The Hartford Financial Services Group

Always thinking ahead.

Ramani AyerChairman and Chief Executive OfficerFebruary 14, 2006

2006 Merrill Lynch Insurance Investor Conference

The Hartford Financial Services Group, Inc.

Safe Harbor StatementCertain statements made in this presentation should be considered forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. These include statements about The Hartford’s future results of operations. We caution investors that these forward-looking statements are not guarantees of future performance, and actual results may differ materially. Investors should consider the important risks and uncertainties that may cause actual results to differ, including those discussed in The Hartford’s earnings press release issued on January 26, 2006, Form 8-K filed on January 26, 2006, Quarterly Report on Form 10-Q filed for the quarter ended September 30, 2005, Annual Report on Form 10-K filed for the year ended December 31, 2004 and other filings we make with the Securities and Exchange Commission. We assume no obligation to update this presentation, which speaks as of today’s date.

The discussion in this presentation of The Hartford’s financial performance includes financial measures that are not derived from generally accepted accounting principles, or GAAP. Information regarding these non-GAAP and other financial measures is provided in the Investor Financial Supplement for the fourth quarter of 2005, and in the Investor Relations section of The Hartford’s website at www.thehartford.com.

2

The Hartford Financial Services Group, Inc.

The Hartford had record net income in 2005 and an ROE over 15%

3

($ in million; except per share amounts)

Year EndedDec-04 Dec-05

Net income 2,115$ 2,281$ 8%Net income per diluted share 7.12 7.46 5%

Core earnings 1,972 2,249 14%Core earnings per diluted share 6.64 7.36 11%

Book value per share (excluding AOCI) 43.55 50.44 16%Net income ROE 16.3% 15.4%

% Change

The Hartford Financial Services Group, Inc.

$507

$1,000

-$91

$2,281$2,115

2001 2002 2003 2004 2005

Net Income ($ Millions)

45% CAGR

3

$37.77 $36.67

$43.55

$50.44

$34.54

2001 2002 2003 2004 2005

Book Value Per Share (Excluding AOCI)

10% CAGR

4

Strong earnings have driven double digit growth in book value per share

The Hartford Financial Services Group, Inc.

Shareholder total returns over the past one, three and five years have surpassed the S&P 500

Total Annualized Return as of 2/10/06

1 Year 3 Year 5 Year

The Hartford (HIG)

S&P 500

11.4% 32.4% 6.7%

7.1% 17.0% 1.1%

5

50%

100%

150%

Feb-01 Aug-01 Feb-02 Aug-02 Feb-03 Aug-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06

The Hartford S&P

The Hartford and S&P Change From 2/10/01 – 2/10/06

The Hartford Financial Services Group, Inc.

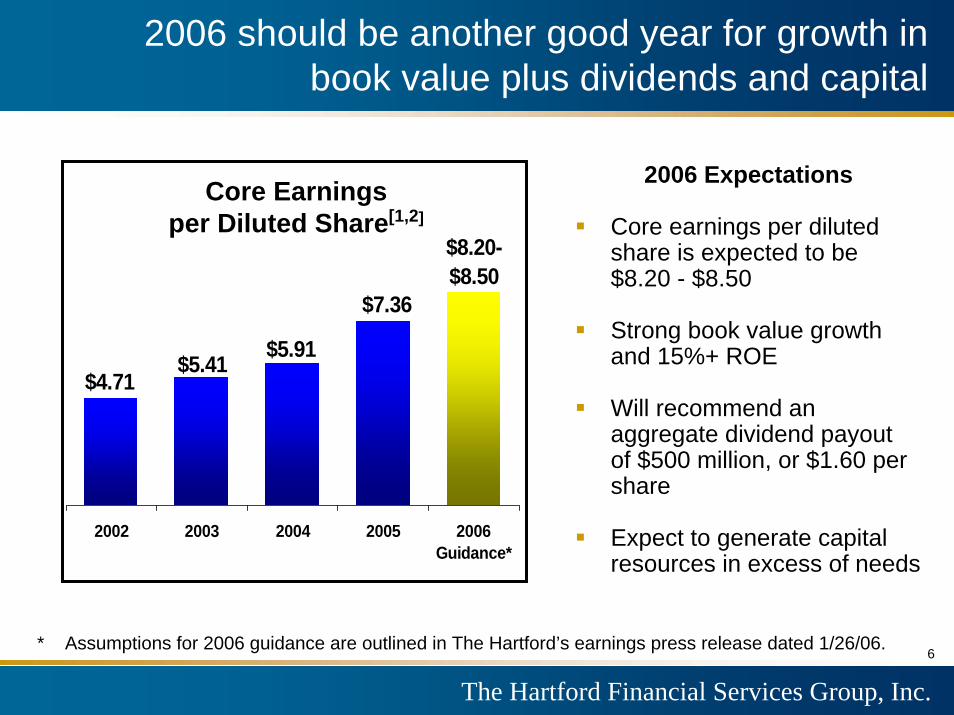

2006 should be another good year for growth in book value plus dividends and capital

$8.20-$8.50

$7.36

$5.91$5.41$4.71

2002 2003 2004 2005 2006Guidance*

Core Earnings per Diluted Share[1,2]

* Assumptions for 2006 guidance are outlined in The Hartford’s earnings press release dated 1/26/06.

2006 Expectations

Core earnings per diluted share is expected to be $8.20 - $8.50

Strong book value growth and 15%+ ROE

Will recommend an aggregate dividend payout of $500 million, or $1.60 per share

Expect to generate capital resources in excess of needs

6

The Hartford Financial Services Group, Inc.

The Hartford has a balanced, growing portfolio of insurance and investment businesses

3

$6.8$7.8

$8.9$10.0 $10.5

2001 2002 2003 2004 2005

P&C Net Written Premiums Ongoing Operations

($ Billions)

12% CAGR

7

$168 $165

$210$249

$277

2001 2002 2003 2004 2005

Assets Under Management Life Operations

($ Billions)

13% CAGR

The Hartford Financial Services Group, Inc.

Institutional Solutions7%

$88M

Individual Life13%

$166M

Retail Products46%

$622M

Retirement Plans6%

$75M

Group Benefits21%

$272M

* Pie chart excludes $112 million of loss in Other

International7%

$96M

2005 Life Core Earnings$1.2 billion*

The Hartford’s life earnings base is becoming more diversified

8

The Hartford Financial Services Group, Inc.

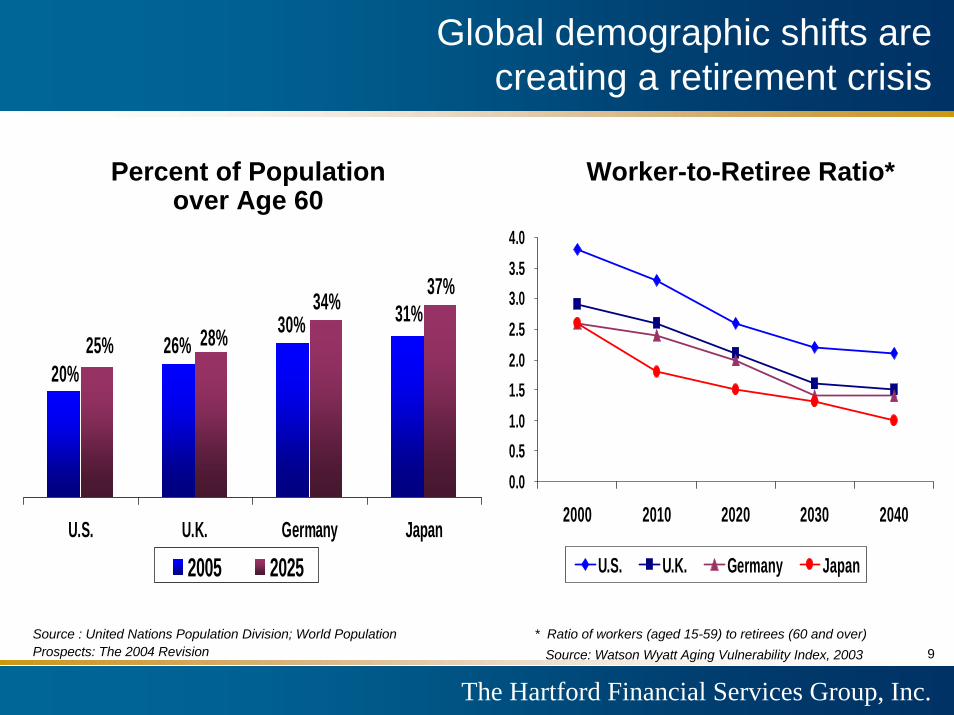

31%30%26%

20%25% 28%

34% 37%

U.S. U.K. Germany Japan

2005 2025

0.00.51.01.52.02.53.03.54.0

2000 2010 2020 2030 2040

U.S. U.K. Germany Japan

Percent of Population over Age 60

Worker-to-Retiree Ratio*

Global demographic shifts are creating a retirement crisis

Source : United Nations Population Division; World Population Prospects: The 2004 Revision 9

* Ratio of workers (aged 15-59) to retirees (60 and over)Source: Watson Wyatt Aging Vulnerability Index, 2003

The Hartford Financial Services Group, Inc.

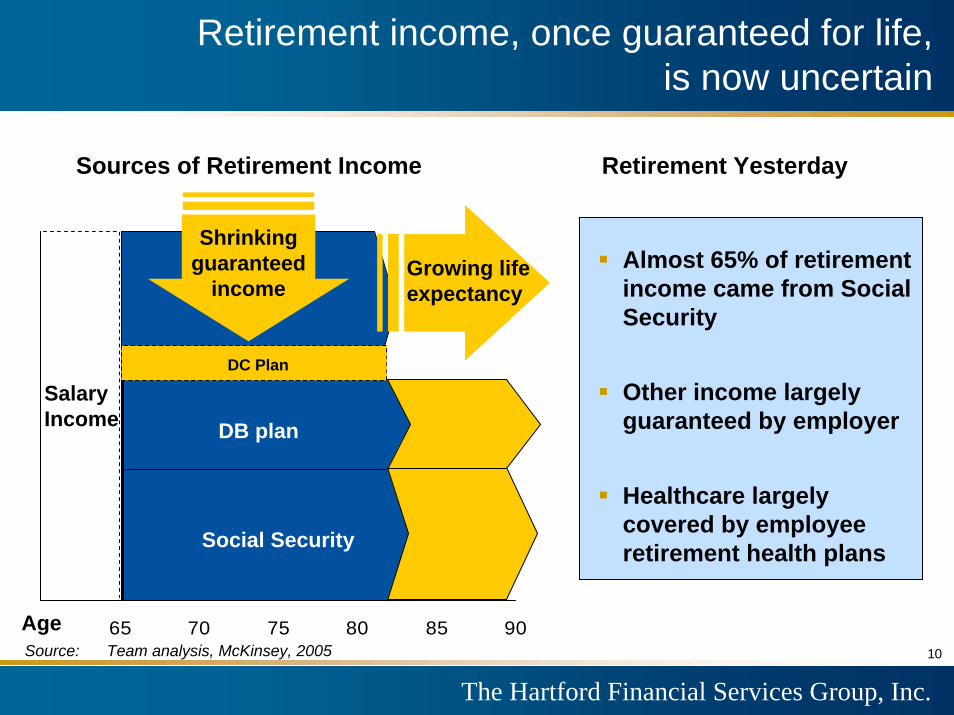

60 65 70 75 80 85 90

DB plan

Social security

Shrinking guaranteed

income

Source: Team analysis, McKinsey, 2005

Retirement income, once guaranteed for life, is now uncertain

Almost 65% of retirement income came from Social Security

Other income largely guaranteed by employer

Healthcare largely covered by employee retirement health plans

Retirement Yesterday Sources of Retirement Income

DB plan

Social security

DB plan

Social Security

Growing lifeexpectancy

Salary Income

Age

DC Plan

10

The Hartford Financial Services Group, Inc.

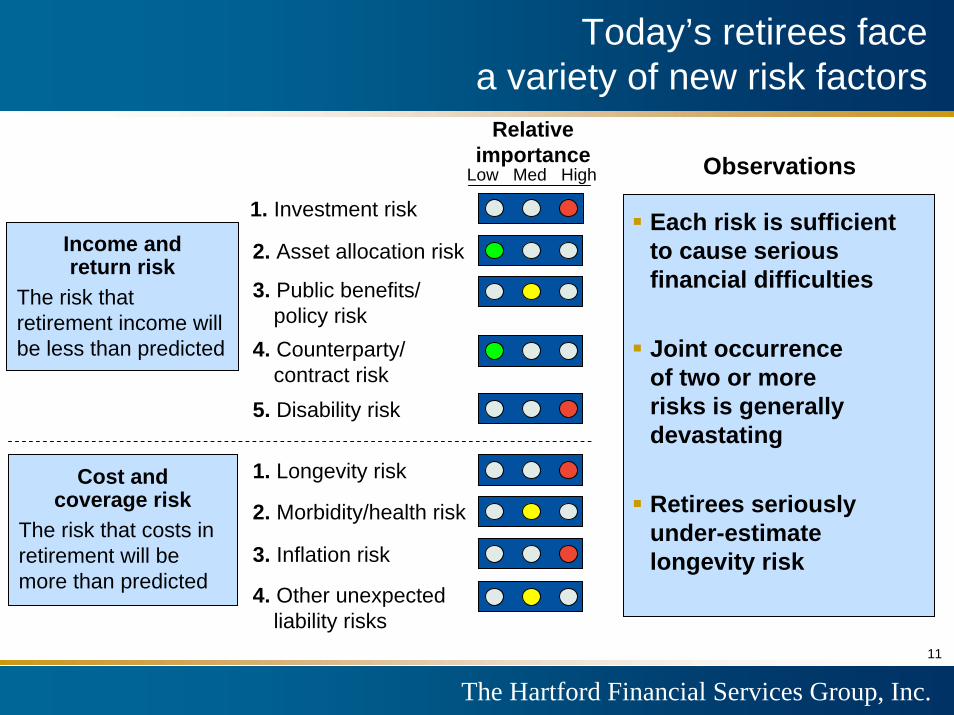

Today’s retirees facea variety of new risk factors

Income and return risk

The risk that retirement income will be less than predicted

Cost and coverage risk

The risk that costs in retirement will be more than predicted

1. Investment risk

Relativeimportance

2. Asset allocation risk

3. Public benefits/policy risk

4. Counterparty/contract risk

5. Disability risk

1. Longevity risk

2. Morbidity/health risk

3. Inflation risk

4. Other unexpected liability risks

ObservationsLow Med High

Each risk is sufficient to cause serious financial difficulties

Joint occurrence of two or more risks is generally devastating

Retirees seriously under-estimate longevity risk

11

The Hartford Financial Services Group, Inc.

Probability of Survival at Age 65

To Age: Male FemaleOne

Member of a

Couple80 71% 71% 94%85 53% 65% 84%90 34% 44% 63%95 17% 23% 36%

100 6% 9% 14%

And a growing need for longevity protection

Based on Society of Actuaries Annuity 2000 Mortality Tables

A male, age 65, has a one-in-three chance of living to age 90

A female, age 65, has a one-in-three chance of living to age 93

One member of a married couple, each age 65, has a one-in-three chance of living to age 96

12

Remarkable Longevity

The Hartford Financial Services Group, Inc.

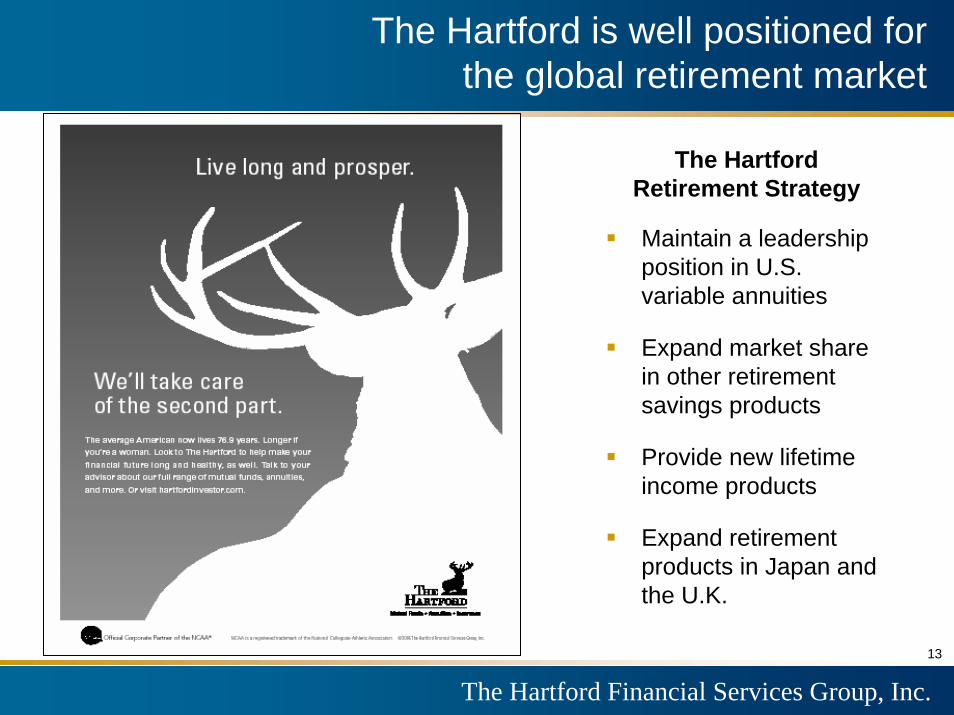

The Hartford is well positioned for the global retirement market

Maintain a leadership position in U.S. variable annuities

Expand market share in other retirement savings products

Provide new lifetime income products

Expand retirement products in Japan and the U.K.

The Hartford Retirement Strategy

13

The Hartford Financial Services Group, Inc.

Hartford Life Annuity Operating Expenses

Hartford Life Annuity Operating Expenses

Operating Expenses Per Account

$105 billion of assets under management will drive earnings

Product innovation will focus on balancing customer value with prudent risk management

New lifetime income feature is gaining traction

Recognized leader in hedging and risk management

Leverage our low cost position to strengthen competitive advantage in market place

14

We will continue to be a leaderin U.S. variable annuities

$105$100

$64

$87$75

2001 2002 2003 2004 2005

The Hartford’s Variable Annuity Assets Under Management

($ in Billions)

The Hartford Financial Services Group, Inc.

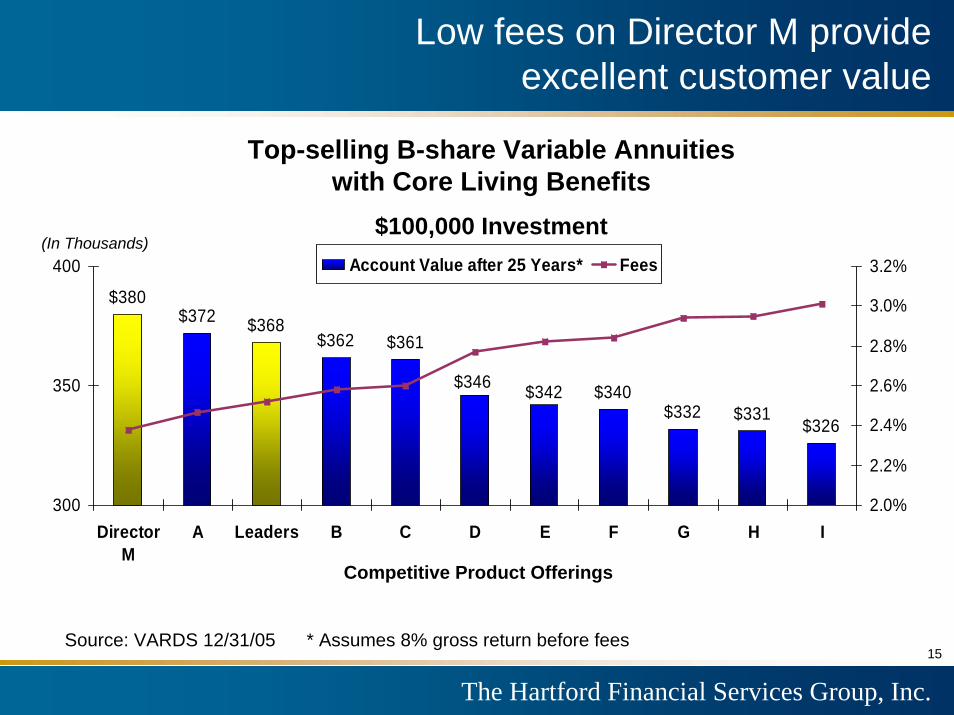

Low fees on Director M provideexcellent customer value

$380$372 $368

$362 $361

$340$332 $331

$326

$342$346

300

350

400

DirectorM

A Leaders B C D E F G H I2.0%

2.2%

2.4%

2.6%

2.8%

3.0%

3.2%Account Value after 25 Years* Fees(In Thousands)

Top-selling B-share Variable Annuities with Core Living Benefits

$100,000 Investment

Competitive Product Offerings

Source: VARDS 12/31/05 * Assumes 8% gross return before fees15

The Hartford Financial Services Group, Inc.

The Hartford’s 401(k) plans havesignificant growth potential

$595$1,400

Mid - Large Plans

(over 1,000 lives)

The Hartford TargetsMicro and Small-Mid

Size Plans(up to 1000 lives)

401(k) Industry Assets Under Management: $2.0 Trillion

Source: LIMRA International “The 401(k) scorecard”

Key Growth Strategies

Leverage our relationships with financial advisors to reach the advisor-sold market

PLANCO wholesaling80 Retirement Plans Specialists

Expand products for small-mid sized plan market

Provide broad investment choices with 60 money managers

Drive persistency with award-winning service

16

The Hartford Financial Services Group, Inc.

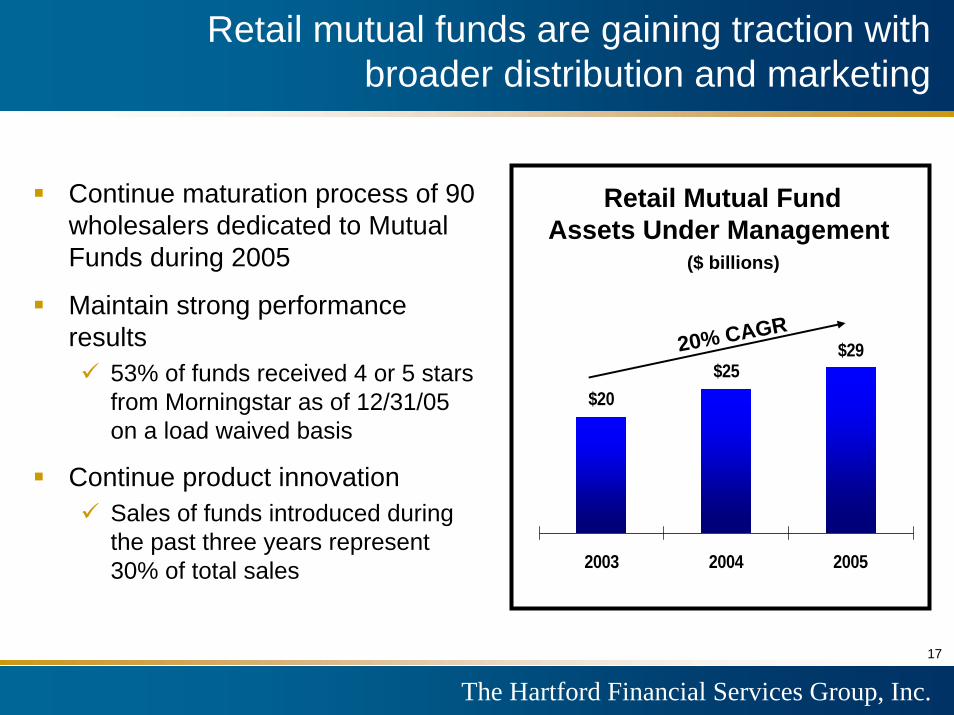

Retail mutual funds are gaining traction with broader distribution and marketing

Continue maturation process of 90 wholesalers dedicated to Mutual Funds during 2005

Maintain strong performance results

53% of funds received 4 or 5 stars from Morningstar as of 12/31/05 on a load waived basis

Continue product innovationSales of funds introduced during the past three years represent 30% of total sales

Retail Mutual Fund Assets Under Management

$20$25

$29

2003 2004 2005

($ billions)

20% CAGR

17

The Hartford Financial Services Group, Inc.

The Hartford has longevity protection products under development

Sources of Retirement IncomeNeed for new sources of retirement income

New products (e.g., longevity protection)

Extension of existing products (e.g., variable annuity with lifetime income, GMWB)

Full use of existing products in retirement context (e.g., annuitization of deferred annuities)

DC Plan Systematic Withdrawals

Non-Qualified Portfolio WithdrawalsIncluding Insurance Payments

Salary Income

DB Plan

Social Security

60 65 70 75 80 85 90

Lifetime Income Products

LongevityProtectionSolutions

Age

18

The Hartford Financial Services Group, Inc.

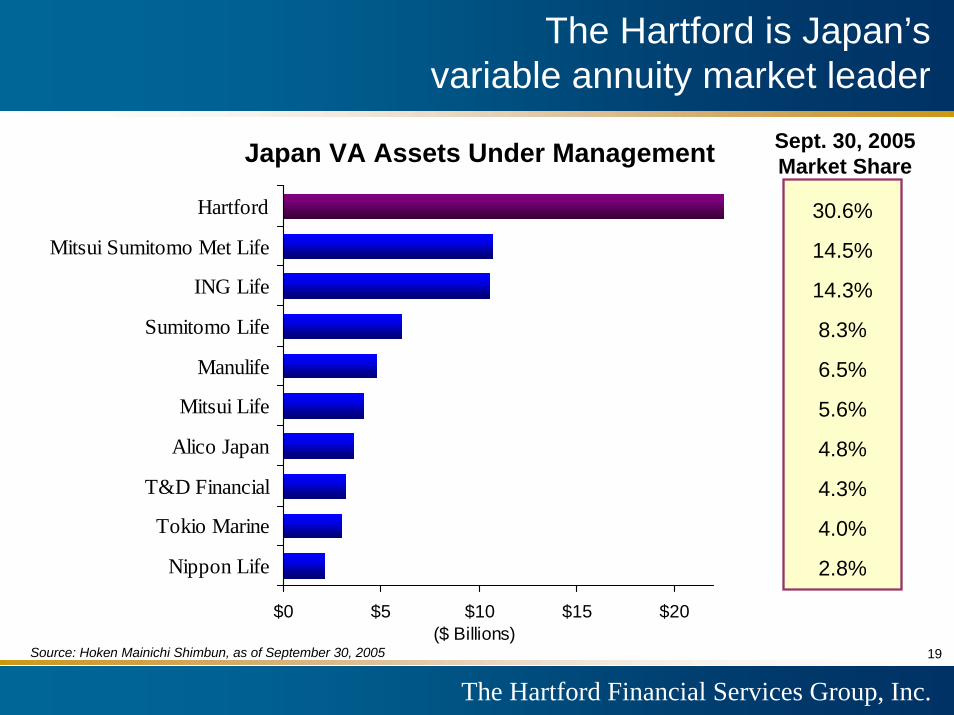

The Hartford is Japan’s variable annuity market leader

$0 $5 $10 $15 $20

Nippon Life

Tokio Marine

T&D Financial

Alico Japan

Mitsui Life

Manulife

Sumitomo Life

ING Life

Mitsui Sumitomo Met Life

Hartford

($ Billions)Source: Hoken Mainichi Shimbun, as of September 30, 2005

Sept. 30, 2005Market ShareJapan VA Assets Under Management

30.6%

14.5%

14.3%

8.3%

6.5%

5.6%

4.8%

4.3%

4.0%

2.8%

19

The Hartford Financial Services Group, Inc.

The total variable annuity industry is poised to growAs of 9/30/05, total industry assets under management were $74 billionTotal variable annuity assets may grow to $250-$400 billion by the end of the decade

New variable annuity product (Adagio V3) provides current income and new fund options

Increase penetration with existing distributors and expand distribution

Leverage variable annuity momentum into other accumulation and retirement products

We have tremendous opportunity to grow in Japan

20

The Hartford Financial Services Group, Inc. 21

The Hartford’s life business is well positioned for 2007 and beyond

Retirement solutions present significant growth opportunities inthe U.S. and Japan

Variable annuitiesMutual funds401(k)New longevity and income products

Scale and risk management allows us to offer products with excellent customer value, at acceptable risk

Strong growth outlooks in group benefits and individual life will drive earnings and diversification

The Hartford Financial Services Group, Inc.

The property and casualty industry is facing stronger headwinds

$329

$379$404

$423

$321

$150

$250

$350

$450

2001 2002 2003 2004 9/30/05 YTD80

90

100

110

120

Net Written Premium Statutory Combined Ratio

Industry Net Written Premium and Combined Ratio

Sources: A.M. Best, I.I.I., I.S.O.

$4.6

$26.5

$5.9

$12.9

$27.5

$55.3

$-

$10

$20

$30

$40

$50

$60

2000 2001 2002 2003 2004 2005

Industry Catastrophe Losses

(In Billions) (In Billions)

22

The Hartford Financial Services Group, Inc.

$-

$2

$4

$6

$8

$10

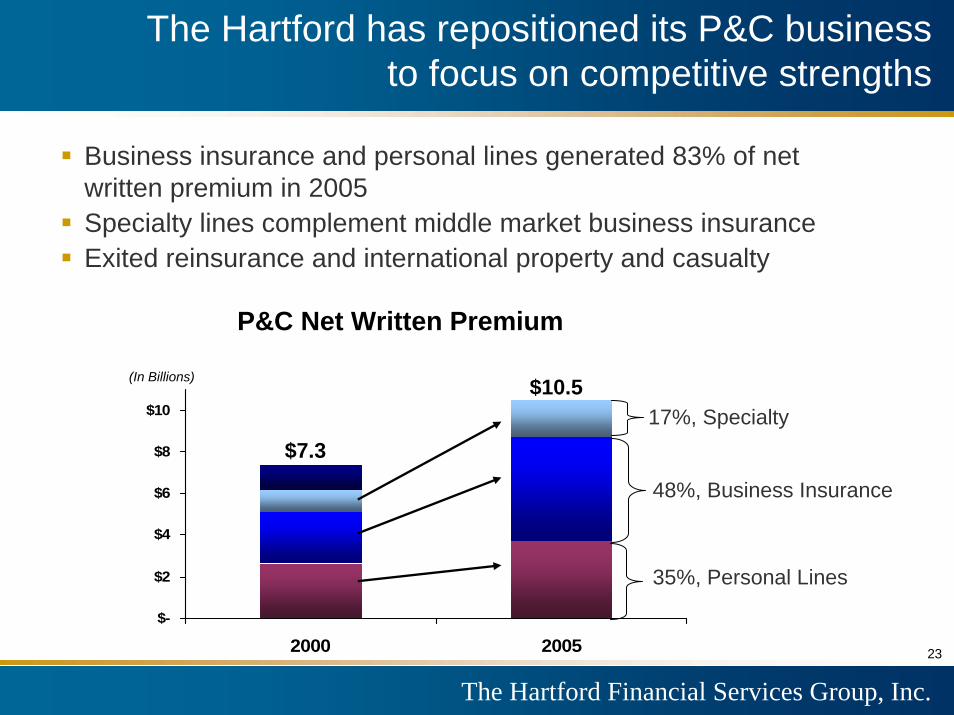

2000 2005

$7.3

$10.5(In Billions)

P&C Net Written Premium

Business insurance and personal lines generated 83% of net written premium in 2005 Specialty lines complement middle market business insuranceExited reinsurance and international property and casualty

17%, Specialty

48%, Business Insurance

35%, Personal Lines

The Hartford has repositioned its P&C business to focus on competitive strengths

23

The Hartford Financial Services Group, Inc.

$-

$1

$2

$3

$4

$5

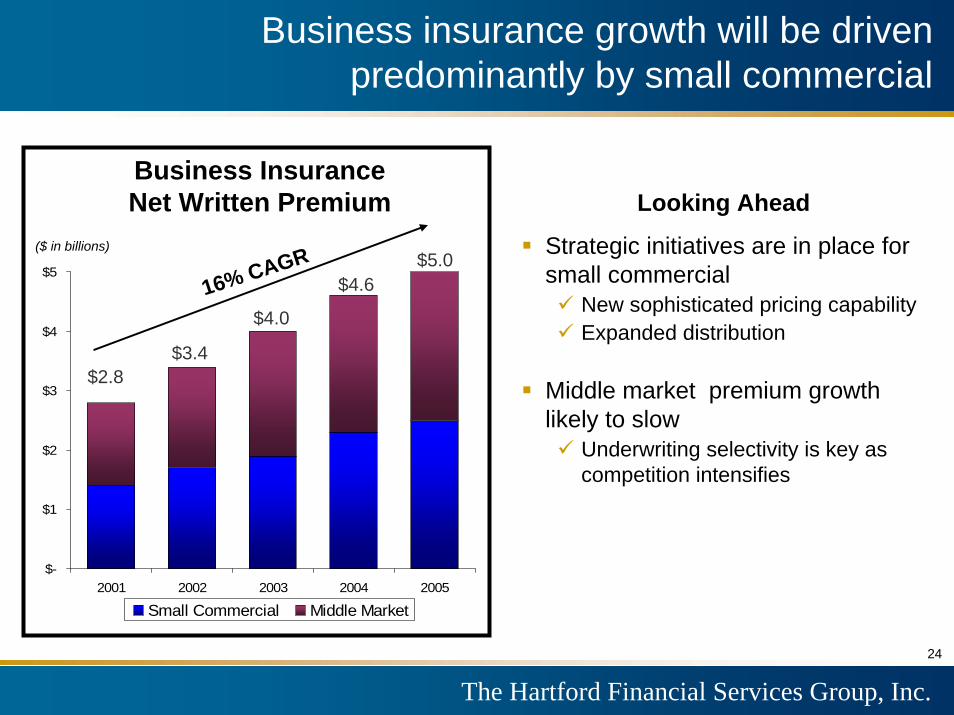

2001 2002 2003 2004 2005

Small Commercial Middle Market

($ in billions)

Looking Ahead

Strategic initiatives are in place for small commercial

New sophisticated pricing capabilityExpanded distribution

Middle market premium growth likely to slow

Underwriting selectivity is key as competition intensifies

Business Insurance Net Written Premium

Business insurance growth will be driven predominantly by small commercial

16% CAGR

$2.8$3.4

$4.0

$4.6$5.0

24

The Hartford Financial Services Group, Inc.

$0

$1

$2

$3

$4

2001 2002 2003 2004 2005

AARP Agency

Personal Lines Agency and AARPNet Written Premium

9% CAGR($ in billions)

In personal lines, product, distribution and technology provide growth opportunities

Looking Ahead

AARP growth will be fueled by aging boomers and new marketing

Dimensions auto and home granular pricing will target profitable new customers

Award-winning service supports customer retention

Investments in agency technology make it easy to offer The Hartford

Increased agency appointments and sales reps will drive quotes

$2.4$2.7 $2.9

$3.1$3.4

25

The Hartford Financial Services Group, Inc.

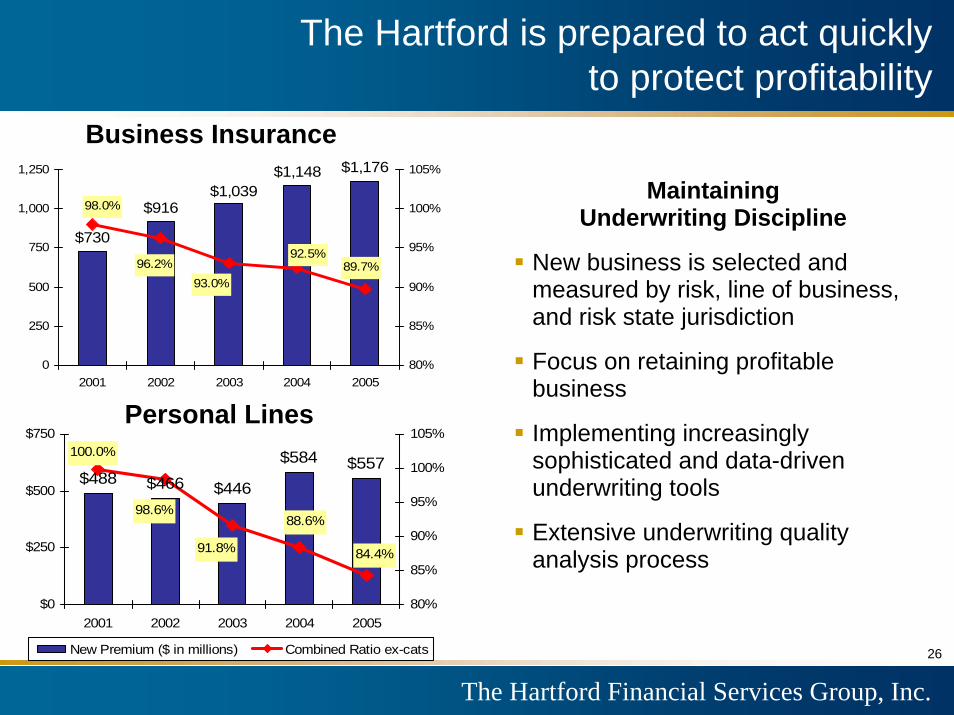

$730

$1,148 $1,176

$916$1,039

89.7%

98.0%

96.2%93.0%

92.5%

0

250

500

750

1,000

1,250

2001 2002 2003 2004 200580%

85%

90%

95%

100%

105%

Business Insurance

Personal Lines

Maintaining Underwriting Discipline

New business is selected and measured by risk, line of business, and risk state jurisdiction

Focus on retaining profitable business

Implementing increasingly sophisticated and data-driven underwriting tools

Extensive underwriting quality analysis process

The Hartford is prepared to act quickly to protect profitability

$488 $466 $446

$584 $557

84.4%

88.6%

100.0%

98.6%

91.8%

$0

$250

$500

$750

2001 2002 2003 2004 200580%

85%

90%

95%

100%

105%

New Premium ($ in millions) Combined Ratio ex-cats 26

The Hartford Financial Services Group, Inc.

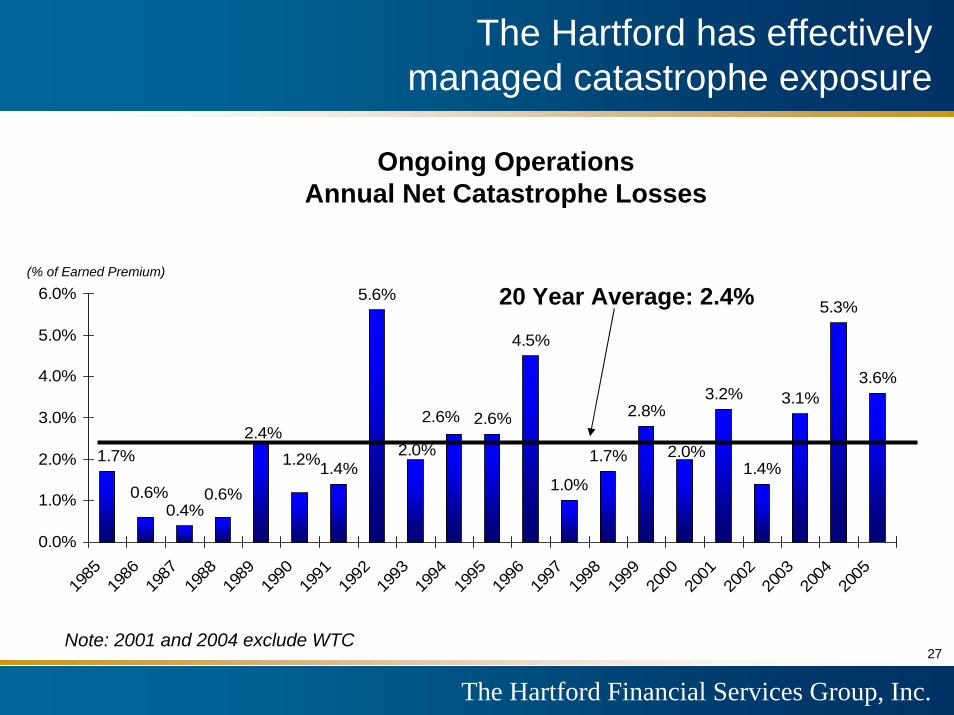

0.4%

1.4%

5.6%

2.6%

4.5%

1.0%

1.7%

2.8%3.2%

1.4%

3.1%

5.3%

3.6%

2.4%2.0%2.0%

2.6%

0.6% 0.6%

1.7% 1.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

(% of Earned Premium)

Ongoing Operations Annual Net Catastrophe Losses

Note: 2001 and 2004 exclude WTC

20 Year Average: 2.4%

The Hartford has effectively managed catastrophe exposure

27

The Hartford Financial Services Group, Inc.

At year-end 2005, The Hartford had a capital margin of $1 billion in excess of rating agency minimums

$500 million in additional capital will likely be generated in 2006

Our primary goal is to deploy that capital to invest in growth at 13% to 15% returns

Alternatively, we will return capital to shareholders

Financial Leverage Excluding AOCI [3]

EnterpriseGoal

Low 20’s

20.0%

23.5%

28.1%29.5%

31.9%

15%

20%

25%

30%

35%

2001 2002 2003 2004 2005

A strong capital position provides capacity for opportunities and protection for unforeseen events

28

The Hartford Financial Services Group, Inc. 38

The Hartford is well positioned for 2006 and beyond

A Market Leader in Key FranchisesVariable Annuities Group BenefitsVariable Life

A Strong Capital Position

Expertise in Risk Management and Pricing

A Foundation for Future Growth Retirement initiatives401(k) and mutual funds Japan variable annuitiesSmall commercial insuranceAgency personal lines

Small Commercial AARP Personal Lines

29

The Hartford Financial Services Group, Inc.

Always Thinking Ahead.

The Hartford Financial Services Group, Inc.

[1] In order to provide a consistent basis of comparison, this chart excludes tax benefits of $76, $30 and $216 for 2002-2004, Bancorp Services litigation charges of $11 and $40 in 2002 and 2003, and the asbestos reserve addition of $1,701 and severance charges of $27 in 2003.

[2] The Hartford uses the non-GAAP financial measure core earnings as an important measure of the Company's operating performance. The Company believes the measure core earnings provides investors with a valuable measure of the performance of the Company's ongoing businesses because core earnings excludes the cumulative effect of accounting changes and the effect of all realized gains and losses (net of tax and the effects of deferred policy acquisition costs) that tend to be highly variable from period to period based on capital market conditions. Core earnings includes net realized gains and losses such as net periodic settlements on credit derivatives and net periodic settlements on the Japan fixed annuity cross-currency swap because these net realized gains and losses are directly related to an offsetting item included in the income statement such as net investment income. Net income is the most directly comparable GAAP measure. A reconciliation of net income to core earnings for the periods presented herein is set forth on page C-8 of our Investor Financial Supplement. Core earnings per share is calculated based on a non-GAAP financial measure. Net income per share is the most directly comparable GAAP measure. A reconciliation of net income per share to core earnings per share for the periods presented herein is set forth on page C-8 of our Investor Financial Supplement.

[3] Includes 75% equity credit on the equity units. 2003 excludes the impact of the CNA transaction.

F-1

Footnotes($ in millions)