the global energy transition - suzhou · the global energy transition paul simons ... the carbon...

TRANSCRIPT

© OECD/IEA 2016 © OECD/IEA 2016

The Global Energy Transition

Paul Simons

Deputy Executive Director International Energy Agency

Suzhou, 30 October 2016

© OECD/IEA 2016

COP21 Paris Agreement gives momentum to renewable energy (RE) and energy efficiency (EE)

• Record additions of RE in 2015, installed capacity surpassed coal

• EE investments grew 6% in 2015 reaching $221bln

Local air pollution & energy security are also key drivers

Energy investment flows confirm a shift to clean energy

Context

© OECD/IEA 2016

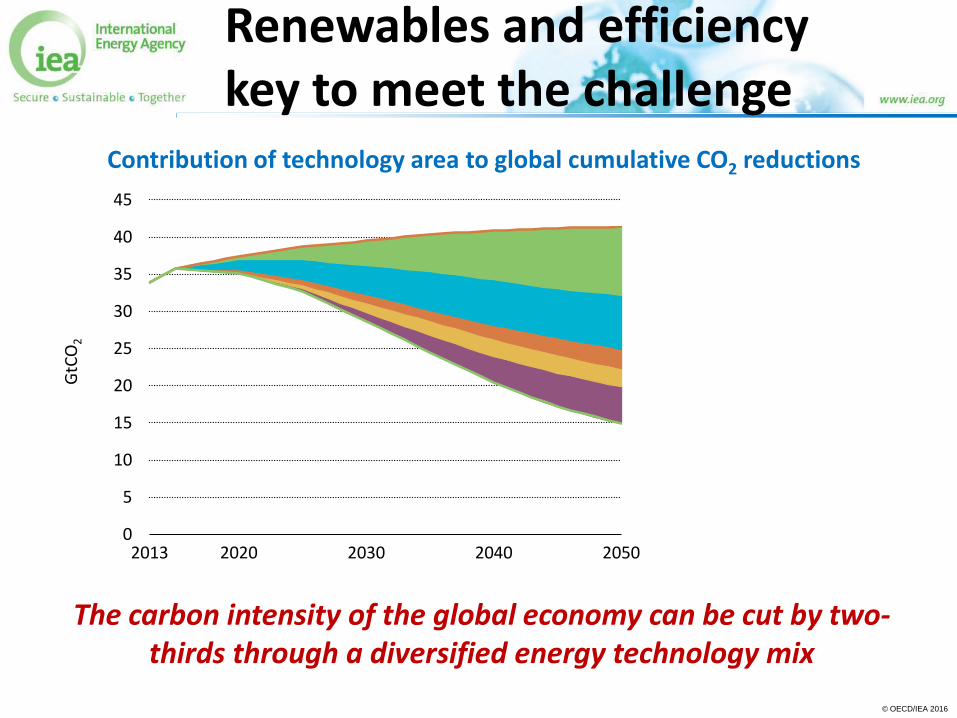

The carbon intensity of the global economy can be cut by two-thirds through a diversified energy technology mix

Contribution of technology area to global cumulative CO2 reductions

Renewables and efficiency key to meet the challenge

0

5

10

15

20

25

30

35

40

45

2013 2020 2030 2040 2050

GtC

O2

Renewables 32%

Energy efficiency 32%

Fuel switching 10%

Nuclear 11%

CCS 15% 2DS

4DS

© OECD/IEA 2016

An 8% reduction in 2015 global energy investment results from a $200 billion decline in fossil fuels, while the share of renewables, networks and efficiency expands

Power Generation

23% Biofuels and Solar

Heat 1%

Renewables 17%

USD 1.8 trillion

Investment flows signal a reorientation of the global energy system

Oil & Gas 46%

Coal 4%

Electricity Networks

14%

Energy Efficiency

12%

Global Energy Investment, 2015

Thermal Power

7%

© OECD/IEA 2016

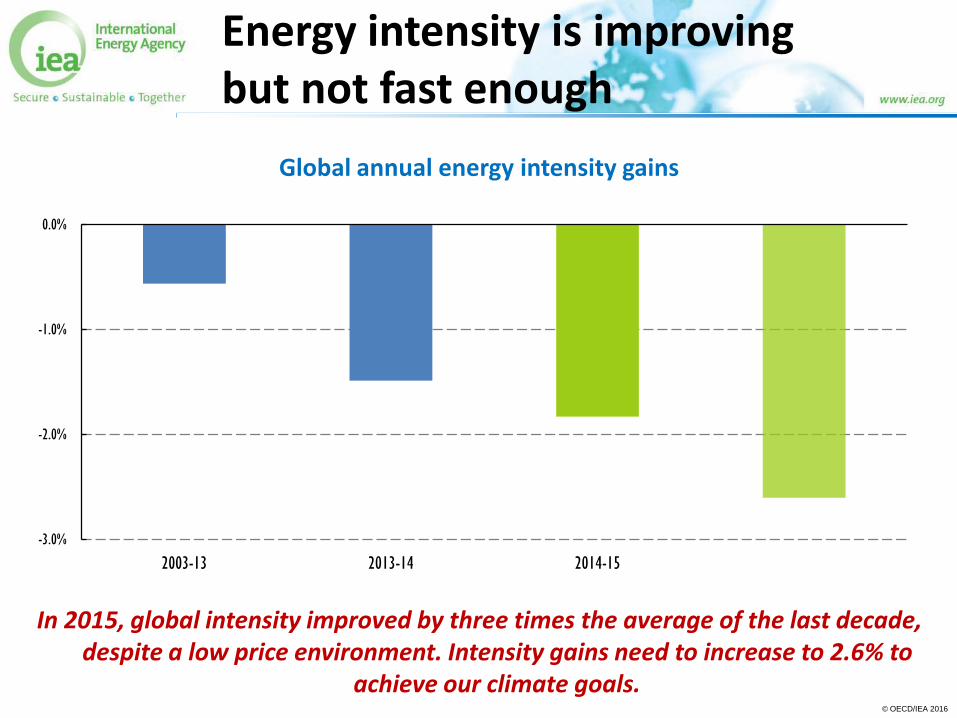

Energy intensity is improving but not fast enough

Global annual energy intensity gains

In 2015, global intensity improved by three times the average of the last decade, despite a low price environment. Intensity gains need to increase to 2.6% to

achieve our climate goals.

-3.0%

-2.0%

-1.0%

0.0%

2003-13 2013-14 2014-15 2016-30

(2 degree goal)

© OECD/IEA 2016

China is an energy efficiency heavyweight

Primary energy savings from efficiency gains since 2000 and renewable energy supply in China

Dramatic progress on energy efficiency saved 350 million tonnes of coal in 2014. Energy savings are as large as China’s renewable energy supply.

0

100

200

300

400

2008 2009 2010 2011 2012 2013 2014

Mtoe

Energy savings

Renewable energy

supply

© OECD/IEA 2016

Vehicle fuel economy standards have helped to moderate price falls

Sales and average annual fuel economy of light-duty trucks, United States

Light-duty truck sales hit record levels in the United States in 2015, but standards ensured overall new vehicle fleet efficiency still improved.

6.5

7.5

8.5

9.5

10.5

11.5

0

2

4

6

8

10

2010 2011 2012 2013 2014 2015

Lge per 10

0 km

Sales (m

illions)

Fuel economy

(right axis)

© OECD/IEA 2016

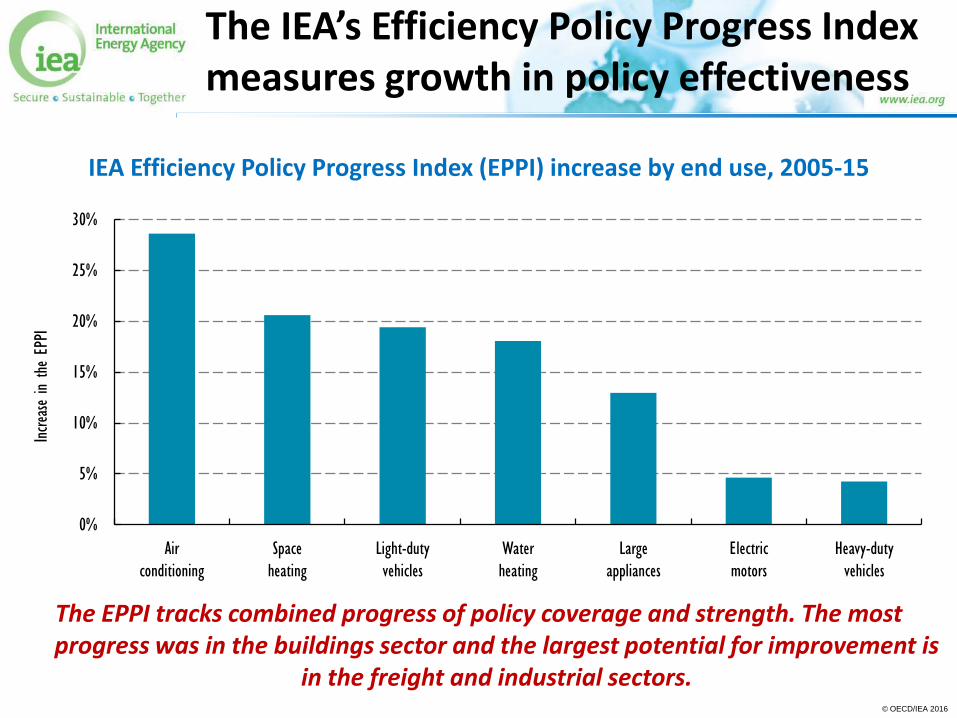

The IEA’s Efficiency Policy Progress Index measures growth in policy effectiveness

IEA Efficiency Policy Progress Index (EPPI) increase by end use, 2005-15

The EPPI tracks combined progress of policy coverage and strength. The most progress was in the buildings sector and the largest potential for improvement is

in the freight and industrial sectors.

0%

5%

10%

15%

20%

25%

30%

Air

conditioning

Space

heating

Light-duty

vehicles

Water

heating

Large

appliances

Electric

motors

Heavy-duty

vehicles

Increase in

the EP

PI

© OECD/IEA 2016

Renewables to remain fastest growing source of electricity generation

Generation from renewables to rise by almost two-fifths over 2015-2021, pushing their share of total electricity generation from 23% to 28%

Indexed electricity generation by fuel (2001-21)

100

120

140

160

180

200

220

240

260

280

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

2001

=10

0

Global power generation Coal Natural gas Renewable electricity generation

© OECD/IEA 2016

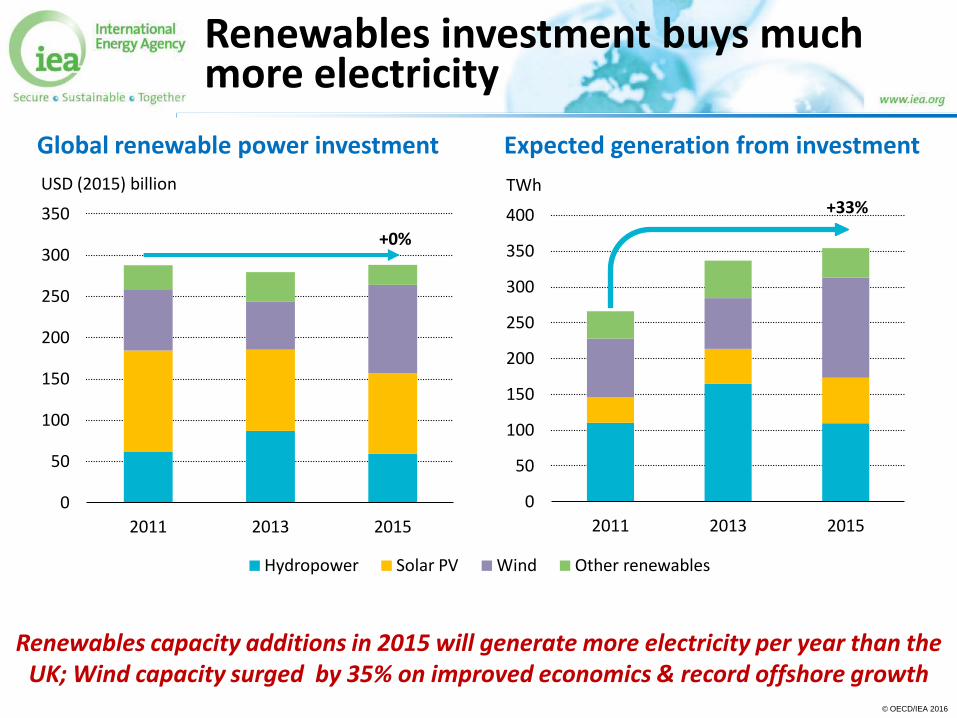

Renewables investment buys much more electricity

Renewables capacity additions in 2015 will generate more electricity per year than the UK; Wind capacity surged by 35% on improved economics & record offshore growth

0

50

100

150

200

250

300

350

2011 2013 2015

USD (2015) billion

Hydropower Solar PV Wind Other renewables

0

50

100

150

200

250

300

350

400

2011 2013 2015

TWh +33%

+0%

Global renewable power investment Expected generation from investment

© OECD/IEA 2016

Solar PV costs continue to decline with increasing competition

Utility-scale solar PV generation costs to fall by another quarter over 2015-21; competitive tenders may result in even faster cost reductions

Utility-scale solar PV generation cost and contract prices

0

100

200

300

400

500

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

USD/

MWh

Global reference UAE Brazil South Africa Germany Mexico Chile

Forecast

Tendered prices:

© OECD/IEA 2016

71%

8%

15%

4%

2%

Hydropower

Bioenergy

Wind

Solar PV

Other renewables

Solar PV & wind account for almost 2/3 of rise in renewables generation; total renewable electricity overpasses 7600 TWh by 2021, equivalent to EU+US today

Renewable electricity generation by source 2015 Renewable electricity generation by source 2021

Wind and solar PV compensate for slower hydropower growth

© OECD/IEA 2016

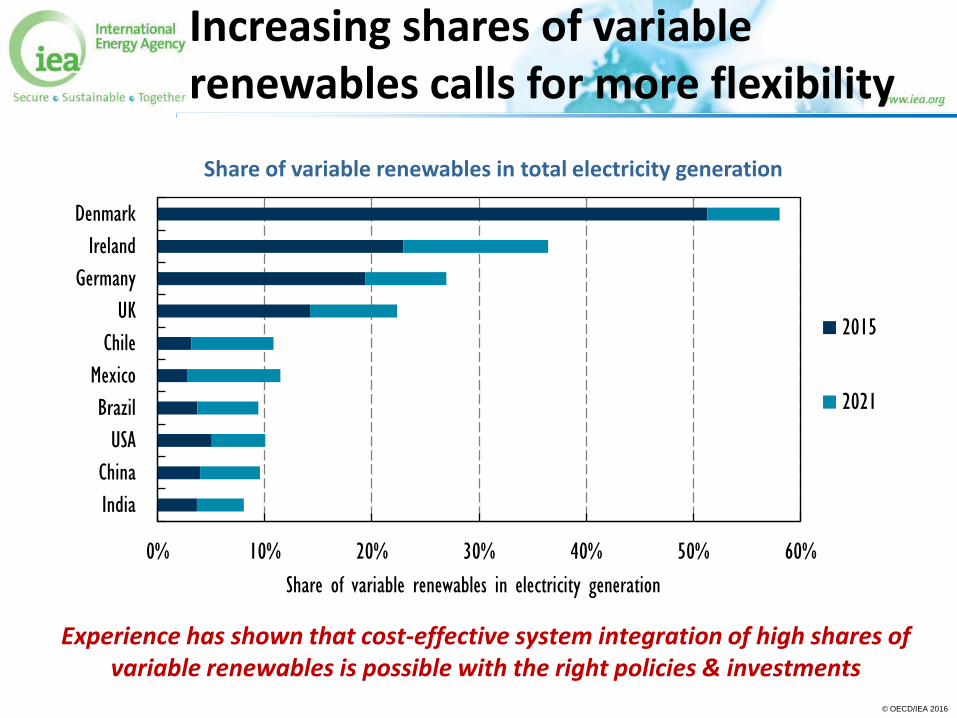

Experience has shown that cost-effective system integration of high shares of variable renewables is possible with the right policies & investments

Share of variable renewables in total electricity generation

0% 10% 20% 30% 40% 50% 60%

India

China

USA

Brazil

Mexico

Chile

UK

Germany

Ireland

Denmark

Share of variable renewables in electricity generation

2015

2021

Increasing shares of variable renewables calls for more flexibility

© OECD/IEA 2016

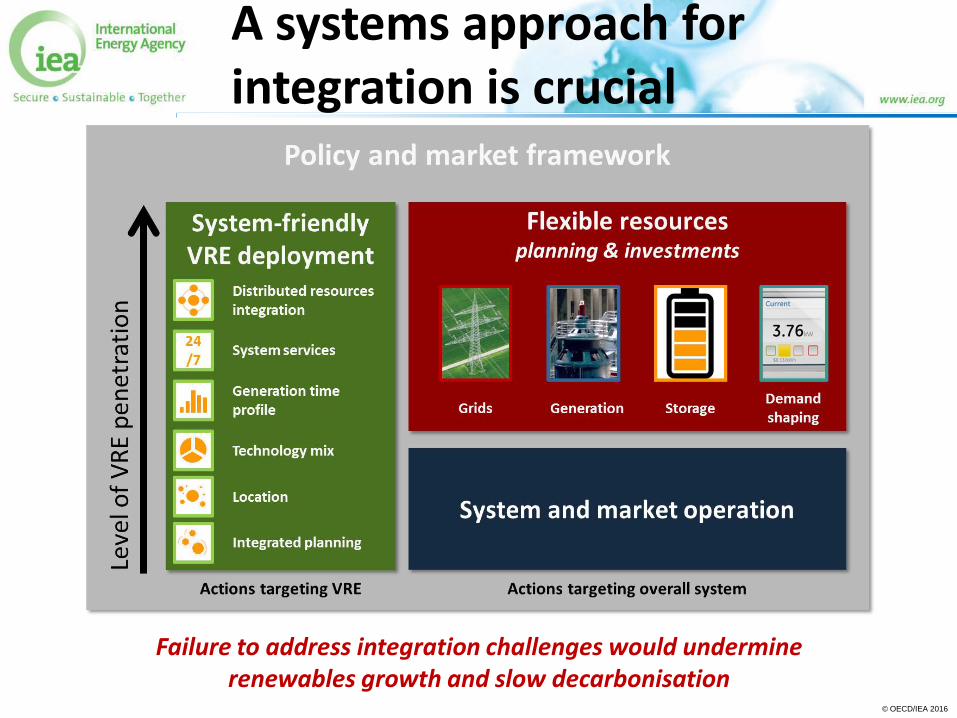

A systems approach for integration is crucial

Failure to address integration challenges would undermine renewables growth and slow decarbonisation

© OECD/IEA 2016

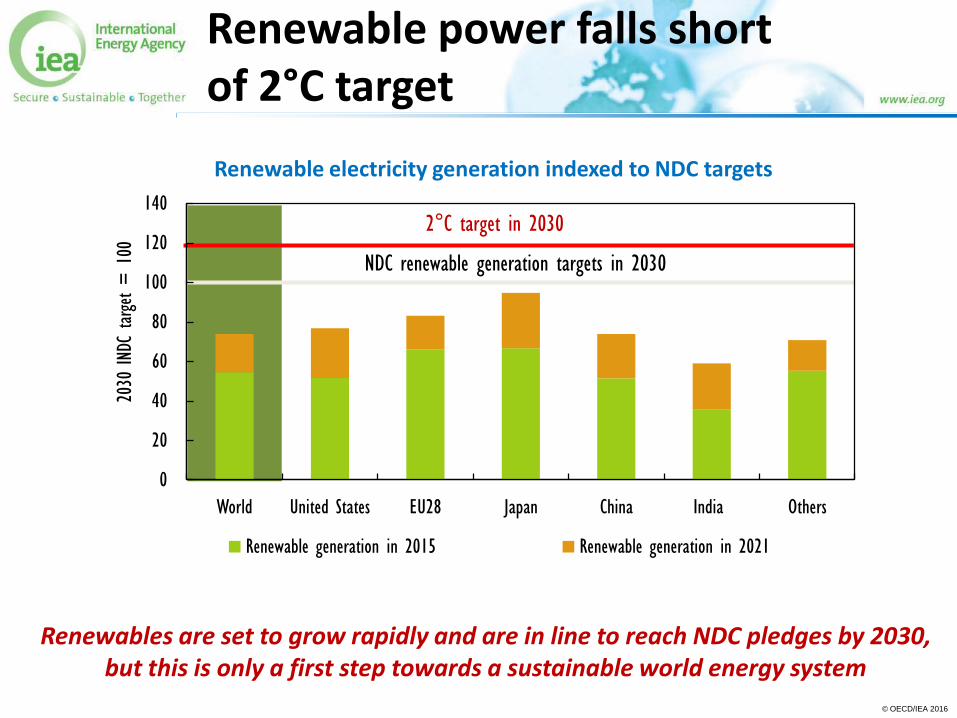

Renewable power falls short of 2°C target

Renewables are set to grow rapidly and are in line to reach NDC pledges by 2030, but this is only a first step towards a sustainable world energy system

Renewable electricity generation indexed to NDC targets

NDC renewable generation targets in 2030

2°C target in 2030

0

20

40

60

80

100

120

140

World United States EU28 Japan China India Others

2030

IND

C target =

100

Renewable generation in 2015 Renewable generation in 2021

© OECD/IEA 2016

Renewables to dominate electricity growth, but less progress in heat and transport

The share of renewables rises in all sectors, despite persistent challenges in heat & transport; interactions between energy efficiency & renewables become critical

Share of renewables in electricity, heat and transport sectors

0%

5%

10%

15%

20%

25%

30%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Share of ren

ewab

les in sector de

man

d

Renewable electricity Renewable heat Biofuels in road transport

© OECD/IEA 2016

Concluding remarks

Clear signs of progress

• Success of technology progress, market innovation and political leadership

We are not on track to below 2 degrees yet

• Efficiency improvements are not fast enough

• More progress needed in heating and transport

An energy system approach is critical to achieve transformation

• Across technologies – renewables and efficiency

• Across sectors – electricity, heating, transport

Continued policy push needed to achieve transformation