the future of risk management thomas garside, partner jonathan mitchell, engagement manager...

TRANSCRIPT

AUTHORSThomas Garside, PartnerJonathan Mitchell, Engagement Manager

Financial Services

THE FUTURE OF RISK MANAGEMENTTEN YEARS AFTER THE CRISIS

During the dog-days of August, a FTSE 100 financial institution, established more than

100 years ago and based in the North of England, suddenly announces a dramatic collapse

in their financial position, and blue-chip investors are left nursing major losses. However it’s

not 2007, it’s now 2017. Ten years on from the start of the Northern Rock crisis, it seems a

reasonable time to ask “so what has changed”?

The last ten years have seen a radical overhaul of risk management at UK banks.

The Northern Rock failure alone would no doubt have prompted big changes. But the

subsequent cascade of events drove massive government and regulatory intervention.

Over the last 10 years, the risk functions of banks have been dominated by the work required

to comply with an avalanche of new regulation.

UK banks have, for the most part, satisfied the new regulatory demands. As a result, they are

much better capitalised than they were in 2007 and with better liquidity and funding ratios.

Despite the risks arising from Brexit and the unwinding of quantitative easing, another crisis

ten years after the last one began seems unlikely.

The next ten years in risk functions will thus be quite unlike the last. The drivers of change

will not be financial recovery and regulatory compliance, but technology-driven changes

to banks’ business models and to the machinery of risk management. Ultimately, the

transformation brought on by these developments could be greater than the cumulative

changes of the last ten years.

Having sketched the story of the last 10 years, and the current state of play in risk

management functions, this report describes the developments that are likely over the

coming years and what CROs can be doing to prepare for them.

THE CRISIS AND ITS EFFECT ON RISK MANAGEMENT

The freezing of much of the wholesale money markets in the summer of 2007 exposed the

funding strategies of many bank and non-bank business models, triggering a cascade of

events that played out on both sides of the Atlantic (see Exhibit 1).

In just over twelve months, more than a dozen major financial institutions had been

rescued on both sides of the Atlantic, structured investment vehicles (SIVs) controlling over

$400 billion of assets had closed, and the first phase of the crisis culminated in the collapse

of Lehman Brothers on the 14th September 2008.

The last quarter of 2008 and the first of 2009 were the darkest days of the banking crisis.

Nearly all major banks in Europe and North America came under sustained pressure.

Morgan Stanley and Goldman Sachs were the only major institutions whose credit default

swap (CDS) spreads exceeded 400bps to survive bankruptcy or government recapitalisation.

Copyright © 2017 Oliver Wyman 1

ExHIBIT 1: TIMELINE 2007–2009

2007

J F M A M J J A S O N D

2008

J F M A M J J A S O N D

2009

J F M A M J J A S O N D

600

800

400

200

0

1000

FTSE UK BANKS INDEX

14 SEP 2007Northern Rock granted emergency funding by Bank of England

6 DEC 2007Cut to UKinterest rates

1 OCT 2007Increase in UKdeposit insurance

17 MAR 2008Bear Sterns rescued by JP Morgan

18 SEP 2008Central banks inject billions of pounds worth of liquidity

29 SEP 2008Nationalisation of Bradford & Bingley; Fortis partially nationalised

30 SEP 2008Dexia receives €6.4 BN state injection

16 Oct 2008UBS £3 BN state injection

2 APR 2009G20 agrees $5 TN financial stimulus package

5 MAR 2009Bank of England begins £75 BN round of Quantitative Easing

8 SEP 2008US Treasury rescues Fannie Mae and Freddie Mac for $187 BN

15 SEP 2008Lehman Brothers files for bankruptcy in the US

3 OCT 2008US creates $700 BNgovt. support programme (TARP)

6 OCT 2008Hypo Real Estate bailed-out by Germany for €50 BN

Nationalisation of Icelandic banking system

21 OCT 2008Germany rescues IKB mortgage bank for €9 BN

13 OCT 2008British Govt. £37 BN rescue plan for RBS, Lloyds and HBOS

Source: Datastream

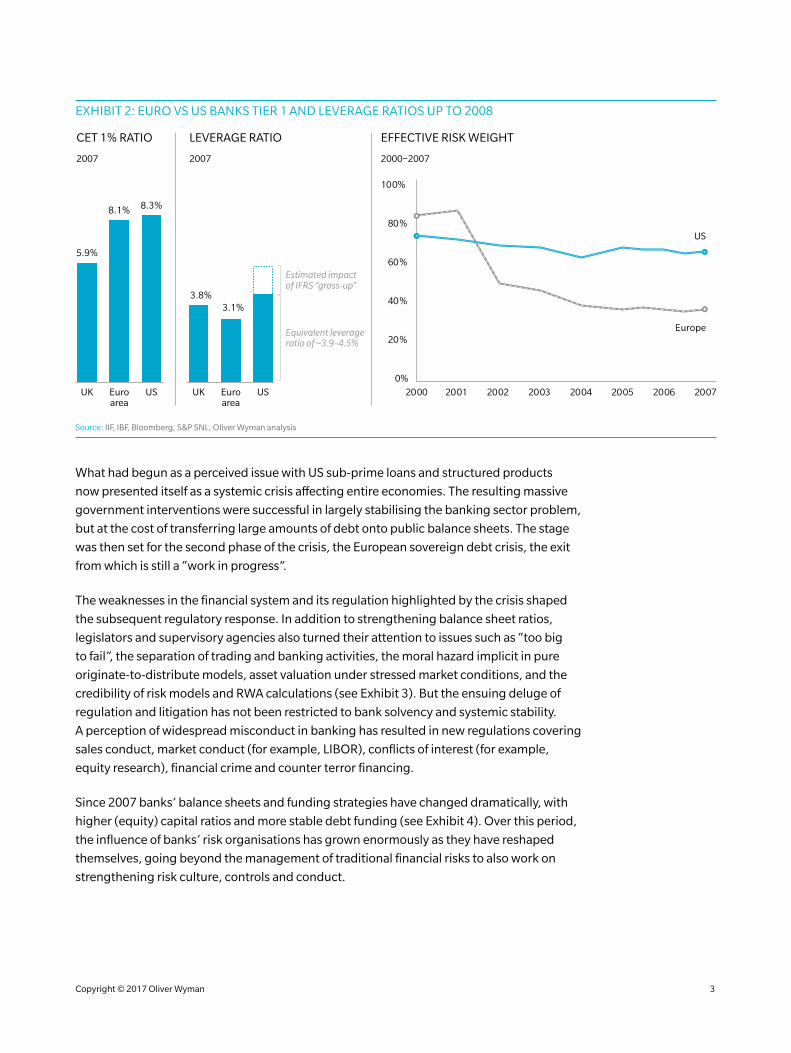

Bank regulation at the time helped to shape the crisis (see Exhibit 2), if only through the “law

of unintended consequences”. Whereas banks in Europe were subject to a brake on risk via

Basel II and Risk Weighted Assets (RWAs), in the United States, where Basel II had not yet

been implemented, banks were instead subject to a brake on their leverage ratio. Thus it

can be broadly argued that failing European banks blew themselves up with leverage, while

failing US banks blew themselves up with risky assets, the most vulnerable being banks

dependent on large quantities of short-term wholesale funding.

Copyright © 2017 Oliver Wyman 2

ExHIBIT 2: EURO VS US BANKS TIER 1 AND LEVERAGE RATIOS UP TO 2008

UK Euroarea

US

5.9%

8.1% 8.3%

3.8%3.1%

Equivalent leverage ratio of ~3.9–4.5%

Estimated impact of IFRS “gross-up”

UK Euroarea

US

2007

CET 1% RATIO

2007

LEVERAGE RATIO

2000–2007

EFFECTIVE RISK WEIGHT

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004

US

Europe

2005 2006 2007

Source: IIF, IBF, Bloomberg, S&P SNL, Oliver Wyman analysis

What had begun as a perceived issue with US sub-prime loans and structured products

now presented itself as a systemic crisis affecting entire economies. The resulting massive

government interventions were successful in largely stabilising the banking sector problem,

but at the cost of transferring large amounts of debt onto public balance sheets. The stage

was then set for the second phase of the crisis, the European sovereign debt crisis, the exit

from which is still a “work in progress”.

The weaknesses in the financial system and its regulation highlighted by the crisis shaped

the subsequent regulatory response. In addition to strengthening balance sheet ratios,

legislators and supervisory agencies also turned their attention to issues such as “too big

to fail”, the separation of trading and banking activities, the moral hazard implicit in pure

originate-to-distribute models, asset valuation under stressed market conditions, and the

credibility of risk models and RWA calculations (see Exhibit 3). But the ensuing deluge of

regulation and litigation has not been restricted to bank solvency and systemic stability.

A perception of widespread misconduct in banking has resulted in new regulations covering

sales conduct, market conduct (for example, LIBOR), conflicts of interest (for example,

equity research), financial crime and counter terror financing.

Since 2007 banks’ balance sheets and funding strategies have changed dramatically, with

higher (equity) capital ratios and more stable debt funding (see Exhibit 4). Over this period,

the influence of banks’ risk organisations has grown enormously as they have reshaped

themselves, going beyond the management of traditional financial risks to also work on

strengthening risk culture, controls and conduct.

Copyright © 2017 Oliver Wyman 3

ExHIBIT 3: REGULATORY TIMELINE SINCE FINANCIAL CRISIS

4,000

2,000

0

6,000

NUMBER OF THOMSON REUTERS REGULATORY ALERTS PER MONTH

Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct

CRD IV, CoRep,FinRep

Basel 2.5 Basel 3Dodd-Frank

Final NSFR

EMIR/OTC

Liikanen

SSM/SREP

PRA RRP

MIFID II

BCBS239

Revised LCR

BCBS248

IFRS9 Final PSD2 TRIMTLAC FRTB

2008 2009 2010 2011 2012 2013 2014 2015 2016

Source: Thomson Reuters, Oliver Wyman analysis

ExHIBIT 4: CET1 RATIO AND WHOLESALE FUNDING MIx FOR UK BANKS 2007–20161,2

60

50

80

70

CET1 RATIO

40

90

21% 24%18%15%12%9%6%3%

Bubble size =

Total RWA

NationwideBuilding Society

HSBC Bank

PERCENTAGE NON-WHOLESALE FUNDING

2007 2016

HBOS

BarclaysStandard Chartered

Royal Bank of Scotland

Lloyds Banking Group

Lloyds Bank Plc

Source: S&P SNL, Oliver Wyman analysis 1. Non-wholesale funding % = (Total liabilities – wholesale funding) / Total liabilities, where wholesale funding includes financial liabilities and repurchase agreements, excludes derivatives and customer deposits

2. RBS CET1 ratio shown is for 2008 as 2007 not reported.

Copyright © 2017 Oliver Wyman 4

WHERE ARE WE NOW?

The financial sector is now undoubtedly more robust. However, it is unclear the degree to

which total risk has reduced. Aggregate levels of indebtedness are still increasing, and risk is

shifting from private to public balance sheets, and from the old to the young (see Exhibits 5

and 6).

ExHIBIT 5: UK LEVELS OF INDEBTEDNESS1/GDP (ExCLUDING FINANCIAL CORPORATIONS) 2007–2016

100

200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

0

300

Private balance sheets

Public balance sheets

PERCENT OF GDP

Source: Eurostat, Oliver Wyman analysis 1. Indebtedness defined as debt securities + loans

ExHIBIT 6: HOME OWNER OCCUPIERS BY AGE 1981–2016

50

25

75

100

16–24

PERCENT

25–34 35–44 45–64 65–74 75+

2015–16

2011–12

2001–02

1991

1981

0

Source: ONS (English Housing Survey)

Copyright © 2017 Oliver Wyman 5

In several European countries there is still a large, and in some cases growing, legacy of the

crisis in the form of NPL stocks. Efforts at national and European levels to tackle this issue

have had mixed success. As Exhibit 7 illustrates, banking crises caused by asset bubbles

(Ireland and Spain, for example) can be overcome more quickly than crises caused by a loss

of economic competitiveness.

The dominating economic issue in the UK is Brexit. Executed badly, the credit quality of UK

businesses and households will deteriorate. At present, however, markets are not pricing

a risk premium into tradable UK corporate debt. The immediate credit-related concern in

the UK is consumer lending (see Exhibit 8). The BoE Financial Stability Report ( June 2017)

and subsequent publications by both the PRA and FCA express concerns about lending

standards and future affordability for borrowers. There is also growing market interest in

what IFRS9 will mean for banks’ reported results, again most notably for consumer credit,

and in its sensitivity to economic deterioration – in both published accounts and in the

results of future regulatory stress tests.

The other obvious source of concern is the effect higher interest rates will have when,

eventually, the BoE lifts them. Low rates have encouraged leverage and inflated the value

of long-term assets. However, given the uncertainties created by Brexit and the consistent

approach of Mark Carney and the MPC, the likelihood of material rate rises anytime soon

must be judged as low.

And, even if credit conditions deteriorate, the much improved capital ratios and debt

funding maturities of UK banks make a repeat of the financial crisis unlikely. This conclusion

is supported by the Bank of England and EBA stress tests, in which UK banks remain viable

under scenarios similar to those of 2008–9 in combination with another round of heavy

misconduct fines.

ExHIBIT 7: NPL RATIO EVOLUTION FOR STRESSED EUROPEAN COUNTRIES 2007–2016

300%

200%

100%

400%

0%

500%

2010 INDEX COUNTRY (2016 NPL RATIO)1

Greece (36%)

Countrieswith remaining NPL problemand no cleardownward trend

Clear downward trend in NPL ratio

Indexed to 2010 = 100%

Portugal (13%1)

Italy (17%)

Spain (6%)Ireland (15%1)

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Source: IMF Global Financial Stability Report, ECB, Oliver Wyman analysis 1. 2016 figures as presented in the IMF Global Financial Stability Report; Portugal and Ireland data is for 2016Q3

Copyright © 2017 Oliver Wyman 6

ExHIBIT 8: UK HOUSEHOLD DEBT TO INCOME 2000–2016

50

100

0

Consumer lending(2016 growth in debt = 6%)

Mortgage lending(2016 growth in debt = 4%)

2000 2002 2004 2006 2008 2010 2012 2014 2016

150PERCENT

Source: ONS, Thomson Reuters, Oliver Wyman analysis

THE IMMEDIATE FUTURE

The evolution of risk management over the last 10 years has been a response to the direct

financial impact of the crisis and to the regulatory agenda that followed. Without another

crisis, its evolution over the coming years will have different drivers. We think three will be

most important.

First, banks continue to operate in very uncertain political and social environments, with

almost no tolerance for further real or perceived misconduct. Second, the competitive

landscape, including both incumbent and disruptive players, will evolve rapidly over the

next five years and this will require a rethinking of many traditional risk management

approaches. Third, investors will ratchet up pressure on banks to consistently meet their cost

of equity and, in addition to constraining losses, risk management is an important part of

both cost containment and revenue growth.

In this context, we think six items should be near the top of a CRO’s current agenda:

1. MANAGING THE NEAR-TERM RISK TRAJECTORY

As noted, there is concern about UK consumer credit and its vulnerability to rising interest

rates and unemployment. Given the post-crisis actions of the Bank of England, credit

losses in the recent past have been benign. Banks must have confidence in their credit

loss forecasting (including under the new IFRS9 accounting standard which is expected to

increase CET1 sensitivity to regulatory stress tests by up to 50 percent) and their ability to

effectively manage significantly higher workloads in collections and recoveries by using

early-warning systems to detect “hotspots” and dynamically allocating scarce experienced

resources. In the next consumer credit cycle conduct issues will also be in focus, and banks

Copyright © 2017 Oliver Wyman 7

will need to ensure that policies, processes, and behaviour incentives are carefully managed,

including questions relating to forbearance.

2. IMPROVING COST AND EFFECTIVENESS

The understandable risk aversion found in many banks can add multiple layers of controls,

going beyond the three lines of defence standard, and beyond what is required by the bank’s

agreed risk appetite. Operating models can benefit from a reset, most often for compliance-

related activities, where structures have evolved rapidly in response to new conduct and

regulatory requirements. Robotic process automation (RPA) is maturing and can now be

applied to an increasing number of standardised tasks. For example, it can reduce process

time by over 50 percent versus previously manual escalation decisions in a transaction

monitoring process, and (demonstrating the complexity of regulatory requirements)

“ChatBot” technology has been used to target a halving in the number of enquiries to

compliance teams. Risk functions must also promote the digitisation of the business. Risk

processes should be “baked in” to new products and workflows from their inception, and not

appended afterwards, which can create a drag on the speed and integrity of execution, and

damages the customer experience.

3. EVOLVING GOVERNANCE FRAMEWORKS AND STRUCTURAL REFORMS

The finalisation of ringfencing, recovery and resolution planning, and now Brexit, throw up a

number of challenges for risk managers. As well as ensuring that new governance structures

can be shown to remain robust under stressed scenarios, the creation of new legal entities

will require the duplication of some activities and the fragmentation of capital and liquidity.

For institutions setting up or significantly expanding Eurozone entities, the additional

requirements of EU IHC entities under SSM supervision will need to be clearly understood

and planned for. Recent client engagements have highlighted the need for management

focus on the careful design of Eurozone entity operating models, and establishing

strengthened governance, risk and control frameworks, so as to avoid short- and medium-

term disruption, and to maximise efficiencies. Location strategies should be put under

renewed focus, particularly under shared service models, with some types of risk operations

(for example, FCC) migrating to mainly offshore or nearshore locations.

4. CONTROLLING NEW THREATS

Concerns around new risks relating to data and cyber risks are front of mind. With increasing

ambitions for the use of data (via big data and advanced analytics techniques) and its wider

distribution (as a result of PSD2), the risks associated with the inappropriate usage or loss

of control of data, multiply dramatically. Managing cyber risk requires banks to have staff

with the right skills, through recruitment or training, and to design effective governance

structures across Line 1 and 2 activities. We estimate that spend on cyber risk now accounts

for 6–8 percent of total IT budget, and that this is increasing. As elsewhere, efforts in cyber

Copyright © 2017 Oliver Wyman 8

security should be guided by risk-return trade-offs. Banks should not spend material sums

on avoiding threats whose probability consists in nothing more than being imaginable.

New risks are not limited to cyber. They can arise out of economic trends, geo-politics,

clients and counterparties, markets and competitors, legislation and regulatory activity,

internal processes and employees, and outsourcing. Properly assessing them requires a

rigorous framework and a management process which ultimately engages the Board. We see

banks increasingly looking to other industries – for example, airlines, pharmaceuticals, the

military – to learn how they continually seek to identify and manage new and critical risks.

5. CONTINUING TO (RE)BUILD REPUTATION AND STRENGTHEN RISK CULTURE

The road to redemption is proving long for UK banks. They remain on the defensive with

the media, the public, politicians and regulators. Banks need to build and display better

risk cultures. Risk teams must engage with the business from the start of innovation and

digitisation processes to ensure that the bank’s reputation and risk culture is protected

under new and changing business models. The risk team must act as an enabler and advisor

to these initiatives rather than an ex-post approver. Raising awareness of risk requires not

only rules but training. We have successfully worked with firms to do this via scenario-based

workshops, bringing risk culture to life with real “dilemmas” faced by each business. Such

training works best when accompanied by a programme of “nudges” to reinforce learnings.

6. ExPLORING AND APPLYING NEW TECHNOLOGIES AND ANALYTICS

The industry has entered an exciting period of technological and analytical innovation.

Banks’ abilities to assemble and manipulate data, and predict trends and propensities,

has changed out of all recognition from a decade ago. New data capture and connection

technologies mean that circumventing legacy system issues is less of a road block than

it has been. Most banks are actively exploring new analytical approaches, including AI

and machine learning. Many of these initiatives are being pursued on an experimental or

champion/challenger basis, and executed using a combination of internal, joint ventured

and crowdsourced resources. Optimising credit decisions in this way can be used to

reduce losses (for example, a 5–10 percent reduction in default rates for a given volume of

applications), grow lending volume (for example, a 10–30 percent increase in new business

while holding credit losses constant), and drive efficiencies (for example by reducing manual

decision making by 50 percent). In compliance, advanced pattern recognition and clustering

techniques have been proven to detect suspicious activity 12 months faster than legacy

systems. Advanced third party solutions are also being incorporated with greater frequency,

enabled by API technology.

Copyright © 2017 Oliver Wyman 9

LOOKING FURTHER AHEAD

With immediate concerns under control, what should a forward-looking CRO be working

on to future-proof the organisation? Because the range of possibilities is wider, risk teams

must prepare across a broad front, and develop increased flexibility to respond. We would

prioritise five areas:

1. CREATE AN AGILE RISK PLATFORM PREPARED FOR MULTIPLE FUTURE SCENARIOS

The banking sector faces a range of future scenarios driven by digital disruption. While

there are “most likely” scenarios, there is still a wide range of possible end states over the

next 5–10 years. At one extreme, it is possible that a purely evolutionary path develops, with

banking incumbents continuing to rule and digital disruption constrained to the margins.

A more likely scenario is that banks continue to dominate, but winners are differentiated by

their ability to exploit new digital opportunities, and to interface or compete with new digital

players in areas where they have established a credible presence. Continuing to push the

range of scenarios, it is possible to envisage a more “even fight”, with current incumbents

and new entrants competing head-on across a wide range of customer segments and

banking services. At the extreme, we could see a scenario where incumbents have largely

been pushed out of many customer segments, and retreat to being utility providers of

balance sheet and cash management services. By definition, it is impossible to pick a single

planning scenario. As a strategic partner to the business, risk management teams should

be fully engaged in the strategic and scenario planning process, and master agile working

practices to accelerate their speed-to-change.

2. MODULARISE THE RISK FUNCTION

Under any of the above scenarios, banks and their risk management teams face a much

more modularised future. Risk managers should assess where each of their current and

future activities can best be performed. Could tasks that remain in-house be migrated to

offshore or near shore locations? Could they be delivered by a similar group elsewhere in

the organisation, such as behavioural analytics? Could they be automated/robotised, or

rely much more heavily on third-party applications? Many banks are already considering

which tasks may be more efficiently delivered by industry utilities or third-party solutions (for

example, AML checks), or where outsourcing or crowdsourcing of analytical development

offers advantages. Based on client work we have already undertaken, there is big difference

in the number of FTEs assigned to internal risk management teams under different industry

scenarios. Under an evolutionary scenario banks are expecting efficiency gains to bring

a 10–20 percent reduction in risk resources, whereas under a fully modularised outcome

internal risk FTEs could reduce by up to 80 percent. Under any likely scenario, vendor

management will become a more important capability for risk functions.

Copyright © 2017 Oliver Wyman 10

ExHIBIT 9: THE RISK FUNCTION OF THE FUTURE WILL FOCUS MORE ON VALUE ADDING AREAS

CURRENT RESOURCE LOCATION

50%

20%

15%

15% 25%

35%

25%

15%Identification and advanced analytics

Management and operations

Traditional risk activities

Stategic risk advice

FUTURE RESOURCE LOCATION

Source: Oliver Wyman analysis

3. BUILD THE NExT GENERATION OF RISK TALENT

The changes outlined above mean that the skills required for tomorrow’s risk organisation

will be quite unlike today’s, with a refocusing of skills away from traditional “production”

activities and towards adaptable analytic and advisory skills (see Exhibit 9).

Success will require risk functions to attract and retain talent that will be competed for both

internally and externally across a range of industries. We consistently find that senior risk

professionals put talent management and influencing skills at the top of their leadership

development requirements.

4. CREATE DATA AS FLExIBLE AS THE ORGANISATION

The more open-ended and query-driven nature of the regulatory “ask”, and the importance

of data flexibility and accuracy across both risk and finance systems, mean that much

remains to be done at many banks. Regulatory and accounting changes continue to

drive the overlap between risk and finance data requirements. Features of the risk data

architecture are often the result of quick responses to new regulation rather than based

on first principles and a target architecture. A number of institutions are exploring a

combined data utility across risk and finance which is independent of current processes and

technology. Exhibit 10 shows typical target architecture.

This is another area where risk and finance teams need to engage in a strategic dialogue with

other areas of the firm, for example, concerning the bank’s API strategies.

Copyright © 2017 Oliver Wyman 11

ExHIBIT 10: INTEGRATED OLIVER WYMAN FRAMEWORK FOR FINANCE AND RISK DATA INFRASTRUCTURE AND MANAGEMENT

FINANCE AND RISK REPORTING OPERATING MODEL

I. Data governance and organisation

II. Change management

Typically finance(Accounting and controlling)

Mandatory external

reporting

Internal management reporting andbank steering

1. Steering support (reporting and analysis)

2. Calculation and methodological capabilities

3. Data

4. Applications (software)

5. Infrastructure (hardware)

Integrated risk measurement

and controlling

Individual risk type risk

measurementand controlling

ALM and liquidity

management

Typically risk Typically treasury

III. D

ata

pol

icie

s,st

and

ard

s an

d m

etri

cs

IV. Data service p

rocesses

Finance and riskdata reporting infrastructure

Finance and riskdata service model

Finance and riskreporting operating model

Source: Oliver Wyman

5. DELIVER ON ANALYTICS AND AUTOMATION

Drawing on the learnings from experimentation with advanced analytic and automation

techniques, risk teams should construct a portfolio of ambitious initiatives to deliver more

effective and efficient decision making. These will include big data applications, pattern

recognition and real-time preventative controls, and increasingly ambitious robotic process

automation. Applying RPA within risk and compliance investigation processes can already

raise productivity by 30–40 percent. But recent advances in cognitive RPA can reduce

workloads by more than 70 percent, freeing up resources for higher value activities. The new

capabilities will need to be integrated into new digital businesses and digitised customer

journeys. Banks are already exploring “social listening” to track customer experience and

identify potential conduct issues. Model risk and model governance will also need to be

rethought, particularly with respect to third party management. The model set must be

continually managed for suitability, performance, and regulatory compliance. Asking the

question “will there be more or fewer models in the future?” does not always elicit the same

answer, as the challenges and costs of managing a large model set becomes more apparent.

Using machine learning across large and newly combined data sets has allowed some

institutions to reduce the number of models they use by an order of magnitude, while also

allowing a much higher frequency of model enhancement and recalibration.

Copyright © 2017 Oliver Wyman 12

CONCLUDING REMARKS

Risk management is at a fascinating point in its evolution. Now recognised to be not

only fundamental to the bank’s financial stability and regulatory compliance, but also an

essential part of a bank’s strategy and operational effectiveness, risk management faces a

period of large scale change. Under any of the scenarios that may play out in banking, risk

functions will need to hone their abilities in many areas. They will need to be able to identify

and address new risks quickly, be more agile and modular, deliver new technology and

techniques rapidly, and work increasingly in partnership with finance, operations, and the

businesses. These changes will require them recruit, develop, and retain staff with skills that

differ significantly from those that are found in risk functions today.

Copyright © 2017 Oliver Wyman 13

www.oliverwyman.com

Oliver Wyman is a global leader in management consulting that combines deep industry knowledge with specialised expertise in strategy, operations, risk management, and organisation transformation.

For more information please contact the marketing department by email at [email protected] or by phone at one of the following locations:

EMEA

+44 20 7333 8333

AMERICAS

+1 212 541 8100

ASIA PACIFIC

+65 6510 9700

Copyright © 2017 Oliver Wyman

All rights reserved. This report may not be reproduced or redistributed, in whole or in part, without the written permission of Oliver Wyman and Oliver Wyman accepts no liability whatsoever for the actions of third parties in this respect.

The information and opinions in this report were prepared by Oliver Wyman. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisors. Oliver Wyman has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Oliver Wyman disclaims any responsibility to update the information or conclusions in this report. Oliver Wyman accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages. The report is not an offer to buy or sell securities or a solicitation of an offer to buy or sell securities. This report may not be sold without the written consent of Oliver Wyman.