the future of pension systems - european...

TRANSCRIPT

1 Jürgen Kohl October 2003

Eurobaromètre spécial

THE FUTURE OF PENSION SYSTEMS

Fieldwork: September - October 2001

Publication: January 2004

Spe

cial

Eur

obar

omet

er 1

61/

Wav

e 56

.1-

Eur

opea

n O

pini

on R

esea

rch

Gro

up E

EIG

This survey was requested by Directorate General Employment and Social Affairs and coordinated by Directorate General Press and Communication

This document does not represent the point of view of the European Commission.

The interpretations and opinions contained in it are solely those of the authors.

Special Eurobarometer

EuropeanCommission

2

This public opinion survey was carried out at the request of the Directorate-General

Employment and Social Affairs and organised by the Public Opinion Analysis Sector of the

Directorate-General Press and Communication.

It was conducted in all the Member at States of the European Union between September 17

and October 26, 2001, under the general coordination of the European Opinion Research

Group EEIG in Brussels.

The technical specifications, the names of the institutes involved in the research and the

questionnaire are annexed.

The European Commission accepts no liability of any kind arising from this report.

The original language of this report is English.

3

TABLE OF CONTENTS Executive Summary ..........................................................................................................................4 Introduction ....................................................................................................................................12 1. Background characteristics of the pensioner population...........................................................14

1.1. Proportion of pensioners within the European Union.............................................................14 1.2. Retirement age......................................................................................................................16

2. Economic well-being of pensioners............................................................................................18 2.1. Standard of living .................................................................................................................18

2.1.1. Current standard of living............................................................................................18 2.1.2. Expected standard of living .........................................................................................21 2.1.3. Comparison of standard of living before and after retirement.......................................24

2.2. Benefit level of state pensions...............................................................................................26 2.2.1. Pensioners...................................................................................................................26 2.2.2. Non-pensioners ...........................................................................................................28 2.2.3. Aspiration level of future pensioners ...........................................................................30

3. The composition of pensioners’ household income ...................................................................33 3.1. Sources of income for current pensioners ..............................................................................33

3.1.1. Main source of income ................................................................................................33 3.1.2. The second most important source of income ..............................................................36

3.2. Expected sources of income for future pensioners .................................................................36 3.3. Preferred sources of income for pensioners ...........................................................................40

4. Goals and principles of pension systems....................................................................................44 4.1. Goals ....................................................................................................................................44

4.1.1. Prevention of poverty in old age..................................................................................44 4.1.2. Maintaining an adequate standard of living..................................................................46 4.1.3. Reducing social inequalities amongst elderly...............................................................48

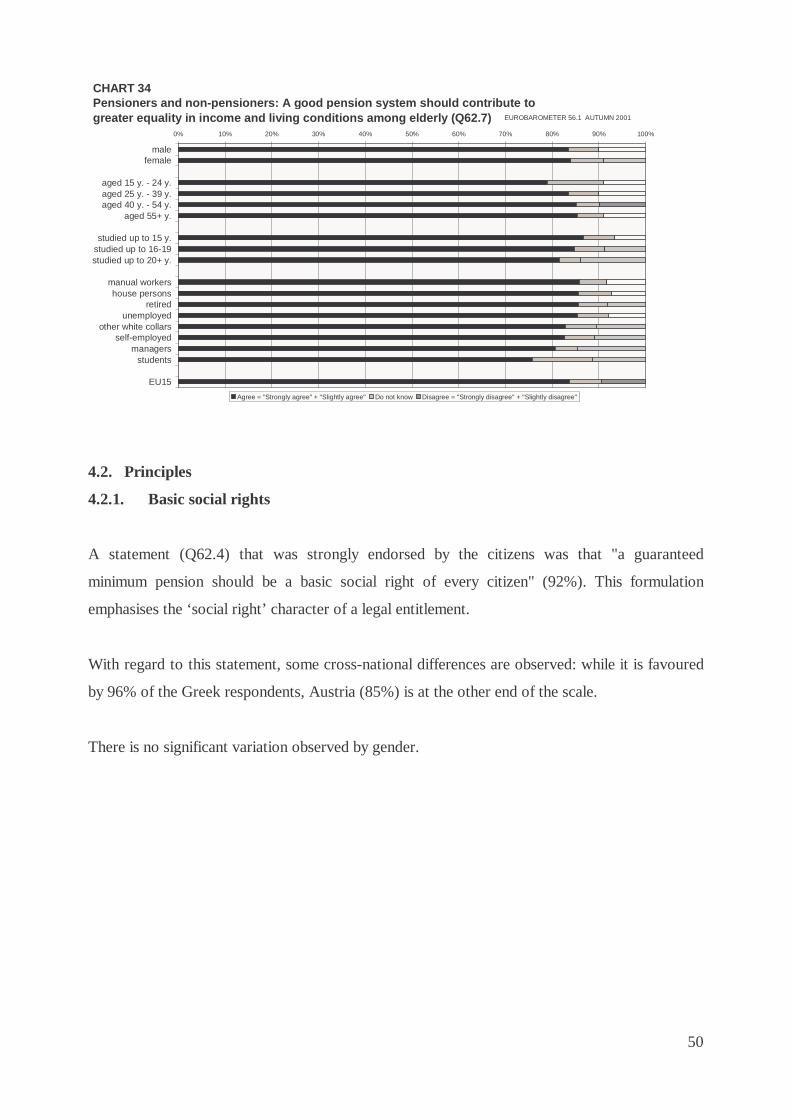

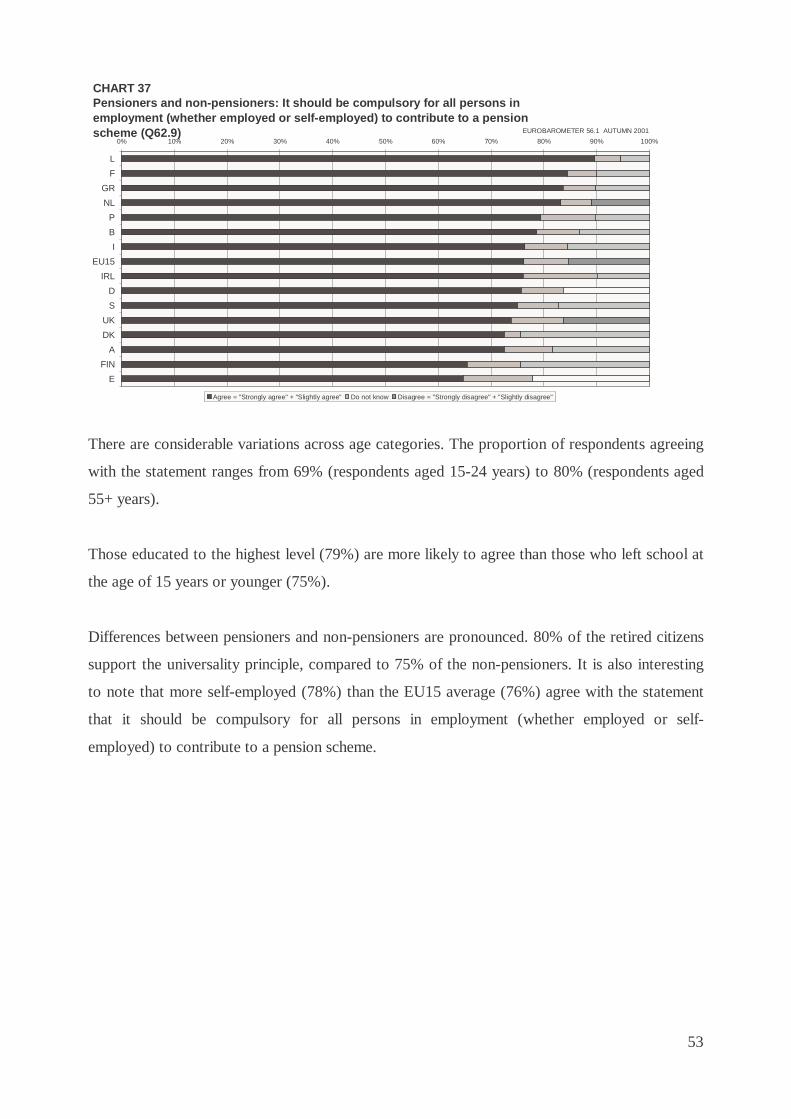

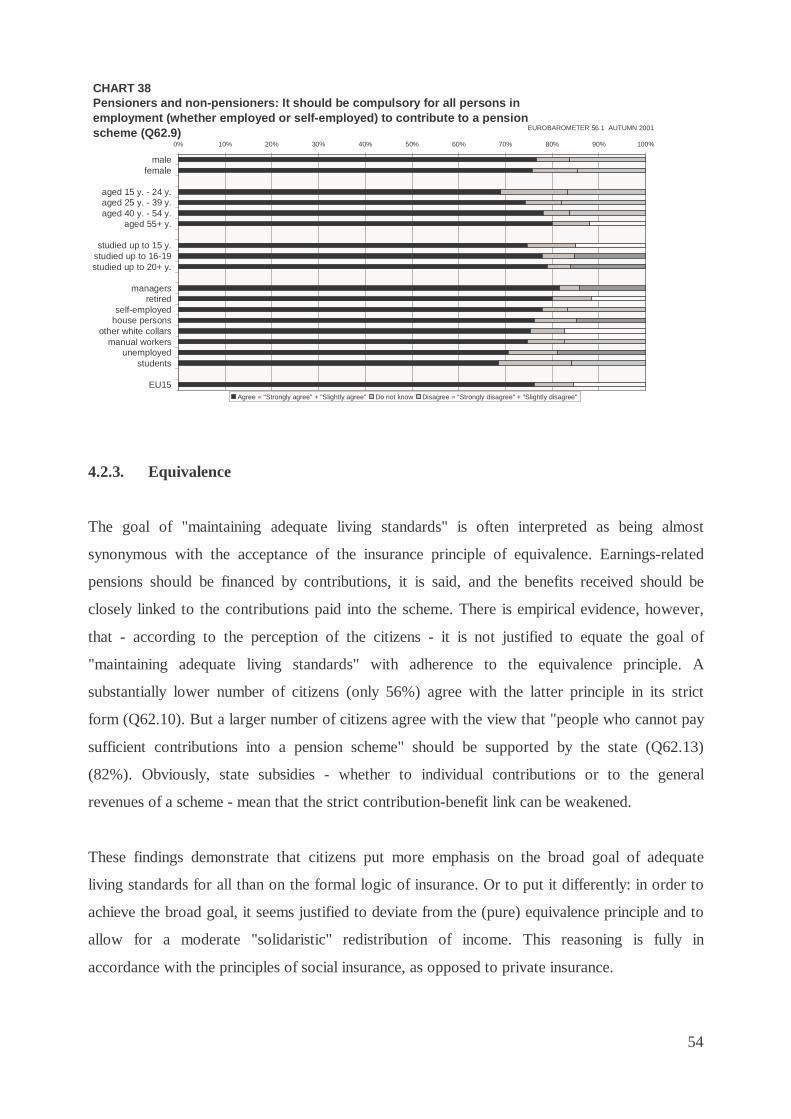

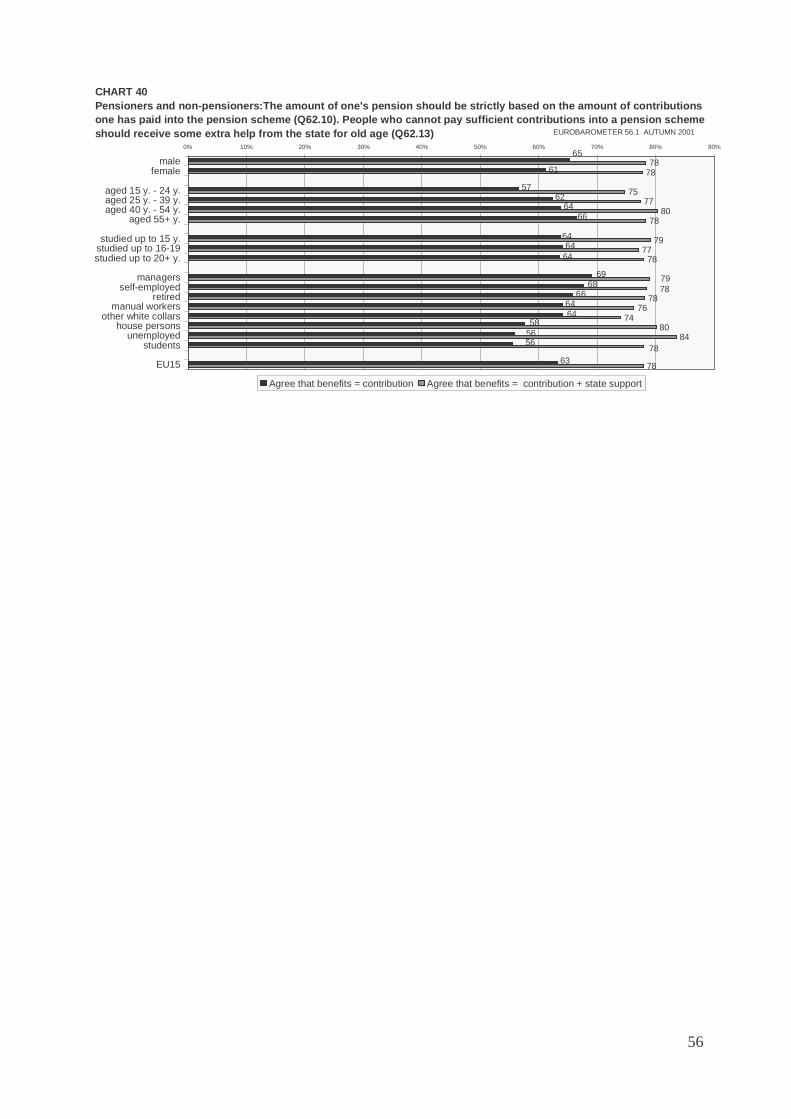

4.2. Principles..............................................................................................................................50 4.2.1. Basic social right.........................................................................................................50 4.2.2. Universality ................................................................................................................52 4.2.3. Equivalence ................................................................................................................54

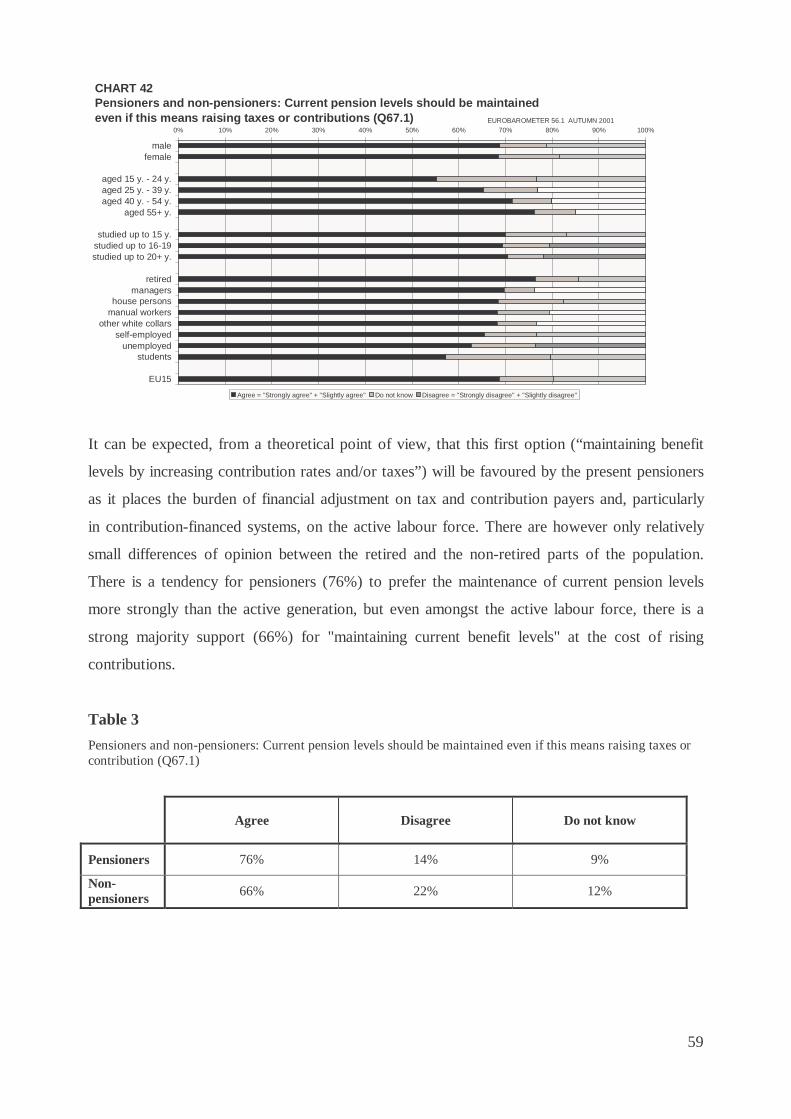

5. Opinions on current policy proposals........................................................................................57 5.1. Direct changes in parameters of pension systems ..................................................................57

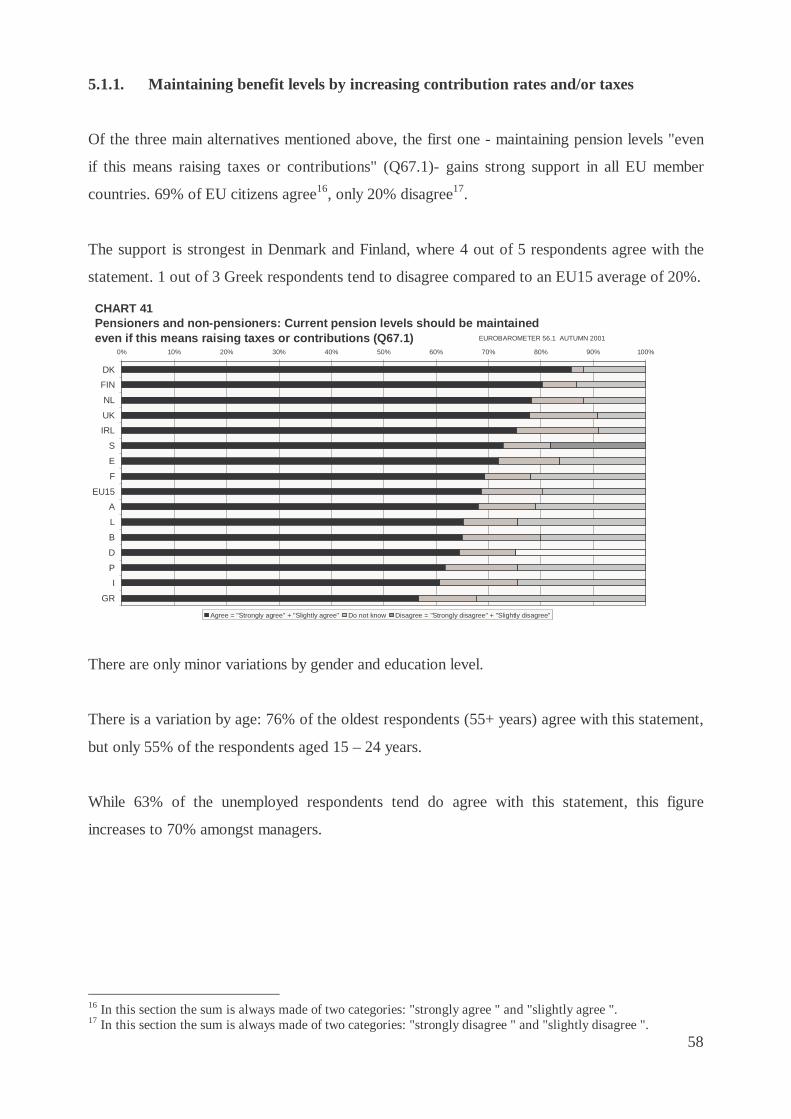

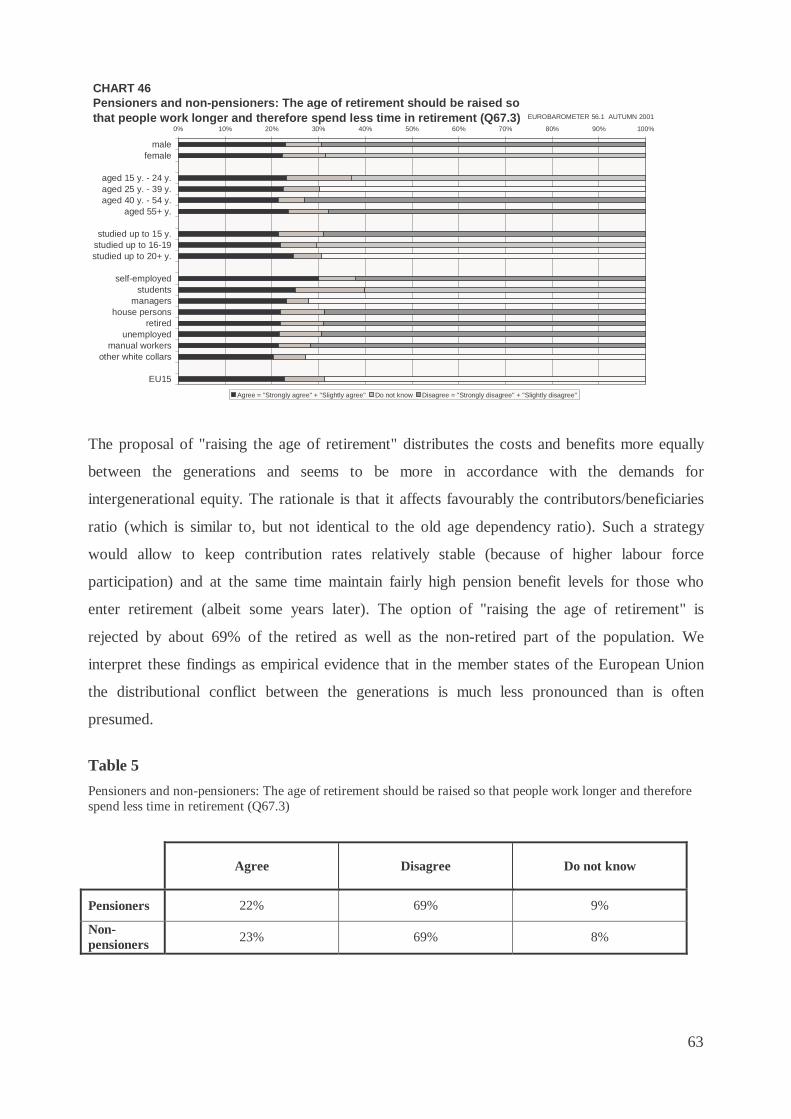

5.1.1. Maintaining benefit levels by increasing contribution rates and/or taxes ......................58 5.1.2. Reducing benefit levels in order to maintain contribution rates ....................................60 5.1.3. Raising the age of retirement .......................................................................................62

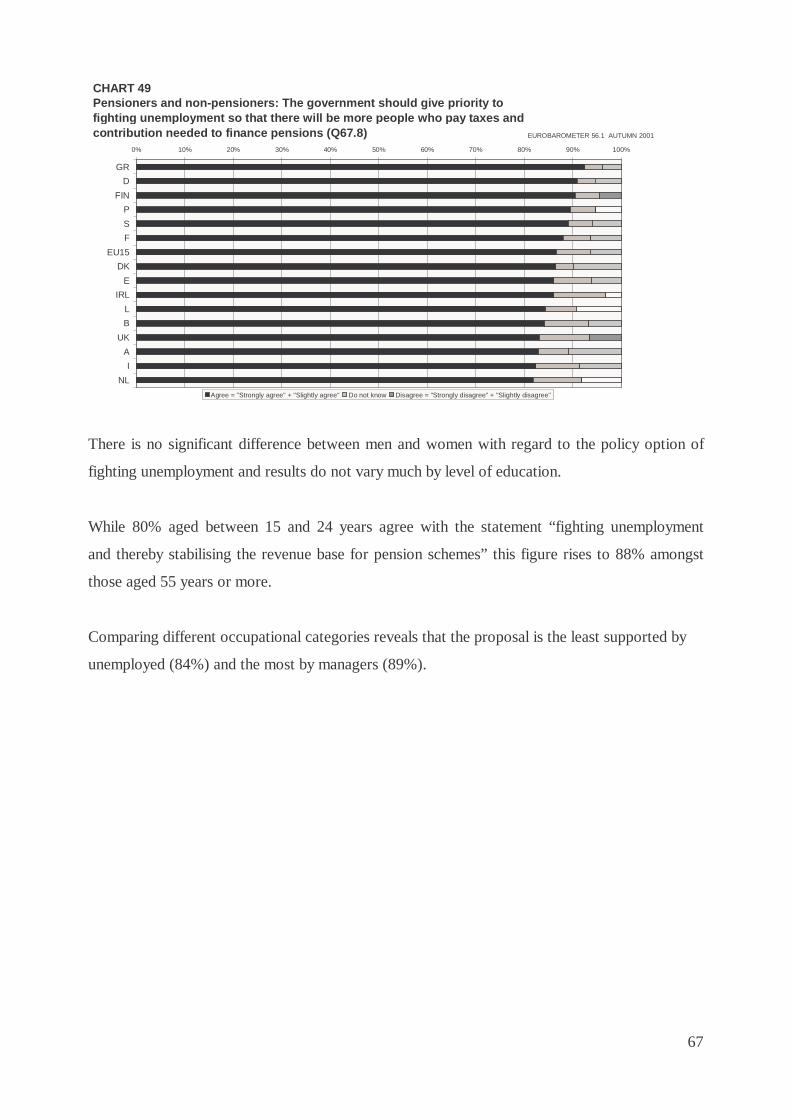

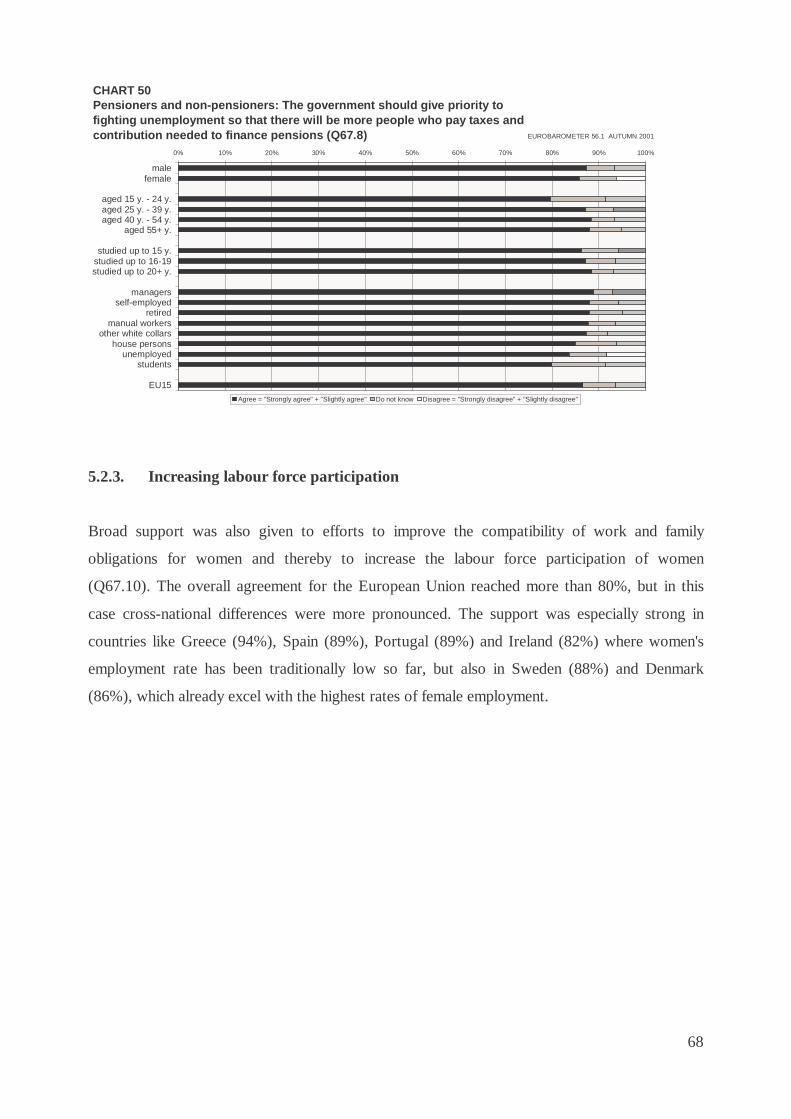

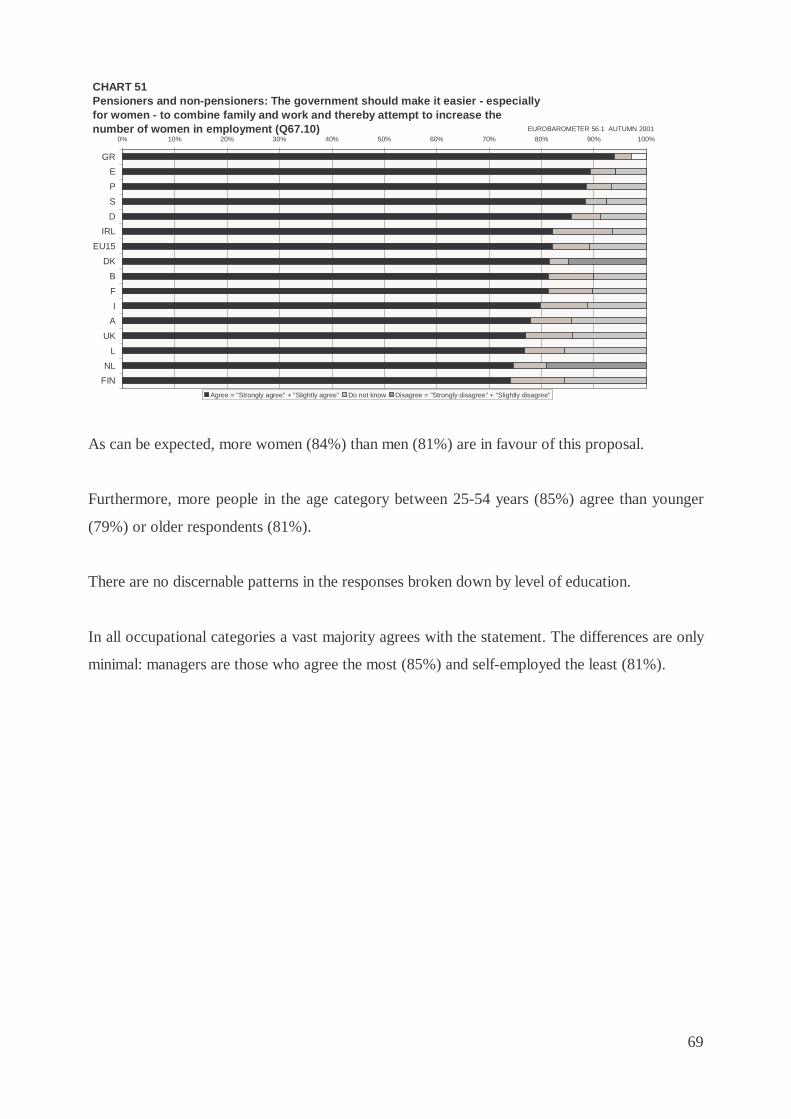

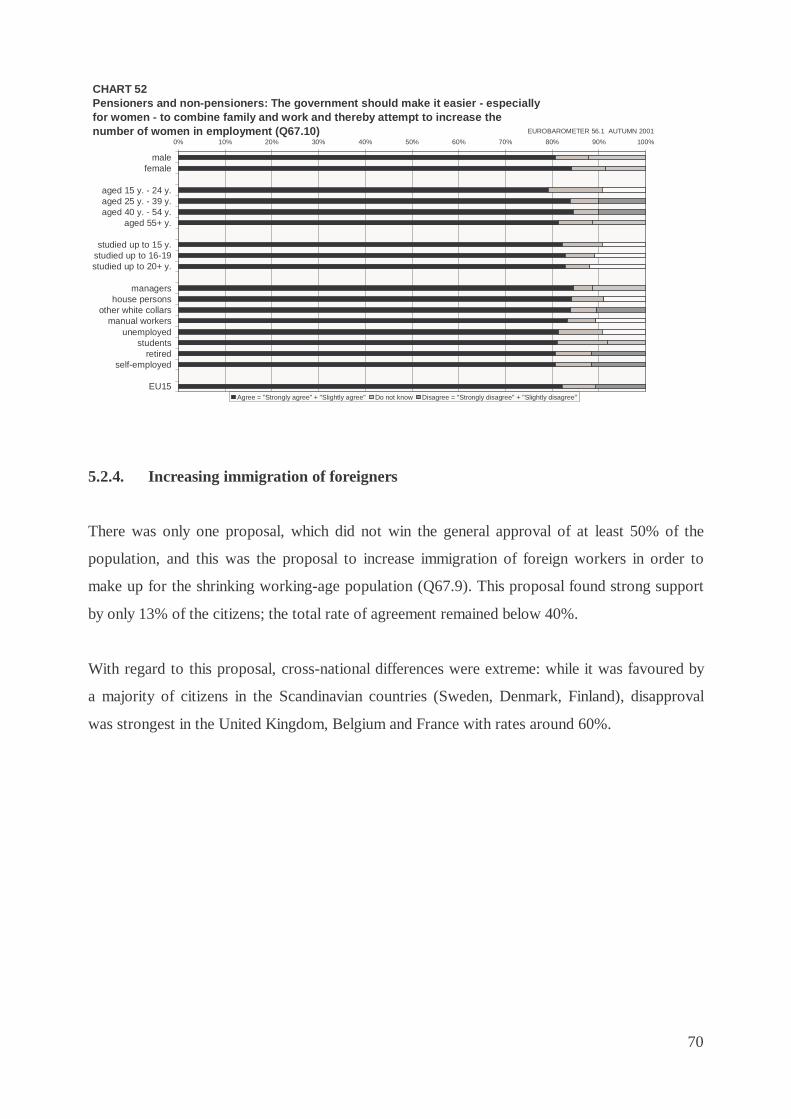

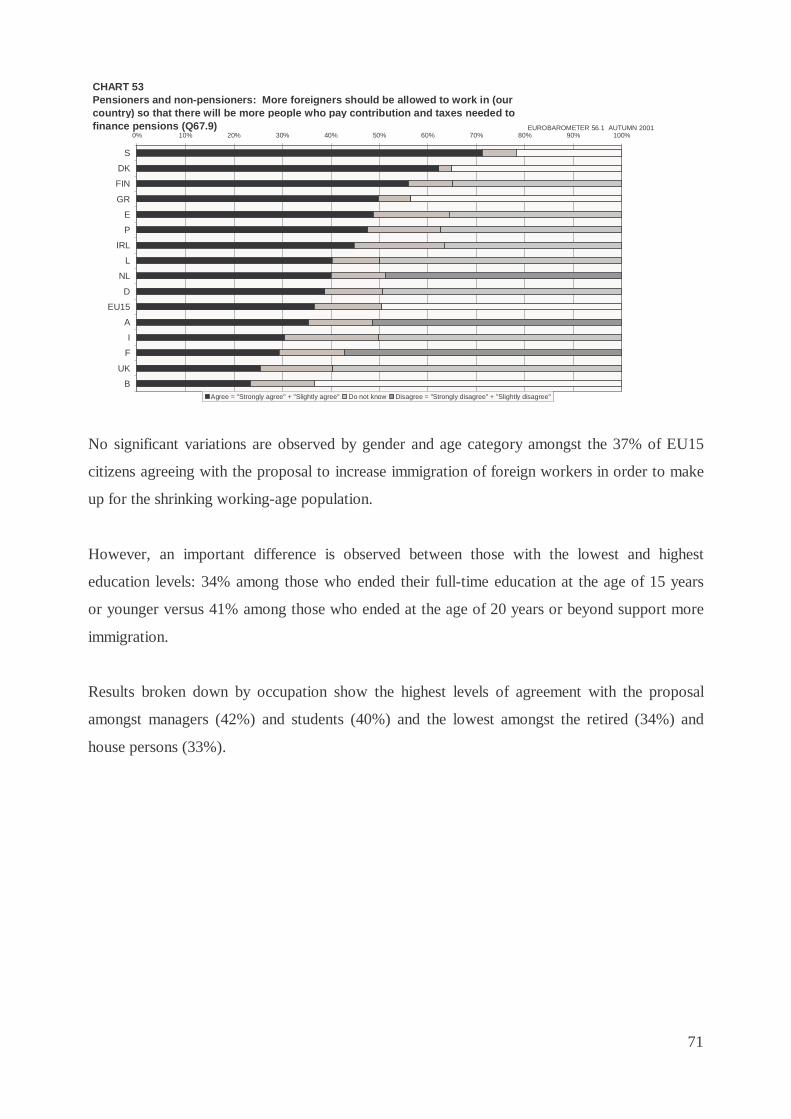

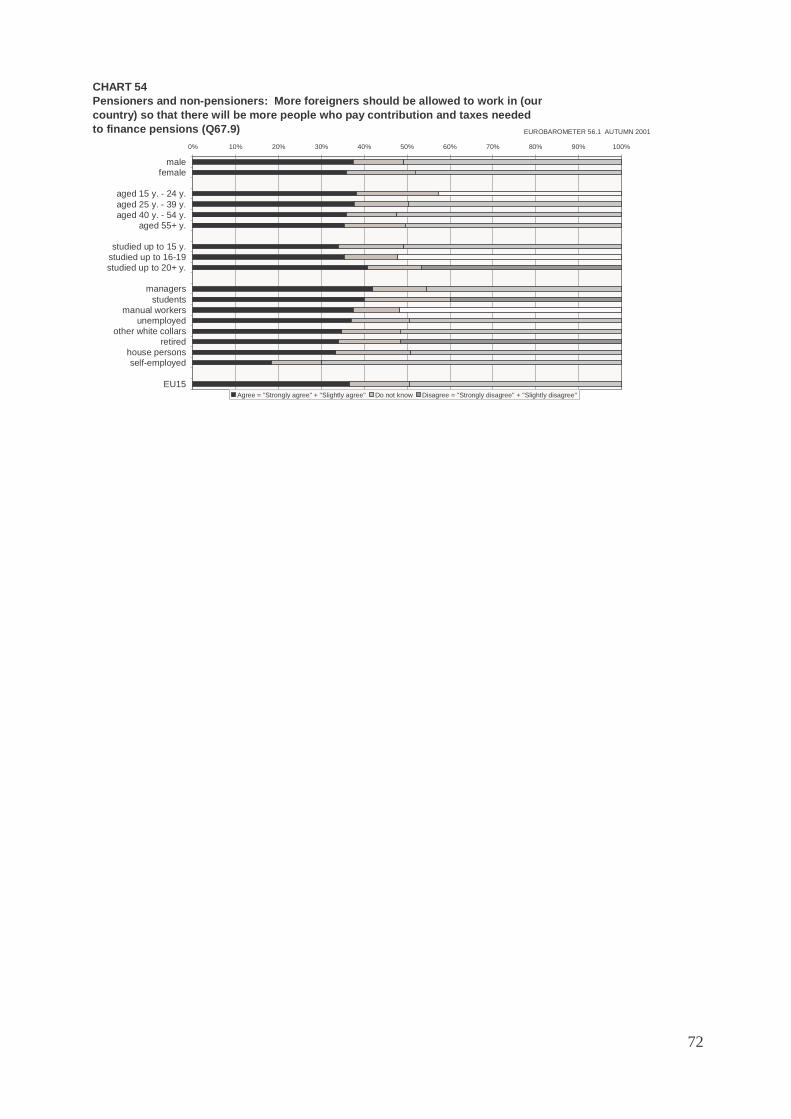

5.2. Indirect changes in parameters of pension systems ................................................................64 5.2.1. Cutting expenditures in other policy areas ...................................................................64 5.2.2. Fighting unemployment ..............................................................................................66 5.2.3. Increasing labour force participation............................................................................68 5.2.4. Increasing immigration of foreigners ...........................................................................70

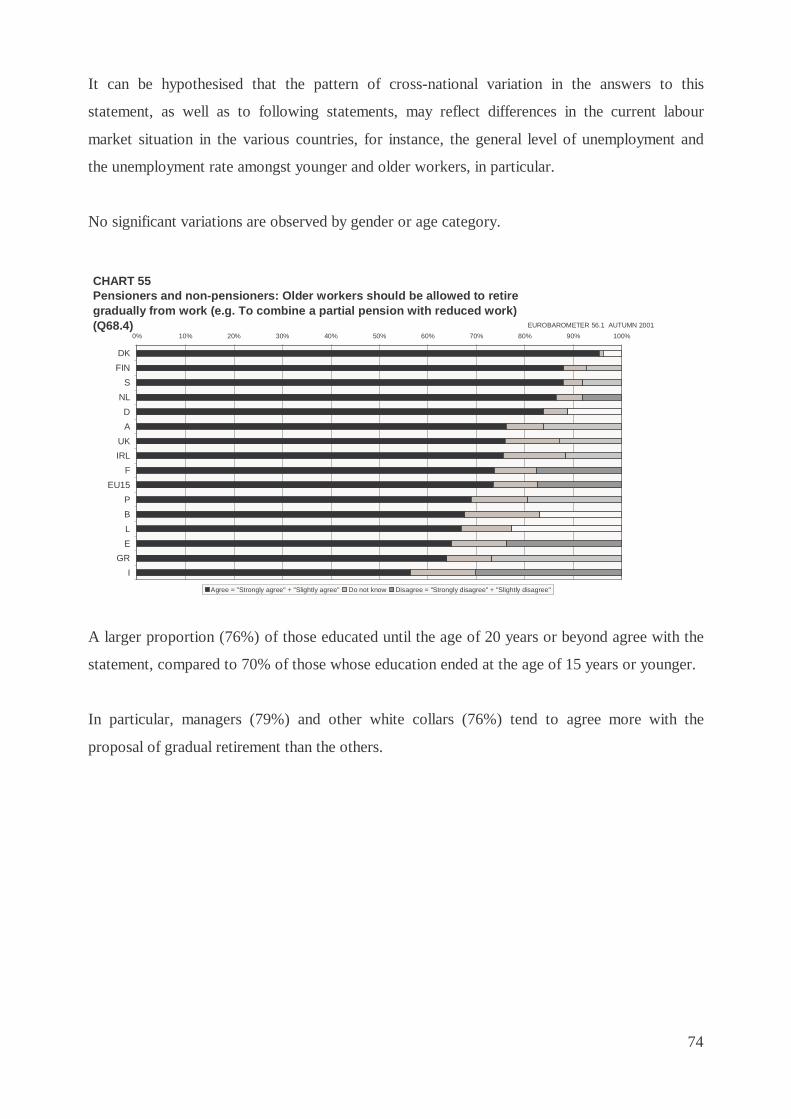

6. Opinions on transition from work to retirement ......................................................................73 6.1. Gradual retirement ................................................................................................................73 6.2. Fixed retirement age .............................................................................................................75 6.3. Influence of retirement age on pension benefits.....................................................................77 6.4. Incentives to retire later ........................................................................................................80

Conclusions .....................................................................................................................................83 Annexes ..........................................................................................................................................86 Annex I: English questionnaire.....................................................................................................87 Annex II : Technical specifications ............................................................................................102 Annex III : List of charts ............................................................................................................104 Annex IV : List of tables ............................................................................................................107

4

EXECUTIVE SUMMARY

Pension reform is currently on the agenda of many national governments and parliaments in the

European Union. While mass unemployment and sluggish economic growth have short-term

effects on the balances of revenues and expenditures of pension schemes (as well as on social

protection schemes in general), longer term structural problems are posed by the shifting

demographic structure (the ageing process) in advanced societies and by increasing life

expectancy. Changes in family structures and in patterns of labour force participation as well as

in working time arrangements and working conditions create additional challenges.

Public acceptance of reform measures is a crucial condition for social policy reform efforts.

Therefore, a comparative cross-national survey on the opinions and attitudes of EU citizens

about pension issues was set up. The survey seeks an answer to the questions such as whether

citizens’ opinions on pension issues vary as much as the existing pension systems in the

member countries do and whether there is a growing awareness of common problems and a

similarity of envisaged solutions to these problems.

This executive summary reflects the views of the EU citizens about pension issues which were

gathered between 17 September and 26 October 2001. Views are assessed across the European

Union and results are presented according to results at EU level and country level.

The present generation of pensioners does not perceive their living standard as

substantially lower than that of the working-age population.

The perception of current living standards is very similar among pensioners and people of

working age. Half of the working-age population describes their present standard living as

average, and 25% as being positive. Amongst pensioners, the percentages of those who describe

their situation as average or positive are only slightly smaller.

However, considerable cross-national differences can be observed concerning the perception of

the present living standards. Pensioners in the Netherlands, Luxembourg, the United Kingdom,

Ireland, Denmark and Greece view their current standard of living much more favourable than

the EU citizens at large. In Portugal, 46% of the citizens describe their living standard as

negative.

5

These differences may be partly due to differences in the general level of economic wealth and

prosperity of countries and their economic performance in recent years. But partly, they are

certainly also due to widely differing institutional arrangements for social security in old age

and, hence, to differences and deficits in the social protection systems of the member states.

For the overwhelming majority of the present generation of pensioners, state or public

pensions constitute the most important source of income.

78% of the pensioners report that state or public pensions are their main source of income.

Other types of income only represent the main source of income for small minorities of

pensioners: for 8% the main income source is occupational pensions, for an additional 3% it is

personal pensions and even fewer pensioners report another main source such as other social

and private transfers, returns from savings or real estate or continued earnings.

There are some major cross-national differences in the main source of income. In Greece, 96%

of the pensioners report that the compulsory state or public pension is their main source of

income. In Finland, on the other hand, the smallest proportion of respondents (12%) says that a

state pension is their main source of income. Finland is the only European Union country where

respondents indicate occupational pensions as the main source of income for current pensioners.

However, this is due to the perception of the statutory earnings-related pension schemes as

occupational schemes.

The current working-age population is more skeptical than the current pensioners

regarding the benefit level of the state pension.

Half of the pensioners report that they do not experience problems getting by with their current

state pension benefit, while only 21% of the working-age population expect not to have

problems.

The aspiration level seems to be quite high. When asked what income replacement level they

would consider sufficient, 53% of respondents would only consider a net income replacement

level of 70% or more as sufficient for the retirement phase; another 16% say they would need

50%-70% of their pre-retirement income, but only 2% can imagine considering an income

6

replacement level of less than 50% as sufficient. However, almost one third of the respondents

could not give a clear indication of what income level they would consider sufficient. As the

respondents come closer to retirement age, the aspiration level drops: around 60% of the

respondents aged 25-54 years consider a net income of 70% or more as sufficient versus 52% of

the non-pensioners older than 55 years.

For future pensioners, state or public pensions are expected to remain the most important

source of income.

61% of the future pensioners expect that state or public pensions will be their main source of

income after retirement. Private pension plans (10%) and occupational schemes (9%) are

expected, by the present working-age population, to gain importance.

In all countries, the current working-age population expects the importance of state or public

pensions to diminish. But in almost all countries, they should continue to be the most important

single source of income for elderly. In Denmark and the United Kingdom, the predominance of

public pensions is, however, expected to be surpassed by occupational and personal pension

schemes taken together.

Non-pensioners would like occupational pension schemes to play a substantial larger role

than that they will probably play in the future.

The non-pensioners were asked how pension benefits should be provided. A majority of the

non-pensioners (56%) shares the opinion that it should mainly be provided by public pension

schemes, while 61% expect these to be the main source of income after retirement.

Substantially more non-pensioners, albeit still a minority, (23%) would like occupational

pension schemes to play a larger role than they will probably play in the future (9% expect them

to play a larger role). Conversely, they would ascribe a smaller role to private arrangements

(8%) than they expect them to play in the future (10%).

In almost all countries non-pensioners desire that public or state pensions are the most

important single source of income for the elderly. Only the Finnish, Dutch, Danish and German

7

non-pensioners desire that occupational and personal pensions (taken together) get more

importance than state or public pensions.

There seems a broad consensus amongst European citizens concerning the goals of

pension policies and even about the prioritisation of certain goals.

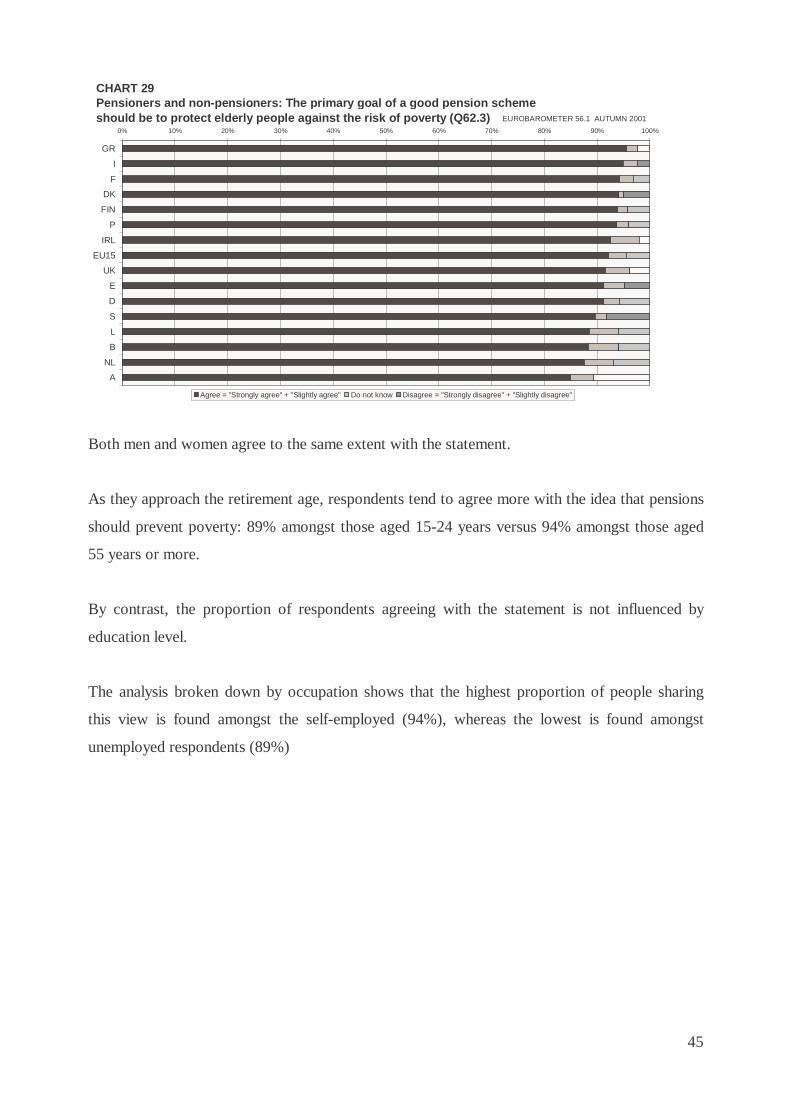

92% of the EU citizens agree with the statement that “the primary goal of a good pension

scheme should be to protect elderly against the risk of poverty”. The proportion of people who

agree with the statement that stresses the social protection function ranges from 96% in Greece

to 85% in Austria. Greece is followed by Italy (95%), France and Denmark (94% each).

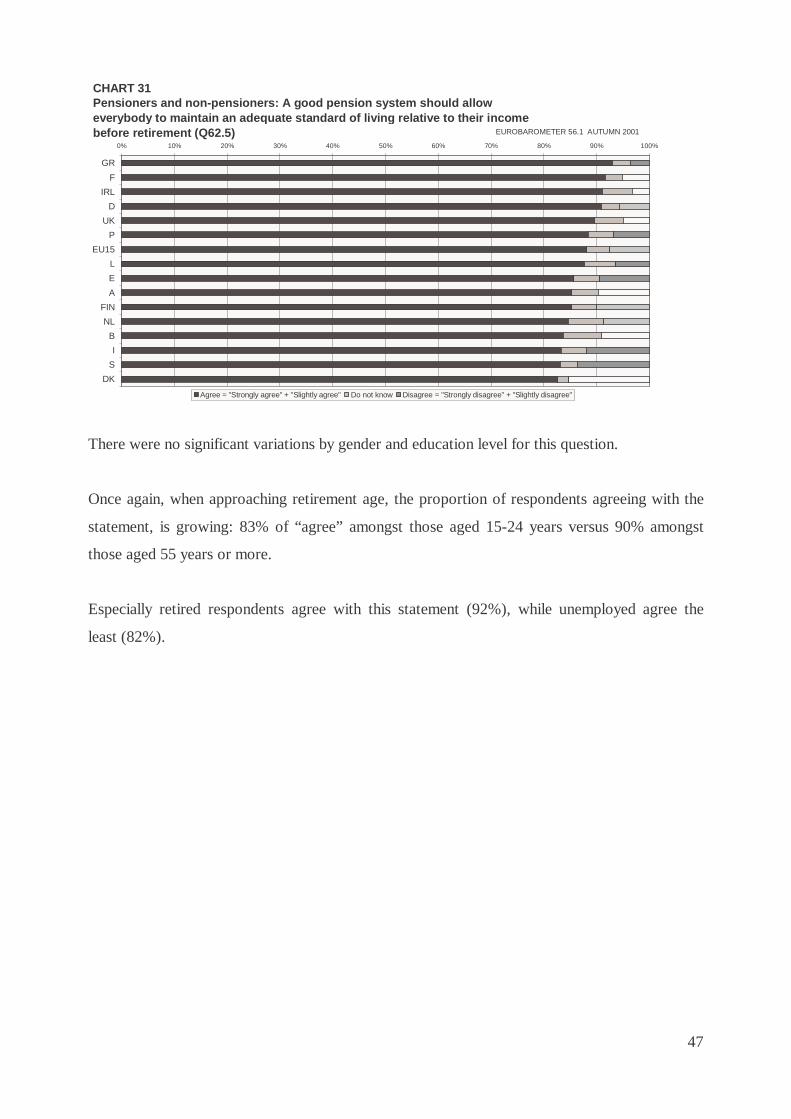

88% of the citizens demand that “a good pension system should allow everybody to maintain an

adequate standard of living relative to their income before retirement”. The support for this

statement ranges from 93% in Greece to 83% in Denmark and is especially strong in countries

like Greece, France, Ireland, Denmark and the UK: more than nine out of ten respondents agree

with it.

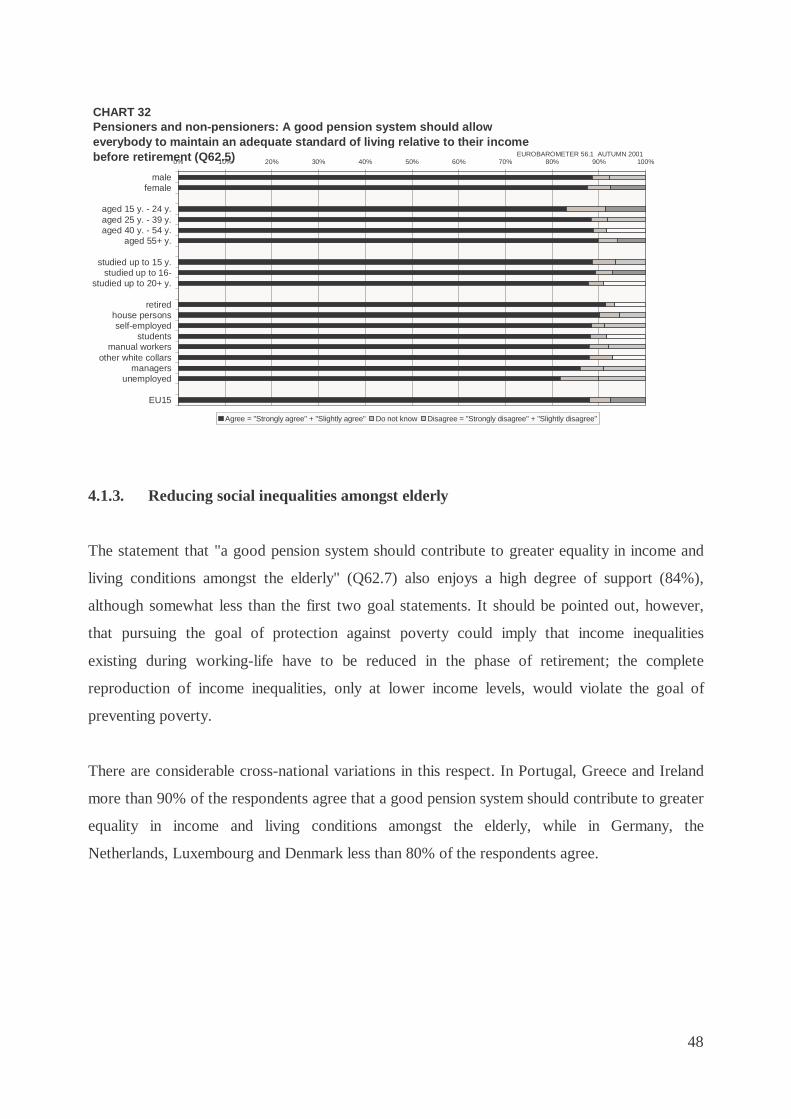

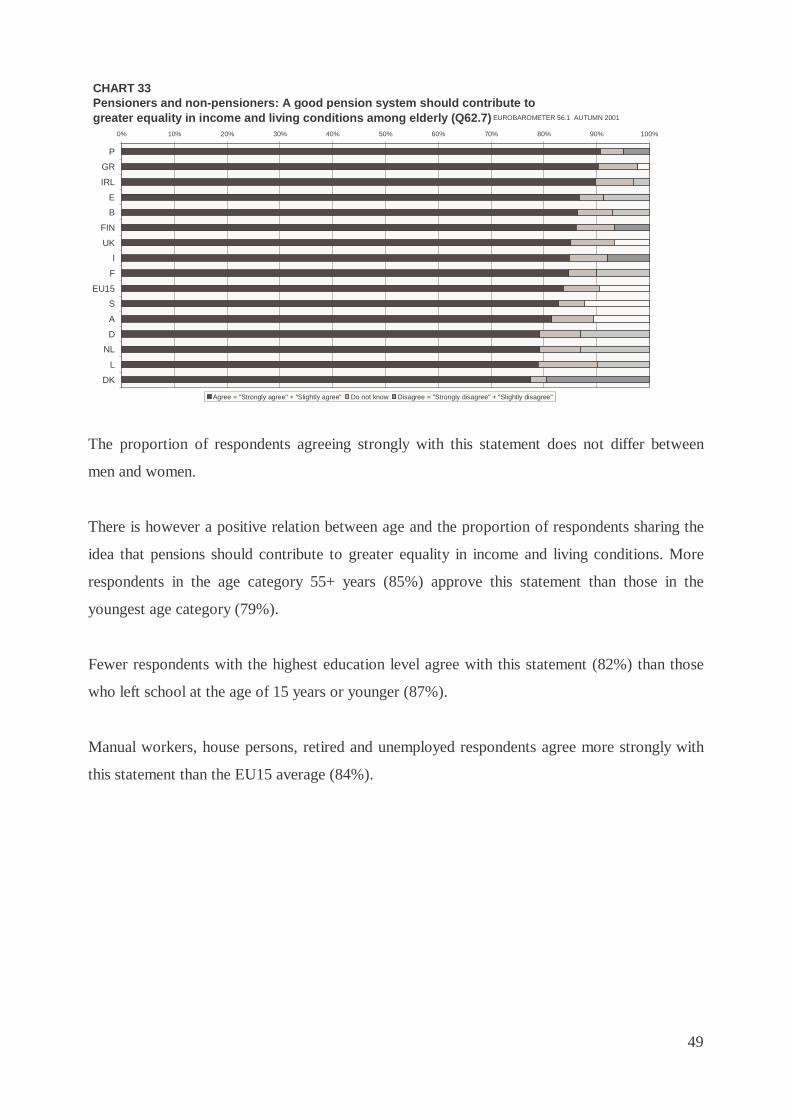

84% support that “a good pension system should contribute to greater equality in income and

living conditions amongst the elderly”. The support is also high, although somewhat less than

the first two goal statements and ranges from 91% in Portugal to 78% in Denmark. In Portugal,

Greece and Ireland more than 90% of the respondents agree that a good pension system should

contribute to greater equality in income and living conditions amongst the elderly.

These findings may be good news for the prospects of European social policy. They are

evidence that the value orientations and the social policy attitudes of citizens in the EU member

countries do not fall as far apart as the institutionalised forms of social security do (especially in

the field of pensions). In other words: for historical reasons, pension systems in the various

European countries have developed in very different ways and have exhibited few signs of

convergence in institutional terms. But there seems to be a great deal of consensus at the level

of citizens’ expectations and evaluations of what constitutes a good pension system.

8

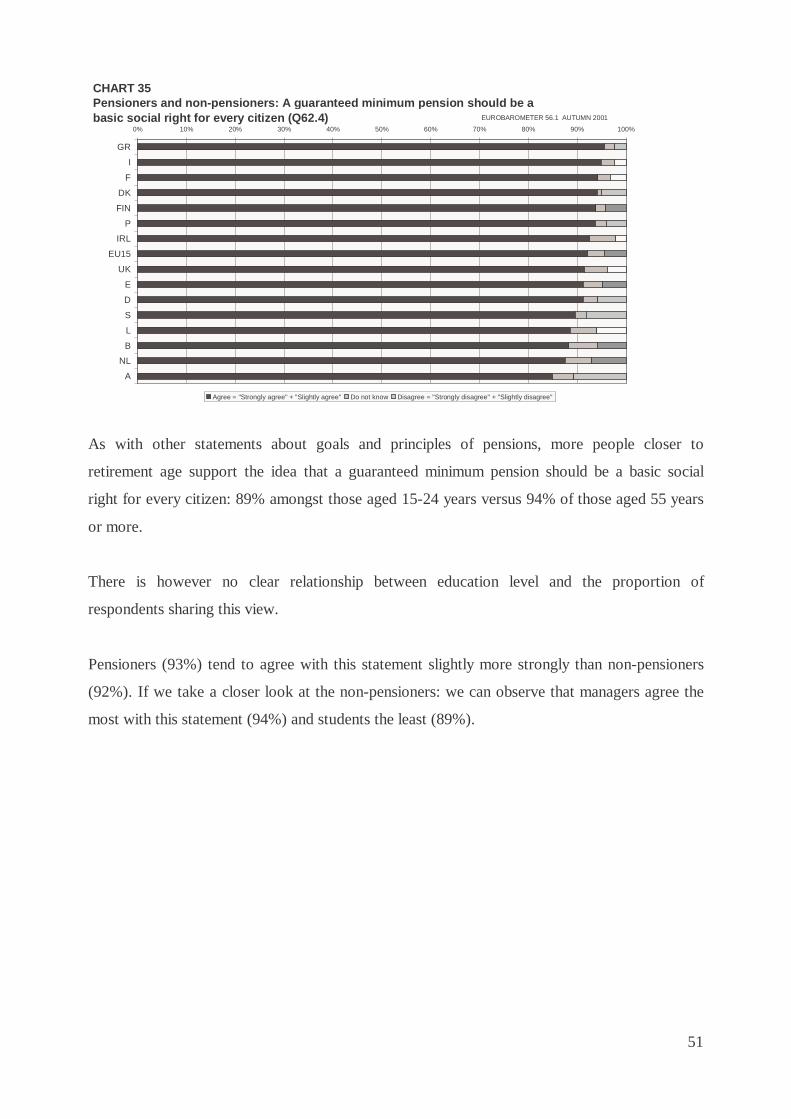

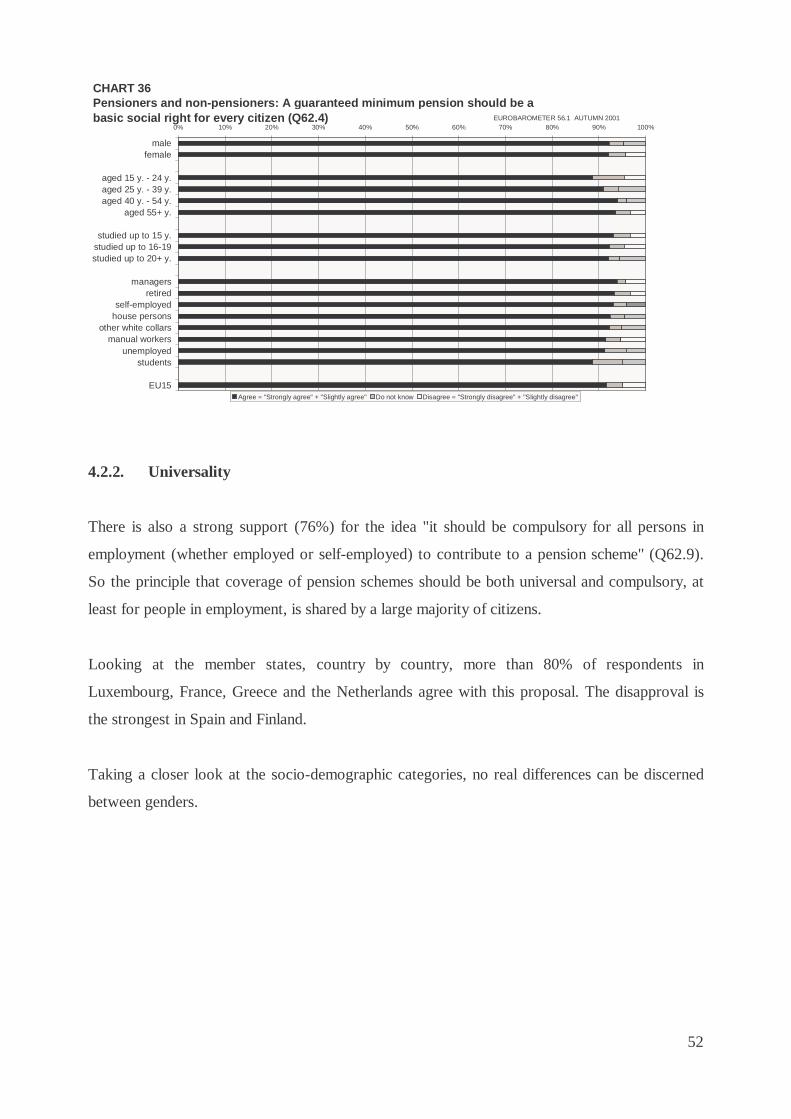

Almost all respondents endorse the basic social right principle of pensions.

92% of the EU citizens agree with the statement that “a guaranteed minimum pension should be

a basic social right of every citizen”. With regard to this statement, the cross-national

differences vary between 96% in Greece and 85% in Austria.

In order to achieve the broad goal of adequate living standards, it seems justified to

deviate from the (pure) equivalence principle and to allow for a moderate “solidaristic”

redistribution of income.

A substantially lower number of citizens (56%) agree with the statement that “the amount of

one’s pension should be strictly based on the amount of contributions one has paid into the

pension scheme”. But a larger number of citizens (82%) agree with the view that "people who

cannot pay sufficient contributions into a pension scheme" should be supported by the state.

In all countries a larger proportion of citizens agree with the “solidaristic” redistribution of

income than with the strict equivalence principle. Germany is the only exception in this regard:

German citizens put more emphasis on the equivalence principle than on the “solidaristic”

redistribution of income.

Maintaining current pension levels “even if this means raising taxes or contributions”

gains the broadest support, while raising the age of retirement “so that people work

longer and therefore spend less time in retirement” proves to be least popular in almost all

EU member states.

Of the three alternatives that have a direct influence on the parameters of pension systems,

“maintaining pension levels, even if this means raising taxes and contributions” gains strongest

support: 69% of the EU citizens agree. The support is the strongest in Denmark and Finland,

where four out of five respondents agree with the statement. One out of three Greek respondents

tend to disagree compared to an EU15 average of 20%.

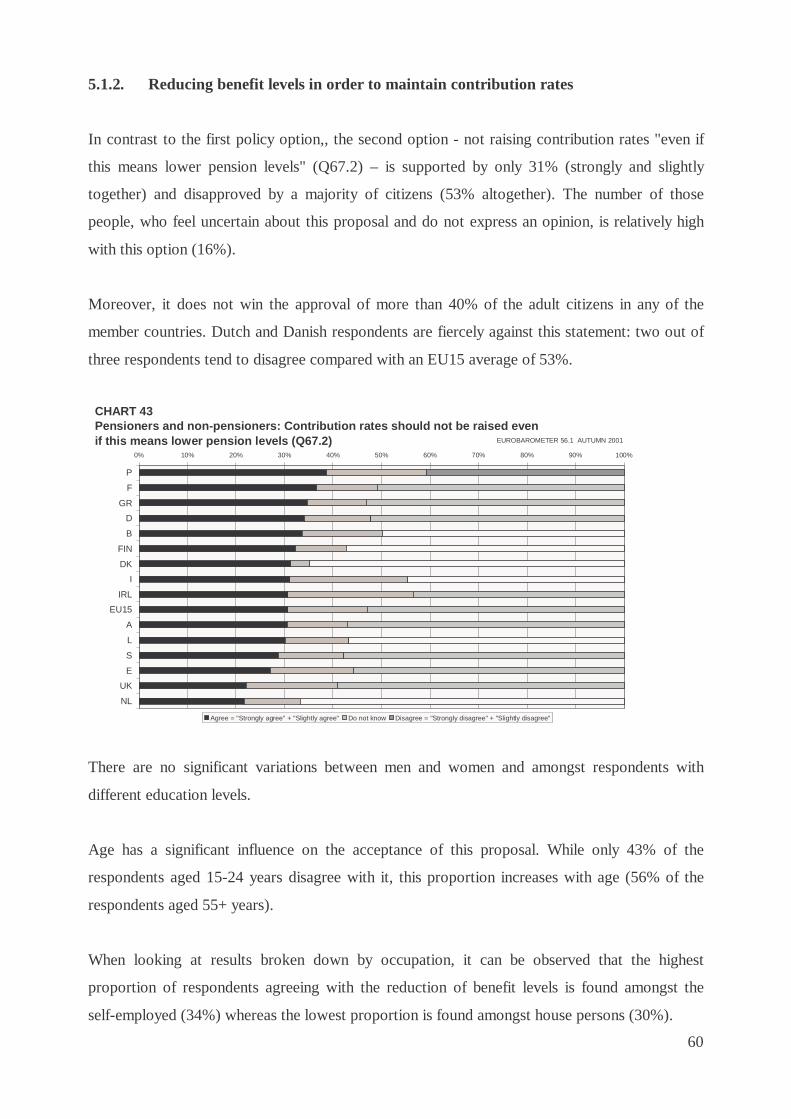

In contrast to the first policy option, the second option “not raising contribution rates, even if

this means lower pension levels" is supported by only 31% of citizens. Moreover, it does not

9

win the approval of more than 40% of respondents in any of the member countries. Dutch and

Danish respondents are fiercely against this statement: two out of three respondents tend to

disagree compared with an EU15 average of 53%.

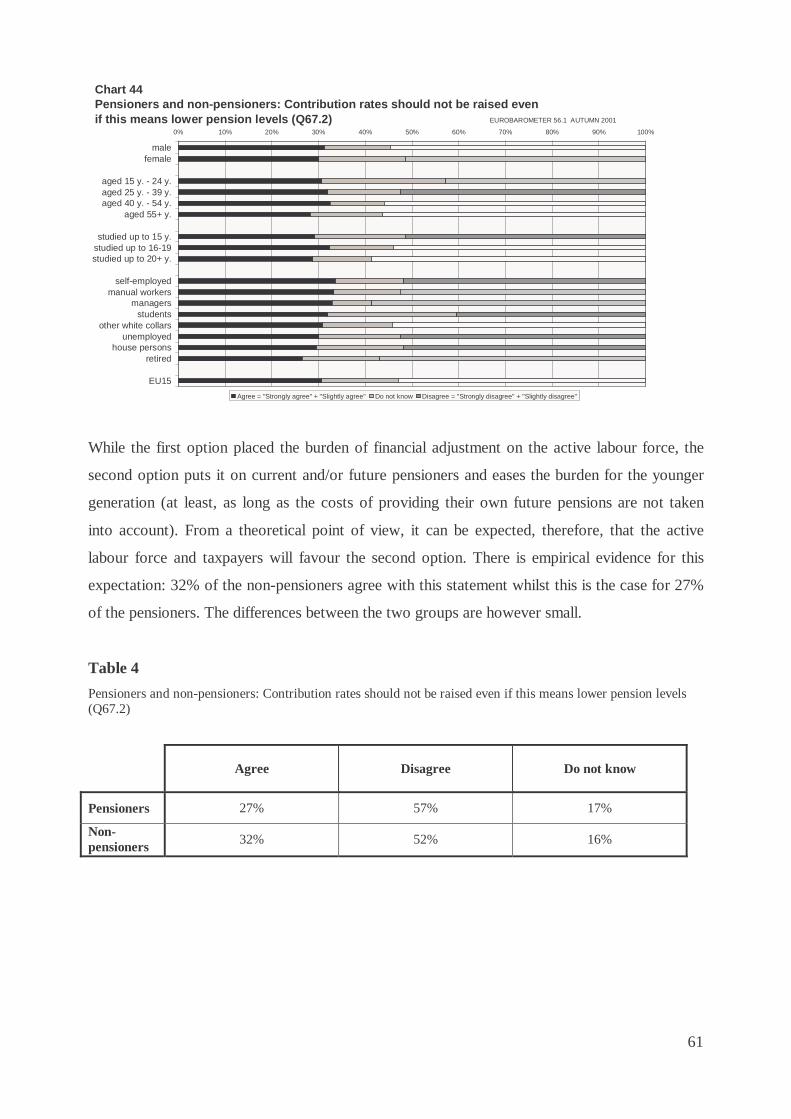

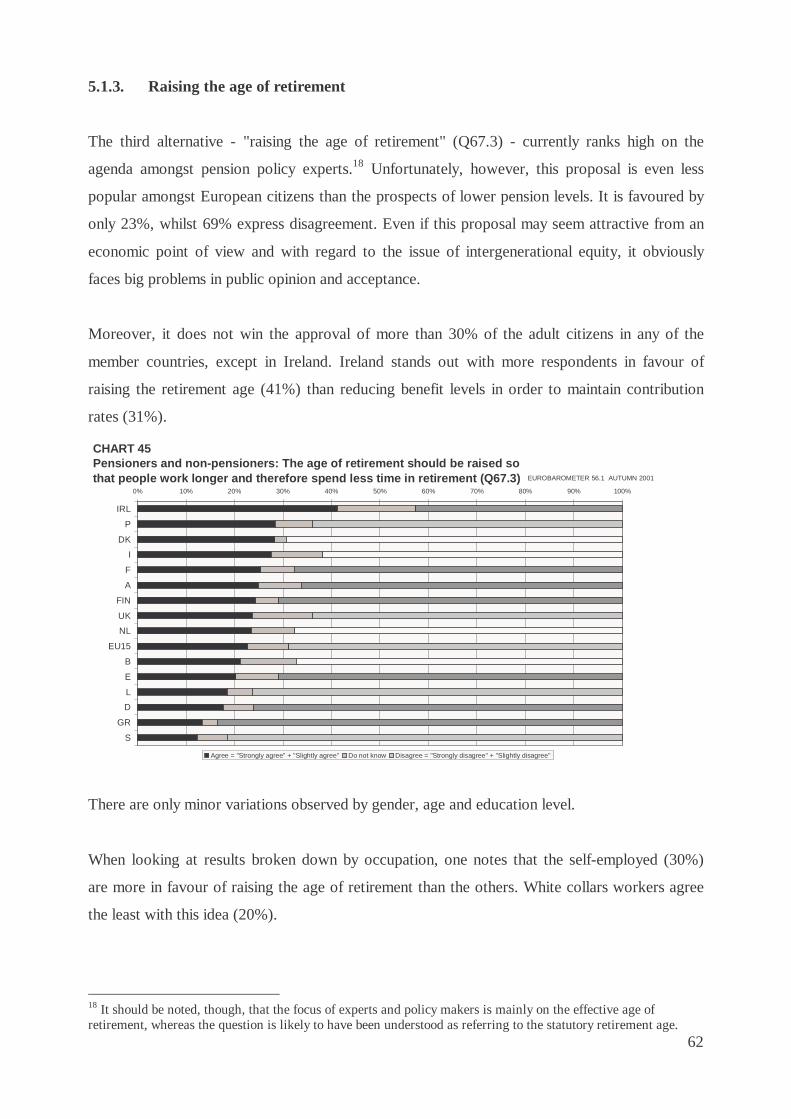

The third alternative, namely "raising the age of retirement", is even less popular amongst

European citizens than the prospects of lower pension levels. It is favoured by only 23%.

Moreover, it does not win the approval of more than 30% of the respondents in any of the

member countries, except in Ireland. Ireland stands out with more respondents in favour of

raising the retirement age (41%) than reducing benefit levels in order to maintain contribution

rates (31%).

We interpret these findings as evidence of a fairly strong normative consensus throughout

Europe concerning the main alternative options for responding to the challenges posed by the

demographic shifts in Western Europe. This fact illustrates the difficult trade-offs that need to

be dealt with by decision makers throughout the EU. The full costs of the policy options that are

preferred by citizens are not yet correctly perceived by the public. Yet, many recent reform

measures undertaken by national governments are at odds with the order of preferences as

revealed by this survey.

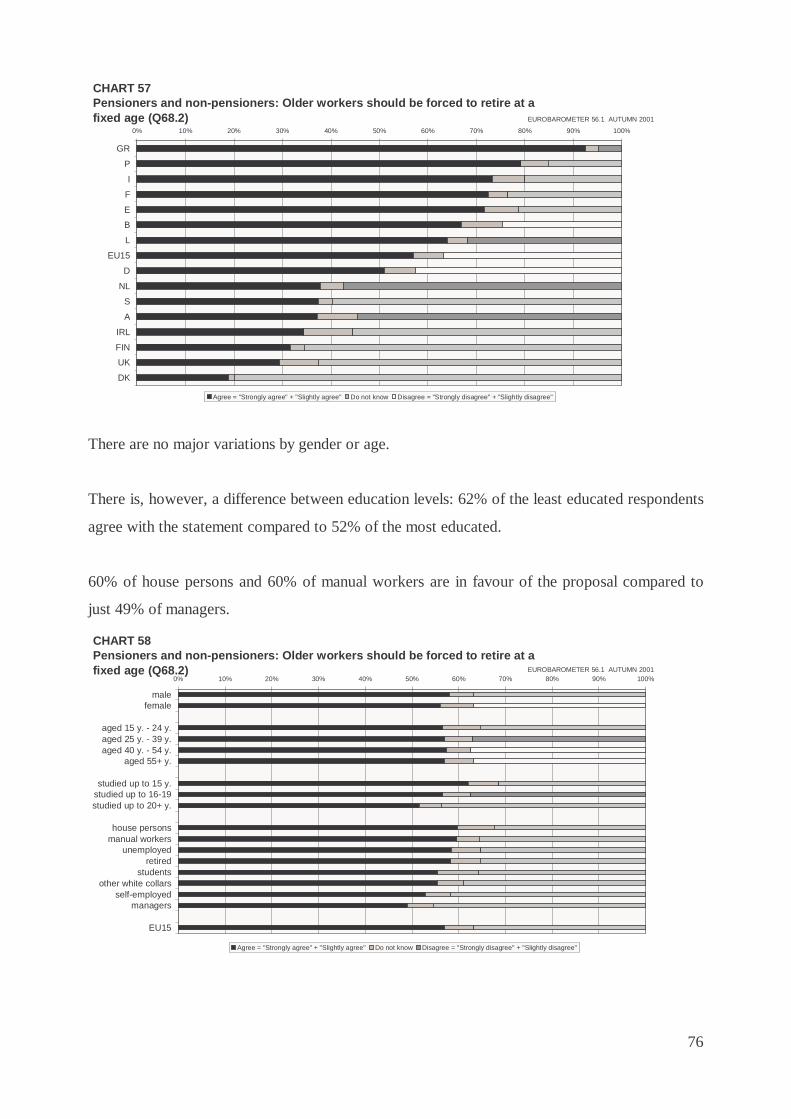

Employers should not discriminate against older workers, but continue to invest in the re-

organisation of work arrangements and (the adaptation of) their qualifications

Age discrimination in the form of excluding workers above a certain age from the labour market

through mandatory retirement remains still widely accepted by public opinion. Under the

currently prevailing labour market conditions of high mass unemployment, a majority (57%) of

the citizens in the EU support the view that older workers should be forced to retire at a fixed

age.

However, there are considerable cross-national variations in this respect. In Greece (93%) and

Portugal (79%) more than three quarters of citizens agree with the proposal. Denmark is at the

other end of the spectrum with fewer than one fifth (19%) of citizens supporting a mandatory

retirement age.

10

The support for a fixed retirement age contrasts, however, with the desire for more individual

flexibility. 75% of the EU citizens support the statement that older workers should be allowed

to retire gradually from work. So, it is important that employers adapt working conditions to the

individual needs and circumstances of older workers by providing more opportunities for part-

time work and gradual retirement.

Looking at the member states country by country, the proportion of respondents agreeing with a

gradual retirement ranges from 95% in Denmark to 56% in Italy. Apart from these extreme

cases, the proportion is 10 percentage points or more above the EU15 average (74%) in Finland,

Sweden, the Netherlands and Germany and 10 percentage points below the average in Greece.

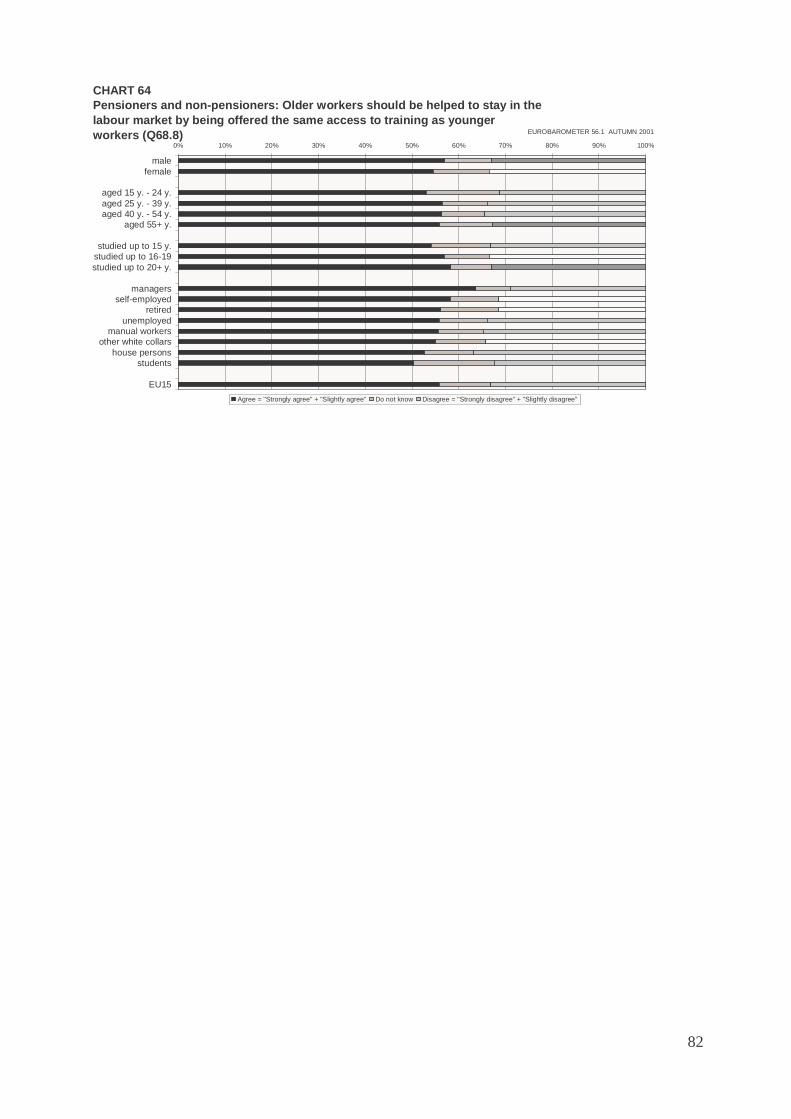

Furthermore, working arrangements should be made more attractive to older workers, in order

to induce them to extend their working life voluntarily, by positive incentives rather than by the

promise of increased pensions alone. The statement that older workers should be helped to stay

in the labour market by being offered the same access to training as younger workers was

generally supported (56%) – particularly among the British, Finnish and Danish respondents

(73%).

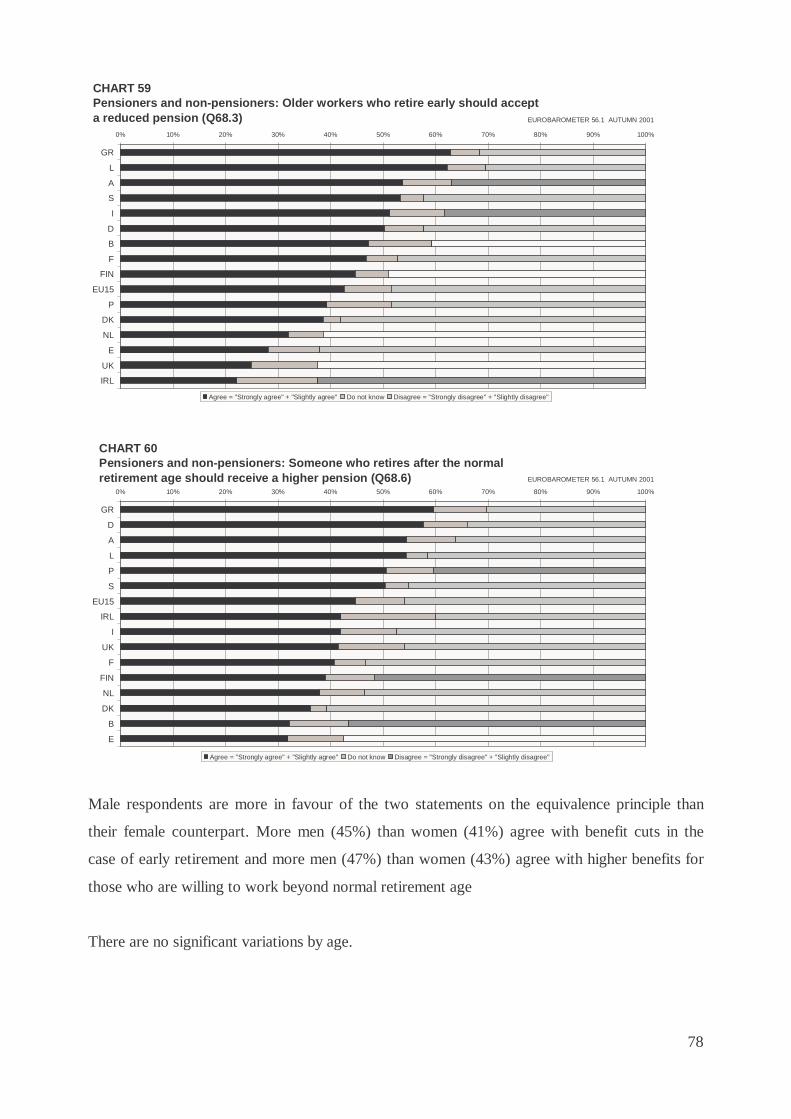

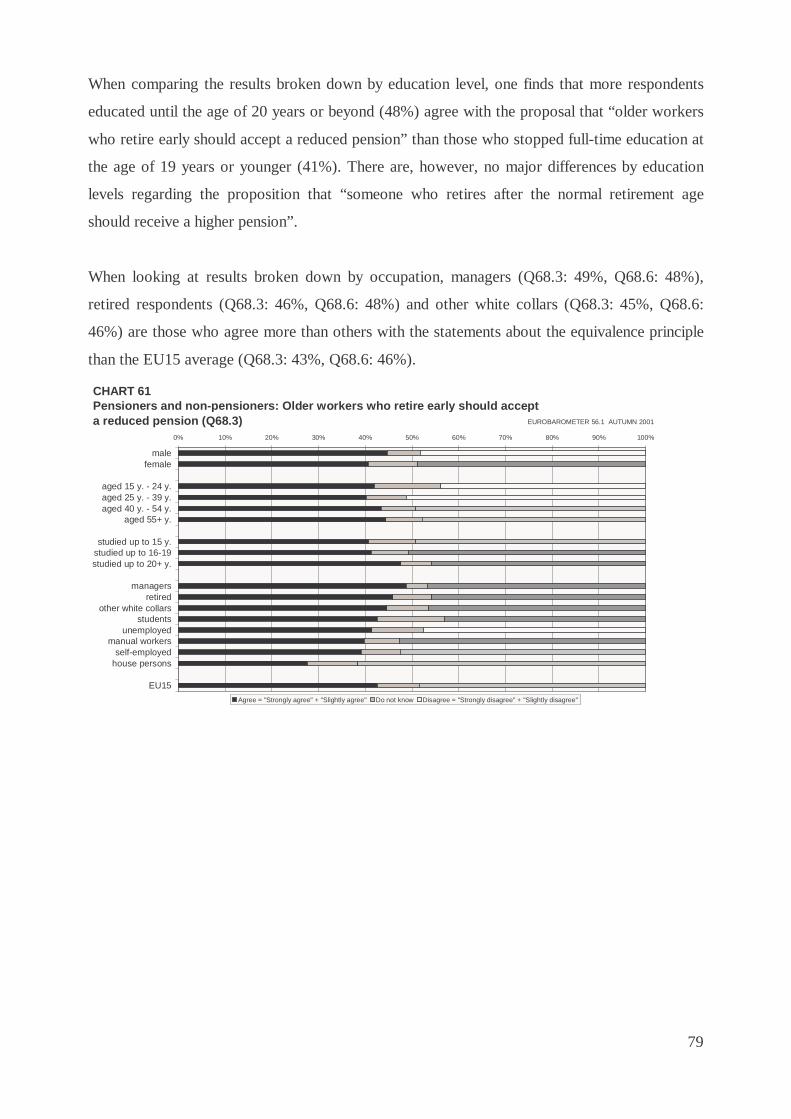

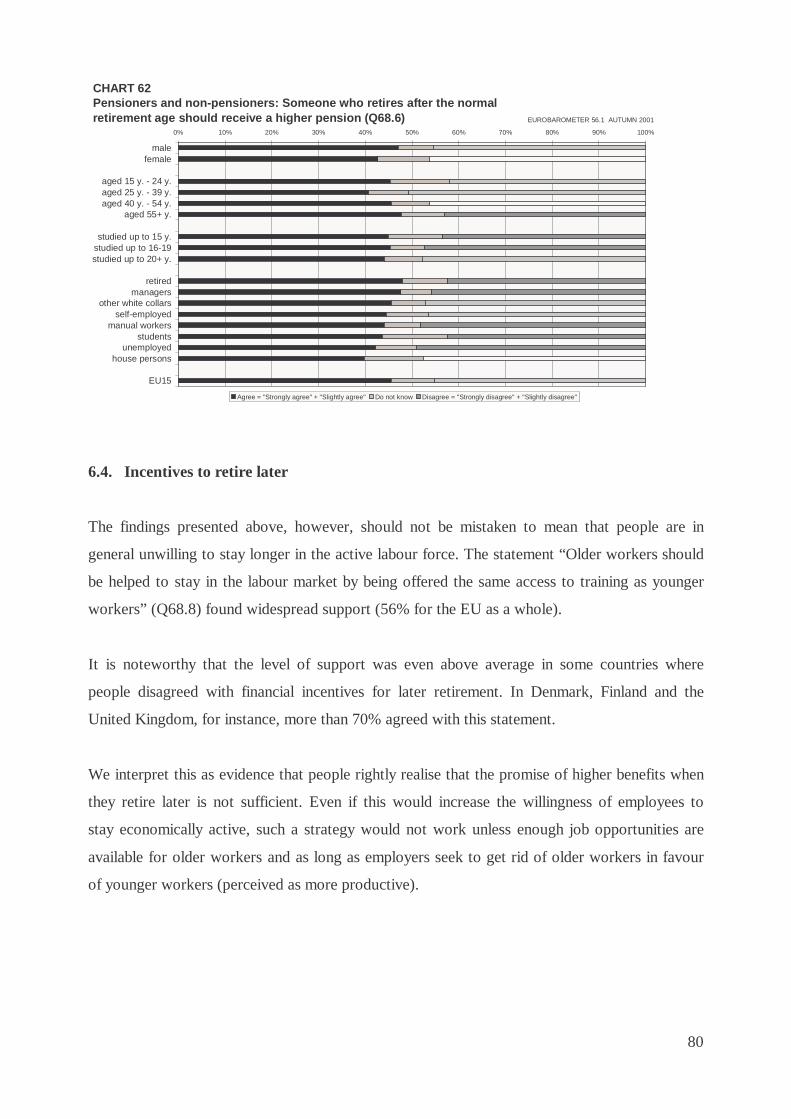

Actuarial incentives for prolonging working lives receive only half-hearted support.

Two statements submitted to respondents can be interpreted as indicators of the degree to which

the (insurance) principle of equivalence is supported amongst the citizens. These two statements

are: “older workers who retire early should accept a reduced pension” and “someone who

retires after the normal retirement age should receive a higher pension”. The results of the

survey show, however, that for the European Union as a whole, not more than half of the

respondents support these statements. Slightly more citizens disagree (49%) with benefit cuts in

the case of early retirement, compared to a proportion of citizens who agree of 43%. The

opinions are equally split (45% agree and 46% disagree) with regard to higher benefits for those

who are willing to work beyond normal retirement age.

However, significant national differences are masked by the EU average. In only five countries,

more than half of the respondents agree with both statements: Greece, Luxembourg, Austria,

Sweden and Germany.

11

Differences in opinions about transitions from work to retirement seem to reflect labour

market conditions.

There are quite substantial cross-national differences in patterns of opinion concerning the

conditions for the transition from work to retirement. These may reflect differences in the actual

labour market situation in the various countries and/or the specific social policy arrangements in

the respective country. For example: if unemployment is high amongst younger workers, this

may give added support to the view that “people in their late 50’s should give up their work to

make way for younger and unemployed people”. Conversely, if there is a shortage of labour in a

country, it seems more reasonable that “older workers should be helped to stay in the labour

market”. In other words: if the labour market situation changes, this will alter the plausibility of

‘adequate’ policy responses. The difference to the “cultural explanation” lies in the assumption

that it is not the value orientation per se, but the (macro) social context, which shapes the

popular support for various policy proposals.

12

INTRODUCTION

Pension reform is currently on the agenda of many national governments and parliaments in the

European Union. While mass unemployment and sluggish economic growth have short-term

effects on the balances of revenues and expenditures of pension schemes (as well as on social

protection schemes in general), longer term structural problems are posed by the shifting

demographic structure (the ageing process) in advanced societies and by increasing life

expectancy. Changes in family structures and in patterns of labour force participation as well as

in working time arrangements and working conditions create additional challenges.

In recent years, pensions policy has also increasingly become an area of common concern for

EU policy and it was decided to apply the “open method of coordination (OMC)” in the area of

pensions. The underlying assumption is that in view of similar demographic, economic and

social challenges and pressures, national pension reform efforts should be guided by and

directed towards a common set of goals agreed at EU level.

For almost all social policy reform efforts, public acceptance of reform measures seems to be a

crucial condition. First, it is a crucial element of mobilizing the political support to get reform

proposals enacted. And second, it is of crucial importance for the long-term sustainability of

pension schemes that the basic principles of existing schemes are in accordance with the basic

value orientations and beliefs (normative interpretations) of the citizens.

Against this background, a comparative cross-national survey on the opinions and attitudes of

the EU citizens about pension issues promises to yield important information for the policy-

making process, at the national and at the EU level. Usually, the main actors involved in the

policy-making process – apart from the politicians themselves – are professional experts:

lawyers, economists, and social administrators with much expertise in their respective fields.

Much of the current reform discussion is focusing on the fiscal implications and economic

effects of certain reform proposals. From such a fragmented and biased decision-making

process, however, the danger arises that the social effects, in particular the distributional

consequences of reform proposals with regard to the (objective) living conditions and economic

well-being of social classes and other social groups (by gender, age, occupational status etc.) are

lost sight of. Moreover, if “social security” is at stake and is taken seriously, the “subjective

dimension” of social security, the citizens’ views and perceptions of their situation should not

be neglected.

13

Which are the expectations of the citizens concerning a ‘good’ or ‘fair’ pension system? Which

goals are to be attained? Which are the underlying concepts of social justice? How do citizens

evaluate their present situation and their future prospects? What is their opinion on current

reform proposals, e.g. the acceptable level of benefits and of contributions, or the adequate

retirement age?

From an EU perspective, probably the most interesting question is whether citizens’ opinions on

pension issues vary as much as the existing pension systems in the member countries do, or

whether there is a growing awareness of common problems and a similarity of envisaged

solutions to these problems. Answers to these questions are relevant for assessing the prospects

of a common EU pension policy.

These are just a few questions about which not very much is empirically known, at least not in a

systematic and comparative way for all EU countries. The Eurobarometer survey 56.1 has

aimed at filling these gaps. It covers a broad range of issues and aspects relevant to pension

policy:

• perceptions of present and future living standards of pensioners,

• data on the income composition of pensioner households,

• opinions on goals and principles of pension systems (and the underlying value

orientations),

• opinions on more specific policy proposals to cope with the problems of financing

pensions, and

• opinions on the transition from work to retirement.

•

The following chapters summarize and highlight some of the most interesting findings.

14

1. Background characteristics of the pensioner population

This first chapter of the report describes the pensioner population. Two main characteristics are

discussed: the proportion of pensioners in the European Union population older than 15 years

(1.1.) and the retirement age of pensioners (1.2.). Besides the age at which the current

generation of pensioners retired, this chapter also consider the age at what the working-age

population intends to retire.

1.1. Proportion of pensioners within the European Union

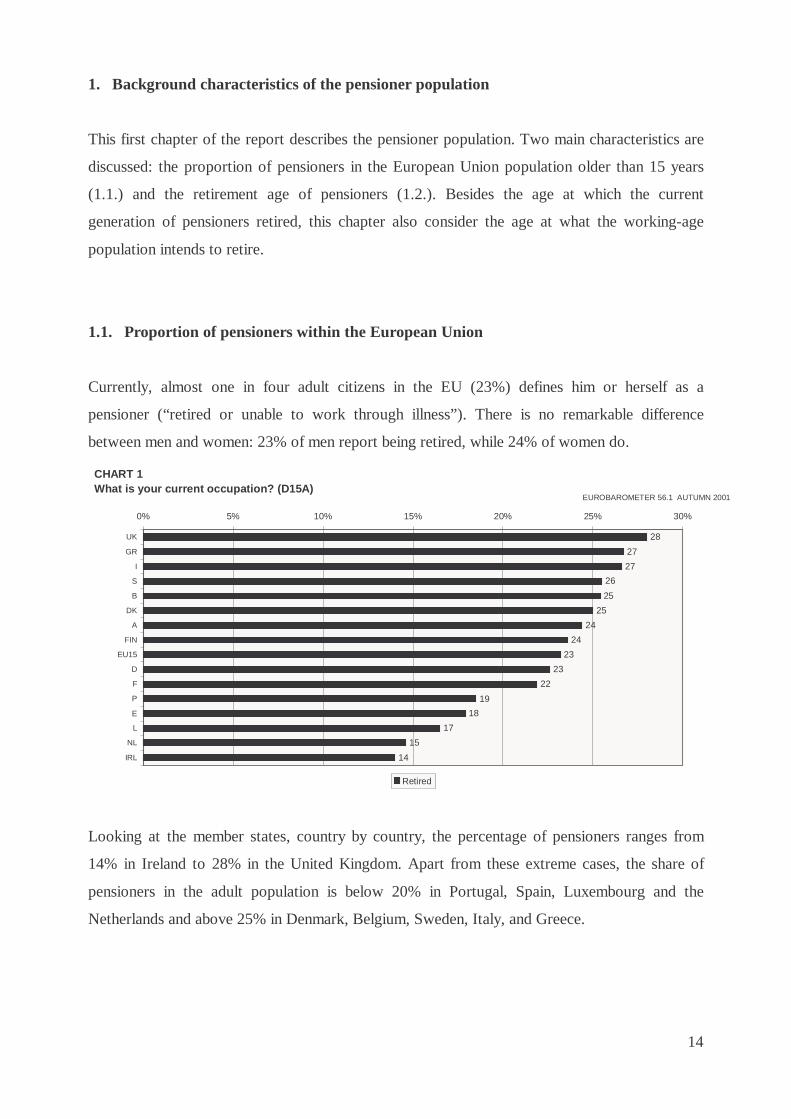

Currently, almost one in four adult citizens in the EU (23%) defines him or herself as a

pensioner (“retired or unable to work through illness”). There is no remarkable difference

between men and women: 23% of men report being retired, while 24% of women do.

Looking at the member states, country by country, the percentage of pensioners ranges from

14% in Ireland to 28% in the United Kingdom. Apart from these extreme cases, the share of

pensioners in the adult population is below 20% in Portugal, Spain, Luxembourg and the

Netherlands and above 25% in Denmark, Belgium, Sweden, Italy, and Greece.

CHART 1What is your current occupation? (D15A)

28

27

27

26

25

25

24

24

23

23

22

19

18

17

15

14

0% 5% 10% 15% 20% 25% 30%

UK

GR

I

S

B

DK

A

FIN

EU15

D

F

P

E

L

NL

IRL

Retired

EUROBAROMETER 56.1 AUTUMN 2001

15

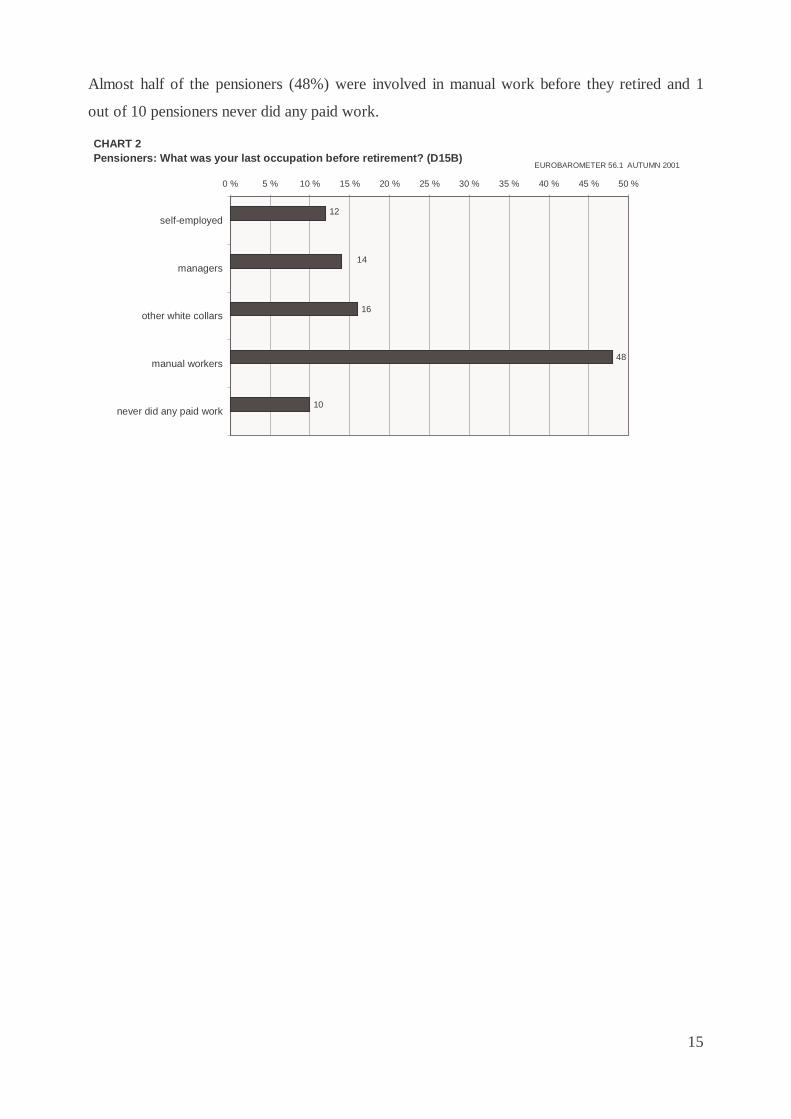

Almost half of the pensioners (48%) were involved in manual work before they retired and 1

out of 10 pensioners never did any paid work.

CHART 2Pensioners: What was your last occupation before retirement? (D15B)

16

48

10

14

12

0 % 5 % 10 % 15 % 20 % 25 % 30 % 35 % 40 % 45 % 50 %

self-employed

managers

other white collars

manual workers

never did any paid work

EUROBAROMETER 56.1 AUTUMN 2001

16

1.2. Retirement age

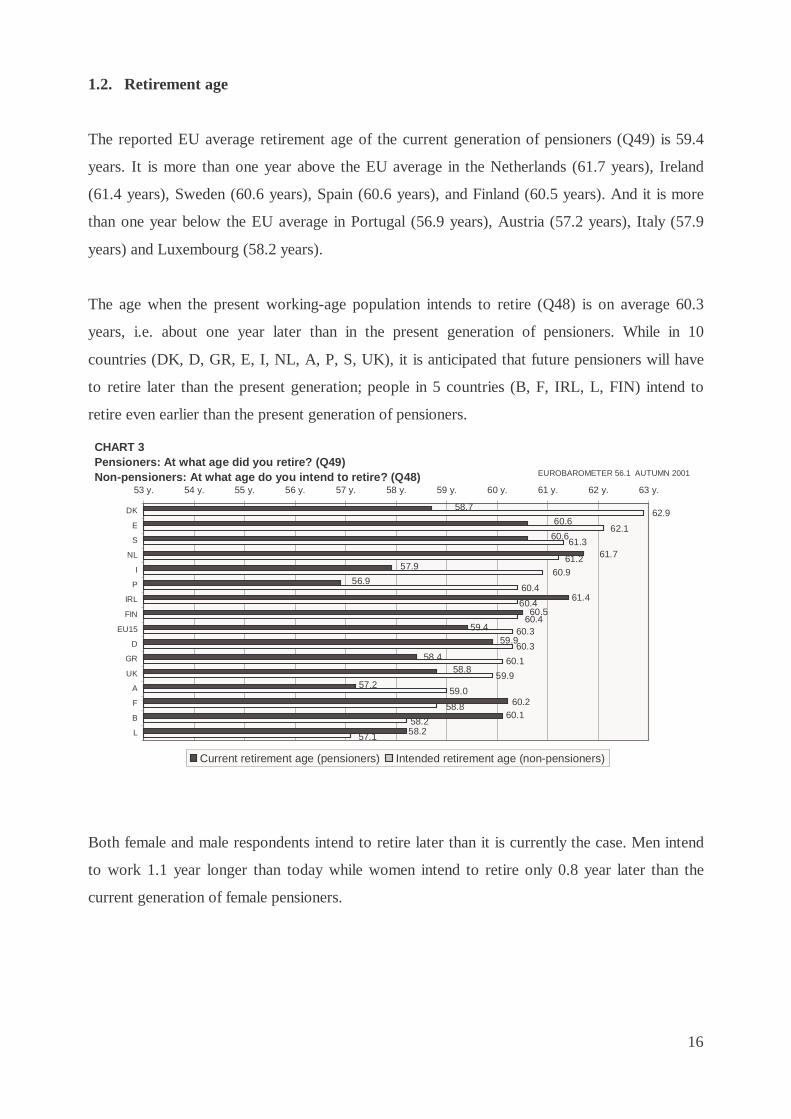

The reported EU average retirement age of the current generation of pensioners (Q49) is 59.4

years. It is more than one year above the EU average in the Netherlands (61.7 years), Ireland

(61.4 years), Sweden (60.6 years), Spain (60.6 years), and Finland (60.5 years). And it is more

than one year below the EU average in Portugal (56.9 years), Austria (57.2 years), Italy (57.9

years) and Luxembourg (58.2 years).

The age when the present working-age population intends to retire (Q48) is on average 60.3

years, i.e. about one year later than in the present generation of pensioners. While in 10

countries (DK, D, GR, E, I, NL, A, P, S, UK), it is anticipated that future pensioners will have

to retire later than the present generation; people in 5 countries (B, F, IRL, L, FIN) intend to

retire even earlier than the present generation of pensioners.

Both female and male respondents intend to retire later than it is currently the case. Men intend

to work 1.1 year longer than today while women intend to retire only 0.8 year later than the

current generation of female pensioners.

CHART 3Pensioners: At what age did you retire? (Q49)Non-pensioners: At what age do you intend to retire? (Q48)

61.4

57.2

60.6

61.757.9

60.5

59.459.9

58.458.8

60.260.1

58.2

58.7

60.6

56.960.9

58.2

58.8

62.1

62.9

61.3

60.4

60.4

59.0

61.2

57.1

60.460.3

60.3

60.1

59.9

53 y. 54 y. 55 y. 56 y. 57 y. 58 y. 59 y. 60 y. 61 y. 62 y. 63 y.

DK

E

S

NL

I

P

IRL

FIN

EU15

D

GR

UK

A

F

B

L

Current retirement age (pensioners) Intended retirement age (non-pensioners)

EUROBAROMETER 56.1 AUTUMN 2001

17

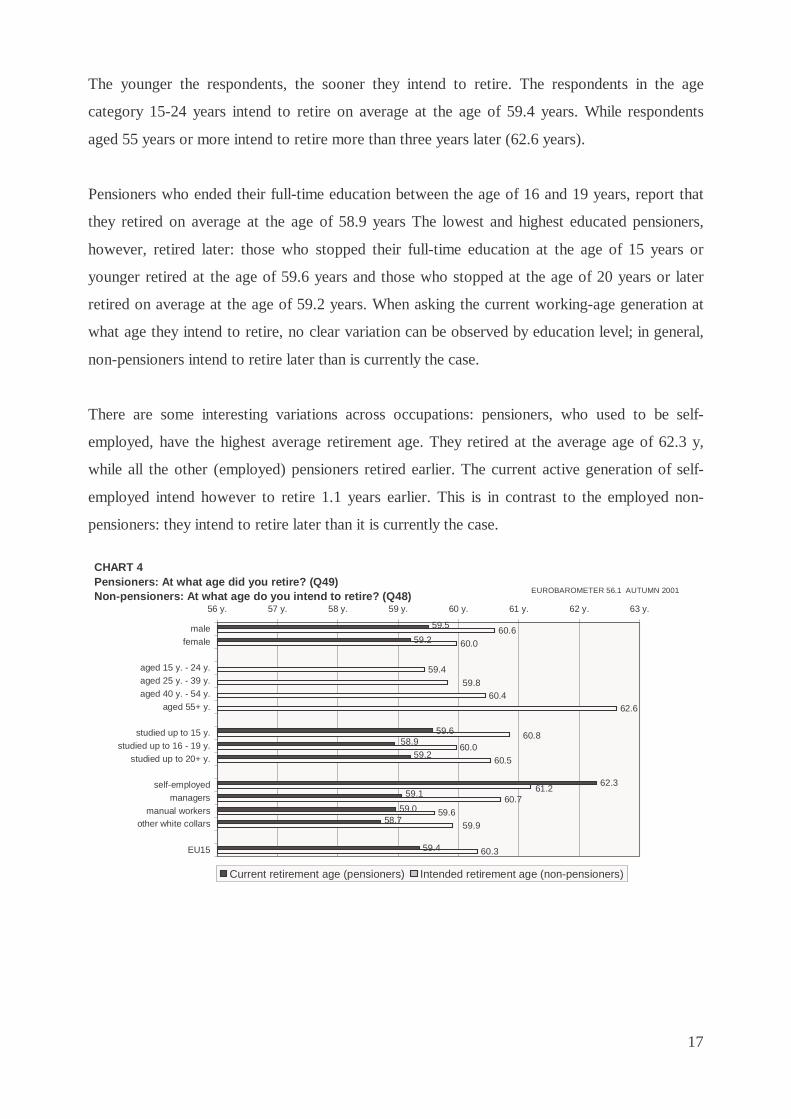

The younger the respondents, the sooner they intend to retire. The respondents in the age

category 15-24 years intend to retire on average at the age of 59.4 years. While respondents

aged 55 years or more intend to retire more than three years later (62.6 years).

Pensioners who ended their full-time education between the age of 16 and 19 years, report that

they retired on average at the age of 58.9 years The lowest and highest educated pensioners,

however, retired later: those who stopped their full-time education at the age of 15 years or

younger retired at the age of 59.6 years and those who stopped at the age of 20 years or later

retired on average at the age of 59.2 years. When asking the current working-age generation at

what age they intend to retire, no clear variation can be observed by education level; in general,

non-pensioners intend to retire later than is currently the case.

There are some interesting variations across occupations: pensioners, who used to be self-

employed, have the highest average retirement age. They retired at the average age of 62.3 y,

while all the other (employed) pensioners retired earlier. The current active generation of self-

employed intend however to retire 1.1 years earlier. This is in contrast to the employed non-

pensioners: they intend to retire later than it is currently the case.

CHART 4 Pensioners: At what age did you retire? (Q49)Non-pensioners: At what age do you intend to retire? (Q48)

59.4

58.759.0

59.162.3

59.258.9

59.6

59.2

59.5

60.3

59.959.6

60.7

60.5

61.2

60.060.8

62.660.4

59.8

59.4

60.060.6

56 y. 57 y. 58 y. 59 y. 60 y. 61 y. 62 y. 63 y.

malefemale

aged 15 y. - 24 y.aged 25 y. - 39 y.aged 40 y. - 54 y.

aged 55+ y.

studied up to 15 y.studied up to 16 - 19 y.

studied up to 20+ y.

self-employedmanagers

manual workersother white collars

EU15

Current retirement age (pensioners) Intended retirement age (non-pensioners)

EUROBAROMETER 56.1 AUTUMN 2001

18

2. Economic well-being of pensioners

This second chapter consist of two main parts.

In the first part the standard of living of pensioners and non-pensioners is discussed.

Successively the focus is set on the current standard of living of pensioners and non-pensioners

(2.1.1.), the standard of living both pensioners and non-pensioners expect to have in the future

(2.1.2.) and the difference in standard of living pensioners experienced before and after

retirement (2.1.3.)

The second part covers the benefit level of state pensions. It answers the question “How the

state pension allows the pensioners to get by” (2.2.1). Besides, attention is given to how the

current working-age population expects to get by with the state pension they will receive in the

future (2.2.2.). The last part of this chapter discusses the level of income replacement the

current working-age population desires to have after retirement (2.2.3.).

2.1. Standard of living

2.1.1. Current standard of living

When asked to assess their present standard of living (Q50), about half of EU citizens describe

it as “average”, about one fourth as being positive1 and another quarter as being negative2.

However, there are considerable cross-national variations in this respect. Citizens in the

Netherlands, Luxembourg, the United Kingdom, Ireland, Denmark and Greece view their

current standard of living much more favourably than the EU citizens at large, while in

Germany and Austria about two thirds of the population cluster in the “average” category. In

Portugal 46% of the citizens describe their living standard as negative.

1 In this section a positive standard of living refers to the sum of the categories “rich”, “very comfortable” and “comfortable”. 2 In this section a negative standard of living refers to the sum of the categories “just getting along”, “poor” and “very poor”.

19

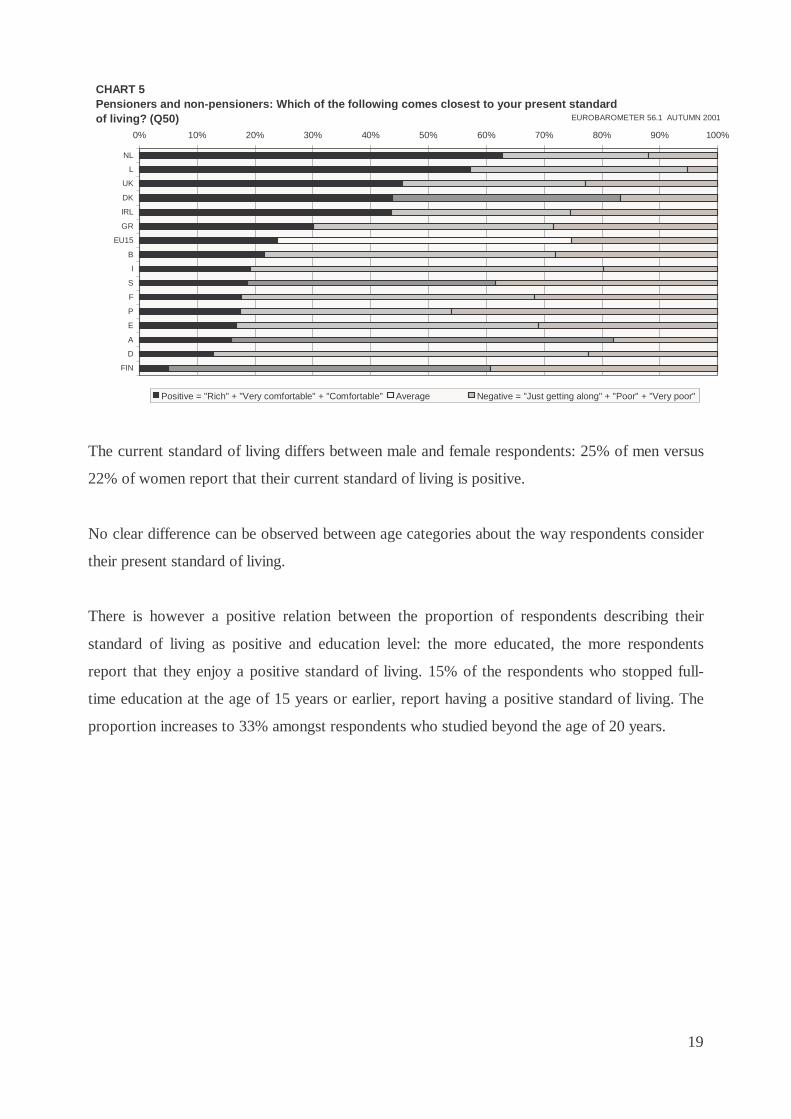

The current standard of living differs between male and female respondents: 25% of men versus

22% of women report that their current standard of living is positive.

No clear difference can be observed between age categories about the way respondents consider

their present standard of living.

There is however a positive relation between the proportion of respondents describing their

standard of living as positive and education level: the more educated, the more respondents

report that they enjoy a positive standard of living. 15% of the respondents who stopped full-

time education at the age of 15 years or earlier, report having a positive standard of living. The

proportion increases to 33% amongst respondents who studied beyond the age of 20 years.

CHART 5Pensioners and non-pensioners: Which of the following comes closest to your present standard of living? (Q50)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

NL

L

UK

DK

IRL

GR

EU15

B

I

S

F

P

E

A

D

FIN

Positive = "Rich" + "Very comfortable" + "Comfortable" Average Negative = "Just getting along" + "Poor" + "Very poor"

EUROBAROMETER 56.1 AUTUMN 2001

20

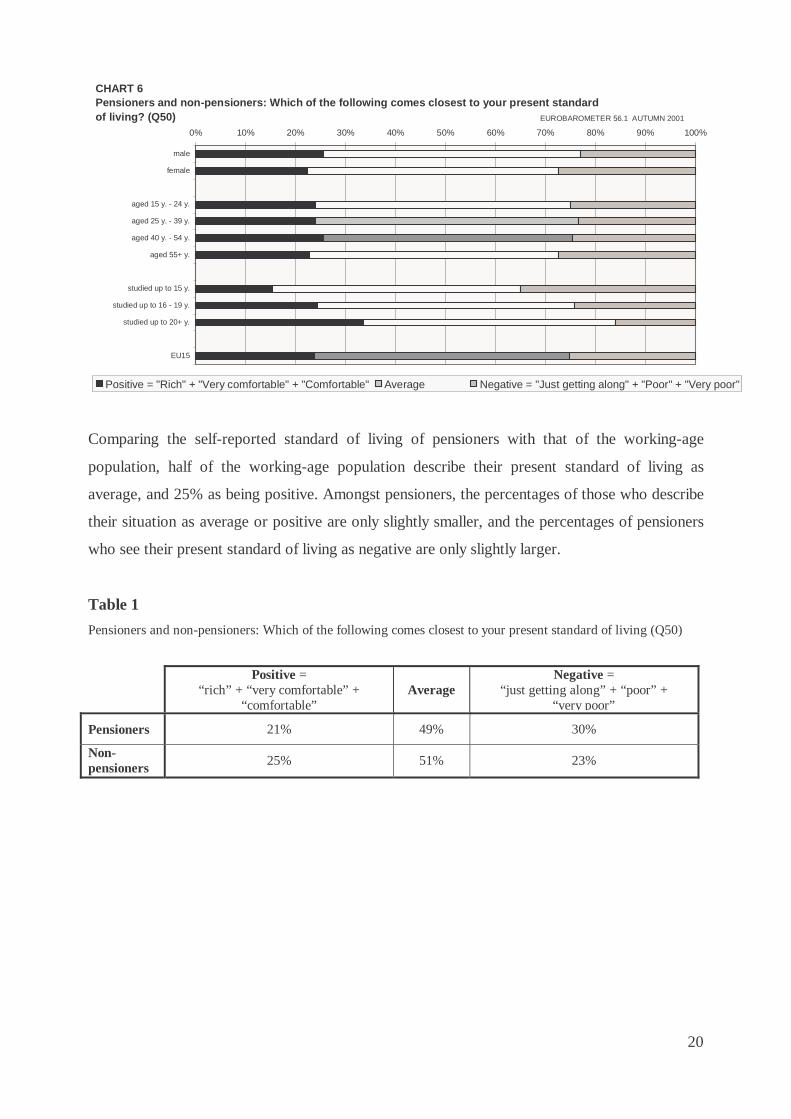

Comparing the self-reported standard of living of pensioners with that of the working-age

population, half of the working-age population describe their present standard of living as

average, and 25% as being positive. Amongst pensioners, the percentages of those who describe

their situation as average or positive are only slightly smaller, and the percentages of pensioners

who see their present standard of living as negative are only slightly larger.

Table 1

Pensioners and non-pensioners: Which of the following comes closest to your present standard of living (Q50)

Positive =

“rich” + “very comfortable” + “comfortable”

Average Negative =

“just getting along” + “poor” + “very poor”

Pensioners 21% 49% 30%

Non-pensioners 25% 51% 23%

CHART 6Pensioners and non-pensioners: Which of the following comes closest to your present standard of living? (Q50)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

male

female

aged 15 y. - 24 y.

aged 25 y. - 39 y.

aged 40 y. - 54 y.

aged 55+ y.

studied up to 15 y.

studied up to 16 - 19 y.

studied up to 20+ y.

EU15

Positive = "Rich" + "Very comfortable" + "Comfortable" Average Negative = "Just getting along" + "Poor" + "Very poor"

EUROBAROMETER 56.1 AUTUMN 2001

21

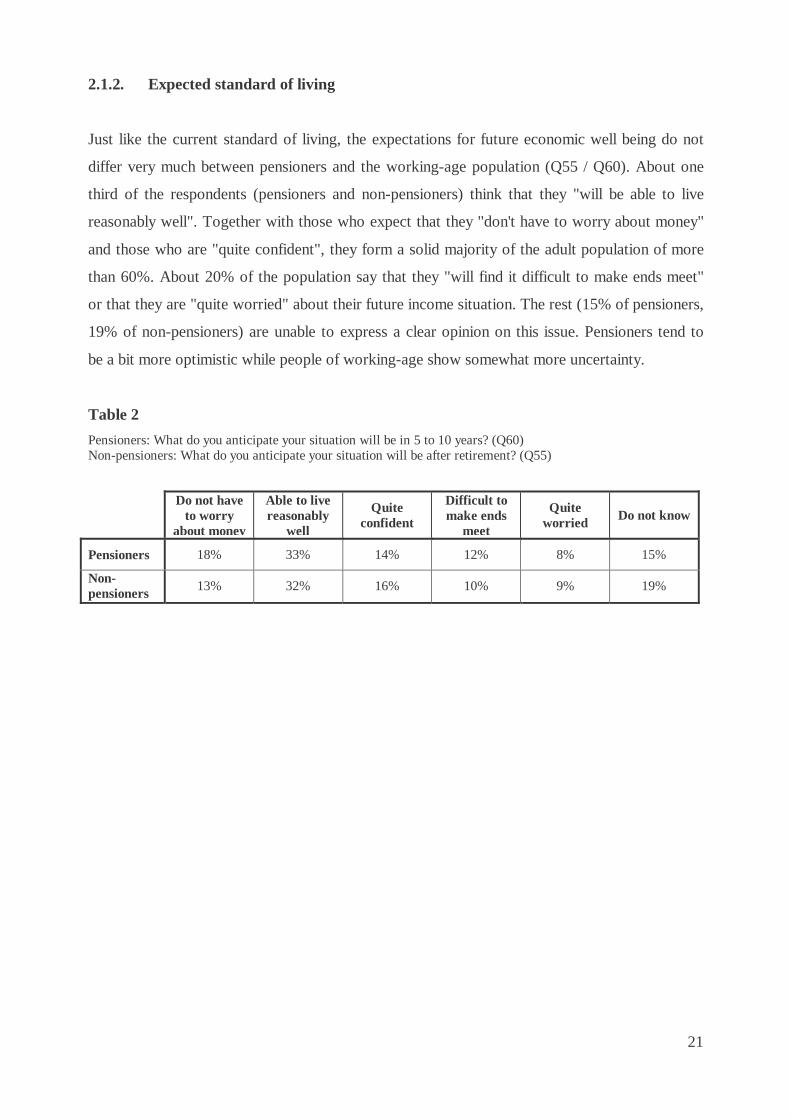

2.1.2. Expected standard of living

Just like the current standard of living, the expectations for future economic well being do not

differ very much between pensioners and the working-age population (Q55 / Q60). About one

third of the respondents (pensioners and non-pensioners) think that they "will be able to live

reasonably well". Together with those who expect that they "don't have to worry about money"

and those who are "quite confident", they form a solid majority of the adult population of more

than 60%. About 20% of the population say that they "will find it difficult to make ends meet"

or that they are "quite worried" about their future income situation. The rest (15% of pensioners,

19% of non-pensioners) are unable to express a clear opinion on this issue. Pensioners tend to

be a bit more optimistic while people of working-age show somewhat more uncertainty.

Table 2

Pensioners: What do you anticipate your situation will be in 5 to 10 years? (Q60) Non-pensioners: What do you anticipate your situation will be after retirement? (Q55)

Do not have

to worry about money

Able to live reasonably

well

Quite confident

Difficult to make ends

meet

Quite worried Do not know

Pensioners 18% 33% 14% 12% 8% 15%

Non-pensioners 13% 32% 16% 10% 9% 19%

22

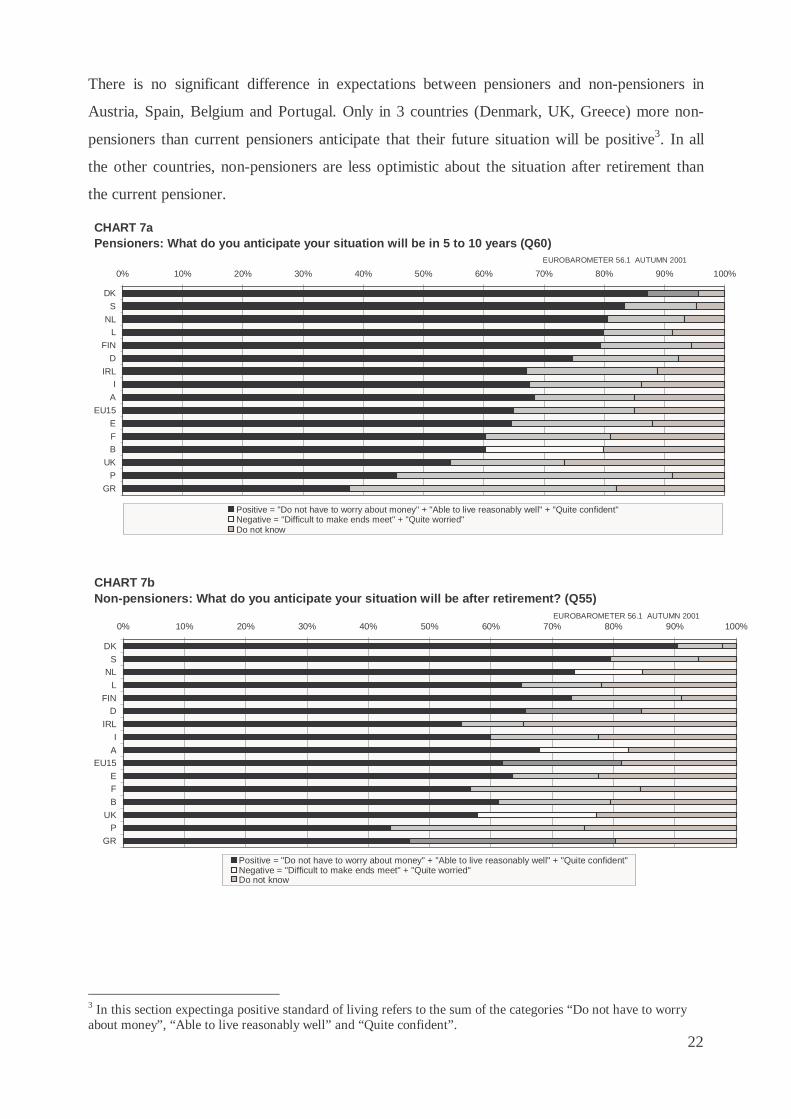

There is no significant difference in expectations between pensioners and non-pensioners in

Austria, Spain, Belgium and Portugal. Only in 3 countries (Denmark, UK, Greece) more non-

pensioners than current pensioners anticipate that their future situation will be positive3. In all

the other countries, non-pensioners are less optimistic about the situation after retirement than

the current pensioner.

3 In this section expectinga positive standard of living refers to the sum of the categories “Do not have to worry about money”, “Able to live reasonably well” and “Quite confident”.

CHART 7aPensioners: What do you anticipate your situation will be in 5 to 10 years (Q60)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

DK

S

NLL

FIN

D

IRLI

A

EU15

E

FB

UK

P

GR

Positive = "Do not have to worry about money" + "Able to live reasonably well" + "Quite confident"Negative = "Difficult to make ends meet" + "Quite worried"Do not know

EUROBAROMETER 56.1 AUTUMN 2001

CHART 7bNon-pensioners: What do you anticipate your situation will be after retirement? (Q55)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

DK

SNL

L

FIND

IRL

I

AEU15

EF

B

UKP

GR

Positive = "Do not have to worry about money" + "Able to live reasonably well" + "Quite confident"Negative = "Difficult to make ends meet" + "Quite worried"Do not know

EUROBAROMETER 56.1 AUTUMN 2001

23

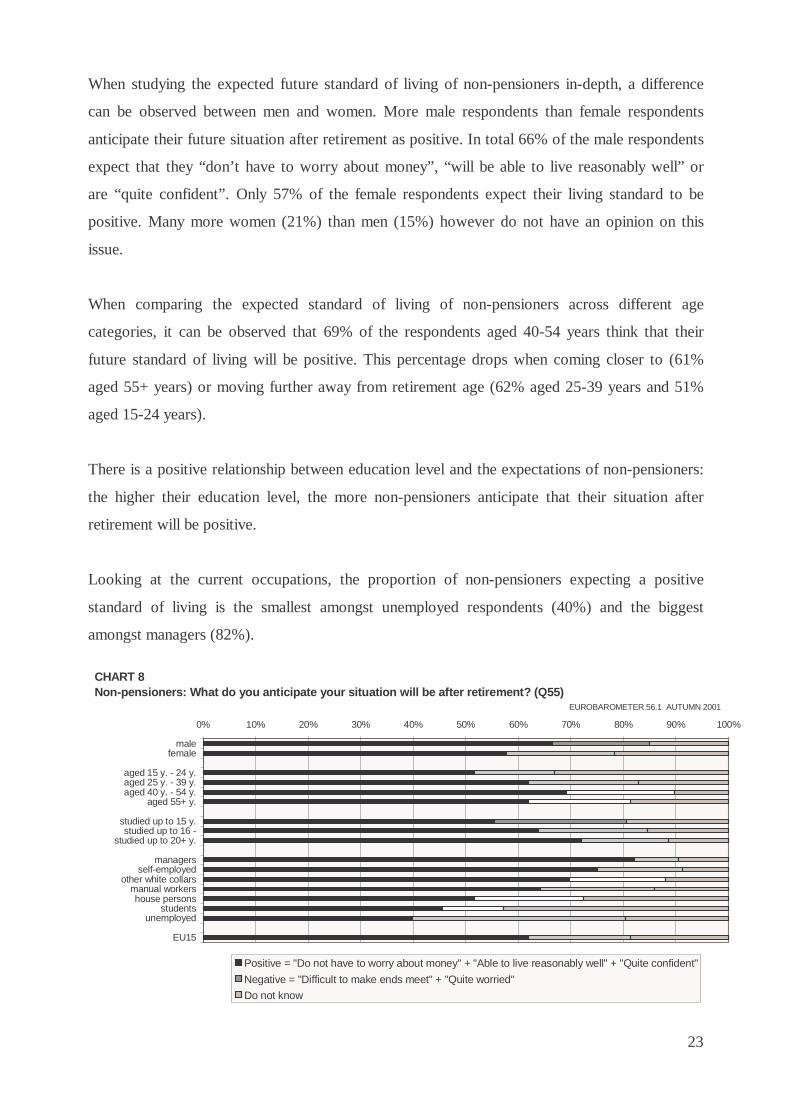

When studying the expected future standard of living of non-pensioners in-depth, a difference

can be observed between men and women. More male respondents than female respondents

anticipate their future situation after retirement as positive. In total 66% of the male respondents

expect that they “don’t have to worry about money”, “will be able to live reasonably well” or

are “quite confident”. Only 57% of the female respondents expect their living standard to be

positive. Many more women (21%) than men (15%) however do not have an opinion on this

issue.

When comparing the expected standard of living of non-pensioners across different age

categories, it can be observed that 69% of the respondents aged 40-54 years think that their

future standard of living will be positive. This percentage drops when coming closer to (61%

aged 55+ years) or moving further away from retirement age (62% aged 25-39 years and 51%

aged 15-24 years).

There is a positive relationship between education level and the expectations of non-pensioners:

the higher their education level, the more non-pensioners anticipate that their situation after

retirement will be positive.

Looking at the current occupations, the proportion of non-pensioners expecting a positive

standard of living is the smallest amongst unemployed respondents (40%) and the biggest

amongst managers (82%).

CHART 8Non-pensioners: What do you anticipate your situation will be after retirement? (Q55)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

malefemale

aged 15 y. - 24 y.aged 25 y. - 39 y.aged 40 y. - 54 y.

aged 55+ y.

studied up to 15 y.studied up to 16 -

studied up to 20+ y.

managersself-employed

other white collarsmanual workershouse persons

studentsunemployed

EU15

Positive = "Do not have to worry about money" + "Able to live reasonably well" + "Quite confident"

Negative = "Difficult to make ends meet" + "Quite worried"

Do not know

EUROBAROMETER 56.1 AUTUMN 2001

24

2.1.3. Comparison of standard of living before and after retirement

Compared to the time before retirement (Q56), 39% of the pensioners regard their financial

situation as more or less the same and another 43% as worse4. More than 11% regard their

financial situation even better5 than before.

In Greece, Luxembourg, Denmark and the Netherlands, about 20% of the pensioners seem to

enjoy a better standard of living than before retirement. On the other hand, about 43% of EU

citizens report their financial situation as worse. In particular, in Portugal (59%), Belgium

(54%), Greece (51%), France (51%) and Ireland (49%) pensioners see themselves worse off

than before retirement. Although these findings are based on subjective self-assessments rather

than objective levels of income, these cross-national differences point to significant differences

in the degree to which pension systems maintain people’s living standards after retirement.

4 A worse situation than before retirement is the sum of two categories: “a bit worse” and “much worse.” 5 A better situation than before retirement is the sum of two categories: “much better” and “a bit better”.

CHART 9Pensioners: Compared to the time before your retirement, is your current financial situation ... ? (Q56)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

GR

L

DK

NL

FIN

S

A

P

E

EU15

D

IRL

I

F

UK

B

Better = "Much better" + "A bit better" More or less the same Worse = "A bit worse" + "Much worse" Do not know

EUROBAROMETER 56.1 AUTUMN 2001

25

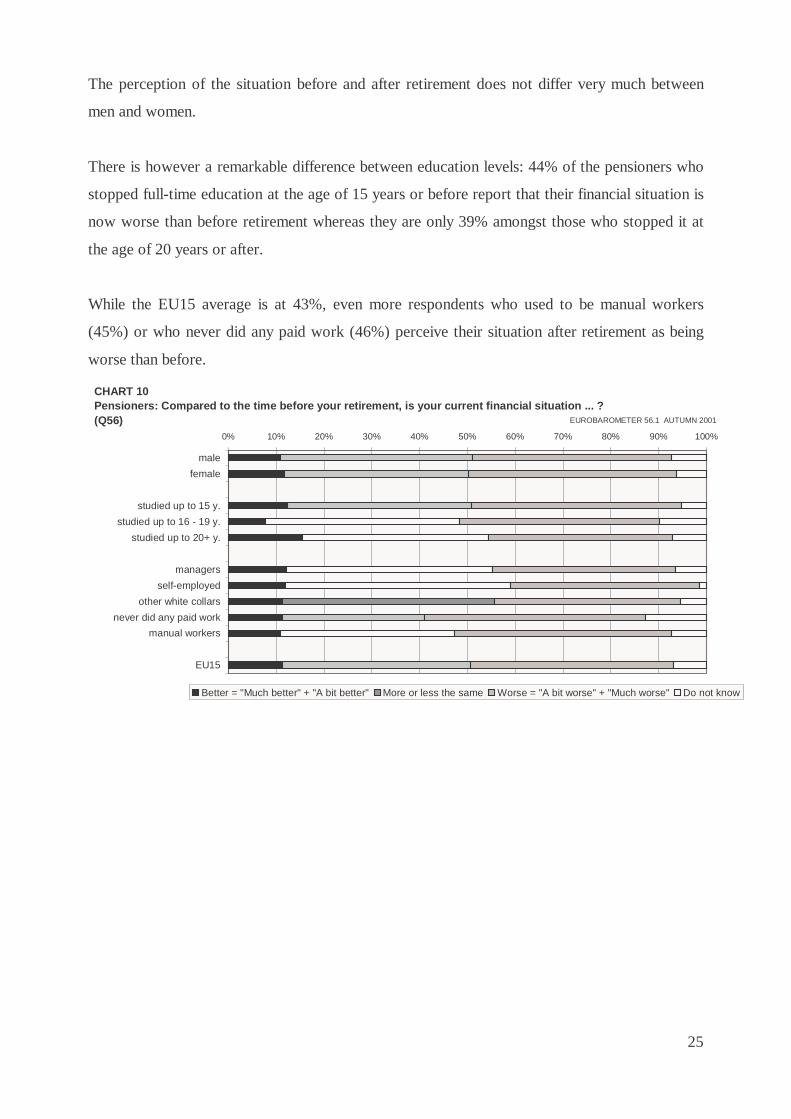

The perception of the situation before and after retirement does not differ very much between

men and women.

There is however a remarkable difference between education levels: 44% of the pensioners who

stopped full-time education at the age of 15 years or before report that their financial situation is

now worse than before retirement whereas they are only 39% amongst those who stopped it at

the age of 20 years or after.

While the EU15 average is at 43%, even more respondents who used to be manual workers

(45%) or who never did any paid work (46%) perceive their situation after retirement as being

worse than before.

CHART 10Pensioners: Compared to the time before your retirement, is your current financial situation ... ? (Q56)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

male

female

studied up to 15 y.

studied up to 16 - 19 y.

studied up to 20+ y.

managers

self-employed

other white collars

never did any paid work

manual workers

EU15

Better = "Much better" + "A bit better" More or less the same Worse = "A bit worse" + "Much worse" Do not know

EUROBAROMETER 56.1 AUTUMN 2001

26

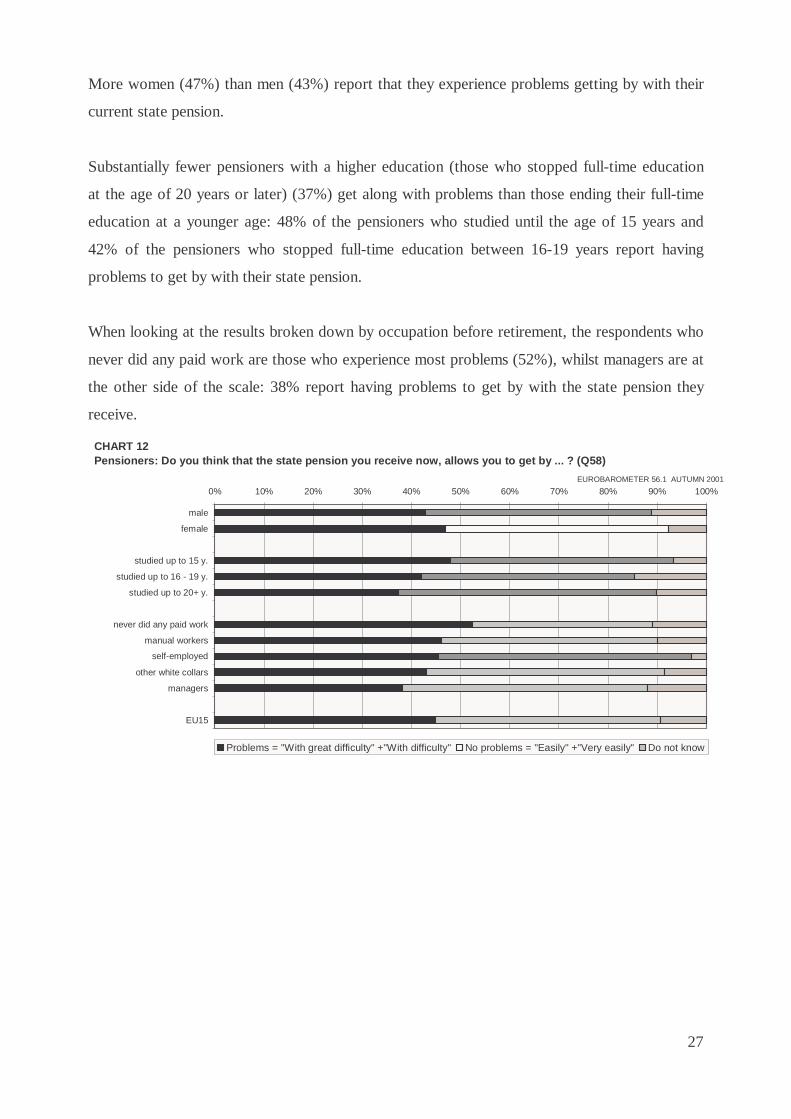

2.2. Benefit level of state pensions6

2.2.1. Pensioners

State (or public) pensions are certainly the most important, but not the only component of

pensioners’ household income. Pensioners were also asked how they managed to get by with

their current state pension benefit (Q58). Even on this basis, i.e. taking only the benefit level of

state pensions into account, half of the pensioners reported that they get along without any

problems7, the other half say they experience problems8.

The countries where a disproportionate large share of pensioners says that they experience

problems are Greece (77%), Portugal (77%) and Ireland (67%).

6 Notions such as 'state' and 'occupational' pensions refer to very different arrangements from one country to another and respondents had not been given a clear definition of what is to be regarded as 'state' or 'occupational' pension. This may limit the comparability of results between countries. In particular, Finnish respondents clearly perceived the statutory earnings-related pension schemes as occupational schemes and regarded only the means-tested national minimum pension as 'state pension'. 7 Getting by without any problems is the sum of two categories: “easily” and “very easily”. 8 Experiencing problems is the sum of two categories: “with great difficulty” and “with difficulty”.

CHART 11Pensioners: Do you think that the state pension you receive now, allows you to get by ... ? (Q58)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

GR

P

IRL

E

FIN

UK

EU15

F

B

I

S

NL

D

DK

A

L

Problems = "With great difficulty" +"With difficulty" No problems = "Easily" +"Very easily" Do not know

EUROBAROMETER 56.1 AUTUMN 2001

27

More women (47%) than men (43%) report that they experience problems getting by with their

current state pension.

Substantially fewer pensioners with a higher education (those who stopped full-time education

at the age of 20 years or later) (37%) get along with problems than those ending their full-time

education at a younger age: 48% of the pensioners who studied until the age of 15 years and

42% of the pensioners who stopped full-time education between 16-19 years report having

problems to get by with their state pension.

When looking at the results broken down by occupation before retirement, the respondents who

never did any paid work are those who experience most problems (52%), whilst managers are at

the other side of the scale: 38% report having problems to get by with the state pension they

receive.

CHART 12Pensioners: Do you think that the state pension you receive now, allows you to get by ... ? (Q58)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

male

female

studied up to 15 y.

studied up to 16 - 19 y.

studied up to 20+ y.

never did any paid work

manual workers

self-employed

other white collars

managers

EU15

Problems = "With great difficulty" +"With difficulty" No problems = "Easily" +"Very easily" Do not know

EUROBAROMETER 56.1 AUTUMN 2001

28

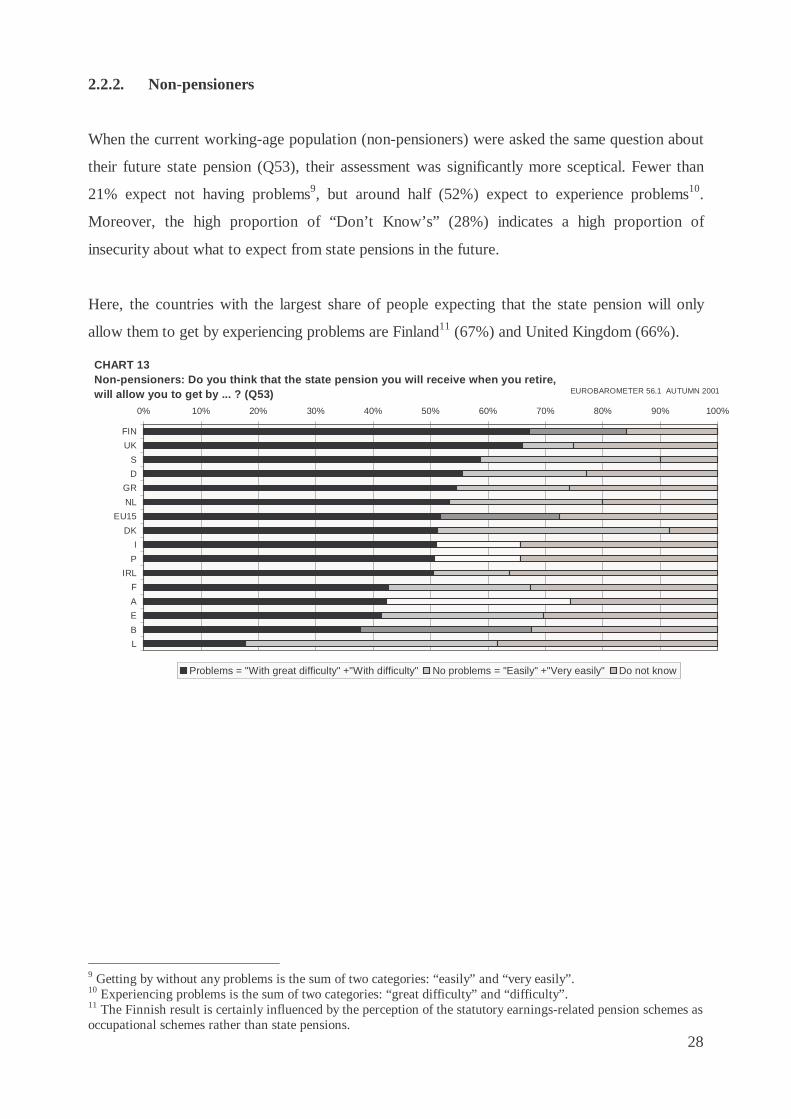

2.2.2. Non-pensioners

When the current working-age population (non-pensioners) were asked the same question about

their future state pension (Q53), their assessment was significantly more sceptical. Fewer than

21% expect not having problems9, but around half (52%) expect to experience problems10.

Moreover, the high proportion of “Don’t Know’s” (28%) indicates a high proportion of

insecurity about what to expect from state pensions in the future.

Here, the countries with the largest share of people expecting that the state pension will only

allow them to get by experiencing problems are Finland11 (67%) and United Kingdom (66%).

9 Getting by without any problems is the sum of two categories: “easily” and “very easily”. 10 Experiencing problems is the sum of two categories: “great difficulty” and “difficulty”. 11 The Finnish result is certainly influenced by the perception of the statutory earnings-related pension schemes as occupational schemes rather than state pensions.

CHART 13Non-pensioners: Do you think that the state pension you will receive when you retire, will allow you to get by ... ? (Q53)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

FIN

UK

S

D

GR

NL

EU15

DK

I

P

IRL

F

A

E

B

L

Problems = "With great difficulty" +"With difficulty" No problems = "Easily" +"Very easily" Do not know

EUROBAROMETER 56.1 AUTUMN 2001

29

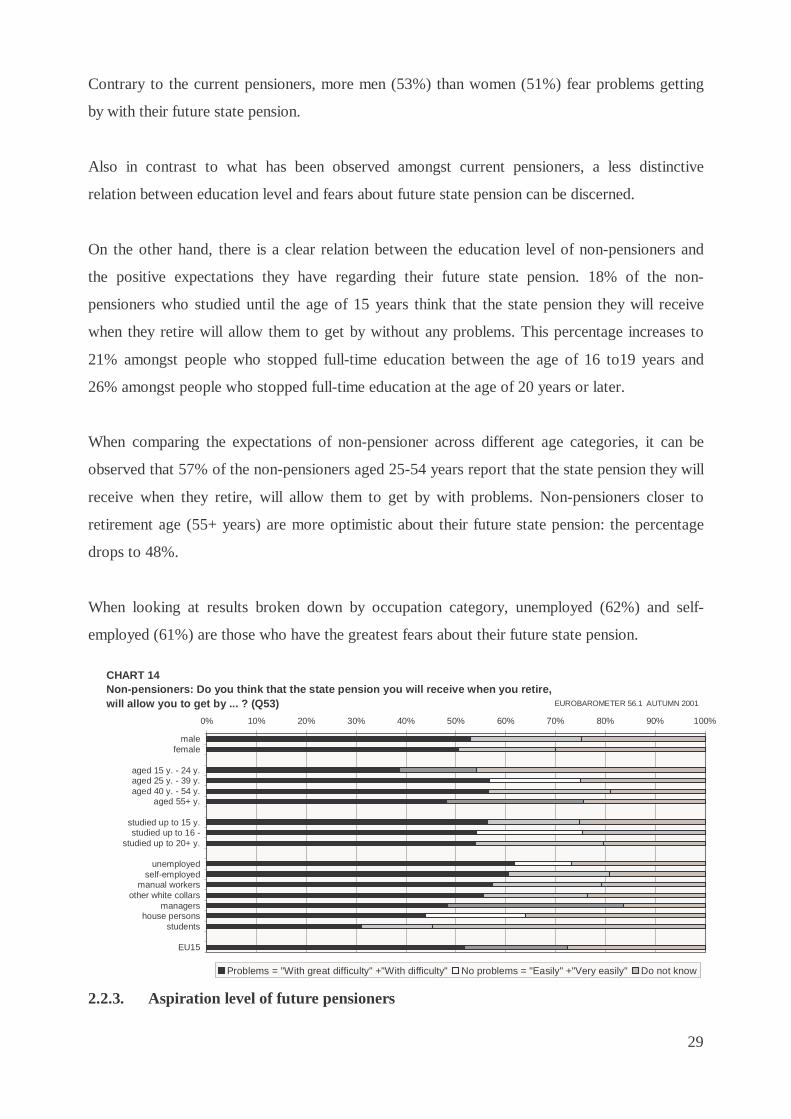

Contrary to the current pensioners, more men (53%) than women (51%) fear problems getting

by with their future state pension.

Also in contrast to what has been observed amongst current pensioners, a less distinctive

relation between education level and fears about future state pension can be discerned.

On the other hand, there is a clear relation between the education level of non-pensioners and

the positive expectations they have regarding their future state pension. 18% of the non-

pensioners who studied until the age of 15 years think that the state pension they will receive

when they retire will allow them to get by without any problems. This percentage increases to

21% amongst people who stopped full-time education between the age of 16 to19 years and

26% amongst people who stopped full-time education at the age of 20 years or later.

When comparing the expectations of non-pensioner across different age categories, it can be

observed that 57% of the non-pensioners aged 25-54 years report that the state pension they will

receive when they retire, will allow them to get by with problems. Non-pensioners closer to

retirement age (55+ years) are more optimistic about their future state pension: the percentage

drops to 48%.

When looking at results broken down by occupation category, unemployed (62%) and self-

employed (61%) are those who have the greatest fears about their future state pension.

2.2.3. Aspiration level of future pensioners

CHART 14Non-pensioners: Do you think that the state pension you will receive when you retire, will allow you to get by ... ? (Q53)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

malefemale

aged 15 y. - 24 y.aged 25 y. - 39 y.aged 40 y. - 54 y.

aged 55+ y.

studied up to 15 y.studied up to 16 -

studied up to 20+ y.

unemployedself-employed

manual workersother white collars

managershouse persons

students

EU15

Problems = "With great difficulty" +"With difficulty" No problems = "Easily" +"Very easily" Do not know

EUROBAROMETER 56.1 AUTUMN 2001

30

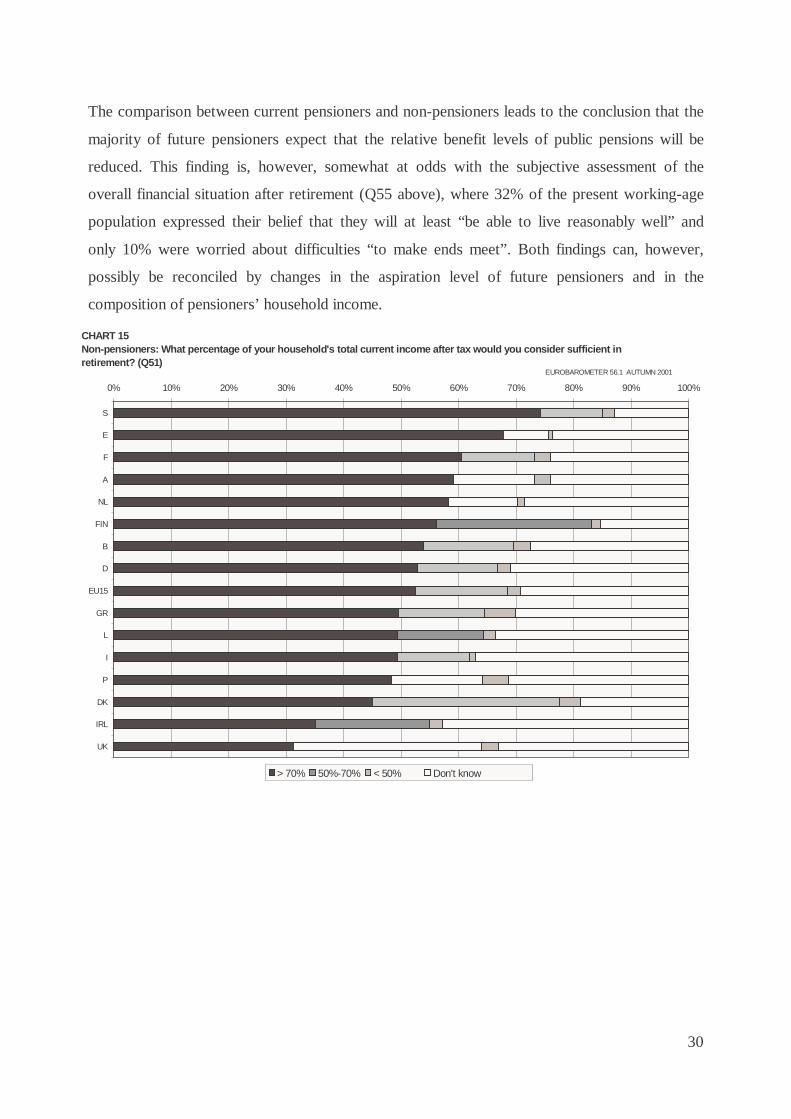

The comparison between current pensioners and non-pensioners leads to the conclusion that the

majority of future pensioners expect that the relative benefit levels of public pensions will be

reduced. This finding is, however, somewhat at odds with the subjective assessment of the

overall financial situation after retirement (Q55 above), where 32% of the present working-age

population expressed their belief that they will at least “be able to live reasonably well” and

only 10% were worried about difficulties “to make ends meet”. Both findings can, however,

possibly be reconciled by changes in the aspiration level of future pensioners and in the

composition of pensioners’ household income.

CHART 15Non-pensioners: What percentage of your household's total current income after tax would you consider sufficient in retirement? (Q51)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

S

E

F

A

NL

FIN

B

D

EU15

GR

L

I

P

DK

IRL

UK

> 70% 50%-70% < 50% Don't know

EUROBAROMETER 56.1 AUTUMN 2001

31

The aspiration level seems to be quite high, though (Q51). When asked what income

replacement level they would consider sufficient, 53% of respondents would only consider a net

income replacement level of 70% or more as sufficient for the retirement phase; another 16%

say they would need 50%-70% of their pre-retirement income, but only 2% can imagine to

consider an income replacement level of less than 50% as sufficient12.

While the European average is at 53%, far more Swedish respondents (74%) consider a net

income replacement of 70% or more as sufficient. This is also the case for Spain (68%), France

(60%), Austria (59%), the Netherlands (58%) and Finland (56%).

The aspiration level of male non-pensioners seems to be higher than that of their female

counterpart. 56% of men and 49% of women would consider a net income replacement of 70%

or more as sufficient.

As the respondents come closer to retirement age, the aspiration level drops: around 60% of the

respondents aged 25-54 years consider a net income of 70% or more as sufficient versus 52% of

the non-pensioners older than 55 years.

People with a higher education have higher aspiration levels about their income after retirement

than those with a lower education.

There are variations across occupations. The proportion of non-pensioners considering a net

income of 70% or more as sufficient is the highest amongst managers (61%) and other white

collars (61%).

12 However, almost one third of the respondents could not give a clear indication of what income level they would

consider sufficient.

32

CHART 16Non-pensioners: What percentage of your household's total current income after tax would you consider sufficient in retirement? (Q51)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

male

female

aged 15 y. - 24 y.

aged 25 y. - 39 y.

aged 40 y. - 54 y.

aged 55+ y.

studied up to 15 y.

studied up to 16 - 19 y.

studied up to 20+ y.

managers

other white collars

manual workers

self-employed

unemployed

house persons

students

EU15

> 70% 50%-70% < 50% Don't know

EUROBAROMETER 56.1 AUTUMN 2001

33

3. The composition of pensioners’ household income

In order to assess the relative importance of various income sources in the household income

package of pensioners, we asked for a ranking of the main source of income, the second most

important source, and any other sources of income. This chapter discusses the sources of

income for current pensioners (3.1.), the sources of income the future pensioners expect (3.2.)

and the sources of income both current and future pensioners prefer (3.3.).

3.1. Sources of income for current pensioners

3.1.1. The main source of income

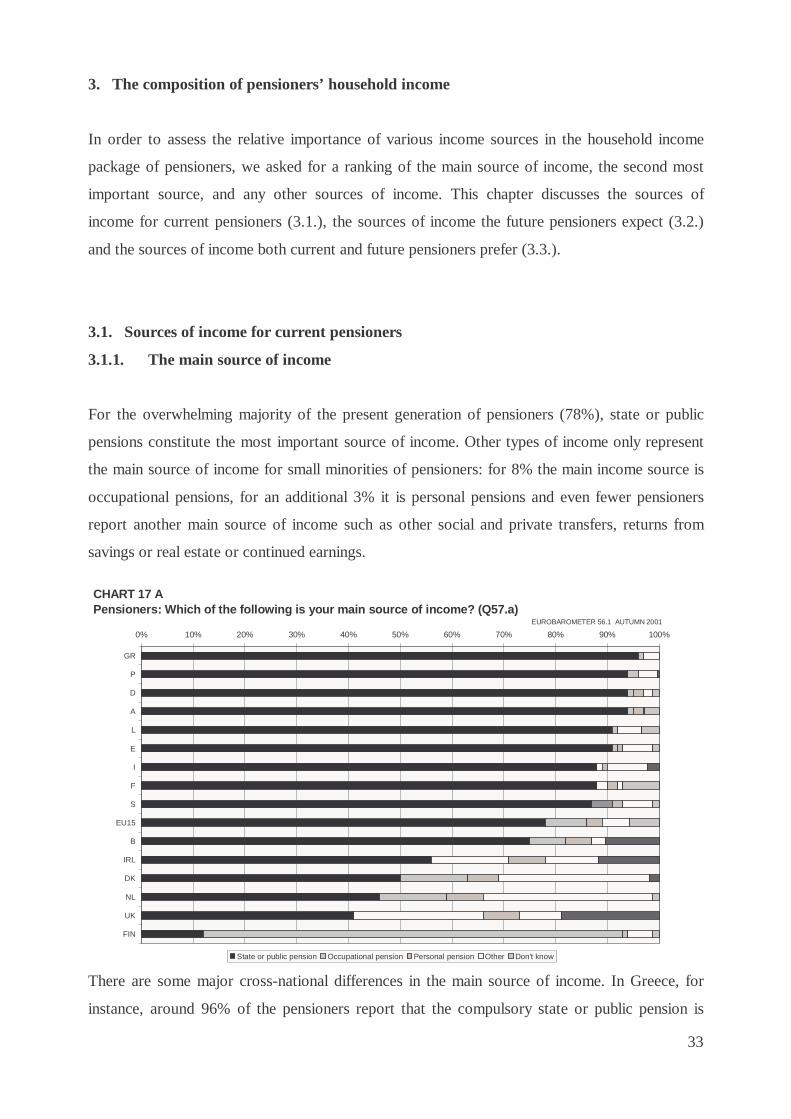

For the overwhelming majority of the present generation of pensioners (78%), state or public

pensions constitute the most important source of income. Other types of income only represent

the main source of income for small minorities of pensioners: for 8% the main income source is

occupational pensions, for an additional 3% it is personal pensions and even fewer pensioners

report another main source of income such as other social and private transfers, returns from

savings or real estate or continued earnings.

There are some major cross-national differences in the main source of income. In Greece, for

instance, around 96% of the pensioners report that the compulsory state or public pension is

CHART 17 APensioners: Which of the following is your main source of income? (Q57.a)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

GR

P

D

A

L

E

I

F

S

EU15

B

IRL

DK

NL

UK

FIN

State or public pension Occupational pension Personal pension Other Don't know

EUROBAROMETER 56.1 AUTUMN 2001

34

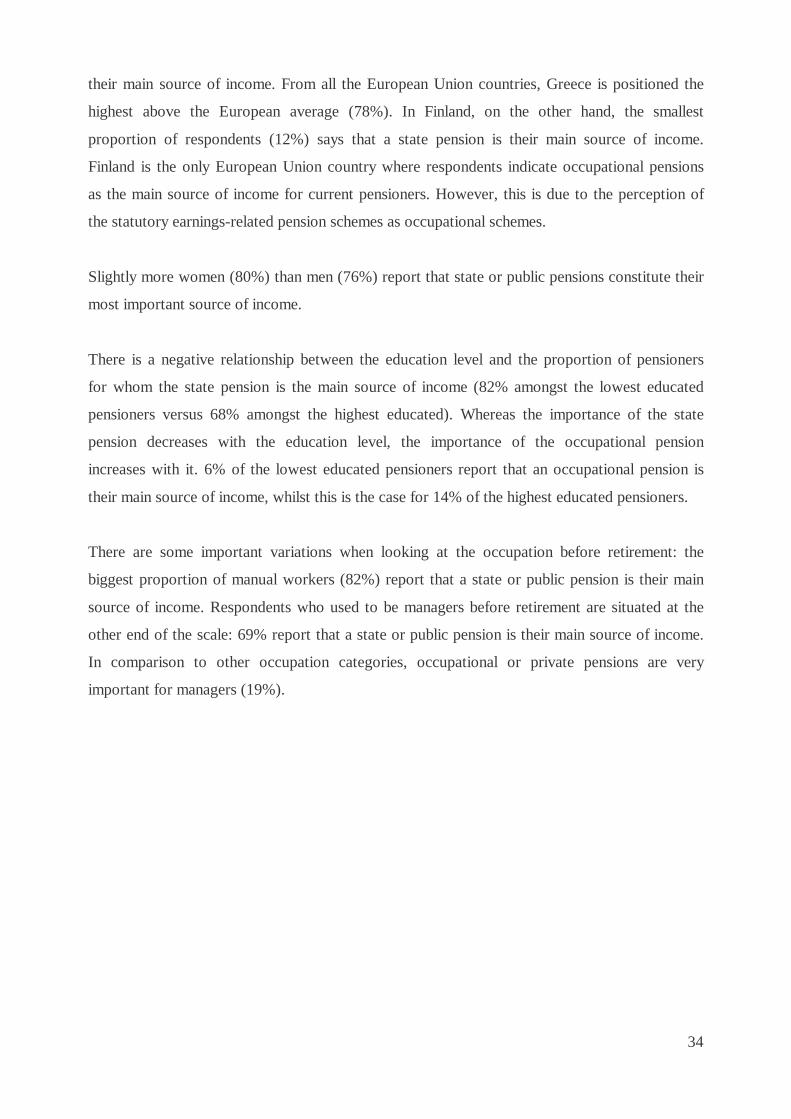

their main source of income. From all the European Union countries, Greece is positioned the

highest above the European average (78%). In Finland, on the other hand, the smallest

proportion of respondents (12%) says that a state pension is their main source of income.

Finland is the only European Union country where respondents indicate occupational pensions

as the main source of income for current pensioners. However, this is due to the perception of

the statutory earnings-related pension schemes as occupational schemes.

Slightly more women (80%) than men (76%) report that state or public pensions constitute their

most important source of income.

There is a negative relationship between the education level and the proportion of pensioners

for whom the state pension is the main source of income (82% amongst the lowest educated

pensioners versus 68% amongst the highest educated). Whereas the importance of the state

pension decreases with the education level, the importance of the occupational pension

increases with it. 6% of the lowest educated pensioners report that an occupational pension is

their main source of income, whilst this is the case for 14% of the highest educated pensioners.

There are some important variations when looking at the occupation before retirement: the

biggest proportion of manual workers (82%) report that a state or public pension is their main

source of income. Respondents who used to be managers before retirement are situated at the

other end of the scale: 69% report that a state or public pension is their main source of income.

In comparison to other occupation categories, occupational or private pensions are very

important for managers (19%).

35

CHART 18Pensioners: Which of the following is your main source of income? (Q57)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

male

female

studied up to 15 y.

studied up to 16 - 19 y.

studied up to 20+ y.

manual workers

other white collars

self-employed

never did any paid work

managers

EU15

State or public pension Occupational pension Personal pension Other

EUROBAROMETER 56.1 AUTUMN 2001

36

3.1.2. The second most important source of income

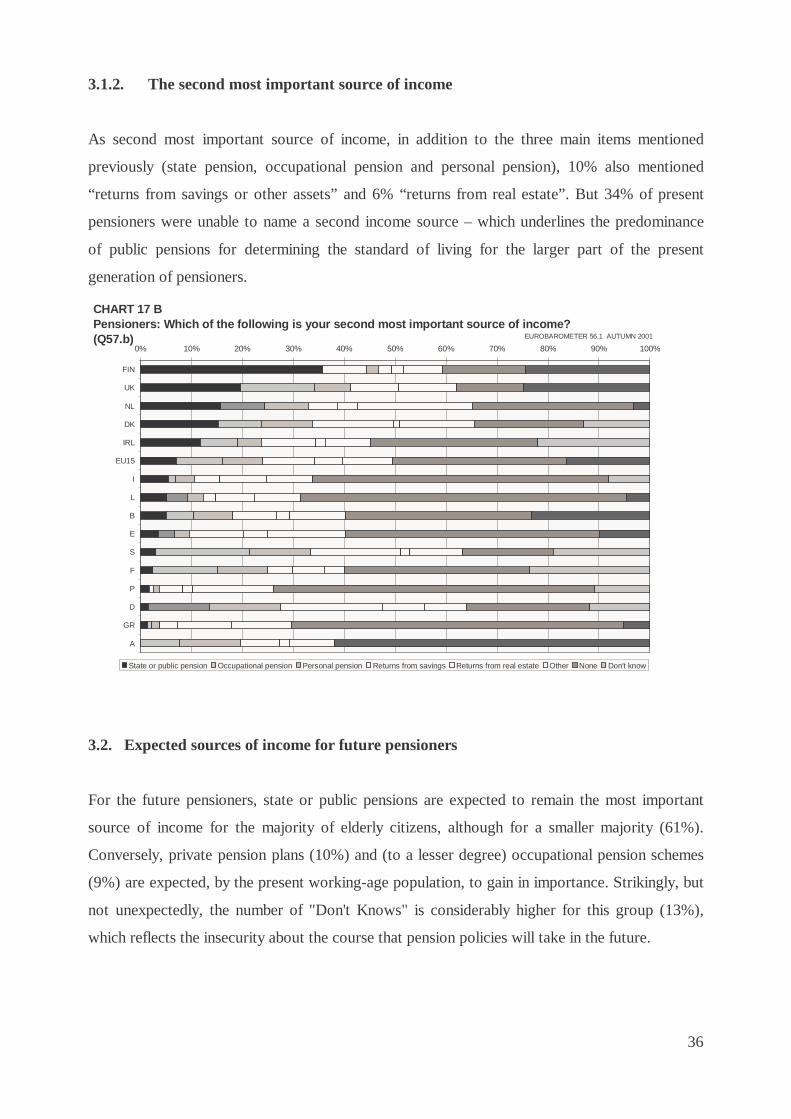

As second most important source of income, in addition to the three main items mentioned

previously (state pension, occupational pension and personal pension), 10% also mentioned

“returns from savings or other assets” and 6% “returns from real estate”. But 34% of present

pensioners were unable to name a second income source – which underlines the predominance

of public pensions for determining the standard of living for the larger part of the present

generation of pensioners.

3.2. Expected sources of income for future pensioners

For the future pensioners, state or public pensions are expected to remain the most important

source of income for the majority of elderly citizens, although for a smaller majority (61%).

Conversely, private pension plans (10%) and (to a lesser degree) occupational pension schemes

(9%) are expected, by the present working-age population, to gain in importance. Strikingly, but

not unexpectedly, the number of "Don't Knows" is considerably higher for this group (13%),

which reflects the insecurity about the course that pension policies will take in the future.

CHART 17 BPensioners: Which of the following is your second most important source of income? (Q57.b)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

FIN

UK

NL

DK

IRL

EU15

I

L

B

E

S

F

P

D

GR

A

State or public pension Occupational pension Personal pension Returns from savings Returns from real estate Other None Don't know

EUROBAROMETER 56.1 AUTUMN 2001

37

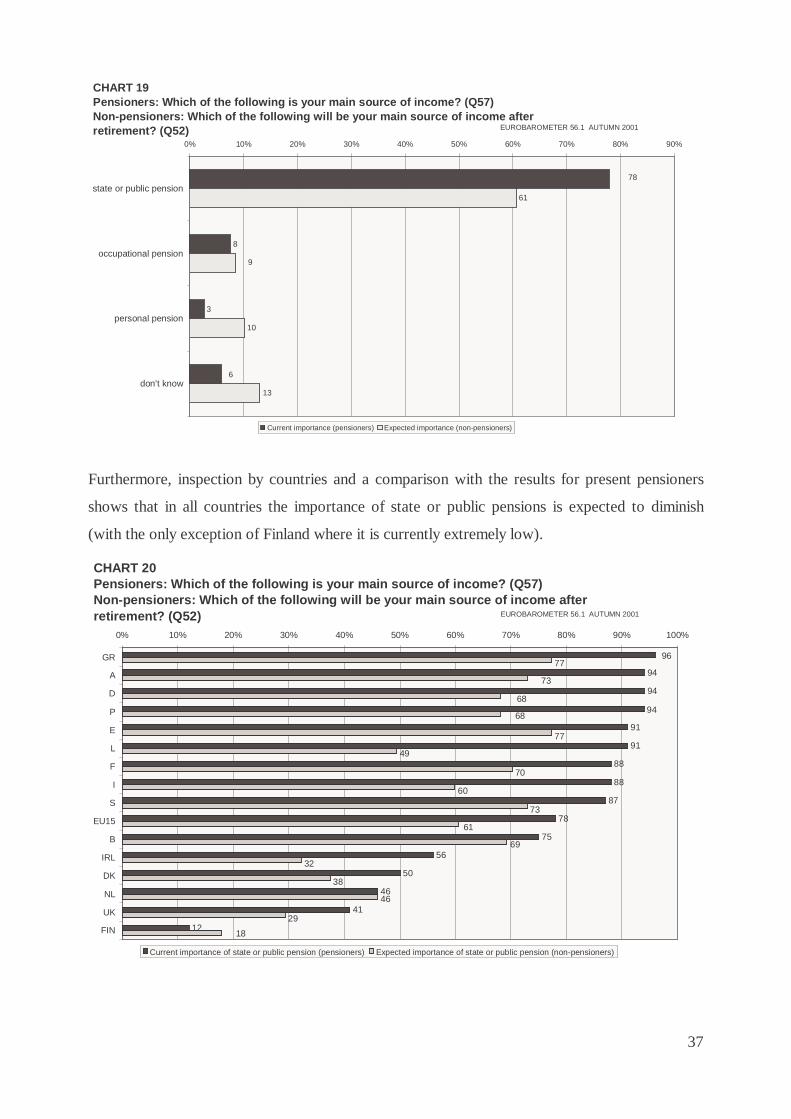

Furthermore, inspection by countries and a comparison with the results for present pensioners

shows that in all countries the importance of state or public pensions is expected to diminish

(with the only exception of Finland where it is currently extremely low).

CHART 19Pensioners: Which of the following is your main source of income? (Q57)Non-pensioners: Which of the following will be your main source of income after retirement? (Q52)

8

3

61

10

13

78

6

9

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

state or public pension

occupational pension

personal pension

don't know

Current importance (pensioners) Expected importance (non-pensioners)

EUROBAROMETER 56.1 AUTUMN 2001

CHART 20Pensioners: Which of the following is your main source of income? (Q57)Non-pensioners: Which of the following will be your main source of income after retirement? (Q52)

94

94

91

91

88

88

87

78

75

56

50

46

41

12

96

94

18

29

46

38

32

69

61

73

60

70

49

77

68

68

77

73

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

GR

A

D

P

E

L

F

I

S

EU15

B

IRL

DK

NL

UK

FIN

Current importance of state or public pension (pensioners) Expected importance of state or public pension (non-pensioners)

EUROBAROMETER 56.1 AUTUMN 2001

38

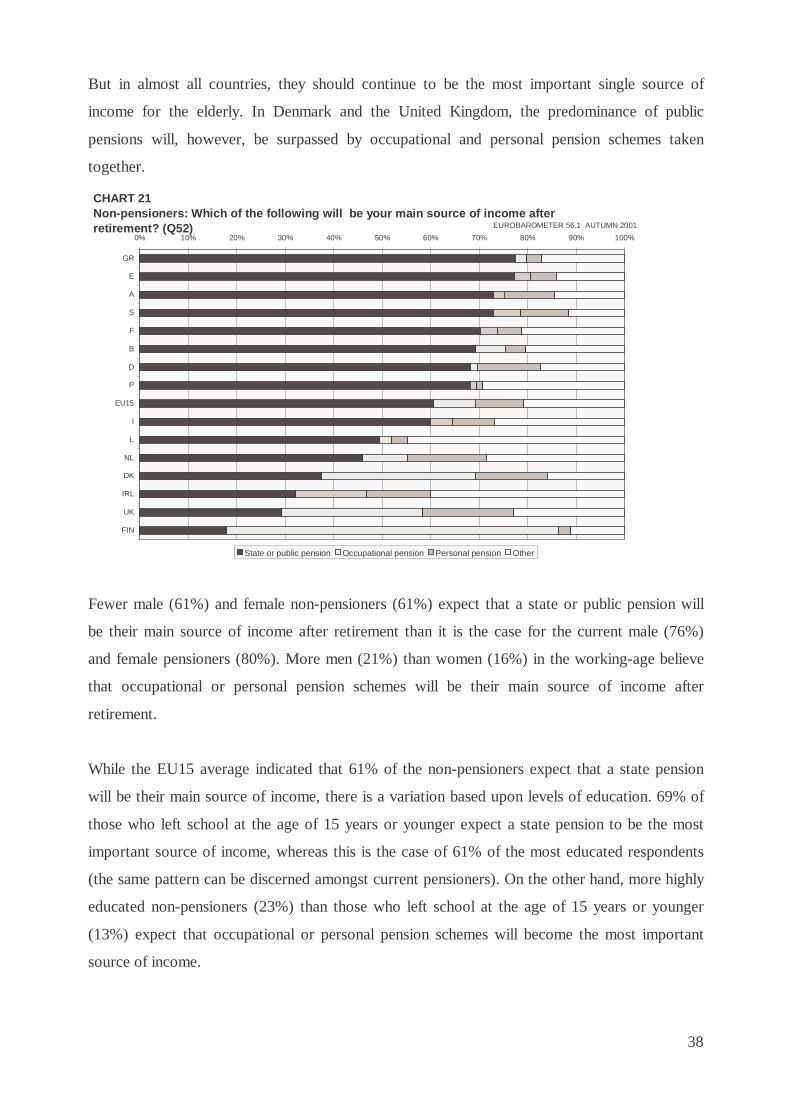

But in almost all countries, they should continue to be the most important single source of

income for the elderly. In Denmark and the United Kingdom, the predominance of public

pensions will, however, be surpassed by occupational and personal pension schemes taken

together.

Fewer male (61%) and female non-pensioners (61%) expect that a state or public pension will

be their main source of income after retirement than it is the case for the current male (76%)

and female pensioners (80%). More men (21%) than women (16%) in the working-age believe

that occupational or personal pension schemes will be their main source of income after

retirement.

While the EU15 average indicated that 61% of the non-pensioners expect that a state pension

will be their main source of income, there is a variation based upon levels of education. 69% of

those who left school at the age of 15 years or younger expect a state pension to be the most

important source of income, whereas this is the case of 61% of the most educated respondents

(the same pattern can be discerned amongst current pensioners). On the other hand, more highly

educated non-pensioners (23%) than those who left school at the age of 15 years or younger

(13%) expect that occupational or personal pension schemes will become the most important

source of income.

CHART 21Non-pensioners: Which of the following will be your main source of income after retirement? (Q52)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

GR

E

A

S

F

B

D

P

EU15

I

L

NL

DK

IRL

UK

FIN

State or public pension Occupational pension Personal pension Other

EUROBAROMETER 56.1 AUTUMN 2001

39

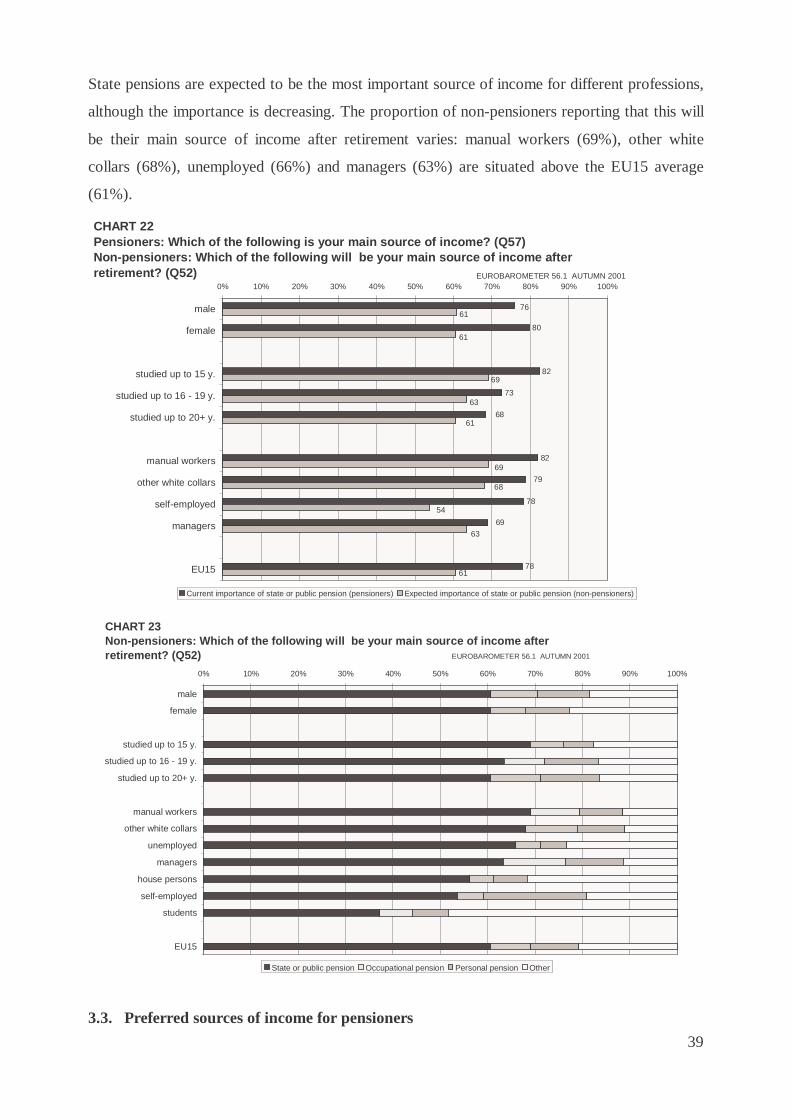

State pensions are expected to be the most important source of income for different professions,

although the importance is decreasing. The proportion of non-pensioners reporting that this will

be their main source of income after retirement varies: manual workers (69%), other white

collars (68%), unemployed (66%) and managers (63%) are situated above the EU15 average

(61%).

3.3. Preferred sources of income for pensioners

CHART 22Pensioners: Which of the following is your main source of income? (Q57)Non-pensioners: Which of the following will be your main source of income after retirement? (Q52)

80

73

82

78

78

69

79

68

76

82

61

63

54

68

69

61

63

69

61

61

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

male

female

studied up to 15 y.

studied up to 16 - 19 y.

studied up to 20+ y.

manual workers

other white collars

self-employed

managers

EU15

Current importance of state or public pension (pensioners) Expected importance of state or public pension (non-pensioners)

EUROBAROMETER 56.1 AUTUMN 2001

CHART 23Non-pensioners: Which of the following will be your main source of income after retirement? (Q52)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

male

female

studied up to 15 y.

studied up to 16 - 19 y.

studied up to 20+ y.

manual workers

other white collars

unemployed

managers

house persons

self-employed

students

EU15

State or public pension Occupational pension Personal pension Other

EUROBAROMETER 56.1 AUTUMN 2001

40

The questions reported in the previous sections refer to the likely shifts in the relative

importance of various income sources. It is a different question, however, to ask people how

pension benefits should be provided. We proposed three alternatives (Q61):

• mainly by state or public pension schemes,

• mainly by occupational pension schemes, or

• mainly by private arrangements.

The pattern of answers shows a certain similarity with the expected importance of the various

sources of income, but also some interesting differences. A clear majority of EU citizens (57%)

shares the opinion that pensions should be mainly provided by public pension schemes. 24%

think that occupational schemes should perform this function, and only 7% think that this task

should be left to (voluntary) private arrangements. For the large majority of citizens, occu-

pational and private-individual schemes may be acceptable as supplementary sources of

income, but not as the main pillar of income security in old age. Thus, an interesting difference

emerges: substantially more people, albeit still a minority (24%), would like occupational

pension schemes to play a larger role than they currently do (8%) and than they will probably

play in the future (9%). And conversely, they would ascribe a smaller role to private

arrangements (7%) than they expect them to play in the future (10%).

CHART 24Pensioners: Which of the following is your main source of income? (Q57)Non-pensioners: Which of the following will be your main source of income (Q52)Pensioners and non-pensioners: How do you think that pensions should be provided?(Q61)

3

61

10

13

24

7

13

8

6

78

9

57

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

state or public pension

occupational pension

personal pension

don't know

Current importance (pensioners) Expected importance (non-pensioners) Desired importance (pensioners and non-pensioners)

EUROBAROMETER 56.1 AUTUMN 2001

41

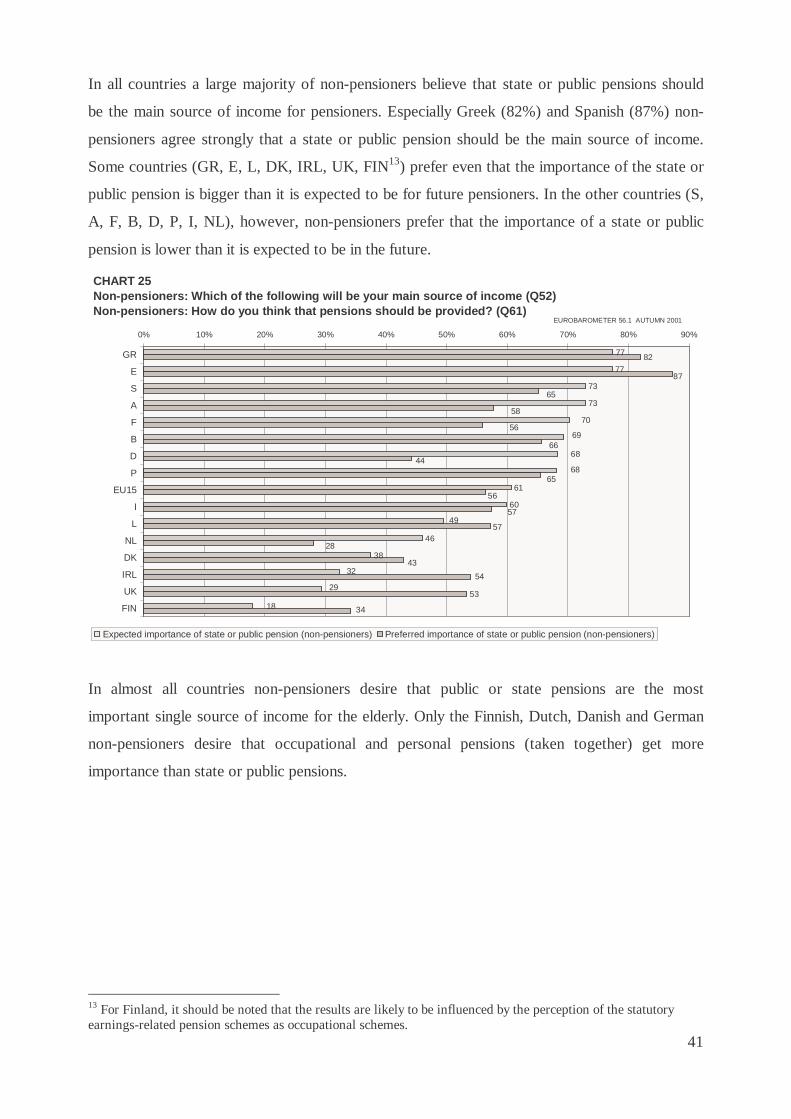

In all countries a large majority of non-pensioners believe that state or public pensions should

be the main source of income for pensioners. Especially Greek (82%) and Spanish (87%) non-

pensioners agree strongly that a state or public pension should be the main source of income.

Some countries (GR, E, L, DK, IRL, UK, FIN13) prefer even that the importance of the state or

public pension is bigger than it is expected to be for future pensioners. In the other countries (S,

A, F, B, D, P, I, NL), however, non-pensioners prefer that the importance of a state or public

pension is lower than it is expected to be in the future.

In almost all countries non-pensioners desire that public or state pensions are the most

important single source of income for the elderly. Only the Finnish, Dutch, Danish and German

non-pensioners desire that occupational and personal pensions (taken together) get more

importance than state or public pensions.

13 For Finland, it should be noted that the results are likely to be influenced by the perception of the statutory earnings-related pension schemes as occupational schemes.

CHART 25Non-pensioners: Which of the following will be your main source of income (Q52)Non-pensioners: How do you think that pensions should be provided? (Q61)

77

77

73

73

61

60

46

38

82

53

49

68

68

32

70

18

29

69

43

28

34

54

57

57

56

65

44

66

56

58

65

87

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

GR

E

S

A

F

B

D

P

EU15

I

L

NL

DK

IRL

UK

FIN

Expected importance of state or public pension (non-pensioners) Preferred importance of state or public pension (non-pensioners)

EUROBAROMETER 56.1 AUTUMN 2001

42

More than half of the male (55%) and female (57%) non-pensioners believe that state or public

pensions should be the most important source of income after retirement. Compared to the

expected importance of state or public pensions, this would imply that both male and female

non-pensioners prefer that state pensions would play a somewhat less important role in the

household income, although state pensions clearly remain by far the preferred main source of

income in old age. Next to state or public pensions, more men (34%) than women (28%)

mention occupational or personal pension schemes as the preferred main source of income.

Time spent on education tends to reduce the preference for state or public pensions as main

income after retirement. While 67% of the non-pensioners educated to the age of 15 years or

less prefer this option, this figure decreases to 54% for those whose education has continued to

the age of 20 years or beyond. All non-pensioners prefer that state pensions play a smaller role

than they are expected to play for the future pensioners.

When looking at results broken down by occupation, especially unemployed (66%) and manual

workers (60%) believe that a state or public pension should be the main source of income.

House persons, self-employed non-pensioners and students prefer even that the importance of

state or public pension increase, whereas other occupational categories believe that the

importance of state or public pension should be diminished. The proportion of managers who

CHART 26Non-pensioners: How do you think that pensions should be provided, mainly by? (Q61)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

E

GR

B

P

S

A

I

L

EU15

F

IRL

UK

D

DK

FIN

NL

State or public pension Occupational pension Personal pension Other

EUROBAROMETER 56.1 AUTUMN 2001

43

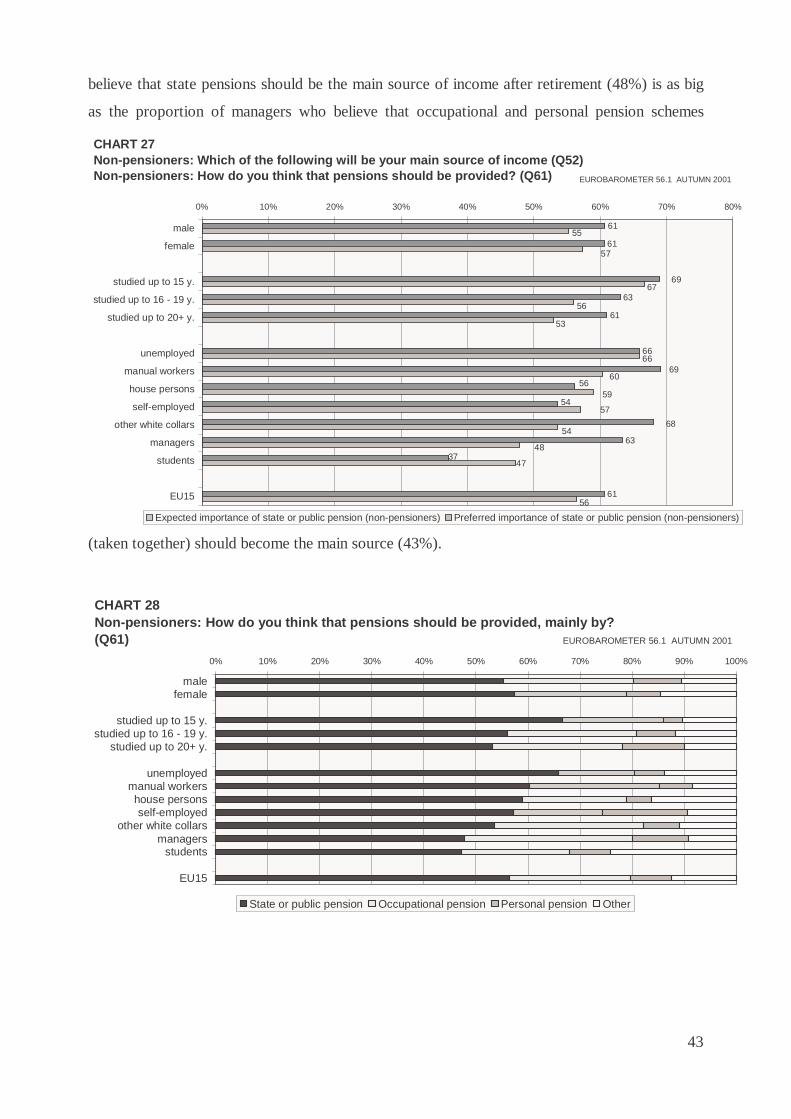

believe that state pensions should be the main source of income after retirement (48%) is as big

as the proportion of managers who believe that occupational and personal pension schemes

(taken together) should become the main source (43%).

CHART 27Non-pensioners: Which of the following will be your main source of income (Q52)Non-pensioners: How do you think that pensions should be provided? (Q61)

61

61

63

61

66

63

61

56

69

69

37

68

54

56

47

48

54

57

59

60

66

53

56

67

57

55

0% 10% 20% 30% 40% 50% 60% 70% 80%

male

female

studied up to 15 y.

studied up to 16 - 19 y.

studied up to 20+ y.

unemployed

manual workers

house persons

self-employed

other white collars

managers

students

EU15

Expected importance of state or public pension (non-pensioners) Preferred importance of state or public pension (non-pensioners)

EUROBAROMETER 56.1 AUTUMN 2001

CHART 28Non-pensioners: How do you think that pensions should be provided, mainly by? (Q61)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

malefemale

studied up to 15 y.studied up to 16 - 19 y.

studied up to 20+ y.

unemployedmanual workershouse personsself-employed

other white collarsmanagers

students

EU15

State or public pension Occupational pension Personal pension Other

EUROBAROMETER 56.1 AUTUMN 2001

44

4. Goals and principles of pension systems

An important issue for the debate about the course future pension reforms should take, are the

normative foundations of pension policies. Therefore, we asked a series of questions about

goals and principles of pension systems in order to investigate the underlying value orientations,

in particular the ideas on social justice held by citizens. More precisely: we asked people

whether they agreed14 or disagreed15 with a series of normative statements which reflect the

desirability of currently discussed reform options (Q62). These statements concern broad goals

such as the prevention of poverty in old age (4.1.1.), maintaining an adequate standard of living

(4.1.2.) and reducing social inequalities amongst the elderly (4.1.3.). Furthermore, the