the future of e- commerce - sharesinvestcoach.com · fairprice and cold storage have e-commerce...

TRANSCRIPT

The Future of E-commerce

Done By: Kenny Ong1

Agenda:1. Introduction2. Industry Analysis3. Forecasts4. Implications5. Emerging Tech6. Conclusion

2

Introduction

3

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 4

Value Chain Analysis - Disintermediation

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 5

Definitions

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech

IndustryAnalysis

6

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 7

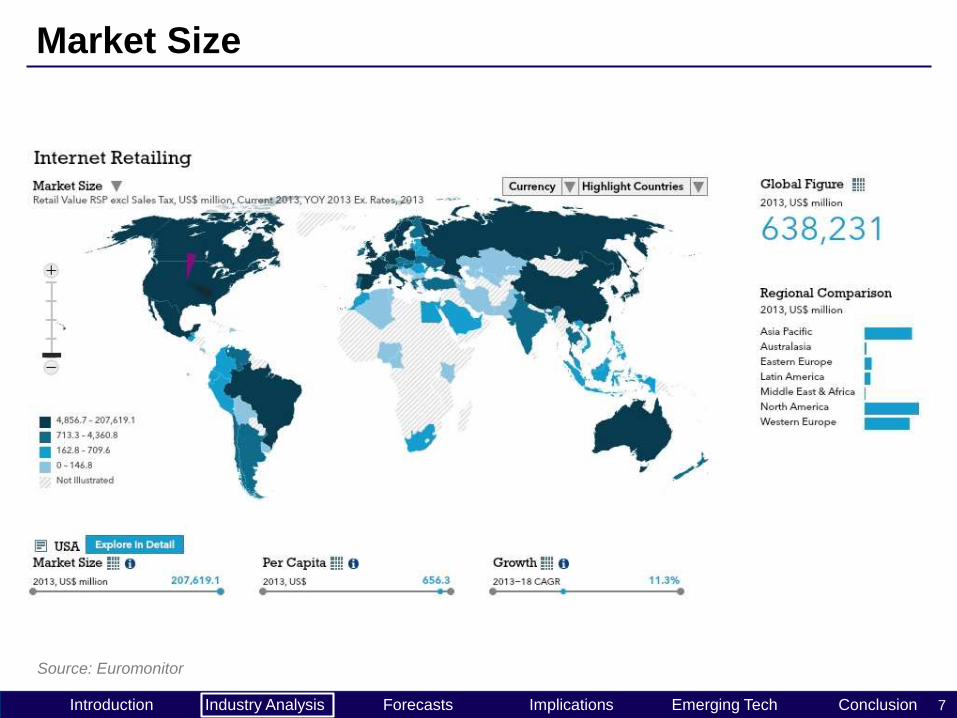

Market Size

Source: Euromonitor

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 8

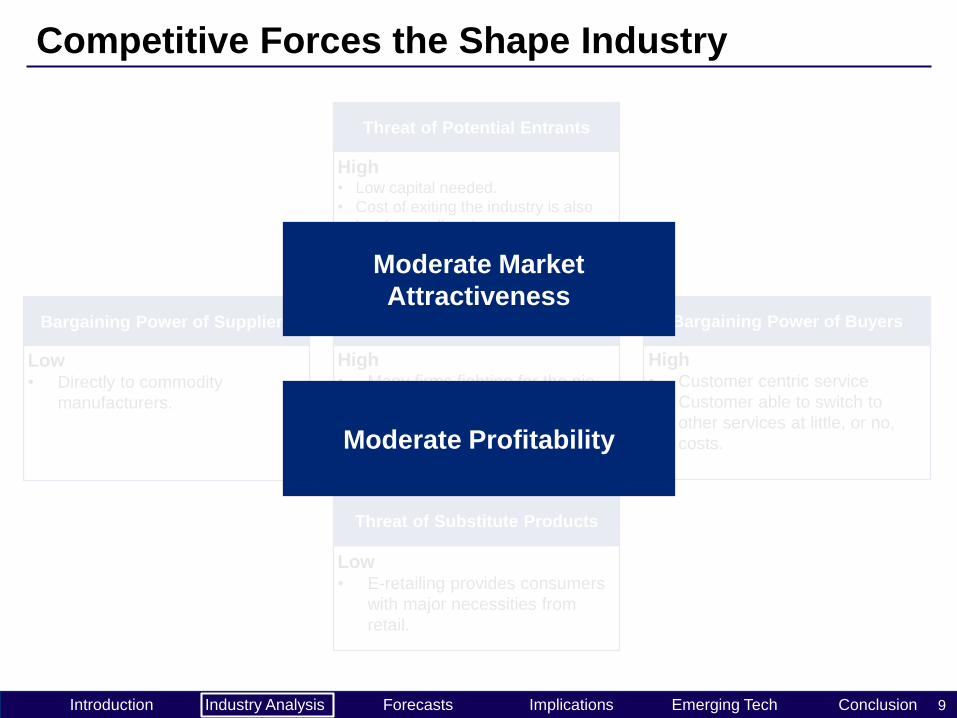

Competitive Forces the Shape Industry

Bargaining Power of Buyers

Moderate• Customer centric service

• Customer able to switch to

other services at little, or no,

costs.

Threat of Potential Entrants

High• Low capital needed.

• Cost of exiting the industry is also

low for smaller players.

Threat of Substitute Products

Low• E-retailing provides consumers

with major necessities from

retail.

Rivalry among Competing Firms

Moderate• Many firms fighting for the pie

with some obvious winners.

Bargaining Power of Suppliers

Low• Directly to commodity

manufacturers.

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 9

Competitive Forces the Shape Industry

Bargaining Power of Buyers

High• Customer centric service

• Customer able to switch to

other services at little, or no,

costs.

Threat of Potential Entrants

High• Low capital needed.

• Cost of exiting the industry is also

low for smaller players.

Threat of Substitute Products

Low• E-retailing provides consumers

with major necessities from

retail.

Rivalry among Competing Firms

High• Many firms fighting for the pie

with some obvious winners.

Bargaining Power of Suppliers

Low• Directly to commodity

manufacturers.

Moderate Market

Attractiveness

Moderate Profitability

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 10

Industry Life Cycle

Source: Emerald Insight

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 11

Historical Growth (2008-2013)

Souce: Euromonitor

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2008 2009 2010 2011 2012 2013

E-C

om

me

rce

Sal

es

(US

Mn

)

World

USA

Western Europe

Japan

China

Indonesia

Singapore

CAGR: 17%

CAGR: 13%

CAGR: 122%

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 12

Historical Growth (2008-2013)

0.0

100,000.0

200,000.0

300,000.0

400,000.0

500,000.0

600,000.0

700,000.0

2008 2009 2010 2011 2012 2013

World

USA

Western Europe

Japan

China

Indonesia

Singapore

CAGR: 17%

CAGR: 13%

CAGR: 122%

Where are we heading to?

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech

Forecasts

13

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 14

Is the how you want to shop?

Soruce: The Columbian

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 15

Or would you rather shop from home?

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 16

Many companies in the US are announcing cuts

More than 1000 stores closed

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 17

Where do they shop at now?

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 18

Online Growth far outstrips Offline Growth

Source: Euromonitor

2008 2009 2010 2011 2012 2013

World(Offline) 10,900,231.2 11,059,031.0 11,513,269.7 12,062,173.9 12,650,706.3 13,277,934.3

World(Online) 281,598.9 300,738.0 364,261.5 458,541.6 545,011.8 638,231.0

WorldGrowth(Offline) 1% 4% 5% 5% 5%

WorldGrowth(Online) 7% 21% 26% 19% 17%

0%

5%

10%

15%

20%

25%

30%

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

TotalR

etailSalesUS$m

n

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 19

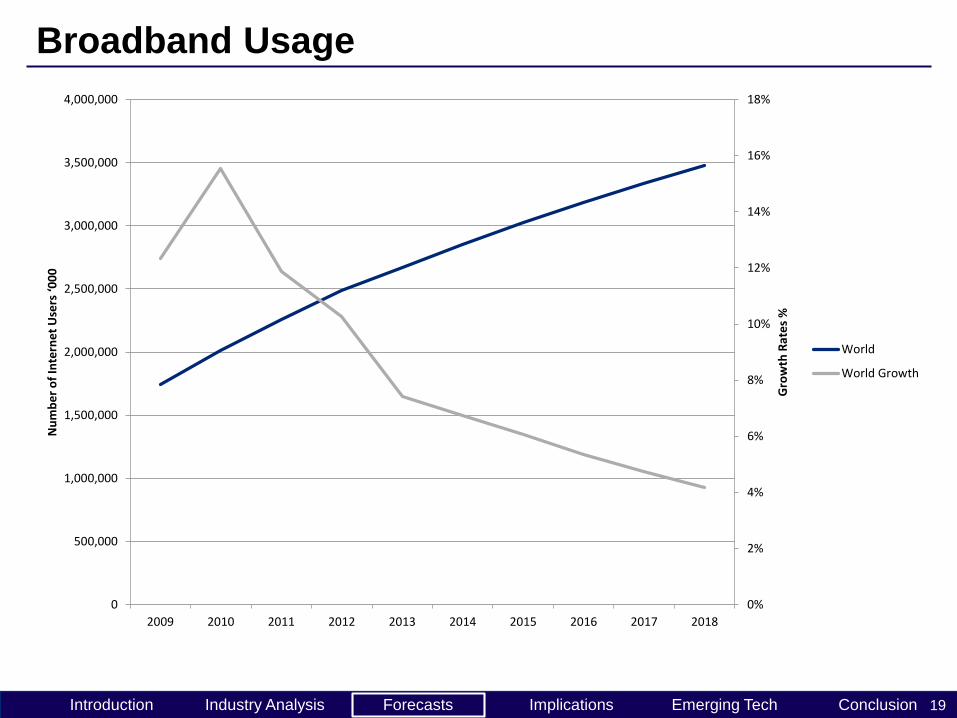

Broadband Usage

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Gro

wth

Rat

es

%

Nu

mb

er

of

Inte

rne

t U

sers

‘00

0

World

World Growth

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 20

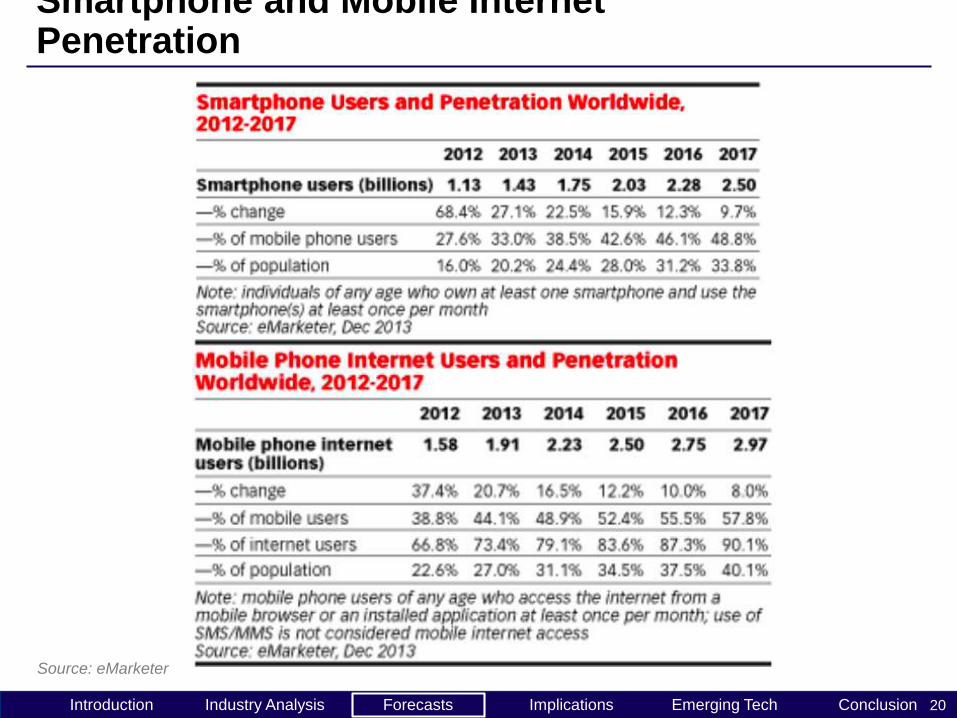

Smartphone and Mobile Internet Penetration

Source: eMarketer

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 21

Time Spent on Internet

Source: Wearesocial

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 22

Global Adspend

Source: Nielsen

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 23

New technologies to make shopping more convenient

Source: Deloitte

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 24

New technologies to make shopping more convenient

Source: Financial Times

Integration with various social

media and touchpoints

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 25

New technologies to make shopping more convenient

Source: H&M

Augmented reality and virtual

fitting rooms

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 26

New technologies to make shopping more convenient

Source: Amazon

2 day shipping? How about

30 minutes with drones?

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 27

E-commerce Industry Forecast

Source: Euromonitor

2013 2014 2015 2016 2017 2018

World (Offline) 13,277,934.3 14,030,864.7 14,904,524.0 15,881,874.8 16,950,398.6 18,129,175.3

World (Online) 638,231.0 757,761.0 890,131.1 1,035,403.4 1,187,387.9 1,346,180.9

World Growth (Offline) 5% 6% 6% 7% 7% 7%

World Growth (Online) 17% 19% 17% 16% 15% 13%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000R

eta

il Sa

les

US$

mn

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech

Implications

28

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 29

Logistics and Delivery Services

Source: JONES LANG LASALLE IP

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 30

E-commerce Software Platforms

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 31

Advertising and Digital Marketing

Source: Singpost

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 32

Payment Services

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech

Emerging Technology

33

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 34

Other Emerging Commerce

M-Commerce

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 35

Other Emerging Commerce

T-Commerce

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 36

Other Emerging Commerce

Source: Google

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech

Conclusion

37

Introduction Forecasts Implications ConclusionIndustry Analysis Emerging Tech 38

Conclusion (Bringing back to Singapore)

Source: Euromonitor

Some Trends

• Pure internet retailers performed better than “bricks and clicks”. In addition, new dominant players such as Zalora Singapore and Qoo10 Singapore are also pure internet retailers.

• Local retailers trying to innovate. EgNoel and local supermarkets NTUC FairPrice and Cold Storage have e-commerce platforms, with Sheng Siong coming up soon.

• Dominant segments are Apparels and Beauty Care with Furnishing being the obvious laggard. However, IKEA launch an augmented reality platform to help make sales.

• More active use of Social Media such as Instagram to help improve brand awareness of smaller players.

S$ Mn 2012 20132013-18

CAGR

Beauty and Personal Care 14.5 16.8 21%

Apparel and Footwear 252.1 267.6 10%

Consumer Electronics 103.2 110.9 1%

Consumer Healthcare 17.3 19.1 16%

Consumer Applicances 2.9 3.6 0%

House Care 1 1 6%

Home Improvement and

Gardening1.9 2.1 4%

Housewares and Home

Furnishings 0.3 0.3 5%

Media Products 45.7 50.7 9%

Food and Drink 59.8 63.9 2%

Traditional Toys and

Games3.3 3.9 11%

Other Internet Retailing 353.5 420.4 15%

Internet Retailing 855.4 960.3 11%