the future of chemical and pharmaceutical production in ... · >> perspectives_2012 the...

TRANSCRIPT

>> PERSPECTIVES_2012 THE FUTURE OF CHEMICAL AND PHARMACEUTICAL PRODUCTION IN GERMANY CMF JUNE 19, 2012 – FACILITATED BY DR. MICHAEL REUBOLD, CHEMANAGER

>> A BUSINESS PERSPECTIVE. THE FUTURE OF VALUE CREATION IN THE GERMAN CHEMICAL & PHARMACEUTICAL INDUSTRY

Dr. Udo Jung The Boston Consulting Group ACHEMA PERSPECTIVES 2012

The future of value creation in the German chemical and pharmaceutical industry

Frankfurt , June 19, 2012 Dr. Udo Jung

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 3

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

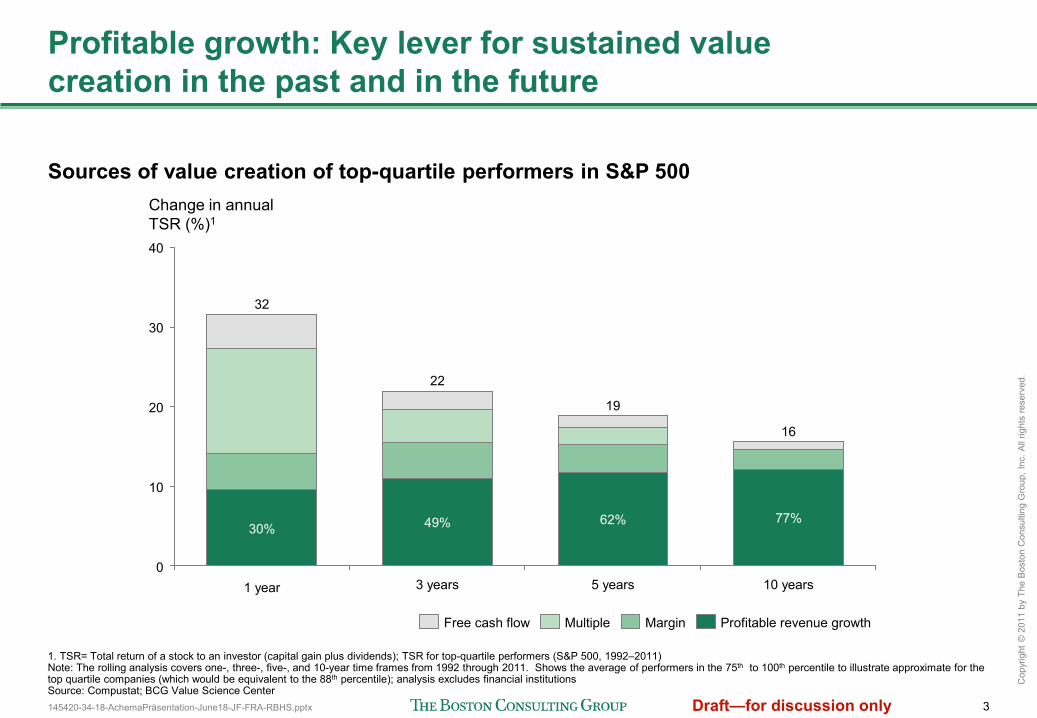

40

30

20

10

0 1 year

32

30%

Change in annual TSR (%)1

Profitable growth: Key lever for sustained value creation in the past and in the future

Sources of value creation of top-quartile performers in S&P 500

Profitable revenue growth Margin Multiple Free cash flow

1. TSR= Total return of a stock to an investor (capital gain plus dividends); TSR for top-quartile performers (S&P 500, 1992–2011) Note: The rolling analysis covers one-, three-, five-, and 10-year time frames from 1992 through 2011. Shows the average of performers in the 75th to 100th percentile to illustrate approximate for the top quartile companies (which would be equivalent to the 88th percentile); analysis excludes financial institutions Source: Compustat; BCG Value Science Center

10 years

16

5 years

19

3 years

22

77% 62% 49%

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 4

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

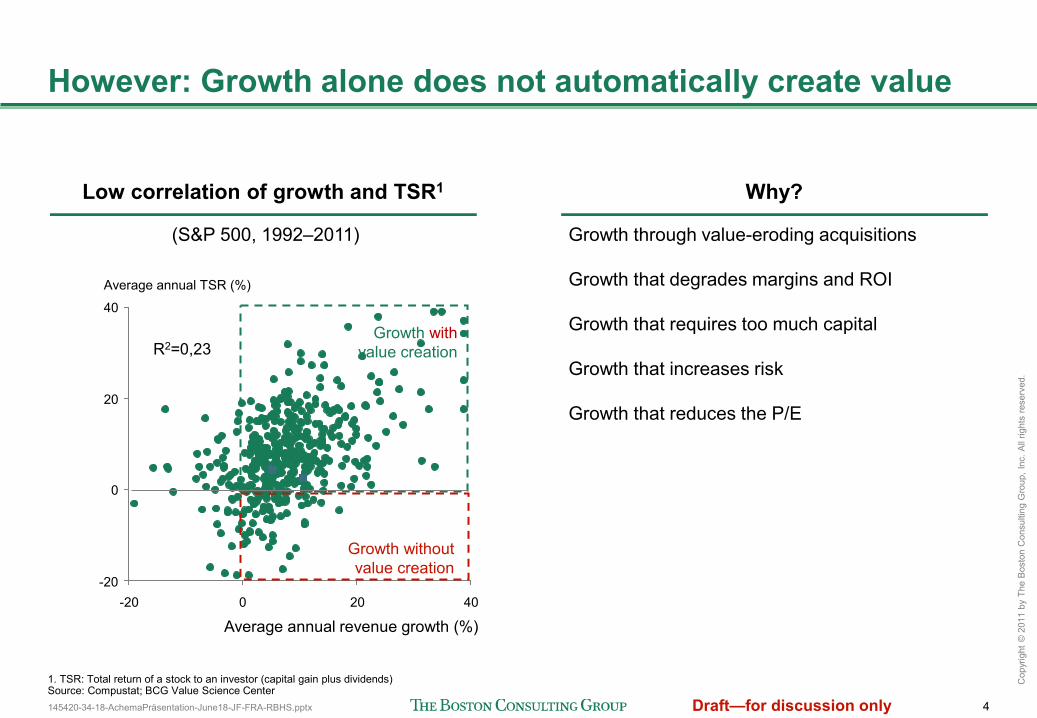

However: Growth alone does not automatically create value

Low correlation of growth and TSR1

(S&P 500, 1992–2011)

Why?

Growth through value-eroding acquisitions Growth that degrades margins and ROI Growth that requires too much capital Growth that increases risk Growth that reduces the P/E

Average annual TSR (%)

40

20

0

-20

Average annual revenue growth (%) 40 20 0 -20

Growth without value creation

Growth with value creation R2=0,23

1. TSR: Total return of a stock to an investor (capital gain plus dividends) Source: Compustat; BCG Value Science Center

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 5

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

Note: GDP as $ in Purchasing Power Parity (PPP) Source: EIU; BCG analysis

Capturing profitable growth in Asia drives business model changes of German chemical and pharmaceutical companies

3.1

Rest of

Latam

3.4

World

3.5

Russia

3.7

Middle East

3.9

C.E. Europe

4.0

China

2010–2025, GDP growth (%) 6

4

2

0

Japan

2.0

EU-15

2.4

USA

2.8

Brazil

4.6

Rest of

Asia

5.2

India

5.5

Middle East

2.7

Rest of

Latam

2.0

EU-15

5.4

USA

9.3

0 World

4.6

RoW

2.9

Brazil

1.2

C.E. Europe

1.3

Japan

Russia

1.6 1.4

7.7

China

7.8

India

2010–2025, GDP growth (Trillion US$) 50 47.9

40

20

10

30

Rest of

Asia

World GDP (K US$)

2010 70.6

2025 118.5 3.5%

x% CAGR

Asia

We are in a two speed world: Asia expected to contribute 45% of global GDP growth until 2025

Asian economies growth compensate for OECD countries underperformance

Asia (ex-Japan) accounts for 45% of overall GDP growth until 2025

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 6

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

16%

55%

6%

2010

Asia Pacific

Western Europe North America South America Rest of World

17%

6% 7%

2030

5% 19%

21%

49%

More than 60% of the total global demand growth in chemicals until 2030 contributed by Asia Pacific

Source: CEFIC Fact and Figures 2011; various analyst reports; company presentations; BCG analysis

+1,310

+224

+305

+132

+180

9% Rest of World

6% South America

14% North America

10% Western Europe

61% Asia Pacific

+2,151

Global chemical demand (€B) 2,353

4,504

Annual growth rate

4.1%

1.9%

2.6%

3.6% 4.4%

3.3%

Growth contribution

Backup

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 7

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

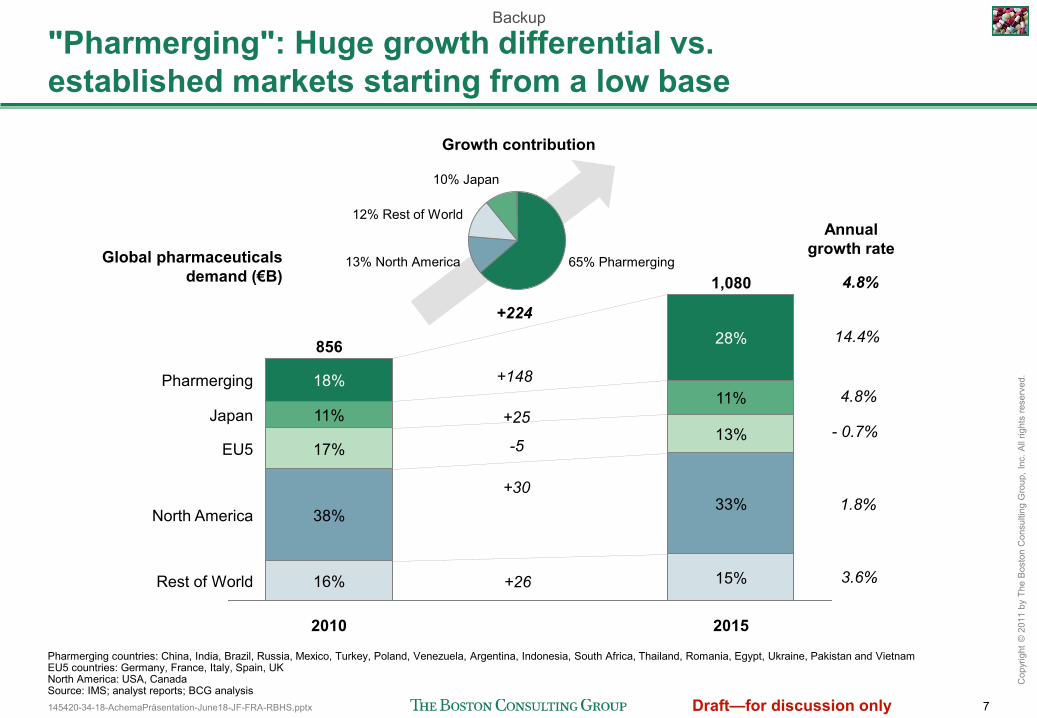

Rest of World

North America

EU5

Japan

Pharmerging

2015

1,080

15%

33%

13%

11%

28%

2010

856

16%

38%

17%

11%

18%

"Pharmerging": Huge growth differential vs. established markets starting from a low base

Pharmerging countries: China, India, Brazil, Russia, Mexico, Turkey, Poland, Venezuela, Argentina, Indonesia, South Africa, Thailand, Romania, Egypt, Ukraine, Pakistan and Vietnam EU5 countries: Germany, France, Italy, Spain, UK North America: USA, Canada Source: IMS; analyst reports; BCG analysis

+148

+25

-5

+30

+26

12% Rest of World

10% Japan

13% North America 65% Pharmerging

+224

Global pharmaceuticals demand (€B)

Annual growth rate

14.4%

4.8%

- 0.7%

1.8%

3.6%

4.8%

Growth contribution

Backup

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 8

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

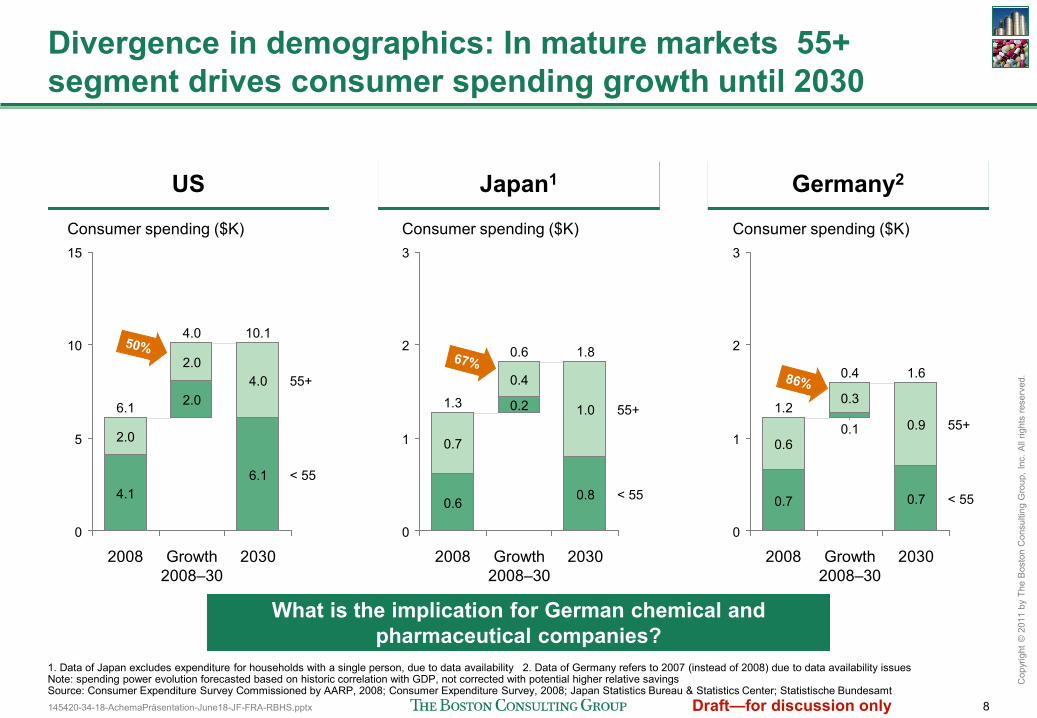

Divergence in demographics: In mature markets 55+ segment drives consumer spending growth until 2030

1. Data of Japan excludes expenditure for households with a single person, due to data availability 2. Data of Germany refers to 2007 (instead of 2008) due to data availability issues Note: spending power evolution forecasted based on historic correlation with GDP, not corrected with potential higher relative savings Source: Consumer Expenditure Survey Commissioned by AARP, 2008; Consumer Expenditure Survey, 2008; Japan Statistics Bureau & Statistics Center; Statistische Bundesamt

US Japan1 Germany2

2030

10.1

6.1

4.0

Growth 2008–30

4.0

2.0

2.0

2008

6.1

4.1

2.0

Consumer spending ($K) 15

10

5

0

< 55

55+

Consumer spending ($K) 3

2

1

0

< 55

55+

2030

1.8

0.8

1.0

Growth 2008–30

0.6

0.2

0.4

2008

1.3

0.6

0.7 0.1

0.3

2008

1.2

0.7

0.6

Growth 2008–30

0.4

2

1

0

< 55

55+

2030

1.6

0.7

0.9

3

Consumer spending ($K)

What is the implication for German chemical and pharmaceutical companies?

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 9

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

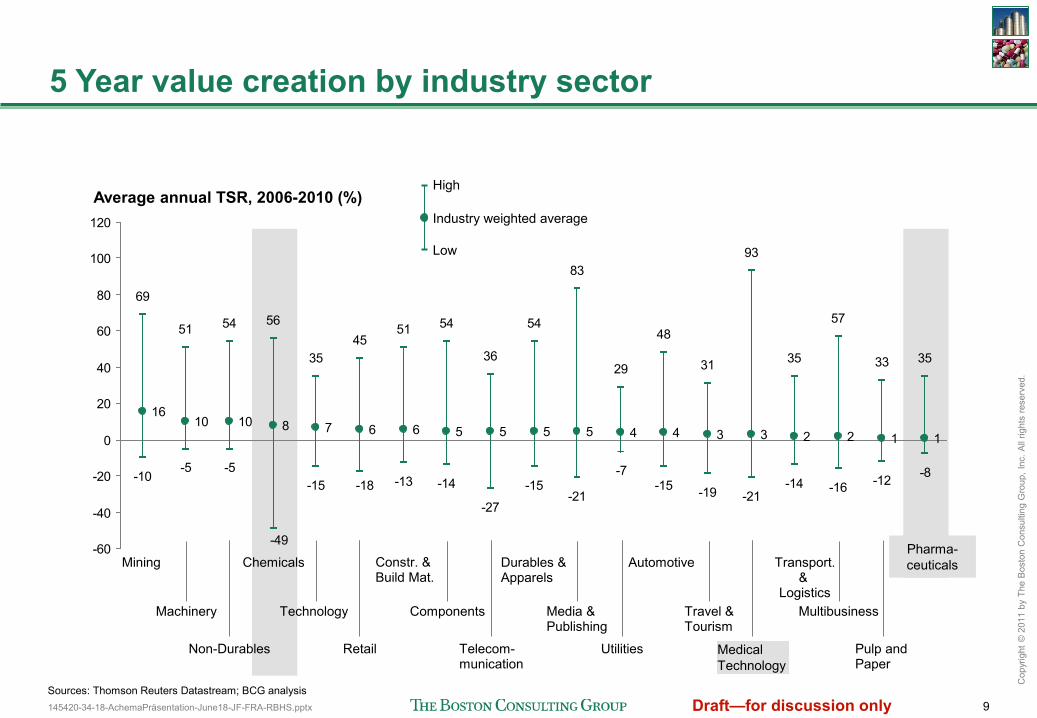

5 Year value creation by industry sector

69

51 54 56

3545

51 54

36

54

83

29

48

31

93

35

57

33 35

1610 10 8 7 6 6 5 5 5 5 4 4 3 3 2 2 1 1

-10-5 -5

-15 -13 -14

-27

-15-21

-7-15 -19 -21

-14 -16 -12 -8-18

-49-60

-40

-20

0

20

40

60

80

100

120

Average annual TSR, 2006-2010 (%) High

Low

Industry weighted average

Chemicals

Machinery

Non-Durables

Mining

Media & Publishing

Travel & Tourism

Pharma- ceuticals

Telecom- munication

Utilities Retail Pulp and Paper

Multibusiness

Automotive

Sources: Thomson Reuters Datastream; BCG analysis

Technology Components

Durables & Apparels

Medical Technology

Transport. &

Logistics

Constr. & Build Mat.

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 11

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

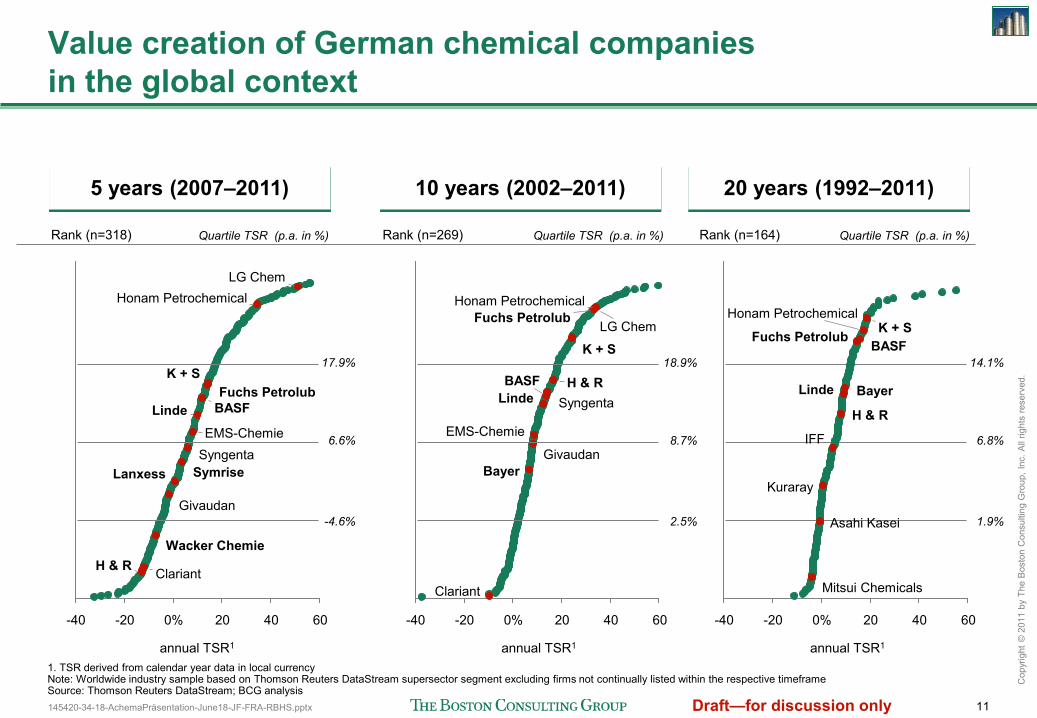

annual TSR1

Rank (n=164) Quartile TSR (p.a. in %)

20 years (1992–2011)

Rank (n=318)

annual TSR1

5 years (2006–2010)

Quartile TSR (p.a. in %)

5 years (2007–2011)

annual TSR1

Rank (n=269)

10 years (2002–2011)

Quartile TSR (p.a. in %)

Fuchs Petrolub K + S

Honam Petrochemical LG Chem

60 40 20 0% -20 -40

H & R Clariant

Wacker Chemie

Givaudan

Lanxess Symrise Syngenta EMS-Chemie

Linde BASF

-40

Clariant

Bayer Givaudan

EMS-Chemie

60 40 20 0% -20

Linde BASF

Syngenta H & R

K + S

Fuchs Petrolub LG Chem

Honam Petrochemical

1. TSR derived from calendar year data in local currency Note: Worldwide industry sample based on Thomson Reuters DataStream supersector segment excluding firms not continually listed within the respective timeframe Source: Thomson Reuters DataStream; BCG analysis

Value creation of German chemical companies in the global context

17.9%

6.6%

-4.6%

18.9%

8.7%

2.5%

14.1%

6.8%

1.9%

60 40 20 0% -20 -40

Mitsui Chemicals

Asahi Kasei

Kuraray

IFF

H & R

Linde Bayer

Fuchs Petrolub BASF

Honam Petrochemical K + S

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 13

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

Observations in value creation patterns in the global chemical industry in the past 5 years

Observation

• Overall Asian chemical companies lead in value creation—especially in base chemicals

• Agro related chemical businesses with superior value creation

• Japan with specific challenges in value creation

• German & European chemical companies with a good track record in diversified and specialty chemicals business models—driven by the ability to manage differentiated business models

1

2

3

4

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 14

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

Global energy and geopolitical trends create challenges for the European and German based chemical industry

Feedstock advantaged countries will continue investing in a scenario of lower gas prices vs. higher naphtha prices

• No great expectations for cheap unconventional gas in Europe • Shale gas revolution in the US reduces European competitiveness in Chemicals

Countries will growing Chemicals demand and advantaged feedstock will increasingly drive their own economic development agenda, which includes localization of chemicals supply sources

• Increase value added to local economies • Reduce imports and increase self sustainability

For specialty chemicals customer proximity (in emerging markets) provides competitive advantage, thus favoring new capacity in demand centers—successful European chemical companies will have to "localize" their global business models Regulatory pressure on the chemical and adjacent sectors (e.g., power) will lead to increased costs in Europe and a potential reduction of European industry competitiveness Larger and integrated new "megasites" in the Middle East and in Asia copy successful European examples Are there unique advantages for European based value add

in production, innovation and business management?

1

2

3

4

5

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 16

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

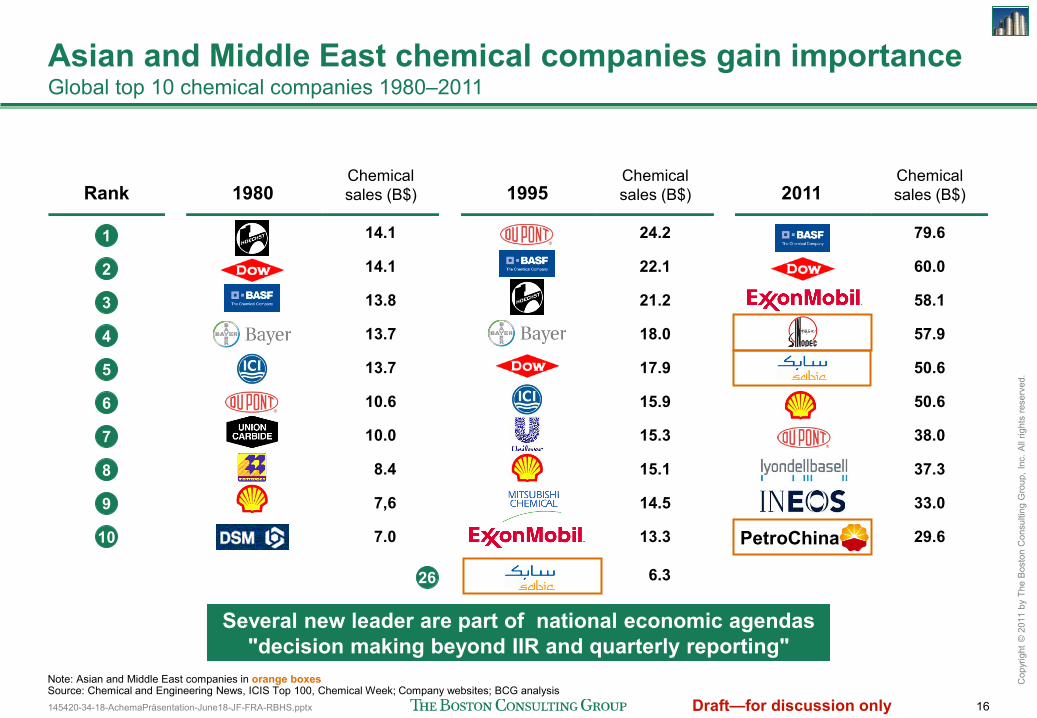

Asian and Middle East chemical companies gain importance Global top 10 chemical companies 1980–2011

Note: Asian and Middle East companies in orange boxes Source: Chemical and Engineering News, ICIS Top 100, Chemical Week; Company websites; BCG analysis

Several new leader are part of national economic agendas "decision making beyond IIR and quarterly reporting"

Rank 1980 Chemical sales (B$) 1995

Chemical sales (B$) 2011

Chemical sales (B$)

79.6

60.0

58.1

57.9

50.6

50.6

38.0

37.3

33.0

29.6

14.1

14.1

13.8

13.7

13.7

10.6

10.0

8.4

7,6

7.0

24.2

22.1

21.2

18.0

17.9

15.9

15.3

15.1

14.5

13.3

6.3

PetroChina

1

2

3

4

5

6

7

8

9

10

26

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 18

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

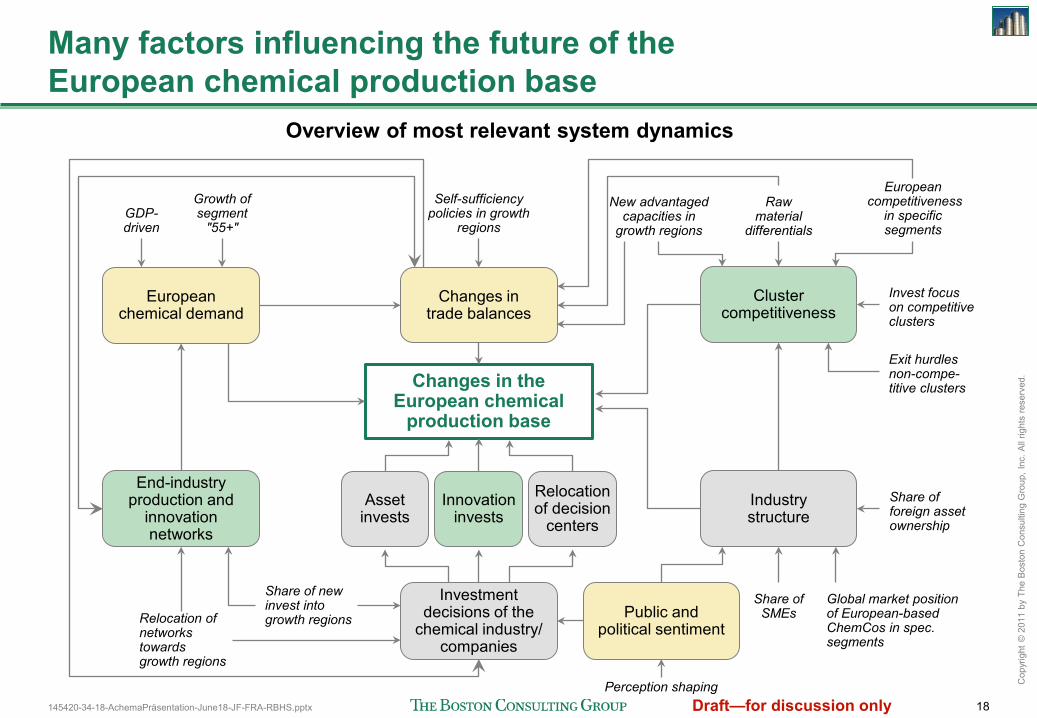

Many factors influencing the future of the European chemical production base

Overview of most relevant system dynamics

Changes in the European chemical

production base

Asset invests

Innovation invests

Relocation of decision

centers

Investment decisions of the

chemical industry/ companies

Public and political sentiment

Industry structure

End-industry production and

innovation networks

Relocation of networks towards growth regions

Share of new invest into growth regions

European chemical demand

GDP- driven

Growth of segment

"55+"

Self-sufficiency policies in growth

regions

Perception shaping

Share of SMEs

Global market position of European-based ChemCos in spec. segments

Share of foreign asset ownership

Cluster competitiveness

New advantaged capacities in

growth regions

Raw material

differentials

European competitiveness

in specific segments

Invest focus on competitive clusters

Exit hurdles non-compe-titive clusters

Changes in trade balances

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 19

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

European Advantage (I): The competiveness of chemical sites and clusters in Europe will become even more decisive

Large

Small to medium size Region

Rheinland-Pfalz (Mainz), DE

Düsseldorf, DE

Vlaams Gewest (Antwerpen), BE

Rhône-Alpes (Lyon), FR

Istanbul, TR

Darmstadt (Frankfurt am Main), DE

Köln, DE

Ege (izmir), TR

Münster, DE

Cheshire (Chester), UK

Nordwestschweiz (Basel), CH

Size (employees)

40,075

25,284

21,937

20,361

18,133

16,250

15,928

10,587

9,590

9,108

8,549

Source: The role of clusters in the chemical industry; BCG analysis

Value added provided by industrial parks and industry cluster • Better access to raw materials

(for chemical industries) • Easier movement of final outputs as

inputs to other downstream sectors • Reduction in energy footprint and

increased efficiency • Common investment in required

infrastructures (rail, ports, pipe- lines, …) reduce investment requirements and minimizes environmental footprint

• Opportunities to coordinate and cooperate in key fields (distribution, R&D, purchasing, …)

• Option to leverage larger scale projects though associations

• .......

A unique "German advantage": cross-industry production, innovation and supply chain clusters—driven by the "Mittelstand champions"

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 20

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

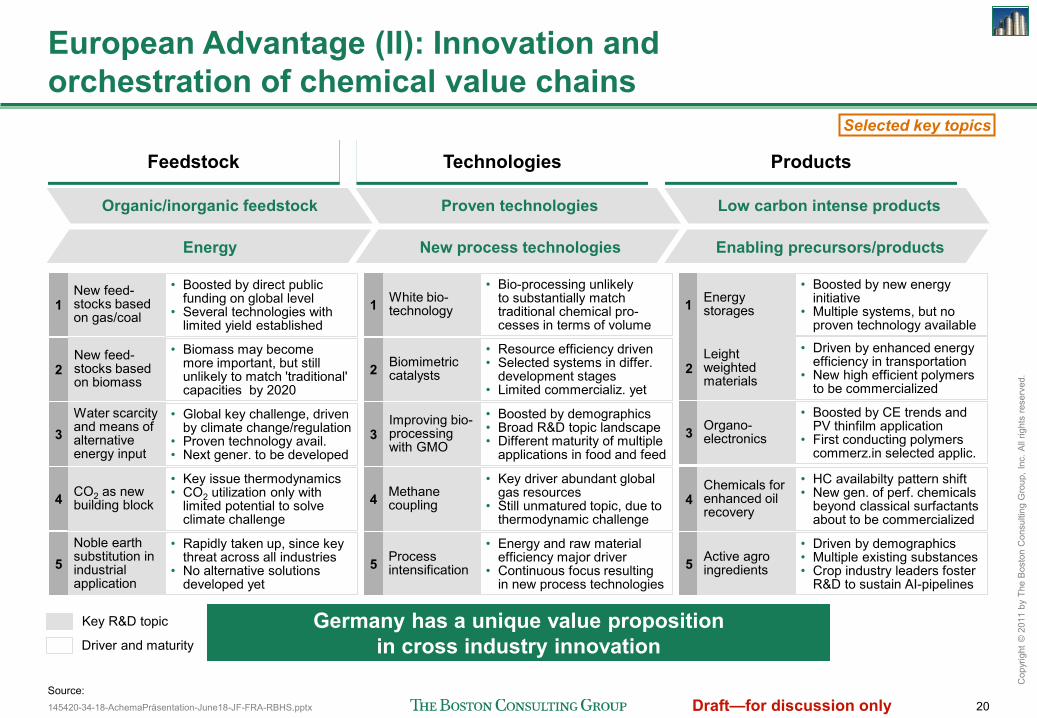

CO2 as new building block

Noble earth substitution in industrial application

• Key issue thermodynamics • CO2 utilization only with

limited potential to solve climate challenge

• Rapidly taken up, since key threat across all industries

• No alternative solutions developed yet

New feed-stocks based on biomass

New feed- stocks based on gas/coal

• Biomass may become more important, but still unlikely to match 'traditional' capacities by 2020

• Boosted by direct public funding on global level

• Several technologies with limited yield established

Water scarcity and means of alternative energy input

• Global key challenge, driven by climate change/regulation

• Proven technology avail. • Next gener. to be developed

Process intensification

Methane coupling

• Energy and raw material efficiency major driver

• Continuous focus resulting in new process technologies

• Key driver abundant global gas resources

• Still unmatured topic, due to thermodynamic challenge

3

• Bio-processing unlikely to substantially match traditional chemical pro-cesses in terms of volume

• Resource efficiency driven • Selected systems in differ.

development stages • Limited commercializ. yet

1

2

5

4

• Boosted by demographics • Broad R&D topic landscape • Different maturity of multiple

applications in food and feed

• Driven by demographics • Multiple existing substances • Crop industry leaders foster

R&D to sustain AI-pipelines

• HC availabilty pattern shift • New gen. of perf. chemicals

beyond classical surfactants about to be commercialized

3

• Boosted by new energy initiative

• Multiple systems, but no proven technology available

• Driven by enhanced energy efficiency in transportation

• New high efficient polymers to be commercialized

1

2

5

4

• Boosted by CE trends and PV thinfilm application

• First conducting polymers commerz.in selected applic.

White bio-technology

Improving bio-processing with GMO

Biomimetric catalysts

Organo-electronics

Leight weighted materials

Active agro ingredients

Chemicals for enhanced oil recovery

Source:

Energy storages

European Advantage (II): Innovation and orchestration of chemical value chains

Products Feedstock

Chemical reactions Energy efficiency

Organic/inorganic feedstock

Energy Energy efficiency

Low carbon intense products

Enabling precursors/products Energy efficiency

Proven technologies

New process technologies

Technologies

3

1

2

5

4

Selected key topics

Key R&D topic

Driver and maturity Germany has a unique value proposition

in cross industry innovation

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 21

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

60 40 20 0% -20 -40

Immunogen Kyowa Hakko

Astellas

Biotest

Pfizer Bayer

Novartis Roche

Sanofi

Novo Nordisk Biogen Idec

60 40 20 0% -20 -40

Evotec Qiagen

Pfizer Morphosys Sanofi

Novartis Stada

AstraZeneca

Biogen Idec Bayer

Merck KGaA Biotest

Novo Nordisk

60 40 20 0% -20 -40

Stada

Evotec

Novartis Qiagen Morphosys Sanofi

Pfizer Merck KGaA

AstraZeneca Bayer Biotest

Biogen Idec

Novo Nordisk

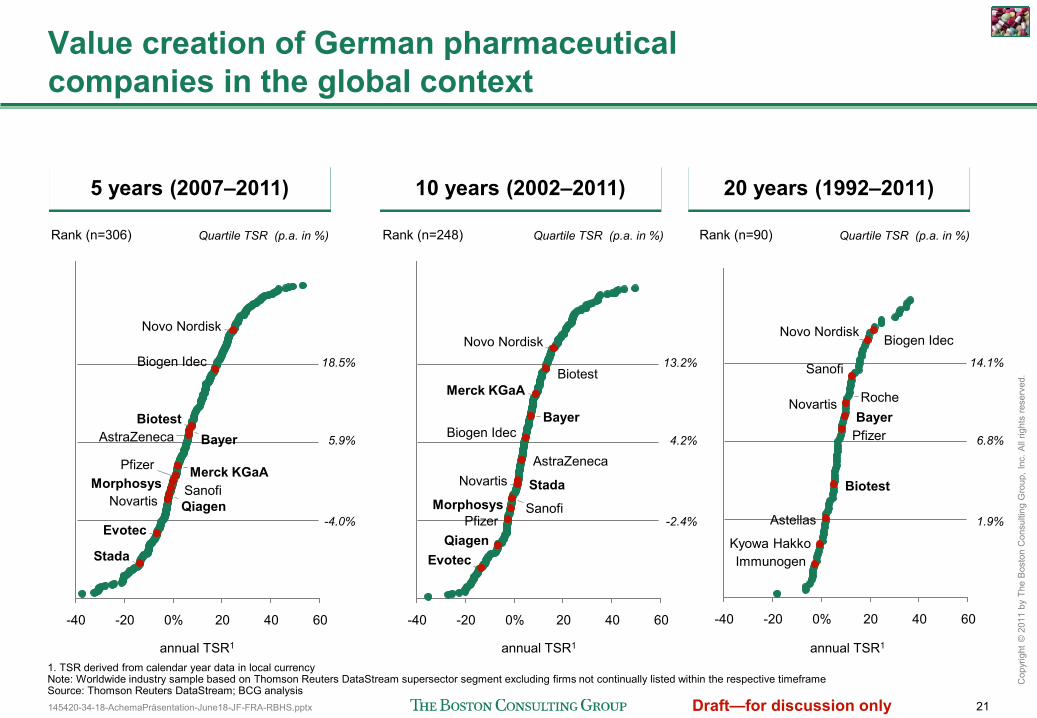

Value creation of German pharmaceutical companies in the global context

annual TSR1

Rank (n=90) Quartile TSR (p.a. in %)

20 years (1992–2011)

Rank (n=306)

annual TSR1

5 years (2006–2010)

Quartile TSR (p.a. in %)

5 years (2007–2011)

annual TSR1

Rank (n=248)

10 years (2002–2011)

Quartile TSR (p.a. in %)

1. TSR derived from calendar year data in local currency Note: Worldwide industry sample based on Thomson Reuters DataStream supersector segment excluding firms not continually listed within the respective timeframe Source: Thomson Reuters DataStream; BCG analysis

18.5%

5.9%

-4.0%

13.2%

4.2%

-2.4%

14.1%

6.8%

1.9%

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 23

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

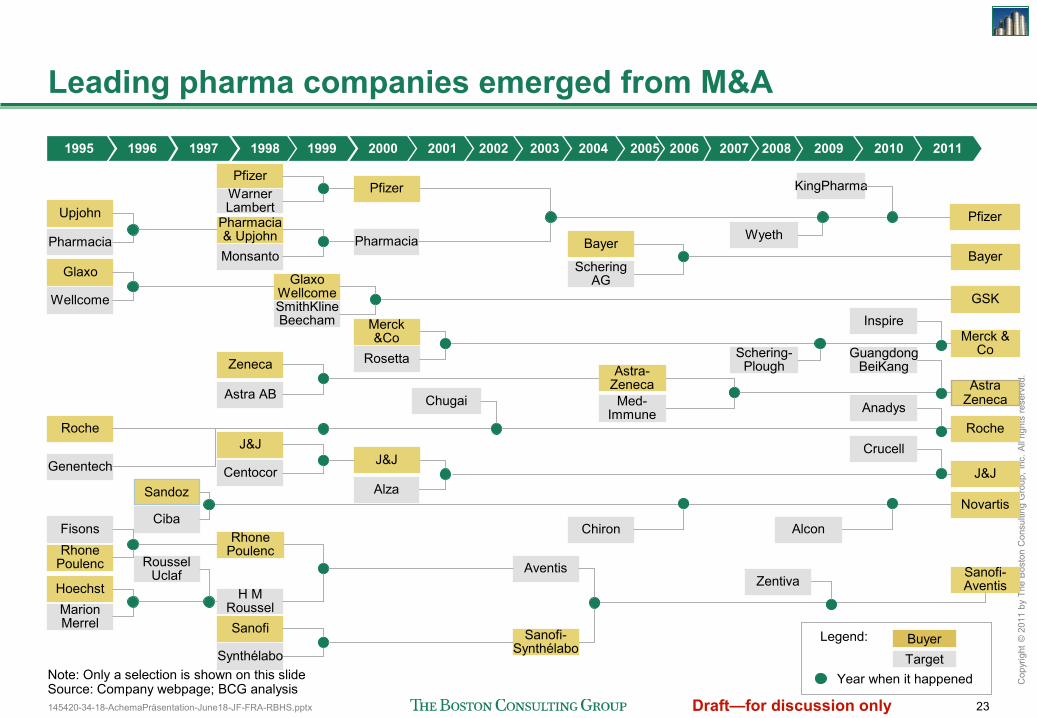

Leading pharma companies emerged from M&A

Note: Only a selection is shown on this slide Source: Company webpage; BCG analysis

Legend:

Target Buyer

Year when it happened

GSK

Merck & Co

Novartis Sandoz

Ciba

Glaxo

Wellcome

Marion Merrel

Hoechst

Roussel Uclaf

Fisons Rhone

Poulenc

Upjohn

Pharmacia

Pfizer

J&J

Sanofi-Aventis

Bayer

Roche Roche

Genentech

Pfizer

J&J

Aventis

Pfizer Warner Lambert

Glaxo Wellcome SmithKline Beecham

Zeneca

Astra AB

J&J

Centocor

Rhone Poulenc

H M Roussel

Merck &Co

Rosetta

Pharmacia Pharmacia & Upjohn Monsanto

Alza

Sanofi

Synthélabo Sanofi-

Synthélabo

Astra-Zeneca Med-

Immune

Bayer

Schering AG

Chugai

Chiron

Astra Zeneca

Wyeth

Schering-Plough

1995 1996 1997 2005 2006 2007 2008 2009 1998 1999 2000 2001 2002 2003 2004 2010 2011

KingPharma

Inspire

Guangdong BeiKang

Anadys

Crucell

Alcon

Zentiva

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 24

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

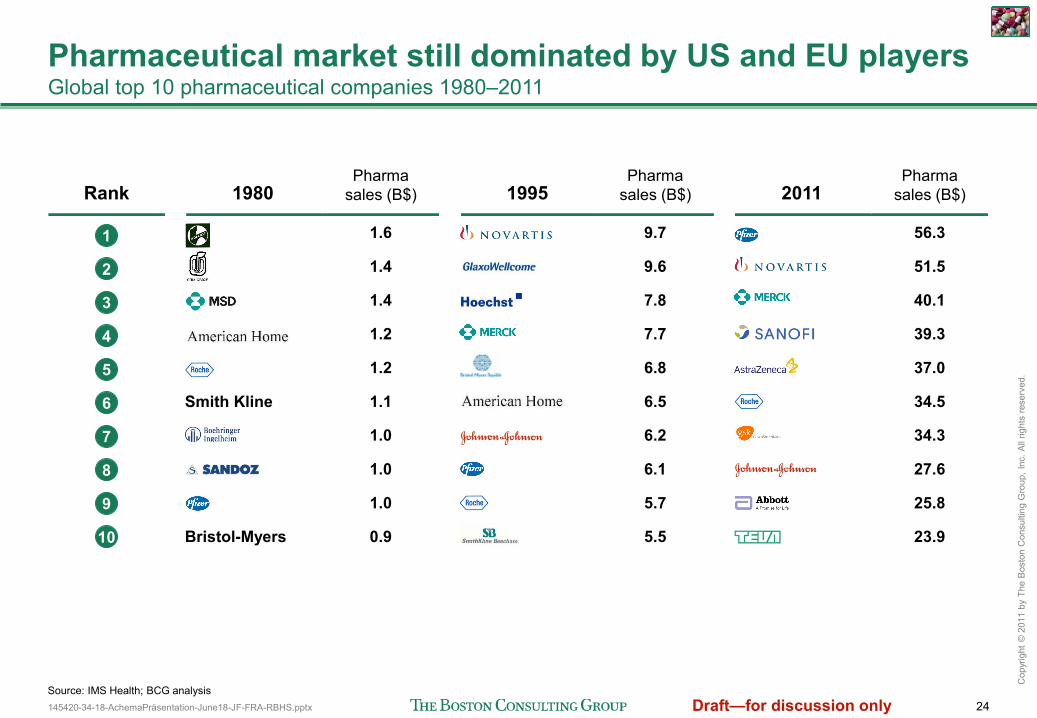

Pharmaceutical market still dominated by US and EU players Global top 10 pharmaceutical companies 1980–2011

Source: IMS Health; BCG analysis

Rank 1980 Pharma

sales (B$) 1995 Pharma

sales (B$) 2011 Pharma

sales (B$)

56.3

51.5

40.1

39.3

37.0

34.5

34.3

27.6

25.8

23.9

1.6

1.4

1.4

1.2

1.2

1.1

1.0

1.0

1.0

0.9

9.7

9.6

7.8

7.7

6.8

6.5

6.2

6.1

5.7

5.5

1

2

3

4

5

6

7

8

9

10

Smith Kline

Bristol-Myers

145420-34-18-AchemaPräsentation-June18-JF-FRA-RBHS.pptx 25

Cop

yrig

ht ©

201

1 by

The

Bos

ton

Con

sulti

ng G

roup

, Inc

. All

right

s re

serv

ed.

Draft—for discussion only

The future of value creation in the German chemical and pharmaceutical industry

Obviously the global context matters • 2-speed global economy, the rise of state owned enterprises in chemicals, self-sustainability

agenda in pharma and in chemicals in many growth regions Company perspective • To grow profitably and to create value European and German based chemical and

pharmaceutical companies will continue to globalize their business models—and invest in "localization" in the growth regions (production, R&D, decision center relocation)

Location perspective • European chemical and pharmaceutical company have proven their ability to create value with

differentiated and diverse business model (management of complexity) • The attractiveness of Europe and Germany as a location for innovation and production is

driven by the "integrated attractiveness" (infrastructure, logistics, resource efficiency) of sites and clusters

• Cross-industry innovation and production cluster are largely a unique German advantage driven by the unmatched density of "Mittelstand-champions"