the financial system, money and prices

TRANSCRIPT

The Financial

System, Money

and Prices

Xi Wang

UMSL, Summer 2015

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

2Learning Objectives

1. Describe the role of financial intermediaries

2. Differentiate between bonds and stocks

Explain how their prices relate to interest rates

3. Explain how the financial system improves the

allocation of savings to productive uses

4. Discuss the three functions of money and how

money is measured

5. Analyze how the lending behavior of commercial

banks affects the money supply

6. Understand the central bank control of the money

supply and its relation to inflation in the long run

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

What is Money? Everyday language: Money means “income” or “wealth”.

In Economics: Money is any asset that can be used in making

purchases

Examples

Currency

Coins

Checking Account Deposits

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

3

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

4

The Financial System

Financial markets are where households invest their current

savings and accumulated past savings (Wealth) by

purchasing financial assets or physical assets.

Financial Asset: is a paper claim (stocks, bonds, loans, etc)

that entitles the buyer to future income from the seller

A loan is a financial asset that is owned by the lender

(typically, banks). It is a bank’s asset and your (borrower)

liability.

Physical Asset: is a claim on a tangible object (house,

machinery, etc) that gives the owner the right to dispose of

the object as he or she wishes (rent it or sell it).

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

5

How Does the Financial System

Allocate Savings?A successful economy typically has a well

functioning financial system that allocates its

savings towards the most productive investments.

Financial Markets provide information to savers

about the most productive (highest rate of return)

investments

Financial Markets help savers to diversify

(investing in several assets with unrelated or

independent risks) so as to share the risks of

individual investment projects while at the same

time funding such risky but worthwhile projects.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

6

Types of Financial Assets - Loans

Loan - is a lending agreement between a particular

lender and a particular borrower. Due to large

information-gathering transaction costs, large

borrowers like the government and large corporations

issue (sell) bonds. Loans are also harder to resell

because they are not as standardized as bonds

Bond – is a legal IOU issued by the borrower. The seller

of the bond (borrower) promises to pay a fixed sum of

interest (called coupon payments) each year and to

repay the principal amount (called face-value) at

maturity. The interest rate on the bond is called its

coupon rate.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

7

Types of Financial Assets - Bonds

The coupon rate that a newly issued bond must

promise so as to be attractive to savers depends

on:

The term of a bond – length of time until maturity.

The longer the term the higher the coupon rate.

Credit Risk – the risk that the borrower will go

bankrupt and hence default. High risk bonds pay

higher coupon rates as in high-yield junk bonds.

Tax Treatment - Municipal bonds are federal tax

free and so offer a lower coupon rate.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

8

Types of Financial Assets - Bonds

Bondholders are free to sell their bonds any time before maturity in the bond market. So you can buy used bonds in the bond market – an organized market for bonds run by professional bond traders.

The market value of a particular bond at any time is called its price. The price of a bond may be equal to, greater than or less than the face-valueof the bond, depending on how the bond coupon rate compares with the prevailing market interest rates.

We will see later that bond prices are inversely related to market interest rates

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

9

Types of Financial Assets: Loan-

Backed SecuritiesLoan-Backed Securities: are assets created by

pooling individual loans and selling shares in

that pool – a process called securitization.

These have become extremely popular over

the past two decades.

Mortgage-Backed securities are a special kind

of the above where individual home

mortgages are pooled and sold as shares to

investors.

Securitization has also been widely applied to

auto, student and credit card loans.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

10

Types of Financial Assets – Loan-

Backed SecuritiesThese Loan-Backed Securities trade on

financial markets like bonds.

They are often preferred by investors because

they provide more diversification and liquidity

as compared to individual loans.(Why? This is a

interesting statement)

However, with so many loans packaged

together, it can often be difficult to assess risks

and evaluate the “true” quality of the

underlying assets – as was painfully obvious

during the financial crisis of 2007-08.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

11

Types of Financial Assets - Stocks

Stock: is a share in the ownership of a company. It

is a financial asset from the owner’s point and a

liability from the company’s point of view.

Stockholders receive regular payments called

dividends (a share of the company’s profits) for

each share of stocks they own.(May not be

constant)

Stockholders also receive returns in the form of

capital gains when price of their stock increases.

Stock prices are determined by the demand and

supply of the stock at stock exchanges.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

12

Types of Financial Assets - Stocks

Why does Microsoft allow you to buy

ownership of their company? Why don’t Bill

gates and Paul Allen (the two founders) sell

bonds for their investment needs and keep

100% ownership with themselves?

Risk aversion – few individuals are risk tolerant

enough to internalize the risks involved in

owning a large company like Microsoft.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

13

Types of Financial Assets - Stocks

While stocks have historically yielded higher

real interest rates (7% for stocks and 2% for

bonds) they are riskier than bonds because, by

law, a company must repay its lenders before

paying out dividends to shareholders. Also, in

the event of default due to bankruptcy the

physical and financial assets after liquidation

goes to bondholders while stock shareholders

typically get nothing.

Loosely speaking – A bond is a promise; a

stock is a hope!

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

14

Types of Financial Assets – Bank

DepositsBank deposit: is a claim on the bank by the

depositor; the bank is obliged to give your

cash back on demand. So bank deposits are

often called demand deposits. It is your

financial asset and a liability for the bank.

On any given day a bank only keeps a

fraction of its deposits as reserves (cash on

hand) in the bank. It loans out the remaining

money to investors.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

15Financial Intermediaries

A Financial Intermediary is an institution that

extends credit to borrowers using funds raised

from savers. Examples – banks, Savings and

Loan, and Credit unions, Mutual Funds, Pension

Funds and Life Insurance Funds.

Banks and other financial intermediaries specialize in

evaluating the quality of borrowers

Principle of Comparative Advantage

They have lower cost of evaluating opportunities than an individual would

They pool the savings of many individuals to make large loans

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

16

Advantages of Banking

Banks gather information, evaluate potential

investments, and direct savings to higher-

return, more productive investments

Service provided to depositors

Banks provide access to credit for small

businesses and homeowners

May be the only source of credit for some investments

When banks make loans, they earn interest

which, in turn, is paid by the bank to its

depositors

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

17Advantages of Banking

Having bank deposits makes payments easier

Checks

ATMs

Debit card

Checks and debit cards are safer than cash(what do I mean by

safe?)

Banks provide a record of your transactions

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Kru

gm

an

an

d W

ells

Ma

cro

eco

nom

ics 2

ed

Slide

18

Banks and the South Korean Miracle

In the 1960s South Korea’s banking system was a mess. Nominal interest rates were low and inflations rates were high. Savers preferred physical assets – real estate and gold. Businesses found it difficult to finance their projects.(Why people choose not to save?Interest rate, yes?)

In 1965 South Korean government reformed the banking system by raising interest rates. National savings rate more than doubled. The rejuvenated banking system financed the great investment boom that followed.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

19

Japanese Banking Crisis of the

1990sJapan’s real estate and stock prices soared

during the boom of the 1980s. Japanese

banks made loans to real estate developers

and they also bought stocks of companies.

When property and stock values fell in the

1990s, Japanese banks fell into severe trouble

Property values decreased and some loans on real estate went into

default

Banks held stocks in companies and the stock values decreased with

recession

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

20

Japanese Banking Crisis of the

1990sIn Japan, banks were the main way saving

was translated into investment

Not so well developed stock and bond markets

Small- and medium-sized businesses suffered from credit shortages

Credit shortages prolonged the recession as businesses struggled to

fund new projects

The recession of the 1990s was fueled by the

virtual breakdown on the banking sector.

The government’s response was too slow.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

21

Bond Prices and Market Interest Rates

Bonds can be sold before their maturity date

Market price of the bond depends on the relationship between the

coupon rate and the interest rate in financial markets

A two-year government bond with principal

$1,000 is sold for $1,000, 1/1/09

Coupon rate is 5%; $50 will be paid 1/1/10; $1,050 will be paid 1/1/11

If you want to sell the bond on 1/1/10, what will

the price be? Depends on the prevailing

market interest rate.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

22

Offer for sale: a government bond with payment of $1,050 due in one year

The competition: Interest rate is 6%; a $1000 invested in a savings account will yield $1,060 in one year

Price of the used bond will be less than $1,000(Savings account amount) (1.06) = $1,050

Used bond price = $991

Bond prices and interest rates are inversely related

Bond Prices and Market Interest Rates

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

23Stock Prices

Price of stock is expected to be $80 in 1 year;

Dividends will be $1 and the current Savings

Market Interest rate is 6%. What is the most you

will be willing to pay for this stock now?

(Price paid now) (1.06) = $81. So Stock price

now = $76.42.

Value would be higher if Dividend were higher

Expected capital gains were higher

Interest rate were lower

Stock prices and r are negatively related.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

24Riskiness and Stock Prices

Most investors dislike risk and require a higher

rate of return on risky assets.

The difference between the required rate of

return to hold risky assets and the rate of return

on safe assets is called Risk Premium

In the previous example suppose a 10% return

is required as risk premium

So Stock price now = $81/1.10 = $73.64

Risk aversion increases the return required of a

risky stock and lowers the selling price

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

25

Rise and Fall of the US Stock Market

Standard & Poor's 500 index rose 60% between

1990 and 1995

More than doubled 1995 – 2000

Lost 40% of its value Jan 2001 – Jan 2003

Returned to Jan 2000 level by Jan 2008

Current Stock Prices depend on the

expectations of buyers of stock about

Future dividends: (+)vely related

Future stock prices (capital gains): (+)vely related

Required Rate of Return = r on safe assets + Risk

Premium: (-)vely related

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

26

Rise and Fall of the US Stock Market

An increase in stock prices could be the result of

Increased optimism about future dividends and/or

capital gains

A fall in the Required Rate of Return

In the 1990s, optimism was high

Strong dividends

Promise of new technologies

Risk premium declined

Increased diversification through mutual funds may have

reduced perceived risk of holding stocks

Investors may have underestimated risk

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

27

Rise and Fall of the US Stock Market

Optimism and risk premium trends reversed

after 2000

Many high-tech firms turned out to be less profitable

than expected

Corporate accounting scandals of 2002 – illegally

inflated profits

The 2000-01 recession

Terrorist attack in US

In 2003 when the economy began to grow

more rapidly, stock prices began to recover.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Money: Three Principal

Uses Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

28

Money is any asset that can be used in making

purchases

Examples include coins and currency, checking

account balances, and traveler's checks

Shares of stock are not money

Money has three principal uses

1. Medium of exchange

2. Unit of account

3. Store of value

Barter is trading goods directly

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Money: Definitions M1 is the sum of currency held outside

banks, traveler’s checks, and balances held

in checking accounts by individuals and

businesses

M2 is M1 plus some additional assets that

are useable in making payments but at

greater cost (including inconvenience) than

currency or checks.

E.g., Savings deposits, small-denomination (< $100,000) time

deposits and Money Market Mutual funds.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

29

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Components of M1 and M2,

Jan 2008 (billions of dollars)T

he

Fin

an

cia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

30

M1

Currency

Demand deposits

Other checkable deposits

Travelers’ checks

M2

M1

Savings deposits

Small-denomination time deposits

Money market mutual funds

1,364.7

758.1

292.5

307.9

6.2

7,498.7

1,364.7

3,903.4

1,224.4

1,006.1

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Are these Money?

Checks, credit cards, debit cards?

These are themselves not money.

The bank deposits that they take the

money from is the actual money.

The cards are just a form of ID, sort of

like your driver’s license.

Similarly, currency inside the bank

(bank reserves) is not money.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

31

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Commercial Banks and the

Creation of Money

Virtual Republic begins with no commercial banking system.

The Government of Virtual Republic, through its Central Bank issues 1 million guilders (currency) Money Supply = 1 m guilders

Lack of security, so people want to place their 1 million guilders in a bank A Commercial Bank is set up

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

32

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Consolidated Balance Sheet of

Virtual Commercial Bank (Initial)T

he

Fin

an

cia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

33

Assets

Currency 1,000,000 guilders

Liabilities

Deposits 1,000,000 guilders

Citizens open accounts and deposit 1 million guilders

• Deposits are liabilities for the bank

• The guilders are an asset for the bank

• Guilders are the bank’s reserves

• Reserves = deposits: 100 percent reserve banking

Reserves are not part of the money supply

Deposits are part of the money supply

For simplicity assume that all guilders are deposited

in the commercial banks.

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Commercial Banks and

the Creation of Money Bank Reserves - Cash or similar assets held by

commercial banks for the purpose of meeting

depositor withdrawals and payments

100% Reserve Banking - Banks hold 100% of

their deposits (liabilities) as reserves

Reserve-Deposit ratio - Reserves/Deposits

Fractional Reserve Banking System - Banks may

also hold a fraction of the deposits as reserves

and loan out the rest to individuals and

businesses; reserve-deposit ratio < 100%

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

34

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Consolidated Balance Sheet of Virtual

Commercial Bank after One Round of LoansT

he

Fin

an

cia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

35

Assets

Currency (= Reserves) 100,000 guilders

Loans to citizens 900,000 guilders

Liabilities

Deposits 1,000,000 guilders

Fractional Reserve Banking System

• Bankers agree they only need a reserve to deposit ratio of

10%

• Required reserves = 100,000 guilders, 10% of deposits

• Loan out the excess reserves of 900,000 guilders

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Consolidated Balance Sheet of Virtual

Commercial Bank After Loans Are Re-depositedT

he

Fin

an

cia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

36

Assets

Currency (=Reserves) 1,000,000 guilders

Loans to citizens 900,000 guilders

Liabilities

Deposits 1,900,000 guilders

People prefer bank deposits to holding cash

• Reserves = 1,000,000 G; Deposits = 1,900,000 G

• Money supply = 1,900,000 G

• Actual Reserve-Deposit ratio = 10/19 = 52.6%

• Required Reserve to deposit ratio = 10%

• Required Reserves = 10% of 1,900,000 = 190,000 G

• Excess Reserves = 1,000,000 - 190,000 = 810,000 G

• Banks can loan the 810,000 guilders

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Consolidated Balance Sheet of Virtual

Commercial Bank After Two Rounds of

Loans and Re-deposits

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

37

Assets

Currency (= reserves) 1,000,000 guilders

Loans to farmers 1,710,000 guilders

Liabilities

Deposits 2,710,000 guilders

Loan proceeds are deposited

• Reserves = 1,000,000 guilders

• Deposits = 2,710,000 guilders

• Money supply = 2,710,000 guilders

• Actual Reserve to deposit ratio = 36.9%

• Excess reserves = 729,000 guilders

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

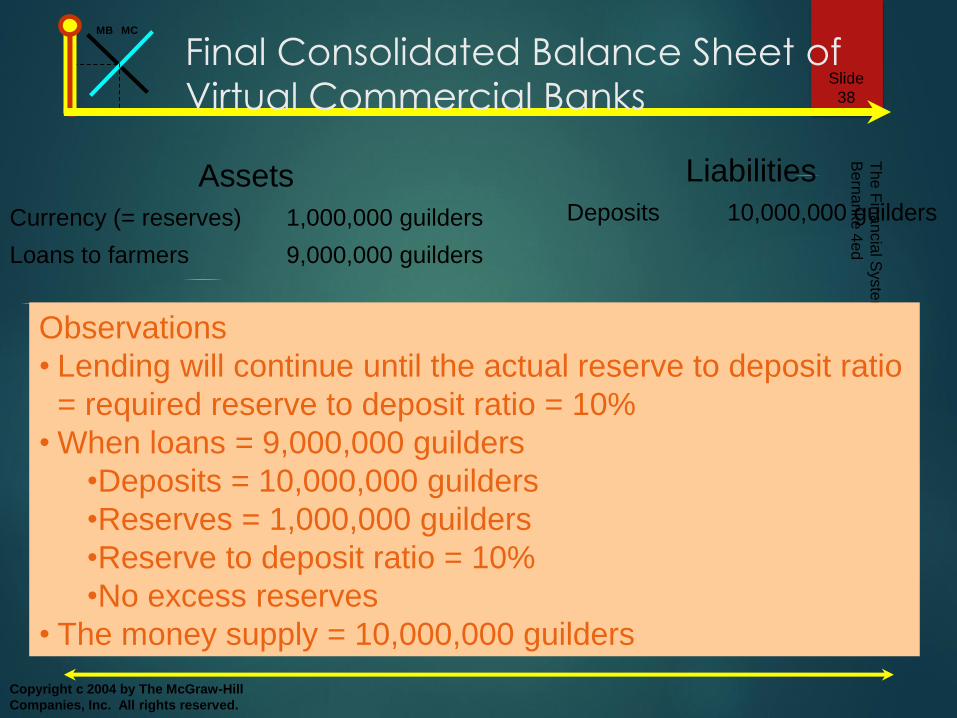

Final Consolidated Balance Sheet of

Virtual Commercial BanksT

he

Fin

an

cia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

38

Assets

Currency (= reserves) 1,000,000 guilders

Loans to farmers 9,000,000 guilders

Liabilities

Deposits 10,000,000 guilders

Observations

• Lending will continue until the actual reserve to deposit ratio

= required reserve to deposit ratio = 10%

• When loans = 9,000,000 guilders

•Deposits = 10,000,000 guilders

•Reserves = 1,000,000 guilders

•Reserve to deposit ratio = 10%

•No excess reserves

• The money supply = 10,000,000 guilders

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Commercial Banks and the Creation

of Money: Observations The use of a fractional-reserve banking system

allows the money supply to grow as a multiple of the reserves. With a 10% reserve-deposit ratio, 1 guilder in reserve can support 10 guilders in deposits.

Bank reserves/bank deposits = desired reserve-deposit ratio

Bank deposits = bank reserves/desired reserve-deposit ratio

If desired reserve-deposit ratio is 5% and bank reserves are $1000, bank deposits will equal $1000/0.05 = $20,000

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

39

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

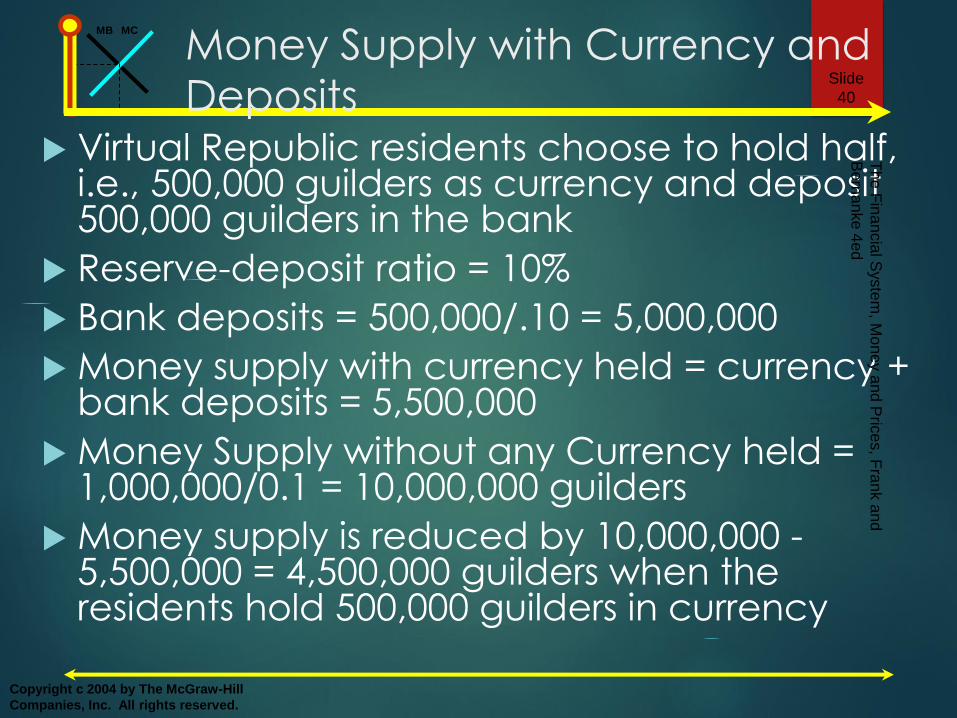

Money Supply with Currency and

Deposits Virtual Republic residents choose to hold half,

i.e., 500,000 guilders as currency and deposit 500,000 guilders in the bank

Reserve-deposit ratio = 10%

Bank deposits = 500,000/.10 = 5,000,000

Money supply with currency held = currency + bank deposits = 5,500,000

Money Supply without any Currency held = 1,000,000/0.1 = 10,000,000 guilders

Money supply is reduced by 10,000,000 -5,500,000 = 4,500,000 guilders when the residents hold 500,000 guilders in currency

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

40

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

41

Does money Supply Rise or Fall at

Christmas

Suppose banks hold $500 billion in reserves and

the public hold $500 billion in cash

Reserve-deposit ratio = 0.20

Money supply = $500 + (500 / 0.20) = $3,000

As Christmas approaches, consumers reduce

bank deposits by $100 billion

Banks have $400 billion in reserves; public holds $600 billion cash

Money supply = $600 + ($400 / 0.20) = $2,600

Reducing bank deposits reduces the money

supply

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

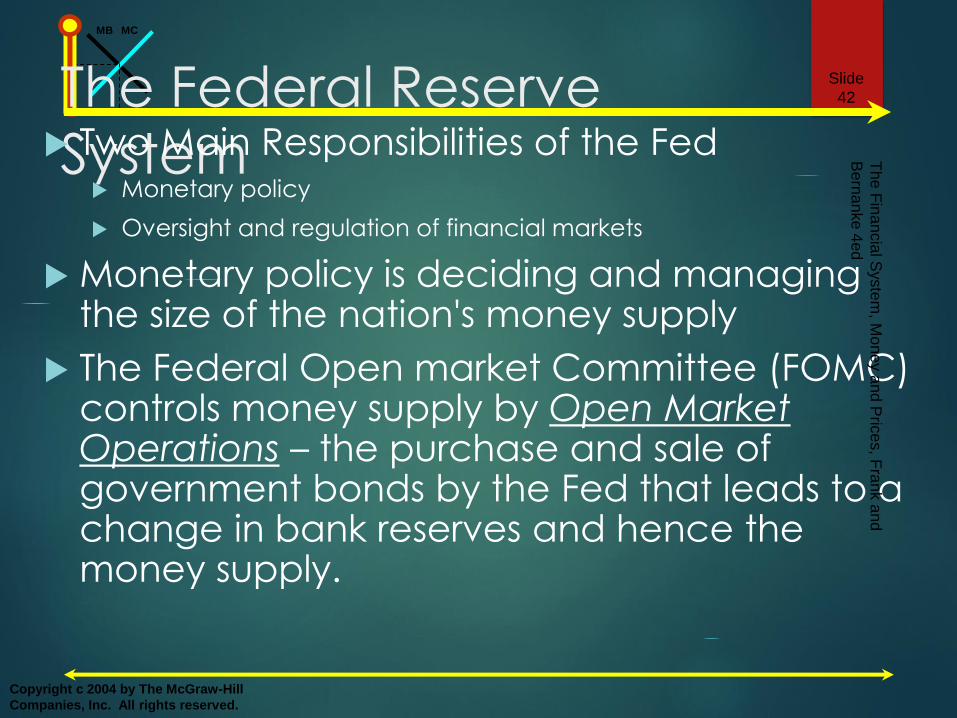

The Federal Reserve

System Two Main Responsibilities of the Fed Monetary policy

Oversight and regulation of financial markets

Monetary policy is deciding and managing the size of the nation's money supply

The Federal Open market Committee (FOMC) controls money supply by Open Market Operations – the purchase and sale of government bonds by the Fed that leads to a change in bank reserves and hence the money supply.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

42

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

The Federal Reserve

System Increasing The Money Supply - Open Market Purchase

The Fed purchases government bonds from the public.

The people deposit the funds they get from their sale of

bonds.

The increase in deposits increase bank reserves.

The money supply increases by a multiple of the increase in

reserves.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

43

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

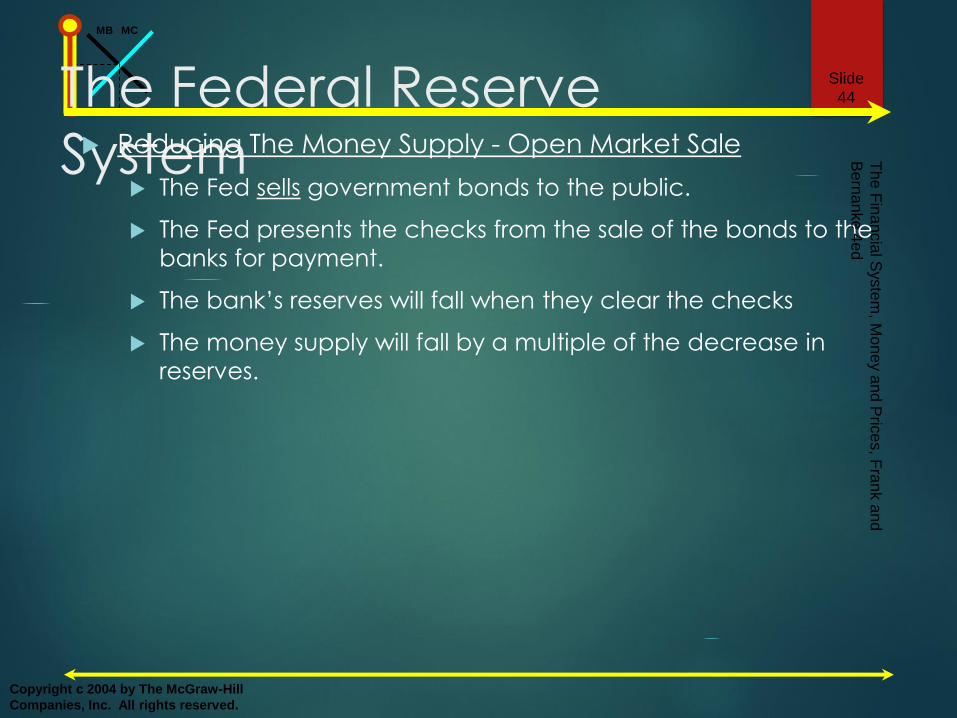

The Federal Reserve

System Reducing The Money Supply - Open Market Sale

The Fed sells government bonds to the public.

The Fed presents the checks from the sale of the bonds to the

banks for payment.

The bank’s reserves will fall when they clear the checks

The money supply will fall by a multiple of the decrease in

reserves.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

44

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

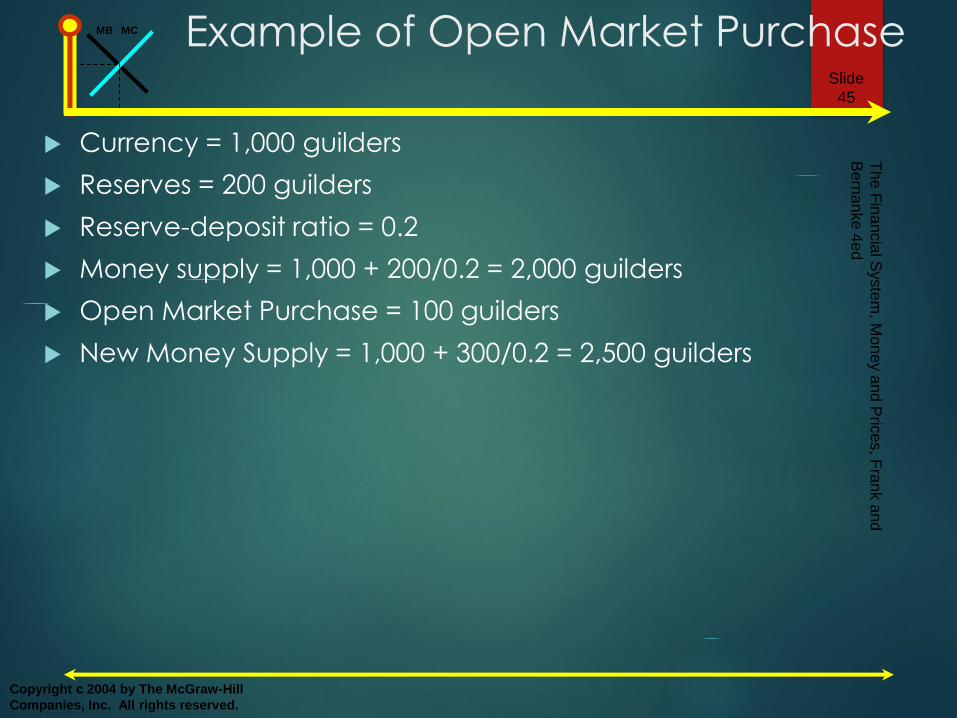

Example of Open Market Purchase

Currency = 1,000 guilders

Reserves = 200 guilders

Reserve-deposit ratio = 0.2

Money supply = 1,000 + 200/0.2 = 2,000 guilders

Open Market Purchase = 100 guilders

New Money Supply = 1,000 + 300/0.2 = 2,500 guilders

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

45

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Money and Prices

Most nations that that have experienced high and sustained

inflation have had unusual increases in their money supply.

In the short run inflation can arise from other sources. But in the

long run inflation is almost always caused by too much money

chasing too few goods.

Indeed, in the long run, money supply is directly proportional to

prices.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

46

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Money and Prices Velocity

The speed at which money circulates – the number of times a

year the typical dollar changes hands.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

47

stockMoney

GDP Nominal

stockMoney

nstransactio of Value Velocity

M

x YP

supply)(money M

GDP) (real x Y level) (price P (V)Velocity

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Money and Prices

Velocity in 2007

M1 = $1,364.2 billion

M2 = $7,447.1 billion

Nominal GDP = $13,843.0 billion

Velocity is determined by a number of factors including technologies such as ATMs and debit cards

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

48

10.15 billion $1,364.2

billion $13,843.0 V M1,

1.86 billion $7,447.1

billion $13,843.0 V M2,

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Money and Inflation in the Long

Run

Recall:

Quantity equation

M x V = P x Y

Assuming V & Y are constant over the

time period

Then P is directly proportional to M.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

49

M

Y x P V

MB MC

Copyright c 2004 by The McGraw-Hill

Companies, Inc. All rights reserved.

Money and Prices

If high rates of money growth lead to inflation, why do countries allow their money supplies to rise quickly?

Huge Govt. Budget deficits

If the govt. cannot tax or borrow from the public, it finances the deficit by printing money.

Th

e F

ina

ncia

l Syste

m, M

on

ey a

nd

Pric

es, F

ran

k a

nd

Be

rna

nke 4

ed

Slide

50

End of Chapter

Summary