the financial impact of data breaches on targeted companies and cyber security companies

TRANSCRIPT

THE FINANCIAL IMPACT OF DATA BREACHES ON TARGETED COMPANIES AND

CYBER SECURITY COMPANIES

A THESIS

Presented to

The Faculty of the Department of Economics and Business

The Colorado College

In Partial Fulfillment of the Requirements for the Degree

Bachelor of Arts

By

William Brokaw

April 2016

THE FINANCIAL IMPACT OF DATA BREACHES ON TARGETED COMPANIES AND

CYBER SECURITY COMPANIES

William Brokaw

April 2016

Economics

Abstract

Using event study methodology, this research examines the financial impact of data

breaches on targeted companies and cyber security companies by measuring their stock

price reactions after the public announcement of a cyber attack. Investigating thirteen

corporate breach events since 2006 and eleven cyber security companies, this study

estimates the cumulative abnormal returns (CAR) over a 3-day window starting the day

before the announcement of a breach. I find that targeted companies and cyber security

companies experience statistically insignificant abnormal returns. The results are

consistent with the theory that investors have difficultly quantifying the financial impact

of breaches on targeted companies. Additionally, the results indicate that cyber security

companies experience more substantial stock price reactions than targeted companies.

KEYWORDS: (Event Study, Data Breaches, Cumulative Abnormal Return, Cyber

Security)

JEL CODES: (G10, G14)

ON MY HONOR, I HAVE NEITHER GIVEN NOR RECEIVED

UNAUTHORIZED AID ON THIS THESIS

Signature

William Brokaw

Acknowledgements

I would like to thank my thesis advisor, Professor Neal Rappaport, for patiently helping

me throughout this process. Without your guidance and insight, this thesis would not

have been completed. Your dedication, humor and knowledge made this process

enjoyable. Most importantly, I want to thank you for fostering my love for economics.

You are a true inspiration.

Additionally, I want to thank my parents, Bags and Kerry, and my siblings, Winslow,

Roz, and Shea, for their unconditional love and support. You guys are the best.

TABLE OF CONTENTS

ABSTRACT

ACKNOWLEDGEMENTS

1 INTRODUCTION 1

2 LITERATURE REVIEW 2

. Breached Company Event Studies Without Significant Results………..

. Breached Company Event Studies With Significant Results……………..

. Cyber Security and IT Consulting Firm Studies……………………………….

. Hypothesis Testing………………………………………………………………………..

3 DATA AND RESEARCH METHODOLOGY 8

4 MODEL 11

4. Breached Company Model……………………………………………………………..

4. Cyber Security Company Model……………………………………………………..

5 RESULTS 15

. Breached Company Results…………………………………………………………...

. Cyber Security Company Results……………………………………………………

6 CONCLUSION 21

Introduction

Using event study methodology, this research examines the financial impact of

data breaches by measuring the stock market reaction on targeted companies and the

cyber security sector, respectively, after the public announcement of an attack. As the

frequency of attacks has progressively increased in the last decade, information security

incidents have become an expected cost of doing business. According to former FBI

director, Robert Mueller, “there are two types of companies: those that have been hacked,

and those that will be.”

While a targeted company’s public announcement could potentially have a

negative impact on shareholder value, the spillover effect on cyber security companies is

more ambiguous. Generally, data leaks call for an increase in cyber security; however, it

is uncertain if the escalation in demand for security outweighs the negative investor

sentiment on the defending cyber security firms when they fail to do their job: protect

clients’ confidential information. In this study, I will examine this paradox through the

implications of the price reaction on public cyber security companies after the event of a

data breach.

Using standard OLS regression analysis, this research estimates the cumulative

abnormal returns (CAR) that both publicly traded targeted companies and publicly traded

cyber security companies experience from the announcement of a data breach. First,

focusing on thirteen firms, this study finds that on average targeted companies experience

daily mean abnormal returns of .2% during the 3-day window starting the day before the

2

public announcement of an attack. However, this negative stock market reaction is

statistically insignificant at the .05 level (p value=.94). Further, during the 3-day window

starting the day before a targeted company announces an attack, on average cyber

security companies experience positive daily abnormal returns of 1.38%. Nevertheless,

again these results are statistically insignificant at the .01 level (p- value=.756). Given

these findings, both targeted companies and cyber security companies experience

statistically insignificant abnormal returns; however, the impact of cyber security

companies is greater than targeted companies.

The remainder of this paper proceeds as follows. In the next section I review the

relevant literature and develop my hypotheses. The third part of this paper explains my

data collection and research methodology. I outline my economic model in the fourth

section. The fifth section reports the results. Finally, I discuss implications of the results

and draw conclusions in the sixth section.

Literature Review

Using event methodology, previous literature evaluates the financial impact on

targeted companies by measuring the cumulative abnormal stock returns after the public

announcement of the incident. Given the extensive amount of research, studies have

found contradictory results when measuring the CAR of victimized firms. In this section,

I first explore the studies that find no significant negative CAR of companies that

experience an attack followed by studies that find a significant negative CAR. Finally, I

3

examine previous research measuring the CAR of public cyber security companies after

the announcement of a data breach.

Breached Company Event Studies Without Significant Results

Campbell, Lawrence, Gordon, Loeb, and Zhou (2003) find no significant negative

stock market reaction from the exposure of company information. However, the authors

propose that the type of attack impacts the returns. While leaks that did not disclose

confidential information had no significant negative impact, breaches involving

unauthorized access to confidential data resulted in significant negative abnormal returns

for the affected company. This research postulates that investors are sensitive to the

nature of the attack and the underlying assets exposed.

Similarly, Kannan, Rees and Sridhar (2007) perform an event study measuring the

CAR of targeted companies and determine that confounding external events carried a

significant impact on the magnitude of CAR. The authors computed cumulative abnormal

returns of targeted firms in relation to a control group of firms and the S&P 500 over 3-

day, 8-day and 30-day windows. They measured the impact of the window length on

different characteristics, including the type of targeted firm, the time period of the event,

and the type of attack.

While at first the overall negative CAR is found statistically significant, the

authors realize that these results were influenced by various circumstantial characteristics

and external factors. Specifically, the authors find that the September 11, 2001 terrorist

attacks significantly impacted stock market reactions; therefore, they designated the

corresponding data leaks as confounded events. Excluding these confounding events,

4

circumstantial characteristics, including the type of attack, type of firm and duration of

event window, proved to have insignificant impacts on CAR respectively.

Breached Company Event Studies With Significant Results

Gatzlaff and McCullough (2010) examine the stock market assessment of the cost

of data hacks at publicly traded companies in which personal information such as

customer or employee data are exposed. Studying 77 incidents between 2004 and 2006,

the authors find the overall effect on shareholder wealth to be negative and statistically

significant.

Taking into account factors that could potentially influence stock market returns,

the authors identify both firm and breach characteristics that could impact the magnitude

and direction of the stock market response. The firm characteristics include: the type of

firm, the firm’s response (did the firm announce the incident before the press?), the firm

size, the frequency of attacks on a particular firm, the firm’s subsidiary status, and finally

the firm’s growth opportunities signified by the market-to-book ratio. Second, the authors

identify hack characteristics that could potentially impact CAR. The characteristics

include: size and type of attack, interaction terms (prior expectations of data security),

and the time period (Gatzlaff & McCullough, 2010).

Overall, Gatzlaff and McCullough (2010) find that shareholders of targeted

companies experience significant negative CAR. Examining the significantly influential

firm characteristics, the authors find that firms that conceal breach information, are

smaller in size, do not have subsidiary status, and have higher growth opportunities

(market to book ratio) experience greater negative CAR, respectively. Further, the

5

authors find that the negative reaction is stronger for hacks of customer and employee

data. They find that the negative cumulative abnormal returns are greater for breaches

occurring in more recent time periods, largely because of increased costs associated with

new legislation. Surprisingly, the other characteristics, including size of breach and

interaction terms are statistically insignificant respectively.

Further, Cardenas, Coronado, Donald, and Parra (2012) examine the CAR, risk

shifts, and volume changes to measure the impact of security infringements on the market

value of a victimized company. Examining the risk shifts, the authors measure the beta

(volatility or risk of a security in relation to the market as a whole) of the companies’

stock after a cyber attack. The authors find that targeted companies experience a negative

CAR that is not statistically significant. However, their analysis shows that a firm’s stock

beta significantly increases, indicating increased risk and stock volatility. Finally, they

observe that the targeted firms experience a significant abnormal trading volume of about

5% during the event window after a breach.

Cyber Security and IT Consulting Firm Studies

While numerous studies examine the abnormal stock returns of targeted

companies, there are few studies exploring the stock price reaction on the defending

cyber security and IT consulting firms. The final segment of this section reviews two

studies investigating the abnormal returns that cyber security providers experience after a

cyber attack.

Chen, Li, Yen and Bata (2011) evaluate the impact of information security

infringements on the stock price of IT consulting firms that “supplied the know-how and

6

infrastructure to create, implement, and maintain those information systems that were

hacked” (Chen et al., 2011). According to their findings, investors, clients and customers

may look beyond the faults of the victimized firms and put the blame on the IT providers

or cyber security firms. The authors investigate 83 incidents affecting a variety of firms

in the US in 2006 and 2007. They find that the market value of IT consulting firms is

positively associated with the disclosure of IT security breaches. According to their

results, IT firms have an average positive 4.01% abnormal return during the 2-day period

following the announcement. However, after examining the event study methodology and

the OLS regression analysis, they find that IT consulting firms experience less positive

CAR as the number of exposed records increases. Therefore, the larger the data attack,

the greater the adverse impact the IT consulting firm experiences. Finally, their findings

suggest that the impacts on IT consulting firms are stronger when certain market sectors

are targeted, namely technology and retail (Chen et al., 2011).

Similarly, Garg, Curtis and Halper (2003) examine the impact of 49 data breaches

between 1996 and 2002 on internet security stock returns. Using event study

methodology, the authors find that overall cyber security companies experience positive

CAR with increases between .9% and 3.3%. However, in analyzing the results, the

authors determine that the denial of service (internet portal inaccessible to users) attacks

in February 2000 were a turning point for investors. Before February 2000 the positive

market reaction of internet security stocks is amplified with average positive returns of

3.8% on the announcement day, increasing to 10.3% over three days (Garg et al., 2003).

However, following the event, cyber security companies experience insignificant positive

returns or even slightly negative returns. According to their research, after the dramatic

7

event, investors expected an increase in cyber attacks and demand for internet security,

leading to higher valuations on cyber security, which in turn led to less significant CAR.

Hypothesis Testing

Following standard research methodology, the null and alternatives hypotheses

for targeted companies are stated below.

H10: Targeted companies experience no abnormal returns from the public announcement

of a data leak.

H11: Targeted companies experience abnormal returns from the public announcement of

a data leak.

While previous literature finds positive stock price reactions for cyber security or

IT consulting companies after public announcements, it is apparent that these results are

contingent on the underlying relationship that a defending company has with the

victimized firm. More specifically, the impact of an attack on cyber security stocks

depends on the market perception of a targeted companies’ level of investment in security

services. If investors believe that a firm invested sufficiently in cyber security before the

incident, one could assume that the cyber security provider would experience a muted or

even negative stock price response. Conversely, if investors believe that a targeted

company invested insufficiently in cyber security, it is possible that a hack could have a

positive impact on cyber security firms as they would experience an increase in business.

This study examines this dichotomy by testing the null and alternative hypotheses below.

8

H20: Cyber security companies experience no abnormal returns after a targeted company

publicly announces a breach event.

H21: Cyber security companies experience abnormal returns after a targeted company

publicly announces a breach event.

Data and Research Methodology

First, in categorizing data attacks, I used a compilation of definitions used by

Chen et al. (2011). The authors state:

Data breaches involve unauthorized access to information leading to the break-ins into

systems and networks and to accidental or unlawful destruction, loss, and alteration of

personal data. For example, a breach that exposes the social security number, credit

card number or personal information of individuals is considered a data breach (Chen

et al., 2011).

Using this information, I researched all cyber attacks since 2006 from the website

Informationisbeautiful.net. After excluding all breaches of government agencies,

universities, and private companies, I compiled a list of public companies that were

categorized as “hacked” since 2006. Hacks are defined as breaches that involve external

parties breaking into the targeted companies’ system. This excludes all exposures

involving data that was lost, accidentally published or stolen from an internal member of

the breached organization.. Narrowing down this sample, my data set is comprised of

companies that experienced a data attack on more than 1,000,000 accounts, and

9

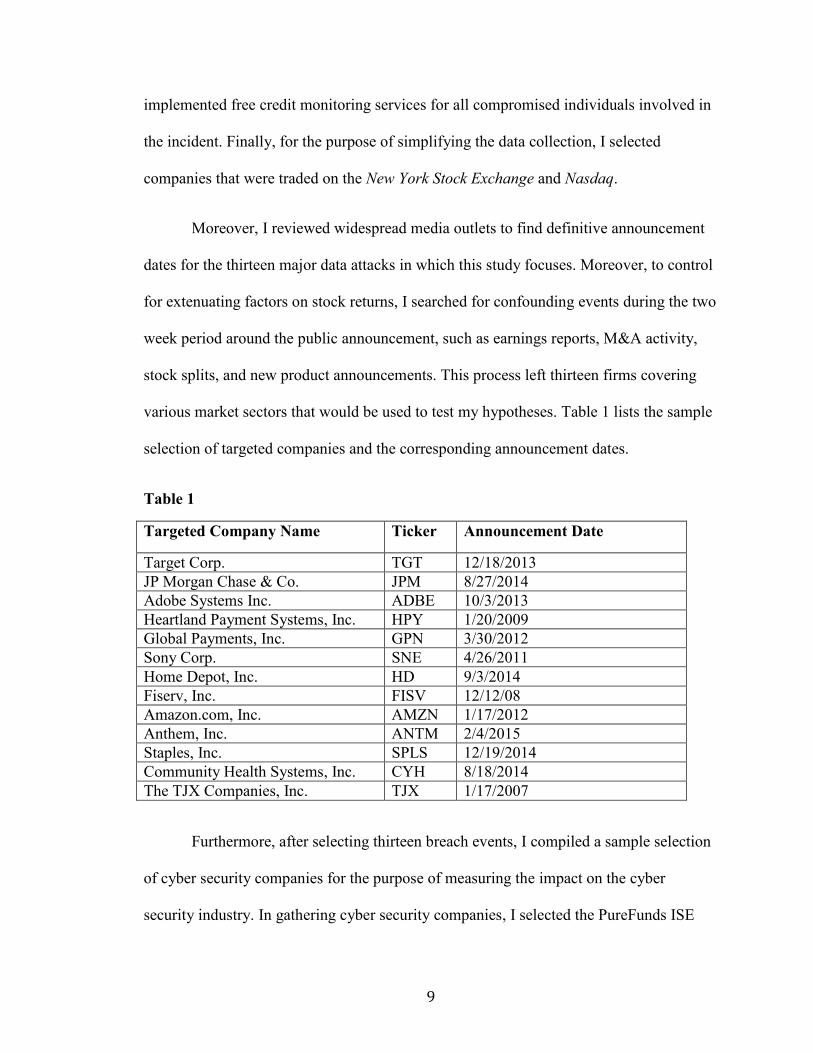

implemented free credit monitoring services for all compromised individuals involved in

the incident. Finally, for the purpose of simplifying the data collection, I selected

companies that were traded on the New York Stock Exchange and Nasdaq.

Moreover, I reviewed widespread media outlets to find definitive announcement

dates for the thirteen major data attacks in which this study focuses. Moreover, to control

for extenuating factors on stock returns, I searched for confounding events during the two

week period around the public announcement, such as earnings reports, M&A activity,

stock splits, and new product announcements. This process left thirteen firms covering

various market sectors that would be used to test my hypotheses. Table 1 lists the sample

selection of targeted companies and the corresponding announcement dates.

Table 1

Targeted Company Name Ticker Announcement Date

Target Corp. TGT 12/18/2013

JP Morgan Chase & Co. JPM 8/27/2014

Adobe Systems Inc. ADBE 10/3/2013

Heartland Payment Systems, Inc. HPY 1/20/2009

Global Payments, Inc. GPN 3/30/2012

Sony Corp. SNE 4/26/2011

Home Depot, Inc. HD 9/3/2014

Fiserv, Inc. FISV 12/12/08

Amazon.com, Inc. AMZN 1/17/2012

Anthem, Inc. ANTM 2/4/2015

Staples, Inc. SPLS 12/19/2014

Community Health Systems, Inc. CYH 8/18/2014

The TJX Companies, Inc. TJX 1/17/2007

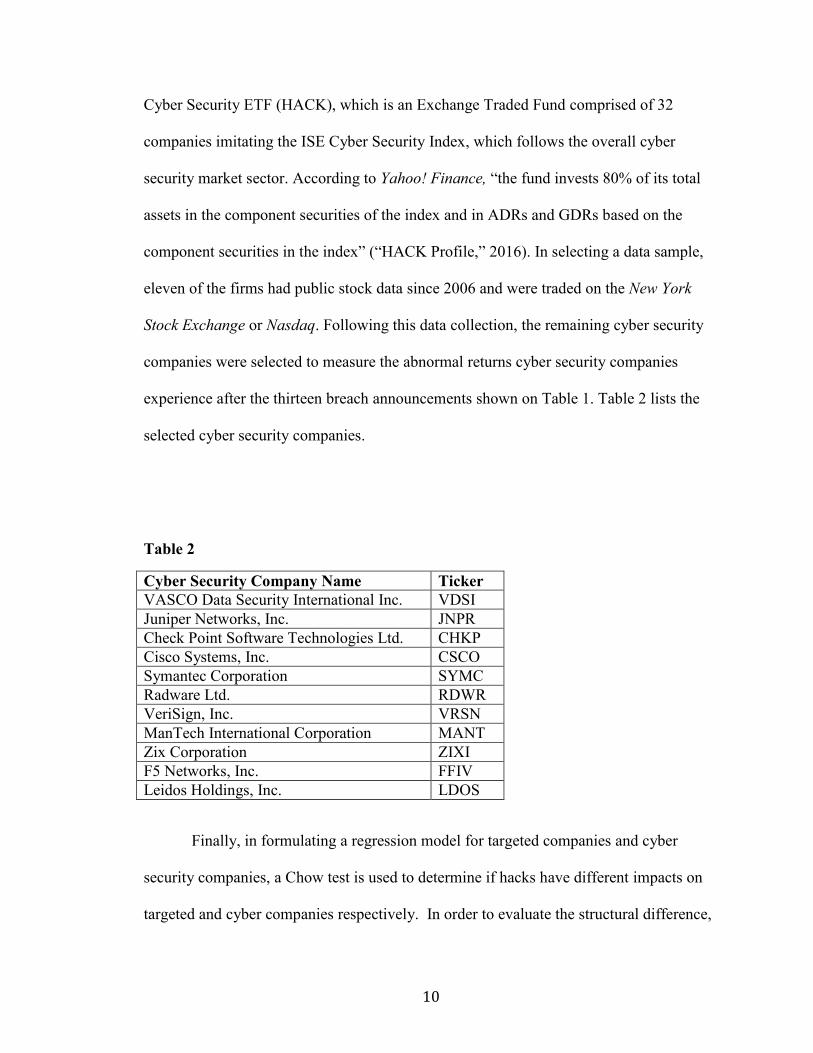

Furthermore, after selecting thirteen breach events, I compiled a sample selection

of cyber security companies for the purpose of measuring the impact on the cyber

security industry. In gathering cyber security companies, I selected the PureFunds ISE

10

Cyber Security ETF (HACK), which is an Exchange Traded Fund comprised of 32

companies imitating the ISE Cyber Security Index, which follows the overall cyber

security market sector. According to Yahoo! Finance, “the fund invests 80% of its total

assets in the component securities of the index and in ADRs and GDRs based on the

component securities in the index” (“HACK Profile,” 2016). In selecting a data sample,

eleven of the firms had public stock data since 2006 and were traded on the New York

Stock Exchange or Nasdaq. Following this data collection, the remaining cyber security

companies were selected to measure the abnormal returns cyber security companies

experience after the thirteen breach announcements shown on Table 1. Table 2 lists the

selected cyber security companies.

Table 2

Cyber Security Company Name Ticker

VASCO Data Security International Inc. VDSI

Juniper Networks, Inc. JNPR

Check Point Software Technologies Ltd. CHKP

Cisco Systems, Inc. CSCO

Symantec Corporation SYMC

Radware Ltd. RDWR

VeriSign, Inc. VRSN

ManTech International Corporation MANT

Zix Corporation ZIXI

F5 Networks, Inc. FFIV

Leidos Holdings, Inc. LDOS

Finally, in formulating a regression model for targeted companies and cyber

security companies, a Chow test is used to determine if hacks have different impacts on

targeted and cyber companies respectively. In order to evaluate the structural difference,

11

I measured the combined regression statistics of the targeted companies’ and cyber

security companies’ abnormal returns. The result for the F statistic was 812.42 compared

to the critical F value of 9.0. Given these results, I reject the Chow test’s null hypothesis

that the F statistic and the critical F value are equal. This indicates that there is a

structural difference between the stock market reactions of targeted companies and cyber

security companies. Consequently, this study uses respective economic models to

evaluate the cumulative abnormal returns of breached and cyber companies.

Model

For the purpose of this study, event study methodology is defined as “the

semistrong version of the efficient markets hypothesis, which maintains that as new

publicly available information is received, it is immediately absorbed by investors and

incorporated into share prices” (Garg et al., 2003). Following this methodology, the

announcement would cause the market to immediately revaluate the affected company

causing a potential fluctuation in share prices.

Breached Company Model

Using event study methodology, the evaluation of CAR is based on the Capital

Asset Pricing Model (CAPM) and the estimation of expected returns is based on the OLS

regression. In this equation, the independent variable is the market index for time (t), and

the dependent variable is the return of firm (i) at time (t) as shown in Equation 1.

Rit =i + i Rmt + it (1)

12

where,

Ri,t= the daily return for firm i in period t;

Rm,t=the daily return for a value-weighted market portfolio of stocks on day t (S&P 500);

i=market model intercept and slope parameter, respectively, for firm i;

i,t=error or disturbance term.

Following previous events studies, my estimation window consists of 120 trading

days prior to the announcement date (t=0), and 20 trading days after the announcement (-

121, 20). This estimation window provides the expected returns for a particular firm in

relation to the S&P 500. In order to measure the abnormal returns, I use a window of 3

days starting one day before the announcement (t=-1, t=0, t=1).

The abnormal return (AR) is computed measuring the disparity between the

firm’s actual stock returns and overall market returns. For the purpose of this study, I

used the S&P 500 index as my market benchmark. The computation of average daily

abnormal returns (AR) is shown in Equation 2.

ARit=Rit – (̑i + ̂̑1 Rmt) (2)

Often times the markets do not fully adjust to new information or announcements

take a couple days to become widespread media. Consequentially, it is necessary to

measure the cumulative abnormal returns of a couple days after the announcement of a

breach. This research measures the cumulative abnormal returns (CAR) during a 3-day

13

event window (t=-1,t=0,t=1) beginning a day before the announcement. The computation

of CAR is shown in Equation 3.

CARi = ∑�=+1�=−1 ARit (3)

Furthermore, using cross-sectional regression analysis, I estimate the regression model in

Equation 4.

ARi = I + 1Rmt + 2Di + it (4)

where,

AR is the mean abnormal return for each day;

Di is an indicator variable for the breach event, where Di =1 during t=-1, t=0, t=1, and

Di=0 otherwise.

Cyber Security Company Model

In determining if cyber security companies experience abnormal returns after the

public announcement of an attack, I use the same economic model as specified above. In

this equation, the independent variable is the market index for time (t), and the dependent

variable is the return of cyber security firm (i) at time (t) as shown in Equation 5.

Rit =i + 1 Rmt + it (5)

where,

Ri,t= the daily return for cyber security firm i in period t;

Rm,t=the daily return for a value-weighted market portfolio of stocks on day t (S&P 500);

14

i=market model intercept and slope parameter, respectively, for cyber security firm i;

i,t=error or disturbance term.

Furthermore, the abnormal returns (AR) and cumulative abnormal returns (CAR) are

expressed in the following equations.

ARit=Rit – (̑i + ̂̑1 Rmt) (6)

CARi = ∑�=+1�=−1 ARit (7)

In order to test the hypotheses, this research uses standard OLS regression analysis to

determine the cross-sectional variance of the samples.

ARi = I + 1Rmt + 2Di + i (8)

where,

AR is the mean daily abnormal return for each day

Di is an indicator variable for the breach event window, where Di =1 during t=-1, t=0,

t=1, and Di =0 otherwise.

15

Results

Breached Company Results

Table 3

Regression of all targeted firms

Percent Daily Return

Percent Daily Market

Return

1.214***

(.0707)

Breach Event .1983

(2.8208)

Constant 1.030***

(.3478)

Number of

Observations

1,833

R Squared

F Stat (2,1830)

F Stat P-value

.441

147.4

0.0000

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

As shown on Table 3, companies experience statistically insignificant abnormal

returns after the announcement of a successful leak. According to the results, the average

daily abnormal return for a targeted firm is roughly .2% during the 3-day window starting

the day before the announcement, and is statistically insignificant at the .05 level (p

value=.94). The coefficient of the indicator variable “Breach Event” specifies the

average daily abnormal return for targeted companies during t=-1, t=0, t=1. In other

words, this value determines the elasticity of the average targeted firm’s returns in

relation the cyber attack. Given these results, I fail to reject the null hypothesis (H10) that

targeted companies experience no significant abnormal returns after their announcement

of a cyber attack. Moreover, in calculating the CAR for all breached companies, the sum

16

of the mean daily abnormal returns is taken for the 3-day window producing a cumulative

abnormal return of .6%. These insignificant results postulate that investors have difficulty

evaluating the financial impact of cyber crime on targeted companies. Because this study

focuses on the initial announcements of potential hacks, the stock price reaction could be

muted from lack of information about the attack characteristics and underlying assets

affected by the incident. These results are consistent with the arguments that data attacks

have insignificant impacts on affected companies.

17

Table 4

Regression of all breached companies using indicator

variables for each company

Percent Daily Return

Percent Daily Market Return 1.2276***

(.0698)

Breach Event .31085

(2.850)

Company Indicator Variables

AMZN .1778

(1.8113)

ANTM .1952

(1.2099)

CYH 1.4122

(1.7190)

FISV -.5255

(1.3272)

GPN -.2674

(1.2092)

HD -.0802

(1.1601)

HPY 7.7411*

(3.284)

JPM -.3388

(1.1255)

SNE .2692

(1.8292)

SPLS 2.4200

(2.1129)

TGT -.3538

(1.4784)

TJX

Constant

-.3713

(1.1342)

.3477

(1.0486)

Number of Observations 1,833

R Squared

F Stat (14,1830)

F Stat P-value

.4309

29.32

0.0000

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Furthermore, the results in Table 4 are computed using indicator variables to

distinguish the impacts of data attacks on the individual companies breached in

18

comparison to the omitted company: Adobe Systems Incorporated. In relation to Adobe

Systems Incorporated, half of the companies have negative shareholder reactions. These

results indicate that targeted companies have experience mixed stock price reactions from

initial announcements. In other words, data breaches generate no definitive stock return

outcome for affected companies.

Cyber Security Company Results

Table 5

Regression of all cyber security companies

Percent Daily Return

Percent Daily Market

Return

.5045***

(.0339)

Breach Event 1.3772

(4.439)

Constant 7.2227***

(1.5806)

Number of

Observations

18,626

R Squared

F Stat (2,18623)

F Stat P-value

.0108

116.17

.0000

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

As shown in Table 5, cyber security companies experience positive daily

abnormal returns after a targeted company publicly announces a data breach. During a 3-

day window period specified as “Breach Event,” average daily abnormal returns are

1.38%, but are statistically insignificant at the .05 level (p- value=.756). Consequentially,

I fail to reject the null hypothesis (H20) that cyber security companies experience no

19

abnormal returns after a targeted company announces a successful data attack. Moreover,

in order to measure the cumulative impact over the 3-day breach event window, I

multiply the average daily abnormal return by 3, which produces a cumulative abnormal

return of 4.14%. While these results are consistent with previous studies’ findings that

data breaches positively impact the stock returns of internet security firms, this study

does not find statistical significance.

Additionally, the R squared value determines how well the economic model fits

the actual data. In other words, R squared measures the degree to which the model

explains the observed outcomes. Given the low R squared value (.0108), I determine that

the model explains only a small percentage of the overall daily returns of the cyber

security industry. While R squared does not reflect the extent to which any particular

independent variable explains the variance of the dependent variable (daily returns of the

cyber security industry), it measures the overall association of the model and the

observed outcomes. Due to countless factors and market “noise” affecting daily stock

returns, it is not surprising that this model explains a small percentage of the daily returns

of the cyber security industry.

20

Table 6

Regression of all cyber security companies using indicator

variables for each company

Percent Average Daily Return

Percent Daily Market Return .5051***

(.0335)

Breach Event 1.6216

(4.3748)

Company Indicator Variables

CSCO -20.9421***

(5.6150)

FFIV 19.5118

(12.2294)

JNPR -19.4895***

(5.7355)

LDOS -2.1564

(6.0148)

MANT -15.9898**

(6.5400)

RDWR -1.2596

(5.5851)

SYMC -21.3389***

(5.4056)

VDSI -16.1599***

(5.3971)

VRSN -9.9807

(6.2718)

ZIXI

Constant

-6.5673

(5.3864)

15.8410

(4.9994)

Number of Observations 18,626

R Squared

F Stat (12,18613)

F Stat P-value

0.0146

36.08

0.0000

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Using indicator variables, Table 6 identifies the average impact of all thirteen

breaches on each cyber security company in relation to the omitted company: Check

21

Point Software Technologies Ltd. In comparison to the returns of Check Point Software

Technologies, all of the cyber companies except F5 Networks (FFIV) have negative stock

returns as specified by the indicator variable coefficients. Theorizing F5 Network’s

results, positive stock returns could be a consequence of an increase in demand of its

services. F5 Networks may see an increase in clients as victimized companies and

vulnerable companies with suboptimal security look to increase their security

mechanisms.

Conclusion

By measuring the disparity of stock market returns after the announcement of

cyber attacks, this study enhances the literature examining the financial impact of data

hacks on targeted and cyber security companies. Although previous literature examines

the CAR of companies after a cyber attack, this study contributes to previous findings

because it examines many recent attacks that haven’t been analyzed in this context.

Moreover, while there are various studies investigating the financial impact on targeted

companies and cyber security companies respectively, previous literature does not use

event study methodology to analyze the combined impact of cyber crime events on both

the targeted company and defending cyber security companies.

Similar to Campbell et al. (2003) and Kannan et al. (2007), this study finds that

cyber attacks have insignificant stock price impacts on targeted companies. More

specifically, the study finds that initial breach announcements have no adverse affects on

targeted companies. Speculating on these results, there are many theories that could

22

explain this lack of investor reaction. First, given the commonality of corporate cyber

crime, breaches could be an expected cost of doing business in today’s digital world. As

the frequency of attacks increases, investors could be numb to announcements declaring

investigations into stolen confidential information.

Additionally, because this study focuses on initial public announcements,

shareholders may not have enough information to accurately evaluate the financial

impact. When companies initially announce potential attacks, the notifications are

generally very ambiguous stating investigations into potential hacks or withholding

information on the underlying assets impacted by the breach. Moreover, even when

companies disclose information about the lost assets and/or amount of records stolen, the

financial impact is still very difficult to quantify. While loss of sensitive data, intellectual

property and customer trust can adversely impact companies in the long-run, investors

cannot determine the full financial implications of information security incidents after the

initial reports. According to a Harvard Business Review, “shareholders still don’t have

good metrics, tools, and approaches to measure the impact of cyber attacks on businesses

and translate that into a dollar value” (Kvochko and Pant, 2015). Given the frequency of

attacks, uncertainty after initial announcements, and lack of ability to quantify the

financial impact, shareholders could be hesitant to immediately sell stock when a

company experiences an information security leak.

While previous studies examine the financial impact of a wide range of cyber

attacks including denial of service, privacy breaches, etc., this study focuses on security

incidents involving third party hackers gaining access to confidential information in

targeted companies’ systems. These breaches are often a result of highly skilled hackers,

23

faulty existing security, and/or inadequate investments in security, consequently,

requiring victimized companies to examine their security mechanisms. In other words,

this excludes data leaks involving an internal party, which is nearly impossible to prevent

with an increase in cyber security.

Additionally, although this study finds no statistically significant effects, it is

consistent with previous literature’s conclusions that cyber security and IT consulting

firms are positively impacted when a targeted firm announces that hackers have exposed

confidential information. Sampling companies comprised of the overall cyber security

market sector, this study finds that cyber companies experience average cumulative

abnormal returns of 4.14% around breach announcements. In speculation, this positive

spillover effect on cyber companies could be a consequence of an increase in demand for

cyber security services. If investors attribute the breach to the targeted companies’

suboptimal investments in cyber security, cyber companies would most likely experience

positive stock returns from increase in expected business. Although cyber firms that

provided security to targeted companies prior to security incidents most likely experience

negative investor reactions, this study indicates that overall the cyber security industry

gains from internet security attacks. The results suggest that investors perceive attacks as

a indication of insufficient investments in security and evidence that cyber security

spending could increase in the future.

Moreover, while it is difficult to accurately quantify the financial impact of cyber

crime, overall attacks cause more prominent price reactions for cyber security stocks than

targeted company stocks. Theorizing these results, it is possible that internet security

companies experience more substantial abnormal returns because there is a greater

24

impact on the materiality of their business. More specifically, while the materiality of

retail stores like Target Corp. remain largely unaffected after an attack, cyber security

companies’ services revolve around cyber crime. The profitability of a cyber security

company could significantly increase from an influx of new clients seeking security after

falling victim to an attack. This could have implications on the different shareholder

responses following an information security incident.

While this research reviews an accurate representation of the cyber security

market sector, a more robust analysis of the cyber security sector would evaluate the

financial impact on the entire PureFunds ISE Cyber Security ETF. Because cyber crime

is a recent phenomenon, most of the holdings of the PureFunds ISE Cyber Security ETF

had initial public offerings in the past five years. Consequentially, this study could only

examine the eleven holdings that have stock data since 2006. Future studies will be able

to cover a more robust sample of the cyber security industry given wider availability of

stock data.

Finally, due to previous litigation on companies like Target Corp., hacked

companies have begun announcing initial breach investigations before any confirmation.

As in the case of JP Morgan Chase & Co, investigations are announced to the public a

few months before the magnitude of the breach is realized. Consequently, the share price

impact from the first announcement of a potential attack could be diluted for targeted and

cyber security companies. Future studies could examine the stock price reaction after

various announcement stages including the initial investigation, confirmation, and size of

the breach.

References

Campbell, K., Gordon, L. A., Loeb, M. P., & Zhou, L. (2003). The economic cost of

publicly announced information security breaches: empirical evidence from the stock

market. Journal of Computer Security, 11(3), 431-448.

Cardenas, J., Coronado, A., Donald, A., Parra, F., & Mahmood, M. A. (2012).

The Economic Impact of Security Breaches on Publicly Traded Corporations:

An Empirical Investigation.

Chen, J. V., Li, H. C., Yen, D. C., & Bata, K. V. (2011). Did IT consulting firms

gain when their clients were breached?. Computers in Human Behavior,28(2),

456-464.

Cost of Data Breach Grows as does Frequency of Attacks. (2015, May 27).

Retrieved April 11, 2016, from http://www.ponemon.org/blog/cost-of-data-

breach-grows-as-does-frequency-of-attacks

Das, S., Mukhopadhyay, A., & Anand, M. (2012). Stock market response to

information security breach: A study using firm and attack

characteristics.Journal of Information Privacy and Security, 8(4), 27-55.

Garg, A., Curtis, J., & Halper, H. (2003). The financial impact of IT security

breaches: what do investors think?. Information Systems Security, 12(1), 22-33.

Gatzlaff, K. M., & McCullough, K. A. (2010). The effect of data breaches on

shareholder wealth. Risk Management and Insurance Review, 13(1), 61-83.

HACK Profile | PureFunds ISE Cyber Security ET Stock - Yahoo! Finance. (n.d.).

Retrieved April 11, 2016, from http://finance.yahoo.com/q/pr?s=HACK%2BProfile

Kannan, K., Rees, J., & Sridhar, S. (2007). Market reactions to information security

breach announcements: An empirical analysis. International Journal of Electronic

Commerce, 12(1), 69-91.

Kvochko, E., & Pant, R. (2015, March 31). Why Data Breaches Don't Hurt Stock Prices.

Retrieved from https://hbr.org/2015/03/why-data-breaches-dont-hurt-stock-prices