the evolution of super-basins - beg.utexas.edu evolution of... · million tonnes oil equivalent....

TRANSCRIPT

Tinker, 2015Tinker 2018Tinker 2018

AAPG ACE

May, 2018

The Evolution of Super-Basins

Scott W. Tinker

Tinker, 2015Tinker 2018

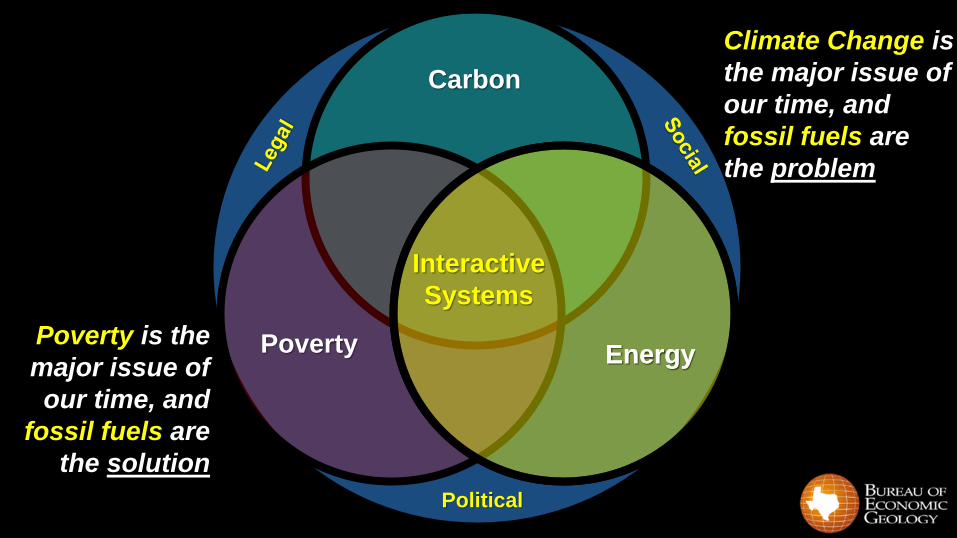

Political

Carbon

Poverty EnergyEnergy

Climate Change is

the major issue of

our time, and

fossil fuels are

the problem

Poverty is the

major issue of

our time, and

fossil fuels are

the solution

Interactive

Systems

Tinker, 2015Tinker 2018

Energy

Environment

Economy

Radical

Middle

Tinker, 2015Tinker 2018

Energy

What role will hydrocarbon

Super Basins play?

Tinker, 2015Tinker 2018

Outline

Global Energy Mix

US Shale Super Basins

Super Basin Sustainability

Tinker, 2015Tinker 2016

Global PopulationEach color on the map represents ~ 1 billion people

Petroleum

Nat Gas

Coal

Nuclear

Hydro Renew

The Global Energy Mix

4331

3135

3840

583 893

365

Tinker 2017

86%

Data: BP Statistical View of World Energy (2016)

Million Tonnes Oil Equivalent

Tinker, 2015Tinker 2016

Global PopulationEach color on the map represents ~ 1 billion people

Petroleum

Nat Gas

Coal

Nuclear

Hydro Renew

The Global Energy MixTinker 2017

86%

Data: BP Statistical View of World Energy (2016)

Million Tonnes Oil Equivalent

1036

881

429

216

151 83

323

15737

5

153

24

862

903

468

264

194 143

426

441

11 1 6 0

183

122

97

2 27 41501

6312798

95362 111

Tinker, 2015Tinker 2016

Global PopulationEach color on the map represents ~ 1 billion people

Petroleum

Nat Gas

Coal

Nuclear

Hydro Renew

Global Energy DemandTinker 2017

Data: BP Statistical View of World Energy (2016)

Million Tonnes Oil Equivalent

1036

881

429

216

151 83

323

157

375

15324

862

903

468

264

194143

426

441

11 1 6 0

183

122

97

2 27 4 1501

6312798

95

362 111

Tinker, 2015Tinker 2016

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Global Energy Consumption (MTOE)

Oil Natural Gas Coal Nuclear Hydro Solar Wind Biomass

Global Energy Mix

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Global Energy Consumption (MTOE)

Oil Natural Gas Coal Nuclear Hydro Solar Wind Biomass

Global Energy Mix

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

0

200

400

600

800

1,000

1,200

1,400

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Renewable Consumption (MTOE)

Hydro Solar Wind Biomass

Global Energy Mix

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

0

200

400

600

800

1,000

1,200

1,400

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Renewable Consumption (MTOE)

Hydro Solar Wind Biomass

Global Energy Mix

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

0

50

100

150

200

250

300

350

400

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Renewable Consumption (MTOE)

Solar Wind Biomass

Global Energy Mix

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

0

50

100

150

200

250

300

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Renewable Consumption (MTOE)

Solar Wind

Global Energy Mix

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

1995 2000 2005 2010 2015

Installed Wind Capacity (MW)

Total Asia Pacific Total Africa Total Middle East

Total S. & Cent. America Total North America Total Europe & Eurasia

Global Energy Mix

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

Global Energy Mix

Growth in U.S. Wind Generation 2000–2014

Iowa

OklahomaKansas

QAe5771

California

Illinois

Texas

2000 2006 2008 2012

45,000

25,000

35,000

20,000

30,000

40,000

5,000

15,000

0

10,000

2002 2004 2010 2014

Million Kwh

Tinker, 2015Tinker 2016

0

50,000

100,000

150,000

200,000

250,000

1996 2001 2006 2011

Installed Photovoltaic Capacity (MW)

China Japan Total North America Total Europe Total Others

Global Energy Mix

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

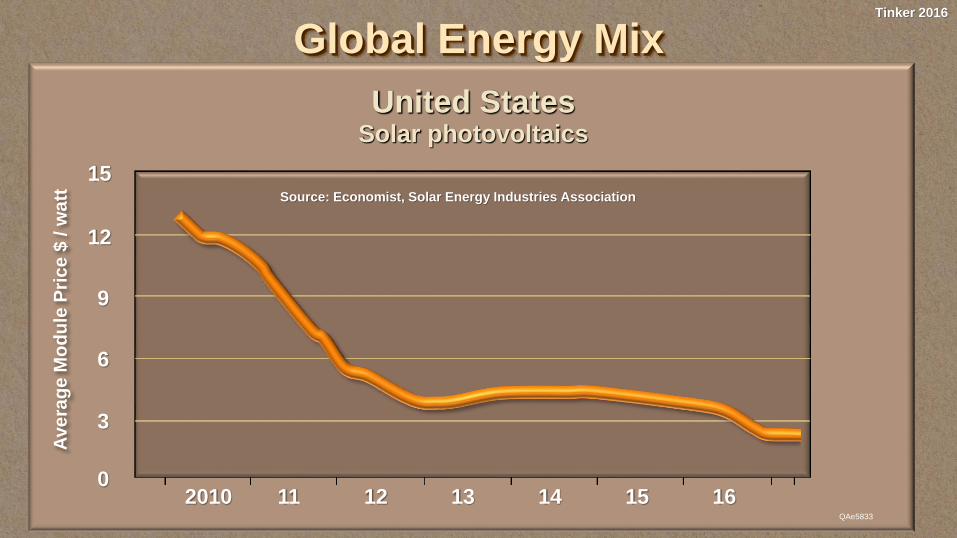

Global Energy Mix

QAe5833

United StatesSolar photovoltaics

2010 13 1411 12 15 16

Source: Economist, Solar Energy Industries Association

Ave

rag

e M

od

ule

Pri

ce

$ / w

att

15

12

9

6

3

0

Tinker, 2015Tinker 2016

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Global Energy Consumption (MTOE)

Oil Natural Gas Coal Nuclear Hydro Solar Wind Biomass

0

50

100

150

200

250

300

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Renewable Consumption (MTOE)

Solar Wind

0

200

400

600

800

1,000

1,200

1,400

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Renewable Consumption (MTOE)

Hydro Solar Wind Biomass

0

50

100

150

200

250

300

350

400

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Renewable Consumption (MTOE)

Solar Wind Biomass

0

100000

200000

300000

400000

500000

1995 2000 2005 2010 2015

Installed Wind Capacity (MW)

Total Asia Pacific Total Africa

Total Middle East Total S. & Cent. America

Total North America Total Europe & Eurasia

0

50,000

100,000

150,000

200,000

250,000

1996 2001 2006 2011

Installed Photovoltaic Capacity (MW)

China Japan Total North America Total Europe Total Others

Global Energy Mix

Data: BP Statistical View of World Energy (2016)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Global Energy Consumption Mix

Oil Natural Gas Coal Nuclear Hydro Solar Wind Biomass

Nuclear

41%

16%

38%

29%

24%

33%

95% 86%

Tinker, 2015Tinker 2016

Source: From the UN, as appeared in The Economist, August 23, 2014

4

10

12

8

6

2

0

1950 1970 1990 2010 2030 2050 2070 2100

Asia

Glo

ba

l Po

pu

latio

n (B

)

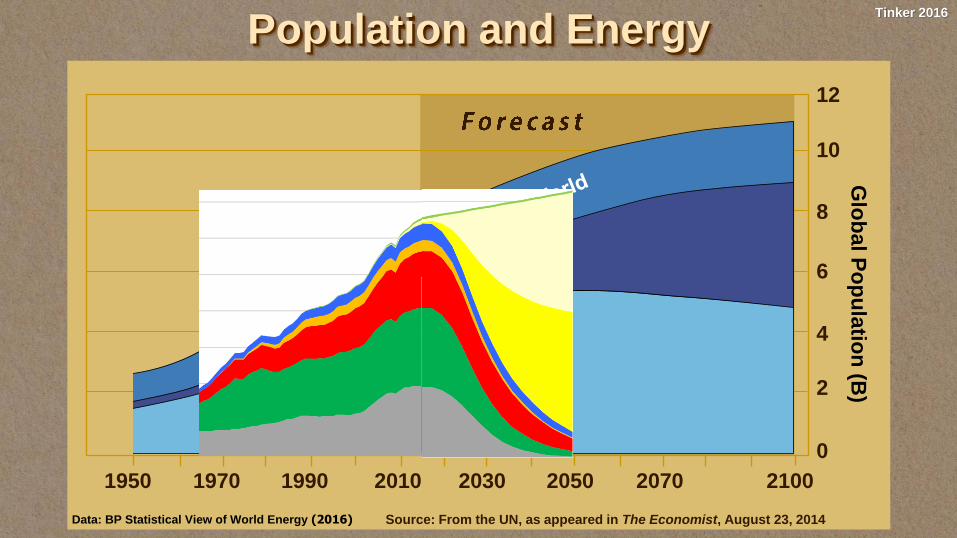

Population and Energy

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

Source: From the UN, as appeared in The Economist, August 23, 2014

4

10

12

8

6

2

0

1950 1970 1990 2010 2030 2050 2070 2100

Asia

Glo

ba

l Po

pu

latio

n (B

)

Asia

Population and Energy

Data: BP Statistical View of World Energy (2016)

Tinker, 2015Tinker 2016

Source: From the UN, as appeared in The Economist, August 23, 2014

4

10

12

8

6

2

0

1950 1970 1990 2010 2030 2050 2070 2100

Asia

Glo

ba

l Po

pu

latio

n (B

)

Asia

Population and Energy

Data: BP Statistical View of World Energy (2016)

~45%

Tinker, 2015Tinker 2016

Source: From the UN, as appeared in The Economist, August 23, 2014

4

10

12

8

6

2

0

1950 1970 1990 2010 2030 2050 2070 2100

Asia

Glo

ba

l Po

pu

latio

n (B

)

Population and Energy

Data: BP Statistical View of World Energy (2016)

“The world

could be 100%

wind, wave and

solar by 2030,

if just for

political will…”~45%

Tinker, 2015Tinker 2016

Source: From the UN, as appeared in The Economist, August 23, 2014

4

10

12

8

6

2

0

1950 1970 1990 2010 2030 2050 2070 2100

Asia

Glo

ba

l Po

pu

latio

n (B

)

Population and Energy

Data: BP Statistical View of World Energy (2016)

~45%

Tinker, 2015Tinker 2016

Source: From the UN, as appeared in The Economist, August 23, 2014

4

10

12

8

6

2

0

1950 1970 1990 2010 2030 2050 2070 2100

Asia

Glo

ba

l Po

pu

latio

n (B

)

Population and Energy

Data: BP Statistical View of World Energy (2016)

~45%

Tinker, 2015Tinker 2016

Source: From the UN, as appeared in The Economist, August 23, 2014

4

10

12

8

6

2

0

1950 1970 1990 2010 2030 2050 2070 2100

Asia

Glo

ba

l Po

pu

latio

n (B

)

Population and Energy

Data: BP Statistical View of World Energy (2016)

~45%

Tinker, 2015Tinker 2016

Source: From the UN, as appeared in The Economist, August 23, 2014

4

10

12

8

6

2

0

1950 1970 1990 2010 2030 2050 2070 2100

Asia

Glo

ba

l Po

pu

latio

n (B

)

Population and Energy

Data: BP Statistical View of World Energy (2016)

~45%

Are there affordable, available, reliable and sustainable:

• fossil energy and nuclear resources to meet this demand?

• renewable energy resources to meet this demand?

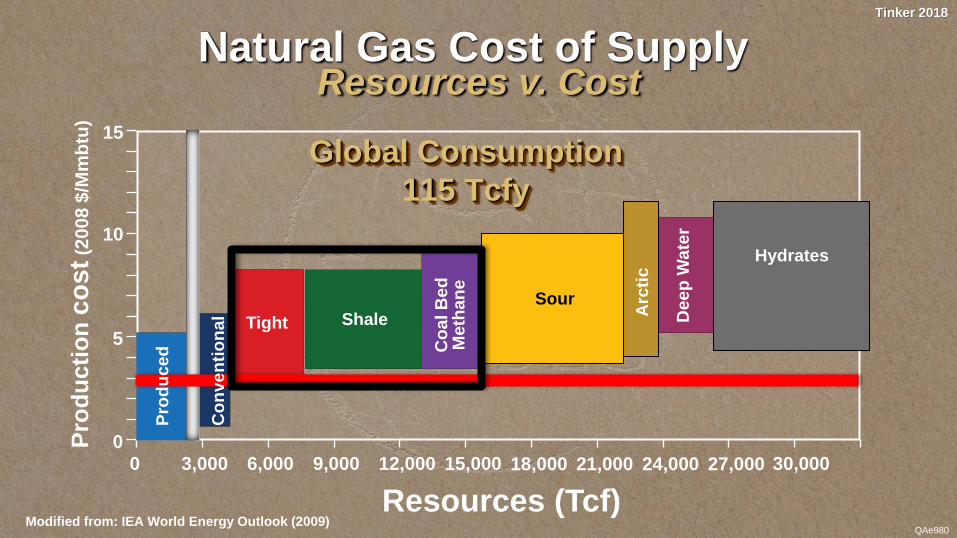

~15,000 TcF

(5X to date)

~2,600 BBO

(2X to date)

Tinker, 2015Tinker 2018

0 3,000 6,000 12,0009,000 15,000 30,00018,000 21,000 24,000 27,000

Resources (Tcf)

Pro

du

cti

on

co

st

(2008 $

/Mb

tu)

Hydrates

15

10

5

0

Natural Gas Cost of Supply

Resources v. Cost

QAe980Modified from: IEA World Energy Outlook (2009)

Global Consumption 2015

123 Tcfy

Arc

tic

Co

nv

en

tio

na

l

Sour

De

ep

Wa

ter

Shale

Co

al

Be

dM

eth

an

e

Tight

Pro

du

ce

d

Tinker, 2015Tinker 2018

Oil Cost of SupplyResources and Cost

0 2000 4000 10,0006000 8000

140

20

0

Resources (billion barrels)

Pro

du

cti

on

co

st

(2

00

8 $

)

Produced MENA

40

60

80

100

120

Arctic

Modified from: IEA World Energy Outlook (2009)

Coal

to

liquids

Gas

to

liquidsOther

conventionaloil

EOR

Deepwater and

ultra-deepwater

Oil shales

Shale oil

Heavy

oil

&

bitumen

CO2 EOR

Tinker, 2015Tinker 2018

Source: From the UN, as appeared in The Economist, August 23, 2014

4

10

12

8

6

2

0

1950 1970 1990 2010 2030 2050 2070 2100

Asia

Glo

ba

l Po

pu

latio

n (B

)

Population and Energy

Data: BP Statistical View of World Energy (2016)

~40%

~25%

~35%

0 0.25 0.5 0.75 1

1

0.75

0.5

0.25

01

0.75

0.5

0.25

0

Natural Gas, Nuclear

Coal, Oil, BiomassWind, Solar, Hydro

Global

Primary

Energy

1965

2015

Natural Gas, Nuclear

Coal, Oil, BiomassWind, Solar, Hydro

2065

40% 25% 35%

60% 30% 10%

80% 15% 5%

40% 40% 20%

2065

Tinker, 2015Tinker 2018

60 Years and CountingW

TI

($/b

arr

el)

Inflation Adjusted Oil Price

Tinker, 2015Tinker 2018

Outline

Global Energy Mix

US Shale Super Basins

Super Basin Sustainability

Tinker, 2015Tinker 2018

For presentation or publication, reference:

Bureau of Economic Geology Shale Resource and Production Project

http://www.beg.utexas.edu/research/programs/shale

Marcellus

Fayetteville

Haynesville

Barnett

Eagle Ford

Bakken/Three Forks

Permian Basin

Production Outlook

• Pace of drilling by year and area,• Expected gas/oil/water

production depending on economics, technology, regulation

Well Economics

Expected well profitability

as a function of

• Well production profile

• Operational

• Market and regulatory parameters

Well Decline Analysis

• Production and its decline for gas/oil/water

• Stimulated/drained rock volume

Geologic Analysis

•Reservoir characterization

•Original-Resource-in-Place

•3-D Geologic Model

Recovery and Productivity

Statistical Analysis

Expected production

as a function of

• Well productivity drivers

• Location and Completion

• Inventory of future wells

• Technically Recoverable Resources

For presentation or publication, reference: Bureau of Economic Geology Shale Resource and Production Project http://www.beg.utexas.edu/research/programs/shale

BEG Tight Oil Resource Assessment (TORA)Integrated Study Workflow

U.S. Shale Gas

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

2005 2010 2015 2020 2025 2030 2035 2040

$/M

MB

tu

TC

F

Marcellus

Haynesville

Fayetteville

Barnett

EIA Price Scenario

Source: BEG Shale Resources and Reserves Team

U.S. Shale Gas

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

2005 2010 2015 2020 2025 2030 2035 2040

$/M

MB

tu

TC

F

Marcellus

Haynesville

Fayetteville

Barnett

EIA Price Scenario

Source: BEG Shale Resources and Reserves Team

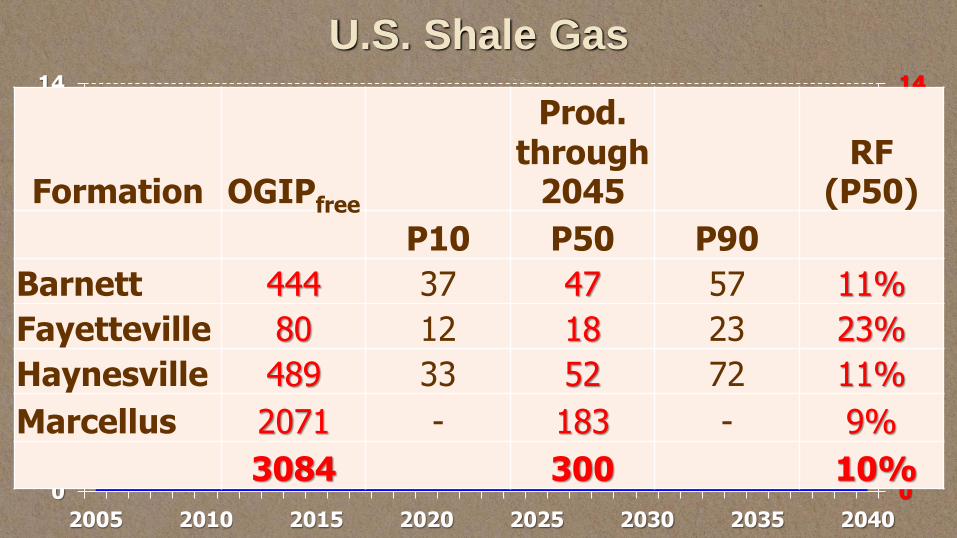

Formation OGIPfree

Prod. through

2045RF

(P50)

P10 P50 P90

Barnett 444 37 47 57 11%

Fayetteville 80 12 18 23 23%

Haynesville 489 33 52 72 11%

Marcellus 2071 - 183 - 9%

3084 300 10%

U.S. Shale Gas 2012

Base High

2017

Low

For presentation or publication, reference: Bureau of Economic Geology Shale Resource and Production Project

http://www.beg.utexas.edu/research/programs/shale

Tinker, 2015Tinker 2018

U.S. Shale Gas 2012

Base High

2017

Low

For presentation or publication, reference: Bureau of Economic Geology Shale Resource and Production Project http://www.beg.utexas.edu/research/programs/shale

$3 $4 $6

$2.75 $3.75 $4.50

2963

653

182 215327

3311

692

158305

415

1

10

100

1000

10000

OGIP TRR Low EUR Base EUR High EUR

TcF

Barnett, FV, HV, Marcellus

5%

9% 16%

2012 BEG Studies

2017 BEG Update

% of OGIP21%

$3 $4 $6

$2.7

5

$3.7

5

$4.5

0

Tinker, 2015Tinker 2018

0 3,000 6,000 12,0009,000 15,000 30,00018,000 21,000 24,000 27,000

Resources (Tcf)

Pro

du

cti

on

co

st

(2008 $

/Mm

btu

)

Hydrates

15

10

5

0

QAe980Modified from: IEA World Energy Outlook (2009)

Global Consumption

115 Tcfy

~ 300 year total resource

Sour

Arc

tic

De

ep

Wa

ter

Shale

Co

al

Be

dM

eth

an

e

Co

nv

en

tio

na

l Tight

Pro

du

ce

d

Natural Gas Cost of SupplyResources v. Cost

Tinker, 2015Tinker 2018

0 3,000 6,000 12,0009,000 15,000 30,00018,000 21,000 24,000 27,000

Resources (Tcf)

Pro

du

cti

on

co

st

(2008 $

/Mm

btu

)

Hydrates

15

10

5

0

QAe980Modified from: IEA World Energy Outlook (2009)

Global Consumption

115 Tcfy

Sour

Arc

tic

De

ep

Wa

ter

Shale

Co

al

Be

dM

eth

an

e

Co

nv

en

tio

na

l Tight

Pro

du

ce

d

Natural Gas Cost of SupplyResources v. Cost

Tinker, 2015Tinker 2018

0 3,000 6,000 12,0009,000 15,000 30,00018,000 21,000 24,000 27,000

Resources (Tcf)

Pro

du

cti

on

co

st

(2008 $

/Mm

btu

)

Hydrates

15

10

5

0

QAe980Modified from: IEA World Energy Outlook (2009)

Global Consumption

115 Tcfy

Sour Arc

tic

De

ep

Wa

ter

Shale

Co

al

Be

dM

eth

an

e

Co

nv

en

tio

na

l

Tight

Pro

du

ce

d

Natural Gas Cost of SupplyResources v. Cost

Tinker, 2015Tinker 2018

0 3,000 6,000 12,0009,000 15,000 30,00018,000 21,000 24,000 27,000

Resources (Tcf)

Pro

du

cti

on

co

st

(2008 $

/Mb

tu)

Hydrates

15

10

5

0

Natural Gas Cost of Supply

Resources v. Cost

QAe980Modified from: IEA World Energy Outlook (2009)

Global Consumption 2015

123 Tcfy

~ 300 year total resource

Arc

tic

Co

nv

en

tio

na

l

Sour

De

ep

Wa

ter

Shale

Co

al

Be

dM

eth

an

e

Tight

Pro

du

ce

d

Reserves are a function of

Price, Cost, Technology,

Policy and Demand

Tinker, 2015Tinker 2018

Gas OilTcf Bbbl

Original In-Place 3100 450

Tech. Recoverable 700 27

Production to date 70 5

Horizontal wells to date ~ Future wells (base case) ~500,000

Gas Oil

Resource-in-Place

Produced to-date

TRR

~75,000~500,000

Fayetteville

~6,500~13,000

Haynesville

~6,000~35,000

Marcellus ~10,500~200,000

Barnett~16,500~63,000

For presentation or publication, reference: Bureau of Economic Geology Shale Resource and Production Project http://www.beg.utexas.edu/research/programs/shale

Tinker, 2015Tinker 2018

Eagle FordOil Production Scenarios

0

100

200

300

400

500

600

700

800

2008 2013 2018 2023 2028 2033 2038 2043

Oil

pro

du

cti

on

MM

bb

l/ye

ar

at $100/bbl

at $80/bbl

at $50/bbl

at $40/bbl

Historical through 2014

For presentation or publication, reference: Bureau of Economic Geology Shale Resource and Production Project http://www.beg.utexas.edu/research/programs/shale

Tinker, 2015Tinker 2018

Shale Oil SupplyEIA price scenario

0

20

40

60

80

100

120

140

160

0

200

400

600

800

1000

1200

2008 2013 2018 2023 2028 2033 2038 2043

$/b

bl

An

nu

al liq

uid

s p

rod

ucti

on

MM

bb

l

Middle Bakken and Three Forks EGLF Eagle Ford WTI price $2013

27 Bbbl out of 450 Bbbl6% Recovery

For presentation or publication, reference: Bureau of Economic Geology Shale Resource and Production Project http://www.beg.utexas.edu/research/programs/shale

Tinker, 2015Tinker 2018

Gas OilTcf Bbbl

Original In-Place 3100 450

Tech. Recoverable 700 27

Production to date 70 5

Horizontal wells to date ~ Future wells (base case) ~500,000

Gas Oil

Resource-in-Place

Produced to-date

TRR

~75,000~500,000

Fayetteville

~6,500~13,000

Eagle Ford

~16,500~90,000

Bakken/Three Forks

~18,000~100,000

Haynesville

~6,000~35,000

Marcellus ~10,500~200,000

Barnett~16,500~63,000

Permian Basinin progress

For presentation or publication, reference: Bureau of Economic Geology Shale Resource and Production Project http://www.beg.utexas.edu/research/programs/shale

Tinker, 2015Tinker 2018

HF: hydraulic fracturingUnc PW: unconventional produced waterConv PW: conventional produced water SWD P: salt water disposal into producing SWD NP: into non-producing intervalsEORI: enhanced oil recovery injection

From Scanlon BEG

Used with Permission

Tinker, 2015Tinker 2018

Flowback

and

Produced

Water

Outlook

For presentation or publication,

reference: Bureau of Economic

Geology Shale Resource and

Production Project

http://www.beg.utexas.edu/research/p

rograms/shale

Tinker, 2015Tinker 2018

Super Basins Environmental Impact

Mining and Manufacturing

Drilling and Completion: Land and Water

Transportation: Pipelines, Trucks, Ships, Rail

Refining and Petrochemicals: Emissions

Combustion: Vehicle and Power Plant Emission

Social and Political

Tinker, 2015Tinker 2018

Mining and Processing Land, Water, Emissions

Manufacturing: Turbines, Panels, Batteries

Production: Land for “Farms”

Transmission: Electricity

Disposal: Landfill

Environmental ImpactRenewables and Batteries

Tinker, 2015Tinker 2018

Outline

Global Energy Mix

US Shale Super Basins

Super Basin Sustainability

Tinker, 2015Tinker 2018

Political

Energy

Environment

Economy

Super

Basins

Infrastructure

Energy Mix

Talent

Education

Data

Analytics

Tinker, 2015Tinker 2018

U.S. Electric Generation Shares (2005-15)

QAe4744Source: EIA

Perc

en

t o

f to

tal

Other

Natural gas

Coal

100%

80%

60%

40%

20%

0%2005 2007 2009 2011 2013 20152006 2008 2010 2012 2014

Nuclear

Renewables

20%

8%

18%

51%

21%

13%

32%

34% 68%

% of

CO2

30%

2%

~ 20% CO2

Reduction!

Tinker, 2015Tinker 2018

0

20

40

60

80

100

120

140

160

180

200

1950 1960 1970 1980 1990 2000 2010

Qu

adri

llio

n B

tuUS Energy Mix

After Jim Sweeney, 2015. Data: EIA, Monthly Energy Review

Oil

Natural Gas

Coal

Nuclear

Total Energy Consumed Imports

HydroBiofuelsWind & Solar

Growth 0.55% less than GDP

80 Quads

“Efficiency”

Fracking

Tinker, 2015Tinker 2018

Electricity and Poverty

QAe5021Sources: World Bank; IEA; World Energy Outlook 2015

Poverty and electricity

access in selected

developing countries,

circles sized by

total population

100

0 40 8020 60 100

80

60

40

20

0

Income % (<$3.10 a day at 2011 PPP†, %)

Ele

ctr

ific

ati

on

ra

te 2

01

3,

%

Africa

Asia

Latin America

* Bangladesh uses

2005 PPP and $2

a day poverty line

† Purchasing power

parity

Vietnam

China

India

Bangladesh*

Brazil

Nigeria

Tanzania

Kenya

Uganda

Ethiopia

Cameroon

Electricity

Poverty

Photos Tinker, Lynch, Ecuador, 2017

Tinker, 2015Tinker 2018

There is “good” energy and

“bad” energy…

What do the “Educators” Communicate

Renewables and batteries are “good”

Fossils and nuclear are “bad”…

Tinker, 2015Tinker 2018

Keep IT in the Ground. Keep THEM in Poverty.

Tinker, 2015Tinker 2018

Super BasinKey Issues

Manage Complexity

• Oil & Gas supply and demand dynamics

• Power sector

• Human infrastructure

• Agriculture

• Regulators, policy makers, public perception

Cooperate and Coordinate

• Across states and stakeholders

• Availability of water, land, energy

• Conflicts of interest

• Planning and Financing

• Law and politics

Tinker, 2015Tinker 2018

Super BasinKey Issues

Manage Complexity

• Oil & Gas supply and demand dynamics

• Power sector

• Human infrastructure

• Agriculture

• Regulators, policy makers, public perception

Cooperate and Coordinate

• Across states and stakeholders

• Availability of water, land, energy

• Conflicts of interest

• Planning and Financing

• Law and politics

New York!

Tinker, 2015Tinker 2018

Sustainability of Super Basins

Energy: Scale and Diversity Matter

Public Engagement: Vital

Education: A Contact Sport

Tinker, 2015Tinker 2018

…for what you do!

Thank You…