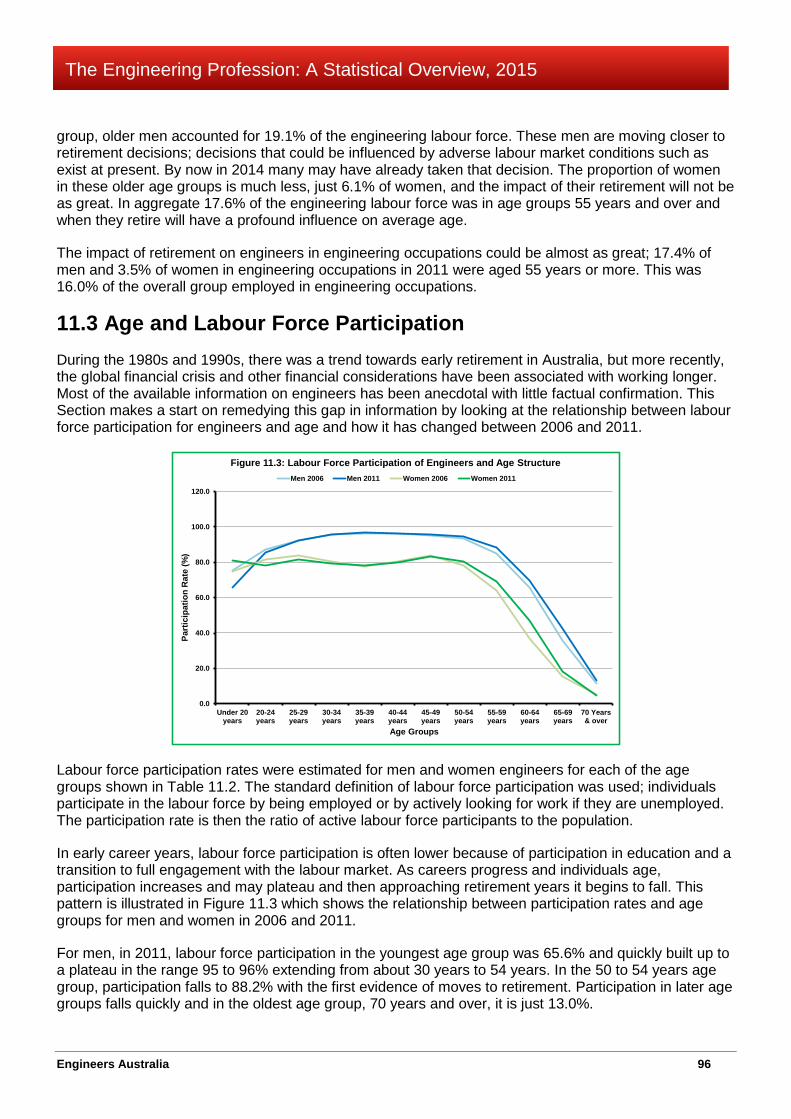

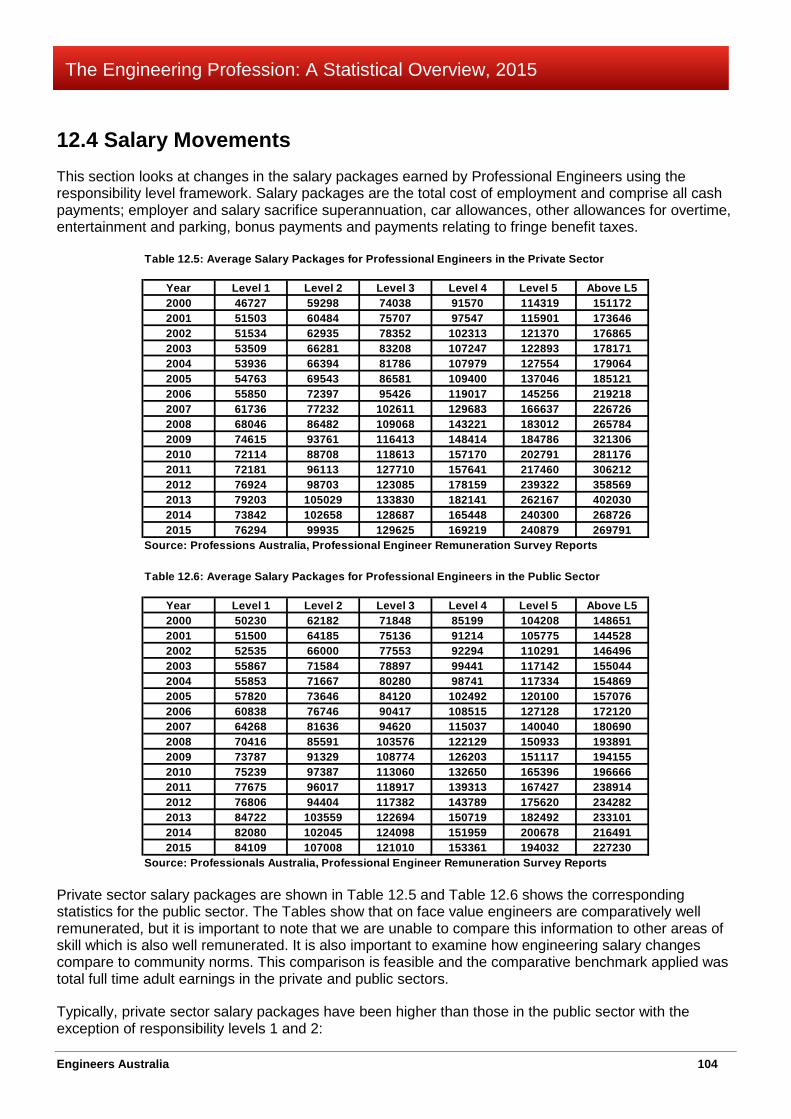

the engineering profession: a statistical overview · the engineering profession: a statistical...

TRANSCRIPT

THE ENGINEERING PROFESSION:

A STATISTICAL OVERVIEW

Twelfth Edition, November 2015

The Engineering Profession: A Statistical Overview, ELEVENTH edition, October 2015

ISBN 978 1 922107 78 7 Author: Andre Kaspura

Email: [email protected] Institution of Engineers Australia 2015

All rights reserved. Other than brief extracts, no part of this publication may be reproduced in any form without the written consent of the publisher. The report can be downloaded at www.engineersaustralia.org.au

Public Affairs and Marketing Engineers Australia 11 National Circuit, Barton ACT 2600 Tel: 02 6270 6555 Email: [email protected]

www.engineersaustralia.org.au

Engineers Australia i

THE ENGINEERING PROFESSION: A STATISTICAL OVERVIEW, 2014

Engineers Australia ii

The Engineering Profession: A Statistical Overview, 2015

CONTENTS Chapter 1 Introduction 1

Main Points 1 1.1 Engineers and Engineering 1 1.2 Objective of the Statistical Overview 2 1.3 The Engineering Team 2 1.4 Competent Practicing Engineers 3 1.5 Data Sources and Caveats 4 1.6 What’s New in this Edition? 5

Chapter 2 Structural Features of the Labour Market 7 Main Points 7 2.1 Key Information 7 2.2 Labour Force Participation 8 2.3 Women in Engineering 9 2.4 Engineers and Engineering 9 2.5 Changes in Demand and Supply 10 2.6 Engineering is Dependent on Skilled Migration 10 2.7 Diversity and labour market Experience 10 2.8 The Source of Migrant Engineers 11

Chapter 3 The Engineering Labour Market over Time 13 Main Points 13

3.1 Background 13 3.2 Survey of Education and Work 14 3.3 Engineering Population 15 3.4 Participation Rates and the Supply of Engineers 16 3.5 The Demand for Engineers 17 3.6 Unemployment 18 3.7 Employment in Engineering Occupations 19

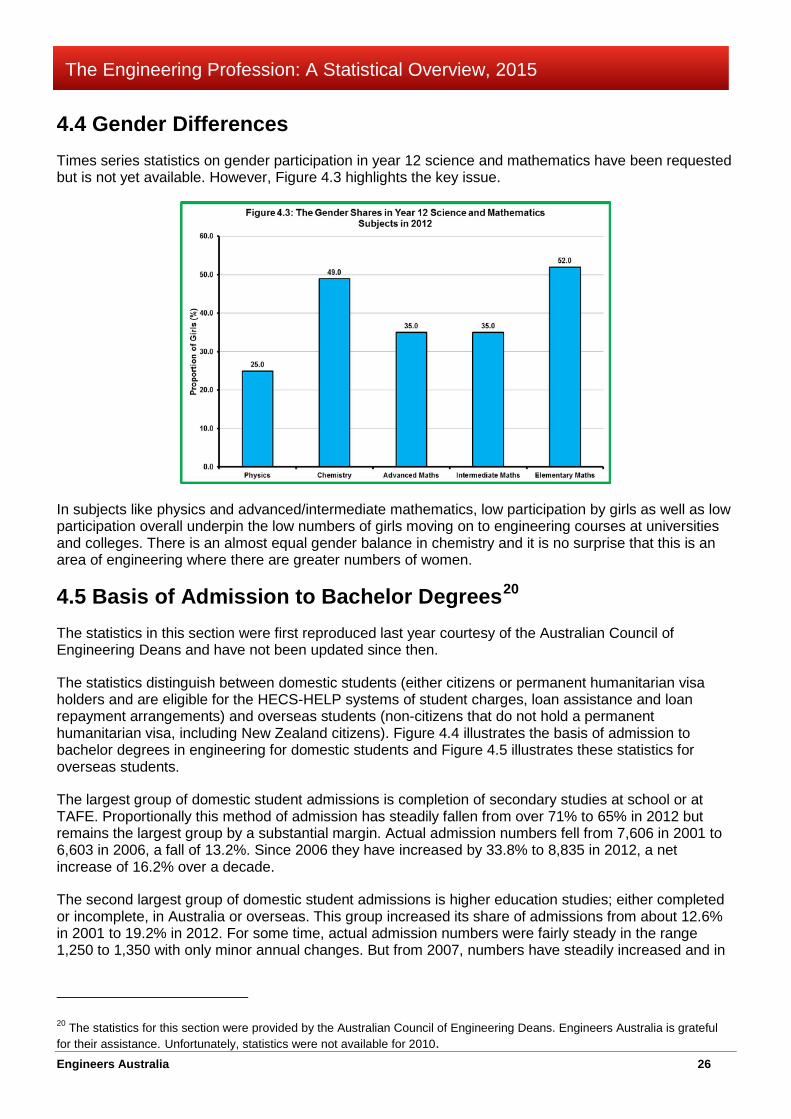

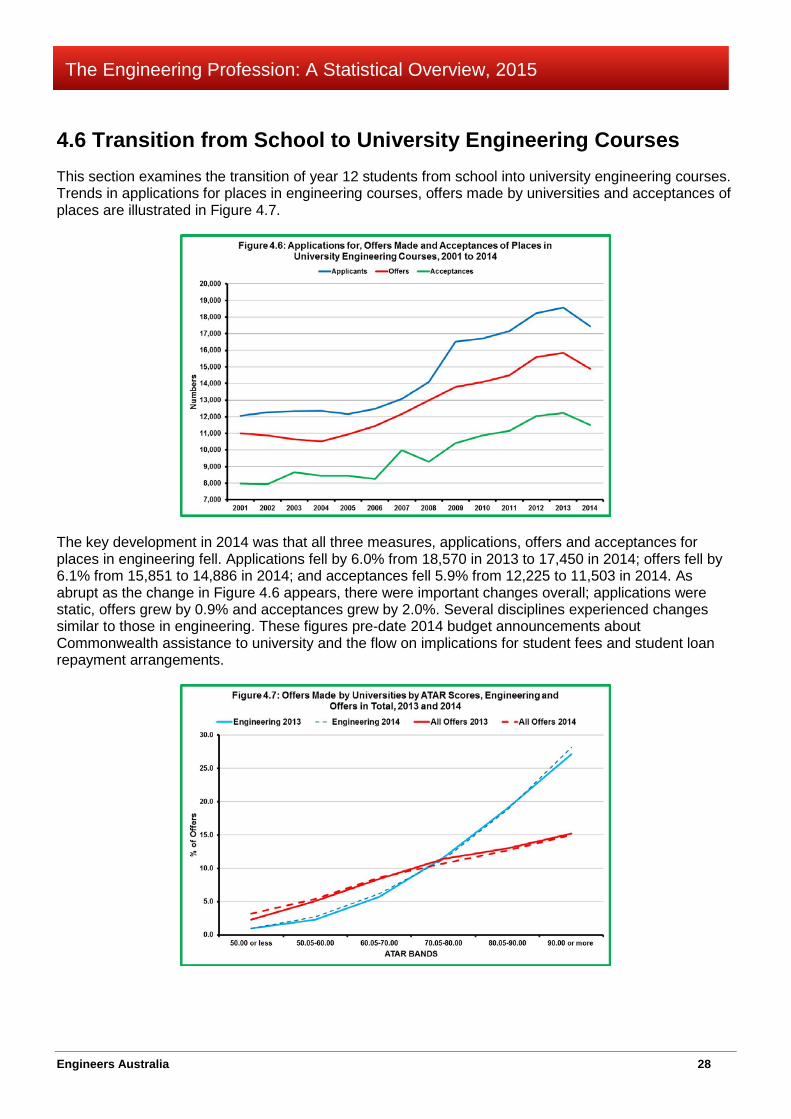

Chapter 4 Transition to Engineering Studies 22 Main Points 22 4.1 School Participation to Year 12 22 4.2 Participation in Science Subjects 23 4.3 Participation in Mathematics Subjects 25 4.4 Gender Differences 26 4.5 Basis of Admission to Bachelor Degrees 26 4.6 Transition from School to University Engineering Courses 28

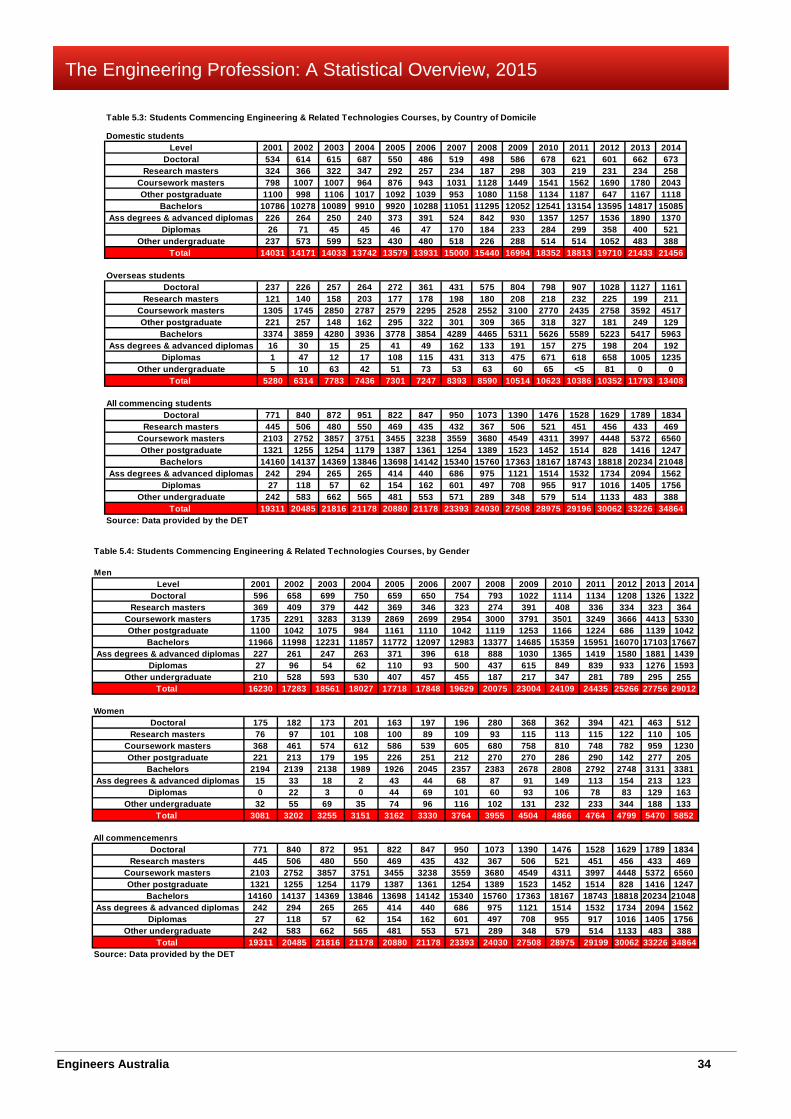

Chapter 5 University Engineering Education 30 Main Points 30 5.1 Course Commencements 31 5.2 Student Enrolments 32 5.3 Course Completions 39 5.4 Annual Retention Rates for Bachelor Degrees 39 5.5 The Engineering Share of Course Completions 41 5.6 State and Territory Shares of Bachelor Degree Completions 43

Engineers Australia iii

The Engineering Profession: A Statistical Overview, 2015

Chapter 6 Developing Our Own Engineers 44 Main Points 44 6.1 Terminology 44 6.2 Labour Market Choices of New Graduates 46 6.3 Labour Market Experiences of New Graduates 47 6.4 Engineering Technologists 48 6.5 Professional Engineers 49 6.6 Associate Engineers 51 6.7 Annual Additions to Supply 53

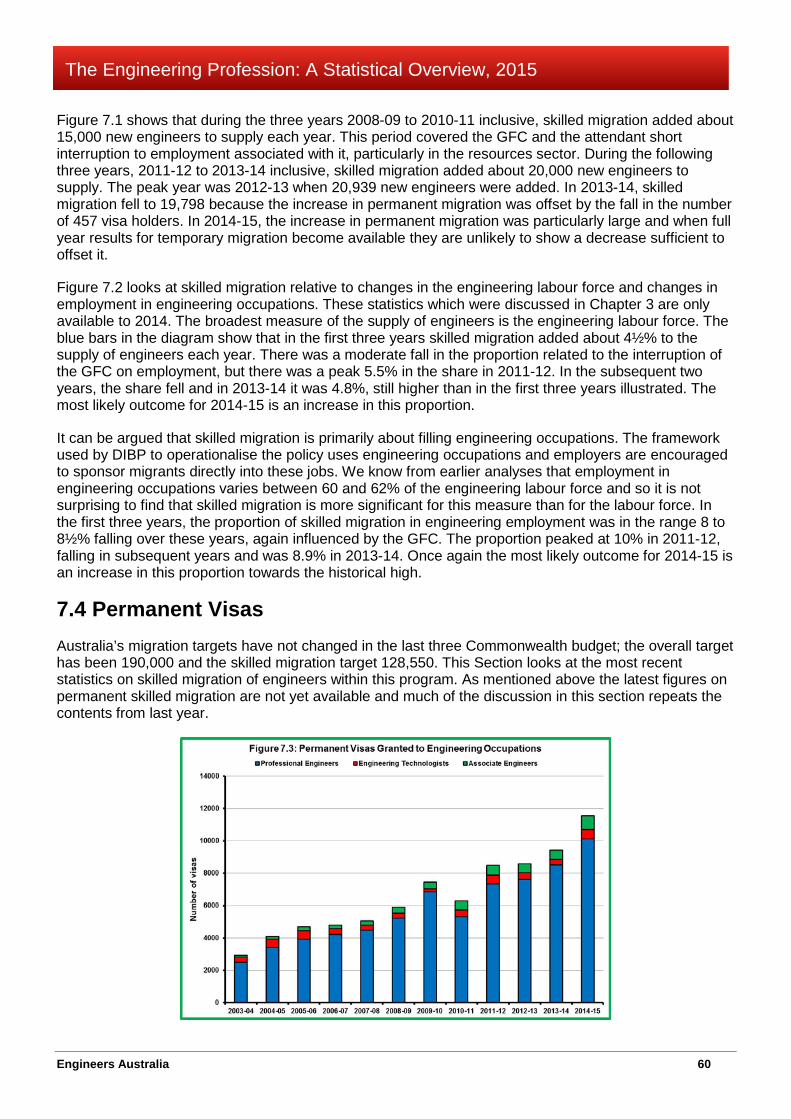

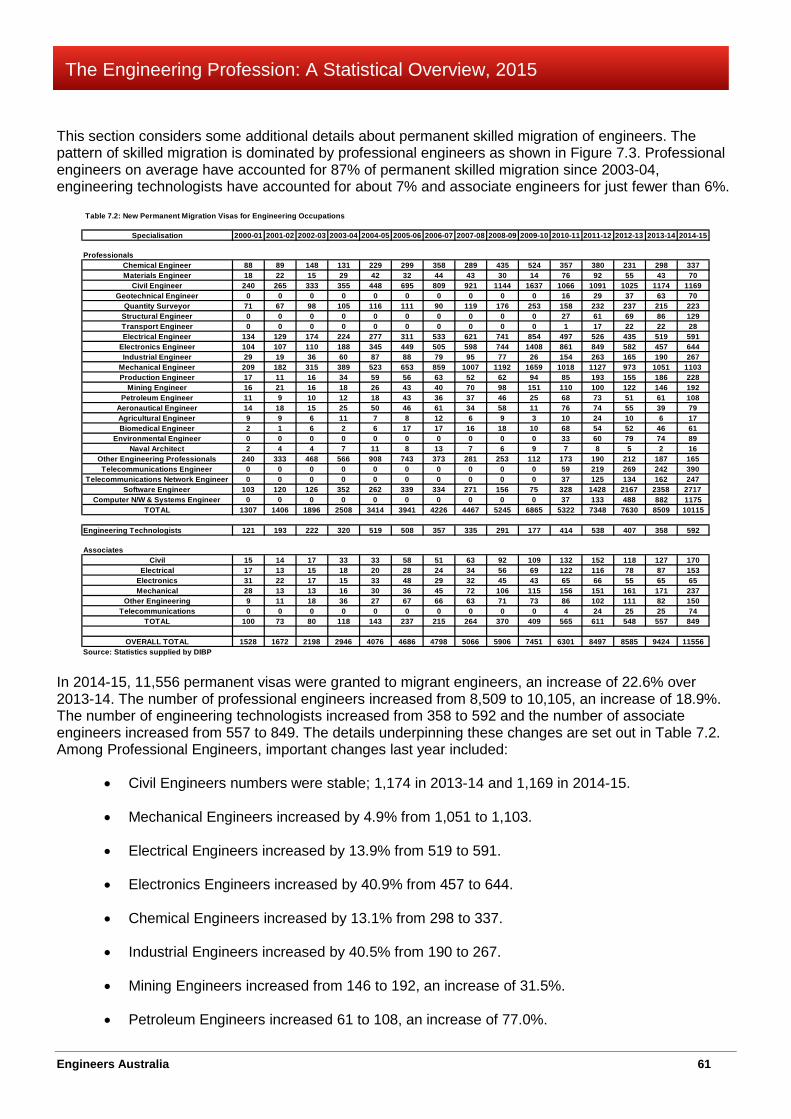

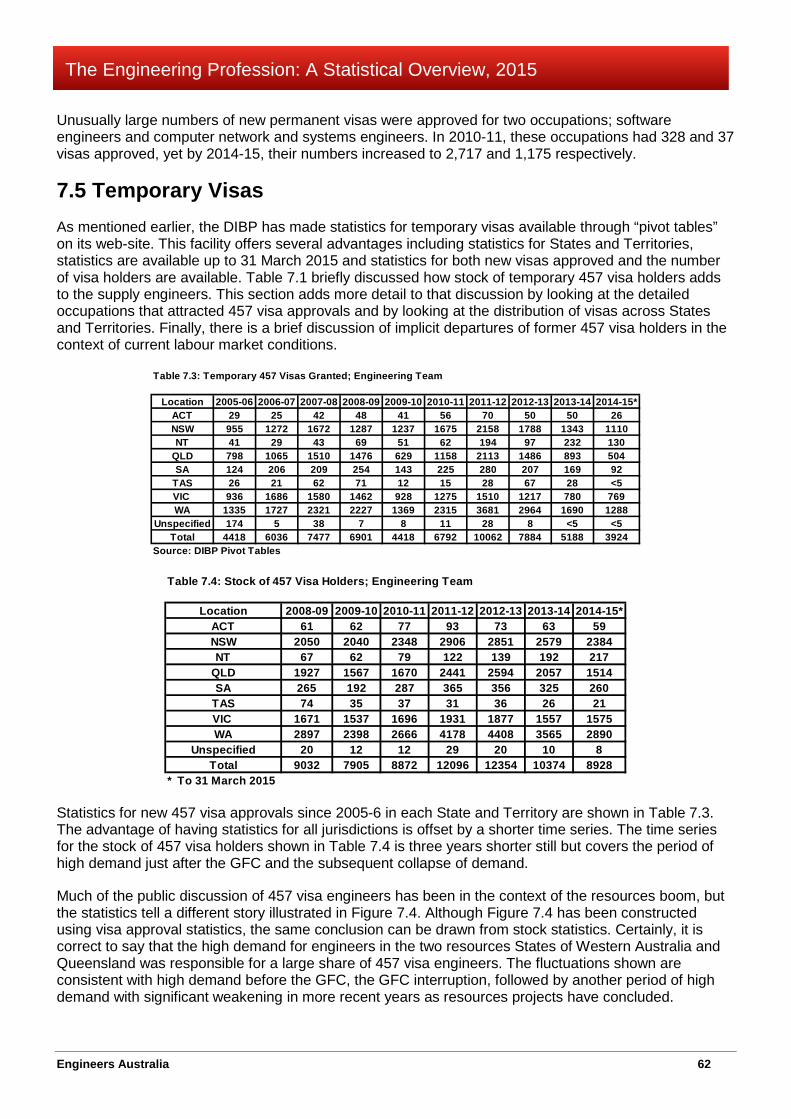

Chapter 7 Skilled Migration 56 Main Points 56 7.1 Australia’s Skilled Migration Policy 56 7.2 Assessing Overseas Engineering Qualifications 57 7.3 Skilled Migration and the Supply of Engineers 58 7.4 Permanent Visas 60 7.5 Temporary Visas 62

Chapter 8 Engineers in Industry 65 Main Points 65 8.1 The ABS Industry System 65 8.2 Broad Characterization of Engineering Work 66 8.3 Employment at Sub-Division Level 68 8.4 What Industries Employ the Most Engineers? 68

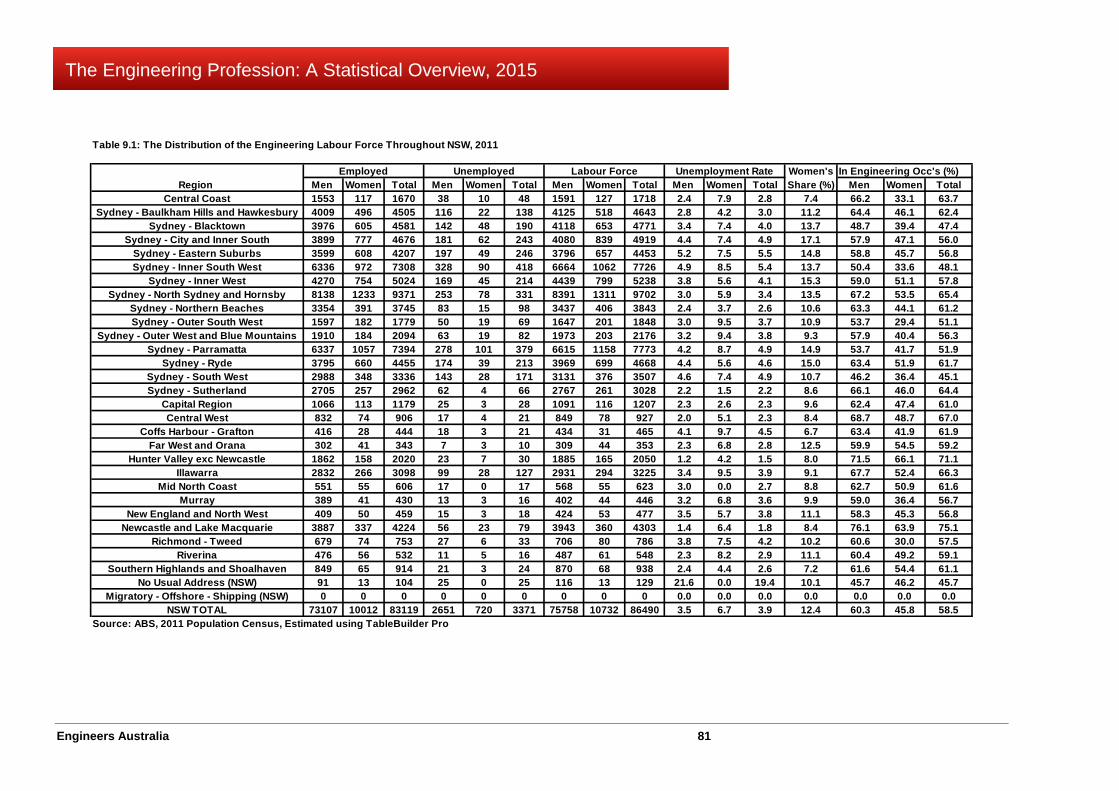

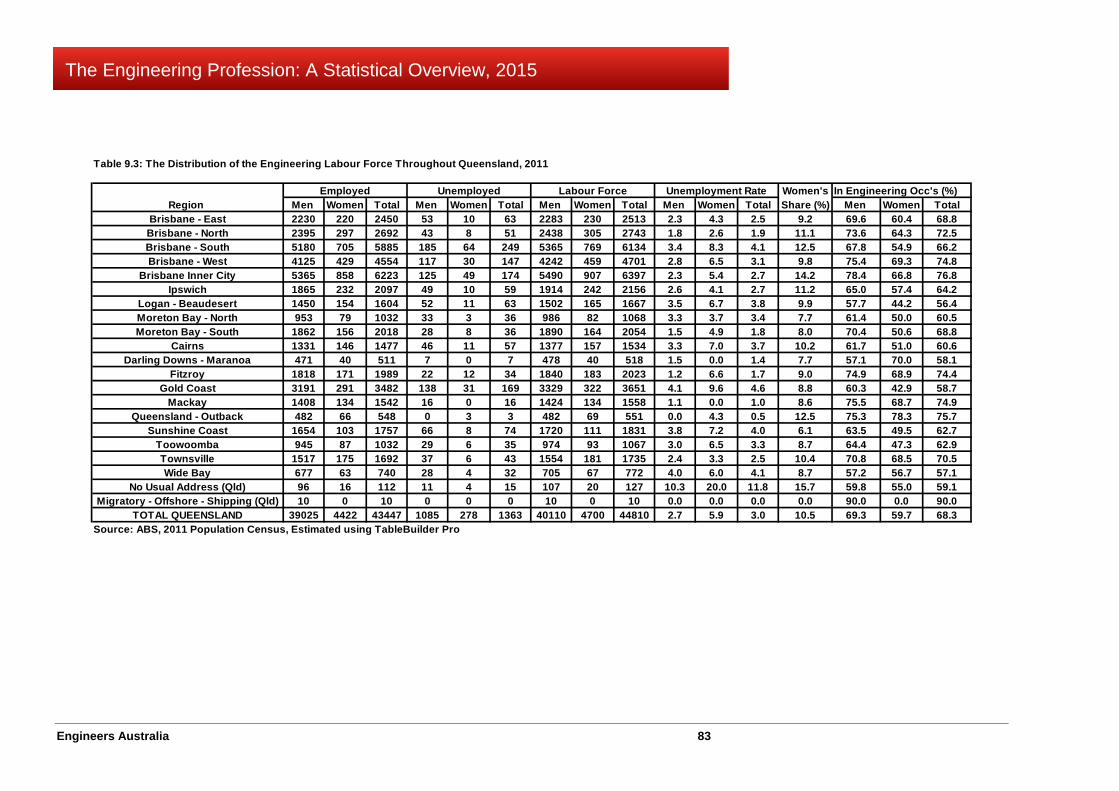

Chapter 9 Geographic Distribution 77 Main Points 77 9.1 The ABS Approach to Geographic Statistics 77 9.2 New South Wales 77 9.3 Victoria 78 9.4 Queensland 78 9.5 South Australia 79 9.6 Western Australia 79 9.7 Tasmania 79 9.8 The Territories 80

Chapter 10 Engineering Specialisations 86 Main Points 86 10.1 Engineering Courses and Engineering Specialisation 86 10.2 Broad Specialist Areas of Engineering 88 10.3 Detailed Engineering Streams 89

Chapter 11 Average Ages and Age Structure 92 Main Points 92 11.1 Average Ages of Engineers 92 11.2 Age Structure and how it has changed 93 11.3 Age and Labour Force Participation 96

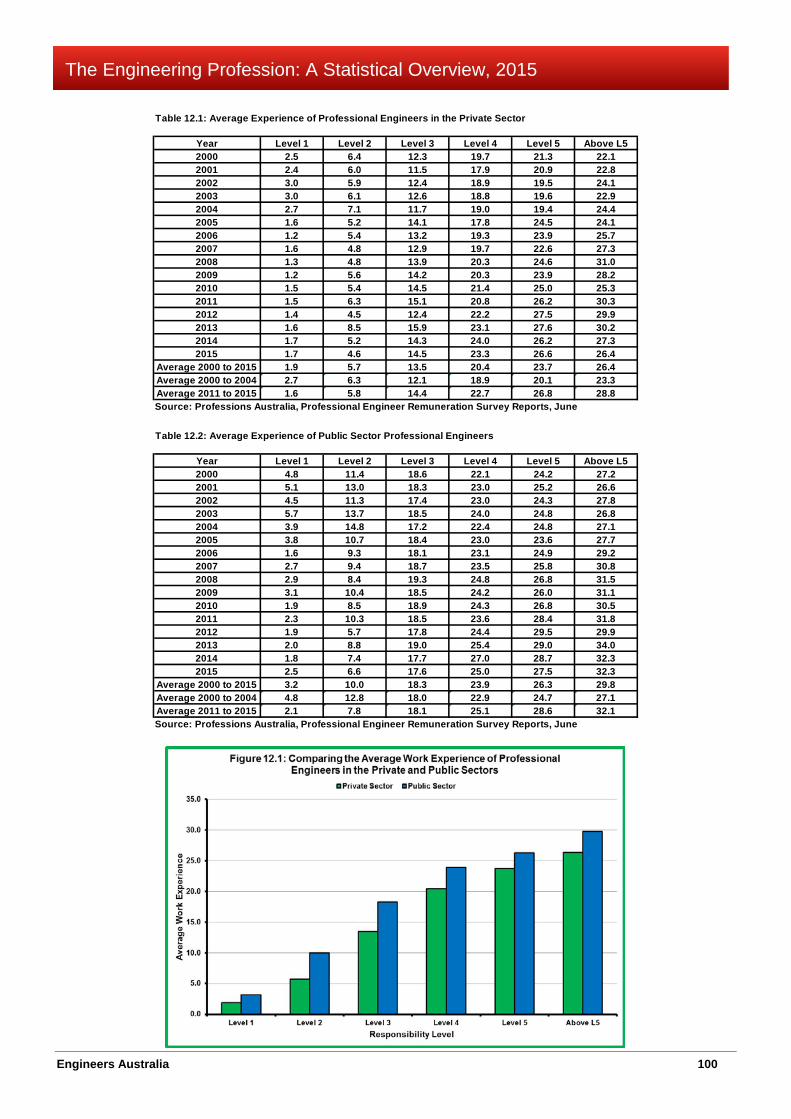

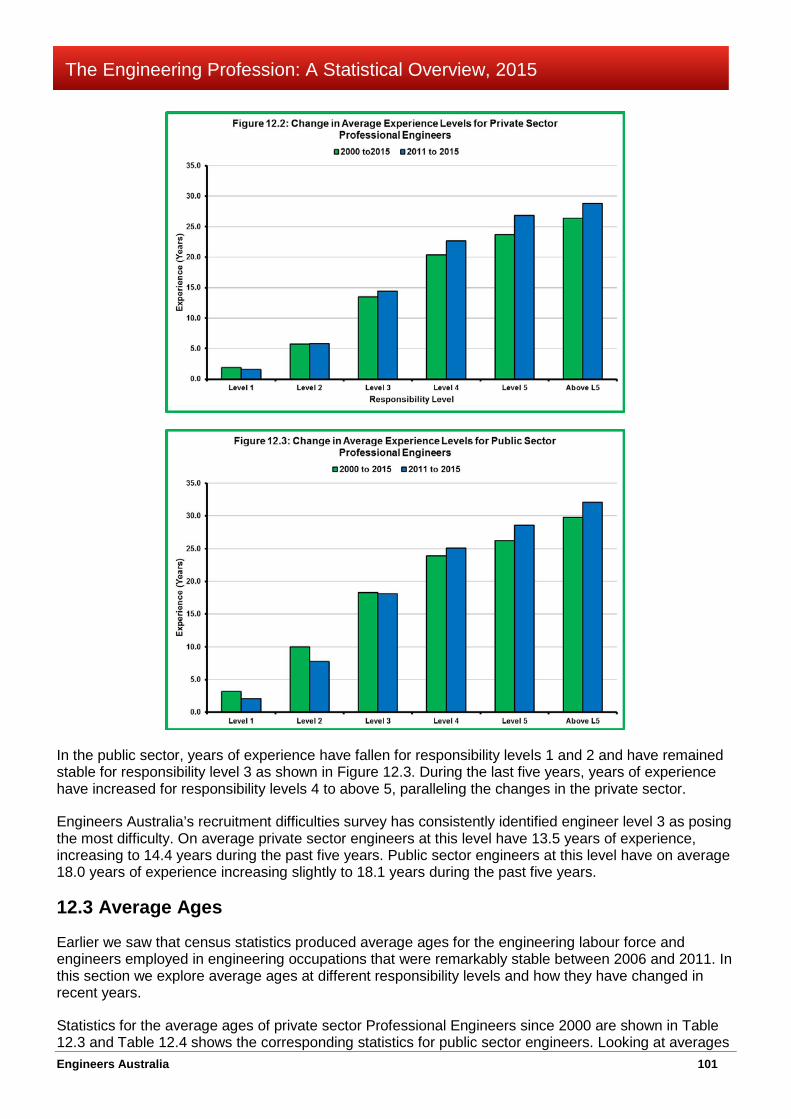

Chapter 12 Experience, Remuneration and Age 98 Main Points 98 12.1 The Framework Used 98 12.2 Experience 99

Engineers Australia iv

The Engineering Profession: A Statistical Overview, 2015

12.3 Average Ages 101 12.4 Salary Movements 104

Chapter 13 Indicators for the Engineering Labour Market 107

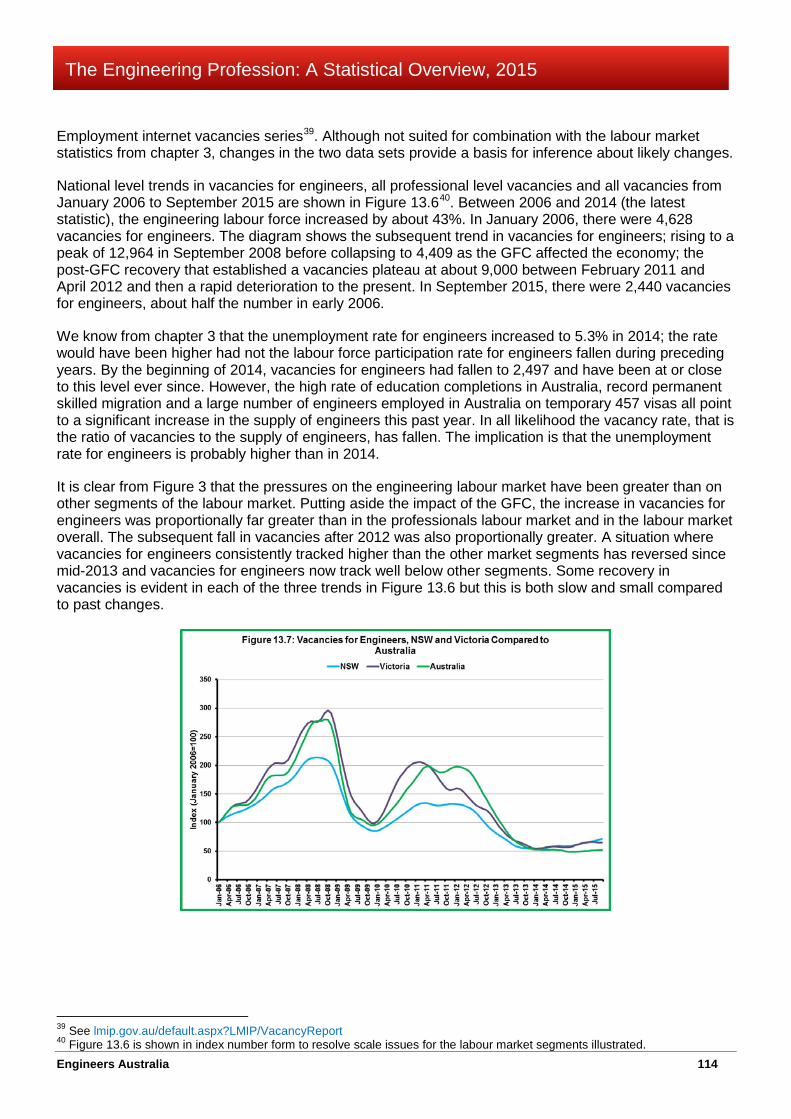

Main Points 107 13.1 The Need for Change Indicators 107 13.2 Trends in Engineering Construction 108 13.3 Vacancies for Engineers 113

Chapter 14 The Engineering Labour Market in 2015 115 Main Points 115 14.1 Assessing the Engineering Labour Market 115 14.2 Supply of Engineers 116 14.3 Demand for Engineers 116

Engineers Australia v

The Engineering Profession: A Statistical Overview, 2015

LIST OF TABLES Chapter 2

Table 2.1: The Engineering Labour Markets in 2006 and 2011 8 Table 2.2: Labour Force Participation in Australia 9

Chapter 3 Table 3.1: Employment Growth in Engineering Compared to Other Groups 18

Chapter 4 Table 4.1: Year 12 School Students, Australia 23 Table 4.2: Participation in Year 12 Science Subjects 24 Table 4.3: Participation in Year 12 Science Subjects 25

Chapter 5 Table 5.1: Domestic Students Commencing Engineering and Related

Technology Courses 33 Table 5.2: Overseas Students Commencing Engineering and Related

Technology Courses 33 Table 5.3: Students Commencing Engineering and Related Technology

Courses, by Country of Domicile 34 Table 5.4: Students Commencing Engineering and Related Technology

Courses, by Gender 34 Table 5.5: Domestic Students Enrolled in Engineering and Related

Technology Courses 35 Table 5.6: Overseas Students Enrolled in Engineering and Related

Technology Courses 35 Table 5.7: Students Enrolled in Engineering and Related Technology

Courses, by Country of Domicile 36 Table 5.8: Students Enrolled in Engineering and Related Technology

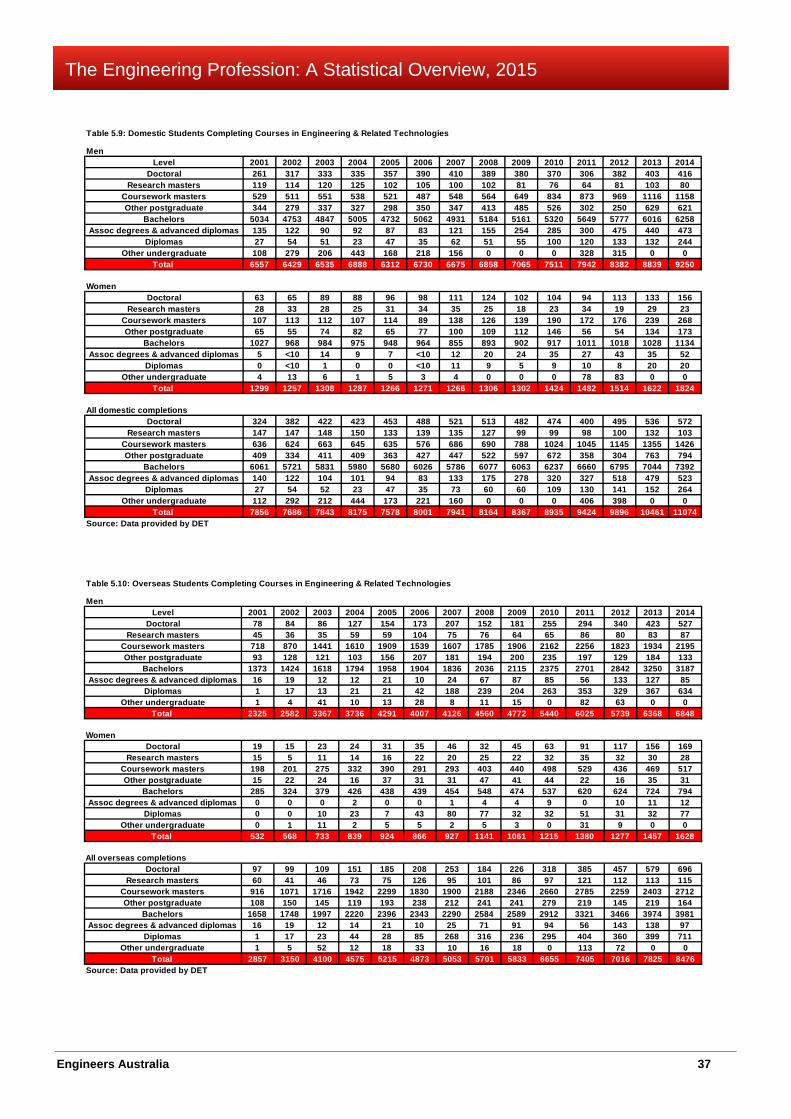

Courses, by Gender 36 Table 5.9: Domestic Students Completing Engineering and Related

Technology Courses 37 Table 5.10: Overseas Students Completing Engineering and Related

Technology Courses 37 Table 5.11: Students Completing Engineering and Related Technology

Courses, by Country of Domicile 38 Table 5.12: Students Completing Engineering and Related Technology

Courses, by Gender 38 Table 5.13: Annual Retention Rates for Bachelor Degree Students, in Engineering And in Institution 40

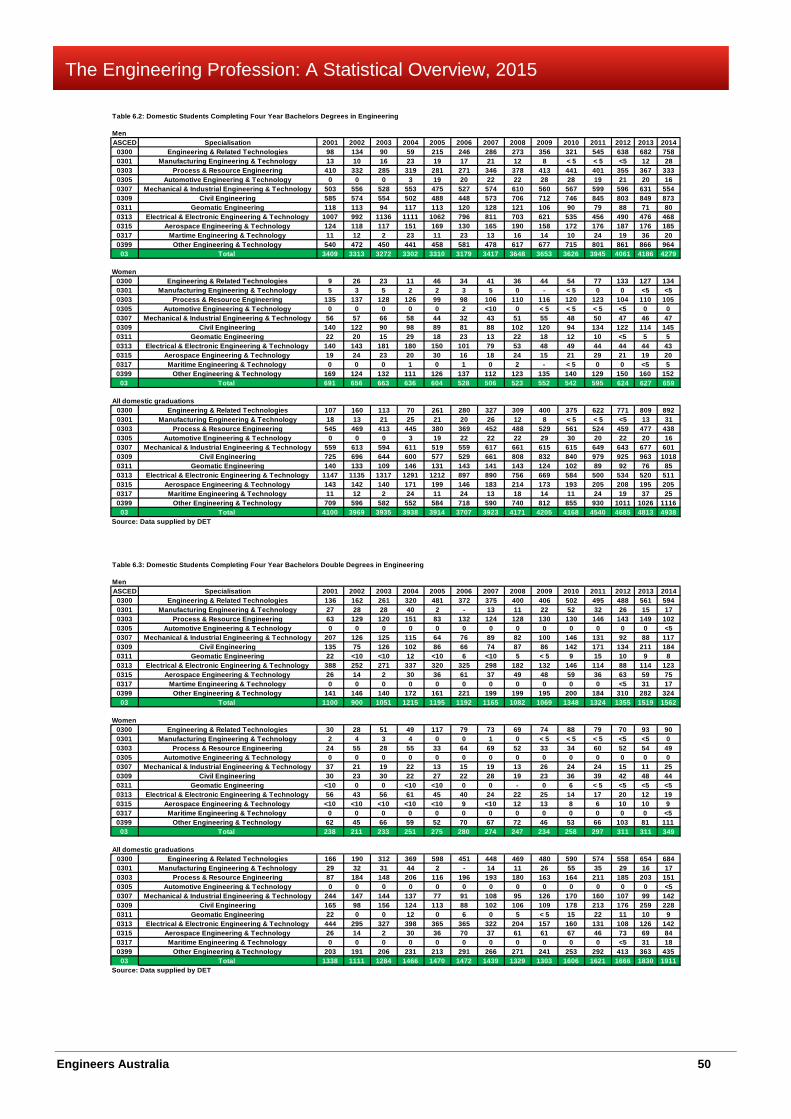

Chapter 6 Table 6.1 Domestic Students Completing Three Year Bachelors Degrees in Engineering 48 Table 6.2 Domestic Students Completing Four Year Bachelors Degrees in Engineering 50 Table 6.3 Domestic Students Completing Four Year Bachelor Double

Degrees in Engineering 50

Engineers Australia vi

The Engineering Profession: A Statistical Overview, 2015

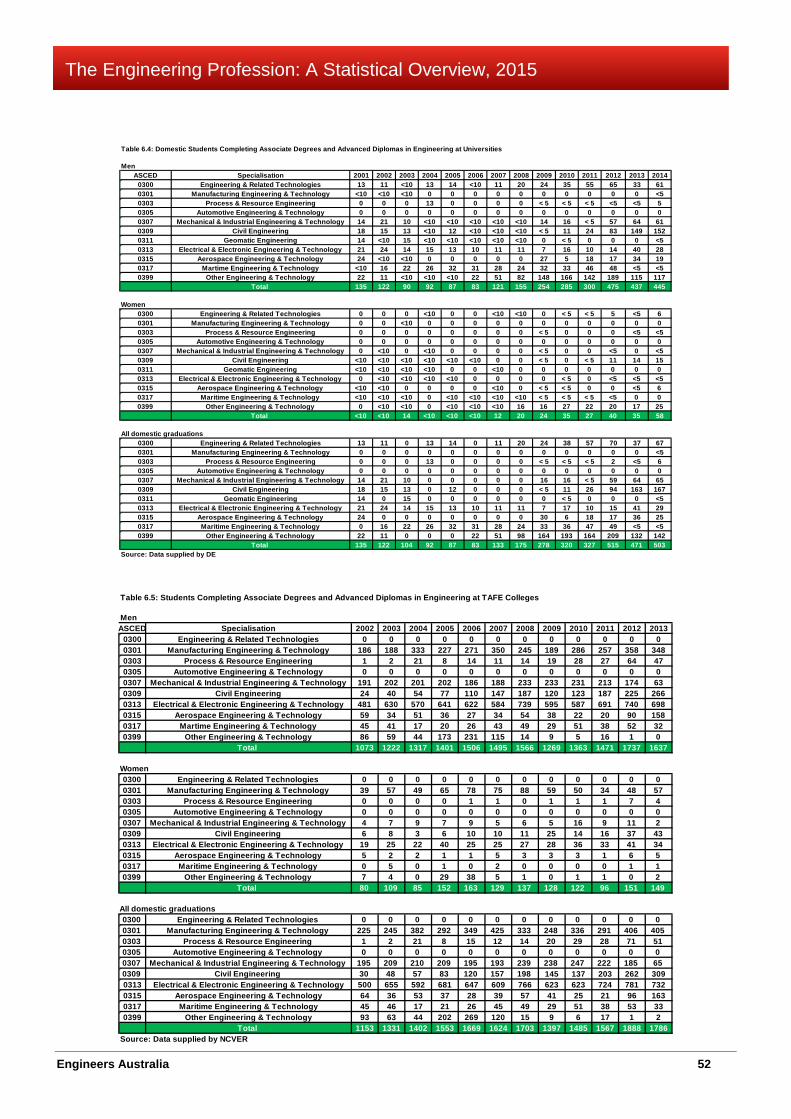

Table 6.4 Domestic Students Completing Associate Degrees and Advanced Diplomas in Engineering at Universities 52

Table 6.5 Completions of Associate Degrees and Advanced Diplomas in Engineering from Australian TAFE Colleges 52

Table 6.7 Changes in the Supply of Engineers as a Result of Domestic Course Completions 53

Chapter 7 Table 7.1 The Stock of Skilled Migrants Added to the Australian

Supply of Engineers 58 Table 7.2 New Permanent Migration Visas for Engineering Occupations 61 Table 7.3 Temporary 457 Visas Granted, Engineering Team 62 Table 7.4: Stock of 457 Visa Holders, Engineering Team 62 Table 7.5 New Temporary 457 Visas Granted, Australia, 2005-06 to 2014-15 64

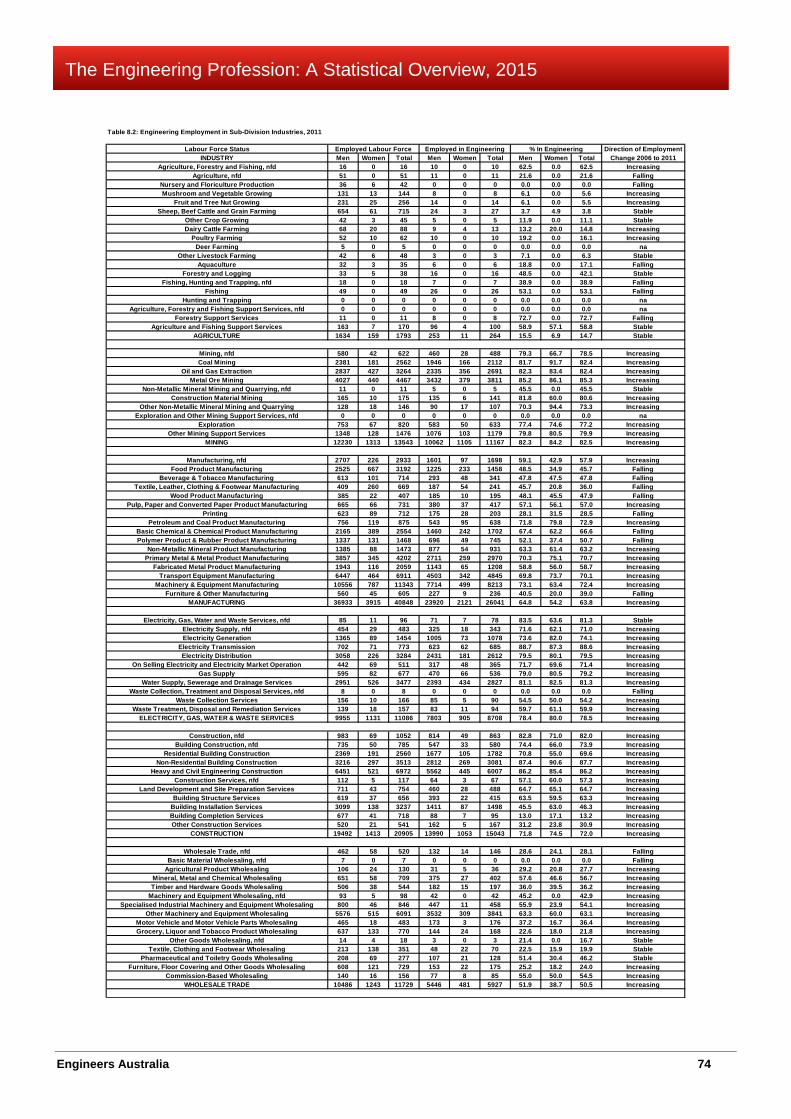

Chapter 8 Table 8.1 A Broad Look at Engineers in Australian Industry 66 Table 8.2: Engineering Employment in Sub-Division Industries 74

Chapter 9 Table 9.1: The Distribution of the Engineering Labour Force Throughout NSW, 2011 81 Table 9.2: The Distribution of the Engineering Labour Force throughout Victoria, 2011 82 Table 9.3: The Distribution of the Engineering Labour Force Throughout

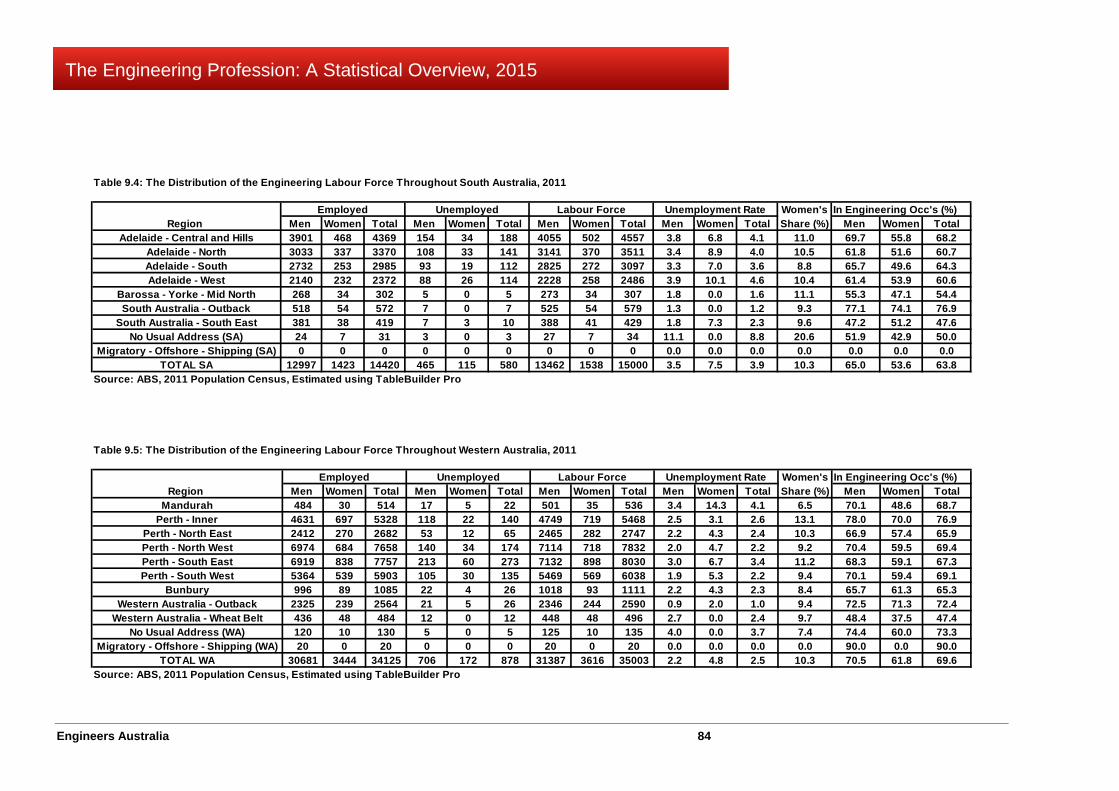

Queensland, 2011 83 Table 9.4: The Distribution of the Engineering Labour Force Throughout

South Australia, 2011 84 Table 9.5: The Distribution of the Engineering Labour Force Throughout

Western Australia, 2011 84 Table 9.6: The Distribution of the Engineering Labour Force Throughout

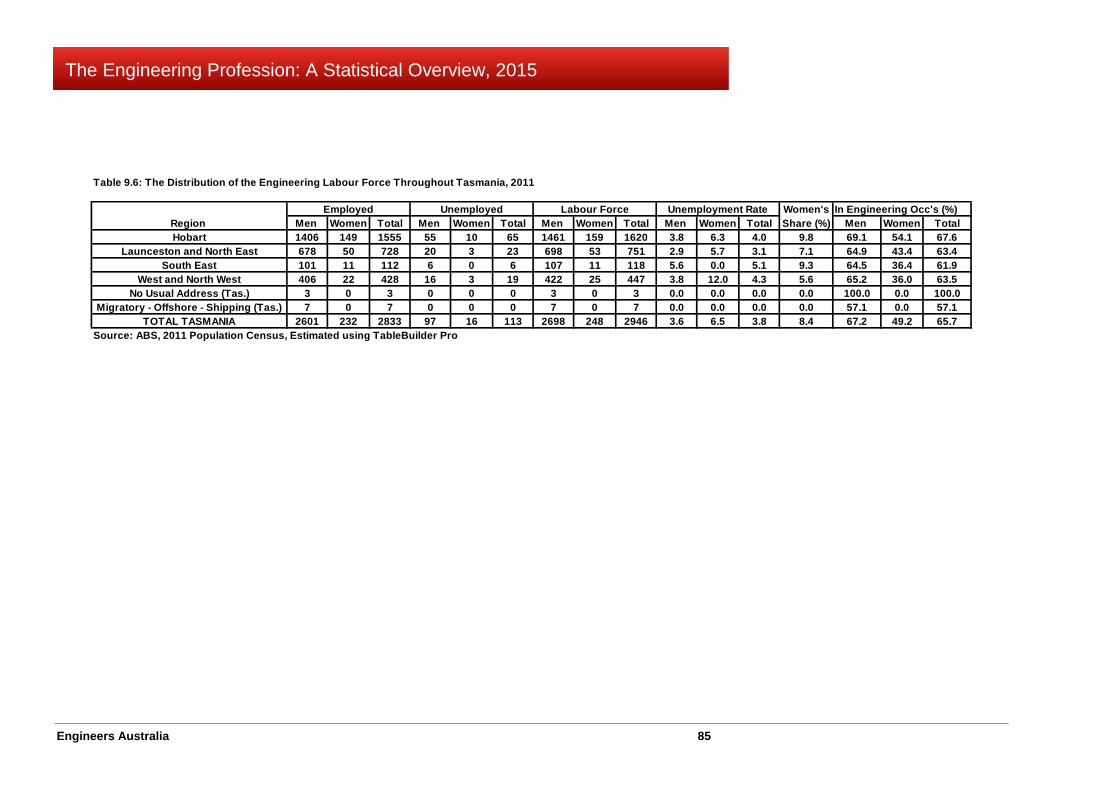

Tasmania, 2011 85

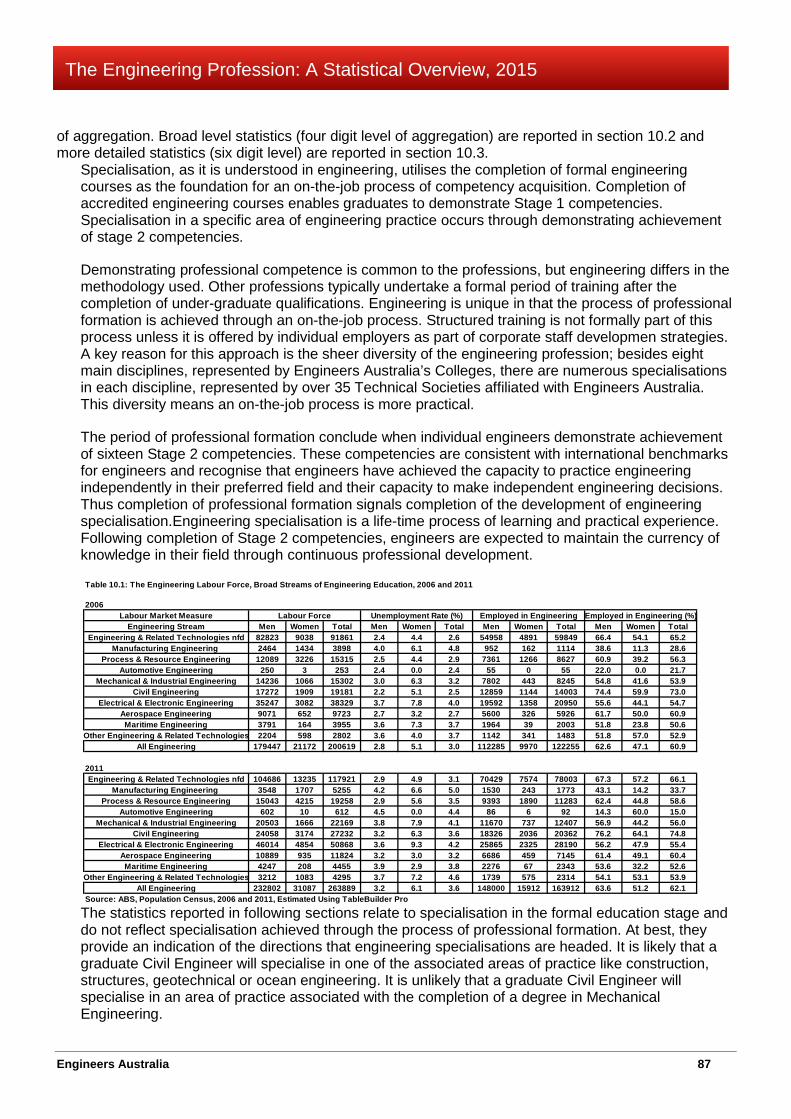

Chapter 10 Table 10.1: The Engineering Labour Force, Broad Streams of Engineering Education, 2006 and 2011 87 Table 10.2: The Engineering Labour Force, Detailed Streams of Engineering Education, 2006 90 Table 10.3: The Engineering Labour Force, Detailed Streams of Engineering Education, 2011 91

Chapter 11 Table 11.1 The Average Age of the Engineering Labour Force 93 Table 11.2 The Age Structure of the Engineering Labour Force, 2006 and 2011 93

Chapter 12 Table 12.1 Average Experience of Professional Engineers in the Private Sector 100 Table 12.2 Average Experience of Public Sector Professional Engineers 100 Table 12.3 Average Age of Private Sector Professional Engineers 102 Table 12.4 Average Age of Public Sector Professional Engineers 103

Engineers Australia vii

The Engineering Profession: A Statistical Overview, 2015

Table 12.5 Average Salary Packages for Professional Engineers in the Private Sector 104 Table 12.6 Average Salary Packages for Professional Engineers in the Public Sector 104 Table 12.8 Average Growth in Professional Engineer Salary Packages 106

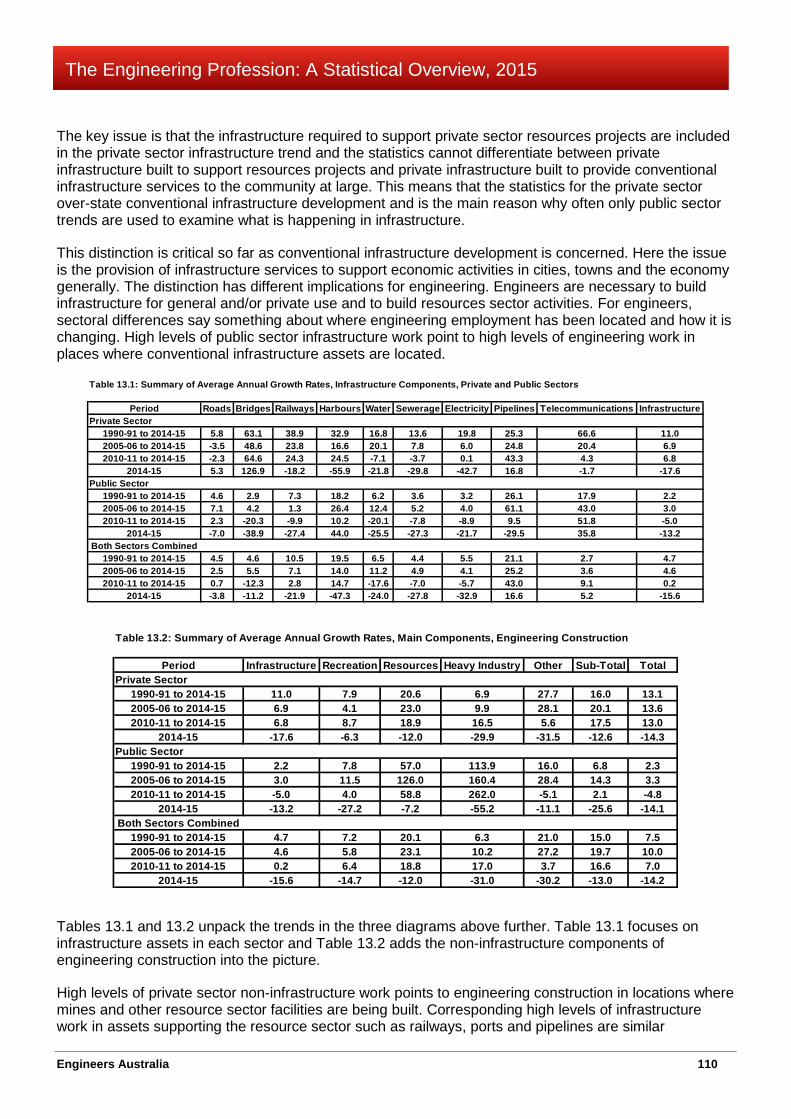

Chapter 13 Table 13.1: Summary of Average Growth Rates, Infrastructure Components, Private and Public Sectors 110 Table 13.2: Summary of Average Annual Growth Rates Main Components, Engineering Construction 110

Engineers Australia viii

The Engineering Profession: A Statistical Overview, 2015

LIST OF ILLUSTRATIONS Chapter 2 Figure 2.1: Overseas Qualified Engineers in 2011, Regions of Birth and Time of Arrival in Australia 12

Chapter 3 Figure 3.1: The Engineering population since 2001 15 Figure 3.2: Labour Force Participation of Engineers Compared to Other

Segments of the Labour Force 16 Figure 3.3: Labour Force Participation, Engineering Team

Compared to Period Average 17 Figure 3.4: Engineering Unemployment Rates Compared to Other Groups 19 Figure 3.5: The Relationship between the Supply of Engineers and

Employment in Engineering Occupations 20

Chapter 4 Figure 4.1: Participation Rates for Students Progressing From Year 10 to Year 12 23 Figure 4.2: Participation in Year 12 Physics and Chemistry Subjects 24 Figure 4.3: The Gender Shares in Year 12 Science and

Mathematics Subjects in 2012 26 Figure 4.4: The Basis for Admission to Bachelor Degrees, Domestic Students 27 Figure 4.5: The Basis for Admission to Bachelor Degrees, Overseas Students 27 Figure 4.6: Applications for, Offers Made and Acceptances of Places in University

Engineering Courses, 2001 to 2014 28 Figure 4.7: Offers Made by Universities by ATAR Scores, Engineering and Offers in Total, 2013 and 2014 28 Figure 4.8: Offers to Students with ATAR Scores Above 90 29

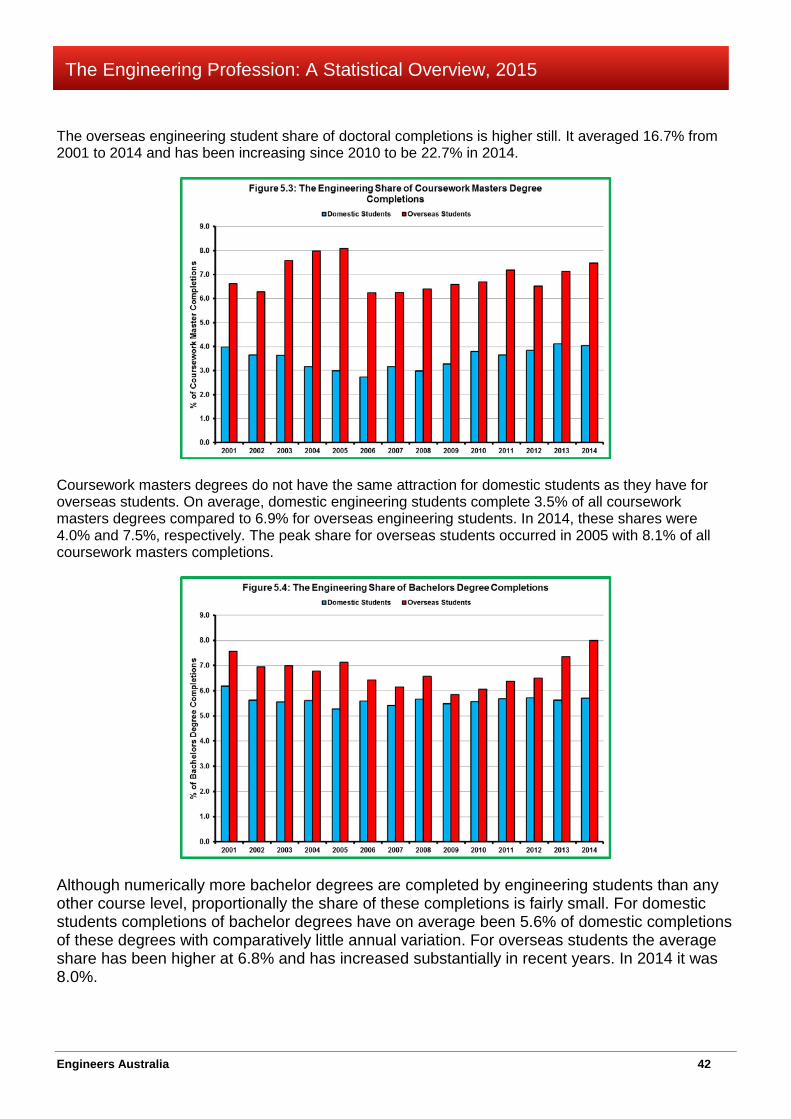

Chapter 5 Figure 5.1: Engineering Share of Total Course Completions 41 Figure 5.2: The Engineering Share of Doctoral Degree Completions 41 Figure 5.3: The Engineering Share of Coursework Masters Degree Completions 42 Figure 5.4: The Engineering Share Of Bachelors Degree Completions 42

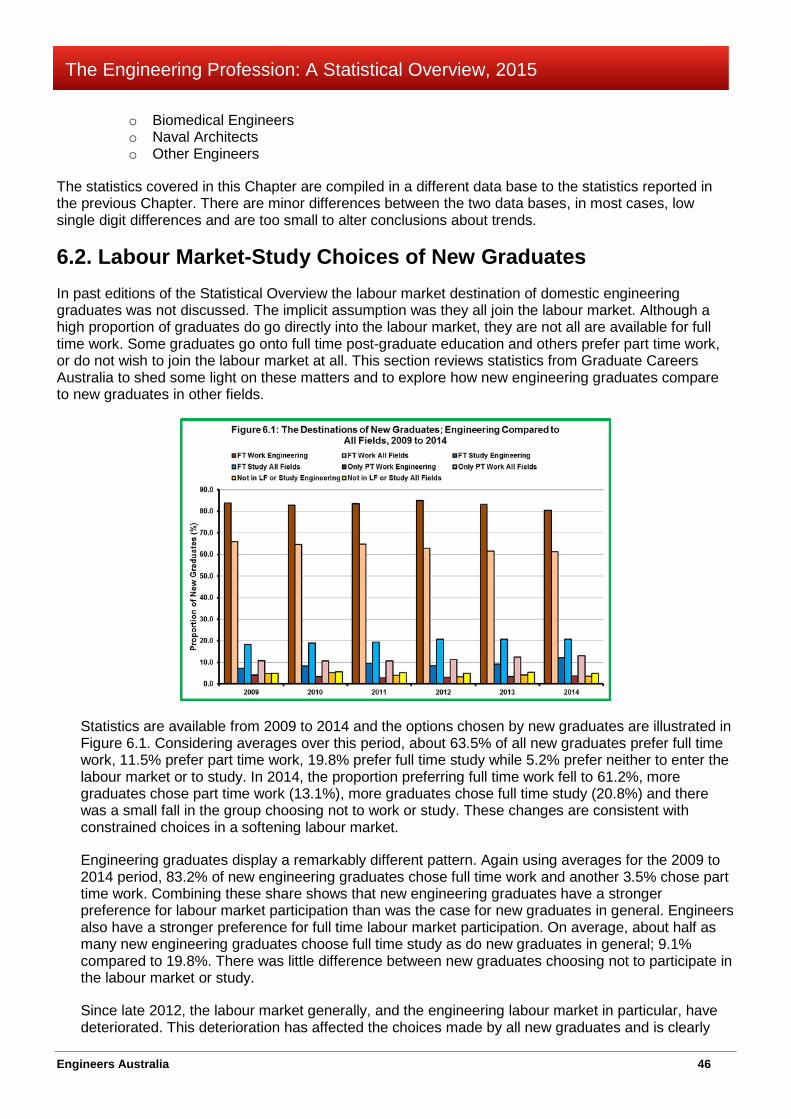

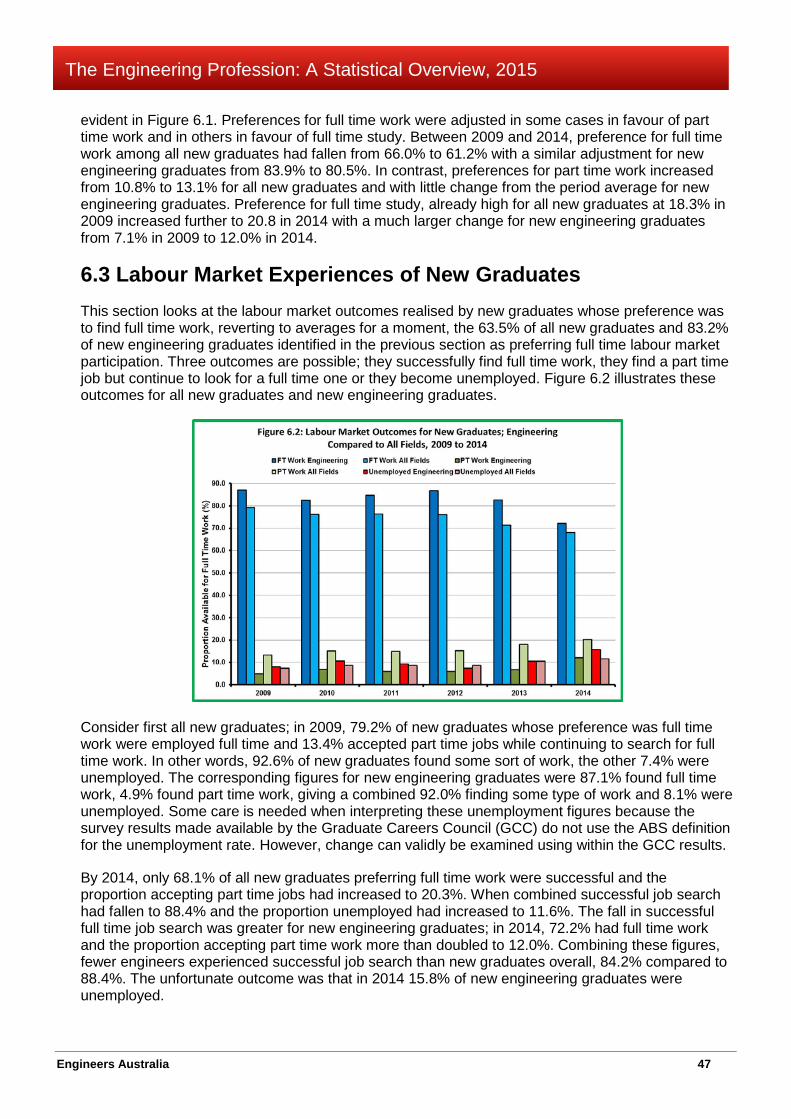

Chapter 6 Figure 6.1: The Destination of New Engineering Graduates Compared to New Graduates in General, 2009 to 2013 46 Figure 6.2: Labour Market Outcomes for New Graduates: Engineering Compared to All Fields, 2009 to 2014 47 Figure 6.3: Changes in the Potential Supply of Engineers from New Course Completions 54 Figure 6.4: The Proportion of Women in Course Completions 54

Engineers Australia ix

The Engineering Profession: A Statistical Overview, 2015

Chapter 7 Figure 7.1 Additions to the Supply of Engineers from Skilled Migration 59 Figure 7.2 The Impact of Skilled Migration on the Supply of Engineers 59 Figure 7.3 Permanent Visas Granted to Engineering Occupations 60 Figure 7.4 New 457 Visa Approvals by Jurisdiction 63 Figure 7.5 Trends in Temporary 457 Visa Engineers 63

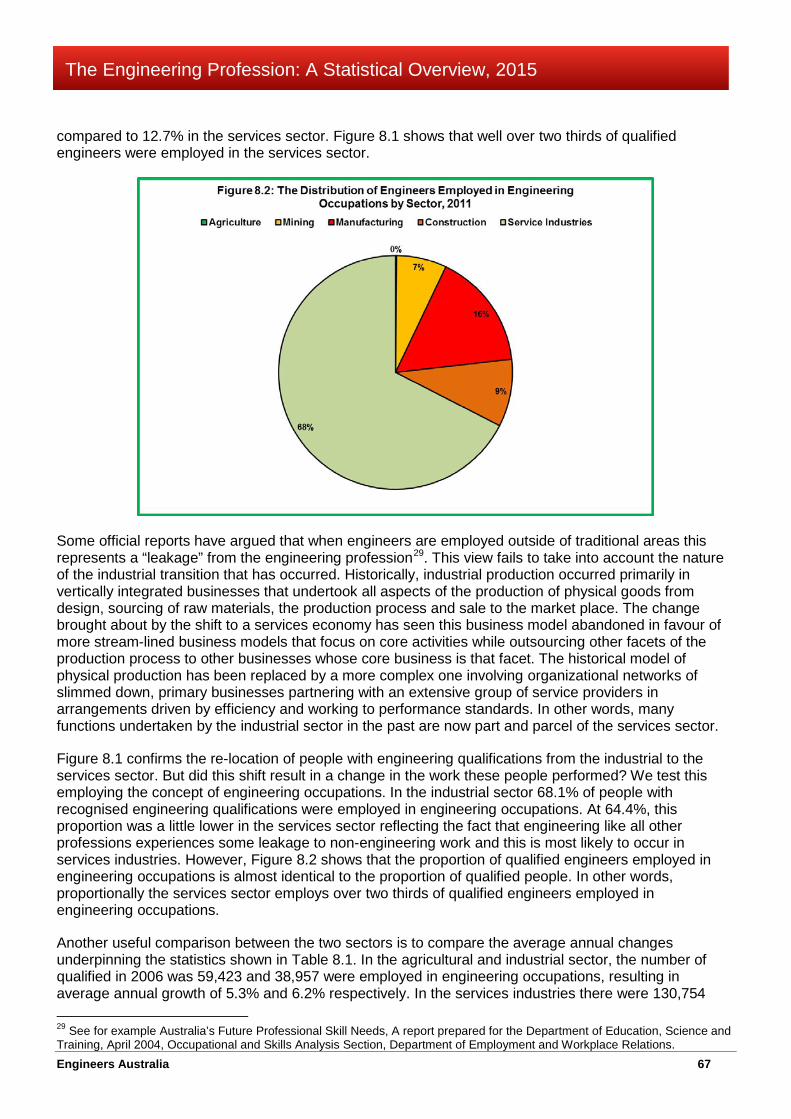

Chapter 8 Figure 8.1 The Distribution of Engineers by Industry Sector, 2011 66 Figure 8.2 The Distribution of Engineers Employed in Engineering Occupations by Sector, 2011 67

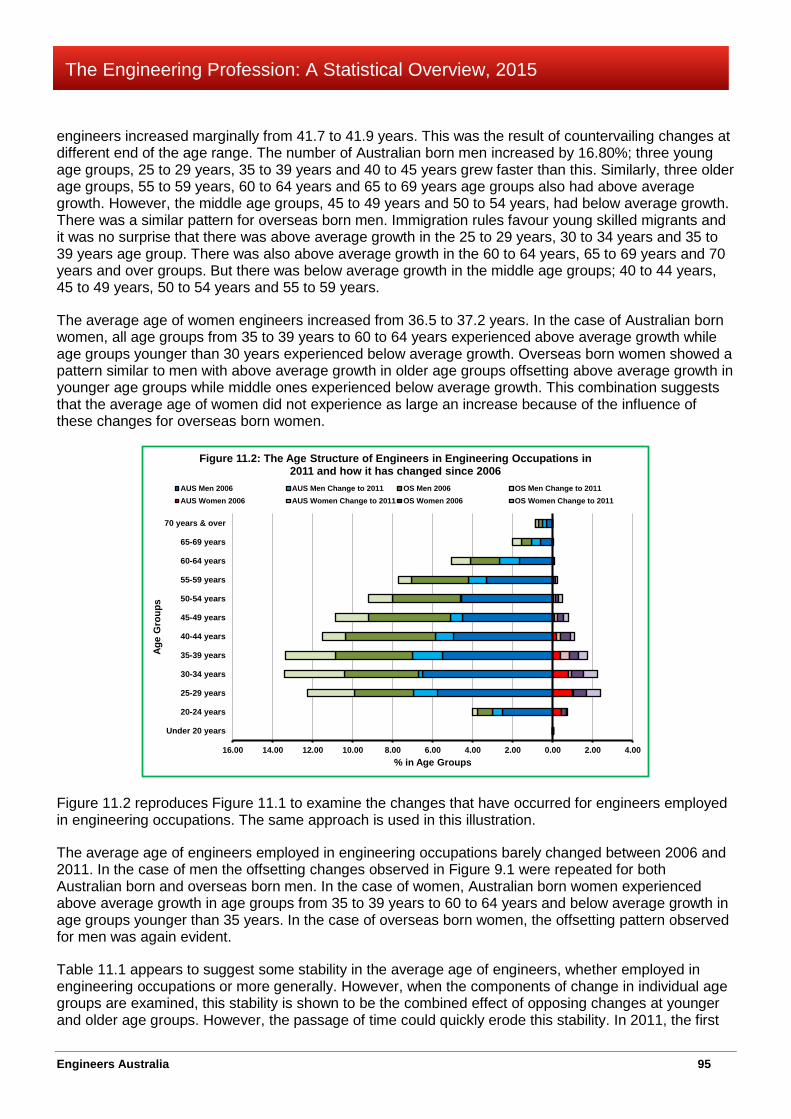

Chapter 11 Figure 11.1 The Age Structure of the Engineering Labour Force in 2011

And how it has changed since 2006 94 Figure 11.2 The Age Structure of Engineers in Engineering Occupations in 2011

And how it has changed since 2006 95 Figure 11.3 Labour Force Participation of Engineers and Age Structure 96 Figure 11.4 The Age Profile of Labour Force Participation in Engineering Compared to All Skilled Areas, 2011 97

Chapter 12 Figure 12.1 Comparing Average Work Experience of Professional Engineers in the Private and Public Sectors 100 Figure 12.2 Change in Average Experience Levels for Private Sector Professional Engineers 101 Figure 12.3 Change in Average Experience Levels for Public Sector Professional Engineers 101 Figure 12.4 Average Ages of Professional Engineers in the Private and Public Sectors 102 Figure 12.5 Average Ages of Professional Engineers in the Private Sector 103 Figure 12.6 Average Age of Professional Engineers in the Public Sector 103 Figure 12.7 Trends in Engineering Salary Packages, Private and Public Sectors 105

Chapter 13 Figure 13.1 Cumulative Private and Public Sector Engineering Construction, 1990-91 to 2014-15 109 Figure 13.2 Trends in the Main Components of Public Sector

Engineering Construction, 1990-91 to 2014-15 109 Figure 13.3 Trends in the Main Components of private Sector

Engineering Construction, 1990-91 to 2014-15 109 Figure 13.4 The Public Sector Engineering Construction Pipeline 111 Figure 13.5 The Private Sector Engineering Construction Pipeline 112 Figure 13.6 Vacancies for Engineers Compared to Professional and

All Vacancies, January 2006 to September 2015 113 Figure 13.7 Vacancies for Engineers, NSW and Victoria Compared to Australia 114 Figure 13.8 Vacancies for Engineers, Major resource States Compared to Australia 115 Figure 13.9 Vacancies for Engineers, SA Tasmania & Territories Compared to Australia 115

Engineers Australia 1

The Engineering Profession: A Statistical Overview, 2015

Chapter 1: Introduction

Main Points This Chapter describes the educational qualifications necessary to be part of the engineering team in Australia. The role of the Statistical Overview in piecing together fragmented labour market statistics on engineers and engineering is briefly explained as are key definitions used throughout the Report. This edition updates statistics on trends in education, skilled migration and the characteristics of engineers. Structural characteristics of the engineering labour force based on 2006 and 2011 census statistics are repeated from last year. New material in this edition is a time series analysis of the demand for and supply of engineers using statistics from the ABS Survey of Education and Work.

1.1: Engineers and Engineering Engineers and engineering are indispensable contributors to Australian prosperity and lifestyles. Engineering services are embodied in almost every good or service consumed or used by Australians, now and in the future. In this respect, engineers are the enablers of productivity growth through their role in converting “brilliant ideas” into new products, new processes and new services. Engineers also ensure that society gets the most out of existing facilities through optimising their operations and maintenance.

Fully competent engineers hold accredited academic credentials in engineering and have then satisfactorily completed a process of professional formation that bridges the gap between academic studies and engineering practice. The time necessary to become an engineer is very long, academic studies are specific and highly analytical and the skills of engineering practice are vital to successful outcomes for the individual and society.

Engineering is not homogeneous and there are numerous areas of engineering practice. To some degree specialisation begins with academic studies, for example, students can choose between degrees in mechanical engineering, civil engineering or electrical engineering. Most specialisation, however, takes place through on-the-job practice during professional formation, for example, a graduate with a degree in civil engineering can choose to practice as a structural engineer, a geotechnical engineer, a coastal engineer or as a civil engineer. More detail on engineering specialisations can be found at www.engineersaustralia.org.au/professional-development/what-engineering

Engineering skills and expertise are unique and other skills cannot substitute for them. When engineering decisions made by engineers are over-ruled by general managers, administrators, accountants, lawyers or politicians, outcomes will be problematic. This has become particularly evident in government procurement of infrastructure and/or highly technical equipment by agencies where engineering positions have been abolished and not replaced by arrangements with the technical competence to formulate engineering decisions and recommendations. There are a host of examples that demonstrate how such short term cost savings have resulted in damaging and expensive outcomes1.

In contrast, the training, skills and experience of engineers are transferable to many other fields of work where they are highly valued. As a consequence qualified engineers are employed in most occupations in the Australian economy, and only about 60% are employed in occupations closely related to engineering. The other 40% are employed in a range of other occupations where analytical and problem solving ability is required. This result means that retaining trained engineers in the profession is just as important as encouraging more people to study and complete engineering qualifications.

1 See for example www.anao.gov.au

Engineers Australia 2

The Engineering Profession: A Statistical Overview, 2015

1.2: Objective of the Statistical Overview Engineers Australia was formed to advance the science and practice of engineering for the benefit of the community. Engineers Australia sets and maintains professional standards for its members consistent with international benchmarks, encourages the development of engineering knowledge and competencies, facilitates the exchange of ideas and information and informs community leaders and decision makers about engineers and engineering issues.

This objective can best be achieved through the dissemination of factual information about engineers and about broader policy issues that involve engineering. The Statistical Overview contributes to these efforts by compiling statistics about engineers in Australia, how many of them practice their profession and where, and the circumstances of their work. The Statistical Overview fills a gap created by the fragmented nature of Australian statistics relating to specific professions.

At the macroeconomic level, high quality statistics to assist labour market policy decisions are available monthly. Unfortunately, Labour Force Survey statistics have not included educational attainment, an overwhelming difficulty when such qualifications are mandatory for entry to the profession. Some analysts have chosen to ignore these limitations and have used occupational breakdowns with no educational constraint2. These apples and oranges comparisons add little to satisfactory policy analysis.

The ABS has recognised this problem in recent revisions to the Labour Force Survey. From May 2015 statistics incorporating educational attainment will be available quarterly. This means that contemporary statistics for the engineering labour market that are directly comparable to the labour market as a whole will become available. Some delay,

The interests of Engineers Australia are best served by compiling statistics that represent the engineering profession as closely as possible and that begins by ensuring that those included in statistical counts are actually qualified to be considered part of the profession. This objective can be achieved, to varying degrees, by building on several sources of official statistics, and some unofficial sources, within the structures of well-known labour market definitions, employing as far as possible the statistical classifications of Australia’s official statistical agency the Australian Bureau of Statistics (ABS). The Statistical Overview has employed an incremental approach improving and refining statistics and adding new ones each edition. The framework for arranging statistics is a simple stock formulation; the opening stock plus additions less losses is the closing stock. The collection is far from complete and several important gaps remain, notably statistics on the retirement of older engineers. However, improvements continue to be made so that the Statistical Overview represents a comprehensive and consolidated collection of Australian statistics on engineers and engineering.

1.3: The Engineering Team In Australia the engineering profession is organised into the engineering team. The engineering team comprises Professional Engineers, Engineering Technologists and Engineering Associates. The three groups are differentiated by educational qualifications, which in conjunction with the process of professional formation undertaken, shape the engineer’s degree of conceptualisation and independent decision-making and so determine the complementarity between the groups in engineering practice. In detail, the roles of the three groups are:

Professional Engineers apply lifelong learning, critical perception and engineering judgment to the performance of engineering services. Professional Engineers challenge current thinking and conceptualise alternative approaches, often engaging in research and development of new engineering

2 See for example the Issues Paper released by the Australian Workplace and Productivity Agency (AWPA) in support of their study of the engineering labour force, www.awpa.gov.au/our-work/sector-specific-skill-needs/Pages?Engineering-workforce-study.aspx

Engineers Australia 3

The Engineering Profession: A Statistical Overview, 2015

principles, technologies and materials. Professional Engineers apply their analytical skills and well developed grasp of scientific principles and engineering theory to design original and novel solutions to complex problems. Professional Engineers exercise a disciplined and systematic approach to innovation and creativity, comprehension of risks and benefits and use informed professional judgment to select optimal solutions and to justify and defend these selections to clients, colleagues and the community. Professional Engineers require at least the equivalent of the competencies in a four year full time Bachelor’s Degrees in engineering.

Engineering Technologists exercise ingenuity, originality and understanding in adapting and applying technologies, developing related new technologies or applying scientific knowledge within their specialised environment. The education, expertise and analytical skills of Engineering Technologists equip them with a robust understanding of the theoretical and practical application of engineering and technical principles. Within their specialisation, Engineering Technologists contribute to the improvement of standards and codes of practise and the adaptation of established technologies to new situations. Engineering Technologists require at least the equivalent of the competencies in a three year full time Bachelor Degree in engineering.

Engineering Associates apply detailed knowledge of standards and codes of practice to selecting, specifying, installing, commissioning, monitoring, maintaining, repairing and modifying complex assets such as structures, plant, equipment, components and systems. The education, training and experience of Engineering Associates equip them with the necessary theoretical knowledge and analytical skills for testing, fault diagnosis and understanding the limitations of complex assets in familiar operating situations. Engineering Associates require at least the equivalent of the competencies in a two year full time Associate Degree in engineering or a two year full time Advanced Diploma in engineering from a university or TAFE college.

1.4 Competent Practicing Engineers Engineers Australia believes that formal qualifications in engineering are the first step towards becoming a competent practicing engineer. Demonstrating professional competence is a common feature of most professions, but in engineering professional formation is entirely an on-the-job process. An important reason for an on-the-job process is that specialisation in engineering primarily takes place when new graduates begin their practical careers. Engineers Australia recognises at least forty-five different fields of engineering practice. Many are indispensable in modern societies, yet involve relatively small numbers. This diversity means that formal course programs as conducted in some professions are impractical.

Successful completion of professional formation is recognised at two levels. To become competent practicing engineers, new graduates must satisfy six criteria:

• Hold accredited qualifications in engineering consistent with the engineering team.

• Undertaken professional formation for a period of up to five years under the supervision of a competent practising engineer.

• Accept and adhere to an approved code of ethics for the practice of engineering.

• Demonstrate that professional formation was acquired in a risk management environment that satisfies relevant Australian risk management standards and an understanding of these standards and how they apply to engineering practice.

• Fully appeciate the need for, and importance of, consumer protection and demonstrate that their practice is covered by one of six options for consumer protection.

Engineers Australia 4

The Engineering Profession: A Statistical Overview, 2015

Engineers Australia recognises highly experienced engineers by the conferring of Chartered Status. To become a Chartered Engineer, competent practicing engineers must additionally demonstrate that they satisfy sixteen competencies recognised and audited internationally in their field of expertise. Chartered engineers are acknowledged leaders in engineering practice. Many professions, like doctors, lawyers or accountants, are regulated by governments and practitioners are unable to operate unless registered. Registration in these cases verifies that individuals have the necessary educational qualifications, have satisfied the standards necessary to be admitted to practice adhere to an appropriate code of ethical conduct and are subject to legal sanction if they practice unethically or negligently. Similar registration provisions apply to common trades like plumbers and electricians. However, except for Queensland, Commonwealth, State and Territories Governments have decided that registration of engineers is not necessary and that self-regulation is preferred.

The voluntary regulation of standards for engineers is one of Engineers Australia’s most important functions. The framework is complex but covers the full range of matters relevant to engineering practice:

• Accreditation of university engineering courses consistent with competencies agreed and audited by the International Engineering Alliance.

• Arrangements for the recognition of competent practicing engineers a Professional Standards Scheme for engineers consistent with existing legislative provisions of Commonwealth, State and Territory governments.

• Arrangements for the conferring of Chartered Status for competent practicing engineers that demonstrate their leadership and engineering capacities against sixteen competencies agreed and audited by the International Engineering Alliance.

• Learned Society arrangements to lead and facilitate advancement of engineering knowledge and practice in numerous specialist fields.

• Arrangements which ensure all members reaffirm the Engineers Australia code of ethics each year when membership is renewed and arrangements for dealing with complaints against members regarding the code of ethics.

1.5: Data Sources and Caveats The three primary sources of official statistics used in the Statistical Overview are the Australian Bureau of Statistics (ABS), the Department of Education and Training (DET) and the Department of Immigration and Border Control (DIBC). The ABS is the official Australian statistical agency and as such is responsible for statistical classification systems and these are used by the other agencies mentioned. From time to time, ABS classification systems change and time delays in the adoption of new systems can cause differences between agencies. There are no such problems at present.

This apparent straight-forward situation does contain some inherent limitations. The most notable one being classification of individuals according to their highest qualification. Thus, a practicing engineer who holds an MBA as well a Bachelor degree in engineering is counted as belonging to the field of their highest qualification. There are numerous other minor issues that do not always accord with our preferences, but because classification systems deal with them consistently over time, any impact on trends is negligible.

The ABS is the source for census statistics covered in the Statistical Overview. These statistics are extracted by Engineers Australia using the ABS TableBuilder facility. The Department of Education and Training is the primary source for higher education statistics and the Department of Immigration and Border Control is the primary source for statistics on skilled migrants granted visas. Limited statistics on TAFE completions are extracted from the National Centre for Vocational Education Research (NCVER) Vocstats system.

Non-official statistics are sourced from a number of sources. For the last eight years, Engineers Australia has included several questions on recruiting difficulties experienced by engineering employers in an

Engineers Australia 5

The Engineering Profession: A Statistical Overview, 2015

annual salaries survey conducted by its subsidiary, Engineers Media. This survey is appropriate because survey respondents, HR managers and business principals, are likely to be better informed about recruiting difficulties than individual engineers. On the other hand, statistics on the characteristics of engineers are better reflected in statistics collected by Professions Australia whose survey respondents are individual engineers. Graduate Careers Council statistics are used to inform the progress of new engineering graduates. Unfortunately, these sources do not employ ABS classification systems making it difficult to compare statistics with official sources.

Engineering is a profession and not simply an occupation; how an engineer is qualified and what he/she does with acquired knowledge and expertise both are important. In common with every field of academic study, completion of engineering qualifications does not necessarily mean that an individual follows a career path closely associated with engineering. The Statistical Overview employs two distinct measures to differentiate between people who have engineering qualifications essential for inclusion in the engineering team and those members of this group who choose employment in engineering.

• The first measure is the conventional economists definition of the labour force constrained to engineering, in other words, the engineering labour force comprises all people with recognised engineering qualifications who are actively engaged in the labour market by being employed or if unemployed, actively seeking work. The engineering labour force is also called the supply of qualified engineers.

• The second measure is based on research by Engineers Australia which identified 52 of 358 four-digit ANZSCO occupations as engineering occupations3. These occupations are not constrained by narrow occupational nomenclature but recognise the wide range of work that engineers are engaged in and recognise the range of occupations that engineers move in typical careers. This measure is the number of qualified engineers retained in work closely related to engineering.

Differentiating between these measures has important policy implications. At one level, encouraging more young people to study and complete recognised engineering qualifications is an important aspect of increasing the supply of qualified engineers. However, when skill shortages occur from time to time, the problem is not just a shortage of qualified engineers, the number of engineers retained in engineering work can be just as, and sometimes more, important.

1.6: What’s New in this Edition? As has been the case in past Editions, a wide range of statistics on engineers and engineering are updated as far as possible. This includes statistics on engineering education including the preparatory stages, skilled migration, experience levels, salary packages and average ages. Statistics obtained from the Graduate Careers Council are also updated. Statistics obtained from the 2006 and 2011 censuses are reproduced, sometimes in restructured form.

One of the disadvantages of census statistics is that with the passage of time they lose contemporary relevance as indicators of labour market circumstances. Since the 2011 census, demand for engineers briefly spiked after the GFC and then collapsed. Although trends in vacancy statistics demonstrate this behaviour, conventional measures of employment, labour supply and unemployment are more useful. Chapter 3 describes the application of ABS statistics from the Survey of Education and Work for this purpose. In time this approach will become unnecessary because the ABS has amended the Labour Force Survey to include educational attainment, a key factor to extend this survey to cover professional groups. However, statistics will need to be accumulated for a few years to be useful.

Other new statistics include statistics on year 12 enrolments in science and mathematics subjects, statistics from the Graduate Careers Council on the pathways chosen by new graduates, including further full time studies and participation in the labour market. Census statistics on the industry

3 Engineers Australia, The Engineering Profession in Australia; A Profile from the 2006 Population Census, September 2010, www.engineersaustralia.org.au

Engineers Australia 6

The Engineering Profession: A Statistical Overview, 2015

distribution of engineers has been redesigned to draw out how engineers fit into the characterisation of Australia as a services economy. For the first time, statistics on the stock of 457 temporary visa holders in Australia are reported as well as statistics on new 457 visas approved significantly improving understanding of the link between skilled migration and the supply of engineers. This year, the Engineering Recruitment Difficulties Survey has been discontinued.

An important change is the approach used in Chapter 13 and 14 to assess the status of the engineering labour market in 2015. As before engineering construction and vacancies are used as indicators of change. The precision is the use of engineering construction has been improved and the Beveridge curve used to underpin interpretation of vacancies trends. Vacancies trends are linked to the time series labour force statistics in chapter 3.

Engineers Australia 7

The Engineering Profession: A Statistical Overview, 2015

Chapter 2: Structural Features of the Labour Market Main Points This Chapter reviews some important structural features of the engineering labour market based on comparisons between 2006 and 2011 census statistics.

Labour force participation for the engineering team is high, but not markedly different from other skills areas where the same levels of qualifications are required. The key difference is that more engineers work full time and fewer work part time than other skilled workers and the labour force as a whole. From the perspective of hours worked these points suggest that labour force participation is particularly high in engineering.

The participation of women in engineering remains very low compared to other skills and the labour force as a whole. This is despite quite high growth in the supply of women engineers.

Contrary to many perceptions, people who have engineering qualifications do not all pursue careers in engineering. Many find employment in the skilled labour force and apply acquired analytical and problem solving skills to more general problems instead of engineering problems. This observation changes how we should view skills shortages as far as engineers are concerned. When shortages occur the problem is not necessarily solved by increasing the number of people with engineering qualifications irrespective of whether they are sourced from Australian universities and colleges or from skilled migration. Retention of qualified people in engineering is the issue and requires entirely different policies.

Retention of qualified engineers in engineering varies by gender and ethnicity. Fewer women than men employ engineering qualifications in engineering and fewer skilled migrants than Australian born engineers employ their engineering qualifications in engineering. The proportion of skilled migrants retained in engineering is particularly low.

Engineering in Australia has become excessively dependent on skilled migration. This was the case prior to 2006, but by 2011 the overseas born component of the profession grew to a majority 53.9% because over 70% of the increase in supply was from skilled migration. In comparison, in 2011 38.4% of the skilled workforce was overseas born as was 27.7% of the overall labour force.

Consistent with the overall migration intake, the source countries for Australia’s intakes of skilled migrant engineers has changed. Migrant engineers come to Australia from most regions of the world. Traditional source countries in North Western Europe remain important but their shares have fallen. In recent years the largest intakes have been from countries in the Southern and Central Asian region. There are increasing numbers of engineers coming from the Americas.

2.1 Key Information The key statistics that describe the engineering labour force and population in 2006 and 2011 are shown in Table 2.1. These statistics were compiled from the ABS 2006 and 2011 censuses data bases using the ABS TableBuilder facility.

In 2011, 322,523 Australians held engineering qualifications consistent with the engineering team; 263,890 actively participated in the labour market with 254,515 being employed and 9,375 being unemployed but actively looking for work. The remainder, 58,633, were not active in the labour market. The majority of these people were retired from the labour market with 69.4% aged 55 years or more. This proportion was even higher for men with 77.8% aged 55 years or more. However, the largest group

Engineers Australia 8

The Engineering Profession: A Statistical Overview, 2015

of women not in the labour force, 42.2%, were aged from 25 to 39 years, often regarded as child rearing years.

There are a number of features of Table 2.1 that warrant comment. Most of these have shown little change over the period shown in the Table and it is likely that any change since 2011 has been minor. Some features not covered by Table 2.1 are also covered. The years between 2006 and 2011 covered the height of the resources boom which had profound effects on the engineering labour market. The resources boom has now transition from the construction of extraction, processing and transportation facilities to the production and sale of resources. Far fewer engineers are needed in this phase and combined with a pronounced slow down in infrastructure development and construction generally has led to a collapse in the demand for engineers which cannot be captured using 2011 census statistics. A more detailed examination of changes in the engineering labour market is left until Chapter 3.

2.2 Labour Force Participation In Australia, engineering is part of the generalisation that more educated people have higher labour force participation. This is demonstrated in Table 2.2 which compares engineering to other skilled groups4 and the general labour force. Labour force participation in engineering is comparable to participation in other skills and participation in both groups is about twenty percentage points higher than in the labour force as a whole. The labour force participation of skilled women whether in engineering or other areas is about ten percentage points lower than for men, a point in common with the overall labour force.

4 When engineering is compared to other skills, qualifications of a level comparable to the engineering team are assumed, that is, at least an associate degree or an advanced diploma.

Table 2.1: The Engineering Labour Markets in the 2006 and 2011 Censuses

2006 CensusLabour force

status Men Women Total Men Women Total Men Women TotalEmployed FT 79915 5794 85709 68051 8365 76416 147966 14159 162125Employed PT 9041 1954 10995 9864 2830 12694 18905 4784 23689

Employed away 4323 558 4881 3297 578 3875 7620 1136 8756TOTAL EMPLOYED 93279 8306 101585 81212 11773 92985 174491 20079 194570

Unemployed (FT) 1309 108 1417 2421 499 2920 3730 607 4337Unemployed (PT) 330 87 417 897 394 1291 1227 481 1708

TOTAL UNEMPLOYED 1639 195 1834 3318 893 4211 4957 1088 6045LABOUR FORCE 94918 8501 103419 84530 12666 97196 179448 21167 200615

Not in labour force 18871 2107 20978 19021 5017 24038 37892 7124 45016ENGINEERING POPULATION 113789 10608 124397 103551 17683 121234 217340 28291 245631

Participation Rate (%) 83.4 80.1 83.1 81.6 71.6 80.2 82.6 74.8 81.7Unemployment Rate (%) 1.7 2.3 1.8 3.9 7.1 4.3 2.8 5.1 3.0

Employed in Engineering 65973 4970 70943 46313 5002 51315 112286 9972 122258% in Engineering 69.5 58.5 68.6 54.8 39.5 52.8 62.6 47.1 60.9

2011 CensusEmployed FT 92614 6785 99399 98910 13214 112124 191524 19999 211523Employed PT 11103 2807 13910 13772 4651 18423 24875 7458 32333

Employed away 4776 794 5570 4148 941 5089 8924 1735 10659TOTAL EMPLOYED 108493 10386 118879 116830 18806 135636 225323 29192 254515

Unemployed (FT) 1888 156 2044 3815 1001 4816 5703 1157 6860Unemployed (PT) 485 120 605 1291 619 1910 1776 739 2515

TOTAL UNEMPLOYED 2373 276 2649 5106 1620 6726 7479 1896 9375LABOUR FORCE 110866 10662 121528 121936 20426 142362 232802 31088 263890

Not in labour force 22867 2476 25343 25418 7872 33290 48285 10348 58633ENGINEERING POPULATION 133733 13138 146871 147354 28298 175652 281087 41436 322523

Participation Rate (%) 82.9 81.2 82.7 82.8 72.2 81.0 82.8 75.0 81.8Unemployment Rate (%) 2.1 2.6 2.2 4.2 7.9 4.7 3.2 6.1 3.6

Employed in Engineering 78290 6636 84926 69710 9276 78986 148000 15912 163912% in Engineering 70.6 62.2 69.9 57.2 45.4 55.5 63.6 51.2 62.1

Source: Compiled using the ABS TableBuilder Pro Facility

Australian Born Overseas Born Engineering Team

Engineers Australia 9

The Engineering Profession: A Statistical Overview, 2015

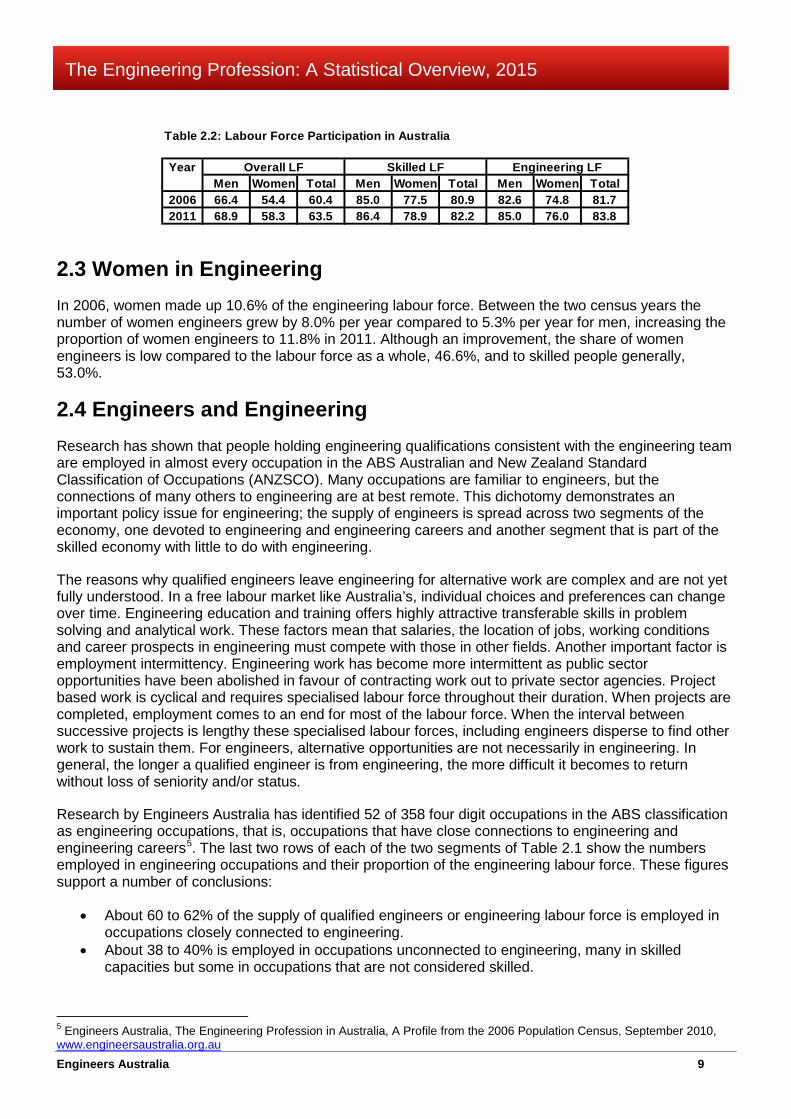

2.3 Women in Engineering In 2006, women made up 10.6% of the engineering labour force. Between the two census years the number of women engineers grew by 8.0% per year compared to 5.3% per year for men, increasing the proportion of women engineers to 11.8% in 2011. Although an improvement, the share of women engineers is low compared to the labour force as a whole, 46.6%, and to skilled people generally, 53.0%.

2.4 Engineers and Engineering Research has shown that people holding engineering qualifications consistent with the engineering team are employed in almost every occupation in the ABS Australian and New Zealand Standard Classification of Occupations (ANZSCO). Many occupations are familiar to engineers, but the connections of many others to engineering are at best remote. This dichotomy demonstrates an important policy issue for engineering; the supply of engineers is spread across two segments of the economy, one devoted to engineering and engineering careers and another segment that is part of the skilled economy with little to do with engineering.

The reasons why qualified engineers leave engineering for alternative work are complex and are not yet fully understood. In a free labour market like Australia’s, individual choices and preferences can change over time. Engineering education and training offers highly attractive transferable skills in problem solving and analytical work. These factors mean that salaries, the location of jobs, working conditions and career prospects in engineering must compete with those in other fields. Another important factor is employment intermittency. Engineering work has become more intermittent as public sector opportunities have been abolished in favour of contracting work out to private sector agencies. Project based work is cyclical and requires specialised labour force throughout their duration. When projects are completed, employment comes to an end for most of the labour force. When the interval between successive projects is lengthy these specialised labour forces, including engineers disperse to find other work to sustain them. For engineers, alternative opportunities are not necessarily in engineering. In general, the longer a qualified engineer is from engineering, the more difficult it becomes to return without loss of seniority and/or status.

Research by Engineers Australia has identified 52 of 358 four digit occupations in the ABS classification as engineering occupations, that is, occupations that have close connections to engineering and engineering careers5. The last two rows of each of the two segments of Table 2.1 show the numbers employed in engineering occupations and their proportion of the engineering labour force. These figures support a number of conclusions:

• About 60 to 62% of the supply of qualified engineers or engineering labour force is employed in occupations closely connected to engineering.

• About 38 to 40% is employed in occupations unconnected to engineering, many in skilled capacities but some in occupations that are not considered skilled.

5 Engineers Australia, The Engineering Profession in Australia, A Profile from the 2006 Population Census, September 2010, www.engineersaustralia.org.au

Table 2.2: Labour Force Participation in Australia

YearMen Women Total Men Women Total Men Women Total

2006 66.4 54.4 60.4 85.0 77.5 80.9 82.6 74.8 81.72011 68.9 58.3 63.5 86.4 78.9 82.2 85.0 76.0 83.8

Overall LF Skilled LF Engineering LF

Engineers Australia 10

The Engineering Profession: A Statistical Overview, 2015

• The proportion of qualified engineers retained in engineering related occupations depends on gender and ethnicity. Fewer women are retained in engineering than men and fewer overseas born qualified engineers are retained in engineering than Australian born.

2.5 Changes in Demand and Supply Both the supply of, and demand for engineers grew strongly between 2006 and 2011. Table 2.1 shows that the supply of engineers increased by 63,275 or 31.5% from 200,615 to 263,890. This change was equivalent to average annual compound growth of 5.6%. The change in demand for engineers was slightly less; 59,945 or 30.8% increasing demand from 194,570 to 254,515. This was equivalent to average annual growth of 5.5%.

During these years annual growth in the demand for engineers was stronger than for the demand for skilled workers6 and overall employment. Average annual growth in demand for skilled workers was 4.6% and despite the buoyant conditions of the time, total employment grew less than half as fast, increasing by 2.0% per year.

This was not the full story. Demand for engineers in engineering occupations grew by an average 6.0% per year. Combined with differential location, industries and experience and areas of engineering practice, this higher growth in demand for engineers to work in engineering gave rise to the skill shortages experienced at the time.

2.6 Engineering is Dependent on Skilled Migration The majority of the engineering labour market has now been born overseas. In 2006, the overseas born segment of the engineering labour force was 48.4% and the Australian born segment was 51.6%. By 2011, this had changed to 53.9% for the overseas born segment and 46.1% for the Australian born segment. The reason for this change was that in recent years most of the increase in the supply of engineers was from overseas:

• Between 2006 and 2011, the supply of engineers increased by 63,275 with average growth of 5.6% per year.

• The supply of overseas born men grew by 7.6% per year and contributed 59.1% of the increase. • The supply of overseas born women grew by 10.0% per year and contributed 12.3% of the

increase. • In contrast, the supply of Australian born engineers grew much slower, by 3.2% per year for men

and 3.4% per year for women and contributed 28.6% of the increase.

In contrast, the overseas born segment of the skilled labour force in 2011 was 38.4% and in the overall labour force it was 27.7%. Although skilled migration is the largest component of Australia’s annual migration intake, the annual intake of migrant engineers grew rapidly throughout the construction phase of the resources boom and as we shall see in a later Chapter, the numbers of permanent migrant engineers have continued even though it has been widely acknowledged that the resources sector has transitioned from construction to production. Fewer engineers are required at this stage.

2.7 Diversity and Labour Market Experience The labour market experience of groups within the engineering labour force varies markedly.

Retention in Engineering

The previous Section pointed out that retention in engineering occupations, that is employment in occupations closely related to engineering, is higher for men than for women and higher for Australian 6 As measured by the demand for people with qualifications whose level is equivalent to those of the engineering team across all areas of skill.

Engineers Australia 11

The Engineering Profession: A Statistical Overview, 2015

born than overseas born qualified engineers. In 2011, the highest retention is for Australian born men 70.6% of whom are employed in occupations close to engineering and the lowest retention is for overseas born women of whom 45.4% are employed in occupations close to engineering.

Unemployment

Unemployment has been higher for women than men qualified engineers irrespective of ethnicity. However, this gap is magnified for overseas born women whose unemployment rates have been almost double that of overseas born men and twice as high as for Australian born women. In 2011, the lowest unemployment rate was 2.1% for Australian born men and the highest was 7.9% for overseas born women. It is important to note that in 2011 the engineering labour market was experiencing high levels of demand.

Full Time and Part Time Work

A feature of engineering is the high proportion of qualified engineers employed full time. The ABS defines full time work as working 35 hours or more per week. In 2011, 86.7% of qualified engineers worked full time compared to 72.3% for all skilled employees and 67.5% for employees in general. Conversely, fewer qualified engineers work part time. The corresponding comparison of part time employees in 2011 was 13.3% for engineers, 27.7% for all skilled employees and 32.5% for employees overall. The majority of these differences are explained by gender; proportionally, more women work part than men; 27.2% in engineering, 38.8% in all skilled areas and 47.5% in overall employment. An interesting point is that while the proportion of women engineers working part time is higher than the proportion of men, numerically there were almost three times as many men employed part time than women.

When the high proportion of full time employment in engineering is combined with the high labour force participation rates previously noted, total hours worked by engineers is on average higher than for the two other groups used for comparison.

Economic Sectors

Most of the increase in engineering employment has been in the private sector. This sector increased its share of engineering employment from 83.1% in 2006 to 84.3% in 2011. The share of engineering employment in the national government sector fell from 7.6% to 6.3% in 2011. There was a small increase in the proportion of State government employment from 7.2% to 7.4% in 2011 and a fall in the proportion of engineers employed in local government from 2.1% to 1.9% in 2011.

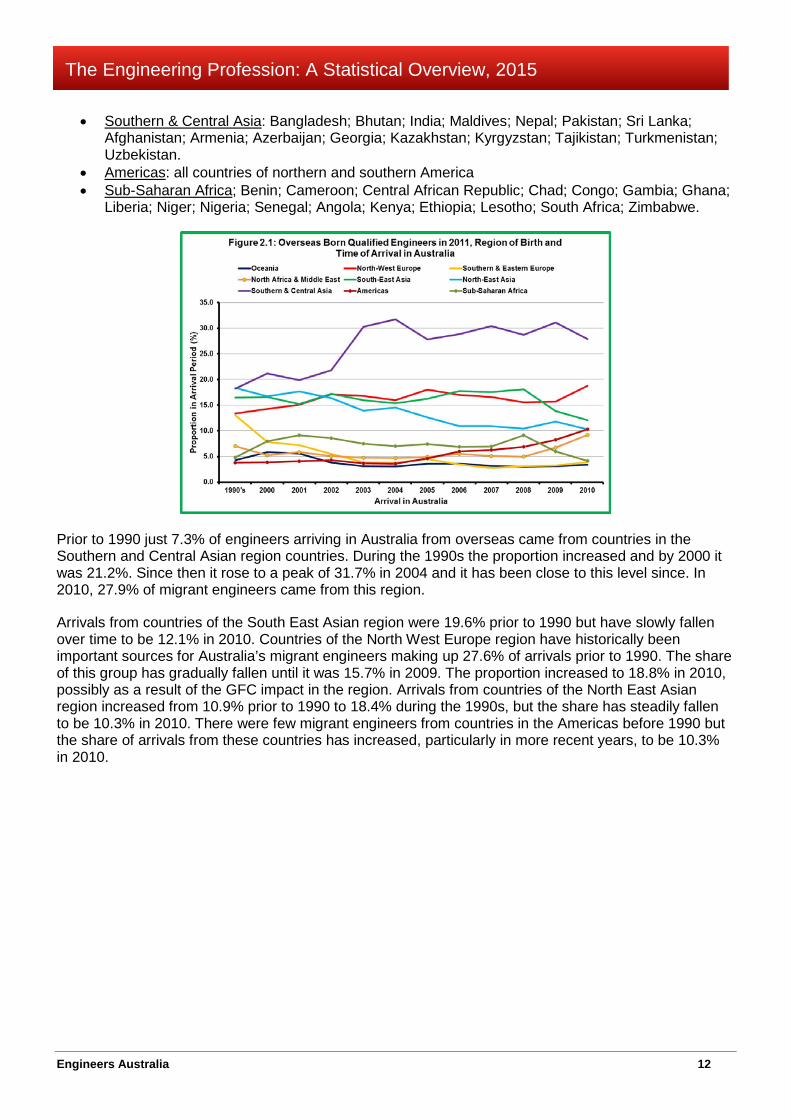

2.8 The Source of Migrant Engineers Since the turn of the century the sources of Australia’s migrant engineers has changed. This is illustrated in Figure 2.1 which shows how long ago the overseas born engineers in Australia in 2011 arrived and their global home regions.

The main countries in each region are as follows: • Oceania and Antarctica: New Zealand and Pacific Island countries • North-West Europe: United Kingdom; Ireland; Austria; Belgium; France; Germany; Netherlands;

Switzerland; Scandinavian countries. • Southern and Eastern Europe: Italy; Malta; Portugal; Spain; Albania; Balkan countries; Greece;

Romania; Ukraine; Belarus; Hungary; Russia; Latvia; Lithuania; Czech Republic. • North Africa & Middle East: Algeria; Egypt; Libya; Morocco; Sudan; Tunisia; Bahrain; Iran; Iraq;

Israel; Jordan; Kuwait; Lebanon; Oman; Qatar Saudi Arabia; UAE; Turkey; Yemen. • South East Asia: Burma; Cambodia; Laos; Thailand; Vietnam; Brunei; Indonesia; Malaysia;

Philippines; Singapore; Timor-Leste. • North East Asia: China; Hong Kong; Macau; Mongolia; Japan; both Koreas.

Engineers Australia 12

The Engineering Profession: A Statistical Overview, 2015

• Southern & Central Asia: Bangladesh; Bhutan; India; Maldives; Nepal; Pakistan; Sri Lanka; Afghanistan; Armenia; Azerbaijan; Georgia; Kazakhstan; Kyrgyzstan; Tajikistan; Turkmenistan; Uzbekistan.

• Americas: all countries of northern and southern America • Sub-Saharan Africa; Benin; Cameroon; Central African Republic; Chad; Congo; Gambia; Ghana;

Liberia; Niger; Nigeria; Senegal; Angola; Kenya; Ethiopia; Lesotho; South Africa; Zimbabwe.

Prior to 1990 just 7.3% of engineers arriving in Australia from overseas came from countries in the Southern and Central Asian region countries. During the 1990s the proportion increased and by 2000 it was 21.2%. Since then it rose to a peak of 31.7% in 2004 and it has been close to this level since. In 2010, 27.9% of migrant engineers came from this region.

Arrivals from countries of the South East Asian region were 19.6% prior to 1990 but have slowly fallen over time to be 12.1% in 2010. Countries of the North West Europe region have historically been important sources for Australia’s migrant engineers making up 27.6% of arrivals prior to 1990. The share of this group has gradually fallen until it was 15.7% in 2009. The proportion increased to 18.8% in 2010, possibly as a result of the GFC impact in the region. Arrivals from countries of the North East Asian region increased from 10.9% prior to 1990 to 18.4% during the 1990s, but the share has steadily fallen to be 10.3% in 2010. There were few migrant engineers from countries in the Americas before 1990 but the share of arrivals from these countries has increased, particularly in more recent years, to be 10.3% in 2010.

Engineers Australia 13

The Engineering Profession: A Statistical Overview, 2015

Chapter 3 The Engineering Labour Market over Time Main Points This Chapter relies on statistics from the annual ABS Survey of Education and Work (SEW) to examine recent developments in the engineering labour market. Announced changes to the monthly ABS Labour Force Survey mean this recourse will not be necessary in the future once sufficient observations for new definitions have been accumulated.

SEW statistics confirm the view based on census statistics that labour force participation by engineers is high, indeed higher than the skilled labour force and substantially higher than the overall labour force. Analysis of changes in engineering labour force participation shows that reductions in participation have played an important role in adjusting the supply of engineers to lower demand.

The GFC impacted engineering more severely than other segments of the labour force in 2009. When this effect is excluded the period 2008 to 2013 was one of especially high demand for engineers. Some of the supply of engineers was absorbed by the skilled labour market and this meant that the demand for qualified engineers in occupations close to engineering was especially high.

Consistent with trends in vacancies statistics, there was a marked change in the engineering labour market in 2014. The demand for the engineering team grew by just 0.9%, a fraction of the growth experienced in previous years. In contrast, the supply of engineers continued to grow by 3.1%.

The result was that the unemployment rate in the engineering labour market increased to 5.3% in 2014. This is now a year ago and the indications from vacancies statistics, from statistics on education completions and skilled migration statistics are that the past year has been a repeat of 2014 and unemployment has likely increased.

A feature of the deterioration in the engineering labour market is that demand for engineers in occupations close to engineering has remained reasonably strong. This observation strengthens the view that public policy concerning the engineering profession should focus on the development of fully competent engineers and their retention in engineering. Growing the number of people who complete engineering qualifications is essential, but insufficient.

3.1 Background For many purposes some of the best statistics are from the ABS Population Census which is conducted every five years. This frequency is not an issue when the focus of interest is a structural issue, but census statistics usually become available 12 to 18 months after the census is held and so are of limited value so far as contemporary change is concerned. The May 2015 Commonwealth Budget provided the ABS with the financial allocations required to conduct the 2016 census. In due course, the results will be used to update structural statistics.

In Australia, changes in the size and structure of the national labour market are usually monitored using statistics from the Australian Bureau of Statistics (ABS) Labour Force Survey (LFS). The LFS is based on 0.32% of the civilian population7 aged 15 years and over and was first conducted in 1960. Since 1978 the LFS has been available monthly.

Historically, the LFS has had limited value for an organization like Engineers Australia which includes mandatory educational qualifications in engineering as a membership condition because the LFS

7 ABS, Information Paper, Labour Force Survey Sample Design, May 2013, Cat No 6269.0, www.abs.gov.au

Engineers Australia 14

The Engineering Profession: A Statistical Overview, 2015

questionnaire did not include questions about respondents’ educational qualifications. Industry and occupation of employment were recorded, but without information about educational attainment, the resulting statistics did not measure engineering as understood by Engineers Australia.

This situation is about to change. The LFS questionnaire has been regularly reviewed and refined and from May 2015 will include educational attainment allowing statistics for the engineering profession to be compiled for the first time8. This is an important development because quarterly statistics on trends in the engineering labour market will be available with no more delay than the labour market information used in government decision making.

The absence of contemporary statistics has been a major barrier to understanding the rapid deterioration in the engineering labour market during the past two years. The main indicator employed by Engineers Australia has been analyses of vacancy trends using statistics produced by the Department of Employment and Training9. These statistics are useful indicators of changes but are not substitutes for comprehensive information about changes in the demand for, and supply of, engineers or about unemployment.

Until sufficient observations from the revised LFS are compiled, Engineers Australia has explored alternative ways to obtain contemporary statistics on trends in the engineering labour force to bridge the gap between 2011 and now. The option chosen was to use the ABS Survey of Education and Work (SEW). The SEW is an annual supplement to the LFS which does cover educational attainment. Until recently access to these statistics as they apply to engineers has been difficult. It was necessary to ask the ABS to extract statistics relating to engineers from each year’s survey on a fee for service basis. This process was made more awkward by standard error limitations which impeded some requests. The ABS has now made SEW statistics for 2011 to 2013 accessible using TableBuilder. Experimentation with these data sets resulted in a more focused request to the ABS for statistics covering prior years.

3.2 Survey of Education and Work The Survey of Education and Work (SEW) is a supplementary survey that draws on the LFS sample and is undertaken annually in May10. Although a subset of the LFS sample there are some differences in survey response rates and the scope of the surveys. The latter are important when comparing trends to other statistics, for example the membership of Engineers Australia.Until 2008, the SEW covered 15 to 64 years age groups. From 2009 until 2012, age groups 65 to 74 years were included in the survey in cases where there was attachment to the labour force. In 2013, all individuals up to 74 years of age were included. These changes mean that some compromise is needed to compile a consistent time series. The most obvious one is to settle on the earlier age range, 15 to 64 years. The shorter interval 2011 to 2014 was used to examine the circumstances of the 65 to 74 years age groups.

In principle, SEW statistics can be compiled by occupation, but given the size of standard errors for many occupations, the results are problematic. Instead, the concept of engineering occupations referred to in Chapter 2 was used and statistics for the aggregate of the 51 (of 358) four digit occupations involved was compiled for each year11.

Ideally, statistics are required for each of the three occupational groups in the engineering team. However, the ABS definition of Bachelor degrees precludes this because it combines full time study durations from three to six years. This means that it is not possible to distinguish between professional engineers and engineering technologists; the two occupational groups need to be considered together in

8 ABS, Information Paper: Forthcoming Changes to Labour Force Statistics, October 2014, Cat No 6292.0, www.abs.gov.au 9 See http://lmip.gov.au/default.aspx?LMIP/VacancyReport 10 ABS, Education and Work, Australia, May 2014, Cat No 6227.0, www.abs.gov.au 11 The research behind this concept is explained in Engineers Australia, The Engineering Profession in Australia; A Profile from the 2006 Population Census, 2010, www.engineersaustralia.org.au

Engineers Australia 15

The Engineering Profession: A Statistical Overview, 2015

a group called degree qualified engineers. It was possible to separate out statistics for associate engineers.

Other noteworthy differences between SEW and census statistics are the exclusion of defence forces from the SEW, the exclusion of people normally resident in another country and exclusion of indigenous communities. Defence is a comparatively large employer of engineers, sufficiently large to cause observable differences employment statistics for other industries. Skilled temporary migrants are normally resident in Australia for the duration of their visas and are included.

This Chapter uses the same labour market concepts as discussed in Chapter 2. However, it is important to bear in mind the differences in the two data sets used. Chapter 2 considers census statistics that cover age groups 19 years and over, and all segments of the population. The statistics in this Chapter have the restrictions outlined in the previous paragraph and cover age groups 15 to 64 years.

3.3 Engineering Population The engineering population is the subset of the population that holds engineering qualifications consistent with the engineering team. Increases in the engineering population occur when new graduates from Australian educational institutions join the labour market after completing engineering qualifications and when overseas engineers join the labour market either as permanent migrants or temporary migrants under 457 visas. The engineering population falls when engineers who are citizens or permanent residents die and when temporary 457 migrant engineers finish contracts in Australia and return to home countries. In this paper, the engineering population also fall when engineers turn 65 years and leave the age range used to compile the time series. Only consideration of net outcomes is feasible.

In 2001, the population with engineering team qualifications was 233,900 and by 2014 it had grown to 416,200, an increase of 77.9%. In most years, annual growth was fairly robust as shown in Figure 3.1. Over the period 2001 to 2014, the engineering population grew by an average 4.6% per year. The impact of the global financial crisis (GFC) reduced growth in 2009 to 0.3%, most likely because temporary migrants on 457 visas did not have contracts renewed and returned to home countries. The most recent statistics showed that the increase in 2014 was 2.2%.

In 2001, there were 178,000 degree qualified engineers, 76.1% of the engineering team population, but over time this group experienced faster growth. By 2014, the population had increased to 330,400 with average annual growth of 5.0% per year. The GFC caused the population of degree qualified engineers

Engineers Australia 16

The Engineering Profession: A Statistical Overview, 2015

to fall by 4.5% in 2009, again most likely due to return of temporary migrants on 457 visas to home countries. In 2014, the increase was 4.2%, robust but lower than the average since 2001.

In 2001, there were 55,900 associate engineers in the population and with average annual growth of 4.3%, by 2014 this had increased to 85,800%. There was much more variability in this population with the numbers of associate engineers falling in five of the thirteen years examined. The population peaked in 2013 at 90,300 associate engineers.

3.4 Participation Rates and the Supply of Engineers

Time series estimates confirm that engineers have very high labour force participation rates compared to the labour force overall as shown in Figure 3.2. Comparison to other skilled groups was limited by data availability and in the diagram degree qualified engineers were compared to degree qualified people in all skilled fields. This comparison showed that labour force participation rates for engineers were higher than for other fields.

Between 2001 and 2014, the average labour force participation rate for the engineering team was 90.2%. Degree qualified engineers had a slightly higher average rate of 90.8%. In comparison, the average participation rate for all degree qualified persons was 87.3% and the average labour force participation rate for the entire labour force was 77.1%.

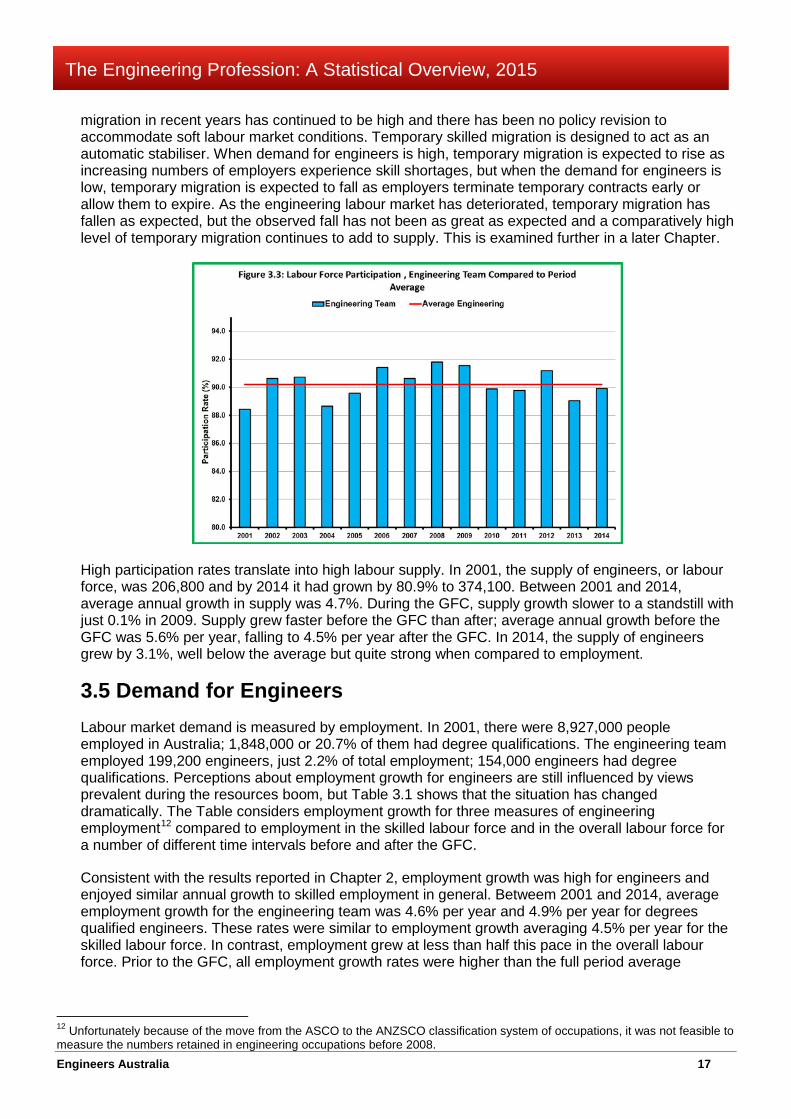

Changes in engineering labour force participation are an important adjustment mechanism in the engineering labour market and this can be demonstrated using Figure 3.3. In most years before the GFC, the participation rate was above average reflecting the attraction of high demand for engineers on labour force participation. The impact of the GFC in 2009 led to falls in participation to below the average in each of the following two years. If instead of falling, participation rates in 2010 and 2011 stayed at the 2009 level, an additional 12,200 engineers would have been in the labour market. Essentially, some engineers chose to retire from the labour market rather than face unemployment. As well, some temporary migrant engineers on 457 visas returned to their home countries.Following the GFC, the engineering labour market recovered, but the recovery was short lived. Vacancies began to fall in December 2012 and Figure 3.3 shows that once again participation played a role. In 2013, the participation rate fell well below average. Had it remained at its 2012 level, the 2013 engineering labour force would have been 8,800 larger. In 2014, participation returned to its average level.

Changes in the engineering labour force are the result of interplay between participation decisions taken by engineers already in Australia and Australia’s skilled migration policies. Permanent skilled

Engineers Australia 17

The Engineering Profession: A Statistical Overview, 2015

migration in recent years has continued to be high and there has been no policy revision to accommodate soft labour market conditions. Temporary skilled migration is designed to act as an automatic stabiliser. When demand for engineers is high, temporary migration is expected to rise as increasing numbers of employers experience skill shortages, but when the demand for engineers is low, temporary migration is expected to fall as employers terminate temporary contracts early or allow them to expire. As the engineering labour market has deteriorated, temporary migration has fallen as expected, but the observed fall has not been as great as expected and a comparatively high level of temporary migration continues to add to supply. This is examined further in a later Chapter.

High participation rates translate into high labour supply. In 2001, the supply of engineers, or labour force, was 206,800 and by 2014 it had grown by 80.9% to 374,100. Between 2001 and 2014, average annual growth in supply was 4.7%. During the GFC, supply growth slower to a standstill with just 0.1% in 2009. Supply grew faster before the GFC than after; average annual growth before the GFC was 5.6% per year, falling to 4.5% per year after the GFC. In 2014, the supply of engineers grew by 3.1%, well below the average but quite strong when compared to employment.

3.5 Demand for Engineers

Labour market demand is measured by employment. In 2001, there were 8,927,000 people employed in Australia; 1,848,000 or 20.7% of them had degree qualifications. The engineering team employed 199,200 engineers, just 2.2% of total employment; 154,000 engineers had degree qualifications. Perceptions about employment growth for engineers are still influenced by views prevalent during the resources boom, but Table 3.1 shows that the situation has changed dramatically. The Table considers employment growth for three measures of engineering employment12 compared to employment in the skilled labour force and in the overall labour force for a number of different time intervals before and after the GFC.

Consistent with the results reported in Chapter 2, employment growth was high for engineers and enjoyed similar annual growth to skilled employment in general. Betweem 2001 and 2014, average employment growth for the engineering team was 4.6% per year and 4.9% per year for degrees qualified engineers. These rates were similar to employment growth averaging 4.5% per year for the skilled labour force. In contrast, employment grew at less than half this pace in the overall labour force. Prior to the GFC, all employment growth rates were higher than the full period average

12 Unfortunately because of the move from the ASCO to the ANZSCO classification system of occupations, it was not feasible to measure the numbers retained in engineering occupations before 2008.

Engineers Australia 18

The Engineering Profession: A Statistical Overview, 2015

The GFC impacted severely on engineering employment but skilled employment growth increased as did overall employment growth. One of the characteristics of engineering employment is that it was particularly strong immediately before and after the GFC. Table 3.1 shows that average annual employment growth for engineers in the period 2008 to 2013, leaving out 2009, was stronger than for period immediately before and for the full period. Indeed, employment growth for the engineering team was an average 5.9% per year, for degree qualified engineers it was 8.0% per year and in engineering occupations it was 7.5% per year. In contrast, skilled employment and overall employment continued to grow consistent with earlier rates.

Statistics on vacancies for engineers began a strong downwards trend in December 201213. Throughout 2013 and into 2014 there were continuing anecdotes about engineers losing their positions for various reasons. The impact of these developments became evident in 2014 when employment growth for the engineering team slowed to 0.9%. Employment for degree qualified engineers was not as badly affected growing by 2.4%. The most interesting result is for employment in engineering occupations which continued to grow by 4.0% per year.

While one factor contributing to the change in 2014 was the impact of the transition from construction to production in the resources sector, another factor was the more widespread softness in the Australian labour market. This view is supported by the sharp contraction in employment growth in the skilled workforce and the fall in employment overall. One of the fastest growing areas of engineering employment was “engineering consulting”. This industry was particularly hard hit by the resources transition and by the downturn in infrastructure investment. However, engineers are employed in most industries throughout the economy and have been affected by soft economic conditions, particularly in manufacturing and construction industries.

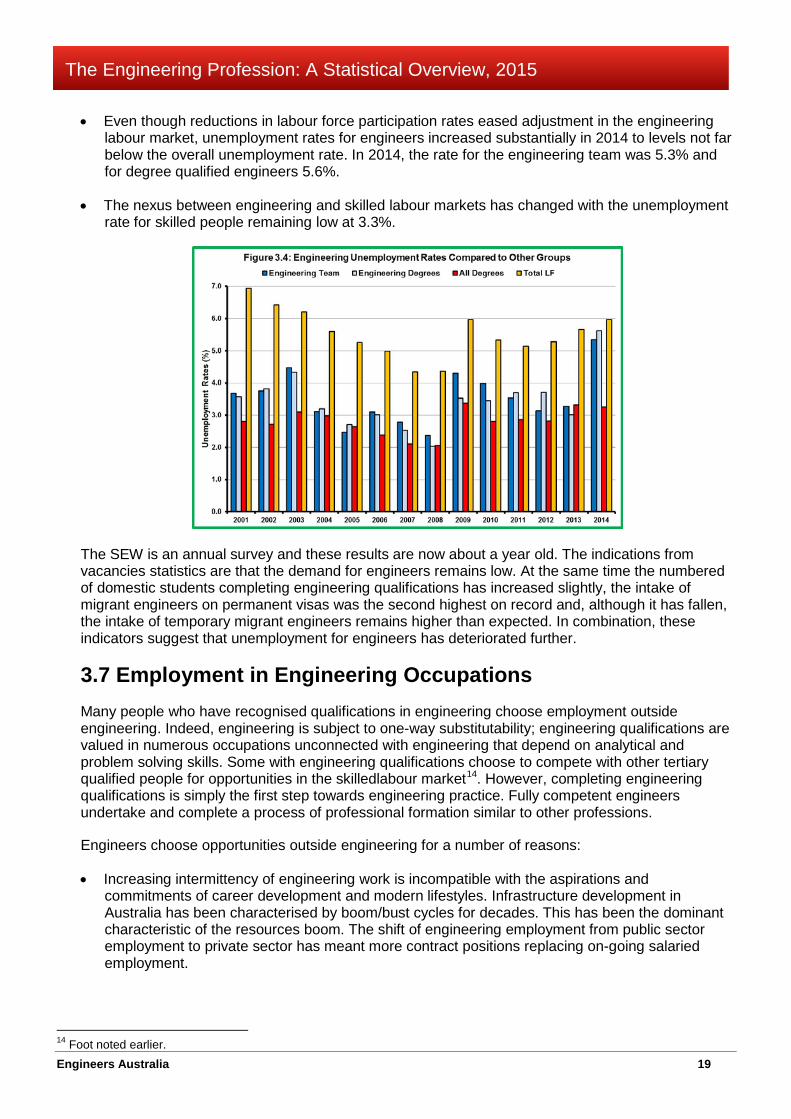

3.6 Unemployment

While employment growth for the engineering team slowed to 0.9% in 2014, supply grew by 3.1% and as a result unemployment has increased. Figure 3.4 compares the trends in unemployment rates for the engineering team, degree qualified engineers, the skilled labour force and the overall labour force since 2001. The blue bars illustrate the trend in unemployment rates for engineers, the engineering team in dark blue and degree qualified engineers in light blue. The red bars are the unemployment rates for the skilled labour force and the overall unemployment rates are in yellow.

Several points can be made about Figure 3.4:

• For most of the period illustrated unemployment rates for skilled people, whether engineers or other skills, were substantially lower than the overall unemployment rates.

• Engineers experienced higher unemployment rates than the skilled labour force in most years. In this regard the structural differences related to gender and ethnicity noted in Chapter 2 are likely to be important.

13 These trends are reported in Monthly Vacancies Updates available from www.engineersaustralia.org.au .

Table 3.1: Employment Growth in Engineering Compared to Other Groups (% pa)

Period Engineering Engineering Engineering All AllTeam Degrees Occupations Degrees Employment

2001 to 2014 4.6 4.9 .. 4.5 1.72001 to 2007 5.2 4.5 .. 4.7 2.1GFC (2009) -1.9 -6.1 -4.6 6.7 1.5

2008 to 2013 less 2009 5.9 8.0 7.5 4.5 1.82014 0.9 2.4 4.0 1.5 -0.7

Engineers Australia 19

The Engineering Profession: A Statistical Overview, 2015

• Even though reductions in labour force participation rates eased adjustment in the engineering labour market, unemployment rates for engineers increased substantially in 2014 to levels not far below the overall unemployment rate. In 2014, the rate for the engineering team was 5.3% and for degree qualified engineers 5.6%.

• The nexus between engineering and skilled labour markets has changed with the unemployment rate for skilled people remaining low at 3.3%.

The SEW is an annual survey and these results are now about a year old. The indications from vacancies statistics are that the demand for engineers remains low. At the same time the numbered of domestic students completing engineering qualifications has increased slightly, the intake of migrant engineers on permanent visas was the second highest on record and, although it has fallen, the intake of temporary migrant engineers remains higher than expected. In combination, these indicators suggest that unemployment for engineers has deteriorated further.

3.7 Employment in Engineering Occupations

Many people who have recognised qualifications in engineering choose employment outside engineering. Indeed, engineering is subject to one-way substitutability; engineering qualifications are valued in numerous occupations unconnected with engineering that depend on analytical and problem solving skills. Some with engineering qualifications choose to compete with other tertiary qualified people for opportunities in the skilledlabour market14. However, completing engineering qualifications is simply the first step towards engineering practice. Fully competent engineers undertake and complete a process of professional formation similar to other professions.

Engineers choose opportunities outside engineering for a number of reasons:

• Increasing intermittency of engineering work is incompatible with the aspirations and commitments of career development and modern lifestyles. Infrastructure development in Australia has been characterised by boom/bust cycles for decades. This has been the dominant characteristic of the resources boom. The shift of engineering employment from public sector employment to private sector has meant more contract positions replacing on-going salaried employment.

14 Foot noted earlier.

Engineers Australia 20

The Engineering Profession: A Statistical Overview, 2015

• Engineers have career ambitions like everyone else and opportunities for career development in engineering are limited and are diminishing over time. Instead, engineers have pursued lateral career moves into other areas of work.

• Although starting salaries for new engineering graduates have been high, analysis of salary changes compared to movements in full time adult earnings shows that engineering remuneration simply has not kept up, especially at junior level15.

• Much of the resources boom has occurred in remote locations unattractive to engineers settled into career paths in urban and more conventional regional settings.