the effects of knowledge complementarities and bank ... annual meetings/2018-milan... · the...

TRANSCRIPT

The Effects of Knowledge Complementarities and Bank Reputation on Participant Banks Choice Decisions

Yi-Ting Hsieh*

Department of Finance

College of Finance

Feng Chia University

Hsin-Hao Fu

Department of Applied Economics

College of Social Sciences and Management

Fo Guang University

* Address correspondence to Yi-Ting Hsieh, Department of Finance, College of Finance, Feng Chia University, No. 100, Wenhwa Rd., Seatwen, Taichung, Taiwan 40724, R.O.C. Tel.:+886-928636412; e-mail: [email protected]

The Effects of Knowledge Complementarities and Bank Reputation on Participant Banks Choice Decisions

Abstract

In our paper, we focus on the decision of lead arrangers on participant bank choices in the syndicated loan market. We extend reputation-building theory (Diamond, 1991) and model the lead arranger’s partner choice problem through the effect of self-related and task-related factors. Our paper show that when lead arrangers have higher reputation, operating efficiency, and market experience, lead arrangers tend to choose less reputable partners. These results help to explain how lead arrangers, through their partner selection decisions, manage the reputation pool among banks in the syndicated loan market.

Keywords: Syndicated Loan Market, Lead Arranger, Participant Bank, Complementarity in Reputation Building.

JEL classification: G20, G29

The Effects of Knowledge Complementarities and Bank Reputation on Participant Bank Choice Decisions

The lessons to be learned from observing men of different characters. The Master said, "When we see men of worth, we should think of equaling them; when we see men of a contrary character, we should turn inwards and examine ourselves."

From Confucian Analects, Book IV: Le Jin 1. Introduction

It is clear that cooperation holds a number of potential benefits in economic and social life. How does one find the optimal partners in the syndicated loan market? To address this problem, we present a novel complementary strategic alliances model for partner selection that helps to develop the reputations or/and relationships of financial intermediaries. Bolton, Katok, and Ockenfels (2005) regarded the long-recognized reputation of financial intermediaries as an effective way to enforce cooperation when information asymmetry exists. However, it is unclear how effective the reputation would be, as the players are essentially strangers or they only know others through word-of-mouth in a market with limited information. Partner choices can be risky because of the high uncertainty about the quality of the resources, and the trustworthiness of the potential partner. Jensen and Roy (2008) propose that the firm-specific status and reputations help decision marker choose exchange partner. Our study focuses explicitly on the impact of reputational status on alliance formation in the syndicated loan market.

For the syndicated loan market, once a lead arranger bank plans to offer a loan, it must decide with which participant banks it would want to co-work. The selection of syndicate partners is important, because it affects both the quality of the loan offering and the prestige or esteem of the other market participants (Sufi, 2007). Our paper considers the mechanism through which such a development of reputation takes place, such as co-branding, syndicated for reputation. In the financial services industry, as in others, having a good reputation helps to resolve the problem of information asymmetries; this is especially important when a financial transaction has long-term implications. By focusing on bank reputation, lead arrangers may mitigate risk and uncertainty when selecting collaborative partners (Barro, 1986; Boot and Thakor, 1993; Chemmanur and Fulghieri, 1994; Shane and Cable, 2002; Fang, 2005; Lewellen, 2006; Ross, 2010; Gopalan, Nanda, and Yerramilli, 2011; Bushman and Wittenberg-Moerman, 2012). Why does not the lead arranger’s access to a good reputation partner ensure syndicated success? Which lead arrangers find good reputations most valuable? Generally, banks are more likely to cooperate with partners with positive reputations for business expertise and integrity but also are likely to avoid the partners that their competitors use. The partner choice problems create an interesting paradox: Banks favor partners with more expertise, but this expertise comes from the

same industry, and banks disfavor partners that could be the potential competitors. This paper addresses these questions. We state that there exists complementarity in reputation-building if the market has more of a demand for reputation.

Based on the concept of complementarity in reputation-building, our paper investigates the lead arranger’s participant bank choice decisions. In syndicated loan markets, an individual’s partner choice tends to make use of potential partners’ reputations, and an individual prefers to choose the ones with good reputations (Fu et al, 2008). Particularly, we examine a market in which lead arrangers face asymmetric information, they have a short-term incentive to exert low effort, but could earn higher profit if it were possible to exploit a good reputation. We view reputation as a commitment device that allows banks to solve the information asymmetry problem. Here, we assume that the participant banks’ reputations are choice items for lead arrangers in the syndicated loan market.

Who wants a good reputation? Our paper documents the manner in which a lead arranger’s specific factors affect the choosing of high-reputation partners. To answer the question, we categorize the factors into two: self-related and task-related factors, the former defined as the prestige that is accorded to actors because of their social positions or firms’ characteristics, and the latter defined as the prestige that is accorded to actors because of their prior performance (Wilson, 1985; Gould, 2002; Jensen and Roy, 2008). We propose, specifically, that self- and task-related factors shape a lead arranger’s choice set of active, considered alternatives, whereas reputation determines the arrangers’ actual selection behavior given the choice set.

By portraying the two categories, i.e., self-related and task-related factors, as the distinct theoretical mechanisms in the decision process, our framework focuses on an overlooked aspect of syndicate partner choice. We simplify complex decision problems by reducing the total number of alternatives using relatively simple decision algorithms. To make a choice among the alternatives within a selected bracket, banks rely on reputations for business expertise. We examined whether banks decided to choice within a selected bracket, the top-three banks. We argue specifically that the business integrity and expertise of a bank to decision banks affects the choice of bank reputation bracket, whereas decision banks’ self-related and task-related characteristics affect the choice of syndicate partners. That is, if a bank decided to use a top-three bank, we examined the factors that determined exactly which of the top-three banks it decided to use.

Our approach is a standard tool in organization literature.1 We used the

1 In the studies on firms’ choice of lenders, Yasuda (2005) proposed that relations between bank

relationships and a firm’s underwriter choice (commercial banks or investment banks) result from a two-stage process in which underwriters first categorize firms on the basis of common characteristics and subsequently observe the underwriting fees charged by the chosen banks. Ljungqvist, Marston, and Wilhelm (2006) also used the two-stage model to observe the effect

direct model to investigate the lead arranger’s partner-choice problem and measure the effect of reputation on the choice of participants. In particular, the goal of this paper is to answer the following questions:

(1) Is bank reputation important for the lead arranger’s decision in selecting its participant banks? If so, what kind of lead arranger characteristics (e.g., bank operational diversification (self-related) and loan market experience (task-related)) would demand high-reputation participant banks? These inferences are drawn from the probit model coefficient in our partner-choice model.

(2) Do the loan market experiences of a lead arranger explain its selection preference toward a participant? Or are the other banks’ actions more compelling than the lead arranger’s characteristics in determining partner selection? These inferences are present in the coefficient in the basic probit model, and they are also drawn by using the conditional logit model (also called McFadden’s choice model).

(3) Does the strength of the bank’s reputation (e.g., whether the bank is a national top-three bank or simply a local top-three bank in the syndicated loan market) matter? How might the importance of the lead arranger’s self-related and task-related factors to its partner choice vary for higher-status reputation banks, such as nationally reputable banks or locally reputable banks? To explore this inference, we used a multinomial logistic regression in which a lead arranger chooses one reputable bank out of multiple choices.

We tested our conductions by combining the following data sources: the Loan Pricing Corporation’s (LPC) Dealscan database for loan information, the BankScope database for the lead arranger’s characteristics and bank ownership structure, and the CEPII distance database for bilateral distance information. We constructed a comprehensive data set consisting of International syndicated loan deals from 2001 to 2014. This data set combined individual-level and lead arranger-level data with bank-specific and loan-specific data. Besides, lender reputation and lenders’ loan market experience data were constructed from the LPC Dealscan database. Special care was taken to account for the significance of roles played by banks in these loans, as well as to sort out the effect of bank mergers on bank affiliations by using the SDC Platinum Mergers and Acquisitions Database and BankScope.

As a result, three findings indicated that a partner’s reputation does play an important role in building reputation in the syndicated loan market. First, we found that a partner’s reputation has a complementary effect between lead arrangers and participant banks. That is, lead arrangers with less reputation,

of analyst behavior on underwriter choice in both equity and debt market. Cantillo and Wright (2000) investigated the lender choice process by using probit regression, a simple and obvious method, to show that intermediaries are indeed at an informational advantage over arm’s-length investors, and that the reorganizational framework best explains how firms choose their lenders.

no top-four auditors, and less credit accountability in the loan market yield positive and significant effects on the demand for high-status reputation partners. This result also applies to foreign-owned lead arrangers. We drew inferences here from the estimates of the reputation-based partner-choice model.

Second, we found that the lead arranger’s loan market experience seriously influences their partner preference type. These findings are also consistent with the complementary effect, that is, the lead arranger with less experience has more incentives to demand high-status reputation partners. On the contrary, lead arrangers with a higher market power in the loan market will decrease demand for highly reputable partners. Moreover, our results indicated that other banks’ activities also affect the syndicate partner choices. From this result, we show that a herding behavior in reputation-based partner choice decisions. In other words, when a small part of the lenders switches to highly reputable partners, the lead arrangers will usually follow. These results are consistent with our earlier hypothesis, the complementary effect and reputation-building hypothesis. These inferences were drawn from the probit partner-choice model and McFadden’s choice model.

Third, our robustness tests found that the foreign-owned and government-owned lead arrangers prefer locally reputable partners than non-reputable partners. We also tested the learning hypothesis in our model. The results indicated that as the lead arrangers drop in rankings, they will increase their demand for high-status reputation partners. However, if the lead arrangers’ rankings reduce severely, they will not change their partner choice decisions. The possible explanation is, in order to get their rankings back, lead arrangers have an incentive to learn from high-status reputation partners.

The rest of the chapter is outlined as follows. The next section describes our theoretical background and offers empirical predictions from the complementary needs hypothesis in the context of syndicate partner choice. The third section describes the data and summary statistics. The fourth section presents and discusses the empirical results. The fifth section shows the further examinations. The sixth section concludes our findings.

2. Conceptual framework: Complementarity in the reputation-building effect

2.1.Background: Global syndicated loan market and reputable bank deals

Over the past two decades, the global syndicated loan market has become one of the most important corporate financing sources. Figure 1 plots the dollar value of syndicated loan deals, and the fraction arranged by reputable banks from 1991 to 2014. In the global syndicated loan market, the issuance grew from approximately $296 billion in 1991 to $5,184 billion in 2014. The volume of syndicated loan deals increased throughout the 1990s, sharply declined after the financial crisis in 2008, and then increased again from 2010 to 2014. On the other hand, reputable bank deals, which used to be a major fraction of syndicate

deals (40%), have gradually dropped around 15% in recent years. In addition, this figure shows a very interesting result related to the recent financial crisis: there was a decreasing tendency for both the total deal value and fraction of reputable deals in 2008 and 2009. We also found that the fraction of reputable deals decreased as the loan market competition increased.

【Insert Figure 1】

Panel A of Table 1 presents a list of the top banks, either involved as arranging banks or participating banks in the syndicated loan market, during the 1991-2014 time period. The list is sorted by the number of deals and amount arranged. The global syndicated loan market was highly concentrated. The top-three banks (hereafter the “Big 3”), JP Morgan, Bank of America, and Citi, usually accounted for 36.2% of all deals during the 1991-2014 period. Panels B and C give further insights into how the syndicated loan market has evolved over different periods. We found that the degree of market concentration, which we defined as the market shares of the biggest three banks, decreased over time, from 54.7% during 1991-2000 (Panel B) to 31.1% during 2001-2014 (Panel C). Moreover, while there were position changes for other top arrangers over the two periods, the Big 3 banks were not affected by these changes, with JP Morgan remaining in the first position, Bank of America in the second, and Citi in the third.

【Insert Table 1】

Since the Big 3 banks syndicated most of their loans, they have achieved oligopolistic market power due to a unique reputation for reducing information asymmetry between the borrowing firms and the investors. These arguments suggest that the Big 3 would do a better job at screening and monitoring than the other lenders. Therefore, alliances with the Big 3 would build reputations and rewards with a particularly positive lender stock price response, which we call “complementarity in the reputation-building effect”2 (Choi and Jeon, 2007).

2.2.Complementarity in the reputation-building effect: Participant banks’ reputation measure (Big3

Global)

Syndicate member formation begins with the selection of the participant bank by the lead arranger. Especially for the larger syndicated deals, the competition of the participant seats tends to be fierce, because bank alliances vie for top positions in underwriting rankings and build a higher reputation with the lead arranger. Sufi (2007) stated that bank reputation, industry

2 We investigated the effects of choosing reputable participant banks on the loan

announcement returns of lead arrangers. Appendix A reports the study results of the lead arranger’s partner-choice model. Our results indicated that lower reputable lead arrangers choosing higher reputable partners in the syndicated loan market is highly, statistically significant and yields positive reactions. These findings are consistent with our argument that complementarity in reputation-building plays an important role in syndicated loan partner choices.

knowledge, and prior relationships are likely to be the important factors in the selection of participant banks. Therefore, the optimal participant banks would be those whose ability or distribution system can complement that of the lead arranger. Empirically, for lead arrangers, the participant bank’s reputation directly affects their choice of partner banks.

In the syndicated loan market, several reasons account for why bank reputation is useful for participant bank selection decisions. First, reputation denotes a narrower expectation of future behavior that is directly based on past demonstrations of that behavior, whereas status denotes a broader expectation that is not necessarily tied to past behavior (Weigelt and Camerer, 1988; Roberts and Dowling, 2002). In particular, reputation can explain how lead arrangers prefer to work with the participant banks with whom they have an embedded relationship to reduce the risk and uncertainty associated with interbank relationships. Second, the focal concern for bank reputation is the nature of the underlying incentives in a relationship, which are consistent with our interest in what motivates participant banks to choose to syndicate with one another. Third, the choice of reputable participant banks will influence the degree of information asymmetry.

Except for bank reputation, to understand how lead arrangers manage the tension between the need for depth and breadth in their networks, it is important to examine the economic context of lead arranger banks, that is, the operating ability or social relationship development of lead arranger banks. To distinguish the effect of bank reputation on the lead arranger’s partner choice decisions, we defined an indicator variable, Big3

Global, which equals one if the

participant bank is one of the biggest three banks3 in a particular year, and zero if otherwise. By using this binary variable, we can definitely investigate the factors that influence the lead arranger’s decision of participant selection. In the next section, we draw on our theoretical discussion of the role of complementarities in partner choices, and examine how complementarities induce reputation anxiety, which affects the choices of reputation brackets, and how reputations of industry expertise and business integrity affect participant bank choices.

2.3.The potential functions of syndicate partners: Bank efficiency (self-related) and loan experience (task-related) complementarities

The previous section argued that bank reputation might affect the syndicated loan partner choice. Our article concluded that it is important that lead arrangers understand the impact of a participant bank’s characteristics and the differences in syndicate members. Another stream of research has explored the importance of choosing the “proper” or “right” partner; this is

3 The Big 3 banks dominate the syndicated loan market in monitoring capacity and quality and

have developed stronger reputations for quality than the other banks. Ross (2010) also reported that using a Big 3 bank provides a strong positive signal in syndicated loan borrowings. Thus, we decided to choose the Big 3 as our main dependent variables to examine the partner-choice decision in the syndicated loan market.

especially pertinent in relation to a firm’s technologies or core markets. It is vital that a participant bank be “complementary” with its lead arranger, since the optimal participant bank selection depends upon the final balance of resources and skills shared by these lenders. Hence, the balance results in the success or failure of a deal in reaching its objectives (Awadzi, 1987; Geringer, 1991; AI-Khalifa and Eggert Peterson, 1999). Therefore, choosing the participant bank is an obvious and important decision.4 It is a definite and specific decision in the creation of a participant bank. Further, we can see what selection criteria are used, and how important they are from the decisions. The significance granted to the selection of a suitable partner is grounded in the importance of compatible and complementary skills, resources, reputations, procedures, and policies to a successful syndicated lending.

Awadzi (1987) examined the relationship between relative bargaining power and partner selection criteria. He argued that the more resources a firm contributes to a joint venture, the greater the likelihood it would be selected as a partner. Similar to Awadzi’s findings, Fernando, Gatchev, and Spindt (2005) focused on the co-underwriter choices model, and developed a theory explaining the equilibrium matching between issuing firms and their underwriter. They showed that, if a firm chooses the higher-status reputation leading underwriter from the available set, their co-managers will be of lower-status reputation, as compared to their lead arrangers. However, these papers did not clearly identify the “complementary resources” contributed by the partners, instead leaving that decision up to the respondents.

Sufi (2007) examined the problem of syndicate member choices. He focused on a group of participant banks and labeled them as “known” or “unknown,” given the different degrees of information asymmetry that they suffered. Sufi identified a list of relationships used by lead arrangers to select partners in this specific type of strategic context, which includes information on improving on or complementing one’s own current information base. However, no determinant was presented regarding relative frequency or the importance attached to each, or how these criteria might have varied from those used for the lead arrangers whose partners did not vary widely in size, or were not oriented toward industry experts. Referring to Diamond’s (1991) reputation-building argument, Yasuda (2005) predicted that the firm’s valuation of bank relationships is inversely related to its firm reputation: firms with lower reputation are expected to value them the most, since they gain the most by choosing an underwriting bank with certification ability. Thus, this choice may be in the same as the participant bank choices of lead arrangers. Lead arrangers with higher reputations have a valuable reputation to lose and

4 We investigated the effects of choosing a reputable participant bank on the loan

announcement returns of lead arrangers. We found that lower reputable lead arrangers choosing higher reputable partners in the syndicated loan market is highly, statistically significant and yields positive reactions. These findings are consistent with our argument that complementarity in reputation-building plays an important role in syndicated loan partner choices.

therefore have sufficient incentives to choose efficient lending decisions; since a partner’s monitoring or certification is costly, this class of lead arrangers prefers higher-status to lower-status reputation partners.

Participant bank selection appears to be an important issue in the formation and operation of syndicated lending, since the chosen participant banks, together with the lead arranger, provide the mix of skills and resources, operating policies and procedures, and overall competitive viability. In particular, the use of participant bank choice can distinguish the factors associated with efficiency from those associated with the effectiveness of the partners’ cooperation. More specifically, “self-related” factors refer to the lead arranger’s characteristics, such as a lead arranger’s reputation, an auditor’s reputation, operational diversification, and ownership structure. On the other hand, “task-related” factors refer to the intimate viability of a proposed bank’s operations, regardless of whether the chosen lending mode involves multiple partners. These variables could be tangible or intangible in nature. The examples include technical knowhow, experiences with different kinds of partners, and loan market experiences. Our main hypothesis suggests that selecting a “complementary” syndicate partner is critical for forming the loan. Our paper will focus on the self-related and task-related selection factors, and their relationship with the variables associated with a syndicate member’s strategic context, specifically the requirements of the syndicate member’s competitive and reputation-building environment.

In this essay, we examined the complementary effect on syndicate partner choices, by using the lead arranger’s demand for high-reputation partner as our main determinant variable. Reputation is an important concern in professional service industries. The intangible nature of professional services places a paramount importance on both confidence and trust. Thus, the role of relational embeddedness in partner selection will be reduced, if the potential partner has established a reputation. We tried to identify “a partner with complementary capabilities,” which may come from the financial capabilities that a potential partner provides, or from trade-offs when a lender is concerned about the alternative complementary skills or resources. Our study offers the concept of self-related and task-related complementarities as a basis for partner choice. Among other considerations, we took the self-related and task-related factors, which affect the lead arranger’s choice decisions, as our hypotheses, as shown in Table 2.

【Insert Table 2】

2.3.1 Bank efficiency (self-related) factors

In terms of the self-related factors for the determinants of the participant bank choices of lead arrangers, we considered the lead arranger’s self-reputation, auditor reputation, operational diversification, and ownership structure. Lead arrangers play an important role in monitoring borrowing

firms to reduce informational asymmetry at an early stage. Fernando, Gatchev, and Spindt (2005) examined issuer-underwriter choice selections, and they found that the co-managers have lower reputations than lead managers. Under complementarity in reputation-building, there have been lower agency problems between lead arrangers and participant banks. This implied that non-reputable lead arrangers have an incentive to reduce monitoring costs by working with relationally reputable partners. Thus, we used an indicator variable, SelfBig3 , to measure this reputation complementary incentive. Besides the lead arranger’s self-reputation, the auditor’s reputation is also an important external independent monitoring mechanism; high auditor reputation likely reduces the likelihood of a bank getting into trouble (Jensen and Meckling, 1976; Watts and Zimmerman, 1981; DeAngelo, 1981; Watts and Zimmerman, 1990; Ball, 2001). We used two binary variables to indicate if a lead arranger’s auditor5 is a Big 4 auditor (PricewaterhouseCoopers, Deloitte & Touche, KPMG, and Ernst & Young): coded one for yes, and zero if otherwise. We expected that the Big 4 auditor (Big4Auditor) will induce the demand for a participant bank’s reputation quality to increase at a decreasing rate.

Recent researches have examined whether banks engaging in diverse activities intensify the agency problems between insiders and outsiders with adverse ramifications for the market’s valuation. Acharya, Hasan, and Saunders (2006) studied the effects of loan portfolio concentration versus diversification on bank performance and risk-taking. They found that diversification is not a guarantee for promoting bank performance. In contrast, Laeven and Levine (2007) found that there is a diversification discount: diversification can provide cost savings to some clients, and their activities might enhance the ability of insiders to expropriate financial institution resources for private gain and thereby lower the market value. However, the banks’ diversification of activities should be considered in participant bank choice decisions. We predicted that when lead arrangers have more diverse activities, this diversification would increase banks’ operational risk. Hence, lead arrangers are more likely to choose higher-reputation participant banks to offset the risk. Following Laeven and Levine (2007) and Berger and Bouwman (2013), we examined different ways to control for operational diversification using two diversification variables (AssetDiversity, EarningDiversity) and one concentration index (LoanConcentration).

Li et al. (2008) suggested that partner selection is an important governance mechanism in interbank alliances. With this study, we have contributed to the previous literature on inter-organizational governance that has stressed the role of the governance structure. Further, we have added to the growing recognition of the ownership structures of participant bank selection in syndicates. Following the literatures on bank ownership structure and corporate governance, 6 we included foreign-owned bank (Foreign),

5 Data on auditors’ names were obtained from BankScope, which provides comprehensive

auditor information for the banks in our sample. 6 Foreign-owned investors have become much more important in domestic financial

government status (Government), the role of the blockholder (Blockholder), and ownership concentration (OwnershipConcentration) as our self-related measures. We used a dummy variable that equals one if the lead arranger is part of a foreign/government/blockholder owner in a given year, and zero if otherwise. Our paper expected that foreign-owned, block-owned, and lead arrangers with higher ownership concentration could help a bank strengthen its competitive position and may also choose lower-reputation participant banks when needed.

2.3.2 Loan experience (task-related) factors

As for the proxies of task-related factors, we considered market power measure variables, experience variables, and other banks’ activity variables: the loan market share, the experience with non-reputable banks, and other banks switching to the Big 3. As for the first measure of loan market experience, we calculated the relative market share of the loan market, which is based on the industry (IndustryShare) and country (CountryShare) for each lead arranger. An advantage of this index is that the higher its value, the higher the market power.

Then, we controlled for whether lead arrangers had recent experiences with participants other than the high-reputation banks. Levinthal and Fichman (1988) found that the risk of breaking a bank relationship increases in the first four years of the relationship, after which it decreases. Therefore, we defined recent experience as having used a non-Big 3 participant in the last three and five years, and used a binary variable as a control variable (EXPnonBig3_3Y; EXPnonBig3_5Y). Lead arrangers that defected very late during the collapse of the Big 3 might have found it harder to find a suitable participant among the Big 3; and lead arrangers that had strong preferences for the Big 3 participant, regardless of the reason, were likely to have left earlier.

Banks’ decision-making is easily subject to other banks’ activities (Jain and Gupta, 1987; Bikhchandani, Hirshleifer, and Welch, 1998). In our empirical tests, we also examined how the other lead arranger’s activities affected the lead arranger’s partner choice decision. We considered whether lead arrangers followed the activities of the other bank in charge of their loans at the Big 3, and

intermediation in the last two decades. Goldberg and Saunders (1981) found that foreign-owned banks have better access to capital markets, superior ability to diversify risks, and the ability to offer some services to multinational clients. Research on the effects of foreign-owned investors has found that foreign-owned investor and entry and fewer restrictions on these banks are associated with more competitive national banking systems (Claessens and Laeven, 2004). On the other hand, some studies have argued that the government ownership of banks is less efficient than private ownership (Buch, 1997; Drakos, 2003; Bonin, Hasan, and Wachtel, 2005). Fries and Taci (2005) found that private banks are more efficient than government-owned banks, and that private banks with majority foreign ownership are the most efficient. Mehran, Morrison, and Shapiro (2011) showed that institutional block owners have incentives to monitor management and seem to positively affect the choice of status brackets. Papers on ownership concentration have stated that concentrated ownership enhances corporate control by improving the monitoring of management (Berle and Means, 1991; Shleifer and Vishny, 1986; Ianotta, Nocera, and Sironi, 2007; Shehzad, Haan, and Scholtens, 2010).

whether most lead arrangers eventually switched to the Big 3 participants. That is, we expected lead arrangers to be more likely to switch to the Big 3 participants than other lead arrangers that had already switched to. We used a binary variable, SwitchedBig3_Dum, coded as one if other local lead arrangers had switched to a particular Big 3 bank. The binary variable fitted the data better than a continuous variable, because the distribution, which refers to the number of local lead arrangers switching to a particular Big 3 bank, was biased. We also considered the continuous variable, SwitchedBig3_Num, referring to the number of other banks that switched to Big 3 in our model. In sum, by exploring these variables, we can observe the scale of banks switched and examine the trade-off choice behavior. An advantage of this variable is that the higher the value, the higher the cost of demand for high-reputation participant banks.

3. Sample and descriptive statistics of high-status participant bank choices

3.1. Sample selection and data sources

For our study, we obtained data from the Loan Pricing Corporation’s (LPC) DealScan database. This database provides comprehensive information about the structure of the loan contract deals, the borrower, the arrangers, and syndicate members. We extracted information on the syndicated loans from 1991 to 2014. There were 135,546 loans reported on DealScan. Then, we focused on the number of lead arrangers who made the choices of syndicate members, resulting in 3,585 lead arrangers collected through the variable LeadArrangerCredit, which identified whether a lender was a lead arranger. Following Fang (2005) and Ross (2010), we distinguished the high-reputation banks (Big 3

Global) from the global syndicated bank group, which represented a

conservative test of our theoretical framework.

To capture the lead arranger’s accounting variables, we obtained bank financial statements from the BankScope database supplied by Bureau Van Dijk. BankScope provided sufficient firm-level accounting data on banks for our model estimation. Besides, we required the bank ownership structure details from the same database. Each choice case was required to include non-missing observations for both accounting and ownership information. For matching bank ownership data, we excluded samples from 1991 to 2000 due to their problematic ownership data. 7 To construct the variables required for our regression analyses, our final sample comprised 20,404 deals and 561 lead arrangers, after matching with BankScope and excluding cases with inadequate information on lead arrangers.

3.2. Descriptive statistics

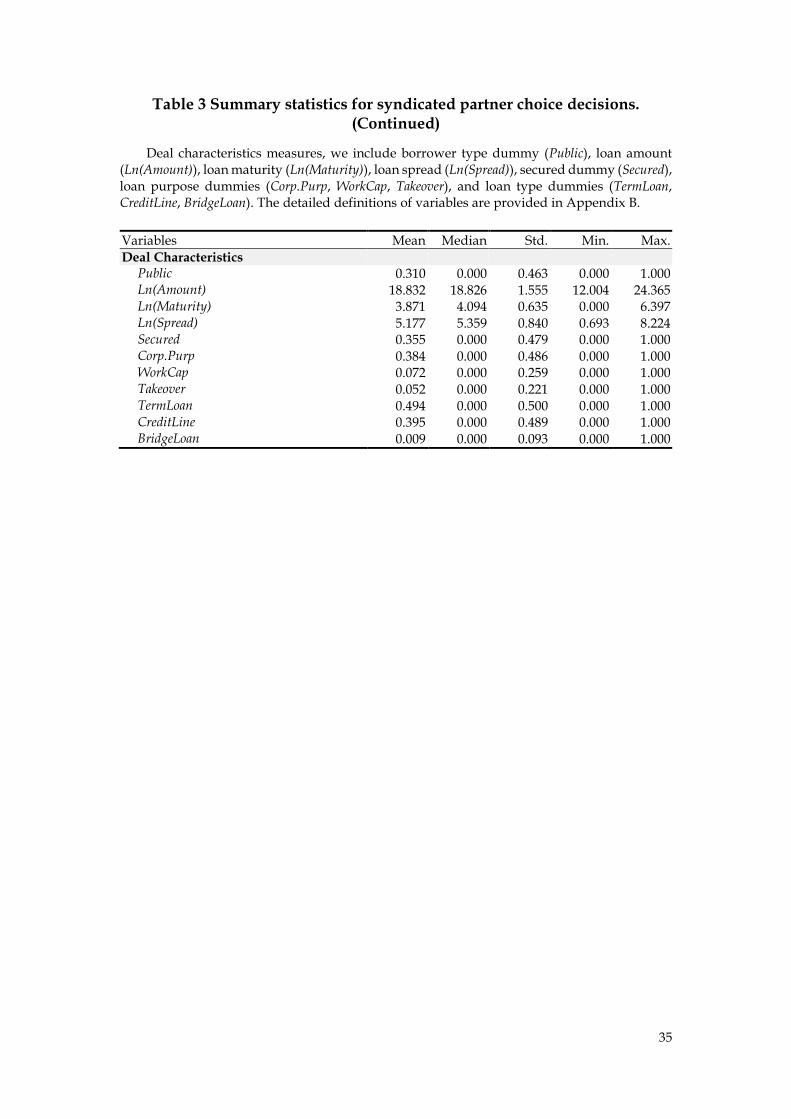

Table 3 provides summary statistics for the remaining 20,404 deals and 561 lead arrangers, and 26,422 choosing cases in the global syndicated loan market

7 BankScope only provides data on the historical bank’s shareholders from 2001 to 2014.

during 2001-2014. Table 3 shows the mean, median, standard derivation, minimum, and maximum of our variables. Given the different characteristics, there are five sets of variable characteristics: (1) our main dependent variable, (2) self-related variables, (3) task-related variables, (4) the lead arranger’s bank characteristics, and (5) deal characteristics. The mean of the likelihood of choosing a Big 3 participant bank is 0.28, and the mean of the likelihood of having the case arranged by the Big 3 lead arrangers is 0.05. This result indicates that most cases are not arranged by reputable banks. However, reputable banks are more likely to be the participant. Table 4 presents bivariate correlations for all of the study’s variables. We calculated conditioning indexes for all models, because some of the correlations in Table 4 are fairly high. The conditioning index using all independent variables has a value lower than 10, which is well below the critical value of 30, thus suggesting that multicollinearity is not a problem (Belsley, Kuh, and Welsch, 1980).

Table 5 presents the summary statistics of all variables used in the paper, for both subsamples of either choosing the Big 3 banks as partners or not. The former has 7,272 cases, and the latter has 19,150 cases. Table 4 shows the differences in all of the variables between the groups of having chosen and not chosen the Big 3. Table 5 supports our definition of the top bracket as the Big 3 partners by showing that the lead arrangers with low-status reputation, high operational diversity, low foreign, government, block ownership, and less ownership concentration, but without the use of the Big 4 auditors, are more likely to choose the Big 3 partners than partners from lower brackets. We also found that lead arrangers with lower market share, more experience with non-reputable partners, and more banks switched to the Big 3 partners are more likely to choose the Big 3 partners than partners from lower brackets. The results in table 5 show that self-related and task-related factors are the determinants of choosing Big 3 partners, and point out the effect of skills or knowledge complementarities.

【Insert Table 3】

【Insert Table 4】

【Insert Table 5】

4. The role of complementary factors in syndicate partner choices

Our participant bank choice model typically used a probit specification, where the dependent variable equaled one if a lead arranger used a Big 3 bank as a partner and zero if it used a non-Big 3 bank. In this setup, all Big 3 banks were treated as homogeneous. Since lead arrangers have self-related and task-related factors, this approach can observe the effect of these factors on syndicate partner choice decisions. All models considered the robust standard errors adjusted for deal clustering because deals syndicated by the same lead arranger might have been affected by the same unobserved deal factors and therefore

did not act completely independently of each other (White, 1980). We estimated the following maximum-likelihood probit regression model:

P(Big 3Global

)=α+β′Self-Related Measures+γ'Lead Arranger Characteristics

+δ'Deal Characteristics+BankSpecification

+Lead arranger's Country+Year Fixed Effect+ε

(1)

P(Big 3Global

)=α+∅′Task-Related Measures+γ'Lead Arranger Characteristics

+δ'Deal Characteristics+BankSpecification

+Lead arranger's Country+Year Fixed Effect+ε

(2)

where Self-Related Measures are self-related factors, including bank reputation (SelfBig3), auditor reputation (AuditorBig4), operational diversification (AssetDiversity, EarningDiversity, LoanConcentration), and ownership structure (Foreign, Government, Blockholder, OwnershipConcentration). Task-Related Measures are task-related factors, including market power (IndustryShare, CountryShare), experiences with non-reputable banks (EXPnonBig3_3Y, EXPnonBig3_5Y), and other banks’ activities (SwitchedBig3_Dum, SwitchedBig3_Num). Lead Arranger Characteristics are the lead arranger’s bank characteristic measures. We controlled for bank size (SIZE), capital adequacy (EA), asset quality (PLL), management performance (CI), earnings and profitability (ROE), and liquidity (LA, LD). Deal Characteristics are deal characteristic variables, such as borrower’s public status (Public), loan amount (Ln(Amount)), maturity (Ln(Maturity)), spread (Ln(Spread)), loan secured (Secured), loan purpose (Corp.Purp, WorkCap, Takeover), and loan type (TermLoan, CreditLine, BridgeLoan). The last set of variables controlled for some additional factors that could affect the demand for high-status partners. Since bank specification types may affect the choice, we controlled for the types of bank specification8 (BankSpecification) in our model. We also controlled for the lead arranger’s country fixed effects

(Lead arranger's Country) and year fixed effects (Year Fixed Effect) to isolate the effect of the skill complementarities.

4.1. Bank reputation and self-related complementarities

This section shows the regression results of equation (1). Table 6 presents the estimation results of the participant bank choice model. The main independent variable is the Big 3 partner. There is strong support for the self-related complementarities hypotheses, which stated that the lead arrangers that were more accountable to high self-reputation, high-reputation auditor, and less operational diversity were more likely to use high-reputation participant

8 BankScope groups banks into twelve specializations: savings banks, private commercial

banks, investment banks/securities houses, Islamic banks, specialized government credit institutions, Central banks, and multi-lateral governmental banks, etc.

banks. Model 1 shows that the lead arranger’s reputation variable is negative and significant, thus suggesting that complementarity in reputation-building through high-status bank reputation decreases the likelihood of the use of a Big 3 partner. This result is consistent with the findings of Fernando, Gatchev, and Spindt (2005). In Model 2, security analysts with high reputation is negative and significant, suggesting that credit accountability through analyst coverage decreases the demand for a Big 3 partner. The finding indicates that high-reputation auditors act as substitutes for high-reputation participant banks in the syndicated loan market, resulting in substantial cost savings. 9 Finally, Models 3-5 show that there is also strong support for our hypothesis, which stated that the lead arranger’s operational diversification increases the likelihood of a lead arranger’s choice of a high-reputation participant bank. In Models 3-4, asset diversity and earning diversity coefficients are positive and significant, indicating that the banks that operated with more diversity and had more diversification discounts were more likely to use a Big 3 partner. In Model 5, the coefficient of the loan concentration is negative and significant. The higher the loan concentration, and hence the more focus on one industry, the more likely lead arrangers will decrease their reliance on relationally embedded partners. These results also support diversification discounts, stating that the diversified banks will lead to more inefficient operation or lending and less valuable banks (Laeven and Levine, 2007). In Table 6, these coefficients have the expected sign and are strongly significant, indicating that self-related factors become more important for partner choice when credit accountability and operating ability complementarities, and hence the need for an information transfer between the lead arranger and the potential participant banks, are greater.

The control variables showed, unsurprisingly, that lead arrangers with a larger size, lower capital adequacy, and less profitability were more likely to use the Big 3 partners, thus confirming that lead arranger capacity is an important concern as well. We also controlled for contract characteristics, bank specification, and the country and year fixed effects in the models. With these variables controlled, the results are consistent with the findings of the previous predictions.

We have presented the manner in which the ownership structure, the self-related factor, affects the lead arranger’s participant bank choice decision in Table 7. Overall, the coefficients are consistent with our arguments in Section 2. The coefficients for foreign-owned and blockholder dummies are negative and significant, which suggests that bank efficiency variables are negatively related to the demand for high-status reputation partners. Model 5 considers the relation between ownership concentration and the extent of operating ability complementarity between the potential partner and the lead arranger. The coefficient has the expected sign and is strongly significant, indicating that

9 Corwin and Schultz (2005) argued that the book managers could limit the number of co-

managers to avoid competition and fees-sharing during the IPO process.

the ownership structure becomes more important for partner selection. Our argument is that the lead arranger with higher ownership concentration and more efficient operation will decrease its demand for high-status reputation partners. Taken together, these results provide strong support for our argument.

We also checked the robustness of our results by changing the ownership estimation elements of the test specification. The results of this robustness test are not tabulated in the paper. We estimated Models 1-4, as presented in Table 7, using the foreign-owned share held, government-owned share held, and blockholder share held to replace these ownership dummy variables. Our conclusions remain unchanged. The coefficients for foreign-owned share held and blockholder share held are negative and statistically significant in the partner choice regression. In terms of the coefficients on lead arranger characteristics, we found that lead arrangers with higher profitability were less likely to choose the high-reputation partners. We also controlled for contract, bank specification, country, and year fixed effects in our models in this robustness test. These findings support the view that the ownership structure of lead arrangers influences the demand for high-reputation participant banks. These results show the importance of self-related skills and operating ability in the participant bank choices of lead arrangers.

【Insert Table 6】

【Insert Table 7】

4.2. Bank reputation and task-related complementarities

Table 8 reports the probit regression results of equation (2). Models 1 and 2 introduce separately the market power variables between task-related skills and the participant bank choices. Most coefficients have the expected sign and are significant. Task-related skills and knowledge are more important for partner selection when the lead arrangers have less market power. Note that a higher market power lowers the demand for high-status reputation partners. These results provide support for our hypotheses.

Model 3 includes the experience with non-Big 3 partners to examine the extent of knowledge complementarity between the potential partner and the lead arranger. The coefficient of 3-years’ experience with non-Big 3 partners is significant and positive, indicating that the demand for high-status partners will increase when lead arrangers do not have experience with Big 3 partners. When we observe the coefficient of 5-years’ experience with non-Big 3 partners, the coefficient is negative but not significant. This result shows that the skills complementarity is less important for partner selection when a lead arranger has a long-term experience with non-Big 3 partners. The use of non-Big 3 partner services increasing the likelihood of using a Big 3 partner only occurred alongside short-term experiences, suggesting that the choice of a Big 3 partner depends on the experience with non-Big 3 services. The results in Model 3 are consistent with the finding of Levinthal and Fichman (1988). They found that the risk of breaking a bank relationship increases in the first four years of the relationship, after which it decreases.

There is a significant high-reputation participant bank need when other banks switch to the Big 3 partners. In Model 4, the coefficient of other bank activities shows that the demand for high-status reputation partners will increase when other banks switch to syndicate with the Big 3 partners. However, in Model 5, we also found a decreasing demand for high-status reputation partners when other banks have a large-scale switching layout. These results show an asymmetric herding behavior in partner choice decision. We found that herding is more likely to be present in the lower-scale switching layout. This implies that lead arrangers tend to herd to the part of other banks’ activities. The result of this test supports the arguments of Jain and Gupta (1987) and Bikhchandani, Hirshleifer, and Welch (1998).

Our models in Table 8 were controlled for the lead arranger’s characteristics, contract characteristics, bank specification, country and year fixed effects. Overall, most coefficients have the expected sign and are significant. Note that task-related complementarity plays an important role in partner choice decisions. Lead arrangers with more loan market experiences, and thus more skills and knowledge, are less likely to demand high-status reputation partners to establish a reputation.

【Insert Table 8】

5. Future research

5.1. Conditional logit regression analyses of syndicate partner choices for task-related complementarities

Most literatures have shown the relative importance of task-related dimensions to syndicate partner choice decisions. 10 We used McFadden’s choice model (McFadden, 1974) to estimate the impact of task-related complementarity on the demand for high-reputation partners, controlling for loan market experiences and other variables. This approach took advantage of the probit design of our data. We have data on 561 lead arrangers from 20,404 loan deals and 45,716 choice cases. Each lead arranger chose among the Big 3 or the non-Big 3; the variable Big3

Global indicates the reputation of the

participant for each alternative. We wanted to explore the relationship of the choices of Big3

Globaland nonBig3

Global to the lead arranger’s experience. We

also have information on the number of banks of each nationality in the lead arranger’s country in the variable, 𝐵𝑎𝑛𝑘𝑠 , that we wanted to include as a regression. We assumed that the lead arrangers’ preferences are influenced by the number of banks in an area but that the number of banks is not influenced by lead arranger preferences. The variable Banks is an alternative-specific variable, and loan market experience variables are case-specific variables. Each lead arranger’s chosen participant is indicated by the variable Choice. To that end, we estimated the following model of Choice:

Choicei:{Big 3Global

and nonBig 3Global

}

=ω'Banksi+ϵ'Task-Related Measures+γ'Lead Arranger Characteristics

+δ'Deal Characteristics+BankSpecification+Lead arranger's Country

+Year Fixed Effect+ε (3)

where Banks is the number of banks in each reputation group in a given loan year. Task-Related Measures are task-related factors, including market power (IndustryShare, CountryShare), experiences with non-reputable banks (EXPnonBig3_3Y, EXPnonBig3_5Y), and other banks’ activities (SwitchedBig3_Dum, SwithcedBig3_Num). Lead Arranger Characteristics are the lead arranger’s bank characteristic measures. We controlled for bank size (SIZE), capital adequacy (EA), asset quality (PLL), management performance (CI), earnings and profitability (ROE), and liquidity (LA, LD). Deal Characteristics are deal characteristic variability, such as borrower’s public status (Public), loan amount (Ln(Amount)), maturity (Ln(Maturity)), spread (Ln(Spread)), loan secured (Secured), loan purpose (Corp.Purp, WorkCap, Takeover), and loan type (TermLoan, CreditLine, BridgeLoan).

10 DeAngelo (1981), Geringer (1991), Vehn et al., (1997), Krigman, Shaw, and Womack (2001),

and Almazan (2002) pointed that industry expertise is a particularly important technical skill or resource in the financial intermediation industry, and it is a relatively important factor for a firm’s strategic.

The last set of variables controlled for some additional factors that can affect the demand for high-status partners. Since bank specification types may affect the choice, we controlled for the types of bank specification (BankSpecification) in our model. We also controlled for the lead arranger’s country fixed effects

(Lead arranger's Country) and year fixed effects (Year Fixed Effect) to isolate the effect of the skill complementarities.

Table 9 presents the results of the maximum likelihood conditional logit regression analysis. The main independent variable is a dummy variable that equals one if the partner is a Big 3, and zero if otherwise. We stated that lower levels of industry or country specialization increase the likelihood of lead arrangers using a particular Big 3 partner but that higher levels of such specialization decrease that likelihood. Models 1 and 2 show support for the argument that industry and country specialization decrease the demand for a high-status reputation partner. These results are consistent with the earlier results from using the probit choice model. We suggest that the industry and country specializations have a significantly stronger impact on partner choice.

Model 3 shows that short-term experience with non-Big 3 services, rather than long-term, affects the lead arrangers’ participant bank decisions. This finding states that the experience with non-Big 3 services increases the likelihood of using a particular Big 3 partner. The results of other banks’ activities influence partner choice decisions in Model 5. We found that other banks increase their switches to a Big 3 partner when involved with a lead arranger. These results confirm again that the role of other banks’ activities is more important in partner selection. Overall, in Table 9, the models are controlled for bank characteristics, contract characteristics, bank specification, country, and year fixed effects. The results remain unchanged. All task-related coefficients have the expected sign and are significant or highly significant. There is some indirect empirical support for the argument: the task-related variables are relatively important organizational factors.

【Insert Table 9】

5.2. The role of strength in bank reputation

We provide further evidence on the determinants of the role of strength in bank reputation in a multivariate setting. Table 10 reports the results of multinomial logit regressions of the type of bank reputation on empirical proxies for the strength of the reputation, such as country-level reputable banks and global-level reputable banks. We also controlled for other potential determinants of the partner choice, such as the lead arranger’s characteristics, loan characteristics, bank specification, country, and year fixed effects.

Specifically, we imputed the different types of reputation in the following multinomial logit regression:

ln [P(Big 3

Country, Big 3

Global)

P(nonBig 3)] =α+γ

1Related+R'Lead Arranger Characteristics

+S'Deal Characteristics+Bank specification

+Lead Arranger's Country +Year Fixed Effect+ε

(4)

The multinomial logit approach allowed us to distinguish and derive simultaneous comparisons among the determinants of country-level reputable (Big 3

Country), global-level reputable (Big 3

Global), and non-reputable (NonBig 3)

banks. For these models, columns (1) and (3) analyzed the probability of choosing locally reputable partners relative to non-reputable partners; columns (2) and (4) analyzed the probability of choosing nationally reputable partners relative to non-reputable partners. As regards Model 1, we argued that the foreign-owned and government-owned lead arrangers have different demands for different kinds of reputable partners. Foreign-owned lead arrangers could be more likely to choose country-level reputable partners, relative to non-reputable partners, due to the fact that foreign-owned banks have more information asymmetry than domestic-owned banks (Dell’Ariccia and Marquez, 2004; Giannetti and Laeven, 2012). Similarly, government-owned lead arrangers could prefer to choose the locally reputable partners, relative to non-reputable partners, indicating that the government-owned lead arrangers have home bias in local partners (Barth, Caprio, and Levine, 2001; Gordon and Li, 2003). In Model 2, we examined the broadened incentives of lead arrangers. The lead arrangers with lower market share will have the incentive to broaden their service line, and then increase their demand for locally or globally reputable banks as partners, relative to non-reputable banks. On the other hand, if the lead arrangers have more market power in the market, they would not demand more reputable banks as their partners. These arguments are consistent with the previous complementary need hypothesis.

To gauge the economic importance of our multivariate findings, we calculated the implied changes in the probability of choosing each type of reputable bank in the determinants of partner choice. The results regarding ownership variables are unchanged. We found that foreign-owned and government-owned lead arrangers not only prefer locally reputable banks, but also support the self-related complementary skills in the relative choices between nationally reputable and non-reputable partners. Regarding the task-related complementary skill test, in our second model, the results are also consistent with the previous findings.

5.3. Learning incentives on syndicate partner choices

In this section, we seek to elucidate the complementary needs by investigating the effects of a bank ranking change on partner choice decision. The major question in this study is whether the ranking change has

informational content or not. Our estimated coefficients are reported in Table 11. The ideal is that if the lead arranger has ranking changes in the market share, they will change their demand for a high-status reputation partner. Overall, our results from the partner choice probit model analyses indicate that the learning incentive and knowledge complementarity play an important role in choosing high-status reputation partners in the downgraded ranking. We found that a lower downgraded lead arranger leads to a greater probability of the demand for high-status reputation partners. A greater proportion of downgraded ranking does not affect the partner choice of lead arrangers. These results provide little evidence of knowledge complementarity with regards to partner choice decisions.

【Insert Table 10】

【Insert Table 11】

6. Conclusion

We extended the previous research (e.g. Sufi, 2007) by showing the importance of complementary skills to syndicate partner choice. First, complementarity is more important to partner selection decisions when the role of bank reputation is more important. Second, when knowledge complementarities between syndicate members are higher, bank reputation is more important to partner selection decisions. Third, demand for high-status reputation partners is less important when lead arrangers have established a reputation or skill in the organizational community.

Our study contributes to the literature in several ways. First, this study developed a complementary framework to analyze partner choices as a staged process whereby status and reputation determine which lead arrangers enter an active choice set and which lead arrangers from the choice set are ultimately chosen. We argued that the choice of high-reputation partners is important because it affects how external audiences view lead arrangers, whereas the choice of partners with higher reputation affects how well the additional resource needs of a borrowing firm are met. A lead arranger’s choice of the status bracket of syndicate partners depends on the extent to which the lead arranger is credit accountable to powerful external audiences that value partner quality, whereas the choice of a high-reputation partner depends on their complementary needs, such as self-related and task-related skills. We used the choice of the Big 3 partners to test our arguments and found that they received strong empirical support. Lead arrangers with lower status, operational/lending diversity, more ownership diversification, and no Big 4 auditors were more likely to use partners from the high-status bracket, whereas lead arrangers’ reputations concerning industry and country expertise and loan market experiences affected the partners used. Our empirical results provided initial evidence that our model represents a useful analytical framework with which to study partner choice in economic markets.

Second, our study contributes not only to research on partner choices, but also more broadly to recent research on the role of bank reputation. Our analysis indicated that when agency risk is higher, bank reputation becomes more important for selecting partners and allowing lead arrangers to expand their networks. This finding contributes to the literature examining conditions influencing the role of bank reputation in partner choice decisions. Sufi (2007) showed that information asymmetry induces lead arrangers to engage in repeat transactions with past partners, and to favor those with a similar status. Baum et al. (2005) found that firms’ performance relative to their aspiration levels determines the willingness to bear the risk of collaborating with unfamiliar partners. Further, Fernando, Gatchev, and Spindt (2005) examined co-manager choices in the syndicated loan market, and they argued that higher-reputation lead arrangers often choose lower-reputation partners. They found the complementary reputation in the syndicated loan market. We have contributed to this literature by using agency theory to identify the additional factors that influence the role of bank reputation in partner choice decisions. In our setting, we considered how general issues relating to asymmetric information, uncertainty, knowledge complementarities, and reputation can lead to changes in interbank networks. We believe that these insights have implications that go beyond the specifics of the empirical context used in this study. Our research resonates with other contexts such as underwriter choice, financing of movies, joint ventures, joint R&D projects, mergers and acquisitions decisions, and other forms of inter-cooperation. By reintroducing partner selection decision-making, future research can explore a whole range of mechanisms that explain tie formation in cooperation.

Third, we have contributed to the syndicated loan market literature (Sufi, 2007; Fernando, Gatchev, and Spindt, 2005) by showing how lead arrangers form interbank relationships. Our research indicated that reliance on trusted partners, through bank reputations, is one potential response to agency problems. Further, information asymmetry problems with borrowing firms are more severe, and hence ex-ante contracting and ex-post monitoring by the lead arrangers and partners are more difficult; lead arrangers are more likely to select reputable partners. This is particularly important when firms are more interdependent because of knowledge complementarities that introduce knowledge asymmetries. In addition, our finding showed that the reputation of partners mitigates the risk of opportunism. In our self-related results, this finding indicated that a partner’s reputational capital may have an important role for an inefficient lead arranger.

Our study has limitations that present opportunities for future research. First, we showed that reputation is a signal of a bank’s quality. However, it is difficult to distinguish among the effects of reputation and network centrality. Robinson and Stuart (2007) pointed out that a firm’s past behavior cannot be observed publicly but that this information can be transmitted through relationships. In this paper, we did not examine how relationships affect partner choice decisions. For future research in the next paper, we will try to

investigate whether distances play an important role in syndicate partner choices. Furthermore, we will also examine the impact of bank competition on the demand for high-status reputation partners by observing the distance between borrowing firms and closest competitors.

Second, borrowing firms in a syndicated loan are involved in the management of the syndicate members. Our paper, however, did not examine the outcomes of this syndicated monitoring for borrowing firms. Although our findings are consistent with those of previous studies on firm collaborations, we showed that reputation is an important driver of partner selection in the syndicated loan market. Further, agency problems at the level of the underlying alliance are an important source of conflicts between syndicate partners. Because of the highly uncertain and risky settings and the associated high levels of outcome uncertainty, monitoring is often complicated, as it is difficult and costly to verify the actions of managers (Park and Ungson, 2001). Investigating how the nature of the syndicate member and the agency problems impact the choice of partners is a useful area for future research.

Third, in syndicated loans, one formal way to deal with the agency problems between lead arrangers and partners is to provide partner firms with sufficient ownership shares of loans to create the appropriate incentives to act in the best interest of the other syndicate members (Wright and Lockett, 2003). However, we did not have access to detailed information on the loan allocation distribution between different members of the syndicate. Future research could examine to what extent formal and informal mechanisms act as enhancers to align the incentives between syndicate members in collaborations.

In closing, our study illustrated the usefulness of analyzing the choice of syndicate partners in economic markets as a staged process in which status and reputation play different roles. We argued that lead arrangers pick a particular status bracket depending on their credit accountability (self-related) and loan market experiences (task-related) to external audiences and then choose a particular reputable partner. Our study therefore represents an important bridge between research focusing on staged decision models, research focusing on status and reputation as signals of quality, and research focusing on the formation of complementary needs by showing that status and reputation are both important at different stages of the choice process.

References

Acharya, V. V., Hasan, I., and Saunders, A. (2006). Should Banks Be Diversified?

Evidence from Individual Bank Loan Portfolios. The Journal of Business,

79(3), 1355-1412.

Al-Khalifa, A. K., and Eggert Peterson, S. (1999). The partner selection process

in international joint ventures. European Journal of Marketing, 33(11/12),

1064-1081.

Almazan, A. (2002). A model of competition in banking: Bank capital vs

expertise. Journal of Financial Intermediation, 11(1), 87-121.

Awadzi, W. K. (1987). Determinants of joint venture performance: a study of

international joint ventures in the United States (Doctoral dissertation,

Louisiana State University and Agricultural and Mechanical College).

Ball, R. (2001). Infrastructure requirements for an economically efficient system

of public financial reporting and disclosure. Brookings-Wharton papers on

financial services, 2001(1), 127-169.

Barro, R. J. (1986). Reputation in a model of monetary policy with incomplete

information. Journal of Monetary Economics, 17(1), 3-20.

Baum, J. A., Rowley, T. J., Shipilov, A. V., and Chuang, Y. T. (2005). Dancing

with strangers: Aspiration performance and the search for underwriting

syndicate partners. Administrative Science Quarterly, 50(4), 536-575.

Berger, A. N., and Bouwman, C. H. (2013). How does capital affect bank

performance during financial crises?. Journal of Financial Economics,

109(1), 146-176.

Berle, A. A., and Means, G. G. C. (1991). The modern corporation and private

property. Transaction publishers.

Bikhchandani, S., Hirshleifer, D., and Welch, I. (1998). Learning from the

behavior of others: Conformity, fads, and informational cascades. The

Journal of Economic Perspectives, 151-170.

Bolton, G. E., Katok, E., & Ockenfels, A. (2005). Cooperation among strangers

with limited information about reputation. Journal of Public Economics,

89(8), 1457-1468.

Bonin, J. P., Hasan, I., and Wachtel, P. (2005). Bank performance, efficiency and

ownership in transition countries. Journal of Banking and Finance, 29(1),

31-53.

Boot, A. W., and Thakor, A. V. (1993). Self-interested bank regulation. The

American Economic Review, 206-212.

Buch, C. M. (1997). Opening up for foreign banks: How Central and Eastern

Europe can benefit1. Economics of Transition, 5(2), 339-366.

Bushman, R. M., and WITTENBERG‐MOERMAN, R. E. G. I. N. A. (2012). The

role of bank reputation in “certifying” future performance implications of

borrowers’ accounting numbers. Journal of Accounting Research, 50(4),

883-930.

Cantillo, M., and Wright, J. (2000). How do firms choose their lenders? An

empirical investigation. Review of Financial studies, 13(1), 155-189.

Chemmanur, T. J., and Fulghieri, P. (1994). Reputation, renegotiation, and the

choice between bank loans and publicly traded debt. Review of Financial

Studies, 7(3), 475-506.

Choi, J. P., and Jeon, D. S. (2007). A leverage theory of reputation building with

co-branding: Complementarity in reputation building. Available at SSRN

1002882.

Claessens, S., and Laeven, L. (2004). What drives bank competition? Some

international evidence. Journal of Money, Credit and Banking, 563-583.

Corwin, S. A., and Schultz, P. (2005). The role of IPO underwriting syndicates:

Pricing, information production, and underwriter competition. The

Journal of Finance, 60(1), 443-486.

DeAngelo, L. E. (1981). Auditor size and audit quality. Journal of accounting

and economics, 3(3), 183-199.

Diamond, D. W. (1991). Monitoring and reputation: The choice between bank

loans and directly placed debt. Journal of political Economy, 689-721.

Drakos, K. (2003). Assessing the success of reform in transition banking 10

years later: an interest margins analysis. Journal of Policy Modeling, 25(3),

309-317.

Fang, L. H. (2005). Investment bank reputation and the price and quality of

underwriting services. The Journal of Finance, 60(6), 2729-2761.

Fernando, C. S., Gatchev, V. A., and Spindt, P. A. (2005). Wanna dance? How

firms and underwriters choose each other. The Journal of Finance, 60(5),

2437-2469.

Fichman, M., and Levinthal, D. A. (1991). Honeymoons and the liability of

adolescence: A new perspective on duration dependence in social and

organizational relationships. Academy of Management Review, 16(2), 442-

468.

Fries, S., and Taci, A. (2005). Cost efficiency of banks in transition: Evidence

from 289 banks in 15 post-communist countries. Journal of Banking and

Finance, 29(1), 55-81.

Fu, F., Hauert, C., Nowak, M. A., and Wang, L. (2008). Reputation-based

partner choice promotes cooperation in social networks. Physical Review

E, 78(2), 026117.

Geringer, J. M. (1991). Strategic determinants of partner selection criteria in

international joint ventures. Journal of international business studies, 41-

62.

Gopalan, R., Nanda, V., and Yerramilli, V. (2011). Does poor performance

damage the reputation of financial intermediaries? Evidence from the loan

syndication market. The Journal of Finance, 66(6), 2083-2120.

Gould, R. V. (2002). The Origins of Status Hierarchies: A Formal Theory and

Empirical Test1. American journal of sociology, 107(5), 1143-1178.

Iannotta, G., Nocera, G., and Sironi, A. (2007). Ownership structure, risk and

performance in the European banking industry. Journal of Banking and

Finance, 31(7), 2127-2149.

Jain, A. K., and Gupta, S. (1987). Some evidence on" herding" behavior of US

banks. Journal of Money, Credit and Banking, 78-89.

Jensen, M. C., and Meckling, W. H. (1976). Theory of the Firm: Managerial

Behavior, Agency Costs and Ownership Structure. Journal of Financial

Economics, 3(4), 305-360.

Jensen, M., and Roy, A. (2008). Staging exchange partner choices: When do

status and reputation matter?. Academy of Management Journal, 51(3),

495-516.

Krigman, L., Shaw, W. H., and Womack, K. L. (2001). Why do firms switch

underwriters?. Journal of Financial Economics, 60(2), 245-284.

Laeven, L., and Levine, R. (2007). Is there a diversification discount in financial

conglomerates?. Journal of Financial Economics, 85(2), 331-367.

Levinthal, D. A., and Fichman, M. (1988). Dynamics of interorganizational

attachments: Auditor-client relationships. Administrative Science

Quarterly, 345-369.

Lewellen, K. (2006). Risk, reputation, and IPO price support. The Journal of

Finance, 61(2), 613-653.

Li, D., Eden, L., Hitt, M. A., and Ireland, R. D. (2008). Friends, acquaintances,

or strangers? Partner selection in R&D alliances. Academy of Management

Journal, 51(2), 315-334.

Ljungqvist, A., Marston, F., and Wilhelm, W. J. (2006). Competing for securities

underwriting mandates: Banking relationships and analyst

recommendations. The Journal of Finance, 61(1), 301-340.

McFadden, D. (1974). The measurement of urban travel demand. Journal of

public economics, 3(4), 303-328.

Mehran, H., Morrison, A. D., and Shapiro, J. D. (2011). Corporate governance

and banks: What have we learned from the financial crisis?. FRB of New

York Staff Report, (502).

Park, S. H., and Ungson, G. R. (2001). Interfirm rivalry and managerial

complexity: A conceptual framework of alliance failure. Organization

science, 12(1), 37-53.

Roberts, P. W., and Dowling, G. R. (2002). Corporate reputation and sustained

superior financial performance. Strategic management journal, 23(12),

1077-1093.

Robinson, D. T., and Stuart, T. E. (2007). Network effects in the governance of

strategic alliances. Journal of Law, Economics, and Organization, 23(1),

242-273.

Ross, D. G. (2010). The “dominant bank effect:” How high lender reputation

affects the information content and terms of bank loans. Review of

Financial Studies, hhp117.

Shane, S., and Cable, D. (2002). Network ties, reputation, and the financing of

new ventures. Management Science, 48(3), 364-381.

Shehzad, C. T., de Haan, J., and Scholtens, B. (2010). The impact of bank

ownership concentration on impaired loans and capital adequacy. Journal

of Banking and Finance, 34(2), 399-408.

Shleifer, A., and Vishny, R. W. (1986). Large shareholders and corporate control.

The Journal of Political Economy, 461-488.

Sufi, A. (2007). Information asymmetry and financing arrangements: Evidence

from syndicated loans. The Journal of Finance, 62(2), 629-668.

Vehn, B. K., Carcello, J. V., Hermanson, D. R., and Hermanson, R. H. (1997).

The determinants of audit client satisfaction among clients of big 6 firms.

Watts, R. L., and Zimmerman, J. L. (1990). Positive accounting theory: a ten year

perspective. Accounting review, 131-156.

Watts, R., and Zimmerman, J. (1981). The markets for independence and

independent auditors. Unpublished manuscript (University of Rochester,

Rochester, NY).

Weigelt, K., and Camerer, C. (1988). Reputation and corporate strategy: A

review of recent theory and applications. Strategic Management Journal,

9(5), 443-454.

White, H. (1980). A heteroskedasticity-consistent covariance matrix estimator

and a direct test for heteroskedasticity. Econometrica: Journal of the

Econometric Society, 817-838.

Wilson, R. (1985). Reputations in games and markets. Game-theoretic models

of bargaining, 27-62.

Wright, M., and Lockett, A. (2003). The Structure and Management of Alliances:

Syndication in the Venture Capital Industry*. Journal of Management

Studies,40(8), 2073-2102.

Yasuda, A. (2005). Do Bank Relationships Affect the Firm's Underwriter Choice

in the Corporate? Bond Underwriting Market?. The Journal of Finance,

60(3), 1259-1292.

Appendix A The Reputable Participant Bank effect on Lead arranger’s stock price response.

Sample of loan announcements from 1991 to 2014 in US syndicated loan market. Global Big 3 participants (Big3

Global) are where the participant is national-level top 3 banks in syndicate loan

market. Country Big 3 participants (Big3Country

) are where the participant is country-level top 3

banks in each local syndicate loan market. Industry Big 3 participants (Big3Industry

) are where

the participant is industry-level top 3 banks in each industry syndicate loan market. National Big 3 participants (SelfBig3) are where the lead arranger is global-level top 3 banks in syndicate loan market. Panel A report full sample result. Subsample result in Panel B. Panel C presents the results for different status lead arrangers choose different status partners. The marks a, b, and c indicate significance at the 1%, 5%, and 10% level, respectively.

Number of loans

Mean Cumulative Abnormal Return

Precision Weighted CAAR

Z-Statistic Percent positive

Panel A: Full sample

Total 1,795 0.08% 0.19% 2.160b 0.47

Panel B: Reputation Status of Participant Banks

Big3Global

1,214 0.28% 0.41% 4.050a 0.50

Big3Country

1,288 0.27% 0.38% 3.795a 0.49

Big3Industry

1,233 0.17% 0.30% 2.938a 0.47