the effectiveness of key performance indicators to …

TRANSCRIPT

0

THE EFFECTIVENESS OF KEY PERFORMANCE

INDICATORS TO MANAGE CLEARING

TRANSACTIONS OPERATIONAL

RISK IN BANK BUKOPIN

PONTIANAK

By

Cesy Iola Kariza 014201100206

A Skripsi presented to the

Faculty of Business President University

in partial fulfillment of the requirements for

Bachelor Degree in Economics Major in Management

February 2015

i

PANEL OF EXAMINERS

APPROVAL SHEET

The Panel of Examiners declare that the Skripsi entitled

“THE EFFECTIVENESS OF KEY

PERFORMANCE INDICATORS TO MANAGE

CLEARING TRANSACTION OPERATIONAL

RISK IN BANK BUKOPIN PONTIANAK” that was

submitted by Cesy Iola Kariza majoring in Management

from the Faculty of Business was assessed and approved

to have passed the Oral Examinations on February 3rd,

2015.

Ir. Yunita Ismail Masjud, M.Si

Chair - Panel of Examiners

Ir. Erny Hutabarat, MBA

Examiner I

Rosita Widjojo, SE., MBA., CRMP

Examiner I

ii

SKRIPSI ADVISER

RECOMMENDATION

LETTER

This Skripsi entitled “THE EFFECTIVENESS OF KEY

PERFORMANCE INDICTORS TO MANAGE

CLEARING TRANSACTION OPERATIONAL RISKS

IN BANK BUKOPIN PONTIANAK” prepared and

submitted by Cesy Iola Kariza in partial fulfillment of the

requirements for the degree of Bachelor of Economics in the

Faculty of Business has been reviewed and found to have

satisfied the requirements for a Skripsi fit to be examined. I

therefore recommend this Skripsi for Oral Defense

Cikarang, Indonesia, 22 January 2015

Acknowledged by, Recommended by,

Vinsensius Jajat Kristanto SE., MM., MBA. Rosita Widjojo, SE., MBA., CRMP

Head, Management Study Program Advisor

iii

DECLARATION OF

ORIGINALITY

I declare that this Skripsi, entitled “THE EFFECTIVENESS OF KEY

PERFORMANCE INDICATORS TO MANAGE CLEARING

TRANSACTION OPERATIONAL RISK IN BANK BUKOPIN

PONTIANAK” is, to the best of my knowledge and belief, an original

piece of work that has not been submitted, either in whole or in part, to

another university to obtain a degree.

Cikarang, Indonesia, January 22nd 2015

Cesy Iola Kariza

iv

ABSTRACT

The objectives of the research is to find out the operational risks in clearing

transaction, the key performance indicators to manage operational risk, and to find

out the effectiveness of key performance indicators to minimize the operational risk

in clearing transaction in Bank Bukopin Pontianak. Research method used is

qualitative. The significance of study for this research is to analyze the

effectiveness of Bank Bukopin Pontianak KPIs, moreover it is expected to be

recommendation for implementing research activities in the same field in the

future. This research is expected to give contribution to Bank Bukopin Pontianak

as consideration for additional KPIs that might minimize the risk rate. This research

is also conducted to analyze the Key Performance Indicators for banking operation,

and focused in how effective that Key Performance Indicators in minimizing risk

in clearing transaction in Bank Bukopin Pontianak. That KPIs is effective since the

clearing risk rate is 1% compared to the clearing standard which is 5%.

Keywords: clearing transaction, risk, key performance indicators.

v

ACKNOWLEDGEMENT

First of all, the researcher would like to say deep gratitude to the presence

of Allah SWT and Muhammad SAW for His grace and blessing so that the

researcher could finish and complete the skripsi successfully. This research is

written as for the completion in the end of academic program to gain Bachelor

Degree of Economic.

In this chance, the researcher would like to say thank you to all who have

helped finish this research;

1. Researcher parents, Rizal and Kartika Dewi, who spiritually and mentally

support and motivate the researcher to finish the research, also researcher

brother, Fajar Muhammad Pramudia, who support the researcher until

finish.

2. Ms. Rosita Widjojo, as advisor, thank you for your guidance, attention,

suggestion, help, and motivation to the researcher until finish the research.

3. Bank Bukopin officers, Mr. Mars Satrio, Mr. Hadi Sandiar, Ms.Risma, Ms.

Ridha, by sparing time to help the researcher to find information to finish

the research.

4. Ms. Marie Ann, thank you so much for the lecturers that you gave to me.

You are a good and fun lecturer.

5. Researcher best friends, Rizki Andira Lauria, who always gives support and

believe in researcher.

6. Gita Kurniasari Sitorus, who always makes the researcher laugh.

7. Ulya Yuthika, who always support and help the researcher.

8. Mazaya Ulfa Rahmatina, Ira Yuli Rodame, Rinda Putri Sari, Suri Hidayat,

and Ety, who always be there and help the researcher.

9. Bilingual Friends, Maulidya Elsera, Reksy Indra Rakasiwie, Aditya

Putrawan, Syf. Suci Armilia, Mafisah, Yustina Octifanny, Zulfadila Hira

Permana, Susilo Nur Aji, Bimo Eka Putra, Raisa Nabila, Satria Nugroho,

and Ghina Khalida.

vi

10. Grandma, Zubaidah, who always sends prayers to the researcher.

11. Everyone who cannot be named one by one to help researcher to finish the

research. Thank you for the support.

Finally, researcher hope this research can be beneficial to the development

of knowledge, especially in risk management.

vii

TABLE OF CONTENTS

Page

PANEL OF EXAMINERS APPROVAL SHEET ................................................... i

SKRIPSI ADVISER RECOMMENDATION LETTER ........................................ ii

DECLARATION OF ORIGINALITY .................................................................. iii

ABSTRACT ........................................................................................................... iv

ACKNOWLEDGEMENT ...................................................................................... v

TABLE OF CONTENTS ...................................................................................... vii

LIST OF TABLES ................................................................................................. ix

LIST OF FIGURES ................................................................................................ x

LIST OF ACRONYMS ......................................................................................... xi

CHAPTER I INTRODUCTION ............................................................................. 1

1.1. Background of Study ....................................................................................... 1

1.2. Problem Identification ..................................................................................... 3

1.3. Statement of The Problem ............................................................................... 3

1.4. Research Objectives ........................................................................................ 4

1.5. Definition of Terms ......................................................................................... 4

1.6. Scope and Limitations ..................................................................................... 5

1.7. Research Benefits ............................................................................................ 5

CHAPTER II REVIEW OF LITERATURE .......................................................... 7

2.1 Theoretical Review ......................................................................................... 7

2.1.1. Key Performance Indicator ............................................................................... 7

2.1.2. The Banking Industry ..................................................................................... 14

2.1.3. Clearing ........................................................................................................... 16

2.1.4. Risk ................................................................................................................. 17

2.1.5. Operational Risk by Basel II ........................................................................... 23

2.2 Subject of Case Study ................................................................................... 25

2.3 Review of Related Research ......................................................................... 25

2.4 Theoretical Framework ................................................................................. 28

viii

CHAPTER III RESEARCH METHODOLOGY ................................................. 32

3.1. Research Questions ....................................................................................... 32

3.2. Setting ........................................................................................................... 33

3.3. Population ..................................................................................................... 34

3.4. Data Source ................................................................................................... 34

3.5. Ethical Consideration .................................................................................... 35

3.6. Research Design ............................................................................................ 35

3.7. Interview Instrument and Protocol ................................................................ 36

3.8. Data Analysis Strategy .................................................................................. 38

3.9. Summary ....................................................................................................... 40

CHAPTER IV ANALYSIS AND INTERPRETATION ...................................... 42

4.1. Company Profile ........................................................................................... 42

4.1.1. Vision and Mission ................................................................................... 42

4.1.2. Corporate Value ........................................................................................ 43

4.1.3. Corporate Subsidiary ................................................................................ 44

4.2. Data Analysis and Interpretation of Result ................................................... 44

CHAPTER V CONCLUSION AND RECOMMENDATION ............................. 62

5.1 Conclusion ..................................................................................................... 62

5.2. Recommendation ........................................................................................... 63

REFERENCES ..................................................................................................... 64

APPENDICES ...................................................................................................... 66

ix

LIST OF TABLES

Page

TABLE 2.1 ELEMENTS OF A KPI ...................................................................... 9

TABLE 2.2 DEFINITION OF RISK .................................................................... 18

TABLE 3.1 SAMPLE INTERVIEW QUESTIONS ............................................ 37

TABLE 4.1 CLEARING PARTICIPANTS IN PONTIANAK ............................ 45

TABLE 4.2 THE DIFFERENCES BETWEEN RTGS AND CLEARING ......... 51

TABLE 4.3 FAILED CLEARING TRANSACTION IN BANK BUKOPIN

PONTIANAK .................................................................................... 54

TABLE 4.4 TEN CHARACTERISTICS HIGH IMPACT KPIS OF BANK

BUKOPIN PONTIANAK ................................................................. 58

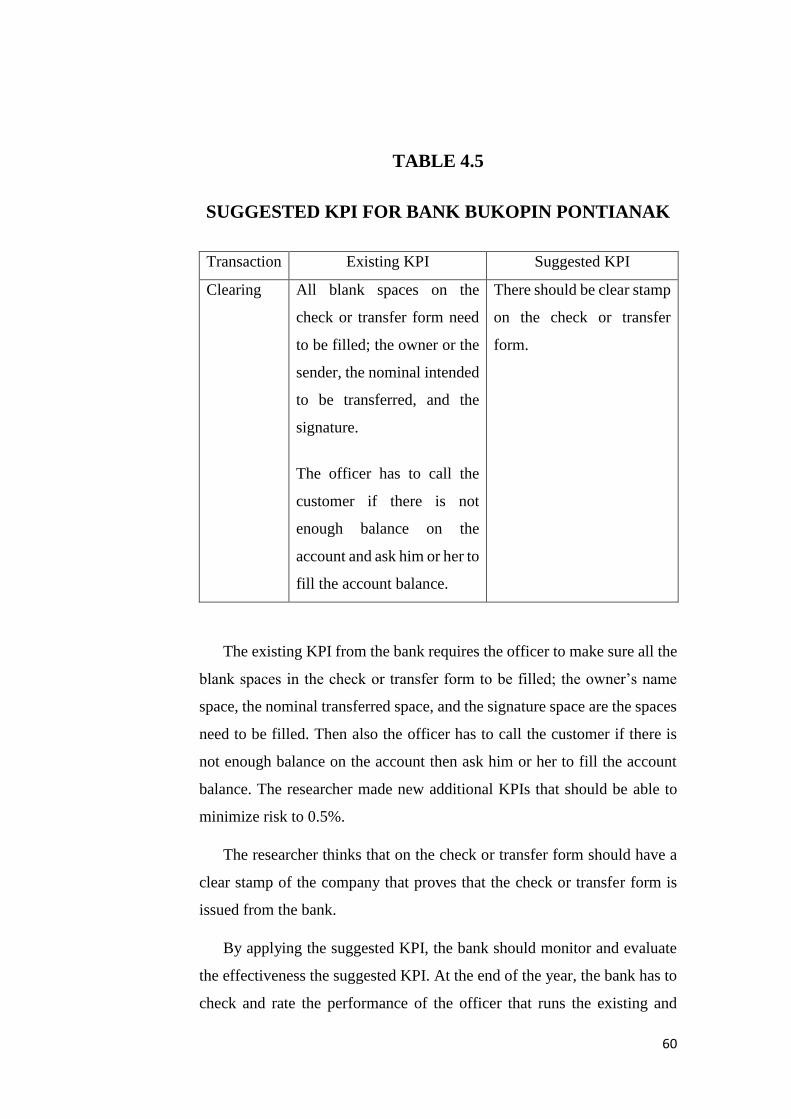

TABLE 4.5 SUGGESTED KPIS FOR BANK BUKOPIN PONTINAK ............ 60

x

LIST OF FIGURES

Page

FIGURE 2.1 A QUANTIFIED APPROACH TO OPERATIONAL RISK

MANAGEMENT ACCORDING TO BASEL II ............................... 24

FIGURE 4.1 CLEARING FLOWCHART ........................................................... 47

FIGURE 4.2 CLEARING PATTERN .................................................................. 50

xi

LIST OF ACRONYMS

Acronym Meaning Page

ATM Automated Teller Machine 1

BCA Bank Central Asia 48

BI Bank Indonesia 32

CCP Central Counter Party 17

KPI Key Performance Indicator 2

MSME Micro, Small, Medium Enterprise 42

RTGS Real Time Gross Settlement 2

SOP Standard Operating Procedure 34

1

CHAPTER I

INTRODUCTION

1.1. Background of Study

The banking industry has important roles as to provide customers with

a variety of services and options. The major roles of a bank are mainly

investing, borrowing, and storing money. Banks involve in transferring

funds from savers to borrowers, or from one party to another party. Banks

also involve in paying for goods and services. Usually customers will use

bank-supplied checks, credit or debit cards, or mobile banking service that

provided by the bank. Banks are the principal source of credit (loanable

funds) for millions of individuals, families and government as well. Banks

also serve people with the source of short-term working capital for

businesses; either it is small, medium, or large-sized business. Besides that,

banks also serve people for long-term business loan to finance the company

or to purchase new plant and equipment.

There is no difference in Bank Bukopin. Bank Bukopin also provides a

safe place to invest, borrowing, and storing money. The bank provides

various products to support different needs of the customers. In Bank

Bukopin Pontianak, there are only some divisions, such as Operational

Division, Credit Division, Human Resource Division, and Marketing

Division. These divisions have their own jobs to be done every day to

process transactions. Operational Division’s main job is to process every

transaction that occurred in the Front Office. There are six employees that

work behind the Back Office. They are the coordinator of the back office,

his assistant, the coordinator of tellers and customer services, the helper for

customer services, the ATM personnel, and the personnel who is in charge

in doing transfer, Real Time Gross Settlement (RTGS), clearing, and

2

collection. Some of these people work from Monday to Saturday to make

sure every job that is assigned to them is running well.

The coordinator of teller and customer service’s job is to process and

double-check any transaction that happened in the Front Office. This

personnel is the one who gives approvals to every transaction done by the

tellers and customer services. The helper for customer services’ job is to

make check-book and transfer form based on the request from the customer

that visited in the customer service’s desk. The helper is also the one who

is responsible in safe deposit box borrowing, and also the one who makes

the report. The ATM personnel is responsible in everything related to the

ATM machine. Then, the personnel in charge of transfer, RTGS, clearing,

and collection is responsible to related transaction. All of these are

supervised by the coordinator of the Back Office.

These jobs come with procedures that the employees should follow.

Following the standard that been set before might help the bank to achieve

their objectives. Besides that, every company needs Key Performance

Indicators (KPIs) to help them to define and measure progress toward

organization objectives. Indeed first thing the company did was set their

objectives. After setting their objectives, the company surly set their KPI to

define and measure progress towards their objectives. Besides that, the KPIs

are also needed to reduce the risk that might happens within the process to

the company objectives. There are some risk that might interfere Bank

Bukopin Pontianak. There are many types of risks that might interfere in

banking industry. There are credit risk, liquidity risk, interest rate risk,

operational risk, exchange risk, and crime risk.

In operational division Bank Bukopin Pontianak, the risk that might

interfere is the operational risk. The operational risk can occurred by the

failures of people, processes, systems, and external events. In Bank

Bukopin Pontianak, the failure in clearing transaction is rarely happens. In

2012 there was no failed clearing transaction. In 2013 there was only 1

3

failed clearing transaction happened. The next year, in 2014 the failed

clearing transaction became 2 transactions.

1.2. Problem Identification

In Bank Bukopin Pontianak, there is a particular procedure of how

clearing transaction should be processed. Besides having procedure, having

Key Performance Indicators are also a necessity for every company,

nevertheless Bank Bukopin Pontianak. Having KPIs might avoid risks and

might support the bank to achieve its objectives. The failed clearing

transactions are increasing year by year. Despite of that, the risk rate of

clearing transaction is not getting close to the risk rate for clearing

transaction that is set by the bank. Therefore, in this study the researcher

intended to analyze how effective are Key Performance Indicators to

minimize the clearing transaction operational risk in Bank Bukopin

Pontianak.

Based on the problem above, the title of this study will be “THE

EFFECTIVENESS OF KEY PERFORMANCE INDICATORS TO

MANAGE CLEARING TRANSACTION OPERATIONAL RISK IN

BANK BUKOPIN”.

1.3. Statement of The Problem

Specifically this study aims to answer the following question:

1. What are the operational risks in clearing transaction in Bank Bukopin

Pontianak?

2. Which key performance indicators to manage operational risk in

clearing transaction in Bank Bukopin Pontianak?

3. How effective are these key performance indicators to minimize the

operational risk in clearing transaction in Bank Bukopin Pontianak?

4

1.4. Research Objectives

Based on the preceding research question, the research objective of the

study can be translated as follow:

1. To find out the operational risk in clearing transaction in Bank Bukopin.

2. To find out which key performance indicators to manage operational

risk in clearing transaction in Bank Bukopin.

3. To find out the effectiveness of key performance indicators to minimize

the operational risk in clearing transaction in Bank Bukopin.

1.5. Definition of Terms

Terms used in this research as follows:

Banking Operation

The legal transactions executed by a bank in its daily business, such as

providing loans, mortgages and investments, depending on the focus and

size of the bank.

Operational Risk

A form of risk that summarizes the risks a company or firm undertakes

when it attempts to operate within a given field or industry.

Operational risk is the risk that is not inherent in check or transfer form,

systematic or market-wide risk. It is the risk remaining after determining

financing and systematic risk, and includes risks resulting from breakdowns

in internal procedures, people and systems. It is also defined as the risk of

loss resulting from inadequate or failed processes, people, and systems or

from external events.

Key Performance Indicator

Performance measurement is a fundamental principle of management. The

measurement of performance is important because it identifies current

5

performance gaps between current and desired performance and provides

indication of progress towards closing the gaps.

Clearing

Movement of a check from the bank in which it was deposited to the bank

on which it was drawn, and the movement of its face amount in the opposite

direction. This process (called 'clearing cycle') normally results in a credit

to the account at the bank of deposit, and an equivalent debit to the account

at the bank on which it was drawn.

1.6. Scope and Limitations

Scope

This study is conducted to analyze the key performance indicators for

clearing transaction.

Limitations

This study is focused in how effective are the existing Key Performance

Indicators in clearing transaction in Bank Bukopin Pontianak.

1.7. Research Benefits

This research can hopefully deliver new knowledge, information, and

suggestions for:

1. Bank Bukopin Pontianak

The output of this research could be useful to the bank as they can

improve their performance and their capabilities to manage operational

risks that might happen anytime.

6

2. The University

To increase the knowledge in the field of banking risk management,

specifically in key performance indicators.

3. Researcher

To find out what are the key performance indicators that can work to

manage operational risk in Bank Bukopin Pontianak.

4. The Future Researcher

The output of the research would become a reference and additional

knowledge to those who would like to do future research about the

analysis of key performance indicators to manage operational risk in

banks.

7

CHAPTER II

REVIEW OF LITERATURE

2.1 Theoretical Review

2.1.1. Key Performance Indicator

Key Performance Indicators (KPIs) are the vital navigation instruments

used by managers to understand whether their business is on a successful

voyage or whether it is veering off the prosperous path (Marr, 2012). A KPI

is a metric measuring how well the organization or an individual performs

an operational, tactical or strategic activity that is critical for the current and

future success of the organization (Eckerson, 2009).

Key performance indicators are financial and non-financial indicators

that organizations use in order to estimate and fortify how successful they

are, aiming previously established long lasting goals. Appropriate selection

of indicators that will be used for measuring is of a greatest importance.

Process organization of business is necessary to be constitute in order to

realize such effective and efficient system or performance measuring via

KPI. Process organization also implies customer orientation and necessary

flexibility in nowadays condition of global competition (Velimirovic,

Vilimiroic, and Stankovic, 2011).

Key performance indicators are the measurement that help an

organization define and measure progress toward organization goals. Once

an organization has analyzed its mission, identified all its stakeholders, and

defined its goals, it needs a way to measure progress toward those goals.

(management.about.com, 2014). KPIs is critical components of all earned

value measurement systems. Terms such as cost variance, schedule

variance, schedule performance index, cost performance index, and time or

8

cost at completion are actually KPIs if used correctly but not always

referred to as such. The need for these KPIs is simple: what gets measured

gets done. If the goal of a performance measurement system is to improve

efficiency and effectiveness, then the KPI must reflect controllable factors

(Kerzner, 2013).

Performance measurement is a fundamental principle of management.

The measurement of performance is important because it identifies current

performance gaps between current and desired performance and provides

indication of progress towards closing the gaps. A key principle of

performance management is to measure what you can manage. In order to

maintain and improve manufacturing performance each function in the

organization must focus on the portion of the indicators that they influence.

Maintenance performance contributes to manufacturing performance

(Weber & Thomas, 2009).

According to Kerzner (2013), KPIs have been used in a variety of

industries and specialized purposes such as:

a. Construction

b. Maintenance

c. Risk management

d. Safety

e. Quality

f. Sales

g. Marketing

h. IT

9

TABLE 2.1

ELEMENTS OF A KPI

Strategy KPIs embody a strategic objective.

Targets KPIs measure performance against

specific targets. Targets are defined in

strategic, planning or budget sessions

and can take different forms (e.g.,

achievement, reduction, absolute,

zero).

Ranges Targets have ranges of performance

(e.g., above, on, or below target).

Encodings Range are encoded in software,

enabling the visual display or

performance (e.g., green, yellow, red).

Encodings can be based on percentages

or more complex rules.

Time Frames Targets are assigned time frames by

which they must be accomplished. A

time frame is often divided into smaller

intervals to provide mileposts of

performance along the way.

Benchmarks Targets are measured against a baseline

or benchmark. The previous year’s

result often serve as a benchmark, but

arbitrary numbers or external

benchmarks may also be used.

Source: Eckerson (2009)

10

According to Eckerson (2009), there are two fundamental types of

KPIs: outcome and drivers. Outcome KPIs—sometimes known as lagging

indicators—measure the output of past activity. They are often financial in

nature, but not always. Examples include revenues, margins, return on

equity, customer satisfaction, an employee retention. On the other hand,

driver KPIs—sometimes known as leading indicators or value drivers—

measure activities that have a significant impact on outcome KPIs. These

KPIs measure activity in its current state (number of sales meetings today)

or a future state (number of sales meeting scheduled for the next two weeks.

The latter is more powerful, since it gives individuals and their managers

more time to adjust behavior to influence a desired outcome.

Another distinction between KPIs by Eckerson (2009) is that some are

based on quantitative data, while others are based on qualitative or

subjective data. Quantitative data measures activity by counting, adding, or

averaging numbers. Operational systems that manage inventory, supply

chain, purchasing, orders, accounting, and so on all gather quantitative data

used by KPIs. Financial KPIs are based on quantitative data, as are

employee injuries, number of training classes and so on. Quantitative data

forms the backbone of most KPIs. But qualitative KPIs are just as

important. The most common ones gauge customer or employee

satisfaction through surveys. While the survey data itself is quantitative, the

measures ate based on a subjective interpretation of a customer’s or

employee’s opinion on various issues. These opinions can help explain why

performance is dropping when all other indicators seem fine. Many

company use customer satisfaction KPIs to refine products and optimize

processes.

According to Eckerson (2009), the key to creating effective KPIs is as

much art as science, but there are many guidelines to help the uninitiated

achieve success. Organizations that create KPIs with the following 10

characteristics are likely to deliver high impact KPIs:

11

a. Sparse:

The fewer KPIs, the better. When it comes to the number of KPIs to

deploy, most performance management practitioners say less is

more. The common argument is that most people can only focus on

a maximum of five to seven items at once; therefore, we should limit

the number of KPIs to that range.

b. Drillable:

Users can drill into detail. The problem with having only a handful

of KPIs is that organization represents a dynamic balance between

strategy and process. Strategy seeks change, while process seeks

stability. The manager can represent strategy with a few KPIs, but

the manager needs hundreds or more to monitor processes, which

often cut across departmental boundaries. Therefore, the best

performance dashboards parse out KPIs and data based on role,

level, and task. The high-level or initial view of a dashboard

contains a handful of strategic KPIs that cascade to hundreds and

thousands of KPIs at more detailed views within a performance

dashboard. This internal cascading is true for all types of

dashboards: strategic, tactical, and operational.

c. Simple:

Users understand the KPIs. KPIs must be easy to understand.

Employees must know what’s being measured and how it’s

calculated. Complex KPIs consisting of indexes, ratios, or multiple

calculations are difficult to understand and, more importantly,

difficult to act on. In short, if users do not understand the meaning

of a KPI, they cannot influence its outcome. It is important to train

people on KPI targets. For instance, is a high score good or bad? If

the metric is customer loyalty, a high score is good, but if the metric

is customer churn, a high score is bad. Sometimes a metric can have

dual polarity; that is, a high score is good only until a certain point.

For instance, a telemarketer who makes 20 calls per hour may be

doing exceptionally well, but one makes 30 calls per hour may not

12

be connecting well with potential clients. An effective scoring and

encoding system is critical to making KPIs simple and

understandable.

d. Actionable:

Users know how to affect outcomes. Not only should KPIs be easy

to understand, but users should also know how to positively affect

the outcome of a KPI.

e. Owned:

KPIs have an owner. Every KPI needs an owner who is accountable

for its outcome. Some think it is imperative that each KPI have only

one owner so there is no potential for finger-pointing, and that the

individual owner feels highly motivated and responsible for

managing the KPI. Others say the opposite: make two people

responsible for a KPI and the manager engenders teamwork. This

coordination might be especially valuable in an organization that

wants to break down departmental silos and cross-pollinate ideas

among different groups.

f. Referenced:

Users can view origins and context. The data has to be clean,

accurate, and most importantly, perceived as accurate. Just being

accurate isn’t enough; users must believe it is as accurate as their

existing reports or spreadsheets (which may be woefully inaccurate,

but are trusted nevertheless). One way to engender trust in KPIs is

to provide reference data about them. Users should be able to right-

click on a KPI or button to reveal a dialogue box that identifies the

business and technical owners of the KPI as well as the details about

the origins of the KPI, how it was calculated, when it was last

updated, and other relevant details.

g. Correlated:

KPIs drive desired outcomes. Ultimately, KPIs need to impact

performance in the proper direction. Unfortunately, many

organizations create KPIs but never evaluate them after the fact to

13

see if they statistically correlate with desired outcomes. This

correlation makes explicit the linkage between driver KPIs and

outcome KPIs and gives executives greater confidence in making

decisions. It is important to correlate KPIs on a continuous basis

because their impact changes over time as the internal, economic,

and competitive landscape shifts. Most KPIs have a finite lifespan;

the manager get most of the value from them in the first year or so.

Afterward, the manager needs to rethink the targets or KPIs to

sustain progress or move to new KPIs that better reflect the current

strategy. But if the manager does not continuously monitoring the

impact of KPIs, the manager will never be able to evaluate any shifts

in their effectiveness. Many organizations spend lots of time and

energy evaluating the effectiveness of their KPIs, especially if

monetary incentives are attached to the results. They use

statisticians to perform regressions that map KPIs to intended results

and engage in discussions with peers and executives to negotiate the

KPIs and targets.

h. Balanced:

KPIs consist of both financial and non-financial metrics. It is also

important that the manager offer a balanced set of KPIs. This is the

philosophical underpinning of the balanced scorecard methodology.

Its creators, Robert Kaplan and David Norton, believe organizations

should measure performance across multiple dimensions of a

business, not just a financial perspective. They advocate a

“balanced” approach to measurement, which helps executives focus

on and invest in the key drivers of long-term growth and

sustainability. Kaplan and Norton offer four perspectives or

categories of metrics: financial, customer, operations, and learning

and growth. They also advocate that organizations create a strategy

map that defines strategic objectives in each perspective and shows

how they interrelate, giving executives a pictorial view of what

drives goals. On a micro level, it’s important that KPIs provide a

14

balanced perspective to individuals whose performance is being

monitored.

i. Aligned:

KPIs do not undermine each other. It is important that KPIs are

aligned and don’t unintentionally undermine each other, a

phenomenon that some call “KPI sub-optimization.”

j. Validated:

Workers cannot circumvent the KPIs. KPIs need to be not only

aligned and balanced, but also tested to ensure workers can’t

“game” the system—or circumvent the KPIs out of laziness or

greed. Organizations need to test their KPIs to ensure workers can’t

affect their outcome without taking the required actions to improve

the business. One way to avoid this problem is to include employees

in defining the KPIs and targets in the first place. They know better

than anyone the nuances involved in the processes and potential

loopholes that may tempt users to game the system. The tendency

to game KPIs increases dramatically once organizations attach

monetary incentives to KPIs. So it’s imperative to test and validate

KPIs in the reality of the workplace before using them as part of an

employee incentive system.

2.1.2. The Banking Industry

A bank can be defined in terms of the economic functions it serves, the

services it offers its customers, or the legal basis for its existence. Certainly

banks can be identified by the functions they perform in the economy. They

are involved in transferring funds from savers to borrowers (financial

intermediation) and in paying goods and services (Rose & Hudgins, 2010).

There are three main types of bank. The first is commercial banks.

Commercial banks sell deposit and make loans to businesses and

15

individuals. The next one is saving banks. Saving banks attract saving

deposits and make loans to individuals and families. The third is investment

banks. Investment banks underwrite issues of new securities from their

corporate customers (Rose & Hudgins, 2010).

Historically banks have been recognized for the great range of financial

services they offer—from checking an debit accounts, credit cards, and

savings plans to loans for businesses, consumers, and governments.

However, bank service menus are expanding rapidly today to include

investment banking (security underwriting), insurance protection, financial

planning, advice for merging companies, the sales of risk-management

services to business and consumers, and numerous other innovative

services. Banks no longer limit their service offerings to traditional services

but have increasingly become general financial-service provider (Rose &

Hudgins, 2010).

According to Rose & Hudgins (2010), the modern bank has to adopt

many roles to remain competitive and responsive to public needs. The

banking principal roles (and the roles performed by any of its competitors)

today include:

1. The intermediation role

Transforming saving received primarily from households into credit

(loans) for business firms and others in order to make investments

in new buildings, equipment, and other goods.

2. The payments role

Carrying out payments for goods and services on behalf of

customers (such as by issuing and clearing checks and providing a

conduit for electronic payments).

16

3. The guarantor role

Standing behind their customers to pay off customer debts when

those customers are unable to pay (such as by issuing letters of

credit).

4. The risk manager role

Assisting customers in preparing financially for the risk of loss to

property, persons, and financial assets.

5. The investment banking role

Assisting corporations and governments in marketing securities and

raising new funds.

6. The savings/investment advisor role

Aiding customers in fulfilling their ling-range goals for a better life

by building and investing savings.

7. The safekeeping/certification of value role

Safeguarding a customer’s valuables and certifying their true value.

8. The agency role

Acting on behalf of customers to manage and protect their property.

9. The policy role

Serving as a conduit for government policy in attempting to regulate

the growth of the economy and pursue social goals.

2.1.3. Clearing

According to European Central Bank (2009), clearing is the process of

transmitting, reconciling and, in some cases, confirming transfer orders

prior to settlement, potentially including the netting of orders and the

establishment of final positions for settlement. Sometimes this term is also

used (imprecisely) to cover settlement. For the clearing of futures and

options, this term also refers to the daily balancing of profits and losses and

the daily calculation of collateral requirements. A set of rules and

procedures whereby financial institutions present and exchange data and/or

17

documents relating to transfers of funds or securities to other financial

institutions at a single location (e.g. a clearing house). These procedures

often include a mechanism for calculating participants’ mutual positions,

potentially on a net basis, with a view to facilitating the settlement of their

obligations in a settlement system is called clearing system. The ones who

can participate in clearing is only clearing member of clearing house.

Clearing house is a common entity (or a common processing

mechanism) through which participants agree to exchange transfer

instructions for funds, securities or other instruments. In some cases, a

clearing house may act as a central counterparty for those participants,

thereby taking on significant financial risks. Clearing fund is a fund

composed of assets contributed by participants in a central counterparty

(CCP) or by providers of guarantee arrangements that may be used to meet

the obligations of a defaulting CCP participant. In certain circumstances, it

may also be used to settle transactions and cover losses and liquidity

pressures resulting from such defaults. A clearing fund serves as insurance

against unusual price movements not covered by the margin calculation in

the event of a member defaulting.

2.1.4. Risk

Risk in an organization context is usually defined as anything that can

impact the fulfillment of corporate objectives (Hopkin, 2012). Risk is a

condition in which there is a possibility of an adverse deviation from a

desired outcome that is expected or hoped for (Vaughan & Vaughan, 2008).

18

TABLE 2.2

DEFINITION OF RISK

Organization Definition of risk

ISO Guide 73

ISO 31000

Effect of uncertainty on objectives.

Note that an effect may be positive,

negative, or deviation from the

expected. Also, risk is often described

by an event, a change in circumstances

or a consequence.

Institute of Risk Management (IRM) Risk is the combination of the

probability of an event and its

consequence. Consequences can range

from positive to negative.

Orange Book from HM Treasury Uncertainty of outcome, within a

range of exposure, arising from a

combination of the impact and the

probability of potential events.

Institute of Internal Auditor The uncertainty of an event occurring

that could have an impact on the

achievement of the objectives. Risk is

measured in terms of consequences

and likelihood.

Source: Hopkin (2012)

19

According to Rose & Hudgins (2010), there are key risks in banking

and financial institutions’ management:

1. Credit Risk

There is, first of all, credit risk. For example, financial

intermediaries make loans and take on securities that are nothing

more than promises to pay. When borrowing customers fail to make

some or all of their promised payments, these defaulted loans and

securities result in losses that can eventually erode capital. Because

owner’s capital is usually no more than about 10 percent of the

volume of loans and risky securities (often much less than that), it

does not take to many defaults before capital simply becomes

inadequate to absorb further losses. At this point, the financial firm

fails and will close unless the regulatory authorities elect to keep it

afloat until a buyer can be found. Credit risk is the risk that a counter

party will not settle the full value of an obligation – neither when it

becomes due, nor at any time thereafter. Credit risk includes

replacement cost risk and principal risk. It also includes the risk of

the settlement bank failing. The change in net asset value due to

changes the perceived ability of counter parties to meet their

contractual obligations also considered credit risk.

2. Liquidity Risk

Depository institution encounter substantial liquidity risk—the

danger running out of cash when cash is needed to cover deposit

withdrawals and to meet credit requests from good customers. For

example, if a depository institution cannot raise cash in timely

fashion, it is likely to lose many of its customers and suffer a loss in

earnings for its owners. If the cash shortage persist, it may lead to

runs by depositors and ultimate collapse. The inability to meet

liquidity needs at reasonable cost is often a prime signal that a

financial firm is in trouble. Liquidity risk is the risk that a counter

party will not settle an obligation in full when it becomes due.

20

Liquidity risk does not imply that a counterparty or participant is

insolvent, since it may be able to effect the required settlement at

some unspecified time thereafter.

3. Interest Rate Risk

Financial intermediaries also encounter risk to their spread—the

danger that revenues from earning assets will decline or that interest

expenses will rise, squeezing the spread between revenues and

expenses and thereby reducing net income. Changes in the spread

are usually related to either portfolio management decisions (i.e.,

changes in the composition of assets and liabilities) or to interest

rate risk—the probability that fluctuating interest rates will result in

significant appreciation or depreciation in the value of and return

from the institution’s assets. In recent years financial firms have

found ways to reduce their interest rate risk exposure, but such risks

have not been completely eliminated—nor can they be.

4. Operational Risk

Financial-service providers also face operational risk due to weather

damage, aging or faulty computer systems, breakdowns in quality

control, inefficiencies in producing and delivering services, natural

disasters, terrorist acts, errors in judgment by management, and

fluctuations in the economy that impact the demand for each

financial service. These changes can adversely affect revenue flows,

operating costs, and the value of the owner’s investment in the

institution (e.g., its stock price).

Operational risk is the risk that deficiencies in information systems

or internal controls, human error or management failures will result

in unexpected losses. This relates to both internal and external

events. It is the risk of loss from an operational failure. Operational

risk permeates all aspects of the risk universe—that is to say it over

laps with and exacerbates all other types of risks, such as market,

credit, liquidity, and underwriting risk. In fact, in the absence of

operational failure, the other risks are much less significant.

21

However, when the banking industry was confronted with this

“boundary issue” many years ago, the Basel Committee ruled that

credit losses driven by operational failure were to be treated as credit

losses for capital adequacy purposes. This compromise ruling,

which was based on historical precedence and expedience, had the

unintended effect of diminishing the importance of operational

risk—not just in banking but across all industries that followed suit.

Under this narrow definition, operational risk was associated with a

low capital charge; therefore, many banks viewed it as a low-

priority issue. Not only did this divert resources and management

attention away from this key risk, but it also obscured the underlying

causes of many of the largest losses.

Operational risk is much more than just operational risk. Operations

risk is a subset of operational risk and is characterized by

unconscious execution errors and processing failures. Because these

risks are generally well known, they also tend to be well managed.

In addition, because these events stem from “normal” operational

failures, the consequential single-event losses are relatively small—

rarely in excess of a million dollars. Operational risk, by contrast, is

driven primarily by “non-normal” operational failures, particularly

conscious violations of professional or moral standards and

excessive risk taking. Examples include sales practice violations

and unauthorized trading activities. Ironically, many multibillion-

dollar losses occur when the perpetrators nominally intend to benefit

their respective firms, but do things that are not in their best long-

term interests.

Operational risk results from costs incurred through mistakes made

in carrying out transactions such as settlement failures, failures to

meet regulatory requirements, and untimely collections.

Operational risk had been defined in the past as all risk that is not

captured in market and credit risk management programs. Early

22

operational risk programs, therefore, took the view that if it was not

market risk, and it was not credit risk, then it was operational risk.

There are four main causes of operational risk that are identified in

standard operational risk definitions. Operational risk events can

occur when there are inadequacies or failures due to:

a. People (human factors)

b. Processes

c. Systems, or

d. External events

There are four main causes of operational risk events: the person

doing the activity makes an error, the process that supports the

activity is flawed, the system that facilitated the activity is broken,

or an external event occurs that disrupts the activity.

5. Exchange Risk

Larger banks and securities firms face exchange risk from their

dealings in foreign currency. The world’s most tradable currencies

float with changing market conditions today. Institutions trading in

these currencies for themselves and their customers continually run

the risk of adverse price movements on both the buying and selling

sides of this market.

6. Crime Risk

Finally, all financial firms encounter significant crime risk. Fraud or

embezzlement by employees or directors can severely weaken a

financial institution and, in some instances, lead to its failure. In

fact, the Federal Deposit Insurance Corporation lists fraud and

embezzlement from insiders as one of the prime causes of recent

bank closing. Moreover, the large amounts of money that banks

keep in their vaults often prove to be an irresistible attraction to

outsiders.

23

2.1.5 Operational Risk by Basel II

Basel II calls operational risks as “the risk of losses resulting from

inadequate or failed internal processes, people and systems, or from internal

events.” That also says legal risks that are exposed to fines, penalties,

damages, resulting from private settlements, etc., but strategic reputational

risks are not included in this definition for the purpose of a minimum

regulatory operational risk capital charge.

According to Basel II, the rigorous, consistent, and quantified approach

to operational risk includes identification, assessment, monitoring, control,

and mitigation. The possible tools that can be used by financial

organizations for assessing operational risks are:

a. Self or risk assessment

A bank assesses its operation and activities against a menu of

potential operational risk vulnerabilities. This process is internally

driven and often incorporates checklists or workshops to identify the

strengths and weakness of the operational risk environment.

b. Risk mapping

In this section, any business units, organizational functions, or

process flows are mapped by risk type. This process can show

particular areas of weaknesses and help prioritize the subsequent

management action.

c. Risk indicators

Statistics or metrics that can provide insight into bank’s risk position

is called risk indicators. These indicators tend to be reviewed on a

periodic basis, monthly or quarterly, to alert banks to changes that

may be indicative of risk concerns.

d. Risk measurement

Variety of approaches can be used to quantify exposure to

operational risk. Data on a bank’s historical loss experience could

provide meaningful information for assessing the bank’s exposure

24

to operational risk and developing a policy to mitigate and control

the risk. The effective way to make good use of the information is

to make a framework for systematically tracking and recording the

frequency, severity, and other relevant information on individual

loss events. Some other organization have also mix internal loss data

with external loss data, scenario analysis, and risk assessment

factors.

FIGURE 2.1

A QUANTIFIED APPROACH TO OPERATIONAL RISK

MANAGEMENT ACCORDING TO BASEL II

Source: Akkizidis & Bouchereau (2005)

Operational risk

Identification

Assessment

MonitoringControl

Mitigation

25

2.2 Subject of Case Study

In Bank Bukopin Pontianak, there is particular procedure and standards

of how clearing transaction should be processed. Processing transactions as

procedure and standards do not truly avoid risks that might happen and

might keep the bank from achieving its goals.

This study aims to find out the operational risks in clearing transaction

in Bank Bukopin Pontianak. In order to find out the operational risks, the

researcher conduct interview with two officers who in charge in dealing

with clearing transaction and also the coordinator in operational division.

The researcher only interviewed this two officers, because they are the ones

who really know about clearing transaction; the process, the standard, the

Key Performance Indicators, and also the operational risks. This study also

aims to find out the key performance indicators to manage operational risk

in Bank Bukopin. Conducting interview and document analysis is the

method researcher use to finding out of those key performance indicators

used to manage operational risk in Bank Bukopin. In this study, the

researcher also wants to find out of how effective key performance

indicators to minimize operational risk in clearing transaction. To find out

about this the researcher conduct interview and analyzing documents.

2.3 Review of Related Research

1. Ricky Linarto (2012) conducted a research about “The Analysis of

Balanced Scorecard Design for PT. Budi Acid Jaya Tbk. (BAJ)”. It is

conducted to determine the performance appraisal system that is

currently in the PT. Budi Acid Jaya Tbk; to improve the control system

in PT. Budi Acid Jaya by using Balanced Scorecard implementation.

The research concludes that to create design performance measurement

26

for PT. Budi Acid Jaya Tbk, and also to create the strategy map as well

as the balanced scorecard to give an advice and image for the company.

2. Andre Abednego (2006) conducted a research about “Perancangan

Indikator Kinerja dengan Menggunakan Balanced Scorecard pada PT.

Faber-Castell International Indonesia”. It is conducted to identify

vision, mission, and company strategy into determining targets; to find

out the key performance indicators that being used recently; to make

Balanced Scorecard design for the company, therefore the company can

measure either the target is being accomplished or not. The research

concludes, by using Balanced Scorecard, the management can get the

more accurate and complete view of the business performance. And also

the Balance Scorecard can be used as the communication tools between

the management and the stakeholder.

3. Sinta (2008) conducted a research about “Usulan Pendekatan Metode

Balanced Scorecard Untuk Mengukur Kinerja CV. Sinta Lestari”. It is

conducted to find out the performance measurement with using

traditional method; to find out performance measurement with using

Balanced Scorecard method. The research concludes, that using

traditional method is less effective, different when using Balanced

Scorecard which create output in each perspective.

4. Fernando (2012) conducted a research about “Pengukuran Kinerja

Berbasis Balanced Scorecard pada PT. Homa Sejahtera”. It is

conducted to make better performance for PT. Homa Sejahtera by

designing Balance Scorecard; to measure performance measurement in

production division by using Key Performance Indicator (KPI); to find

out which KPI that needed to be fix based on the measurement output.

The research concludes the KPI that needed to be fix in the performance

is in the customer perspectives.

5. Nivia Ayusari (2012) conducted a research about “Analisis Pengukuran

Kinerja Berbasis Balanced Scorecard pada Departemen Produksi PT.

Bakrie Building Industries”. It is conducted to determine the good

performance measurement for production department with the Key

27

Performance Indicator design on PT. Bakrie Building Industries; to

analyze the output of performance measurement in the production

department with the balanced scorecard method; to analyze the

operational activity in production department in supporting execution

strategy planning that already had before. The research concludes the

performance measurement is measured by four perspectives or by

balanced scorecard method.

28

2.4 Theoretical Framework

START

OBSERVATION

DATA COLLECTION

OPERATIONAL RISK

CLEARING

TRANSACTION

KPI

ANALYZING

INTEPRETATION OF

DATA ANALYSIS

RESEARCH CONCLUSION

AND RECOMMENDATION

END

YES

NO

29

Observation is the first thing researcher do to find out the problem

within the company. After finding the problem, the researcher will collect

data through interview and document analysis. The researcher focuses on

the operational risk in clearing transaction. The researcher find out whether

the clearing transaction has KPI or not. If there is KPI for clearing then the

researcher will analyze that existing KPI, whether the KPI can minimize the

risk or not and also whether that KPI is effective or not. If there is not, then

the researcher will analyze the clearing transaction again and construct the

new KPI that should work effectively for minimizing risks that might

happen in that bank. After analyzing the KPI, the researcher will interpret

the finding. Lastly, the researcher will make conclusion and

recommendation toward the finding.

Operational Definition

Key Performance Indicator

A KPI is a metric measuring how well the organization or an individual

performs an operational, tactical or strategic activity that is critical for the

current and future success of the organization.

Risk Management

The practice of identifying potential risks in advance, analyzing them and

taking precautionary steps to reduce or curb the risk.

Clearing transaction

The process of transmitting, reconciling and, in some cases, confirming

transfer orders prior to settlement, potentially including the netting of orders

and the establishment of final positions for settlement. Sometimes this term

is also used (imprecisely) to cover settlement. For the clearing of futures

and options, this term also refers to the daily balancing of profits and losses

and the daily calculation of collateral requirements.

30

2.5 Summary

In every company there should be procedure and standard to make the

company achieve its goals and also to minimize the risks that might happen

to that company. Nevertheless for Bank Bukopin Pontianak. This research

aims to find out the operational risks in clearing transaction in Bank

Bukopin. To find out the operational risks, the researcher conduct interview

with officers who in charge in dealing with clearing transaction and also the

coordinator in operational division. This study also aims to find out the key

performance indicators to manage operational risk in Bank Bukopin. To

find out the key performance indicators Bank Bukopin, the researcher will

ask questions related to that. Besides asking questions in the interview, the

researcher will also analyzing documents. The next thing researcher wants

to find out is about how effective key performance indicators to minimize

operational risk in clearing transaction. To find out about this the researcher

conduct interview and analyzing documents.

There are five related previous researches. They are The Analysis of

Balanced Scorecard Design for PT. Budi Acid Jaya Tbk. (BAJ) by Ricky

Linarto and Perancangan Indikator Kinerja dengan Menggunakan Balanced

Scorecard pada PT. Fiber-Castell International Indonesia by Andre

Abednego. There are also Usulan Pendekatan Metode Balance Scorecard

Untuk Mengukur Kinerja CV. Sinta Lestari by Sinta, Pengukuran Kinerja

Berbasis Balanced Scorecard pada PT. Homa Sejahtera by Fernando, and

Analisis Pengukuran Kinerja Berbasis Balanced Scorecard pada

Departemen Produksi PT. Bakrie Building Industries by Nivia Ayusari.

The first thing researcher do is observing. After that, the researcher will

collect data through interview and document analysis to related problem.

The next this researcher do is focusing on operational risk in clearing

transaction. Then, the researcher will analyzing whether the clearing

transaction has KPI or not. If the clearing transaction has KPI, then the

31

researcher will analyze the KPI. The researcher will analyze whether the

KPI is effective to minimize the risk or not. If the clearing transaction does

not have KPI, then the researcher will make the KPI that should work to

minimize risks. After analyzing the KPI, the researcher will interpret the

data and compare it with the bank’s standards. Finally the researcher makes

conclusions and recommendations for the effectiveness of KPIs in clearing

transactions.

32

CHAPTER III

RESEARCH METHODOLOGY

3.1. Research Questions

The researcher sets to find out the effectiveness of key performance

indicators to manage the clearing transaction operational risk in Bank

Bukopin. Research was conducted by observing Bank Bukopin,

interviewing the authorized officer, and document analysis on several

sources.

Research question one (RQ1): What are the operational risks in

clearing transactions in Bank Bukopin Pontianak?

Proposition one (P1): Operational risk in clearing transaction is system

failure for Bank Indonesia (BI) online.

According to Rose & Hudgins, operational risk is the risk that deficiencies

in information systems or internal controls, human error or management

failures will result in unexpected losses. It is the risk of loss from an

operational failures.

Research question two (RQ2): Which key performance indicators to

manage operational risk in clearing transaction in Bank Bukopin

Pontianak?

Proposition two (P2): To discover what the key performance indicators are

to manage operational risk in clearing transaction compared with the

operational risk standard.

According to Eckerson, Key Performance Indicator is a metric measuring

how well the organization or an individual performs an operational, tactical

or strategic activity that is critical for the current and future success of the

organization.

33

Research question three (RQ3): How effective are these key

performance indicators to minimize the operational risk in clearing

transaction in Bank Bukopin Pontianak?

Proposition three (P3): To find out if the key performance indicator is

effective compared to the standards of the operational risk in clearing

transaction.

According to Eckerson, organizations that create KPIs with 10

characteristics (sparse, drillable, simple, actionable, owned, referenced,

correlated, balance, aligned, and validated) are likely create effective and

high impact KPIs.

3.2. Setting

This research is about the effectiveness of key performance indicators

in Bank Bukopin Pontianak. The research took place in Bank Bukopin

Pontianak in its operational division where the clearing transaction happens.

The observation was conducted since April to July 2014.

The researcher observed the clearing transaction process in that office. First

the check or transfer form from customer is received by the authorized

officer from the front office. Then the officer will input the information

from the check or transfer form to the system which is connected online to

Bank Indonesia. After input all the check or transfer form to the online

system, the officer will print the recap and bring them to Bank Indonesia.

Then, at 11am, the officer will bring all the check or transfer form and the

recap to Bank Indonesia. The recap is given to BI and the check or transfer

form are put based on the originate bank.

The next is the authorized officer will return to the office to check the

received check or transfer form from the other banks customer. The officer

34

will check on owners’ balance, stamp, and signature. These are the

requirements that needs to be fulfilled so that the transaction can be proceed.

At 2pm, the officer will go back to Bank Indonesia says that the check or

transfer form that he has checked fulfill the requirements and can be

processed. The officer reports to Bank Indonesia which customer has not

enough balance, or if the stamp and signature is do not match with the

specimen. Finally, the officer return to the office again and process the

clearing.

3.3. Population

Population is generalization area that consist of the object or subject that

has certain qualities and characteristics that are determined by the

researchers to study and the drawn the conclusions (Sugiono, 2011). The

population in this research is the employees of Bank Bukopin Pontianak

since the research took place in Bank Bukopin Pontianak.

3.4. Data Source

In this research, data collection procedure that were used by the

researcher were by using primary data and secondary data. The interview

and observation are the primary data. The researcher interviewed the Bank

Bukopin Pontianak authorized officers and observed the bank especially in

the operational division.

Secondary data is the document analysis. The researcher analyzes any

documents related to the research object. The documents used in this

research is the SOP handbooks that explains about the operation of the bank,

especially clearing transaction. The SOP hand book was borrowed from

35

Bank Bukopin Pontianak and required just to be read at the office. The

researcher also used books, journals, and internet articles as the information

for this research.

3.5. Ethical Consideration

The interviewees required not to be recorded during the interview. The

confidential company documents that given by the bank is not allowed to

be shown. At the end of the research, the result will be the right of the

interviewees. The usage of the research is the benefit that the interviewees

might achieve.

3.6. Research Design

In doing scientific research there are two methods. They are qualitative

and quantitative method. The differences between qualitative and

quantitative research are by the type of data, research process, instrument

used in collecting data and also the purpose of the research.

Qualitative research is generated from the broad answer to specific

questions in interviews, or from responses to open-ended questions in a

questionnaire or through observation, or from already available information

gathered from various sources (Sekaran, 2010). In this research, based on

the topic, the researcher uses qualitative method in order to analyze the

effectiveness Key Performance Indicators to manage clearing transaction

operational risk in Bank Bukopin and also using case study as the research

design. Case study is a detailed study based upon the observation of the

intrinsic details of individuals, groups of individuals, and organizations

(Malholtra, 2008). The researcher is using case study because the researcher

observes the key performance indicators within a specific bank.

36

The research process used by the researcher is observation to find out

the problem within the company. After finding the problem, the researcher

will collect data through interview and document analysis. The researcher

focuses on the operational risk in clearing transaction. The researcher would

like to find out whether the clearing transaction has KPI or not. If there is

KPI for clearing then the researcher will analyze that existing KPI, whether

the KPI is effective to minimize the risk or not. If there is not, the researcher

will construct the new KPI that should work for minimizing risks that might

happen in that bank. After analyzing the KPI, the researcher will interpret

the finding. Lastly, the researcher will make conclusions and

recommendations based on the findings.

3.7. Interview Instrument and Protocol

Interview is a fact finding technique to gather information from

individuals through face to face interaction. Interview is used to find fact,

validate fact, get clearance data, get end-user, identify needs, and unite idea

and opinion. Interviewer is the one who responsible to organize and conduct

interview. Interviewee will answer the questions asked. There are two types

of interview, such as:

1) Structured interview

The interviewer has already prepared particular questions to get the

desired responds from the interviewee.

2) Unstructured Interview

Interviewer gives general questions, then the interviewee will

answer those. Usually the answers given will be out of the context.

This type of interview will not work well for analysis and system

design.

37

TABLE 3.1

SAMPLE INTERVIEW QUESTIONS

Indicator Question

Key Performance Indicator 1. Is there any Key Performance

Indicator used in this company to

manage operational risk? What

are they?

(if there is one(s))

2. Are they useful in making

progress toward the company’s

goal?

(if there is none)

3. Do you think if there is Key

Performance Indicator(s) in this

company, will it able to reduce

the operational risk that might

happen to the company?

Operational Risk

(Clearing)

1. What is clearing?

2. How is the procedure? How is the

Standard Operating Procedure

(SOP)?

3. Is there any risk in doing

Clearing?

4. How to handle the risk?

The interview questions are the research instrument. The interviewees

for these questions are the employee of Bank Bukopin Pontianak who

responsible in running transfer, clearing, and collection transactions and the

coordinator of operational division. The researcher only interview this two

persons because this two persons have deep knowledge about clearing

transaction. The authorize officer of clearing transaction indeed know

everything about clearing. The coordinator of operational division surely

know how clearing transaction is and what the key performance indicators

are.

38

In this research, the researcher used structured interview, the researcher

has already prepared for the questions and there might be some questions

popped up and give the researcher more information. The questions that

going to be asked are about operational risks, Key Performance Indicator,

the procedure and operational risks of clearing.

There are two type questions that can be used in the interview; they are

open-ended questions and close-ended questions. Open-ended questions are

questions that allow to be answered in any ways. This type of questions is

usually used on the semi-structured interview. The close-ended questions

are questions that limit respondent’s answers into specific options or direct

and short responds. In this research, the researcher used open-ended

questions in conducting the interview.

3.8. Data Analysis Strategy

Qualitative method usually gathered by observations, interviews or

focus groups and the data is also gathered from written documents and

through case studies, it less emphasis on counting numbers of people who

think or behave in certain ways and more emphasis on explaining why

people think and behave in certain ways.

There are two types of techniques design used to determine the way of

taking sample and choosing the sample consist of probability sampling and

non-probability sampling (Malhotra, 2009). Probability sampling is a type

of sampling that have common chances of being selected as sample. In

contrast, non-probability sampling is a type of sampling that have unequal

chances of being include in the sample. Non-probability sampling includes

convenience sampling, quota sampling, and purposive sampling.

Convenience sampling is selecting the easiest population members from

which to obtain information. Quota sampling finds and interviews a

prescribed number of people in each of several categories. Purposive

39

sampling is choosing the sample based on who the researcher thought will

be appropriate for the research. This is often chosen when there is a limited

number of people that have expertise in the area being researched.

According to the topic of the research, purposive sampling is used as

the sampling design technique. In the area that being researched there are

two officers whom considered as expertise and perfect to be interviewed.

Besides interview, the researcher also observes the operational process in

Bank Bukopin Pontianak. Observation is another fact finding technique by

observing directly and write about that systematically toward the research

object. The researcher observed and write about the activity in operational

division. Then, the researcher also analyzes documents from the bank which

is Bank Bukopin SOP hand book and other literatures.

Proving the qualitative research is reliable and valid is different with

proving the reliability and validity of quantitative research. In qualitative

research, reliability is an examination of the stability or consistency of

responses. Qualitative validity is based on determining if the findings are

accurate from the standpoint of the researcher, the participant or the reader

(Creswell, 2009).

The reliability of this research is proven by the consistency answer from

the interviewees during the interview. Validity in this research is proven by

the corresponded findings that the researcher discovers when comparing the

interview result with the SOP hand book.

40

3.9. Summary

In this research, there are three research questions. They are:

1. What are the operational risks in clearing transaction in Bank

Bukopin Pontianak?

2. Which key performance indicators to manage operational risk in

clearing transactions in Bank Bukopin Pontianak?

3. How effective are these key performance indicators to minimize the

operational risk in clearing transaction in Bank Bukopin Pontianak?

The proposition that researcher made for research question number one

is system failure for BI online. To discover what are the key performance

indicators to manage operational risk in clearing transaction compared with

operational risk standard. For question number three, the researcher

intended to find out if the key performance indicators are effective

compared to the standard of operational risk in clearing transaction.

Observation was conducted at Bank Bukopin Pontianak since April to

July 2014. The researcher interviewed two officers in Bank Bukopin

Pontianak. This officer is responsible in running transfer transactions,

clearing transactions, and collection transactions. The other officer is the

coordinator of operational division.

The researcher analyzes documents related to the research object. The

researcher used books, journals, and internet articles. The researcher also

uses office documents that were borrowed from Bank Bukopin Pontianak.

The interviewees asked not to be recorded during the interview. The

documents borrowed are also not allowed to be copied or taken home, so

documents are only allowed to read at the office. The result of the research

will be the right of the interviewees, and the usage of the research is the

benefit that the interviewees might achieve.

41

The researcher uses qualitative method and case study analysis. In this

research, the researcher use purposive sampling as the sampling design

technique. In the area being researched there are two officers whom

considered as expertise and perfect to be interviewed. The interviewees are

the employee of Bank Bukopin Pontianak who responsible in running

transfer, clearing, and collection transactions and also the coordinator of

operational division.

The researcher used structured interview, where the researcher has

already prepared for the questions. There also might be some questions

popped up during the interviews to give the researcher more information.

Therefor the researcher also used an unstructured interview. The questions

that going to be asked are about operational risks, Key Performance

Indicator, the procedure and operational risks of clearing transaction.

42

CHAPTER IV

ANALYSIS AND INTERPRETATION

4.1. Company Profile

Bank Bukopin is a medium-up size national private bank which focus