the effect of esg investing on stock returns and risk

TRANSCRIPT

The Effect of ESG Investing on Stock

Returns and Risk

University of Amsterdam, Amsterdam Business School

MSc Business Economics – Finance

Master Thesis

Supervised by Prof. Jeroen Ligterink

Cagri Yürür, 10846352

August, 2017

Statement of Originality This document is written by Cagri Yürür who declares full responsibility for the contents of this document. I declare that the text and the work presented in this document is original and that no sources other than those mentioned in the text and its references have been used in creating it. The Faculty of Economics and Business is responsible solely for the supervision of completion of the work, not for the contents.

Acknowledgement I would like to express my gratitude to my supervisor Professor Jeroen Ligterink for his useful comments, remarks and efforts throughout the process of this research. Without his dedication and constant feedback this thesis would not have been accomplished in the way presented and I am more than thankful for his supervision during my student life.

Abstract Does ESG investing have a significant effect on the stock market? This thesis investigates the financial market’s reaction to the implementation of environmental, social, and governance relat-ed investment rules in accordance to the Principles of Responsible Investing. By grouping com-panies according to their ESG performances I compare their stock returns. Although both the high ESG-performance portfolios, as well as the low ESG-performance portfolios display nega-tive alphas, high-ESG-performance lead to a less negative return. Since this difference is not sig-nificant, no arbitrage opportunity arises. I interpret these findings as supportive of the Efficient Markets Hypothesis.

Table of Contents

Statement of Originality .................................................................................................. 2

Acknowledgement ........................................................................................................... 3

Abstract ............................................................................................................................ 4

Table of Contents ............................................................................................................ 5

1 Introduction .......................................................................................................... 6

2 Literature Review ................................................................................................. 9

3 Hypotheses ......................................................................................................... 18

3.1 Hypothesis 1: Shunned stocks hypothesis ............................................................. 18

3.2 Hypothesis 2: Errors in expectations hypothesis ................................................... 18

4 Methodological Approach and Data ................................................................ 19

4.1 Approach .............................................................................................................. 19

4.2 Methodology ........................................................................................................ 19

4.3 Data Preparation ................................................................................................... 214.3.1 Index .................................................................................................................... 21

4.4 Computation of Performance ............................................................................... 234.4.1 Further Selection .................................................................................................. 25

5 Results ................................................................................................................. 27

6 Robustness Check .............................................................................................. 31

6.1 Percentiles ............................................................................................................ 31

7 Conclusion .......................................................................................................... 39

References ...................................................................................................................... 40

Appendix ........................................................................................................................ 44

1 Introduction In recent decades the concept of Socially Responsible Investing (SRI) – also called Responsible

Investment (RI) – has become highly relevant for a large number of investors and enjoys increas-

ing attention in academic literature (Derwall et al., 2011; Sievänen et al., 2013). Driven by climate

change in general, and environmental catastrophes such as oils spills1 and nuclear disasters2 in

particular, environmental issues have become a prominent topic in contemporary societies chal-

lenging global politics to confront environmental concerns (Bauer and Hann, 2010). In addition

to legislation as a driving force, it has been the effort of international institutions and their initia-

tives to raise consumers’ and investors’ awareness of responsibility as market participants in gen-

eral (Renneboog et al., 2008). International conventions such as the United Nations Global

Compact (UNGC) and the United Nations Principles for Responsible Investment (PRI) for ex-

ample provide investors with guidelines for their SRI practices and encourage commitment to

them (Della Croce et al., 2011). Apart from these drivers, Porter and Kramer (2006) highlight

reputational concerns that, in the 1990s, forced many companies to integrate particular environ-

mental, social, and governance (ESG) issues that had not previously been part of their business

responsibility.

Despite being a popular trend, there remains no consensus on a specific definition of SRI. Ac-

cording to the European Social Investment Forum (Eurosif, 2016), SRI can be understood as a

long-term oriented approach to investing that aims to incorporate environmental, social and gov-

ernance (ESG) factors into investment decisions.3 ESG factors are also commonly referred to as

corporate social responsibility (CSR4) criteria in economics literature5.

As outlined by the PRI (2015), ESG investing is an investment approach that aims for better risk

management and higher sustainability in long-term returns.

1 For example, the Exxon Valdez (1989) and Deepwater Horizon oil spills (2010). 2 For example, the Chernobyl (1986) and Fukushima nuclear disasters (2011). 3More fully, Eurosif understands SRI to be ‘a long-term oriented investment approach, which integrates ESG factors

in the research, analysis and selection process of securities within an investment portfolio. It combines funda-mental analysis and engagement with an evaluation of ESG factors in order to better capture long term returns for investors, and to benefit society by influencing the behaviour of companies’ (2016). European SRI Study, p.9.

4 Renneboog et al. (2008) define CSR as corporate decisions that foster social and corporate governance as well as ethical and environmental issues.

5 ‘SRI relates to CSR because socially responsible investors essentially evaluate companies’ CSR characteristics to determine the social responsibility level of their investment portfolios.’ (Derwall et al., 2011).

The European SRI Study (Eurosif, 2016) highlights the rising tendency to SRI engagement. The

report underlines the fact that increasing numbers of investors take on both direct and indirect

costs in order to achieve a certain level of ESG compliance. While SRI was initially undertaken by

retail investors, institutional investors have become its main drivers since the 1980s (Sievänen et

al, 2013). From 1995 to 2010, the volume of assets under management (AuM) that follow SRI

strategies grew by 380% while the broader universe of professionally managed assets grew by

only 260% (Nofsinger and Varma, 2014). During the last two years, SRI investing in the United

States alone has grown by more than 33%. Last year, nearly 22% of the total AuM in the US were

involved in SRI (USSIF, 2016). In 2015, nearly 50% of AuM globally were managed by institu-

tional investors who were signatories to the PRI (PRI 2015) and committed themselves to inte-

grate ESG criteria in their investment process. In 2016, the number of these signatories reached

more than 1440 (Henke 2016) with total AuM of about $60 trillion (Amel-Zadeh and Serafeim,

2017). As of today, the principles have about 1780 signatories6.

Since 1970, more than 2000 studies have been published on this matter, yet, to this date, empiri-

cal analyses have not led to a shared conclusion, and the debate on the effect of ESG criteria on

corporate financial performance has continued (CFP) (Friede et al 2015)7.

This master’s thesis aims to contribute to the existing literature by analysing the effect of ESG

compliance on stock returns. In this paper, ESG compliance on ESG performance scores are

proxied and expected returns are calculated with the help of the capital asset pricing model

(CAPM). While other studies have focused solely on one particular ESG component8, this paper

investigates not only social, but environmental and governance related aspects as well. A compa-

ny might have a commendable governance structure but lack eco-friendliness or social perfor-

mance. It is of great interest to examine a company’s performance on all SRI aspects. This work

employs ESG performance scores determined by the ESG research provider MSCI ESG KLD

STATS. Based on each company’s individual ESG performance, hypothetical portfolios are con-

structed in order to compare financial performance both in a single factor framework (CAPM) as

well as in a multifactor framework based on Carhart (1997). To prove robustness of this work,

the data is partitioned into different percentiles and investigated on each ESG pillar separately.

Moreover, the sample is analysed regarding its distribution of industries. As some sectors might

show a higher sensitivity to certain ESG issues, this information will contribute to a robustness

6 United Nations Principles for Responsible Investing, https://www.unpri.org/directory/ . 7 Also see Table 1 for diverse results. 8 E.g. Gompers et al. (2003) focus on governance; Derwall et al. (2005) focus on environmental issues; Derwall et al.

(2011) focus on (the social component of) employee satisfaction. See Table 1 for other examples.

analysis. Derwall et al. (2005) define six environmentally sensitive sectors9 which are included in

my robustness check.

It is concluded that ESG investing displays negative alphas in both the simple CAPM framework

and the multifactor framework based on Carhart (1997). This effect is significant at the 0.1%

level. Surprisingly, not only the portfolio with high ESG ratings, but also that with low ESG rat-

ings, negative alphas. Nevertheless, the difference in returns is not significant, dementing the idea

of a riskless trading strategy. The results support both positive and negative views on ESG in-

vesting, that is, both the low-ranked and the high-ranked ESG portfolios performs badly. My

suggestion is that merely a balanced portfolio is the right strategy to follow, supporting the Effi-

cient Market Hypothesis. The results hold true even after applying the before-mentioned robust-

ness checks.

This thesis is organised as indicated in what follows. The most relevant literature is reviewed in

the second chapter of this thesis. A brief overview of SRI practices, from their early stages to

their current state, contributes to a greater understanding of the subject, and is followed by the

display of market efficiency as a focal point of the SRI debate. Starting from the macro-level and

leading on towards a more detailed perspective, different theories on the positive and negative

channels of SRI are presented.

The third chapter concerns the two contrary hypotheses of 1) shunned stocks, and 2) errors in

expectations.

In chapter 4, the methodological approach of the research is illustrated, followed by an elabora-

tion of the underlying data and its preparation.

In the fifth chapter, the results of this study are presented. Additional robustness checks are pro-

vided in the sixth chapter. Finally, in the seventh chapter the approach of this thesis in general as

well as its results, are components of the discussion and are tied to a conclusion.

The appendix provides detailed information regarding the performance indicators being used in

the ESG index.

9 Electric utilities, chemistry, metal, mining, aerospace & defence and petroleum.

2 Literature Review The intention of this thesis is to contribute to the existing research in several ways. At a broad

level, it is based in the field of SRI. This was historically a niche sector, being purely ethically

based (Richardson and Cragg, 2010; Renneboog et al., 2008). A simple approach was taken with a

straightforward negative screening, excluding shareholdings in companies that were considered

unethical (Sparkes and Cowton, 2004). As SRI investors differ in their ethical norms (De Colle

and York, 2009), negative screening in its contemporary state displays different levels of strictness

and is applied to a variety of businesses. Referred to as the second-generation of screens, portfo-

lios are also based on positive screens where shares with superior ESG performance are selected.

The basis of this analysis is formed by the so-called third-generation screening. It entails the con-

sideration of both negative and positive ESG criteria into the investment decisions. (Renneboog

et al., 2008).

At a micro level, this thesis intends to contribute towards filling the gap in research on the effect

of SRI on stock returns, which up to the present has not yet led to consistent results. This is illus-

trated by Aktas et al. (2011), who covered the ongoing debate between institutional investors on

whether ESG investing results in financial benefits.

According to Modern Portfolio Theory, SRI practices are claimed to be oppositional and to

shrink investment opportunities. In his 1970 Efficient Market Theory, Eugene Fama asserted that

in an efficient market all available information is “fully reflected” in stock prices (Fama 1970)10.

Since Fama’s assertion is linked to a theoretical equilibrium where (I) transaction costs are non-

existent, (II) all market players have equal access to all information available and (III) have ho-

mogenous expectations of future stock prices. It remains an unachievable ideal, however, it func-

tions as a theoretical benchmark in academic research.

From an ESG investor perspective and in subsequent general opinion, the first assumption (i) can be disregarded as ESG investors do not face different transaction costs compared to conven-tional investors as both rely on the same restricted investment universe. Renneboog et al. (2008) mention the possibility of different management fees being charged by mutual funds. Gil-Bazo et al. (2010) empirically investigated whether SRI funds charge higher fees than mutual funds as a result of potential extra costs for SRI screenings. The authors found no conclusive evidence. Re-garding the second assumption (ii), it is argued that ESG information is not ‘costless’ and simul-taneously available to all market participants. ESG data available free of charge is generally wholly

10 Later Fama (1995) changed this assertion to a ‘good estimate of a stock’s intrinsic value’.

qualitative and is considered to be incomplete and inconsistent due to its dependence on volun-tary reporting (Park and Lavenel (2013). The integration of ESG data into investment decisions relies on the services of third-party ESG data providers (e.g. MSCI ESG Research, EIRIS Ltd., Sustainalytics) that collect and quantify this ESG information which they charge certain fees for. On this account ESG information comes with certain price and is not simultaneously available to all investors. Therefore, the third assumption (iii) regarding homogenous expectations is also challenged. Proponents of SRI refer to described information advantage as an argument for mar-ket inefficiency which allows opportunities for exploitation by ESG investors (e.g. Sparkes 2002).

This discussion is fuelled by contrary results concerning the direct effects of ESG investing. One

of the earliest studies on SRI by Alexander and Bucholz (1978) defends the efficiency of stock

markets as described by Fama (1970). The authors used social responsibility rankings and applied

Jensen’s (1968) capital asset-pricing model to measure stock performance on a risk-adjusted basis.

In order to investigate the potential effect of social responsibility on security risk, rank-order cor-

relations between social responsibility and risk were calculated. Their results indicated a low in-

significant correlation. Based on their measurements, the authors state that new information rele-

vant to earnings outlook is immediately reflected by current stock prices and declare that any

effects of SRI are non-existent.

Another common argument against research supportive of ESG investing is the potential for

endogeneity through reverse causality. It is often disputable whether SRI increases financial per-

formance or if successful companies are more willing to engage in SRI because they possess the

resources to do so (Fisher-Vanden and Thorburn, 2011). El Ghoul et al (2011) name two differ-

ent hypotheses regarding causal direction. The good management hypothesis holds that enhanced

CSR improves a firm’s relationship with its key stakeholders and leads to better financial perfor-

mance. Their slack resource hypothesis, on the other hand, claims that improved financial per-

formance leads to resource slack which allows firms to invest in and improve CSR. To ensure the

robustness of their results, El Ghoul et al. employed instrumental variables-estimation method

and use lagged values as an independent variable in their regression model.

Moreover, Langbein and Posner (1980) provide conventional arguments in opposition to ESG

compliance which focus on indirect ESG costs as lacking diversification opportunities and in-

creasing risk due to the exclusionary approach of ESG compliance.

Further contrary results were found in another study about exclusionary practices by Hong and

Kacperczyk (2009). The authors attest that negative screening involves certain costs due to a lack

of diversification. Yet, these costs are considered rather small as there are few excluded stocks in

the stocks universe. The authors analyse the investing environment of publicly traded stocks in-

volved in tobacco alcohol and gambling – also known as sin stocks11. Investigating the ownership

structure of these stocks, they found that sin stocks’ cost of capital is affected by their neglect by

institutional investors. The paper argues that fewer sin stocks are held by institutions that are

exposed to ‘social norm pressure due to the public nature’ of their businesses and their diverse

constituencies. The authors list institutions such as pension funds, universities, religious organisa-

tions, banks and insurance companies as among these institutions. Their results indicate that sin

stocks are relatively cheap when benchmarked against comparable stocks as their market-to-

book, price-to-earnings and price-to-EBITDA ratios are significantly smaller than their compara-

bles'(see Table 1). Surprisingly, the application of the Carhart (1997) model results in US stocks

outperforming comparable stocks by 26 basis points per month, or 3.1% per year relative to

comparable stocks(21basis points per month or 2.5% per year for European stocks). Hong and

Kacperczyk (2009) imply that higher stock returns can be seen as compensation for future litiga-

tion costs since sin stocks face substantial litigation risk.

On the other hand, Moskowitz (1972) considers companies with solid corporate social perfor-

mance (CSP) more likely to show high financial performance. Following his argument, socially

aware management will also possess the requisite skills to run a successful business resulting in

equivalent financial performance. Increased environmental and social performance in particular

are identified as an indication of management quality (Fombrun and Shanley ,1990).

Employing a more comprehensive view/wider focus on ESG issues, Galema et al. (2008) take

into account the overall CSR performance of stocks. They use ESG scores from KLD Research

and Analytics, Inc12 that are partitioned into six different themes13 and find SRI firms’ valuation

ratios to be 15-20% lower than those of comparable stocks (see Table 1). Their research indicates

that only diversity, environment and product performance to have a significant impact. A long-

short investment strategy with community-strength and -concern portfolios yields an alpha of

3.4% per year.

According to Porter and Kramer (2006), another potentially positive effect of CSR on risk is

linked to reputation. Since potential reputational damage constitutes a factual threat to firm value,

the authors recognise CSR practices as generating reputational benefits and consider them as an

important factor in risk management. McGuire et al. (1988) acknowledge a potential reputational

11 Note: Hong and Kacperczyk focused on tobacco, alcohol and gambling, but did not include companies involved

in adult entertainment since there were very few publicly traded companies that were relevant. The authors also omitted the defence industry since it was not clear for them whether it is considered ‘sinful’. Instead they added companies from the Fama and French (1997) industry grouping ‘guns’ to their robustness analyses.

12 Today known as MSCI ESG KLD STATS 13 Community involvement, corporate governance, diversity, employee relations, environment and product.

upswing from social and environmental efforts that can better a firm’s access to finance. Another

study by Cahan et al. (2005) also highlights the reputational channel but refutes an absolute ef-

fect. Their findings point out the importance of media favourability due to the significant interac-

tion between this and CSR performance. The research concludes that only in cases of favourable

media coverage can high CSR performance can to higher firm value or lower cost of capital.

This view is also supported by studies focusing on the social dimension of ESG compliance,

more precisely on employee related issues. Edmans (2011) conducted a study based on an em-

ployee survey by Levering and Moskowitz (1993) and investigated the financial effects of em-

ployee satisfaction. His findings demonstrate a positive relationship with stock returns. Edmans’

multifactor regressions lead to significant alphas (see Table 1) for high employee-satisfaction

portfolios and therefore highlight the benefit of employee relations as a component of social

ESG screens. Nevertheless, the authors note that the implications of their findings are unclear for

future stock returns. Since intangibles are difficult to incorporate into stocks prices, it remains an

open question whether the market will learn about the positive correlation resulting in it to dis-

appearing in the long run. A study by Derwall et al. (2011) that fills this research gap shares the

argument of underestimated ESG issues. Edmans’ research focus is summarised and referred to

as the errors-in-expectations hypothesis. The authors investigated and compared it with the

shunned-stock hypothesis based on the work of Heinkel (2001) and Hong and Kacperczyk

(2009). Derwall et al. (2011) studied the outperformance of socially-strong stock portfolios with

high employee-ratings as well as the outperformance of controversial sin stocks. Their findings

confirm the temporary nature of errors-in-expectations, as both portfolios demonstrate superior

returns but strong-employee stocks outperform only in the short-run and yield no significant

alphas in an expanded examination period. A crucial part of the study is the breakdown of SRI

investors into values-oriented versus profit-oriented ones which provides a theoretical foundation

for both hypotheses.

While the academic literature used to have a homogenous understanding of an SRI investor –

one who grounds his investment decisions solely in social and personal values – Derwall et at.

demand attention on another type of market player, the profit-seeking SRI investor. This inves-

tor’s approach integrates ESG issues but still conforms to traditional wealth-maximising goals.

Furthermore, the consideration of environmental criteria into investment decisions can have pos-

itive effects as the findings of Derwall et al. (2005) indicate. The authors use the eco-efficiency

ratings of US companies in order to construct equity portfolios. They found that best-in-class14

stocks outperform worst-in-class stocks by 6 percentage points per year during 1997-2003. Aktas

et al. (2011) found evidence for the value creation of SRI within a mergers and acquisitions

framework. They identify the environmental and social performance of a target firm as having a

positive influence on the acquiring firm’s cumulative abnormal return (CAR). The authors reject

the idea of SRI as a value-destroying action that makes socially responsible firms more common

targets for disciplinary take-overs. According to Aktas et al., value creation for acquirer share-

holders does not originate in over-investment in SRI by the target company. Rather, the acquirer

learns from and adapts to the target’s SRI practices and experience.

Shifting back to the stock market, Nofsinger and Varma (2014) computed return alphas for SRI

mutual funds in non-crisis and crisis periods. They document the outperformance of socially re-

sponsible mutual funds during periods of market crises – at the cost of underperformance during

non-crisis periods. The authors consider SRI funds as an attractive investment option for down-

side-risk protection due to the asymmetry of these returns. Henke (2016) investigated the finan-

cial impact of ESG screening on corporate bond funds and claims to provide further evidence

for market inefficiency and mispriced ESG risks. His results confirm the beneficial effects of

CSR activities that lead to a reduction of corporate risks for investors. SRI funds are observed to

be especially successful during market declines and therefore constitute an attractive investment

for long-term investors. Overall, Henke supports the mitigation of ESG risks in bond portfolios

and found no evidence of a trade-off between SRI and financial objectives. He identifies worst-

in-class exclusion as a better implementation of ESG information rather than a best-in-class

screening.

Given this ongoing dispute on the effectiveness of ESG investing, this thesis fills a research gap

in that it provides a more comprehensive investigation through analysing recent ESG compliance

data from 2013-2015. While the abovementioned studies focus solely on one particular ESG

component15, this paper investigates the combination of social, environmental and governance-

related aspects together.

My findings are supportive on both views of ESG investing. On the one hand, I find that both

high and low ESG-performance portfolios display negative alphas, but that high ESG-

performance lead to a less negative return. This is an interesting result and could indicate that

14 When using the terms “best-in-class” and “worst-in-class” the literature refers to investment portfolios that are

based on the ESG performance of companies that exhibit the best and respectively worst ESG ratings within a sample (Nagy et al (2013)

15 E.g. Gompers et al. (2003) focus on governance; Derwall et al. (2005) focus on environmental issues; Derwall et al. (2011) focus on employee satisfaction (social component). See Table 1 for other examples.

neither of these ‘extremes’, but rather a well-balanced portfolio leads to positive alphas. Whether

this is the case, is subject to future research.

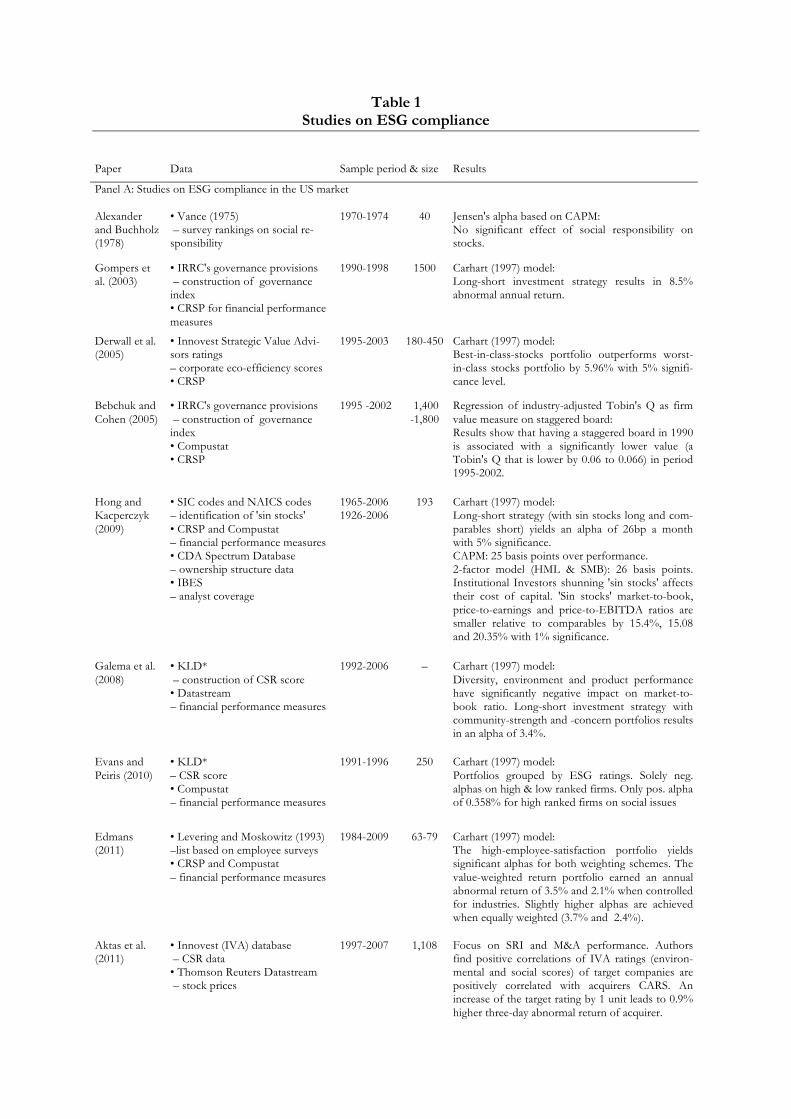

Table 1 Studies on ESG compliance

Paper Data Sample period & size Results

Panel A: Studies on ESG compliance in the US market Alexander and Buchholz (1978)

• Vance (1975) – survey rankings on social re-sponsibility

1970-1974 40 Jensen's alpha based on CAPM: No significant effect of social responsibility on stocks.

Gompers et al. (2003)

• IRRC's governance provisions – construction of governance index • CRSP for financial performance measures

1990-1998 1500 Carhart (1997) model: Long-short investment strategy results in 8.5% abnormal annual return.

Derwall et al. (2005)

• Innovest Strategic Value Advi-sors ratings – corporate eco-efficiency scores • CRSP

1995-2003 180-450 Carhart (1997) model: Best-in-class-stocks portfolio outperforms worst-in-class stocks portfolio by 5.96% with 5% signifi-cance level.

Bebchuk and Cohen (2005)

• IRRC's governance provisions – construction of governance index • Compustat • CRSP

1995 -2002 1,400 -1,800

Regression of industry-adjusted Tobin's Q as firm value measure on staggered board: Results show that having a staggered board in 1990 is associated with a significantly lower value (a Tobin's Q that is lower by 0.06 to 0.066) in period 1995-2002.

Hong and Kacperczyk (2009)

• SIC codes and NAICS codes – identification of 'sin stocks' • CRSP and Compustat – financial performance measures • CDA Spectrum Database – ownership structure data • IBES – analyst coverage

1965-2006 1926-2006

193 Carhart (1997) model: Long-short strategy (with sin stocks long and com-parables short) yields an alpha of 26bp a month with 5% significance. CAPM: 25 basis points over performance. 2-factor model (HML & SMB): 26 basis points. Institutional Investors shunning 'sin stocks' affects their cost of capital. 'Sin stocks' market-to-book, price-to-earnings and price-to-EBITDA ratios are smaller relative to comparables by 15.4%, 15.08 and 20.35% with 1% significance.

Galema et al. (2008)

• KLD* – construction of CSR score • Datastream – financial performance measures

1992-2006 – Carhart (1997) model: Diversity, environment and product performance have significantly negative impact on market-to-book ratio. Long-short investment strategy with community-strength and -concern portfolios results in an alpha of 3.4%.

Evans and Peiris (2010)

• KLD* – CSR score • Compustat – financial performance measures

1991-1996 250 Carhart (1997) model: Portfolios grouped by ESG ratings. Solely neg. alphas on high & low ranked firms. Only pos. alpha of 0.358% for high ranked firms on social issues

Edmans (2011)

• Levering and Moskowitz (1993) –list based on employee surveys • CRSP and Compustat – financial performance measures

1984-2009 63-79 Carhart (1997) model: The high-employee-satisfaction portfolio yields significant alphas for both weighting schemes. The value-weighted return portfolio earned an annual abnormal return of 3.5% and 2.1% when controlled for industries. Slightly higher alphas are achieved when equally weighted (3.7% and 2.4%).

Aktas et al. (2011)

• Innovest (IVA) database – CSR data • Thomson Reuters Datastream – stock prices

1997-2007 1,108 Focus on SRI and M&A performance. Authors find positive correlations of IVA ratings (environ-mental and social scores) of target companies are positively correlated with acquirers CARS. An increase of the target rating by 1 unit leads to 0.9% higher three-day abnormal return of acquirer.

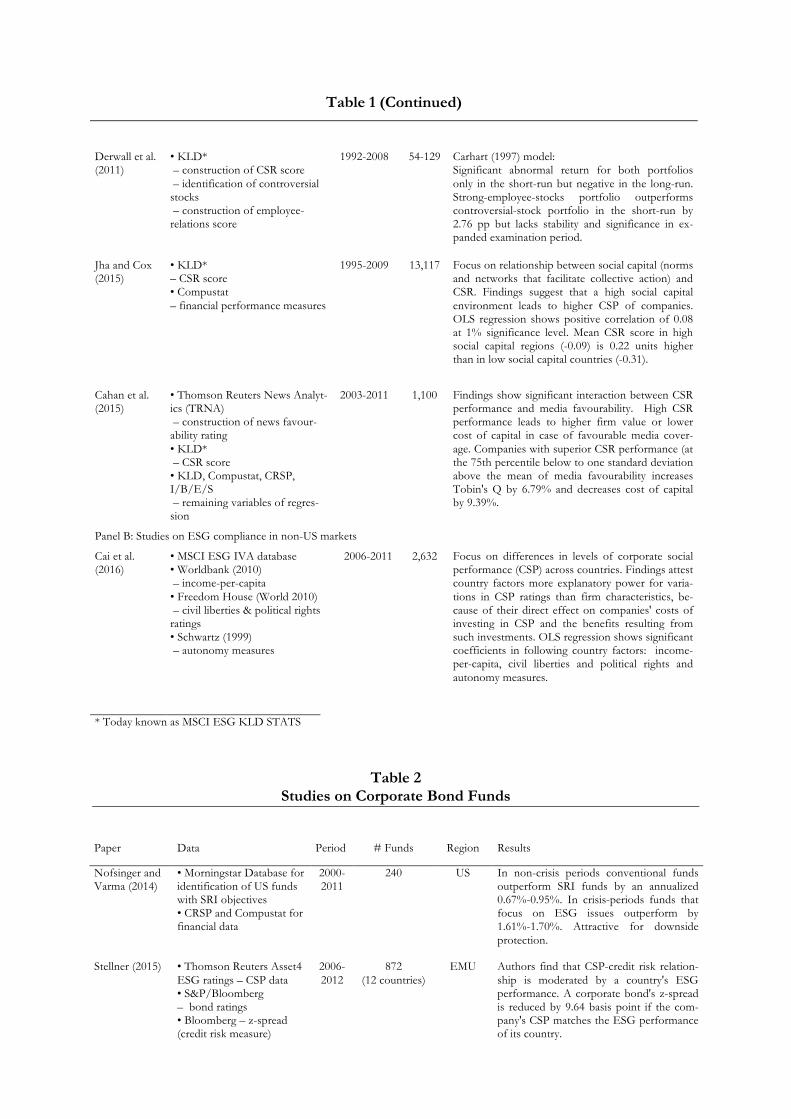

Table 1 (Continued)

Derwall et al. (2011)

• KLD* – construction of CSR score – identification of controversial stocks – construction of employee-relations score

1992-2008 54-129 Carhart (1997) model: Significant abnormal return for both portfolios only in the short-run but negative in the long-run. Strong-employee-stocks portfolio outperforms controversial-stock portfolio in the short-run by 2.76 pp but lacks stability and significance in ex-panded examination period.

Jha and Cox (2015)

• KLD* – CSR score • Compustat – financial performance measures

1995-2009 13,117 Focus on relationship between social capital (norms and networks that facilitate collective action) and CSR. Findings suggest that a high social capital environment leads to higher CSP of companies. OLS regression shows positive correlation of 0.08 at 1% significance level. Mean CSR score in high social capital regions (-0.09) is 0.22 units higher than in low social capital countries (-0.31).

Cahan et al. (2015)

• Thomson Reuters News Analyt-ics (TRNA) – construction of news favour-ability rating • KLD* – CSR score • KLD, Compustat, CRSP, I/B/E/S – remaining variables of regres-sion

2003-2011 1,100 Findings show significant interaction between CSR performance and media favourability. High CSR performance leads to higher firm value or lower cost of capital in case of favourable media cover-age. Companies with superior CSR performance (at the 75th percentile below to one standard deviation above the mean of media favourability increases Tobin's Q by 6.79% and decreases cost of capital by 9.39%.

Panel B: Studies on ESG compliance in non-US markets

Cai et al. (2016)

• MSCI ESG IVA database • Worldbank (2010) – income-per-capita • Freedom House (World 2010) – civil liberties & political rights ratings • Schwartz (1999) – autonomy measures

2006-2011 2,632 Focus on differences in levels of corporate social performance (CSP) across countries. Findings attest country factors more explanatory power for varia-tions in CSP ratings than firm characteristics, be-cause of their direct effect on companies' costs of investing in CSP and the benefits resulting from such investments. OLS regression shows significant coefficients in following country factors: income-per-capita, civil liberties and political rights and autonomy measures.

* Today known as MSCI ESG KLD STATS

Table 2 Studies on Corporate Bond Funds

Paper Data Period # Funds Region Results

Nofsinger and Varma (2014)

• Morningstar Database for identification of US funds with SRI objectives • CRSP and Compustat for financial data

2000-2011

240 US In non-crisis periods conventional funds outperform SRI funds by an annualized 0.67%-0.95%. In crisis-periods funds that focus on ESG issues outperform by 1.61%-1.70%. Attractive for downside protection.

Stellner (2015) • Thomson Reuters Asset4 ESG ratings – CSP data • S&P/Bloomberg – bond ratings • Bloomberg – z-spread (credit risk measure)

2006-2012

872 (12 countries)

EMU Authors find that CSP-credit risk relation-ship is moderated by a country's ESG performance. A corporate bond's z-spread is reduced by 9.64 basis point if the com-pany's CSP matches the ESG performance of its country.

Table 2 (Continued) Henke (2016) • Sustainalytics

– ESG ratings • CRSP – financial performance measures (US sample) • Bloomberg – financial performance measures (Eurozone)

2001-2014

412 total (103 SRI)

US & Eurozone

Focus: Impact analysis of ESG screening on corporate bond funds via application of five-factor model: Annual alphas of SRI funds outperform conventional funds in US by 0.33%, in Eurozone by 0.49%. Findings support hypotheses of misprized ESG risks and corporate risk reduction through CSR activities. SRI funds' especially successful during market declines, thus attractive for long-term investors. Mitigation of ESG risk in bond portfolios leads to no trade-off between SRI and financial objectives. Conclusion: worst-in-class exclusion as a better strategy rather than best-in-class screening.

3 Hypotheses This thesis examines stock performance of firms based on their CSR level. My intention is to

compare two conflicting hypotheses in this field, the “shunned stocks hypothesis” and the “er-

rors in expectations hypothesis” which will be further explained in the following.

Hypothesis 1: Shunned stocks hypothesis

Hypothesis 1 suggests that socially controversial stocks show superior returns. This is due to the

fact that values-driven investors avoid these stocks and therefor push their prices, ceteris paribus,

below responsible stocks’. This hypothesis is based on Hong and Kacperczyk (2009) who state

that “sin stocks” are neglected by institutional investors, making these stocks relatively cheap. I

extend their scope of work by not only investigating stocks that are active in the fields of alcohol,

tobacco and gambling, but all stocks and their corresponding CSR rating. To evidence superior

returns in controversial stocks, I am looking at differences in alphas in the CAPM model (simple

and extended). I expect positive alphas for socially controversial stocks for this hypothesis to

hold true.

Hypothesis 2: Errors in expectations hypothesis

On the other hand, hypothesis 2 suggests that socially responsible stocks show higher risk-

adjusted returns due to a certain market inefficiency regarding the recognition of CSR practices.

Stocks of companies with higher ESG performance show lower risk and those of low ESG per-

formance show higher risk. This hypothesis is more in line with the works of Edmans (2011) and

Pantzalis and Park (2009). Similar to hypothesis 1, a difference in alphas in the CAPM model will

show whether socially responsible stocks show higher risk-adjusted returns. This would be ob-

servable in positive alphas for this type of stocks.

4 Methodological Approach and Data

Approach

This research conducts an analysis based on data provided by Morgan Stanley Capital Interna-

tional (MSCI) ESG Research. MSCI ESG Research is a widely accepted provider of in-depth

ESG research, ratings and indices. Its services are profit based, hence its index with the distinc-

tion from AAA to CCC ratings is not fully available for the research purpose of this study. In-

stead, it is aimed to use company specific ESG ratings from MSCI ESG KLD STATS provided

through WHARTON data base. This dataset consists of companies’ individual ESG scores which

amount to 36,000 observations and will be used to scale ESG compliance. The MSCI ESG KLD

STATS offers various variables indicating environmental, social and governance performance. In

order to proxy ESG performance, 34 performance indicators (see appendix) are picked based on

37 ESG key issues, originating from the three pillars Environment, Social and Governance. Re-

spective performance indicators are selected in accordance to the methodology of MSCI ESG

Research (ESG Ratings Methodology Executive Summary, Feb 2017). Each key issue is a binary

score and represents either a positive or negative performance indicator. In line with MSCI

methodology, positive and negative attributes will be summed to arrive at an overall ESG score,

where a positive indicator adds a point and negative one subtracts a point (Statman 2005). Fur-

ther it is aimed to construct portfolios consisting of the highest and lowest ESG performance

deciles and mimic an investment strategy that buys the high-ESG portfolio and sells the one with

low ESG scores in order to investigate whether this strategy generates abnormal stock returns.

Financial variables of respective companies are based on CSRP-Data, also available through

WHARTON data base. The list of respective companies from MSCI ESG KLD STATS is

merged with CRSP stock information. All ESG data is based on the time period 2013-2015.

Methodology

In the first step, the portfolio performance is measured through the Capital Asset Pricing Model

(CAPM) in order to account for differentials in the portfolios’ market risks. An ordinary least-

squares regression is used for estimation of the model:

𝑅"# − 𝑅%# = 𝛼" + 𝛽"(𝑅+# − 𝑅%#) + 𝜀"#

where 𝑅"# = return on portfolio 𝑖 in month 𝑡 𝑅%# = one month U.S. T-bill rate at 𝑡 𝑅+# = return on a value weighted market proxy in month 𝑡 𝜀"# = an error term

The market proxy and risk-free rate are available at the Kenneth French Data Library16. The

model beta, 𝛽" , is interpreted a measure of a portfolio’s market-risk exposure, and Jensen’s alpha,

𝛼" , constitutes the average abnormal return in excess of the return of the market proxy. The un-

derlying assumption of this framework is that the alpha is an accurate estimate of risk-adjusted

performance.

In the second step, the portfolios are analysed within Carhart’s (1997) multifactor framework that

controls not only for market but also size, book-to-market and momentum effects. It is con-

structed using Fama and French’s (1993) three-factor model adding Jagadeesh and Titman’s

(1993) one-year momentum anomaly

𝑅"# = 𝛼" + 𝛽0"𝑅𝑀𝑅𝐹#34 + 𝛽4"𝑆𝑀𝐵"#–4 + 𝛽8"𝐻𝑀𝐿"#–4 + 𝛽;"𝑀𝑜𝑚𝑒𝑛𝑡𝑢𝑚"#–# + 𝜀"#

where Rit is the monthly return on a portfolio in excess to a monthly risk free rate; RMRFt-1 is the

excess return on a value-weighted aggregate market proxy; and SMB (small-minus-big), HML

(high-minus-low) and Momentum are returns on zero investment factor-mimicking portfolios for

size, book-to-market-equity, and one-year momentum in stock returns (Gompers et al. 2003)17. α

is the most important variable and is used to measure over performance. This model will be used

to compare portfolios with different levels of ESG compliance. The differences in alpha esti-

mates between entities or rather portfolios with high and low ESG scores indicate whether rat-

ings contribute to excess returns.

Financial Data is obtained via WRDS from CRSP Monthly Stock. The monthly returns for each

stock are calculated according to following equation

𝑟"# = 𝑙𝑛(𝑃𝑟𝑖𝑐𝑒"4)−𝑙𝑛(𝑃𝑟𝑖𝑐𝑒"#34)

By using log returns the calculations achieve more numerical stability and statistical significance 16 Available at mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html, or through WRDS. 17 For details of the construction of SMB and HML, see Fama and French (1993). Momentum is constructed accord-ing to Carhart (1997) as the equal-weight average of firms with the highest 30 percent eleven-month returns lagged one month minus the equal-weight average of firms with the lowest 30 percent eleven-month returns lagged one month.

than with arithmetic returns.

Data Preparation

Index

The basic idea to assess the proposed hypotheses is to observe the effect responsible investing

has on the stock return by using panel data. Before analysing stock returns, each firm’s ESG per-

formance has to be captured and quantified within an index. Relevant variables are only available

for the years 2013, 2014 and 2015. In order to confront this “small-sample” problem, I followed

Derwall et al. (2005) by extending the data 2 years backwards until 2011. The authors approve

this approach in consideration of the low variability of this kind of data. They concede a potential

“look-ahead” bias to accompany to this procedure but I obtained similar results for the non-

extrapolated period.

Company-specific ESG performance measures are annually displayed. According to Goss and

Roberts (2011), ESG information can lag up to 3 years since the metrics can take several years to

acquire. In order to control for this possible source of endogeneity only companies with 3 years

of consecutive data are included. This restriction leads to a sample of 1,827 companies per year.

The index is built by summarizing binary performance indicators leading to a total ESG score for

each year. Finally, the companies’ performance average over the entire period is calculated.

Aggregating the performance prohibits from rebalancing stock portfolios annually and also does

not allow for an ESG-tilt investment strategy, however the calculation of the average stands in

full accordance to the methodology used by Evans and Peiris (2010) who base their analysis on

the Domini Social Index (DSI). The underlying data points the authors make use of are part of

the same data set as the one this paper bases its analysis on. The index, maintained by Kinder,

Lydenberg, Domini (KLD) Research & Analytics18, later became part of MSCI ESG KLD

STATS when MSCI ESG acquired KLD in 201019.

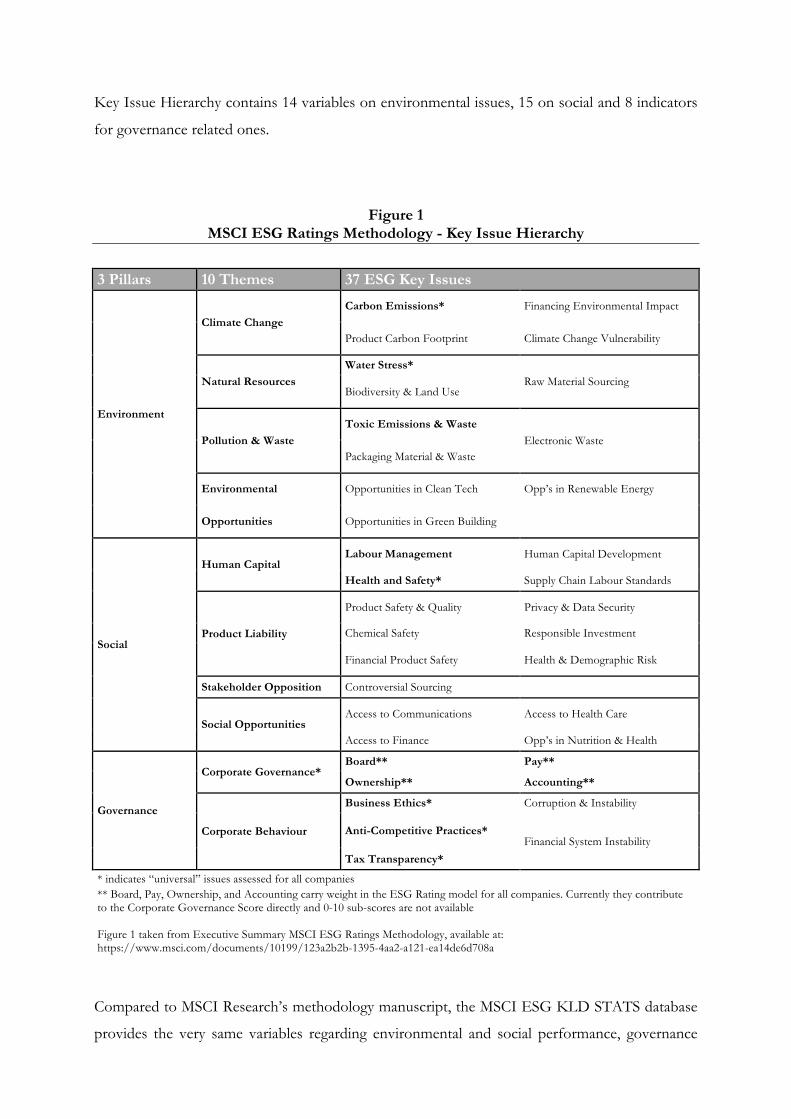

In order to profile individual companies’ performance, I use the MSCI ESG KLD STATS data

which solely contains raw binary ESG scores without historic industry-specific weighting infor-

mation. Relevant ESG performance indicators are chosen in accordance to the Key Issue Hierar-

chy of MSCI ESG Ratings Methodology (2015) consisting of 37 variables in total (see Figure 1).

18 Heinkel et al. (2001) 19 Source: https://wrds-web.wharton.upenn.edu/wrds/query_forms/navigation.cfm?navId=280)

Key Issue Hierarchy contains 14 variables on environmental issues, 15 on social and 8 indicators

for governance related ones.

Figure 1 MSCI ESG Ratings Methodology - Key Issue Hierarchy

3 Pillars 10 Themes 37 ESG Key Issues

Environment

Climate Change Carbon Emissions* Financing Environmental Impact

Product Carbon Footprint Climate Change Vulnerability

Natural Resources Water Stress*

Raw Material Sourcing Biodiversity & Land Use

Pollution & Waste Toxic Emissions & Waste

Electronic Waste Packaging Material & Waste

Environmental Opportunities in Clean Tech Opp’s in Renewable Energy

Opportunities Opportunities in Green Building

Social

Human Capital Labour Management Human Capital Development

Health and Safety* Supply Chain Labour Standards

Product Liability

Product Safety & Quality Privacy & Data Security

Chemical Safety Responsible Investment

Financial Product Safety Health & Demographic Risk

Stakeholder Opposition Controversial Sourcing

Social Opportunities Access to Communications Access to Health Care

Access to Finance Opp’s in Nutrition & Health

Governance

Corporate Governance* Board** Pay**

Ownership** Accounting**

Corporate Behaviour

Business Ethics* Corruption & Instability

Anti-Competitive Practices* Financial System Instability

Tax Transparency*

* indicates “universal” issues assessed for all companies ** Board, Pay, Ownership, and Accounting carry weight in the ESG Rating model for all companies. Currently they contribute to the Corporate Governance Score directly and 0-10 sub-scores are not available Figure 1 taken from Executive Summary MSCI ESG Ratings Methodology, available at: https://www.msci.com/documents/10199/123a2b2b-1395-4aa2-a121-ea14de6d708a

Compared to MSCI Research’s methodology manuscript, the MSCI ESG KLD STATS database

provides the very same variables regarding environmental and social performance, governance

related variables, however differ from the Ratings Methodology with the exception of 2 indica-

tors. Since MSCI uses a separate in-house index for governance related issues, there is no full

disclosure in the database (see Figure 1). In order to circumvent this lack of information, 4 gov-

ernance variables were picked from the dataset featuring similarities with the Key Issue Hierar-

chy. After dropping variables with unusable data my index results in 34 variables in total - 14

environmental, 15 social and 6 governance-related variables with 4 governance variables as well

as 1 social variable being negatively defined.

Computation of Performance

Every company is described by 34 binary variables that are 0 or 1. Usually a 1 represents extraor-

dinary efforts regarding an ESG issue. For example, the variable Recycling is defined as an indica-

tion for extraordinary efforts related to recycling and therefore minimizing one’s environmental

footprint. If a company is attested with a 0 regarding this indicator, that does not conclude pollu-

tion or negligence in recycling but neutrality. Missing values are therefore treated as neutral and

respectively 0. For negatively defined variables the underlying data is also binary but have to de-

ducted when summarised. Labour Standards for example is defined as an indication of controver-

sies related to the safety of a firm’s employees and therefore has to be deducted from a compa-

ny’s overall performance if the underlying data is equal to 1. Since the number of governance

variables is underrepresented and mostly negatively defined, their inclusion could skew the index

results. Yet, representative results are not endangered since computation is performed for envi-

ronmental, social and governance indicators separately. Summary statistics are provided for all 3

years as well as for the average of the total period.

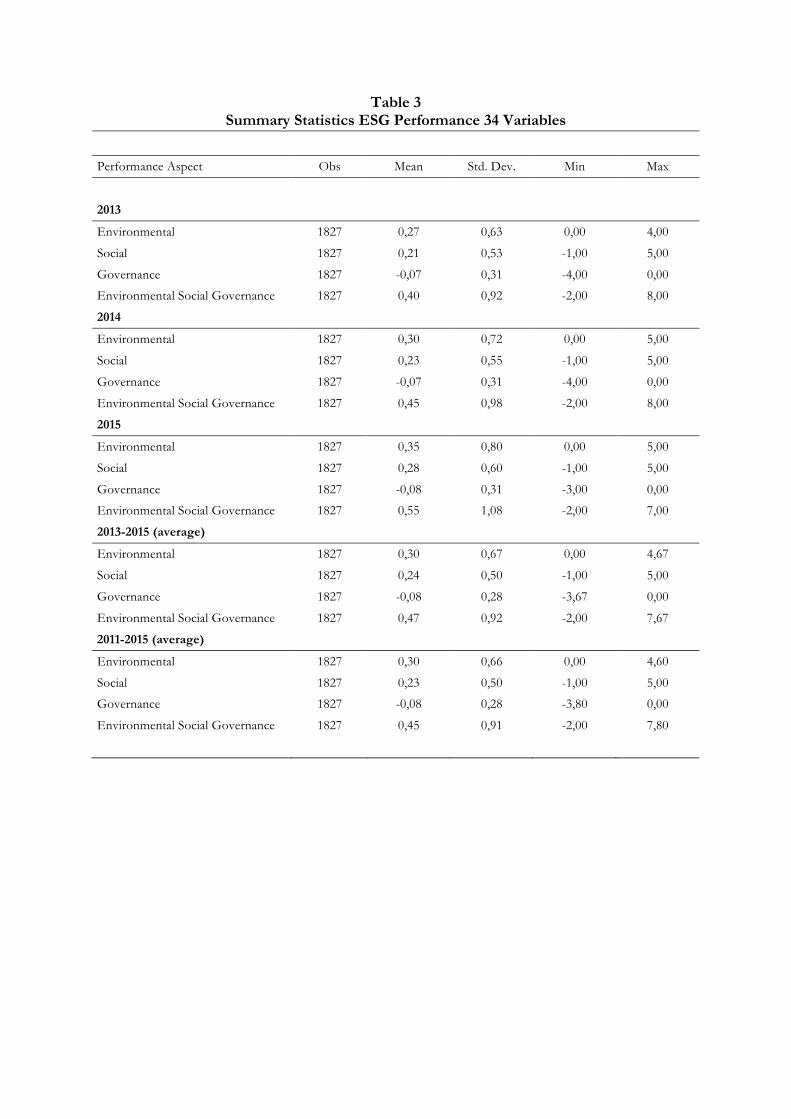

Table 3 Summary Statistics ESG Performance 34 Variables

Performance Aspect Obs Mean Std. Dev. Min Max

2013 Environmental 1827 0,27 0,63 0,00 4,00

Social 1827 0,21 0,53 -1,00 5,00

Governance 1827 -0,07 0,31 -4,00 0,00

Environmental Social Governance 1827 0,40 0,92 -2,00 8,00

2014 Environmental 1827 0,30 0,72 0,00 5,00

Social 1827 0,23 0,55 -1,00 5,00

Governance 1827 -0,07 0,31 -4,00 0,00

Environmental Social Governance 1827 0,45 0,98 -2,00 8,00

2015 Environmental 1827 0,35 0,80 0,00 5,00

Social 1827 0,28 0,60 -1,00 5,00

Governance 1827 -0,08 0,31 -3,00 0,00

Environmental Social Governance 1827 0,55 1,08 -2,00 7,00

2013-2015 (average) Environmental 1827 0,30 0,67 0,00 4,67

Social 1827 0,24 0,50 -1,00 5,00

Governance 1827 -0,08 0,28 -3,67 0,00

Environmental Social Governance 1827 0,47 0,92 -2,00 7,67

2011-2015 (average) Environmental 1827 0,30 0,66 0,00 4,60

Social 1827 0,23 0,50 -1,00 5,00

Governance 1827 -0,08 0,28 -3,80 0,00

Environmental Social Governance 1827 0,45 0,91 -2,00 7,80

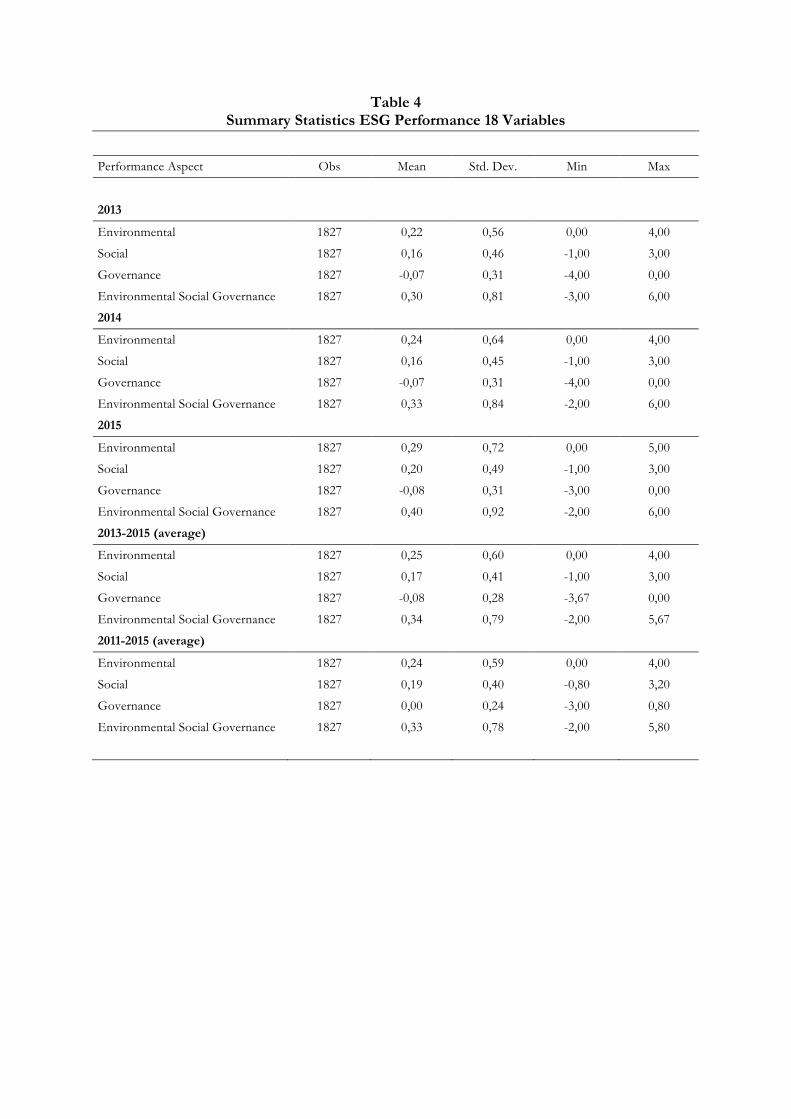

Further Selection

With the objective of increased quality of computed results, variables were eliminated with re-

spect to their explanatory power. A flaw in the data set is that a lot of variables have missing val-

ues which can lead to diluted results. In order to make the analysis justifiable, I picked 18 out of

the 34 variables which have a reliable amount of values (dropped variables have more than 90%

of missing values). Reviewing these hand-picked variables showed that there are 6 environmental,

6 social (1 negatively defined) and 4 governance related (1 negatively defined) variables left. Hav-

ing all three ESG pillars covered, as well as all ten ESG themes, I conclude that the picked varia-

bles are representative, given that all “universal” issues are included in the analysis The distribu-

tion of this new sample does not change significantly. The remaining variables are Carbon Emis-

sions (env_str_d), Energy Efficiency (env_str_o), Water Stress (env_str_h), Raw Material Sourc-

ing (env_str_j), Toxic Emissions & and Waste (env_str_b), Beneficial Products & Services

(env_str_a), Health & Safety Strength (emp_str_g), Health & Safety Concern (emp_con_b), Hu-

man Capital Management (emp_str_l), Quality (pro_str_a), Chemical Product Safety (pro_str_g),

Privacy & Data Security (pro_str_i), Access to Capital (pro_str_d), Executive Compensation

(cgov_con_k), Controversial Investments (cgov_con_l), Business Ethics (cgov_con_m), Antitrust

(pro_con_e) and Other Concerns (cgov_con_x), disregarded variables are Product Carbon Foot-

print (env_str_p), Financing Environmental Impact (env_str_k), Climate Change Vulnerability

(env_str_q), Biodiversity & Land Use (env_str_i), Recycling (env_str_c), Electronic Waste

(env_str_n) Green Buildings (env_str_l), Renewable Energy (env_str_m), Financial Product Safe-

ty (pro_str_h), Responsible Investment (pro_str_j), Health & Demographic Risk (pro_str_k),

Controversial Sourcing (emp_str_n), Access to Communications (pro_str_e), Benefits to Eco-

nomically Disadvantaged (pro_str_c) and Opportunities in Nutrition & Health(pro_str_f).

Table 4 Summary Statistics ESG Performance 18 Variables

Performance Aspect Obs Mean Std. Dev. Min Max

2013 Environmental 1827 0,22 0,56 0,00 4,00

Social 1827 0,16 0,46 -1,00 3,00

Governance 1827 -0,07 0,31 -4,00 0,00

Environmental Social Governance 1827 0,30 0,81 -3,00 6,00

2014 Environmental 1827 0,24 0,64 0,00 4,00

Social 1827 0,16 0,45 -1,00 3,00

Governance 1827 -0,07 0,31 -4,00 0,00

Environmental Social Governance 1827 0,33 0,84 -2,00 6,00

2015 Environmental 1827 0,29 0,72 0,00 5,00

Social 1827 0,20 0,49 -1,00 3,00

Governance 1827 -0,08 0,31 -3,00 0,00

Environmental Social Governance 1827 0,40 0,92 -2,00 6,00

2013-2015 (average) Environmental 1827 0,25 0,60 0,00 4,00

Social 1827 0,17 0,41 -1,00 3,00

Governance 1827 -0,08 0,28 -3,67 0,00

Environmental Social Governance 1827 0,34 0,79 -2,00 5,67

2011-2015 (average) Environmental 1827 0,24 0,59 0,00 4,00

Social 1827 0,19 0,40 -0,80 3,20

Governance 1827 0,00 0,24 -3,00 0,80

Environmental Social Governance 1827 0,33 0,78 -2,00 5,80

5 Results In this section the empirical results are presented. As explained in the previous section, two re-

gression models have been applied. First, the simple CAPM framework was used to measure al-

phas in portfolio returns and then the more sophisticated Carhart multifactor framework.

5.1 Simple CAPM Framework

With focus on market risk, portfolio performance was measured first within the CAPM frame-

work according to the regression model

𝑅"# − 𝑅%# = 𝛼" + 𝛽"(𝑅+# − 𝑅%#) + 𝜀"# where 𝛼" is return above the market premium, or simply called alpha. It represents the percentage

return of the respective portfolio per month in addition to the market premium.

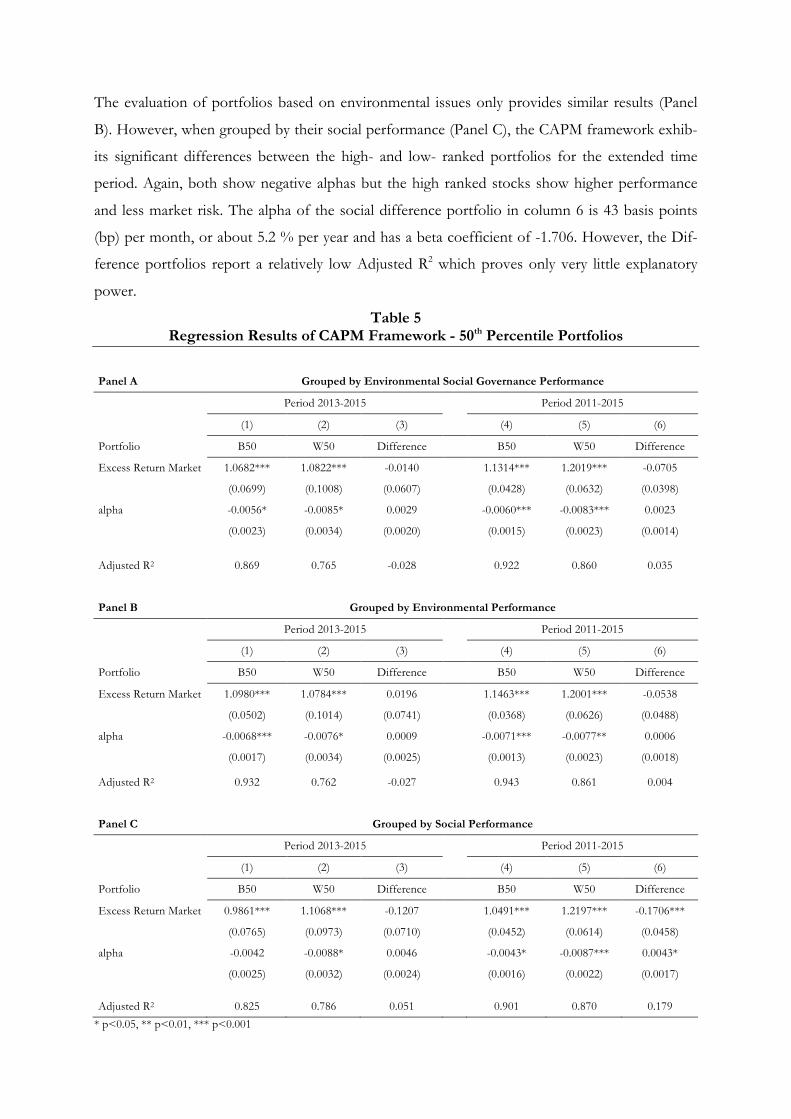

For the period of 2013-2015 and 2011-2015, Table 5 illustrates the performance evaluation re-

sults of high- and low-ranked portfolios on ESG compliance as well as the respective ‘Difference’

portfolio returns. The attribution of high- and low-ranked comprises a distinction between firms

above and below the 50th percentile. Difference portfolio returns are constructed by subtracting

low ESG-level portfolio returns from the returns of high ESG-level stocks. Panel A reports on

performance differences within overall ESG compliance, containing all 18 indicators. Panel B

reports on differentials between portfolios grouped solely on environmental issues and Panel C

illustrates results of stocks grouped on social issues only.

Looking at the observation period of 2013-2015 in Panel A, both, the high-ranked firms’ as well

as the low-ranked firms’ alphas are negative, with -0.56% for high-ranked firms and -0.85% for

low-ranked firms respectively. This result is significant at the 5% level for both the high-ranked

firms and the low-ranked firms. While low-ranked ESG stocks exhibit a slightly lower alpha, this

difference is not significant while tested separately. A difference portfolio of high-ranked firms

minus low-ranked firms yields an alpha of 0.29%, which is not significant at the 5% level. A

comparison of the betas shows that the portfolios also did not differ significantly in their market

risk exposure. Similar results were achieved by looking at the extended observation period. The

increased amount of data led to a higher significance (0.1%). The high-ranked firms show a nega-

tive alpha of -0.60% and the low-ranked firms a negative alpha of -0.83%. Still, the difference in

returns turns out not to be significant.

The evaluation of portfolios based on environmental issues only provides similar results (Panel

B). However, when grouped by their social performance (Panel C), the CAPM framework exhib-

its significant differences between the high- and low- ranked portfolios for the extended time

period. Again, both show negative alphas but the high ranked stocks show higher performance

and less market risk. The alpha of the social difference portfolio in column 6 is 43 basis points

(bp) per month, or about 5.2 % per year and has a beta coefficient of -1.706. However, the Dif-

ference portfolios report a relatively low Adjusted R2 which proves only very little explanatory

power.

Table 5 Regression Results of CAPM Framework - 50th Percentile Portfolios

Panel A Grouped by Environmental Social Governance Performance

Period 2013-2015 Period 2011-2015

(1) (2) (3) (4) (5) (6)

Portfolio B50 W50 Difference B50 W50 Difference

Excess Return Market 1.0682*** 1.0822*** -0.0140 1.1314*** 1.2019*** -0.0705

(0.0699) (0.1008) (0.0607) (0.0428) (0.0632) (0.0398)

alpha -0.0056* -0.0085* 0.0029 -0.0060*** -0.0083*** 0.0023

(0.0023) (0.0034) (0.0020) (0.0015) (0.0023) (0.0014) Adjusted R2 0.869 0.765 -0.028 0.922 0.860 0.035

Panel B Grouped by Environmental Performance

Period 2013-2015 Period 2011-2015

(1) (2) (3) (4) (5) (6)

Portfolio B50 W50 Difference B50 W50 Difference

Excess Return Market 1.0980*** 1.0784*** 0.0196 1.1463*** 1.2001*** -0.0538

(0.0502) (0.1014) (0.0741) (0.0368) (0.0626) (0.0488)

alpha -0.0068*** -0.0076* 0.0009 -0.0071*** -0.0077** 0.0006

(0.0017) (0.0034) (0.0025) (0.0013) (0.0023) (0.0018)

Adjusted R2 0.932 0.762 -0.027 0.943 0.861 0.004

Panel C Grouped by Social Performance

Period 2013-2015 Period 2011-2015

(1) (2) (3) (4) (5) (6)

Portfolio B50 W50 Difference B50 W50 Difference

Excess Return Market 0.9861*** 1.1068*** -0.1207 1.0491*** 1.2197*** -0.1706***

(0.0765) (0.0973) (0.0710) (0.0452) (0.0614) (0.0458)

alpha -0.0042 -0.0088* 0.0046 -0.0043* -0.0087*** 0.0043*

(0.0025) (0.0032) (0.0024) (0.0016) (0.0022) (0.0017)

Adjusted R2 0.825 0.786 0.051 0.901 0.870 0.179

* p<0.05, ** p<0.01, *** p<0.001

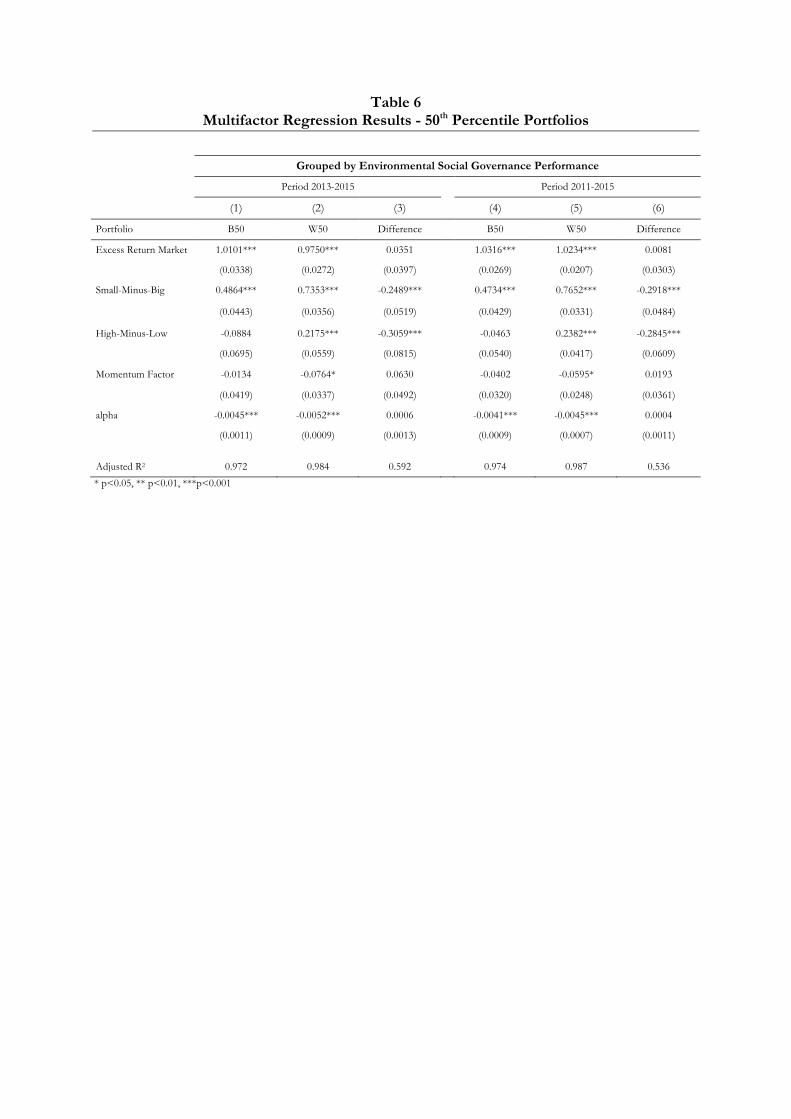

5.2 Multifactor regression

Next to the simple CAPM framework, the Carhart model was applied to measure portfolio per-

formance according to the regression model

𝑅"# = 𝛼" + 𝛽0"𝑅𝑀𝑅𝐹#34 + 𝛽4"𝑆𝑀𝐵"#–4 + 𝛽8"𝐻𝑀𝐿"#–4 + 𝛽;"𝑀𝑜𝑚𝑒𝑛𝑡𝑢𝑚"#–# + 𝜀"#

where 𝛼" is still the return above the market premium and shows the percentage return of the

respective portfolio per month in addition to the market premium.

In Table 6, multifactor regression results for stocks according to their overall ESG performance

is illustrated based on 18 performance indicators. Stocks are grouped by yearly ratings above and

below the 50th percentile. B50 represents the portfolio being in the top 50 percent of ratings,

whereas W50 being the portfolio with the bottom 50 percent ratings. Regressions are applied for

different time periods.

The alphas of the difference portfolios depict the abnormal return of what could have been

achieved by a zero-investment strategy that buys a highly compliant SRI portfolio and short sells

a highly non-compliant SRI portfolio.

Compared to the single-factor results, Table 6 reports several differences. Again, the high-ranked

(B50) as well as the low-ranked (W50) portfolios demonstrate significant negative alphas for both

the extended time period from 2011-2015 and the original from 2013-2015. The factor adjusted

returns of the extended period are -41 and -45 basis points per month or about -4.9% and -5.4%

per year. Factor loadings for the determinant SMB are generally significantly positive, which im-

plies a bias towards small-cap stocks within the sample. The HML coefficient of low-ranked

companies suggests that the portfolios are significantly tilted towards value stocks with low book-

to-market ratios. The negatively significant coefficients of low-ranked portfolios on the Momen-

tum factor suggest that stocks with relatively bad past-year performance to have relatively poor

overall SRI rankings. Compared to the CAPM framework, the Adjusted R2s of the difference

portfolios regressions have increased, but yield no significant alphas.

Table 6 Multifactor Regression Results - 50th Percentile Portfolios

Grouped by Environmental Social Governance Performance

Period 2013-2015 Period 2011-2015

(1) (2) (3) (4) (5) (6)

Portfolio B50 W50 Difference B50 W50 Difference

Excess Return Market 1.0101*** 0.9750*** 0.0351 1.0316*** 1.0234*** 0.0081

(0.0338) (0.0272) (0.0397) (0.0269) (0.0207) (0.0303)

Small-Minus-Big 0.4864*** 0.7353*** -0.2489*** 0.4734*** 0.7652*** -0.2918***

(0.0443) (0.0356) (0.0519) (0.0429) (0.0331) (0.0484)

High-Minus-Low -0.0884 0.2175*** -0.3059*** -0.0463 0.2382*** -0.2845***

(0.0695) (0.0559) (0.0815) (0.0540) (0.0417) (0.0609)

Momentum Factor -0.0134 -0.0764* 0.0630 -0.0402 -0.0595* 0.0193

(0.0419) (0.0337) (0.0492) (0.0320) (0.0248) (0.0361)

alpha -0.0045*** -0.0052*** 0.0006 -0.0041*** -0.0045*** 0.0004

(0.0011) (0.0009) (0.0013) (0.0009) (0.0007) (0.0011)

Adjusted R2 0.972 0.984 0.592 0.974 0.987 0.536 * p<0.05, ** p<0.01, ***p<0.001

6 Robustness Check

6.1 Percentiles

Chapter 5 illustrated the performance evaluation results of high- and low-ranked portfolios on

ESG compliance as well as the respective "Difference” portfolio returns through distinction be-

tween firms above and below 50th percentile. As this is a merely rough split, I furthermore inves-

tigate into the more “extreme” companies, namely the stocks in the 1st percentile and stocks in

the 5th percentile.

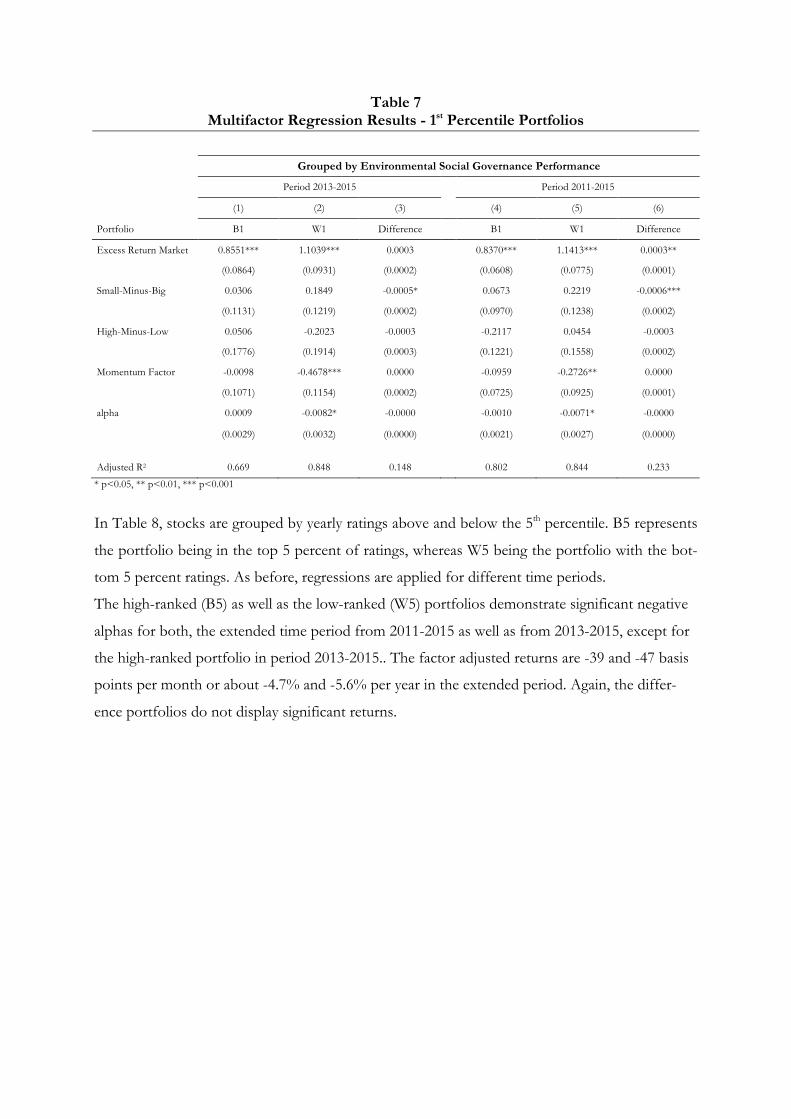

In Table 7, multifactor regression results for stocks according to their overall ESG performance

is illustrated based on 18 performance indicators. Stocks are grouped by yearly ratings above and

below the 1st percentile. B1 represents the portfolio being in the top 1 percent of ratings, whereas

W1 being the portfolio with the bottom 1 percent ratings. Regressions are applied for different

time periods.

The alphas of the difference portfolios depict the abnormal return of what could have been

achieved by a zero-investment strategy that buys a highly compliant SRI portfolio and short sells

a highly non-compliant SRI portfolio.

The high-ranked (B1) portfolio shows positive, insignificant alphas, the low-ranked (W1) portfo-

lios demonstrate significant negative alphas for the time period of 2013-2015. For the extended

time period from 2011-2015 the factor adjusted returns are -10 and -71 basis points per month or

about -1.2% and -8.5% per year. Except for the determinant Momentum, factor loadings are

generally insignificant. The Difference portfolios do not achieve significant returns, supporting

the findings of chapter 5.

Table 7 Multifactor Regression Results - 1st Percentile Portfolios

Grouped by Environmental Social Governance Performance

Period 2013-2015 Period 2011-2015

(1) (2) (3) (4) (5) (6)

Portfolio B1 W1 Difference B1 W1 Difference

Excess Return Market 0.8551*** 1.1039*** 0.0003 0.8370*** 1.1413*** 0.0003**

(0.0864) (0.0931) (0.0002) (0.0608) (0.0775) (0.0001)

Small-Minus-Big 0.0306 0.1849 -0.0005* 0.0673 0.2219 -0.0006***

(0.1131) (0.1219) (0.0002) (0.0970) (0.1238) (0.0002)

High-Minus-Low 0.0506 -0.2023 -0.0003 -0.2117 0.0454 -0.0003

(0.1776) (0.1914) (0.0003) (0.1221) (0.1558) (0.0002)

Momentum Factor -0.0098 -0.4678*** 0.0000 -0.0959 -0.2726** 0.0000

(0.1071) (0.1154) (0.0002) (0.0725) (0.0925) (0.0001)

alpha 0.0009 -0.0082* -0.0000 -0.0010 -0.0071* -0.0000

(0.0029) (0.0032) (0.0000) (0.0021) (0.0027) (0.0000)

Adjusted R2 0.669 0.848 0.148 0.802 0.844 0.233

* p<0.05, ** p<0.01, *** p<0.001

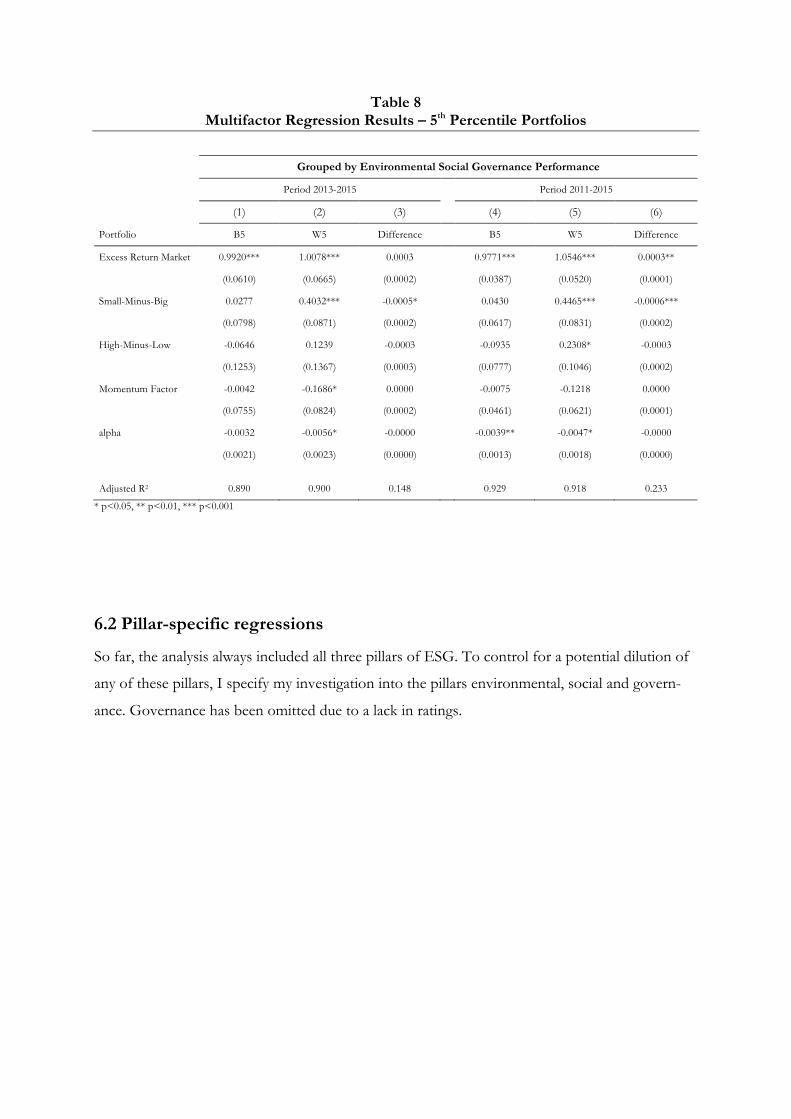

In Table 8, stocks are grouped by yearly ratings above and below the 5th percentile. B5 represents

the portfolio being in the top 5 percent of ratings, whereas W5 being the portfolio with the bot-

tom 5 percent ratings. As before, regressions are applied for different time periods.

The high-ranked (B5) as well as the low-ranked (W5) portfolios demonstrate significant negative

alphas for both, the extended time period from 2011-2015 as well as from 2013-2015, except for

the high-ranked portfolio in period 2013-2015.. The factor adjusted returns are -39 and -47 basis

points per month or about -4.7% and -5.6% per year in the extended period. Again, the differ-

ence portfolios do not display significant returns.

Table 8 Multifactor Regression Results – 5th Percentile Portfolios

Grouped by Environmental Social Governance Performance

Period 2013-2015 Period 2011-2015

(1) (2) (3) (4) (5) (6)

Portfolio B5 W5 Difference B5 W5 Difference

Excess Return Market 0.9920*** 1.0078*** 0.0003 0.9771*** 1.0546*** 0.0003**

(0.0610) (0.0665) (0.0002) (0.0387) (0.0520) (0.0001)

Small-Minus-Big 0.0277 0.4032*** -0.0005* 0.0430 0.4465*** -0.0006***

(0.0798) (0.0871) (0.0002) (0.0617) (0.0831) (0.0002)

High-Minus-Low -0.0646 0.1239 -0.0003 -0.0935 0.2308* -0.0003

(0.1253) (0.1367) (0.0003) (0.0777) (0.1046) (0.0002)

Momentum Factor -0.0042 -0.1686* 0.0000 -0.0075 -0.1218 0.0000

(0.0755) (0.0824) (0.0002) (0.0461) (0.0621) (0.0001)

alpha -0.0032 -0.0056* -0.0000 -0.0039** -0.0047* -0.0000

(0.0021) (0.0023) (0.0000) (0.0013) (0.0018) (0.0000)

Adjusted R2 0.890 0.900 0.148 0.929 0.918 0.233

* p<0.05, ** p<0.01, *** p<0.001

6.2 Pillar-specific regressions

So far, the analysis always included all three pillars of ESG. To control for a potential dilution of

any of these pillars, I specify my investigation into the pillars environmental, social and govern-

ance. Governance has been omitted due to a lack in ratings.

Table 9 Multifactor Regression Results – 50th Percentile Portfolios

Grouped by Environmental Performance

Period 2013-2015 Period 2011-2015

(1) (2) (3) (4) (5) (6)

Portfolio B50 W50 Difference B50 W50 Difference

Excess Return Market 1.0551*** 0.9738*** 0.0814 1.0722*** 1.0253*** 0.0469

(0.0365) (0.0266) (0.0433) (0.0321) (0.0202) (0.0356)

Small-Minus-Big 0.2946*** 0.7572*** -0.4627*** 0.3009*** 0.7770*** -0.4760***

(0.0478) (0.0348) (0.0567) (0.0513) (0.0322) (0.0569)

High-Minus-Low -0.0379 0.1499** -0.1878* 0.0368 0.1699*** -0.1332

(0.0751) (0.0546) (0.0890) (0.0646) (0.0406) (0.0716)

Momentum Factor -0.0492 -0.0575 0.0083 -0.0588 -0.0498* -0.0090

(0.0453) (0.0329) (0.0536) (0.0383) (0.0241) (0.0425)

alpha -0.0056*** -0.0046*** -0.0010 -0.0054*** -0.0040*** -0.0014

(0.0012) (0.0009) (0.0015) (0.0011) (0.0007) (0.0012)

Adjusted R2 0.966 0.985 0.674 0.964 0.988 0.560

* p<0.05, ** p<0.01, *** p<0.001

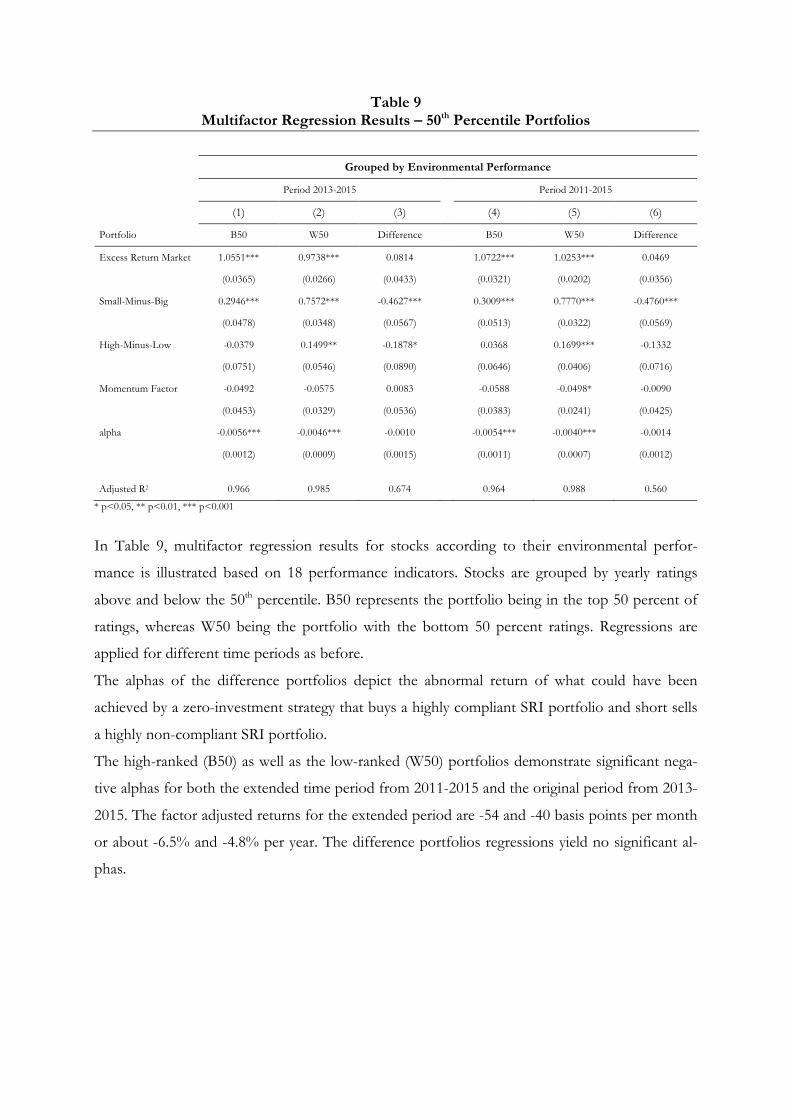

In Table 9, multifactor regression results for stocks according to their environmental perfor-

mance is illustrated based on 18 performance indicators. Stocks are grouped by yearly ratings

above and below the 50th percentile. B50 represents the portfolio being in the top 50 percent of

ratings, whereas W50 being the portfolio with the bottom 50 percent ratings. Regressions are

applied for different time periods as before.

The alphas of the difference portfolios depict the abnormal return of what could have been

achieved by a zero-investment strategy that buys a highly compliant SRI portfolio and short sells

a highly non-compliant SRI portfolio.

The high-ranked (B50) as well as the low-ranked (W50) portfolios demonstrate significant nega-

tive alphas for both the extended time period from 2011-2015 and the original period from 2013-

2015. The factor adjusted returns for the extended period are -54 and -40 basis points per month

or about -6.5% and -4.8% per year. The difference portfolios regressions yield no significant al-

phas.

Table 10 Multifactor Regression Results – 50th Percentile Portfolios

Grouped by Social Performance

Period 2013-2015 Period 2011-2015

(1) (2) (3) (4) (5) (6)

Portfolio B50 W50 Difference B50 W50 Difference

Excess Return Market 0.9394*** 1.0003*** -0.0609 0.9634*** 1.0440*** -0.0806*

(0.0436) (0.0267) (0.0491) (0.0312) (0.0210) (0.0356)

Small-Minus-Big 0.4805*** 0.7125*** -0.2320** 0.4638*** 0.7397*** -0.2759***

(0.0570) (0.0349) (0.0642) (0.0497) (0.0335) (0.0568)

High-Minus-Low -0.1307 0.1818** -0.3124** -0.1129 0.2264*** -0.3393***

(0.0895) (0.0548) (0.1008) (0.0626) (0.0422) (0.0715)

Momentum Factor 0.0407 -0.0934** 0.1341* 0.0006 -0.0743** 0.0749

(0.0540) (0.0330) (0.0608) (0.0372) (0.0251) (0.0425)

alpha -0.0037* -0.0054*** 0.0017 -0.0029* -0.0048*** 0.0019

(0.0015) (0.0009) (0.0017) (0.0011) (0.0007) (0.0012)

Adjusted R2 0.947 0.985 0.592 0.961 0.987 0.589

* p<0.05, ** p<0.01, *** p<0.001

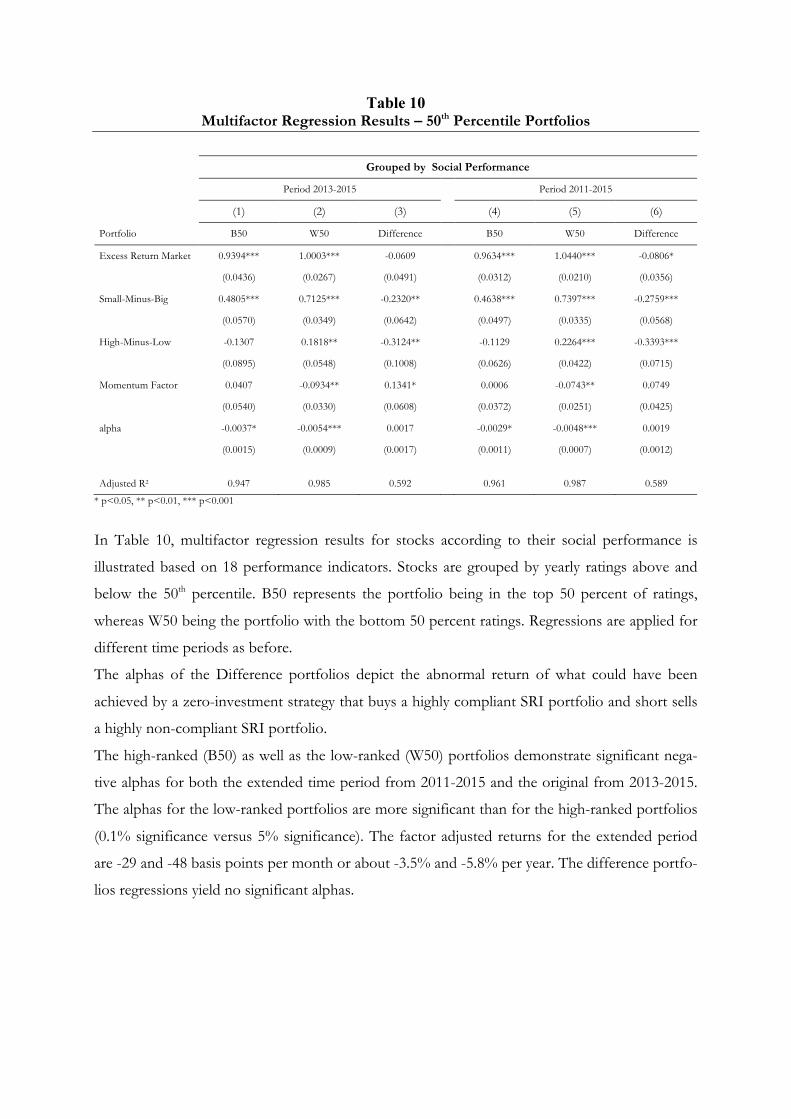

In Table 10, multifactor regression results for stocks according to their social performance is

illustrated based on 18 performance indicators. Stocks are grouped by yearly ratings above and

below the 50th percentile. B50 represents the portfolio being in the top 50 percent of ratings,

whereas W50 being the portfolio with the bottom 50 percent ratings. Regressions are applied for

different time periods as before.

The alphas of the Difference portfolios depict the abnormal return of what could have been

achieved by a zero-investment strategy that buys a highly compliant SRI portfolio and short sells

a highly non-compliant SRI portfolio.

The high-ranked (B50) as well as the low-ranked (W50) portfolios demonstrate significant nega-

tive alphas for both the extended time period from 2011-2015 and the original from 2013-2015.

The alphas for the low-ranked portfolios are more significant than for the high-ranked portfolios

(0.1% significance versus 5% significance). The factor adjusted returns for the extended period

are -29 and -48 basis points per month or about -3.5% and -5.8% per year. The difference portfo-

lios regressions yield no significant alphas.

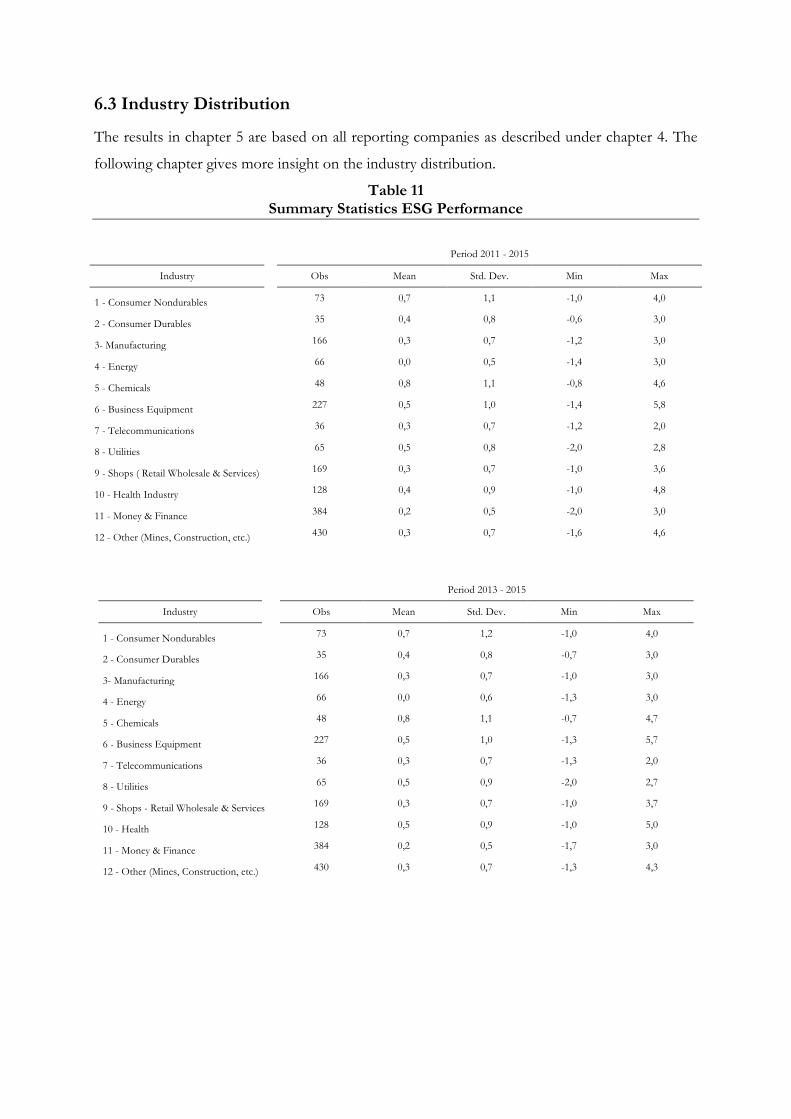

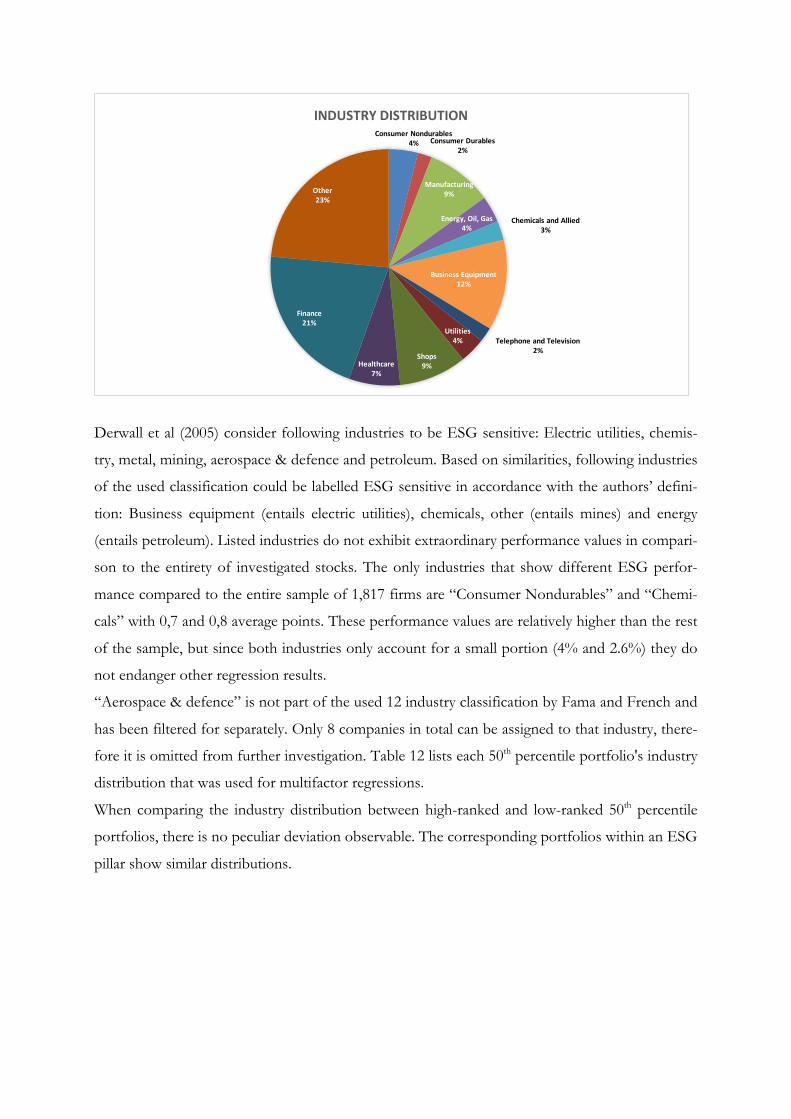

6.3 Industry Distribution

The results in chapter 5 are based on all reporting companies as described under chapter 4. The

following chapter gives more insight on the industry distribution.

Table 11 Summary Statistics ESG Performance

Period 2011 - 2015

Industry

Obs Mean Std. Dev. Min Max

1 - Consumer Nondurables

73 0,7 1,1 -1,0 4,0

2 - Consumer Durables

35 0,4 0,8 -0,6 3,0

3- Manufacturing

166 0,3 0,7 -1,2 3,0

4 - Energy

66 0,0 0,5 -1,4 3,0

5 - Chemicals

48 0,8 1,1 -0,8 4,6

6 - Business Equipment

227 0,5 1,0 -1,4 5,8

7 - Telecommunications

36 0,3 0,7 -1,2 2,0

8 - Utilities

65 0,5 0,8 -2,0 2,8

9 - Shops ( Retail Wholesale & Services) 169 0,3 0,7 -1,0 3,6

10 - Health Industry

128 0,4 0,9 -1,0 4,8

11 - Money & Finance

384 0,2 0,5 -2,0 3,0

12 - Other (Mines, Construction, etc.) 430 0,3 0,7 -1,6 4,6

Period 2013 - 2015

Industry

Obs Mean Std. Dev. Min Max

1 - Consumer Nondurables

73 0,7 1,2 -1,0 4,0

2 - Consumer Durables

35 0,4 0,8 -0,7 3,0

3- Manufacturing

166 0,3 0,7 -1,0 3,0

4 - Energy

66 0,0 0,6 -1,3 3,0

5 - Chemicals

48 0,8 1,1 -0,7 4,7

6 - Business Equipment

227 0,5 1,0 -1,3 5,7

7 - Telecommunications

36 0,3 0,7 -1,3 2,0

8 - Utilities

65 0,5 0,9 -2,0 2,7

9 - Shops - Retail Wholesale & Services 169 0,3 0,7 -1,0 3,7

10 - Health

128 0,5 0,9 -1,0 5,0

11 - Money & Finance

384 0,2 0,5 -1,7 3,0

12 - Other (Mines, Construction, etc.) 430 0,3 0,7 -1,3 4,3

Derwall et al (2005) consider following industries to be ESG sensitive: Electric utilities, chemis-

try, metal, mining, aerospace & defence and petroleum. Based on similarities, following industries

of the used classification could be labelled ESG sensitive in accordance with the authors’ defini-

tion: Business equipment (entails electric utilities), chemicals, other (entails mines) and energy

(entails petroleum). Listed industries do not exhibit extraordinary performance values in compari-

son to the entirety of investigated stocks. The only industries that show different ESG perfor-

mance compared to the entire sample of 1,817 firms are “Consumer Nondurables” and “Chemi-

cals” with 0,7 and 0,8 average points. These performance values are relatively higher than the rest

of the sample, but since both industries only account for a small portion (4% and 2.6%) they do

not endanger other regression results.

“Aerospace & defence” is not part of the used 12 industry classification by Fama and French and

has been filtered for separately. Only 8 companies in total can be assigned to that industry, there-

fore it is omitted from further investigation. Table 12 lists each 50th percentile portfolio's industry

distribution that was used for multifactor regressions.

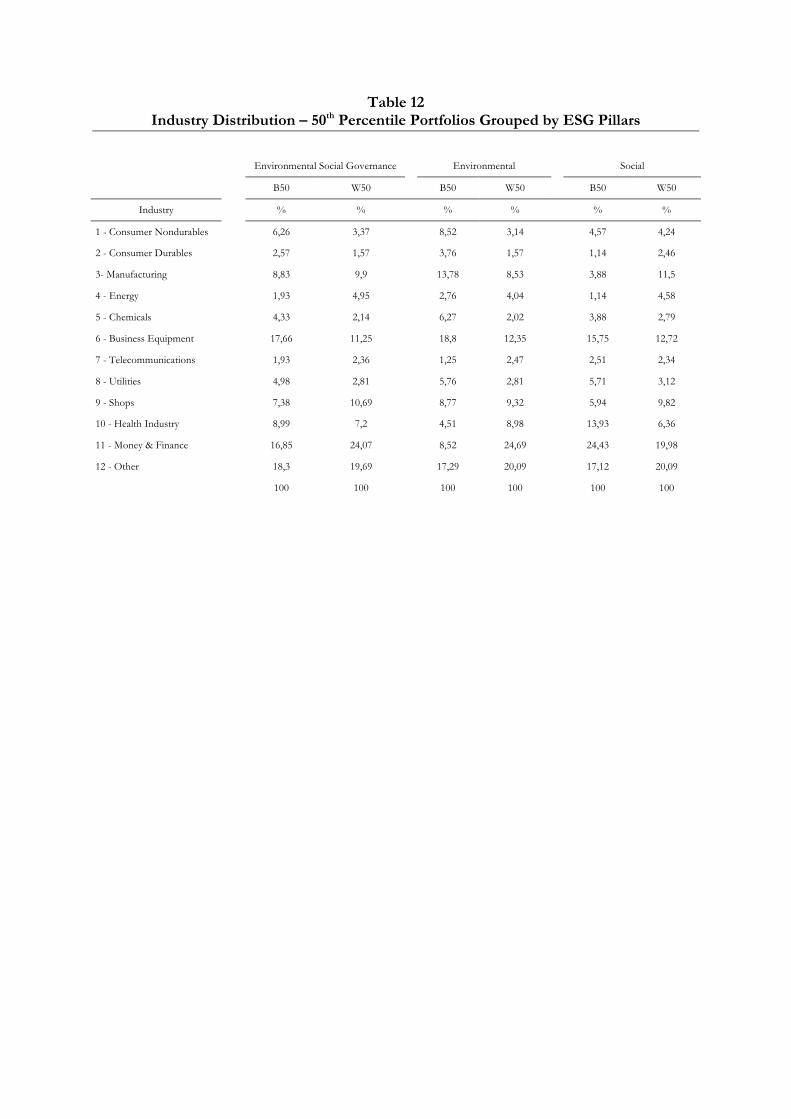

When comparing the industry distribution between high-ranked and low-ranked 50th percentile

portfolios, there is no peculiar deviation observable. The corresponding portfolios within an ESG

pillar show similar distributions.

ConsumerNondurables4% ConsumerDurables

2%

Manufacturing9%

Energy,Oil,Gas4%

ChemicalsandAllied3%

BusinessEquipment12%

TelephoneandTelevision2%

Utilities4%

Shops9%Healthcare

7%

Finance21%

Other23%

INDUSTRYDISTRIBUTION

Table 12 Industry Distribution – 50th Percentile Portfolios Grouped by ESG Pillars

Environmental Social Governance Environmental Social

B50 W50 B50 W50 B50 W50

Industry

% % % % % %

1 - Consumer Nondurables 6,26 3,37 8,52 3,14 4,57 4,24

2 - Consumer Durables

2,57 1,57 3,76 1,57 1,14 2,46

3- Manufacturing

8,83 9,9 13,78 8,53 3,88 11,5

4 - Energy

1,93 4,95 2,76 4,04 1,14 4,58

5 - Chemicals

4,33 2,14 6,27 2,02 3,88 2,79

6 - Business Equipment

17,66 11,25 18,8 12,35 15,75 12,72

7 - Telecommunications

1,93 2,36 1,25 2,47 2,51 2,34

8 - Utilities

4,98 2,81 5,76 2,81 5,71 3,12

9 - Shops 7,38 10,69 8,77 9,32 5,94 9,82

10 - Health Industry

8,99 7,2 4,51 8,98 13,93 6,36

11 - Money & Finance

16,85 24,07 8,52 24,69 24,43 19,98

12 - Other 18,3 19,69 17,29 20,09 17,12 20,09

100 100 100 100 100 100

7 Conclusion In the beginning, I positioned this thesis among related literature and pointed out the ongoing

discussion around the effectiveness of ESG investing. The two conflicting hypotheses of 1)

Shunned Stocks, namely socially controversial stocks showing positive returns due to negligence

and 2) Errors in Expectations, namely socially responsible stocks showing positive returns due to

a market inefficiency in recognizing CSR practices, were investigated by analysis of portfolio re-

turns of stocks with high ESG ratings and stocks with low ESG ratings.

Neither hypothesis 1, nor hypothesis 2 could be evidenced in the empirical analysis. With respect

to the first hypothesis, I found that socially controversial stocks show negative alphas. This

would indicate an argument in favor of ESG investing, whereas the empirical analysis also

showed negative alphas for socially responsible stocks and hereby declining hypothesis 2 as well.

Refining these results by smaller percentiles and separating environmental and social characteris-

tics leads to similar results.

These results add to the line of ambiguous research results on ESG investing, but can be inter-

preted as an indication of efficient markets. In fact, neither the controversial, nor the responsible

stocks can generate extra returns. I suggest that only a well-balanced market portfolio delivers the

best risk adjusted returns.

Finally, this thesis also leaves room for further investigation. A continued difficulty throughout

the analysis was the poor availability of data on ESG compliance. Since MSCI ESG Research

updated their key issue hierarchy in recent years, it resembles a rather new innovation and there-

fore misses a longer trace of historical data. As the future will probably bring an increased availa-

bility of data and more refined indicators, this research could be redone on an increased data set.