the economic outlook and monetary policy · the path of this recovery has been below past deep...

TRANSCRIPT

The Economic Outlook and Monetary Policy

May 24, 2016Rosemont, IL

David OppedahlSenior Business [email protected]

The path of this recovery has been below past deep recession recovery cycles

average annualized growth: 2.4%

average annualized growth: 5.3%

average annualized growth: 5.4%

95

100

105

110

115

120

125

130

135

140

95

100

105

110

115

120

125

130

135

140

-8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18 20 22 24 26

Business cycle recovery pathindex - business cycle trough = 100

1981-82

2008-09

1974-75

quarters before trough quarters after trough

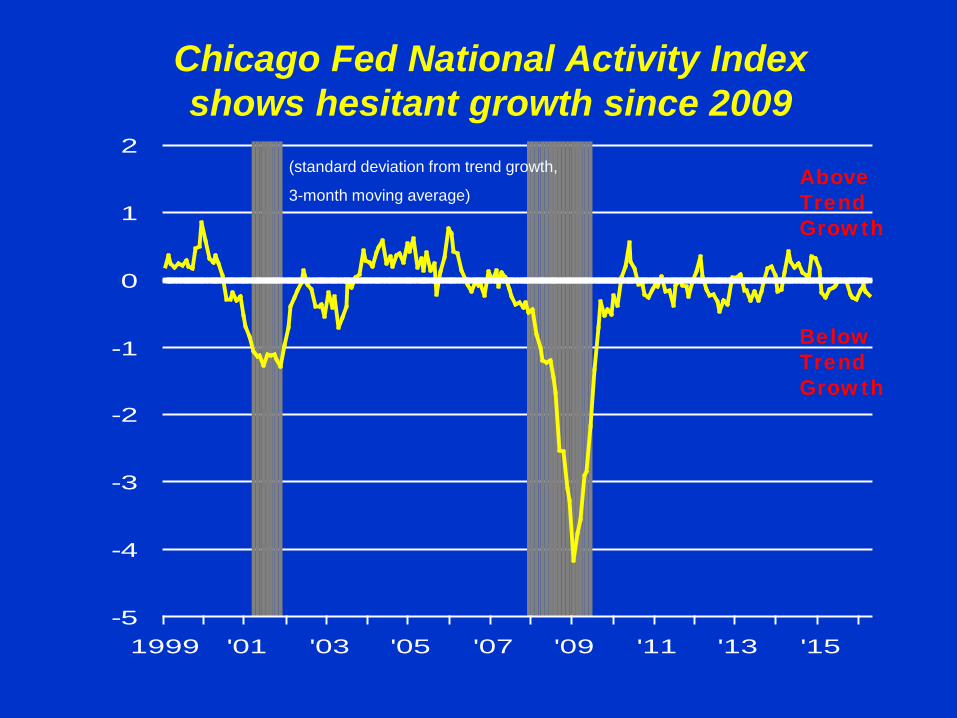

Chicago Fed National Activity Indexshows hesitant growth since 2009

-5

-4

-3

-2

-1

0

1

2

1999 '01 '03 '05 '07 '09 '11 '13 '15

AboveTrendGrowth

BelowTrendGrowth

(standard deviation from trend growth,

3-month moving average)

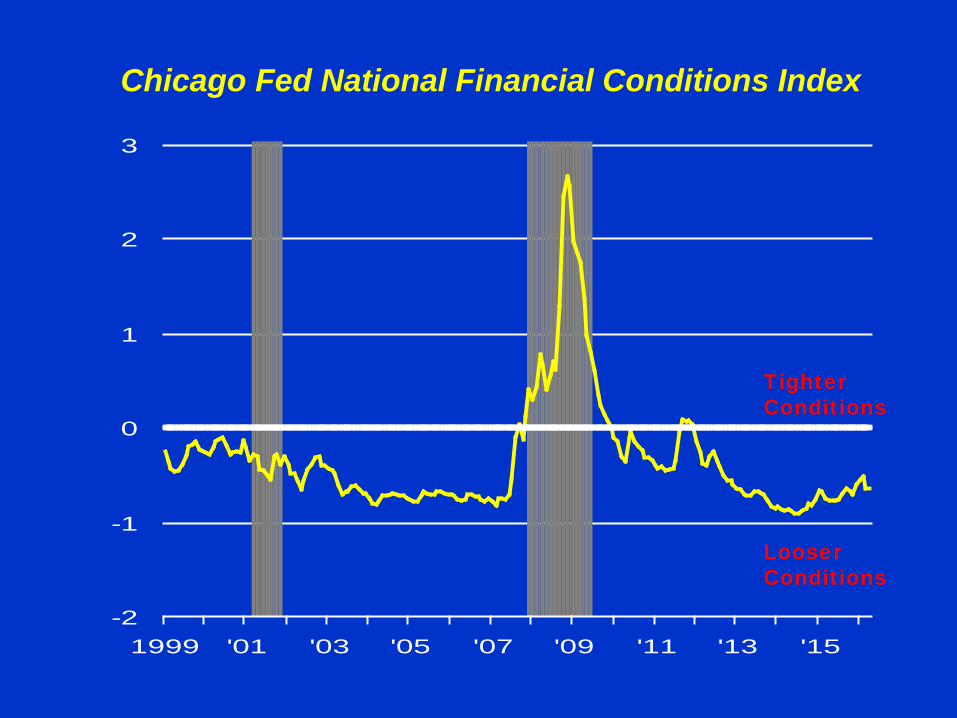

Chicago Fed National Financial Conditions Index

-2

-1

0

1

2

3

1999 '01 '03 '05 '07 '09 '11 '13 '15

TighterConditions

LooserConditions

In December 2015, the FOMC raised the Fed Funds rate target to a range from 0.25% to 0.50%

0

1

2

3

4

5

6

7

1999 '01 '03 '05 '07 '09 '11 '13 '15

Federal Funds Rate (effective),

Yields in percent per annum

Quantitative easing was necessary

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Assets of the Federal ReserveBi l lions of dollars

Term Auction Credit

Securities Held Outright

Central Bank Swaps

Maiden Lane II & III

Commercial Paper Facility

2007 2008 2009

Term Asset-Backed SecuritiesLoan Facility

AIG Support

Maiden Lane

2010 2011 2012 2013 2014 2015

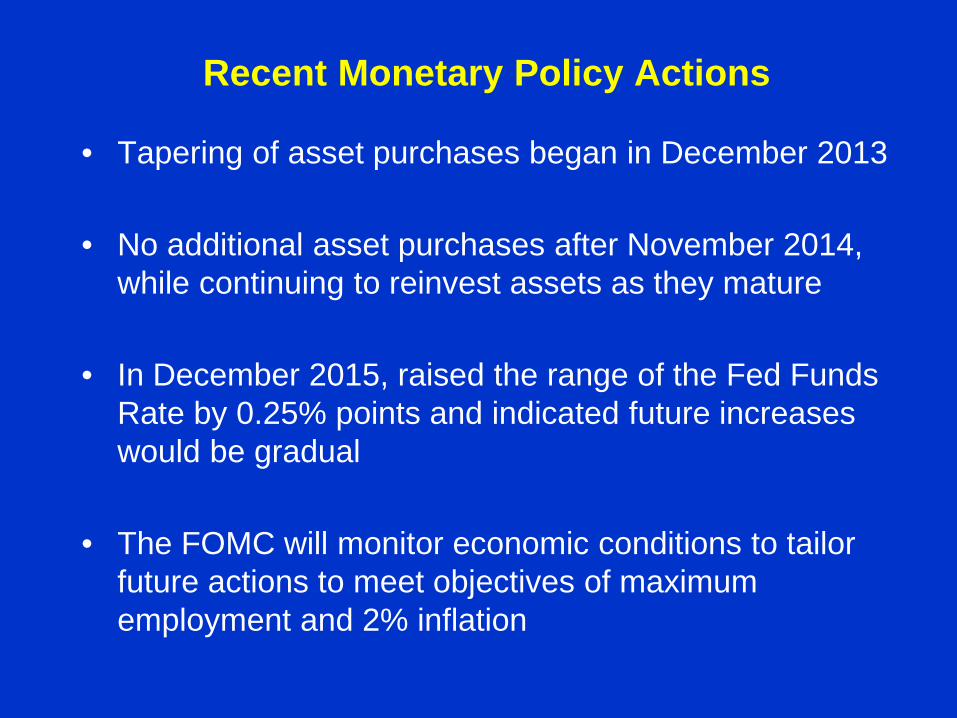

Recent Monetary Policy Actions

• Tapering of asset purchases began in December 2013

• No additional asset purchases after November 2014, while continuing to reinvest assets as they mature

• In December 2015, raised the range of the Fed Funds Rate by 0.25% points and indicated future increases would be gradual

• The FOMC will monitor economic conditions to tailor future actions to meet objectives of maximum employment and 2% inflation

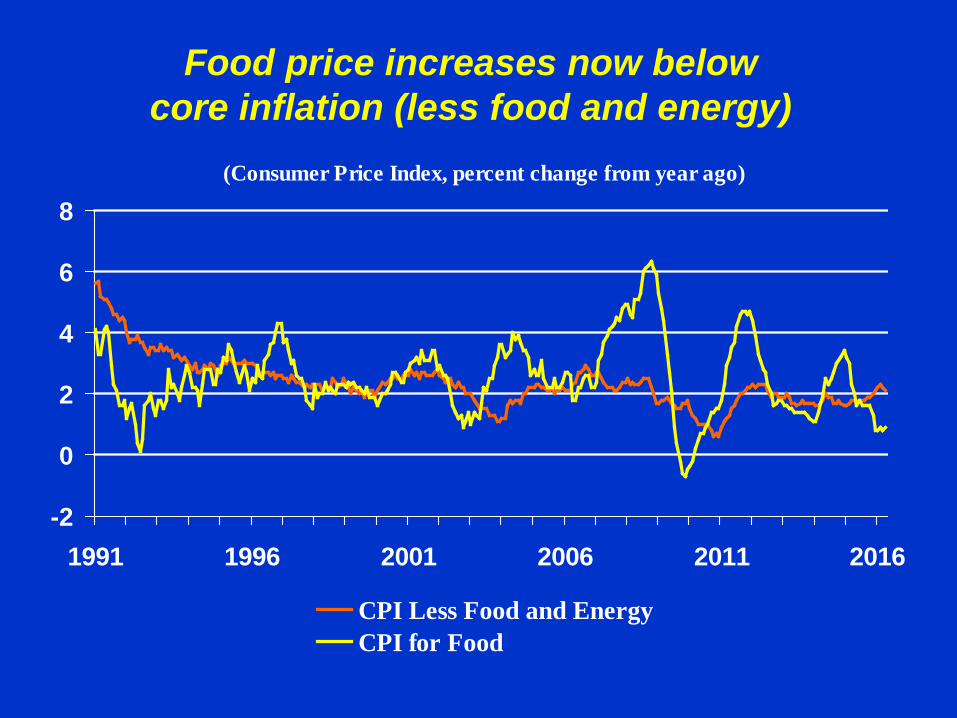

Food price increases now belowcore inflation (less food and energy)

(Consumer Price Index, percent change from year ago)

-2

0

2

4

6

8

1991 1996 2001 2006 2011 2016

CPI Less Food and EnergyCPI for Food

Oil prices plummeted and lowergas prices boosted consumer saving/spending

(2010 $/barrel)

0

50

100

150

1971 1976 1981 1986 1991 1996 2001 2006 2011 2016

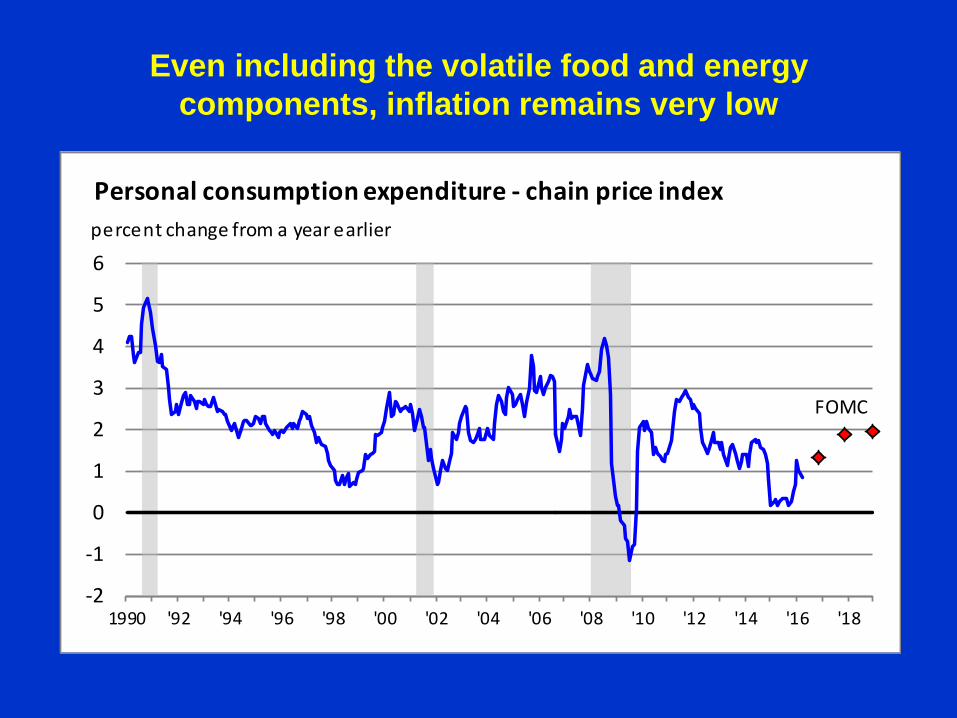

Even including the volatile food and energy components, inflation remains very low

-2

-1

0

1

2

3

4

5

6

1990 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18

Personal consumption expenditure - chain price indexpercent change from a year earlier

FOMC

Employment grew by nearly 2.7 million jobsover the past year

-8

-6

-4

-2

0

2

4

6

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Total employmentpercent

Monthly change (saar)

Percent change from a year earlier

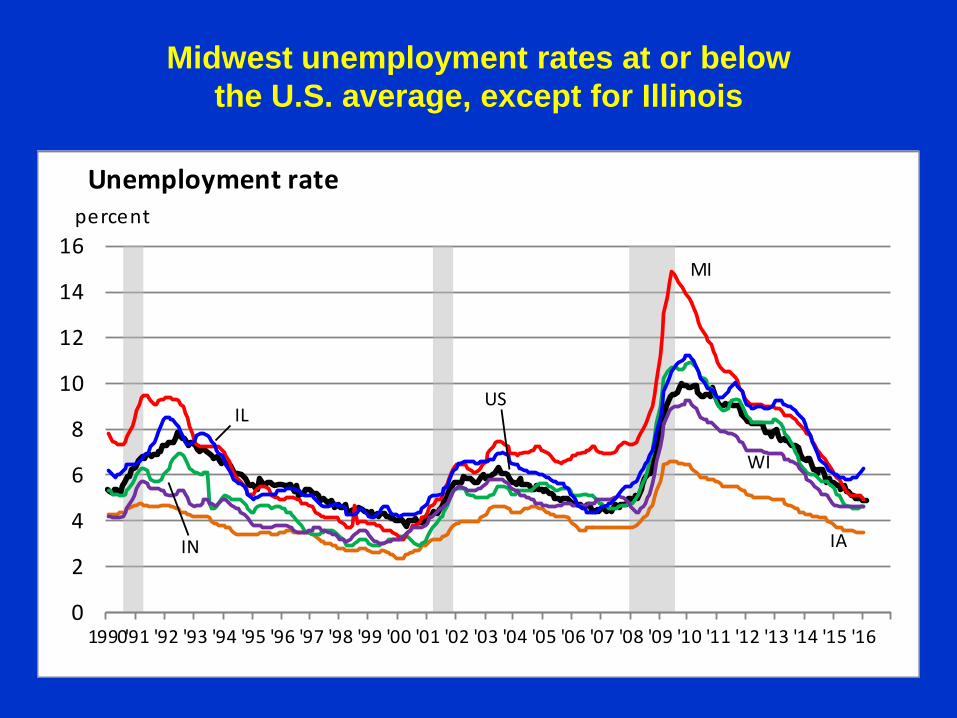

Midwest unemployment rates at or belowthe U.S. average, except for Illinois

0

2

4

6

8

10

12

14

16

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

MI

Unemployment ratepercent

USIL

IN IA

WI

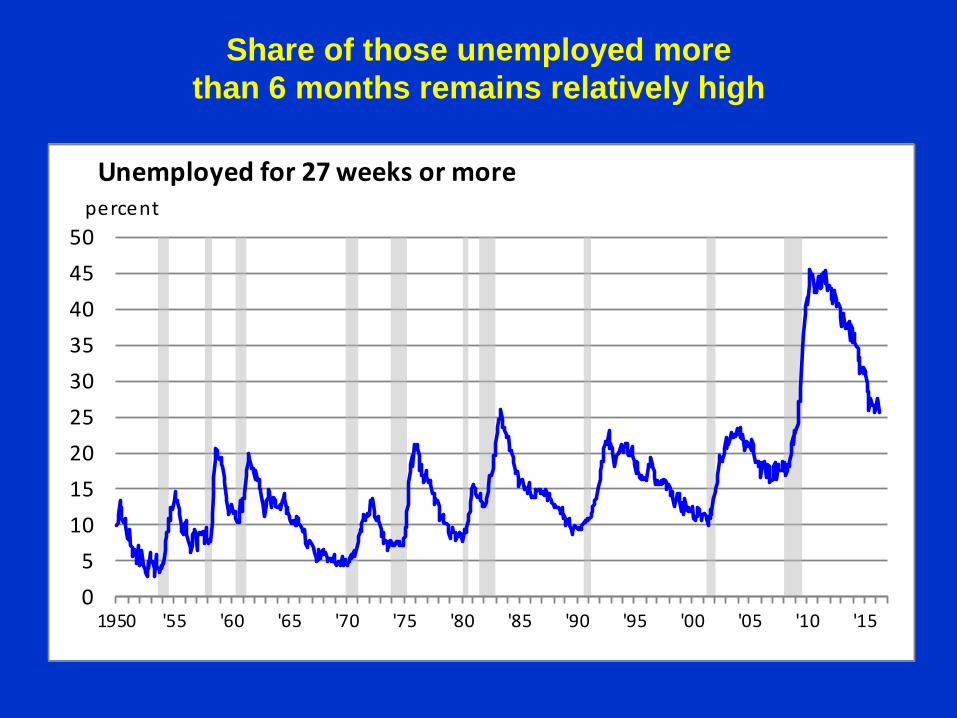

Share of those unemployed morethan 6 months remains relatively high

05

101520253035404550

1950 '55 '60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '10 '15

Unemployed for 27 weeks or morepercent

Before edging up, the labor force participationrate fell to a level last seen in 1977

5859606162636465666768

1950 '55 '60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '10 '15

Labor force participation ratepercent

Wages and benefit cost increases remain weak

0

1

2

3

4

5

6

7

8

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Employment cost indexpercent change from year ago

benefit costs

wages and salaries

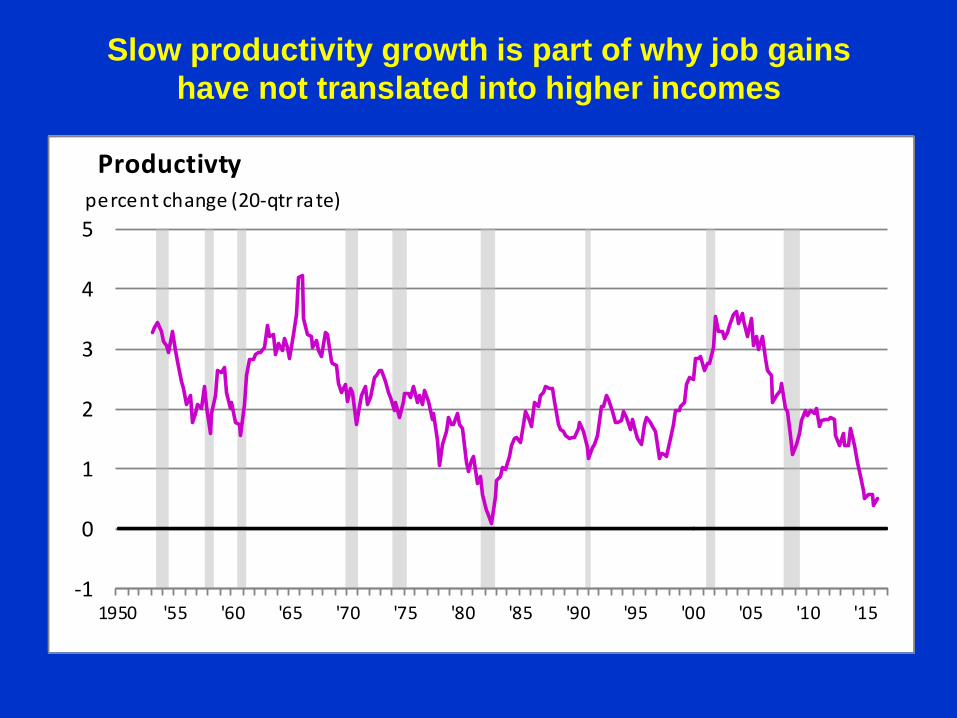

Slow productivity growth is part of why job gainshave not translated into higher incomes

-1

0

1

2

3

4

5

1950 '55 '60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '10 '15

Productivtypercent change (20-qtr rate)

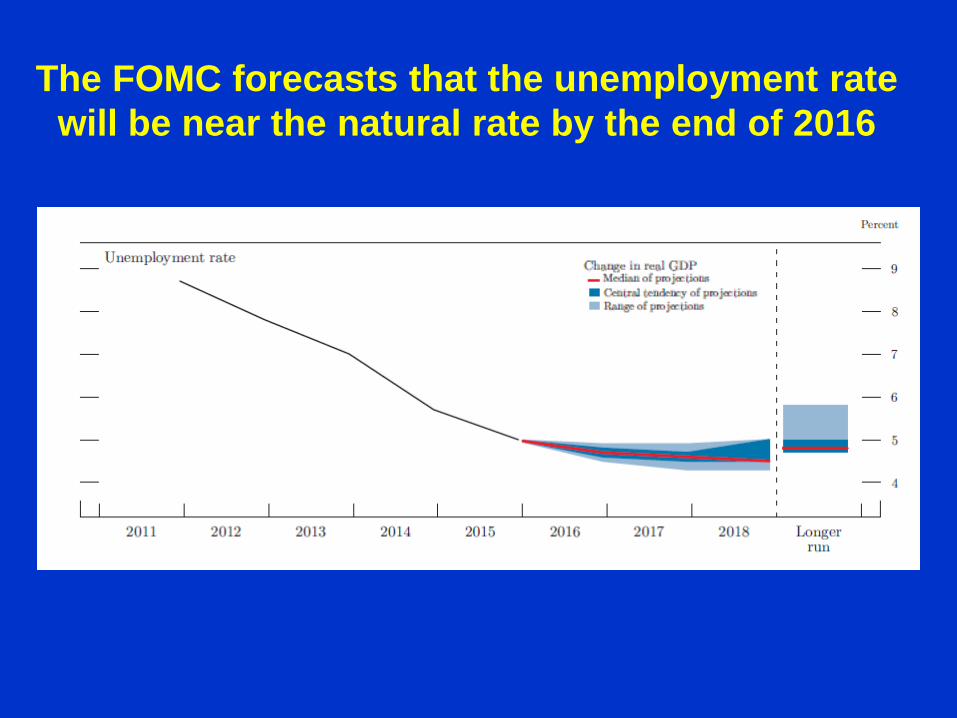

The FOMC forecasts that the unemployment ratewill be near the natural rate by the end of 2016

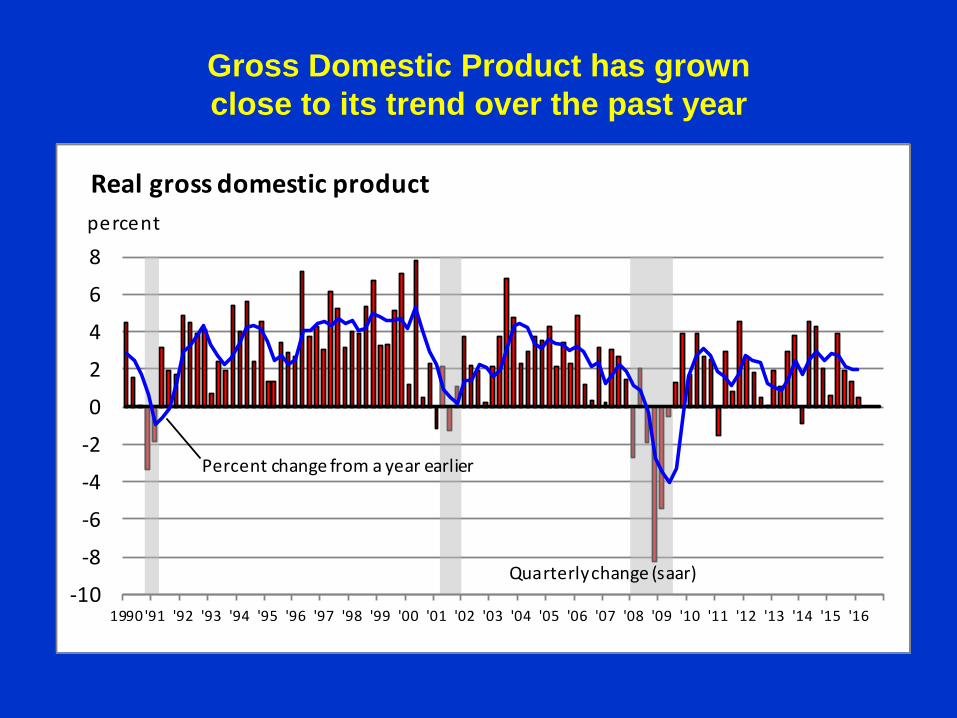

Gross Domestic Product has grownclose to its trend over the past year

-10

-8

-6

-4

-2

0

2

4

6

8

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Real gross domestic productpercent

Quarterly change (saar)

Percent change from a year earlier

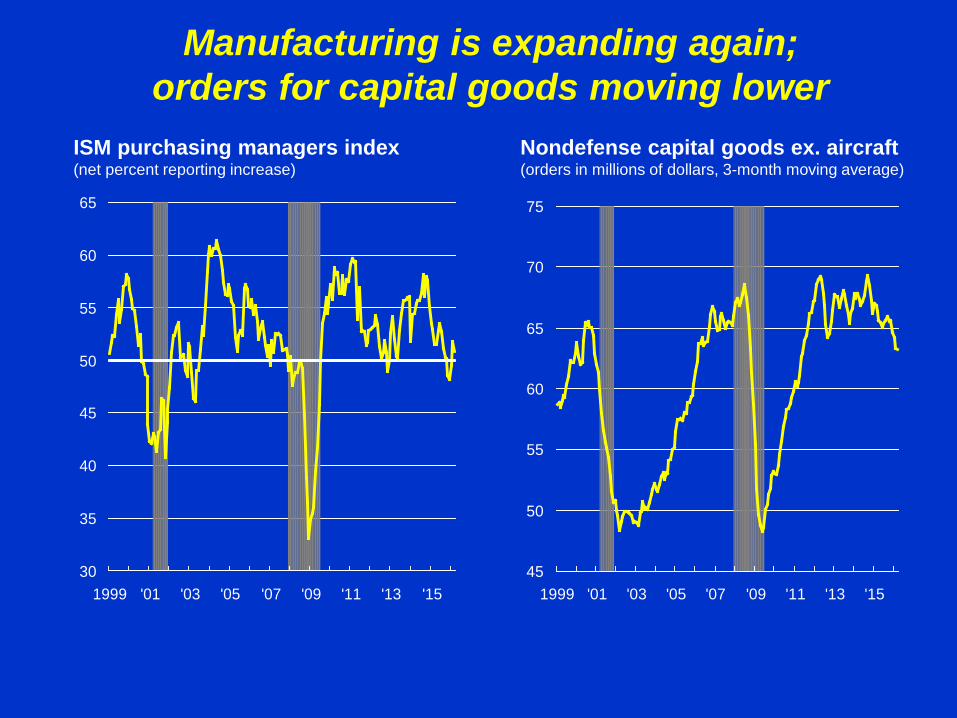

Manufacturing is expanding again;orders for capital goods moving lower

Nondefense capital goods ex. aircraft (orders in millions of dollars, 3-month moving average)

45

50

55

60

65

70

75

1999 '01 '03 '05 '07 '09 '11 '13 '1530

35

40

45

50

55

60

65

1999 '01 '03 '05 '07 '09 '11 '13 '15

ISM purchasing managers index(net percent reporting increase)

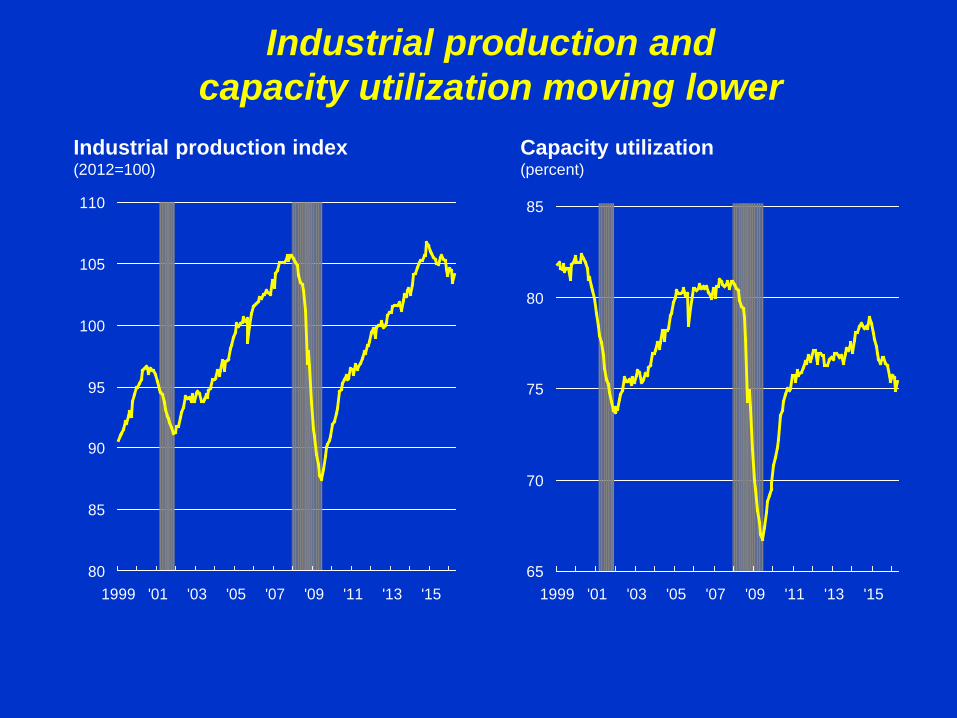

Industrial production andcapacity utilization moving lower

Capacity utilization (percent)

65

70

75

80

85

1999 '01 '03 '05 '07 '09 '11 '13 '1580

85

90

95

100

105

110

1999 '01 '03 '05 '07 '09 '11 '13 '15

Industrial production index(2012=100)

A broad-based recovery with vehicles, computers, primary metals, and machinery leading the way

-50 -25 0 25 50 75 100 125 150 175

ManufacturingDurable Goods

Wood ProductsNonmetallic Mineral Products

Primary MetalsFabricated Metal Products

MachineryComputer and Electronic Components

Electrical Eqpt, Appliances & ComponentsMotor Vehicles and Parts

Aerospace & Miscellaneous Transport EquipFurniture and Related Products

Miscellaneous Durable GoodsNondurable Manufacturing

Food, Beverages, and TobaccoTextile and Product Mills

Apparel and Leather GoodsPaper

Printing and Related Support ActivitiesChemicals

Petroleum and Coal ProductsPlastics and Rubber Products

Other Manufacturing

Industrial output: June 2009 - April 2016percent change

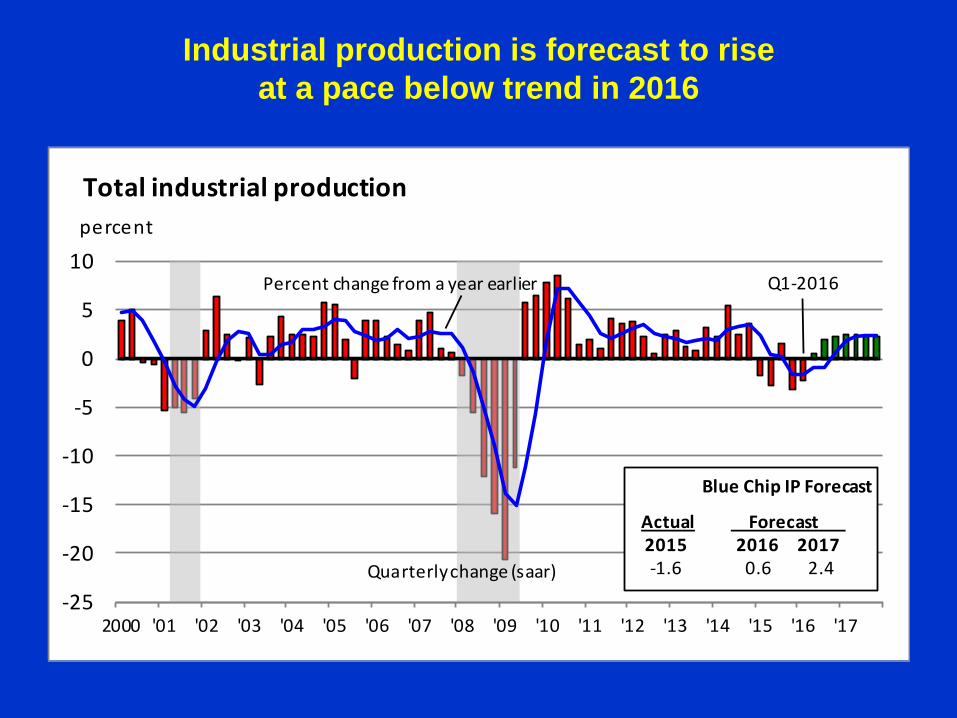

Industrial production is forecast to riseat a pace below trend in 2016

-25

-20

-15

-10

-5

0

5

10

2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

Total industrial productionpercent

Quarterly change (saar)

Percent change from a year earlier Q1-2016

Blue Chip IP Forecast

Actual Forecast 2015 2016 2017-1.6 0.6 2.4

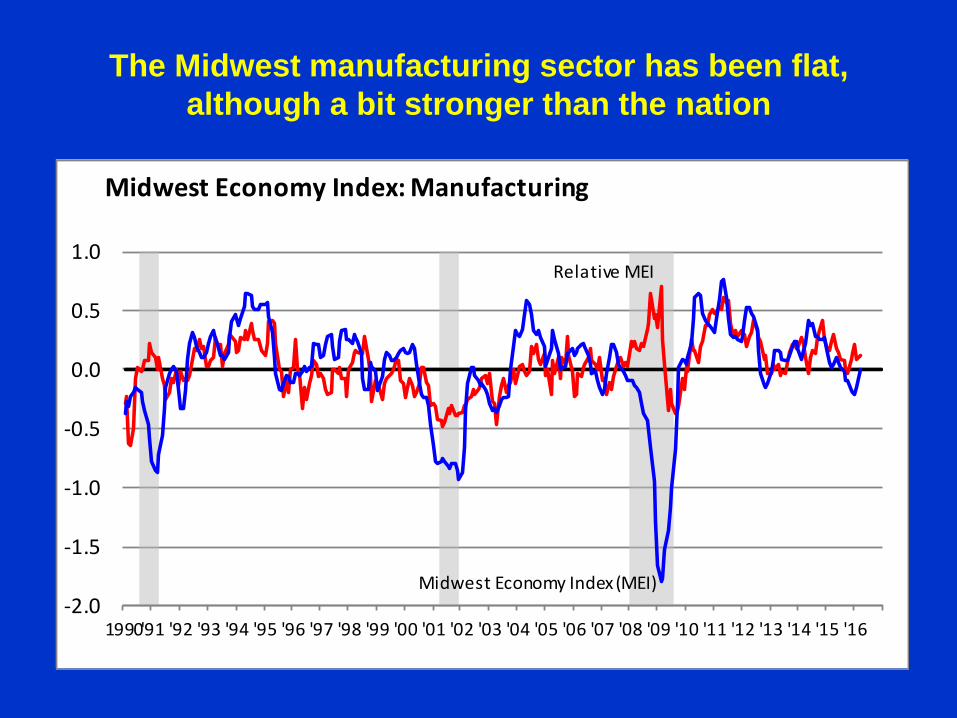

The Midwest manufacturing sector has been flat,although a bit stronger than the nation

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1990'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Midwest Economy Index (MEI)

Midwest Economy Index: Manufacturing

Relative MEI

Housing market tanked and moving up from bottom

Housing starts (millions of units, 3-month moving average, SAAR)

0.5

1.0

1.5

2.0

2.5

1999 '01 '03 '05 '07 '09 '11 '13 '153

4

5

6

7

8

9

1999 '01 '03 '05 '07 '09 '11 '13 '15

Home mortgage rate(percent, effective rate for all loans closed)

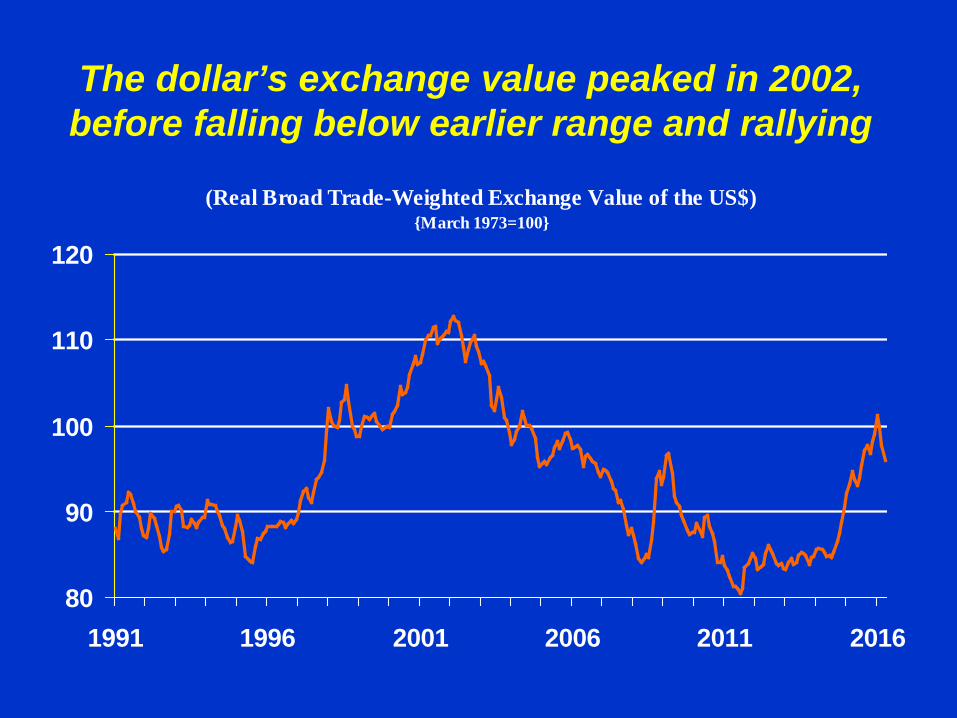

The dollar’s exchange value peaked in 2002, before falling below earlier range and rallying

(Real Broad Trade-Weighted Exchange Value of the US$){March 1973=100}

80

90

100

110

120

1991 1996 2001 2006 2011 2016

U.S. exports and imports decreased in 2015

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1992 1995 1998 2001 2004 2007 2010 2013

trill

ion

$ Exports

Imports

The Federal Funds Rate is anticipated to remainbelow the neutral rate through the end of 2018

The FOMC expects GDP to grow nearits trend through 2018 and in the longer run

•The outlook is for the U.S. economy to expand at apace around trend through 2018

Summary

•Employment is expected to rise moderately with theunemployment rate edging lower

•Remaining slack in the economy keeps the inflation raterelatively low, rising toward 2%

•Growth in manufacturing output should resume•Housing turned the corner, but still has far to go•Net exports remain a wild card given world conditions

www.chicagofed.org