the economic effects of territorial taxation, with remarks by jason

TRANSCRIPT

The economic effects of

territorial taxation, with remarks by Jason Furman

March 31, 2014

Please take this time to silence any mobile devices.

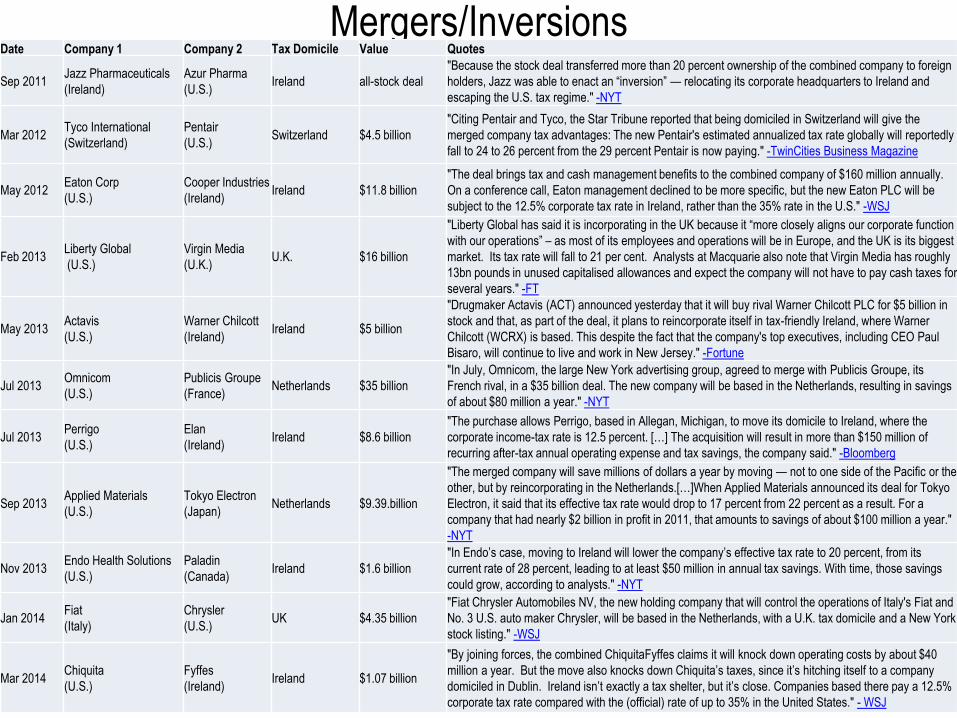

Mergers/Inversions Date Company 1 Company 2 Tax Domicile Value Quotes

Sep 2011 Jazz Pharmaceuticals

(Ireland)

Azur Pharma

(U.S.) Ireland all-stock deal

"Because the stock deal transferred more than 20 percent ownership of the combined company to foreign

holders, Jazz was able to enact an “inversion” — relocating its corporate headquarters to Ireland and

escaping the U.S. tax regime." -NYT

Mar 2012 Tyco International

(Switzerland)

Pentair

(U.S.) Switzerland $4.5 billion

"Citing Pentair and Tyco, the Star Tribune reported that being domiciled in Switzerland will give the

merged company tax advantages: The new Pentair's estimated annualized tax rate globally will reportedly

fall to 24 to 26 percent from the 29 percent Pentair is now paying." -TwinCities Business Magazine

May 2012 Eaton Corp

(U.S.)

Cooper Industries

(Ireland) Ireland $11.8 billion

"The deal brings tax and cash management benefits to the combined company of $160 million annually.

On a conference call, Eaton management declined to be more specific, but the new Eaton PLC will be

subject to the 12.5% corporate tax rate in Ireland, rather than the 35% rate in the U.S." -WSJ

Feb 2013 Liberty Global

(U.S.)

Virgin Media

(U.K.) U.K. $16 billion

"Liberty Global has said it is incorporating in the UK because it “more closely aligns our corporate function

with our operations” – as most of its employees and operations will be in Europe, and the UK is its biggest

market. Its tax rate will fall to 21 per cent. Analysts at Macquarie also note that Virgin Media has roughly

13bn pounds in unused capitalised allowances and expect the company will not have to pay cash taxes for

several years." -FT

May 2013 Actavis

(U.S.)

Warner Chilcott

(Ireland) Ireland $5 billion

"Drugmaker Actavis (ACT) announced yesterday that it will buy rival Warner Chilcott PLC for $5 billion in

stock and that, as part of the deal, it plans to reincorporate itself in tax-friendly Ireland, where Warner

Chilcott (WCRX) is based. This despite the fact that the company's top executives, including CEO Paul

Bisaro, will continue to live and work in New Jersey." -Fortune

Jul 2013 Omnicom

(U.S.)

Publicis Groupe

(France) Netherlands $35 billion

"In July, Omnicom, the large New York advertising group, agreed to merge with Publicis Groupe, its

French rival, in a $35 billion deal. The new company will be based in the Netherlands, resulting in savings

of about $80 million a year." -NYT

Jul 2013 Perrigo

(U.S.)

Elan

(Ireland) Ireland $8.6 billion

"The purchase allows Perrigo, based in Allegan, Michigan, to move its domicile to Ireland, where the

corporate income-tax rate is 12.5 percent. […] The acquisition will result in more than $150 million of

recurring after-tax annual operating expense and tax savings, the company said." -Bloomberg

Sep 2013 Applied Materials

(U.S.)

Tokyo Electron

(Japan) Netherlands $9.39.billion

"The merged company will save millions of dollars a year by moving — not to one side of the Pacific or the

other, but by reincorporating in the Netherlands.[…]When Applied Materials announced its deal for Tokyo

Electron, it said that its effective tax rate would drop to 17 percent from 22 percent as a result. For a

company that had nearly $2 billion in profit in 2011, that amounts to savings of about $100 million a year."

-NYT

Nov 2013 Endo Health Solutions

(U.S.)

Paladin

(Canada) Ireland $1.6 billion

"In Endo’s case, moving to Ireland will lower the company’s effective tax rate to 20 percent, from its

current rate of 28 percent, leading to at least $50 million in annual tax savings. With time, those savings

could grow, according to analysts." -NYT

Jan 2014 Fiat

(Italy)

Chrysler

(U.S.) UK $4.35 billion

"Fiat Chrysler Automobiles NV, the new holding company that will control the operations of Italy's Fiat and

No. 3 U.S. auto maker Chrysler, will be based in the Netherlands, with a U.K. tax domicile and a New York

stock listing." -WSJ

Mar 2014 Chiquita

(U.S.)

Fyffes

(Ireland) Ireland $1.07 billion

"By joining forces, the combined ChiquitaFyffes claims it will knock down operating costs by about $40

million a year. But the move also knocks down Chiquita’s taxes, since it’s hitching itself to a company

domiciled in Dublin. Ireland isn’t exactly a tax shelter, but it’s close. Companies based there pay a 12.5%

corporate tax rate compared with the (official) rate of up to 35% in the United States." - WSJ

The economic effects of

territorial taxation, with remarks by Jason Furman

March 31, 2014

Please take this time to silence any mobile devices.

Beijing

Boston

Brussels

Chicago

Frankfurt

Hong Kong

Houston

London

Los Angeles

Moscow

Munich

New York

Palo Alto

Paris

São Paulo

Shanghai

Singapore

Sydney

Tokyo

Toronto

Vienna

Washington, D.C.

Wilmington

Current Trends and Issues in Redomiciliation Transactions

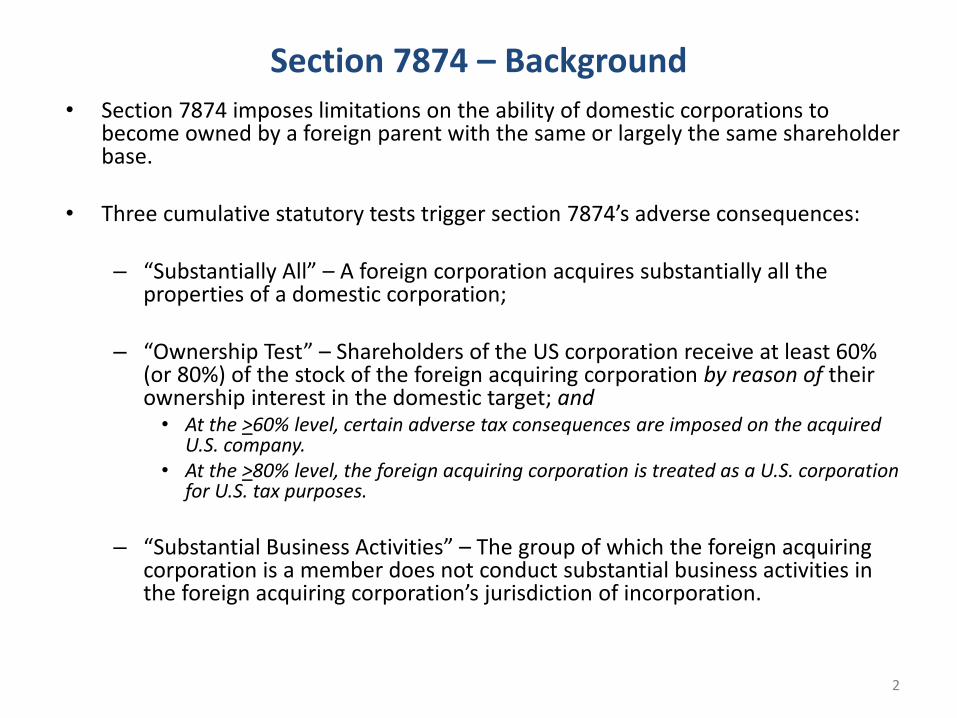

Section 7874 – Background • Section 7874 imposes limitations on the ability of domestic corporations to

become owned by a foreign parent with the same or largely the same shareholder base.

• Three cumulative statutory tests trigger section 7874’s adverse consequences: – “Substantially All” – A foreign corporation acquires substantially all the

properties of a domestic corporation;

– “Ownership Test” – Shareholders of the US corporation receive at least 60% (or 80%) of the stock of the foreign acquiring corporation by reason of their ownership interest in the domestic target; and • At the >60% level, certain adverse tax consequences are imposed on the acquired

U.S. company. • At the >80% level, the foreign acquiring corporation is treated as a U.S. corporation

for U.S. tax purposes.

– “Substantial Business Activities” – The group of which the foreign acquiring

corporation is a member does not conduct substantial business activities in the foreign acquiring corporation’s jurisdiction of incorporation.

2

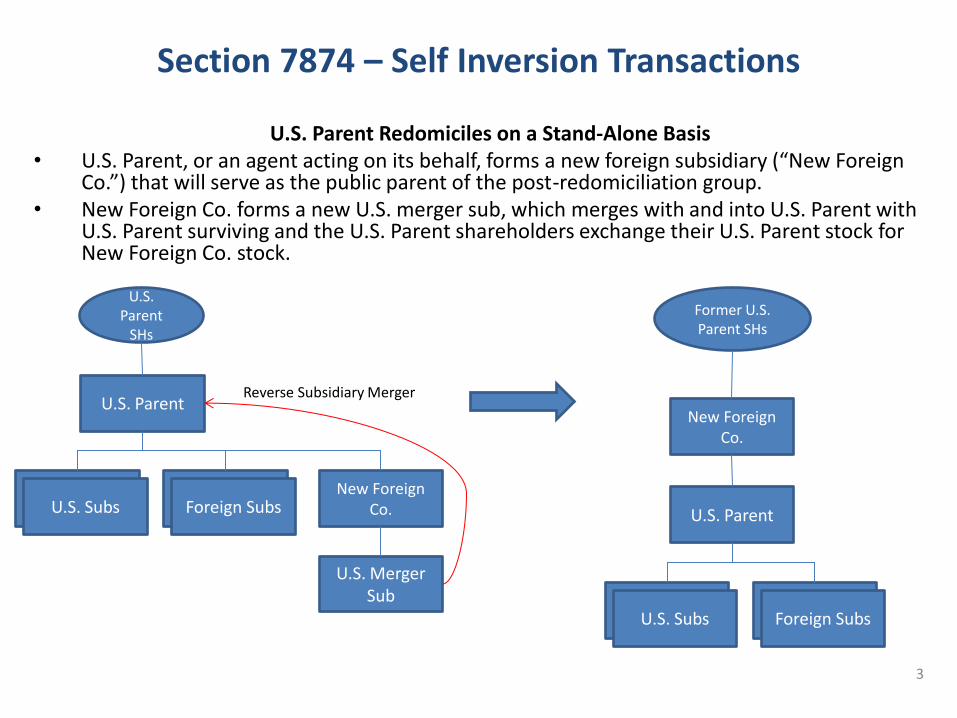

Section 7874 – Self Inversion Transactions

U.S. Parent Redomiciles on a Stand-Alone Basis • U.S. Parent, or an agent acting on its behalf, forms a new foreign subsidiary (“New Foreign

Co.”) that will serve as the public parent of the post-redomiciliation group. • New Foreign Co. forms a new U.S. merger sub, which merges with and into U.S. Parent with

U.S. Parent surviving and the U.S. Parent shareholders exchange their U.S. Parent stock for New Foreign Co. stock.

3

New Foreign Co.

U.S. Parent

U.S. Parent

SHs

New Foreign Co.

Former U.S. Parent SHs

U.S. Subs Foreign Subs

U.S. Merger Sub

Reverse Subsidiary Merger

U.S. Parent

U.S. Subs Foreign Subs

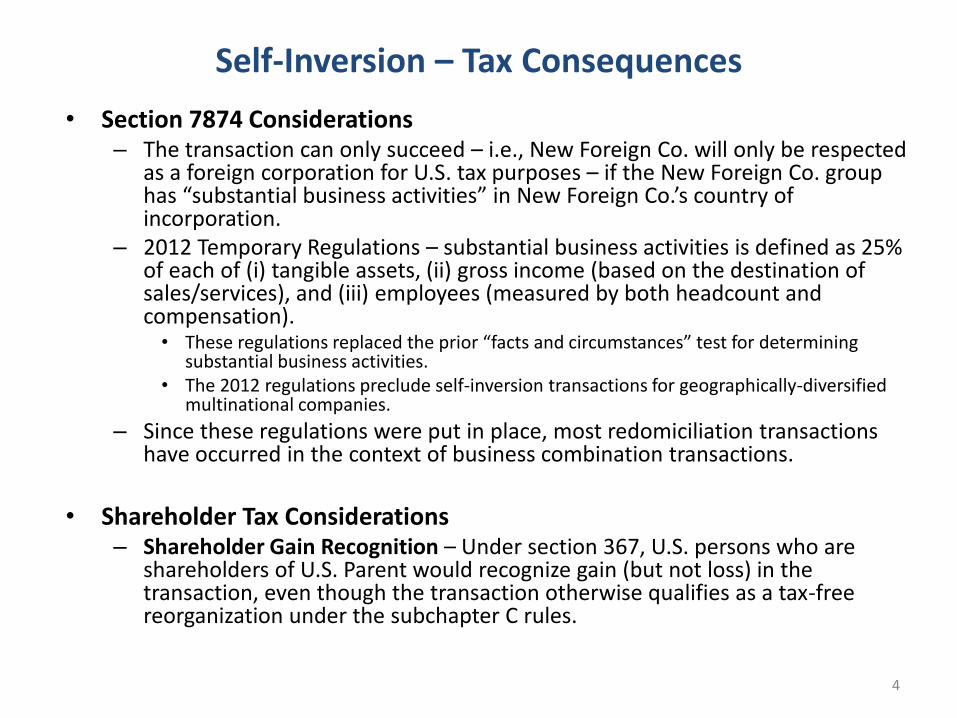

Self-Inversion – Tax Consequences

• Section 7874 Considerations – The transaction can only succeed – i.e., New Foreign Co. will only be respected

as a foreign corporation for U.S. tax purposes – if the New Foreign Co. group has “substantial business activities” in New Foreign Co.’s country of incorporation.

– 2012 Temporary Regulations – substantial business activities is defined as 25% of each of (i) tangible assets, (ii) gross income (based on the destination of sales/services), and (iii) employees (measured by both headcount and compensation). • These regulations replaced the prior “facts and circumstances” test for determining

substantial business activities. • The 2012 regulations preclude self-inversion transactions for geographically-diversified

multinational companies.

– Since these regulations were put in place, most redomiciliation transactions have occurred in the context of business combination transactions.

• Shareholder Tax Considerations

– Shareholder Gain Recognition – Under section 367, U.S. persons who are shareholders of U.S. Parent would recognize gain (but not loss) in the transaction, even though the transaction otherwise qualifies as a tax-free reorganization under the subchapter C rules.

4

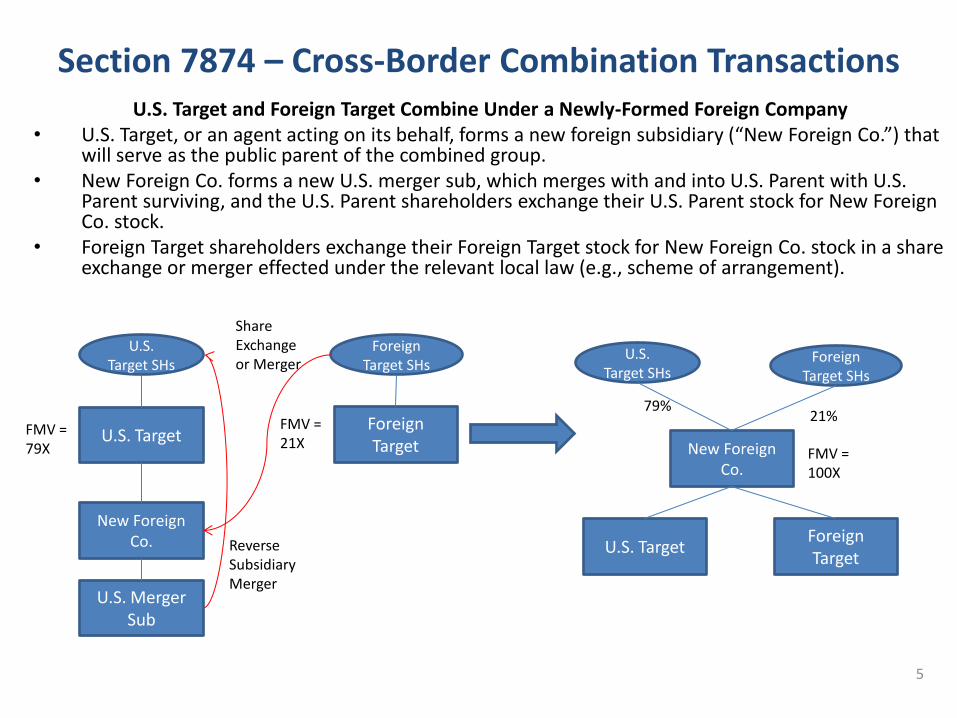

Section 7874 – Cross-Border Combination Transactions U.S. Target and Foreign Target Combine Under a Newly-Formed Foreign Company

• U.S. Target, or an agent acting on its behalf, forms a new foreign subsidiary (“New Foreign Co.”) that will serve as the public parent of the combined group.

• New Foreign Co. forms a new U.S. merger sub, which merges with and into U.S. Parent with U.S. Parent surviving, and the U.S. Parent shareholders exchange their U.S. Parent stock for New Foreign Co. stock.

• Foreign Target shareholders exchange their Foreign Target stock for New Foreign Co. stock in a share exchange or merger effected under the relevant local law (e.g., scheme of arrangement).

5

New Foreign Co.

U.S. Target

U.S. Target SHs

FMV = 79X

Foreign Target SHs

21X Cash

New Foreign Co.

U.S. Target SHs

Foreign Target SHs

FMV = 100X

79% 21%

U.S. Target

Foreign Target

FMV = 21X

Foreign Target

U.S. Merger Sub

Reverse Subsidiary Merger

Share Exchange or Merger

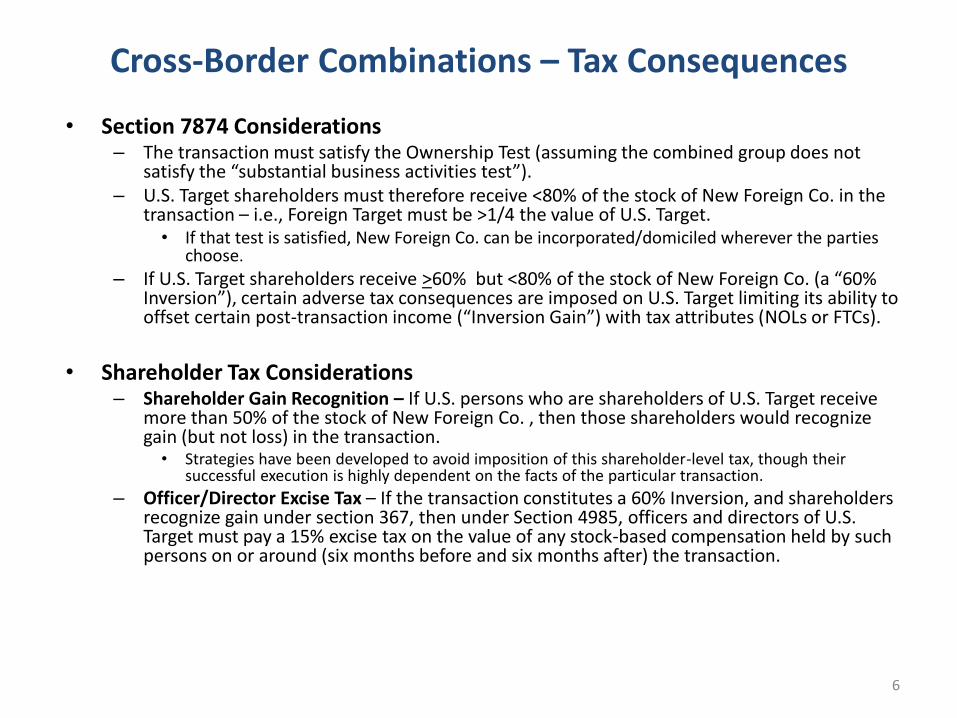

Cross-Border Combinations – Tax Consequences

• Section 7874 Considerations – The transaction must satisfy the Ownership Test (assuming the combined group does not

satisfy the “substantial business activities test”). – U.S. Target shareholders must therefore receive <80% of the stock of New Foreign Co. in the

transaction – i.e., Foreign Target must be >1/4 the value of U.S. Target. • If that test is satisfied, New Foreign Co. can be incorporated/domiciled wherever the parties

choose.

– If U.S. Target shareholders receive >60% but <80% of the stock of New Foreign Co. (a “60% Inversion”), certain adverse tax consequences are imposed on U.S. Target limiting its ability to offset certain post-transaction income (“Inversion Gain”) with tax attributes (NOLs or FTCs).

• Shareholder Tax Considerations

– Shareholder Gain Recognition – If U.S. persons who are shareholders of U.S. Target receive more than 50% of the stock of New Foreign Co. , then those shareholders would recognize gain (but not loss) in the transaction. • Strategies have been developed to avoid imposition of this shareholder-level tax, though their

successful execution is highly dependent on the facts of the particular transaction.

– Officer/Director Excise Tax – If the transaction constitutes a 60% Inversion, and shareholders recognize gain under section 367, then under Section 4985, officers and directors of U.S. Target must pay a 15% excise tax on the value of any stock-based compensation held by such persons on or around (six months before and six months after) the transaction.

6

Benefits of Redomiciliation Transactions

• Platform for Foreign Growth and Acquisitions

• Intercompany Leverage

• Migration of Intellectual Property

• Repatriation Flexibility

7

Practical Consequences of Cross-Border Transactions

• Management can generally remain U.S.-based. – Given the “place of incorporation” test for tax residence under U.S. law, the location of

management or board meetings is irrelevant to the foreign parent’s tax domicile.

– Several legislative proposals have proposed adopting a “managed and controlled test” for corporate tax residence.

– The 7874 proposals in the Obama Administration’s FY 2015 budget would impose a “managed and controlled test” in the context of cross-border migration transactions.

• Board meetings may have to be in the desired tax domicile to achieve tax residence under the relevant foreign law. – E.g., Ireland requires at least some board meetings to be held in Ireland.

– Foreign countries’ use of “managed and controlled” or “place of effective management” tests, rather than place of incorporation tests, can permit the new foreign parent company to be incorporated in one country and tax resident in another – e.g., Dutch-incorporated but U.K. tax resident.

• The combined group would be expected to increase its non-U.S. operating presence over time due to foreign growth and acquisitions.

8

The economic effects of

territorial taxation, with remarks by Jason Furman

March 31, 2014

Please take this time to silence any mobile devices.

Johannes Voget

ITPF/AEI Conference on the Economic Effects of

Territorial Taxation

Home Country Tax Effects on Mergers,

Inversions, and Headquarters Location

Empirical Evidence

Outline

3 Papers

Slides 3+4: Direction of M&As Huizinga, H.P. and J. Voget (2009), International taxation and the direction and volume of cross-

border M&As, Journal of Finance 64, p. 1217 - 1249.

Slides 5+6: Relocation of Headquarters Voget, J. (2011), Relocation of headquarters and international taxation, Journal of Public

Economics 95, p. 1067 – 11081

Remainder: Effects of Territorial and Worldwide Corporation Tax Systems

on Outbound M&As Feld, L.P., M. Ruf, U. Scheuering, U. Schreiber, and J. Voget (2013), Effects of Territorial and

Worldwide Corporation Tax Systems on Outbound M&As, Centre for European Economic

Research Discussion Paper No. 13-088

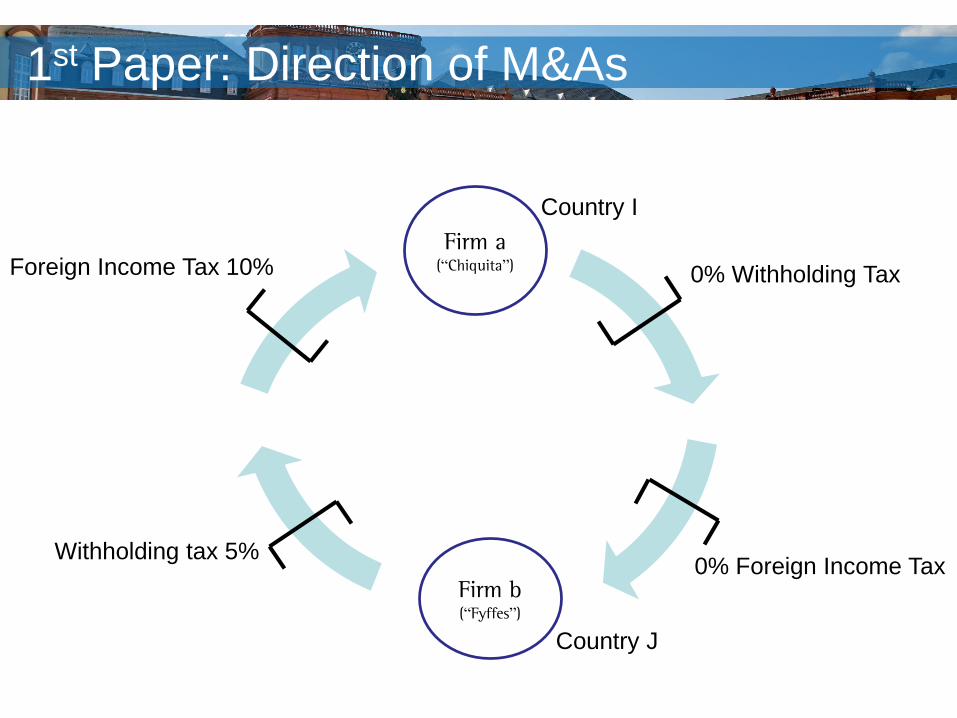

1st Paper: Direction of M&As

Firm a(“Chiquita”)

Firm b(“Fyffes”)

Country I

Country J

Withholding tax 5%

Foreign Income Tax 10% 0% Withholding Tax

0% Foreign Income Tax

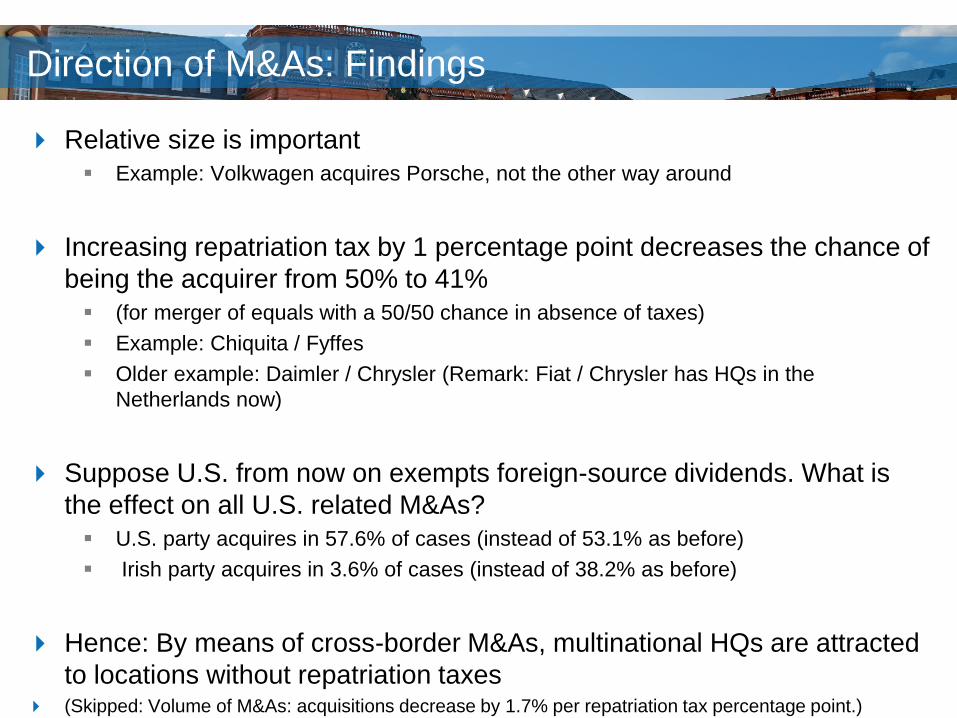

Direction of M&As: Findings

Relative size is important

Example: Volkwagen acquires Porsche, not the other way around

Increasing repatriation tax by 1 percentage point decreases the chance of

being the acquirer from 50% to 41%

(for merger of equals with a 50/50 chance in absence of taxes)

Example: Chiquita / Fyffes

Older example: Daimler / Chrysler (Remark: Fiat / Chrysler has HQs in the

Netherlands now)

Suppose U.S. from now on exempts foreign-source dividends. What is

the effect on all U.S. related M&As?

U.S. party acquires in 57.6% of cases (instead of 53.1% as before)

Irish party acquires in 3.6% of cases (instead of 38.2% as before)

Hence: By means of cross-border M&As, multinational HQs are attracted

to locations without repatriation taxes (Skipped: Volume of M&As: acquisitions decrease by 1.7% per repatriation tax percentage point.)

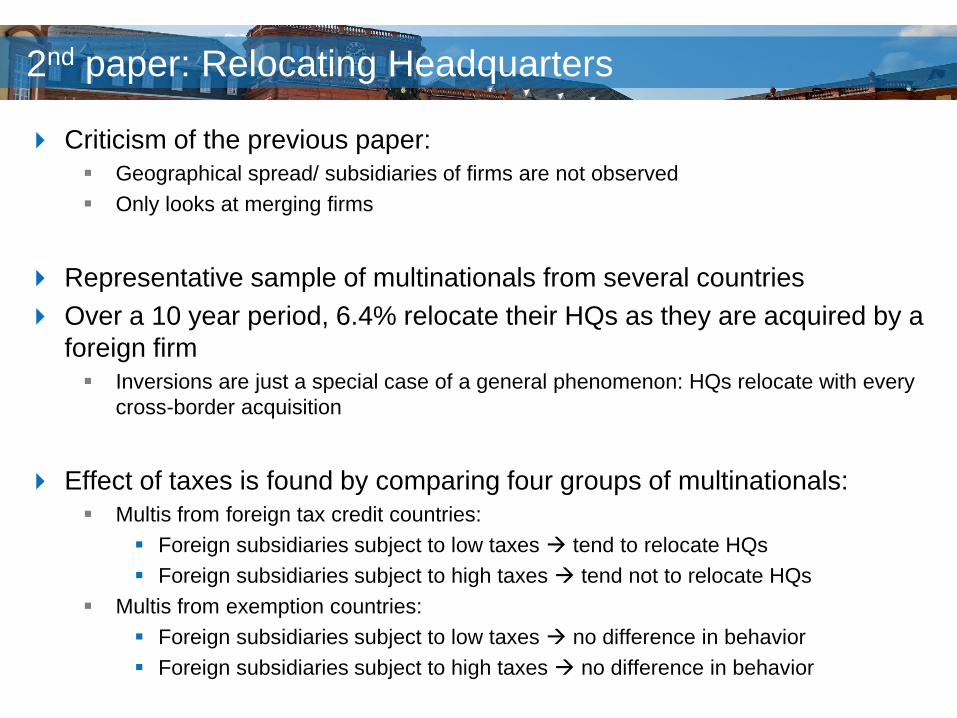

2nd paper: Relocating Headquarters

Criticism of the previous paper:

Geographical spread/ subsidiaries of firms are not observed

Only looks at merging firms

Representative sample of multinationals from several countries

Over a 10 year period, 6.4% relocate their HQs as they are acquired by a

foreign firm

Inversions are just a special case of a general phenomenon: HQs relocate with every

cross-border acquisition

Effect of taxes is found by comparing four groups of multinationals:

Multis from foreign tax credit countries:

Foreign subsidiaries subject to low taxes tend to relocate HQs

Foreign subsidiaries subject to high taxes tend not to relocate HQs

Multis from exemption countries:

Foreign subsidiaries subject to low taxes no difference in behavior

Foreign subsidiaries subject to high taxes no difference in behavior

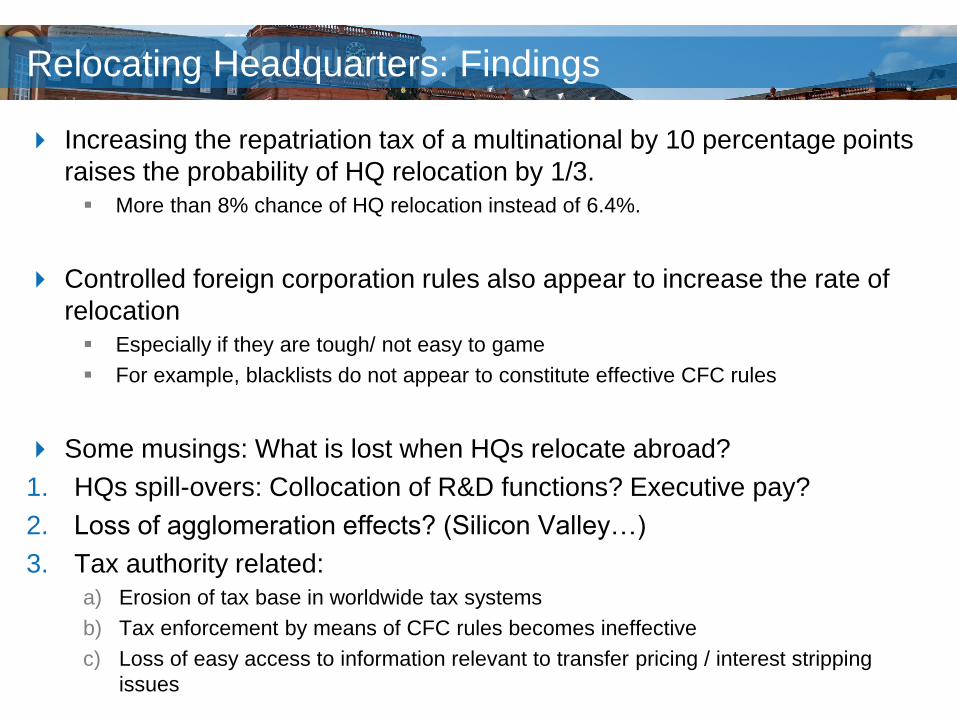

Relocating Headquarters: Findings

Increasing the repatriation tax of a multinational by 10 percentage points

raises the probability of HQ relocation by 1/3.

More than 8% chance of HQ relocation instead of 6.4%.

Controlled foreign corporation rules also appear to increase the rate of

relocation

Especially if they are tough/ not easy to game

For example, blacklists do not appear to constitute effective CFC rules

Some musings: What is lost when HQs relocate abroad?

1. HQs spill-overs: Collocation of R&D functions? Executive pay?

2. Loss of agglomeration effects? (Silicon Valley…)

3. Tax authority related:

a) Erosion of tax base in worldwide tax systems

b) Tax enforcement by means of CFC rules becomes ineffective

c) Loss of easy access to information relevant to transfer pricing / interest stripping

issues

3rd paper: Credit vs Exemption and Outbound M&As

Recent opportunity for research:

Japan and the U.K. both switched from a foreign tax credit system to exempting

foreign source dividends in 2009

First time that we observe an actual switch in international taxation regimes in major

capital exporting countries.

So, is there an effect of repatriation taxes on M&As? Direct identification!

In particular: Is there a competitive disadvantage in the market for

corporate control due to repatriation taxes?

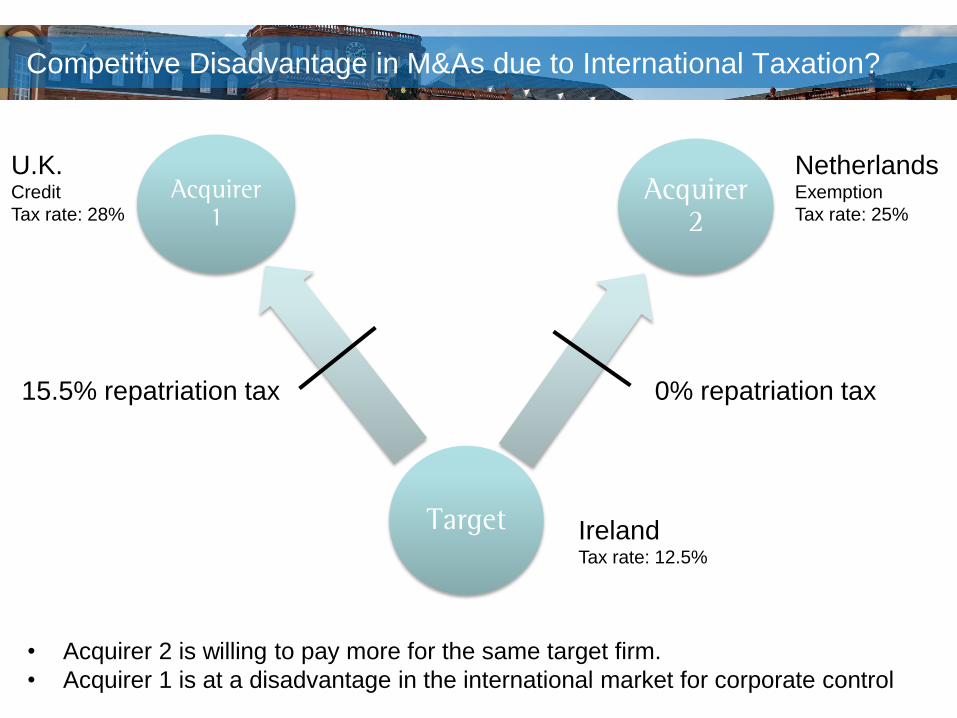

Competitive Disadvantage in M&As due to International Taxation?

Target

Acquirer 2

Acquirer 1

U.K.Credit

Tax rate: 28%

NetherlandsExemption

Tax rate: 25%

IrelandTax rate: 12.5%

15.5% repatriation tax 0% repatriation tax

• Acquirer 2 is willing to pay more for the same target firm.

• Acquirer 1 is at a disadvantage in the international market for corporate control

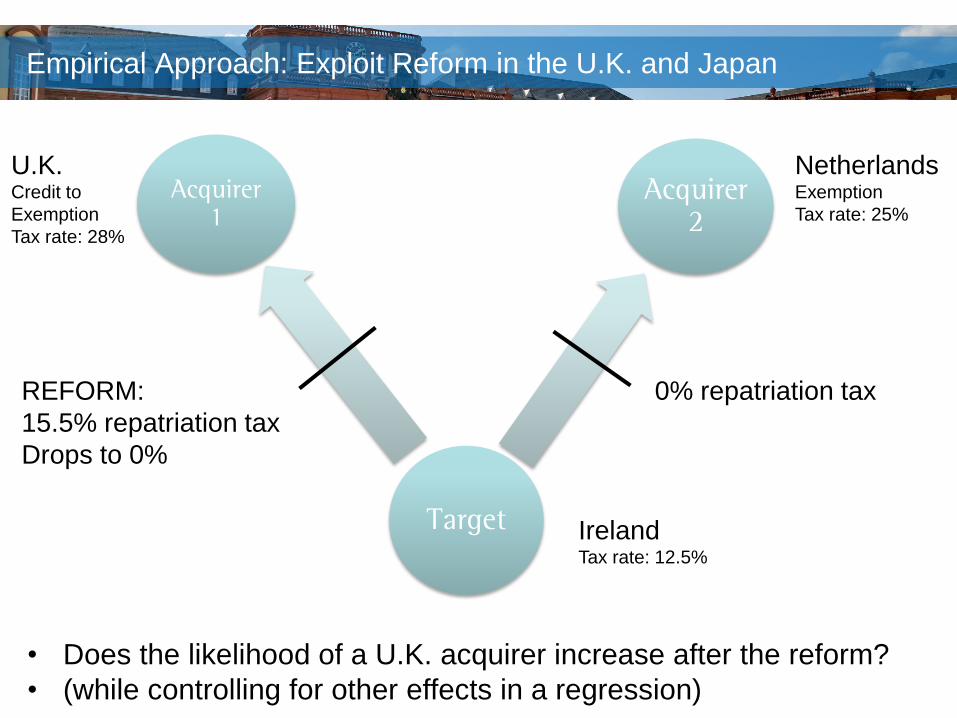

Empirical Approach: Exploit Reform in the U.K. and Japan

Target

Acquirer 2

Acquirer 1

U.K.Credit to

Exemption

Tax rate: 28%

NetherlandsExemption

Tax rate: 25%

IrelandTax rate: 12.5%

REFORM:

15.5% repatriation tax

Drops to 0%

0% repatriation tax

• Does the likelihood of a U.K. acquirer increase after the reform?

• (while controlling for other effects in a regression)

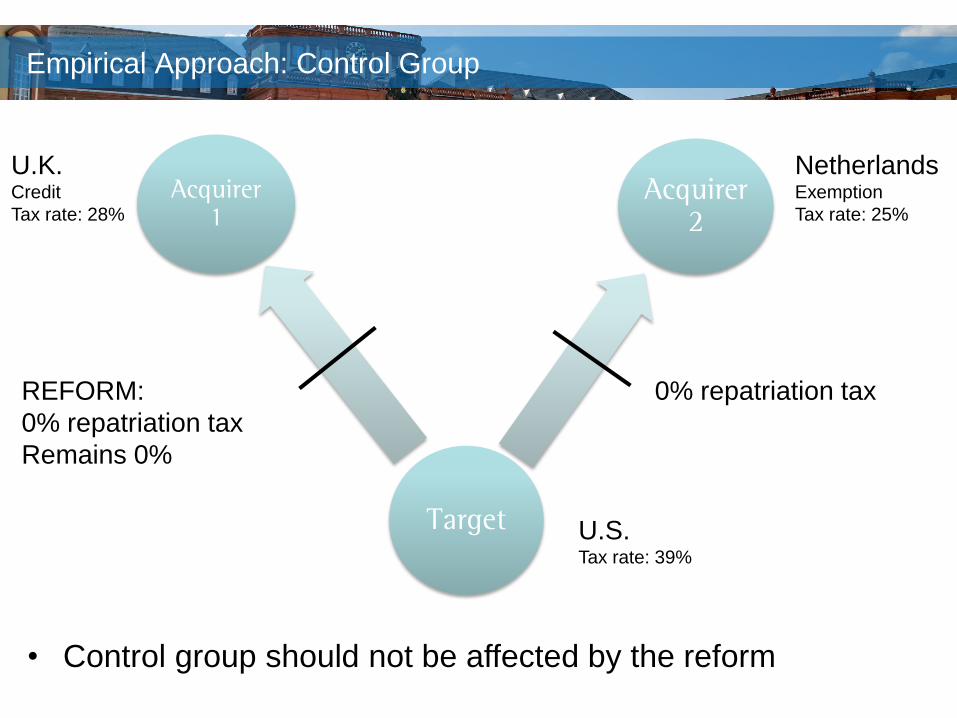

Empirical Approach: Control Group

Target

Acquirer 2

Acquirer 1

U.K.Credit

Tax rate: 28%

NetherlandsExemption

Tax rate: 25%

U.S.Tax rate: 39%

REFORM:

0% repatriation tax

Remains 0%

0% repatriation tax

• Control group should not be affected by the reform

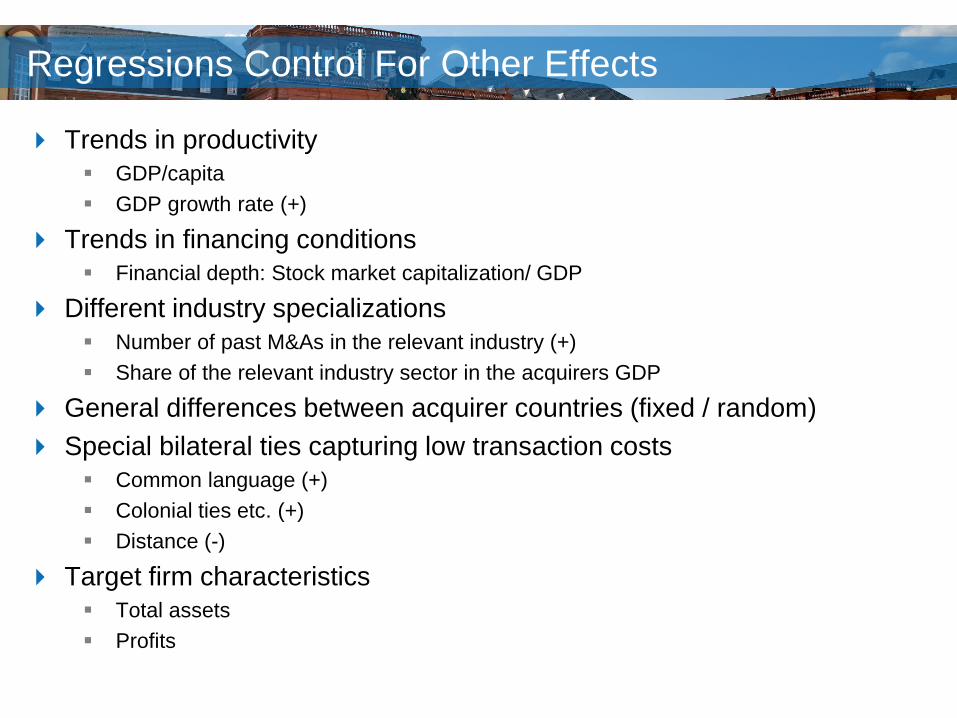

Regressions Control For Other Effects

Trends in productivity

GDP/capita

GDP growth rate (+)

Trends in financing conditions

Financial depth: Stock market capitalization/ GDP

Different industry specializations

Number of past M&As in the relevant industry (+)

Share of the relevant industry sector in the acquirers GDP

General differences between acquirer countries (fixed / random)

Special bilateral ties capturing low transaction costs

Common language (+)

Colonial ties etc. (+)

Distance (-)

Target firm characteristics

Total assets

Profits

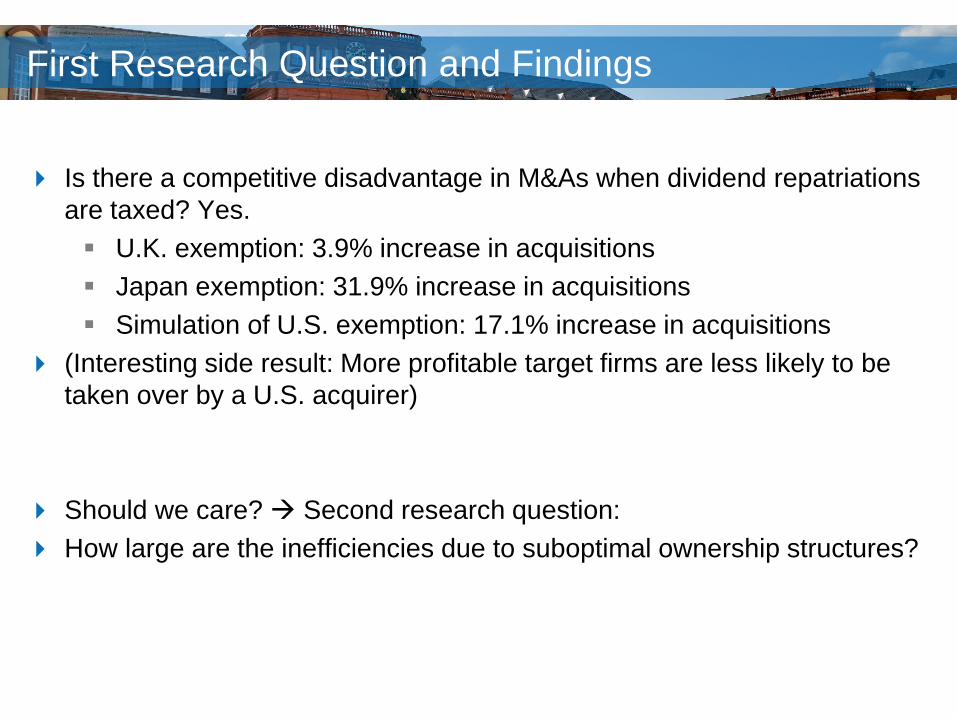

First Research Question and Findings

Is there a competitive disadvantage in M&As when dividend repatriations

are taxed? Yes.

U.K. exemption: 3.9% increase in acquisitions

Japan exemption: 31.9% increase in acquisitions

Simulation of U.S. exemption: 17.1% increase in acquisitions

(Interesting side result: More profitable target firms are less likely to be

taken over by a U.S. acquirer)

Should we care? Second research question:

How large are the inefficiencies due to suboptimal ownership structures?

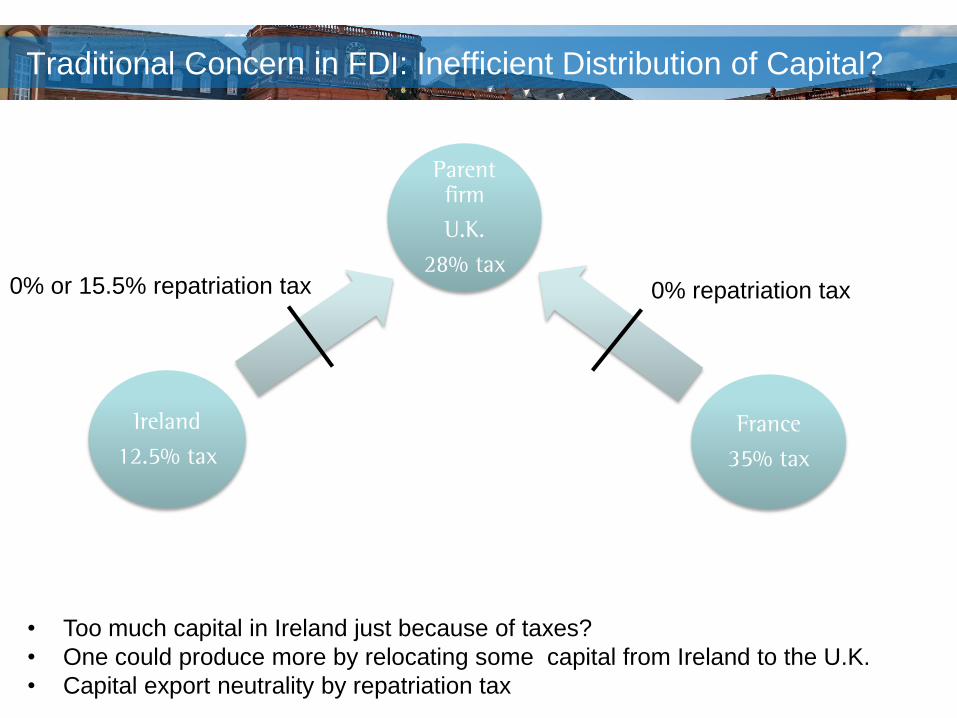

Traditional Concern in FDI: Inefficient Distribution of Capital?

Parent firm

U.K.

28% tax

France

35% tax

Ireland

12.5% tax

0% or 15.5% repatriation tax 0% repatriation tax

• Too much capital in Ireland just because of taxes?

• One could produce more by relocating some capital from Ireland to the U.K.

• Capital export neutrality by repatriation tax

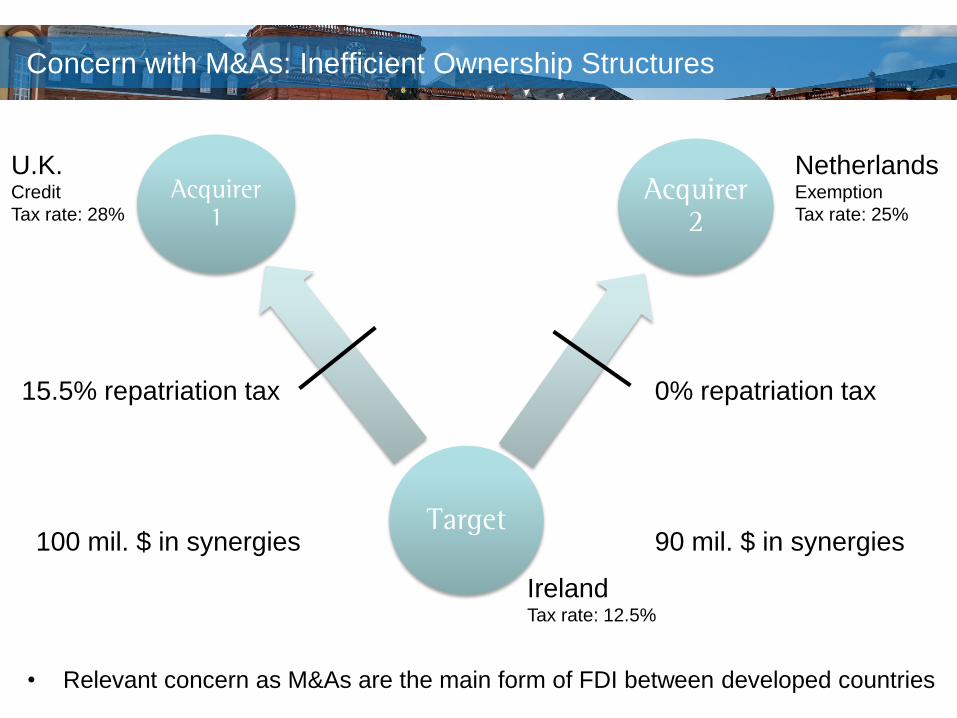

Concern with M&As: Inefficient Ownership Structures

Target

Acquirer 2

Acquirer 1

U.K.Credit

Tax rate: 28%

NetherlandsExemption

Tax rate: 25%

IrelandTax rate: 12.5%

15.5% repatriation tax 0% repatriation tax

• Relevant concern as M&As are the main form of FDI between developed countries

100 mil. $ in synergies 90 mil. $ in synergies

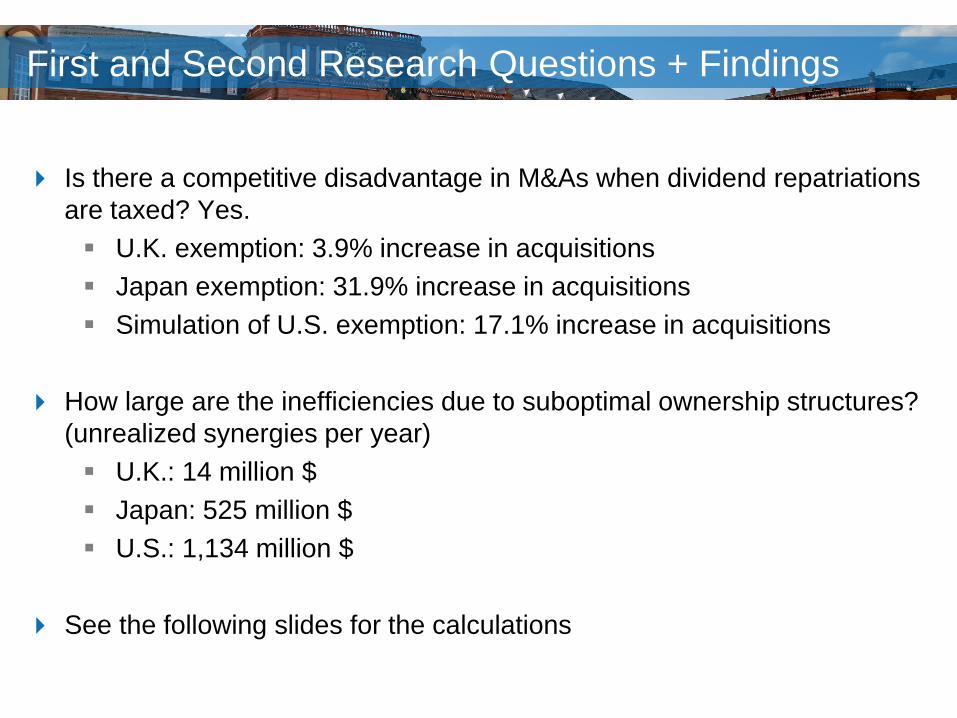

First and Second Research Questions + Findings

Is there a competitive disadvantage in M&As when dividend repatriations

are taxed? Yes.

U.K. exemption: 3.9% increase in acquisitions

Japan exemption: 31.9% increase in acquisitions

Simulation of U.S. exemption: 17.1% increase in acquisitions

How large are the inefficiencies due to suboptimal ownership structures?

(unrealized synergies per year)

U.K.: 14 million $

Japan: 525 million $

U.S.: 1,134 million $

See the following slides for the calculations

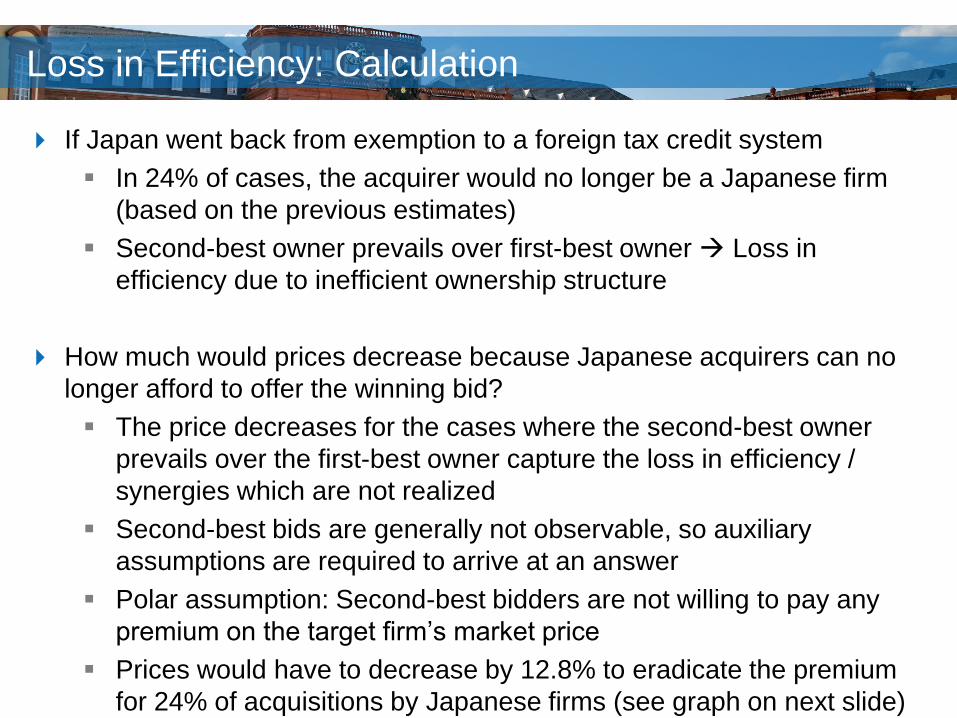

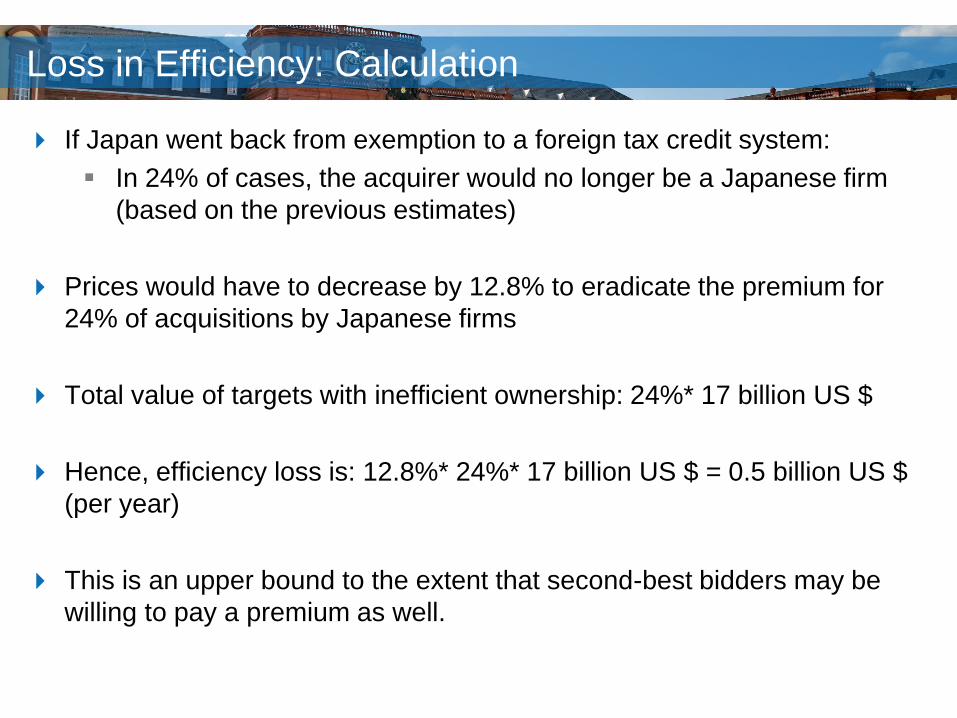

Loss in Efficiency: Calculation

If Japan went back from exemption to a foreign tax credit system

In 24% of cases, the acquirer would no longer be a Japanese firm

(based on the previous estimates)

Second-best owner prevails over first-best owner Loss in

efficiency due to inefficient ownership structure

How much would prices decrease because Japanese acquirers can no

longer afford to offer the winning bid?

The price decreases for the cases where the second-best owner

prevails over the first-best owner capture the loss in efficiency /

synergies which are not realized

Second-best bids are generally not observable, so auxiliary

assumptions are required to arrive at an answer

Polar assumption: Second-best bidders are not willing to pay any

premium on the target firm’s market price

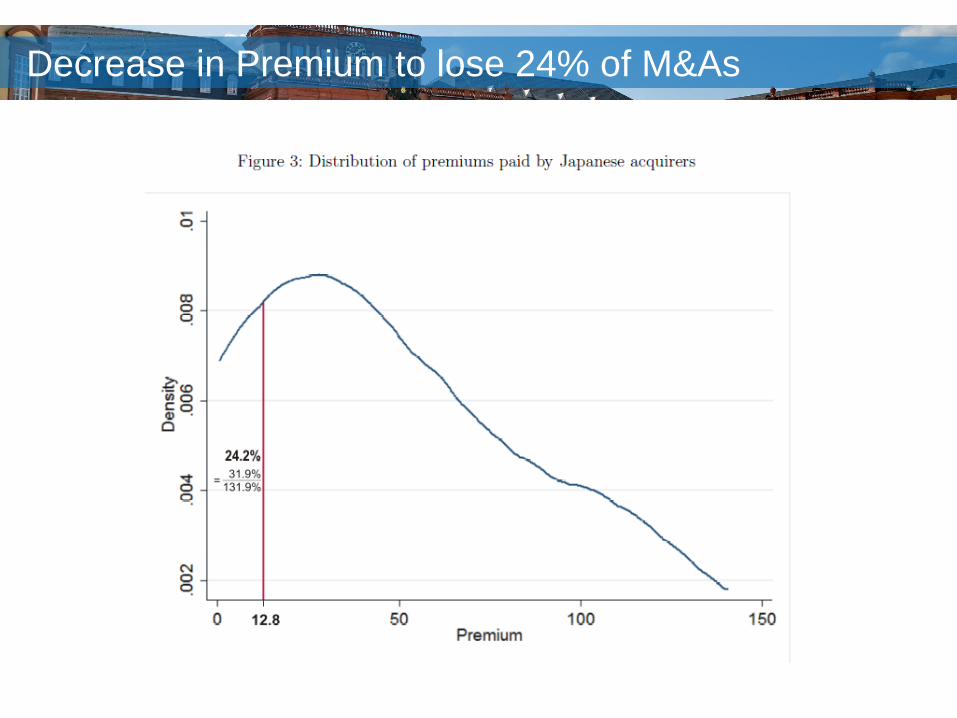

Prices would have to decrease by 12.8% to eradicate the premium

for 24% of acquisitions by Japanese firms (see graph on next slide)

Decrease in Premium to lose 24% of M&As

Loss in Efficiency: Calculation

If Japan went back from exemption to a foreign tax credit system:

In 24% of cases, the acquirer would no longer be a Japanese firm

(based on the previous estimates)

Prices would have to decrease by 12.8% to eradicate the premium for

24% of acquisitions by Japanese firms

Total value of targets with inefficient ownership: 24%* 17 billion US $

Hence, efficiency loss is: 12.8%* 24%* 17 billion US $ = 0.5 billion US $

(per year)

This is an upper bound to the extent that second-best bidders may be

willing to pay a premium as well.

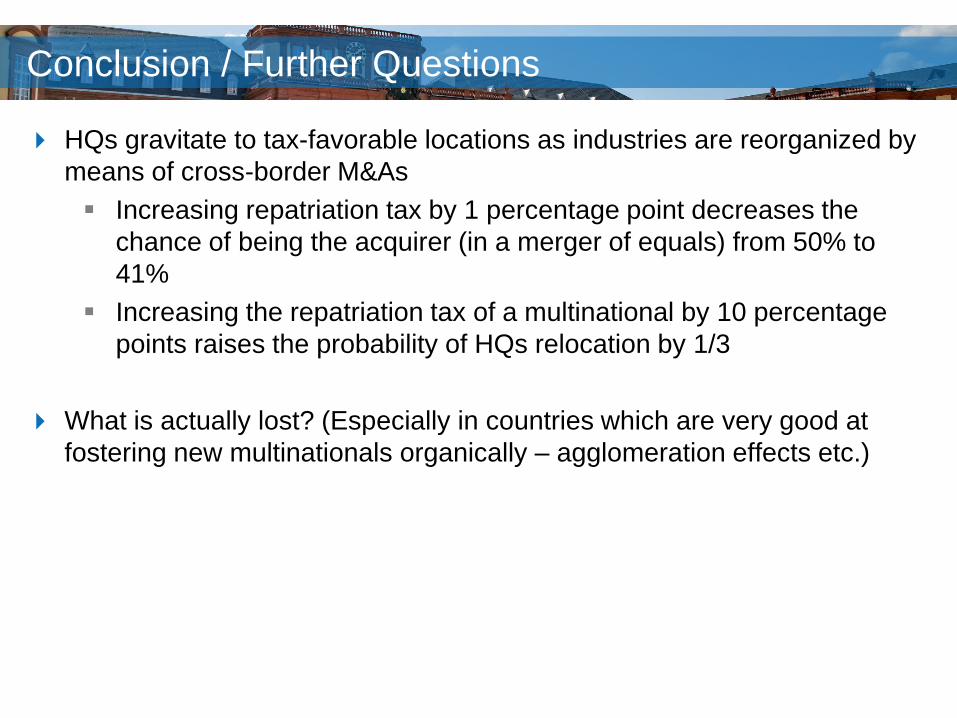

Conclusion / Further Questions

HQs gravitate to tax-favorable locations as industries are reorganized by

means of cross-border M&As

Increasing repatriation tax by 1 percentage point decreases the

chance of being the acquirer (in a merger of equals) from 50% to

41%

Increasing the repatriation tax of a multinational by 10 percentage

points raises the probability of HQs relocation by 1/3

What is actually lost? (Especially in countries which are very good at

fostering new multinationals organically – agglomeration effects etc.)

Conclusion / Further Questions

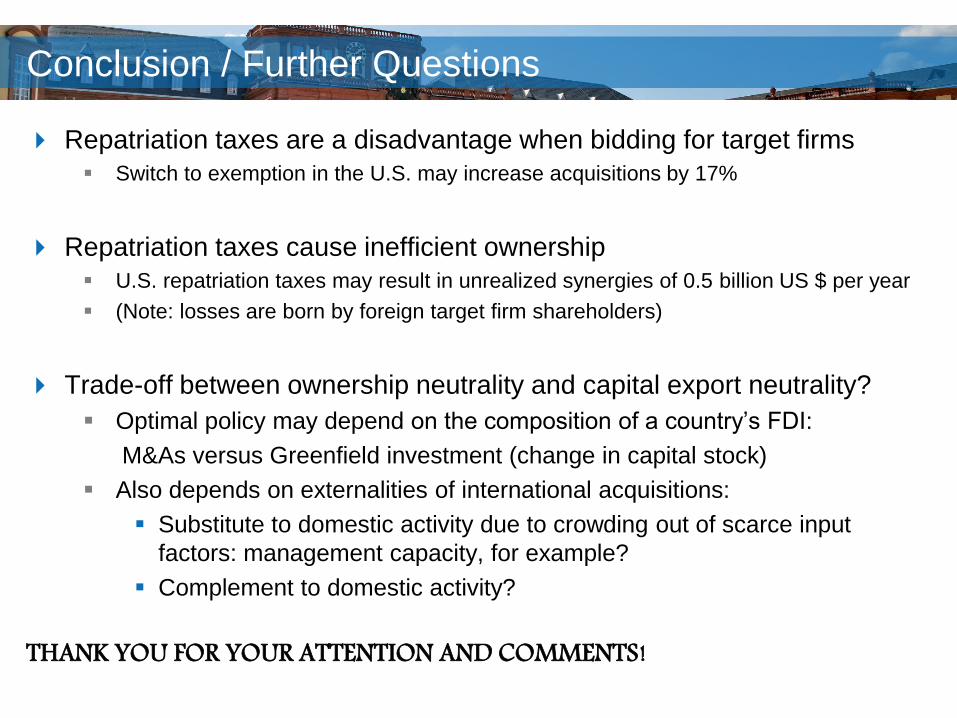

Repatriation taxes are a disadvantage when bidding for target firms

Switch to exemption in the U.S. may increase acquisitions by 17%

Repatriation taxes cause inefficient ownership

U.S. repatriation taxes may result in unrealized synergies of 0.5 billion US $ per year

(Note: losses are born by foreign target firm shareholders)

Trade-off between ownership neutrality and capital export neutrality?

Optimal policy may depend on the composition of a country’s FDI:

M&As versus Greenfield investment (change in capital stock)

Also depends on externalities of international acquisitions:

Substitute to domestic activity due to crowding out of scarce input

factors: management capacity, for example?

Complement to domestic activity?

THANK YOU FOR YOUR ATTENTION AND COMMENTS!

The economic effects of

territorial taxation, with remarks by Jason Furman

March 31, 2014

Please take this time to silence any mobile devices.

The economic effects of

territorial taxation, with remarks by Jason Furman

March 31, 2014

Please take this time to silence any mobile devices.

Initial incorporation decisions of U.S.-headquartered firms

Susan Morse

University of Texas School of Law

Presentation prepared for

ITPF/AEI Conference

Economic Effects of Territorial

Taxation

March 31, 2014

Ways to invert The hard way: an ex post transaction

The easy way: incorporate outside the U.S. initially

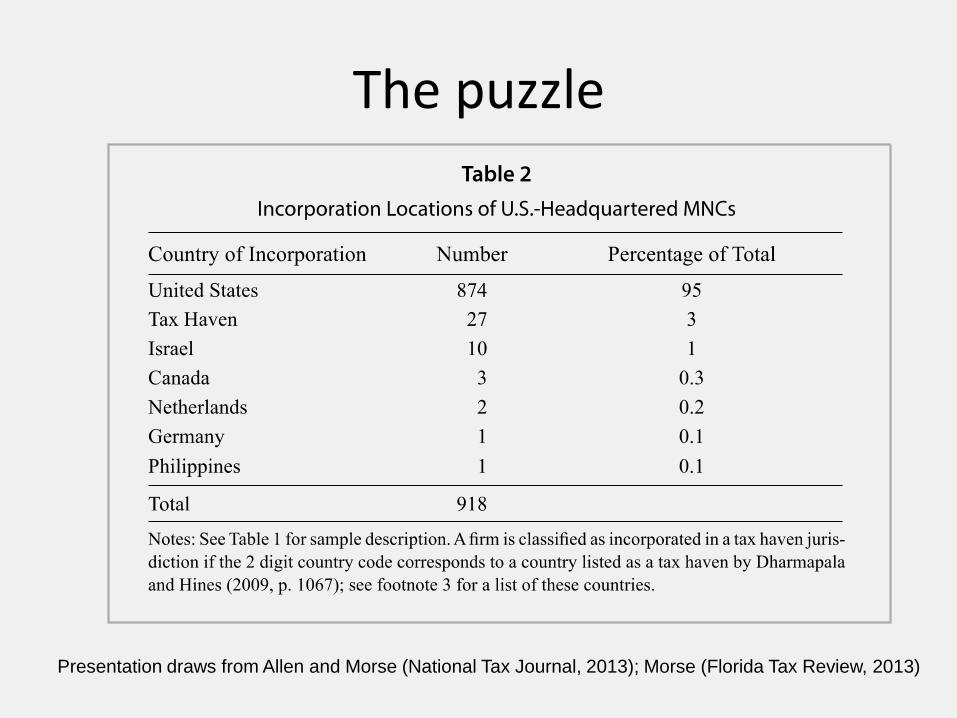

The puzzle

Presentation draws from Allen and Morse (National Tax Journal, 2013); Morse (Florida Tax Review, 2013)

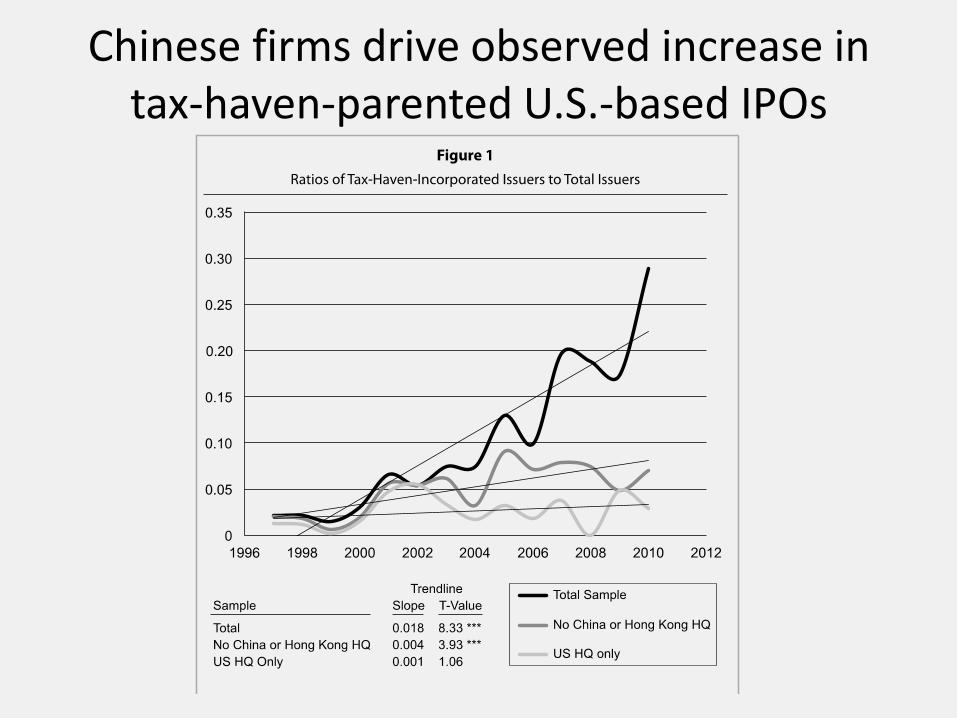

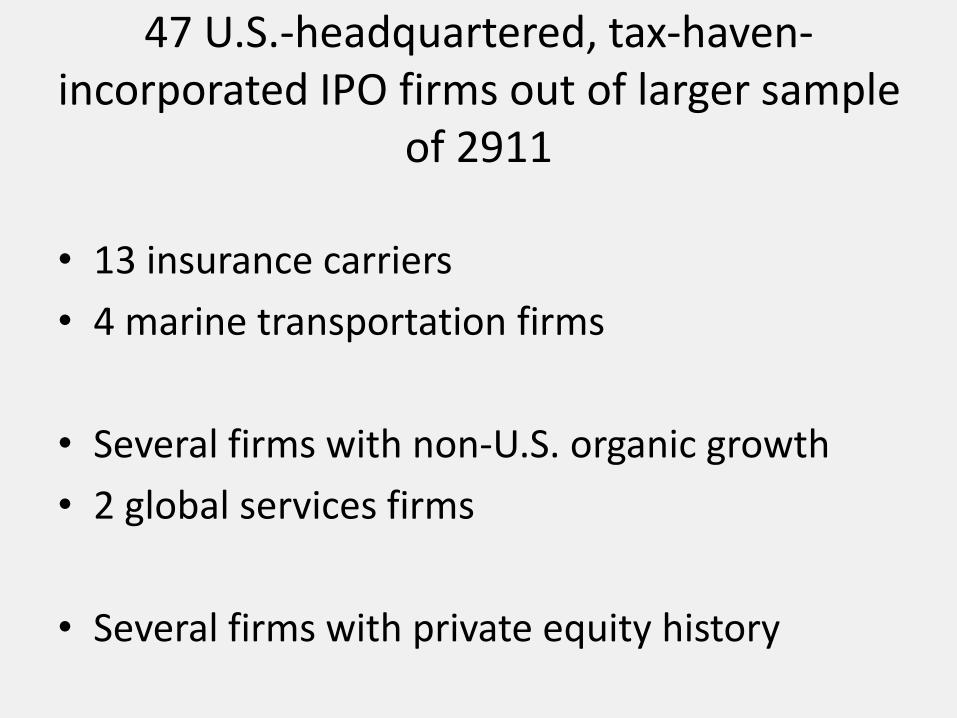

Chinese firms drive observed increase in tax-haven-parented U.S.-based IPOs

47 U.S.-headquartered, tax-haven-incorporated IPO firms out of larger sample

of 2911

• 13 insurance carriers

• 4 marine transportation firms

• Several firms with non-U.S. organic growth

• 2 global services firms

• Several firms with private equity history

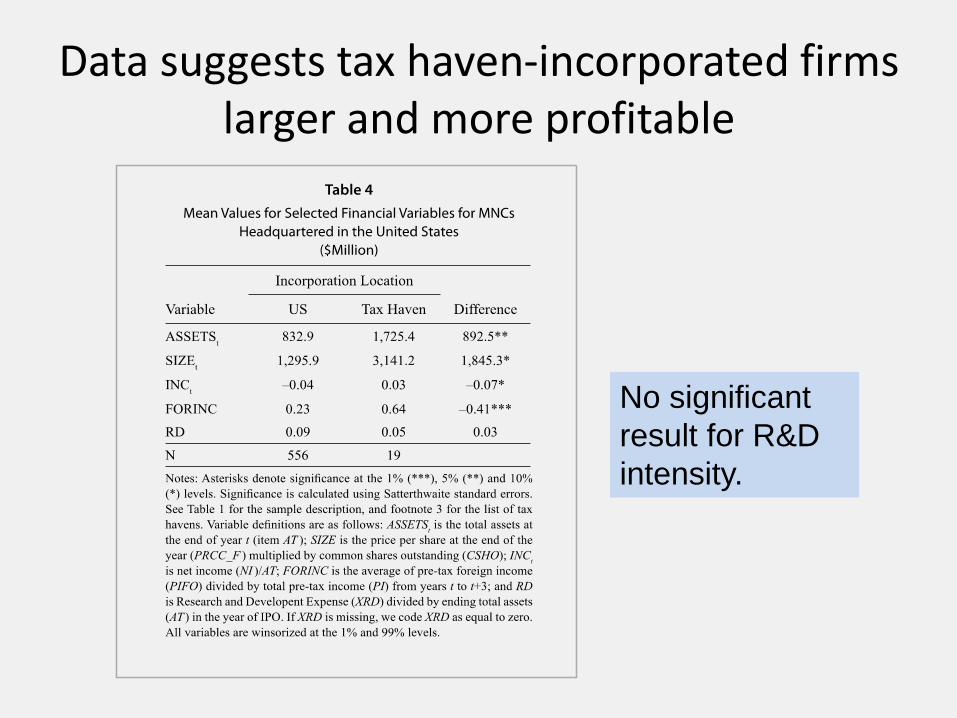

Data suggests tax haven-incorporated firms larger and more profitable

No significant

result for R&D

intensity.

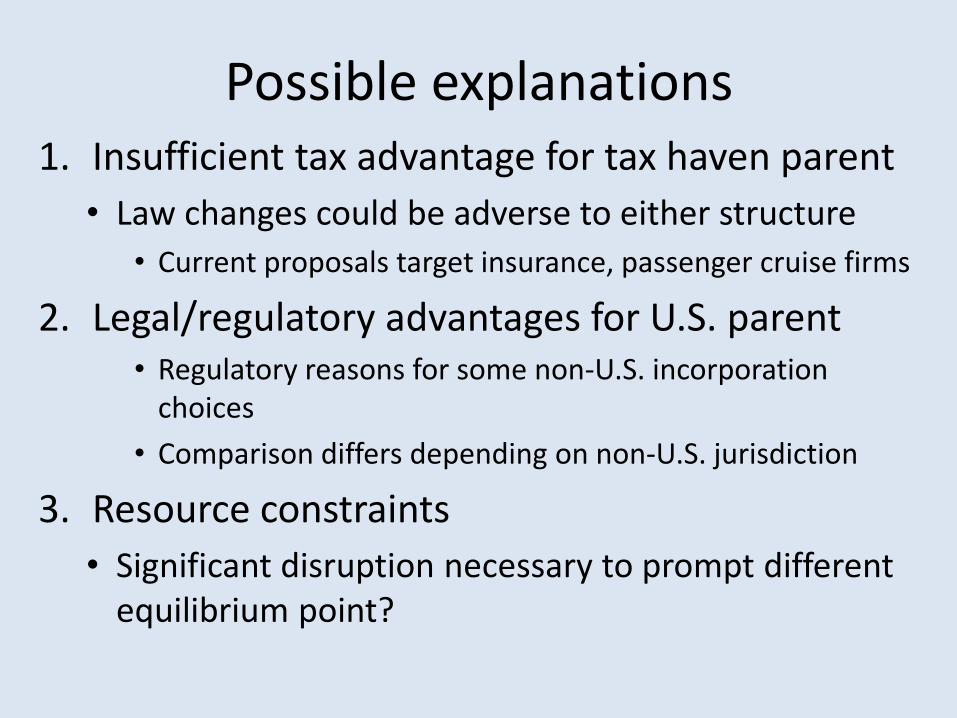

Possible explanations 1. Insufficient tax advantage for tax haven parent

• Law changes could be adverse to either structure

• Current proposals target insurance, passenger cruise firms

2. Legal/regulatory advantages for U.S. parent • Regulatory reasons for some non-U.S. incorporation

choices

• Comparison differs depending on non-U.S. jurisdiction

3. Resource constraints

• Significant disruption necessary to prompt different equilibrium point?

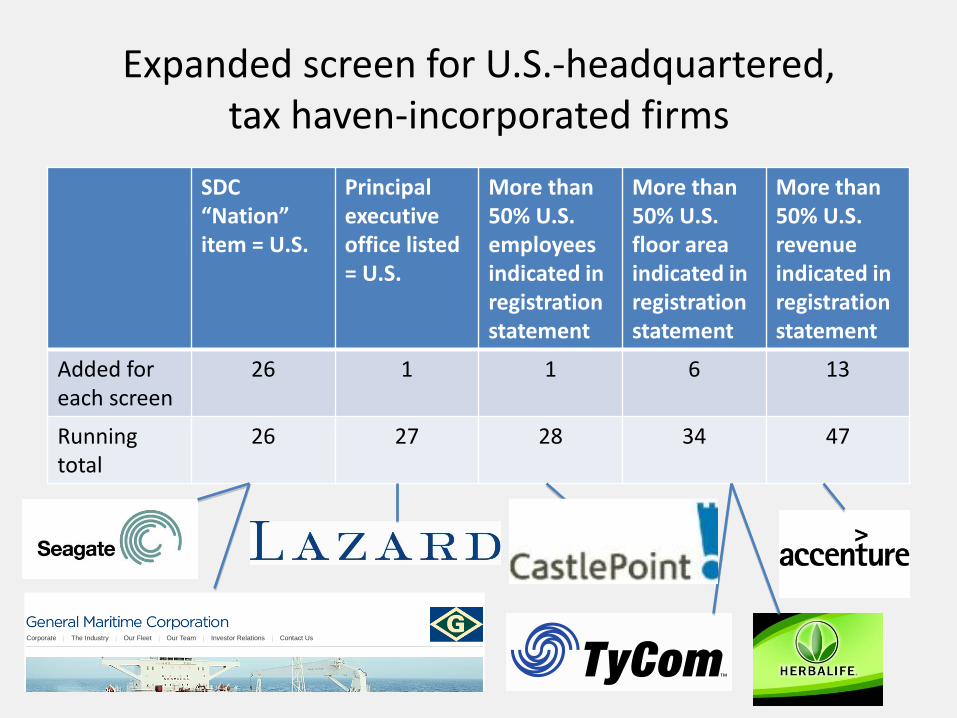

Expanded screen for U.S.-headquartered, tax haven-incorporated firms

SDC “Nation” item = U.S.

Principal executive office listed = U.S.

More than 50% U.S. employees indicated in registration statement

More than 50% U.S. floor area indicated in registration statement

More than 50% U.S. revenue indicated in registration statement

Added for each screen

26 1 1 6 13

Running total

26 27 28 34 47

Corporate The Industry Our Fleet Our Team Investor Relations Contact Us

THE GENERAL MARITIME VISION

Our vision is to become the leading marine link in the international energy supply chain;

providing innovative and superior transportation services to a diverse client base while creating

value for shareholders.

THE GENERAL MARITIME COMMITMENT

General Maritime is dedicated to safely providing seaborne energy transportation services

utilizing an organization of qualified professionals to achieve unparalleled customer.

GENERAL MARITIME’S CORE VALUES

Quality and professionalism

Safety and protection of the crews, cargo, and environment

Loyalty to stakeholders

Responsiveness to our customers

Continuous self-improvement

FEATURED NEWS

GENERAL MARITIME ANNOUNCES AMENDMENTS T OCREDIT FACILITIES

GENERAL MARITIME CORPORATION TO PRESENT ATTHE JEFFERIES 2011 GLOBAL SHIPPINGCONFERENCE

GENERAL MARITIME RECEIVES NOTICE OFNON-COMPLIANCE WITH NYSE MINIMUM SHAREPRICE LISTING RULE

© General Maritime Corp. All rights reserved.

General Maritime Corporation is a

leading provider of international

seaborne energy transportation

services, owning and operating one

of the largest tanker fleets in the

world.

This Week's IPOs: CastlePoint Holdings, Cheniere

Energy Partners, Glu Mobile, Haynes International

by: SA Editor Abbi Adest

March 18, 2007 | includes: CPHL, CQP, GLUU, HAYN

IPOs on deck for this week include: CastlePoint Holdings (CPHL), a property, casualty insurance and reinsurance

company; Cheniere Energy Partners (CQP), a natural gas development company; Glu Mobile (GLUU), a mobile

game publisher; and Haynes International (HAYN) a high-performance alloy manufacturing company.

All quotations are from the companies' most recent S-1 filings with links provided for each company.

CASTLEPOINT HOLDINGS, LTD. (CPHL)

Business Overview (from prospectus)

We are a Bermuda holding company organized to provide property and casualty insurance and

reinsurance business solutions, products and services primarily to small insurance companies and

program underwrit ing agents in the United States. We were incorporated in November 2005 to take

advantage of opportunities that we believe exist in the insurance and reinsurance industry for

traditional quota share reinsurance, insurance risk-sharing and program business as well as insurance

company services that can be purchased on a stand-alone, or unbundled basis, to small insurance

companies and program underwriting agents.

Offering: 6.1 million shares at $13.00-15.00 per share. Net proceeds of approximately $76.5 million will be used to

"further capitalize CastlePoint Re, and for general corporate purposes. We will not receive any of the proceeds from

the sale of common shares by the selling shareholders."

Lead Underwriters: Friedman Billings, Cochran Caronia

Financial Highlights:

Total revenues were $92.5 million in 2006, which consisted of net premiums earned (85.4% of the total

revenues), commission income (2.5% of the total revenues) and net investment income (12.1% of the

total revenues)... Our net income was $10.5 million in 2006. The net income increased each quarter

throughout 2006 primarily as a result of increasing underwriting and investment leverage throughout

the year. Our average return on equity was 5.1% for the year ended December 31, 2006. The return

was calculated by dividing net income of $10.5 million by weighted average shareholders' equity of

$207.3 million. Our return on equity increased by quarter in line with our increase in net income and

was 9.8% for the three months ended December 31, 2006... Gross and net written premiums were

$165.2 million in 2006. Included in the gross and net written premiums of $165.2 million was $40.9

million of written premiums from Tower representing 30% of Tower's unearned premiums for the

brokerage business as of March 31, 2006. The total amount of written premiums assumed from Tower

Countries classified as tax havens Andorra Anguilla Antigua and Barbuda Aruba Bahamas Bahrain Barbados Bermuda British Virgin Islands Cayman Islands Channel Islands Cook Islands Cyprus Dominica Gibraltar Hong Kong

Ireland Isle of Man Jordan Lebanon Liberia Lichtenstein Luxembourg Macao Maldives Malta Marshall Islands Mauritius Monaco Montserrat Nauru Netherland Antilles

Niue Panama Saint Kitts and Nevis Saint Lucia Saint Vincent and the

Grenadines Samoa San Marino Seychelles Singapore Switzerland Tonga Turks and Caicos Vanuatu Virgin Islands

Following Dharmapala and Hines (2009)