the design & use of activity- based costing systems · the design & use of activity-based...

TRANSCRIPT

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-1

5The Design & Use of Activity-

Based Costing Systems

Student Tutorial

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-2

Is it important to knowhow the work of the

organization is done?

Is it important to knowhow the work of the

organization is done?

Do we need costs to provide incentives for

improvements?

Do we need costs to provide incentives for

improvements?

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-3

yesyes

Activity based costing has been developed inresponse to these questions.

Activity based costing has been developed inresponse to these questions.

Is it important to knowhow the work of the

organization is done?

Is it important to knowhow the work of the

organization is done?

Do we need costs to provide incentives for

improvements?

Do we need costs to provide incentives for

improvements?

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-4

A discreet unit of work for which an organization candefine inputs (resources used) and outputs

A discreet unit of work for which an organization candefine inputs (resources used) and outputs

Activities for the outsourced hiring processinclude background checks on applicants

Activities for the outsourced hiring processinclude background checks on applicants

Activities for the production process include setting up equipment to make a specific product

Activities for the production process include setting up equipment to make a specific product

Activity-Based Costing

WHAT IS AN ACTIVITY?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-5

Activity-Based CostingQuestion #1

Preliminary cost allocationsassign costs to:

A. DepartmentsB. ProductsC. ActivitiesD. Expenses

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-6

Activity-Based CostingQuestion #1

Preliminary cost allocationsassign costs to:

A. DepartmentsB. ProductsC. ActivitiesD. Expenses

Nope, tryagain.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-7

Activity-Based CostingQuestion #1

Preliminary cost allocationsassign costs to:

A. DepartmentsB. ProductsC. ActivitiesD. Expenses

Uh,uh.Think aboutthe title of

the chapter!Try again.

Uh,uh.Think aboutthe title of

the chapter!Try again.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-8

Activity-Based CostingQuestion #1

Preliminary cost allocationsassign costs to:

A. DepartmentsB. ProductsC. ActivitiesD. Expenses

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-9

Activity-Based CostingQuestion #1

Preliminary cost allocationsassign costs to:

A. DepartmentsB. ProductsC. ActivitiesD. Expenses

It’s not calledEXPENSE-

Basedcosting! Try

again.

It’s not calledEXPENSE-

Basedcosting! Try

again.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-10

Activity-Based CostingQuestion #2

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-11

Activity-Based CostingQuestion #2

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

Think aboutwhy we areallocating

these costs.Try again.

Think aboutwhy we areallocating

these costs.Try again.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-12

Activity-Based CostingQuestion #2

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-13

Activity-Based CostingQuestion #2

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

Assigning toActivities is for

preliminaryallocations.Try again.

Assigning toActivities is for

preliminaryallocations.Try again.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-14

Activity-Based CostingQuestion #2

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

Final cost allocations assign coststo:

A. Departments

B. Products

C. Activities

D. Expenses

Uh, uh.Try again.Uh, uh.

Try again.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-15

Stage One:Processes and

Activities

Stage One:Processes and

Activities

Stage Two:Several products

or services

Stage Two:Several products

or services

ABC TRACES TWO STAGE FLOW OFRESOURCES

ABC TRACES TWO STAGE FLOW OFRESOURCES

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-16

Physical resources Human resources

Production process 2

Manual injection molding

D. Mold partsE. Inspect quality

Business process 3

Process orders

F. Receive customer ordersG. Coordinatecustomer orders

Baby care products Baby container products

Activity-Based Costing

Production process 1

Computer-controlled injection molding

A. Mold partsB. Test quality of partsC. Assemble product

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-17

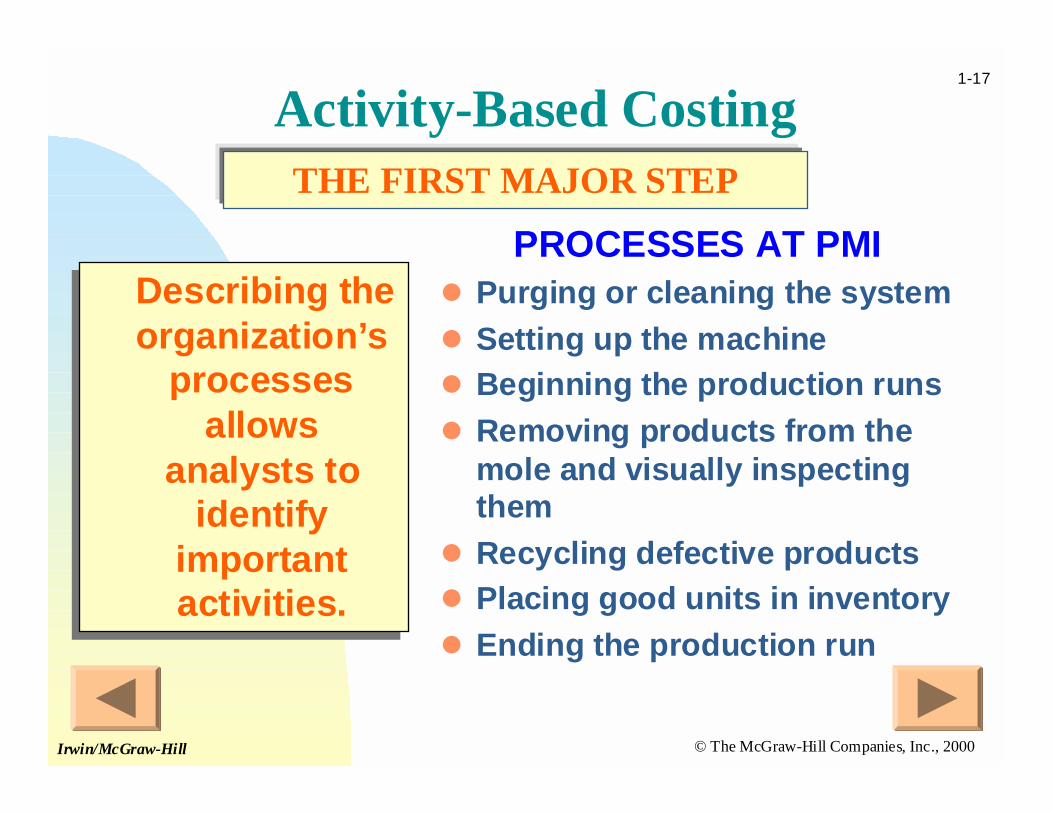

Describing theorganization’s

processesallows

analysts toidentify

importantactivities.

Describing theorganization’s

processesallows

analysts toidentify

importantactivities.

PROCESSES AT PMI! Purging or cleaning the system

! Setting up the machine

! Beginning the production runs

! Removing products from themole and visually inspectingthem

! Recycling defective products

! Placing good units in inventory

! Ending the production run

THE FIRST MAJOR STEP

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-18

Purge system(eliminate previousplastic and color)

Purge system(eliminate previousplastic and color)

Set up machineSet up machine

Begin production runBegin production run

Remove products and inspect

Remove products and inspect

Place good productsin inventory

Place good productsin inventory

End Production RunEnd Production Run

Injection-molding Process At PMI

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-19

Manufacture of mold (outsourced)

Manufacture of mold (outsourced)

Design of product with customer

Design of product with customer

Purge system(eliminate previousplastic and color)

Purge system(eliminate previousplastic and color)

Set up machineSet up machine

Begin production runBegin production run

Remove products and inspect

Remove products and inspect

Place good productsin inventory

Place good productsin inventory

End Production RunEnd Production Run

Deliverproducts tocustomer on

demand

Deliverproducts tocustomer on

demand

Supply ofplasticpellets

(inputs)by rail

(outsourced)

Supply ofplasticpellets

(inputs)by rail

(outsourced)

Injection-molding Process At PMI

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-20

Manufacture of mold (outsourced)

Manufacture of mold (outsourced)

Design of product with customer

Design of product with customer

Business processesFinance and accounting

LegalMarketingPurchasing

Human resources

Business processesFinance and accounting

LegalMarketingPurchasing

Human resources

Recycledefectiveproducts

Recycledefectiveproducts

Purge system(eliminate previousplastic and color)

Purge system(eliminate previousplastic and color)

Set up machineSet up machine

Begin production runBegin production run

Remove products and inspect

Remove products and inspect

Place good productsin inventory

Place good productsin inventory

End Production RunEnd Production Run

Supply ofplasticpellets

(inputs)by rail

(outsourced)

Supply ofplasticpellets

(inputs)by rail

(outsourced)

Deliverproducts tocustomer on

demand

Deliverproducts tocustomer on

demand

Injection-molding Process At PMI

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-21

THE HIERARCHY OF RESOURCES

componentscomponents

labourlabour

energyenergypartsparts

materialsmaterials

Resources that are acquired specifically for individual units of product or service

Resources that are acquired specifically for individual units of product or service

Unit-levelResourcesUnit-levelResources

Directly traceable to the decision toproduce the level

of output

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-22

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #3

Which resources in the list below are most likelyacquired specifically for individual units of

product or service?

Which resources in the list below are most likelyacquired specifically for individual units of

product or service?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-23

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #3

Which resources in the list below are most likelyacquired specifically for individual units of

product or service?

Which resources in the list below are most likelyacquired specifically for individual units of

product or service?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-24

Higher Level ResourcesHigher Level Resources

Acquired as a result of the decision to make a group,or batch of similar products.

Acquired as a result of the decision to make a group,or batch of similar products.

Batch-levelBatch-level

MaterialsMaterials

Equipment Applicable to the BatchEquipment Applicable to the Batch

Specialized LabourSpecialized Labour

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-25

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #4

Which resources in the list below are acquiredas a result of the decision to make a group, or

batch of similar products?

Which resources in the list below are acquiredas a result of the decision to make a group, or

batch of similar products?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-26

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #4

Which resources in the list below are acquiredas a result of the decision to make a group, or

batch of similar products?

Which resources in the list below are acquiredas a result of the decision to make a group, or

batch of similar products?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-27

Higher Level ResourcesHigher Level Resources

Acquired as a result of the decision to produce andsell a specific product or service.

Acquired as a result of the decision to produce andsell a specific product or service.

Product-levelProduct-level

Personnel Applicable to that Product or ServicePersonnel Applicable to that Product or Service

Specialized EquipmentSpecialized EquipmentSoftwareSoftware

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-28

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #5

Which resources in the list below are acquiredas a result of the decision to produce and sell a

specific product or service?

Which resources in the list below are acquiredas a result of the decision to produce and sell a

specific product or service?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-29

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #5

Which resources in the list below are acquiredas a result of the decision to produce and sell a

specific product or service?

Which resources in the list below are acquiredas a result of the decision to produce and sell a

specific product or service?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-30

Specialized EquipmentSpecialized EquipmentSoftwareSoftware

Higher Level ResourcesHigher Level Resources

Acquired as a result of the decision to serve specificcustomers

Acquired as a result of the decision to serve specificcustomers

Customer-levelCustomer-level

Personnel Dedicated to SpecificCustomers

Personnel Dedicated to SpecificCustomers

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-31

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #6

Which resources in the list below are acquiredas a result of the decision to serve specific

customers?

Which resources in the list below are acquiredas a result of the decision to serve specific

customers?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-32

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #6

Which resources in the list below are acquiredas a result of the decision to serve specific

customers?

Which resources in the list below are acquiredas a result of the decision to serve specific

customers?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-33

Higher Level ResourcesHigher Level Resources

Acquired as a result of the decision to provide a general capacity to produce products and services.

Acquired as a result of the decision to provide a general capacity to produce products and services.

Facility-levelFacility-level

Business support services

Buildings Management

Labour force

Land

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-34

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #7

Which resources in the list below are acquiredas a result of the decision to provide a generalcapacity to produce products and services?

Which resources in the list below are acquiredas a result of the decision to provide a generalcapacity to produce products and services?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-35

a. Hourly labour employed tomeet production levels

b. Utility costs to operateproduction machinery

c. Issuance of engineeringchange orders

d. Machine setup

e. Materials used to make theproduct

f. Product design

g. Inserting components

h. Purchase ordering

i. Material handling

j. Parts administration

k. Plant depreciation

l. Plant management

m. Customer servicepersonnel

Activity-Based Costing Question #7

Which resources in the list below are acquiredas a result of the decision to provide a generalcapacity to produce products and services?

Which resources in the list below are acquiredas a result of the decision to provide a generalcapacity to produce products and services?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-36

Structural Cost DriversStructural Cost Drivers

They determine or drive the overall make-up and structure of costs

They determine or drive the overall make-up and structure of costs

Executional Cost DriversExecutional Cost Drivers

They determine how the organization carries out itswork and causes resources to be consumed by that work

They determine how the organization carries out itswork and causes resources to be consumed by that work

More elaborate designMore elaborate designLarge sizeLarge size Special featuresSpecial features

Activity-Based Costing

Workprocedures

Workprocedures

Workmethods

Workmethods

Workpolicies

Workpolicies

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-37

UNIT-LEVEL ACTIVITESThe work efforts that transform resources into individual

products and resources

UNIT-LEVEL ACTIVITESThe work efforts that transform resources into individual

products and resources

CUSTOMER- LEVEL ACTIVITESPerformed to meet the needs of specific customers

CUSTOMER- LEVEL ACTIVITESPerformed to meet the needs of specific customers

BATCH-LEVEL ACTIVITES Manufacturing or service technology that affect multiple

units of activity equally and simultaneously

BATCH-LEVEL ACTIVITES Manufacturing or service technology that affect multiple

units of activity equally and simultaneously

PRODUCT - LEVEL ACTIVITESSupport specific products or service lines

PRODUCT - LEVEL ACTIVITESSupport specific products or service lines

FACILITY-LEVEL ACTIVITIESSupport all of the organizations processes

FACILITY-LEVEL ACTIVITIESSupport all of the organizations processes

Activity-Based Costing

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-38

Tracing Resources To Activities ToProducts And Services

Facility-level resources

Product-level resources

Customer-level resources

Batch-level resources

Unit-level resources

Resources Costs of activitiesCosts of products

and services

Stage 1: tracing use of resources

Stage 2: assigning cost

Facility-level activities

Product-level activities

Customer-level activities

Unit-level activities

Batch-level activities

Facility-level costs

Product-level costs

Customer-level costs

Batch-level costs

Unit-level costs

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-39

Stage 1: Measuring The Cost OfActivities

Identifying and classifying activitiesIdentifying and classifying activities

TOP DOWN APPROACHAnalysis teams develop activities based on the team’s

understanding of the organization’s processes

TOP DOWN APPROACHAnalysis teams develop activities based on the team’s

understanding of the organization’s processes

INTERVIEW OR PARTICIPATIVE APPROACHAnalysis teams interview employees or form teams of

employees to identify the activities they perform

INTERVIEW OR PARTICIPATIVE APPROACHAnalysis teams interview employees or form teams of

employees to identify the activities they perform

RECYCLING APPROACHReuse documentation of processes used of other

purposes

RECYCLING APPROACHReuse documentation of processes used of other

purposes

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-40

Stage 1: Measuring The Cost OfActivities

Selecting cost- driver basesSelecting cost- driver bases

Cost drivers cause Costs to be incurred

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-41

Stage 1: Measuring The Cost OfActivities

Selecting cost- driver basesSelecting cost- driver bases

Cost drivers cause Costs to be incurred

Increases or decreases in cost driver bases

cause

Increases or decreases in the level of activity

to be performed

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-42

Stage 1: Measuring The Cost OfActivities

Selecting cost- driver basesSelecting cost- driver bases

Cost drivers cause Costs to be incurred

Increases or decreases in cost driver bases

cause

Increases or decreases in the level of activity

to be performed

The level of an activitydirectly affects

Its use of resources and its cost

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-43

Stage 1: Measuring The Cost OfActivities

1. Entering purchase orders a. Number of setups2. Material handling b. Time worked for shop3. Maintain machines c. Number of orders4. Setups d. Square footage5. Janitorial cleaning activity e. Number of parts6. Part administration f. Number of moves7. Production order g. Maintenance hours 8. Engineering h. Direct labour hours

Identify the most likely cost- driver basefor each activity:

Identify the most likely cost- driver basefor each activity:

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-44

Stage 1: Measuring The Cost OfActivities

1. Entering purchase orders c a. Number of setups2. Material handling f b. Time worked for shop3. Maintain machines g c. Number of orders4. Setups a d. Square footage5. Janitorial cleaning activity d e. Number of parts6. Part administration e f. Number of moves7. Production order c g. Maintenance hours 8. Engineering b h. Direct labour hours

Identify the most likely cost- driver basefor each activity:

Identify the most likely cost- driver basefor each activity:

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-45

Selecting Cost Driver Bases

An appropriate costdriver base should:

An appropriate costdriver base should:

Have a cause-effect relationship with the activityand the use of resources (costs).

Have a cause-effect relationship with the activityand the use of resources (costs).

Be feasible to measureBe feasible to measure

Predict or explain activities’ use of resources(cost) with reasonable accuracy

Predict or explain activities’ use of resources(cost) with reasonable accuracy

Be based on the practical capacity of theresources to support activities

Be based on the practical capacity of theresources to support activities

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-46

Unit Batch Product Customer Facility

Materials none EquipmentWarehousing

personneland equpment

PersonnelFacilities

Resource Level

Resource Name

Resource Cost-DriverBase(s)

Number of units by type

Product type Customer

type

Time(hours), Product parts, Customer orders, Newproducts, Change orders, Employee, Headcount

Stage 1: Cost-driver Bases ForTracing Costs To Activities At PMI

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-47

Measuring resource costs of activities Measuring resource costs of activities

Tracing use of resources to activities allowsorganizations to accurately measure the costs of the

resources used in the various elements of workperformed by its employees and caused by its

processes.

Tracing use of resources to activities allowsorganizations to accurately measure the costs of the

resources used in the various elements of workperformed by its employees and caused by its

processes.

ChangeProcesses

AddProducts

DropCustomers

This information allows analysts to accurately predictresource demands and the costs or cost savings of

changing activities

This information allows analysts to accurately predictresource demands and the costs or cost savings of

changing activities

Stage 1: Measuring The Cost OfActivities

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-48

Tracing resource costs to activities at PMITracing resource costs to activities at PMI

MargaretSmythe’sresourcesand costs

1.2 Advertising and Promotion1.3 Sales1.5 Ordering Processing3.4 Design products for manufacturability

3.7.1 Manage manufacturing costs and quality5.1 Process customer change orders5.2 Resolve customer problems with orders5.3 Expedite customer orders5.4 Follow up with customers6.1 Management meetings

STEP TWO:Employees were asked toindicate how much time

they worked on eachactivity

STEP TWO:Employees were asked toindicate how much time

they worked on eachactivity

STEP ONE:Physical resources that

support variousactivities were identified

STEP ONE:Physical resources that

support variousactivities were identified

Stage 1: Measuring The Cost OfActivities

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-49

Computing the cost of activitiesComputing the cost of activities

1.2 Advertising and Promotion1.3 Sales1.5 Ordering Processing3.4 Design products for manufacturability

3.7.1 Manage manufacturing costs and quality5.1 Process customer change orders5.2 Resolve customer problems with orders5.3 Expedite customer orders5.4 Follow up with customers6.1 Management meetings

Productionteam’s

resourcesand costs

Productionteam’s

resourcesand costs

Stage 1: Measuring The Cost OfActivities

Accumulate costs of resourcesused by each activity acrossemployees, departments, and

functions

Accumulate costs of resourcesused by each activity acrossemployees, departments, and

functions

Sum the costs ofeach resource

used by activity

Sum the costs ofeach resource

used by activity

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-50

Measuring Stage 2 Cost DriverRates

Computing the cost of activitiesComputing the cost of activities

Cost of Activity 3.4: Design Products for ManufacturabilityCost of Activity 3.4: Design Products for Manufacturability

Resource Cost per hourTime spent per week

Activity cost per

week

Margaret Smyth $20.00/hr 1 hour $20.00Production Team-ABurton $20.00/hr 1 hour $20.00Kowalski $12.00/hr 0.5 hour $6.00Total cost from these resources $46.00

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-51

If higher-level resources are both necessary andused for lower-level activities, should the costs used from higher-level resource be counted as the costs

of the lower-level activities?

no

Measure the cost of activitiesas the amount of spending forresources acquired to perform

these activities

Advocatesof throughputand unit level

costing . . .

You would not identify all theresources used by the lower-

level activities

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-52

If higher-level resources are both necessary andused for lower-level activities, should the costs used from higher-level resource be counted as the costs

of the lower-level activities?

no

Measure the cost of activitiesas the amount of spending forresources acquired to perform

these activities

Measure the cost of activitiesas the amount of spending forresources acquired to perform

these activities

Advocatesof throughputand unit level

costing . . .

You would not identify all theresources used by the lower-

level activities

You would not identify all theresources used by the lower-

level activities

yes

Count higher level costs aspart of lower-level activities

Count higher level costs aspart of lower-level activities

Advocatesof absorption

(or full)costing . . .

You average higher-levelresources over lower-

level activities

You average higher-levelresources over lower-

level activities

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-53Measuring Stage 2 Cost DriverRates

Condensing the Activity ListCondensing the Activity List

For product costing purposesFor product costing purposes

Fewer categories ofactivities allow analyststo assign product cost

more easily in the secondstage-tracing costs toproducts and services

Fewer categories ofactivities allow analyststo assign product cost

more easily in the secondstage-tracing costs toproducts and services

Condense the activityCondense the activity

Simplifies internalcommunications

Simplifies internalcommunications

Reduces the amount ofinformation needed

Reduces the amount ofinformation needed

Use the same costdriver for both

stages of analysis

Use the same costdriver for both

stages of analysis

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-54

Measuring Stage 2 Cost DriverRates

Tracing of Costs to Products and ServicesTracing of Costs to Products and Services

ABC unit level costing ABC full-costing

Assigns as many coststo products and

services as possible,regardless of the levelof the resource, based

on the use of resources

Assigns as many coststo products and

services as possible,regardless of the levelof the resource, based

on the use of resources

Traces only the costs ofunit-level

resources suppliedand used to

products and services

Traces only the costs ofunit-level

resources suppliedand used to

products and services

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-55

Measuring Stage 2 Cost DriverRates

Tracing of Costs to Products and ServicesTracing of Costs to Products and Services

Beveragecontainer

Babycareproduct

ABC unit level costing

$0.73

Unit levelcost=$0.73

ABCfull-costing

$2.40

Unit levelcost=$0.73

Difference=higher-levelcost=$1.67

ABC unit level costing

15.78

Unit levelcost=$15.78

ABCfull-costing

$31.13

Difference=higher-levelcost=$15.35

Unit levelcost=$15.78

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-56

Tracing of Costs to Products andServices

Tracing of Costs to Products andServices

Compute: unit-level and full-ABC costs per unit.Direct material : $10,000 / 5,000 units = $2 per unit Labour used: $5,000/ 5,000 units = $1 per unitBatch setup costs and materials: $500 per batch X 2batches = $1,000.Facility level equipment used: $20,000 per product.Special shipping for customers: $100 per order X10 orders = $1,000.Manufacturing scheduling: $250 per employee X 4employees = $1,000.

Compute: unit-level and full-ABC costs per unit.Direct material : $10,000 / 5,000 units = $2 per unit Labour used: $5,000/ 5,000 units = $1 per unitBatch setup costs and materials: $500 per batch X 2batches = $1,000.Facility level equipment used: $20,000 per product.Special shipping for customers: $100 per order X10 orders = $1,000.Manufacturing scheduling: $250 per employee X 4employees = $1,000.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-57

ABC unit level costing

Compute: unit-level ABC costs per unit.

Direct material : $10,000 / 5,000 units = $2.00 Labour used: $5,000/ 5,000 units = $1.00

Cost per unit = $3.00

Compute: unit-level ABC costs per unit.

Direct material : $10,000 / 5,000 units = $2.00 Labour used: $5,000/ 5,000 units = $1.00

Cost per unit = $3.00

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-58

ABC full-costingCompute: full-ABC costs per unitDirect material : $10,000 / 5,000 units = $2 per unit Labour used: $5,000/ 5,000 units = $1 per unit

$3 unit levelBatch setup costs and materials:$500 per batch X 2 batches = $1,000.Facility level equipment used per product = $20,000Special shipping for customers: $100 per order X 10 orders = $1,000.Manufacturing scheduling: $250 per employee X 4 employees = $1,000.

$23,000/5,000 units = $4.60 per unit full-ABC costs per unit = $7.60 per unit

Compute: full-ABC costs per unitDirect material : $10,000 / 5,000 units = $2 per unit Labour used: $5,000/ 5,000 units = $1 per unit

$3 unit levelBatch setup costs and materials:$500 per batch X 2 batches = $1,000.Facility level equipment used per product = $20,000Special shipping for customers: $100 per order X 10 orders = $1,000.Manufacturing scheduling: $250 per employee X 4 employees = $1,000.

$23,000/5,000 units = $4.60 per unit full-ABC costs per unit = $7.60 per unit

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-59

Measuring Stage 2 Cost DriverRates

Product ProfitabilityProduct Profitability

Product profitability

Product profitability

IProfit calculatedusing ABC unit-

level costs

IIProfit calculatedusing ABC full

costing

Difference = classification ofresource costs and information

generated

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-60

Measuring Stage 2 Cost DriverRates

Product and Customer ProfitabilityProduct and Customer Profitability

CustomerProfitability

CustomerCosting

Analysis of the costs ofactivities at each level

devoted to serving specific customers

Combines customer costing with revenues earned from customers

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-61

Measuring Stage 2 Cost DriverRates

Estimating the costs of new products using ABCEstimating the costs of new products using ABC

ABC can be used for estimating the costs of newproducts and services if processes and activities

to make them are similar

The major benefit of using ABC for estimating the costs of new product and services is that it provides a

template for identifying and measuring relevant costsat all levels

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

1-62

End of

Chapter

55