the darker side of securitization: how subprime...

TRANSCRIPT

The Darker Side of Securitization: The Darker Side of Securitization: How Subprime Lending Led to a Systemic Crisis

Richard J. Herring

The Wharton Finance Club

The Wharton School, University of Pennsylvania

April 21, 2008

OverviewOverviewFinancial Alchemy: How subprime mortgages were transformed into investment grade debt

The alphabet soup of securitization

Wh What went wrong

Why it became a systemic threat

P li i Policy issues re:AccountingThe Ratings AgenciesThe Ratings AgenciesBasel I & II

Is the worst over?

Traditional Lending: Buy & HoldTraditional Lending: Buy & HoldBank originates loangBank underwrites loanB k f d lBank funds loanBank services loanBank holds loan on b/s until repaidPerforms workout if necessaryPerforms workout if necessary

New Model: Originate & DistributeNew Model: Originate & DistributeBank may originate (but so may another entity)y g y y

Bank may underwrite (but so may another entity)

Bank may assess credit risk and/or rating agencyBank may assess credit risk and/or rating agency

Bank may fund or may sell to a Trust

B k h ld b & ll iti d Bank may hold or may buy & sell a securitized tranche

k b hBank may service (but so may another entity)

If a workout is necessary, what happens?

SecuritizationSecuritizationDefinition: “Packaging and selling of loans and other assets backed by securities”Rationale: the sum of the properly packaged parts is worth more than the wholeAdvantages to banksAdvantages to banks

Risk management flexibilityInterest rateLiquidityLiquidityCredit risk

FeesR d ti f it l i t i t d Reduction of capital requirements, reserve requirements and deposit insurance premiums

Advantages to borrowersLower costWider range of options

Securitizations Began with the GSEsGSEs

Securitization of residential mortgages g gImproved transparencyEnhanced diversificationIncreased liquidityLowered costsPermitted banks to use capital more efficiently, in an originate and distribute approach

Relied on guarantees from GSEs

Private Securitizations Replaced GSE guarantee with1. Ratings2. Statistical models to support credit tranching3. Monoline insurance

Alphabet soup of innovationsAlphabet soup of innovationsRMBSCDOs, CDO2,ABCPSIVsCLOs

Became an off-balance sheet banking systemLost transparency of original model

Real Housing Prices, 1975-2007Source: U.S. Office of Housing Enterprise Oversight

180

g p g

160

100

140

dex

197

5=1

100

120Ind

80

Technique applied even to nonprime mortgagesnonprime mortgages

Subprime: mortgages to borrowers with weakCredit historiesCredit scores (repayment capacity)Or incomplete credit historiesOr incomplete credit histories

Low doc loans

No doc loans

Liar loans

Alt-A: mortgages to borrowers w. non-standard features re: Borrower Borrower, Property or Loan

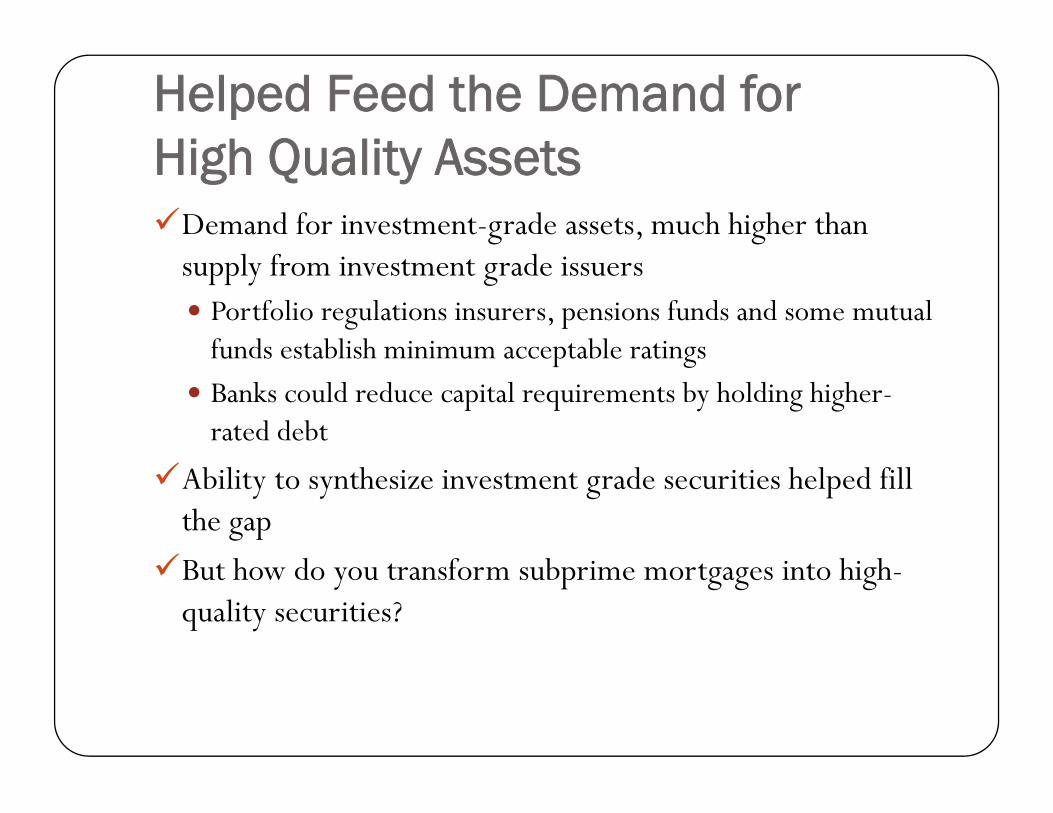

Helped Feed the Demand for High Quality AssetsHigh Quality Assets

Demand for investment-grade assets, much higher than supply from investment grade issuers

Portfolio regulations insurers, pensions funds and some mutual funds establish minimum acceptable ratingsfunds establish minimum acceptable ratingsBanks could reduce capital requirements by holding higher-rated debt

Ability to synthesize investment grade securities helped fill the gap

B h d f b h hBut how do you transform subprime mortgages into high-quality securities?

Where Did the Subprime Go? 2From to RMBS to CDO to CDO2 to ABCP & SIVs

Subprime loan originatedInitially funded by warehouse lines of credit to mortgage brokers (about 90 days)H ld b i fl l d ’ b/ til d h Held briefly on lender s b/s until seasoned, shows statistically predictable performanceSold to SPV and securitized as RMBSSo to S V a secu t e as S

Equity and risky debt may be difficult to sell

Resecuritize equity and risk debt in CDOsEquity and risky debt may still be difficult to sell

May securitize equity and risky debt tranches of CDO in CDO2CDOOr may be purchased and pooled for ABCP

How CDOs Helped Transform Subprime Mortgage into AAA CreditsSubprime Mortgage into AAA Credits

Source: IMF Global Financial Stability Report (IMFGFSR), 4/08, Box 2.2.,p. 60

Conduits, SIVs & SIV-Lites,

Source: IMFGFSR, 4/08, p. 71

Credit EnhancementsCredit EnhancementsExcess servicingOver‐collateralizationSubordination and residual tranchingSubordination and residual tranchingPerformance triggersM li iMonoline insuranceCredit Default Swaps• CDOs are Synthetic if backed by CDSs

Very Rapid Growth in Issuance of Structured CreditStructured Credit

I i liIncreasing reliance onCDOs2000: $150 billion2007: $1.2 trillion$

Source: IMFGFSR, 4/08, Box 2.1, p. 56.

Became a dominant source of revenue for most LCFIs revenue for most LCFIs Growth in Trading Profits, Commissions & Fees Largely Reflects Growth in Structured Credits

Source: Bank of England Financial Stability Review, October 2007, p. 38.

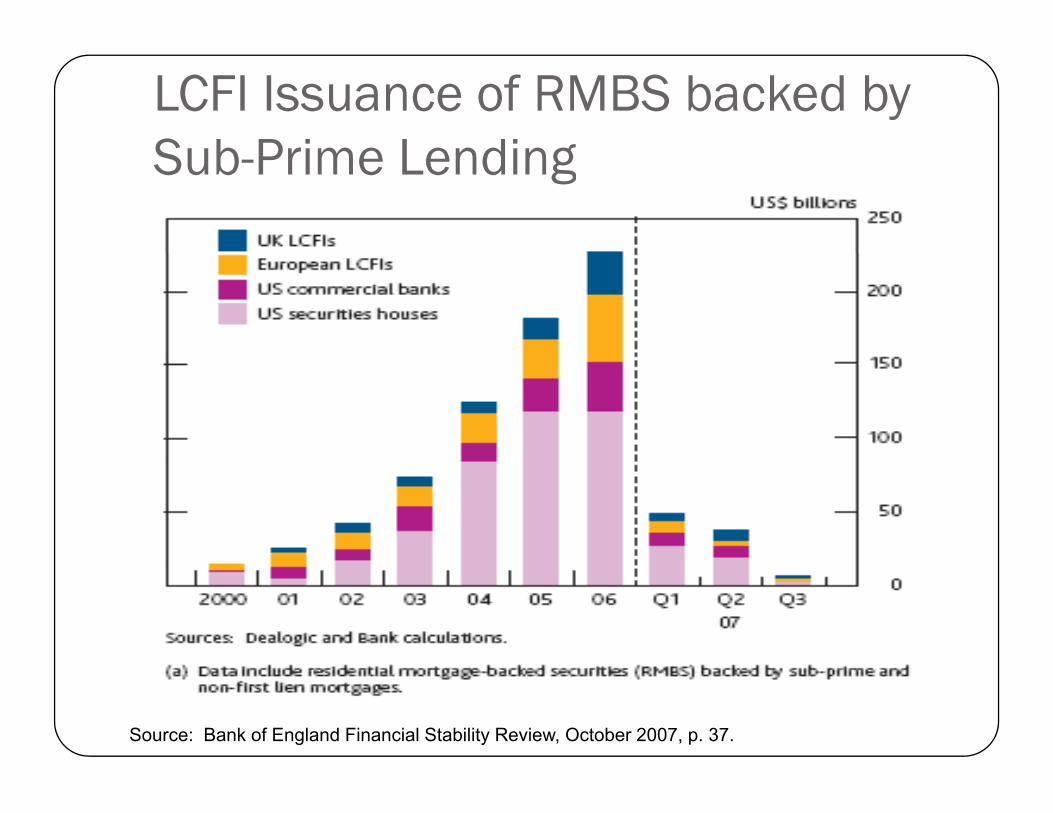

LCFI Issuance of RMBS backed by Sub Prime LendingSub-Prime Lending

Source: Bank of England Financial Stability Review, October 2007, p. 37.

Deterioration in Subprimes Raised Alarm60-Day Delinquencies by Mortgage Vintage Year (in % of Original Balance)

Months after origination

Source: IMF Global Financial Stability Review, April 2008, p. 6

1. Predatory lending: Subprime borrowers can be financially

7 Pitfalls in Subprime Mortgage Credit Securitization

be financially unsophisticated – either unaware of all options available or unable to make the best choice between options.

MORTGAGOR

WAREHOUSE

4. Moral hazard: In order to maintain the value of the underlying asset (the house), the mortgagor has to pay insurance and maintain the property. In, or

ORIGINATOR

ARRANGER

WAREHOUSE LENDER

CREDIT RATING

2. Mortgage fraud: The originator, who sells a pool of mortgages to the arranger, has an information advantage

approaching delinquency, there is little incentive to do this.

ARRANGER CREDIT RATING AGENCY

ASSET MANAGER

SERVICER

over the arranger regarding quality of the borrower. An originator, collaborating with the borrower, may misrepresent the information on the

3. Adverse selection: The ASSET MANAGERinformation on the

application.arranger has more information about the quality of the mortgage loans – so, the arranger can choose to securitize the bad loans and retain the good ones.

5. Moral hazard: Given that the servicer’s income increases the longer the loan is serviced, keeping the loan on its books for as long as possible is preferred – therefore, it has a

f t dif th t f

INVESTOR6. Principal‐agent: While the investor provides funding for the mortgage‐backed security, the asset manager conducts the due diligence on the investments and finds the best price for

7. Model error: The rating agencies are paid by the arranger and not

preference to modify the terms of a delinquent loan to delay foreclosure.

the investments and finds the best price forthe trades – the asset manager may not take sufficient effort on behalf of the investor.

are paid by the arranger and not investors for their opinion. Their rating relies on models, which are susceptible to errors.

Source: Ashcraft and Schuermann (2007): “Understanding the Securitization of Subprime Mortgage Credit”

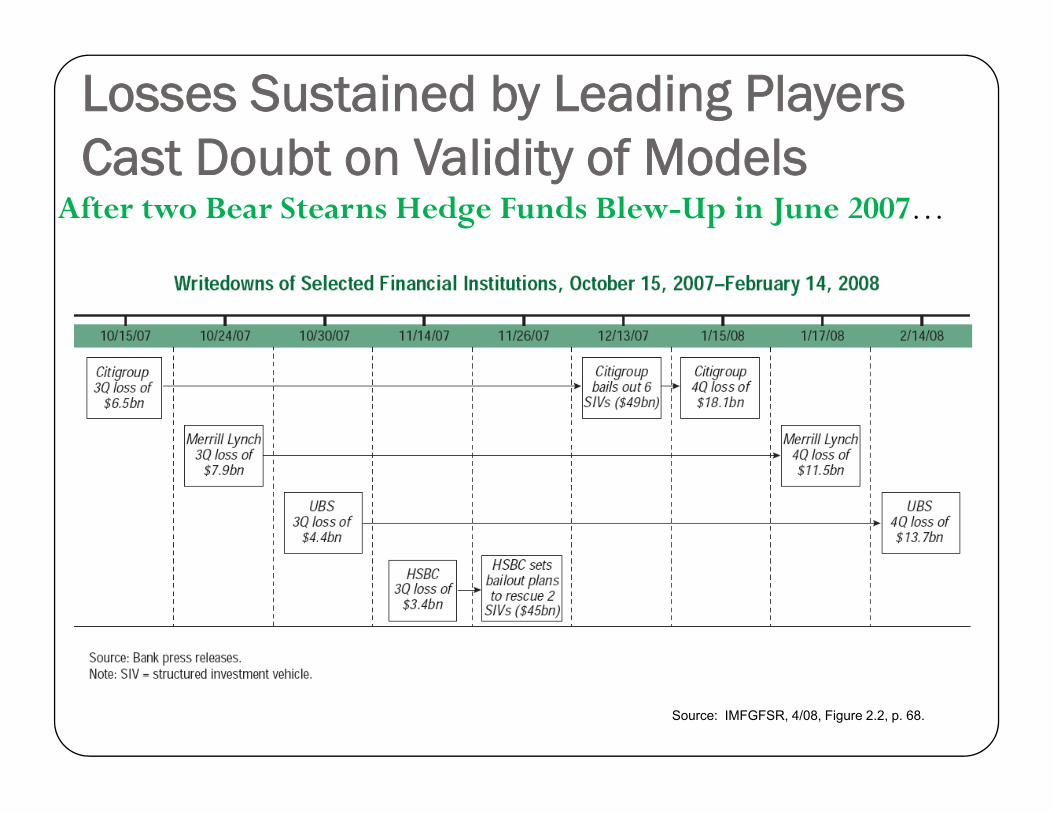

Losses Sustained by Leading Players Cast Doubt on Validity of ModelsCast Doubt on Validity of Models

After two Bear Stearns Hedge Funds Blew-Up in June 2007…

Source: IMFGFSR, 4/08, Figure 2.2, p. 68.

Multi-Notch Downgrades Undermined Confidence in RatingsUndermined Confidence in Ratings

68%

47% on Credit Watch*

*As of 1/31/08 Source: IMFGFSR, 4/08, Box 2.3, p. 61.

CDS Market Took an Even More Pessimistic View Pessimistic View

Source: IMFGFSR, 4/08, Figure 1.3, p. 7.

Losses Threatened Solvency of Monoline InsurersMonoline InsurersAt yearend 2006 Monoline insurers supported about $800 bn in structured finance obligations

Source: IMFGFSR, 4/08, Figure 1.14, p.17.

The Damage Spread RapidlyThe Damage Spread RapidlyLosses undermined 3 main supports for private sector securitization1. Ratings2 Statistical models2. Statistical models3. Monoline insurers

Sharp decline in risk appetitep pp

Concerns about solvency of systemically important firms

Flight to simplicityg p y

Flight to quality

Pressures to deleverage financial systemg y

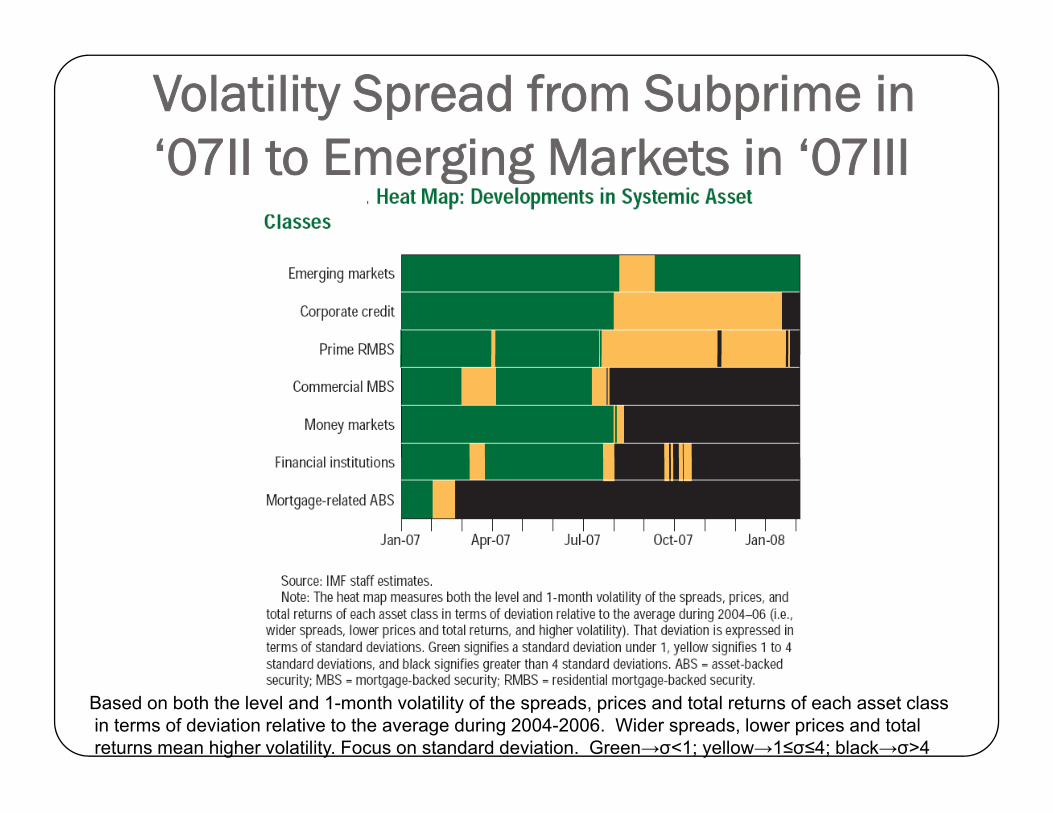

Volatility Spread from Subprime in ‘07II to Emerging Markets in ‘07III‘07II to Emerging Markets in ‘07III

Based on both the level and 1-month volatility of the spreads, prices and total returns of each asset classin terms of deviation relative to the average during 2004-2006. Wider spreads, lower prices and totalreturns mean higher volatility. Focus on standard deviation. Green→σ<1; yellow→1≤σ≤4; black→σ>4

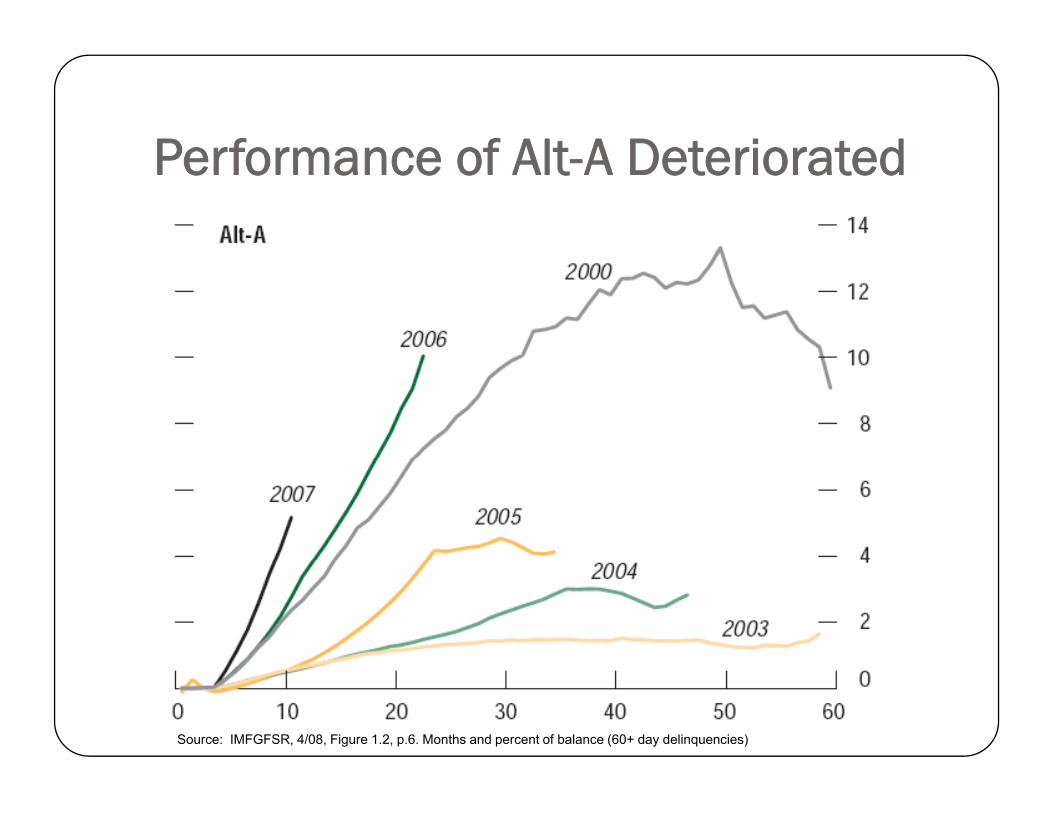

Performance of Alt A DeterioratedPerformance of Alt-A Deteriorated

Source: IMFGFSR, 4/08, Figure 1.2, p.6. Months and percent of balance (60+ day delinquencies)

As Did Performance of Non-Agency Prime (Jumbo)Prime (Jumbo)

Source: IMFGFSR, 4/08, Figure 1.2, p.6.

Looming Resets in 2008Looming Resets in 2008$250 bn of Subprime Mortgages scheduled to g greset

$29 bn of Alt-A Mortgages scheduled to reset$ g g

$82 bn in Prime Mortgages to reset

Most ARMs have floors and caps thus further Most ARMs have floors and caps, thus further monetary easing may not help

R fi i ill b diffi ltRefinancing will be difficultTighter underwriting standardsFixed rates still elevated

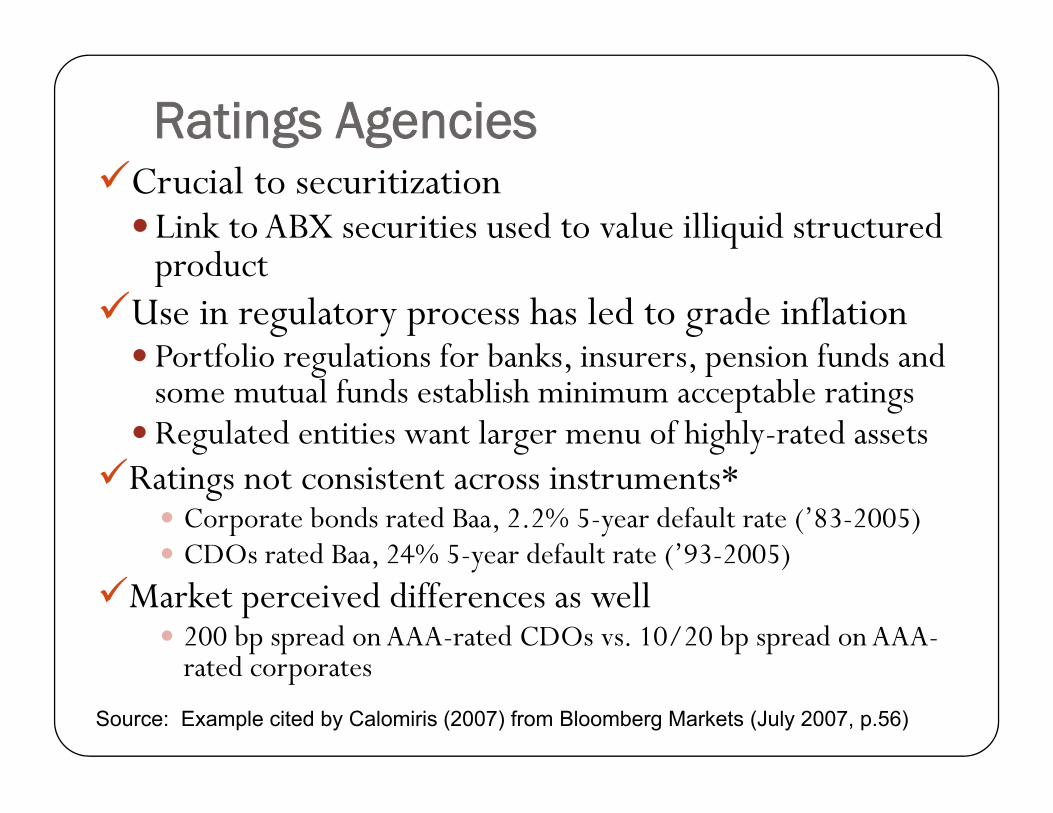

Policy Issues: Role of Ratings AgenciesAgencies

Ratings AgenciesCrucial to securitization

Link to ABX securities used to value illiquid structured dproduct

Use in regulatory process has led to grade inflationPortfolio regulations for banks insurers pension funds and Portfolio regulations for banks, insurers, pension funds and some mutual funds establish minimum acceptable ratingsRegulated entities want larger menu of highly-rated assets

Ratings not consistent across instruments*Corporate bonds rated Baa, 2.2% 5-year default rate (’83-2005)CDOs rated Baa 24% 5-year default rate (’93-2005)CDOs rated Baa, 24% 5 year default rate ( 93 2005)

Market perceived differences as well200 bp spread on AAA-rated CDOs vs. 10/20 bp spread on AAA-

t d trated corporates

Source: Example cited by Calomiris (2007) from Bloomberg Markets (July 2007, p.56)

Market Perceived Differences As WellMarket Perceived Differences As Well

Source: IMFGFSR, 4/08, Box 2.3, p.62.

IMF highlighted 3 Flaws in MethodologyMethodology1. Underestimated PDs and LGDs2. Underestimated correlations3. Underestimated speed with which

f d t i t d d it f lperformance deteriorated and severity of lossVery slow to react to evidence of rising delinquencies in rating new issuesq g

Ratings of ABS CDOs based on default probabilities and loss severities associated with

d ABS h h d l rated ABS rather than underlying mortgages• CDO rating may be delayed for downgrade of ABS

and analysis of complex cash flow dynamicsy p y• Downgrades of ABS tend to compound

Undermined CredibilityUndermined CredibilityOld questions about conflicts of interest heightened

Played active role in facilitating origination of d dstructured products

Revenue from securitizations accounts for hl h lf f i ’ froughly half of agencies’ fees

Ratings slow to reflect deterioration in d l i l f i iunderlying pools of securities

Past errors individual corporates or sovereigns, t ti b d t lnot an entire, broad asset class

Would investors be better servedWould investors be better served…By disclosures of actual PDs and LGDs for yeach issue rather than letter grades?By different scales for structured credits?yBy additional ratings for market, liquidity, and downgrade risk?and downgrade risk?By regulations that do not delegate judgments to the ratings agencies?judgments to the ratings agencies?

Policy Issues: Valuation of illiquid securitiessecurities

Most CDOs held as “Available for sale”

Source: IMF Global Financial Stability Report, April 2008, p. 65

Auditors require evidence thatAuditors require evidence that…Sale price is not indicative of fair value before accepting a reclassification from level 2 to level 3

Forced sale by liquidator may not be indicativey q ySimilar sale by solvent entity may be indicative

Meant to discourage “cherry picking” of Meant to discourage cherry picking of valuations

Post SOX auditors may be very cautiousPost-SOX, auditors may be very cautious

Source: IMF Global Financial Stability Review, April 2008, p. 66.

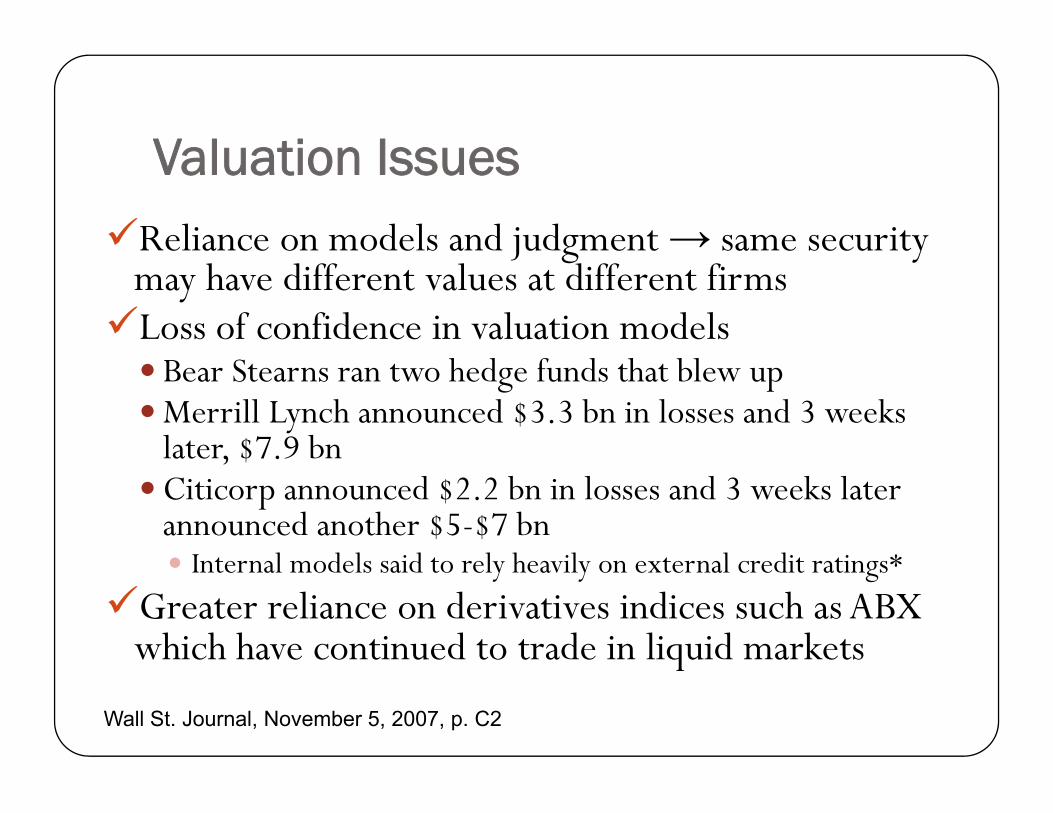

Valuation IssuesValuation IssuesReliance on models and judgment → same security j g ymay have different values at different firmsLoss of confidence in valuation models

Bear Stearns ran two hedge funds that blew upMerrill Lynch announced $3.3 bn in losses and 3 weeks later, $7.9 bnlater, $7.9 bnCiticorp announced $2.2 bn in losses and 3 weeks later announced another $5-$7 bn

I t l d l id t l h il t l dit ti *Internal models said to rely heavily on external credit ratings*

Greater reliance on derivatives indices such as ABX which have continued to trade in liquid markets q

Wall St. Journal, November 5, 2007, p. C2

Fears that Fair Value Accounting May Contribute to CrisisMay Contribute to Crisis

Fair values intended to represent exit valuepIf markets overshoot, so will fair values

If f i l t i t l If fair values trigger asset sales, may contribute to further downward pressure on pricesCould exacerbate downward liquidity spiralq y p

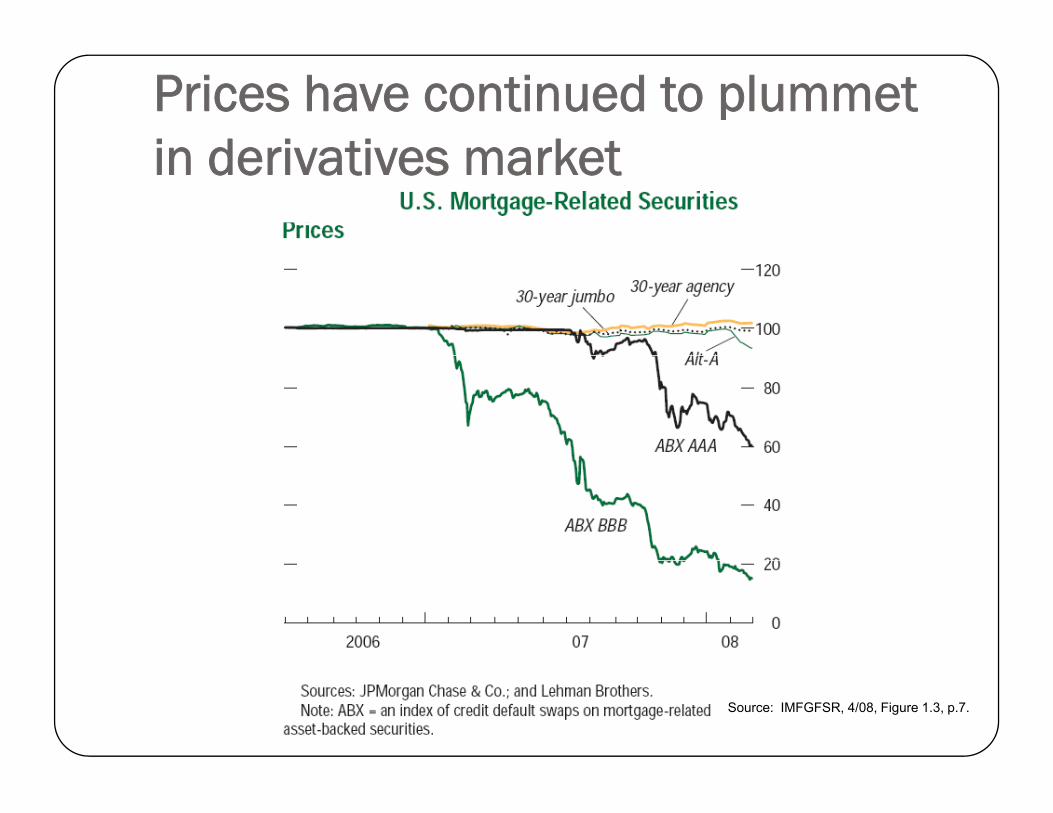

Prices have continued to plummet in derivatives market in derivatives market

Source: IMFGFSR, 4/08, Figure 1.3, p.7.

Spreads Continue to Widen on CMBSCMBS

Source: IMFGFSR, 4/08, Figure 1.7, p.9.

As Do Spreads on Leveraged LoansAs Do Spreads on Leveraged LoansSome banks have retained rather than accept loss

As CLOs unwind As CLOs unwind, may be forced to take more leveraged loans on b/s

Source: IMFGFSR, 4/08, Figure 1.10, p.10.

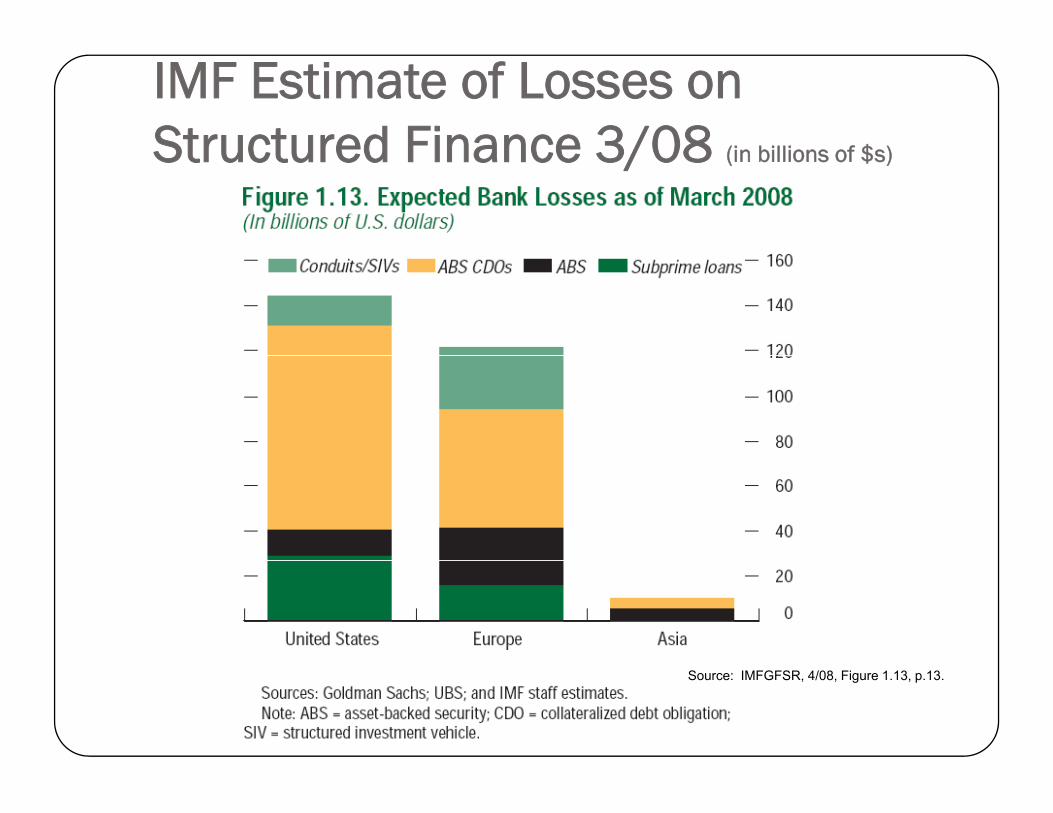

IMF Estimate of Losses on Structured Finance 3/08 (in billions of $s)Structured Finance 3/08 (in billions of $s)

Source: IMFGFSR, 4/08, Figure 1.13, p.13.

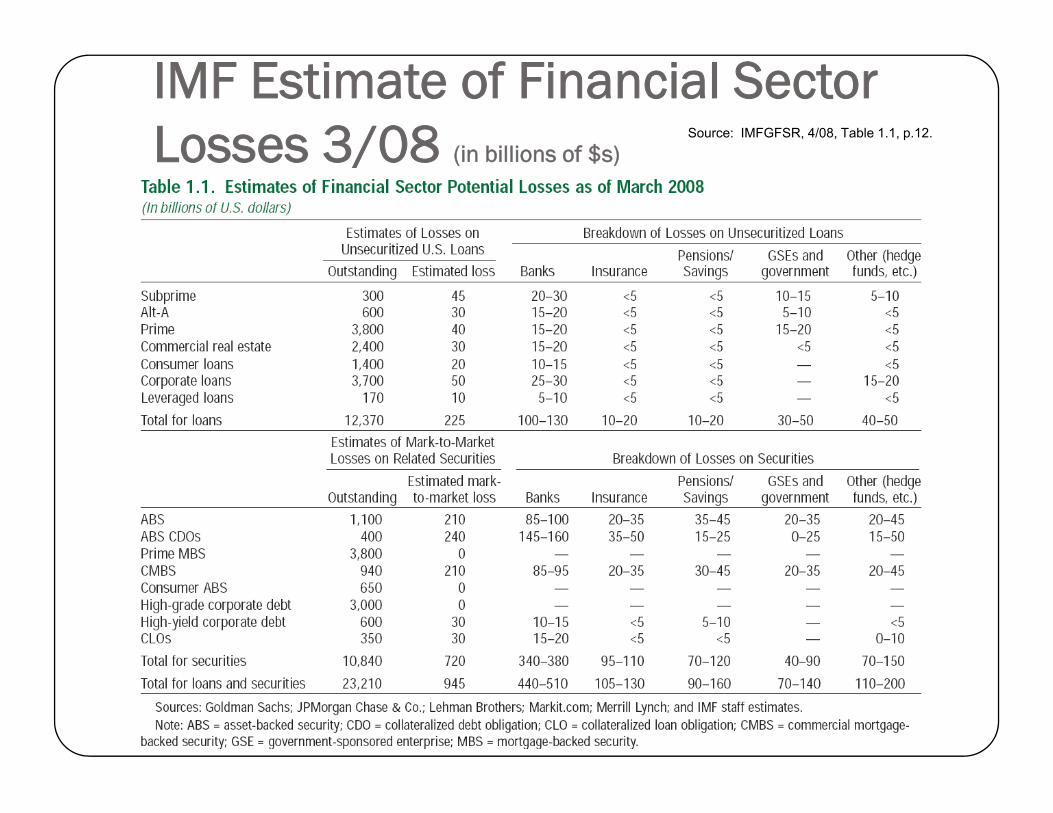

IMF Estimate of Financial Sector Losses 3/08 (in billions of $s)

Source: IMFGFSR, 4/08, Table 1.1, p.12. Losses 3/08 (in billions of $s)

Policy Issues: Adequacy of DisclosureDisclosure

The SEC & DisclosureThe SEC & DisclosureExamined mortgage-related markets 4 times between 1998 & 2007, but found no significant concerns re: transparency

R l i AB i ll l l l f Regulation AB requires collateral-level performance reports, but allowed issuers to choose how to disclose – Most chose to disclose only to First American Loan – Most chose to disclose only to First American Loan Performance

Neither GAAP nor IFRS require instrument specific Neither GAAP nor IFRS require instrument specific disclosures

Opaque Mitigation PracticesOpaque Mitigation PracticesTypical foreclosure costs are $60k and likely to increase as home prices ddecrease* Servicers use loan modifications to avoid classifying loans in default

Post-modification default rate still 35-40% higher than non-modified loans

“Re-aging” policy varies across servicersSome reclassify loan as performer as soon as 1 modified payment is madeOthers require several consecutive payments

Practices mask true condition of subprime loans as they deteriorate and overstates performance of pool

Tends to favor riskier tranchesI d f i i l f h fl b di d Improved performance ratios trigger release of cash flows to subordinated tranches

*Source: Joe Mason, “Mortgage Loan Modifications: Promises & Pitfalls,” October, 2007

Variations in disclosure across countriescountries

SEC requires quarterly disclosure

Europe less prescriptive

CFO can exercise “professional judgment” about scale and timing of loss recognitions

Same asset may be valued differently in different institutions

Piecemeal release of increasingly larger losses raises b concerns about

Integrity of financial reportingM t’ f it i k Management’s grasp of its risk exposures

Uncertainty & Lack of InformationUncertainty & Lack of Information

L k f l it b t h th i k id Lack of clarity about where these risks now reside overhangs markets

Financial institutions are subject to an increasing opacity j g p ydiscountSkepticism re: assertions that

‘Our exposures are highly rated” or Our exposures are highly rated or “We have offsetting hedges” or “We have a rigorous risk management process”

A t d ti l i f ti iti l f th Accurate and timely information are critical for the market to differentiate among borrowers and price risk

Banks Pay an Opacity Premium

LIBOR spread over T-Bills from 5/1/07-4/1/08

200

250

150

s Po

ints

50

100

Bas

i

0

Date

Policy Issues: Basel IPolicy Issues: Basel I

Basel I Created Strong Incentives to Securitizeto Securitize

On b/s mortgage had 50% risk weightg g g

Off b/s line of credit had 0% risk weight if less than 1 yeary

Capital requirement against CP less than against mortgagemortgage

Provides strong incentive to fund rather than dissolve ABCP Conduits

Basel I Did not Constrain Growth in Assets or Address Liquidity RiskAssets or Address Liquidity Risk

Source: IMFGFSR, 4/08, Box 1.3, p.31.

Policy Issues: Basel IIPolicy Issues: Basel II

Would Basel II have prevented problems?problems?

SIVs would still have been off/b/sMust only meet accounting criteria

Would require some capital for back-up facilities of 364 days lor lessUS already implemented such a rule in 2004 and did not restrain Citi

More than 3x as much exposure as Bank of America & JP Morgan Chase combined**Exposure to subprime varied from actual loans to most highly-rated slices of CDOsof CDOsSponsored 7 SIVs

**Call report data, 6/30/07, Outstanding principal balance of residential loans sold and securitized with servicing retained or with recourse or seller-provided credit enhancement: BofA = $73 6bnwith servicing retained, or with recourse, or seller-provided credit enhancement: BofA = $73.6bn, JPMorgan Chase: $80.5 bn, Citibank: $584.9 bn. See Calomiris (2007)

When is off b/s really off b/s?When is off b/s really off b/s?Legal and accounting standards may not be sufficient for prudential purposes

Reputational risk may overrideM f l bli t d t t l ll t d titi fi i ll t May feel obligated to support legally-separated entities financially to maintain reputation in market – SIVs, conduits, money market mutual funds, hedge funds

N i & i i New instruments & structures may contain contingent liabilities

Under what circumstance might it be necessary to extend Under what circumstance might it be necessary to extend support to separate asset management companies, SPVs and conduits?

Basel IIBasel IIStandardized Approach relies heavily on external ratings

If agencies get it wrong for entire categories of securities, a new source of systemic risk

Internal Ratings Based Approaches rely on internal te a at gs ase pp oac es e y o te a models

But even the most sophisticated players have found their i t l d l li blinternal models unreliable

Basel II does not impose a capital charge for reputational risk

Paulson has called for a review of treatment of off-b/s vehiclesOthers believe Pillar 2 is sufficient

h f h l l f l hWe may have a test of the pro-cyclicality of Basel II much sooner than anyone expected

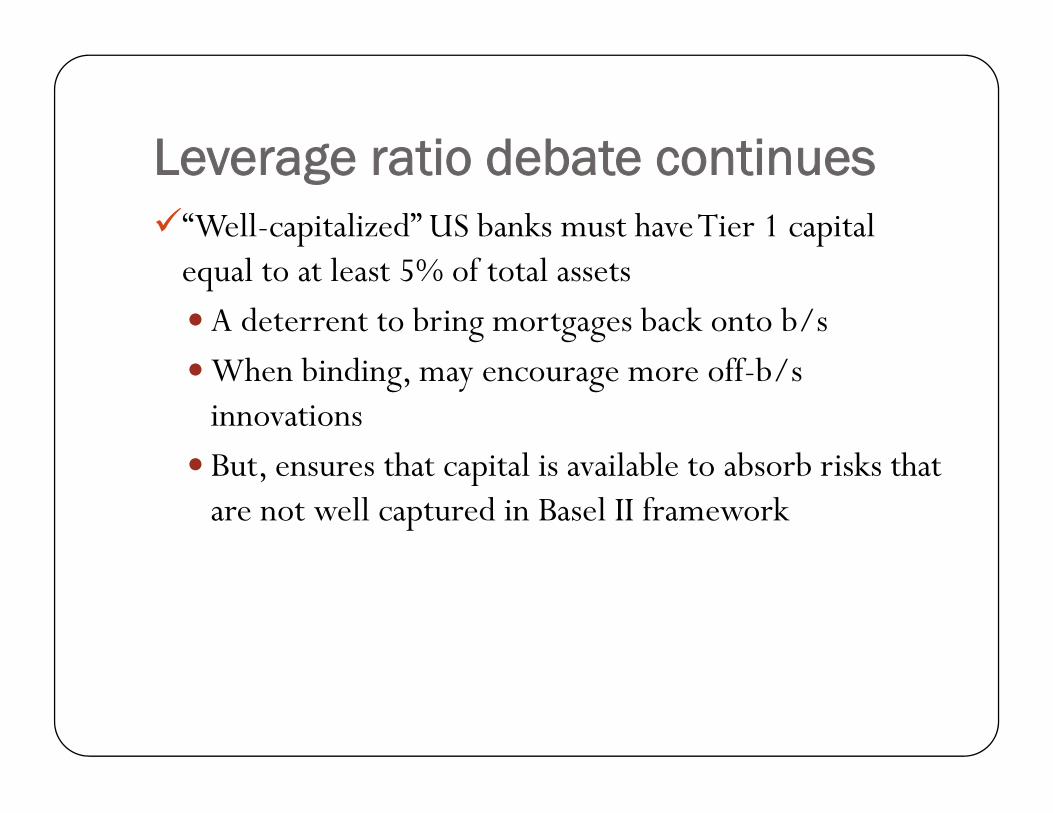

Leverage ratio debate continuesLeverage ratio debate continues“Well-capitalized” US banks must have Tier 1 capital equal to at least 5% of total assets

A deterrent to bring mortgages back onto b/sWhen binding, may encourage more off-b/s innovationsB t th t it l i il bl t b b i k th t But, ensures that capital is available to absorb risks that are not well captured in Basel II framework

How Big is the Crisis?How Big is the Crisis?

IMF Comparison with Past CrisesIMF Comparison with Past Crises

Source: IMFGFSR, 4/08, Figure 1.12, p.13.

Financial Policy OptionsFinancial Policy Options

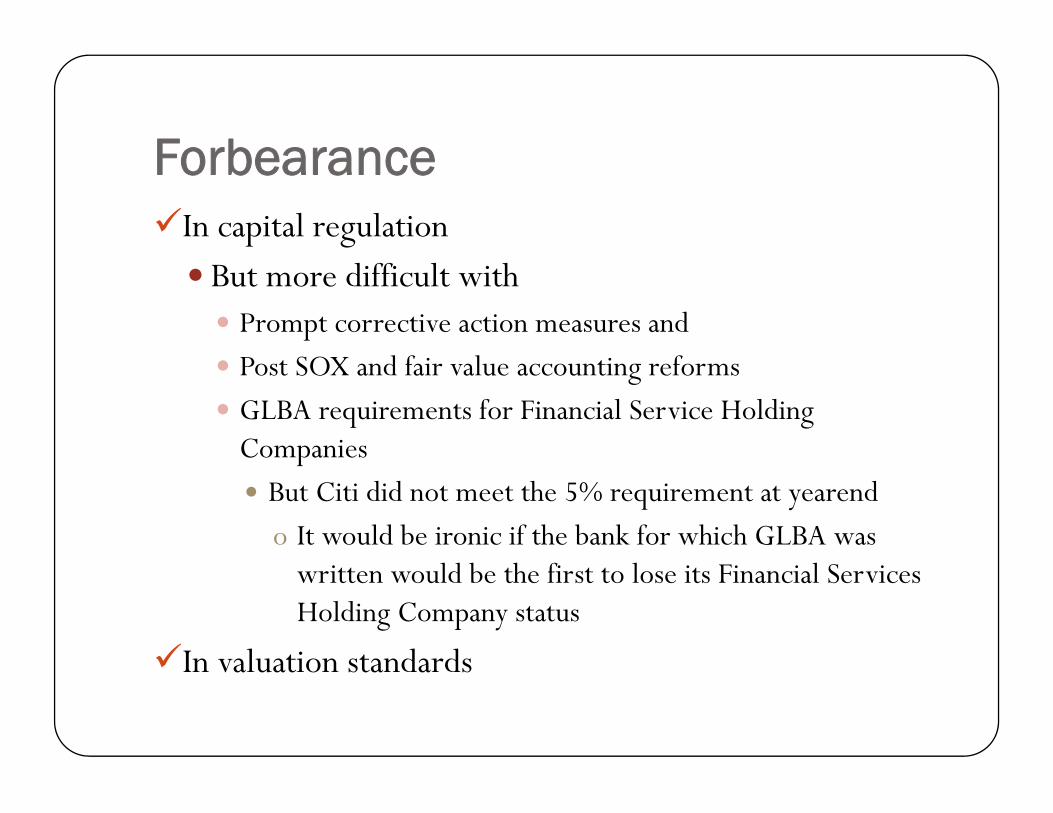

ForbearanceForbearanceIn capital regulation

But more difficult with Prompt corrective action measures and

d f l fPost SOX and fair value accounting reformsGLBA requirements for Financial Service Holding Companiesp

But Citi did not meet the 5% requirement at yearendo It would be ironic if the bank for which GLBA was

written would be the first to lose its Financial Services Holding Company status

In valuation standardsIn valuation standards

Provide liquidityProvide liquidityMonetary policy

Insure aggregate liquidity is sufficientAdjust monetary policy to compensate for crisis-induced credit crunchcrunch

Swap high-quality liquid assets for risky securitiesBroadened access at discount windowTerm auction facilitiesWarehouse $30 bn of Bear Stearn’s assets

Major Concern: Increase rate of inflation to relieve burden on debtors and stop the d li i h i idecline in housing prices

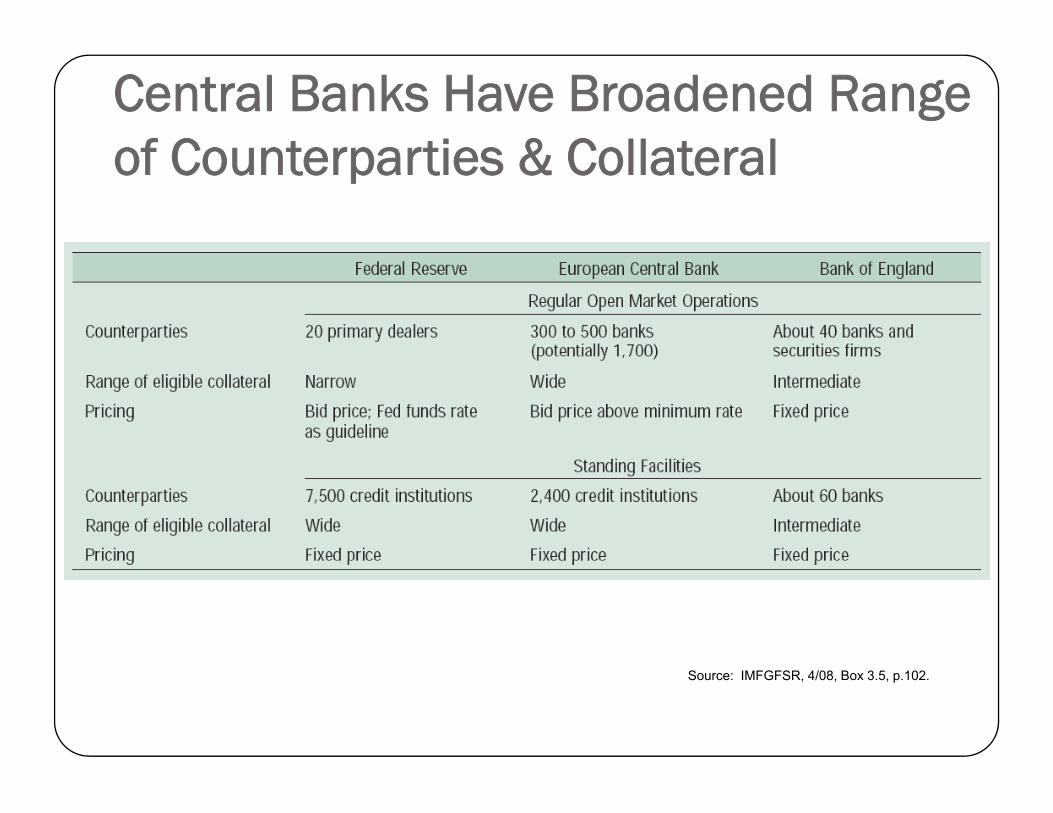

Central Banks Have Broadened Range of Counterparties & Collateralof Counterparties & Collateral

Source: IMFGFSR, 4/08, Box 3.5, p.102.

Crisis has Decapitalized Banking SystemLoss of excess servicing from securitizations

Direct losses from holdings of downgraded securitiesg g

Losses from honoring implicit guarantees backing-up off b/s vehicles

Extensions of liquidityPurchases of securities

L f i t i f t th t l b iti dLosses from inventories of assets that can no longer be securitized

Loss of important continuing source of bank revenue

Capital challengeCapital challengeReplace lost capital Acquire new capital to bring much of off-balance sheet banking system q p g g yback onto bank balance sheetsOr reduce holdings of risky assets

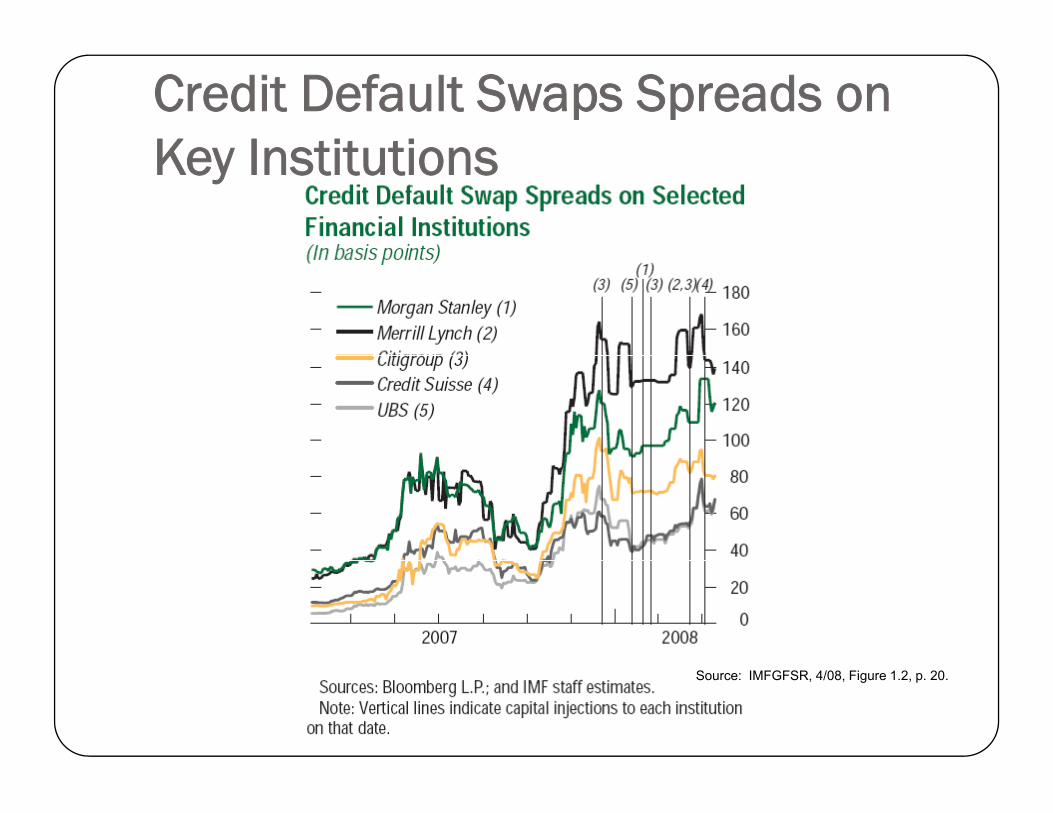

Credit Default Swaps Spreads on Key InstitutionsKey Institutions

Source: IMFGFSR, 4/08, Figure 1.2, p. 20.

RecapitalizationRecapitalizationMonetary authorities: Lower short-term rates yrelative to long-term rates to enable banks to increase spread earnings and rebuild capitalg

Banks issue new capital, especially convertible debt

Sovereign Wealth Funds

Sovereign Wealth Funds to the Rescue

Lessons for Risk ManagersLessons for Risk Managers

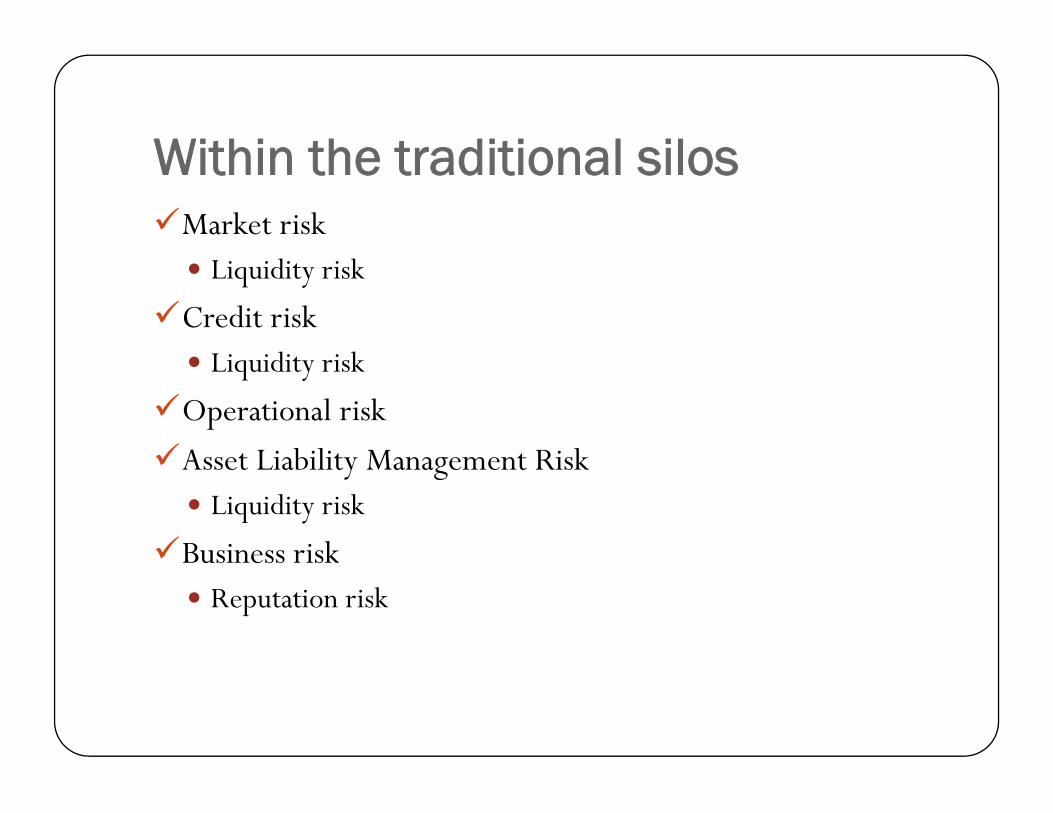

Within the traditional silosWithin the traditional silosMarket risk

Liquidity risk

Credit riskLi idi i kLiquidity risk

Operational risk

Asset Liability Management RiskAsset Liability Management RiskLiquidity risk

Business riskBusiness riskReputation risk

Across the silosFailure to realign risk management to deal with convergence of risk types

Failure to anticipate correlations across assets and asset typesFailure to anticipate correlations across assets and asset types

Failure to understand consequences of reputation risk

Need reassessment of KuUK, we knew less than we thought we did about models, ratings and insurance

u, we must recognize that our knowledge of tail events is highly uncertainBasel may insistent on a 99 97% level of confidence but do delude yourself into Basel may insistent on a 99.97% level of confidence, but do delude yourself into thinking that you know it

U, in large complex financial and economic systems, some dynamics, may simply be unknowablesimply be unknowable

How far will house prices How far will house prices fall?•Average home equity has fallen to 50%

d•May see a 3rd wave of defaults on prime mortgagesg g