the competitive landscape of destination marketing ... · ceo staff-team marketing the destination....

TRANSCRIPT

The Competitive Landscape of Destination Marketing & Development

Berkeley W. Young

Young Strategies, Inc.

This presentation and its content may not be shared or duplicated without the prior written expressed permission of Berkeley Young

AlabamaArizona California Florida Georgia IowaIllinois KansasKentuckyLouisiana

Client DestinationsThe Young Strategies project team, both individually and collectively have conducteddestination research and planning in thirty-two states:

Massachusetts MichiganMinnesotaMississippiMissouriMontanaNebraska New JerseyNew MexicoNew YorkNorth Carolina

North Dakota OklahomaPennsylvaniaSouth Carolina South DakotaTennesseeTexasVirginiaWashingtonWest VirginiaWyoming

Competition is a GREAT Thing

Competition or Coopetition?

• Destinations

• Lodging

• Restaurants

• Attractions

• Entertainment

• Retail

• Events

• Associations

• Conferences

Competing for….

Within every day

We change the way we compete

We adapt to the situation

We compete

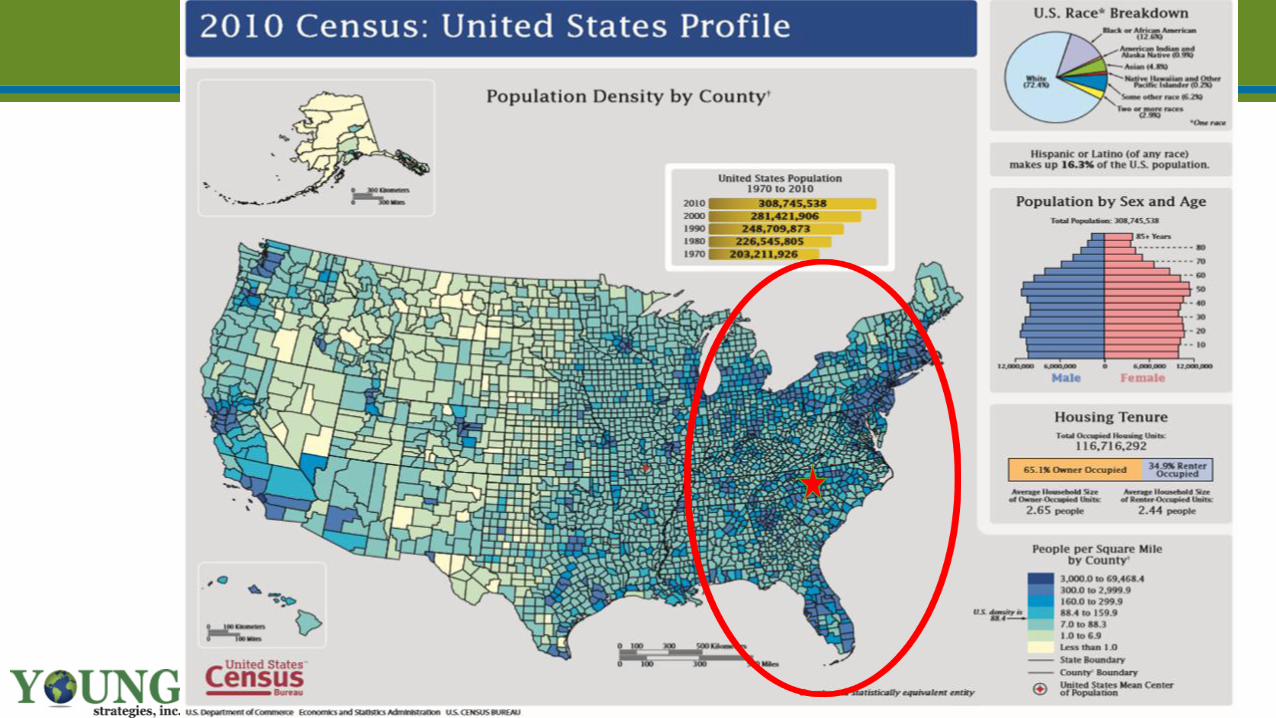

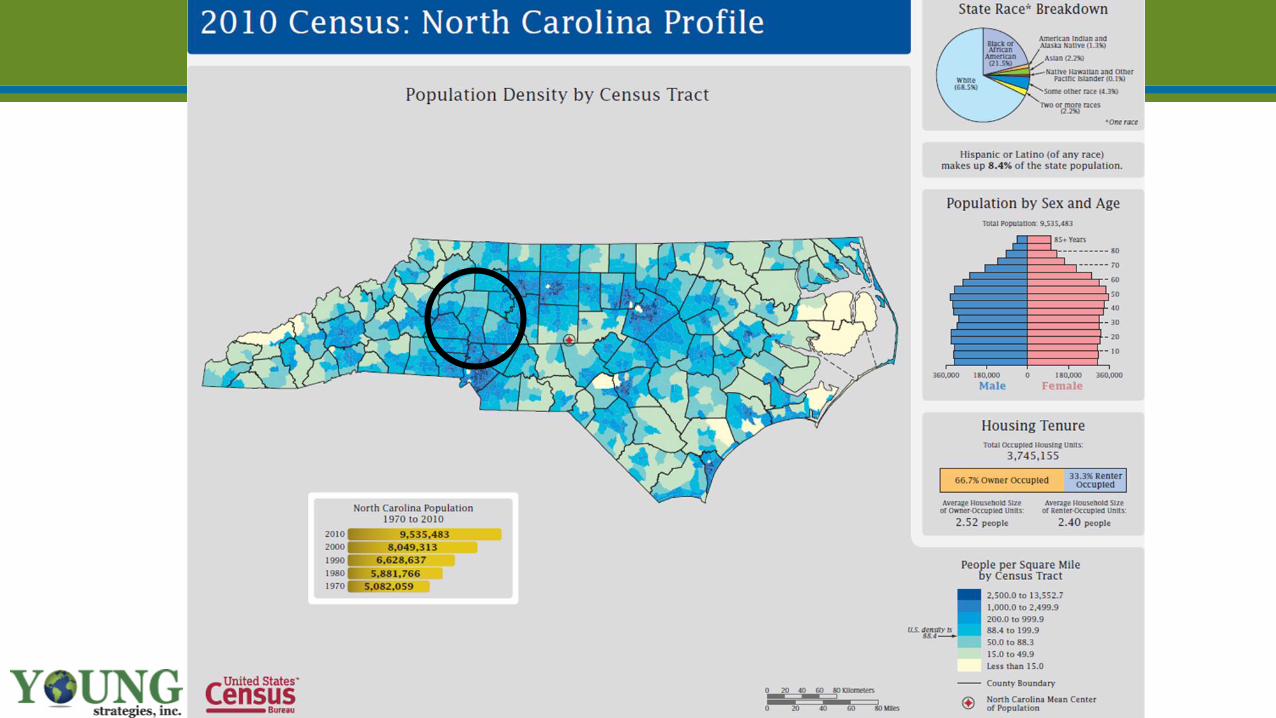

Competition Among Communities Is Intense

Destinations in the competitive landscape

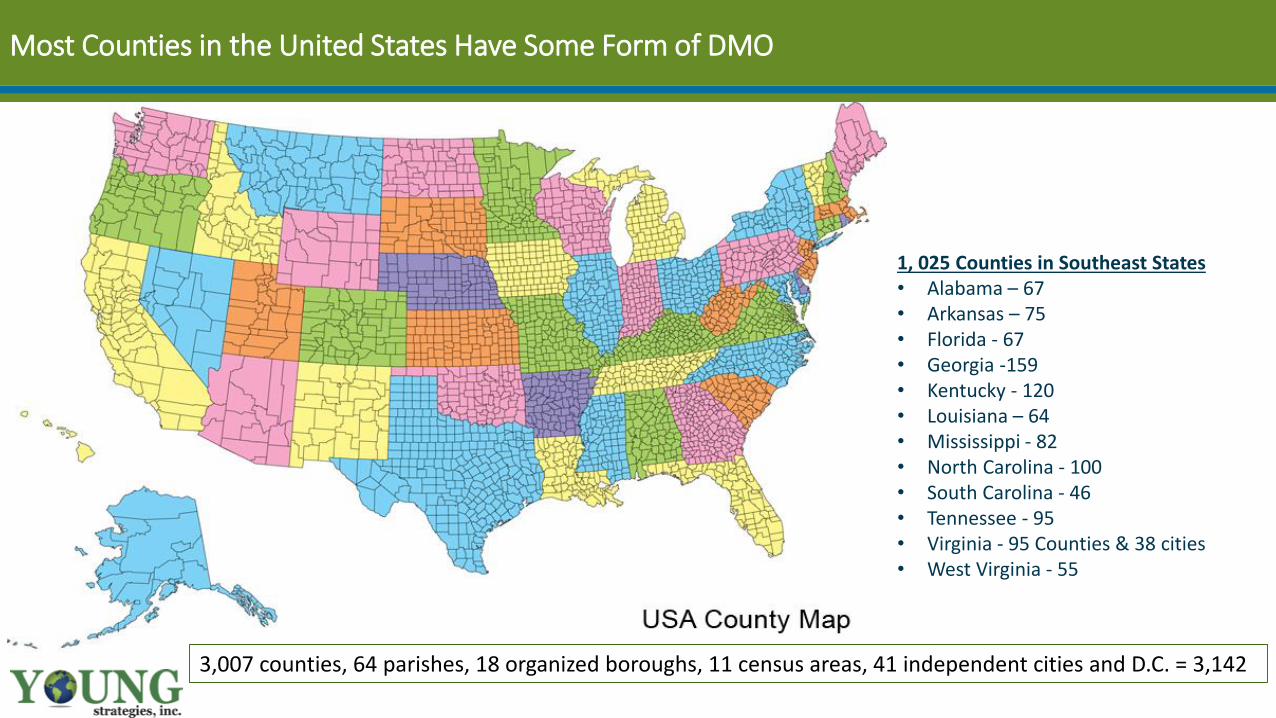

1, 025 Counties in Southeast States• Alabama – 67• Arkansas – 75• Florida - 67• Georgia -159• Kentucky - 120• Louisiana – 64• Mississippi - 82• North Carolina - 100• South Carolina - 46• Tennessee - 95• Virginia - 95 Counties & 38 cities • West Virginia - 55

Most Counties in the United States Have Some Form of DMO

3,007 counties, 64 parishes, 18 organized boroughs, 11 census areas, 41 independent cities and D.C. = 3,142

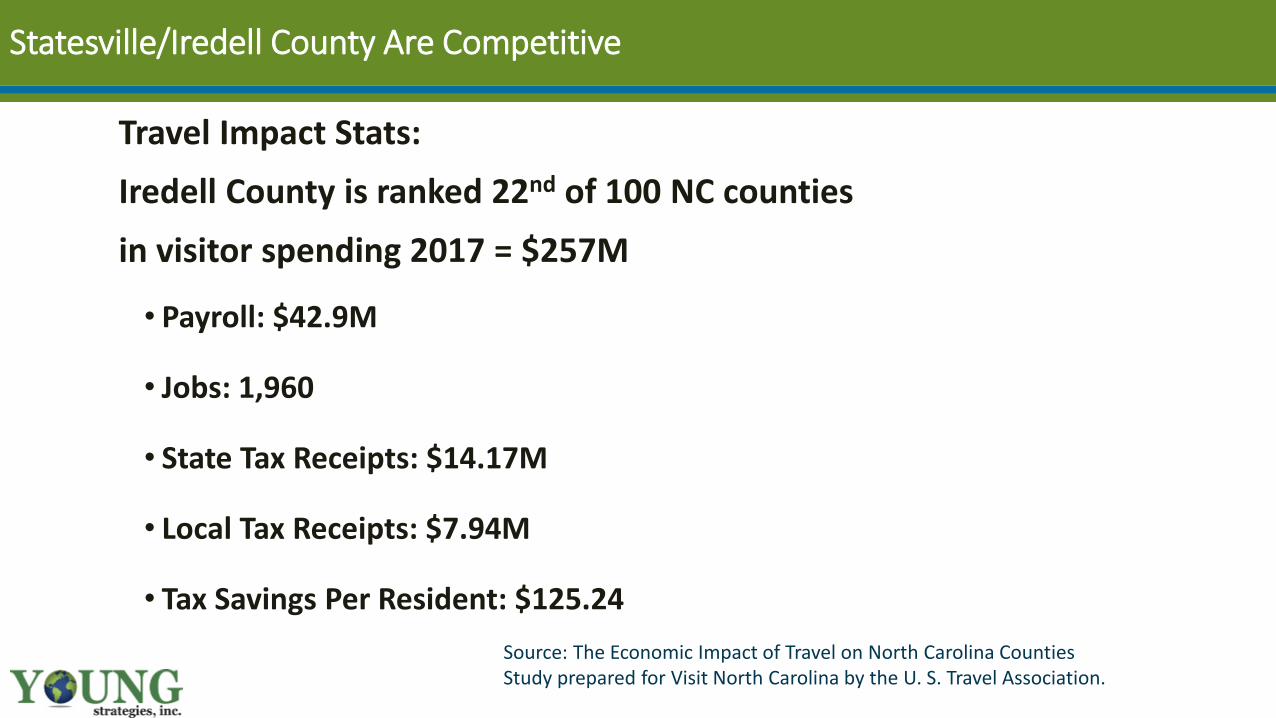

Statesville/Iredell County Are Competitive

Travel Impact Stats:

Iredell County is ranked 22nd of 100 NC counties

in visitor spending 2017 = $257M

• Payroll: $42.9M

• Jobs: 1,960

• State Tax Receipts: $14.17M

• Local Tax Receipts: $7.94M

• Tax Savings Per Resident: $125.24

Source: The Economic Impact of Travel on North Carolina CountiesStudy prepared for Visit North Carolina by the U. S. Travel Association.

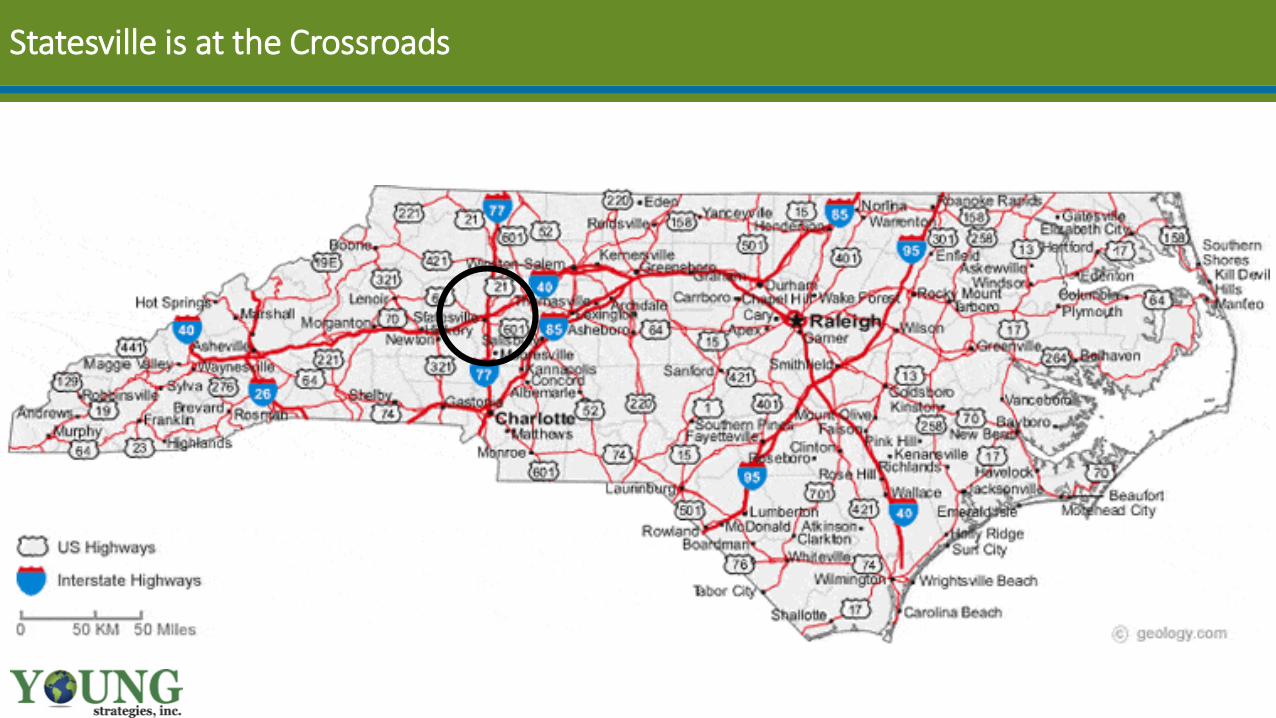

Statesville is at the Crossroads

“Tourism” is a segment of the travel Industry

• Business travel• Conference/meetings• Team sports• Motorcoach tours• Leisure getaways & vacations• University/education

In 2014, the foundation lost a total of $62 million, or $176,000 every day, Mitchell Reiss, President, Colonial Williamsburg

“The commercial businesses have been running at a loss for many, many years,” Reiss said.

• Hamilton premiered in July, 2015

• Through May, 2017 Hamilton has Grossed $111,867,904 with a total of 408,496 seats sold.

• The cast album has sold over 428,000 copies domestically

• At $100 million a year, the Broadway production of Hamilton would pass the $1 billion mark in a decade

Destinations Have to be Updated to be Relevant

Selling begins when the customer says “No”.

Overcoming objection.

My snow is bigger than yours!

Did you know that Syracuse is the

snowiest big city in the entire United

States?! According to Weather.com,

Syracuse is #1 out of America’s 20

Snowiest Major Cities – accumulating

126.3 inches annually). Some people shy

away from that but not us. We brag about

it. Hard.

We bragged so much that Winter

decided to move here and made us the

#OFFICIALHOMEOFWINTER. He

needed a place where he could be

himself – no matter what he threw at

us. He’s got his own story, and he

needed a place where he could be that

guy.

Competition for the Household Leisure SpendEntertainment and Activities:

• Attractions

• College Sports

• Professional Sports

• Concerts and theater

• Children’s activities

• Gaming

Consumer Expenditure Survey (CE) data from 1934–1936 show that, even during the Great Depression, spending on entertainment accounted for 5.4 percent of the household budget. – US Department of Labor

Facilities to drive the off-seasonEntertainment and Activities:

• Attractions

• Sports

• Concerts and theater

• Children’s activities

• Events

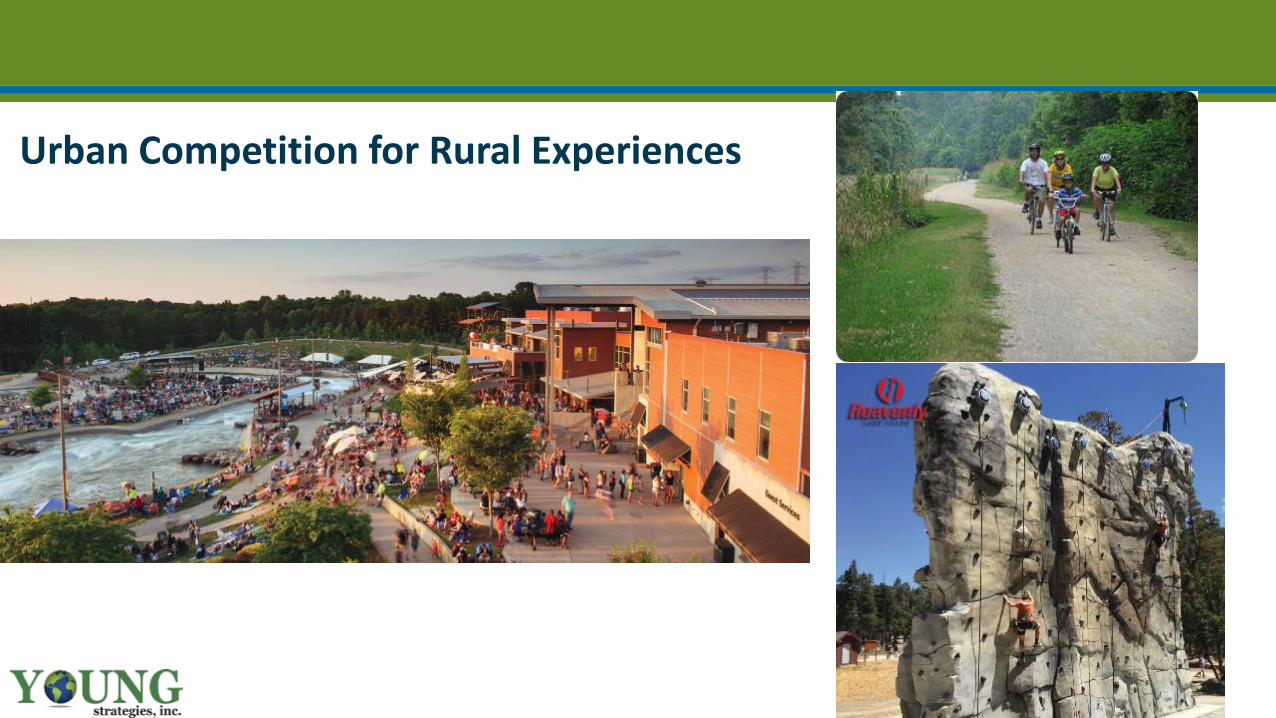

Urban Competition for Rural Experiences

Competition is NOT always two way street

South Padre Island

South Padre Island

Competition in the Workforce

Competition From Your Own Citizens

Growth From Unexpected Audiences

Barter TheaterCreeper Trail

Successful marketing startswith solid research

You MUST monitor the ever changing behavior of YOUR visitors

Why would they visit your destination?

Why would they come back?

Why would they recommend you to others?

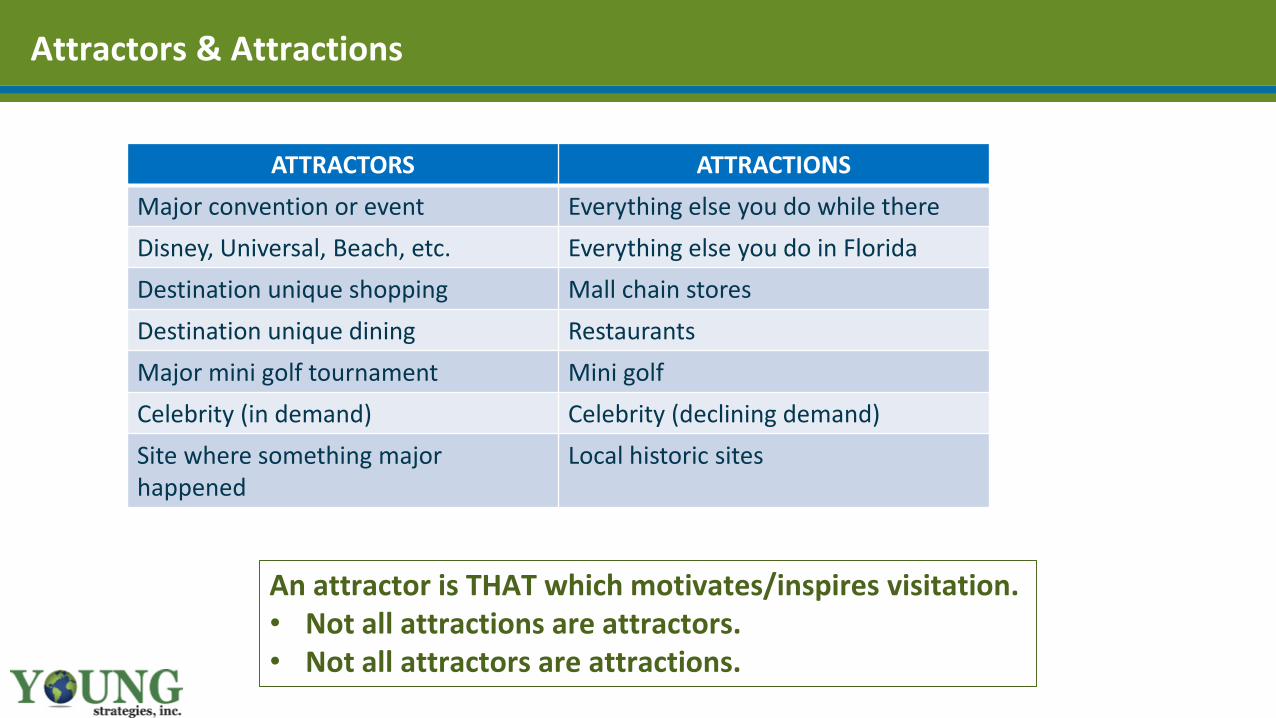

Attractors & Attractions

ATTRACTORS ATTRACTIONS

Major convention or event Everything else you do while there

Disney, Universal, Beach, etc. Everything else you do in Florida

Destination unique shopping Mall chain stores

Destination unique dining Restaurants

Major mini golf tournament Mini golf

Celebrity (in demand) Celebrity (declining demand)

Site where something major happened

Local historic sites

An attractor is THAT which motivates/inspires visitation.• Not all attractions are attractors.• Not all attractors are attractions.

The Constant Conundrum

Human Technology

Marketers must ask themselves:

• What do I need to know?

• What is my budget?

• How much will it cost?

• How reliable will it be?

• Will it be actionable?

AI?

Putting it All Together

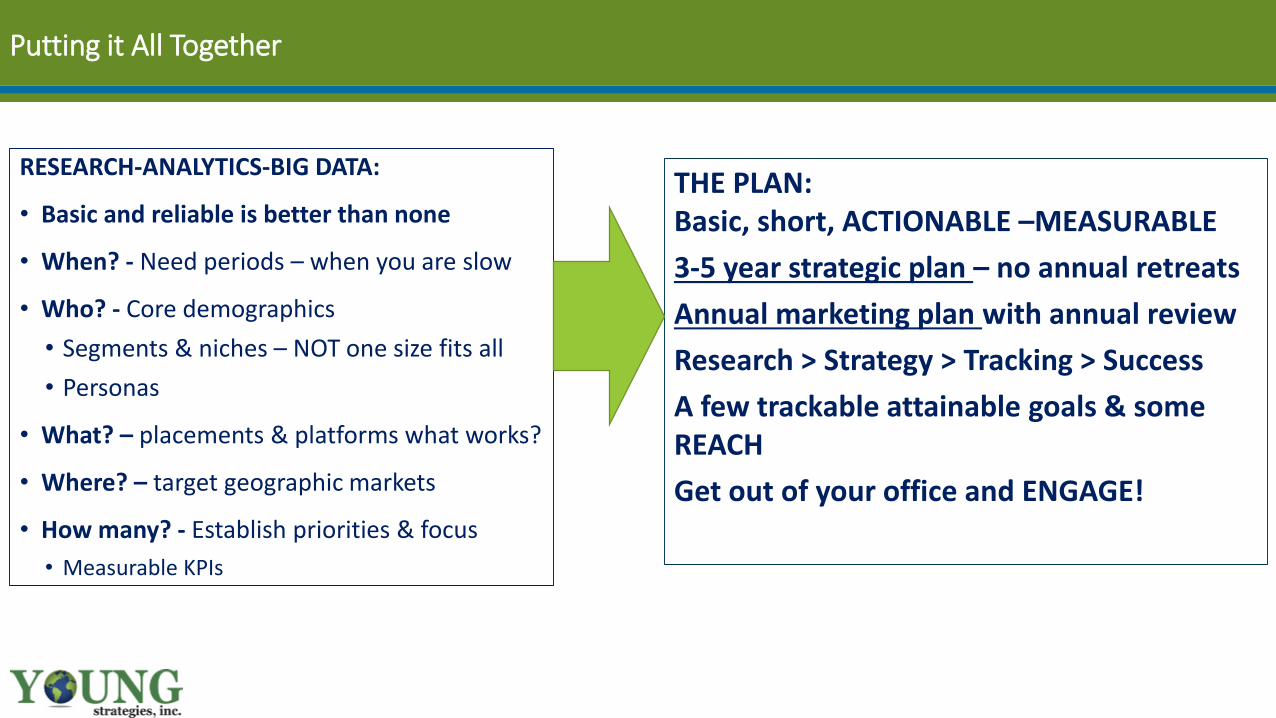

RESEARCH-ANALYTICS-BIG DATA:

• Basic and reliable is better than none

• When? - Need periods – when you are slow

• Who? - Core demographics

• Segments & niches – NOT one size fits all

• Personas

• What? – placements & platforms what works?

• Where? – target geographic markets

• How many? - Establish priorities & focus

• Measurable KPIs

THE PLAN:Basic, short, ACTIONABLE –MEASURABLE

3-5 year strategic plan – no annual retreats

Annual marketing plan with annual review

Research > Strategy > Tracking > Success

A few trackable attainable goals & some REACH

Get out of your office and ENGAGE!

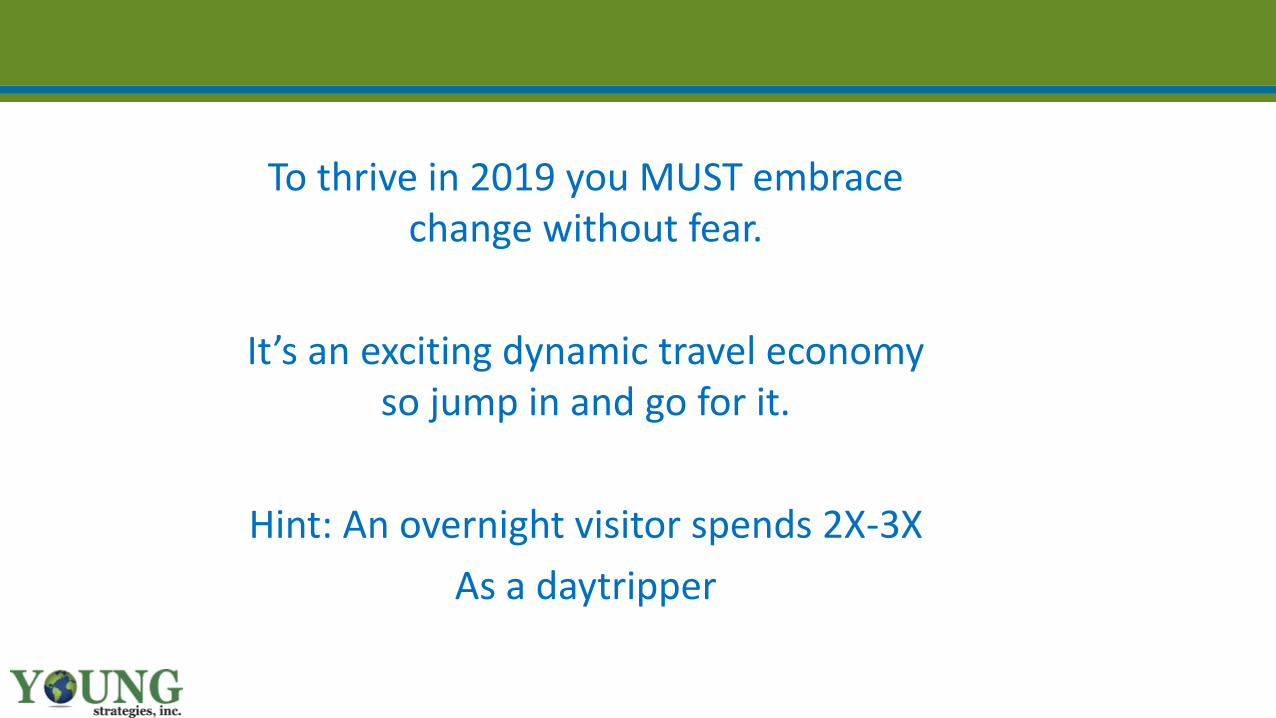

To thrive in 2019 you MUST embrace change without fear.

It’s an exciting dynamic travel economy so jump in and go for it.

Hint: An overnight visitor spends 2X-3X

As a daytripper

Statesville Lodging Product

Name of Establishment Class Open Date RoomsBest In Town Motel Economy Class Oct 1950 25Lodge Inn & Suites Economy Class Jun 1966 130Masters Inn Statesville Economy Class Jun 1968 120Days Inn Statesville Economy Class Aug 1970 99Hallmark Inn Motel Economy Class Jun 1980 39Red Roof Inn Statesville Economy Class Sep 1984 115Brookwood Inn Economy Class Jun 1985 117Ramada Statesville Midscale Class Dec 1985 134Quality Inn & Suites Statesville Midscale Class Jul 1986 107Comfort Inn & Suites Statesville Upper Midscale Class Jan 1987 111Americas Best Value Inn Statesville Economy Class Jun 1992 40Economy Inn Economy Class Jun 1993 59Best Western Statesville Inn Midscale Class Apr 1995 69Sleep Inn Statesville Midscale Class Feb 1998 69Motel 6 Statesville Economy Class May 1999 50Microtel Inn & Suites by Wyndham Statesville Economy Class May 1999 64Hampton Inn Statesville Upper Midscale Class Jan 2007 80Courtyard Statesville Mooresville Lake Norman Upscale Class Jun 2009 94Holiday Inn Express & Suites Statesville Upper Midscale Class Jun 2009 77Hilton Garden Inn Statesville Upscale Class Apr 2017 104

20 Lodging Properties Rooms = 1703

1980’s6 hotels, 623 rooms, 37% of inventory

1990’s6 hotels, 351 rooms, 21% of inventory

2000’s3 hotels, 251 rooms, 15% of inventory

Last Decade1 hotel, 104 rooms, 6% of inventory

Prior to 19804 hotels, 374 rooms, 22% of inventory

Research to Identify Target Growth Times- 33 -

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

52 Week Occupancy TrendJanuary - March, 2018 & April - December, 2017

SUN MON TUES WED THURS FRI SAT

Daily Occupancy %’s # of days % of YR

Days reported at 60% - 69% 52 14.2%

Days reported at 70% - 79% 59 16.2%

Days reported at 80% - 89% 54 14.8%

Days reported at 90% - 100% 24 6.6%

Total # of Days 60% or higher occupancy

189 nights = 51.8% of the year

Source: STR

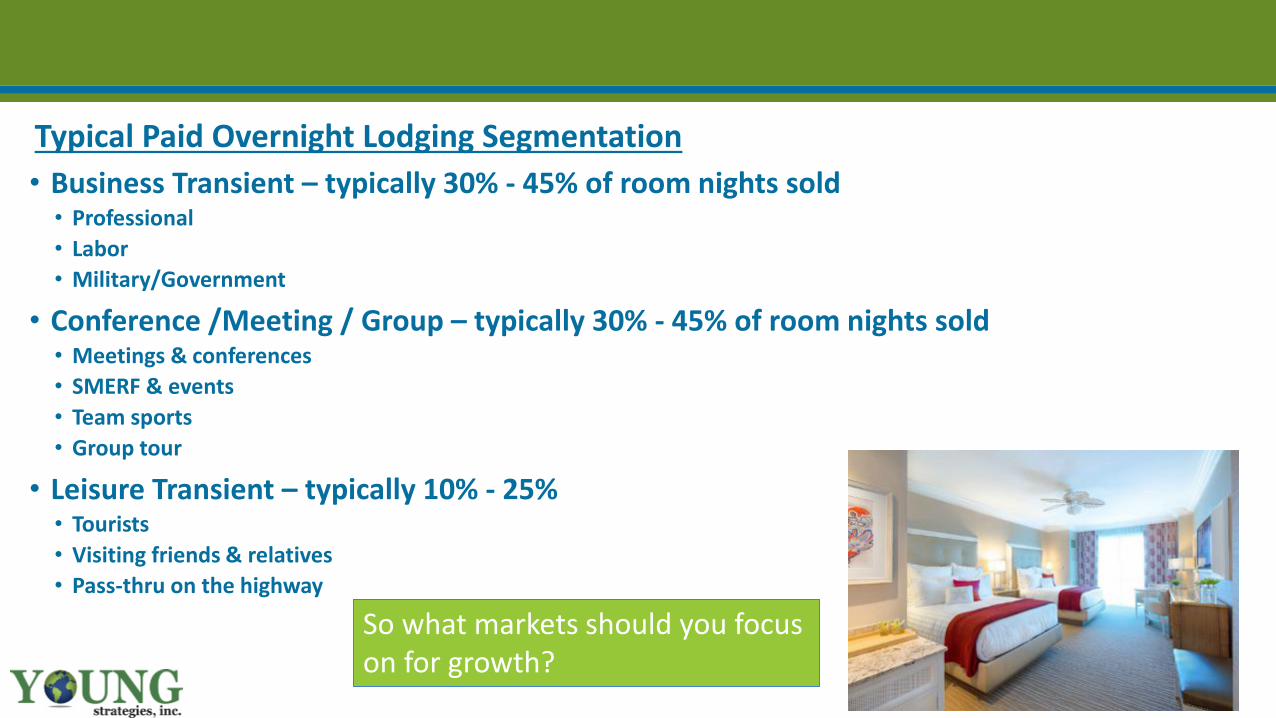

Tourism is a Segment of the Travel IndustryTypical Paid Overnight Lodging Segmentation

• Business Transient – typically 30% - 45% of room nights sold• Professional

• Labor

• Military/Government

• Conference /Meeting / Group – typically 30% - 45% of room nights sold• Meetings & conferences

• SMERF & events

• Team sports

• Group tour

• Leisure Transient – typically 10% - 25%• Tourists

• Visiting friends & relatives

• Pass-thru on the highway

So what markets should you focus on for growth?

CVB/DMO Leadership Structure

Communication & Reporting; Runs the DMO

Board:• Long-Range Vision• Policy & Oversight• Advocacy with partners• Advocacy with electeds

Vision & Plan for thedestination

Board

Exec

Com

Visionary Strategic Plan:• Dedicated Funding• Board of Travel Industry Leaders• Focused Staff• Measurable ROI - Accountability

CEO

Staff-Team

Marketing the Destination

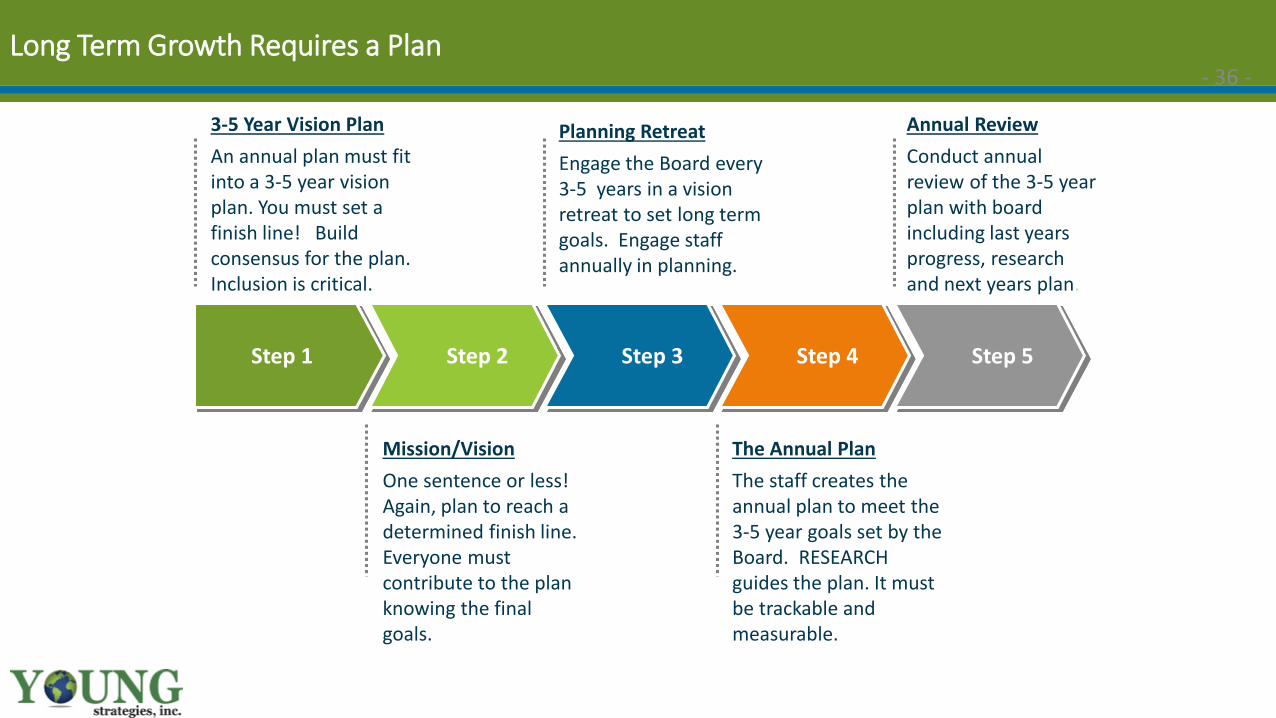

Long Term Growth Requires a Plan- 36 -

3-5 Year Vision Plan

An annual plan must fit into a 3-5 year vision plan. You must set a finish line! Build consensus for the plan. Inclusion is critical.

Step 1 Step 2 Step 3 Step 4 Step 5

Planning Retreat

Engage the Board every 3-5 years in a vision retreat to set long term goals. Engage staff annually in planning.

Annual Review

Conduct annual review of the 3-5 year plan with board including last years progress, research and next years plan.

Mission/Vision

One sentence or less! Again, plan to reach a determined finish line. Everyone must contribute to the plan knowing the final goals.

The Annual Plan

The staff creates the annual plan to meet the 3-5 year goals set by the Board. RESEARCH guides the plan. It must be trackable and measurable.

Standard CVB/DMO Staff Structure- 37 -

Board of Directors

President/CEO

Vice President of Brand

Development

Director of Communication

s

Director of Digital

Marketing

Marketing Manager

Vice President of Business

Development

Director of Business

Development

Marketing Manager

Director of Sports

Development

Director of Business

Development

Vice President of Visitor

Experience

Director of Event Services

Director of Visitor Services

Office Manager

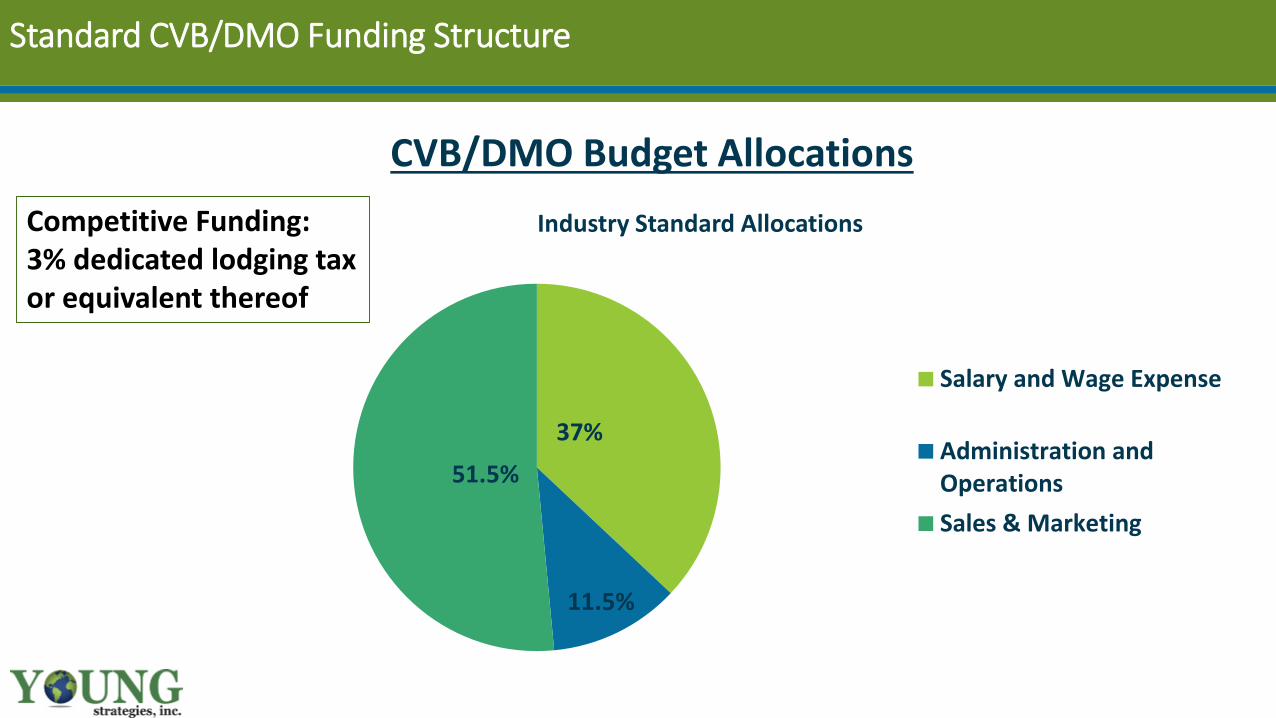

37%

11.5%

51.5%

Industry Standard Allocations

Salary and Wage Expense

Administration andOperations

Sales & Marketing

CVB/DMO Budget Allocations

Standard CVB/DMO Funding Structure

Competitive Funding:3% dedicated lodging taxor equivalent thereof

Growth Opportunity

Insert travel party spending and taxes chart

2018 Overnight Spending Impact

Statesville 2018 Daily Lodging Room Inventory 1,703

Statesville Annual Lodging Room Inventory (1,703 x 365 days) 621,595

2018 Lodging Occupancy Percentage (estimate) 60%

2018 Lodging Room Nights Occupied (estimate) 372,957

2018 Average Daily Spending Per Travel Party (estimate) $225.00

Total Overnight (paid lodging) Visitor Spending $83,915,325

Value of 1% Occupancy in 2018

Statesville Annual Lodging Room Inventory 1,703

1% Occupancy (1,703 X 365 X .01 =) 6,216

Visitor Spending Generated $1,398,600

Take- Aways

• Competition makes us work harder, makes us better!

• Regular competitive Assessments – internal & external (research)

• Invest in sales and marketing to grow travel spending & impact

• You need a sales and marketing team to compete

• You need a vision for Statesville as a destination

• Destination for….Meetings? Team sports? Weekend Getaways?

• A common enemy unites a group – declining market share in NC is the enemy

• Your biggest competitor may be YOU if you don’t embrace change

Contact Information

Berkeley Young,

Young Strategies, Inc

704-677-4018

facebook/young strategies

LinkedIn/berkeleyyoung

YOUNG STRATEGIES, INC

• Destination research and strategic planning

• Research for 150+ destinations in 27 states

• Communities, regions and states

• Travel industry focused

• National research data and trends analysis

• Writing and speaking

• Board workshops & planning sessions

• Listening to travelers