the classical gold standard (and its downfall). the world economy under the gold standard gold...

Post on 21-Dec-2015

219 views

TRANSCRIPT

The classical gold standard (and its downfall)

The world economy under the Gold Standard

• Gold Standard comes into being after 1870– Other countries emulate Britain, as Britain becomes a trade superpower– “Network externalities” in converging to common standard

• A system characterized by:– fixed parities of national currencies vis-à-vis gold– Free capital mobility– Settlement of payments imbalances in gold– National economic policies characterized by priority placed on currency

and exchange-rate stability• Associated with extensive financial globalization

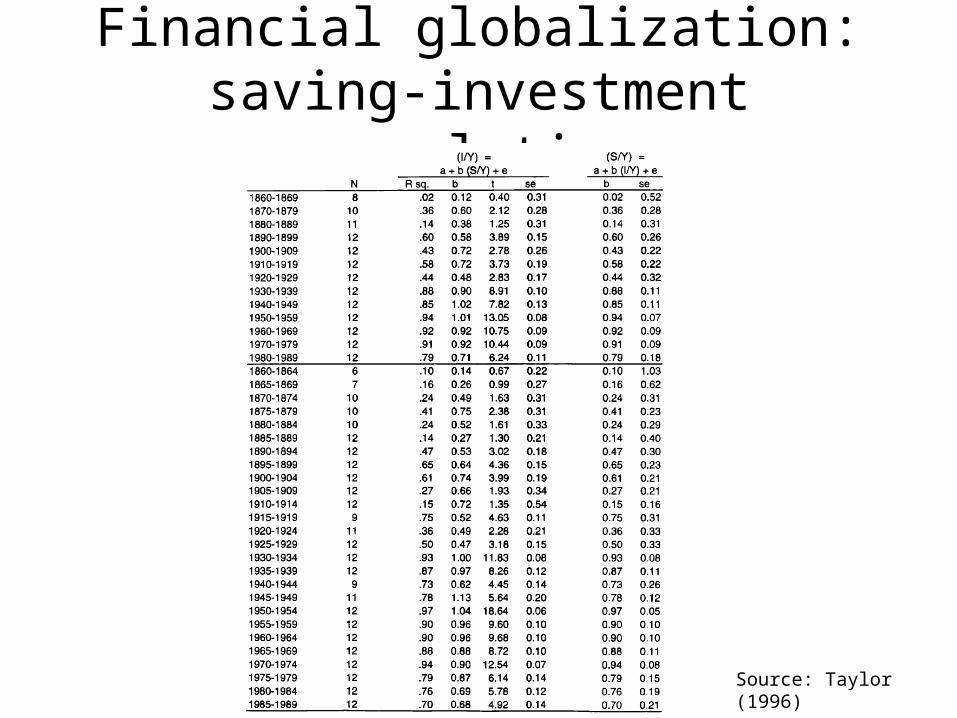

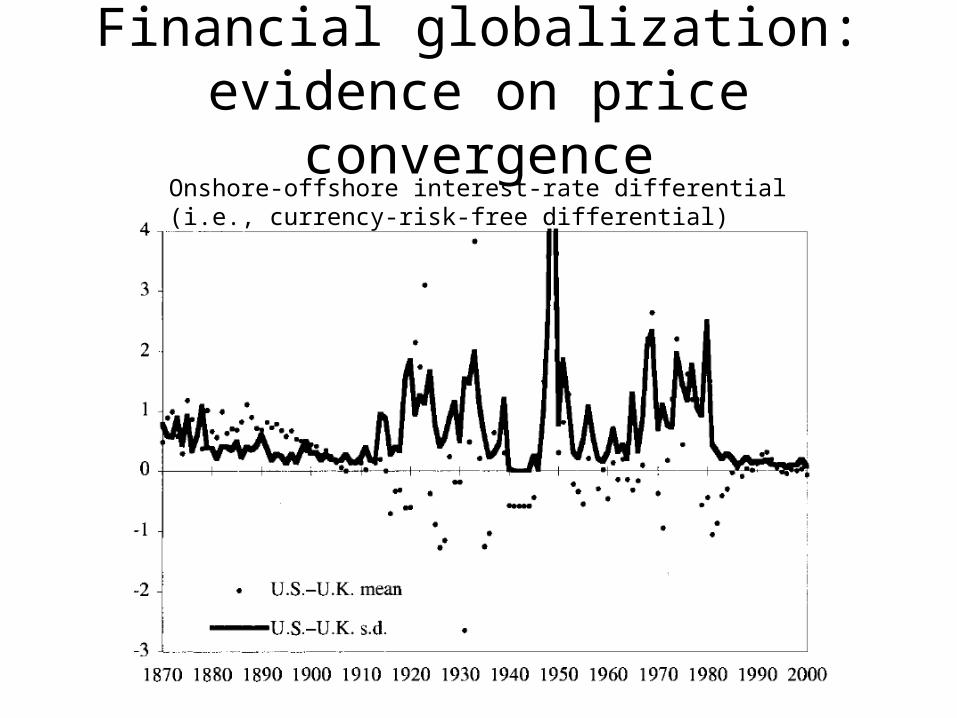

– Large net capital flows (CA surpluses/deficits)– Relatively low national saving-investment correlations – Convergence in interest rates

• And rapid growth of trade (as we have seen)– Common monetary standard and fixed parities take reduce the risk and

uncertainty in international trade

Financial globalization: saving-investment correlations

Source: Taylor (1996)

Financial globalization: evidence on price convergence

Onshore-offshore interest-rate differential (i.e., currency-risk-free differential)

Gold Standard complemented by exercise of political power

• Large amounts of international lending possible only if repayment is guaranteed– The problem of sovereign risk

• Managed under GS through exercise of political and military power by center countries

• Enforcement of repayment through – war and invasion

• Invasion of Egypt in 1882 by Britain to “restore political stability” and ensure debt continues to be repaid

– taking over revenue collection (Ottoman Empire)• Set up in 1881, the Imperial Debt Administration collects revenue to

pay back European creditors – gunboat diplomacy (Latin America)

• E.g. Roosevelt corrollary

Political underpinnings of international exchange, redux

“Theodore Roosevelt’s 1904 Corollary to the Monroe Doctrine … signaled an important shift in political and economic relations between the United States and Latin America as well as between the United States and Europe in the Western Hemisphere. The corollary stated that the American government would ensure that Central and Latin American countries repaid their debts and that the United States would act as the region’s policeman to ensure peace and stability”

…we show that, on average, Central and South American sovereign debt issues

listed on the London Stock Exchange rose by 74 percent after one year and by 91 percent nearly two years after the initial pronouncement of the Roosevelt Corollary. Our econometric evidence suggests that the most plausible explanation for the enormous rally that occurred in Latin American sovereign bonds was the announcement of the corollary and actions by the American government that established the credibility of the policy. Specifically, the United States sent gunboats to Santo Domingo in 1905 and took over customs collection to pay foreign creditors after it defaulted on its external debt and European powers threatened to intervene.

-- Mitchener and Weidenmier, (2005)

Logic of adjustment under the Gold Standard (I)

• Aggregate money supply determined not by economic policy, but by supply of gold– If gold supply lags behind demand for money, price deflation is

the result– Example: deflation of price level during 1870s-1890s by c. 20%– Who is hurt? Debtors who have taken on fixed-rate debt (e.g.

farmers)

• Political consequences: populism in U.S.– Led by farming and silver mining interests– William Jennings Bryant (democratic candidate for President in

1896): “You shall not crucify mankind upon a cross of gold”– Wizard of Oz as an allegory about the evils of the gold standard

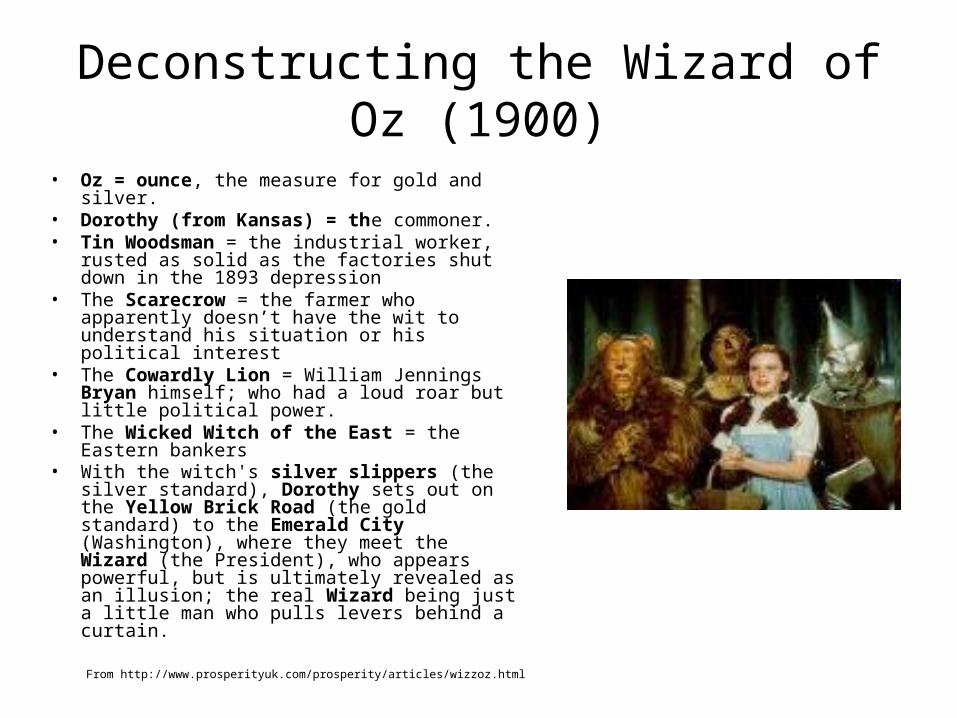

Deconstructing the Wizard of Oz (1900)

• Oz = ounce, the measure for gold and silver. • Dorothy (from Kansas) = the commoner. • Tin Woodsman = the industrial worker, rusted

as solid as the factories shut down in the 1893 depression

• The Scarecrow = the farmer who apparently doesn’t have the wit to understand his situation or his political interest

• The Cowardly Lion = William Jennings Bryan himself; who had a loud roar but little political power.

• The Wicked Witch of the East = the Eastern bankers

• With the witch's silver slippers (the silver standard), Dorothy sets out on the Yellow Brick Road (the gold standard) to the Emerald City (Washington), where they meet the Wizard (the President), who appears powerful, but is ultimately revealed as an illusion; the real Wizard being just a little man who pulls levers behind a curtain.

From http://www.prosperityuk.com/prosperity/articles/wizzoz.html

Logic of adjustment under the Gold Standard (II)

• Balance-of-payments deficits and surpluses result in corresponding changes in domestic money supplies

• The “automatic adjustment mechanism”– Changes in price levels caused by gold in/outflows result in movements

in international competitiveness that correct the initial imbalance• Hume’s price-specie flow mechanism

– Alternatively, changes in money supplies caused by gold in/outflows result in movements in interest rates that correct the initial imbalance

• Deficit => reduction in money supply => rise in interest rates => capital inflows

• More likely mechanism in practice, since capital flows respond much more quickly than trade in goods

• Central banks speed up the process by moving interest rates pre-emptively, without much gold crossing international borders

– Stabilizing capital flows• Move in anticipation of CB action• And therefore vitiate the need for actual changes in interest rates• Depends on high degree of credibility of parity

What central banks could not do under the GS

• Alter the exchange rate– Obviously

• Engage in countercyclical monetary policy– Cut interest rates in downturn, because that would result in a

gold outflow and threaten the exchange rate parity• Act as a lender of last resort to the domestic banking

system– Because the money supply is linked directly to the gold reserves– Unless they could borrow from abroad

• E.g. Bank of England during the Baring Brothers crisis in 1890– The LLR function was privatized in the U.S.

• J.P. Morgan uses his own money to save banking system during 1907 financial panic (the Fed did not exist at the time, and was created only subsequently in 1913)

The institutional/ideological underpinnings of the Gold Standard

• Priority accorded to preserving the GS• Eichengreen: “[The Central Banks’] capacity to defend gold

convertibility in the face of domestic and foreign disturbances rested on limits on the political pressure that could be brought to bear on [it] to pursue other objectives incompatible with the defense of gold convertibility.” (29)

• The GS as a “socially constructed institution”– It worked because people expected CBs would act to make it work, i.e.

maintain parity at any cost

• Limited role of fractional reserve banking, until later in the period– Hence bank runs and financial panics less of a problem

• The role of ideas– No well-articulated or widely believed theory of how government policy

could affect the business cycle

Logic of adjustment under the Gold Standard (III)

• Real economic costs if wage-price flexibility not complete– Deficit => reduction in money supply

=> deflation, and reduction in aggregate demand

=> unemployment if wages are not flexible downwards

– Same result through interest-rate channel (less investment)

• Political consequences: Britain in interwar period– Paper currencies in the war and floating currencies during the 1920s

– Britain restores GS at prewar parity in 1925• But given intervening inflation, this turns out to be an overvalued parity,

leaving Britain with a BOP deficit and loss of gold reserves• Without stabilizing capital inflows, BoE had to acquiesce in reduced

money supply and high interest rates• Resulting in deflation and exacerbating unemployment (20%)• Britain goes off gold in September 1931, followed by others later

Independent monetary policy

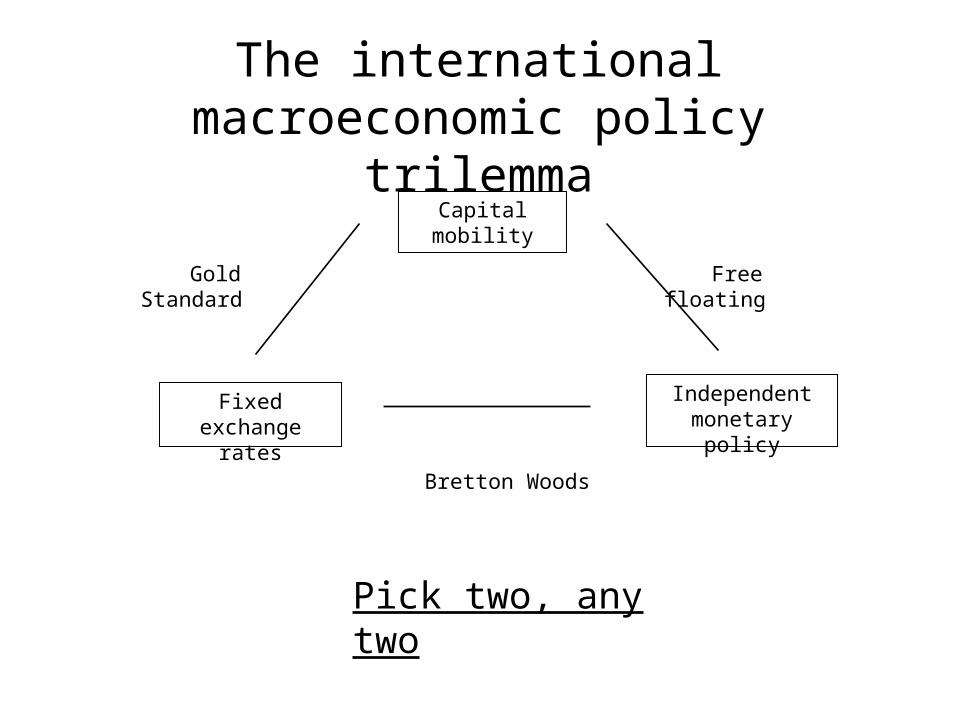

The international macroeconomic policy trilemma

Gold Standard

Pick two, any two

Free floating

Bretton Woods

Fixed exchange rates

Capital mobility

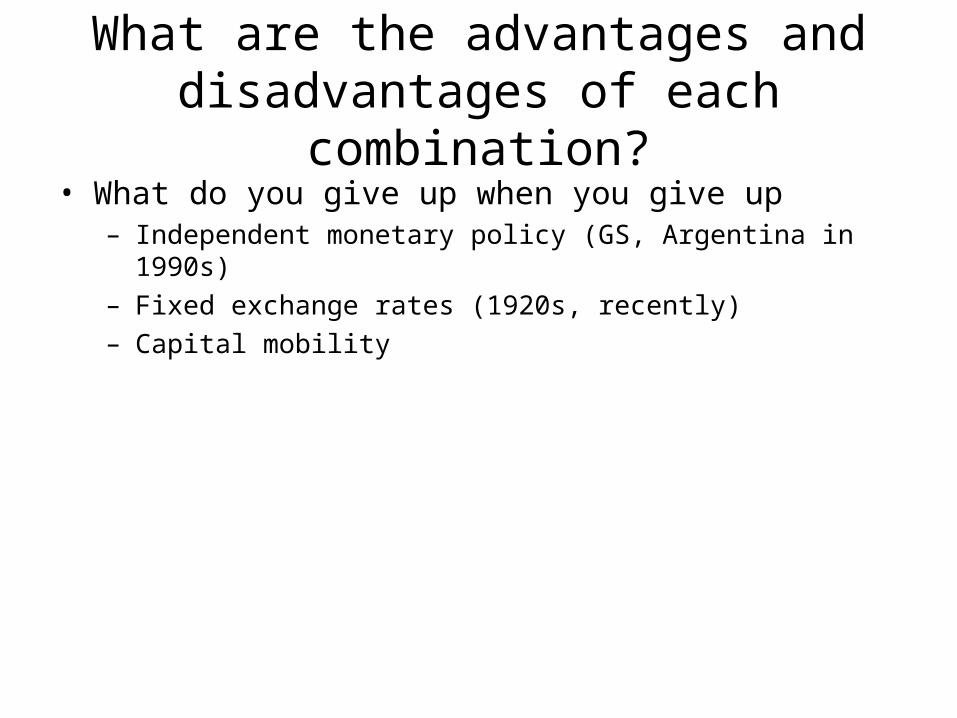

What are the advantages and disadvantages of each combination?

• What do you give up when you give up– Independent monetary policy (GS, Argentina in 1990s)– Fixed exchange rates (1920s, recently)– Capital mobility

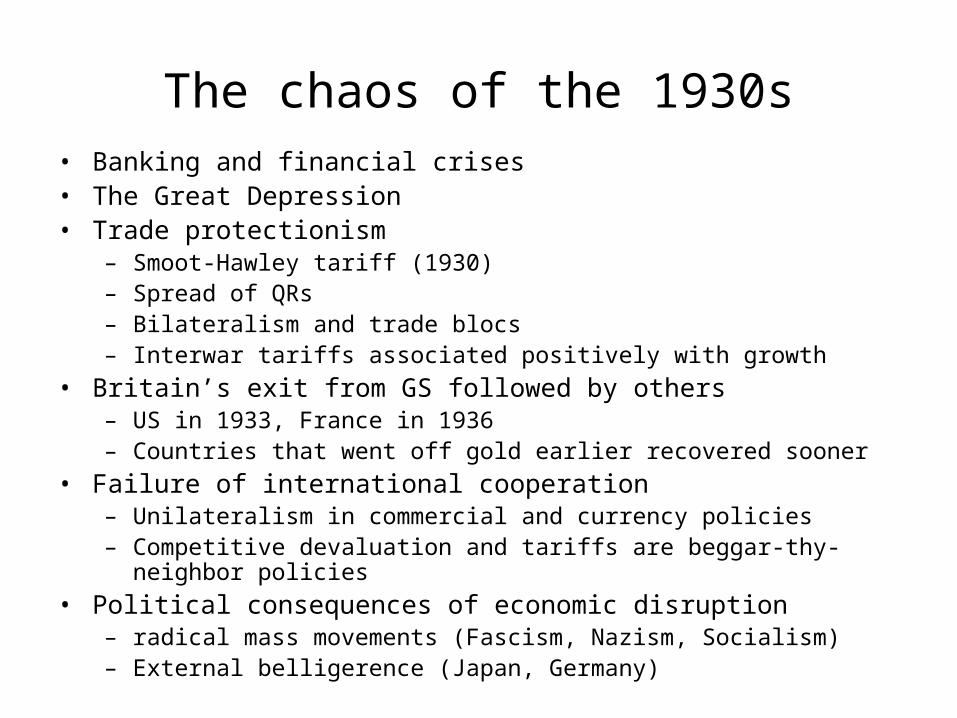

The chaos of the 1930s• Banking and financial crises• The Great Depression• Trade protectionism

– Smoot-Hawley tariff (1930)– Spread of QRs– Bilateralism and trade blocs– Interwar tariffs associated positively with growth

• Britain’s exit from GS followed by others– US in 1933, France in 1936– Countries that went off gold earlier recovered sooner

• Failure of international cooperation– Unilateralism in commercial and currency policies– Competitive devaluation and tariffs are beggar-thy-neighbor policies

• Political consequences of economic disruption– radical mass movements (Fascism, Nazism, Socialism)– External belligerence (Japan, Germany)

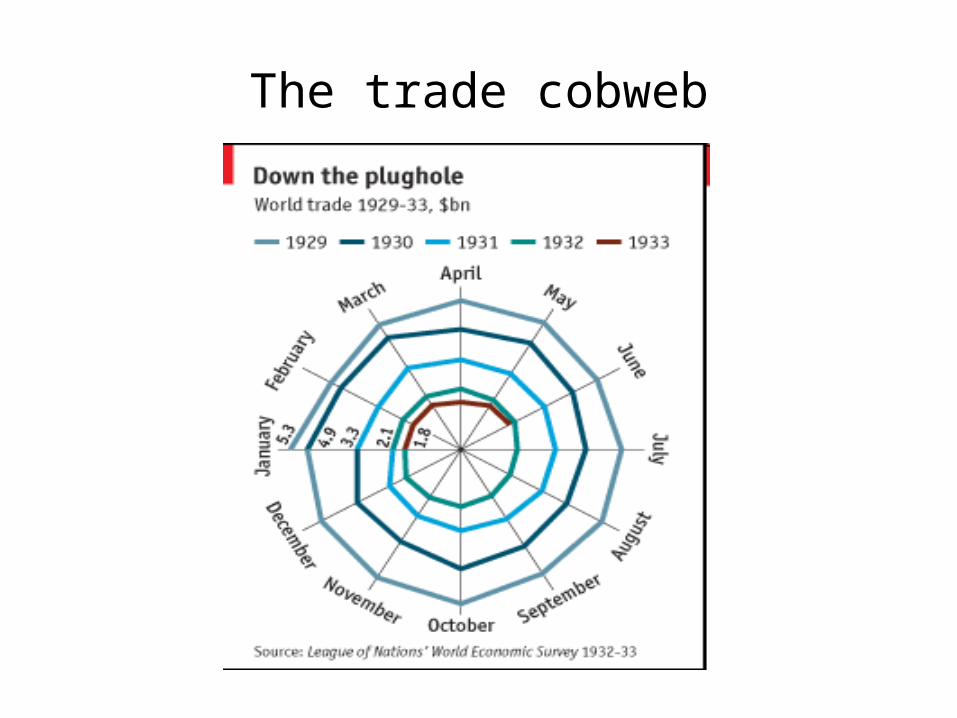

The trade cobweb

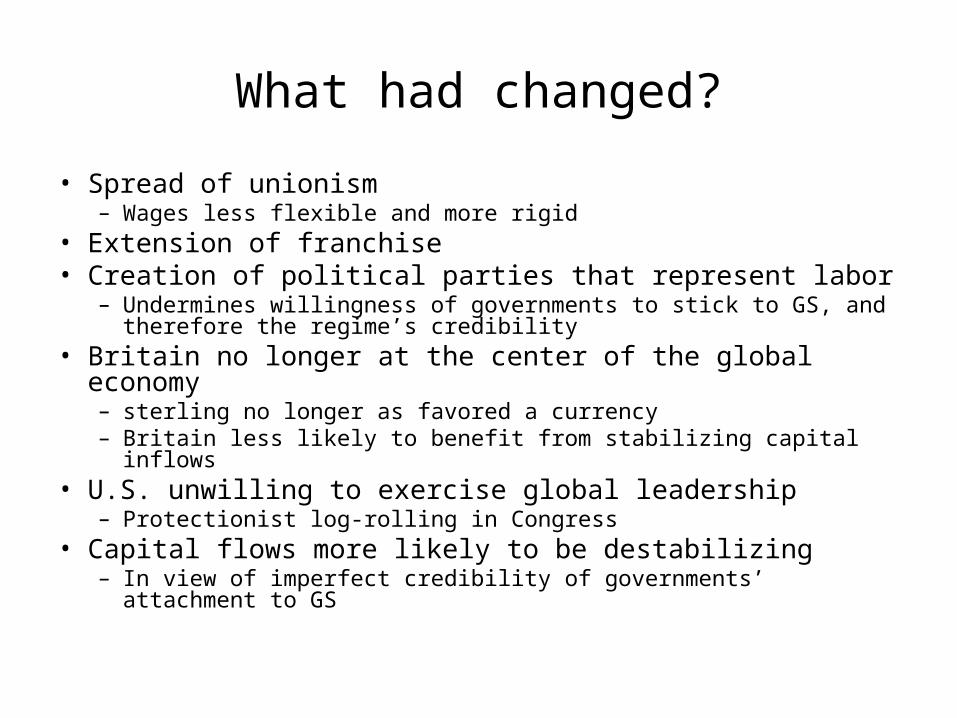

What had changed?

• Spread of unionism– Wages less flexible and more rigid

• Extension of franchise• Creation of political parties that represent labor

– Undermines willingness of governments to stick to GS, and therefore the regime’s credibility

• Britain no longer at the center of the global economy– sterling no longer as favored a currency– Britain less likely to benefit from stabilizing capital inflows

• U.S. unwilling to exercise global leadership– Protectionist log-rolling in Congress

• Capital flows more likely to be destabilizing– In view of imperfect credibility of governments’ attachment to GS

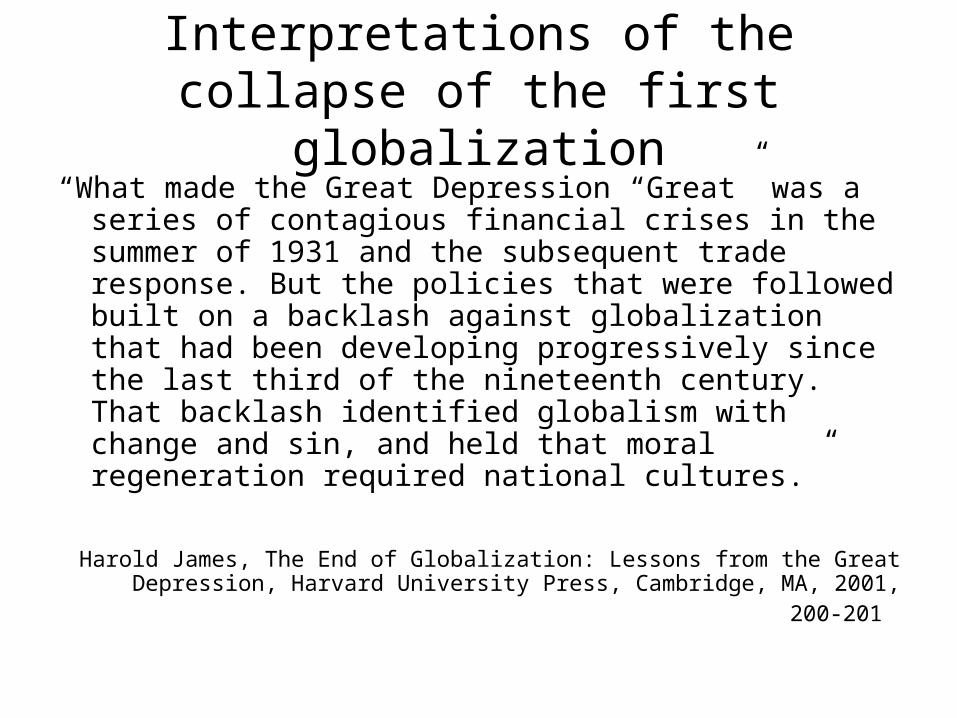

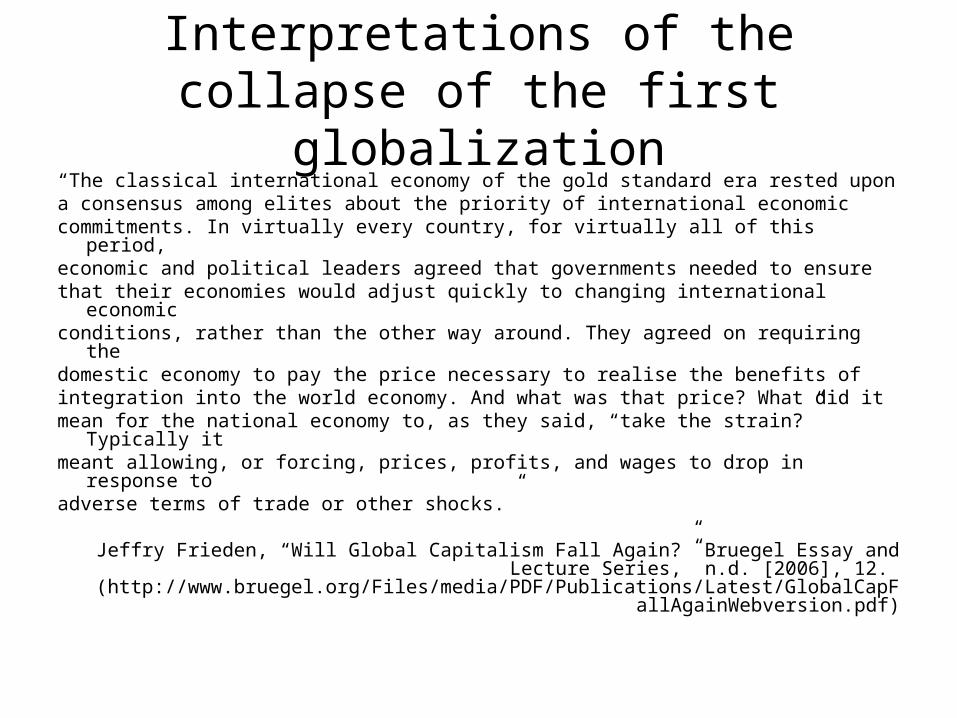

Interpretations of the collapse of the first globalization

“What made the Great Depression “Great” was a series of contagious financial crises in the summer of 1931 and the subsequent trade response. But the policies that were followed built on a backlash against globalization that had been developing progressively since the last third of the nineteenth century. That backlash identified globalism with change and sin, and held that moral regeneration required national cultures.”

Harold James, The End of Globalization: Lessons from the Great Depression, Harvard University Press, Cambridge, MA, 2001, 200-201

“The classical international economy of the gold standard era rested upona consensus among elites about the priority of international economiccommitments. In virtually every country, for virtually all of this period,economic and political leaders agreed that governments needed to ensurethat their economies would adjust quickly to changing international economicconditions, rather than the other way around. They agreed on requiring thedomestic economy to pay the price necessary to realise the benefits ofintegration into the world economy. And what was that price? What did itmean for the national economy to, as they said, “take the strain?” Typically itmeant allowing, or forcing, prices, profits, and wages to drop in response toadverse terms of trade or other shocks.”

Jeffry Frieden, “Will Global Capitalism Fall Again?” Bruegel Essay and Lecture Series,” n.d. [2006], 12.

(http://www.bruegel.org/Files/media/PDF/Publications/Latest/GlobalCapFallAgainWebversion.pdf)

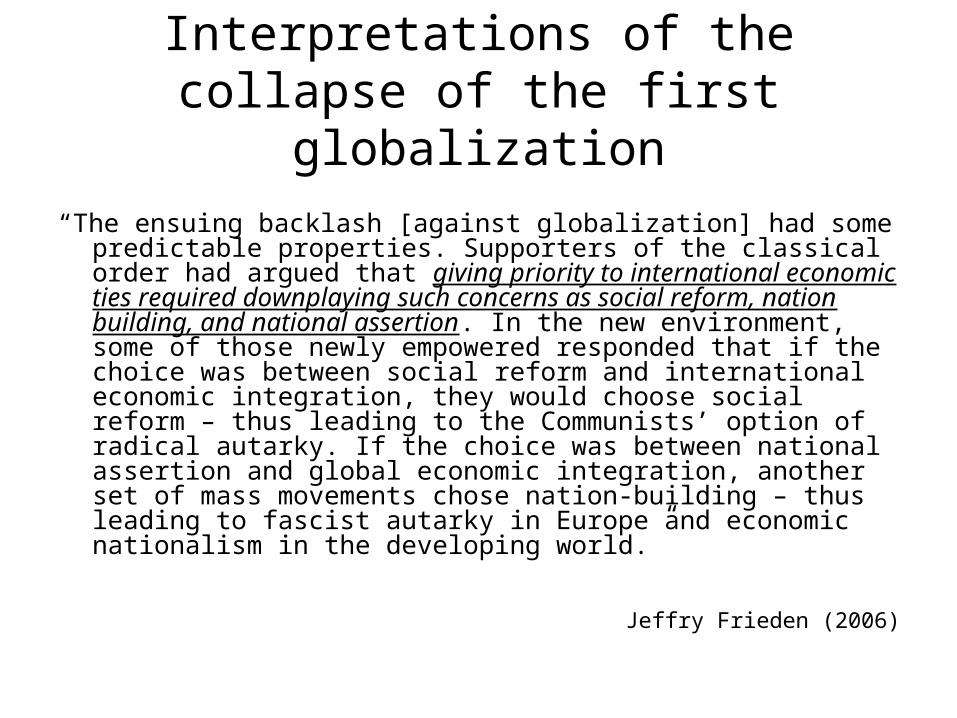

Interpretations of the collapse of the first globalization

“The ensuing backlash [against globalization] had some predictable properties. Supporters of the classical order had argued that giving priority to international economic ties required downplaying such concerns as social reform, nation building, and national assertion. In the new environment, some of those newly empowered responded that if the choice was between social reform and international economic integration, they would choose social reform – thus leading to the Communists’ option of radical autarky. If the choice was between national assertion and global economic integration, another set of mass movements chose nation-building – thus leading to fascist autarky in Europe and economic nationalism in the developing world.”

Jeffry Frieden (2006)

Interpretations of the collapse of the first globalization

Lessons of history

What do we learn?

Three storylines about the collapse of earlier wave of globalization, 1815-1913 (as summarized by Harold James 2001)

1. Inherent instabilities in global finance 2. Social and political backlash3. Overloading of institutions that manage globalization

What is common in each of these explanations is the imbalance between the global nature of markets and the national nature of institutions of governance

As a result, even globalization, even when it seems most secure, rests on weak foundations.

Can a similar reversal occur today?