the charlotte region: alive and well charlotte commercial market forecast march 27, 2012

TRANSCRIPT

The Charlotte Region: Alive and WellCharlotte Commercial Market Forecast

March 27, 2012

A Promise of Value. lincolnharris.com

The most common characteristic of the Charlotte region:

CHANGE

3 types of people:Those who fear change

Those who watch changeThose who embrace & enact change

A Promise of Value. lincolnharris.com

Non-residential construction permits trend upwards

Jan-

09

Apr-0

9

Jul-0

9

Oct-0

9

Jan-

10

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

Apr-1

1

Jul-1

1

Oct-1

1

Jan-

12$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

Monthly non-residential construction permit value

2009-2010 avg: $60 million/month

2011-YTD 2012 avg: $107.7 million/month

Source: Charlotte Chamber of Commerce March 2012 Economic Indicators – Charlotte/Mecklenburg Building Standards Department

January 2012 spiked to $226 million due to construction at Ballantyne and corporate relocation build outs

A Promise of Value. lincolnharris.com

Charlotte’s office market is returning to health

Source: Lincoln Harris Research Department

47.1% of net move in activity in 2011 was from companies new to the Charlotte area

20002001

20022003

20042005

20062007

20082009

20102011

-500,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

0.00%

4.00%

8.00%

12.00%

16.00%

20.00%

24.00%

Net absorption New development Overall vacancy

Ch

arl

ott

e o

ffice

net

ab

sorp

tion

Ch

arl

ott

e o

ffice

vaca

ncy

A Promise of Value. lincolnharris.com

Major players that grew or expanded into Charlotte in 2011

Compass Group Connextions Extended Stay SnapAV Wake Forest

University Akima Lash Group MNES Capgemini FBI FNB United

Bradley Arant HireRight Certus Bnak Chelsea Therapeutics Northeastern

University Heels.com Deb Group CNL Crosland QuikTrip Lockton Ravin Partners

Source: Lincoln Harris Research Department

This is just a sampling of the diverse firms that grew organically or relocated to Charlotte recently

A Promise of Value. lincolnharris.com

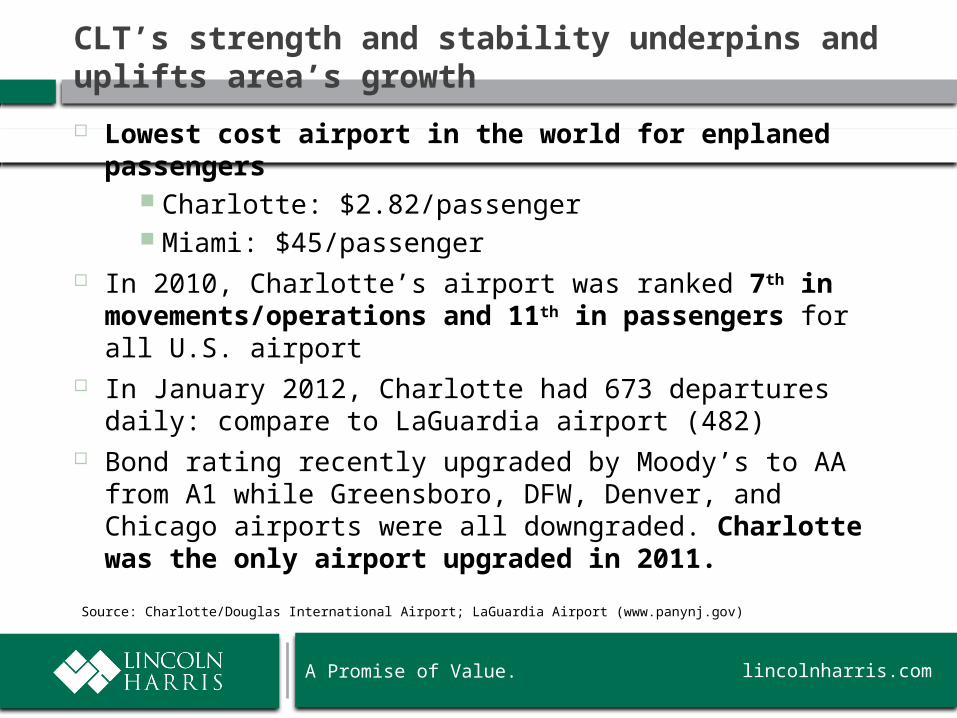

CLT’s strength and stability underpins and uplifts area’s growth

Lowest cost airport in the world for enplaned passengers

Charlotte: $2.82/passenger Miami: $45/passenger

In 2010, Charlotte’s airport was ranked 7th in movements/operations and 11th in passengers for all U.S. airport

In January 2012, Charlotte had 673 departures daily: compare to LaGuardia airport (482)

Bond rating recently upgraded by Moody’s to AA from A1 while Greensboro, DFW, Denver, and Chicago airports were all downgraded. Charlotte was the only airport upgraded in 2011.

Source: Charlotte/Douglas International Airport; LaGuardia Airport (www.panynj.gov)

A Promise of Value. lincolnharris.com

Charlotte’s airport growth continues, outpacing national trends

2,000,000.0

2,200,000.0

2,400,000.0

2,600,000.0

2,800,000.0

3,000,000.0

3,200,000.0

3,400,000.0

3,600,000.0

3,800,000.0

CLT total monthly passenger traf-fic

CLT total passenger traffic (enplanements & de-planements)

Year

Total annual

passenger traffic

% Change

from previous year

2011

39,043,708 2.06%

2010

38,254,207 10.76%

2009

34,536,666 -0.58%

2008

34,739,020 4.74%

2007

33,165,688 11.69%

2006

29,693,949 N/A

Source: Charlotte/Douglas International Airport Aviation Activity for January 2012

After enjoying nearly 11% growth in 2010, CLT again boosted its passenger traffic by 2% in 2011

A Promise of Value. lincolnharris.com

CLT is a key component of Charlotte’s burgeoning logistics hub

Jan-

09

Apr-0

9

Jul-0

9

Oct-0

9

Jan-

10

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

Apr-1

1

Jul-1

1

Oct-1

1

Jan-

120.0

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0

12,000.0

14,000.0

CLT cargo enplaned/deplaned (tons)

CLT cargo enplaned/deplaned (tons)

Year

Total annual cargo

enplaned/ deplaned

% Change

from previous year

2011 137,943 2.68%

2010 134,342 12.37%

2009 119,551 -9.44%

2008 132,009 -7.57%

2007 142,819 -15.82%

2006 169,649 -7.33%

2005 183,072 0.05%

2004 182,978 18.47%

2003 154,448 -12.46%

2002 176,436 -9.92%

2001 195,870 -11.11%

2000 134,342 N/A

After years of declining cargo tonnage, cargo routed through Charlotte has expanded in 2010 and 2011

Source: Charlotte/Douglas International Airport Aviation Activity for January 2012

A Promise of Value. lincolnharris.com

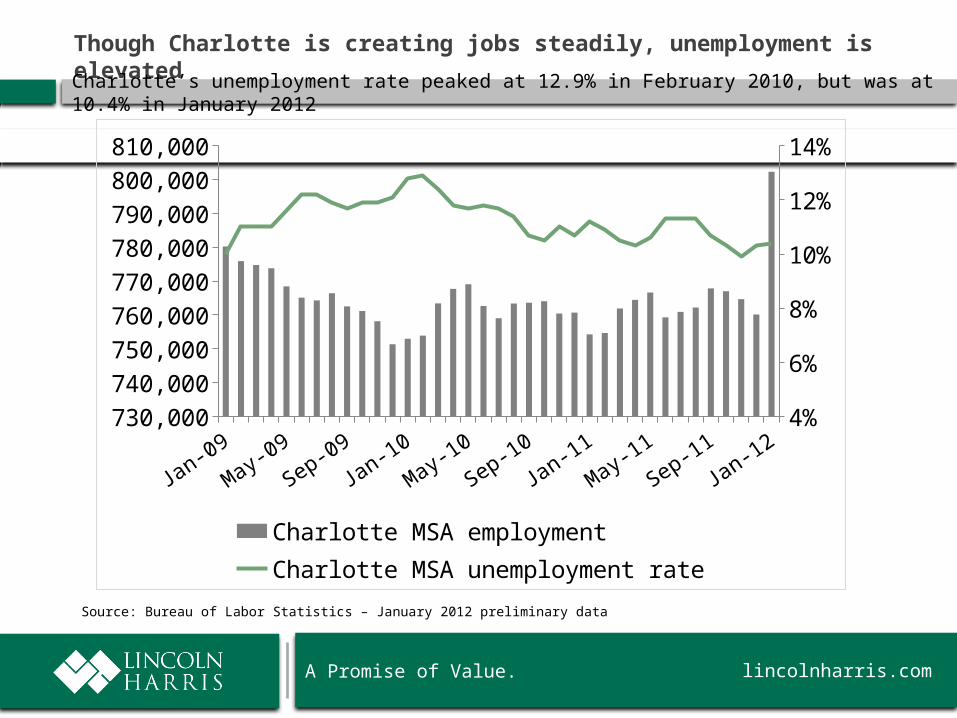

Though Charlotte is creating jobs steadily, unemployment is elevated

Source: Bureau of Labor Statistics – January 2012 preliminary data

Charlotte’s unemployment rate peaked at 12.9% in February 2010, but was at 10.4% in January 2012

Jan-09

May-09

Sep-09Jan-10

May-10

Sep-10Jan-11

May-11

Sep-11Jan-12

730,000

740,000

750,000

760,000

770,000

780,000

790,000

800,000

810,000

4%

6%

8%

10%

12%

14%

Charlotte MSA employmentCharlotte MSA unemployment rate

A Promise of Value. lincolnharris.com

Since January 2010, Charlotte has enjoyed widespread private sector hiring

Series1

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Mining, Logging, & Construction

Manufacturing

Trade, Transportation, & Utilities

Information

Financial Activities

Professional & Business Services

Education & Health Services

Leisure & Hospitality

Other Services

Government

Trade-related positions increased 8,400, while professional and business jobs jumped 14,900 during that time

Source: Bureau of Labor Statistics – Not seasonally adjusted data by industry from January 2010 to January 2012

A Promise of Value. lincolnharris.com

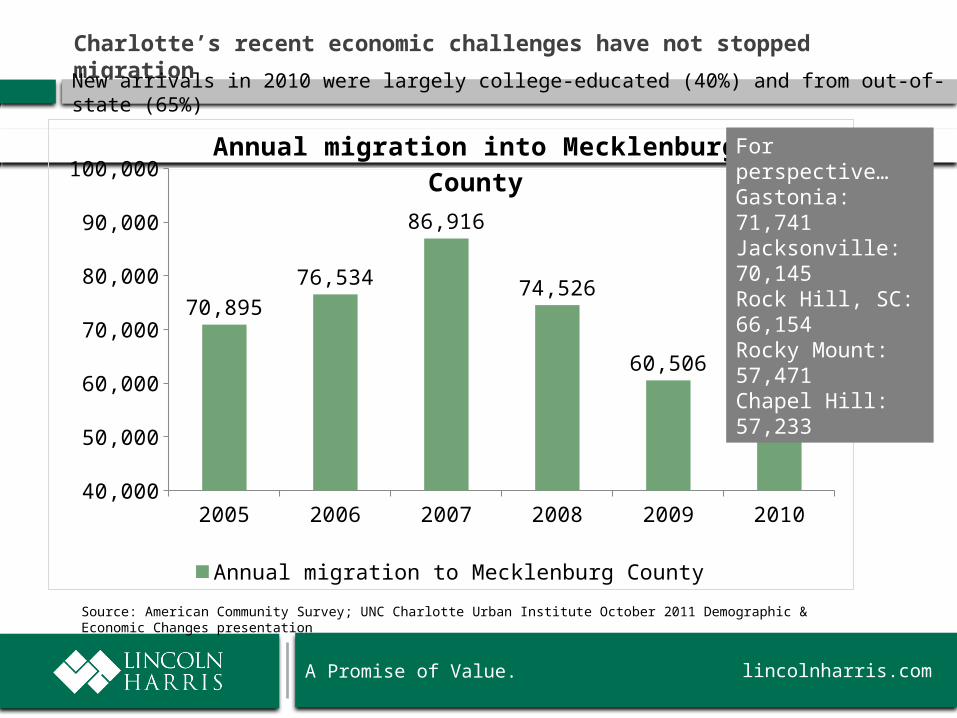

Charlotte’s recent economic challenges have not stopped migration

2005 2006 2007 2008 2009 201040,000

50,000

60,000

70,000

80,000

90,000

100,000

70,89576,534

86,916

74,526

60,506

66,376

Annual migration into Mecklenburg County

Annual migration to Mecklenburg County

Source: American Community Survey; UNC Charlotte Urban Institute October 2011 Demographic & Economic Changes presentation

New arrivals in 2010 were largely college-educated (40%) and from out-of-state (65%)

For perspective…Gastonia: 71,741Jacksonville: 70,145Rock Hill, SC: 66,154Rocky Mount: 57,471Chapel Hill: 57,233

A Promise of Value. lincolnharris.com

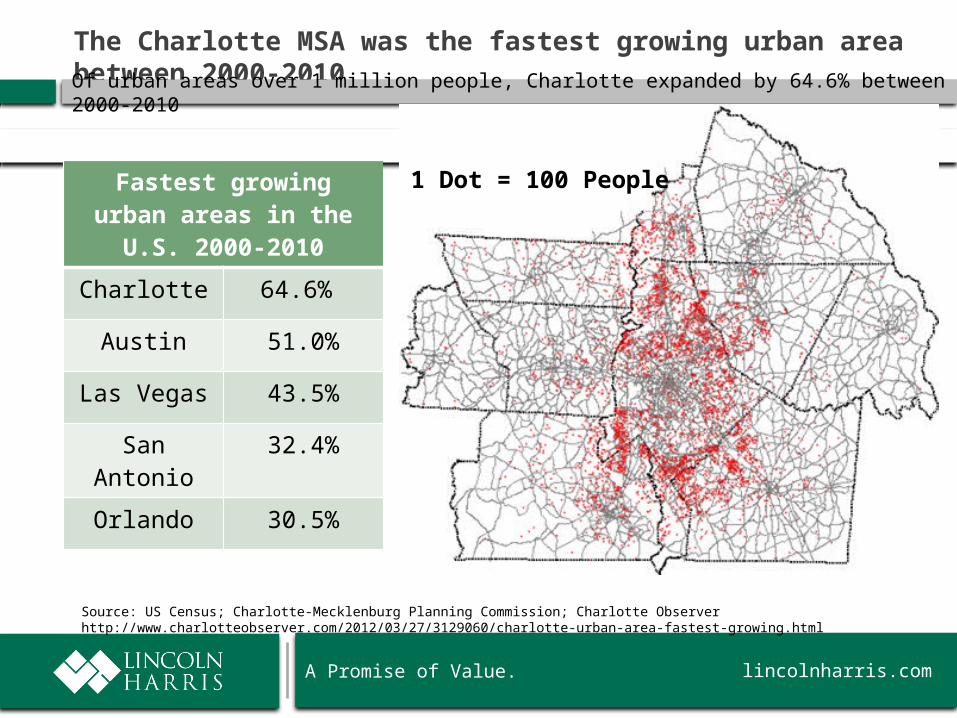

The Charlotte MSA was the fastest growing urban area between 2000-2010Of urban areas over 1 million people, Charlotte expanded by 64.6% between 2000-2010

Fastest growing urban areas in the

U.S. 2000-2010

Charlotte 64.6%

Austin 51.0%

Las Vegas 43.5%

San Antonio

32.4%

Orlando 30.5%

Source: US Census; Charlotte-Mecklenburg Planning Commission; Charlotte Observer http://www.charlotteobserver.com/2012/03/27/3129060/charlotte-urban-area-fastest-growing.html

1 Dot = 100 People

A Promise of Value. lincolnharris.com

Population growth and a shift towards more dense development is a significant challenge – and opportunity Community resources and a strong future-oriented plan for Charlottes needs to develop in-line with growth

Source: U.S. Census 2010; Charlotte-Mecklenburg Planning Commission

With this scale of growth, responsible, growth-oriented planning is an absolute necessity for strategic success

A Promise of Value. lincolnharris.com

Biggest issues facing Charlotte in the near- and mid-term?

Most prevalent concerns that people voice about Charlotte

Concentrated banking community Educational system Airport that is highly reliant on one major airline Leadership

However, none of these issues should be truly frightening or regarded as insurmountable as the economy improves. There are many reasons to believe in Charlotte’s bright future.