the case for consumer engagement in the funding of...

TRANSCRIPT

IAAHS 2007IAA Health Section Colloquium

13th – 16th May 2007CTICC

www.iaahs2007.com

The case for consumer engagement in the funding of healthcare

Adrian Gore, CEO Discovery

Agenda

1. Context

2. Discovery’s approach to healthcare funding

3. Does consumer engagement work? A data analysis

1. Context

South Africa has a large population, with disparate access to healthcare resources

Insured Uninsured Private sector Public sector

Healthcare spendingPopulation

40.5m 6.9m R75bn R59bn

VariableVariableVariable South Africa High Income Population*South Africa High South Africa High

Income Population*Income Population* United StatesUnited States

Household Income (USD at PPP)Household Income (USD at PPP) $44,977$44,977 $41,994$41,994

Possession of college / university degreePossession of college / university degree 66.7%66.7% 32.7%32.7%

Access to the internetAccess to the internet39.5%39.5% 59.6%59.6%

Own / rent a cellular telephoneOwn / rent a cellular telephone 94.6%94.6% 42.5%42.5%

Households with two or more motor vehiclesHouseholds with two or more motor vehicles

Access to digital satellite / digital cable TV at homeAccess to digital satellite / digital cable TV at home

60.2%60.2%

23.1%23.1%

55.5%55.5%

33.7%33.7%

Note: *High income population refers to the top 20% of earners; Most data points are estimates based on the most recently available informationSource: AMPS 2000; U.S. Census Bureau; Statistics SA

South Africa’s high-income population displays similar tendencies to US population

Healthcare funding models – who makes the choices?

Supply-sidecontrol

HospitalsPhysiciansMedical services

ContractsManaged careProtocolsNetworksDisease management

Demand-sidecontrol Patients

InformationEmpowering choices & doctor-patient relationships

The Medical Schemes Act legislates community-rating for premium determination

29(n) The terms and conditions applicable to the admission of a person as a member and his or her dependants, which terms and conditions shall

provide for the determination of contributions on the basis of income or the number of dependants or both the income and the number of dependants,

and shall not provide for any other grounds, including age, sex, past or present state of health, of the applicant or one or more of the applicant's dependants, the frequency of rendering of relevant health services to an applicant or one or more of the applicant's dependants other than for the

provisions as prescribed.

CHAPTER 5: RULES OF MEDICAL SCHEME

Source: Monitor - Discovery Health Global Health Plan Markets Database, William M. Mercer, Towers Perrin, Watson/Wyatt, PwC, Hewitt Associates, Kaiser Family Foundation, U.S. Census, Mercer National Accounts Survey, Discovery Health, Monitor Analysis

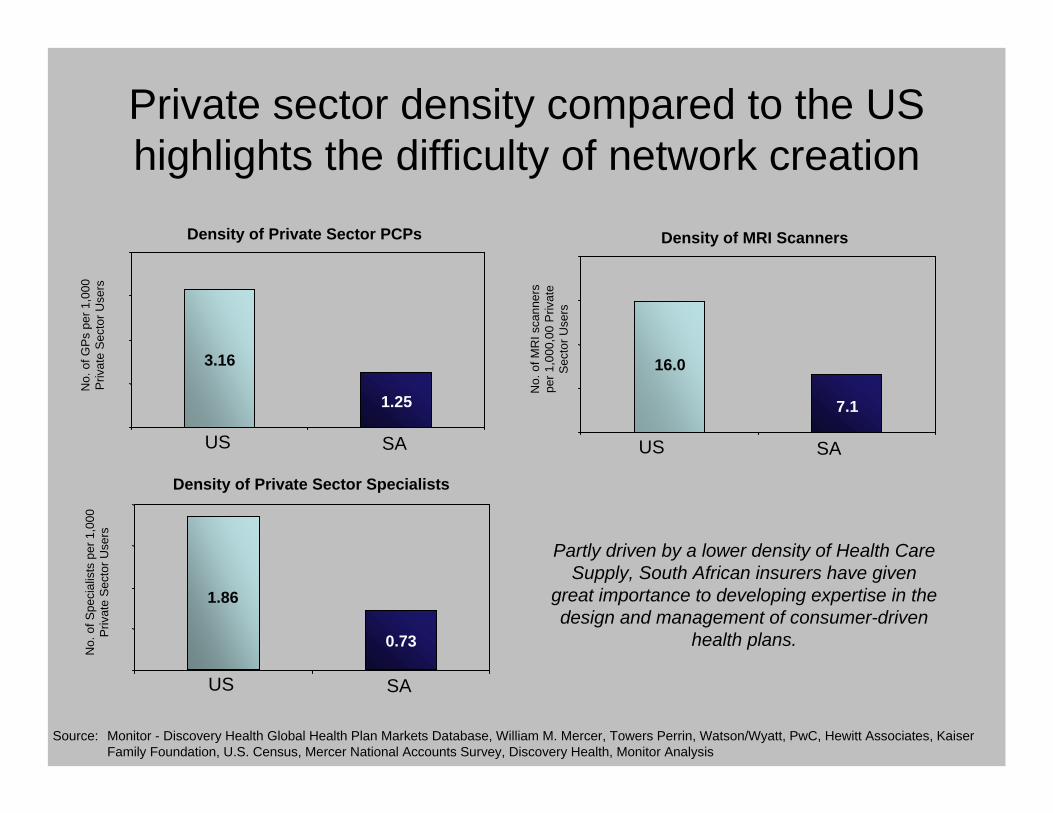

Density of Private Sector PCPs

No.

of G

Ps

per 1

,000

P

rivat

e S

ecto

r Use

rs

1.25

3.16

US SA

No.

of S

peci

alis

ts p

er 1

,000

Priv

ate

Sec

tor U

sers

Density of Private Sector Specialists

0.73

1.86

US SA

Density of MRI Scanners

No.

of M

RI s

cann

ers

per 1

,000

,00

Priv

ate

Sec

tor U

sers

7.1

16.0

US SA

Partly driven by a lower density of Health Care Supply, South African insurers have given

great importance to developing expertise in the design and management of consumer-driven

health plans.

Private sector density compared to the US highlights the difficulty of network creation

2.Discovery’s approach to healthcare funding – engaging the consumer in health and wellness

UncontrollableUncontrollable

ControllableControllable

Prevention and fitnessPrevention and fitness

CDH as a model solution

Triangle of healthcare utilization

Cost

Frequency

Health SavingsAccount

Health SavingsAccount

VitalityVitality

InsuredbenefitsInsuredbenefits

Discovery’s consumer-engaged model

Discovery currently covers over 2m lives on consumer-directed plans

0

500,000

1,000,000

1,500,000

2,000,000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Covered lives as at 31 December

Manufacturing

ReligiousMiningGovernment Medical

AgricultureLeisure

EducationEntertainmentTransportation

Professionals

Engineering

Retail

Other

ServicesFinancial

Technology

1 to 10

11 to 50

51 to 100

101 to 500

501 to 1,000

Above 1,000

Member distribution by Industry

Member distribution by Group Size

Sample List of Discovery Clients

Diversity of Discovery’s membership

HSA limits consumer choice to areas where rational decisions can be made

Health SavingsAccount

Health SavingsAccount

InsuredbenefitsInsuredbenefits

Structure of the Vitality Wellness program

3. Does consumer engagement work?- A data analysis

Robust actuarial data set on which to conduct the analysis

Annual lapse rate

0.0%

1.0%

2.0%

3.0%

4.0%

2003 2004 2005 200660

70

80

90

100

110

120

2003 2004 2005 2006

Life months (millions)

Discovery’s membership base is typical of the overall insured population

Risk Equalisation Fund Impact

Source: Centre for Actuarial Research

0

5

10

15

20

25

30

35

40

<-50

%

-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10% -5% 0% 5% 10%

15%

20%

25%

30%

35%

40%

45%

50%

>50%

REF Impact on Contributions

Num

ber o

f Sch

emes

(n=1

41)

Members pay moreMembers pay less

Discovery

-

Key questions

1. The effect of Health Savings Accounts

2. The effect of consumer-induced preventative care

The effect of Health Savings Accounts

1. Are HSA’s good for the healthy and sick?

2. Do people change their behaviour?

3. Is there an adverse effect on health?

4. Is there a point where HSA’s result in systemic changes to the health system?

Are HSA’s good for the healthy and sick?

Day-to-day expenditure analysis

Consumer driven plan Traditional plan

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Claims incurred (R’000s)

60%

70%

80%

90%

100%

110%

120%

130%

benefits/claims

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Claims incurred (R’000s)

60%

70%

80%

90%

100%

110%

120%

130%

benefits/claims

60%

70%

80%

90%

100%

110%

120%

130%

benefits/claims Members are

better off because of the use it or keep it model

Members are better off because benefits are largely unlimited

Cov

erag

e %

Level of sickness

Day-to-day expenditure analysis

Consumer driven planConsumer driven plan Traditional planTraditional plan

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Claims incurred (R’000s)

60%

70%

80%

90%

100%

110%

120%

130%

benefits/claims

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Claims incurred (R’000s)

60%

70%

80%

90%

100%

110%

120%

130%

benefits/claims

60%

70%

80%

90%

100%

110%

120%

130%

benefits/claims

Healthy ? Sick

Cov

erag

e %

Level of sickness

Impact on transient group

Longitudinal study of transient behaviour

Healthy Transient Sick

42% 22% 36%

Year

1

2

3

8%

37% 29%

3%

29% 40%

87% of initial transient group shift, meaning that the transient members are ultimately better off

Do people change their behaviour?

HSA limits consumer choice to areas where rational decisions can be made

Health SavingsAccount

Health SavingsAccount

InsuredbenefitsInsuredbenefits

Longitudinal study – Is the medical trend of services covered mainly by MSA’s under control?

Indexed Real PCP spend pmpm(Comprehensive Plans Only)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Total Exposure Considered: ±38.5m member months over 5.5 years* Real rate calculated by adjusting for CPI inflation as per Statistics SA

Yr 1 Yr 5.5

Indexed Real Pathology spend pmpm(Comprehensive Plans Only)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2000

01

2000

04

2000

07

2000

10

2001

01

2001

04

2001

07

2001

10

2002

01

2002

04

2002

07

2002

10

2003

01

2003

04

2003

07

2003

10

2004

01

2004

04

2004

07

2004

10

2005

01

2005

04

In-Hospital Out-of-Hospital

Indexed Real Physical Therapy spend pmpm(Comprehensive Plans Only)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

2000

01

2000

04

2000

07

2000

10

2001

01

2001

04

2001

07

2001

10

2002

01

2002

04

2002

07

2002

10

2003

01

2003

04

2003

07

2003

10

2004

01

2004

04

2004

07

2004

10

2005

01

2005

04

Total Exposure Considered: ±38.5m member months over 5.5 years* Real rate calculated by adjusting for CPI inflation as per Statistics SA

Longitudinal study – Long-term medical trend of pathology and physical therapy services

In-Hospital Out-of-Hospital

Yr 1 Yr 5.5 Yr 1 Yr 5.5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dermatologists Dieticians Homeopaths Physical Therapists

Insured benefit

Funded from MSA

Rel

ativ

e co

sts

per m

embe

r per

mon

th

21% reduction

30% reduction

24% reduction

40% reduction

21% to 40% increase in medical practitioner spend when funded from the insured benefit

Case study 1: Impact on Hormone Replacement Therapy Spend

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8Ja

n-99

Mar

-99

May

-99

Jul-9

9

Sep-

99

Nov

-99

Jan-

00

Mar

-00

May

-00

Jul-0

0

Sep-

00

Nov

-00

Am

ount

pai

d pe

r mem

ber

per m

onth

(Ran

ds)

Covered from Savings Account

Covered from Insured Chronic Benefit

Case study 2: Impact on Attention Deficit Disorder Spend

Ritalin - average claims

0

50

100

150

200

250

Jan-

99

Mar

-99

May

-99

Jul-9

9

Sep-

99

Nov

-99

Jan-

00

Mar

-00

May

-00

Jul-0

0

Sep-

00

Nov

-00

Act

ual s

pend

Paid from Insured chronic benefitPaid from Savings Account

MRI - In Hospital Relative Utilisations

0.00

0.25

0.50

0.75

1.00

1.25

1.50

Q1-

2000

Q2-

2000

Q3-

2000

Q4-

2000

Q1-

2001

Q2-

2001

Q3-

2001

Q4-

2001

Q1-

2002

Q2-

2002

Q3-

2002

Q4-

2002

Q1-

2003

Q2-

2003

Q3-

2003

Q4-

2003

Q1-

2004

Q2-

2004

Q3-

2004

Q4-

2004

Q1-

2005

Q2-

2005

Co-

paym

ent r

emov

ed

Case study: Impact of consumer-driven healthcare in curbing in-hospital MRI utilisation

Is there an adverse effect on health?

Longitudinal study – Does the hospital admit rate increase with duration on the CDHC Plan?

0

20

40

60

80

100

120

2002 2003 2004 2005 2006

Yr of joining 2nd calendar year 3rd calendar year 4th calendar year 5th calendar year > 5 calendar years

Relative Hospital Events per 1000 members per month (Comprehensive Plans, 2nd Year Claims = 100)

No evidence of negative longer-term health implications

Longitudinal study – Hospital admit rates for chronic and non-chronic members

Admit Rate for Comprehensive plansby Duration - Chronic

0

20

40

60

80

100

120

2002 2003 2004 2005 2006 2002 2003 2004 2005 20060

20

40

60

80

100

120

Yr of joining 2nd calendar year 3rd calendar year 4th calendar year 5th calendar year > 5 calendar years

Admit Rate for Comprehensive plansby Duration – Non-chronic

Longitudinal study – Hospital admit rates for diabetic members

Admit Rate For Diabetic Members

50

60

70

80

90

100

110

120

2002 2003 2004 2005 2006

Yr of joining 2nd calendar year 3rd calendar year 4th calendar year 5th calendar year > 5 calendar years

Is there a point where HSA’s result in systemic changes to the health system?

Penetration of plans with HSA’s

*Estimated using HSA premiums as % of Total as per the Council of Medical Schemes Reports

Estimated market share of plans with HSAs *

0%

10%

20%

30%

40%

50%

60%

70%

80%

1998 1999 2000 2001 2002 2003 2004

Growth in medicine prices – consumers are able to influence price

OH Medicine - AcuteIH Drugs

Trend in Real Medicine Price Over Time

60

70

80

90

100

110

120

Feb-

01

May

-01

Aug

-01

Nov

-01

Feb-

02

May

-02

Aug

-02

Nov

-02

Feb-

03

May

-03

Aug

-03

Nov

-03

Feb-

04

May

-04

Aug

-04

Nov

-04

Feb-

05

May

-05

Medicine Pricing

Regulations

The effect of Health Savings Accounts

1. Are HSA’s good for the healthy and sick?

2. Do people change their behaviour?

3. Is there an adverse effect on health?

4. Is there a point where HSA’s result in systemic changes to the health system?

The effect of consumer-induced preventative care

1. Do people respond to incentives in preventative care?

2. Does a properly structured preventative care program impact on healthcare costs?

3. Is selection more important than behaviour?

Structure of the Vitality Wellness program

Do people respond to incentives in preventative care?

Vitality membership exceeds 1.2m members

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

1999 2000 2001 2002 2003 2004 2005 2006

Vitality lives Covered lives

Vitality has materially impacted the quantum of preventative care sought

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Prostatescreening

Cholesterolscreening (male)

Cholesterolscreening(female)

Mammograms Pap smears

Non-Vitality

Does a properly structured preventative care program impact on healthcare costs?

Do members at higher statuses have lower claims? Correlation between Vitality Status and

hospital admissions

50

60

70

80

90

100

Blue Bronze Silver GoldNon-Vitality

Non-Vitality

How Big are the Savings?

0%

50%

100%

150%

200%

GP consultations

Specialist consultations

Prescribed medication scripts

Hospital admissions

Tota

l cla

ims:

Blu

e Vi

talit

y m

embe

rs a

s a

% o

f br

onze

and

abo

ve m

embe

rs

Engaged Vitality member benchmark – Bronze and above

members

How Big are the Savings?

84%

86%

88%

90%

92%

94%

96%

98%

100%

Increase in engagement

10%

3.5%

20%

7%

30%

11%Percentage of current spend

on GP and specialist

consultations, medication

and hospitals

Current spend levels on GP and specialist

consultations, medication and hospitals

Is selection more important than behaviour?

Higher Vitality engagement amongst members with chronic illness

0%

10%

20%

30%

40%

50%

60%

<30 30-44 45-59 60+

Bronze and above Vitality participants All members

Chronic condition rate – family size of 3

Chr

onic

dis

ease

pre

vale

nce

Is the effect of moving through the statuses that results in lower claims? Longitudinal comparison of

common group who subsequently diverged

1998 1999 2000 2001 2002 2003

Members who upgraded one or more statuses

Control group: Members who remained on Blue

Common base period of inactivity (Blue status)

3m life months

208,431 entrants in 1998

5.7m life months

664,595 life months

Is the effect of moving through the statuses that results in lower claims? Longitudinal comparison of

common group who subsequently diverged

* Those on Blue 1998-2001 who subsequently changed status relative to those who remained on Blue

1998 1999 2000 2001 2002 20030.80

0.85

0.90

0.95

1.00

1.05

1.10

Chr

onic

PLP

M re

lativ

e to

con

trol

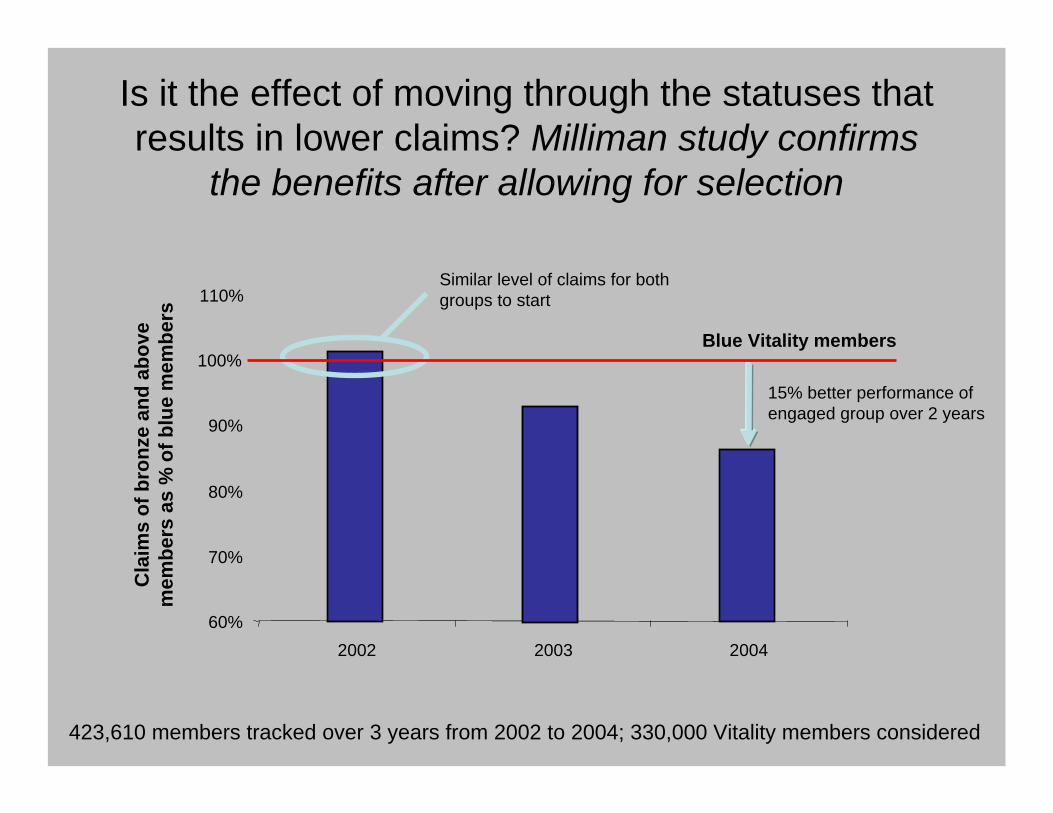

Is it the effect of moving through the statuses that results in lower claims? Milliman study confirms

the benefits after allowing for selection

60%

70%

80%

90%

100%

110%

20032002 2004

Cla

ims

of b

ronz

e an

d ab

ove

mem

bers

as

% o

f blu

e m

embe

rs

Blue Vitality members

15% better performance of engaged group over 2 years

Similar level of claims for both groups to start

423,610 members tracked over 3 years from 2002 to 2004; 330,000 Vitality members considered

The effect of consumer-induced preventative care

1. Do people respond to incentives in preventative care?

2. Does a properly structured preventative care program impact on healthcare costs?

3. Is selection more important than behaviour?

Key questions

The effect of Health Savings Accounts:1. Are HSA’s good for the healthy and sick?2. Do people change their behaviour?3. Is there an adverse effect on health?4. Is there a point where HSA’s result in systemic changes to the health

system?

The effect of preventative care:1. Do people respond to incentives in preventative care?2. Does a properly structured preventative care program impact on

healthcare costs?3. Is selection more important than behaviour?

Questions?

IAAHS 2007IAA Health Section Colloquium

13th – 16th May 2007CTICC

www.iaahs2007.com

The case for consumer engagement in the funding of healthcare

Adrian Gore, CEO Discovery