the buyers’ bonus mortgage program steve calem, mba, cmps vice president, real estate lending...

TRANSCRIPT

The Buyers’ Bonus Mortgage Program

Steve Calem, MBA, CMPS

Vice President, Real Estate Lending

American Bank

Tel: 240-482-0264

Buyers’ Bonus Mortgage Program - Program Highlights -

•The Buyers’ Bonus Mortgage Program feature allows seller/builder-paid principal and interest payments, for up to the first six (6) months, on one (1) unit primary residences that are:

• purchase-money transactions only• existing properties (previously occupied), or • newly constructed homes (not previously occupied)

Excellent option for Builders to sell slower-moving inventory!

Buyers’ Bonus Mortgage Program - Program Highlights -

•The amount of the principal and interest payments paid by the seller/builder must be for the full amount of the borrower’s principal and interest monthly payment.

•Partial payments and payments in half-month increments, such as, 1.5 months, 2.5 months and 3.5 months, are not allowed.

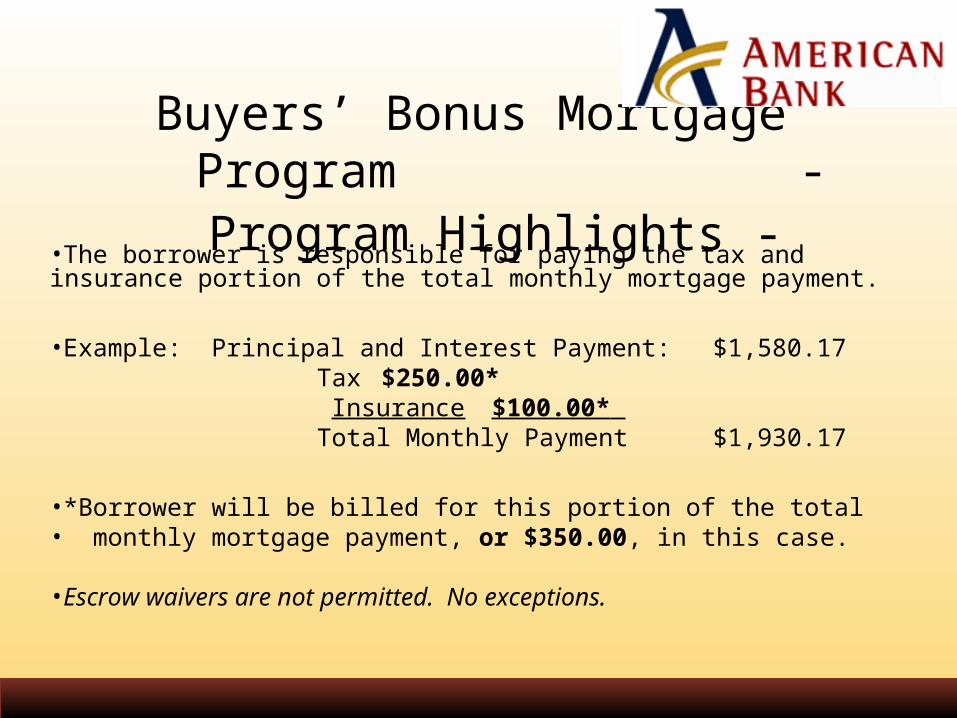

Buyers’ Bonus Mortgage Program - Program Highlights -

•The borrower is responsible for paying the tax and insurance portion of the total monthly mortgage payment.

•Example: Principal and Interest Payment: $1,580.17 Tax $250.00* Insurance $100.00* Total Monthly Payment $1,930.17

•*Borrower will be billed for this portion of the total• monthly mortgage payment, or $350.00, in this case.

•Escrow waivers are not permitted. No exceptions.

Buyers’ Bonus Mortgage Program - Program Highlights -

Eligible Occupancy Types

– One (1) unit primary residences– Units located in “warrantable” condominium projects– Units located in “warrantable” condominium conversion

projects, and– PUD projects

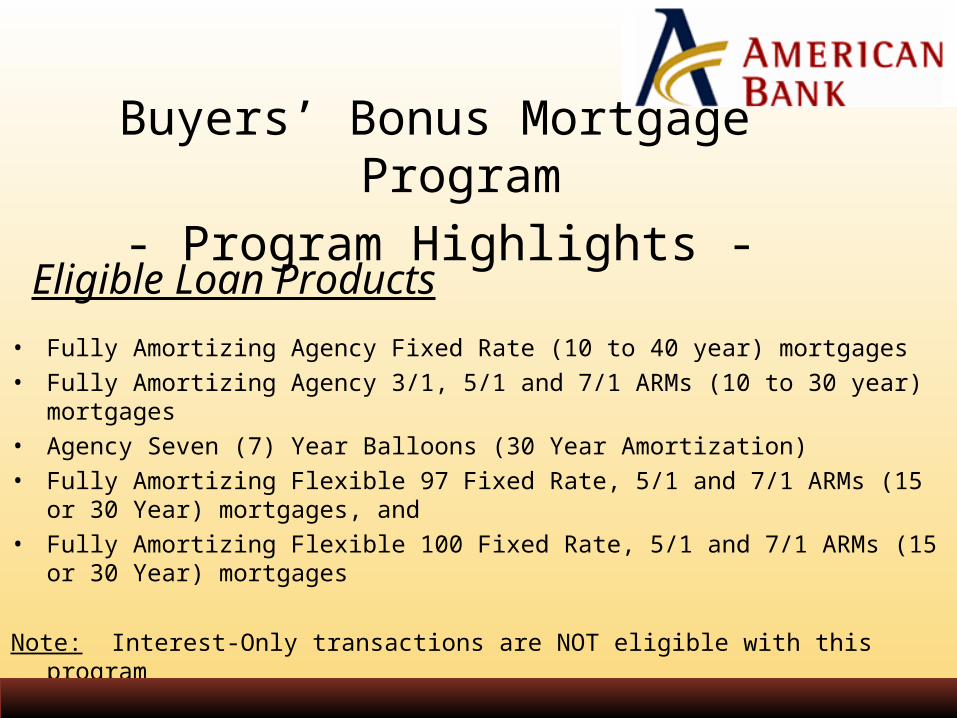

Eligible Loan Products

Buyers’ Bonus Mortgage Program

- Program Highlights -

• Fully Amortizing Agency Fixed Rate (10 to 40 year) mortgages• Fully Amortizing Agency 3/1, 5/1 and 7/1 ARMs (10 to 30 year) mortgages • Agency Seven (7) Year Balloons (30 Year Amortization)• Fully Amortizing Flexible 97 Fixed Rate, 5/1 and 7/1 ARMs (15 or 30 Year)

mortgages, and• Fully Amortizing Flexible 100 Fixed Rate, 5/1 and 7/1 ARMs (15 or 30 Year)

mortgages

Note: Interest-Only transactions are NOT eligible with this program

• Fully Amortizing Agency Express No Income Verification Fixed Rate and 7/1 ARMs (10 to 40 year) mortgages

• Fully Amortizing Agency Shortcut Fixed Rate (10-40 year), 3/1, 5/1 and 7/1 Arms, and

• Fully Amortizing Conforming Portfolio LIBOR 3/1, 5/1 and 7/1 (10-30 year) (Full Documentation and No Income Verification Options)

Note: Interest-Only transactions are NOT eligible with this program

Eligible Loan Products (cont’d)

Buyers’ Bonus Mortgage Program

- Program Highlights -

Buyers’ Bonus Mortgage Program - Program Highlights -

Eligible Loan Products (cont’d)Fully Amortizing Fannie Mae MyCommunity MortgageTM

Programs:

• MyCommunity 97 (15-30 year) Fixed Rate and 7/1 ARMs• MyCommunity 100 (15-30 year) Fixed Rate and 7/1 ARMs • MyCommunity 100 Plus (15-30 year) Fixed Rate and 7/1

ARMs Note: Interest-Only and 40 year terms are NOT eligible under

the Buyers’ Bonus Loan Program

Buyers’ Bonus Mortgage Program - Program Highlights -

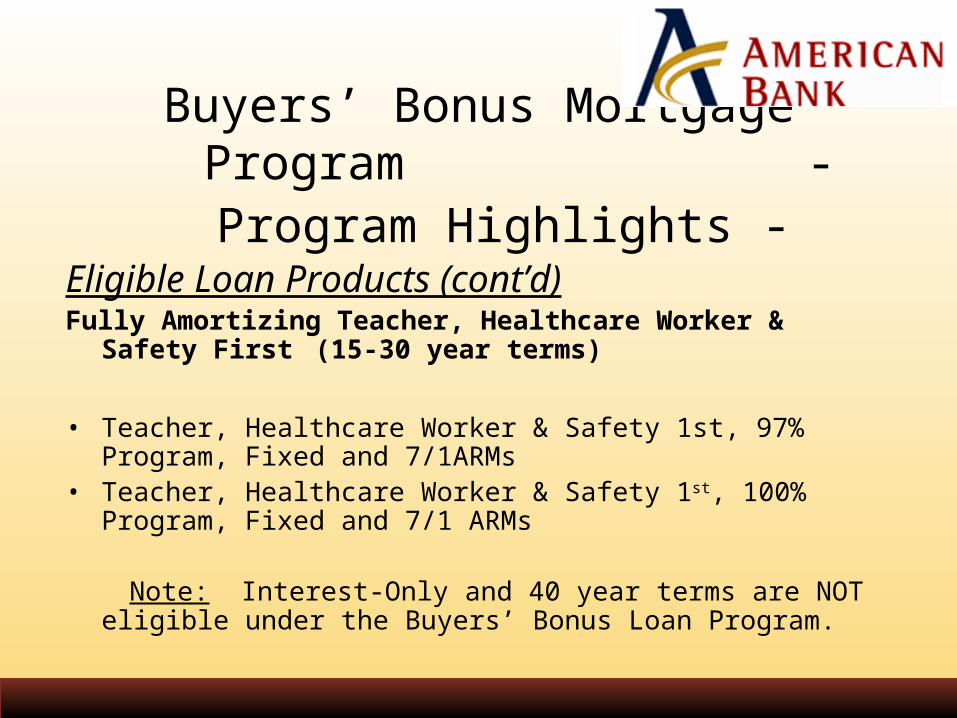

Eligible Loan Products (cont’d)Fully Amortizing Teacher, Healthcare Worker & Safety

First (15-30 year terms)

• Teacher, Healthcare Worker & Safety 1st, 97% Program, Fixed and 7/1ARMs

• Teacher, Healthcare Worker & Safety 1st, 100% Program, Fixed and 7/1 ARMs

Note: Interest-Only and 40 year terms are NOT eligible under the Buyers’ Bonus Loan Program.

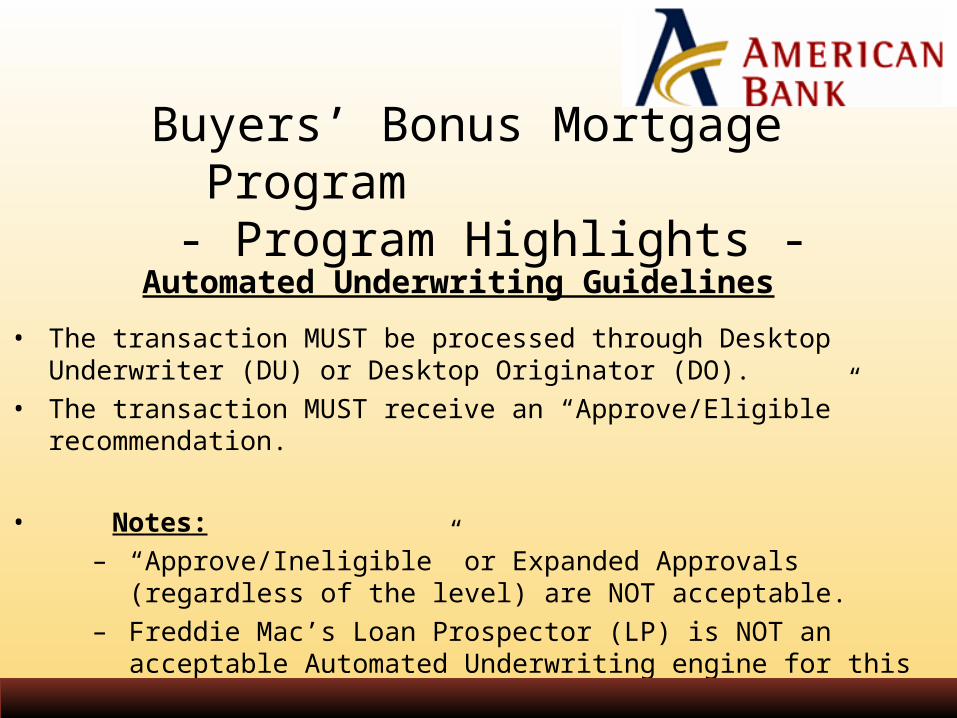

Automated Underwriting Guidelines

Buyers’ Bonus Mortgage Program

- Program Highlights -

• The transaction MUST be processed through Desktop Underwriter (DU) or Desktop Originator (DO).

• The transaction MUST receive an “Approve/Eligible” recommendation.

• Notes: – “Approve/Ineligible” or Expanded Approvals (regardless of

the level) are NOT acceptable.– Freddie Mac’s Loan Prospector (LP) is NOT an acceptable

Automated Underwriting engine for this program.

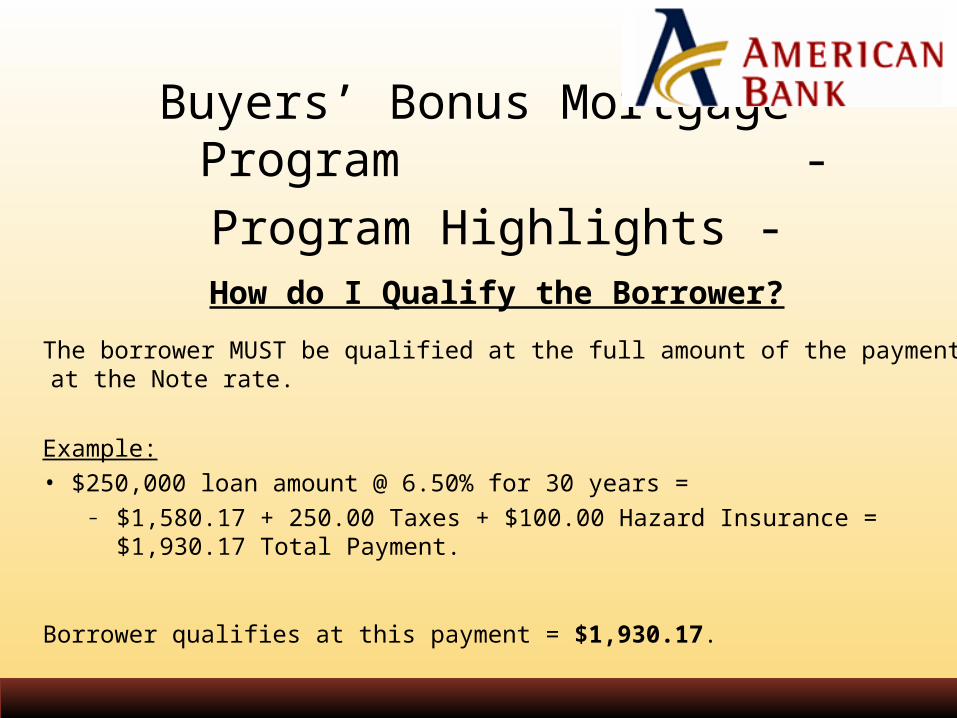

How do I Qualify the Borrower?

The borrower MUST be qualified at the full amount of the payment at the Note rate.

Example: • $250,000 loan amount @ 6.50% for 30 years =

– $1,580.17 + 250.00 Taxes + $100.00 Hazard Insurance = $1,930.17 Total Payment.

Borrower qualifies at this payment = $1,930.17.

Buyers’ Bonus Mortgage Program

- Program Highlights -

The amount of the principal and interest payments made by the seller/builder MUST be included in the calculation of the total “Seller Contribution” limits.

Example: If the total contribution limit is 6% or $15,000, (based on a $250,000 loan amount), and 6 months of the total Principal and Interest payments at $1,580.17, equaled $9,481.02 or approximately 4%, the $9,481.02 counts towards the total seller contribution limits. The seller has an additional $5,518.98 or approximately 2% (in this example) to use towards the borrower’s other closing costs.

Seller Contribution Limits

Buyers’ Bonus Mortgage Program - Program Highlights -

Buyers’ Bonus Mortgage Program

- Program Highlights -

Important items to remember about this program:

• Seller contributions CANNOT be applied towards the borrower’s minimum contribution towards the transaction or downpayment.

• Seller contributions MAY NOT exceed ACTUAL COSTS, resulting in cash to the borrower.

Seller Contribution Limits (cont’d)

Under the “Buyers’ Bonus Mortgage Loan Program, the seller contributions* may be applied to the actual costs of:• Permanent interest rate buydowns,• Temporary buydowns,• Closing costs (including discount points),• Prepaid items: interest, taxes, hazard, mortgage insurance, etc.),• Cost of property repairs, and • Up to the first six (6) months of the borrower’s P&I payments.

* In all cases, these contributions are subject to contribution limits.

Seller Contribution Limits (cont’d)

Buyers’ Bonus Mortgage Program

- Program Highlights -

The “Buyers’ Bonus Mortgage Program Agreement” Form (COR 0012) must be signed by:

• The Lender• The Borrower, and• The Provider of the Funds (i.e., the Seller or Builder)

Closing a Loan with a “Buyers’ Bonus” Contribution

Buyers’ Bonus Mortgage Program - Program Highlights -

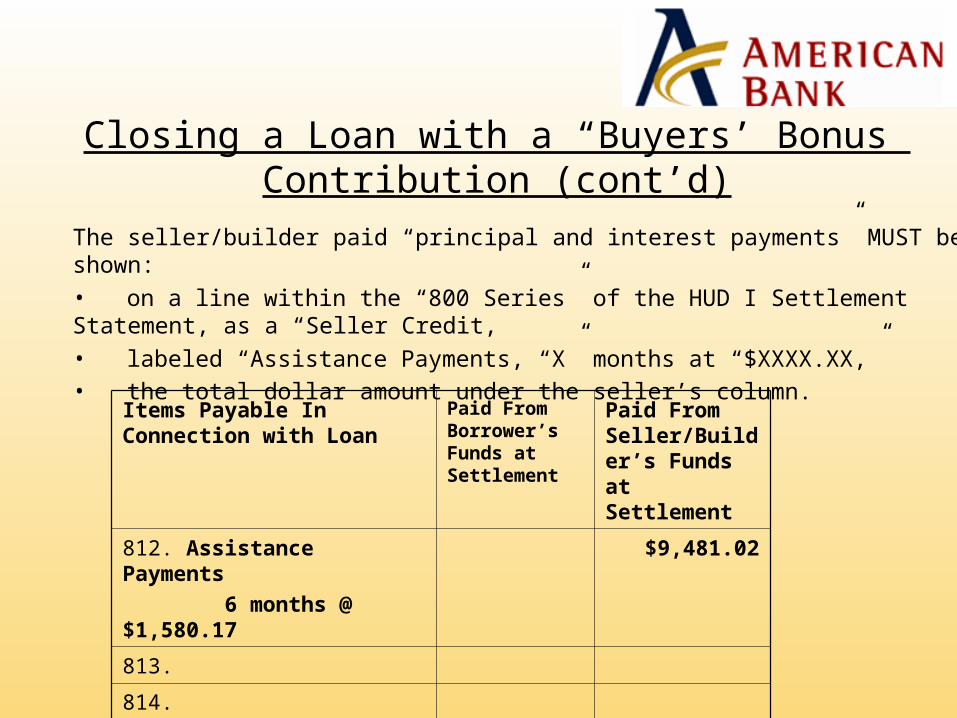

The seller/builder paid “principal and interest payments” MUST be shown:• on a line within the “800 Series” of the HUD I Settlement Statement, as a “Seller Credit, • labeled “Assistance Payments, “X” months at “$XXXX.XX,” • the total dollar amount under the seller’s column.

Items Payable In Connection with Loan

Paid From Borrower’s Funds at Settlement

Paid From Seller/Builder’s Funds at Settlement

812. Assistance Payments

6 months @ $1,580.17

$9,481.02

813.

814.

Closing a Loan with a “Buyers’ Bonus” Contribution (cont’d)

Important items to remember about this program:

The amount of the “principal and interest payments” paid by the Seller/Builder MUST for the FULL AMOUNT of the principal and interest portion of the monthly payment.

Partial payments are NOT allowed.

Payments in half-month increments (i.e., 1.5 months, 2.5 months, 3.5 months, etc.) are NOT allowed.

Closing a Loan with a “Buyers’ Bonus” Contribution (cont’d)

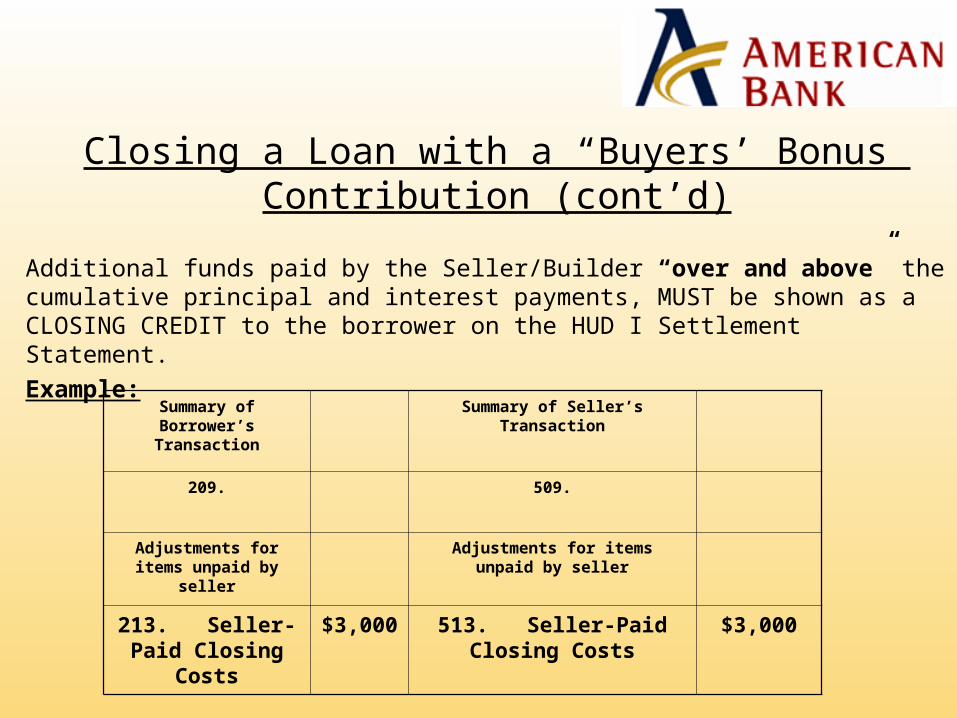

Additional funds paid by the Seller/Builder “over and above” the cumulative principal and interest payments, MUST be shown as a CLOSING CREDIT to the borrower on the HUD I Settlement Statement.Example:

Summary of Borrower’s Transaction

Summary of Seller’s Transaction

209. 509.

Adjustments for items unpaid by seller

Adjustments for items unpaid by seller

213. Seller-Paid Closing Costs

$3,000 513. Seller-Paid Closing Costs

$3,000

Closing a Loan with a “Buyers’ Bonus” Contribution (cont’d)

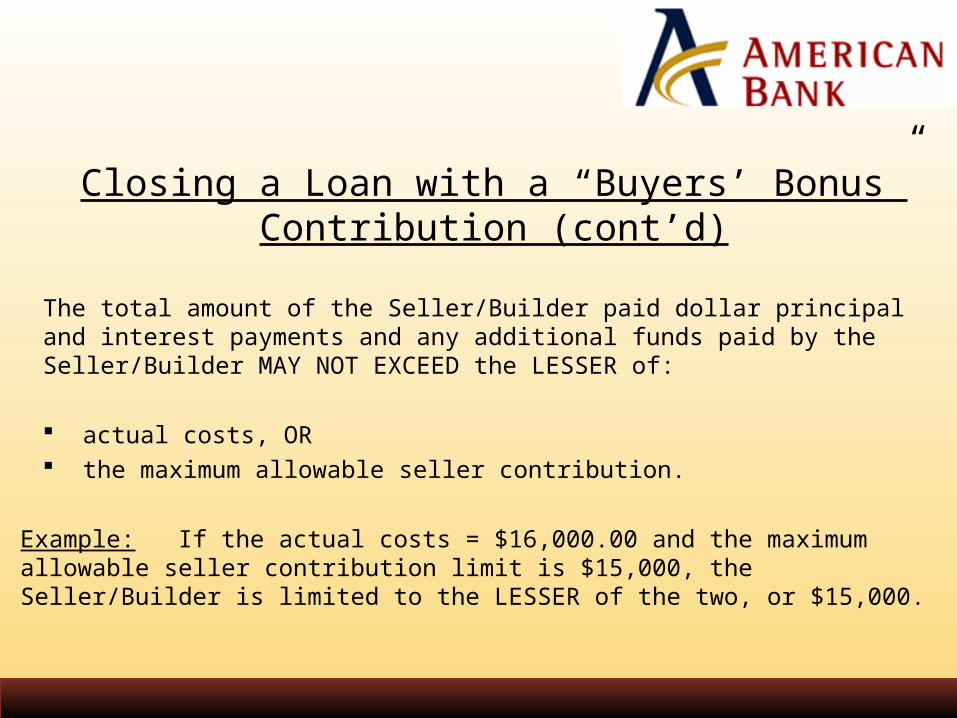

The total amount of the Seller/Builder paid dollar principal and interest payments and any additional funds paid by the Seller/Builder MAY NOT EXCEED the LESSER of:

actual costs, OR the maximum allowable seller contribution.

Example: If the actual costs = $16,000.00 and the maximum allowable seller contribution limit is $15,000, the Seller/Builder is limited to the LESSER of the two, or $15,000.

Closing a Loan with a “Buyers’ Bonus” Contribution (cont’d)

What happens once American Bank Mortgage receives the loan?

The Seller/Builder paid PRINCIPAL AND INTEREST payments shown on the HUD I Settlement Statement, will be disbursed by the Servicer on a monthly basis, and

The borrower will be billed for the TAX and INSURANCE escrow payments.

Note: Escrow waivers are NOT permitted. No Exceptions.

The Servicer will back out the Seller/Builder paid INTEREST for year-end reporting purposes on the IRS Form 1098.

Closing a Loan with a “Buyers’ Bonus” Contribution (cont’d)

Answer: This program allows for seller contributions, and not seller concessions, which still must be subtracted from the sales price before calculating the LTV. Seller contributions are now calculated on the LTV rather than the TLTV and can be as much as 9% depending on the LTV.

Questions and Answers

Question: Can you clarify whether or not this is a seller concession or a seller contribution?

Answer: Calculating the principal and interest cannot be done until the terms of the mortgage have been determined. The Buyers’ Bonus Mortgage Program is used to attract homebuyers. The borrower may need to renegotiate with the builder/seller once the program they want is known.

Questions and Answers

Question: How do you calculate the amount the seller is paying towards principal and interest up front?

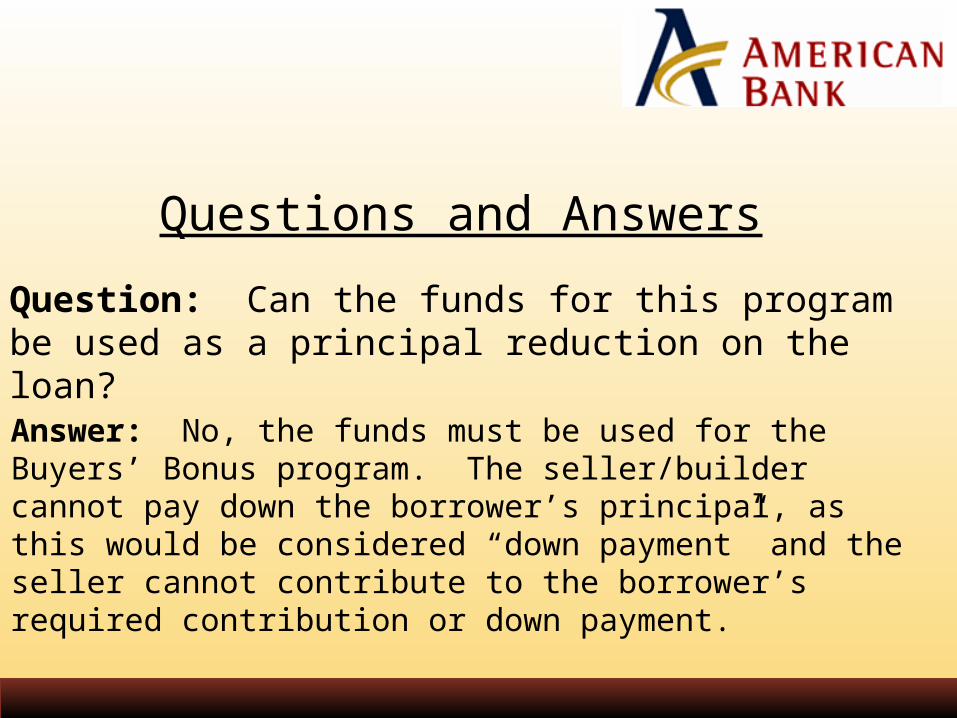

Answer: No, the funds must be used for the Buyers’ Bonus program. The seller/builder cannot pay down the borrower’s principal, as this would be considered “down payment” and the seller cannot contribute to the borrower’s required contribution or down payment.

Questions and Answers

Question: Can the funds for this program be used as a principal reduction on the loan?

Answer: The seller/builder paid principal and interest payments shown on the HUD-1 will be disbursed by the servicer on a monthly basis, and the borrower will be billed for the tax and insurance escrow payments.

Questions and Answers

Question: Can the funds for this program be used as a principal reduction on the loan?

Answer: Yes. Since the tax and insurance payment from the borrower triggers the Principal and Interest to be applied to the loan by the Servicer, if the borrower makes their tax and insurance payment late, this will cause the entire payment to be applied late.

Questions and Answers

Question: What if the borrower pays their Tax and Insurance payment late? Will the payment be counted as late?

Answer: The borrower will pay the estimated amount until the taxes are re-assessed.

Questions and Answers

Question: For a new construction property, where the taxes are estimated, how much will the borrower actually pay?

Answer: The seller/builder paid principal and interest payments must be shown on a line within the 800 series of the HUD-1 settlement statement as a seller credit and labeled “Assistance Payments, X months at $XXX.XX”, with the total dollar amount under the seller’s column. Additional funds paid by the seller/builder over and above the cumulative principal and interest payments must be shown as a closing cost credit to the borrower on the HUD-1 settlement statement.

Questions and Answers

Question: Are the seller contributions itemized on the HUD-1?

Answer: The borrower can only get money back on a 100% TLTV loan if it is over and above the required investment. The Flex 100, for example, requires that the borrower put in a minimum of $500 of their own funds towards closing costs and prepaids. The borrower cannot get this money back at closing.

Questions and Answers

Question: Is the borrower allowed to receive money back from the earnest money deposit (EMD) at closing?

Answer: The maximum seller contribution depends on your program and loan terms. The maximum seller contribution can be anywhere from 3% to 9%, depending on the LTV. Remember, this program is only for 1 Unit Primary residences.

Questions and AnswersQuestion: Is the maximum seller contribution six percent (6%)?

Answer: As long as they are not required repairs the appraiser or underwriter needs done prior to closing.

Questions and Answers

Question: Can the money the borrower is saving from not making the first six (6) months principal and interest payments be put towards repairs to the house?

Answer: Since this is an Agency program, the maximum loan amount allowed is the conforming loan limit of $417,000.

Questions and Answers

Question: What is the maximum loan amount allowed on the Buyers’ Bonus Mortgage Program?

Answer: American Bank does not issue a 1098 to the seller. The lender should advise the seller to check with their tax preparer to see how the interest they are paying on behalf of their buyer will impact their taxes. Also, the Servicer will back out the seller/builder paid interest for year-end reporting purposes to the borrower, since they cannot use as part of the interest paid on the loan. The borrower does not pay it, so they are not allowed to claim it on their taxes.

Questions and Answers

Question: Is the 1098 issued to the buyer or the seller?