the business environment in china in the year · pdf filethe business environment in china in...

TRANSCRIPT

Confidential © InterChina

The Business Environment in

China in the Year 2013

InterChina ConsultingNovember 2012

Confidential © InterChina

Jan BorgonjonPresident

2012 has been the year where the dazzling China growth of the last 10-15years has come to an end. Slower growth does not mean slow growthhowever, and corporate performance has been between acceptable to verygood, depending on the sector. With the successful conclusion of the PartyCongress this November, the political situation has cleared up and weexpect a relatively stable period ahead.For 2013, we foresee a year of continued growth, but slower and morefragmented and with higher uncertainty. Costs will go up and growth mightslow as China´s shifts to a new growth model. However GDP growth willremain at 6-7% for the next decade, while income levels will go up,consumption will continue to grow, innovation and value added in theeconomy will increase, as will quality requirements. On the other hand, theoperational environment will be challenging, as companies will have tocontinue to deal with increasing costs, HR shortages and protectionism.Growth will vary across different sectors and different regions, and this willpresent a new challenge.One important new development is the start of an industrial consolidationprocess which will provide many acquisition opportunities, as Chinesecompanies might be more open to sell at realistic prices. At the same timecompetitive pressure and entry barriers are increasing. Less competitivecompanies, both Chinese and foreign ones, will suffer now that there is lessundifferentiated growth. China will require not only major commitment interms of people and investment, but also world class operational excellencein order to remain competitive.In conclusion, we see a better year ahead, but only for those companieswhich are ready for the challenge.

Jan Borgonjon, Beijing, November 2012

Introduction: looking ahead to 2013, a year of consolidation

2

Confidential © InterChina 3

• One Slide On InterChina

• The Big Consumption Trends

• Category Focus: Wine

• Category Focus: Olive Oil

• Category Focus: Cheese

• Available Resources

• Appendix: InterChina Profile

• Appendix: F&B Experience

21

34567

3

8

InterChina

Established 18 years ago, InterChina is one of the early entrants in the consulting industry in China. Over the years, we have become a reference boutique Strategy

and M&A advisory firm.

With 55 advisors in our two China offices (Shanghai and Beijing), InterChina is one of the stronger advisors in our service segment. 90% of our staff are Chinese professionals (MBA, CPA, CFA, etc) and 10% are expatriates from various

nationalities.

The InterChina Strategy practice occupies a leading position in the Strategy advisory market in China, with more than 500 projects in our key industry sectors (Consumer

& retail, health, auto components, chemical and machinery)

Our M&A Practice ranks among China´s top 5 cross border advisory firm in the Mid Market for M&A, with 160 deals and a 7 billion Usd transaction value of which are

90% cross border and 80% Buy Side.

Confidential © InterChina

InterChina Leading Strategy and M&A advisory firm in China

• Our Value• China specialist.• Strategy and M&A advisory• Sector expertise driven.• 18 years continuous track record.

• Our People• Bicultural partnership.• 50 consultants & advisors.• Chinese, senior, industrial, technical.• Located in China, EU, US offices.

• Our Clients• Medium-sized to Fortune 500.• 500 strategy projects.• 160 investment transactions (USD 7 bn).• 2/3 of projects are returning clients

• Our Reach: IMAP• Global mid-market M&A organization. 3rd

in global rankings (Thomson Reuters)• 39 offices, 30 countries, 400 professionals.• Over 200 transactions per annum.• Exclusive China partner since 2006.

4

Confidential © InterChina

Strategy Advisory

• Expansion strategies• Market penetration• Profit protection

InterChina Strategy Practice, 201222 projects, closely following the needs of changing market forces.

Main client issues 2012

Restructure sales channels and way-to-market to reach customers faster and better.

Access consumers in T2 and T3 cities, profitably.

Enter mid-quality market segment; 2nd brand strategy through acquisition or organically

Finding the right approach for inorganic growth in pending sector consolidation.

Localize operations and production, acquisition of local companies to be ‘more Chinese’.

Change of business model, integrate downstream, to capture more value.

InterChina’s sector groups, since 18 years

• Tracking market trends: More than 2,000 Senior Interviews/year.

• Maintain Sector Network: Ongoing contacts with China´s top 20 players.

• > 50 advisors with relevant industry background

• Support both our Strategy and M&A projects.

Automotive & Components

Machinery & Equipment

Chemicals

Healthcare

F&B- Retail

5

Deal with Cost Inflation for both short-term optimization and long-term strategic move

Confidential © InterChina

Chinese Outbound

6

CarburesEngineering and Manufacturing company

Harbin Guanglian Aeronautic Composite Materials & Process

Mounting Co., Ltd.Carbon Fiber parts

池州东升药业有限公司

Chizhou Ruick PharmaceuticalManufacturer of API

Medichem S.A.Manufacturer of API

Leading medical device provider

Manufacturer & Distributor of Medical Devices

China

A global leader in filtration

Filter manufacturer China

Bengbu Haoye Filter Company

Danobat GroupMachine tools manufacturer

China North Railway Corporation Railway equipment producer

Leading medical device providerSweden

Manufacturer & Distributor of Medical Devices

China

InterChina M&A Practice, 201225 ongoing projects. 7 successful closings, 3 transactions pending of approval.

Confidential © InterChina 7

• One Slide On InterChina

• The Big Consumption Trends

• Category Focus: Wine

• Category Focus: Olive Oil

• Category Focus: Cheese

• Available Resources

• Appendix: InterChina Profile

• Appendix: F&B Experience

21

34567

7

8

China: Long Term Trends

This is a difficult time to form a clear opinion on the future of China. Given the long term challenges, China has no choice but to shift to a consumption driven growth

model and some basic changes are already happening. As a consequence of this shift in domestic policy, the high growth period is coming to an end.

However, China will continue to grow at around 7%-8% in the next decade. Growth will gradually slow down to the 6% range as the country consolidates further.

In the long term, the Chinese business environment will be characterized by temporary macro economy imbalances, middle class growth (Retail, F&B, Healthcare, T3-4 urban

growth (environment, service industry), cost increases, industrial upgrading, consolidation and continued protectionism.

This situation will lead to an active restructuring of corporate and product strategies, and a very active M&A arena, where consolidation, aggressive inbound investment in

specific sectors (F&B, Healthcare, Auto) and the emergence of Chinese outbound investment will be key factors.

Confidential © InterChina

The Long Term: The state-led investment model is no longer sustainable…

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2000 2002 2004 2006 2008 2010 2012

Billion USD

Japan

China

German

South Africa

Russia

France

US

India

Brazil

Foreign Reserves

2011

15%

0

2008 20092007 2010

10%

5%

Net export contribution to GDPGDP growth

Net Export Contribution to GDP

Persons entering the job market

Jul2011

May2011

Mar2011

Nov2011

Jan2011

Sep2011

Jan2012

30%

0

Sep2012

40%

20%

Jul2012

May2012

-20%-10%

10%

Mar2012

Monthly Realized FDI YoY Change

Cumulative Growth

GDP Comparison of Major Economies

0

5

10

15

20

25

2006 2008 2010 2012 2014 2016 2018 2020

Million

The state-led investment model was well-suited to sustain massive growth in the past…

…relying on underlying supporting factors that are diminishing

0

500

1,000

1,500

2,000

2,500

3,000

3,500

20042001 2003 20052002 201120102009200820072006

Billion USD

Source: World Bank, State Administration of Foreign Exchange, National Bureau of Statistics of China 8

Confidential © InterChina

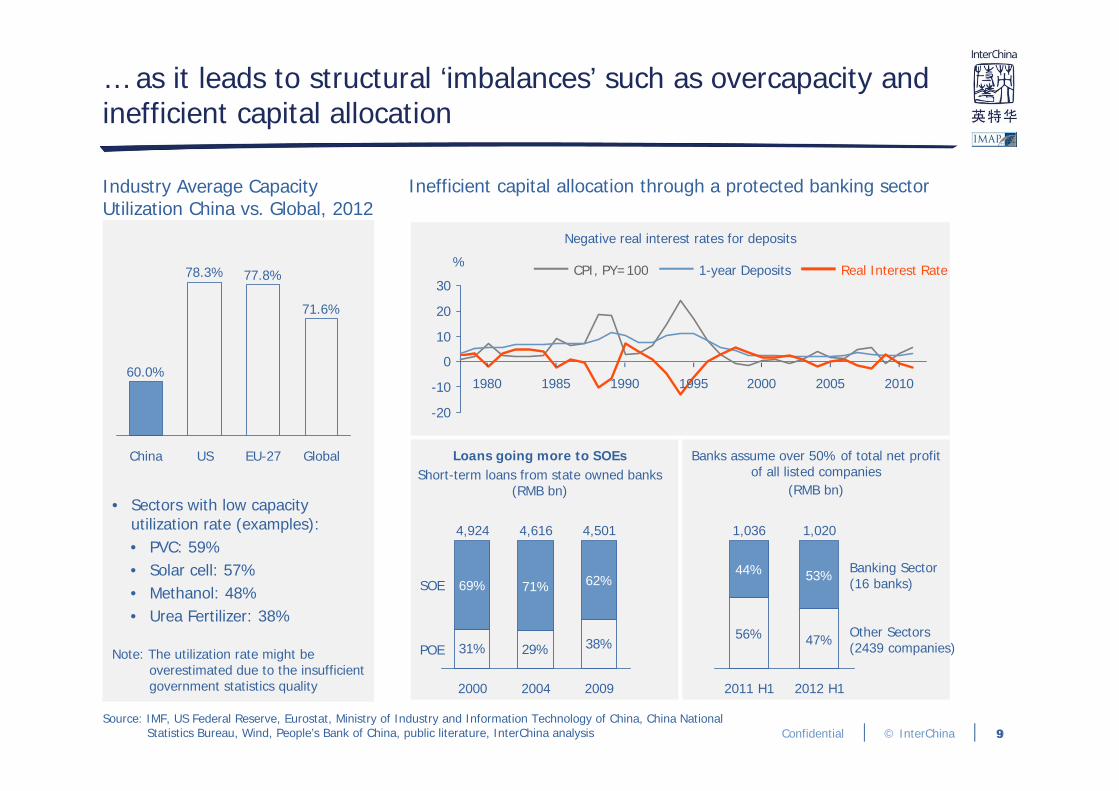

… as it leads to structural ‘imbalances’ such as overcapacity and inefficient capital allocation

Loans going more to SOEsShort-term loans from state owned banks

(RMB bn)

9

Industry Average Capacity Utilization China vs. Global, 2012

Global

71.6%

EU-27

77.8%

US

78.3%

China

60.0%

Note: The utilization rate might be overestimated due to the insufficient government statistics quality

• Sectors with low capacity utilization rate (examples):• PVC: 59%• Solar cell: 57%• Methanol: 48%• Urea Fertilizer: 38%

Inefficient capital allocation through a protected banking sector

Negative real interest rates for deposits

-20

-10

0

10

20

30

%

2010200520001995199019851980

Other Sectors (2439 companies)

Banking Sector (16 banks)

2012 H1

1,020

47%

53%

2011 H1

1,036

56%

44%

Banks assume over 50% of total net profit of all listed companies

(RMB bn)

Source: IMF, US Federal Reserve, Eurostat, Ministry of Industry and Information Technology of China, China National Statistics Bureau, Wind, People’s Bank of China, public literature, InterChina analysis

31% 29% 38%POE

SOE

2009

4,501

62%

2004

4,616

71%

2000

4,924

69%

Real Interest Rate1-year DepositsCPI, PY=100

9

Confidential © InterChina

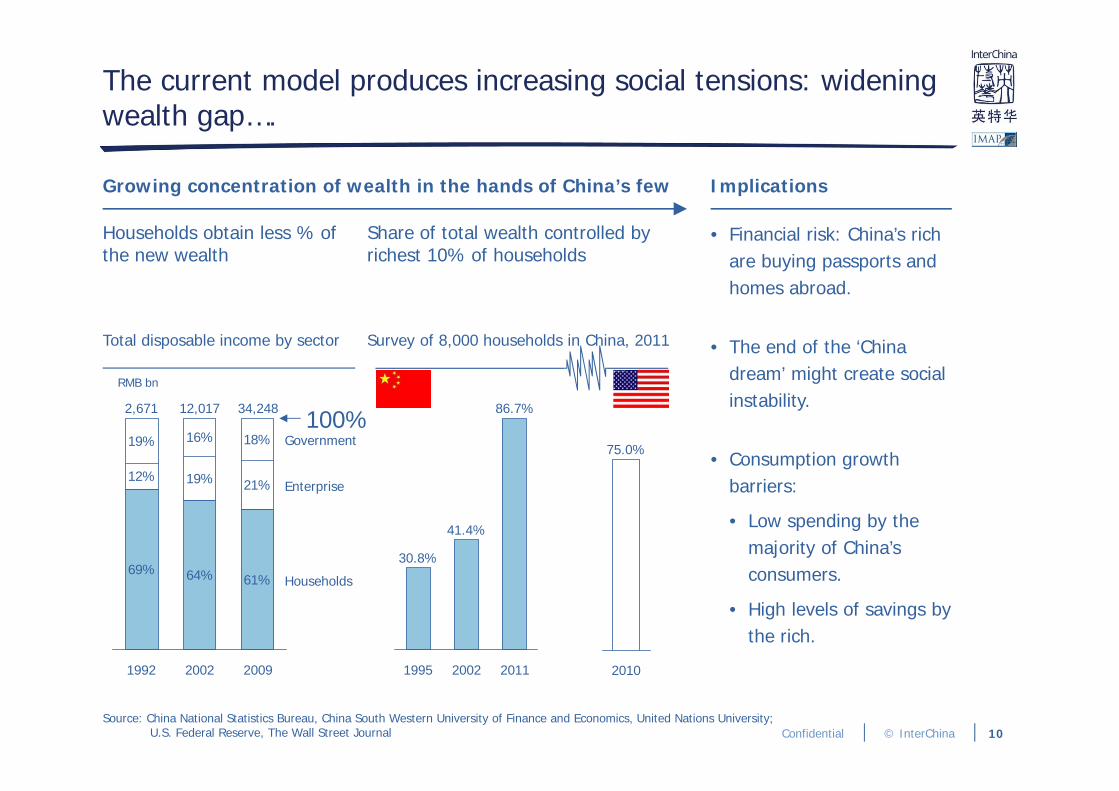

The current model produces increasing social tensions: widening wealth gap….

Source: China National Statistics Bureau, China South Western University of Finance and Economics, United Nations University;U.S. Federal Reserve, The Wall Street Journal

Growing concentration of wealth in the hands of China’s few Implications

• Financial risk: China’s rich are buying passports and homes abroad.

• The end of the ‘China dream’ might create social instability.

• Consumption growth barriers:

• Low spending by the majority of China’s consumers.

• High levels of savings by the rich.

Share of total wealth controlled by richest 10% of households

2011

86.7%

2002

41.4%

1995

30.8%

75.0%

2010

10

Households obtain less % of the new wealth

69% 64% 61%

12% 19% 21%

19% 16% 18%

Enterprise

Government

Households

100%

2009

34,248

2002

12,017

1992

2,671

Total disposable income by sector

RMB bn

Survey of 8,000 households in China, 2011

Confidential © InterChina

… and growing corruption: getting worse, including at company level

Source: Transparency International, The Supreme Court of China

Transparency International Corruption Perceptions Index (CPI)* - China

China Supreme Court: Corruption and Bribery Cases Received

3.63.53.63.63.53.33.23.1

4.75.1

1996

2.4

2005 2006 20072000 2009 2011201020081988-1992

1980-1985

16,000

18,000

20,000

22,000

24,000

200820062004 2010200220001998

Highly corrupt 0

very clean 10

No. of Cases

Note: * The CPI ranks countries/territories based on how corrupt their public sector is perceived to be. It is a composite index, a combination of polls, drawing on corruption-related data collected by a variety of reputable institutions. The CPI reflects the views of observers from around the world, including experts living and working in the countries/territories evaluated.

Implications and Outlook

• Corruption threatens China’s attractiveness to business and investment

• In spite of token government efforts, corruption is a structural problem that permeates the whole state system.

• Implementation of anti corruption measures on the provincial level remains a challenge

• We expect corruption to grow at all levels, including at company level

11

Confidential © InterChina

II. Or straightforward emigration

The middle class is getting concerned… ….and voting with its feet?

I. Sending kids abroad

Source: Ministry of Education of China, US Dept. of Homeland Security, Bureau of Consular Affairs, U.S. Department of State, Wall Street Journal analysis of data from People’s Bank of China, China Customs, MOFCOM and SAFE

Annual flow of Chinese students studying overseas(Persons)

1,106,400

413,600339,700284,700

118,68939,000

22%

2017E2012E2011201020052000

CAGR 2006-2011

Chinese students enrolled in the US - more Chinese students going abroad at a younger age

(Persons)

Graduate

Under-graduate

High school and below

2011

157,600

59.2%

36.5%

4.3%

2006

62,591

85.5%

14.4%0.1% 153%

45%

12%

87%53%

30%

Chinese

Others

2011

3,463

70%

2009

4,218

47%

2005

349

13%

US green cards to foreign investors*(Persons)

III. Capital flight

* To qualify for this type of permit foreigners need to invest at lease USD 500,000.

Estimated capital flight at USD 225 bil.

• Confirmed capital flight.• But claimed to be largely driven by

ODI.

3% of China’s GDP!

12

Confidential © InterChina 13

Exports

Fixed-Asset Investment

Low-End Manufacturing

Domestic Consumption

Service Sector Development

Industrial Upgrading (Innovation)

Financial Reform

Fair Competition

Therefore China is embarking on a new development path

Old Model (1990s – 2000s)

New Model For The Future

13

Confidential © InterChina 14

The government is fully aware of the need for change and is taking measures: the 12th 5 year plan

• “China’s growth is ‘unsteady, imbalanced, uncoordinated, and unsustainable “ (Wen Jiabao, 2007)

• The new development model is defined in the 12th Five Year Plan

• During 2011/2012 substantial measures have been taken to reform further the financial system

• Opposition of interest groups can be expected.

• Strong political action will be necessary and can be expected under the new government

Key Measures of The 12th Five-year Plan

• Restructuring economy, increasing domesticconsumption• Lower GDP growth target: 7%• Long-term domestic consumption to replace

exports as the primary growth driver.• Raise salaries, strengthen social security, and

reduce medical costs to increase consumerspending power.

• Boost industrial competitiveness• Developing strategic emerging industries, which

will drive economic growth and industrialcompetitiveness over the coming decades.

• Consolidating traditional industries, such aspetrochemicals and steel

• Advancing science and technology• Building domestic capacity to develop high-end

technologies through indigenous innovation,technology absorption, and R&D.

14

Confidential © InterChina 15

• One Slide On InterChina

• The Big Consumption Trends

• Category Focus: Wine

• Category Focus: Olive Oil

• Category Focus: Cheese

• Available Resources

• Appendix: InterChina Profile

• Appendix: F&B Experience

21

34567

15

8

2013: Trends and Expectations

2013 will be a year of continued growth, but slower and fragmented and with higher uncertainty.

The operational environment will be challenging. Cost increases and HR will remain a problem while protectionism and industrial overcapacity in particular in state controlled sectors will impede fair competition. On the other hand industrial

consolidation will finally start and will create many opportunities for western companies.

We see clear potential in certain industries (Healthcare, Consumer & Retail, Environment, and industrial areas linked to productivity increases and higher

technology). Both sales and profits will continue to grow in these sectors. Other industries, however, will have more conservative (automotive,) or even negative

prospects (construction, export related areas).

This fragmentation of the Chinese economy in high speed and low speed growth sectors is new and will create new dynamics. As China remains the largest or one

of the largest markets and the biggest growth opportunity in many sectors, companies will have to continue to adapt a more competitive and more demanding

environment in which only the best will win.

Confidential © InterChina

2013 Forecast: continued growth, but slower and fragmented, with higher uncertainty

• Growth 7 – 8 %

• Exports and Inbound Investment: stable or

slight decrease

• Consumption and Retail Sales: growing, driven

by T2/3/4 cities.

• Public Investment: growing, but more slowly

• Sector Consolidation expected

Slower growth ….

• Inflation risks remains possible with anti crisis

packages

• Sector Protectionism

• Industrial Overcapacity

… with increasing downside

And, HIGHER UNCERTAINTY• Impact of the international economy

• The speed of the new government to work towards the new model is unknown

• Room for new, more limited stimulus, but constrained by inflation

• Uncertainty on development of real estate market

• Lack of liquidity, in particular for SME’s and non-state companies

• Big differences across different sectors and different regions

16

Confidential © InterChina 17

Key Themes 2013

• Consumption growth, but slowing down

• Cost Increases

• HR: increasing challenge

• Protectionism

• Consolidation & M&A Opportunities

• Outbound investment

• FDI: revisiting the China strategy

2

1

3

4

6

5

7

Confidential © InterChina

Consumption growth to continue, but at lower speed and with a mixture of expectations in different sectors…

“China is a still booming market for us, and our growth rate is planned at 20% - 30% in 2013, and we will keep on increasing the investment in the current factory.”

- A MNC pharma company

“We decided to bring more products to China, and revamp our strategy in China. This will bring us 25% growth next year in China and China will be the largest and best performing market for us”

– A Major Confectionary MNC

“In October, Coca-Cola (KO, Fortune 500) said that sales in China grew an anemic 2% compared to 11% a year ago.”

- CNN News

“The automotive sector might experience a relatively slow development stage with 5% - 10% growth rate in 2013”

- A leading European Automaker

“Our China business is having another strong year. But as I‘ve said before, China is going to have its inevitable ups and downs. ... We now face a slowing economy. But that doesn’t change our long-term outlook in China one iota. Our annual performance has been pretty consistent, and I expect this to continue.”

– Yum! Chairman and CEO David C. Novak0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Q1

2012

Q2

-14%

-10%

-6%

-2%

2%

6%

10%

14%

18%

22%

26%

LHS: Urban Household LHS: Rural HouseholdRHS: Urban % Change RHS: Rural % Change

Source: China National Statistics Bureau 18

“There is still good growth in the dairy market. Yes, The western consumer market is growing very fast while developed cities like Beijing and Shanghai are slowing down”

– A major dairy value chain player

RMB %

Per Capita Annual Consumption of Urban and Rural Households

Confidential © InterChina

…, inland and western regions are more positive

% y-o-y

8

6

4

26

24

22

20

2

18

16

14

12

10

RMB bn

8,000

6,000

4,000

20,000

2,000

18,000

16,000

14,000

12,000

10,000

02011

6,930

11,462

20102009200820072006200520042003200220012000

1,333

2,233

Interior Growth

Interior Value

Costal Growth

Costal Value

Retail Sales of Consumer Goods By RegionCoastal (East, North East) vs. Interior (West, Central)

346

8

20082007200620052004200320022001

20

22

2

18

16

14

12

10

RMB bn

8,000

6,000

4,000

20,000

2,000

18,000

16,000

14,000

12,000

10,000

02011

9,416

1,963

20102009

% y-o-y

6

4

30

28

26

24

2000

1,765

T2+T3 Growth

T2+T3 Value

T1 Growth

T1 Value

Retail Sales of Consumer Goods By City Tiers

Source: China National Statics Bureau 19

Confidential © InterChina

Long-term consumption growth has short term implications

• Consumer business need to reach scale in China, and when they do, they need to shift from a centralized national structure to a more empowered and well resourced regional structure.

• Global Profile• Global leader in alcoholic beverages. Revenue of Euro 8.2bn in 2011.• Strong portfolio of brands: Chivas, Ballantine's, Glenlivet, Jameson

(Whiskey), Absolut (vodka), Martell (cognac), Havana Club, etc.

• Position in China• No. 1 imported alcoholic beverage player with 50% market share.• China sales achieved 24% growth in 2011• China Sales structure: HQ in Shanghai. 6 regions, with each region

run like a country. Sales cover 400 cities, including T3 and T4 cities. • KSFs: Winning the rising middle classes by expanding from the

coastal cities to the interior and smaller cities, and adapting offer in products and consumption patterns (Martell and Chivas Regal).

• Future Plans in China• Future growth target: Well above the market average.

20

Pernod Ricard in China Implications

Source: Company annual report 201120

Confidential © InterChina 21

Key Themes 2013

• Consumption growth, but slowing down

• Cost Increases

• HR: increasing challenge

• Protectionism

• Consolidation & M&A Opportunities

• Outbound investment

• FDI: revisiting the China strategy

2

1

3

4

6

5

7

Confidential © InterChina

Productivity improvements will not be sufficient, and MNCs are nowfacing longer-term strategic implications

Source: China’s Statistics Bureau, InterChina AnalysisNote: Salary Adjusted by Productivity = Index of Salary / Index of Productivity

710

250

1,086

540

786

436

217153122

87

1119987

100

0

100

200

300

400

500

600

700

800

900

1,000

1,100

20052004

Salary Adjusted by Productivity (Slow Salary Growth)

Salary Adjusted by Productivity(Fast Salary Growth)

Average Salary (Slow Growth Scenario)

Average Salary (Fast Growth Scenario)

2020201920182017

Manufacturing Productivity

20162015201420132012

441

20112010

217

2009200820072006

CAGR 2004 –2010

CAGR 2010 –2015E

CAGR 2015E –2020E

13.8% 20% 15%

13.8% 15% 12.5%

16.5% 12% 10%

-2.3% 7.1% 4.5%

-2.3% 2.7% 2.3%

China’s Labor Cost and Productivity In the Urban Manufacturing Sector

Tipping Point

The tipping point refers to the period 2012-2016 that the growth of manufacturing productivity is likely to

lag behind the salary increase in China’s urban manufacturing sector.

… and drivers are shifting to operational excellence, through technology upgrades, innovation, revamp of business model etc,

to offset the impact of rising costs.

In China’s manufacturing sector, the productivity growth was driven

largely by investment…

22

Confidential © InterChina

Export-oriented or low value-added companies have already started torelocate or restructure their manufacturing footprints

Cited reasons for restructuring or relocation: rising labor and freight costs, quality issues, difficulty in dealing with products’ customization, etc.

Relocation

• Move all or the majority of operations back to home countries, typically to US or Europe.

• Usually involves small-scale operations in China.

Restructuring Manufacturing Footprints

• Usually diversification of manufacturing facilities between China and other LCCs, but not a full or majority relocation.

• Usually involves large-scale operations and typically low value-added sectors.

23

Confidential © InterChina

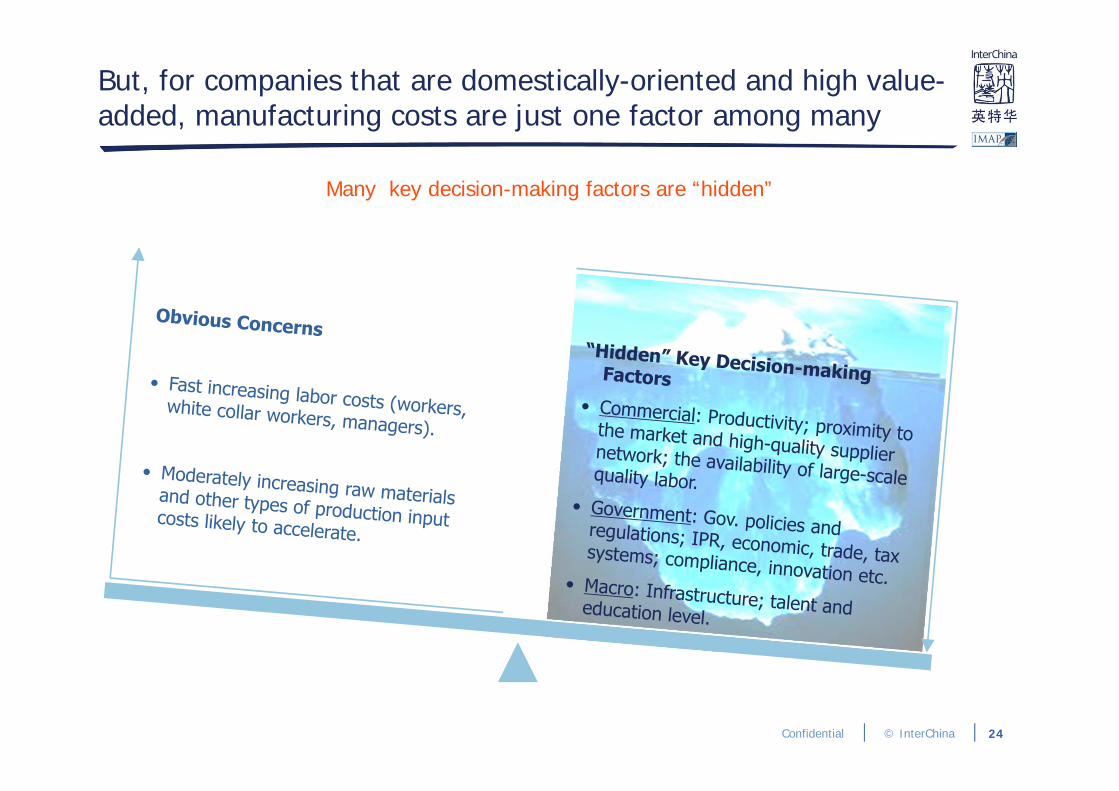

But, for companies that are domestically-oriented and high value-added, manufacturing costs are just one factor among many

Many key decision-making factors are “hidden”

24

Confidential © InterChina

Companies will combine both revenue growth and marginprotection strategies. Operational excellence will be key

Higher Focus on China Sales1

Revamped Manufacturing Model2

Modified Business Model4

Geographical Relocation5

More Value-added Products/Services3

• Likely Trend: The companies with a focus on China’s market are likely to stay in China. These “hidden” factors below the iceberg are likely to outweigh the rising costs.

• Example Sectors: This includes capital-intensive companies and quite a few labor-intensive companies with a strong footprint in China.

• Implication: Various strategic actions are required to deal with cost inflation effectively.

• Operational excellence will be key………

…but require strategic changesCompanies with a strong focus on China’s market will stay…

25

Confidential © InterChina 26

Key Themes 2013

• Consumption growth, but slowing down

• Cost Increases

• HR: increasing challenge

• Protectionism

• Consolidation & M&A Opportunities

• Outbound investment

• FDI: revisiting the China strategy

2

1

3

4

6

5

7

Confidential © InterChina

Labor shortage with decreasing supply

Source: Chinese Academy of Social Science, China Central Policy Research Office

The one-child policy might be relaxed by 2020 or before, depending on economic development and social pressures.

Pressure on the labor force

0 5 10 15 20 25

2016

2019

2008

2017

2010

2020

20122013

2011

2006

2018

2009

2007

20152014

People entering the job market

• From 2005~2008 there was only 0.4% growth in working-age population, far less than the global average of 1.2%.

• China’s working age population in 2020 will be 1,013 million, far larger than the EU’s 280 million in 2020. However, new labor entering the market will decrease after 2009.

• Overall labor force may decline in 2016~2019.

Unit: Millions

27

Confidential © InterChina

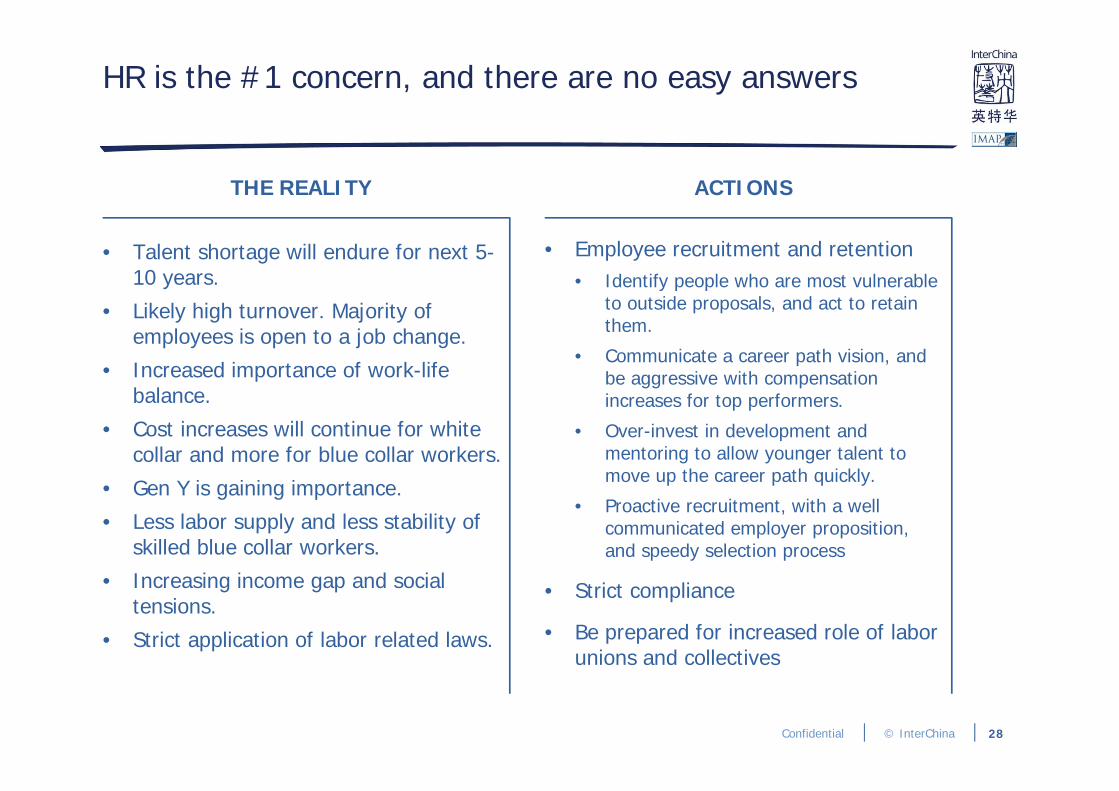

HR is the #1 concern, and there are no easy answers

THE REALITY

• Talent shortage will endure for next 5-10 years.

• Likely high turnover. Majority of employees is open to a job change.

• Increased importance of work-life balance.

• Cost increases will continue for white collar and more for blue collar workers.

• Gen Y is gaining importance.

• Less labor supply and less stability of skilled blue collar workers.

• Increasing income gap and social tensions.

• Strict application of labor related laws.

ACTIONS

• Employee recruitment and retention• Identify people who are most vulnerable

to outside proposals, and act to retain them.

• Communicate a career path vision, and be aggressive with compensation increases for top performers.

• Over-invest in development and mentoring to allow younger talent to move up the career path quickly.

• Proactive recruitment, with a well communicated employer proposition, and speedy selection process

• Strict compliance

• Be prepared for increased role of labor unions and collectives

28

Confidential © InterChina 29

Key Themes 2013

• Consumption growth, but slowing down

• Cost Increases

• HR: increasing challenge

• Protectionism

• Consolidation & M&A Opportunities

• Outbound investment

• FDI: revisiting the China strategy

2

1

3

4

6

5

7

Confidential © InterChina

Protectionism is here to stay…

Depends on Sectors• Strategic importance.• Availability of competitive

or SOE players• Ease of control

Sectors Affected• E.g. steel, auto, chemical,

financial services, telecom, railway, and energy.

• Possible new sectors, e.g. machinery and machine tools.

Dynamic Situation• Windows of opportunity

come and go.

Protectionism on Demand Side• Market control via public auctions or tenders, in a way that is

favoring local players.• Setting sector industry standards to match local R&D and

technologies.

Protectionism on Supply Side • Restrictions to invest in certain industries.• Requirements of local content and therefore local manufacturing.• Requirements on technology transfer against market access.

Encouragement of Local R&D and Technology upgrades• Subsidies to conduct R&D, and loans to acquire technologies

globally (licenses, etc).• To acquire companies globally so that the company’s technology

and brand could be developed in China.

Access to finance• Lower requirements and economic conditions for state owned

companies.

30

Confidential © InterChina

… as forces for protectionism continue to outweigh the ones against

Forces Past Present Near Future

Distant Future

The hand of domestic politics ? ?

Interest groups

FDI as catalyst Neutral

The economic argument

Chinese companies go global N/A

China’s global responsibilities

The Forces Supporting protectionism have been getting stronger since previous years

Against - Strongly

Neutral

Support - Strongly

31

Key Themes 2013

• Consumption growth, but slowing down

• Cost Increases

• HR: increasing challenge

• Protectionism

• Consolidation & M&A Opportunities

• Outbound investment

• FDI: revisiting the China strategy

2

1

3

4

6

5

7

36

Key Themes 2013

• Consumption growth, but slowing down

• Cost Increases

• HR: increasing challenge

• Protectionism

• Consolidation & M&A Opportunities

• Outbound investment

• FDI: revisiting the China strategy

2

1

3

4

6

5

7

• Engineering prowess. • Strong brands.• Reduce exposure to Chinese

domestic economy.• Overseas market.

Motivations of the Buyer

Motivations of the Seller

Deal Details

Polish state-owned bulldozers

manufacturer

Chinese state-owned construction equipment

manufacturer

German high-tech concrete pumps

manufacturer

• Hands on technology.• The premium brand to extend

its product range.• Offset domestic rivalry pressure.• Worldwide distribution network

to improve its market coverage outside of China.

German concrete

equipment manufacturer

Chinese state-owned construction machinery

manufacturer

Chinese state-owned construction machinery

maker

• R&D and production capacity. • Distributor and dealer network

in Eastern Europe.• High-quality brand. • A strong complementary

product mix.

LiuGong- HSW Acquisition Sany-Putzmeister Acquisition XCMG- Schwing Acquisition

• Expansion in China.• Capital need.

• In 2012, LiuGong acquired HSW’s subordinate civil engineering machinery business unit for RMB 335 mn.

• Facilitated by IMAP.

• In 2012, Sany acquired Putzmeister.

• The transaction value is EUR 360 mn (Sany pays 90% and Citic 10%).

• Financing need of owner; distressed operation.

• Market expansion in China.

• In 2012, XCMG acquired 52% of Schwing’s stake.

• German management remains in charge

• Access to the Chinese growth market.

• Financing need of owner; distressed operation.

41Source: Mergemarket, Public Literature

Key Themes 2013

• Consumption growth, but slowing down

• Cost Increases

• HR: increasing challenge

• Protectionism

• Consolidation & M&A Opportunities

• Outbound investment

• FDI: revisiting the China strategy

2

1

3

4

6

5

7

Confidential © InterChina

However, companies are still optimistic on growth and profitability….

27%

20% 17% 19%

65%78% 80% 78%

Pessimistic

Neutral

Optimistic

2012

3%

2011

3%

2010

2%

2009

8%

43%50% 45% 48%

34% 34% 37% 36%

16%18%16%23%

EU CORPORATE BUSINESS OUTLOOK IN THE NEXT TWO YEARS

Source: EUCCC Business Confidence Survey 2012

GROWTH PROFITABILITY

78% optimistic about growth outlook

84% optimistic/neutral about profitability outlook

2009 2010 2011 2012

44

Confidential © InterChina

… as China remains the major strategic option for most MNCs

European Companies: Importance of China in companies' overall global strategy, 2012

US Companies: China’s Prominence in Overall Company Strategy, 2012

23%

Increasingly important

74%

Declining in importance

Same level of importance

3% 5%

22%

One of many non-key priorities Not a priority

1%Top priority

Among top five priorities

72%

Source: European Business in China Confidence Survey 2012, The US-China Business Council Member Confidence Survey 2012 45

N = 557

45

Confidential © InterChina

…. But most continue to do well

Retail, franchising

Healthcare

Aerospace, High Tech Equipment

Clean Tech (e.g. Water)

Consumer & Retail

Machinery

Automotive

Fine Chemicals

• Strong domestic demand, supportedby the government and financialsector.

• Likely technology gap in China,leaving room for foreign companies.

• Forecasted growth patterns both interms of sales (above 15%), andprofits.

• Strong M&A and investments

• Driven by domestic demand.• Good but lower growth in T1 and 2 cities, with

the appearance of new markets in T3 and 4 cities.• Strong domestic and foreign competition.• Overcapacity in many sectors• Directly affected by cost inflation• Margin maintenance is a key issue• Forecasted growth in the range of 10%, with

even or decreasing profit contribution.• Increasing sale-side M&A activities (e.g. carve

outs, restructuring) and consolidation buy-sideinvestments.

Strong Growth

Average Growth (with some doubts)

White Goods

46

Confidential © InterChina

Big differences across sectors: some weaker….

Renewable Energy and Export Related (light industry, low cost driven)

Construction related (cement, steel, heavy duty machinery, some chemical sectors)

• Continue to suffer both the domestic slow down of China’s real estate and infrastructure market and the global crisis in the EU and USA.

• Tremendous overcapacity, which might get worse.

• High level of local protectionism, making consolidation and smart investment difficult.

• Hit by strong cost pressures. Possible threat of very aggressive pricing strategies (dumping?) both in local market and in export sales.

• Forecasted to run at less than 60% capacity utilization rate, incurring losses.

• Two conflicting investment drivers by local players: on one hand, divestments, closure and carve outs; on the other hand, further and aggressive investments towards consolidation and further capacity expansion (protective measures).

Weak Growth

47

Confidential © InterChina 48

• One Slide On InterChina

• The Big Consumption Trends

• Category Focus: Wine

• Category Focus: Olive Oil

• Category Focus: Cheese

• Available Resources

• Appendix: InterChina Profile

• Appendix: F&B Experience

21

34567

48

8

Conclusion

We consider that 2013 will be a year of continued growth, but slower and fragmented, with higher uncertainty.

We see clear potential in certain industries (Healthcare, F&B, Retail, Environment, and industrial areas linked to productivity increases and higher

technology). Both sales and profits will continue to grow in these sectors.

Other industries, however, will have a more conservative (automotive) or even negative prospects (construction and export related areas). This fragmentation of the Chinese economy on high speed and low speed growth sectors will be

new and create new dynamics.

The operational environment will face certain challenges. We are specially worried about the increasing industrial bubble and constant capacity increases

in State Owned led segments, as well as in the increasing protectionism in such industries.

Confidential © InterChina

Health care

Strategic redirection to meet uneven sector development

Food industry, Retail, franchising

Environment / Clean tech

• 20-30% growth.• Speed & Channels• Buy Side M&A and JVs.

Automotive/ Machinery

• 10% growth. Profit tensions (cost/Price)

• Regional Coverage.• Buy Side M&A and JVs.• Chinese Outbound.

• 10 – 15% growth.• Tier 2/3 cities. Channels. Critical

Mass. • Buy Side M&A and JVs.

• 20% growth. • Protectionism. JVs.

Machinery

• 10% Growth• Local manufacturing, China tailor

made technology, local brands. • JV/ M&A. Chinese out bound

Chemicals

• 5-15% growth.• Technology Revamp (JV). • Consolidation. M&A

Construction Sector/ Equipment

• 0-5%. • Overcapacity. Consolidation. • Outbound- Protection strategies.

49

Confidential © InterChina

Conclusion: continued growth opportunities in a more complex environment

• Temporary inbalances: Industrial bubble, real estate bubble, regional debt tensions. -> be ready for economic shocks (e.g. Domestic dumping in overcapacity segments).

• Continued substantial cost increases are inevitable -> requires a strategic approach and a shift to operational excellence

• Protectionism is there to stay -> adjust corporate practices through proactive government relations and alliances with Chinese players

• Consolidation will change the dynamics of many sectors and will offer opportunities for western companies companies -> participate proactively in the consolidation process

• Continued global expansion of Chinese companies -> Increasing possibilities for local and global alliances with Chinese companies

50

Confidential © InterChina 51