the british retail energy market: politicians and re-regulation?

TRANSCRIPT

The British retail energy market: politicians and re-

regulation?Professor Michael Harker

ESRC Centre for Competition Policy and UEA Law School

University of East Anglia

Privatisation, regulation and liberalisation• National gas market

incumbent

• 14 regional electricity markets

• RPI-X price-caps for electricity and gas incumbents only

• Main entrants other incumbents

• Gradual deregulation from 2000 to 2002, all caps removed April 2002

• Significant industry consolidation – foreign entry through acquisition of incumbent firms, vertical integration

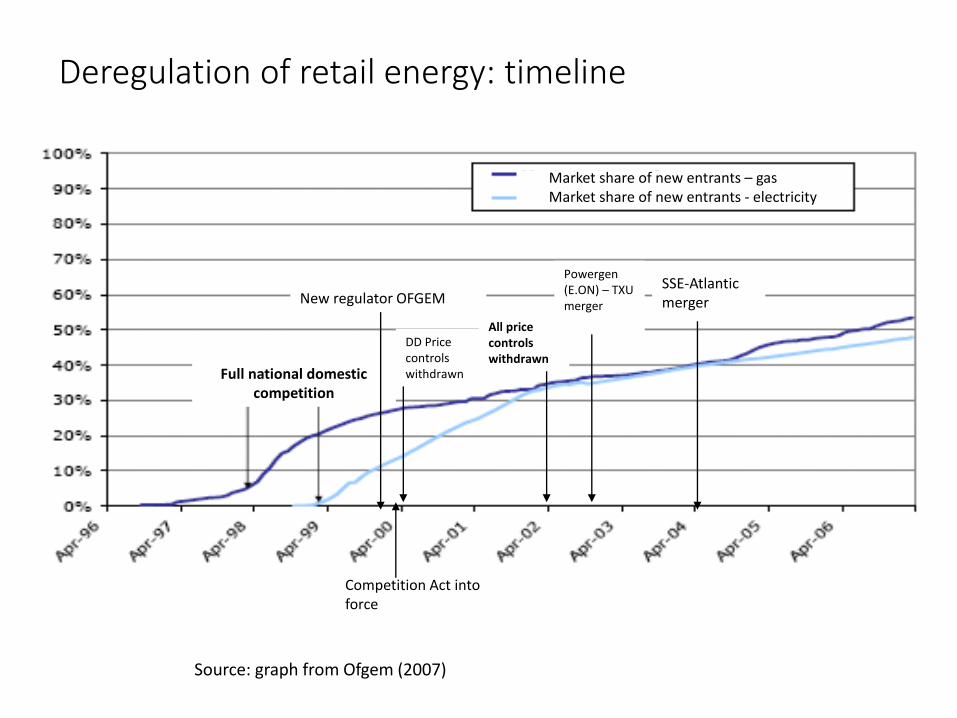

Deregulation of retail energy: timeline

Market share of new entrants – gasMarket share of new entrants - electricity

Full national domestic competition

New regulator OFGEM

Competition Act into force

DD Price controls withdrawn

All price controls withdrawn

Source: graph from Ofgem (2007)

SSE-Atlantic merger

Powergen(E.ON) – TXU merger

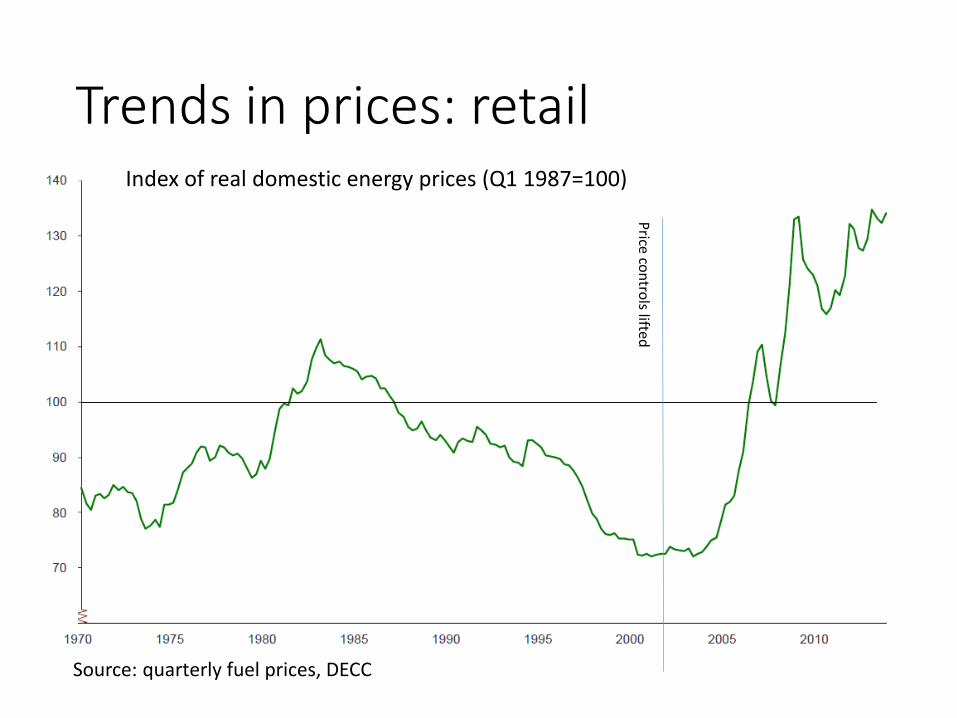

Trends in prices: retailIndex of real domestic energy prices (Q1 1987=100)

Source: quarterly fuel prices, DECC

Price co

ntro

ls lifted

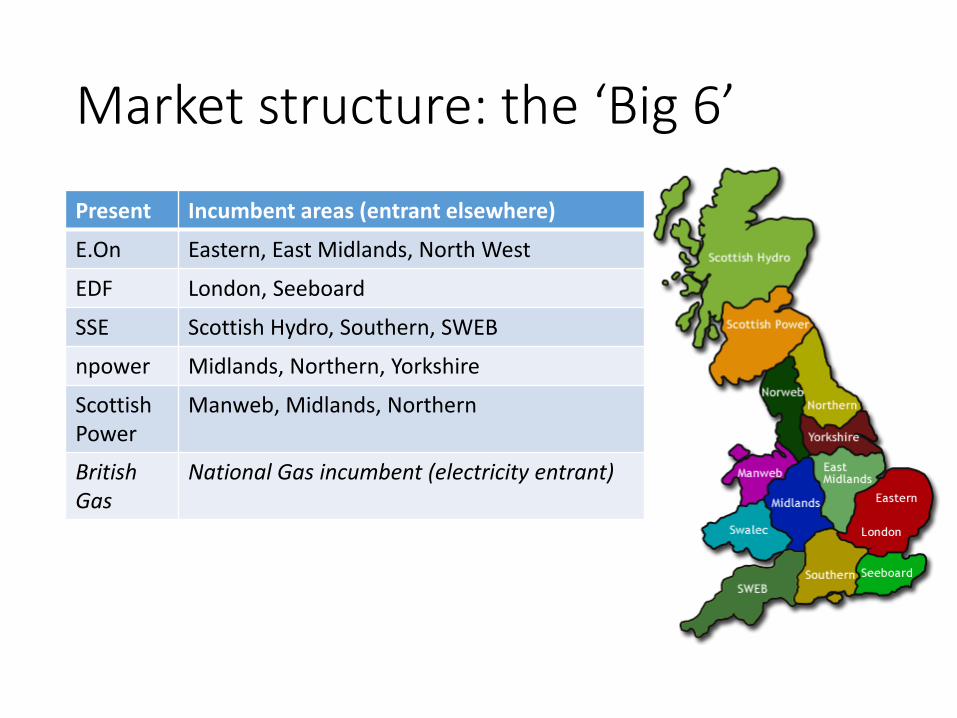

Market structure: the ‘Big 6’

Present Incumbent areas (entrant elsewhere)

E.On Eastern, East Midlands, North West

EDF London, Seeboard

SSE Scottish Hydro, Southern, SWEB

npower Midlands, Northern, Yorkshire

Scottish Power

Manweb, Midlands, Northern

BritishGas

National Gas incumbent (electricity entrant)

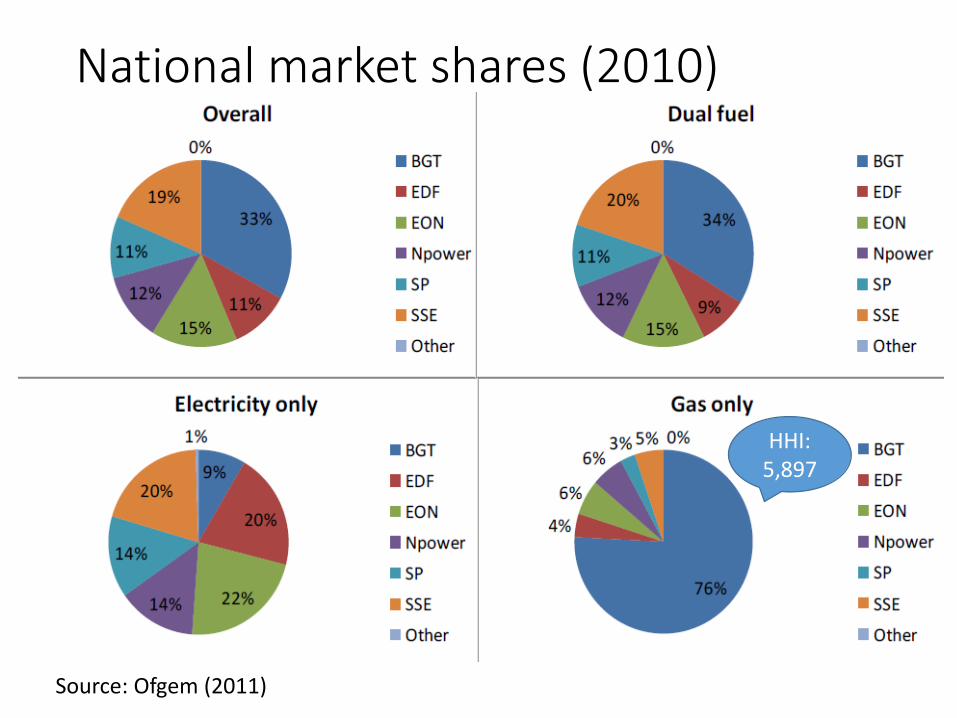

National market shares (2010)

Source: Ofgem (2011)

HHI: 5,897

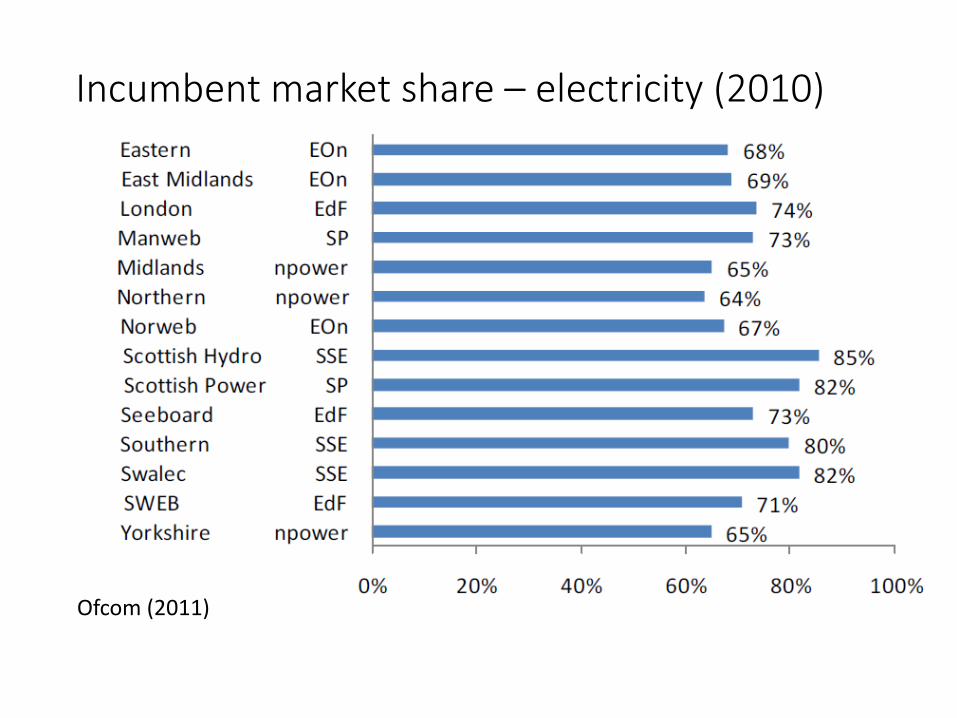

Incumbent market share – electricity (2010)

Ofcom (2011)

‘Sticky’ consumers

• Sticky consumer – remained with the incumbent, switched to a dual-fuel deal offered by incumbent, or switched back to incumbent

Ofcom (2008, 2011)

Savings foregone

• Significant savings could be made if consumers switched tariffs (both payment and suppliers)

Switch from Dual fuel Electricityonly

Gas only

Direct debit £160-196 £27-86 £5-36

Standard credit

£236-323 £59-117 £25-82

Prepayment £237-239 £66-109 £42-66

Average savings over 2010 per customer if moved to the supplier with lowest direct debit tariff

Why are some consumers not switching?• Behavioural reasons – status quo bias (Ofcom,

2008)

• Consumers who do switch may choose a more expensive tariff (Waddams and Wilson)

• Tariff complexity and ‘confusopoly’

• Substantial growth in tariffs: Ofgem c.900 tariffs (August 2012); DECC estimates 650 ‘dead’ tariffs; Which claims to have found people on 1,440 tariffs (March 2013)

Who are the ‘sticky’ consumers

• [Graph from ….

Profile of customers who have never switched, weighted against the British population

Source: Ofcom / MORI (2008); Ofcom (2011)

Re-regulating to tackle ‘unfair’ pricing and tariff complexity

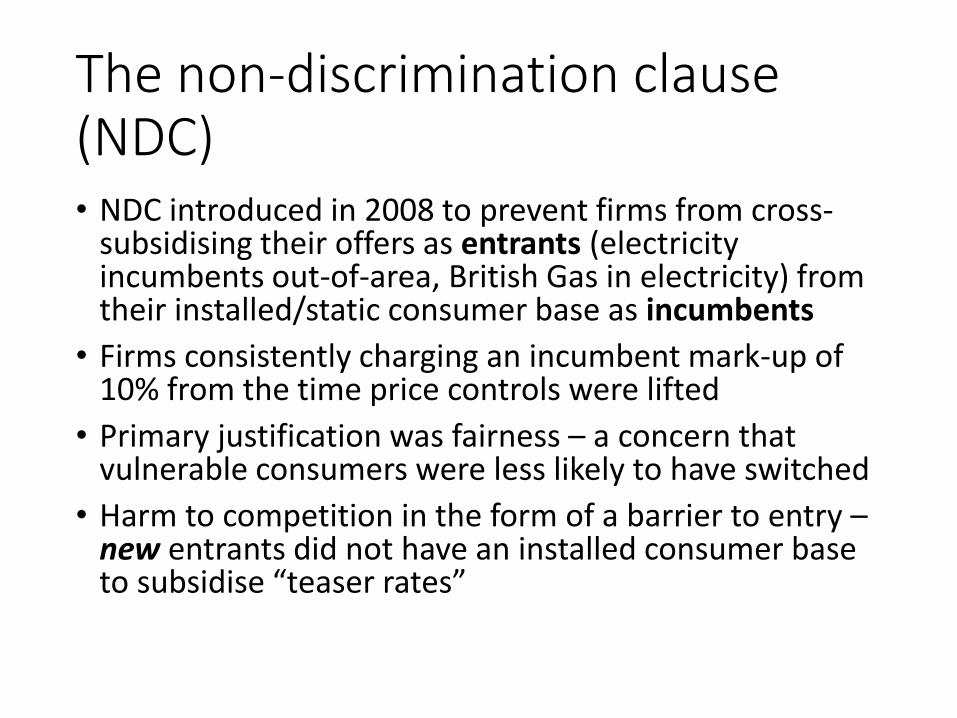

The non-discrimination clause (NDC)• NDC introduced in 2008 to prevent firms from cross-

subsidising their offers as entrants (electricity incumbents out-of-area, British Gas in electricity) from their installed/static consumer base as incumbents

• Firms consistently charging an incumbent mark-up of 10% from the time price controls were lifted

• Primary justification was fairness – a concern that vulnerable consumers were less likely to have switched

• Harm to competition in the form of a barrier to entry –new entrants did not have an installed consumer base to subsidise “teaser rates”

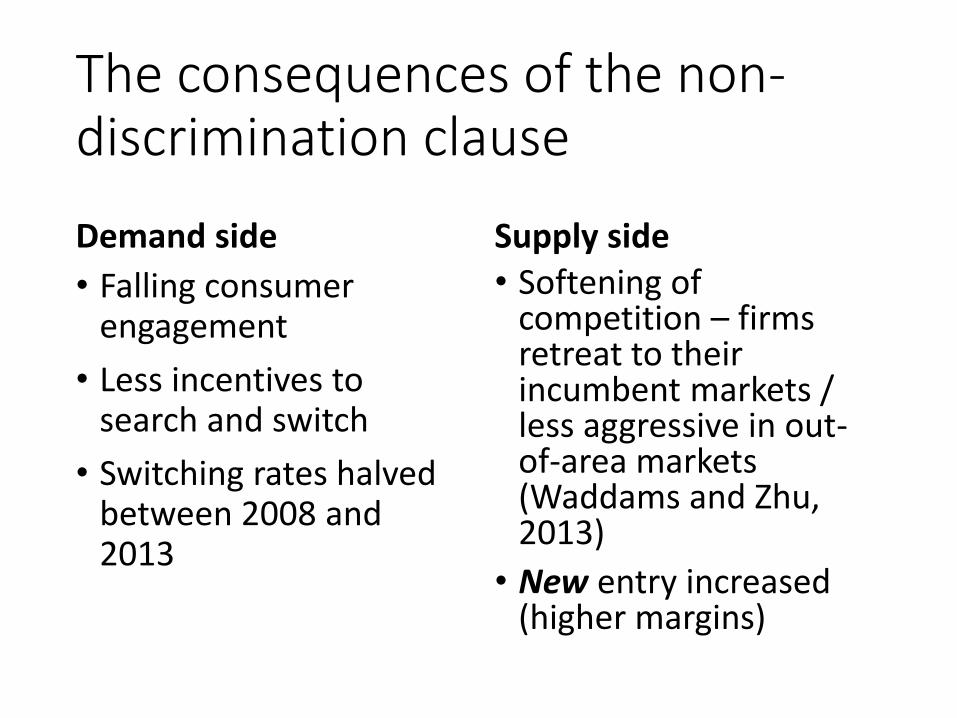

The consequences of the non-discrimination clause

Demand side

• Falling consumer engagement

• Less incentives to search and switch

• Switching rates halved between 2008 and 2013

Supply side• Softening of

competition – firms retreat to their incumbent markets / less aggressive in out-of-area markets (Waddams and Zhu, 2013)

• New entry increased (higher margins)

The PM’s intervention

• Prime Minister’s Questions (17 October 2012):• Chris Williamson (Derby North) (Lab): At the Prime Minister’s

energy summit last year, he promised faithfully that he would take action to help people reduce their energy bills. Will he tell the House and the country: how is it going?

• The Prime Minister: We have encouraged people to switch, which is one of the best ways to get energy bills down. I can announce, which I am sure the hon. Gentleman will welcome, that we will be legislating so that energy companies have to give the lowest tariff to their customers—something that Labour did not do in 13 years, even though the Leader of the Labour party could have done it because he had the job.

Ofgem’s ‘fairness agenda’

• A result of Ofgem’s review of the market 2008-2011:

• Limit to four the number of tariffs offered by supplier (per payment type) (Dec 13)

• Suppliers tell customers when there is a cheaper live tariff (March 14)

• Consumers on ‘dead’ tariffs will be switched to a cheaper variable deal (Oct 13 / June 2015)

Legislation: Ministerial back-stop powers • Energy Act 2013, s.139: enable the Minister to prescribe

types, and limit numbers, of tariffs; and specify certain types of consumers to be moved from one tariff to anther

• Sun-set clause (Dec 18);

• Amendments made to the Bill (in Committee stage)

• “The provision will give the Secretary of State the power to make it compulsory for suppliers to move those who could save money on to the cheapest, live standard variable-rate tariffs. This is the meat of what the Prime Minister was pledging to do. Customers would have the ability to opt out of the process, if they wish, while the remainder would save money without having to lift a finger.”

Conclusions

• Lifting of price controls – regulation appeared to be successful in the context of falling / stable prices

• Sharp price increases result in increased attention from politicians

• Many of the ‘problems’ with the retail energy market have resulted from consumer inertia

• Real distributional concerns because those who have not switched (paying the highest prices) are the least well-off

Competing policy goals

• For competition to work you need ‘winners and losers’

• ‘Reward’ those who search and switch

• NDC has resulted in less switching and higher prices for all consumers

• Enforced switching by suppliers will reduce incentives to switch

‘Thin end of the wedge’

• Labour party commitments on energy if it wins the next election

• “Price freeze” – 20 months following from May 2015

• Restructuring the industry: “breaking-up the Big 6”

• “Ofgem has failed” – should be replaced with a body with “real teeth”