the bric effect - u.s. chamber of commerce bric effect jim o’neill managing director head of...

TRANSCRIPT

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 1

The BRIC Effect

Jim O’NeillManaging Director Head of Global Economics, Commodities and Strategy Research

March 29 2010

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 2

GDP Forecasts

Source: GS Global ECS Research

GS Consensus* GS Consensus*USA 0.4 -2.4 2.6 3.1 2.4 3.0Japan -1.2 -5.2 2.2 1.9 1.7 1.6Euroland 0.5 -4.0 1.2 1.1 1.9 1.5UK 0.6 -4.9 1.7 1.4 3.4 2.3Europe 0.8 -3.9 1.4 1.2 2.3 1.8China 9.6 8.7 11.4 9.9 10.0 9.1India 6.7 6.6 8.2 8.2 8.7 7.9Brazil 5.1 -0.1 6.4 5.3 5.0 4.6Russia 5.6 -7.9 4.5 3.9 5.5 4.6BRICs 7.9 5.1 9.4 8.4 8.8 8.0Advanced Economies 0.5 -3.1 2.3 2.4 2.5 2.5

World 2.8 -0.7 4.6 4.3 4.7 4.3* Consensus Economics March 2010

% yoy 2008 20092010 2011

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 3

Domestic Demand Forecasts (%)

% yoy 2008 2009 (f) 2010 (f) 2011 (f)

USA -0.7 -3.4 2.3 1.9Japan -1.3 -4.0 1.5 1.3Euroland 0.6 -3.4 0.3 1.2UK 0.1 -5.3 1.2 2.5China 9.0 13.0 12.4 9.9India 4.8 4.9 7.6 9.7BRICs 8.1 7.0 9.8 9.3

Advanced Economies 0.2 -3.4 1.9 2.0

World 2.6 -0.4 4.4 4.4

Source: GS Global ECS Research

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 4

Change in US$ Size of GDP from 2000 to 2009

0500

100015002000250030003500400045005000

US$bn

Source: IMF, GS Global ECS Research*2000 GDP was adjusted for the updated 2003 re-base of the series.

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 5

Inflation Forecasts

Source: GS Global ECS Research

GS Consensus* GS Consensus*

USA 3.8 -0.3 1.9 2.2 0.5 1.9Japan 1.4 -1.4 -1.0 -1.1 -0.5 -0.3Euroland 3.3 0.3 1.0 1.1 1.6 1.4UK 3.6 2.2 2.5 2.6 1.4 1.7Europe 3.5 0.8 1.4 1.4 1.7 1.5China 5.9 -0.7 3.5 3.2 2.8 3.3India 8.4 3.4 5.0 3.3 5.5 6.6Brazil 5.7 4.9 5.1 4.6 5.4 4.7Russia 14.1 11.7 5.3 7.1 6.6 6.9BRICs 7.5 2.2 4.2 3.8 4.0 4.6Advanced Economies 3.4 0.2 1.5 1.6 1.2 1.6

World 5.4 1.6 2.9 2.9 2.7 3.1* Consensus Economics March 2010

% yoy 2008 20092010 2011

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 6

‘Crisis’ Indicator

-2

-1

0

1

2

3

4

5

6

90 92 94 96 98 00 02 04 06 08 10

Index

GS FSI (Financial Stress Index

Source: GS Global ECS Research

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 7

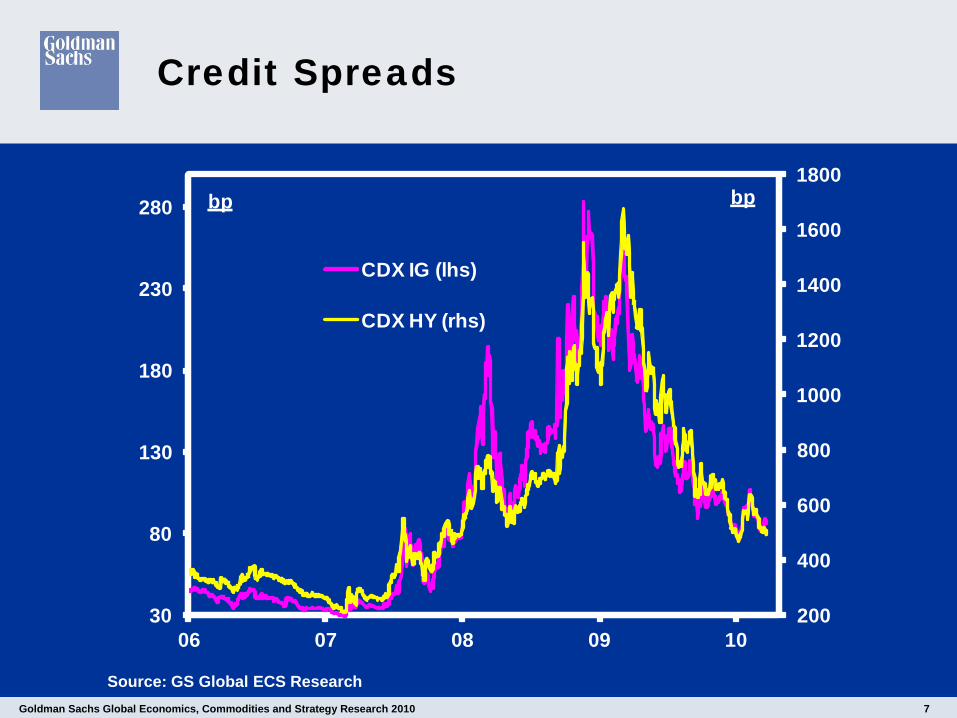

Credit Spreads

200

400

600

800

1000

1200

1400

1600

1800

30

80

130

180

230

280

06 07 08 09 10

bpbp

CDX IG (lhs)

CDX HY (rhs)

Source: GS Global ECS Research

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 8

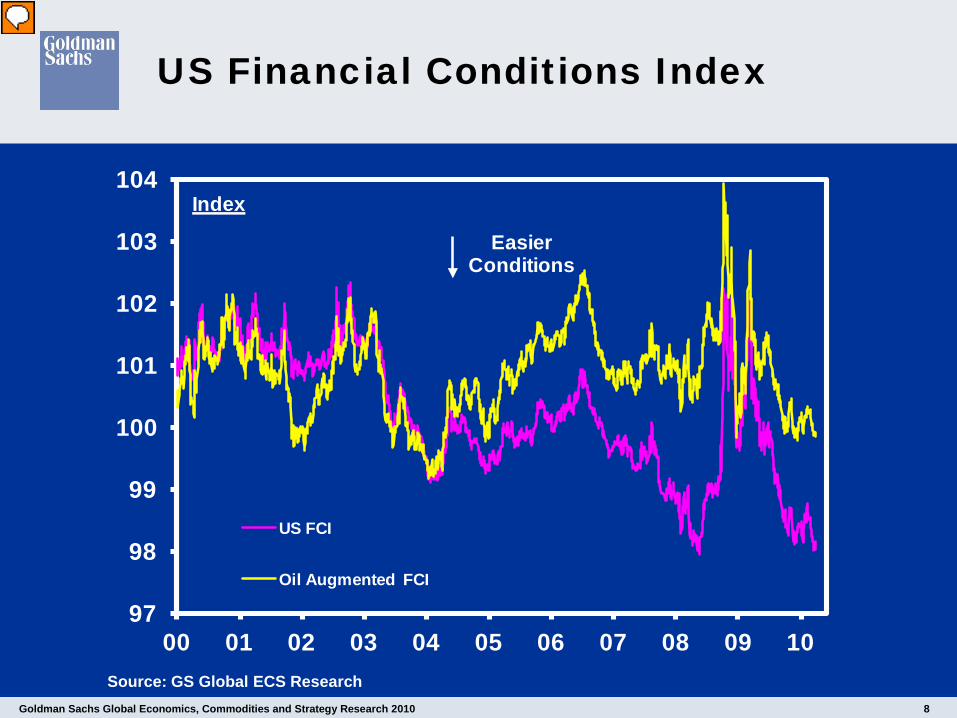

US Financial Conditions Index

Source: GS Global ECS Research

97

98

99

100

101

102

103

104

00 01 02 03 04 05 06 07 08 09 10

Index

US FCI

Oil Augmented FCI

Easier Conditions

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 9

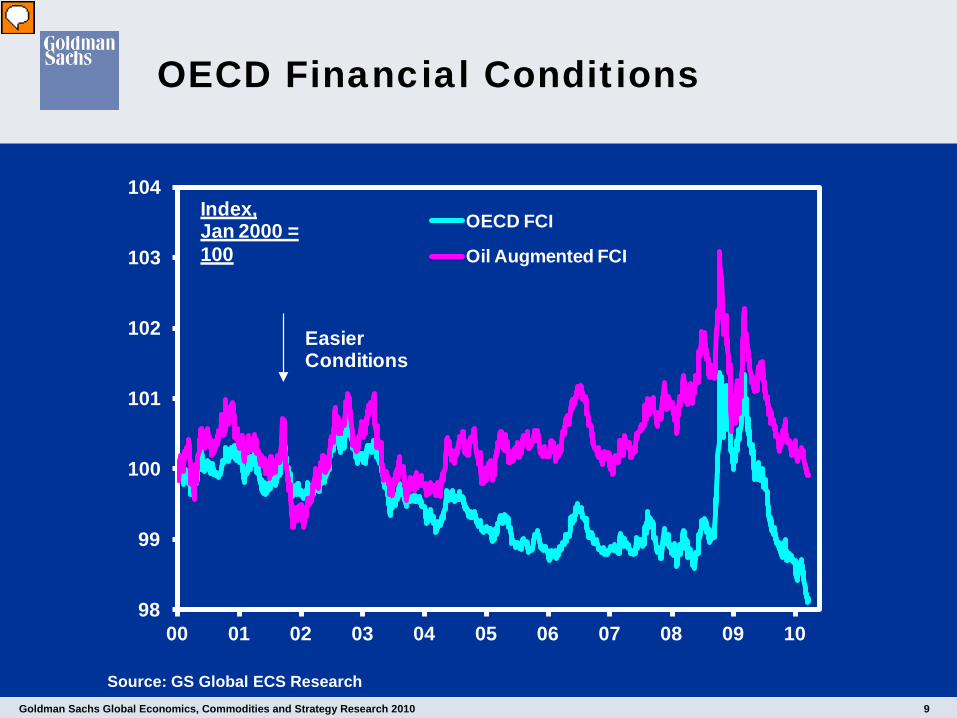

OECD Financial Conditions

Source: GS Global ECS Research

98

99

100

101

102

103

104

00 01 02 03 04 05 06 07 08 09 10

Index, Jan 2000 = 100

OECD FCI

Oil Augmented FCI

Easier Conditions

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 10

UK Financial Conditions Index

Source: GS Global ECS Research

92

93

94

95

96

97

98

99

100

101

102

98 99 00 01 02 03 04 05 06 07 08 09 10

Index

UK FCI

Easier Conditions

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 11

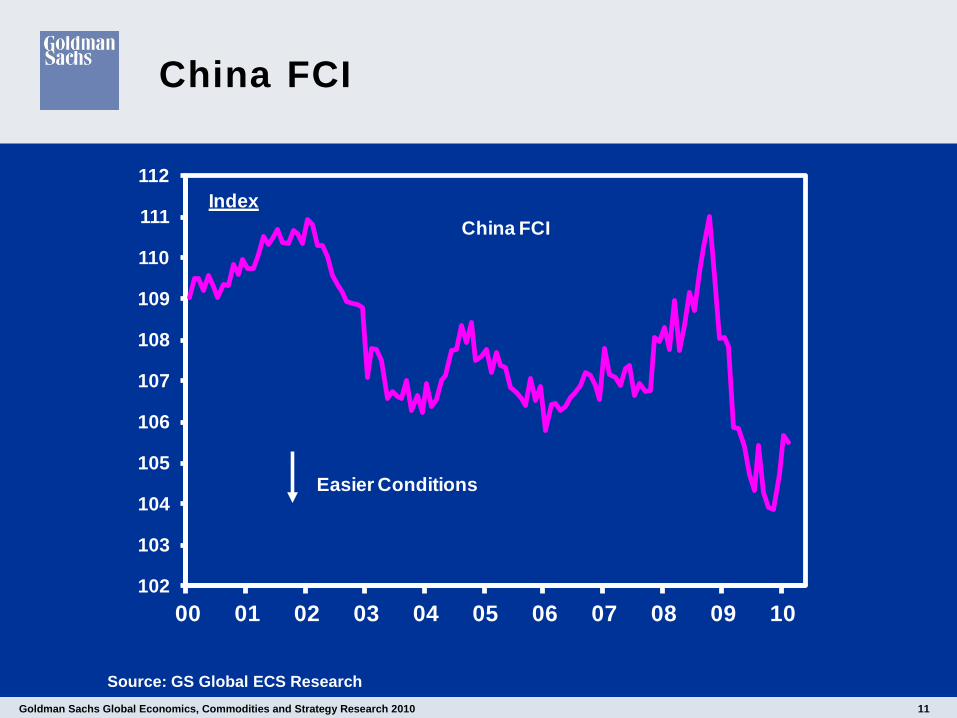

China FCI

Source: GS Global ECS Research

102

103

104

105

106

107

108

109

110

111

112

00 01 02 03 04 05 06 07 08 09 10

Index

Easier Conditions

China FCI

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 12

GLI vs IP

Source: GS Global ECS Research

-20

-16

-12

-8

-4

0

4

8

98 99 00 01 02 03 04 05 06 07 08 09 10

% yoy

GLI

G7 IP

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 13

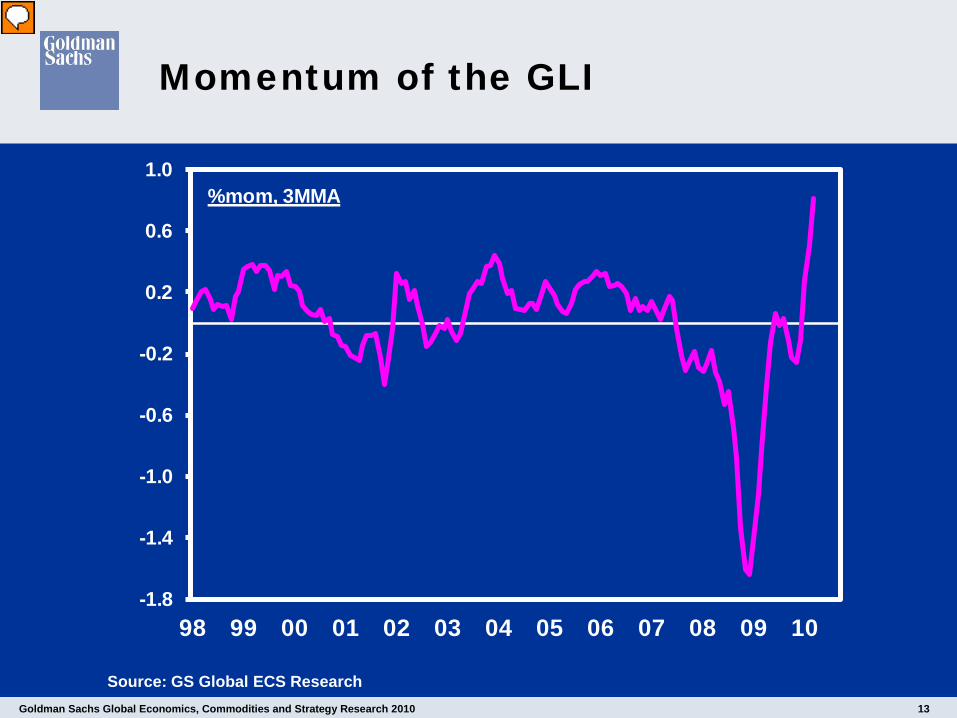

Momentum of the GLI

Source: GS Global ECS Research

-1.8

-1.4

-1.0

-0.6

-0.2

0.2

0.6

1.0

98 99 00 01 02 03 04 05 06 07 08 09 10

%mom, 3MMA

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 14

Monthly Direction of GLI Components

Source: GS Global ECS Research

UpBusiness Confidence Aggregate

GS Australian Dollar Trade Weighted IndexS&P GS Industrial Metals Index

US Initial Jobless ClaimsFlat

Belgian Manufacturing Survey

Japan IP Inventory/Sales Ratio

US Durable Goods Inventory/Shipments RatioDown

Consumer Confidence AggregateISM New Orders Less Inventories

Korean Exports

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 15

Korean Exports Year on Year Since 2006

Source: GS Global ECS Research

-70

-50

-30

-10

10

30

50

70

90

01 02 03 04 05 06 07 08 09 10

% yoy

% qoq sa ann

% chgFebruary

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 16

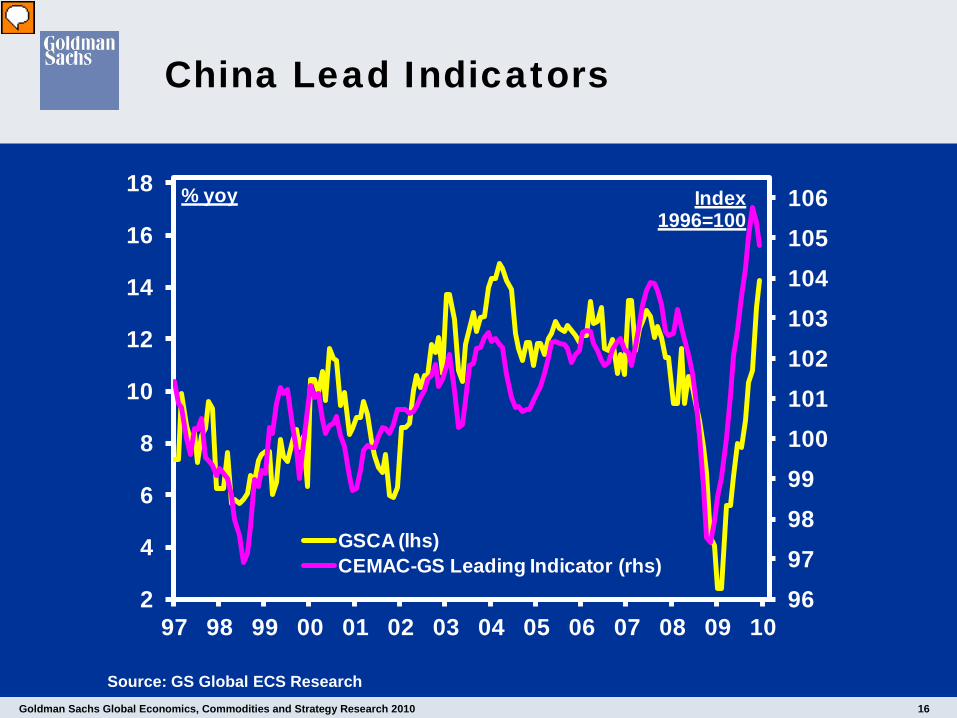

China Lead Indicators

Source: GS Global ECS Research

96979899100101102103104105106

2

4

6

8

10

12

14

16

18

97 98 99 00 01 02 03 04 05 06 07 08 09 10

Index1996=100

% yoy

GSCA (lhs)CEMAC-GS Leading Indicator (rhs)

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 17

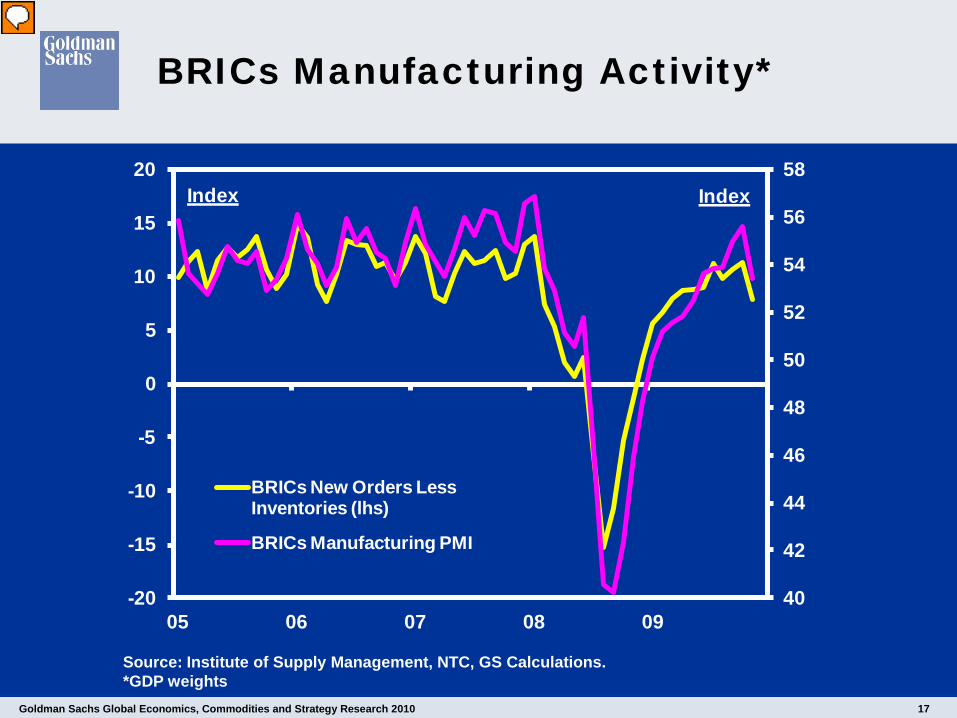

BRICs Manufacturing Activity*

Source: Institute of Supply Management, NTC, GS Calculations.*GDP weights

40

42

44

46

48

50

52

54

56

58

-20

-15

-10

-5

0

5

10

15

20

05 06 07 08 09

IndexIndex

BRICs New Orders Less Inventories (lhs)

BRICs Manufacturing PMI

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 18

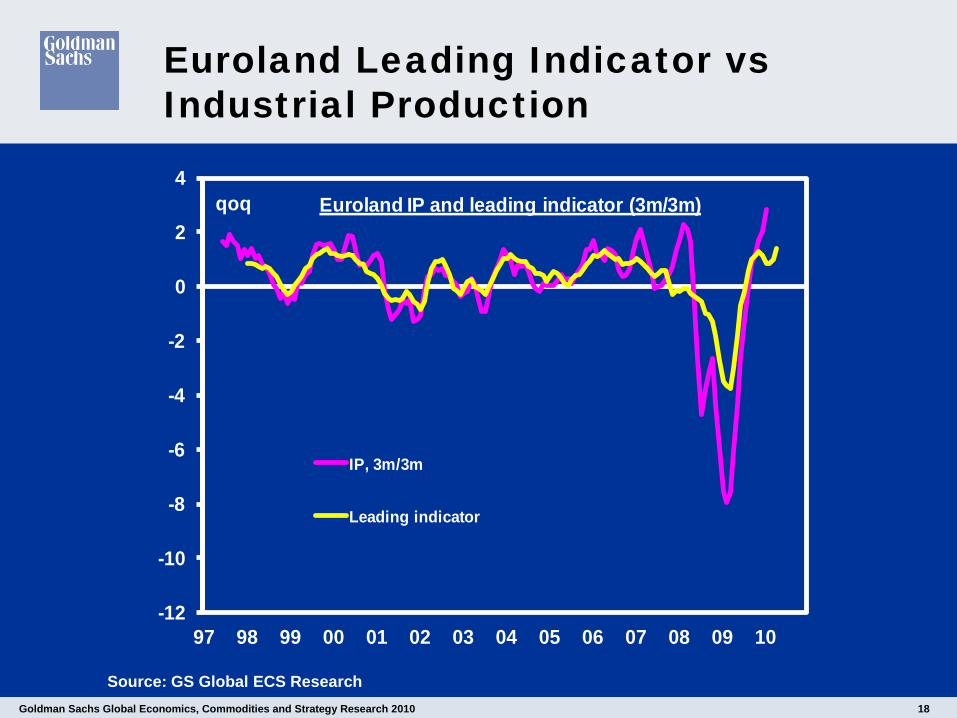

Euroland Leading Indicator vs Industrial Production

Source: GS Global ECS Research

-12

-10

-8

-6

-4

-2

0

2

4

97 98 99 00 01 02 03 04 05 06 07 08 09 10

qoq

IP, 3m/3m

Leading indicator

Euroland IP and leading indicator (3m/3m)

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 19

UK Services PMI

Source: GS Global ECS Research

35

40

45

50

55

60

65

97 98 99 00 01 02 03 04 05 06 07 08 09 10

Index

UK Services PMI

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 20

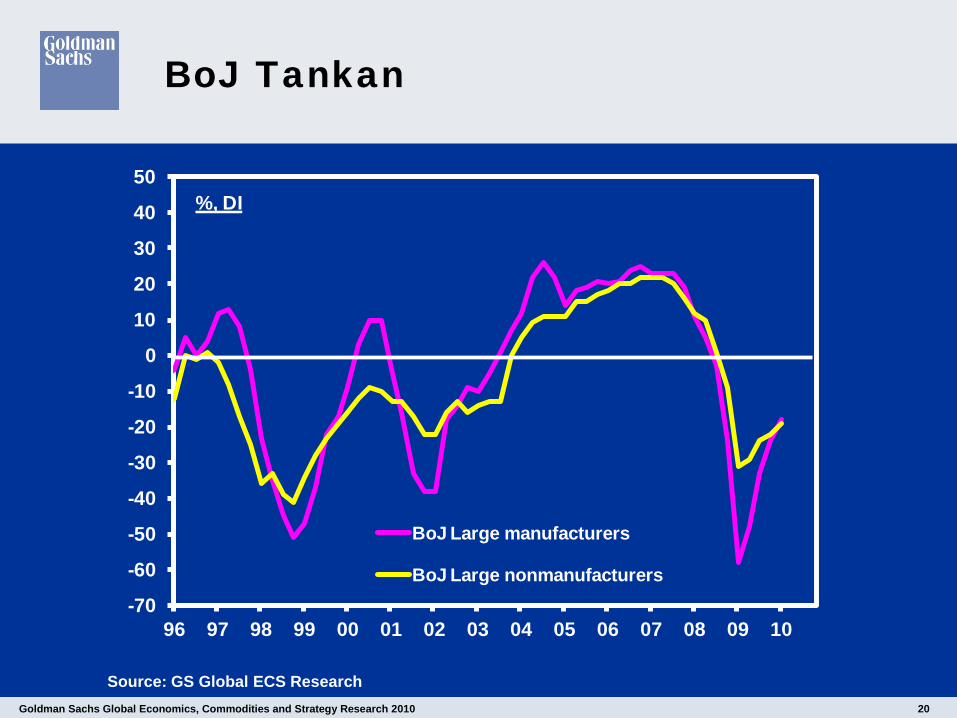

BoJ Tankan

Source: GS Global ECS Research

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

%, DI

BoJ Large manufacturers

BoJ Large nonmanufacturers

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 21

Relative Manufacturing Production

Source: GS Global ECS Research

60

70

80

90

100

110

120

06 07 08 09 10

indexJan06=100

Germany

Japan

Korea

Taiwan

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 22

US House Prices vs Income

3.0

4.0

5.0

6.0

7.0

8.0

9.02.5

3.0

3.5

4.0

4.5

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

House Price/Income Ratio* (left)Mortgage Rate (right, inverted)

Percent

* S.a. median home price divided by median family income.Source: Department of Commerce. FRB. NAR.

Ratio

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 23

Share of Private Consumption in US GDP

Source: GS Global ECS Research

65

66

67

68

69

70

71

72

90 92 94 96 98 00 02 04 06 08 10

% GDP

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 24

US Export and Import Growth

Source: GS Global ECS Research

-30

-25

-20

-15

-10

-5

0

5

10

15

20

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

3M MA,% yoy

Exports

Non-oil Imports

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 25

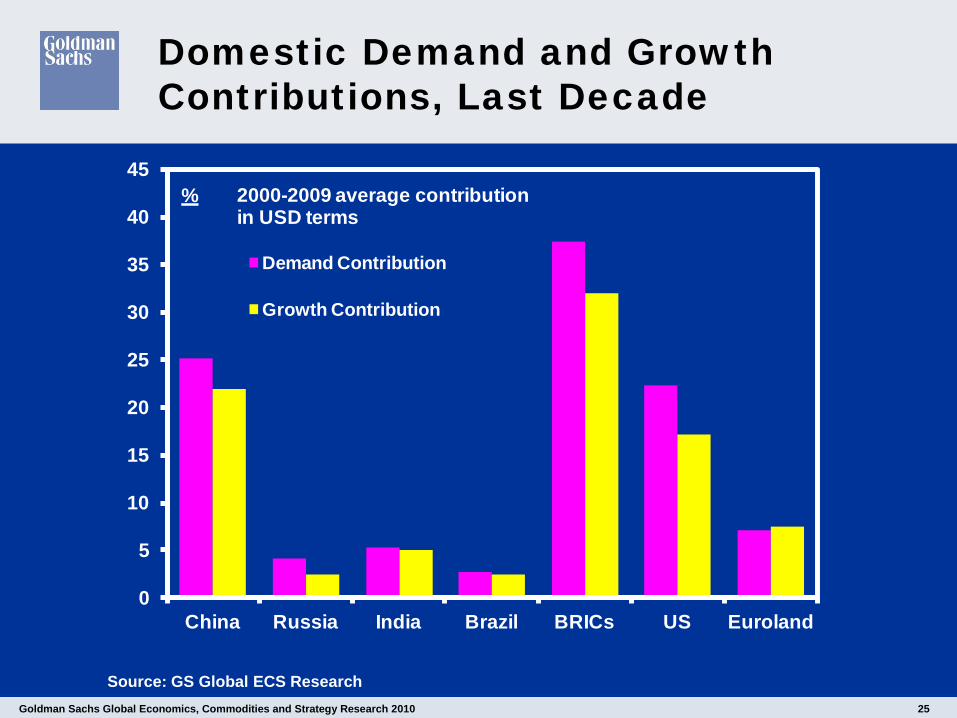

Domestic Demand and Growth Contributions, Last Decade

Source: GS Global ECS Research

0

5

10

15

20

25

30

35

40

45

China Russia India Brazil BRICs US Euroland

%

Demand Contribution

Growth Contribution

2000-2009 average contribution in USD terms

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 26

Retail Sales US and BRICs

Source: GS Global ECS Research

-12

-8

-4

0

4

8

12

16

20

24

28

32

36

04 05 06 07 08 09 10

%yoy

USA Brazil BRICsRussia China India*

* Private final consumption

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 27

Recent Trend in Real Retail Sales

Source: GS Global ECS Research

-60

-40

-20

0

20

40

60

80

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10

USD Billion Jan 2007

U.S.

China

Change in Real Retail Sales Since Jan 2007

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 28

Real Retail Sales in Developed vs EM

-60

-40

-20

0

20

40

60

80

100

120

140

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10

Bil$ WorldAdvancedEmerging

Source: National Sources, GS Global ECS Research.

Change in Real Retail Sales Since Jan 2007

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 29

Chinese Export and Import Growth

Source: GS Global ECS Research

-40

-20

0

20

40

60

80

05 06 07 08 09 10

%yoy, 3MMA

Total Exports

Total Imports

Non-Commodity Imports

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 30

Germany’s Exports to Asia rising –stabilisation elsewhere

60

70

80

90

100

110

120

130

140

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10

indexJan07=100

Source: Haver Analytics, GS calculations

ChinaIndiaRussiaUSUKFranceJapanItalySpain

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 31

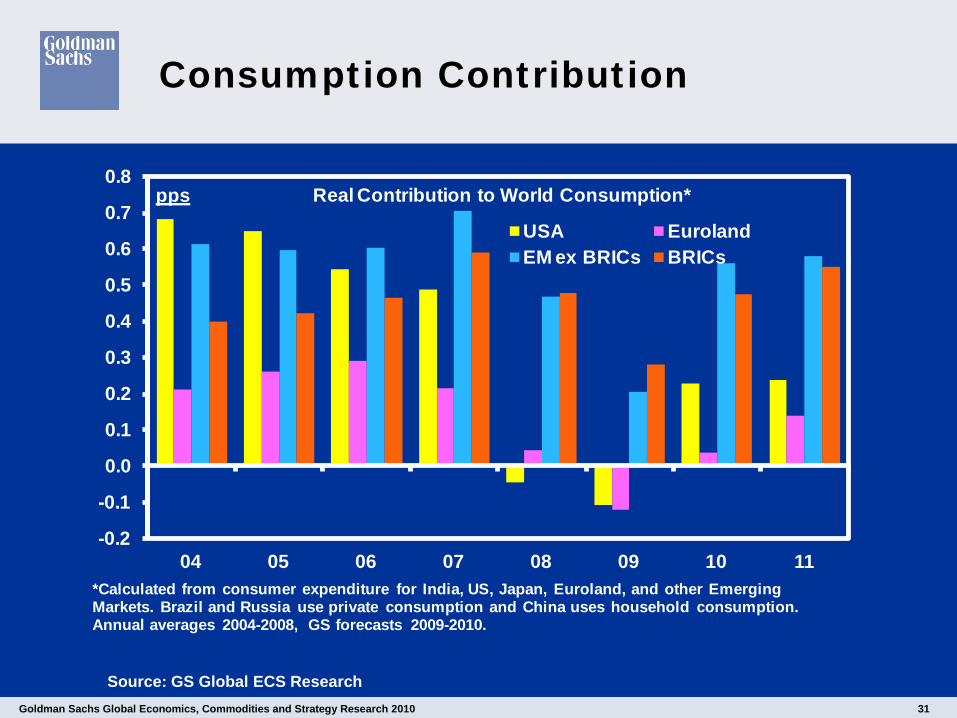

Consumption Contribution

Source: GS Global ECS Research

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

04 05 06 07 08 09 10 11

pps

USA EurolandEM ex BRICs BRICs

Real Contribution to World Consumption*

*Calculated from consumer expenditure for India, US, Japan, Euroland, and other Emerging Markets. Brazil and Russia use private consumption and China uses household consumption. Annual averages 2004-2008, GS forecasts 2009-2010.

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 32

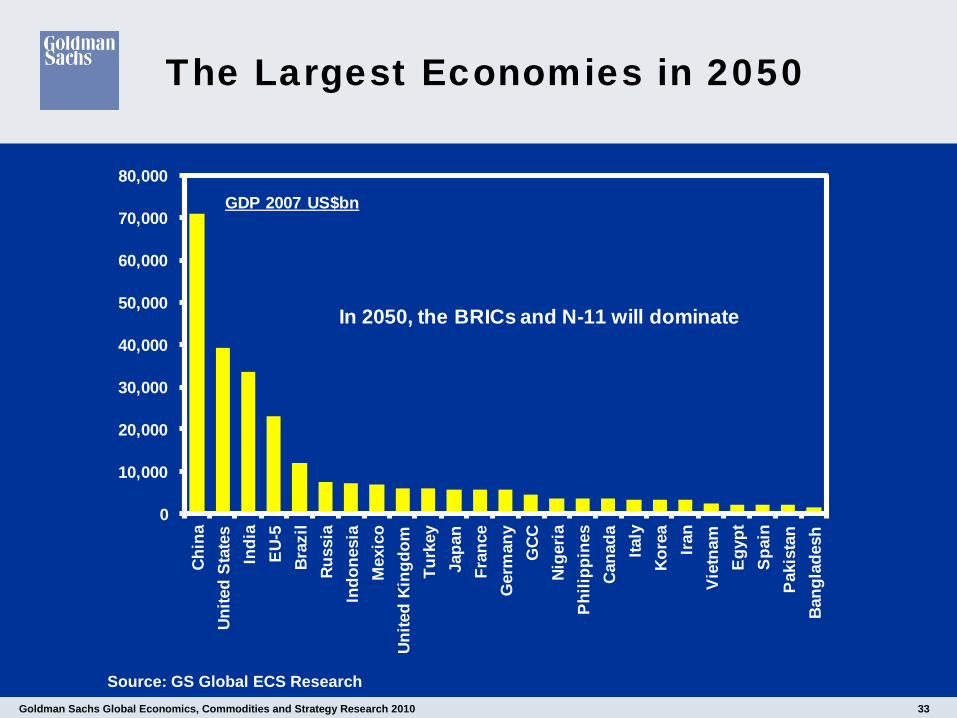

The Largest Economies in 2050

Source: GS Global ECS Research

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000GDP 2007 US$bn

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 33

The Largest Economies in 2050

Source: GS Global ECS Research

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000Ch

ina

Unite

d St

ates

Indi

aEU

-5Br

azil

Russ

iaIn

done

sia

Mex

ico

Unite

d Ki

ngdo

mTu

rkey

Japa

nFr

ance

Ger

man

yG

CCNi

geria

Phili

ppin

esCa

nada

Italy

Kore

aIra

nVi

etna

mEg

ypt

Spai

nPa

kist

anBa

ngla

desh

GDP 2007 US$bn

In 2050, the BRICs and N-11 will dominate

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 34

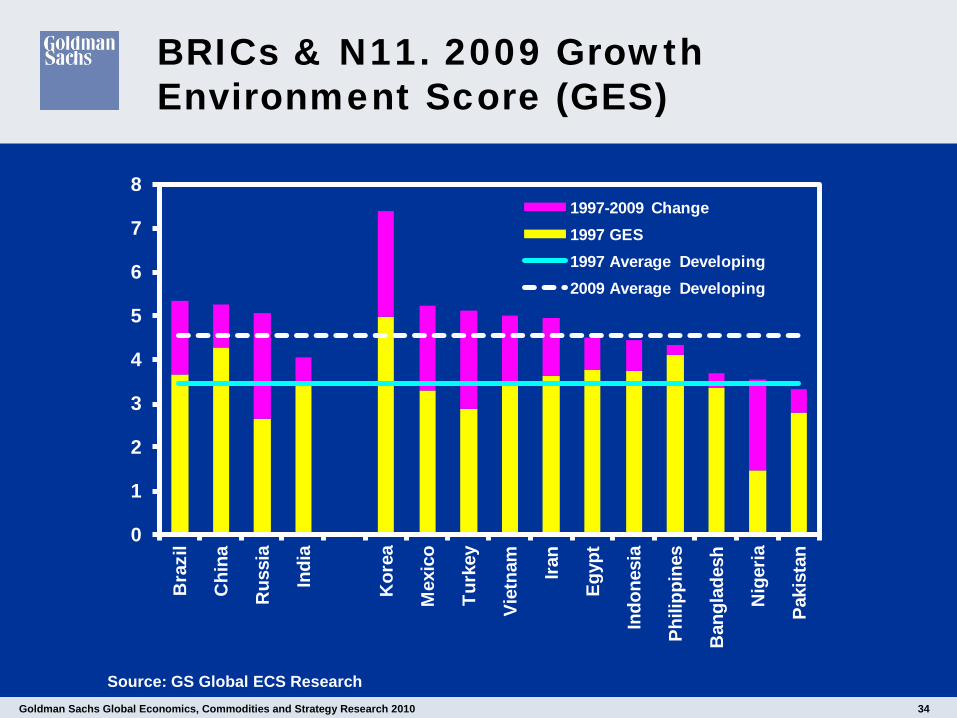

BRICs & N11. 2009 Growth Environment Score (GES)

Source: GS Global ECS Research

0

1

2

3

4

5

6

7

8B

razi

l

Chi

na

Rus

sia

Indi

a

Kor

ea

Mex

ico

Turk

ey

Viet

nam

Iran

Egyp

t

Indo

nesi

a

Phili

ppin

es

Ban

glad

esh

Nig

eria

Paki

stan

1997-2009 Change1997 GES1997 Average Developing2009 Average Developing

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 35

GES Scores for BRICs vs Korea

Source: GS Global ECS Research

Brazil China India Russia KoreaTotal 5.3 5.2 4.0 5.1 7.4

Rule of Law 4.4 4.3 5.2 3.2 6.6Corruption 4.9 4.1 4.3 3.0 5.9Political Stability 4.8 4.4 3.0 3.8 5.8Lifeexp 7.5 7.6 5.9 6.5 8.8Inflation 8.6 8.5 7.9 6.5 8.8External Debt 8.5 9.1 8.4 7.6 ..GovtDebt 4.0 4.8 0.0 7.1 5.6GFCF 3.8 8.0 6.9 4.4 5.9Schooling 7.4 6.2 4.2 6.9 9.7Openness 2.2 4.0 3.1 2.2 5.0Computers 2.1 0.8 0.4 1.8 7.7Mobiles 6.4 4.2 2.1 10.0 9.0Internet 4.7 2.2 1.0 2.8 10.0

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 36

Maplecroft Risk Indices

Dynamic Structural

BRICsBrazil 6.2 6.0Russia 2.5 5.8India 3.9 3.1China 5.4 3.5N11Bangladesh 3.1 1.7Egypt 4.9 4.3Indonesia 4.1 3.6Iran 1.9 4.0Mexico 6.5 6.1Nigeria 2.4 2.1Pakistan 2.2 1.3Philippines 3.8 4.3South Korea 8.3 8.9Turkey 6.0 5.9Vietnam 5.5 3.9USA 8.9 8.9Germany 9.2 9.2Luxembourg 9.7 9.5Source: Maplecroft

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 37

Each Country’s Share of Euroland GDP

0

5

10

15

20

25

30G

erm

any

Fran

ce

Italy

Spai

n

Net

herla

nds

Bel

gium

Aus

tria

Gre

ece

Finl

and

Irela

nd

Portu

gal

Slov

akia

Luxe

mbo

urg

Slov

enia

Cyp

rus

Mal

ta

% Euroland GDP

Country's Share of Euroland GDP (2009)

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 38

Cyclically Adjusted Budget Deficit (%GDP)**

Gross general government debt (% of GDP)***

Germany* -1.9 76.3France -7.0 77.8Italy -3.5 114.9Spain -10.0 55.2Netherlands -3.2 61.5Belgium -4.6 97.9Austria -3.3 67.6Greece -12.6 113.4Finland -0.5 39.6Ireland -9.6 64.5Portugal -6.6 76.6Slovakia -6.0 34.7*Countries listed according to their share of Euroland GDP.**Source: European Commission***Source: Eurostat, GS estimates.

Euroland Budget Deficit and Government Debt

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 39

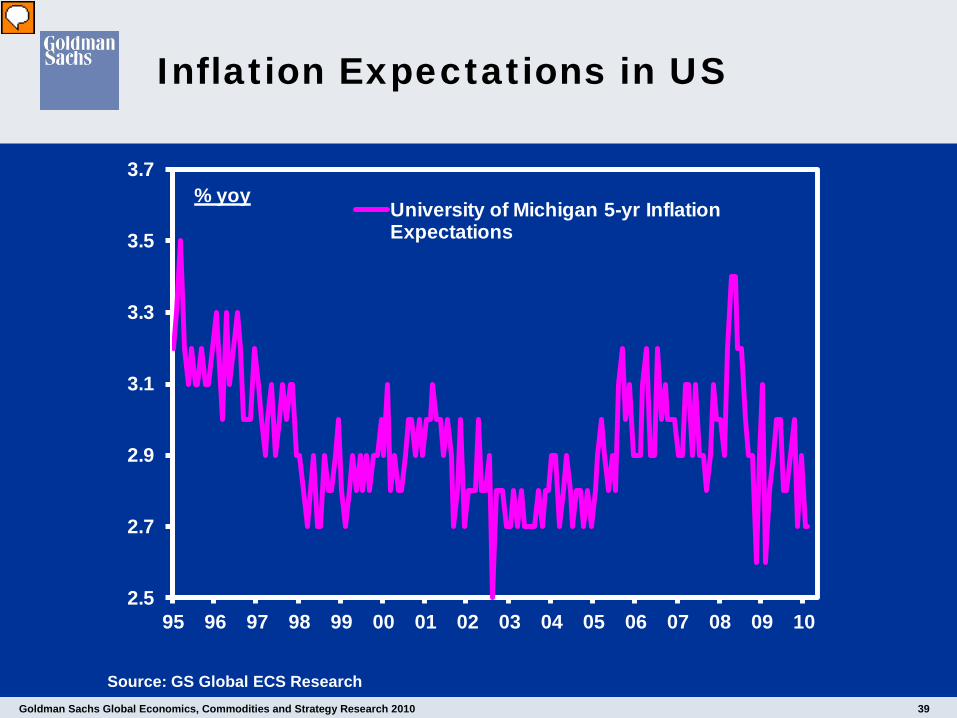

Inflation Expectations in US

Source: GS Global ECS Research

2.5

2.7

2.9

3.1

3.3

3.5

3.7

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

% yoyUniversity of Michigan 5-yr Inflation Expectations

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 40

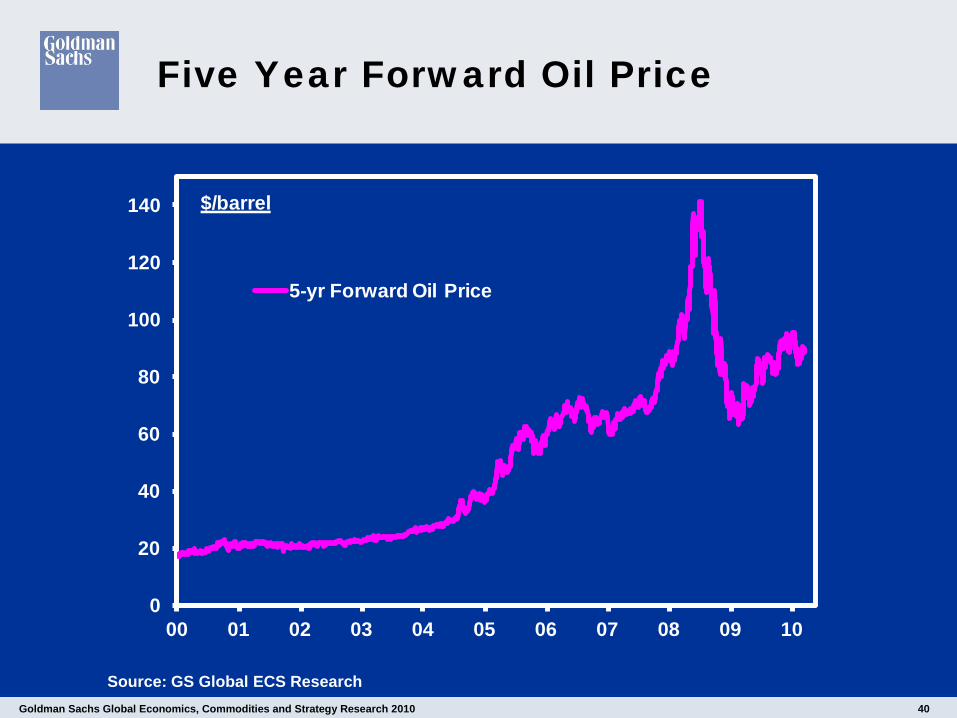

Five Year Forward Oil Price

Source: GS Global ECS Research

0

20

40

60

80

100

120

140

00 01 02 03 04 05 06 07 08 09 10

$/barrel

5-yr Forward Oil Price

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 41

GSDEER Estimates for Major Countries

Spot* GSDEER Q1-2010

% Deviation from GSDEER

5-Yr Forecast

EUR/$ 1.33 1.22 10 1.20

$/Yen 91.90 105.52 15 108.12

£/$ 1.49 1.59 -6.6 1.55

$/CNY 6.82 6.84 0.3 5.85

$/CAD 1.03 1.15 11.8 1.16

AUD/$ 0.91 0.79 14.3 0.79

$/KRW 1138 1274 12.0 975

$ TWI 210.8 232.1 -10.1 -

*as of 24 March 2010

Source: GS Global ECS Research

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 42

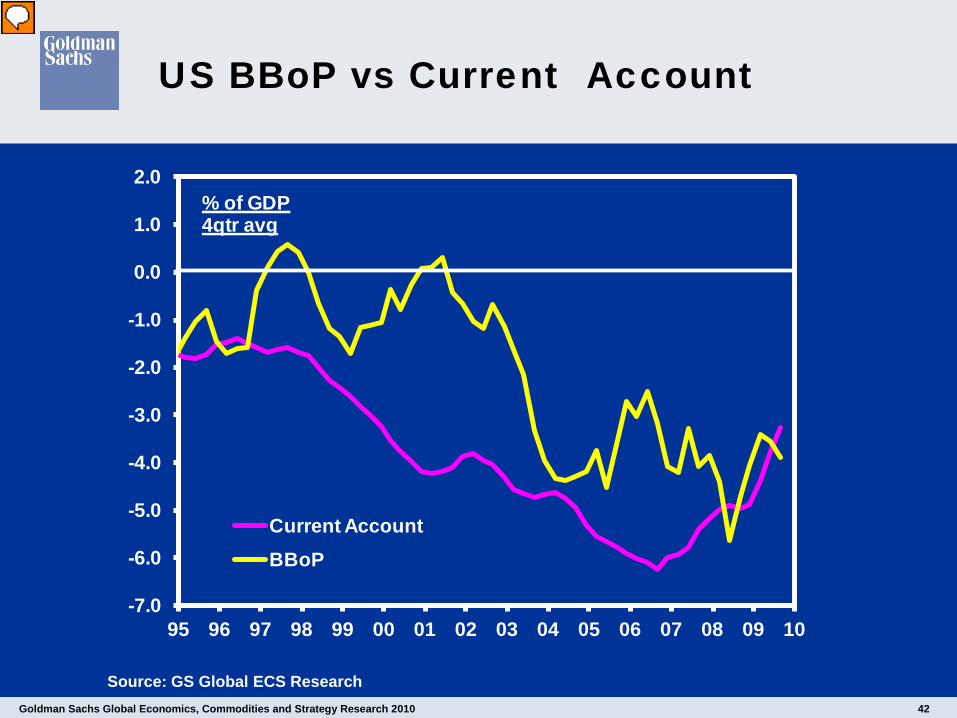

US BBoP vs Current Account

Source: GS Global ECS Research

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

% of GDP4qtr avg

Current AccountBBoP

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 43

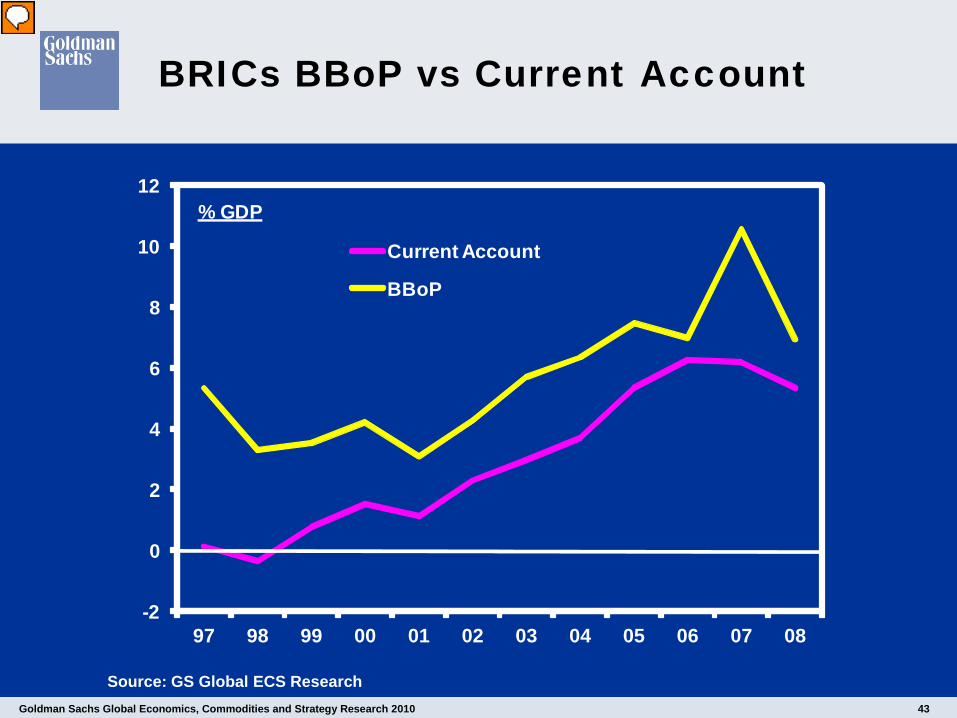

BRICs BBoP vs Current Account

-2

0

2

4

6

8

10

12

97 98 99 00 01 02 03 04 05 06 07 08

% GDP

Current Account

BBoP

Source: GS Global ECS Research

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 44

Euroland: BBoP vs Current Account

Source: GS Global ECS Research

-5

-4

-3

-2

-1

0

1

2

3

4

5

98 99 00 01 02 03 04 05 06 07 08 09 10

BBoP

Current Account

% of GDP12-Month Mov. Avg.

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 45

Japan: BBoP vs Current Account

Source: GS Global ECS Research

-10

-8

-6

-4

-2

0

2

4

6

8

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

% of GDP, 12MMA

BBoP

Current Account

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 46

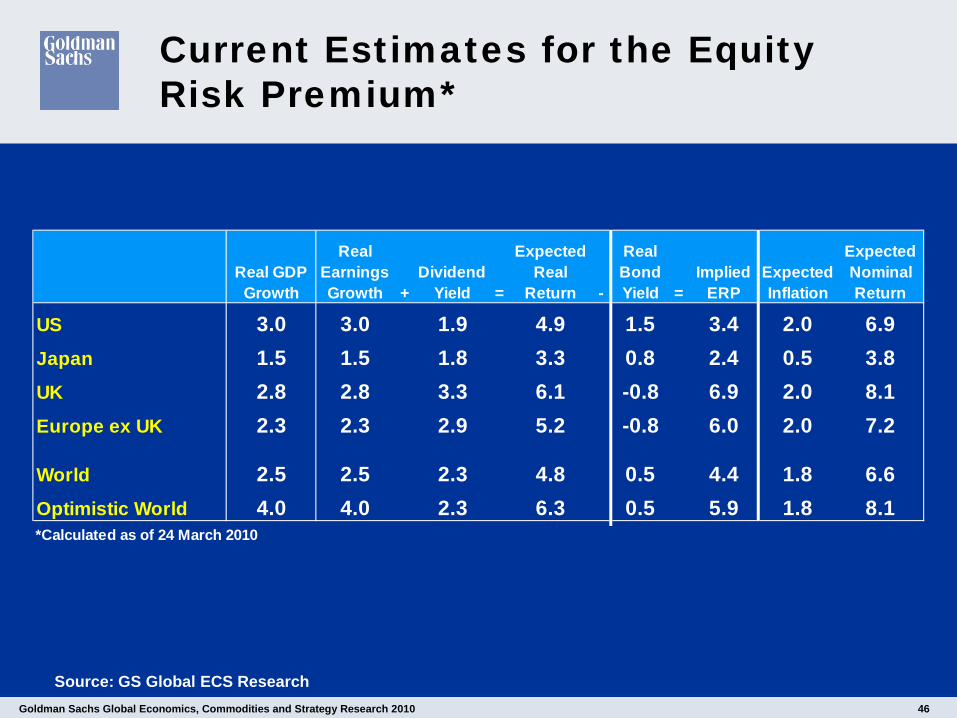

Current Estimates for the Equity Risk Premium*

Source: GS Global ECS Research

Real GDP Growth

Real Earnings Growth +

Dividend Yield =

Expected Real

Return -

Real Bond Yield =

Implied ERP

Expected Inflation

Expected Nominal Return

US 3.0 3.0 1.9 4.9 1.5 3.4 2.0 6.9Japan 1.5 1.5 1.8 3.3 0.8 2.4 0.5 3.8UK 2.8 2.8 3.3 6.1 -0.8 6.9 2.0 8.1Europe ex UK 2.3 2.3 2.9 5.2 -0.8 6.0 2.0 7.2

World 2.5 2.5 2.3 4.8 0.5 4.4 1.8 6.6Optimistic World 4.0 4.0 2.3 6.3 0.5 5.9 1.8 8.1*Calculated as of 24 March 2010

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 47

Trend in Forward P/Es

Source: GS Global ECS Research

0

5

10

15

20

25

30

35

06 06 07 08 08 09 10

12mth forward PE

United States JapanChina IndiaEurope RussiaBrazil

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 48

Interest Rate Forecasts

Source: GS Global ECS Research

3-month horizon 6-month horizon 12-month horizon

Current* Forward Forecast Forward Forecast Forward ForecastUS 3M 0.3 0.4 0.3 0.6 0.3 1.2 0.3

10Y 3.9 4.0 3.5 4.2 3.3 4.5 3.5Canada 3M 0.5 0.6 0.4 1.1 0.4 1.9 1.2

10Y 3.5 3.7 3.5 3.8 3.5 4.0 3.8Australia 3M 4.4 4.7 4.7 5.1 4.8 5.5 5.4

10Y 5.7 5.8 5.3 5.8 5.5 5.9 6.0Japan 3M 0.4 0.2 0.4 0.3 0.4 0.3 0.4

10Y 1.3 1.4 1.5 1.5 1.5 1.6 1.8Euroland 3M 0.6 0.7 0.8 0.9 1.0 1.4 1.5

10Y 3.1 3.1 3.3 3.2 3.3 3.3 3.4UK 3M 0.7 0.7 0.8 0.9 1.3 1.5 2.4

10Y 4.0 4.1 4.0 4.2 4.0 4.5 4.3Sweden 3M 0.5 0.7 0.5 1.1 1.0 1.8 2.5

10Y 3.0 3.1 3.3 3.2 3.4 3.4 3.8Switzerland 3M 0.3 0.3 0.3 0.4 0.5 1.2 1.0

10Y 1.8 1.9 2.0 1.9 2.1 2.1 2.3Close 24 March 10

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 49

Foreign Exchange Forecasts

3-months 6-months 12-months

Current* Forward Forecast Forward Forecast Forward Forecast

EUR/$ 1.33 1.33 1.45 1.33 1.45 1.33 1.35$/¥ 92.1 92.0 92.0 92.0 94.0 91.6 98.0EUR/¥ 122.8 122.8 133.4 122.7 136.3 122.2 132.3EUR/CHF 1.43 1.43 1.44 1.43 1.42 1.42 1.40CHF/¥ 85.91 85.93 92.64 85.94 95.99 85.83 94.50$/CHF 1.07 1.07 0.99 1.07 0.98 1.07 1.04EUR/£ 0.90 0.90 0.87 0.90 0.84 0.90 0.84£/$ 1.49 1.49 1.67 1.49 1.73 1.49 1.61£/¥ 137.1 137.0 153.3 136.8 162.3 136.2 157.5£/CHF 1.60 1.59 1.66 1.59 1.69 1.59 1.67EUR/NOK 8.04 8.08 8.00 8.11 7.90 8.18 7.80EUR/SEK 9.69 9.69 9.60 9.69 9.40 9.71 9.00A$/$ 0.91 0.90 0.95 0.89 0.95 0.87 0.90NZ$/$ 0.70 0.70 0.74 0.69 0.74 0.68 0.70$/C$ 1.02 1.02 1.00 1.03 1.00 1.03 1.08$/CNY 6.83 6.80 6.83 6.76 6.83 6.68 6.49

* Close 24 March 10

Source: GS Global ECS Research

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 50

Top Trades for 2010

Source: GS Global ECS Research

Trade Entry Level Target

1. Short S&P 500 Dec10/Dec11 Forward Starting Variance Swap 28.20 21.00

2. Long Russian Equities (RDXUSD) 1645.9 2050

3. Long GBP/NZD 2.29 2.60

4. Pay UK Rates vs. Receiving AUD Rates via 1-yr Forward 2-yr Swaps -268.5bp -150bp

5. Pay 2y Rates in Turkey 8.77% 12.00%

6. Long Credit Protection on Spain, Short Credit Protection on Ireland 70.2bp 20bp

7. Long 'Growth' FX Current 103.5 111.8

8. Long PLN/JPY 32.1 37.5

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 51

Disclaimer

I, Jim O’Neill hereby certify that all of the views expressed in this report accurately reflect personal views, which have not been influenced by considerations of the firm’s business or client relationships.

Global product; distributing entities

The Global Investment Research Division of Goldman Sachs produces and distributes research products for clients of Goldman Sachs, and pursuant to certain contractual arrangements, on a global basis. Analysts based inGoldman Sachs off ices around the w orld produce equity research on industries and companies, and research on macroeconomics, currencies, commodities and portfolio strategy. This research is disseminated in Australiaby Goldman Sachs JBWere Pty Ltd (ABN 21 006 797 897) on behalf of Goldman Sachs; in Canada by Goldman Sachs & Co. regarding Canadian equities and by Goldman Sachs & Co. (all other research); in Hong Kong byGoldman Sachs (Asia) L.L.C.; in India by Goldman Sachs (India) Securities Private Ltd.; in Japan by Goldman Sachs Japan Co., Ltd.; in the Republic of Korea by Goldman Sachs (Asia) L.L.C., Seoul Branch; in New Zealand byGoldman Sachs JBWere (NZ) Limited on behalf of Goldman Sachs; in Russia by OOO Goldman Sachs; in Singapore by Goldman Sachs (Singapore) Pte. (Company Number: 198602165W); and in the United States of Americaby Goldman Sachs & Co. Goldman Sachs International has approved this research in connection w ith its distribution in the United Kingdom and European Union.

European Union: Goldman Sachs International, authorised and regulated by the Financial Services Authority, has approved this research in connection w ith its distribution in the European Union and United Kingdom;Goldman, Sachs & Co. oHG, regulated by the Bundesanstalt für Finanzdienstleistungsaufsicht, may also distribute research in Germany.

General disclosuresThis research is for our clients only. Other than disclosures relating to Goldman Sachs, this research is based on current public information that w e consider reliable, but w e do not represent it is accurate or complete, and itshould not be relied on as such. We seek to update our research as appropriate, but various regulations may prevent us from doing so. Other than certain industry reports published on a periodic basis, the large majority ofreports are published at irregular intervals as appropriate in the analyst's judgment.

Goldman Sachs conducts a global full-service, integrated investment banking, investment management, and brokerage business. We have investment banking and other business relationships w ith a substantial percentage ofthe companies covered by our Global Investment Research Division. SIPC: Goldman, Sachs & Co., the United States broker dealer, is a member of SIPC (http://w w w .sipc.org).

Our salespeople, traders, and other professionals may provide oral or w ritten market commentary or trading strategies to our clients and our proprietary trading desks that reflect opinions that are contrary to the opinionsexpressed in this research. Our asset management area, our proprietary trading desks and investing businesses may make investment decisions that are inconsistent w ith the recommendations or view s expressed in thisresearch.

We and our aff iliates, off icers, directors, and employees, excluding equity and credit analysts, w ill from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives, if any,referred to in this research. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction w here such an offer or solicitation w ould be illegal. It does not constitute a personal recommendation or take into accountthe particular investment objectives, f inancial situations, or needs of individual clients. Clients should consider w hether any advice or recommendation in this research is suitable for their particular circumstances and, ifappropriate, seek professional advice, including tax advice. The price and value of investments referred to in this research and the income from them may fluctuate. Past performance is not a guide to future performance,future returns are not guaranteed, and a loss of original capital may occur. Fluctuations in exchange rates could have adverse effects on the value or price of, or income derived from, certain investments.

Certain transactions, including those involving futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Investors should review current options disclosure documents w hich areavailable from Goldman Sachs sales representatives or at http://w w w .theocc.com/publications/risks/riskchap1.jsp. Transactions cost may be signif icant in option strategies calling for multiple purchase and sales of optionssuch as spreads. Supporting documentation w ill be supplied upon request.

All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client w ebsites. Not all research content is redistributed to our clients or available to third-partyaggregators, nor is Goldman Sachs responsible for the redistribution of our research by third party aggregators. For all research available on a particular stock, please contact your sales representative or go tow w w .360.gs.com

Disclosure information is also available at http://w w w .gs.com/research/hedge.html or from Research Compliance, 200 West Street, New York, NY 10282.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of The Goldman Sachs Group, Inc.

© Copyright 2010, The Goldman Sachs Group, Inc. All Rights Reserved.