the bottom line on management tools - a look at their use and effectiveness across th

TRANSCRIPT

7/30/2019 The Bottom Line on Management Tools - A Look at their Use and Effectiveness across th

http://slidepdf.com/reader/full/the-bottom-line-on-management-tools-a-look-at-their-use-and-effectiveness 1/2

their competitive position, lessthan 50% of this year’s survey respondents cited improvingeconomic conditions in theirindustry, and 65% expressedconcern about how they willmeet their growth targets.

Bain & Company launched itsmulti-year research project in1993 to get the facts aboutmanagement tools. The primary

objective of this ongoing study is to provide managers with theinformation they need to iden-

tify, select, implement and inte-grate tools that will improvebottom line results. To qualify for inclusion a tool must berelevant to senior management,topical (as evidenced by cover-age in the business press), andmeasurable.

Over the past nine years, Bainhas assembled a database thatnow includes 6 323 respondents

from 70 countries in Europe,North America, Asia, Africaand South America. In this lastedition, Bain received 708 com-pleted surveys from a broadcross-section of internationalsenior executives (a well-ba-lanced mix of line and staff,corporate and divisional ma-nagers). These managers –300of who also agreed to personal,

follow-up interviews– representa full range of industries andcompany sizes. Roughly 43% of the companies are in the below $600 million bracket, 20% inthe $600 million to $2 billion,and 37% in the $2 billion andabove range.

The global 2002 study alsocompared results with thosecompiled in 2000 and found that

the most widely used toolsremained the same: StrategicPlanning, Benchmarking and

Mission and Vision Statements.Each was used by over 80% of survey participants. In leantimes, tools requiring large cashoutlays were used the least:Stock Buybacks, Corporate Venturingand Merger Integration Teams.

While usage increased in 2002,satisfaction rates remainedrelatively the same. Companieswere most satisfied with tools

that provide focus, both inter-nally and externally, namely:Corporate Code of Ethics,Strategic Planning and CoreCompetencies.

REGIONAL VARIANCES

The survey results suggest thatattitudes and tool usage vary by

region, which paints a strikingdifference in the ways managersapproach dealing with eco-nomic uncertainty.

North America is the only region to include Contingency Planning, not CustomerSegmentation, in its top 10.Europe counts CoreCompetencies in its top 10but not Corporate Code of Ethics. Interestingly, Asia Pacificresembles the global top 10preferences most closely, shift-

ing only in its ranking of the10th and 11th most used tool.The most striking change inSouth American tool usageis the fall from favour of Balanced Scorecard.

Asian managers also embracedthe broadest use of managementtechniques and placed greateremphasis on customer-focusedtools, such as CRM and

Customer Segmentation.European managers placeda greater premium onKnowledge Management andChange Management. NorthAmerican managers focusedlargely on cost cutting versusrevenue growth, using suchmethods as Downsizing,Outsourcing, Reengineering,and Stock Buybacks.

Over the past decade,executives have witnessedan explosion of managementtools and techniques ranging from TQM to CRM andfrom Reengineering to

Benchmarking. The term“management tool” now encompasses a broad spectrumof approaches to management–from simple planning softwareto complex organisationaldesigns, to revised businessphilosophies. Many of thesetools offer conflicting advice.One may call for keeping all your customers while anotheradvises you to focus only on

the most profitable. But all of these tools have one thing incommon: they promise to make

their users more successful.Today beleaguered managers–struggling to demonstratethat they can adapt to rapidchange in an increasingly challenging world– areturning to management toolsin unprecedented numbers.

Faced with a continuing

economic slump, companies are–more than ever– relying onmanagement tools and tech-niques to reach elusive growthtargets. According to an ongo-ing Bain & Company survey,there has been a dramaticincrease in the number andtypes of analytical methodsthat companies are applying tosqueeze profits and producti-vity during the current down-

turn –a jump of nearly 60% from2000 to 2002. While 51% hadused the recession to improve

Bain & Company · Hong Kong · Johannesburg · London · Los Angeles · Madrid · Mexico City · Milan · page 2

Top 10 Used Tools by Region

The Bottom Line on Management A Look at their Use and Effectiveness across the World

North South

Global Top 10 Europe America Asia America

1. Strategic Planning 1 1 1 22. Benchmarking 4 3 3 13. Mission and Vision Statements 5 2 4 44. Customer Segmentation 3 12 2 65. Corporate Codes of Ethics 13 4 9 86. CRM 2 10 5 117. Customer Surveys 6 7 11 38. Outsourcing 8 5 7 59. Growth Strategies 9 8 8 9

10. Pay-for-Performance 10 6 6 7

7/30/2019 The Bottom Line on Management Tools - A Look at their Use and Effectiveness across th

http://slidepdf.com/reader/full/the-bottom-line-on-management-tools-a-look-at-their-use-and-effectiveness 2/2

Bain & Company · Munich · New York · Paris · Rome · San Francisco · São Paulo · Seoul page 3

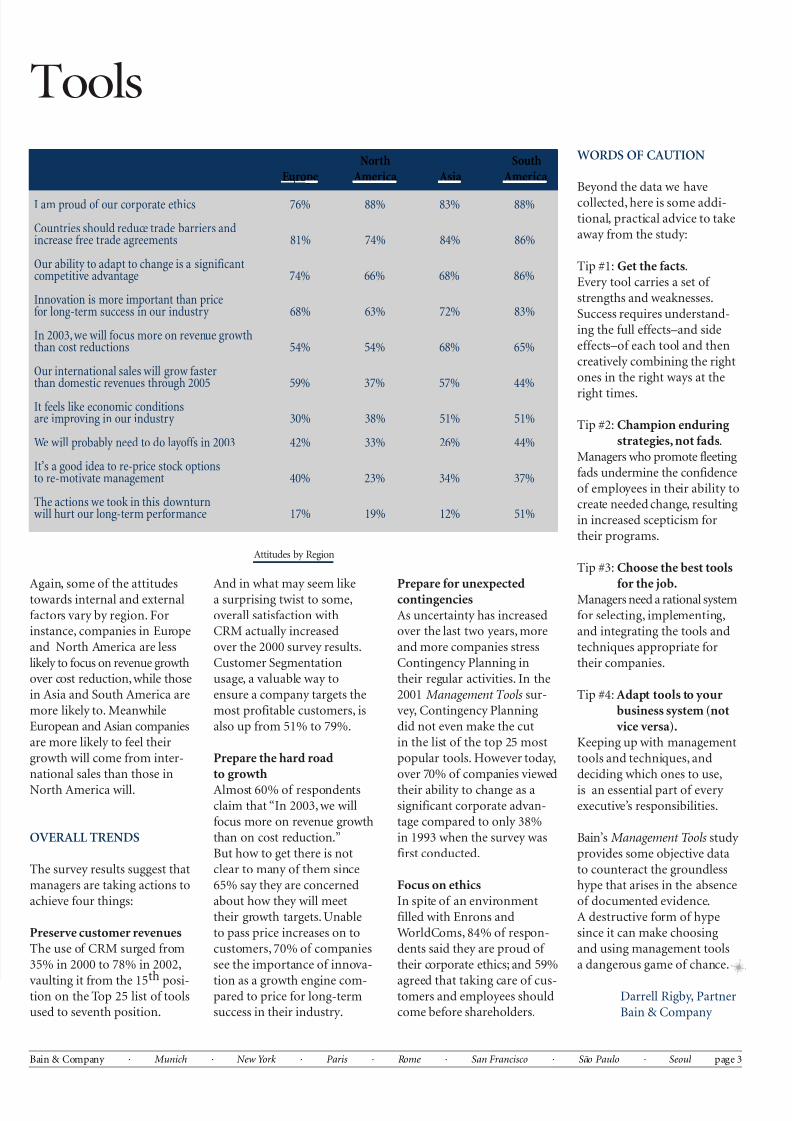

Again, some of the attitudestowards internal and externalfactors vary by region. Forinstance, companies in Europeand North America are lesslikely to focus on revenue growthover cost reduction, while thosein Asia and South America aremore likely to. MeanwhileEuropean and Asian companiesare more likely to feel theirgrowth will come from inter-national sales than those in

North America will.

OVERALL TRENDS

The survey results suggest thatmanagers are taking actions toachieve four things:

Preserve customer revenuesThe use of CRM surged from35% in 2000 to 78% in 2002,

vaulting it from the 15th posi-tion on the Top 25 list of toolsused to seventh position.

And in what may seem likea surprising twist to some,overall satisfaction withCRM actually increasedover the 2000 survey results.Customer Segmentationusage, a valuable way toensure a company targets themost profitable customers, isalso up from 51% to 79%.

Prepare the hard roadto growth

Almost 60% of respondentsclaim that “In 2003, we willfocus more on revenue growththan on cost reduction.”But how to get there is notclear to many of them since65% say they are concernedabout how they will meettheir growth targets. Unableto pass price increases on tocustomers, 70% of companiessee the importance of innova-

tion as a growth engine com-pared to price for long-termsuccess in their industry.

Prepare for unexpectedcontingenciesAs uncertainty has increasedover the last two years, moreand more companies stressContingency Planning intheir regular activities. In the2001 Management Tools sur-vey, Contingency Planningdid not even make the cutin the list of the top 25 mostpopular tools. However today,over 70% of companies viewed

their ability to change as asignificant corporate advan-tage compared to only 38%in 1993 when the survey wasfirst conducted.

Focus on ethicsIn spite of an environmentfilled with Enrons andWorldComs, 84% of respon-dents said they are proud of their corporate ethics; and 59%

agreed that taking care of cus-tomers and employees shouldcome before shareholders.

WORDS OF CAUTION

Beyond the data we havecollected, here is some addi-tional, practical advice to takeaway from the study:

Tip #1: Get the facts.Every tool carries a set of strengths and weaknesses.Success requires understand-ing the full effects–and sideeffects–of each tool and thencreatively combining the rightones in the right ways at the

right times.

Tip #2: Champion enduring strategies, not fads.

Managers who promote fleetingfads undermine the confidenceof employees in their ability tocreate needed change, resultingin increased scepticism fortheir programs.

Tip #3: Choose the best tools

for the job.Managers need a rational systemfor selecting, implementing,and integrating the tools andtechniques appropriate fortheir companies.

Tip #4: Adapt tools to yourbusiness system (not vice versa).

Keeping up with managementtools and techniques, anddeciding which ones to use,

is an essential part of every executive’s responsibilities.

Bain’s Management Tools study provides some objective datato counteract the groundlesshype that arises in the absenceof documented evidence.A destructive form of hypesince it can make choosingand using management toolsa dangerous game of chance.

Darrell Rigby, PartnerBain & Company

Tools

North South

Europe America Asia America

I am proud of our corporate ethics 76% 88% 83% 88%

Countries should reduce trade barriers andincrease free trade agreements 81% 74% 84% 86%

Our ability to adapt to change is a significantcompetitive advantage 74% 66% 68% 86%

Innovation is more important than pricefor long-term success in our industry 68% 63% 72% 83%

In 2003, we will focus more on revenue growththan cost reductions 54% 54% 68% 65%

Our international sales will grow fasterthan domestic revenues through 2005 59% 37% 57% 44%

It feels like economic conditionsare improving in our industry 30% 38% 51% 51%

We will probably need to do layoffs in 2003 42% 33% 26% 44%

It’s a good idea to re-price stock optionsto re-motivate management 40% 23% 34% 37%

The actions we took in this downturnwill hurt our long-term performance 17% 19% 12% 51%

Attitudes by Region