the big - marketresearch · 2.5.4 growing demand for telematics services.....42 2.5.5 moving...

TRANSCRIPT

The Big

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 2

Table of Contents

1 Chapter 1: Introduction ................................................................................... 18

1.1 Executive Summary ....................................................................................................................................... 18

1.2 Topics Covered .............................................................................................................................................. 19

1.3 Historical Revenue & Forecast Segmentation ............................................................................................... 20

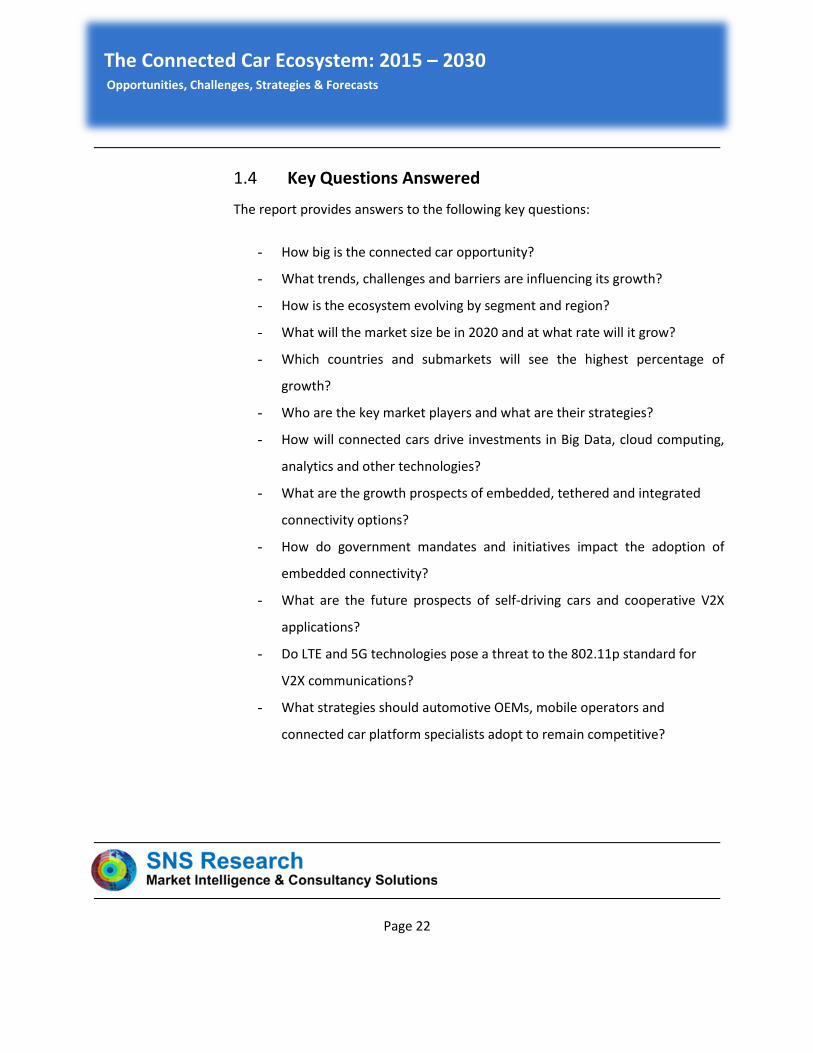

1.4 Key Questions Answered ............................................................................................................................... 22

1.5 Key Findings ................................................................................................................................................... 23

1.6 Methodology ................................................................................................................................................. 24

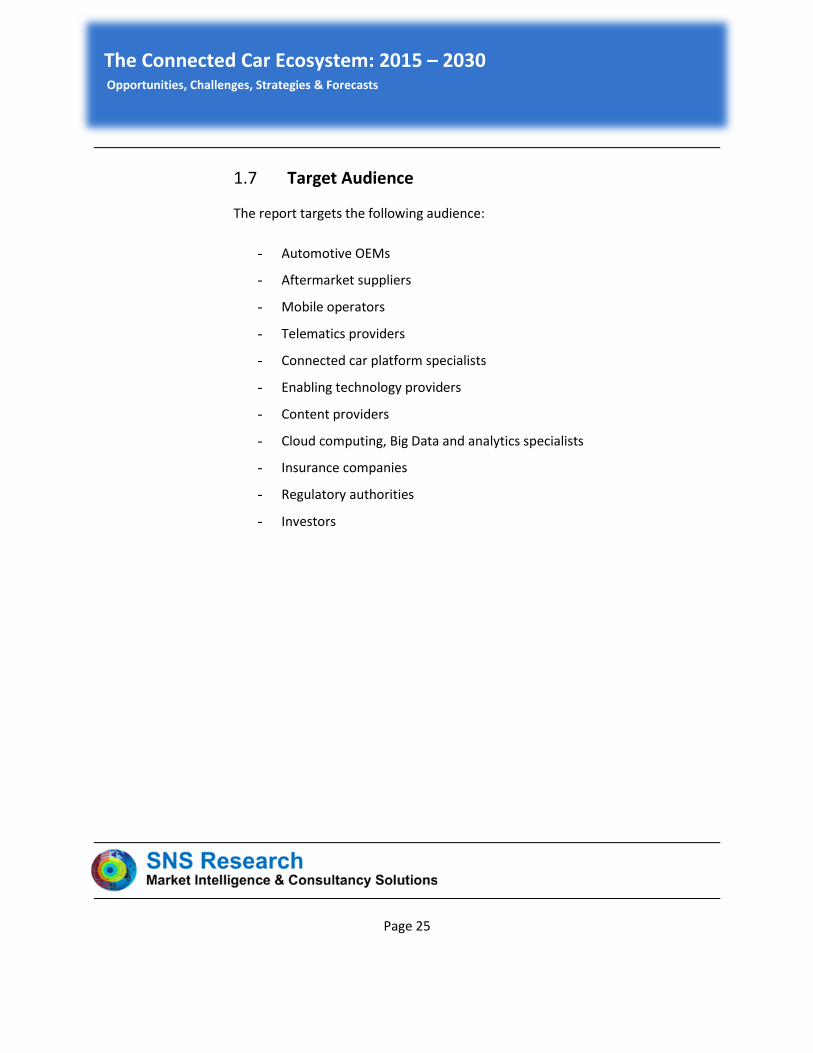

1.7 Target Audience ............................................................................................................................................ 25

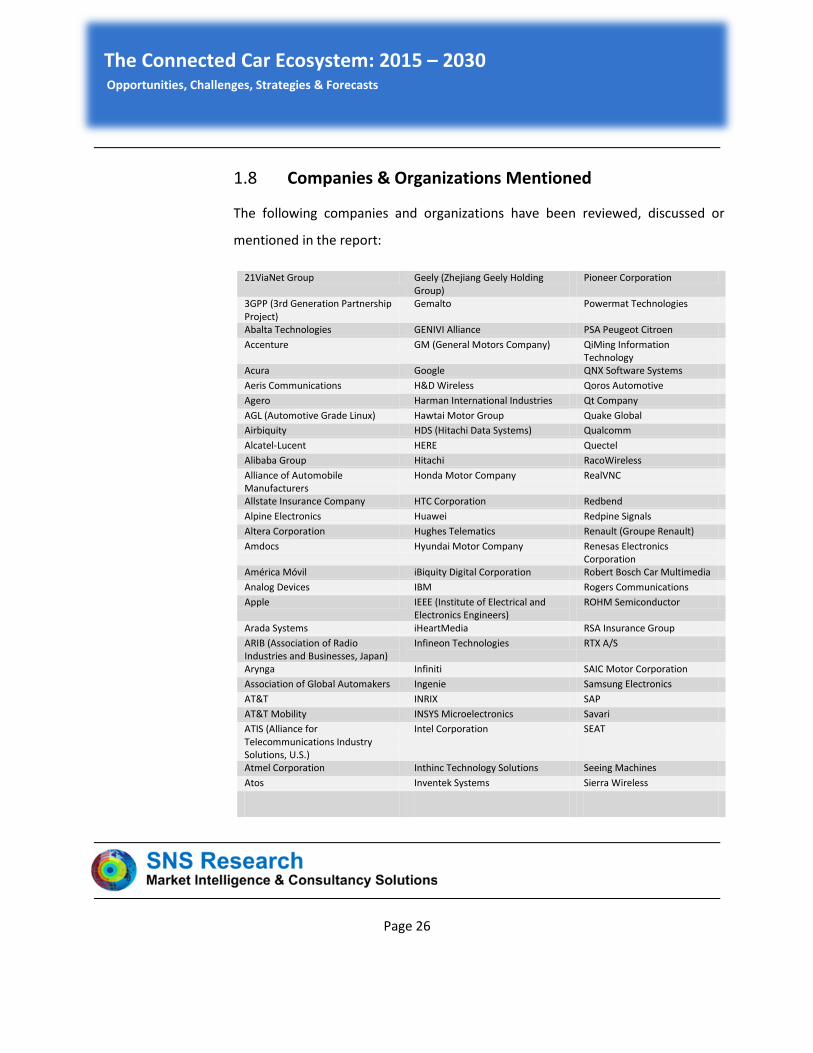

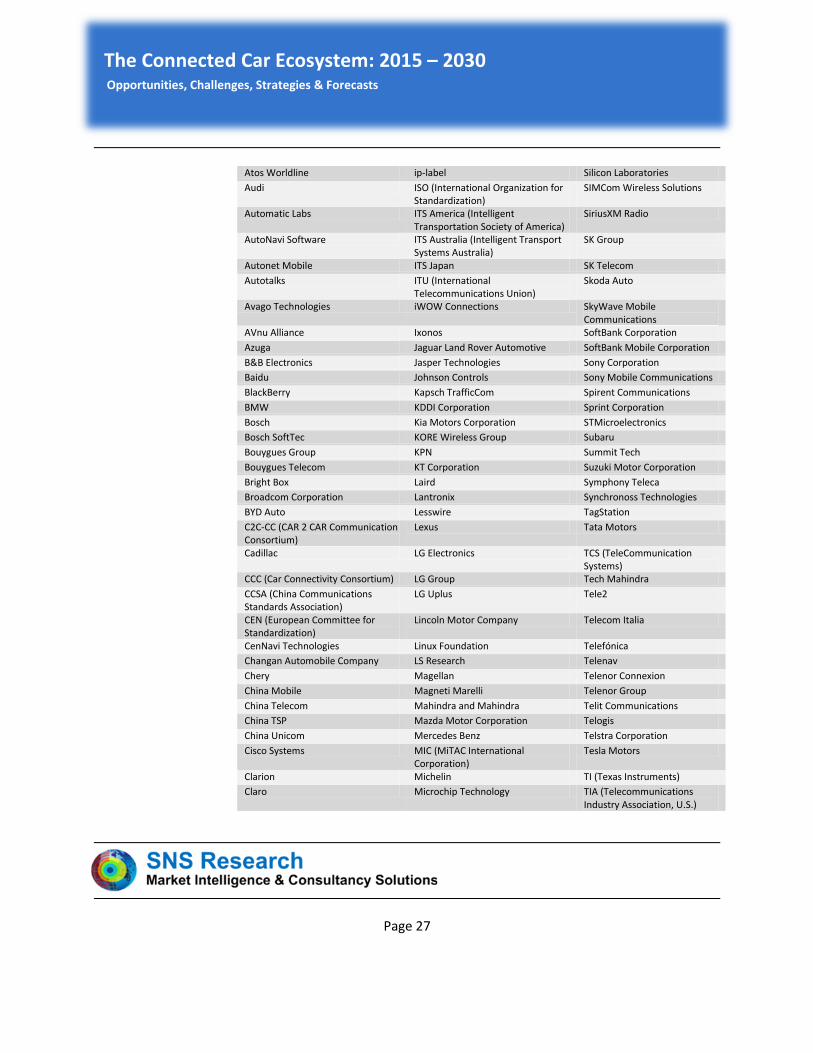

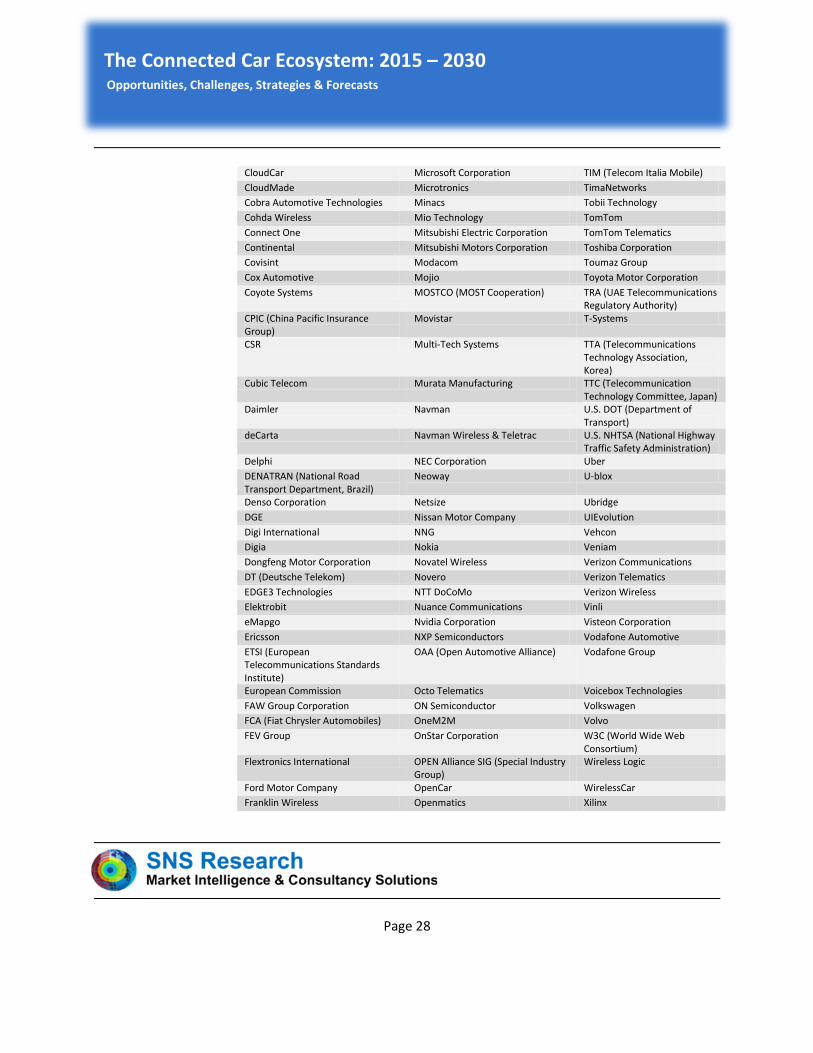

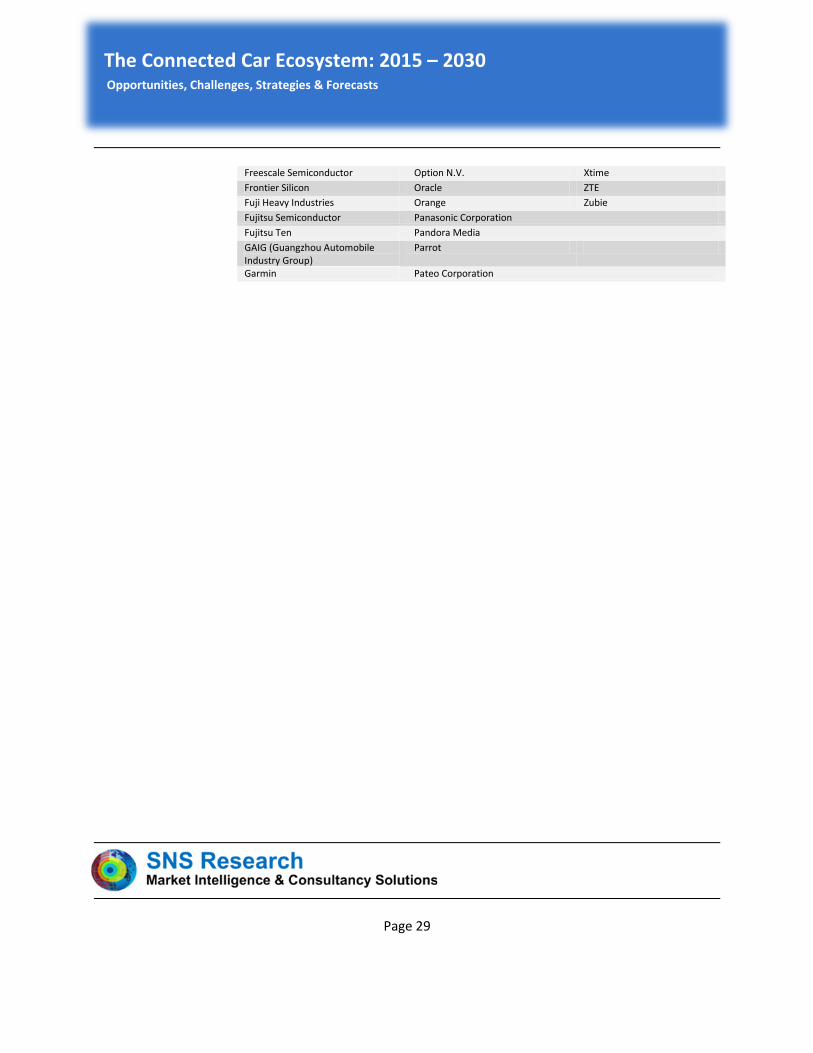

1.8 Companies & Organizations Mentioned ....................................................................................................... 26

2 Chapter 2: An Overview of Connected Cars ...................................................... 31

2.1 What are Connected Cars? ............................................................................................................................ 31

2.2 Connectivity Approaches............................................................................................................................... 32

2.2.1 Embedded ......................................................................................................................................... 32

2.2.2 Tethered ............................................................................................................................................ 32

2.2.3 Integrated .......................................................................................................................................... 32

2.3 Comparison of OEM Connected Car Programs ............................................................................................. 33

2.4 Key Enabling Technologies ............................................................................................................................ 34

2.4.1 M2M Connectivity & Mobile Networks ............................................................................................. 34

2.4.2 Smart Device Integration & Tethering ............................................................................................... 34

2.4.3 Ethernet & Short Range Wireless ...................................................................................................... 35

2.4.4 V2X (Vehicle-to-Everything) Communications .................................................................................. 35

2.4.5 Navigation Systems ........................................................................................................................... 36

2.4.6 Infotainment Systems ....................................................................................................................... 36

2.4.7 HMI (Human Machine Interface) Technologies ................................................................................ 36

2.4.7.1 Display, Touchscreens & Tactile Feedback .................................................................................................... 36

2.4.7.2 Voice Recognition ......................................................................................................................................... 37

2.4.7.3 Gesture Control ............................................................................................................................................. 37

2.4.7.4 Proximity Sensors .......................................................................................................................................... 37

2.4.7.5 Eye Tracking .................................................................................................................................................. 38

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 3

2.4.8 ADAS: Sensors & Other Technologies................................................................................................ 38

2.4.9 Operating Systems & Software Platforms ......................................................................................... 39

2.4.10 Cloud Computing ............................................................................................................................... 39

2.4.11 Big Data & Analytics .......................................................................................................................... 40

2.4.12 Other Technologies ........................................................................................................................... 41

2.5 Market Growth Drivers ................................................................................................................................. 41

2.5.1 Proliferation of Mobile Broadband ................................................................................................... 41

2.5.2 Connected Infotainment: A Key Purchase Factor .............................................................................. 41

2.5.3 Integration: Benefiting from the Smartphone Ecosystem ................................................................ 41

2.5.4 Growing Demand for Telematics Services ......................................................................................... 42

2.5.5 Moving Towards Intelligent Transportation & Autonomous Driving ................................................ 42

2.5.6 Enhancing Safety & Security .............................................................................................................. 42

2.5.7 Customer Retention & Additional Revenue Streams ........................................................................ 43

2.5.8 Growing Adoption of Electric Vehicles .............................................................................................. 43

2.5.9 Regulatory Initiatives & Mandates .................................................................................................... 43

2.6 Market Barriers ............................................................................................................................................. 44

2.6.1 Standardization Complexities ............................................................................................................ 44

2.6.2 Addressing Driver Distraction Concerns ............................................................................................ 44

2.6.3 Privacy & Security Issues ................................................................................................................... 44

2.6.4 Consumer Acceptance & Monetizing Services .................................................................................. 45

2.6.5 Product Lifecycle ............................................................................................................................... 45

2.6.6 Connectivity in Rural Areas ............................................................................................................... 45

2.6.7 Roaming ............................................................................................................................................. 45

3 Chapter 3: Key Application Areas ..................................................................... 46

3.1 Communications & Infotainment ............................................................................................................... 46

3.1.1 Hands-Free Calling & Messaging ....................................................................................................... 46

3.1.2 In-Vehicle WiFi Hotspots ................................................................................................................... 46

3.1.3 News & Weather Updates ................................................................................................................. 46

3.1.4 Web Browsing & Social Networking .................................................................................................. 47

3.1.5 Multimedia Streaming & Downloads ................................................................................................ 47

3.1.6 Live Agent Services ............................................................................................................................ 47

3.2 Navigation & Location Services .................................................................................................................. 48

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 4

3.2.1 Navigation, Traffic Information & Alternative Routing ..................................................................... 48

3.2.2 POI (Point of Interest) Search ............................................................................................................ 48

3.2.3 Location Based Marketing ................................................................................................................. 48

3.2.4 Geo-Fencing Applications .................................................................................................................. 49

3.2.5 Fleet Management ............................................................................................................................ 49

3.2.6 ETC (Electronic Toll Collection) .......................................................................................................... 49

3.3 Vehicle Management ................................................................................................................................. 50

3.3.1 Remote Diagnostics, Performance Monitoring & Maintenance ....................................................... 50

3.3.2 OTA (Over-the-Air) System Updates ................................................................................................. 50

3.3.3 UBI (Usage Based Insurance) ............................................................................................................. 50

3.4 Safety & Security ........................................................................................................................................ 51

3.4.1 Crash Alerting Systems ...................................................................................................................... 51

3.4.2 Roadside & Accident Assistance ........................................................................................................ 51

3.4.3 Keyless Authentication ...................................................................................................................... 52

3.4.4 Driver Monitoring & Fatigue Detection ............................................................................................. 52

3.4.5 Early Warning Systems ...................................................................................................................... 52

3.5 Driver Assistance & Autonomous Driving .................................................................................................. 53

3.5.1 Connected ADAS Features ................................................................................................................. 53

3.5.2 Intelligent Transportation ................................................................................................................. 53

3.5.3 Parking Assistance ............................................................................................................................. 53

3.5.4 Self-Driving Cars ................................................................................................................................ 54

3.6 Other Applications ..................................................................................................................................... 54

4 Chapter 4: Collaboration, Standardization & Regulatory Landscape ................. 55

4.1 Consortiums & Collaborative Projects ....................................................................................................... 55

4.1.1 CCC (Car Connectivity Consortium) ................................................................................................... 55

4.1.2 OAA (Open Automotive Alliance) ...................................................................................................... 55

4.1.3 C2C-CC (CAR 2 CAR Communication Consortium) ............................................................................. 56

4.1.4 GENIVI Alliance .................................................................................................................................. 56

4.1.5 AGL (Automotive Grade Linux) .......................................................................................................... 57

4.1.6 OPEN Alliance SIG (Special Industry Group) ...................................................................................... 57

4.1.7 MOSTCO (MOST Cooperation) .......................................................................................................... 58

4.1.8 AVnu Alliance .................................................................................................................................... 58

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 5

4.1.9 Regional Projects ............................................................................................................................... 59

4.1.10 Others ................................................................................................................................................ 60

4.2 Standardization Initiatives ......................................................................................................................... 61

4.2.1 3GPP (3rd Generation Partnership Project) ...................................................................................... 61

4.2.2 IEEE (Institute of Electrical and Electronics Engineers) ..................................................................... 61

4.2.3 OneM2M ........................................................................................................................................... 62

4.2.4 ISO (International Organization for Standardization) ........................................................................ 63

4.2.5 ETSI (European Telecommunications Standards Institute) ............................................................... 63

4.2.6 CEN (European Committee for Standardization) .............................................................................. 64

4.2.7 W3C (World Wide Web Consortium) ................................................................................................ 64

4.3 Government Mandates & Initiatives .......................................................................................................... 65

4.3.1 U.S. DOT’s V2V Connectivity Initiative .............................................................................................. 65

4.3.2 European Union’s eCall ..................................................................................................................... 65

4.3.3 Russia’s ERA-GLONASS ...................................................................................................................... 66

4.3.4 Brazil’s SINIAV & SIMRAV 245 ........................................................................................................... 66

5 Chapter 5: Connected Car Industry Roadmap & Value Chain ............................ 68

5.1 Industry Roadmap ...................................................................................................................................... 68

5.1.1 2015 – 2020: The Emergence of Connected Car Programs ............................................................... 68

5.1.2 2020 – 2025: Large Scale Proliferation of Advanced Telematics & Infotainment ............................. 69

5.1.3 2025 – 2030: The Era of Self-Driving Cars & Cooperative V2X Applications ..................................... 69

5.2 Value Chain ................................................................................................................................................ 70

5.2.1 Enabling Technology .......................................................................................................................... 70

5.2.1.1 Hardware Providers ...................................................................................................................................... 71

5.2.1.2 Software Providers ........................................................................................................................................ 71

5.2.2 Production ......................................................................................................................................... 71

5.2.2.1 Automotive OEMs ......................................................................................................................................... 71

5.2.2.2 Aftermarket Suppliers ................................................................................................................................... 72

5.2.3 Distribution ........................................................................................................................................ 72

5.2.3.1 Dealers .......................................................................................................................................................... 72

5.2.3.2 Other Intermediaries .................................................................................................................................... 72

5.2.4 Services & Solutions .......................................................................................................................... 73

5.2.4.1 Connected Car Platform Specialists .............................................................................................................. 73

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 6

5.2.4.2 Telematics Providers ..................................................................................................................................... 73

5.2.4.3 Connectivity Providers .................................................................................................................................. 73

5.2.4.4 Content Providers ......................................................................................................................................... 74

5.2.4.5 Cloud Platform Providers .............................................................................................................................. 74

5.2.4.6 Big Data & Analytics Specialists..................................................................................................................... 74

5.2.4.7 Insurance Companies .................................................................................................................................... 74

5.2.4.8 Supplementary Service Providers ................................................................................................................. 75

5.2.5 End Users ........................................................................................................................................... 75

5.2.5.1 Vehicle Owners ............................................................................................................................................. 75

6 Chapter 6: Key Market Players ......................................................................... 76

6.1 21ViaNet Group ......................................................................................................................................... 76

6.2 Abalta Technologies ................................................................................................................................... 77

6.3 Accenture ................................................................................................................................................... 78

6.4 Acura .......................................................................................................................................................... 79

6.5 Aeris Communications ............................................................................................................................... 80

6.6 Airbiquity .................................................................................................................................................... 81

6.7 Alcatel-Lucent ............................................................................................................................................ 82

6.8 Alibaba Group ............................................................................................................................................ 83

6.9 Allstate Insurance Company ...................................................................................................................... 84

6.10 Alpine Electronics ....................................................................................................................................... 85

6.11 Altera Corporation ..................................................................................................................................... 86

6.12 Amdocs ....................................................................................................................................................... 87

6.13 América Móvil ............................................................................................................................................ 88

6.14 Analog Devices ........................................................................................................................................... 89

6.15 Apple .......................................................................................................................................................... 90

6.16 Arada Systems ............................................................................................................................................ 91

6.17 Arynga ........................................................................................................................................................ 92

6.18 AT&T ........................................................................................................................................................... 93

6.19 Atmel Corporation ..................................................................................................................................... 94

6.20 Atos ............................................................................................................................................................ 95

6.21 Audi ............................................................................................................................................................ 96

6.22 Automatic Labs ........................................................................................................................................... 97

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 7

6.23 Autonet Mobile .......................................................................................................................................... 98

6.24 Autotalks .................................................................................................................................................... 99

6.25 Avago Technologies ................................................................................................................................. 100

6.26 Azuga ........................................................................................................................................................ 101

6.27 B&B Electronics ........................................................................................................................................ 102

6.28 Baidu ........................................................................................................................................................ 103

6.29 BlackBerry ................................................................................................................................................ 104

6.30 BMW ........................................................................................................................................................ 105

6.31 Bosch ........................................................................................................................................................ 106

6.32 Bouygues Telecom ................................................................................................................................... 107

6.33 Bright Box ................................................................................................................................................. 108

6.34 BYD Auto .................................................................................................................................................. 109

6.35 Cadillac ..................................................................................................................................................... 110

6.36 CenNavi Technologies .............................................................................................................................. 111

6.37 Changan Automobile Company ............................................................................................................... 112

6.38 Chery ........................................................................................................................................................ 113

6.39 China Mobile ............................................................................................................................................ 114

6.40 China Telecom .......................................................................................................................................... 115

6.41 China TSP .................................................................................................................................................. 116

6.42 China Unicom ........................................................................................................................................... 117

6.43 Cisco Systems ........................................................................................................................................... 118

6.44 Clarion ...................................................................................................................................................... 119

6.45 CloudCar ................................................................................................................................................... 120

6.46 CloudMade ............................................................................................................................................... 121

6.47 Cohda Wireless......................................................................................................................................... 122

6.48 Connect One............................................................................................................................................. 123

6.49 Continental ............................................................................................................................................... 124

6.50 Covisint ..................................................................................................................................................... 125

6.51 Cox Automotive ........................................................................................................................................ 126

6.52 Coyote Systems ........................................................................................................................................ 127

6.53 CPIC (China Pacific Insurance Group) ....................................................................................................... 128

6.54 CSR ........................................................................................................................................................... 129

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 8

6.55 Cubic Telecom .......................................................................................................................................... 130

6.56 Delphi ....................................................................................................................................................... 131

6.57 Denso Corporation ................................................................................................................................... 132

6.58 Digi International ..................................................................................................................................... 133

6.59 Digia ......................................................................................................................................................... 134

6.60 Dongfeng Motor Corporation .................................................................................................................. 135

6.61 DT (Deutsche Telekom) ............................................................................................................................ 136

6.62 EDGE3 Technologies ................................................................................................................................. 137

6.63 Ericsson .................................................................................................................................................... 138

6.64 FAW Group Corporation .......................................................................................................................... 139

6.65 FCA (Fiat Chrysler Automobiles) .............................................................................................................. 140

6.66 FEV Group ................................................................................................................................................ 141

6.67 Flextronics International .......................................................................................................................... 142

6.68 Ford Motor Company ............................................................................................................................... 143

6.69 Franklin Wireless ...................................................................................................................................... 144

6.70 Freescale Semiconductor ......................................................................................................................... 145

6.71 Frontier Silicon ......................................................................................................................................... 146

6.72 Fujitsu Semiconductor ............................................................................................................................. 147

6.73 Fujitsu Ten ................................................................................................................................................ 148

6.74 GAIG (Guangzhou Automobile Industry Group) ...................................................................................... 149

6.75 Garmin...................................................................................................................................................... 150

6.76 Geely (Zhejiang Geely Holding Group) ..................................................................................................... 151

6.77 Gemalto .................................................................................................................................................... 152

6.78 GM (General Motors Company) ............................................................................................................... 153

6.79 Google ...................................................................................................................................................... 154

6.80 H&D Wireless ........................................................................................................................................... 155

6.81 Harman International Industries .............................................................................................................. 156

6.82 Hawtai Motor Group ................................................................................................................................ 157

6.83 HERE ......................................................................................................................................................... 158

6.84 Hitachi ...................................................................................................................................................... 159

6.85 Honda Motor Company............................................................................................................................ 160

6.86 HTC Corporation ....................................................................................................................................... 161

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 9

6.87 Huawei ..................................................................................................................................................... 162

6.88 Hyundai Motor Company ......................................................................................................................... 163

6.89 iBiquity Digital Corporation ...................................................................................................................... 164

6.90 IBM ........................................................................................................................................................... 165

6.91 iHeartMedia ............................................................................................................................................. 166

6.92 Infineon Technologies .............................................................................................................................. 167

6.93 Infiniti ....................................................................................................................................................... 168

6.94 Ingenie ...................................................................................................................................................... 169

6.95 INRIX ......................................................................................................................................................... 170

6.96 INSYS Microelectronics ............................................................................................................................ 171

6.97 Intel Corporation ...................................................................................................................................... 172

6.98 Inthinc Technology Solutions ................................................................................................................... 173

6.99 Inventek Systems ..................................................................................................................................... 174

6.100 ip-label ................................................................................................................................................. 175

6.101 iWOW Connections .............................................................................................................................. 176

6.102 Ixonos ................................................................................................................................................... 177

6.103 Jaguar Land Rover Automotive ............................................................................................................ 178

6.104 Jasper Technologies ............................................................................................................................. 179

6.105 Johnson Controls ................................................................................................................................. 180

6.106 Kapsch TrafficCom ............................................................................................................................... 181

6.107 KDDI Corporation ................................................................................................................................. 182

6.108 Kia Motors Corporation ....................................................................................................................... 183

6.109 KORE Wireless Group ........................................................................................................................... 184

6.110 KPN ...................................................................................................................................................... 185

6.111 KT Corporation ..................................................................................................................................... 186

6.112 Laird ..................................................................................................................................................... 187

6.113 Lantronix .............................................................................................................................................. 188

6.114 Lesswire ............................................................................................................................................... 189

6.115 Lexus .................................................................................................................................................... 190

6.116 LG Electronics....................................................................................................................................... 191

6.117 LG Uplus ............................................................................................................................................... 192

6.118 Lincoln Motor Company ...................................................................................................................... 193

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 10

6.119 LS Research .......................................................................................................................................... 194

6.120 Magneti Marelli ................................................................................................................................... 195

6.121 Mahindra and Mahindra ...................................................................................................................... 196

6.122 Mazda Motor Corporation ................................................................................................................... 197

6.123 Mercedes Benz .................................................................................................................................... 198

6.124 MIC (MiTAC International Corporation) .............................................................................................. 199

6.125 Michelin ............................................................................................................................................... 200

6.126 Microchip Technology.......................................................................................................................... 201

6.127 Microsoft Corporation ......................................................................................................................... 202

6.128 Microtronics ......................................................................................................................................... 203

6.129 Minacs .................................................................................................................................................. 204

6.130 Mitsubishi Electric Corporation ........................................................................................................... 205

6.131 Mitsubishi Motors Corporation ........................................................................................................... 206

6.132 Modacom ............................................................................................................................................. 207

6.133 Mojio .................................................................................................................................................... 208

6.134 Multi-Tech Systems.............................................................................................................................. 209

6.135 Murata Manufacturing ........................................................................................................................ 210

6.136 Navman Wireless & Teletrac ............................................................................................................... 211

6.137 NEC Corporation .................................................................................................................................. 212

6.138 Neoway ................................................................................................................................................ 213

6.139 Nissan Motor Company ....................................................................................................................... 214

6.140 NNG...................................................................................................................................................... 215

6.141 Nokia .................................................................................................................................................... 216

6.142 Novatel Wireless .................................................................................................................................. 217

6.143 Novero ................................................................................................................................................. 218

6.144 NTT DoCoMo ........................................................................................................................................ 219

6.145 Nuance Communications ..................................................................................................................... 220

6.146 Nvidia Corporation ............................................................................................................................... 221

6.147 NXP Semiconductors ............................................................................................................................ 222

6.148 Octo Telematics ................................................................................................................................... 223

6.149 ON Semiconductor ............................................................................................................................... 224

6.150 OpenCar ............................................................................................................................................... 225

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 11

6.151 Openmatics .......................................................................................................................................... 226

6.152 Option N.V. .......................................................................................................................................... 227

6.153 Oracle ................................................................................................................................................... 228

6.154 Orange ................................................................................................................................................. 229

6.155 Panasonic Corporation......................................................................................................................... 230

6.156 Pandora Media .................................................................................................................................... 231

6.157 Parrot ................................................................................................................................................... 232

6.158 Pateo Corporation ............................................................................................................................... 233

6.159 Pioneer Corporation ............................................................................................................................ 234

6.160 Powermat Technologies ...................................................................................................................... 235

6.161 PSA Peugeot Citroen ............................................................................................................................ 236

6.162 QiMing Information Technology .......................................................................................................... 237

6.163 Qoros Automotive ............................................................................................................................... 238

6.164 Quake Global ....................................................................................................................................... 239

6.165 Qualcomm ........................................................................................................................................... 240

6.166 Quectel................................................................................................................................................. 241

6.167 RealVNC ............................................................................................................................................... 242

6.168 Redpine Signals .................................................................................................................................... 243

6.169 Renault (Groupe Renault) .................................................................................................................... 244

6.170 Renesas Electronics Corporation ......................................................................................................... 245

6.171 Rogers Communications ...................................................................................................................... 246

6.172 ROHM Semiconductor ......................................................................................................................... 247

6.173 RSA Insurance Group ........................................................................................................................... 248

6.174 RTX A/S ................................................................................................................................................ 249

6.175 SAIC Motor Corporation ...................................................................................................................... 250

6.176 Samsung Electronics ............................................................................................................................ 251

6.177 SAP ....................................................................................................................................................... 252

6.178 Savari ................................................................................................................................................... 253

6.179 SEAT ..................................................................................................................................................... 254

6.180 Seeing Machines .................................................................................................................................. 255

6.181 Sierra Wireless ..................................................................................................................................... 256

6.182 Silicon Laboratories .............................................................................................................................. 257

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 12

6.183 SIMCom Wireless Solutions ................................................................................................................. 258

6.184 SiriusXM Radio ..................................................................................................................................... 259

6.185 SK Telecom ........................................................................................................................................... 260

6.186 Skoda Auto ........................................................................................................................................... 261

6.187 SkyWave Mobile Communications ...................................................................................................... 262

6.188 SoftBank Mobile Corporation .............................................................................................................. 263

6.189 Sony Corporation ................................................................................................................................. 264

6.190 Spirent Communications ..................................................................................................................... 265

6.191 Sprint Corporation ............................................................................................................................... 266

6.192 STMicroelectronics .............................................................................................................................. 267

6.193 Subaru .................................................................................................................................................. 268

6.194 Summit Tech ........................................................................................................................................ 269

6.195 Suzuki Motor Corporation ................................................................................................................... 270

6.196 Synchronoss Technologies ................................................................................................................... 271

6.197 Tata Motors ......................................................................................................................................... 272

6.198 TCS (TeleCommunication Systems) ..................................................................................................... 273

6.199 Tech Mahindra ..................................................................................................................................... 274

6.200 Telecom Italia ....................................................................................................................................... 275

6.201 Telefónica ............................................................................................................................................ 276

6.202 Telenav ................................................................................................................................................. 277

6.203 Telenor Group ...................................................................................................................................... 278

6.204 Telit Communications .......................................................................................................................... 279

6.205 Telogis .................................................................................................................................................. 280

6.206 Telstra Corporation .............................................................................................................................. 281

6.207 Tesla Motors ........................................................................................................................................ 282

6.208 TI (Texas Instruments) ......................................................................................................................... 283

6.209 TimaNetworks ...................................................................................................................................... 284

6.210 Tobii Technology .................................................................................................................................. 285

6.211 TomTom ............................................................................................................................................... 286

6.212 Toshiba Corporation ............................................................................................................................ 287

6.213 Toyota Motor Corporation .................................................................................................................. 288

6.214 Uber ..................................................................................................................................................... 289

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 13

6.215 U-blox ................................................................................................................................................... 290

6.216 Ubridge ................................................................................................................................................ 291

6.217 UIEvolution .......................................................................................................................................... 292

6.218 Vehcon ................................................................................................................................................. 293

6.219 Veniam ................................................................................................................................................. 294

6.220 Verizon Communications ..................................................................................................................... 295

6.221 Vinli ...................................................................................................................................................... 296

6.222 Visteon Corporation ............................................................................................................................. 297

6.223 Vodafone Group .................................................................................................................................. 298

6.224 Voicebox Technologies ........................................................................................................................ 299

6.225 Volkswagen .......................................................................................................................................... 300

6.226 Volvo .................................................................................................................................................... 301

6.227 Wireless Logic ...................................................................................................................................... 302

6.228 WirelessCar .......................................................................................................................................... 303

6.229 Xilinx..................................................................................................................................................... 304

6.230 ZTE ....................................................................................................................................................... 305

6.231 Zubie .................................................................................................................................................... 306

7 Chapter 7: Market Analysis & Forecasts ......................................................... 307

7.1 Global Outlook of Connected Cars .............................................................................................................. 307

7.2 Segmentation by Connectivity Model ......................................................................................................... 308

7.3 Embedded Car Connections ........................................................................................................................ 309

7.3.1 GSM ................................................................................................................................................. 311

7.3.2 CDMA-2000 ..................................................................................................................................... 311

7.3.3 W-CDMA .......................................................................................................................................... 312

7.3.4 TD-SCDMA ....................................................................................................................................... 312

7.3.5 LTE ................................................................................................................................................... 313

7.3.6 Satellite & Other Technologies ........................................................................................................ 313

7.4 Tethered Car Connections ........................................................................................................................... 314

7.4.1 Wireless ........................................................................................................................................... 315

7.4.2 Wireline ........................................................................................................................................... 316

7.5 Integrated Car Connections......................................................................................................................... 316

7.5.1 Apple CarPlay .................................................................................................................................. 318

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 14

7.5.2 Android Auto ................................................................................................................................... 318

7.5.3 MirrorLink ........................................................................................................................................ 319

7.5.4 Others .............................................................................................................................................. 319

7.6 Segmentation by Application Category ....................................................................................................... 320

7.6.1 Communications & Infotainment .................................................................................................... 320

7.6.2 Navigation & Location Services ....................................................................................................... 321

7.6.3 Vehicle Management ...................................................................................................................... 321

7.6.4 Safety & Security ............................................................................................................................. 322

7.6.5 Driver Assistance & Autonomous Driving ....................................................................................... 322

7.7 Segmentation by Region ............................................................................................................................. 323

7.7.1 Asia Pacific ....................................................................................................................................... 324

7.7.2 Europe ............................................................................................................................................. 325

7.7.3 Middle East & Africa ........................................................................................................................ 326

7.7.4 Latin & Central America .................................................................................................................. 327

7.7.5 North America ................................................................................................................................. 328

7.8 Top Country Markets................................................................................................................................... 329

7.8.1 Brazil ................................................................................................................................................ 329

7.8.2 Canada ............................................................................................................................................. 330

7.8.3 China ................................................................................................................................................ 331

7.8.4 Egypt ................................................................................................................................................ 332

7.8.5 France .............................................................................................................................................. 333

7.8.6 Germany .......................................................................................................................................... 334

7.8.7 India ................................................................................................................................................. 335

7.8.8 Indonesia ......................................................................................................................................... 336

7.8.9 Italy .................................................................................................................................................. 337

7.8.10 Japan................................................................................................................................................ 338

7.8.11 Mexico ............................................................................................................................................. 339

7.8.12 Russia ............................................................................................................................................... 340

7.8.13 Saudi Arabia ..................................................................................................................................... 341

7.8.14 South Africa ..................................................................................................................................... 342

7.8.15 South Korea ..................................................................................................................................... 343

7.8.16 UK .................................................................................................................................................... 344

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 15

7.8.17 USA .................................................................................................................................................. 345

8 Chapter 8: Conclusion & Strategic Recommendations .................................... 346

8.1 Why is the Market Poised to Grow? ........................................................................................................... 346

8.2 Competitive Industry Landscape: Acquisitions, Alliances & Consolidation ................................................. 346

8.3 Geographic Outlook: Which Countries Offer the Highest Growth Potential? ............................................. 347

8.4 The Role of Mobile Operators ..................................................................................................................... 348

8.4.1 Capitalizing on Connectivity ............................................................................................................ 348

8.4.2 Innovating Beyond Connectivity: AT&T’s Drive Platform ................................................................ 348

8.5 Connected Car Platforms: Moving Towards Cloud Centric Offerings ......................................................... 349

8.5.1 Consolidating Disparate Functions .................................................................................................. 349

8.5.2 Cloud Based Platforms .................................................................................................................... 349

8.6 Addressing Privacy Concerns: The Stance of Automotive OEMs ................................................................ 350

8.7 Impact of Government Initiatives ............................................................................................................... 350

8.8 Smartphone Integration .............................................................................................................................. 351

8.8.1 What Key Offerings Are Available? ................................................................................................. 351

8.8.2 OEMs Are Keen to Offer Multiple Solutions .................................................................................... 351

8.9 Monetizing the Connected Car Opportunity: The Changing Role of Automotive OEMs ............................ 352

8.9.1 Evolving Business Models ................................................................................................................ 352

8.9.2 Entering Other Connected Markets ................................................................................................ 352

8.10 Integration with Smart Cities ................................................................................................................... 353

8.11 V2X Networks: Do LTE & 5G Technologies Pose a Threat to 802.11p? .................................................... 354

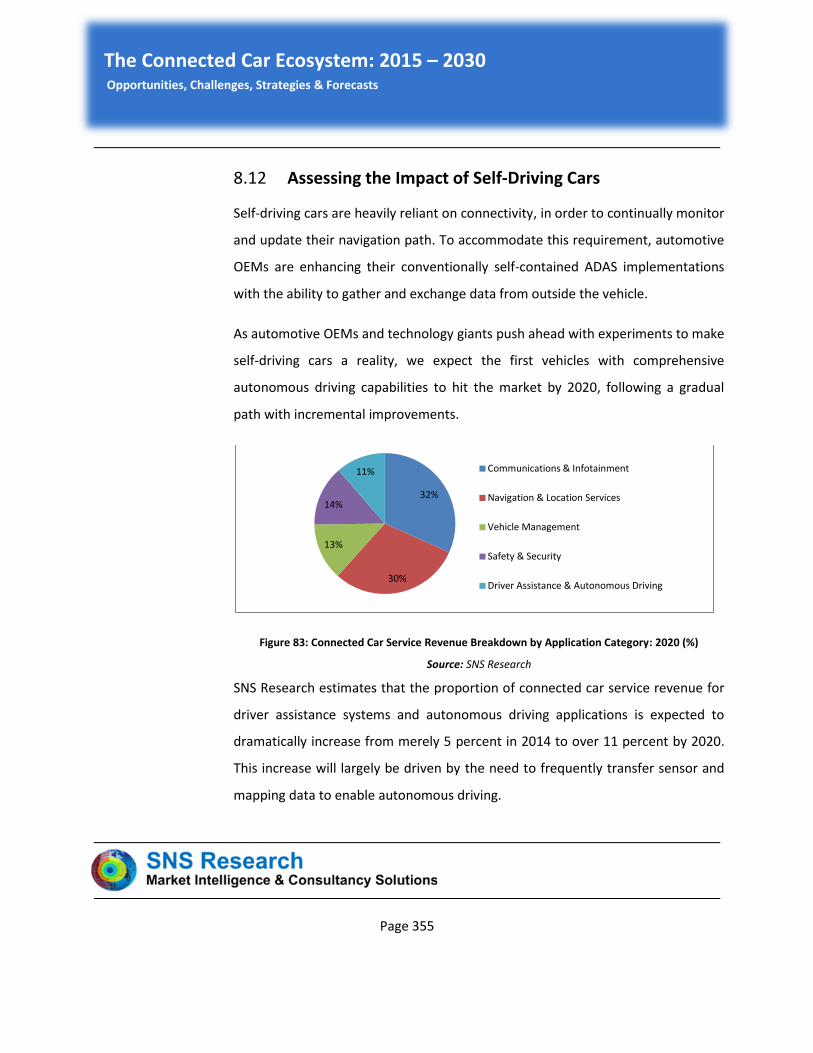

8.12 Assessing the Impact of Self-Driving Cars ................................................................................................ 355

8.13 Strategic Recommendations .................................................................................................................... 356

8.13.1 Automotive OEMs ........................................................................................................................... 356

8.13.2 Telematics & Connected Car Platform Specialists ........................................................................... 356

8.13.3 Mobile Operators ............................................................................................................................ 357

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 16

List of Figures

Figure 1: Key Connected Car Applications ............................................................................................................................................................... 31

Figure 2: Comparison of Key OEM Connected Car Programs (Q3’2015).................................................................................................................. 33

Figure 3: Global Big Data & Analytics Technology Investments in the Automotive Sector: 2015 - 2030 ($ Billion) ................................................. 40

Figure 4: Connected Car Industry Roadmap ............................................................................................................................................................ 68

Figure 5: Connected Car Value Chain ...................................................................................................................................................................... 70

Figure 6: Global Connected Car Installed Base: 2015 - 2030 (Millions) ................................................................................................................. 307

Figure 7: Global Connected Car Service Revenue: 2015 - 2030 ($ Billion) ............................................................................................................. 308

Figure 8: Global Connected Car Installed Base by Connectivity Model: 2015 - 2030 (Millions) ............................................................................. 308

Figure 9: Global Connected Car Service Revenue by Connectivity Model: 2015 - 2030 ($ Billion) ........................................................................ 309

Figure 10: Global Embedded Car Connections: 2015 - 2030 (Millions) .................................................................................................................. 309

Figure 11: Global Embedded Car Connection Service Revenue: 2015 - 2030 ($ Billion) ........................................................................................ 310

Figure 12: Global Embedded Car Connections by Technology: 2015 - 2030 (Millions) .......................................................................................... 310

Figure 13: Global GSM Embedded Car Connections: 2015 - 2030 (Millions) ......................................................................................................... 311

Figure 14: Global CDMA-2000 Embedded Car Connections: 2015 - 2030 (Millions) ............................................................................................. 311

Figure 15: Global W-CDMA Embedded Car Connections: 2015 - 2030 (Millions) .................................................................................................. 312

Figure 16: Global TD-SCDMA Embedded Car Connections: 2015 - 2030 (Millions) ............................................................................................... 312

Figure 17: Global LTE Embedded Car Connections: 2015 - 2030 (Millions) ........................................................................................................... 313

Figure 18: Global Satellite & Other Embedded Car Connections: 2015 - 2030 (Millions) ...................................................................................... 313

Figure 19: Global Tethered Car Connections: 2015 - 2030 (Millions) .................................................................................................................... 314

Figure 20: Global Tethered Car Connection Service Revenue: 2015 - 2030 ($ Billion)........................................................................................... 314

Figure 21: Global Tethered Car Connections by Technology: 2015 - 2030 (Millions) ............................................................................................ 315

Figure 22: Global Wireless Tethered Car Connections: 2015 - 2030 (Millions) ...................................................................................................... 315

Figure 23: Global Wireline Tethered Car Connections: 2015 - 2030 (Millions) ...................................................................................................... 316

Figure 24: Global Integrated Car Connections: 2015 - 2030 (Millions) .................................................................................................................. 316

Figure 25: Global Integrated Car Connection Revenue: 2015 - 2030 ($ Billion) ..................................................................................................... 317

Figure 26: Global Integrated Car Connections by Technology: 2015 - 2030 (Millions) .......................................................................................... 317

Figure 27: Global Apple CarPlay Connections: 2015 - 2030 (Millions) ................................................................................................................... 318

Figure 28: Global Android Auto Connections: 2015 - 2030 (Millions) .................................................................................................................... 318

Figure 29: Global MirrorLink Connections: 2015 - 2030 (Millions) ........................................................................................................................ 319

Figure 30: Global Other Integrated Car Connections: 2015 - 2030 (Millions) ........................................................................................................ 319

Figure 31: Global Connected Car Service Revenue by Application Category: 2015 - 2030 ($ Billion) .................................................................... 320

Figure 32: Global Connected Car Service Revenue for Communications & Infotainment: 2015 - 2030 ($ Billion) ................................................ 320

Figure 33: Global Connected Car Service Revenue for Navigation & Location Services: 2015 - 2030 ($ Billion) .................................................... 321

Figure 34: Global Connected Car Service Revenue for Vehicle Management: 2015 - 2030 ($ Billion) ................................................................... 321

Figure 35: Global Connected Car Service Revenue for Safety & Security: 2015 - 2030 ($ Billion) ......................................................................... 322

Figure 36: Global Connected Car Service Revenue for Driver Assistance & Autonomous Driving: 2015 - 2030 ($ Billion) .................................... 322

Figure 37: Connected Car Installed Base by Region: 2015 - 2030 (Millions) .......................................................................................................... 323

Figure 38: Connected Car Service Revenue by Region: 2015 - 2030 ($ Billion) ...................................................................................................... 323

Figure 39: Asia Pacific Connected Car Installed Base: 2015 - 2030 (Millions) ........................................................................................................ 324

Figure 40: Asia Pacific Connected Car Service Revenue: 2015 - 2030 ($ Billion) .................................................................................................... 324

The Connected Car Ecosystem: 2015 – 2030 Opportunities, Challenges, Strategies & Forecasts

..

Page 17