the bas agent - icb.org.au

TRANSCRIPT

The Institute of Certified Bookkeepers

Phone: 1300 85 61 81 email: [email protected] web: www.icb.org.au

THE BAS AGENT

August 2012

ICB Definitive Guide

Volume 2: Applying the Code of Conduct

Not all bookkeepers are BAS Agents!

Not all BAS agents do Bookkeeping!This guide has been updated following each relevant development of the law and systems to do with BAS Agents.

This 4th Edition replaces and updates:The Definitive Guide Volume 1 - NEW BAS Agent registration 16 March, 2009The Definitive Guide Volume 2 -The new BAS Agent Regime 3 August, 2009 The Definitive Guide Volume 3 - The BAS Agent August 2011

The law and guidance from the TPB continues to change, keep track at: www.ICB.org.au/BAS_Agent Subscribe to the ICB Newsletter

The Institute of Certified Bookkeepers is a:• Member based• Not-for-profit• Professional Association of Bookkeepers for Bookkeepers

The vision of ICB is to provide Bookkeepers with the co-operative forum to be the best they can be.

We are about bookkeepers: Recognition, Education & Resources

Bookkeepers helping Bookkeepers help Business

August 2012 Not to be duplicated or re-distributed in part or in full without written permission from ICB

The Institute of Certified BookkeepersLevel 27Rialto South Tower525 Collins StreetMelbourne 3000 Tel: 1300 85 61 81Fax: 1300 85 73 93

ContentsIt’s law: now what? 5

Explanation and Clarification 6 What is a BAS Service? 6 What is a BAS Agent allowed to do? 7

Explanation of Acceptable Business Structures In light of the TASA2009 8 ICB Guidance Note - Applying the Code of Conduct 9

Section A – Are you signing a statement or declaration? 10Section B – You are signing a declaration or statement 11Section C: Did you take “reasonable steps to ensure the accuracy of the entire document”? 12Section D – You are providing a BAS Service, which may include signing a statement. 13What extent of checking? 13Schedule: Checklist Agree on the extent of checking 14Section E – Adhering to acceptable conduct 15Section F – false or misleading statement 17

Legislative Extracts 22Meaning of BAS service (Sn. 90-10) 22The Code of Professional Conduct (Sn. 30-10) 22

Honesty and integrity 22Independence 22Competence 21Other responsibilities 22Making false or misleading statements 23Signing of declarations etc. 23

Understanding the TASA 2009 code of conduct (ICB comment) 24

Reasonable Care 26Whether you are a BAS Agent or not 26Inheriting Messy files 26The ‘interesting’ accountant 27The ‘interesting’ client 27The ATO 27

ICB Checklist 30Applying the code to a specific client 30Section A – Are you signing a statement or declaration? 31Section B – Who prepared the statement? 31Section C: Did you take “reasonable steps to ensure the accuracy of the entire document”? 31Section D – What extent of checking? 32Section E – Applying the code (in addition to that implied above) 32Section F – false or misleading Statement 33

Review of Bookkeepers ability to service a client in accordance with Professional Standards and Code of Conduct 35

Contents (cont.)

Authority for BAS Agent to act on behalf of the Taxpayer in respect to the taxpayers dealings with the Australian Taxation Office 37

Authority to Lodge Electronically 38

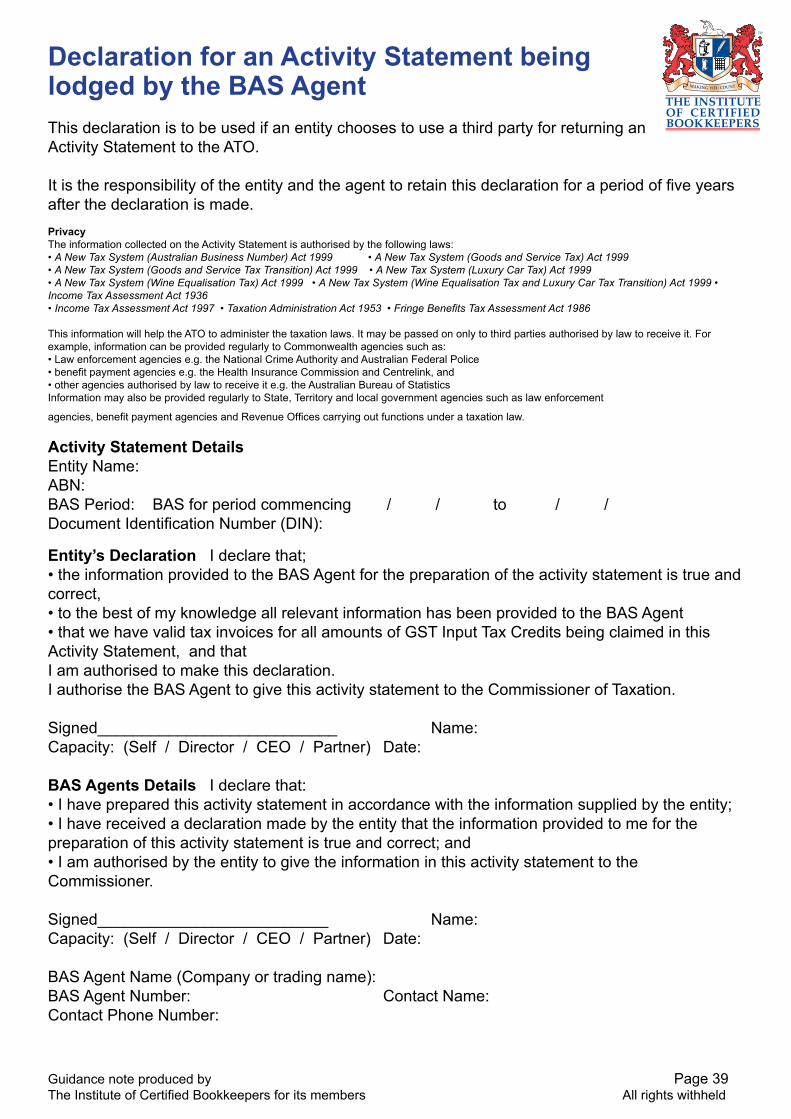

Declaration for an Activity Statement being lodged by the BAS Agent 39

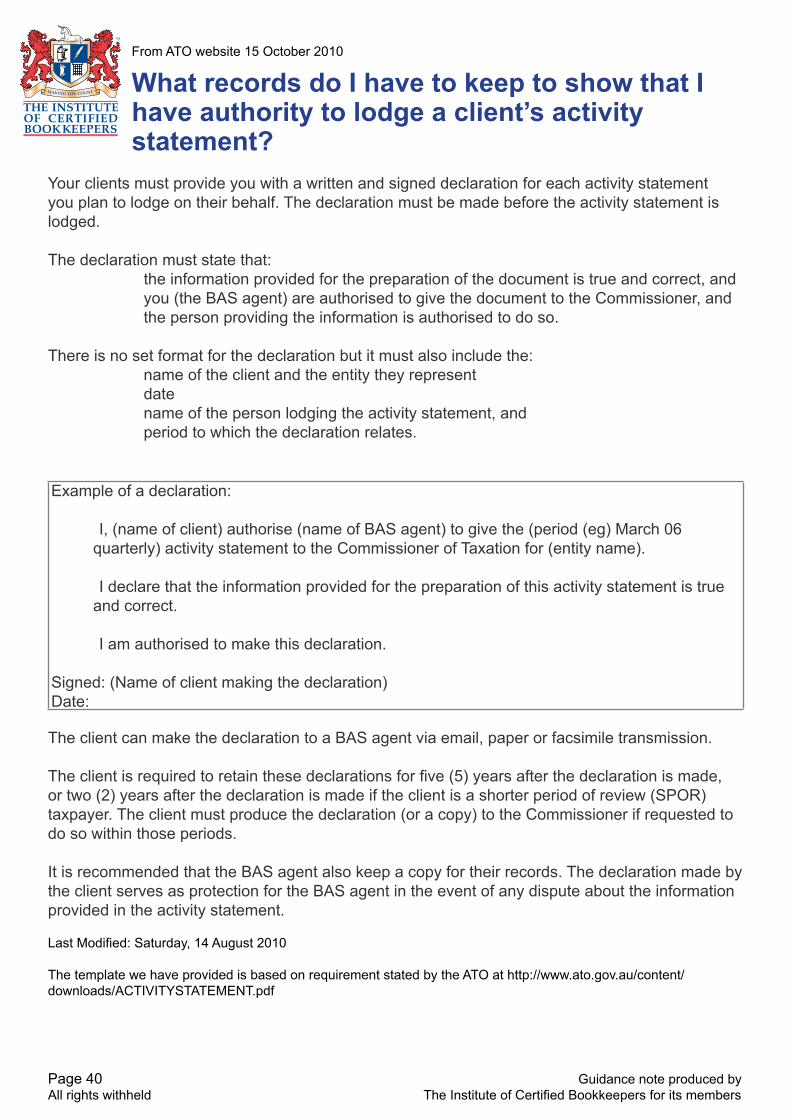

What records do I keep to show that I have authority to lodge a client’s activity statement? 40 Authority to Lodge Payment Summary (EMPDUPE) Electronically 41

Payment Summary (EMPDUPE) Details 42What records do I have to keep to show that I have authority to lodge on a client’s behalf? 43

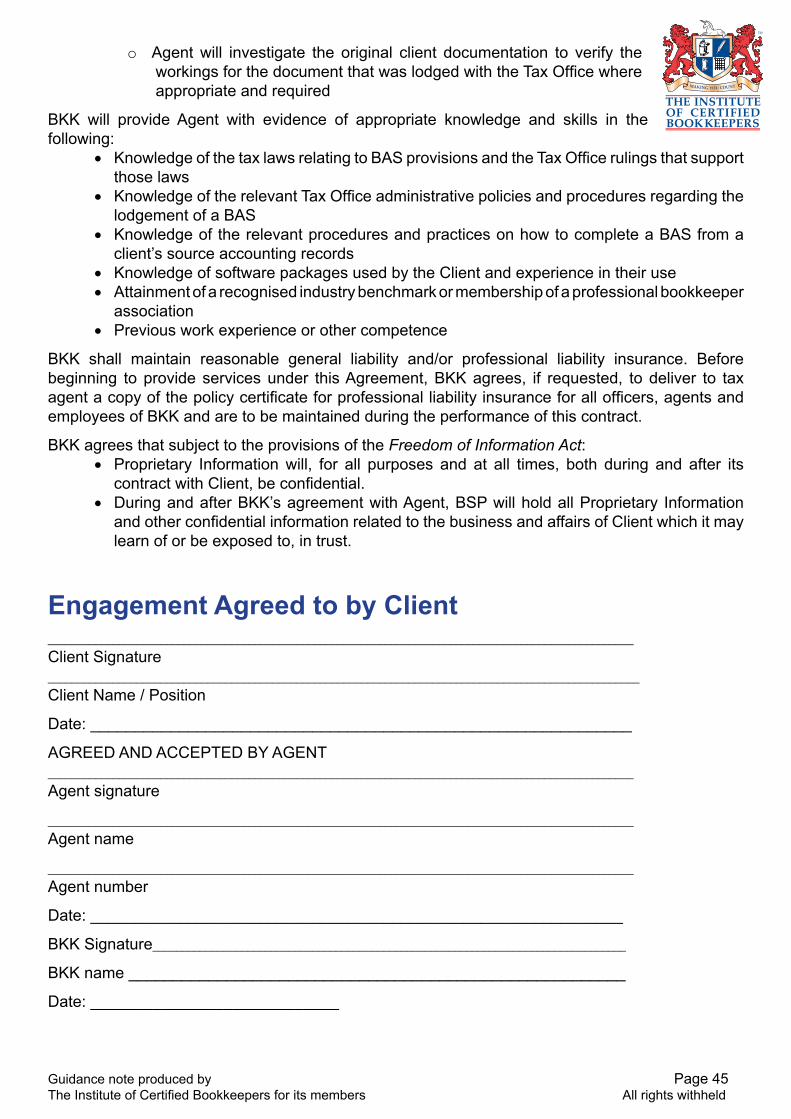

External Agent Engagement Agreement 45

Engagement Agreed to by Client 47

Contractual Agreement 48

Additional Requirements from the TPB 50

Benefits of ICB Membership 51

Guidance note produced by Page 5 The Institute of Certified Bookkeepers for its members All rights withheld

It’s law: now what?

Only registered “BAS Agents” may provide “BAS Services” for a fee or reward.

“For a fee” means the law does not apply to employees of the business whose BAS is being

considered or the business owners themselves. This law only applies to contract bookkeepers etc.

Therefore people or entities providing service to clients that fall within the definition of a BAS

Service must have registered BAS Agents working with them.

An Individual must either be, or be supervised by, a registered BAS Agent (or tax agent).

Entities must have a sufficient number of BAS Agents involved in its supervision, systems and

review.

Employees of an entity who provide BAS Services to clients where that entity/business is providing

the BAS Services to the client must either be BAS Agents themselves or supervised by BAS

Agents.

Page 6 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

Sn. 90-10 Meaning of BAS service

(1) A BAS service is a *tax agent service: (a) that relates to:

(i) ascertaining the liabilities, obligations or entitlements of an entity that arise, or could arise, under a *BAS provision; or (ii) advising an entity about the liabilities, obligations or entitlements of the entity or another entity that arise, or could arise, under a BAS provision; or(iii) representing an entity in their dealings with the Commissioner in relation to a BAS provision;

and (b) that is provided in circumstances where the entity can reasonably be expected to rely on the service for either or both of the following purposes:

(i) to satisfy liabilities or obligations that arise, or could arise, under a BAS provision; (ii) to claim entitlements that arise, or could arise, under a BAS provision.. (2) A service specified in the regulations for the purposes of this subsection is not a BAS service.

BAS Provisions can be understood to be completion of the payable amount boxes on the BAS. • GST amount collected or paid • FBT Instalment amount or credit claim

• WET payable or refundable amounts • Luxury Car Tax amounts• Fuel Tax Credit amounts • PAYG Withholding amount payable • PAYG Instalments amount payable

Explanation and Clarification

Classroom or onsite training• general training on the use of software is NOT a BAS Service• general training around how GST works or is reported in the software is NOT a BAS service

Install and configure software

• general software / bookkeeping / accounting configuration – No• specifically determining what GST codes apply when – Yes• advising on legal compliance of the business tax invoice – Yes• configuring how a BAS like report is to be produced – Yes• implementing a default GST code list provided by a registered Agent to the business – No

If the client is relying on this install and configuration service to help that client ascertain their future GST/BAS obligations then it is a BAS Service.

Bookkeeping• following instructions – No• transfer data onto a computer program - No• enter data – No• code transactions (based on instructions) – No• process payments – No• prepare bank reconciliations - No

What is a BAS Service?

Guidance note produced by Page 7 The Institute of Certified Bookkeepers for its members All rights withheld

Advanced Bookkeeping• If the client is relying on another registered BAS/Tax agent – Nootherwise• preparing an approved form – Yes• lodging an approved form – Yes• giving advice about a BAS provision – Yes• “transacting” with the ATO on behalf of a client – Yes• Anything and everything where work is reviewed by another registered BAS agent – No• Reconciling facets of the accounting records for a period – No• Providing generic reports – No• Preparing a report that is used to prepare the BAS – Yes

What is a BAS Agent allowed to do? A BAS Agent is issued a licence that says they can:

Advise a client, provide certainty to a client or represent that client to the tax office in relation to:• All GST matters• Wine Tax, Fuel Tax, Luxury Car Tax matters• Payment of FBT • All aspects of Payroll that relate to the withholding of tax amounts and the reporting of that

amount to the employee and the Tax office• All aspects of other PAYG Withholding amounts: ie no ABN, Interest & Dividend• All aspects of the payment of income tax via PAYG Instalments

A Tax Agent can also do these and then other areas of tax also.

What does this mean?

A registered Agent may:• Design and set up compliance systems• Advise the client on how the above areas of law affect them• Review a client’s operations in relation to these areas of law and provide certainty to that

client that they are getting it right.

These tasks cannot be done by a bookkeeper who is not a registered Agent.

So, what can a Bookkeeper do who is not a BAS Agent?• They can follow systems designed by others• They can process• They can reconcile and produce results but not if the client is relying on those, without

further action to be certain that they are meeting their obligations• They should raise questions and not answer them

A BAS Agent can be a business with one or more qualified persons (registered BAS Agent/s) and others working, performing BAS Services, being supervised and controlled by the qualified person.

This is legal!

Page 8 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

Explanation of Acceptable Business Structures In light of the TASA2009

AN INDIVIDUAL May only provide BAS Services to a client if:

a. they are an employee/owner/director of the entity for whom they are providing the service

orb. they are registered in their own right as a Registered Agent with the TPB.

or

c. they are engaged by a person who is a Registered Agent to provide services to that persons clients, where that person has supervision and control over the individual

or

d. they are engaged by an entity (through contract or employment) where that entity has another Registered Individual who is providing the satisfactory supervisory services of all work performed by/for the entity

A PARTNERSHIP May only provide BAS Services to a client if:

a. they have engaged another registered entity or person to provide the satisfactory supervision of all BAS Service work performed by the partnership

A COMPANY (including a trust) May only provide BAS Services to a client if:

a. they have engaged another registered entity or person to provide the satisfactory supervision of all BAS Service work performed by the company.

A NON REGISTERED INDIVIDUAL/ENTITY provides BAS SERVICES by contracting another agent to supervise. Many bookkeepers will seek to continue to provide bookkeeping services and assist in provision of BAS Services to their clients.

They may only assist in the provision of the BAS Service to their clients IF the client has also engaged a Registered Agent to ultimately provide the BAS Service, thereby taking supervision of the work performed by the bookkeeper.

The bookkeeper will not perform the BAS Services other than as directed by the agent whom is being relied on by the client.

The nature of this tri-party agreement is that the client is relying on the agent and not the bookkeeper for the provision of the BAS Services. The agent may be utilising the bookkeeper to perform some of the work but under the agents supervision and responsibility.

Resources available for to support this article (go to www.icb.org.au/ICB_Resources/BAS_Agent_Information):

Engaging an External Agent (page 43) Client Engagement Letter (page 45) Contractor Agreement (page 46)

Guidance note produced by Page 9 The Institute of Certified Bookkeepers for its members All rights withheld

What process should the BAS Agent follow to ensure compliance with the code of conduct and the civil penalty provisions?

ICB Guidance Note

(P10)

(P12)

(P15)

(P13)(P11)

(P19)

Page 10 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

What process should the BAS Agent follow to ensure compliance withthe code of conduct & the civil penalty provisions?

A detailed checklist of processes and thoughts to determine how you are permitted to engage with a client: (Summary checklist provided on page 31)

Maybe a BAS Agent is engaged to do the final work on lodging a BAS but is asked/told to rely on a report provided to them by internal staff (for at least part of the BAS related information).

Section A – Are you signing a statement or declaration?

A1 Are you signing a declaration or statement in relation to the taxpayer?

• “Signing a Declartion or Statement” applies in the context of a BAS Agent when that agent is elctronically lodging through the ATO Portal or other mechanism, expecially if using your AUSkey (Electronic Signature)

• If an agent was to be physically signing a form on behals/as an authorised contact etc. of a client (not recommended by ICB) this would definately be included.

• If you are providing tax forms to the client for signing, after signing to them that the forms are correct then this set of requirements may apply but in any case the requirements of the code in Section D would apply.

A2 Is the statement required or permitted by a BAS Provision?

BAS Provisions• Collection & Payment of FBT• GST tax law• Wine tax law• Luxury Car tax law• Fuel tax law• PAYG withholding & instalment

If no to either question then move to Section D (extent of the work).

If yes to both then Section B (signing a statement) first

(P13)

Guidance note produced by Page 11 The Institute of Certified Bookkeepers for its members All rights withheld

SECTION B – You are signing a declaration or statement in relation to the taxpayer required by a BAS Provision.

B1: Did you prepare the statement?

If the answer to B1 is YES then you are permitted to sign subject to the section below Section E (adhering to acceptable conduct)

Or

B2: Did another Tax Agent or BAS Agent prepare the statement?

If the answer to B2 is YES then you are permitted to sign as you are able to assume that agent also complies with their legal obligations under the TASA2009. Therefore prove that the work was provided by that other agent. (Template letter for obtaining work from another agent available at www.icb.org.au)

Or

B3: Did another person who is working under the supervision and control of yourself (or another agent) prepare the statement?

If the person worked for another agent then it is likely you can just refer to B2 above, however it may be wise to still apply these supervision and control tests.

Supervision and Control: Are you satisfied that it has been prepared following the steps you require and to the standard you require, the way you require?Have you actually checked?

Supervision & Control Did you supervise the process followed? &Did you review the work performed? &

Do you have documents, procedure notes &/or checklists that were followed to prove the review and the supervision?Therefore…..Has the statement been prepared as if you had done it? (If your answer to all these supervision & control questions is yes then the answer to B3 is YES)

If the answer to B3 is YES then move to Section E (adhering to acceptable conduct).

If the answer to all of B1, B2 & B3 is No then you may still be able to sign it if you can demonstrate you took reasonable steps (Section C)

Yes , I am signing a statement

Page 12 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

Section C - Did you take “reasonable steps to ensure the accuracy of the entire document”?

(this applies when you are signing a statement that did not comply with Section B)

Reasonable Steps: The taking of reasonable steps could be deomanstrated by evidence that the agent reviewed the document before signing it or by evidence of appropriate alternative review or monitoring arrangments (Explanatory Memorandum).

You may still be able to sign the statement if you can demonstrate you took reasonable steps to review the statement:Are you satisfied the preparer understands the requirements of how to comply?Are you satisfied that the preparer complied with legal requirements?Have you checked any area of the BAS where there is a risk of a material mistake? What steps do you need to take to satisfy yourself to a reasonable extent that the statement is

correct? Did you review the process that was followed? &Did you review the work performed? &Do you have documents, procedure notes &/or checklists that were followed to prove the re-

view and any alterations required?

What extent of work does the client require you to take? (Section D)If the client limits your scope of work such that you cannot take “reasonable steps” to verity that accuracy of the statement then you cannot sign the statement however you may be able to advise the client on the aspects of the statement (Section D)

If the answer is YES you did take reasonable steps then move to Section E (adhering to acceptable conduct)

If the answer is No then eitheri. Do not sign the declaration or statement, &ii. Advise the client to the extent that you are able to advise refer section D.

or

iii. Do what is necessary to “take Reasonable Steps to ensure the accuracy of the document”

If B1, B2 & B3 = NO!-> then take reasonable steps

Guidance note produced by Page 13 The Institute of Certified Bookkeepers for its members All rights withheld

SECTION D – You are providing a BAS Service, which may include signing a statement.What extent of checking?

Am I being provided with information that I am to rely on, as being correct? No because I have to make sure it is correct, or No because I am doing the work, or Yes because the client has said I am to rely on that information.In all cases the requirements of the code must be applied which includes providing information as follows.

Advise the preparer/business of their compliance obligations and ensure that they have an understanding of the law and each of the requirements to comply with that law to the extent required?

Yes/No ProvidedAreas: Tax invoice obligations on all purchases ☐ ☐ Taxable purpose for all claims for Input Tax Credits ☐ ☐ Charging GST on all taxable supplies ☐ ☐ PAYG Withholding obligations ☐ ☐ PAYG Instalment ☐ ☐ Application of WET / FTC / LCT ☐ ☐

What level of checking does the client require me to do? ☐ I do it all:

• Still provide notices of their obligations &• refer to section E

☐ None: • Advise them of each area of their obligations (as above) &• Confirm in writing that you are not engaged to check or confirm their compliance.

Refer template “client doesn’t require checking” &• Refer Section E. 10/10 reliance on the business

☐ Ensure it is correct: 0/10 reliance on the business.• Advise them of each area of their obligations (as above) &• Confirm in writing the level of checking (see below) &• Perform work refer section E

Process required:• Confirm in writing that you are engaged to check or confirm their compliance.• Provide cost estimates upfront and then revise frequently.• Receive further consent from the client at each step or revision of cost or services.Perform

work in accordance with conduct required (Refer section E)

I am providing a BAS Service

Page 14 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

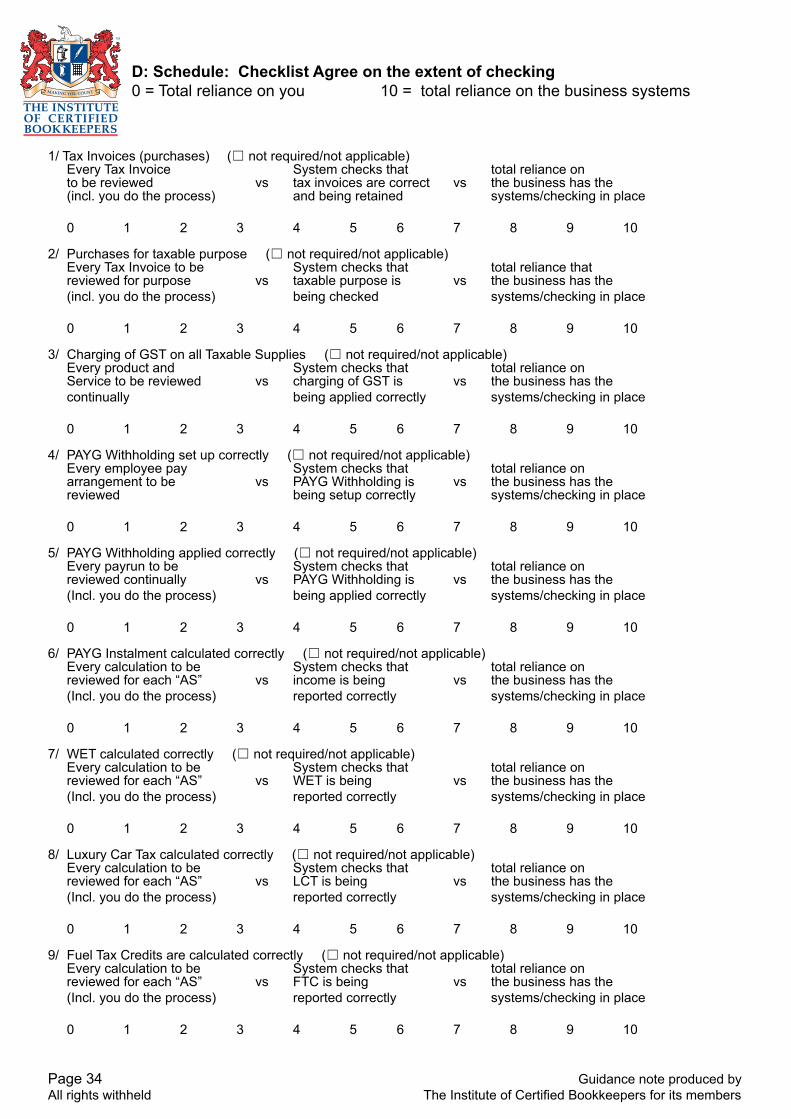

D: Schedule: Checklist to Agree on the extent of checking 0 = Total reliance on you 10 = Total reliance on the business systems

1/ Tax Invoices (purchases) (☐ not required/not applicable) Every Tax Invoice System checks that total reliance on to be reviewed vs tax invoices are correct vs the business has the (incl. you do the process) and being retained systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

2/ Purchases for taxable purpose (☐ not required/not applicable) Every Tax Invoice to be System checks that total reliance that reviewed for purpose vs taxable purpose is vs the business has the (incl. you do the process) being checked systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

3/ Charging of GST on all Taxable Supplies (☐ not required/not applicable) Every product and System checks that total reliance on Service to be reviewed vs charging of GST is vs the business has the continually being applied correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

4/ PAYG Withholding set up correctly (☐ not required/not applicable) Every employee pay System checks that total reliance on arrangement to be vs PAYG Withholding is vs the business has the reviewed being setup correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

5/ PAYG Withholding applied correctly (☐ not required/not applicable) Every payrun to be System checks that total reliance on reviewed continually vs PAYG Withholding is vs the business has the (Incl. you do the process) being applied correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

6/ PAYG Instalment calculated correctly (☐ not required/not applicable) Every calculation to be System checks that total reliance on reviewed for each “AS” vs income is being vs the business has the (Incl. you do the process) reported correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

7/ WET calculated correctly (☐ not required/not applicable) Every calculation to be System checks that total reliance on reviewed for each “AS” vs WET is being vs the business has the (Incl. you do the process) reported correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

8/ Luxury Car Tax calculated correctly (☐ not required/not applicable) Every calculation to be System checks that total reliance on reviewed for each “AS” vs LCT is being vs the business has the (Incl. you do the process) reported correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10 9/ Fuel Tax Credits are calculated correctly (☐ not required/not applicable)

Every calculation to be System checks that total reliance on reviewed for each “AS” vs FTC is being vs the business has the (Incl. you do the process) reported correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

Guidance note produced by Page 15 The Institute of Certified Bookkeepers for its members All rights withheld

SECTION E – adhering to acceptable conduct(based on the TASA2009 Code of conduct provisions that are specifically related to the actual provision of service to a client.)

If the client has stated that the scope of work you are required to do is limited or restricted to certain areas, or if you do all the processing, reporting and preparing of statements to be made, then:

In relation to all areas of that client you must still:a) Act honestly and with integrityb) Act lawfully in the best interest of your client (generally)c) Act lawfully in the best interest of your client over any personal interest you may have in

that client or their business affairs (be and act independent)d) Advise the client of their rights and obligations of the relevant tax laws that are materially

related to the work you are doing

In relation to the areas that you HAVE been engaged to perform work then you must:e) Have and provide competent servicef) Have knowledge and skillsg) Take reasonable care to ascertain/understand the clients relevant state of affairsh) Take reasonable care to ensure tax laws are applied correctlyi) Advise the client of their rights and obligations of the relevant tax laws

(Each of these aspects of the code are to be applied to the extent and in respect to the areas that you are providing BAS Services to the client)

Section FHowever:You must not make a statement, prepare a statement, permit an entity to make or prepare a statement, to the commissioner that:

j) Is false, incorrect or misleading in a material particulark) Omits anything that causes the statement to be misleading

Concepts explaineda) Act honestly and with integrity

Would a reasonable person assess that your actions were taken while you were acting honestly and with integrity?

b) Act lawfully in the best interest of your client (generally)“Acting lawfully in the best interests” means you advise the client of the correct law, you assist the client to comply with the correct law, you do not allow the client to make false claims because it suits them. “Best interest” implies that they will not be subject to penalties etc for taking a certain action as that action was not lawful.

c) Act lawfully in the best interest of your client over any personal interest you may have in that client or their business affairsThis deals with ensuring you act as though you are totally independent of any interest in or outcome that your client may or may not achieve in the conduct of their business. You advise, act, perform your work, report to the client without alteration because of any effect it may have on you.

Page 16 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

d) Advise the client of their rights and obligations of the relevant tax laws that are materially related to the work you are doingRefer section D.

If you are engaged by a client then we believe you have an obligation to advise that client, at least in general terms, in writing, their rights and obligations of applying the relevant tax laws correctly. You may not be engaged to advise or review an area, but as an Agent to provide a general advice sheet on the area of law and then confirm that you are not engaged to check that application of law should meet your obligation.

e) Have and provide competent serviceProvision of competent service would rely on #f below “have the relevant knowledge and skills” and therefore you would be able to use appropriate process and techniques to effectively provide the correct service to the client. Do you have processes, template workpapers, systems to ensure competent service? Do you have the relevant skills and knowledge to provide a competent service? Have you recently undertaken any technical material review, industry information review, ATO material review to ensure you are applying the correct laws competently?

f) Have relevant knowledge and skillsHow can you prove that your knowledge and skills are up to date? When did you last update your knowledge either by yourself or via external training to ensure you were current and understood all aspects of the area? Do you or one of your team have “expertise” in the area?

g) Take reasonable care to ascertain/understand the clients relevant state of affairsHave you asked sufficient questions and “within reason” the right questions to understand the client, their business and the areas that you are being asked to advise on?Would another external advisor look at what you did ask and the level of research or investigation you undertook and be satisfied that it was sufficient to then advise the client?What is “reasonable” will vary from one set of client circumstances to the next set of client circumstances: based on level of client knowledge, size of business, intricacy of client business.

h) Take reasonable care to ensure tax laws are applied correctlyHave you spent enough time considering the clients affairs but also the relevant aspects of tax laws in order to ensure everything has been considered?Have you the processes to ensure all aspects of the tax law have been considered?What is “reasonable” will vary from one set of client circumstances to the next set of client circumstances: based on level of client knowledge, size of business, intricacy of client business.

i) Advise the client of their rights and obligations of the relevant tax laws Provide information statements and guidance notes to the client that gives them an understanding of what their obligations are. Noting the client should not be abdicating their obligations in total.

Guidance note produced by Page 17 The Institute of Certified Bookkeepers for its members All rights withheld

Section F – false or misleading Statement

You must not make a statement, prepare a statement, permit an entity to make or prepare a statement to the commissioner that:

j) Is false, incorrect or misleading in a material particulark) Omits anything that causes the statement to be misleading

Exclusions from this paper

Code of conduct provisions not included above:Comply with taxation laws in your own personal affairsAccount for client money you held/holdDo not disclose client information to a third partyArrangements for management of conflicts of interestNot knowingly obstruct the administration of taxation lawsMaintain the required Professional Indemnity InsuranceRespond to the requests from the TPB

SUMMARY CONCEPT

Who does the client think is advising them on this matter?Who is the client relying on for this matter to be correct?

Meet that expectation!

Page 18 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

CASE STUDIES

Example If the client says “don’t do that piece of work” or “don’t check that system” what do I do?

If the excluded area is not directly related to the work that you are doing then: a) Act honestly and with integrity

- confirm it in writing- ask questions if you perceive they need to be asked (but its ok if you don’t get answers)- However turning a blind eye to “non-compliance” would compromise integrity.

b) Act lawfully in the best interest of your client (generally)- Provide the general advice on the client meeting their obligations

c) Act lawfully in the best interest of your client over any personal interest you may have in that client or their business affairs- as always, act in the same way as though you have no personal interest

d) Advise the client of their rights and obligations of the relevant tax laws that are materially related to the work you are doing- provide more specific advice on how the client has been and should be meeting their

obligations- assist the client to meet these obligations (if that is included in your engagement)

You must not make a statement, prepare a statement, permit an entity to make or prepare a statement to the commissioner that:

j) Is false, incorrect or misleading in a material particulark) Omits anything that causes the statement to be misleading

Example The BAS Agent has a view on appropriate treatment and it differs from that of the Tax Agent. You have:

• taken steps to ascertain the treatment• you have interaction with another agent• you obtain the specific tax treatment from the tax agent • you apply that advice

It would appear you have taken reasonable care to ensure the correct tax treatment. Ensure you refer to that separate advice in your notes to the client.

• or you take a more conservative action and not apply the treatment and raise questions, advising the client in writing what you have done in preparation of the reports

Example The BAS Agent has obtained/been provided direction by that Tax Agent.You have:

• taken steps to ascertain the treatment• you have interaction with another agent• you obtain the specific tax treatment from the tax agent • you apply that advice

It would appear you have taken reasonable care to ensure the correct tax treatment. Ensure you refer to that separate advice in your notes to the client.

Guidance note produced by Page 19 The Institute of Certified Bookkeepers for its members All rights withheld

ExampleThe client has two different accounting systems.

1) the first accounts for all transactions relating to clients funds (often referred to as the Trust Account) and produces a GST report for these transactions. This is the processing work you do.

2) the second for the operating expenses of the business and this program also produces a GST report for the general/operating expenses (usually referred to as the General account). You have no input into this account.

The client requires you to combine the two reports and complete the BAS form (paper copy).

ANSWERIn relation to all areas of that client you must still:

e) Act honestly and with integrity- confirm it in writing- ask questions if you perceive they need to be asked (but its ok if you don’t get answers)- However turning a blind eye to “non-compliance” would compromise integrity.

f) Act lawfully in the best interest of your client (generally)- Provide the general advice on the client meeting their obligations

g) Act lawfully in the best interest of your client over any personal interest you may have in that client or their business affairs- as always, act in the same way as though you have no personal interest

h) Advise the client of their rights and obligations of the relevant tax laws that are materially related to the work you are doing- provide more specific advice on how the client has been and should be meeting their

obligations- assist the client to meet these obligations (if that is included in your engagement)

In relation to the areas that you HAVE been engaged to perform work then you must:a) Have and provide competent service

- processes, checklists, procedures, workpapersb) Have knowledge and skills

- experience, training, c) Take reasonable care to ascertain/understand the clients relevant state of affairs

- ask questions on all related areas- confirm level that the client wishes you to investigate

d) Take reasonable care to ensure tax laws are applied correctly- ensure you do have an understanding of the relevant laws

e) Advise the client of their rights and obligations of the relevant tax laws

If you are the one making a statement to the commissioner or signing it when that statement, at least in part, is based on a statement prepared by someone else (refer Section A) then you must either supervise and control their work or take reasonable steps to ensure the statement is accurate.

If you are engaged to process and provide certainty about the one account but are told to totally rely on the other report for the second account then confirm the extent of engagement (Section D) and provide advice to the client about their obligations.

Do the work, bring in the numbers from the report provided and produce the combined reports for the client, possibly including the BAS for the client to “sign off”. Noting on all work notes and the notes to the client that you have relied on the figures provided as directed.

Page 20 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

However: You must not make a statement, prepare a statement, permit an entity to make or prepare a statement to the commissioner that:

f) Is false, incorrect or misleading in a material particularg) Omits anything that causes the statement to be misleading

So if you have concerns you would need to raise those matters with the client and we would advise not to proceed to drafting the BAS that is to be lodged, in such circumstances.

ExampleWhat if the client says to adjust the GST collected figure down because of cashflow issues?What if the client says they will adjust the GST collected figure down because of cashflow issues?What if the client says to ignore something and they will take care of it?

• Provide the general advice to them of their rights and obligations.

• If you know they are making a statement that leaves something out then you should cease your engagement.

• If you provide reports based on your work that, the client then chooses to use or not use or use part of or adjust, then you have provided your reports based on correct process and procedure with your knowledge and skills and competence. The client has then acted, without you, to lodge or adjust then you have not been involved in any part of the “making a statement”. Next appointment you are engaged to prepare the same report for the following month – ask questions, advise and prepare the report.

• What if the client says they will accept the interest penalty for late payment or reporting? Is that “Acting in the best interests” of the client? It wasn’t your action. If they tell you not to lodge until it will be after any due date? We would advise you not to lodge it with your credentials (BAS Agent Portal or your AUSkey as it reflects on your practice) however technically this is not a code breach. Is any of this making a statement that is false? No.

• What if the client says they will deal with the consequence of not reporting an item correctly, when you know it is incorrect? That would be “making or permitting to be made a statement that is misleading” so no you cannot.

• What if the client says they will deal with any consequence of not reporting an item, or researching an item further to ensure it is reported correctly? Then you would need to ensure you have advised them of their rights and obligations. If the client has instructed you NOT to find out the right answer in their circumstances then ensure you confirm the extent of your engagement in writing.

• What if you know that the treatment the client wishes to apply is wrong and they say they will deal with any consequence of not dealing with that item any further, nor take advice from you in relation to that item? Then advise them generally of their rights and obligations, confirm in writing that you are not engaged to advise specifically on the area, but ALSO you cannot be part of making or permitting to be made a statement that is misleading. Therefore provide reports on what you have been engaged to do.

Guidance note produced by Page 21 The Institute of Certified Bookkeepers for its members All rights withheld

• What if you have a financial interest (a part ownership by you, or maybe a relative of yours) in the business? You must act in the same way as if the actions and behaviour and reporting of the client had no effect on you at all. Would a totally independent person assess that you had acted in the same way that they would have, without regard to any personal interest.

ExampleWhat if you think something might be wrong but you have not been engaged to review that area of the clients business?

The law uses the phrases: “…to the circumstances in relation to which you are providing advice to the client””…related to the tax agent services you provide””…relevant to…thing you are doing on behalf of the client”.

Therefore

• provide the client with information or • raise the question • but you do not need to take it further.

You are not obliged to look or investigate matters the client has not engaged you to do.• Agree and document: areas of engagement• Provide (at least general) advice / information sheets• Do not lodge or permit to be lodged an incorrect statement• Take reasonable care to apply tax laws correctly• Sack the “interesting” client

ExampleWhat if you know something is wrong but you have not been engaged to review that area of the clients business?

The law uses the phrases: “…to the circumstances in relation to which you are providing advice to the client””…related to the tax agent services you provide””…relevant to…thing you are doing on behalf of the client”.

Therefore • provide the client with information or • raise the question • but you do not need to take it further.

You are not obliged to look or investigate matters the client has not engaged you to do.• Agree and document: areas of engagement• Provide (at least general) advice / information sheets• Do not lodge or permit to be lodged an incorrect statement• Take reasonable care to apply tax laws correctly• Sack the “interesting” client

Page 22 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

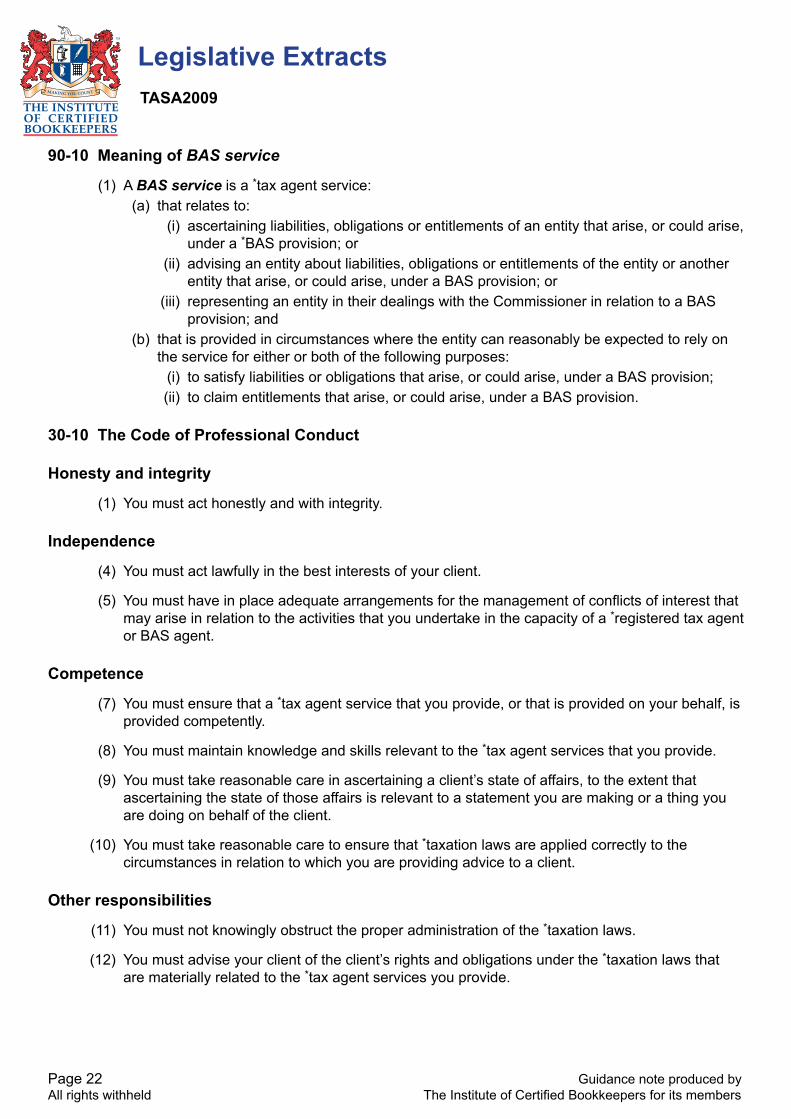

Legislative ExtractsTASA2009

90-10 Meaning of BAS service

(1) A BAS service is a *tax agent service: (a) that relates to: (i) ascertaining liabilities, obligations or entitlements of an entity that arise, or could arise,

under a *BAS provision; or (ii) advising an entity about liabilities, obligations or entitlements of the entity or another

entity that arise, or could arise, under a BAS provision; or (iii) representing an entity in their dealings with the Commissioner in relation to a BAS

provision; and (b) that is provided in circumstances where the entity can reasonably be expected to rely on

the service for either or both of the following purposes: (i) to satisfy liabilities or obligations that arise, or could arise, under a BAS provision; (ii) to claim entitlements that arise, or could arise, under a BAS provision. 30-10 The Code of Professional Conduct Honesty and integrity

(1) You must act honestly and with integrity. Independence

(4) You must act lawfully in the best interests of your client.

(5) You must have in place adequate arrangements for the management of conflicts of interest that may arise in relation to the activities that you undertake in the capacity of a *registered tax agent or BAS agent.

Competence

(7) You must ensure that a *tax agent service that you provide, or that is provided on your behalf, is provided competently.

(8) You must maintain knowledge and skills relevant to the *tax agent services that you provide.

(9) You must take reasonable care in ascertaining a client’s state of affairs, to the extent that ascertaining the state of those affairs is relevant to a statement you are making or a thing you are doing on behalf of the client.

(10) You must take reasonable care to ensure that *taxation laws are applied correctly to the circumstances in relation to which you are providing advice to a client.

Other responsibilities

(11) You must not knowingly obstruct the proper administration of the *taxation laws.

(12) You must advise your client of the client’s rights and obligations under the *taxation laws that are materially related to the *tax agent services you provide.

Guidance note produced by Page 23 The Institute of Certified Bookkeepers for its members All rights withheld

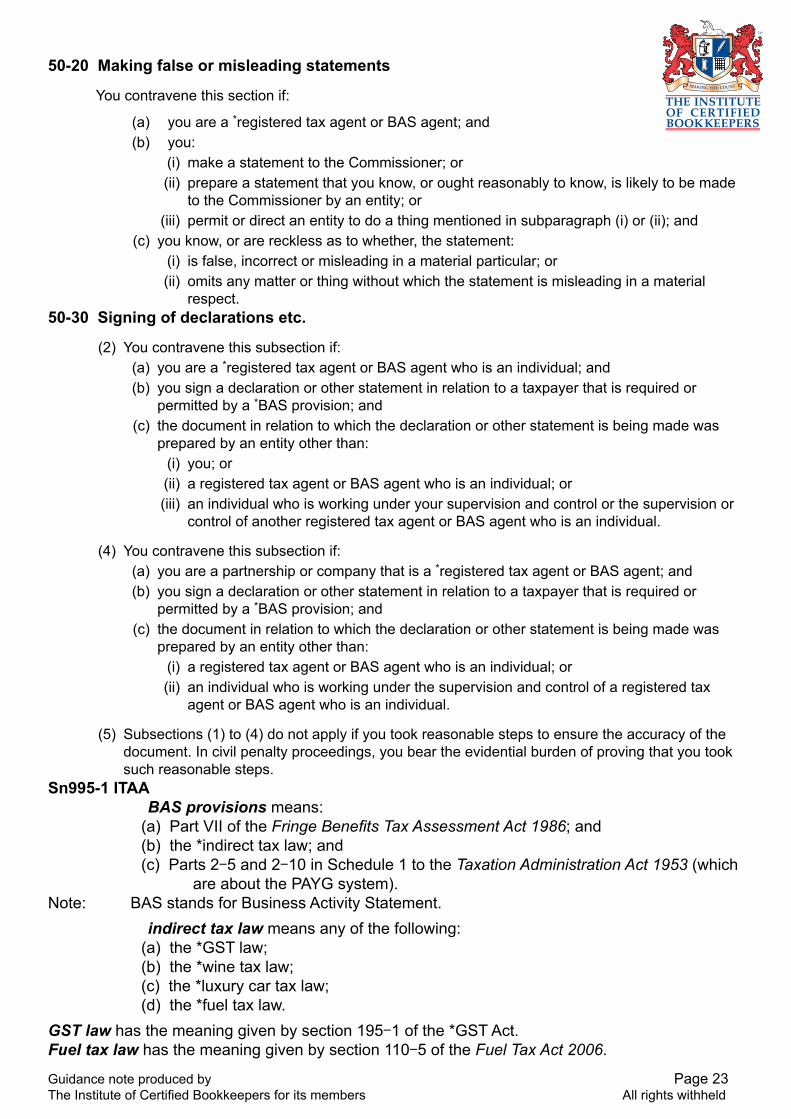

50-20 Making false or misleading statements

You contravene this section if:

(a) you are a *registered tax agent or BAS agent; and (b) you:

(i) make a statement to the Commissioner; or (ii) prepare a statement that you know, or ought reasonably to know, is likely to be made

to the Commissioner by an entity; or (iii) permit or direct an entity to do a thing mentioned in subparagraph (i) or (ii); and (c) you know, or are reckless as to whether, the statement: (i) is false, incorrect or misleading in a material particular; or (ii) omits any matter or thing without which the statement is misleading in a material

respect.50-30 Signing of declarations etc.

(2) You contravene this subsection if: (a) you are a *registered tax agent or BAS agent who is an individual; and (b) you sign a declaration or other statement in relation to a taxpayer that is required or

permitted by a *BAS provision; and (c) the document in relation to which the declaration or other statement is being made was

prepared by an entity other than: (i) you; or (ii) a registered tax agent or BAS agent who is an individual; or (iii) an individual who is working under your supervision and control or the supervision or

control of another registered tax agent or BAS agent who is an individual.

(4) You contravene this subsection if: (a) you are a partnership or company that is a *registered tax agent or BAS agent; and (b) you sign a declaration or other statement in relation to a taxpayer that is required or

permitted by a *BAS provision; and (c) the document in relation to which the declaration or other statement is being made was

prepared by an entity other than: (i) a registered tax agent or BAS agent who is an individual; or (ii) an individual who is working under the supervision and control of a registered tax

agent or BAS agent who is an individual.

(5) Subsections (1) to (4) do not apply if you took reasonable steps to ensure the accuracy of the document. In civil penalty proceedings, you bear the evidential burden of proving that you took such reasonable steps.

Sn995-1 ITAABAS provisions means:

(a) Part VII of the Fringe Benefits Tax Assessment Act 1986; and (b) the *indirect tax law; and (c) Parts 2‑5 and 2‑10 in Schedule 1 to the Taxation Administration Act 1953 (which

are about the PAYG system).Note: BAS stands for Business Activity Statement.

indirect tax law means any of the following: (a) the *GST law; (b) the *wine tax law; (c) the *luxury car tax law; (d) the *fuel tax law.GST law has the meaning given by section 195‑1 of the *GST Act.Fuel tax law has the meaning given by section 110‑5 of the Fuel Tax Act 2006.

Page 24 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

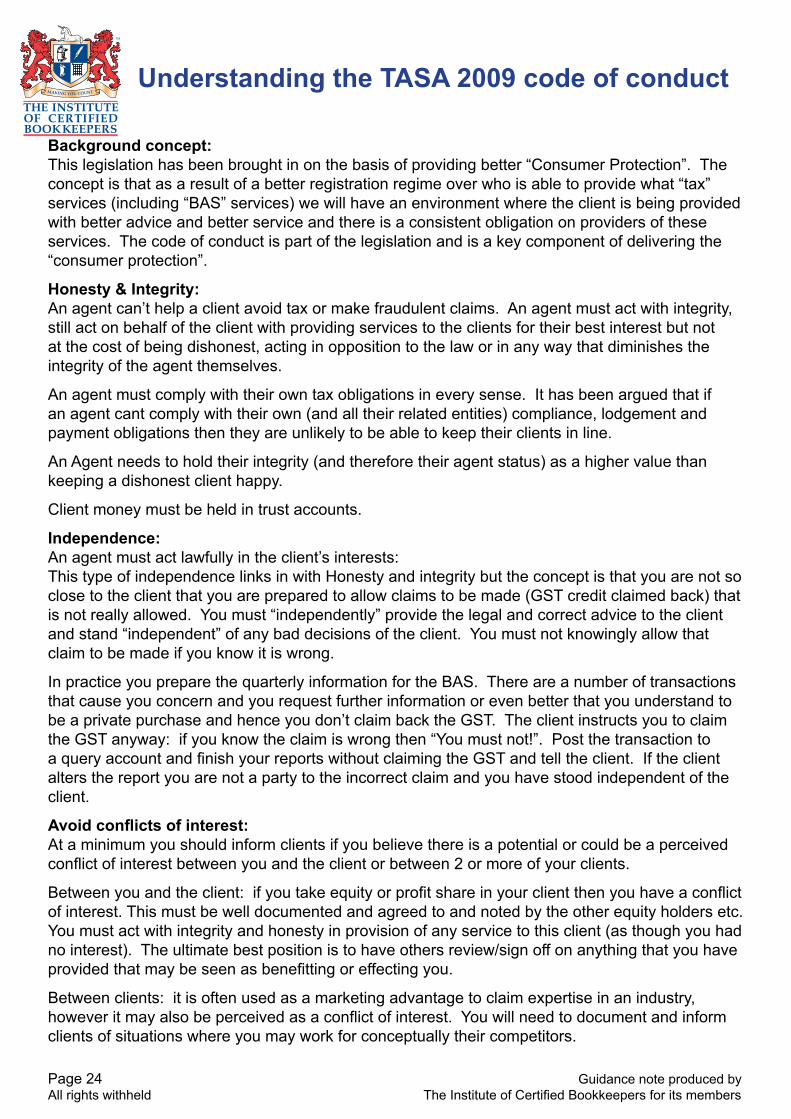

Understanding the TASA 2009 code of conduct Background concept:This legislation has been brought in on the basis of providing better “Consumer Protection”. The concept is that as a result of a better registration regime over who is able to provide what “tax” services (including “BAS” services) we will have an environment where the client is being provided with better advice and better service and there is a consistent obligation on providers of these services. The code of conduct is part of the legislation and is a key component of delivering the “consumer protection”.

Honesty & Integrity:An agent can’t help a client avoid tax or make fraudulent claims. An agent must act with integrity, still act on behalf of the client with providing services to the clients for their best interest but not at the cost of being dishonest, acting in opposition to the law or in any way that diminishes the integrity of the agent themselves.

An agent must comply with their own tax obligations in every sense. It has been argued that if an agent cant comply with their own (and all their related entities) compliance, lodgement and payment obligations then they are unlikely to be able to keep their clients in line.

An Agent needs to hold their integrity (and therefore their agent status) as a higher value than keeping a dishonest client happy.

Client money must be held in trust accounts.

Independence:An agent must act lawfully in the client’s interests: This type of independence links in with Honesty and integrity but the concept is that you are not so close to the client that you are prepared to allow claims to be made (GST credit claimed back) that is not really allowed. You must “independently” provide the legal and correct advice to the client and stand “independent” of any bad decisions of the client. You must not knowingly allow that claim to be made if you know it is wrong.

In practice you prepare the quarterly information for the BAS. There are a number of transactions that cause you concern and you request further information or even better that you understand to be a private purchase and hence you don’t claim back the GST. The client instructs you to claim the GST anyway: if you know the claim is wrong then “You must not!”. Post the transaction to a query account and finish your reports without claiming the GST and tell the client. If the client alters the report you are not a party to the incorrect claim and you have stood independent of the client.

Avoid conflicts of interest:At a minimum you should inform clients if you believe there is a potential or could be a perceived conflict of interest between you and the client or between 2 or more of your clients.

Between you and the client: if you take equity or profit share in your client then you have a conflict of interest. This must be well documented and agreed to and noted by the other equity holders etc. You must act with integrity and honesty in provision of any service to this client (as though you had no interest). The ultimate best position is to have others review/sign off on anything that you have provided that may be seen as benefitting or effecting you.

Between clients: it is often used as a marketing advantage to claim expertise in an industry, however it may also be perceived as a conflict of interest. You will need to document and inform clients of situations where you may work for conceptually their competitors.

Guidance note produced by Page 25 The Institute of Certified Bookkeepers for its members All rights withheld

Competence:Are you competent/qualified/experienced/knowledgeable to provide that service to the client? How to be competent? Take reasonable care! Ask questions on anything you aren’t certain about? Seek clarification of information. Seek expert opinion on areas that you are certain about. This would include issues where you question some of the information provided to you ie Stock level looks too low.

Raise issues with the client: If you some across a transaction or situation that you believe the client should be seeking advice or assistance to comply then you are obliged to advise the client. If the client does not ask you to provide that assistance then you must not be a party to acting without that advice but we don’t believe that you must provide advice or assistance when you are not engaged to do so.

Take Reasonable Steps! Review the information provided by the client. Review and raise issues about that information (areas of concern, areas to research to become certain about), seek expert assistance or clarification on the issue, advise the client of the issues, advise the client of the research and view.

Undergo Continuing Professional EducationKeep up to date, talk to others, research and be trained – details of exactly what the Board requires are yet to be issued. There is an obligation to undergo 15 hours education per year. ICB will continue to issue lists and connections to relevant Education providers. ICB will continue to provide Education through its regional network meetings and also the Annual Conference.

Other Responsibilities:You must comply with the administrative provisions of the law.Keeping records, comply with demands (Sn 263) notices.

Help clients know and comply with tax obligations!Agents must agree with clients the areas that they have been engaged by that client to be “responsible” to assist that client. Specifically note in writing what you are doing and what you aren’t doing. Then for the areas that you are engaged you must be advising and helping the clients in those areas. Help them understand, advise them when you need to, not just when they ask!

Professional Indemnity Insurance:Under the legislation the Board “may” require PI insurance. They do and they have prescribed it. As an ICB member in practice you or the bookkeeping business you are working for must have PI insurance in order to be providing services as a outsource bookkeeping service provider. ICB requirements and the TPB requirements overlap and do not conflict.

Follow Board directives:If you become a registered Agent then you are obliged to comply with Board directions or requests.

What happens if you breach the code?The Board has the ability to: Caution, require an agent to undergo a form of training, require an agent to work under the supervision of another agent, restrict the services that the agent is allowed to provide, suspension or cancellation of the agents registration.

If we turn this to the positive then the Board has the ability to have agents work with other agents in order to provide competent services or have an agent limit their range of services to specialty areas.

Page 26 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

Reasonable Care Whether you are a BAS Agent or not

Principals of dealing with difficult clients, accountants and inheriting messy files!The bookkeeper and BAS Agent’s world continues to evolve at a rapid pace and the fear of being blamed for wrong information, financials and lodgements is more apparent now than ever.Professional bookkeepers integrity must always be held high. As a registered BAS Agent, you cannot knowingly be part of lodging a BAS when you know there is GST over claims, equally a bookkeeper must query and clarify instructions when posting an expense that may not be part of the business.

In the real world, there are many circumstances where bookkeepers are confronted with questionable issues that sometimes involve prior bookkeepers, the “interesting” accountant, the “interesting” client and sometimes all 3. ICB is constantly asked to provide guidance and support on these areas; here are some principals of practice to ensure your highest integrity always stands and a process is followed to ensure you arent being accused of being “interesting”.

What does the client think is happening? How well documented and specified is your task list?Communication! Communication! Communication! is critical in all circumstances. Do nothing without an acceptance in writing from the client of what work they require you to perform. Equally always obtain confirmation for access to the client information on the portal and for every BAS lodged.

You must be honest and complete in taking reasonable care to provide services and advice on the matters that you have been asked to consider. In other words “Don’t solve problems that you have not been specifically asked to solve.”

Inheriting Messy filesA new client can often hold surprises and the prior bookkeepers’ work is sometimes hard to follow and in some circumstances not correct.

Is it your role to change the bookkeeping of the past to match the way you would have done it? The answer, No, unless the client specifically asks you to take the responsibility to change it and for you to be satisfied it is correct.

If the client engages you to fix all problems, then outline the issues in writing, provide a cost estimate and proceed and seek payment each step of the way. If the client chooses to only engage you on the future, then draw a line in the sand and proceed.

Suggested steps to follow:i. Use the “ICB initial file review” to do a complete audit of file so that you find as many issues upfront as possible.ii. Inform the client of the problems found in writing not just in a discussion.iii. Suggest to the client to inform the accountant about what is now happeningiv. Be guided by the client and accountant as to what work is required, don’t just fix it v. On confirmation of what work is to be performed, confirm the details in writing at least via email, to help prevent any subsequent confusion. This communication must also include the basis of fees and estimated costs.vi. If additional problems are found, inform the client and accountant, establish how to proceed and again confirm this in writing.vii. If the client only engages you to perform the current work and not address the issues or the past, then draw a line in the sand and move forward. Create a journal to fix the opening balances if needed and proceed from there. Inform the client and accountant of the journal.

Guidance note produced by Page 27 The Institute of Certified Bookkeepers for its members All rights withheld

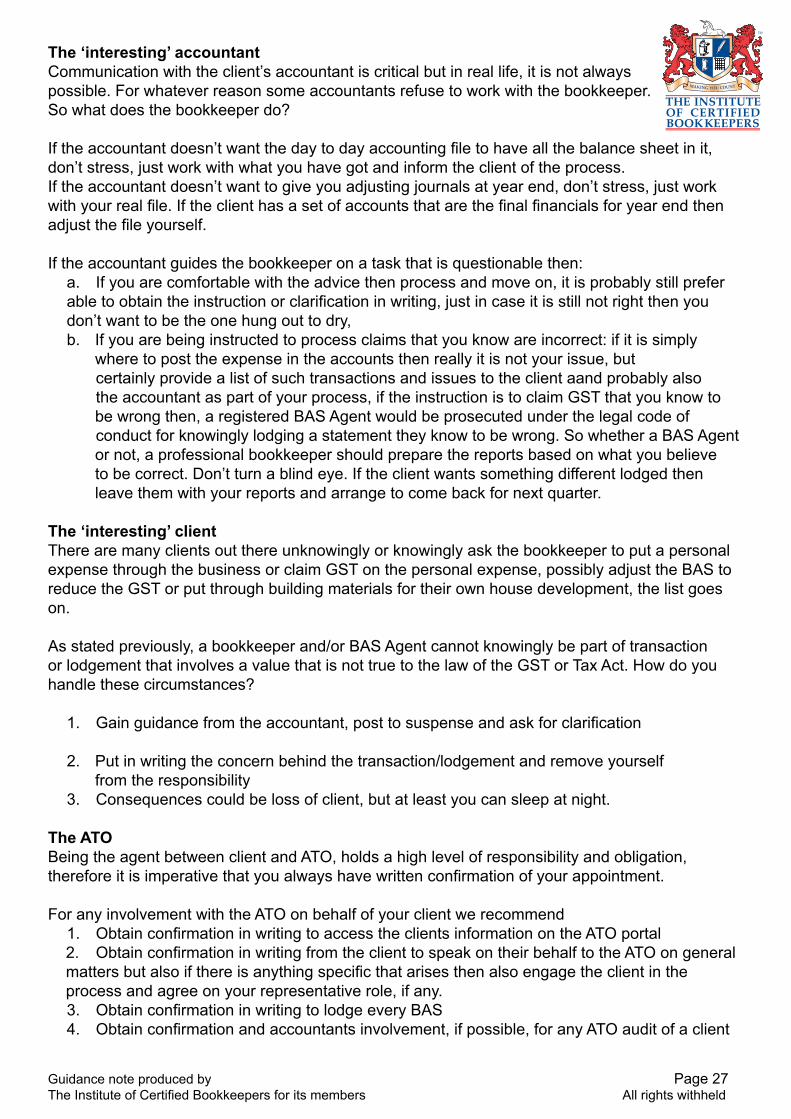

The ‘interesting’ accountant Communication with the client’s accountant is critical but in real life, it is not always possible. For whatever reason some accountants refuse to work with the bookkeeper. So what does the bookkeeper do?

If the accountant doesn’t want the day to day accounting file to have all the balance sheet in it, don’t stress, just work with what you have got and inform the client of the process.If the accountant doesn’t want to give you adjusting journals at year end, don’t stress, just work with your real file. If the client has a set of accounts that are the final financials for year end then adjust the file yourself.

If the accountant guides the bookkeeper on a task that is questionable then:a. If you are comfortable with the advice then process and move on, it is probably still prefer able to obtain the instruction or clarification in writing, just in case it is still not right then you don’t want to be the one hung out to dry,b. If you are being instructed to process claims that you know are incorrect: if it is simply

where to post the expense in the accounts then really it is not your issue, but certainly provide a list of such transactions and issues to the client aand probably also the accountant as part of your process, if the instruction is to claim GST that you know to be wrong then, a registered BAS Agent would be prosecuted under the legal code of conduct for knowingly lodging a statement they know to be wrong. So whether a BAS Agent or not, a professional bookkeeper should prepare the reports based on what you believe to be correct. Don’t turn a blind eye. If the client wants something different lodged then leave them with your reports and arrange to come back for next quarter.

The ‘interesting’ clientThere are many clients out there unknowingly or knowingly ask the bookkeeper to put a personal expense through the business or claim GST on the personal expense, possibly adjust the BAS to reduce the GST or put through building materials for their own house development, the list goes on.

As stated previously, a bookkeeper and/or BAS Agent cannot knowingly be part of transaction or lodgement that involves a value that is not true to the law of the GST or Tax Act. How do you handle these circumstances?

1. Gain guidance from the accountant, post to suspense and ask for clarification

2. Put in writing the concern behind the transaction/lodgement and remove yourself from the responsibility

3. Consequences could be loss of client, but at least you can sleep at night.

The ATOBeing the agent between client and ATO, holds a high level of responsibility and obligation, therefore it is imperative that you always have written confirmation of your appointment.

For any involvement with the ATO on behalf of your client we recommend1. Obtain confirmation in writing to access the clients information on the ATO portal2. Obtain confirmation in writing from the client to speak on their behalf to the ATO on general matters but also if there is anything specific that arises then also engage the client in the process and agree on your representative role, if any.3. Obtain confirmation in writing to lodge every BAS4. Obtain confirmation and accountants involvement, if possible, for any ATO audit of a client

Page 28 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

For your own integrity and well being1. Bill for all your time, life is too short to work for nothing2. Get paid regularly and don’t let the debt build up3. Ask the question, can you live with doing the job when so much of it is out of your control.

4. If your agreement with the client is to not see all the records but to process on instructions - then that’s fine, but document it5. If you know it can’t be proved, then you cannot process a GST claim - you can still allocate the expense to an expense account but maybe use a GST QUE code and not claim it till proof is provided6. Prove that you have asked the questions

In summary, there are many variations of real life experiences that may potentially put the bookkeeper and/or BAS Agent in hot water but we feel whatever those circumstances may be you must always wear the bookkeeping CAP

Communicate

Ask for guidance

Put in writing

Reasonable care – how to actThe Accountant has sent through the end of year adjustment journals which include some interesting items. eg The “entertainment” account balance for the year has been transferred to “Travel Expenses”.

What is our obligation? What should we do? What should we not do? (As a bookkeeper and/or as a BAS Agent)Professional Bookkeepers need to agree with the client on the terms of their engagement. What is the role of the bookkeeper? Bookkeepers typically process transactions and provide the reports at least, to the accountant at the end of the year. The accountant does their thing and returns financial reports to the client. If they are good they also return adjusting journal/s with explanations so that the clients real data file can be altered and brought into line with accountants adjustments. Many times the bookkeeper need to work out the journal to bring the balance sheet into line with the end of year financials.

So as a bookkeeper, who is engaged to follow these instructions, you do make the adjustments and move on.

A professional bookkeeper would raise any issues with the client, if they see anything that they would call a concern or of interest. Raise the issue and move on.

Note Your obligations are limited to the services that you are “providing to the client”. Why the clarification? You are not required to do work that is not part of what the client has engaged you to do. You are not required to look behind rocks unless the client has engaged you to look. You are not required to find areas of non-compliance of your client unless your client has engaged you to advise them in relation to that area of their business.

Guidance note produced by Page 29 The Institute of Certified Bookkeepers for its members All rights withheld

However, neither are you allowed to turn a blind eye when a tax law is being broken. You cannot be a part of a client breaking or bending tax law. If you know that something is wrong and the client or accountant has (nudge, nudge, wink, wink) told you to ignore it or just accept it, you cannot be a part of that - do not lodge a BAS that you KNOW is wrong.

There is a difference between what you know is wrong and what you have questions about. If you have questions, ask those questions, obtain the answers/directions in writing from the tax agent and move on. If it is an area the tax agent/accountant is engaged to advise and not you then you are able to follow that direction and advice. However you cannot blindly accept a client instruction to ignore “ensuring the taxation laws are applied correctly” we recommend you do not be a part of lodging anything that you believe is wrong.

viii. So the client or accountant sends through the above adjustment for “entertainment”.The BAS Agent could initially accept the adjustment.However what if you are aware that FBT is not being considered.The application of FBT to an expense is out of the scope for BAS Agents. It is the role of Tax Agent. Therefore if the tax agent has advised on the adjustment ensure it is in writing and accept the adjustment.

ix. The adjustment sent to you includes an adjustment to claim back further GST input tax credits on the entertainment expenses (shifted to travel) that you previously didn’t claim. Remember that you cannot claim back GST on non-deductible expenses. This is where the two roles of; the tax agent who advises on income tax matters and whether expenses are deductible or not, interacts significantly with the role of the BAS Agent, who typically is responsible for completion of the BAS and hence the amount of GST being claimed back.

x. What if it is clearly wrong and any reasonable person knows that the expense is not claimable? Say Golf Club Membership. FBT can be applied to any expense including Golf Club Memberships/school fees and the above concept would apply. Many bookkeepers are responsible for the payroll however salary sacrifice or packaged expenses and the entire application of FBT and employee reimbursements in relation to FBT can be handled totally outside of the Payroll system, so simply that you have not been advised there is a salary sacrifice or FBT in place does not mean that it is not allowable.

xi. If your role for a client includes; the payroll, the BAS and all related GST treatments, the workers compensation remuneration declarations, the preparation of Payment Summaries (which includes amounts of reportable fringe benefits) we may well have a problem. Given this all inclusive role: What if entertainment and golf club memberships are moved to “travel” or “purchases” and you are instructed to claim back the GST and not show any thing on the payment summaries? Simple: You cannot be a part of it. It is not reasonable for you to turn a blind eye to such a mistaken application of the tax laws. Prepare the reports and BAS as you would normally, move the expenses to a Suspense account of some description (on the balance sheet), advise the client of your treatment and don’t be a part of an illegitimate claim or apparently incorrect declaration to the tax office.

Page 30 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

ICB CHECKLIST Applying the code to a specific client

Client _____________________________________________ Date_______________________

Engagement _________________________________________________ Who____________

What process should the BAS Agent follow to ensure compliance with the code of conduct and the civil penalty provisions?

(P31)

(P31)

(P31)

(P32)

(P33)

Guidance note produced by Page 31 The Institute of Certified Bookkeepers for its members All rights withheld

A checklist of processes and thoughts to determine how you are permitted to engage with a client:Client _____________________________________________ Date_______________________

Engagement _________________________________________________ Who____________

Application of the TASA2009 to BAS Agents performing a BAS Service

Are you allowed to provide this service?It must be a BAS Service in relation to a BAS Provision

Section A – Are you signing a statement or declaration?A1 Are you signing a declaration or statement in relation to the taxpayer? Lodging it via your BAS Agent portal Lodging it via your AUSkey credential using other software (ECI, GovReports) Physically signing a form (not recommended) Providing a completed form for the client to sign (grey area) No: Section D Yes: Section B

Section B – Who prepared the statement?B1: You Yes: Section EB2: Another Tax Agent or BAS Agent Yes Sign & Section F Proof obtainedB3: Another person under your supervision and control

Did you supervise the process followed? Did you review the work performed?

Do you have documents, procedure notes &/or checklists that were followed to prove the review and the supervision?Therefore…..Has the statement been prepared as if you had done it?

If Yes then Section E If No to all then Section C

Section C: Did you take “reasonable steps to ensure the accuracy of the entire document”?Are you satisfied the preparer understands the requirements of how to comply?Are you satisfied that the preparer complied with legal requirements?Have you checked any area of the BAS where there is a risk of a material mistake? What steps do you need to take to satisfy yourself to a reasonable extent that the statement

is correct? Did you review the process that was followed? Did you review the work performed? Do you have documents, procedure notes &/or checklists that were followed to prove the

review and any alterations required?If the client limites your scope of work such that you cannot take “reasonable steps’ to verify

the accuracy of the statment then you cannot sign the statement however you may be able to advise the client on aspects of the statement (Section D)

If YES then Section E If No then Do not sign & Advise the client to the extent Section D.SECTION D – What extent of checking?

Page 32 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

In all cases Advise the preparer/business of their compliance obligations

Yes/No Provided Areas: Tax invoice obligations on all purchases ☐ ☐ Taxable purpose for all claims for Input Tax Credits ☐ ☐ Charging GST on all taxable supplies ☐ ☐ PAYG Withholding obligations ☐ ☐ PAYG Instalment ☐ ☐ Application of WET / FTC / LCT ☐ ☐

What level of checking does the client require me to do? Refer Schedule for D☐ 100% I do it all: ☐ X% Ensure their processing is correct: _________ %☐ 0% None:

• Advise them of each area of their obligations &• Confirm in writing the level of checking (see below) &• Provide cost estimates upfront and then revise frequently.

Section E – Applying the code (in addition to that implied above)In relation to all areas of that client you must still:

a) Act honestly and with integrityb) Act lawfully in the best interest of your client (generally)c) Act lawfully in the best interest of your client over any personal interest you may have in

that client or their business affairs (be and act independent)d) Advise the client of their rights and obligations of the relevant tax laws that are materially

related to the work you are doing (refer Section D) In relation to the areas that you HAVE been engaged to perform work then you must:

e) Have and provide competent service• Do you have processes, template workpapers?

f) Have knowledge and skills• Do you have the relevant skills and knowledge? • Have you recently undertaken any technical material review, industry information

review, ATO material review?• How can you prove that your knowledge and skills are up to date? • When did you last update your knowledge either by yourself or via external training

to ensure you were current and understood all aspects of the area? • Do you or one of your team have “expertise” in the area?

g) Take reasonable care to ascertain/understand the clients relevant state of affairs• Have you asked sufficient questions and “within reason” the right questions to

understand the client, their business and the areas that you are being asked to advise on?

• Would another external advisor look at what you did ask and the level of research or investigation you undertook and be satisfied that it was sufficient to then advise the client?

h) Take reasonable care to ensure tax laws are applied correctly• Have you spent enough time considering the clients affairs but also the relevant

aspects of tax laws in order to ensure everything has been considered?• Have you the processes to ensure all aspects of the tax law have been considered?

i) Advise the client of their rights and obligations of the relevant tax laws (refer Sn D)

Guidance note produced by Page 33 The Institute of Certified Bookkeepers for its members All rights withheld

Section F – false or misleading Statement

You must not make a statement, prepare a statement, permit an entity to make or prepare a statement, to the commissioner that:

a) Is false, incorrect or misleading in a material particularb) Omits anything that causes the statement to be misleading

Are you satisfied you meet this standard? Yes: Proceed No: Don’t prepare the statement – Advise and ask questions?

SUMMARY

Who does the client think is advising them on this matter?Who is the client relying on for this matter to be correct?

Meet that expectation!

Page 34 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

D: Schedule: Checklist Agree on the extent of checking 0 = Total reliance on you 10 = total reliance on the business systems

1/ Tax Invoices (purchases) (☐ not required/not applicable) Every Tax Invoice System checks that total reliance on to be reviewed vs tax invoices are correct vs the business has the (incl. you do the process) and being retained systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

2/ Purchases for taxable purpose (☐ not required/not applicable) Every Tax Invoice to be System checks that total reliance that reviewed for purpose vs taxable purpose is vs the business has the (incl. you do the process) being checked systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

3/ Charging of GST on all Taxable Supplies (☐ not required/not applicable) Every product and System checks that total reliance on Service to be reviewed vs charging of GST is vs the business has the continually being applied correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

4/ PAYG Withholding set up correctly (☐ not required/not applicable) Every employee pay System checks that total reliance on arrangement to be vs PAYG Withholding is vs the business has the reviewed being setup correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

5/ PAYG Withholding applied correctly (☐ not required/not applicable) Every payrun to be System checks that total reliance on reviewed continually vs PAYG Withholding is vs the business has the (Incl. you do the process) being applied correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

6/ PAYG Instalment calculated correctly (☐ not required/not applicable) Every calculation to be System checks that total reliance on reviewed for each “AS” vs income is being vs the business has the (Incl. you do the process) reported correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

7/ WET calculated correctly (☐ not required/not applicable) Every calculation to be System checks that total reliance on reviewed for each “AS” vs WET is being vs the business has the (Incl. you do the process) reported correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

8/ Luxury Car Tax calculated correctly (☐ not required/not applicable) Every calculation to be System checks that total reliance on reviewed for each “AS” vs LCT is being vs the business has the (Incl. you do the process) reported correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

9/ Fuel Tax Credits are calculated correctly (☐ not required/not applicable) Every calculation to be System checks that total reliance on reviewed for each “AS” vs FTC is being vs the business has the (Incl. you do the process) reported correctly systems/checking in place

0 1 2 3 4 5 6 7 8 9 10

Guidance note produced by Page 35 The Institute of Certified Bookkeepers for its members All rights withheld

Review of Bookkeepers ability to service a client in accordance with Professional Standards and Code of ConductA bookkeeper should recognise any skills requiring improvement or business practices requiring management initially and upon a periodic review.

Reviewer__________________________________________ Date____________________

Client_______________________________________________

Do we have the skills / competence to service this client?Software ____________________

Details of Competence______________________________Banking interactions ( ) Cheque writing, ( )Electronic payments,

( )Deposit Cheques ( )Statements electronic bank feedSales Process: standard / unique skills required ____________________________

_________________________Bookkeeping skills:

Notable items__________________________________________GST standard / Specialist Sales (ITS) / Importing / _________________________Payroll: Standard / Salary Packaging / Employment Law

Are there any areas here where we need to up skill or obtain some guidance?

Are there any areas here where we need to ensure a specific person is involved or specific person review is required?

In working with this client are we satisfied that our honesty and integrity is upheld?Do they require us to claim expenses for private matters?Do they require us to ignore cash received?Do they require us to claim GST when it is not appropriate?Have they required us to lodge a BAS that we know contains mistakes?Do we help this client breach their legal requirements?

Do we hold money in our possession / bank for this client? If so: Is it held in a separate bank account (not necessary but advisable) Is it accounted for? Is it ever used for other purposes? Does anyone in this business have any form of connection with any person in the clients business? Our person Their person Connection

___________________________ _______________________ ___________________________ _______________________ ___________________________ _______________________

Is the business owner aware of the connection?Has the business owner specifically consented to you continuing to act for them despite this connection?

Page 36 Guidance note produced by All rights withheld The Institute of Certified Bookkeepers for its members

Details of where this consent is stored ___________________________

How would this connection potentially create a problem?

If our person is responsible for calculating payments to their person what procedure is in place to ensure overpayments are not made?

Does any other client have any business or personal interaction with any other client? Other client Clients person Connection

_________________________ _______________________ __________________________ _______________________ __________________________ _______________________

Is this business owner aware of the connection?

Is the other client business owner aware of the connection?

Has the business owner specifically consented to you continuing to act for them despite this connection? Details of where this consent is stored ___________________________

How would this connection potentially create a problem?

If our person is responsible for calculating/making payments/invoices to client B what procedure is in place to ensure errors are not made?

What business area related to this client should we plan to undertake some additional training?

Types of transaction?

Understanding of industry?

Understanding of areas of GST / PAYG law that relate to this client?

What direction should we seek from the accountant to ensure we abiding by requirements?

Guidance note produced by Page 37 The Institute of Certified Bookkeepers for its members All rights withheld

AUTHORITY FOR BAS Agent to act on behalf of the Taxpayer in respect to the taxpayers dealings with the Australian Taxation OfficeThis authority extends to all areas agreed between the Taxpayer and the BAS Agent which the BAS Agent is permitted to undertake by law, including but not limited to;Adding the Taxpayer to the Client List of the BAS Agent with the ATO ECI lodgement facilityAdding the Taxpayer to the Client List of the BAS Agent on the ATO BAS Agent view of the