the advantages of being an independent contractor: tax tips and more presenters: carolyn r. stall,...

TRANSCRIPT

The Advantages of Being an Independent Contractor: Tax Tips and MorePresenters: Carolyn R. Stall, Managing Director of UHY Advisors William W. Almond, Financial Advisor at Strategic Financial Partners

About Merchant Warehouse• Established in 1998• Over 65,000 merchants• 170+ employees• 3.5 billion in annual processing volume• 2009 ETA ISO of the Year

Agenda• The differences between an employee and an independent

contractor• The tax advantages of being self-employed • Reducing your tax bill with business related deductions• Organizing your tax records• Managing your cash flow• How to choose the best retirement plan• Strategies for paying your estimated taxes• Internal Revenue Service forms for Independent Contractors

***This presentation is intended to provide general information. It should not be construed as legal or tax advice. Please consult your legal or tax advisor.

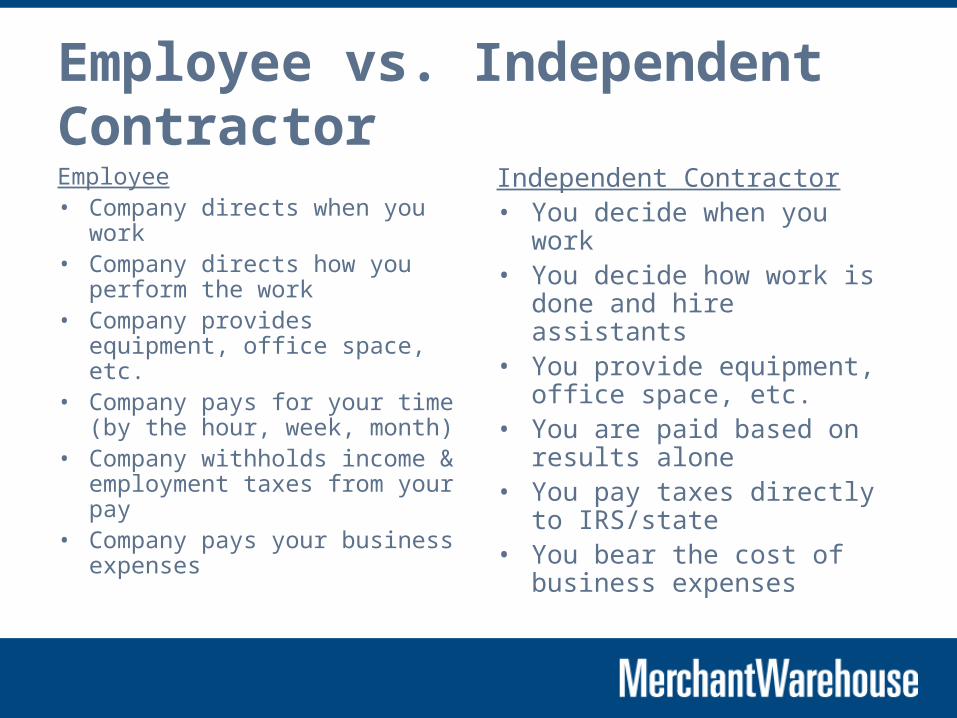

Employee vs. Independent ContractorEmployee• Company directs when you work• Company directs how you

perform the work• Company provides equipment,

office space, etc.• Company pays for your time (by

the hour, week, month)• Company withholds income &

employment taxes from your pay• Company pays your business

expenses

Independent Contractor• You decide when you work• You decide how work is done and

hire assistants• You provide equipment, office

space, etc.• You are paid based on results

alone• You pay taxes directly to IRS/state• You bear the cost of business

expenses

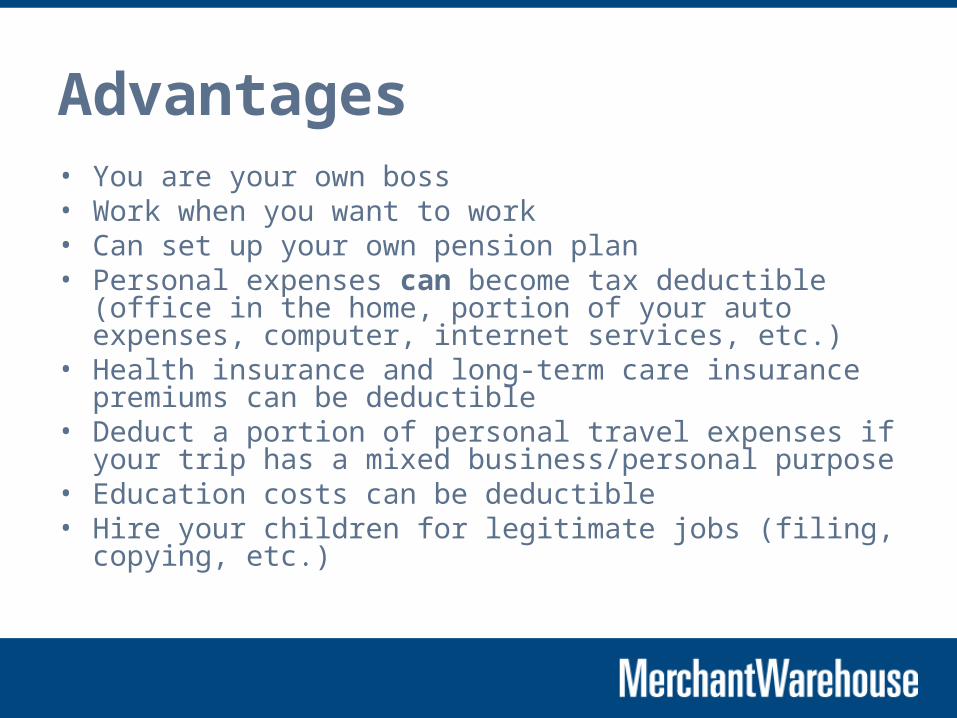

Advantages• You are your own boss• Work when you want to work• Can set up your own pension plan• Personal expenses can become tax deductible (office in the home,

portion of your auto expenses, computer, internet services, etc.)• Health insurance and long-term care insurance premiums can be

deductible• Deduct a portion of personal travel expenses if your trip has a

mixed business/personal purpose• Education costs can be deductible• Hire your children for legitimate jobs (filing, copying, etc.)

How to Report Income & Expenses• Entity organization - Sole Proprietor, LLC, Partnership,

Corporation• Typically a Cash Basis taxpayer

– Report income when received– Report expenses when paid

• Income - Reported to you on Form 1099 MISC "Non employee compensation"

• Expenses - Keep track of your expenses/retain receipts

Travel Expenses• Auto expense - Standard business mileage rate of

$.50/mile for 2010 or actual expenses including gas, oil, repairs, insurance, taxes, etc.

• Travel expenses such as airfare, train fare, parking, taxis, tolls, etc, for any business activities: to meet with clients or potential clients, to attend seminars/training, etc.

• Hotel expenses and meals while away from home

Office Expenses• Office-in-your-home expenses such as a portion of your real estate taxes,

mortgage interest, insurance, utilities, etc. based upon a % of the home that your home office takes up

• Rent for office space, office equipment• Home office equipment such as desks, file cabinets, lamps, rugs, etc.• Repair and maintenance expenses for business equipment• Office expenses such as supplies, stationery, cards, files, etc. • Telephone expenses for dedicated business phone line and cell phones (if

used for business AND personal, only the cost of business calls are deductible)

• Internet access costs such as cable equipment, internet provider costs, etc.

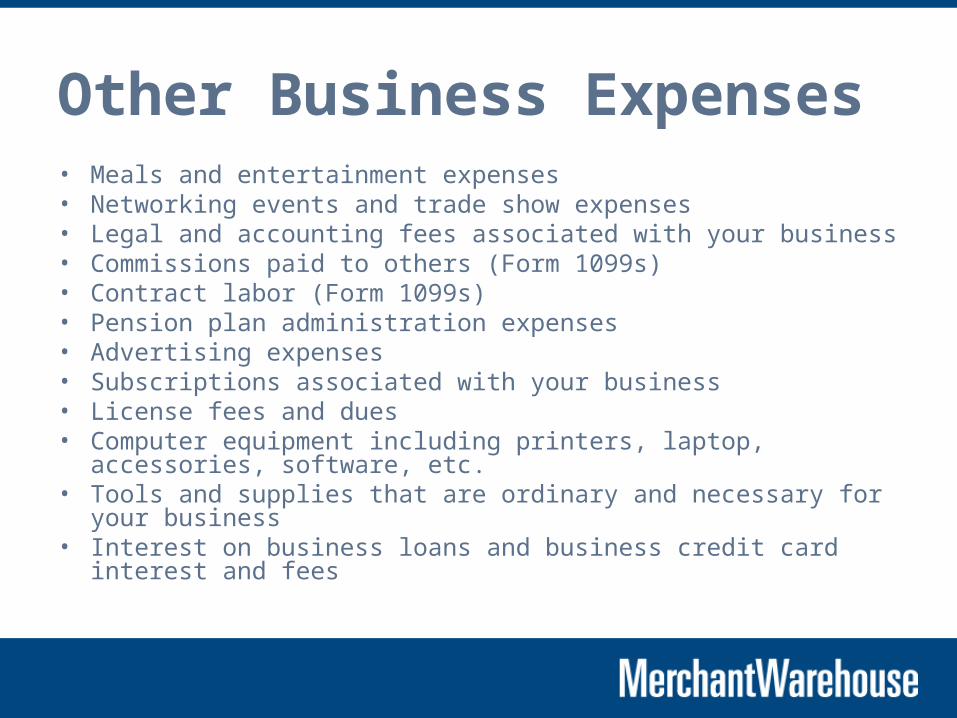

Other Business Expenses• Meals and entertainment expenses• Networking events and trade show expenses• Legal and accounting fees associated with your business• Commissions paid to others (Form 1099s)• Contract labor (Form 1099s)• Pension plan administration expenses• Advertising expenses• Subscriptions associated with your business• License fees and dues• Computer equipment including printers, laptop, accessories, software, etc.• Tools and supplies that are ordinary and necessary for your business• Interest on business loans and business credit card interest and fees

Organizing Your Tax Records & Getting Started

• Determine your "entity" structure (sole proprietor, LLC, corporation)• Register to do business with your state or local government• Set up a business bank account• Consider using QuickBooks or other accounting software• Use one credit card for all business expenses• Try to avoid mixing business and personal expenses together• Need receipt for expenses over $25• File receipts based on type (all meal receipts, travel receipts, etc.)• Keep files by calendar year• Use payroll service to pay employees/pay tax withholdings/file

employer tax forms

Managing Your Cash Flow• Accelerate expenses and defer income• Credit card expenses considered "paid" when

charged• Quarterly estimated tax payments for federal and

state income taxes, including self employment taxes• Build cash reserves• Use home equity line rather than credit card debt

[

How to Choose the Best Retirement Plan

Traditional IRA Roth IRA SEP IRA

Who can establish? Individual with earned income Individual with earned income Corps, Sub-Chapter S, Self-employed, Partnerships, etc

Max. eligibility requirements

Earned income and under the age 70 1/2

Modified adjusted gross income <$120k for single filers and <$177k for joint

Worked for employer during any period of three of the last immediately preceding 5 years, at least 21 years of age, $550 annual compensation

Contribution limits Individual: 100% of earned income up to $5,000 per individual to all IRAs

Individual: 100% of earned income up to $5,000 per individual to all IRAs

Employer: 25% of each employee’s compensation (maximum $49,000; $245,000 salary cap)

Advantages Pre-tax contributions & tax-deferred growth

Tax-deferred growth & tax-free income

Simple to establish and maintain. No annual IRS filing requirements. Contributions deductible for employer

When must the planbe established?

4/15/2010 for 20094/15/2010 for 2009 By tax-filing date plus extensions

When must contributions be made?

4/15/2010 for 2009 4/15/2010 for 2009Employer – by tax-filing dateplus extensionsEmployee – on deferral basis

[

How to Choose the Best Retirement Plan

Traditional IRA Roth IRA SEP IRA

Distributions before age 59 ½

10% tax penalty unless thedistribution is because of death,disability, a qualifying rollover; a direct transfer, the timely withdrawalof an excess contribution, certainqualified medical or educationalexpenses and a first-time homepurchase ($10,000 limit in aggregateto all IRAs). Waived if the distributionis part of a series of substantiallyequal periodic payments made overthe individual’s life expectancy.

10% tax penalty unless the distribution is because of death, disability, a qualifying rollover; a direct transfer, the timely withdrawal of an excess contribution, certain qualified medical or educational expenses and a first-time home purchase ($10,000 limit in aggregate to all IRAs). Waived if the distribution is part of a series of substantially equal periodic payments made over the individual’s life expectancy.

10% tax penalty utilizing substantially equal payments, death, disability, medical expenses, exceeding 7.5% of AGI or purchase of health insurance while employed

Distributions for ages 59 ½-70 ½

No tax penalty No tax penalty No tax penalty

Distribution after age 70 ½

Required minimum distributions aslate as April 1 following the year inwhich the individual reaches age701/2

Required minimum distributions as late as April 1 following the year in which the individual reaches age 701/2

Required minimum distributions (may remove aggregate total from one account)

How are distributions taxed?

Taxed as ordinary income Principal and earnings withdrawn are tax-free Taxed as ordinary income

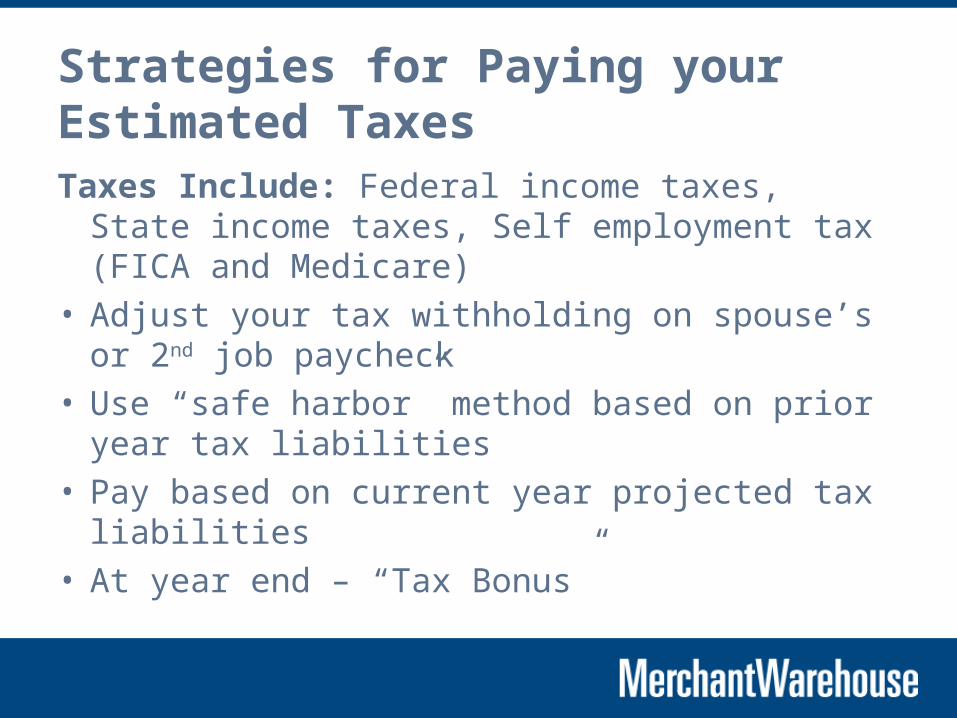

Strategies for Paying your Estimated Taxes

Taxes Include: Federal income taxes, State income taxes, Self employment tax (FICA and Medicare)

• Adjust your tax withholding on spouse’s or 2nd job paycheck

• Use “safe harbor” method based on prior year tax liabilities

• Pay based on current year projected tax liabilities• At year end – “Tax Bonus”

Internal Revenue Service Forms for ICs

• Form W-9 - to provide Identification Number to Merchant Warehouse

• Form 1099 MISC - Reports income paid to you during calendar year

• Form 1040 - Schedule C • www.irs.gov • www.business.gov

Merchant Warehouse ISO/Agent Program

• The security of a financially sound ISO• Generous bonuses and benefits• Uniquely fair agent contract• Innovative technology• In-house/dedicated customer and technical

support• Guaranteed lifetime residuals• Marketing support• In-depth sales training

Questions?Interested in becoming an independent sales agent for

Merchant Warehouse? Contact:– Doug Small - 617-896-5590 ext 2535

Be sure to visit us at the ETA Annual Meeting & Expo, April 13-15th, Mandalay Bay, Las Vegas

Enter for a chance to win our ultimate new office give-away!