the 2011 economy: what exactly does a recovery look like? r. christopher jones, ph.d

Post on 20-Dec-2015

216 views

TRANSCRIPT

The 2011 Economy:What Exactly Does a Recovery Look Like?

R. Christopher Jones, Ph.D.

2

So, where are we?

We’re actually in a recovery that isn’t strong enough to make up the massive job loss Recession technically over June 2009 6 consecutive quarters Real GDP growth Decent growth in retail sales Industrial production of business equipment up Inflation and interest rates remain low, but food

& fuel prices are rising S & P 500 up 12 percent

3

So, where are we?

BUT.. We’ve only created 1.2 million jobs this year We lost 8.6 million jobs in 2008 and 2009 GDP needs to grow at 3.5% or more to see

significant improvement in unemployment rate Industrial production of consumer goods and

durable goods still anemic Increasing Federal debt and expansive

monetary policy creates inflation concerns Housing sector still pathetic

4

What about Florida?

Still bad, worse than the nation as a whole Real estate, tourism continue to suffer Stimulus may be a “paper tiger” for Florida Anti-growth supporters haven’t helped the cause

The horse’s back is cracked Growth & vacations carried us to prosperity The recession stopped both Tourist sector will rebound before real estate We’re not really affordable anymore

5

How Bad Is It?

The “Good” News We are recovering, yet modestly We’ve had recessions of similar magnitude in the

past, and we’ve recovered from them Mid 70’s & early 80’s recessions 72% of economic growth positive since WWII U.S. per capita GDP growth since 1890 has

averaged just under 2% per year Our ability to innovate has served as the

cornerstone for prolonged economic growth

6

How Bad Is It?

The “Bad” News We’re dealing with structural problems of a

serious nature Monetary system is facing serious challenges An increasingly leveraged economy (debt) Relentless global competition Economic pressures created by generational shifts

Are we dealing with a “new normal”? Higher unemployment, lower incomes We’re in a “transitional struggle” w.r.t. production Tough choices lie ahead

7

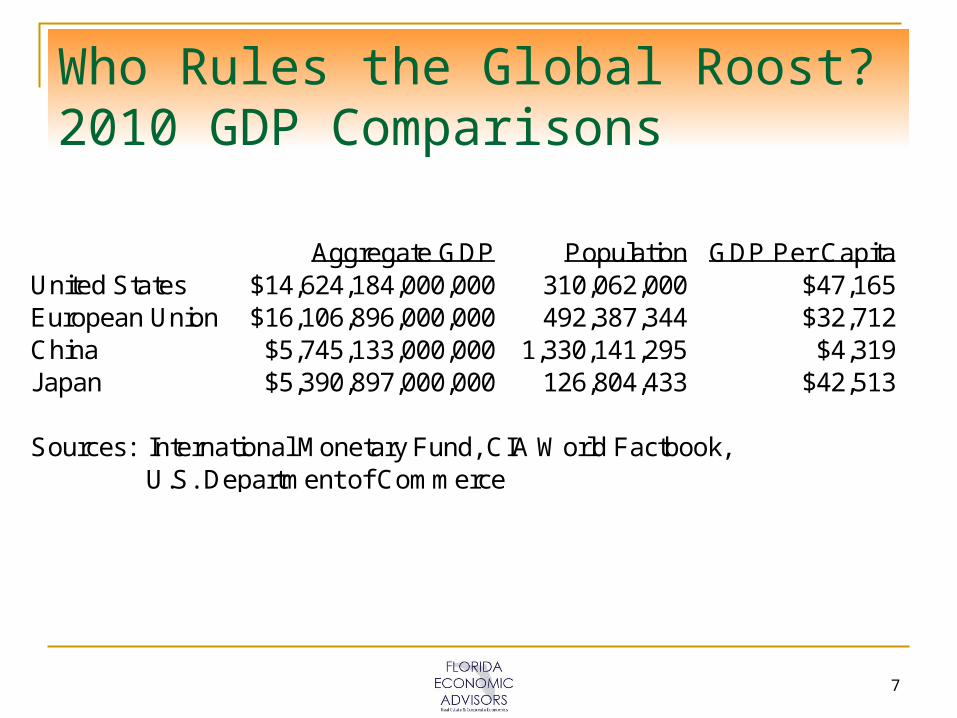

Who Rules the Global Roost?2010 GDP Comparisons

Aggregate GDP Population GDP Per CapitaUnited States $14,624,184,000,000 310,062,000 $47,165European Union $16,106,896,000,000 492,387,344 $32,712China $5,745,133,000,000 1,330,141,295 $4,319Japan $5,390,897,000,000 126,804,433 $42,513

Sources: International Monetary Fund, CIA World Factbook, U.S. Department of Commerce

8

Long-Term GDP Growth 1890-2006

9

U.S. Real GDP 1947-2010

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

$12,000

$13,000

$14,000

Q3

47

Q2

50

Q1

53

Q4

55

Q3

58

Q2

61

Q1

64

Q4

66

Q3

69

Q2

72

Q1

75

Q4

77

Q3

80

Q2

83

Q1

86

Q4

88

Q3

91

Q2

94

Q1

97

Q4

99

Q3

02

Q2

05

Q1

08

Q4

10

Bill

ion

s

10

U.S. Real GDP Annualized % Growth

1947-2010

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%Q

3 47

Q2

50

Q1

53

Q4

55

Q3

58

Q2

61

Q1

64

Q4

66

Q3

69

Q2

72

Q1

75

Q4

77

Q3

80

Q2

83

Q1

86

Q4

88

Q3

91

Q2

94

Q1

97

Q4

99

Q3

02

Q2

05

Q1

08

Q4

10

11

U.S. Unemployment Rate 1948-2010

2.03.0

4.05.06.0

7.08.09.0

10.011.0

Jun

-48

Jul-

50A

ug

-52

Sep

-54

Oct

-56

No

v-58

Dec

-60

Jan

-63

Feb

-65

Mar

-67

Ap

r-69

May

-71

Jun

-73

Jul-

75A

ug

-77

Sep

-79

Oct

-81

No

v-83

Dec

-85

Jan

-88

Feb

-90

Mar

-92

Ap

r-94

May

-96

Jun

-98

Jul-

00A

ug

-02

Sep

-04

Oct

-06

No

v-08

Dec

-10

Per

cen

t

12

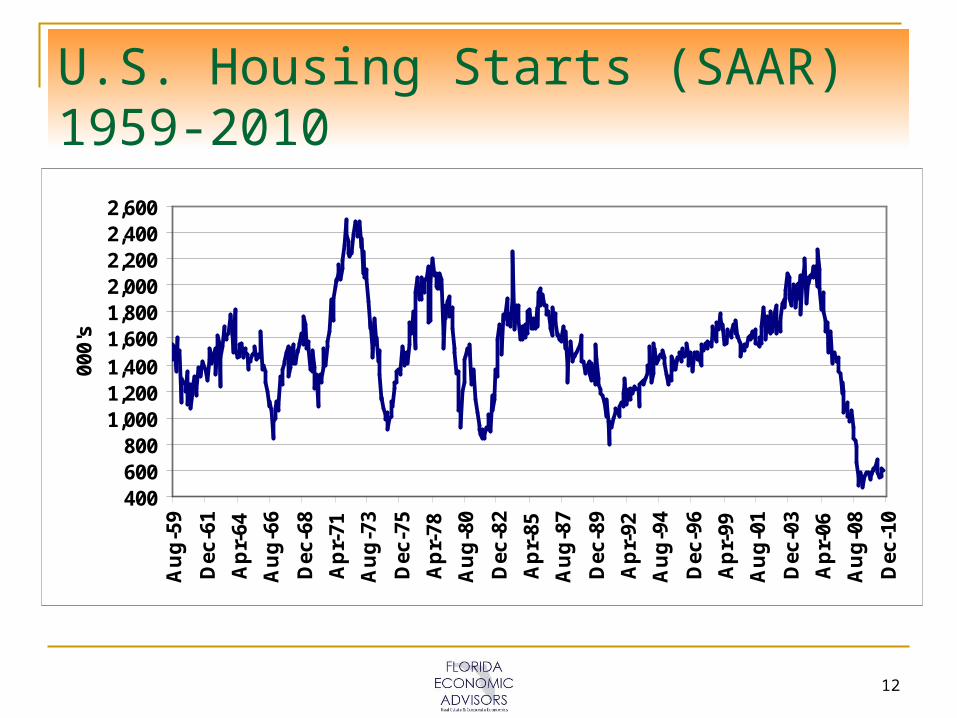

U.S. Housing Starts (SAAR) 1959-2010

400600800

1,0001,2001,4001,6001,8002,0002,2002,4002,600

Au

g-5

9

Dec

-61

Ap

r-64

Au

g-6

6

Dec

-68

Ap

r-71

Au

g-7

3

Dec

-75

Ap

r-78

Au

g-8

0

Dec

-82

Ap

r-85

Au

g-8

7

Dec

-89

Ap

r-92

Au

g-9

4

Dec

-96

Ap

r-99

Au

g-0

1

Dec

-03

Ap

r-06

Au

g-0

8

Dec

-10

000'

s

13

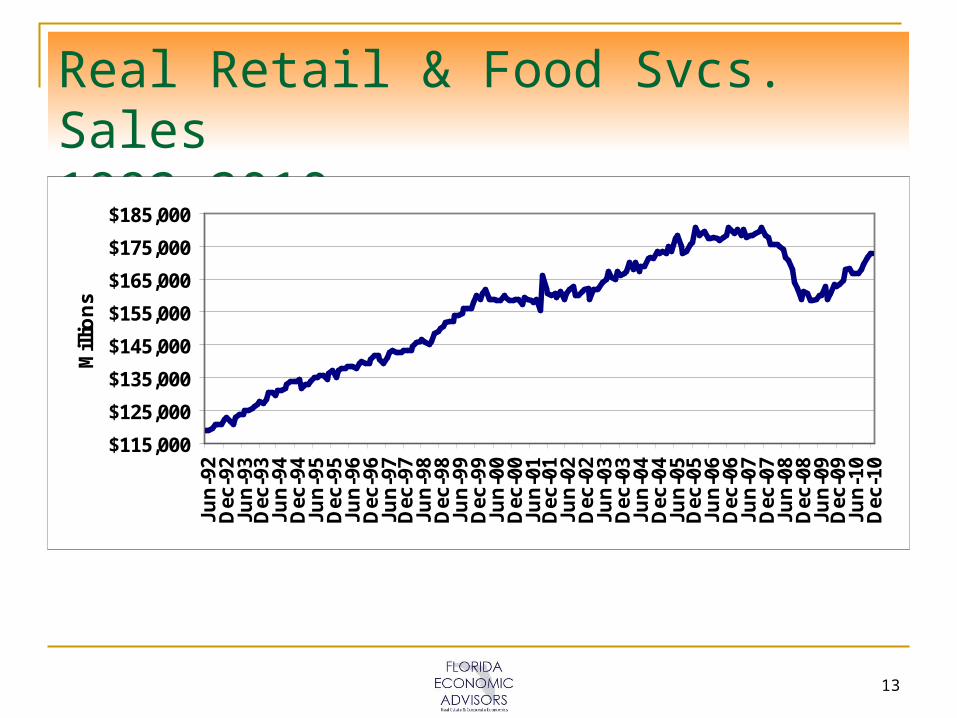

Real Retail & Food Svcs. Sales 1992-2010

$115,000

$125,000

$135,000

$145,000

$155,000

$165,000

$175,000

$185,000Ju

n-9

2D

ec-9

2Ju

n-9

3D

ec-9

3Ju

n-9

4D

ec-9

4Ju

n-9

5D

ec-9

5Ju

n-9

6D

ec-9

6Ju

n-9

7D

ec-9

7Ju

n-9

8D

ec-9

8Ju

n-9

9D

ec-9

9Ju

n-0

0D

ec-0

0Ju

n-0

1D

ec-0

1Ju

n-0

2D

ec-0

2Ju

n-0

3D

ec-0

3Ju

n-0

4D

ec-0

4Ju

n-0

5D

ec-0

5Ju

n-0

6D

ec-0

6Ju

n-0

7D

ec-0

7Ju

n-0

8D

ec-0

8Ju

n-0

9D

ec-0

9Ju

n-1

0D

ec-1

0

Mill

ion

s

14

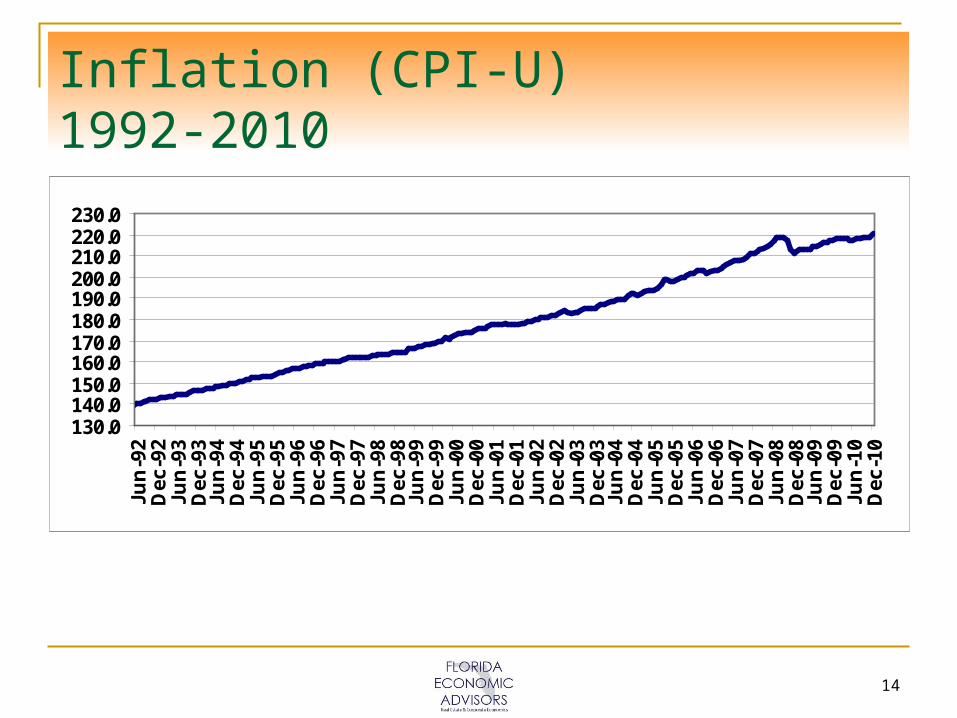

Inflation (CPI-U) 1992-2010

130.0140.0150.0160.0170.0180.0190.0200.0210.0220.0230.0

Jun

-92

Dec

-92

Jun

-93

Dec

-93

Jun

-94

Dec

-94

Jun

-95

Dec

-95

Jun

-96

Dec

-96

Jun

-97

Dec

-97

Jun

-98

Dec

-98

Jun

-99

Dec

-99

Jun

-00

Dec

-00

Jun

-01

Dec

-01

Jun

-02

Dec

-02

Jun

-03

Dec

-03

Jun

-04

Dec

-04

Jun

-05

Dec

-05

Jun

-06

Dec

-06

Jun

-07

Dec

-07

Jun

-08

Dec

-08

Jun

-09

Dec

-09

Jun

-10

Dec

-10

15

Real Per Capita Disposable Personal Income 1959-2010

$8,000$10,000$12,000$14,000$16,000$18,000$20,000$22,000$24,000$26,000$28,000$30,000$32,000$34,000

Jul-

59Ja

n-6

1Ju

l-62

Jan

-64

Jul-

65Ja

n-6

7Ju

l-68

Jan

-70

Jul-

71Ja

n-7

3Ju

l-74

Jan

-76

Jul-

77Ja

n-7

9Ju

l-80

Jan

-82

Jul-

83Ja

n-8

5Ju

l-86

Jan

-88

Jul-

89Ja

n-9

1Ju

l-92

Jan

-94

Jul-

95Ja

n-9

7Ju

l-98

Jan

-00

Jul-

01Ja

n-0

3Ju

l-04

Jan

-06

Jul-

07Ja

n-0

9Ju

l-10

16

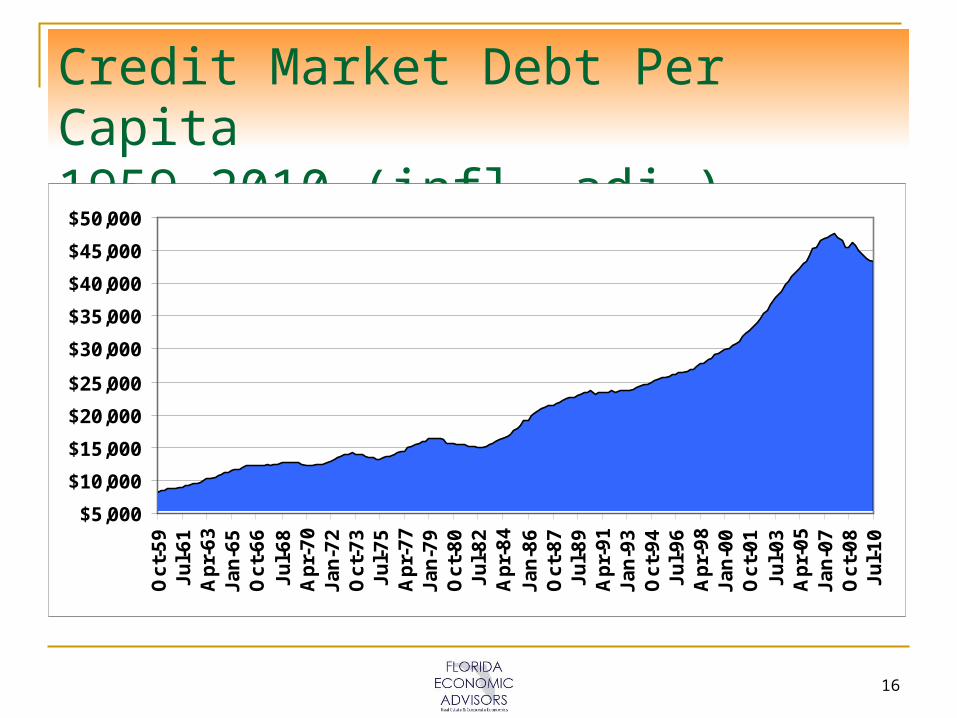

Credit Market Debt Per Capita 1959-2010 (infl. adj.)

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

Oc

t-5

9J

ul-

61

Ap

r-6

3J

an

-65

Oc

t-6

6J

ul-

68

Ap

r-7

0J

an

-72

Oc

t-7

3J

ul-

75

Ap

r-7

7J

an

-79

Oc

t-8

0J

ul-

82

Ap

r-8

4J

an

-86

Oc

t-8

7J

ul-

89

Ap

r-9

1J

an

-93

Oc

t-9

4J

ul-

96

Ap

r-9

8J

an

-00

Oc

t-0

1J

ul-

03

Ap

r-0

5J

an

-07

Oc

t-0

8J

ul-

10

17

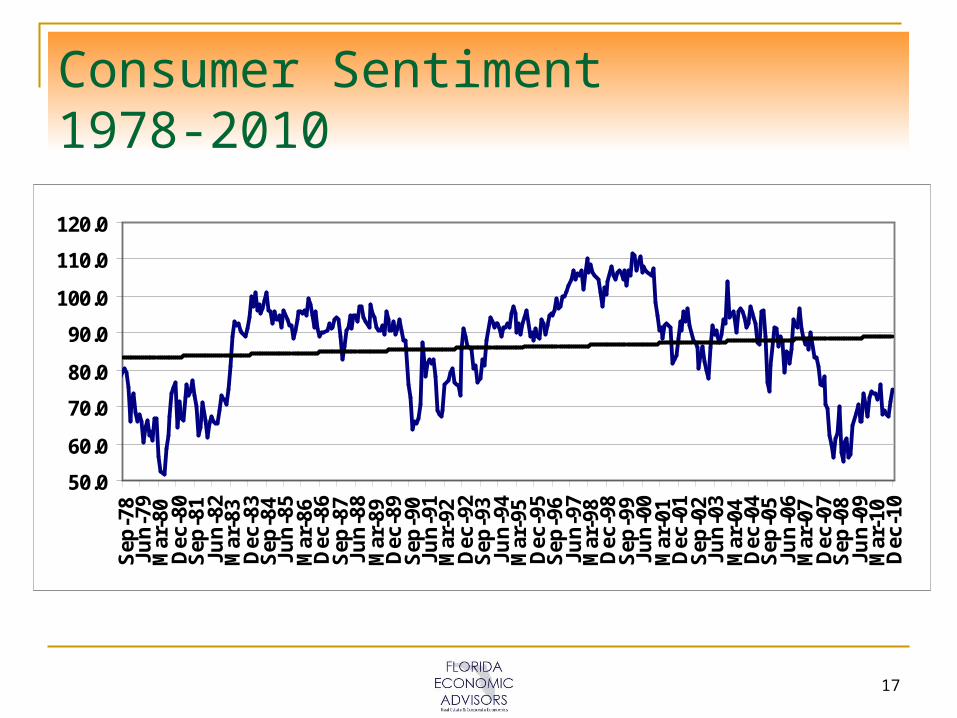

Consumer Sentiment 1978-2010

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

Sep

-78

Jun

-79

Mar

-80

Dec

-80

Sep

-81

Jun

-82

Mar

-83

Dec

-83

Sep

-84

Jun

-85

Mar

-86

Dec

-86

Sep

-87

Jun

-88

Mar

-89

Dec

-89

Sep

-90

Jun

-91

Mar

-92

Dec

-92

Sep

-93

Jun

-94

Mar

-95

Dec

-95

Sep

-96

Jun

-97

Mar

-98

Dec

-98

Sep

-99

Jun

-00

Mar

-01

Dec

-01

Sep

-02

Jun

-03

Mar

-04

Dec

-04

Sep

-05

Jun

-06

Mar

-07

Dec

-07

Sep

-08

Jun

-09

Mar

-10

Dec

-10

18

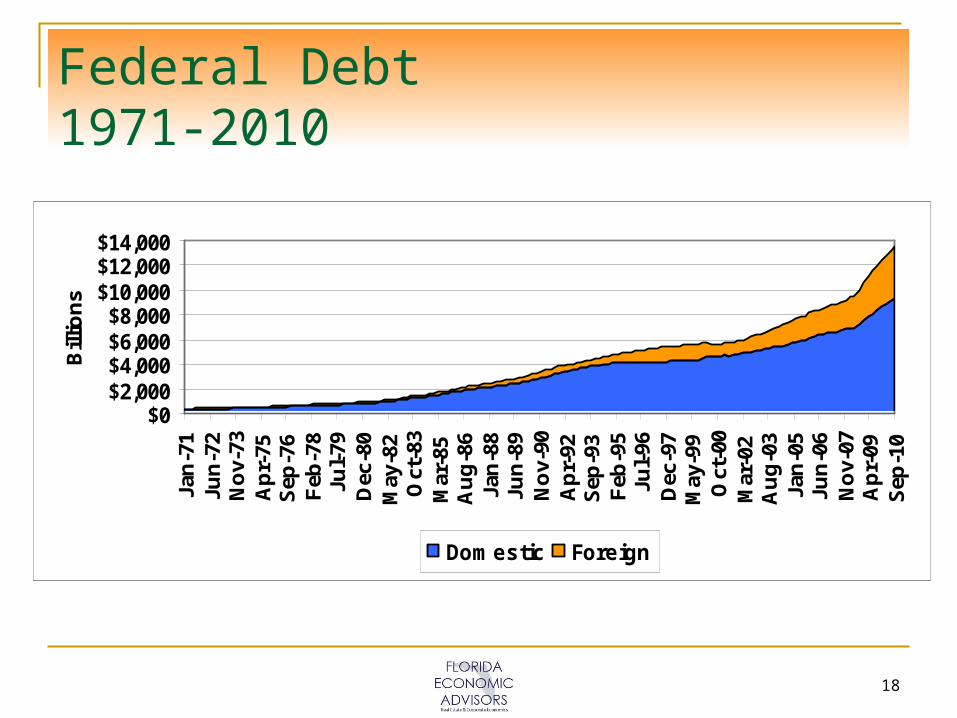

Federal Debt 1971-2010

$0$2,000$4,000$6,000$8,000

$10,000$12,000$14,000

Jan

-71

Jun

-72

No

v-73

Ap

r-75

Sep

-76

Feb

-78

Jul-

79D

ec-8

0M

ay-8

2O

ct-8

3M

ar-8

5A

ug

-86

Jan

-88

Jun

-89

No

v-90

Ap

r-92

Sep

-93

Feb

-95

Jul-

96D

ec-9

7M

ay-9

9O

ct-0

0M

ar-0

2A

ug

-03

Jan

-05

Jun

-06

No

v-07

Ap

r-09

Sep

-10

Bill

ion

s

Domestic Foreign

19

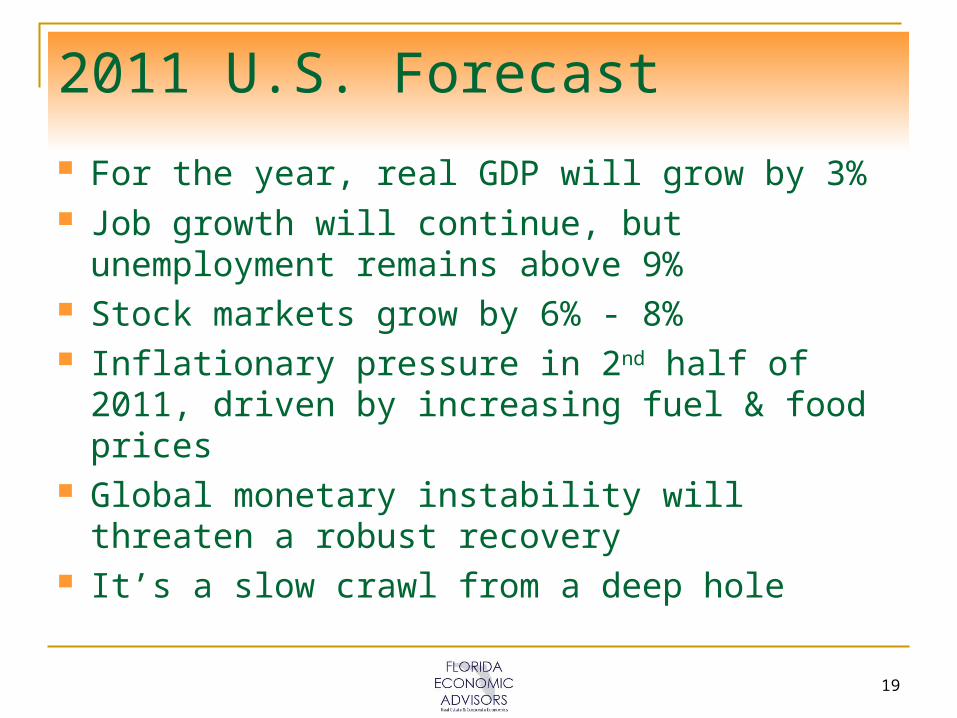

2011 U.S. Forecast

For the year, real GDP will grow by 3% Job growth will continue, but unemployment

remains above 9% Stock markets grow by 6% - 8% Inflationary pressure in 2nd half of 2011, driven

by increasing fuel & food prices Global monetary instability will threaten a

robust recovery It’s a slow crawl from a deep hole

20

Florida: The Facts

Dec. 2007 to Jul. 2010: Lost 930,800 jobs Equivalent to losing 92% of Orlando MSA, or

83% of Tampa-St. Pete-Clearwater MSA Jul. – Nov. 2010: Gained 131,500 jobs 11.6% unemployment (Dec. 2010) 14,346 housing starts from Aug. – Dec. ’10,

compared to 20,934 starts Aug. – Dec. ’08 Home prices are down 35.6% from their Q4

2006 peak – comparable with early 2004 prices

21

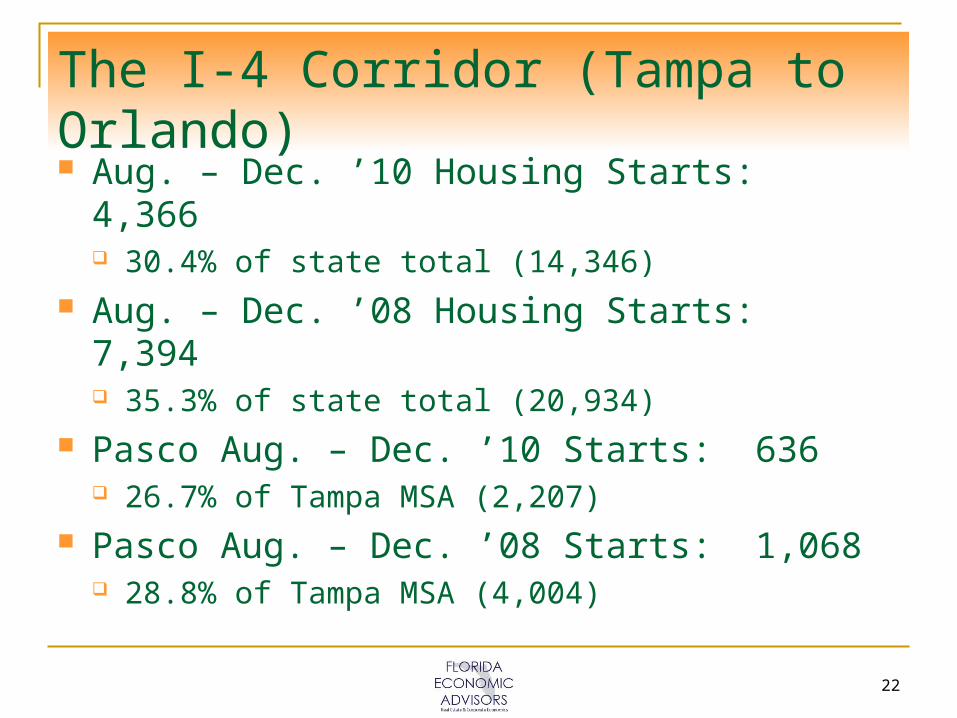

The I-4 Corridor (Tampa to Orlando)

Dec. 2007 to Jul. 2010: Lost 283,200 jobs Equivalent to losing all of Seminole County,

1.6x Pasco County, or 1.3x Polk County Jul. – Nov. 2010: Gained 49,100 jobs Unemployment (Dec.): Tampa MSA 12.0%,

Orlando MSA 11.3%, Lakeland MSA 12.5% Pasco: Lost 7,969 jobs Dec. ’07 to Jul. ’10 Jul. – Nov. 2010, Pasco: Lost 2,922 jobs Pasco (Dec.): 13.0% unemployment

22

The I-4 Corridor (Tampa to Orlando)

Aug. – Dec. ’10 Housing Starts: 4,366 30.4% of state total (14,346)

Aug. – Dec. ’08 Housing Starts: 7,394 35.3% of state total (20,934)

Pasco Aug. – Dec. ’10 Starts: 636 26.7% of Tampa MSA (2,207)

Pasco Aug. – Dec. ’08 Starts: 1,068 28.8% of Tampa MSA (4,004)

23

Florida Metro Economic Activity 2008-2010

FLORIDA INDICATORSBY MSA 2010 2009 2008

Aug. Sep. Oct. Nov. Dec. Aug. Sep. Oct. Nov. Dec. Aug. Sep. Oct. Nov. Dec.Housing Starts (Permits)

Florida 3,196 2,772 2,630 2,710 3,038 2,802 3,040 2,881 3,002 3,495 5,825 5,245 3,634 3,052 3,178Tampa-St. Pete 436 490 434 501 346 491 524 434 1,074 1,054 1,189 858 694 699 564Orlando 384 321 300 360 310 327 284 387 324 363 626 850 435 452 364Jacksonville MSA 277 242 204 215 165 293 354 328 266 285 293 354 337 301 283Miami-Ft. Laud-PB 438 348 527 478 324 248 309 312 200 249 824 558 447 255 735Lakeland 123 88 122 86 65 92 112 106 68 92 188 121 145 123 86

Employment (000's)Florida 7,179.1 7,181.6 7,208.5 7,253.9 n.a 7,168.6 7,162.0 7,183.5 7,216.9 7,237.3 7,657.8 7,629.2 7,600.6 7,607.9 7,607.2Tampa-St. Pete 1,118.2 1,121.9 1,120.7 1,127.9 n.a 1,123.8 1,124.3 1,123.8 1,126.4 1,128.2 1,195.3 1,190.2 1,184.6 1,183.9 1,185.8Orlando 997.5 995.7 1,007.9 1,013.5 n.a 998.1 995.6 999.6 1,001.9 1,005.7 1,070.7 1,064.1 1,060.1 1,058.0 1,056.0Jacksonville MSA 576.3 576.5 578.8 582.7 n.a 578.1 577.2 579.0 584.3 585.7 616.2 615.5 614.2 615.6 613.0Miami-Ft. Laud-PB 2,162.9 2,171.0 2,175.7 2,192.1 n.a 2,166.4 2,168.3 2,174.3 2,186.8 2,200.1 2,319.2 2,315.0 2,308.2 2,320.4 2,328.8Lakeland 192.2 192.6 193.6 194.5 n.a 193.2 193.4 194.1 195.3 196.3 206.2 206.7 205.2 205.7 205.8

Unemployment (%)Florida 12.4 12.0 11.6 12.2 11.6 11.2 11.4 11.5 11.4 11.6 7.1 7.1 7.2 7.5 8.0Tampa-St. Pete 12.6 12.4 11.9 12.6 12.0 11.6 11.8 11.9 12.2 12.4 7.3 7.3 7.5 8.0 8.4Orlando 12.0 11.8 11.3 11.9 11.3 11.1 11.5 11.5 11.7 11.8 6.5 6.5 6.8 7.4 7.7Jacksonville MSA 11.9 11.5 11.0 11.6 11.0 10.7 10.8 10.9 11.1 11.2 6.6 6.4 6.4 6.8 7.2Miami-Ft. Laud-PB 12.8 12.1 11.8 12.1 11.8 11.1 11.0 11.2 10.7 11.1 7.0 6.9 7.1 7.1 7.7Lakeland 13.5 13.3 12.6 13.3 12.5 12.4 12.7 12.6 12.7 12.7 7.8 7.8 7.8 8.2 8.5

n.a.: Data not available as of 1/27/11Sources: U.S. Dept. of Commerce, U.S. Dept. of Labor, Florida Agency for Workforce Innovation

24

Florida Home Price Index (Q1 1980 = 100)

0

50

100

150

200

250

300

350

400

450

500

Ap

r-75

Jan

-76

Oct

-76

Jul-7

7A

pr-

78Ja

n-7

9O

ct-7

9Ju

l-80

Ap

r-81

Jan

-82

Oct

-82

Jul-8

3A

pr-

84Ja

n-8

5O

ct-8

5Ju

l-86

Ap

r-87

Jan

-88

Oct

-88

Jul-8

9A

pr-

90Ja

n-9

1O

ct-9

1Ju

l-92

Ap

r-93

Jan

-94

Oct

-94

Jul-9

5A

pr-

96Ja

n-9

7O

ct-9

7Ju

l-98

Ap

r-99

Jan

-00

Oct

-00

Jul-0

1A

pr-

02Ja

n-0

3O

ct-0

3Ju

l-04

Ap

r-05

Jan

-06

Oct

-06

Jul-0

7A

pr-

08Ja

n-0

9O

ct-0

9Ju

l-10

25

The Question of Florida Recovery When?

We may just be hitting bottom now Some signs of stabilization/uptick

How? Yesterday’s model won’t work tomorrow (growth

fueled by low-cost housing and loose mortgages) Central Florida Especially Vulnerable

Less economically diverse than S. Florida 30% of the state’s job losses in I-4 corridor I-4 is the only major artery linking the Tampa and

Orlando markets

26

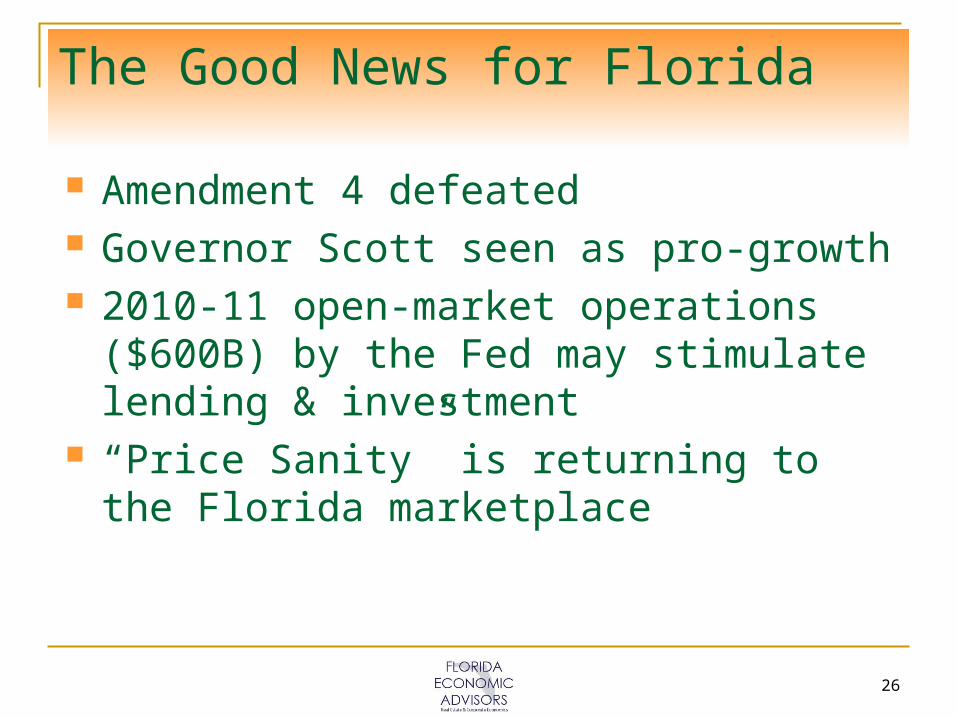

The Good News for Florida

Amendment 4 defeated Governor Scott seen as pro-growth 2010-11 open-market operations ($600B) by

the Fed may stimulate lending & investment “Price Sanity” is returning to the Florida

marketplace

27

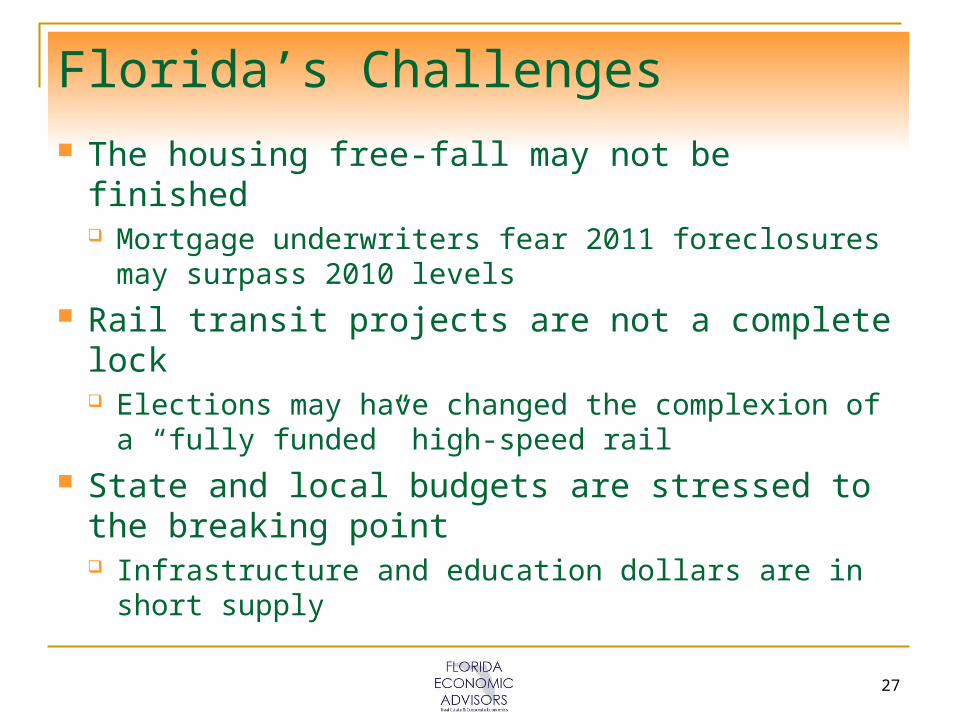

Florida’s Challenges

The housing free-fall may not be finished Mortgage underwriters fear 2011 foreclosures

may surpass 2010 levels Rail transit projects are not a complete lock

Elections may have changed the complexion of a “fully funded” high-speed rail

State and local budgets are stressed to the breaking point Infrastructure and education dollars are in short

supply

28

Florida Recovery North v. South

Southeast Florida’s more diversified economy will recover before the rest of the state

SW and Central Florida, heavily dependent on real estate and population growth, will continue to sputter through late 2011

Unemployment around 10.5 percent by early 2012 The “New” Normal

Slower growth in traditional economic sectors Future prosperity reliant on further diversification

of the economic base