thai study white paper final - bonsucro | home page · pdf fileppp: public-private...

TRANSCRIPT

WHITEPAPER

THAISUGARCANESECTOR&SUSTAINABILITY

PhengkhouaneManivong

EmmanuelleBourgois

FairAgoraAsiaCoLtd

www.fairagora.com Drive Change. Create Value. 2

TABLEOFCONTENTS

TABLEOFCONTENTS..............................................................................................................................................2

ACKNOWLEDGEMENTS......................................................................................................................................2

GLOSSARY...............................................................................................................................................................4

EXECUTIVESUMMARY...........................................................................................................................................5

THAISUGARCANESECTORANDSUSTAINABILITY..................................................................................................7

1. METHODOLOGY................................................................................................................................................7

1.1MARKETRESEARCHANDANALYSIS..............................................................................................................7

1.2 STAKEHOLDERENGAGEMENT.....................................................................................................................8

2. SUGARCANEPRODUCTIONINTHAILAND.........................................................................................................9

2.1.SUGARCANECULTIVATION..........................................................................................................................9

2.2ETHANOL....................................................................................................................................................12

3. SUGARCANEPROCESSINGINTHAILAND........................................................................................................13

3.1SUGARCANEMILLS.....................................................................................................................................13

3.2CRUSHINGCAPACITY..................................................................................................................................14

4. THESUGARCANESECTORINTHAILAND.........................................................................................................15

4.1ORGANISATIONOFTHESUGARCANESECTOR...........................................................................................15

4.2WTOCOMPLAINT.......................................................................................................................................18

4.3CONSUMPTIONANDTRADE.......................................................................................................................19

5. STAKEHOLDERCONSULTATIONONSUSTAINABILITYINSUGARCANE............................................................23

5.1SUGARCANEPRODUCTION–FARMLEVEL.................................................................................................23

5.2SUGARCANEPROCESSING–MILLLEVEL....................................................................................................25

5.3SUGARCANETRADING................................................................................................................................27

5.4SWOTFORSUGARCANESUSTAINABILITY..................................................................................................29

6. CONCLUSIONSANDRECOMMENDATIONS.....................................................................................................33

7. REFERENCES....................................................................................................................................................34

8. APPENDICES....................................................................................................................................................35

AppendixA:Questionnaire–English&Thaiversions......................................................................................35

AppendixB:Focusgroupdiscussion–Invitationandoverview.......................................................................39

AppendixC:Thailand'sexportsofrawsugar(MTRV)......................................................................................40

AppendixD:Thailand'sexportsofrefinedsugar(MTRV)................................................................................41

AppendixE:Rainfalldata,2011-2015.............................................................................................................42

AppendixF:CaneburninginThailand..............................................................................................................43

AppendixG:Workshopnotes-FairAgorasessioninBonsucroTechnicalWeek.............................................44

ACKNOWLEDGEMENTS

www.fairagora.com Drive Change. Create Value. 3

Co-ordinatedbyBonsucro,thisstudywasinitiatedandfundedbyPepsiCowithsupportfromCorbion.

Wewouldliketothanktherespondentsandintervieweeswhosharedtheirexperienceandexpertisethroughoutandhelpedthisreporttoreflecttheviewsofstakeholdersacrossthesugarcanesector.

Pleasenote that the interpretationsand text in thisdocumentare thoseof theauthoranddonotnecessarilyreflecttheviewsoropinionsofBonsucrooritsmembers.

www.fairagora.com Drive Change. Create Value. 4

GLOSSARY

AEC:ASEANEconomicCommunity

AFTA:ASEANFreeTradeAgreement

ASEAN:TheAssociationofSouthEastAsianNations

CCS:CommercialCaneSugar

EIMP:EnvironmentalInformationandMonitoringProgram

MOAC:MinistryofAgricultureandCooperatives

MT:MetricTonne

MTRV:MetricTonsRawValue

OCSB:OfficeoftheCaneandSugarBoard

PPP:Public-privatepartnerships

RID:RoyalIrrigationDepartment

TCSC:ThaiCaneandSugarCompanyLimited

www.fairagora.com Drive Change. Create Value. 5

EXECUTIVESUMMARY

ThiswhitepaperwaswrittentoprovideBonsucroandotherstakeholderswithtop-lineinformationregardingtheThaisugarcaneindustrybasedonup-to-datemarketintelligence,technicaldata,andrelevantgovernmentpolicy.Thedatacollectedinthereportwasfurthercontextualisedthroughfocusgroup discussions and interviews with representatives from the sugarcane industry, non-profitorganisations,academicinstitutionsandgovernmentsectorsofThailand,aswellasanonlinesurvey.Aspartoftheconsultation,stakeholdersidentifiedsomeofthesocial,economic,andenvironmentalchallengesintheThaisugarcaneindustry,aswellaskeyopportunitiesfordrivingthesustainabilityagendaforwardusingtheBonsucroProductionStandardasareferencepoint.

MarketOverview

Sugarcane is one of Thailand’smost important agricultural crops and critical to its economy. Thesugarcane supply chain - consisting of the growers, millers and associated logistics personnel -provides jobs for more than 1.5 million people and generates almost $6 billion USD per year.Additional revenue isgenerateddownstreamthroughtheuseofby-productsandexcessmaterialsfromthesugar industry intheformofethanol,biomasselectricity,paperpulp, fertiliserandotherproducts.

TheThaisugarindustryishighlycompetitive,bothdomesticallyandintheworldmarket.Fordecades,governmentalpolicieslikeTheCaneandSugarActsupportedtheindustryandhelpedtostabilisethesector,enablingsugarcanemillstomaintaintheirprofitabilityevenduringtimesofdepressedsugarpricesintheworldmarket.Morespecifically,thequotasystemguaranteestheavailabilityofsugarfordomesticconsumption,andthegovernmentprovidesamechanismforthefairdistributionofincomebetween cane growers andmillers—70% and 30%, respectively. The domestic price is capped toensurethesteadysupplyofsugarfordomesticconsumptionaswellasincomefortheindustryandcanegrowers.

At theproduction level, costs (excluding transportation) inThailandaregenerally lower than theircompetitors and the seasonofproduction (November toApril) reduces competition in theexportmarket.However,Thaisugarcanemillsarefacedwithhighvariationinoutputduetoclimatechange.GiventhatThaicaneareasarerain-fedwithonly10%inirrigatedzones, it isprojectedthatseveredroughtwillcontinuetocausedamagetothesugarcaneinthenext2years.

Itisyettobeseenifthesystemwillcontinuetohavethesameeffectontheindustry.

Exports

Aftertwodecadesofconsiderablegrowthintheexportmarket,Thailandnowexportsasmuchas70-75% of total domestic sugar and is theworld’s second-largest exporter after Brazil.Major exportdestinationsarewithintheASEANmarketswhereThailandisabletobenefitfromlowertariffsduetothe free trade agreement and lower transportation costs due to the proximity of major exportdestinationslikeIndonesiaandChinawheredemandsforimportedsugarareincreasing.

Challenges

However, beyond these advantages, new challenges are arising for modern and sustainableagriculture,withagrowingneedtomonitorandimproveenvironmentalsustainability,socialimpact,andeconomicperformance.Atthesametime,limitedlawenforcementremainsachallenge,aswell

www.fairagora.com Drive Change. Create Value. 6

as limited environmental and social monitoring at the farm level (e.g. Health & Safety, labourregulations,biodiversityandecosystemimpactsincludingEnvironmentalInformationandMonitoringProgram(EIMP)/Nitrogen&Phosphorus(N&P)/Agrichemicals).Atasystemlevel,littleglobalresearchontheeconomicsandtechniquesofcanegrowingimpedestheemergenceof innovativeandwell-balancedsolutionsforeachofthevarioustypesoffarmers.

RecommendationsBonsucrooffersalogicalframeworktomeasureenvironmental,socialandeconomicindicatorsandthrough its collaborativeplatform,helps facilitatea comprehensivevalue chainapproach toallowgrowers,producersandbuyerstospeakthesamelanguageusingcomparablemetricsandtoolstomeasureandmonitorperformance.Asmoresugarcanestakeholdersusetheframework,theabilitytomonitorenvironmental,social,andeconomicoutcomesfromthesugarcanesectorwill improveandbecomeeasierforstakeholderstouse(andreferto).Actionsidentifiedashavingthepotentialtopositivelyaffectthesugarcanesectorare:

ü Mechanisationofharvestü Dedicatedinvestmentschemesforimprovementü Environmentalmonitoringandmanagementü Increasedeconomicresearchandfinancialriskmodellingü Farmertrainingingoodagriculturepracticesanddatacollection

Tomaximisethepotentialofthesectorandimplementchanges,corecapacitybuildingprogrammesareneededtobuildindustryknowledge,withfinancialmechanismsputinplacetoenableinvestment.Access to loansor other financial tools (or incentives) are also needed to supportmechanisation,irrigation and/or the adoption of other technologies to drive improved quality and productivityincluding innovative incentives directed towards farmers andmillers to reduce the environmentalfootprintofsugarcane.

Improvedstakeholderengagement:governmentandfarmers

To address some of the biggest challenges in the sugarcane industry, greater engagement andcollaborationisneededacrossthesupplychain,andwiththeGovernmentofThailandandfarmersinparticular. In relation to the Government, stakeholders informed that better policy and technicalsupportwasneededSpecificareasofsupportrequiredfromgovernmentincluded:

ü Evaluatingwaterquantityuseandpermittingcapacitytoprovidesufficientwatersupplieswithoutdrainingaquiferreserves.;

ü Supportingfinancialmechanismsforinvestments;ü Implementingmonitoringmechanismsfrombothproductqualityperspectiveaswellas

humanresourceandsocialaspects;andü Restricting/banningtheburningofcane,withfinancialsupportformechanisationprovided.

To achieve these ambitions, farmers need to adopt new, more sustainable farming practices —somethingthattheyareoftenslowindoingbecauseofthepotentialriskinvolved,thelackoftechnicalknowledgeand/orability to invest in required inputs.Thedevelopmentofapilotor testgroupoffarmers was recommended as the best way to demonstrate impact, with farmers collecting andcommunicatingoutcomesalongtheway.AnylessonslearnedwiththepilotgroupcouldthenbeusedtoscaletheadoptionofsustainablepracticesalongwithotherBonsucroimprovementprogrammes.

www.fairagora.com Drive Change. Create Value. 7

THAISUGARCANESECTORANDSUSTAINABILITY

Thiswhite paper provides a high-level overviewof the Thai sugarcane industry and identifies keyopportunitiesfordrivingthesustainabilityagendaforwardusingtheBonsucrostandardasareferenceframework. It isbasedondatacollected fromadesktop reviewofup-to-datemarket intelligence,technical data, and government policy, as well as from insight acquired through stakeholderengagementintheformofinterviews,focusgroupdiscussionsandquestionnaires.

1. METHODOLOGY

1.1MARKETRESEARCHANDANALYSIS

Marketresearchwasbasedonadesktopreviewofup-to-datemarketintelligence,technicaldata,andrelevant government policy, including available literature on social, environmental and economicaspectsofsugarcaneproductioninThailand.1

Table1-Objectivesofthewhitepaperstudy

Identificationofkeystakeholders

• Keystakeholdersin/outsideThailandidentifiedandinvitedtoparticipateininterviews,focusgroupdiscussionsand/orquestionnaire.

• Criteriaforselection–abilitytoenable/influencethesectorinrelationtosustainableperformance:environmental,social,andeconomicimpacts.

Thaisugarcanemarketanalysis

• Nationalsignificanceofsugarcaneinrelationtoemployment,GDP,landarea,foreignexchange,wateruseandimpact,aswellasotherpotentialissuesofimportance.

• Economicperformanceofmillinggroupsandfarmers(high-levelassessment),specificallyfarmerlivelihoods(annualincome),inputoptimisationandcosts(e.g.fertiliserandpesticideuse),aswellasfarmproductivityanddiversification.

• GeopoliticalfactorsandotherrelatedissuesaffectingSouth-eastAsiancountries,includingpotentialimpactsoftheASEANfree-tradeagreement.

Considerationofkeysustainabilityfactors

• Keydriversaffectingthesugarcanesectorinrelationtosocial,environmentalandeconomicfactorsofproduction/processing;

• GapanalysisofmainsustainabilityindicatorsasdefinedintheBonsucroProductionStandard(sixmainprinciples).

• Outlookonthepotentialexpansionofsugarcaneintonaturalhabitats,areaswherelandtenureconflictsexist,andarablelandwheresugarcanewillcompetewithothercrops.

1ResearchwasconductedinFebruary2017.

www.fairagora.com Drive Change. Create Value. 8

1.2 STAKEHOLDERENGAGEMENT

Tohelpcontextualisetheinformationacquiredthroughthedesktopreview,keystakeholderswiththeability to enable and/or influence the sugarcane industry in relation to social, environmental andeconomic performance were identified and invited to participate in interviews, focus groupdiscussions,and/orquestionnaires.AnadditionalworkshopsessionwasincludedaspartofBonsucro’sTechnicaltrainingweekinThailand,withcommentsintegratedintotheconsultationfeedback.

Thoseparticipating in theconsultation includedrepresentatives fromthesugarcane industry,non-profit organisations, academic institutions and government sectors of Thailand. Information andinsightacquired through thisprocesswerecritical for identifyingandanalysingkeyaspectsof thesugarcane industryandusedto identifyvarioussocial,economic,andenvironmentalopportunitiesandchallengesintheThaisugarcaneindustryatthefarm,millandmarket(trade)level.

A) Questionnaire

Inearly2017,aquestionnaireonsustainabilityintheThaisugarcanesectorwasdraftedandcirculatedonlineinThaiandEnglishtokeystakeholderslocatedinandoutsideofThailand(AnnexA).Theaimofthequestionnairewasto:ü Engage with selected representatives from industry, not-for-profit organisations, and

Governmentalagencies;ü Exploreopportunitiesandchallengesinsustainability(andimplementation)inThailand;andü Identifygapsandkeydriversaffectingthesugarcanesectorinrelationtosocial,environmental

andeconomicissues.

Atotalof24questionnaireswerereturnedandtoencourageopenfeedback,theywereanonymous.

B) Focusgroupdiscussions

Inparallelwiththequestionnaire,severalfocusgroupdiscussionswereorganisedwith32participants(seeAppendixB).Forthoseunabletoattendthepre-scheduledfocusgroup,eitheraspecificfocusgroupwasorganisedorindividualinterviewswereset,inpersonoroverthephone.Arangeofparticipantswasselectedtoreflecttheviewsfromacrossthesugarcaneindustryaswellaskeystakeholdergroupsfromthefollowing:ü Sectorrepresentativesandindustryexperts(16peoplefrom11organisations),bothrelatedand

non-relatedtothesustainabilityarea;ü Not-for-profit representatives (8 people from 3 organisations) with strong involvement and

knowledgeofthesector;and,ü Governmentalagenciesrepresentatives(8peoplefrom5organisations),includingthosefrom

academiaandresearchinstitutions.

C) Technicalweekworkshop

InMay 2017, FairAgora facilitated a workshop session with participants from Bonsucro’sTechnicaltraininginThailand.2TheaimwastopresentfindingsofthisWhitePaperaswellastogetinputonthekeychallengesandopportunitiesfacingmillsandfarmsinThailand,plus

2 Technicalweekwasheld fromMay22 toMay27 inThailand (2017). TheFairAgoraworkshopwason theafternoonofMay26.

www.fairagora.com Drive Change. Create Value. 9

recommendationsforactionstobetakenbyBonsucro(andotherstakeholders)toaddress.These opportunities and challenges were then framed in the context of Bonsucro’sProductionStandardtobetterunderstandthelevelofreadiness(orcompliance)atmillandfarmlevel. Intotal,20participants fromthetechnical trainingattendedtheworkshop(18wererepresentativesofthesugarcaneindustry–primarilymills;alongwithonefarmerandaconsultant).

2. SUGARCANEPRODUCTIONINTHAILAND

2.1.SUGARCANECULTIVATION

InThailand,sugarcaneiscultivatedin47provincesandcoversabout8%ofthetotalagriculturalland.3Productionisdividedinto93%oftheplantationforcrushingatthesugarmilland7%oftheplantationforseedlings4forfieldplantingandplantingareaisincompliancewiththeNotificationoftheOCSB.5

Thesugarcanecropcyclevariesbyregiondependingonthevarietyofcaneplantedaswellastheregionofproduction.Forexample,sugarcanegrowersinthenorth-easternregionplanttheircaneinOctober or November,while in the eastern and central regions, planting is in fromNovember toFebruary.Ittakesanywherefrom10to14monthstosugarcanetomatureforharvesting.

Figure1-LocationofsugarcanegrowingareasandsugarcanemillsinThailand(2016).

Source:Sugarcaneproductionannualreport2016,OCSB.

3Exactareaundersugarcanecultivationis1,776,264ha.AgriculturallandofThailand:24millionha(47%ofCountry’stotalland)42016OCSBSugarcaneproductionreport5OCSBNotifications-TheZoningofSugarcaneCultivationandtheNotificationofNationalEnvironmentBoardNo.25entitledSoilQualityStandards.

www.fairagora.com Drive Change. Create Value. 10

A) Zoning

In 2012, the government of Thailand initiated the “Agricultural Crop Zoning system”, whichestablisheddifferentagriculturalproductionzonesbasedonseveralfactors,suchaslandsuitabilityfactors (soil,water, and sunlight), existing land use, crop requirements, andmarket demand. Thezoningpolicyencouragedfarmerstoswitchfromricecultivationtotheproductionof‘cashcrops’suchascassava,palmoil,sugarcane,maize,etc.inordertosupportbioethanolproduction.6Eventhoughthe area planted with rice has decreased as a result of the policy, Thailand remains the biggestproducerandexporterofriceworldwide.

Figure2-MaincommercialcropsofThailandSource:OfficeofAgriculturalEconomics

Therelativelyhighpriceofsugarcanecomparedtoothercropsmadeitmoreattractivetofarmers,resultinginasignificantexpansionofsugarcanecultivationbyanaverageof8%peryearsince2010.

B) Farmsize

Themajorityof sugarcane farmsaresmallandmediumfarms,52%and31%, respectivelywithanannualproductioncapacityfromabout1,000to2,000MT.Only17%offarmsareconsideredlarge,with theirannualproductionmore than2,000MT.Nearlyhalfof thesmall sugar farmsare in theNorth-easternregion,whichisanewlocationforsugarcaneplantations.

Table2-SugarcaneproductionbyfarmsizeandregioninThailand(2014)

Typology Plantedarea(ha)

Productioncapacity(MT/year)

Sugarcanefarmersbyregion Total(bytypologies)Northern Central Western North-

easternSmall <10 >1,000 45% 47% 21% 67% 52%Medium 10-32 1,000-2,000 40% 35% 44% 20% 31%Large >=32 >2,000 15% 19% 35% 13% 17%

Total(byregions) 22% 33% 6% 39% 100%Source:SurveyofKhonKhaenUniversity,2014.

6Governmentpolicy&EnvironmentalsustainabilityandclimatebenefitofgreentechnologyforbioethanolproductioninThailand,KawasakiETAL,2015

www.fairagora.com Drive Change. Create Value. 11

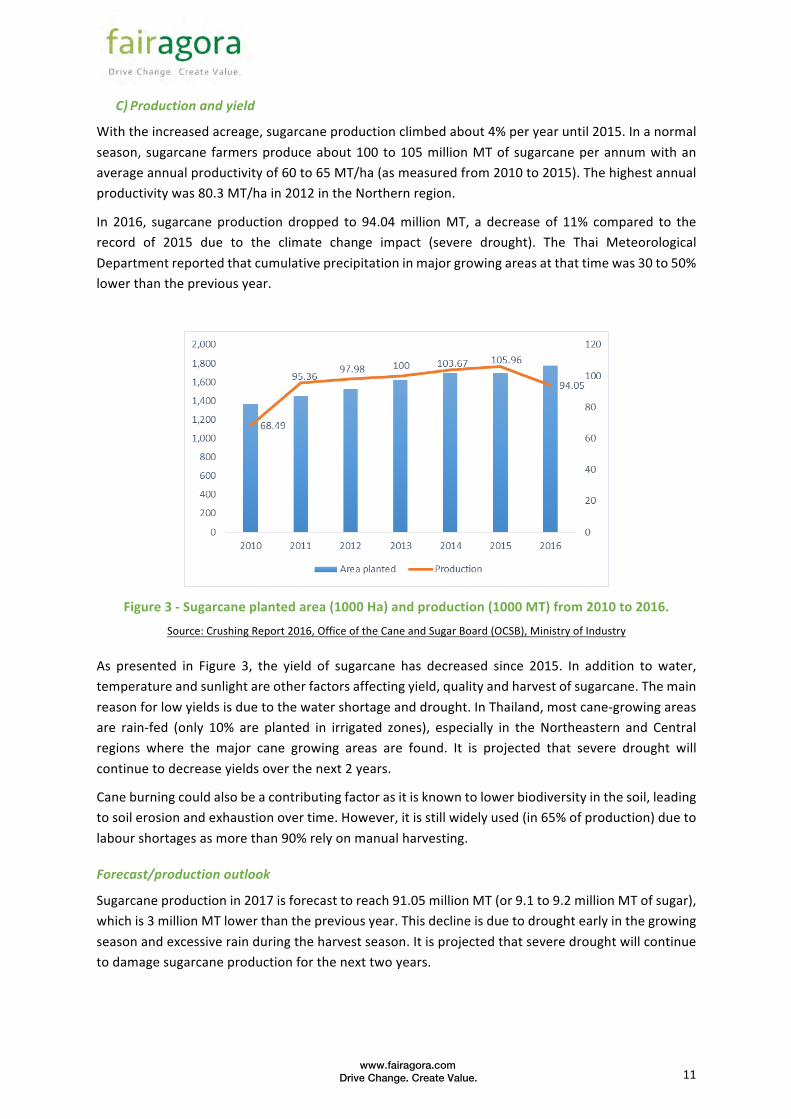

C) Productionandyield

Withtheincreasedacreage,sugarcaneproductionclimbedabout4%peryearuntil2015.Inanormalseason,sugarcane farmersproduceabout100 to105millionMTofsugarcaneperannumwithanaverageannualproductivityof60to65MT/ha(asmeasuredfrom2010to2015).Thehighestannualproductivitywas80.3MT/hain2012intheNorthernregion.

In 2016, sugarcane production dropped to 94.04millionMT, a decrease of 11% compared to therecord of 2015 due to the climate change impact (severe drought). The Thai MeteorologicalDepartmentreportedthatcumulativeprecipitationinmajorgrowingareasatthattimewas30to50%lowerthanthepreviousyear.

Figure3-Sugarcaneplantedarea(1000Ha)andproduction(1000MT)from2010to2016.

Source:CrushingReport2016,OfficeoftheCaneandSugarBoard(OCSB),MinistryofIndustry

As presented in Figure 3, the yield of sugarcane has decreased since 2015. In addition towater,temperatureandsunlightareotherfactorsaffectingyield,qualityandharvestofsugarcane.Themainreasonforlowyieldsisduetothewatershortageanddrought.InThailand,mostcane-growingareasare rain-fed (only 10% are planted in irrigated zones), especially in the Northeastern and Centralregions where the major cane growing areas are found. It is projected that severe drought willcontinuetodecreaseyieldsoverthenext2years.

Caneburningcouldalsobeacontributingfactorasitisknowntolowerbiodiversityinthesoil,leadingtosoilerosionandexhaustionovertime.However,itisstillwidelyused(in65%ofproduction)duetolabourshortagesasmorethan90%relyonmanualharvesting.

Forecast/productionoutlook

Sugarcaneproductionin2017isforecasttoreach91.05millionMT(or9.1to9.2millionMTofsugar),whichis3millionMTlowerthanthepreviousyear.Thisdeclineisduetodroughtearlyinthegrowingseasonandexcessiverainduringtheharvestseason.Itisprojectedthatseveredroughtwillcontinuetodamagesugarcaneproductionforthenexttwoyears.

www.fairagora.com Drive Change. Create Value. 12

2.2ETHANOL

The majority of sugarcane in Thailand is used for sugarproductionbutasmallamount–rangingfrom1to6%-isusedforethanolproduction,whichvariesannuallydependingonworld sugar prices and relative profitability of sugar overethanol. This accounts for around 30% of total ethanolproductioninThailand.

Thai producers have a production capacity of around 4.44millionlitresofethanolperday.Ethanolproductionin2014was1,058.3millionlitres,an11.5%increasefrom2013.

Presently,thereare24ethanolproductionplantsinThailand.These plants produce ethanol from sugar,molasses, and cassava. The registered daily productioncapacity is about 5.04 million litres and the actual production is 4.4 million litres. The ethanolproductionfromsugarjuiceandmolassesis2.3millionmetrictonnesperday,whichismanagedby11ethanolprocessors.

A) Domesticconsumption

Ethanol consumption jumped to 3.2million litres per day in 2014, up 23.1% from 2013. Ethanolconsumptionreached3.5millionlitresperdayinthefirstfourmonthsof2015-9.4%greaterthanthesameperiodayearearlier.Theproductionofethanolisprojectedtorisebecausedemandisgrowing.

Table3-Ethanolconsumption(millionlitres/day)2013-2015

Year Ethanolconsumption(millionlitres/day)

Ethanolproduction(millionlitres)

2013 2.6 936.52014 3.2 1,058.32015 3.5 405.3

(YTD-April2015)Source:DepartmentofAlternativeEnergyDevelopmentandEfficiency(DEDE)

B) Gasohol

Theuseofethanolasafuelisexpectedtogrowcontinuouslyduetosupportivegovernmentpoliciesthat encourage people to use alternative fuels. Ethanol, when blendedwith gasoline in differentproportions,iscalledgasohol.GasoholusedinvehiclesinThailandcomesinthreegrades:E10(a10:90mixture of ethanol and gasoline), E20 (20:80), and E85 (85:15). The retail price of gasoline forautomobilesinThailandishigherthanthepriceofgasoholbecausethepriceofgasolineincludesahighercontributiontotheOilFund.BytheendofJune2015,theE20gasoholpricewas23.5%cheaperthangasoline.ThedemandforgasoholandethanolrosesignificantlysinceJanuary2013afterthesaleof91-octanegasolinewasbanned.

Molasses

Molassesiscommercializedbothforthedomestic and export markets. For thedomestic market, molasses is used invarious industries, such as liquordistilleries, monosodium glutamateproduction, ethanol production, animalfeed industry, and other industries.Thailand mainly exports molasses toSouthKorea,Vietnam,andTaiwan.

www.fairagora.com Drive Change. Create Value. 13

3. SUGARCANEPROCESSINGINTHAILAND

3.1SUGARCANEMILLS

SugarcanemillsinThailandemployanestimated50,000workersin 27different provinces. Themajority (nearly 75%) are in theCentral and North-eastern regions (see Figure 4). There arecurrently 55 OCSB registered sugarcane mills operating inThailand.7Thesemillsareownedandoperatedby22companies.The top5 companiesproduceover60%of themarket shareofsugarsold inthedomesticmarketundertheQuotaAallocation(whitesugarfordomesticconsumption).

TheMitrPholandThaiRoongRuangGrouparethelargestoftheprocessor companies, accounting for 20% and 14% of totalproductioncapacityofsugarinthecountry,respectively.Botharealsomajorexportersofsugarandranked3rdand4thofallsugarexportersintheworldmarket.8

• MitrPhol-6sugarcanemillsinThailand,alllocatedintheNorthernregion.Allmillshaverefineriesattachedandproducewhitesugarwithatotalprocessingcapacityof130,500MTofsugarcanedaily,yieldingasugaroutputofapproximately2MTperyear.MitrPholoperatesglobally,with10additionalmillsin4countries.9

• ThaiRoongRuangGroup-9sugarcanemillsinThailand,2ofwhichwererecentlyestablishedin2015and2016.Allmillshaverefineriesattachedandproducewhitesugar,withacrushingcapacityof264,435MTofsugarcanedaily.Theyieldingsugaroutputisapproximately2millionMT.

7Fournewplantswereestablishedin2016:twosugarmillsbytheThaiRoongRuangGroupand2othernewmillswiththetotalcrushingcapacitiesof40,000MTofcaneperday.8WorldTopExport,2016.9MitrPholoperates7sugarmillsinChinaand1sugarmillineachofthefollowing,LaosPDR,andAustralia(inpartnershipwithMSFSugarLimited).

Companyname Numberofmills

Annualcrushingcapacity

(MTofsugar)1 MitrPholGroup 6 20.682 ThaiRoongRuangGrou 7 15.193 ThaiEkalakGroup(KTIS) 3 9.84 TamakaGroup(KSL) 5 8.755 KorachGroup 2 5.846 RermUdomGroup 2 5.727 WangKanaiGroup 4 5.458 SuphanburiGroup 1 5.259 BanpongGroup 4 4.2610 KumpawapiGroup 2 3.811 KamPangPetchCo.,Ltd. 2 3.5512 ThaiKanchanaburi 2 3.1613 MitrKasetrGroup 2 2.3514 PrachuapSugarIndustryCo.,Ltd 1 2.2915 RajburiSugarCo.,Ltd. 1 2.1516 PranburiSugarIndustryCo.,Ltd. 1 1.9517 EasternSugar&CanePublicCo. 1 1.3618 RayongSugarCo.,Ltd. 1 1.2619 KhonburiSugarPublicCo.,Ltd. 1 1.0320 SaharuangCo.,Ltd. 1 1.0121 E-SaanSugarIndustryCo.,Ltd. 1 0.5922 BurirumSugarPublicCo.,Ltd. 1 0.52

Total 51 105.96

Table4-Thaisugarprocessorsandcrushingcapacity(2015)

Figure4-Sugarcanemillsbyregions(2015).

www.fairagora.com Drive Change. Create Value. 14

3.2CRUSHINGCAPACITY

TheaverageannualcrushingcapacityofsugarcanemillsinThailandisbetween100to106millionMTofsugarcane(orequivalenttosugaroutputof10to11millionMT).Theextractionrateisbetween100to108kgofsugarperMTofsugarcanewithanaverageof104.73kgofsugarperMTofsugarcane.

Table5-YieldofSugarcaneandsugar(2007–2016)

Year Sugarcaneproduction(millionMT)

Sugarproduction(millionMT)

Extractionrate(kgsugar/tcane)

C.C.S(%)

2007 63.79 6.72 105.33 11.912008 73.31 7.80 106.63 12.102009 66.46 7.19 108.13 12.282010 68.48 6.93 101.17 11.582011 97.98 10.24 104.47 12.042012 95.36 9.66 101.33 11.782013 100.00 10.02 100.24 11.642014 103.67 11.33 108.94 12.562015 105.96 11.34 107.01 12.232016 94.04 9.78 104.05 11.95

Source:Crushingreport2016,OCSB,MinistryofIndustry

In2016,sugarproductiondroppedsignificantlyfrom11.34millionMTto9.78millionMTduetothedecreaseinsugarcaneproduction.Theextractionratewasalso2.7kglessat104.05kgofsugarperMTofsugarcane,(approximately3%lower)duetothedryweatherconditions.

Forecast/outlook

Under the 10-year Cane and Sugar Strategy (2015 – 2026), the Thai government approved theconstructionof13newsugarcanemills in2016andallowedtheexpansionof6existingsugarcanemills.Theexpansionisexpectedtoincreasetheproductioncapacityby466,300MTofsugarcaneperday,leadingtoadailycapacityofatleast1.1millionMT.

www.fairagora.com Drive Change. Create Value. 15

4. THESUGARCANESECTORINTHAILAND

4.1ORGANISATIONOFTHESUGARCANESECTOR

ThesugarcanesectorandsugarindustryinThailandhavebeenhighlyregulatedbythegovernmentsince the approval of the Cane and Sugar Act in 1984 (B.E. 2527). This Act aims tomaintain theeconomicstabilityofthecountryandsafeguardtheinterestsofsugarcanefarmersintheproductionanddistributionofsugarcane.Thecontinuedgrowthandstabilityofthesugarindustryensuresregularincomes to cane growers and sugar mill owners while providing price stability to consumers. Inaddition,itallowssugarcanemillstomaintaintheirprofitabilityevenduringtimesofdepressedsugarpricesintheworldmarket.UnderthisAct,varioussupportmeasureshavebeenputinplacethroughtheOfficeoftheCaneandSugarBoard(OCSB)undertheMinistryofIndustry,amediationbodytobridgesugarcanegrowersandsugarcanemills.

ThemainfeaturesoftheCaneSugarActincludethecontrolofsugarcaneproduction,theallocationofsalesquotas,thesettingofpricesforsugarcaneandsugar,andarevenuesharingsystem(describedbelow).

A) Controlofsugarcaneproduction

Currently, there are 336,851 sugarcane growers (or planters) which belong to 33 sugarcaneassociations.Allsugarcaneplanterswhowishtoselltheirproducetoasugarmillmustbeformally

Table6-Expansionofsugarcanemillsandcapacities(2016-2021)

www.fairagora.com Drive Change. Create Value. 16

registeredasa“sugarcaneplanter”bytheOCSB.Themajorityofsugarcaneplanter’sassociations(27of 33) fall into one of three sugarcane federations. The remaining 6 associations operateindependently (Figure 2). At the end of the supply chain, there are 7 sugar trading companiesoperating both as traders and shippers and aregroupedunderatradeassociation.

Allsugarcanegrowerassociationsmustfullymeettheregistrationcriteria:

(i) consistofatleast600members,and(ii) supplyatleast55%oftheirproductiontoa

sugarmill.

Sugarcane mills and traders must be licensed tooperate.InApril2015,anewrequirementforfactorylicensing was announced as part of a governmentprogramme to increase capacity by increasing thenumberofmills.Theminimumdistancebetweennewandexistingsugarcanemillswasrevisedfrom80kmto50kmandtheconstructionofanynewsugarmillmustbecompletedwithinfiveyears.TheregistrationismanagedbyadifferentbureauoftheOCSB.

Figure5-OrganisationofThaisugarcanesectorbyplanters,millsandtraders

B) Contractfarming

InThailand,onlyafewsugarcanemillsoperateandowntheirownplantations,withthemajoritysourcingfromcontractedsugarcanegrowers.Ingeneral,thesugarcanemillssupportthecontractedfarmersintermsofinputs(canevarietiesandfertilisers),farmequipmentandmechanisationservices,andshort-termfinancing.Thegeneralpracticeisforsugarcanemillstosignacontractwiththeleader(orquotahead)forthesugarcanegrowers.Thequotahead,whoisoftenasugarcanegrowerwithalargecanearea,supervisesthecaneprovidedbysugarcanegrowersinhisnetwork(orlookrai).Thenumberofcontractsissuedbythemillsrangesfrom2to77quotaheadspermillwithanaverageof50quotaheads.

C) Allocationofsalesquotas

Sugarisacategorisedasacontrolledgoodundergovernmentalregulations.TheOCSBallocatesthequantityofsugarsolddomesticallyandforexportinto3Quotas:Aisforsugarsolddomestically;Bisforexportundertheindustry’slong-termcontracts;andCisforexportundertheindividualexportcontracts-shortertermcontractsallocatedafterAandBarefulfilled.

55SugarcaneMills

SugarMillassociations

Sugartraders Sugartraderassociations

337KSugarcanePlanters

6IndependentSugarcaneGrowers

Associations

27SugarcanePlanter's

Associations

3SugarcanePlanter's

Federations

www.fairagora.com Drive Change. Create Value. 17

Figure6-AllocationofsugarquotasA,BandC.

These quota allocations are intended to control excess sugar output. However, as exports aremeasured in calendar years (January-December) while production is by crop year (October-September)thereisaslightdifferencebetweentheexportquotaandtheactualshipmentvolumes.

D) Settingpricesforsugarcaneandsugar

Thepriceofsugarcaneispre-determinedonanannualbasisbytheOCSBandannouncedinOctober.Beforethestartofsugarproductioneveryyear,theOCSBestimatetherevenuefromthesaleofsugartosettheinitialsugarcaneprice.Thispriceisusedbythesugarmillersasabasisforcalculatingtheinitial pricepaid to sugarcaneplanters.At theendof the sugarproduction cycle,which is usuallyaroundSeptember,theOCSBwillre-evaluatetherevenuefromthesaleofsugarandannouncethefinalsugarcaneprice.Iftheactualfinalprice,basedonactualworldprice,islowerthantheinitialpricesetbyOCSB,theCaneandSugarFundcompensatesthemillersfortheshortfall.However,Ifthefinalsugarcanepriceishigherthantheinitialprice,themillerscompensatethesugarcaneplanters.

ThedomesticsugarpriceisalsocontrolledbytheMinistryofIndustry(viatheOCSB)andtheMinistryofCommerce.TheOCSBestablishesthesugarpriceatthefactorygateandtheCentralBoardpricingof goodsand servicesestablishes the retail priceof sugar. In2016, the factorywholesalepriceofrefinedsugarwas19THB/kg10,excludingthe7%ofVAT.Retailpricesforsugaralsoremainfixedat21.85THB/kg11(includingVAT)forwhitesugarand22.85THB/kg12forrefinedsugar.Thesepricesarehigher than the world price resulting in a competitive advantage for Thai sugar businesses overinternationalcompetitorsinthedomesticmarket.

E) Revenuesharingsystem:

In1984,theOCSBestablishedaprofit-sharingsystembetweensugarcaneplantersandsugarcanemillsat70:30basedonactual income (afterdeductedcostsand taxes) frombothdomesticandexportmarkets.Thisisusedtostabilisecostsarisingfrommilling,transportationandotherassociatedcosts.

10Approximately$0.24USD/lb11Approximately$0.28USD/lb12Approximately$0.30USD/lb

QuotaA:Whitesugarfordomestic

consumptiononly

• TheOCSBestimatestheyearlysugartobeconsumeddomesticallyandthenallocatessugarquotastoeachsugarfactoryinThailand.Asaresult,thesesugarproducerswillnotbeabletosellabovetheregulatedamountofsugargovernedbyOCSB.

QuotaB:Rawsugarforexportonly

(0.8millionMT)

• ThesugarmillshavetodeliverrawsugartotheThaiCaneandSugarCompanyLimited(TCSC),whichiscooperativelyestablishedbyfarmers,sugarmillsandgovernmentofficials.

QuotaC:Raw/white/refinedsugarfor

export(balanceremainingafterallocatingQuotaAandB)

• QuotaCisforrawsugar,whitesugar,orrefinedsugarthatOCSBallowsfactoriestoproduceforexportaftertheallocatedamountofbothQuotaAandBhasbeenfulfilled

www.fairagora.com Drive Change. Create Value. 18

Figure7-Benefitallocationschemebetweensugarcanefarmersandsugarcanemills

Source:KBSAnnualReport,2015.

Thebenefitallocationschemebetweensugarcanefarmersandsugarcanemillsis70:30.Thismeansthat70%oftheindustry’snetprofitisallocatedtosugarcanefarmersand30%tosugarcompanies.Aftertheendofeachproductionseason,QuotaBisdeterminedbytheCaneandSugarBoardandtheExecutiveBoardcalculatesthefinalsugarpricefromthenetprofitthatisaccruedinthatproductionyear.

4.2WTOCOMPLAINT

InApril2016,BrazilchallengedThailand’sprofitsharingsystemwhenitinitiatedconsultationsattheWorldTradeOrganisation(WTO).AccordingtoBrazilianofficials,theprofit-sharingsystem(alongwithexportquotasandhighfixeddomesticprices),isanirregularsubsidythatartificiallyincentivizedtheproductionofsugarduringaperiodofrecordlevellowpricesandbenefittedThailandattheexpenseofotherproducingcountriesandinviolationofglobaltradeagreements.13ThecaseissimilartoonesuccessfullydisputedbyBrazilagainsttheEUsugarregimemorethanadecadeagoin2005forcedtheEUtoreviewitssugarpolicies.

SincetheinitialcomplaintbyBrazil,GuatemalaandtheEuropeanUnionalsojoinedtheprocess.InSeptember2016,Thailandagreedtooverhaulitssugarproductionanditsdistributionsystemforthefirsttimeinmorethanthreedecades.TheOSCBdiscussedtheissuewithBrazilandagreed(inprinciple)torevokeitscurrent70:30profit-sharingsystemandsubsequentlyleadtocancellingitsquotasystemandfloatingdomesticsugarprices.14Althoughthenewlawandregulationsareexpectedtobeappliedtothe2017/18crops,itisnotyetclearwhetherthesemeasureswillbesufficienttopreventtheconsultationattheWTOfrommovingforward.AsofMay2017,theWTOhadnotyetbeennotifiedoftheagreedsolution.

13Availableat-https://www.wto.org/english/tratop_e/dispu_e/cases_e/ds507_e.htm.14Availableathttps://www.internationalsugarjournal.com/thailand-to-reform-its-sugar-regime/

www.fairagora.com Drive Change. Create Value. 19

4.3CONSUMPTIONANDTRADE

SugarconsumptioninThailandisclassifiedasdirectorindirectconsumption.Basedonthe2.6millionMTofdomesticconsumptionin2016,theratiowas52.24%fordirectconsumptionversus47.76%fortheindirectconsumption(usedbytheindustry).Thiswasinthesameproportionasthepreviousyear.

A) Domesticconsumption

Thedomestic consumptionaccounts for25 to30%of the total sugaroutput. The sugarquota fordomestic consumption falls into Quota A: white sugar for domestic consumption only slightlyincreasedfrom2.30millionMTin2012to2.60millionMTin2016,up15%from2012and4%from2015. This is due to growing household and industrial uses and the anticipation of a slightimprovementintheeconomy.

Figure8-SugarusebyindustryinThailand(2016).

Source:USDA:Thaisugarannualreport2016

Forindustrialuses,over90%ofsugarisusedinbeverages(excludingalcoholicdrinks),food,anddairy,at47%,25%and20%,respectively.Otherusesincludeotherdairyproducts,medical(pharmaceuticalproducts),andconfectionaryproducts.

Table7-Allocationofsugarquota(millionMT),2012to2016

Year Totalsugarproduction(millionMT)

QuotaA(1)

(millionMT)QuotaB(2)

(millionMT)QuotaC(3)

(millionMT)2012 10.24 2.30 0.8 7.142013 10.02 2.61 0.8 6.612014 11.33 2.40 0.8 8.132015 11.33 2.50 0.8 8.032016 9.78 2.60 0.8 6.38

(1)QuotaA:whitesugarfordomesticconsumptiononly;(2)QuotaB:0.8millionMTofrawsugarforexportonly(3)QuotaC:balanceremainingafterQuotaAandBforre-export.

Source:CrushingReport2016,OfficeoftheCaneandSugarBoard(OCSB),MinistryofIndustry.

B) ExportMarket

47%

25%

20%

3% 3% 2%

Thailand'sSugarUtilisationbyIndustry

Beverages

Food

Dairy

Medical

Bread&alcohol

Confectionary

www.fairagora.com Drive Change. Create Value. 20

Thailandremainsamajorsugarproducerandistheworld’ssecond-largestexporterafterBrazil.Sugarexportsincreasedfrom7.57millionMTin2014to8.27millionMTin2015,risingby9.24%(mostlyintheformofrawsugarexports).Withthequotasystemestablishedbythegovernment,Thaisugarproductionreliesheavilyonexports-ashighas70to75%oftotalsugaroutput.

Figure9-Thailand'sdomesticconsumptionandexportsofsugar(MT),2010–2016.Source:USDA:Thaisugarannualreport2016

Morethan90%ofThailand’ssugarexportsaresoldtoAsiancountries,resultinginacostcompetitiveadvantageforThailandcomparedtootherglobalexportersmainlyduetopreferentialtermsoftradeundertheASEANFreeTradeAgreement(orAFTA).IneffectsinceDecember2015,AFTAgivesThailandduty-freeaccesstomostASEANmarkets,exceptforthePhilippines(5%dutyonsugarimports)andIndonesia(variablerateof5to10%),andMyanmar(variablerateof0to5%).Thailandalsobenefitsfromlowertransportationcostsduetoitsgeographicallocationandproximitytoexportdestinations.Theoverallcostsavingsamountstoabout15USDperMTcomparedtonon-ASEANsuppliers.

Table8-ThailandExportdataofsugar(milltonnes)2010–2016

Year Rawsugar(milltonnes)

Refinedsugar(milltonnes)

Total(milltonnes)

2010 1.97 2.65 4.622011 4.22 2.66 6.882012 4.92 2.88 7.802013 5.99 3.08 6.792014 3.70 3.14 7.572015 4.43 4.34 8.272016 4.4 0.46 4.86

Source:ThailandSugarannualreport2016,USDA

www.fairagora.com Drive Change. Create Value. 21

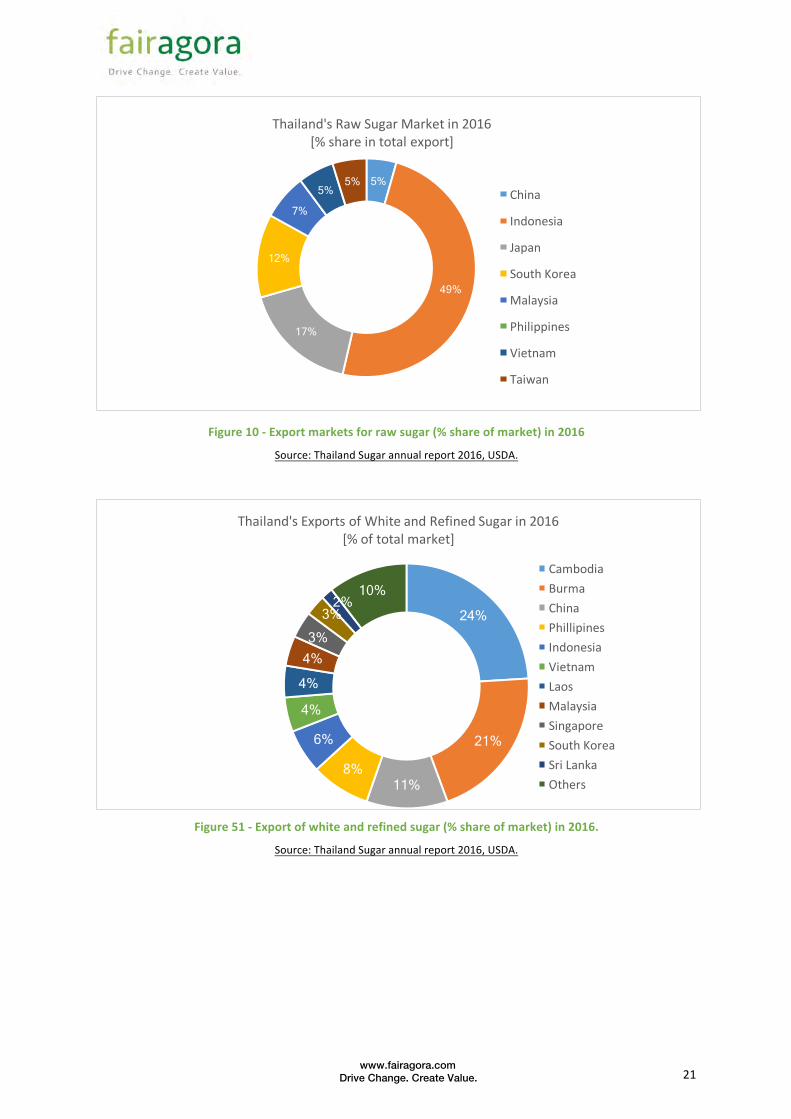

Figure10-Exportmarketsforrawsugar(%shareofmarket)in2016Source:ThailandSugarannualreport2016,USDA.

Figure51-Exportofwhiteandrefinedsugar(%shareofmarket)in2016.Source:ThailandSugarannualreport2016,USDA.

5%

49%

17%

12%

7%

5% 5%

Thailand'sRawSugarMarketin2016[%shareintotalexport]

China

Indonesia

Japan

SouthKorea

Malaysia

Philippines

Vietnam

Taiwan

24%

21%

11% 8%

6%

4%

4% 4% 3%

3% 2%

10%

Thailand'sExportsofWhiteandRefinedSugarin2016[%oftotalmarket]

CambodiaBurmaChinaPhillipinesIndonesiaVietnamLaosMalaysiaSingaporeSouthKoreaSriLankaOthers

www.fairagora.com Drive Change. Create Value. 22

Table9-ASEANsugarbalanceprospectiveto2020(8.5millionMTdeficitperyear).

Source:Thaisugarmillersgroup,2016.

Forecast/outlook

Thailandisinagoodpositionduetoitsstrategiclocation,favourablecommitmentsunderdifferentFree Trade Agreements, and its experience and expertise in the sugar business. According to theThailandindustrialoutlook2016–2018byKrungsriBank,thesugarindustryisexpectedtoimprovegraduallyoverthenextthreeyears,duemainlytothereboundinsugarpricesandasaresultofthefollowingfactors:

• Recoveryofworlddemand:ThedemandofsugarfromIndia(theworld’sbiggestsugarconsumingcountry)isexpectedtoincreaseduetoeconomicgrowth.Inaddition,Asiaisasugardeficitregion,shortof8.5millionMTayear.

• Riseinimports:Themajorconsumers,especiallyinChinaandtheEU,mayincreaseimportsof sugar by 10% per year after the closure of their domestic sugarcanemills. Moreover,concernsovertheexpectedreductioninworldsugaroutputhavealsoinducedmanycountriestoraisesugarimports.Sugarproducersandexporterscouldthenhavemorebargainingpowerintheworldmarket.

• Slowdowninsupply:Itisexpectedthattheworldsugarsupplywillgraduallydecreasealongwith the trend of decliningworld sugar prices during the next several years. Additionally,turbulentweatherchangeshavediscouragedtheexpansionofsugarcaneplantationareas.Itisestimatedthatworldsugaroutputcoulddecreasebyanaveragerateof3-5%peryear.

• Continuingethanolproduction inBrazil:Theproductioncapacitythathasbeenkeptat thesame level has helped maintain demand for sugarcane which in turn results in a highsugarcaneprice(acostofsugarproduction).ThishasalsolessenedworriesovertheincreaseofBrazil’ssugarproductionandexports.

Country Sugarproduction(millionMT)

Sugarconsumption(millionMT)

Supply/Demand

Thailand 13.00 3.67 +9.33Philippines 2.60 2.75 -0.15Indonesia 2.8 7.77 -4.97Vietnam 1.7 2.12 -0.42Singapore 0 0.31 -0.31Malaysia 0 2.00 -2.00Myanmar 0.60 0.75 -0.15Cambodia 0.02 0.35 -0.32Laos 0.08 0.83 -0.03Total 20.80 19.80 0.99

www.fairagora.com Drive Change. Create Value. 23

5. STAKEHOLDERCONSULTATIONONSUSTAINABILITYINSUGARCANE

Information and insight acquired through the stakeholder interviews and focus group discussionswere used to identify various social and environmental opportunities and challenges in the Thaisugarcaneindustryatthefarm,millandmarket(trade)level.

Figure12–Sugarcanevaluechainfromagriculturalproductiontoprocessingandtrading.

Outcomes from the stakeholder consultation were used to identify actions needed to move thesustainability agenda forward and to outline key elements for the design and implementation ofBonsucroimprovementprogrammes.Thefindingsarepresentedbyasegmentofthevaluechaininthefollowingsections(Sections5.1-3),includingopportunities,challenges,andrecommendationsforeach,andconsolidatedintoaSWOTchartinSection5.4(seeFigure18).Finally,theresponseswerereviewed in the context of the Bonsucro Production Standard to better understand the level ofreadinessatthemillandfarmlevel.AsummaryofthemainpointsofdiscussionisprovidedinSection5.5withnotesfromthesessionincludedintheAppendixG.

5.1SUGARCANEPRODUCTION–FARMLEVEL

A) Opportunities

Using the information gathered for this white paper, low production costs and the competitiveproductionseasonwereidentifiedastwomainopportunitiestogrowingsugarcaneinThailand.

Opportunities(oradvantages)forsugarcanegrowers:• Lowproductioncosts:Thecostofsugarcane(excludingtransportation)isabout1,049

THB/MT(oraround13.6cents/lb),whichissecondonlytoBrazil’sat11.2cents/lb15.• Competitiveproductionseason:Thailand’ssugarproductionseason(NovembertoApril)isdifferentfromBrazil’s(ApriltoOctober),whichdecreasescompetitionintheexportmarket.

Whenaskedabouttheopportunities(orfutureadvantages)forsugarcanegrowinginThailand(Figure13),around30%ofconsultationparticipantsidentifiedthecompetitiveproductionseasonasonethemainadvantagesbutthemajoritynotedotheraspectssuchasthepotentialexpansionofsugarcanecultivationandfarmertrainingasmoresignificant.

Figure6-OpportunitiesforThailand–Sugarcanegrowing

15ThaiSugarCaneIndustry–KrungsriBank2016-2018Outlook

Sugarcaneproduction(farmlevel)

Sugarcaneprocessing(milllevel)

Sugarcanetrading(marketlevel)

0% 10% 20% 30% 40% 50% 60% 70%

lowproductioncosts

competitiveproductionseason

other

Q.Whataremainopportunitiesinsugarcanegrowing?

www.fairagora.com Drive Change. Create Value. 24

Amongworkshopparticipants,theconsensuswasthatThaisugarcaneisassociatedwithanumberofpositiveattributesthatprovidefarmerswithacertaindegreeoffinancialsecurityandstability.Biophysicalcharacteristicsofsugarcane,likethereplantingcycle(every3to5years)andtherelativelyfavourablegrowingconditionsofThailandwerementionedasthemainadvantages.Millrepresentativesalsoinformedthattheyprovidefinancialsupporttotheirfarmers,usuallyintheformofdirectloansforproductioninputsatthebeginningoftheseason.

Despitetheopportunitiesavailabletothem,themajorityofworkshopparticipantsinformedthatfewopportunities were being fully realised. Examples like the improved use of green fertiliser andtechniqueslikecroprotationwerecitedasbetteragriculturalpracticesthatcouldimproveproduction,but they are not widely implemented. There were also opportunities to diversify, particularly inrelationtosugarcaneby-productsbecausethevaluechainisalreadyorganisedandcoordinated,aswellastheproductionofnewcropslikemaize,tapiocaetc.However,itwasnotedthatadviceandassistancefromagronomistsoragricultureexpertswouldberequiredtodoso.

B) Challenges

Inrelationtochallenges, research indicatedthat therewerethreemain issues facing farmers: lowsugarcaneyields,improperagriculturepracticesandvariablesugarcanequality.

Mainchallengesforsugarcanegrowers:• Lowsugarcaneyield:Mostcaneareasarerain-fedwithonly10%inirrigatedzonesdueto

therelocationofcaneareaintheNorth-easternregion.Someirrigatedareasarefacingwatersupplyissues-severedroughtislikelytocausedamageoverthenext2years.

• Improperagriculturepractices:Canediseaseispartiallyduetoimproperagriculturepractices.Therelianceononlyafewsugarcanevarietiesalsogreatlyincreasestheriskandspreadofdisease.Whenanewvarietybecomespopular,forinstance,itisusedextensivelyinthatarea.Itisthensubjecttoinfectioninalargearea.

• Variablecanequality:Caneburningiswidespread,accountingformorethan60%ofcaneproduction.Themainreasonsforcaneburningarelabourshortagesandmanualharvestingpractices(mechanisedharvestingislessthan10%).TheOCSBencouragesthesugarcanemillstoadoptapremiumpricesystemforthefreshly-cutproduct.

Stakeholdersidentifiedcaneburning(63%)aswellaslowsugarcaneyield(50%)andlabourshortagesasbeingthemainchallengesaffectingsugarcaneproductioninThailand(Figure14).

Figure7-ChallengesforThailand–Sugarcaneproduction.

0% 10% 20% 30% 40% 50% 60% 70%

Q.Whatarebiggestchallengesinsugarcanegrowing?

www.fairagora.com Drive Change. Create Value. 25

Allthreeworkshopgroupsemphasisedtheincreasingcostsofproduction,mainlyintermsoflabourand transportation costs, as factors that reduced profit available for reinvestment back intoproduction(viaproductivityimprovementorsustainabilityinitiatives).Insomecases,thesecostsareperpetuatingbadbehaviour, as illustratedwith theexample that farmerswerecontinuing to loadtrucksover25tons–thelegallimit-inordertosaveonextratransportcosts.Asameanstosupportbetterfarmpractices(orimprovecompliance),whetherinrelationtoloadingtransportvehicleswithinthe legal weight limits or improving cane quality such as by cutting green or reducing soil/sandcontamination,onewayformillstoincentiviseisthrough“queuecutting”duringharvest.

Across all the stakeholder consultation groups, the need formore farmer training to support theincreaseduptakeofbestpracticewashighlightedasbeingcriticaltoachievinganyimprovementsinsustainability(orotherwise).Learningfromdifferentproduction/managementpracticesusedinothercountrieswasofparticular interest tothemill representatives,witharecommendationtousetheBonsucrostandardasthecommonframeworktohelpbenchmarkbestpractice.

C) Recommendations

To maximise the potential for change with Bonsucro and/or other sustainable productionprogrammes, farmerswithsufficientareaofproduction,access towatersupplyandcanegrowingknowledgeneed tobe trained to implementbetter farmingpractices throughmodernagriculturaltechniques.Toidentifyfarmersreadytoengageandadoptimprovements,itwasrecommendedthatthey are first screened using a cost-analysis or risk-basedmodel to assess/analyse profit and lossbeforeplantingandafterharvesttofilteroutfarmerswithalreadyviablefarmoperations.ThiswouldnotonlypilotalternativesolutionsbutalsoleadtosuccessstoriesandachangeofagendastoensurescalabilityofsustainablepracticesandBonsucroimplementation.

To further improve industry performance, government policies should evaluatewater capabilitiesavailable to provide the regions with sufficient water supplies without draining aquifer reserves.Government support should also be dedicated to developing loans or financial tools to supportmechanisation,whichisrequiredfrombothaqualityperspectiveaswellashumanresourceandsocialaspect.

5.2SUGARCANEPROCESSING–MILLLEVEL

A) Opportunities

Themainopportunitiesidentifiedforsugarproductionwereinrelationtogovernmentregulationandsupportmeasurescurrently inplace inThailand.Theyallowsugarcaneproducerstomaintaintheirprofitability,evenduringthetimesofdepressedsugarpricesintheworldmarket,aswellasmarketdiversificationofby-productsthathelpsearnadditionalincome.

Opportunities(oradvantages)identifiedinclude:• Governmentsupportmeasures/policies:i)restrictionsofsugarmillandtraderlicenses,ii)

controloversugaroutputthroughquotaallocations(bothdomesticandexports),iii)fixeddomesticretailprices,whicharehigherthanworldprices,allowingThaibusinessesanadvantageovercompetitorsinthedomesticmarket,andiv)establishmentofabenefitsharingsystembetweensugarcaneplantersandsugarcanemills(70:30),whichhelpsstabilisefactorycosts.

• Valorisationofby-products:Sugarcanemillsalsoearnadditionalincomefrominvestmentinrelatedbusinesses-mostofwhichuseby-productsandexcessmaterialsfromthesugar

www.fairagora.com Drive Change. Create Value. 26

industryasinputssuchasethanol,biomasselectricitygeneration,paperpulp,fertiliser,particleboard,etc.

Figure8-OpportunitiesforThailandinrelationtoSugarcaneproduction.

Participants identified the benefit sharing system between the planters and mills (46%) anddiversificationofsugarcaneby-products(27%)asthemainstrengthsofproductionatthemill level(Figure15).GivenrecentdiscussionsattheWTO(seeSection4.2),however,thesesupportmeasureswillprobablyneedtochange,inwhichcasealternativemethodstosupporttheviabilityofthesectorneedtobeconsidered.Oneoptiontoexploreisthedevelopmentofstrategicpartnershipswithkeystakeholderssuchasdonors, public institutions, investors, buyers etc. underwhat couldbecomePublic-PrivatePartnerships (PPPs) to tackle production efficiency. Pilot programmes could be designed to testrelevanceandreplicabilityofkeypartnershipsandshouldincludepublicsupporttomaximiselong-termgovernmentalinvolvement.

B) Challenges

Themainchallengesforsugarcanemills:

• Highvariationinoutput:Thereiscurrentlyawidevariationinthequalityofsugarcaneanditisexpectedthatthiswillincreaseinthefutureduetoclimatechangeissues(i.e.severefloodanddrought).Ultimately,thismayleadtoa10%annualdecreaseinoutput.16

• Supplyofcane:Toimproveproductivity,farmersneedtobeincentivisedandtrainedinbetterproductionpractices.However,changesinfarmingpracticemayrequireinvestment–andfinancialsupportisneededtofacilitatethis,especiallyforcapitalintensiveinvestmentsinmechanisation,irrigationorbroadertechnologies.

• Environmental/climatechange:thechallengesfacedbysugarproducersareintensifiedwithclimatechangeeffectsaswellassocialimpactstosugarcanefarmersandcommunities.

16AnnualdecreaseasestimatedbytheSugarcanePlantersAssociation.

0% 5%

10% 15% 20% 25% 30% 35% 40% 45% 50%

Q.Whataremainopportunitiesinsugarcaneproduction?

www.fairagora.com Drive Change. Create Value. 27

Figure9-ChallengesforThailandinrelationtosugarcaneproduction

Approximatelyhalf of theparticipants identified climate changeas thebiggest challengeaffectingsugarcane production, with over 65% highlighting the potential impact of drought on futureproductionasaparticularchallenge(Figure16).

C) Recommendations

Farmer training and financial support for investments in mechanisation, irrigation and othertechnologyareneededtoimprovethequality(andquantity)ofcanesupply.Themillrepresentativesattheworkshopexpressedasignificantinterestininvestinginfarmersusingmoresustainableandmodernagriculturepracticeswherethereisaclearreturnoninvestmenttoensureprofitability.

Targeted efforts should also be made to recruit and retain younger generations by positioningagricultureasaviable formofemployment.The introductionofmoremodernagriculturethroughmechanisationandtechnologycouldbeaninterestingwaytoattractthenextgenerationoffarmersandhelpsecurethefutureofagricultureinThailand.

5.3SUGARCANETRADING

A) Opportunities

Opportunitiesidentifiedforsugartraders:• Proximitytomainexportdestinations:ThebiggestadvantagefortheThaisugarmarketlies

initsproximitytoAsianmarkets,particularlyIndonesiaandChina,whosedemandsforimportedsugarareincreasingeveryyear.

• EconomicIntegration:ThailandisoneoftheleadingsugarexportersamongASEANcountries,exportingabout2.73millionMTofsugaryearly,whichrepresents51%ofthesugardemandinthisregion.FurthermarketliberalisationundertheAECisanadditionalopportunityforThailandtoexpanditsmarketshareintheregion,especiallyinIndonesia,whichisthelargestexportmarketforsugarfromThailand.

0% 10% 20% 30% 40% 50% 60% 70% 80%

highvariationinoutput

climatechangeissues

severeflood drought other

Q.Whatarebiggestchallengesinsugarcaneproduction?

www.fairagora.com Drive Change. Create Value. 28

Figure10-OpportunitiesforThailandinrelationtosugarproduction/trade.

Approximately50%oftheparticipantsidentifiedThailand’sproximitytothemainexportdestinationsaswellastheeconomicintegrationofASEANcountriesasthemainadvantagesforThaisugartraders(Figure17).However,thesemarketopportunitiesarebasedontheproductionandtradeofsugarasa raw commodity anddonot reflect possible opportunities for certified sustainable sugar.Where‘Bonsucrocertified’sugaristraded,thepriceisnottheonlyfactortobeconsidered,asotheraspectsrelatingtosourcingriskandcompliancerequirementsalsoshapethediscussion.

Atpresent,itismainlycompanieswithclearsustainabilitypoliciesandcommitmentstoresponsiblesourcingthataredrivingindustryeffortstowardsenvironmental,social,andeconomicsustainability.Thesecompanies,whichareusuallydirectlylinkedtoconsumer-facingbrands,taketheircommitmenttowardsustainablesupplyseriously,byindicatingtheirpreferencesandrequirements,andbyfindingnewways toengagewith their supply chain todeliver shared valueonagreed indicators (i.e. theBonsucrostandard).Thismeansthattheyareabletoinvestinmoresustainableproductionsystemsandconsideradditionalfactorsbeyondpricewhensourcingsugar.

B) Challenges

Thetradeinsugarcaneisdrivenbyworldmarketpriceandisdirectlyaffectedbypricefluctuationsandthepriceofrelatedcommodities(i.e.oil).

Mainchallengesforsugartraders:• Continuedtrendoflowworldmarketprice:Worldsugarpricesarenotexpectedtoincrease

markedlyintheshort-term,possiblyonlytoanaverageof14.5-16cents/lb.Thisisduetothecombinedeffectsofdownwardpressuresfromexistinghighsugarstockpiles,prolongeddepressedoilprices,andthecurrentsluggishspeculativedemandinthecommoditymarkets.

Ifthepriceistheonlyfactorconsideredwhenbuyingsugar,thenthelowworldmarketpricewillbeasignificantchallenge for theThai sugarcane industry in thecomingyears,especially ifgovernmentsupportmeasuresareremoved(orevenreduced)inresponsetocomplaintsviatheWTO.ForthosetradinginBonsucrosugar,whichprovidesaddedvalueforsomebuyers,themainchallengefortraderswill be to increase the volume of certified sugar. The key scalability factor lies in progressing the

0%

10%

20%

30%

40%

50%

60%

proximitytomainexportdestinations

economicintegrations

marketpricefluctuations

other

Q.Whatarethemainopportunitiesinsugarproduction/trade?

www.fairagora.com Drive Change. Create Value. 29

sustainability dialogue with more buyers in new territories about developing sustainabilitycommitments and greater brand support. To make that step, pilot programmes that assess therelevance, identify failures and consolidate success could be used to trial implementation of andincreasesupplychainsupportforsustainability.

C) Recommendations

Althoughthetypeandextentof futuresupportmechanismsprovidedbytheThaigovernmentareunknown,atleastaproportionofthecurrentsubsidiesneedtoberedirectedbackintotheindustryinaformthatdoesnotcontraveneWTOconventionstohelpmaintaintheviabilityofthesector.

Recommendedsupportstructuresinclude:• farmertrainingprogrammes;• R&Dinagriculturetechnology;and• loandevelopmentorotherfinancialtoolstosupportmechanisationandtheadoptionof

betteragriculturaltechnologies.

5.4SWOTFORSUGARCANESUSTAINABILITY

Witha senseof limitednatural resourceson theplanet, and increasedclimate changeactionandconsumer awareness, Bonsucro offers a platform to invest and trade in sustainable sugar. TheBonsucroplatform,supportedbyametric-basedstandardforproductionaswellasachainofcustody,has the potential to provide immense added value and is in line with current Thai legal andgovernmental frameworks regarding environmental and social aspects of sugarcane growing,productionandtradingaswellasgreenenergyandby-productsupport.

Usingthechallengesandopportunitiesidentifiedintheprecedingsection,stakeholderswereaskedtoidentifyspecificstrengthsandweaknesseswithrespecttocompliancewithBonsucroinThailandaswell as possible opportunities for improvement aswell as threats to social and environmentaloutcomes. Figure18 summarises someof theperceived strengths,weaknesses,opportunitiesandthreats(S.W.O.T)andisbasedontheopinionsexpressedbystakeholders.

www.fairagora.com Drive Change. Create Value. 30

Figure11-Analysisofstrengths,weaknesses,opportunitiesandthreats(SWOT)forThaisugarcaneandcompliancewiththeBonsucrostandard.

5.5OPPORTUNITIESANDCHALLENGESINTHECONTEXTOFTHEBONSUCRO

UsingtheBonsucrostandardasaframework,opportunitiesandchallengesidentifiedbyparticipantsintheBonsucroTechnicalWeekWorkshopwerediscussedinthecontextofthestandard’sprinciples.Where‘opportunities’wereassigned,thegroupdiscussedwhetheritindicatedalevelofawarenessorreadinessofcompliance.Where‘challenges’wereassigned,therewasadiscussionaboutwhetherthisindicatedlimited/lowreadinessoranindicationofcomplianceconcerns.Belowisasummaryofthemainpointsofdiscussion.

Principle1–obeythelaw

ThediscussionunderPrinciple1focussedonthedemonstrationoftitletolandandwaterastherewas significant concern expressed in the group that themajority of smallholders, aswell asmostcontractfarmers,wouldfinditdifficulttoprovideevidenceofcompliance.Asexplained,inThailand,there are different kinds of land titles (like rice ownership certification or permits) and these areassociatedwithdifferentlanduserights,whichspecifythetypeofactivityandarea.About70to80%of the land is rentedby farmers froman agent or someone they trust – usually through a verbalcontractandoftenthrougha long-termarrangement.However, the legalsystem isnot favourableregarding rights transfer especially for farmers (even if they have used the land for generations)

Strengths- environmentalperformanceandpositivesocial

impact- Legalframeworkandgovernmentalpolicies- Labourlaw&rights- Righttolandandwateruse- Millproductionmonitoring- Millemployees'training- Energyefficiencymonitoring- Emissionsreductionandwasterecycling

Weaknesses- keyimprovementareas

- Limitedlegal/regulatoryenforcement- Waterconsumptionmonitoring- Health&safety(farmlevel)- Limitedlabourandhumanrightsmonitoringatfarmlevel- Biodiversityandecosystemmonitoring(EIMP,N&P,Agro-chemicals)- Limitedresearchoneconomicsofcanegrowing

OpportunitiesforContinuousImprovement

- Mechanisation- togetherwithinvestmentschemes

- GHGemissionscalculation- R&Dforyield,tillage,groundcover

afterharvest,soilpH,etc.- Economicresearch/cost-analysisondesignoffinancialriskmodellingtoolforprofit/loss(pre-assessmentat

farmlevel)- Farmertrainingongoodagriculture

practices

Threatstoenvironmental/socialoutcomes

- Waterconsumptionagainstwaterreserveinspecificareas- GHGemissionsfromcaneburning- Unintendedconsequencesofgreenenergypromotionandlandusediversification(waterresources,GHGemissions,soilerosion,ruralpoverty)- Limitedlabourandhumanrightsperformancemonitoring- Socialjusticemechanism:grievance,multi-stakeholderengagementetc.

www.fairagora.com Drive Change. Create Value. 31

becausetheyneedofficialdocumentationtodoso.Thismeansthatthefamilymayinheritthelandbutcannotsellit.

With respect towateruseandaccess,permitsare required todig forartesianwells.Even thoughfarmers are aware of this requirement, these permits are not always obtained, particularly insituations where proof of land title/use rights is lacking.Mills are concerned that if they requirefarmers to get water permits as part of the certification process, the farmersmay be subject toretroactivefinesandotherpenaltieswhichcoulddestroytheirrelationshipandco-operationand/orengagementwiththeimplementationofthestandard.

Workshop participants recommended that Bonsucro review these indicators in the context ofThailandandconsidertherealintentoftheindicators;thatis,towhatextentisthereariskorconflictoverownershiporland/wateruse?ItwassuggestedthatBonsucroadapttheindicatorstostatethatlandshouldnotbeacquiredthroughillegalmeansorfromreservedland,forexample.Analternativewouldbetoprovideclearauditorguidanceonthisissuesothattheintentionbehindtheindicatoriswhatisbeingassessed.

Principle2–respectinglabourrights/humanrights

ThediscussionunderPrinciple2focussedontheimportanceofinvestmentcapabilityasameanstoimproveworkingconditions. Investmentwasneededtosupportbetterenforcementandtocreateconditions that fostered betterworking environments. For example, in terms of child labour, thegroupfeltstronglythatwhilethiswasnotaproblematthemills–andthattherewasahighlevelofawarenessaboutbothchildandforcedlabour.Theyacceptedthatforsmallholderfarms,itwaslikelythat all family members were engaged to some extent in farm activities so the challenge was,therefore, to improveawarenessof the typesandextentofacceptableactivitiesandthenhowtoaddress(andcompensatefor)thepotentiallossoflabour.

Anotherwaytofacilitatecompliancewasbyinvestingintechnologyorequipmentthatcontributestobetter/saferworkingconditions.Investmentinmechanisationatthefarmlevel,forexample,reduceslabour requirements andmore specifically, the use of labour in cane cutting which is potentiallyhazardous.AnotherexampleprovidedwastheuseofPPE.Atthemilllevel,thelevelofPPEusebyemployeeswashighbecauseitwasprovided,anduseenforced,bythemills.UseofPPEatthefarmswasmuchmoreofaproblem,especiallywhereitwasnotbeingprovidedbythefarms.

Principle3–managinginput,productionandprocessingefficiencies

Workshopparticipantswereclearthatinvestmentcapitalwasneededtoimproveefficienciesinmillsandfarmsbutthefocusofthediscussionwasonfarmsasbetter-qualitysugarcanewasidentifiedascritical to both. To improve, farmers needed greater access to free and more consistent farmertrainingprogrammesdesignedaroundimprovingagriculturepracticesanddatacollectionmethods.Itwasfeltthatthisknowledgewouldultimatelyhelptoincreaseyieldsandproductivityviafeedbackloops, theassumptionbeing that if farmers couldmonitor relevant indicators (e.g.quality, inputs,productivityetc.),theycouldthenmakedecisionsbasedontheresultsandmanageproductionmoreefficiently.

www.fairagora.com Drive Change. Create Value. 32

Principle4–activelymanagingbiodiversityandecosystemservices

Whenreviewingprinciple4,participantsrelatedtheissueofbiodiversitymainlytotheagro-chemicalsbeingappliedtothefield(perhectareandperyear).Theycitedtheuseofalternatives(e.g.greenfertilizers)andcroprotationaspracticesthatcouldleadtomoreefficientsoilmanagement,resultingingreateroptimisationofanyappliedagro-chemicals,includingN,P&Kfertilizer.Althoughtherewasagooddegreeofgeneralknowledgeintheroomaboutthis issue, inpractice,specialisedtechnicalsupportintheformoflocalagronomists,forexample,wouldberequiredtohelpfarmsadapttolocalconditionstoensuresuccessfulimplementation.

Principle5–continuouslyimprovingkeyareasofthebusiness

Discussionsrelatingtoprinciple5centeredaroundkeyareasidentifiedduringtechnicalweekwhichincluded:watermanagement,mechanisationofharvest,sugarcanequalityandsocialcompliance.Tofostercontinuousimprovementefforts,workshopparticipantsstatedthatloandevelopmentorotherfinancial/ technology tools had to be expanded andmademore accessible to farmers. They alsoreiteratedtheneedforfreeandmoreconsistenttrainingprogrammestobuildcapacity.

Therestofthediscussionfocussedonwaterandmorespecifically,howtoaddressmanagementonawiderscalegiventhe increasingpressureonwaterresources.Participantswere largelyawarethatwaterusehadtobereducedinirrigatedareastoconservewaterandtoavoiddrainingaquifers.Toaddressthewiderissuesofwatermanagement,however,bettersystemsneededtobeusedacrossThailand,startingwithanevaluationofwateravailabilityinlinewithregionalwatersuppliersanduseofclearindicatorsthatmeasureefficiency.

Principle 6 – Additional mandatory requirements for biofuels under the EU Renewable EnergyDirectiveandrevisedFuelQualityDirective17

Underprinciple6,thegroupdiscussedcaneburninganditsrelative impactonclimatechangeandotherfactorsofproductionsuchassoilquality. Itwassuggestedthatburningcould leadto loweryieldsandhighercostsofproductionbutifitwasreduced(oreliminated),itwouldresultinareductionofGHGemissionsandalsoimprovedsoilmanagement,whichiscrucialtosustainingahighbiodiversityvalue.Atthefieldlevel,mechanisedharvestingwouldeffectivelyreducethedemandforburninginThailandaslongastheequipmentwasappropriateforsmallholderfarmsandlocalconditions.

WorkshopparticipantsconcludedthatitwouldbeverydifficulttostopburninginThailandunlessaban (or restriction) was supported by government regulation and then enforced accordingly. Ifmanagedonavoluntarybasis,thegroupquestionedthespeedatwhichachangewouldoccurandwhether enough farmers would ever stop burning cane - even if better access to appropriatemachinerywasprovided.Itwasthereforerecommendedthatalloptionstostopcaneburningarefullyexplored,includingtheneedforfinancialandexpertknowledgesupport.

17EURenewableEnergyDirective–2009/28/ECandFuelQualityDirective-2009/30/EC.

www.fairagora.com Drive Change. Create Value. 33

6. CONCLUSIONSANDRECOMMENDATIONS

Thisreportwaswrittentoinspireaction,co-operation,andtransparencyamongstakeholderswishingtoimproveeconomic,environmentalandsocialsustainabilityinthesugarcaneindustryinThailand.As part of the consultation process, stakeholders identified some of the social, economic, andenvironmental challenges in theThai sugarcane industry,aswellaskeyopportunities todrive thesustainability agenda forward. The Bonsucro performance framework was identified as a logicalframework tomeasure these sustainability indicators and through its collaborative platform, as ameanstofacilitateacomprehensivevaluechainapproachthatallowsgrowers,producersandbuyerstousecomparablemetricsandtoolstomeasureandmonitorperformance.

ActionsidentifiedbystakeholdersashavingthepotentialtopositivelyaffectthesugarcanesectorinThailandincluded:

ü Mechanisationofharvestü Dedicatedinvestmentschemesforimprovementü Environmentalmonitoringandmanagementü Increasedeconomicresearchandfinancialriskmodellingü Farmertrainingingoodagriculturepracticesanddatacollection

Inordertoimplementtheseimprovementsandmaximiseimpact,capacitybuildingprogrammesareneeded to build industry knowledge and financial support mechanisms put in place to enableinvestment. Thedevelopmentof anewsetof innovative incentivesdirected towards farmersandmillerstoreducetheenvironmentalfootprintofsugarcaneisalsoneededtosupportmechanisation,irrigationand/ortheadoptionofothertechnologiestodriveimprovedqualityandproductivity.

Improvedstakeholderengagement:governmentandfarmers

To address some of the biggest challenges in the sugarcane industry, improved stakeholderengagement and collaboration is needed across the supply chain, and with the Government ofThailandandfarmersinparticular.InrelationtotheGovernment,stakeholdersinformedthatgreaterpolicyandtechnicalsupportwasneededinthefollowingareas:

ü Evaluatingwaterquantityuseandpermittingcapacitytoprovidesufficientwatersupplieswithoutdrainingaquiferreserves.;

ü Supportingfinancialmechanismsforinvestments;ü Implementingmonitoringmechanismsfrombothproductqualityperspectiveaswellas

humanresourceandsocialaspects;andü Restricting/banningtheburningofcane,withfinancialsupportformechanisationprovided.

Theimportanceofengagingwithfarmerswasalsohighlightedasapriorityissue,withtheultimateaimto improvequalityandproductiononthefarm.Toachievetheseaims, farmershavetoadoptnew,moresustainablepractices–somethingtheyareoftenslowindoingbecauseofthepotentialriskinvolved,limitedtechnicalknowledgeorabilitytoinvestinrequiredinputs.Itwassuggestedthatapilotortestgroupoffarmerstrialnewapproacheswhilecollectingdatatodemonstrateoutcomesandimpactstotheirpeersalongtheway.Anylessonslearnedwiththefarmergroupcouldthenbeused to scale the adoption of sustainable practices along with other Bonsucro improvementprogrammes.

www.fairagora.com Drive Change. Create Value. 34

7. REFERENCES

• Governmentpolicy&environmentalsustainabilityandclimatebenefitofgreentechnology

forbioethanolproductioninThailand,Kawasakietal.,2015.

• ISO,November2015,QuarterlyOutlook:Estimatedproductionanduseofethanolinthe

worldmarketyear2014/2015.

• IVongkusokit,July2016,BangkokSugarConferenceNewChallengesandOpportunitiesof

ThaiSugarIndustry.

• KTaechaphimol,KhonKaenUniversity,2014,Projectcost,productivityandknowledge

transfertoreducethecostofsugarcaneproduction2557/58.

• OCSB,April2016,Annualreport2016.

• PWeerathaworn,2015,Developmentsonglobalsugarcanemarkets:challengesforThailand

producers.

• TRIS,August2015.IndustryResearch:SugarIndustry.WPitakpaibulkij,RJarurungsipong,R

Suntornpagasit,NRakthum.

• ThaiSugarMillersCorp.Ltd,2016.Thaisugarindustry’challenges,trendsandcurrent

developmentsaffectingtheindustry.RHiangrat.

• Thailandindustrialoutlook2016–2018,WareeratPetcheechoung,KrungsriBank.

• USDA:Thaisugarannualreport2016.BRichey,PPrasertsri,2016.

• WPetchseechoung,May2016,SugarindustryThailand,IndustryOutlook2016-18.

www.fairagora.com Drive Change. Create Value. 35

8. APPENDICES

APPENDIXA:QUESTIONNAIRE–ENGLISH&THAIVERSIONS

www.fairagora.com Drive Change. Create Value. 36

www.fairagora.com Drive Change. Create Value. 37

www.fairagora.com Drive Change. Create Value. 38

www.fairagora.com Drive Change. Create Value. 39

APPENDIXB:FOCUSGROUPDISCUSSION–INVITATIONANDOVERVIEW

www.fairagora.com Drive Change. Create Value. 40

APPENDIXC:THAILAND'SEXPORTSOFRAWSUGAR(MTRV)

2010 2011 2012 2013 2014 2015 2016

China 782,081 1,248,555 1,786,363 1,768,320 1,713,410 1,839,027 1,839,027

Indonesia 533,887 1,107,829 868,700 748,868 771,205 647,831 647,831

Japan 134,261 507,330 482,409 499,226 375,251 462,343 462,343

NorthKorea 120,375 324,600 372,543 181,750 477,524 254,130 254,130

SouthKorea 81,372 43,400 99,220 131,328 62,579 201,620 201,620

Malaysia 56,367 53,282 182,791 114,866 243,136 187,067 187,067

Philippines 4,617 192,673 839,576 50,838 495,016 170,227 170,227

Russia 1,539 2,334 1,898 17,852 31,801 18,357 18,357

Singapore 22,868 23,784 20,993 0 15,940 14,525 14,525

SriLanka 8,824 7,643 513 20,366 15,800 7,454 7,454

Tanzania 0 205 282 564 53,917 462 462

Taiwan 7,206 19,971 149 66 129 203 203

UnitedStates 20,273 18,515 3,263 0 0 0 0

UAE 29,365 3,335 0 0 0 0 0

Vietnam 31,652 174,542 49,453 33,858 37,298 0 0

Others 138,547 495,536 212,883 137,002 137,450 130,500 130,500

1,973,234 4,223,534 4,921,036 3,704,904 4,430,456 3,933,746 3,933,746

www.fairagora.com Drive Change. Create Value. 41

APPENDIXD:THAILAND'SEXPORTSOFREFINEDSUGAR(MTRV)

2010 2011 2012 2013 2014 2015China 20,894 95,507 157,083 214,068 263,704 756,115Burma 13,086 34,934 49,210 116,818 138,118 706,838Cambodia 468,756 409,016 632,147 683,528 564,631 518,834Malaysia 35,858 28,869 98,018 157,085 225,600 266,312Vietnam 179,179 263,384 249,518 146,661 53,552 192,682Singapore 101,933 174,113 130,786 109,053 136,511 156,655Laos 31,987 44,443 85,028 32,743 39,710 107,848SouthKorea 544 14,408 22,730 41,363 63,772 99,452SriLanka 68,108 44,071 51,789 50,572 95,894 78,586Indonesia 522,883 103,610 135,254 81,076 80,847 73,597Philippines 266,813 126,829 81,961 74,316 50,059 65,256Jordan 27 12,085 51,266 66,076 96,070 38,788Syria 0 10,745 7,838 27,606 35,310 35,821Tanzania 9,071 28,576 24,813 58,744 39,854 25,094SaudiArabia 803 18,470 9,067 32,927 34,928 21,353Kenya 5,566 31,898 42,496 95,632 36,575 13,936UAE 21,645 45,597 13,669 27,266 62,199 11,718India 348,499 6,426 7,592 7,218 10,657 10,229Brunei 6,337 6,561 6,561 2,247 4,494 6,206Yemen 1,498 3,123 5,466 2,649 7,655 4,826Maldives 776 936 990 936 1,284 2,318Russia 0 776 161 0 497 776Somalia 0 0 0 5,992 15,539 535Pakistan 178,485 2,676 936 348 6,133 408Bangladesh 2,140 11,856 0 266 767 348Iran 0 6,420 0 0 98 15NorthKorea 5,230 4,140 0 0 2,140 0Others 354,896 1,128,162 1,010,893 1,047,206 1,073,442 1,143,551

2,645,014 2,657,631 2,875,272 3,082,396 3,140,040 4,338,097

www.fairagora.com Drive Change. Create Value. 42

APPENDIXE:RAINFALLDATA,2011-2015

Source:OCSB,2016

www.fairagora.com Drive Change. Create Value. 43

APPENDIXF:CANEBURNINGINTHAILAND

www.fairagora.com Drive Change. Create Value. 44

APPENDIXG:WORKSHOPNOTES-FAIRAGORASESSIONINBONSUCROTECHNICALWEEK

SUGARCANEGROWERSOpportunitiesPositiveattributesofsugarcane:

- ClimateinThailandisconducivetocanegrowing- Caneonlyneedsreplantingevery3-5years- Contractfarmsreceivedirectsupportfrommills(e.g.loansforproductioninputs,machines)

Advantagestobefullyrealised:- Opportunitiestoimprovepracticeswithgreenfertiliserandcroprotation- Diversification–valuechainisorganisedandco-ordinated,withmarketopportunitiesavailableto

producersinrelationtoby-products.Thereisalsothepotentialforfarmerstodiversifyagriculturalproductionandplantothercropssuchastapioca,maizeetc.butfarmerswouldneedsomesupportfromthemilltodothis.

- Middlemen–currentlydistributequotatofarmersandactasbrokersbetweenmillsandfarmers.Giventheirroleandlevelofinteraction,isthereanopportunitytousemiddlemenmoreeffectivelytocollect/managefarmerdataand/ordisseminateinformation?

ChallengesLowproductivity

- Indicationthattherearepathogens/disease–Ratoonstuntingdisease-butneedteststoconfirmandbettercropvarietiestomitigate

- Productivity-Lowyieldduetosoilquality.IncreasingtonnageperhawillalsoincreasesugarperHA.- Caneburningstillwidelyused(thisreducesyield)butmechanisedoptionsareexpensiveandneedto

becheapertobeaccessibletosmallerfarmersCostsofproduction

- Farmersdon’thavemoneysoneedaccesstocapital–especiallyafternaturaldisasterslikemajordroughtsorfloods.

- Shortageoflabour–nobodywantstocutcaneinThailandanymoresotheyoftenrelyonmigrantlabourersinsteadbutthecostoflabourisgettinghigher,furtherreducingavailableprofit

- Canetruckscannotbeloadedmorethan25tons(nowalegalrequirement)butcanefarmerskeepdoingitbecauseotherwise,itcoststhemmoremoney(foradditionaltruckloads).

Other- Milldoesn’townlandsohardtocontrol/changefarmpractices- Farmerselection–itisdifficulttogetfarmerstochange(especiallywheremillshavenodirect

ownershiporcontractwiththem).- Mostfarmersdonothaveevidencetoprovelandownership(orrighttowateruse)

RecommendationsStopburningcane–itleadstoloweryieldsandhighercosts(morewaste!).AlternativeformsofmechanisationthatcanbeusedinThailand(andinsmallholderfarms)needtobeexplored.Farmertraining

- Farmertraining/education–Educationforfarmersshouldbefreeandfocusonareastosuchasproductivitytraining,newtechniques,soiladaptationetc.Thetrainingcouldbethroughagronomistsfrommills,fromextensionagentsorcolleges.

- Trainingprograms–shouldonlyinvolvefarmersthatarereadytoadoptnewpractices.Ascreeningprocessisneededbecausemillswanttomakesurethattherightfarmersparticipate–thosethatwillhelpimproveyieldbyadoptingnewpracticesandcollectingdatatodemonstrateimpact.

- DatacollectiontrainingneededforfarmersResearchandinvestment

www.fairagora.com Drive Change. Create Value. 45

- Increaseresearchintonewscientificfarmingtechniques(asopposedtotraditionalmethods),withbespokeadviceavailabletoaddressfield-specificissues(e.g.basedonsoiltype)

- Breednewvarietiesofsugarcane(orimproveexchangeprogrammeswithothercountries)

SUGARCANEMILLSChallenges

- Sugarisacommoditywithlimitedmarketopportunities–itisthesameproductsotoexpandopportunities,needtofindnewmarkets(likeIndiaandChina).TherecommendationistogetBonsucrocertificationtodifferentiateitfromothersources.

- CCSisinconsistentsoneedtoadjustthevaluetogetahigherpercentageofsugar.Note:factorsaffectingCCSlevel=soil,geography,andTK

Equipment/machines- Millsaregenerallylow-tech-betterequipment/technologyisneededinmanylocationse.g.new

high-pressureboilerstoimproveefficiency(resultinginlowerenergyconsumption)butthisrequiressignificantcapitalinvestment.Maintenancecostscanalsobehighduetodamagefromsand,rocksandothercontaminantsfoundinsugarcanebutqualitycontrolwithfarmerstoreducethequantityofdirtonsugarcane(pricerelatedcontrolmechanism)hasthepotentialtolowercosts.

Recommendations- Needtohaveacontinuousimprovementprograminplacewithtransportcompanies,millersand

farmersneedtoimprovethewaytheyarecuttingcaneandhowtomakebetteruse,thiswillhelptoreducecost