textile industry: profile and dsm options - infohouseinfohouse.p2ric.org/ref/28/27014.pdftextile...

TRANSCRIPT

Electric Power Research Institute

TEXTILE INDUSTRY: PROFILE AND DSM OPTIONS

Prepared by RESOURCE DYNAMICS CORPORATION and BATrELLE-COLUMBUS DIVISION

R E P O R T S U M M A R Y SUBJECTS Demand-side planning / Industrial / Market assessment

TOPICS Demand-side management Industrial technology alternatives Demand-side planning Marketing Electrotechnology Load management

AUDIENCE Customer service representatives / Demand-side, R&D, and corporate planners / Marketing managers

Textile Industry: Profile and DSM Options Demand-side management approaches and emerging electro- technologies promise to increase the efficiency and productivity of the textile industry. This guidebook provides utilities with a comprehensive overview of the textile industry's challenges, manufacturing processes, technologies, and energy-use patterns, as well as opportunities for electrotechnologies and demand-side management options.

BACKGROUND Throughout the utility industry, demand-side management (DSM) is gain- ing greater acceptance as a resource that promotes value for utilities as well as their customers. The great diversity in industrial business situations and energy-use patterns, however, often makes it difficult to understand how to apply DSM in the industrial sector. By better understanding their customers' needs and the technology options available, utilities can develop programs that are more successful in promoting DSM and electrotechnology applications.

OBJECTIVES To identify opportunities for improving energy efficiency, enhancing pro- ductivity, and promoting load management objectives.

-To help utilities develop and implement DSM programs.

APPROACH On the basis of literature surveys and interviews with experts in the textile and utility industries, investigators created this guidebook to describe the textile industry and advise on the selection of appropriate DSM and electro- technology approaches. As background for their research, they relied on the DSM framework developed under EPRl's DSM project (report -

.~ EAIEM-3597).

RESULTS This guidebook presents a detailed profile of the textile industry, providing information about the markets, processes, technologies, and energy-usage patterns of the major types of customers in this industry. Following the

- ~

framework of the DSM project, it presents the DSM technologies and market implementation methods appropriate for achieving the various load-shape objectives within the textile industry. It describes a step-by-step approach for the development of a DSM plan that can help not only the utility but

~

EPRl CU-6789s Electric Power Research Institute

~~~ ~

also textile customers, through lower energy costs, greater productivity, and improved product quality.

This textile industry guidebook is part of a broad framework of tools and data designed to assist utilities in working with the industrial sec- tor. These products help utilities better understand and meet the needs of their industrial customers. They also suggest how utilities can help achieve their load-shape objectives in the industrial sector. Among EPRl's other industry-related products is IMlS (Industrial Market Infor- mation System software), available through the Electric Power Software Center, to help utilities identify markets for various electrotechnologies. In addition, lndustrial Load Shaping: An lndustrial Application of DSM (report CU-6726) describes a methodology and real-world applications of DSM in the industrial sector. Tech Applications and Tech Commentaries, available through EPRl's Centers for Materials Production and Materials Fabrication, further explain how industries can benefit from electrotech- nologies. And lndustry Briefs, currently under development and available in mid-1990, will provide insight into industrial processes, technologies, and energy-use patterns at the three- and four-digit SIC level. When used together, these documents will aid in development of DSM pro- grams that will benefit both utilities and their industrial customers.

EPRl PERSPECTIVE

-~ ~ ~~~

~

~~

~

PROJECT RP2885-1 EPRl Project Manager: Paul C. Meagher Customer Systems Division Contractors: Resource Dynamics Corporation; Battelle-Columbus Division

For further information on EPRl research programs, call EPRl Technical Information Specialists (415) 855-2411.

Textile Industry: Profile and DSM Options

CU-6789 Research Project 2885-1

Final Report, July 1990

Prepared by

RESOURCE DYNAMICS CORPORATION 8605 Westwood Center Drive

Vienna, Virginia 22180

BATTELLE-COLUMBUS DIVISION 505 King Avenue

Columbus, Ohio 43201

Prepared for

Electric Power Research Institute 3412 Hillview Avenue

Palo Alto, California 94304

EPRl Project Manager P C. Meagher

Demand-Side Planning Program Customer Systems Division

ORDERING INFORMATION

Requests for copies of this report should be directed to Research Reports Center . (RRC), Box 50490, Palo Alto, CA 94303, (415) 965-4081. There is no charge for reports requested by EPRl member utilities and affiliates, U.S. utility associations, U.S. government agencies (federal, state, and local), media, and foreign organizations with which EPRl has an information exchange agreement. On request, RRC will send a catalog of EPRl reports.

Clecinc Power Research Institute and EPRl are registewd service mark of Electric Power Research Institute, Inc

Copyright 0 1990 Electric Power Research Institute, Inc All rights reserved

NOTICE This report was prepared by the organmtion(s) named below as an account Of w r k sponsored by the Electr~c Power Research Institute. Inc (EPRI) Neither EPRI, members of EPRI. the arganiralion(s) named below, nor any pefson acting on behalf Of any of them, (a) makes any warranty, enpress or impled. with respect to the use of any information. apparatus. method. or process disclosed in this repon 01 that such use may not infringe privately owned rights: or (b) assumes any liabilities with respect to the use of, or lor damages resulting from the use of. any information. apparatus. method, or process disclosed in this report.

Prepared by Resource Dynamics Corporation Vienna. Virginia and Banelie-Columbus Division Columbus, Ohio

ABSTRACT

The T e x t i l e I n d u s t r y Guidebook provides e l e c t r i c u t i l i t y p lanning, marketing, and customer serv ice s t a f f w i t h a p r a c t i c a l t o o l t o b e t t e r understand the t e x t i l e indus t ry and t h e chal lenges i t faces: i t s manufacturing processes, technologies, and energy use; and i t s o p p o r t u n i t i e s f o r demand-side management (DSM). concludes w i t h guidance and summary data f o r developing and eva lua t ing DSM plans t o r e a l i z e such oppor tun i t ies .

The Guidebook

iii

ACKNOWLEDGMENTS

The Resource Dynamics Corporat ion and Battelle-Columbus D i v i s i o n wish t o thank t h e numerous t e x t i l e companies, associat ions, equipment supp l i e rs , government agencies and u t i l i t i e s t h a t ass i s ted i n p rov id ing in format ion used i n t h i s study. p a r t i c u l a r no te were t h e con t r i bu t i ons o f D r . Gary N. Mock o f North Caro l ina State U n i v e r s i t y and N. James Covington.

O f

Paul Meagher o f t h e Demand-Side Planning Program o f t h e Customer Systems D i v i s i o n (CSD) coordinated t h i s p ro jec t . I. L e s l i e Harry and K. R. Amarnath o f CSD's I n d u s t r i a l Program provided va luable review and inpu t , as w e l l as t h e T e x t i l e Indus t r y Scoping Study, an important precursor t o t h i s Guidebook.

Resource Dynamics Corporat ion B a t t e l le-Columbus D i v i s i o n February, 1990

V

CONTENTS

Sect i o n

EXECUTIVE SUMMARY Purpose o f t h e Guidebook The T e x t i l e Indus t r y Business and Product Trends Manufacturing Processes and Energy Use Ge t t i ng Star ted : Charac ter iz ing Potent i a1 DSM Oppor tun i t ies

1 OVERVIEW OF THE TEXTILE INDUSTRY Purpose o f the Guidebook The T e x t i l e Indus t r y Business and Product Trends E l e c t r i c i t y ' s Role i n Improving Competit iveness Oppor tun i t ies f o r the E l e c t r i c U t i l i t y I ndus t r y How t o Use t h i s Guidebook Organizat ion o f t h i s Guidebook

2 MEETING TEXTILE-CUSTOMER NEEDS THROUGH ELECTRICITY T e x t i l e E l e c t r i c i t y Use by Indus t r y Segment and Process Importance o f E l e c t r i c i t y Competing Technologies and Energy Sources Technology Acqu is i t i on and Decision Making A b i l i t y t o Modify E l e c t r i c i t y Use DSM Program Oppor tun i t ies and Constraints

3 DSM PLANNING AND IMPLEMENTATION S e t t i n g DSM Object ives I d e n t i f i c a t i o n o f Appropr iate DSM Programs Eva lua t ion and Se lec t ion o f DSM Programs Program Implementation Program Moni to r ing

5-1 5-1 5-1 5-5 5-8 5-13

1-1 1-1 1 - 2 1-3 1-5 1-6 1 - 7 1-10

2-1 2 - 3 2 - 3 2 - 5 2 - 7 2 - 9 2-11

3 - 1 3-2 3- 2 3 - 3 3-8 3-8

v i i

CONTENTS (Continued)

Section

4 DEVELOPING A DSM PLAN FOR THE TEXTILE INDUSTRY Organiz ing f o r DSM Step 1. I d e n t i f y and Character ize T e x t i l e Customers Step 2. Analyze T e x t i l e E l e c t r i c Loads and End Uses Step 3. I d e n t i f y Appl icable DSM Technologies and Process Changes Step 4. I d e n t i f y Market Implementation Methods Step 5. Evaluate and Select DSM Programs Step 6. Develop Tex t i l e - Indus t r y DSM Plan

APPENDIX A OVERVIEW OF THE TEXTILE INDUSTRY The T e x t i l e Indus t r y Supp l ie rs t o t h e T e x t i l e Indus t r y Major Markets and End Uses o f T e x t i l e M i l l Products

Regional Impacts o f T e x t i l e Production Segmentation and Spec ia l i za t i on Indus t r y Concentrat ion Competit ive Forces and Imports Cost-Based Competit ion Impact o f Competit ive Responses Business and Product Trends

APPENDIX B MANUFACTURING PROCESSES AND ENERGY USE U n i t Processes i n Dry Processing U n i t Processes i n Wet Processing T e x t i l e Production Costs T e x t i l e Manufacturing Processes and Technologies Energy Consumption in t h e T e x t i l e Indus t r y

E l e c t r i c i t y Use i n t h e T e x t i l e Indus t r y Energy Consumption by S p e c i f i c Processes

4 - 1 4 - 1 4 - 2 4 - 5 4-8 4 - 9 4-15 4-18

A- 1 A - 1 A - 3 A - 5 A-8 A-12 A-13 A-14 A-17 A-22 A-25

8- 1 B-8 8-12 8-14 6-17 B-19 8-25 B-30

v i i i

CONTENTS (Continued)

Sect ion

APPENDIX C TEXTILE INDUSTRY ELECTROTECHNOLOGY EQUIPMENT SUPPLIERS Adjustable Speed Dr ive Equipment Suppl iers Heat Exchangers and Heat Recovery Equipment Suppl iers I n f r a r e d Processing Equipment Suppl iers I n d u s t r i a l Process Heat Pump Equipment Suppl iers Microwave Heating and Drying Equipment Suppl iers Radiofrequency Heating and Dry ing Equipment Suppl iers

U l t r a v i o l e t Cur ing Equipment Suppl iers

APPENDIX D DESCRIPTIONS OF SELECTED ELECTROTECHNOLOGIES FOR THE TEXTILE INDUSTRY

Radiofrequency Drying and Heating I n d u s t r i a l Process Heat Pumps Membrane Processes U l t r a v i o l e t Cur ing

Microwave Processing

c -1 c - 3 c - 4

C-6 c - 7 C-8 c -9

D - 1

0- 1 0-6 D-17 D-32 D-42

i x

ILLUSTRATIONS

Fiqure

5-1

5-2

5-3

5-4

2-1

2-2

4-1

4-2

4-3

A - 1

A-2

A-3

8-1

8-2

8-3

8-4

B-5

8-6

8-7

8-8

B-9

The T e x t i l e Complex

Import Share o f T e x t i l e Markets

Basic Processes i n T e x t i l e Manufacturing

Importance o f E l e c t r i c i t y as an Energy Source:

Basic Processes i n T e x t i l e Manufacturing

Importance o f E l e c t r i c i t y as an Energy Source

Load P r o f i l e s f o r T e x t i l e M i l l s

U t i l i t y vs. Customer Benef i t s

I l l u s t r a t i v e DSM Plan: S t ra teg i c Conversation

The T e x t i l e Complex

End Uses o f T e x t i l e M i l l Products

1985 T e x t i l e Indus t r y Shipments by Sta te

Basic Processes i n T e x t i l e Manufacturing

Yarn Formation: Process Flow, Energy Inputs, and Process Outputs

Fabr ic Formation: Process Flow, Energy Inputs, and Process Outputs

F loo r Coverings: Process Flow, Energy Inputs, and Process Outputs

Nonwovens: Process Flow, Energy Inputs, and Process Outputs

T e x t i l e F in ish ing : Process Flow, Energy Inputs , and Process Outputs

1985 T e x t i l e Energy Use

1985 T e x t i l e Indus t r y E l e c t r i c i t y End Uses

1985 Manufacturing E l e c t r i c i t y Use by Region

T e x t i l e Indus t r y

5-2

5-5

5-8

s- 10

2-1

2-4

4-6

4-18

4-20

A - 2

A - 7

A-8

8-1

8-3

8-4

8-5

8-6

8-7

8-26

8-27

8-29

x i

ILLUSTRATIONS (Continued)

Figure

B-10

D- 1

D-2

D-3

0-4

D-5

D-6

D-7

D-8

D-9

D-10

D-11

D-12

D-13

D-14

1985 Process Heat Energy Sources

Dry ing o f T e x t i l e Spools

Closed-Cycle Heat Pump System

Open-Cycle Heat Pump

Open-Cycle I n d u s t r i a l Heat Pump

Permse lec t iv i t y o f RO and UF Membranes

General ized Schematic o f T e x t i l e Treatment Processes

Membrane-Based Hybr id L i q u i d Separation Process

Spiral-Wound, Hollow-Fine-Fiber, and Flat-Element Membrane

Cross Sect ion of a Tubular RO Membrane and Schematic o f a Tubular RO Membrane Module

The Separat ion Spectrum

UV Cur ing Process

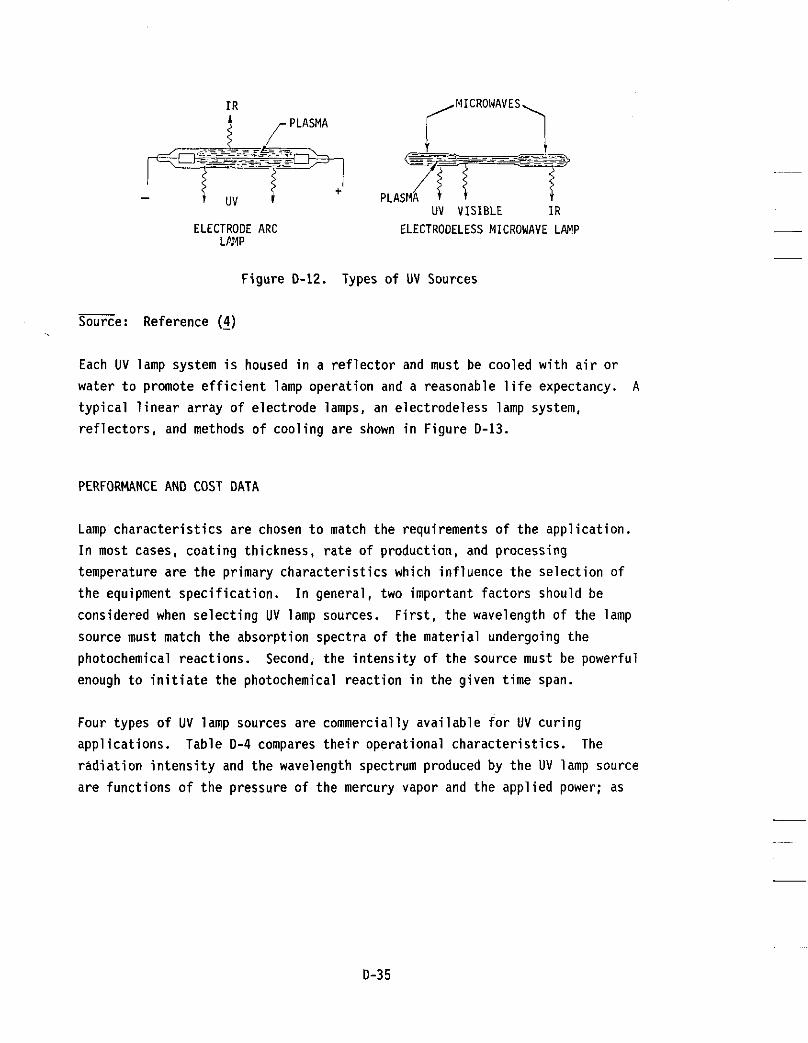

Types o f UV Sources

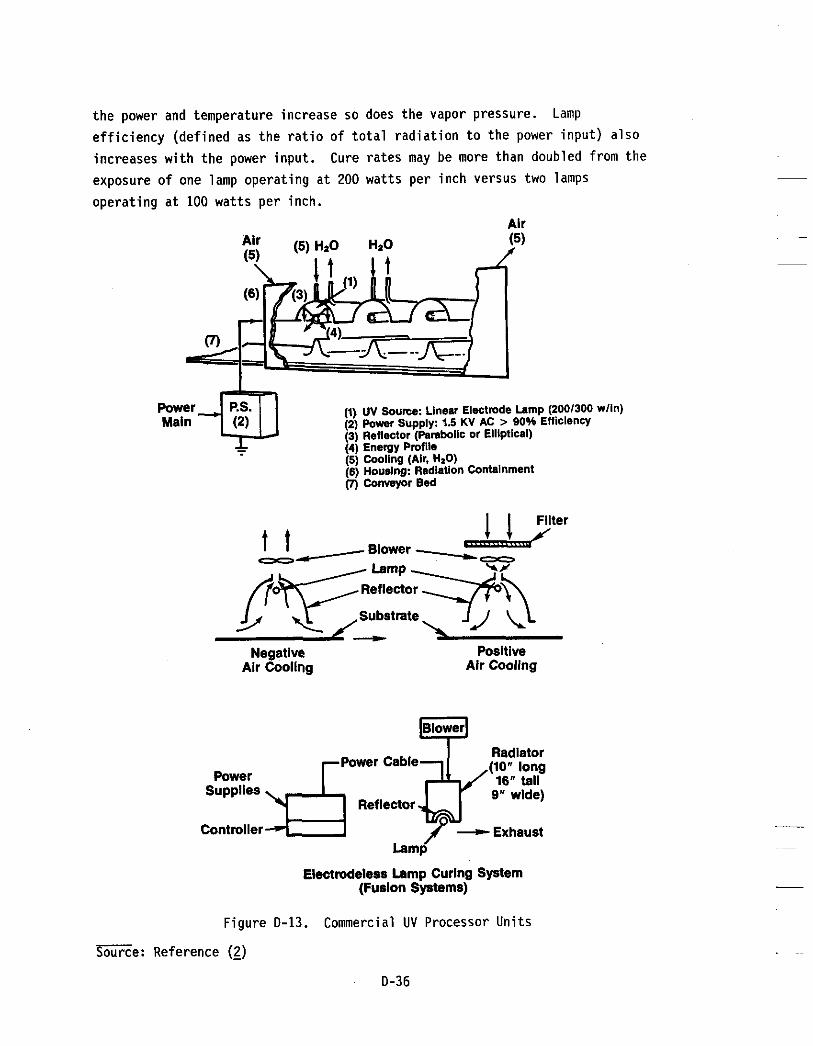

Commercial UV Processor Un i ts

Schematic Representation o f D i e l e c t r i c Hysteres is Heating

D-15 Comparison o f Microwaves and Conventional Drying

B-35

D-3

D-6

0-7

D-10

D-19

D-20

D-23

D-24

D-25

D-27

D-33

D-35

D-36

D-42

D-43

x i i

TABLES

s-1

S-2

s-3

s - 4

1-1

2 - 1

2-2

2-3

2 - 4

4-1

4-2

4 - 3

4-4

4 - 5

A-1

A-2

A-3

A-4

A-5

A-6

A-7

A-8

Textile Industry Summary: Industry Segments

Textile Industry Summary: Unit Processes or End Uses

Textile Industry Summary:

Textile Industry Summary: DSM Market Implementation Methods

Textile Industry Summary:

1985 Electricity Consumption by Specific Textile Processes

1985 Non-Electric Energy Consumption by Specific Textile Processes

Selected Competing Energy Technologies

1985 Textile Industry Electricity Costs and Intensity

Textile Industry Summary: lndustry Segments

Textile Industry Summary:

Textile Industry Summary:

Textile Industry Summary:

Textile Industry Summary:

1985 Overview of the U.S. Textile Industry

1985 Suppliers to the Textile Industry (Projected)

1985 Manufacturing Sector Suppliers to the Textile Industry (Projected)

1985 Manufacturing Sector Buyers of Textile Mill Products (Projected)

1986 Regional Manufacturing Activity

1985 Textile Industry Manufacturing Activity

1986 Regional Impacts o f Textile Manufacturing

Ratios of Primary Product Specialization in Selected Textile Mills (Percent)

DSM Technologies and Process Changes

DSM Technologies and Process Changes

Industry Energy Use

Unit Processes or End Uses

DSM Technologies and Process Changes

DSM Market Implementation Methods

xiii

5-14

5-17

5-20

5-23

1-8

2- 4

2- 6

2- 8

2-12

4- 4

4- 7

4 - 1 0

4 - 1 2

4-16

A- 2

A- 3

A- 4

A- 6

A-10

A-11

A-11

A-13

Table

A-9

A-10

A - 1 1

A-12

A-13

A-14

A-15

A-I6

A-17

B-1

8-2

8-3

8-4

B-5

B-6

8-7

B-8

B-9

B-10

B-11

B-12

TABLES (Continued)

Share o f T e x t i l e Shipments Accounted f o r by 20 Largest Companies (Percent)

Import Share o f T e x t i l e Markets (Percent)

Index o f Production f o r t h e T e x t i l e Indus t r y

Hourly Compensation Rates f o r T e x t i l e Production Workers

1983-1985 Permanent T e x t i l e Plant Closings i n the Southeast

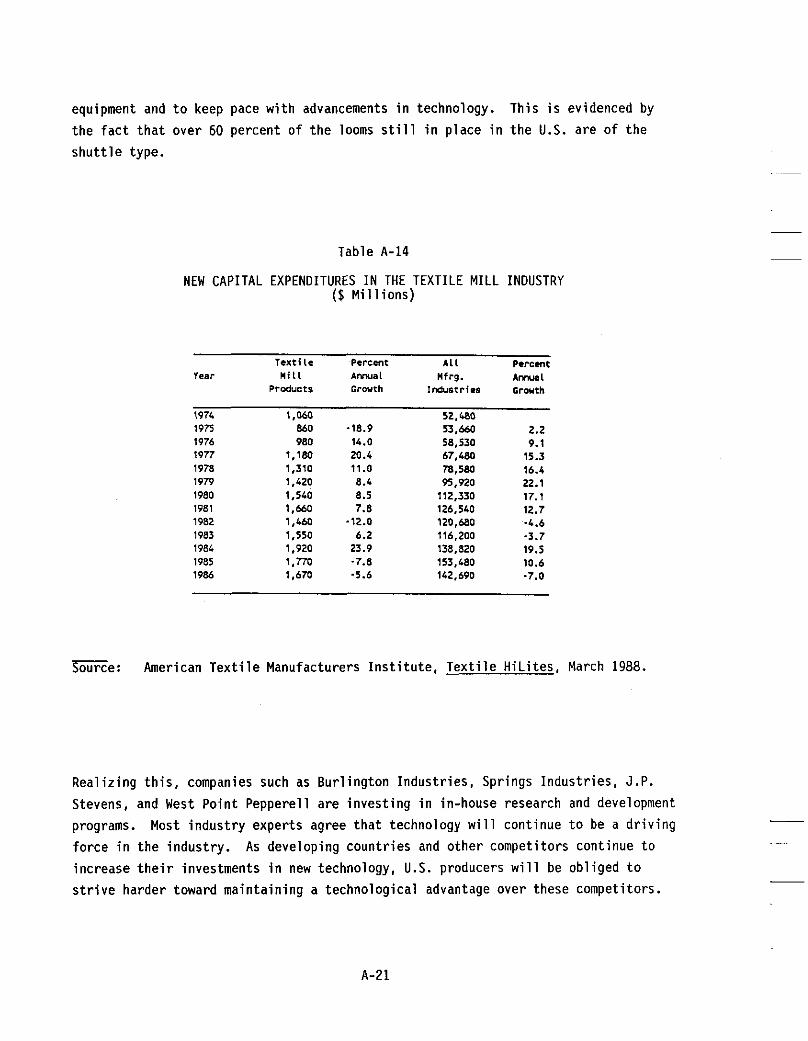

New Cap i ta l Expenditures i n t h e T e x t i l e M i l l I ndus t r y

Trends i n U.S. T e x t i l e Indus t r y P r o d u c t i v i t y ( P r o d u c t i v i t y Indexes - 1977 = 100)

Comparative Rates o f Modernization i n Spinning and Weaving, 1985 (Percent)

Import Share o f T e x t i l e Machinery Market (Percent)

Dry and Wet Processing M i l l s Categories

T e x t i l e Indus t r y Average Costs Per D o l l a r o f Output by Cost Category and 3 - D i g i t S I C , 1985

T e x t i l e Indus t r y U n i t Labor Cost by Type, 1985

Sta te-o f - the-Ar t Text i 1 e Manufacturing Techno1 og i es--Dry Processing

Sta te-o f - the-Ar t T e x t i l e Manufacturing Technologies--Wet Processing

Advanced T e x t i l e Manufacturing Technologies

Tota l Energy Consumption i n t h e T e x t i l e Indus t r y

1985 T e x t i l e Indus t r y Energy Costs and Energy I n t e n s i t y

Energy I n t e n s i t y i n t h e T e x t i l e Indus t r y

Energy P r o d u c t i v i t y Trends i n t h e T e x t i l e Indus t r y

E l e c t r i c i t y Consumption i n t h e T e x t i l e Indus t r y

1985 T e x t i l e Indus t r y E l e c t r i c i t y Use i n t h e Southeast

A-14

A-15

A-16 ~

A-18

A-20

A-21

~

A-23

A-24

A-25

B-8

8-14

8-16

B-18

8-20

B-21

B-22

B-22

B-24

8-24

B-26

8-29

x i v

TABLES (Continued)

6-13 Energy Consumption in Dry Processing Mills

6-14 1985 Electricity Consumption by Specific Textile Operation

6-15 Energy Consumption in Wet Processing Mills

6-16 1985 Non-Electric Energy Consumption by Specific Textile Processes

D-1 Summary of Capital and Operating Costs for Closed-Cycle Heat Pumps

D-2 Summary of Projected Capital Costs for New and Retrofit MVR Systems

D-3 Comparison of Types of Membrane Permeators

D-4 UV Lamp Operating Characteristics

D-5 Comparative Microwave Drying Data

6-31

6-32

6-34

6-36

D-13

0-14

D-28

D-37

D-45

xv

EXECUTIVE SUMMARY

Electricity is more than just the largest energy source for textile manufacturers; it is a unique and invaluable resource for improving their troubled competitive position. promise to increase significantly the efficiency and productivity of the industry.

Automation and emerging electric-based textile processing technologies

PURPOSE OF THE GUIDEBOOK

This Textile Industry Guidebook is designed to provide electric utility planning, marketing, and customer service staff with a practical tool to :

0 Understand the textile industry and the challenges it faces

0 Understand energy use and the different processes and technologies found within the industry

Identify and characterize opportunities for improving energy efficiency, enhancing productivity, and promoting load management as sound approaches that will benefit both the customer and the utility

Help develop a demand-side management (DSM) plan to realize such opportunities.

0

0

The purpose of this Executive Summary is to acquaint the reader with the primary conclusions of the study and the technical information covered in the Guidebook.

THE TEXTILE INOUSTRY

The textile mill industry produces spun yarns, thread, woven and knit fabrics, and floor coverings such as rugs and carpets. as synthetic leathers, and miscellaneous textile products such as tire cord.

It also produces nonwoven fabrics such

The textile mill industry (or for the purposes of this study, simply the textile industry) is part of the "textile complex," a system of independent enterprises

s- 1

involving many segments outside of SIC 22 and tied together by complex business relationships. Figure S-1 highlights some of the relationships between these segments.

Natural Fiber Manmade Fiber Producers Producers SICS 01,02 SIC 28

Furnishings SICS 22.23,25 SICS 26,30,

31,37.39

Figure S-1. The Textile Complex

In addition t o the textile industry (SIC 22), the textile complex consists of suppliers and markets for the textile industry. Suppliers include natural fiber producers in the agriculture industry (SICs 01 and 02), manmade fibers from the chemical industry (SIC 28), and textile machinery producers (SIC 3552). Markets include industrial fabrics (SICS 26, 30, 31, 37, and 39) , home furnishings (SICs 22, 23, and 25), and apparel (SIC 23).

The textile industry is its own biggest supplier, accounting for over 40 percent o f its inputs on a dollar basis. percent, and the agriculture sector accounts for another 8 percent.

The chemical industry represents nearly 30

The three major end-use markets (apparel fabrics, home furnishings, and industry fabrics) each account for about one-third of all textile industry shipments.

Standard Industrial Classification (SIC 22) consists of the following 3-digit SIC sectors:

SIC 221 - Cotton weaving mills SIC 222 - Manmade fiber weaving mills SIC 223 - Wool weaving and finishing mills SIC 224 - Narrow fabric mills SIC 225 - Knitting mills SIC 226 - Textile finishing (except wool) SIC 227 - Floor covering mills SIC 228 - Yarn and thread mills SIC 229 - Miscellaneous textile mills.

Reqional Impacts

Approximately 80 percent of the total U . S . textile shipments originate from the Southeast region, while about 9 percent of shipments originate from the Mid- Atlantic states of New Jersey, New York, and Pennsylvania.

Wool weaving and finishing mills (SIC 223) and narrow fabric mills (SIC 224) are concentrated in New England. This region accounts for 77 percent and 50 percent, respectively, of shipments in these two textile industry sectors. Due to the bulky nature of carpets (SIC 227), transportation costs are high, so floor covering mills are more widely dispersed in the U.S. than textile mills producing other textile products. California, Texas, North Carolina, and Tennessee.

Major carpet and rug mills are found in Georgia,

Industry Concentration

The textile industry consists of about 5,300 companies operating over 7,000 mills, ranging from highly integrated to small, independent plants. companies are small establishments performing single operations on a contract basis for other mills. The most common type of textile mill is the greige mill, in which spinning, knitting, and weaving operations are combined to produce greige goods--unfinished textile products.

Many of these

5-3

Industry concentration varies from segment to segment. The highest concentration ratios are found in the cotton and manmade fiber industries (SICs 221 and 222) where the 50 largest firms accounted for approximately 97 and 90 percent of shipments in those sectors, respectively. The four largest firms accounted for 41 and 40 percent, respectively. The industry segments with the lowest concentration ratios are the knitting mills, textile finishing, and yarn and thread mills. Many of these mills are small, independently owned operations.

With the recent number of mergers and acquisitions, these concentration ratios have increased considerably.

Production Costs

Production costs in the textile industry, as in all other manufacturing sectors, consist of labor, raw material, energy, and other costs such as the cost of financial and insurance services, capital charges, and non-production supplies. Across all 3-digit textile SIC categories, raw material costs account for 40-70 percent of the average costs per dollar of output, averaging about 60 percent.

Raw materials consist mostly of fiber or yarn staple. chemical dyes are also a major raw material. textile sector whose raw materials cost captures the largest share (69 percent) o f

a dollar of output.

In finishing plants, The floor coverings industry is the

Labor costs average about 22 percent per dollar of output in the textile industry, but is as high as 29.7 percent in narrow fabric mills (where considerable detailed work is required to produce specialty items such as laces, beltings, ribbons, and bindings) and as low as 11.9 percent in floor covering mills (SIC 227).

Fossil energy costs average about 1.3 percent of dollar output in SIC 22, but are higher in the textile finishing segment (SIC 226) due to the many fossil-fuel- based finishing and coating processes in that particular segment. Electricity cost per dollar of output in the textile industry as a whole averages about 2.3 percent. sector (SICs 20-39) averages about 1.4 percent. Spinning and weaving mills are the most electricity intensive. electricity costs are 3 . 9 percent, 3.5 percent, and 3.8 percent of shipments, respectively.

Electricity cost per dollar of output for the entire manufacturing

In these mills (SICs 221, 222, and 228)

s-4

BUSINESS AN0 PRODUCT TRENDS

In t h i s , t h e o l d e s t o f American manufacturing i ndus t r i es , many of the bas ic manufacturing methods have no t changed f o r decades o r longer. The t e x t i l e i ndus t r y i s conservat ive and has been slow t o accept techno log ica l change. Recently, however, cheaply produced fo re ign t e x t i l e products have gained a foo tho ld i n many domestic markets f o r c i n g we l l -es tab l i shed manufacturers t o reexamine t h e i r competit iveness. new chemical f i b e r s , and soph is t i ca ted t e x t i l e machinery must now be accommodated. Domestic and i n t e r n a t i o n a l compet i t ion and technology have combined t o fo rce changes i n t e x t i l e manufacturing methods.

R is ing labor costs , a rap id ly -g rowing array o f

R is ing imports o f t e x t i l e products now present a formidable economic t h r e a t desp i te steady increases i n shipments, m i l l consumption o f f i b e r , and capac i ty u t i l i z a t i o n . As shown i n F igure S-2, i n 1975, 14 percent o f a l l t e x t i l e goods so ld i n t h i s count ry were imported; over 37 percent were imported i n 1986. apparel f a b r i c s sector , impor ts captured over 50 percent o f t he market i n 1986.

I n the

Apparel and Apparel Fabric

1970 1975 1980 1985

Year

Figure S-2. import Share o f T e x t i l e Markets

s-5

Most U.S. i n d u s t r i e s have seen domestic market shares he ld by impor ts increase due t o a s t rong U.S. d o l l a r and a U.S. government p o s i t i o n favo r ing f r e e t rade. t e x t i l e i n d u s t r y s i t u a t i o n has been a d d i t i o n a l l y a f f e c t e d by i t s h igh l abo r i n t e n s i t y (some 22 percent o f t o t a l output d o l l a r s ) and by i t s dependence on f o r e i g n sources f o r t e x t i l e machinery. t e x t i l e machinery market. t o seek ways t o improve performance by working towards f i v e impor tant goals described i n t h e f o l l o w i n g paragraphs.

The

Imports ho ld nea r l y 60 percent o f t he This compet i t ion has forced t h e U.S. t e x t i l e i ndus t r y

Improving Labor P r o d u c t i v i t y

I n response t o increased f o r e i g n compet i t ion, t h e i ndus t r y i s now at tempt ing t o reduce the l a b o r content o f i t s products. employment dec l ined 15 percent w h i l e shipments increased by 13 percent. were a l so cut, and constant d o l l a r value-added per f u l l t ime equ iva len t employee i n t h e t e x t i l e i n d u s t r y grew f a s t e r than the average f o r a l l manufacturing. t e x t i l e f i r m s c u t l abo r costs , they increased c a p i t a l expenditures.

Between 1980 and 1985, t e x t i l e i ndus t r y Wages

A s

Improving Process E f f i c i e n c y

T e x t i l e manufacturing invo lves mu1 t i p l e , r e p e t i t i v e batch processing. This genera l l y requ i res considerable manual inspec t ion and i n t e r v e n t i o n because most technologies do n o t perform op t ima l l y o r lend themselves t o automation. In the pas t , workers had t o be employed t o de tec t and r e p a i r breakages r e s u l t i n g from poor f i b e r q u a l i t y and t o avoid over- o r under-processing o f f a b r i c i n the f i n i s h i n g processes. Now, automation i s made poss ib le by the increased use o f syn the t ics , more un i fo rm q u a l i t y i n na tu ra l f i b e r s , and advanced sp inn ing and weaving technologies.

Synthe t ic f i b e r s and improved na tu ra l f i b e r s e l im ina te t h e need f o r constant manual inspec t ion . New technologies o f f e r f a s t e r f i b e r and fab r i c processing speeds and d imin ish the r i s k o f expensive and t ime consuming breakage r e p a i r s . Today, some t e x t i l e producers are experimenting w i t h fas te r -d ry ing dyes and technologies designed t o e l im ina te many in termediate process steps. companies a re a l so moving toward computerized mon i to r ing and c o n t r o l o f product ion processes and automated inspec t ion procedures t o ensure f i b e r , yarn, and f a b r i c q u a l i t y a t a l l p roduc t ion stages.

T e x t i l e

S-6

Improving Product Quality

The development of durable synthetic fibers and higher agricultural standards for natural fibers has yielded improvements in yarn strength, uniformity, and cleanliness. o f which can be attributed to technology advances: improved fiber blends can be achieved by opening and picking equipment; new carding technology achieves better integration of fibers which results in fewer breakages; new loom designs process yarns at faster speeds; and state-of-the-art spinning machines produce first- quality fabric in a shorter period than conventional equipment.

These advances in fiber quality lead to higher fabric quality, much

Reducins Production Costs

Although the U.S. textile industry's productivity level grew at a faster rate than the average for all manufacturing between 1976 and 1986 (5.2 percent annually compared to 2.8 percent), additional productivity improvements must be realized to maintain a presence in today's competitive market. production costs through a number of methods. production processes, for example, combining processes or using faster-drying dyes, would allow products to get to market more quickly. developments in fiber and fabric types require that newly-developed production processes be carefully researched to ensure applicability to all fibers and fabrics.

Textile companies can lower Simplifying and accelerating

Today's rapid

Meeting Environmental Requlations

Electrotechnologies can be used, directly and indirectly, to meet federal, state, and local environmental restrictions placed on the textile industry. Direct environmental benefits from electrotechnologies appear to be promising. For example, membrane separation processes allow for recycling and recovery of useful thermal energy and chemicals used in textile drying and finishing, thus reducing the amount of hazardous chemicals disposed of by mills. Heat exchangers and heat recovery systems perform the same recycling task with similar advantages. Electricity used in lieu of conventional thermal processes eliminates or reduces point-source emissions. of conventional thermal energy processes are replaced with electric-based technologies.

This indirect benefit can be substantial if large numbers

s-7

MANUFACTURING PROCESSES AND ENERGY USE

Floor Covering

Formation -+ Formation Yarn

Typica l t e x t i l e manufacturing f a c i l i t i e s are made up o f one o r more o f f i v e bas ic processes: f a b r i c , f l o o r coverings, and nonwoven f a b r i c ) , and f i n i s h i n g . then be ca tegor ized i n t o two types o f processing, d r y and wet.

yarn formation, t h ree classes o f ma te r ia l format ion (woven/kn i t ted These processes can

I Finishing/

; Dyeing

I

Basic T e x t i l e Processes

I I I

Nonwoven

Figure categor ies.

5-3 dep ic t s t h e r e l a t i o n s h i p among these processes and processing Each o f t h e f i v e bas ic processes i s b r i e f l y descr ibed below.

b Fabric Formation

I

I

Wet Processing (Finishing Mills)

Dry Processing 1- (Greige Mills)

Figure S-3. Basic Processes i n T e x t i l e Manufacturing

Yarn Formation. var ious p i ck ing , combing, and t w i s t i n g processes. as p ick ing , card, and combing machines gather f a b r i c s l oose ly i n t o a c o r d - l i k e form known as a s l i v e r . increase al ignment, then through a rov ing frame t o apply t w i s t .

Natura l o r manmade f i b e r s o r blends are spun i n t o yarn through Yarn format ion equipment such

These s l i v e r s are passed through drawing frames t o

S-8

Woven o r K n i t t e d Fabr ic Formation. Fabr ic format ion i nvo l ves t h e conversion o f yarn i n t o f a b r i c . A warping machine winds numerous separate strands o f yarn onto a beam. s ta rch , wax, o i l s , and water, t o coat and strengthen t h e yarn i n p repara t i on f o r f u r t h e r processing. The yarn i s then woven o r k n i t t e d i n t o grey, o r unf in ished, f a b r i c .

A s lash ing machine t r e a t s t h e yarn w i t h a s ize , which i s a ho t s o l u t i o n o f

F l o o r Covering Formation. t u f t i n g , a process where yarn i s at tached t o t h e carpet backing d i r e c t l y .

F loo r coverings are produced e i t h e r by weaving o r by

Nonwoven Fabr i c Formation. bound toge the r us ing adhesive chemicals o r heat. i n t h e i n d u s t r i a l and home f u r n i s h i n g sectors. p e c u l i a r operat ions t o t h i s process.

I n nonwoven f a b r i c format ion, yarns o r f i b e r s are Nonwoven f a b r i c s a re mainly used

Web forming and bonding are

F in i sh inq . i nc lude bleaching, mercer iz ing, dyeing, san fo r i z ing , and heat s e t t i n g . These operat ions are designed t o impart q u a l i t i e s such as c o l o r fastness, f e e l , and p r o t e c t i o n f rom shrinkage.

F i n i s h i n g processes vary w i t h t h e f a b r i c and product end-use; they

These f i v e bas i c processes i n v o l v e numerous and sometimes r e p e t i t i v e batch operat ions, which can be placed i n t o two broad categor ies--dry and wet, depending on whether o r n o t a l i q u i d i s involved.

Dry processing o f t e n takes p lace i n gre ige m i l l s and inc ludes a l l t h e t e x t i l e processing operat ions t h a t take p lace through t h e stage where t h e yarn i s spun and t h e woven o r k n i t t e d grey f a b r i c i s formed (except s lashing) . opening, blending, carding, spinning, weaving, and k n i t t i n g .

They i nc lude

Wet processing i nvo l ves t h e m a j o r i t y o f processes t h a t dye o r f i n i s h t h e spun yarn o r woven/knit g r e i g e f a b r i c o r f l o o r covering. Also inc luded i n wet processing i s

s lashing, which takes p lace p r i o r t o f a b r i c o r yarn dyeing and/or f i n i s h i n g but invo lves t h e a p p l i c a t i o n o f l i q u i d chemicals t o t h e yarn. in tegrated.

Some m i l l s are now

s-9

T e x t i l e Indus t r y Energy Use

As shown i n F igure 5-4, e l e c t r i c i t y provides 31 percent o f the t o t a l energy used i n t h e t e x t i l e i n d u s t r y and represents t h e i n d u s t r y ' s l a r g e s t source. compares w i t h t h e market share o f 19 percent he ld by e l e c t r i c i t y f o r the e n t i r e manufacturing sec to r (SICS 20-39).

This

Coal 19%

Figure S-4. Importance o f E l e c t r i c i t y T e x t i l e Indus t r y as an Energy Source:

Less than one percent o f e l e c t r i c i t y i s self-generated. t e c h n i c a l l y v i a b l e op t i on f o r meeting some o f t h e i n d u s t r y ' s e l e c t r i c needs, due t o t h e l a r g e amounts o f process steam requ i red f o r d r y i n g and f i n i s h i n g , t h e existence o f waste products ( f i b e r s t h a t can be i nc ine ra ted ) , and t h e presence o f waste heat. However, many t e x t i l e p l a n t s are small establ ishments which may no t be able t o a f f o r d t h e c a p i t a l investment requ i red t o cogenerate.

Cogeneration i s a

The pr imary end uses o f e l e c t r i c i t y i n the t e x t i l e m i l l i ndus t r y are motor d r i v e , l i g h t i n g , and process heat.

e l e c t r i c i t y consumed i n the t e x t i l e m i l l i ndus t ry . L igh t i ng , represent ing 15 percent, i s t h e nex t l a r g e s t e l e c t r i c i t y consumer: process heat ing app l i ca t i ons represent on l y about 2 percent.

Motor d r i v e accounts f o r 83 percent o f t h e

Motor d r i v e e l e c t r i c i t y use i s broken down i n t o ma te r ia l s processing (45 percent ) , ma te r ia l s hand l ing (35 percent) , and pumps, fans, and compressors (about 20

s-10

percent). Materials-processing equipment performs the separating, combing, and other materials-processing steps that are carried out during spinning and weaving. Opening and card machinery, which use their steel fingers for plucking and combing, and spinning machinery, which twists and separates fibers, are materials- processing equipment.

Materials-handling activities take place throughout textile manufacturing, starting from the rotating fiber-opening machinery to finishing, where fabric is printed or heat set using rollers and rolling frames. Materials handling also takes place during fabric formation where bales of fiber are moved through the mill.

Pumps, fans, and compressors account for a large portion of the electricity used in HVAC systems. About 20 percent of the energy used in finishing mills is electricity, mostly to power small motors scattered through the mill. Pumps are used for fluid processing in dyeing to pump dyes, rinse water, and other liquids into and out of dye becks. and finishing and for blowers in opening and blending machines.

Fans are also used in convection ovens used for drying

Textile Plant Enerqy Use and DSM Opportunities

The importance of energy in a particular textile mill depends on the type o f

processing that is done at the mill--wet or dry. In general, dry processes are electricity intensive while wet processes are fossil-energy intensive.

Dry Processing. The spinning, twisting, and weaving processes performed in these mills require considerable amounts of motive power. operations performed in the dry processing mill use electricity as the primary energy source. boilers burning natural gas, coal, fuel oil, or other petroleum products.

Except for slashing, all

Steam used in the slashing operation is usually generated by

Electricity supplies about 80 percent of the total energy requirements in greige mill (dry mills). in dry processing. Most of the increases will come from automation programs. A s more companies automate their plants and install computerized systems for process control, their reliance on uninterrupted electric power will increase, but only slightly.

There are few opportunities for further electricity penetration

New technology developments that might increase electricity consumed by

s-11

drive motors include mechanical moisture-removal devices such as vacuum extractors and roller squeezers.

Since a typical greige mill will have many motors running during a normal work day, there are numerous opportunities for conservation and load management in dry processing. For example, high-efficiency electric motors with adjustable speed drives can help this equipment run more efficiently, reducing overall electricity costs.

HVAC systems are also very important in greige mills because they must work with the machinery to filter out the large amounts of debris, lint, and other material generated during production processes. Impaired air quality from the collection of cotton dust in the air, for example, may create a hazard to operators as well as a risk of potentially fouling the machinery. Opportunities for heat recovery exist for HVAC systems designed to capture waste heat from machinery and redirect it into the ventilation system, thus eliminating hot spots. More-efficient spinning, weaving, and knitting technologies will also provide opportunities for conservation.

Wet Processinq. mainly to heat liquids and chemical dyes and to dry and finish textiles. heating is dominated by fossil fuels because they can heat evenly and inexpensively with readily available technologies. In textile processing, the quantity of heat, temperature, and method of application varies widely. Some methods (such as singeing) require direct applications of open flame, eliminating the possibility of electric process heat applications. Others require steam cans or calendars for the application of heat and pressure. In all cases the application and maintenance of a certain temperature is crucial to avoid over- or under-processing. The design and application flexibility of gas equipment allows ready application of heat in those processes where heat is required.

Wet processing often requires large inputs of thermal energy, Process

The textile firm's ability to modify electricity use is more pronounced in wet processing applications than in dry. spun yarn and woven or knit greige fabric. process called slashing, which takes place prior to fabric or yarn dyeing and/or finishing and involves the application of liquid chemicals to the yarn in order to improve weaving efficiency by strengthening the yarn. technologies now compete with conventional fossil-fuel-fired technologies for

The majority of wet processes dye or finish Also included in this category is a

A variety of electric

5-12

s lash ing , d ry ing , dyeing, and cur ing . Approaches f o r modi fy ing e l e c t r i c i t y use i n wet processing inc lude:

0 Increased app l i ca t i ons o f process heat ing technologies --Radiofrequency - - I n f r a r e d ' - - U l t r a v i o l e t cu r ing

--Membrane s e p a r a t i o d f i l t r a t i o n techniques - - I n d u s t r i a l process heat pumps/heat recovery systems --Thermal energy storage - -U l t rason ics --Process automation.

Examples o f i n s t a l l a t i o n s i nc lude us ing i n d u s t r i a l process heat pumps and

f i l t r a t i o n techniques t o recover waste chemicals and us ing e l e c t r i c heat ing technologies t o rep lace convent ional dyeing and d r y i n g processes. HVAC oppor tun i t i es a l s o e x i s t . t h e removal o f vapors, odors, fumes, and o the r contaminants.

0 Increased app l i ca t i ons o f o the r e lect ro technologies

F i n i s h i n g p lan ts r e q u i r e l a r g e v e n t i l a t i n g systems f o r

GETTING STARTED: CHARACTERIZING POTENTIAL DSM OPPORTUNITIES

As noted p rev ious l y , e l e c t r i c u t i l i t i e s have many oppor tun i t i es t o he lp t h e t e x t i l e i n d u s t r y f u r t h e r improve i t s compet i t ive p o s i t i o n , w h i l e a t t h e same t i m e

advancing u t i l i t y DSM ob jec t i ves . These oppor tun i t i es range from o v e r a l l energy conservat ion, t o load management, t o t h e a p p l i c a t i o n o f s p e c i f i c e l e c t r o - technologies.

I n he lp ing t o understand t h e t e x t i l e i ndus t r y and i t s p o t e n t i a l DSM oppor tun i t i es , a se r ies o f f o u r t a b l e s has been developed t o prov ide a f i r s t s tep i n c h a r a c t e r i z i n g t h e a v a i l a b l e DSM opt ions and t o summarize t h e techn ica l i n fo rma t ion prov ided i n t h i s Guidebook.

Please note t h a t t h e i n fo rma t ion represented i n each o f t h e tab les r e f l e c t s

t y p i c a l t e x t i l e p lan ts . Because s i g n i f i c a n t v a r i a t i o n s i n p l a n t design and processing equipment e x i s t , caut ion i s requi red i n us ing t h i s in format ion.

I ndus t r y Seqments

The f i r s t t a b l e (Table t h r e e - d i g i t S I C segments o f t h e t e x t i l e indus t ry .

S -1 ) summarizes t h e key c h a r a c t e r i s t i c s o f t h e n ine The in format ion includes key

S-13

T a b l e S - l

TEXTILE INDUSTRY SUMMARY: INDUSTRY SEGMENTS

industry Segment

(3-Digit Sic)

industry Trendrl comments

Industry Products

2 1 . Cotton Weaving

),err, uphoirtery. and surgical abricr

Growthin home furnishin in durtrial.and medical mar?&;

De<iinemapparel markets More CanlinuOuS produdion More frequent air changer fOT

Domination byaiviet looms product quality

12 . Manmade Fib, Weaving

I r e s . drapery. upholrlery ibergiarr.ilnd automotive abri'r

Growth in automotive and

More v"nuOus production More frequent air changer for

Domination byair.jet looms

Detline in apparel markets Espetiaily strong Lompetifion

Somespare 'apacityfar DSM Small part of textile industry

industria markets

product quality

from import i

13 - Wool Weavins Finishing

lianketi and overmat material ,nd other woolen fabrics

24. Narrow Fabric Mills

libbonrand bindings Growth in woven label. eiastx tape. and zipper markets

Decline in other markets small partoftextile industry

;iris'. boys', women'r.and men's mriery, bathing suits. neckties. lati, knitted underwear and Lightwear. jersey fabrics. lace ioodr. gloves. mittenr. and

2 5 - Knitting Mills

iedtpr&dr

>ved finished fabrics. dved Growth in blocked knits Batchdyeing has reduced dveina time

1 6 - Textile Finishing

. . ii irhed broadwoven fabrics. 8nd dyed finished narrowfabrics Inb;a& in the ele<trir

requirements from continuous d eing printing,and bLsch;na oro~e ises

Growth in tufted nylon carpst and offire carpet square1 markets

Growth in the YIB of open-end and air-Jet spinning

2 1 - Floor Coverin, Mi lk

Growth in rewing thread and textured nylon markets

Most plants havealready modernized

Growth of opemend spinning Detiine of ring spinning

Growth in syntheticnonwoven felts forautomotive. carpet. andfurniture markets

Decline in lace and upholstery padding

Growth in coated fabrics

28 - Yarnand Thread Mills

farnr, spooled yarnr.and1hread )f allfibertypes

29. Miscellaneou Textiles

mgtalion leather. o i l h t h . tire :ord. bonded fiber fabrics. braidei :ord. feitr. piiiawfiliingr. pips :overing. burlap,and other onw woven fabrics

S-14

Table S - 1 (Continued)

AppraximateAllo~atlonof EnergyUfeAmang Unif Pio~errerorEndUrer. %*

T m

'I. 0 -

/ 51

-

i

/

/

i

i

/

i i

37 -

4

-

23 -

23

-

21

-

32

30

-

25

- 14 and Waste

-

:"el Mark6 Shares by lndurtry

Segment. peK.e"l

5-15

i ndus t r y products, summary i n d i c a t o r s , i ndus t r y t rends , and energy use by u n i t process est imates.

As shown i n Table range from 0.7 percent f o r F loo r Covering M i l l s ( S I C 227) t o 3.9 percent f o r Cotton Weaving ( S I C 221). ( S I C 22) i s 2.3 percent; t h i s percentage i s q u i t e a b i t h ighe r than t h e 1 .4

percent f o r a l l o f manufactur ing ( S I C S 20-39). Th is suggests t h a t , on t h e whole, t e x t i l e customers should be more i n t e r e s t e d i n assessing t h e i r use of e l e c t r i c i t y than t h e average i n d u s t r y customer.

S-1 , f i g u r e s f o r "Purchased E l e c t r i c i t y as a % o f Shipments"

The e l e c t r i c i t y percentage f i g u r e f o r a l l o f t e x t i l e s

The opera t i ng p a t t e r n f i g u r e s d e p i c t t h e t e x t i l e i n d u s t r y as genera l l y running th ree s h i f t s pe r day, f i v e days a week w i t h an e x t r a catch-up and maintenance s h i f t on Saturdays. of p a t t e r n i s genera l l y no t favorable f o r major amounts o f load s h i f t i n g .

As a process i ndus t r y w i t h a h i g h l a b o r i n t e n s i t y , t h i s type

The f i g u r e s r e f l e c t i n g t h e a l l o c a t i o n o f energy use among u n i t process o r end uses c l e a r l y show t h e degree o f e l e c t r i c i t y use i n t h e d r y processing a c t i v i t i e s (spinning, weaving, etc.) versus t h e degree o f f o s s i l - f u e l use i n t h e wet processing a c t i v i t i e s (dyeing, d ry ing , f i n i s h i n g , etc.) . With t h e process heat ing e lec t ro techno log ies (radiofrequency, i n f ra red , etc.) t a rge ted on many o f those wet

processing a c t i v i t i e s , i t i s easy t o see how a small percentage o f market pene t ra t i on by these e lect rotechnologies could y i e l d s i g n i f i c a n t changes i n e l e c t r i c use.

holds a 31-percent f u e l market share, t h e average market share f o r i n d i v i d u a l i ndus t r y segments ( 3 - d i g i t S I C S ) va r ies s i g n i f i c a n t l y f rom 11 percent t o 59 percent.

Even though i n t h e e n t i r e t e x t i l e i n d u s t r y (SIC 2 2 ) , e l e c t r i c i t y

Add i t i ona l i n d u s t r y and business t rend in format ion about t h e t e x t i l e i n d u s t r y i s provided i n Appendix A.

I ndus t r y Processes and End Uses

The second t a b l e (Table processes i n t h e t e x t i l e i ndus t r y . p o t e n t i a l o f each u n i t process f o r achieving a l t e r n a t i v e load shape ob jec t i ves and notes regard ing processing t rends f o r each u n i t process i n t h e t e x t i l e i ndus t r y .

S-2) summarizes t h e c h a r a c t e r i s t i c s o f t h e key u n i t Included are i n d i c a t o r s o f the r e l a t i v e

S-16

- I < A

- r ID 2 5 Y

-i m x 2 r- m

z 0 t VI + W < VI c x zz D

-

2 .. c z -i

m W 0 0 m VI VI m VI

0 W

m z 0 c VI m VI

-

The opportunities for strategic load growth are primarily in the electrification of processes previously served by competing fuels. The most opportune processes include warping/slashing, washing, dyeing, drying, and finishing. of these processes fall into the wet processing category.

Naturally, most

Strategic conservation opportunities exist in wet as well as dry processing. Solid opportunities also exist in plant services, particularly in HVAC and materials hand1 ing.

Load manaqement opportunities are tied to the ability of customers to modify existing loads and/or timing of electricity consumption. management opportunities exist i n plant services.

Most of the load

Flexible load shape programs have only limited application in the textile industry. and finishing.

The major application areas are HVAC, opening/blending/picking, drying,

Some of the major processing trends featured in the table include:

0 Increase of open-end spinning

0 Potential penetration of radiofrequency into warping and slashing processes and into drying of bulky packages of fiber and yarn

0 Growth of air-jet looms

0 Trend toward combining desizing with scouring and bleaching (DSB)

0 Development of more-efficient technologies and processes for dyeing and finishing

Growth of automation and shop floor communications systems for materials handling

0

0 Increased regulatory scrutiny over waste treatment and plant ambient conditions.

Descriptions of these unit processes can be found in Appendix 8; additional process information can be found in the U.S. Department of Energy study on textile industry energy use (1).

S-18

DSM Technologies and Process Chanqes

Numerous opt ions ho ld p o t e n t i a l f o r s i g n i f i c a n t p r o d u c t i v i t y improvements, as

w e l l as p o t e n t i a l f o r some f a i r l y l a rge energy-use changes. The key technologies i n the t e x t i l e i ndus t r y appear t o be t h e process heat ing opt ions ( i n f r a r e d , radiofrequency, u l t r a v i o l e t , and u l t rason ics ) , HVAC-related op t ions ( a i r supply and c h i l l e r system op t im iza t i on ) , and the energy -e f f i c i en t and env i ronmenta l ly o r i en ted opt ions ( i n d u s t r i a l process heat pumps, h i g h - e f f i c i e n c y motors, process automation, and membrane processing).

The t h i r d t a b l e (Table 5-3) summarizes the DSM technology and process change oppor tun i t i es i n t h e t e x t i l e indust ry . The in fo rmat ion inc ludes l i s t s o f t he load shape ob jec t ives , u n i t processes, and indus t r y segments f o r which any o f 30 d i f f e r e n t DSM technologies and process changes are app l icab le . t he p o t e n t i a l impacts, compet i t ion, and t rends associated w i t h the technology.

Also inc luded are

As mentioned be fore , these summary tab les are intended as a s t a r t i n g p o i n t on ly . Var ia t ions i n a p p l i c a b i l i t y may r e s u l t due t o unique cond i t ions a t a customer's p lan t . Add i t i ona l in fo rmat ion about some o f t he process heat ing, energy- e f f i c i e n t , and env i ronmenta l ly o r ien ted opt ions can be found i n Appendix D.

Add i t iona l i n fo rma t ion about the HVAC-related and conservat ion-re la ted opt ions can be found i n Appendix E and i n t h e U.S. Department o f Energy study on t e x t i l e i ndus t r y energy use( ' ) .

DSM Market Implementation Methods

Due t o the h igh d i v e r s i t y o f t h e i n d u s t r i a l sector , customer needs and bene f i t s associated w i t h a DSM program may vary by s i z e and type o f customer. requ' ire d i f f e r e n t market implementation methods f o r d i f f e r e n t customer segments. Applying t h e appropr ia te market implementation method t o a s p e c i f i c techn ica l a l t e r n a t i v e requ i res i n s i g h t s i n t o t h e technology and t h e customer's dec is ion-

making process. appropr ia te implementation methods the re are a few gu ide l ines .

This may

While i t i s d i f f i c u l t t o genera l i ze the se lec t i on o f t he

Market implementation methods are v i t a l i n enhancing t h e market penet ra t ion o f DSM programs. cooperation, customer in fo rmat ion , d i r e c t customer contac t , d i r e c t i ncen t i ves , and a l t e r n a t i v e p r i c i n g .

These methods may be grouped i n t o f i v e major categor ies: t rade a l l y

s-19

T a b l e S-3

T E X T I L E INDUSTRY SUMMARY: DSM TECHNOLOGIES AND PROCESS CHANGES

ApplKable Load Shew Applinble UnitPIoccsIeI olEndUILI Objartwrs

s-20

Table S-3 (Continued)

Appli'abl* Industry Segments I

s-21

The f o u r t h t a b l e (Table methods can be used t o f o s t e r customer adoption o f t h e DSM technology o r process change oppor tun i ty . promoting each o f t h e 30 DSM technologies o r process changes. a l so inc luded t o p rov ide contex t f o r such promotional a c t i v i t i e s .

S-4) summarizes how the var ious market implementation

The in fo rmat ion i nd i ca tes how use fu l each method i s i n Marketing notes a r e

In programs i n v o l v i n g new technologies, customers face considerable u n c e r t a i n t i e s w i t h regard t o performance and appropr ia te app l i ca t i on . technology a p p l i c a t i o n and t e s t i n g centers, case s tud ies , t r a i n i n g seminars, performance warrant ies, and t rade a l l i e s are appropr ia te methods f o r reducing such unce r ta in t y . Customer aud i t s are use fu l i n i d e n t i f y i n g showcase app l i ca t i ons .

Demonstration p r o j e c t s ,

For programs i n v o l v i n g proven technologies, u t i l i t i e s can focus t h e i r resources on q u a l i f y i n g leads and p rov id ing f i n a n c i a l incent ives . De ta i l ed f e a s i b i l i t y s tud ies are needed f o r those proven technologies w i t h app l i ca t i ons and economic assessments t h a t are p a r t i c u l a r l y s i t e - s p e c i f i c o r are being implemented f o r the pr imary purpose o f t a k i n g advantage o f a l t e r n a t i v e p r i c i n g programs o r load management.

Another f a c t o r i n f l u e n c i n g implementation methods i s s e n s i t i v i t y t o cos t . programs focus on a p p l i c a t i o n areas where e l e c t r i c i t y i s i n d i r e c t compet i t ion w i t h o ther f u e l s o r non -e lec t r i c processes. Here f i n a n c i a l i ncen t i ves such as promotional r a t e s o r rebates a re appropr ia te.

Some

F i n a l l y , t he re i s t h e degree o f con t ro l t he u t i l i t y has over the program implementation. In some cases a u t i l i t y w i l l have on ly i n d i r e c t con t ro l over i ndus t r y o r technology trends. For example, t he swi tch t o a i r - j e t processing i n a

t e x t i l e m i l l i s in f luenced by many f a c t o r s ou ts ide the sphere o f i n f l uence o f a

u t i l i t y . However, u t i l i t i e s may in f l uence technology choices i n d i r e c t l y through j o i n t a d v e r t i s i n g programs o r by working w i t h engineering f i r m s o r t rade associat ions.

Special s i t u a t i o n s w i t h regard t o t h e customer o r t he program may warrant dev ia t i on f rom these general gu ide l ines . categor ies o f market implementation methods are provided i n Sect ion 4. equipment vendors f o r severa l o f t h e key DSM technologies i s provided i n Appendix C.

B r i e f desc r ip t i ons o f t he f i v e major A l i s t o f

s-22

Technologies

Changer

Ulilviolet Cvring

Open.End Spinning

Air.leIPiO~esting

Foam Prortrfing

T a i l Lighting

High-Ellicirnry Lightin!

T a b l e S - 4

T E X T I L E INDUSTRY SUMMARY: DSM MARKET IMPLEMENTATION METHODS

ApplVable Marketlmplt

Electric utilities need to work closely with their textile customers to take advantage of DSM opportunities. is a major barrier. Several factors argue for an increased utility focus on textile customers to help overcome this barrier:

Lack of convincing and demonstrable information

Underestimated impact of electricity. The potential impact of electricitv on textile manufacturina is considerablv underestimated bv most textiie firms.

Greater consideration is given to raw materials (such as fiber and chemicals) and labor, yet energy cost per dollar of value added to the textile industry is 9 . 3 percent; significantly higher than the 6 percent value for all manufacturing. Similarly, electricity costs per dollar of value added exceeds that for all manufacturing.

Many textile companies do not consider either energy ~

or electricity to be important inputs to their production process. -~

Lack of widespread information about electrotechnologies and DSM nroorams. New. efficient electrotechnolooies are not beina aoolied in

~ ~d ~~ ~~~ ~ . . . ..... .

iexzile mills as often as they could be. will not sell on their inherent advantages (faster speeds, energy and space savings) alone because the textile industry is not as energy- conscious as many other industry sectors. In addition, cost-cutting opportunities resulting from other DSM programs await action by the industry.

These technologies iipically

Lack of information about electricity consumption. Few firms monitor mill enerav consumotion at the level where energy characteristics for each process are known with certainty. energy standards to facilitate energy cost reduction is hampered.

Without-this information, setting

The electric utility industry can play a significant role in informing its textile customers of the benefits of existing and emerging technologies and DSM programs. This can assist utilities in competing with fossil-fuel technologies, in retaining customers, and in achieving their DSM objectives. The DSM efforts of many utilities (especially those in the Southeast) could be hindered without a strategic plan designed to include textile customers.

REFERENCE

1. Badin, Joseph S . and Lowitt, Howard E., Energetics, Incorporated, The U.S. Textile Industry: An Energy Perspective, U.S. Department of Energy through its Pacific Northwest Laboratory, Report DOE/RL/D1830--T56, Washington, D.C., January 1988. -

s-24

Section 1

OVERVIEW OF THE TEXTILE INDUSTRY

Electric utilities are vital allies of their textile customers. The textile industry relies heavily on electricity. It is used far more than natural gas, fuel oil, or any other single energy source. textile manufacturing processes and faces little competition in many applications.

Electricity powers and controls most

Electricity is more than just another energy source for textile manufacturers; it is a unique and invaluable resource for improving their troubled competitive position. Automation and emerging electric-based textile processing technologies promise to increase the efficiency and productivity of the U.S. textile industry. impacts of electrotechnologies grow, electricity will increase even more in importance to textile producers.

As the

PURPOSE OF THE GUIDEBOOK

This Textile Industry Guidebook is designed to provide utility planning, marketing, and customer service staff with practical information to explore and implement demand-side management (DSM) programs. DSM focuses on planning and implementing utility activities designed to influence customer electricity use in ways that benefit both the utility and the customer. Activities falling under the industrial DSM umbrella include load shaping programs, electrotechnology marketing, rate programs, conservation and productivity audits, rebate and trade ally programs, economic development, standby generation programs, and other customer-oriented programs. representatives, field sales staff, and strategic planners to:

In particular, the Guidebook is designed to aid utility marketing

0

0

Understand the textile industry and the challenges it faces

Understand energy use and the different processes and technologies found within the industry

Identify and characterize opportunities for improving energy efficiency, enhancing productivity, and promoting load management as ways to benefit both the customer and the utility

Develop a demand-side management (DSM) plan to realize such opportunities.

0

0

1-1

The Guidebook exp la ins the s i g n i f i c a n t impacts o f e l e c t r i c i t y on t e x t i l e i ndus t r y p r o d u c t i v i t y and describes t y p i c a l app l i ca t i ons and b e n e f i t s o f e lec t ro techno log ies and DSM programs i n t e x t i l e processing. about t e x t i l e i ndus t r y needs and t h e r o l e o f e l e c t r i c i t y i n meeting these requirements. s t a f f t o i d e n t i f y and work w i t h t h e i r customers' p l a n t managers, energy dec is ion makers, and equipment supp l ie rs t o implement decis ions f o r the mutua l l y b e n e f i c i a l use o f e l e c t r i c i t y i n t e x t i l e m i l l s . Factors and approaches t h a t can enhance t h e t e x t i l e i n d u s t r y ' s acceptance o f u t i l i t y OSM s t ra teg ies and steps t o design and implement a market ing p lan ta rge ted a t t e x t i l e i ndus t r y customers are a l so examined.

The Guidebook provides d e t a i l e d in fo rmat ion

,It a lso provides an easy-to-use se t of gu ide l ines t h a t a l l ow u t i l i t y

THE TEXTILE INDUSTRY

The t e x t i l e i n d u s t r y produces spun yarns, thread, woven and k n i t f a b r i c s , and f l o o r coverings such as rugs and carpets. miscellaneous t e x t i l e products such as t i r e cord, cordage, and twine. I n d u s t r i a l C l a s s i f i c a t i o n (SIC) 22 cons is ts o f the f o l l o w i n g 3 - d i g i t S I C sectors:

It a lso produces nonwoven f a b r i c s and Standard

S I C 221 - Cotton weaving m i l l s

S I C 222 - Manmade f i b e r weaving m i l l s

S I C 223 - Wool weaving and f i n i s h i n g m i l l s

S I C 224 - Narrow f a b r i c m i l l s

S I C 225 - K n i t t i n g m i l l s

S I C 226 - T e x t i l e f i n i s h i n g (except wool)

S I C 227 - F loo r cover ing m i l l s

S I C 228 - Yarn and thread m i l l s

S I C 229 - Miscellaneous t e x t i l e m i l l s .

There are over 7,000 t e x t i l e m i l l s i n t h e Uni ted States. The t e x t i l e i ndus t r y i s highly-concentrated, w i t h about 80 percent o f t h e i n d u s t r y ' s products o r i g i n a t i n g from t h e Southeast. Carol ina, Georgia, Alabama, Tennessee, and V i r g i n i a . I n 1985, t e x t i l e shipments from these s i x s ta tes represented approximately 75 percent o f the t o t a l shipments f o r S I C 22. Apparel f a b r i c s , home fu rn ish ings , and i n d u s t r i a l f a b r i c s , such as f i b e r - r e i n f o r c e d components and f i b e r s used i n the medical, m ic roe lec t ron i c , pharmaceutical, defense, and aerospace sectors, are the l a r g e s t end users of

The m a j o r i t y o f t h e m i l l s are loca ted i n North and South

1-2

manufactured t e x t i l e goods. and 31 percent, respec t i ve l y , o f a l l t e x t i l e m i l l shipments i n 1985.

These th ree major end-use sectors accounted f o r 35, 33 ,

BUSINESS AND PRODUCT TRENDS

In t h i s , t h e o l d e s t o f American manufacturing i n d u s t r i e s , many o f t h e bas ic manufactur ing methods have n o t changed f o r decades o r longer. i s conservat ive and has been slow t o accept technologica l change. however, cheaply produced f o r e i g n t e x t i l e products have gained a foo tho ld i n many domestic markets f o r c i n g wel l -estab l ished manufacturers t o reexamine t h e i r competit iveness. f i b e r s , and soph is t i ca ted t e x t i l e machinery must now be accommodated. i n t e r n a t i o n a l compe t i t i on and technology have combined t o f o r c e changes i n t e x t i l e manufacturing methods.

The t e x t i l e i ndus t r y Recently,

R is ing l abo r cos ts , a r a p i d l y growing a r ray o f new chemical Domestic and

R is ing imports o f t e x t i l e products now present a formidable economic t h r e a t despi te steady increases i n shipments, m i l l consumption o f f i b e r , and capaci ty u t i l i z a t i o n . I n 1975, 14 percent o f a l l t e x t i l e goods so ld i n t h i s country were imported; over 37 percent were imported i n 1986. In t h e apparel f a b r i c s sec tor , impor ts captured over 50 percent o f t h e market i n 1986. Four major f a c t o r s account f o r t h i s sharp r i s e i n imports. F i r s t , a s t rong U.S. d o l l a r du r ing t h e e a r l y 1980s made imports r e l a t i v e l y inexpensive compared t o domestic goods. Second, t h e U.S. Government's p o s i t i o n f a v o r i n g f r e e t r a d e meant t h a t t he re were no b a r r i e r s f o r t e x t i l e producers in newly i n d u s t r i a l i z e d and developing nat ions. the same modern t e x t i l e machinery t h a t has improved t h e U.S. t e x t i l e manufacturing. F i n a l l y , l a b o r costs overseas are o n l y a f r a c t i o n o f those i n t h e United States.

Th i rd , many o f these coun t r i es invested i n

This compet i t ion has fo rced t h e U.S. t e x t i l e i ndus t r y t o reexamine market ing s t r a t e g i e s and t o seek ways t o improve performance by working toward several important goals:

Improvins Labor P r o d u c t i v i t y

T r a d i t i o n a l l y , t h e t e x t i l e i ndus t r y has been h i g h l y l abo r i n tens i ve . ranks s i x t e e n t h i n value o f shipments when compared t o a l l o the r manufacturing i ndus t r i es ; however, i t i s t h e t e n t h l a r g e s t i n d u s t r i a l employer, and over 80 percent o f i t s l a b o r f o r c e i s employed i n product ion.

The indus t r y

In response t o increased

1-3

foreign competition, the industry is now attempting to reduce the labor content of its products. percent while shipments increased by 13 percent. dollar value-added per full time equivalent employee in the textile industry grew faster than the average for all manufacturing. As textile firms cut labor costs, they increased capital expenditures. As a result, the industry's capital ~

expenditure increased from $2,110 per production worker in 1980 to nearly $3,300 per production worker in 1985.

Between 1980 and 1985, textile industry employment declined 15 Wages were also cut, and constant

-~

Improving Process Efficiency

Textile manufacturing involves multiple, repetitive batch processing. This generally requires considerable manual inspection and intervention because most technologies do not perform optimally or lend themselves to automation. In the past, workers had to be employed to detect and repair breakages resulting from poor fiber quality and to avoid over- or under-processing of fabric in the finishing processes. more-uniform quality in natural fibers, and advanced spinning and weaving technologies. constant manual inspection. New technologies offer faster fiber and fabric processing speeds and diminish the risk of expensive and time-consuming breakage repairs. Today, some textile producers are experimenting with faster-drying dyes and technologies designed to eliminate many intermediate process steps. Textile companies are also moving toward computerized monitoring and control of production processes and automated inspection procedures to ensure fiber, yarn, and fabric quality at all production stages.

Now, automation is made possible by the increased use of synthetics,

Synthetic fibers and improved natural fibers eliminate the need for

Improving Product Quality

With the development of durable synthetic fibers and higher agricultural standards for natural fibers, yarn strength, uniformity, and cleanliness have been improved. These advances in fiber quality lead to higher fabric quality, much of which can be - attributed to technology advances: and picking equipment; new carding technology achieves better integration of fibers which results in fewer breakages; new loom designs process yarns at faster speeds; and state-of-the-art spinning machines produce first-quality fabric in a shorter period than conventional equipment.

improved fiber blends can be achieved by opening

-

1-4

Reducing Production Costs

Price competition is a major driving force in the textile industry. Worldwide, producers seek competitive advantages by maintaining tight controls over labor, raw material, and other production costs. Producers in developing countries, especially Asia, have an edge over their American counterparts because their productivity levels have grown faster since the late 1970s. Thus, while the U . S . textile industry's productivity level grew at a faster rate than the average for all manufacturing between 1976 and 1986 (5.2 percent annually compared, to 2.8 percent), additional productivity improvements must be realized to maintain a presence in today's competitive market.

Textile companies can lower production costs through a number of methods. Simplifying and accelerating production processes by, for example, combining processes or using faster-drying dyes, would allow products to get to market more quickly. developed production processes be carefully researched to ensure applicability to all fibers and fabrics.

Today's rapid developments in fiber and fabric types require that newly-

ELECTRICITY'S ROLE IN IMPROVING COMPETITIVENESS

The textile industry consumed 25.9 billion kWh of electricity in 1985. This consumption level represents 31 percent of the industry's total energy requirements. Thus it should not be surprising that changes in the use of electricity through DSM

programs can be of vital importance to the industry. More specifically, textile companies can improve their competitive position by sharpening their capabilities in the following areas:

0 PricefCost Control - Producing at reduced raw material, labor, or other production costs

0 Production Speed - Applying faster, efficient production methods with minimum waste while simultaneously maintaining product quality

0 Process Control - Monitoring and controlling all stages of the lengthy production process to avoid costly mistakes, maintain product quality, and optimize complex operations

Reliability - Ensuring that equipment and processes will operate without over- or under-processing, while maintaining color, yarn, and fabric quality.

0

1-5

The newer, more versatile, and powerful electric-driven machines have faster processing speeds which can increase flexibility and productivity in yarn and fabric formation. inspection procedures at various production stages can ensure yarn and fabric quality. Robotics, for example, are an effective means of efficient yarn quality inspection. Finally, streamlined and accelerated dyeing, drying, and finishing processes can cut down on overall production time and thereby lower costs.

Computerized monitoring and cbntrol of processes and automated

OPPORTUNITIES FOR THE ELECTRIC UTILITY INDUSTRY

Electric utilities have many opportunities to help the textile industry improve its competitive position, while at the same time advancing utility DSM objectives. These opportunities range from overall energy conservation, to load management, to the application of specific electrotechnologies. This Guidebook will help utility staff to understand these DSM opportunities.

Regardless of the types of programs being considered, electric utilities need to work closely with their textile customers to take advantage of DSM opportunities. Lack o f convincing and demonstrable information is a major barrier. Several factors argue for an increased utility focus on textile customers to help overcome this barrier:

0 Underestimated impact of electricity. The potential impact of electricity on textile manufacturinq is considerably underestimated by most textile firms. to be important inputs to their production process. Greater consideration is given to raw materials (such as fiber and chemicals) and labor, yet energy cost per dollar of value added for the textile industry is 9.3 percent;'significantly higher than the 6 percent value for all manufacturing. Similarly, electricity cost per dollar of value added exceeds that for all manufacturing.

0 Lack of widespread information about electrotechnologies and DSM programs. New, efficient electrotechnologies are not being applied in textile mills as often as they could be. These technologies typically will not sell on their inherent advantages (faster speeds and energy and space savings) alone because the textile industry is not as energy-conscious as many other industry sectors. In addition, cost-cutting opportunities resulting from other DSM programs await action by the industry.

Many textile companies do not cbnsider either energy or electricity

0 Lack of information about electricity consumption. enerov consumotion at the level where enerav characteristics for each

Few firms monitor mill

proc& are khown with certainty. standards to facilitate energy cost reduction is hampered.

Without"ihis information, setting energy

1-6

The e l e c t r i c u t i l i t y i n d u s t r y can p l a y a s i g n i f i c a n t r o l e i n in forming i t s t e x t i l e customers o f t h e b e n e f i t s o f e x i s t i n g and emerging technologies and DSM programs. This can a s s i s t u t i l i t i e s i n competing wi th f o s s i l - f u e l technologies, i n r e t a i n i n g customers, and i n achiev ing t h e i r DSM object ives. (espec ia l l y those i n t h e Southeast) could be hindered w i thou t a s t r a t e g i c p l a n designed t o i nc lude t e x t i l e customers.

The DSM e f f o r t s o f many u t i l i t i e s

To a i d t h e p lanner i n i d e n t i f y i n g and q u a n t i f y i n g t h e p o t e n t i a l impact o f DSM oppor tun i t i es , Table 1-1 summarizes key app l i ca t i on , market, and energy c h a r a c t e r i s t i c s o f 30 DSM technologies and process changes.

HOW TO USE THIS GUIDEBOOK

This Guidebook i s designed f o r p lanning and market ing personnel o f e l e c t r i c u t i l i t i e s . abreast o f developments i n t h e t e x t i l e i ndus t r y t h a t may a f f e c t t h e i r energy decis ions. i t s manufactur ing methods and energy use. which technologies and DSM programs are app l i cab le i n t h e t e x t i l e i ndus t r y , t o determine how c r u c i a l they are i n t h e manufacturing process, and t o evaluate t h e impact o f t h e i r adoption. DSM requ i res a unique coupl ing o f u t i l i t y ob jec t i ves , needs, and s t r a t e g i e s w i th those o f i t s customers. personnel developing DSM p lans , t h i s Guidebook l i s t s DSM o p p o r t u n i t i e s i n t h e t e x t i l e i n d u s t r y and conta ins in format ion about how t o l i n k t h e u t i l i t y ' s o v e r a l l DSM e f f o r t s w i t h t h e t e x t i l e customers' product ion processes and app l i ca t i ons . t h e same t ime, i t prov ides a l i s t o f problems and c o n s t r a i n t s associated w i th t h e p lanning o f DSM programs f o r t e x t i l e customers.

The Guidebook a l lows u t i l i t y planners and f i e l d representat ives t o keep

Appendices A and B p rov ide d e t a i l e d i n fo rma t ion about t h e i n d u s t r y and This Guidebook may be used t o i d e n t i f y

For t h e s t r a t e g i c market ing

A t