text starts here - qm.discovery.co.za

TRANSCRIPT

Discovery Insure Training guide

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 2 of 249

Confidential

Introduction to the training manual

The purpose of this document

Disclaimer This document is for training and information only and must not be seen as advice as defined and

contemplated in the Financial Advisory and Intermediary Services Act, 37 of 2002.

Although Discovery has taken reasonable care to ensure the content, material and data are accurate and

secure; Discovery does not warrant or guarantee the correctness or accuracy of these amounts or data.

Reliance on them is at your own risk.

All examples and case studies in this document are for illustrative purposes only and the product specific

technical documents must always be referenced and relied on for technical product details.

Discovery will not be liable for any actions taken or advice given by any person based on the correctness of

this information.

This guide was designed and developed by the Discovery Institute of Training and may not be amended,

reproduced, distributed or published without the prior written consent of the Discovery Institute of Training.

This Training Guide is designed to assist you through the learning process as you become

familiar with Discovery Insure. There is a focus on the Discovery Insure product, Vitality Drive

and all the elements of the processes, specifically new business, SmartAdvice, servicing,

integration, commission and claims. As part of the preparation for our training on Discovery

Insure, start with the ‘Introduction to short-term insurance’ training guide that covers the

basics of short-term insurance. The ‘Introduction to short-term insurance’ training guide will

include the basics of short-term insurance for each particular section, e.g. the basics of

short-term insurance for motor vehicle cover, the basics of short-term insurance for

household contents cover etc. In conjunction with this Training Guide, there is a

Presentation Pack, workbook, the Discovery Insure Plan Guide, financial technical guide and

annexures. It is advisable to make notes as you go through the presentation.

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 3 of 249

Confidential

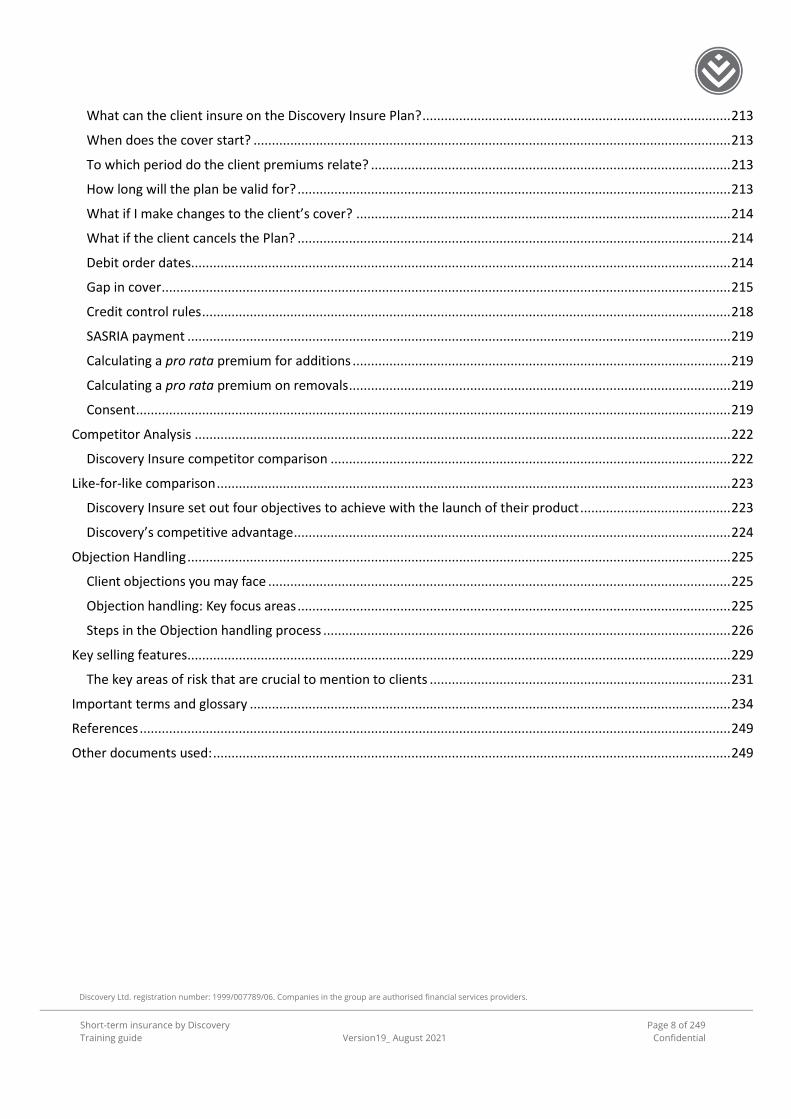

Table of contents Introduction to the training manual .............................................................................................................................. 2

The purpose of this document .................................................................................................................................. 2

Table of contents ........................................................................................................................................................... 3

Key to the symbols used in this guide ........................................................................................................................... 9

Icons........................................................................................................................................................................... 9

Discovery Insure Plan suite .......................................................................................................................................... 10

Our plan options are: ............................................................................................................................................... 10

Different rewards programmes ................................................................................................................................... 10

What is a rewards programme? .............................................................................................................................. 10

Different rewards programmes available in the market ......................................................................................... 11

What is Vitality Drive? ................................................................................................................................................. 13

Vitality Drive reward options................................................................................................................................... 13

Vitality Drive status ..................................................................................................................................................... 13

Diamond Vitality Drive status .................................................................................................................................. 13

Clients Can Earn Up to 1 600 Vitality Drive Points Every Month................................................................................. 14

Clients can earn up to 1 100 Vitality Drive points a month for improving their driving behaviour ........................ 14

Clients earn up to 350 Vitality Drive points a month for improving their knowledge and awareness ................... 19

When client’s Vitality Drive points will reflect ........................................................................................................ 24

Vitality Drive Fuel Cash Back Option ........................................................................................................................... 25

Fuel cash back .......................................................................................................................................................... 25

Three simple steps to start earning fuel cash back ................................................................................................. 25

The Insure Funder Account (IFA) – clients can double their fuel cash back by having it paid into their Insure Funder Account ....................................................................................................................................................... 27

Perfect driving days ................................................................................................................................................. 31

Young Adult benefit ................................................................................................................................................. 32

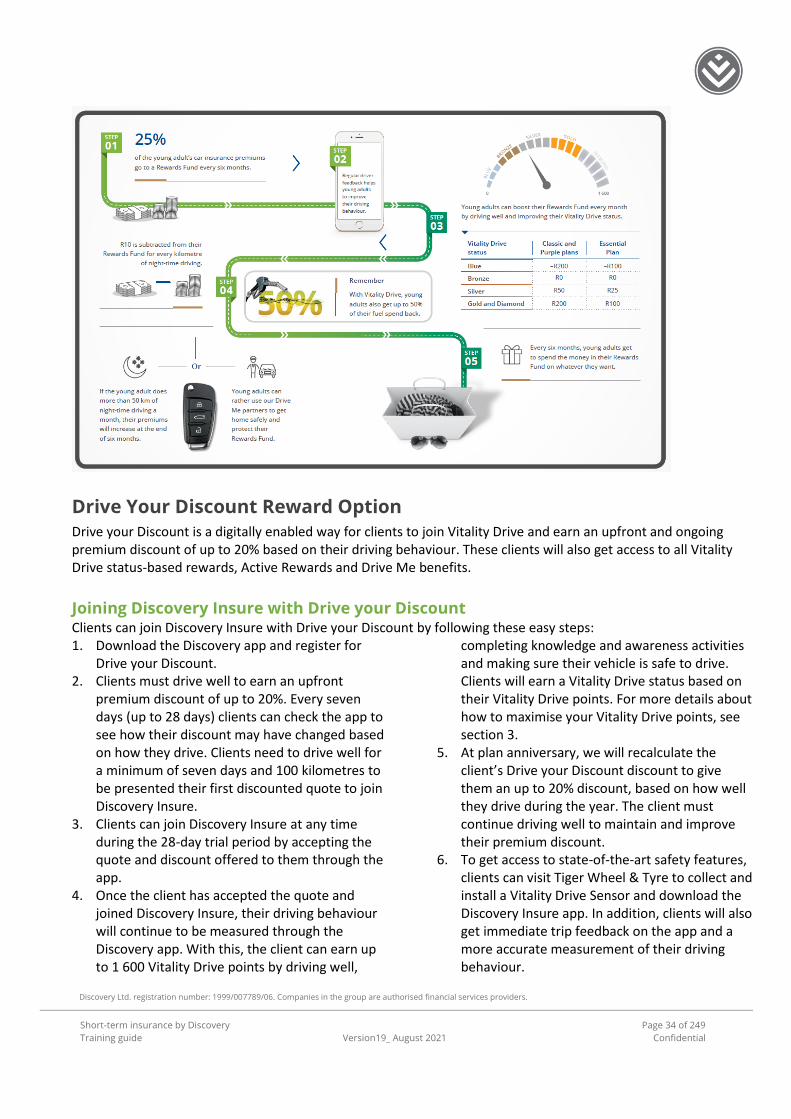

Drive Your Discount Reward Option ........................................................................................................................... 34

Joining Discovery Insure with Drive your Discount ................................................................................................. 34

Clients transitioning between Drive your Discount and fuel cash back .................................................................. 36

Rewards and Benefits Available On All Plans And ....................................................................................................... 37

Reward Options (Fuel Cash Back and Drive Your Discount) .................................................................................... 37

Drive Me benefits .................................................................................................................................................... 44

Vitality Drive 65+ ..................................................................................................................................................... 45

Vehicle Safety Features ............................................................................................................................................... 46

Impact Alert ............................................................................................................................................................. 46

Vehicle panic button ................................................................................................................................................ 47

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 4 of 249

Confidential

Find my vehicles ...................................................................................................................................................... 47

Weather warnings ................................................................................................................................................... 48

Crowd Search: Intelligent technology to keep drivers safe ..................................................................................... 48

Standalone DQ-Track safety features ...................................................................................................................... 48

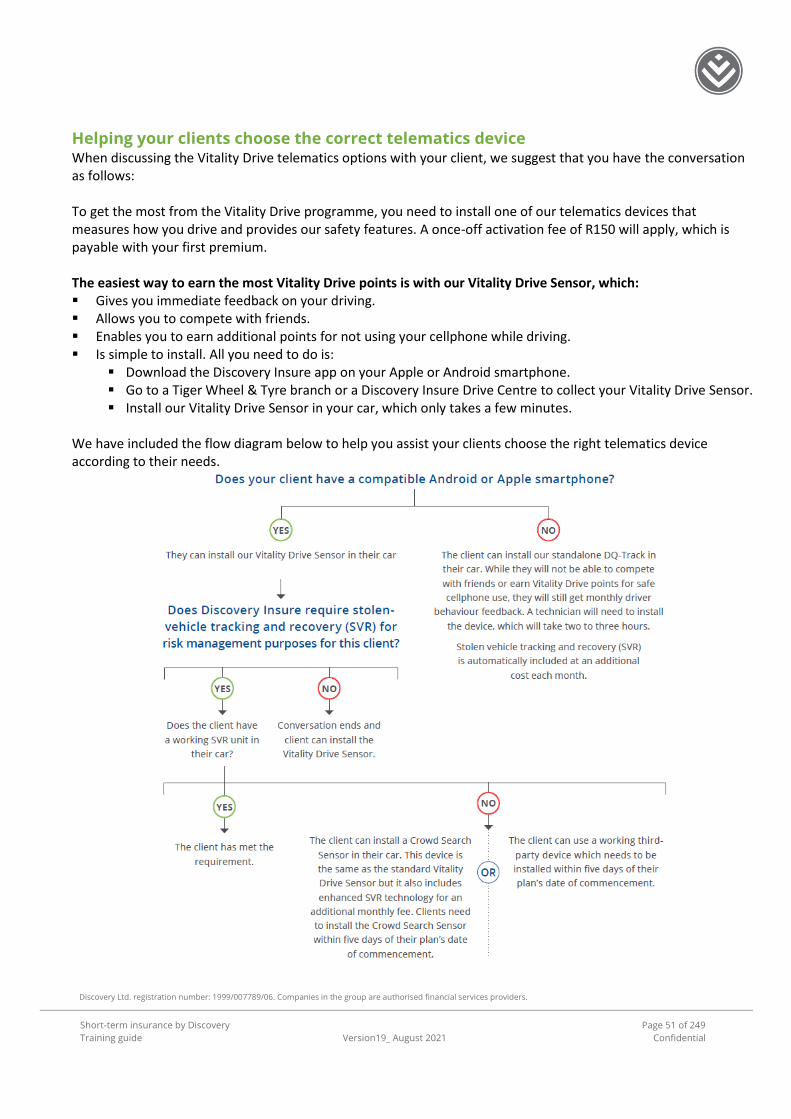

Vitality Drive Telematics Devices................................................................................................................................. 49

Benefits and features of Vitality Drive telematics devices ...................................................................................... 49

How do we use a client’s Vitality Drive telematics device information? ................................................................ 49

Telematics device options ....................................................................................................................................... 50

When will driving data reflect ................................................................................................................................. 55

Cancelling cover or switching vehicles .................................................................................................................... 55

Testing the telematics device .................................................................................................................................. 56

Ctrack terms and conditions .................................................................................................................................... 56

Responsibility restrictions ....................................................................................................................................... 57

Vitality Drive For Motorcycles ..................................................................................................................................... 57

If the motorcycle is insured with other vehicles ..................................................................................................... 57

If the motorcycle is the only vehicle insured........................................................................................................... 58

Vitality Drive programme rewards and safety features for motorcycles ................................................................ 58

Vitality Drive Example ................................................................................................................................................. 59

Client selects the Vitality Drive programme ............................................................................................................ 59

Discovery’s motor insurance ....................................................................................................................................... 62

Important terms you need to understand .............................................................................................................. 62

Discovery’s motor insurance ................................................................................................................................... 63

How is a vehicle covered for loss or damage? ........................................................................................................ 66

What happens when the clients claim? .................................................................................................................. 67

Extra equipment cover ............................................................................................................................................ 67

How are 4x4 vehicles covered? ............................................................................................................................... 68

Wheel and tyre cover .............................................................................................................................................. 68

Driver options – Who is allowed to drive the vehicle?............................................................................................ 69

Selecting the correct driver on the policy ............................................................................................................... 69

Vehicle usage ........................................................................................................................................................... 69

Excess structures ..................................................................................................................................................... 70

Benefits included ..................................................................................................................................................... 72

Optional benefits ..................................................................................................................................................... 77

General .................................................................................................................................................................... 89

Legal claims.............................................................................................................................................................. 95

Understanding claim rejections ............................................................................................................................... 97

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 5 of 249

Confidential

The repair process ................................................................................................................................................... 99

SmartAdvice........................................................................................................................................................... 101

Risk Management .................................................................................................................................................. 103

Household contents .............................................................................................................................................. 107

Discovery’s Household Contents insurance .......................................................................................................... 108

Benefits Included ................................................................................................................................................... 117

Optional benefits ................................................................................................................................................... 122

Exclusions .............................................................................................................................................................. 123

General .................................................................................................................................................................. 124

What every client should know ............................................................................................................................. 125

Discovery Insure Claims process ........................................................................................................................... 126

Understanding claim rejections ................................................................................................................................. 127

Buildings insurance, covers ................................................................................................................................... 131

Optional benefits ................................................................................................................................................... 138

Summary of Plan exclusions on Essential Plan ...................................................................................................... 139

Exclusions .............................................................................................................................................................. 140

General ...................................................................................................................................................................... 141

Electric fence ......................................................................................................................................................... 141

Understanding how water damage is covered ..................................................................................................... 142

What every client needs to know .......................................................................................................................... 144

Discovery Insure Claims process ............................................................................................................................... 146

Understanding claim rejections ............................................................................................................................. 147

Building Claims: Reason why claims get rejected. ................................................................................................ 147

The settlement process ......................................................................................................................................... 147

SmartAdvice............................................................................................................................................................... 148

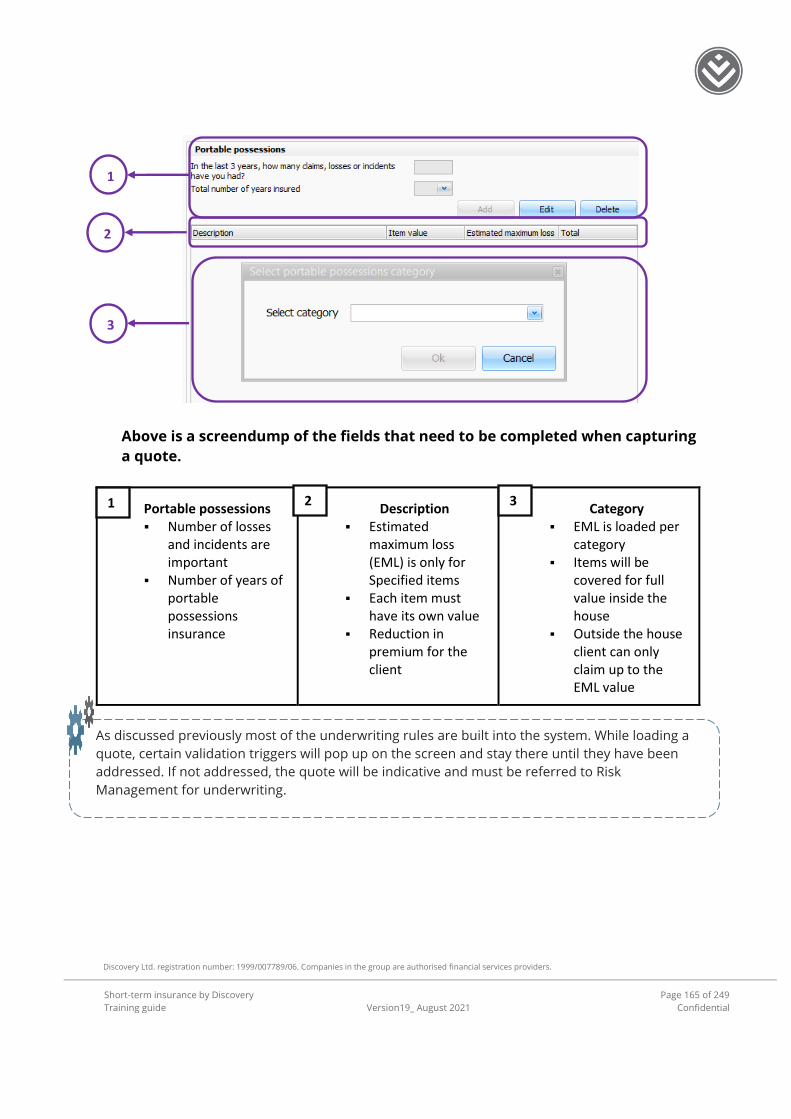

Portable possessions cover ....................................................................................................................................... 150

Important terms you need to understand ............................................................................................................ 150

Understanding portable possessions cover .......................................................................................................... 150

Discovery Insure’s portable possessions cover ..................................................................................................... 154

What items are covered? ...................................................................................................................................... 154

Features of the Discovery Insure portable possessions policy .............................................................................. 155

My Jeweller ............................................................................................................................................................ 157

Theft from unattended vehicles ............................................................................................................................ 158

Upgrade to the latest Apple or Samsung phone every year ................................................................................. 158

Safe deposit box benefit ........................................................................................................................................ 158

Dual insurance ....................................................................................................................................................... 159

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 6 of 249

Confidential

Screen protector benefit ....................................................................................................................................... 160

General information .................................................................................................................................................. 161

Understanding laptop cover .................................................................................................................................. 161

What every client should know ................................................................................................................................. 161

Clients need to be aware of the following ............................................................................................................ 161

General clothing and personal effects .................................................................................................................. 161

Specified items ...................................................................................................................................................... 161

The claims process ................................................................................................................................................. 162

Portable possessions claims: reasons why claims are rejected ............................................................................ 163

Exclusions .............................................................................................................................................................. 164

SmartAdvice............................................................................................................................................................... 164

Discovery’s Watercraft Insurance ............................................................................................................................. 167

Important terms you need to understand ............................................................................................................ 167

What is Watercraft Insurance?.............................................................................................................................. 167

Events that are covered......................................................................................................................................... 168

Benefits included ................................................................................................................................................... 169

Optional benefits ................................................................................................................................................... 169

Conditions for cover .............................................................................................................................................. 171

Exclusions .............................................................................................................................................................. 171

What every client should know ............................................................................................................................. 173

Discovery Insure claims process ................................................................................................................................ 174

Understanding claim rejections ............................................................................................................................. 174

SmartAdvice............................................................................................................................................................... 175

Discovery’s Personal liability insurance ..................................................................................................................... 177

What is Personal liability insurance? ..................................................................................................................... 177

Benefits included ................................................................................................................................................... 179

Exclusions .............................................................................................................................................................. 181

SmartAdvice............................................................................................................................................................... 182

Services ...................................................................................................................................................................... 184

Roadside assistance when an insured vehicle breaks down ................................................................................. 184

Direction Assist ...................................................................................................................................................... 186

Trip Monitor .......................................................................................................................................................... 186

HomeAssist ............................................................................................................................................................ 186

HomeProtector ...................................................................................................................................................... 186

FastTrack claims..................................................................................................................................................... 186

Smartphone app .................................................................................................................................................... 187

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 7 of 249

Confidential

The services and benefits provided through SmartClaims include ....................................................................... 188

Auto claims ............................................................................................................................................................ 188

Legal support benefit: ........................................................................................................................................... 189

Insure quote analysis (IQA) ................................................................................................................................... 190

SmartAdvice........................................................................................................................................................... 190

Integration ................................................................................................................................................................. 191

Select clients .......................................................................................................................................................... 192

Summary of Integration ........................................................................................................................................ 193

Quoting and Tools ..................................................................................................................................................... 195

SmartAdvice........................................................................................................................................................... 195

FAZ ......................................................................................................................................................................... 195

Ai Quote ................................................................................................................................................................. 196

Other tools for you to use ..................................................................................................................................... 197

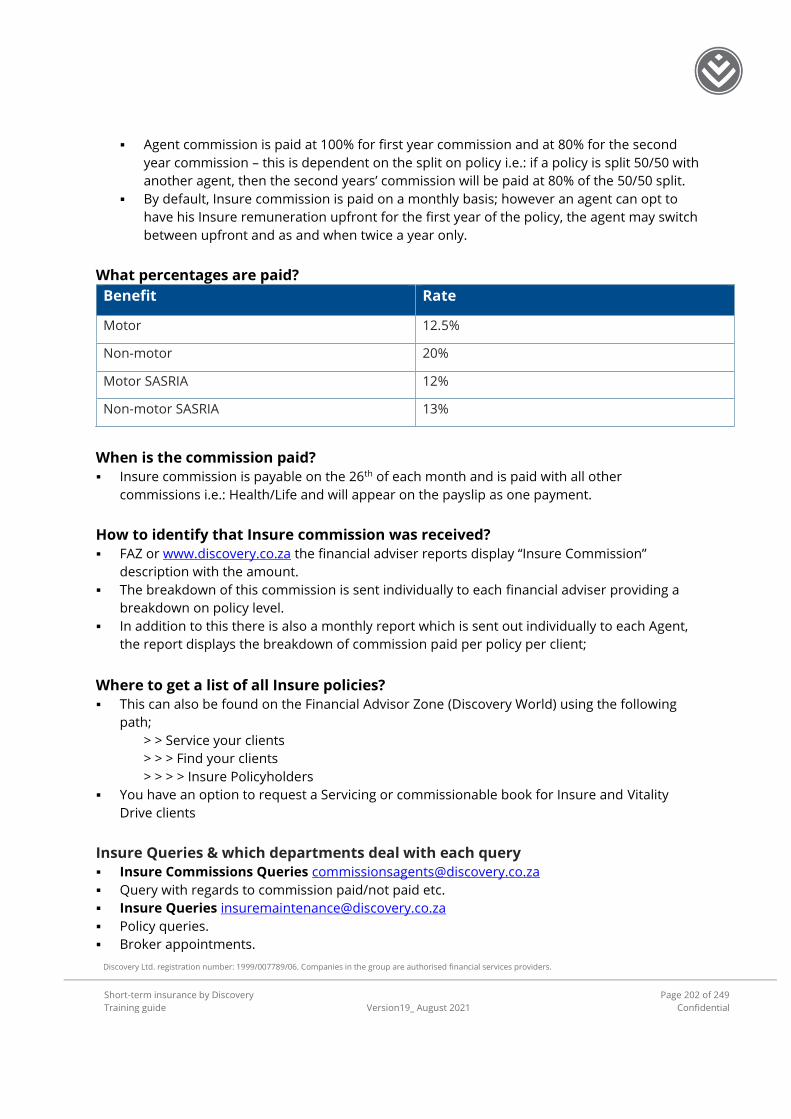

Commission ............................................................................................................................................................... 201

Overview ................................................................................................................................................................ 201

Binder agreements ................................................................................................................................................ 203

Claims ........................................................................................................................................................................ 204

Why claims are not paid ........................................................................................................................................ 204

The type of cover is not available .......................................................................................................................... 204

The asset was not insured ..................................................................................................................................... 205

The policy terms and conditions have been breached.......................................................................................... 205

Events not covered ................................................................................................................................................ 206

Conditions that influence the outcome of the claim ............................................................................................ 206

General claims ....................................................................................................................................................... 207

Towing and storage process .................................................................................................................................. 209

Towing procedure after repatriation .................................................................................................................... 209

Windscreen and window glass .............................................................................................................................. 209

Notifying the police ............................................................................................................................................... 209

Claims preparation costs ....................................................................................................................................... 209

Settlement of the claim ......................................................................................................................................... 210

Legal proceedings in the client’s name ................................................................................................................. 210

Discovery Insure functions on the Discovery Smartphone apps ........................................................................... 210

Proof of ownership ................................................................................................................................................ 210

Online Vault ........................................................................................................................................................... 211

How to log a claim ..................................................................................................................................................... 211

Payments ................................................................................................................................................................... 213

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 8 of 249

Confidential

What can the client insure on the Discovery Insure Plan? .................................................................................... 213

When does the cover start? .................................................................................................................................. 213

To which period do the client premiums relate? .................................................................................................. 213

How long will the plan be valid for? ...................................................................................................................... 213

What if I make changes to the client’s cover? ...................................................................................................... 214

What if the client cancels the Plan? ...................................................................................................................... 214

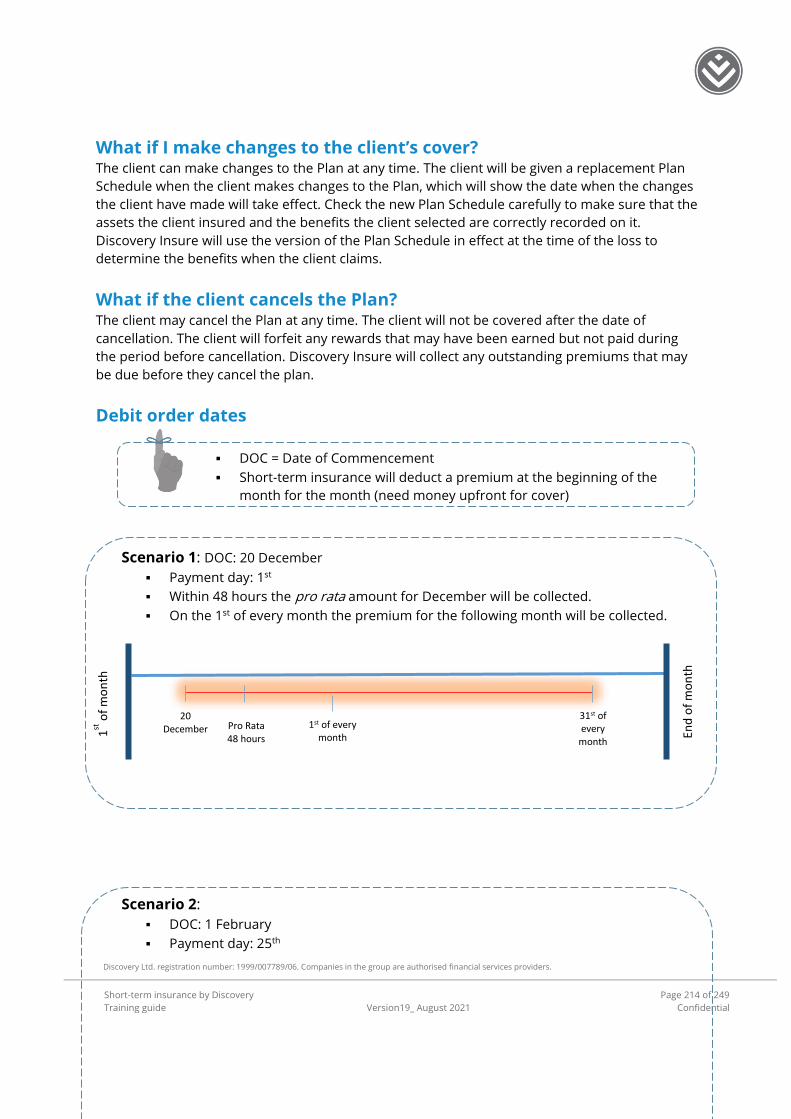

Debit order dates................................................................................................................................................... 214

Gap in cover ........................................................................................................................................................... 215

Credit control rules ................................................................................................................................................ 218

SASRIA payment .................................................................................................................................................... 219

Calculating a pro rata premium for additions ....................................................................................................... 219

Calculating a pro rata premium on removals ........................................................................................................ 219

Consent .................................................................................................................................................................. 219

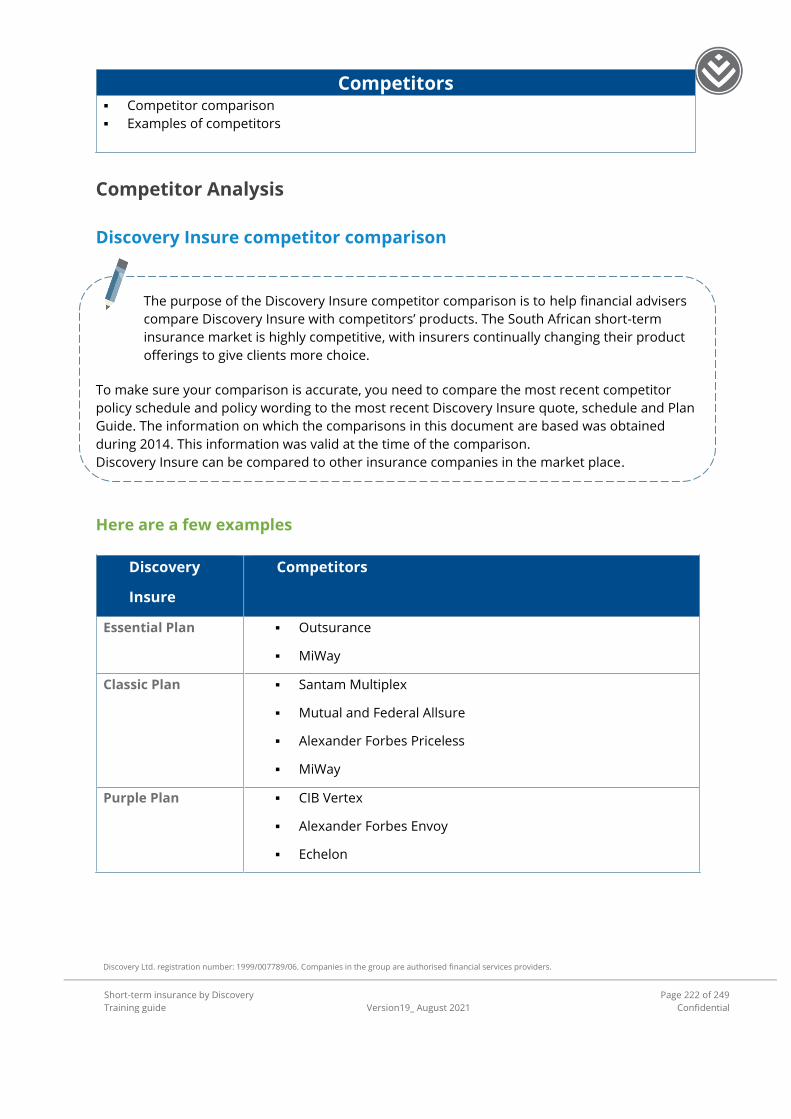

Competitor Analysis .................................................................................................................................................. 222

Discovery Insure competitor comparison ............................................................................................................. 222

Like-for-like comparison ............................................................................................................................................ 223

Discovery Insure set out four objectives to achieve with the launch of their product ......................................... 223

Discovery’s competitive advantage ....................................................................................................................... 224

Objection Handling .................................................................................................................................................... 225

Client objections you may face .............................................................................................................................. 225

Objection handling: Key focus areas ...................................................................................................................... 225

Steps in the Objection handling process ............................................................................................................... 226

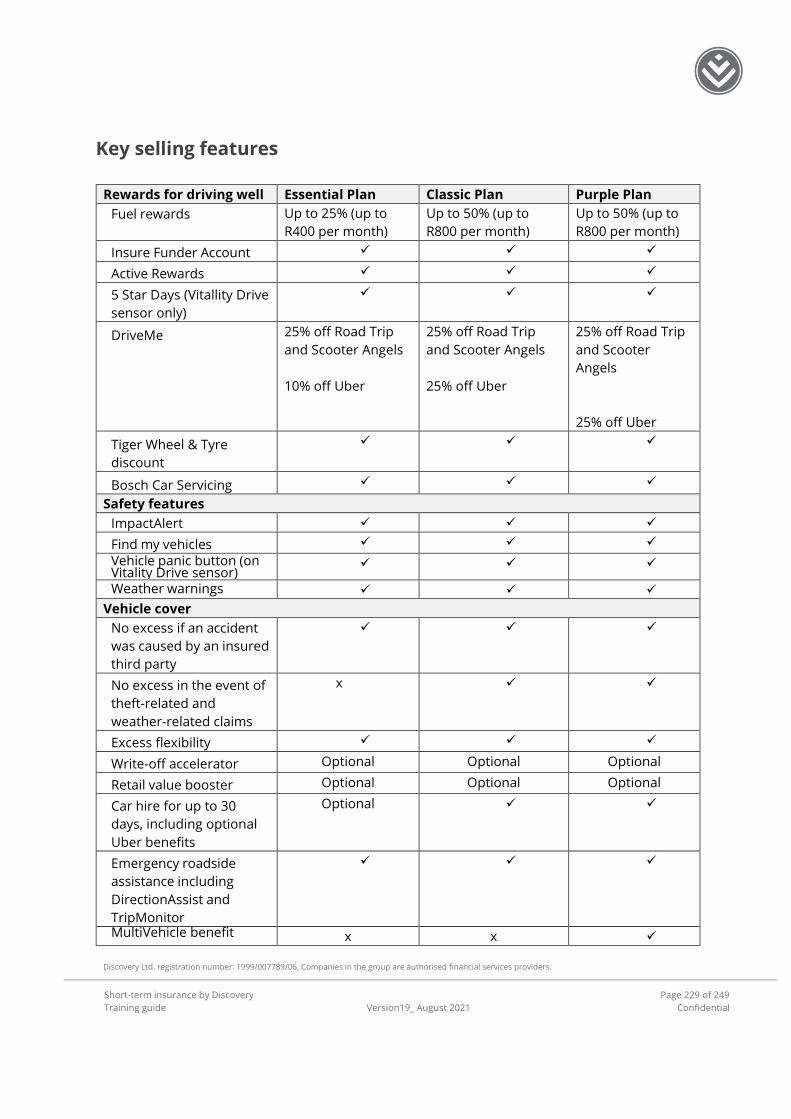

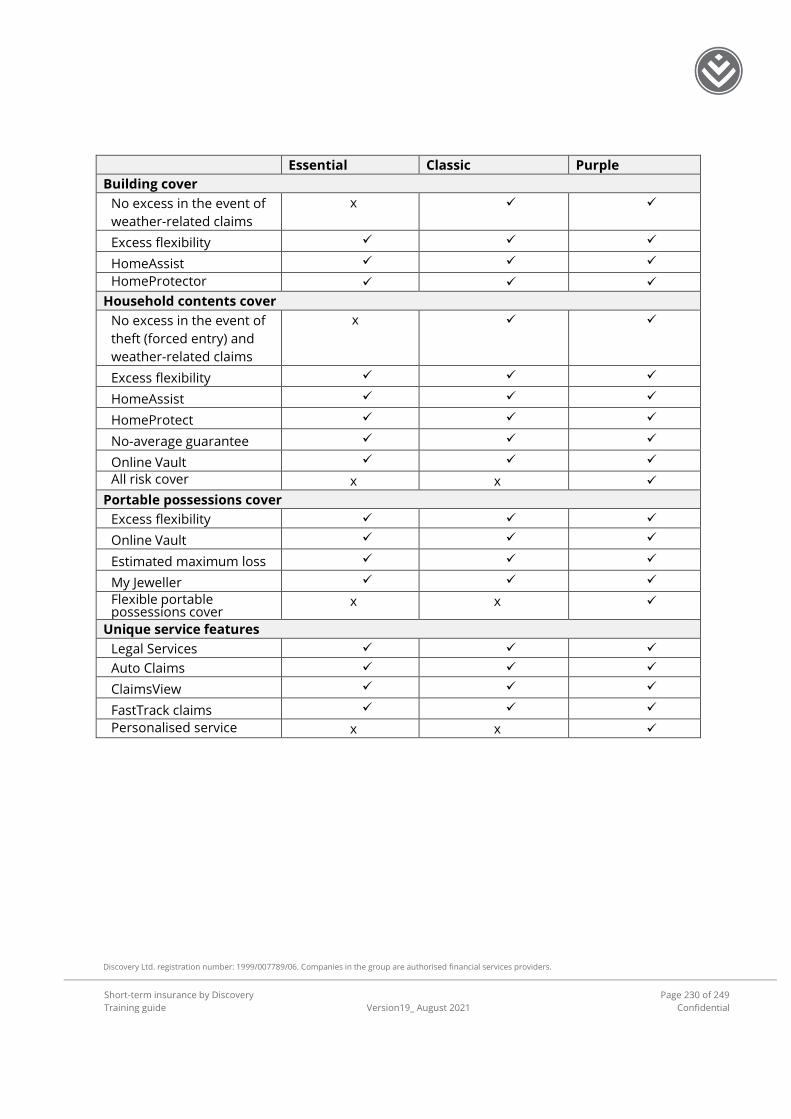

Key selling features .................................................................................................................................................... 229

The key areas of risk that are crucial to mention to clients .................................................................................. 231

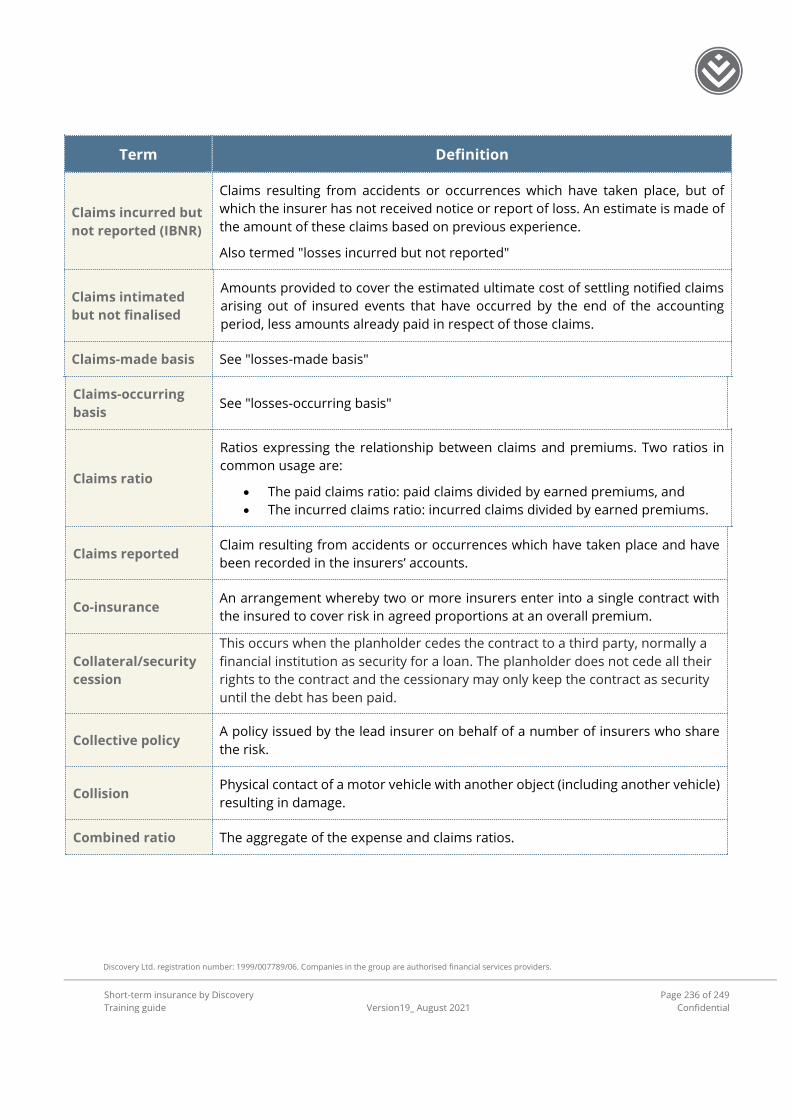

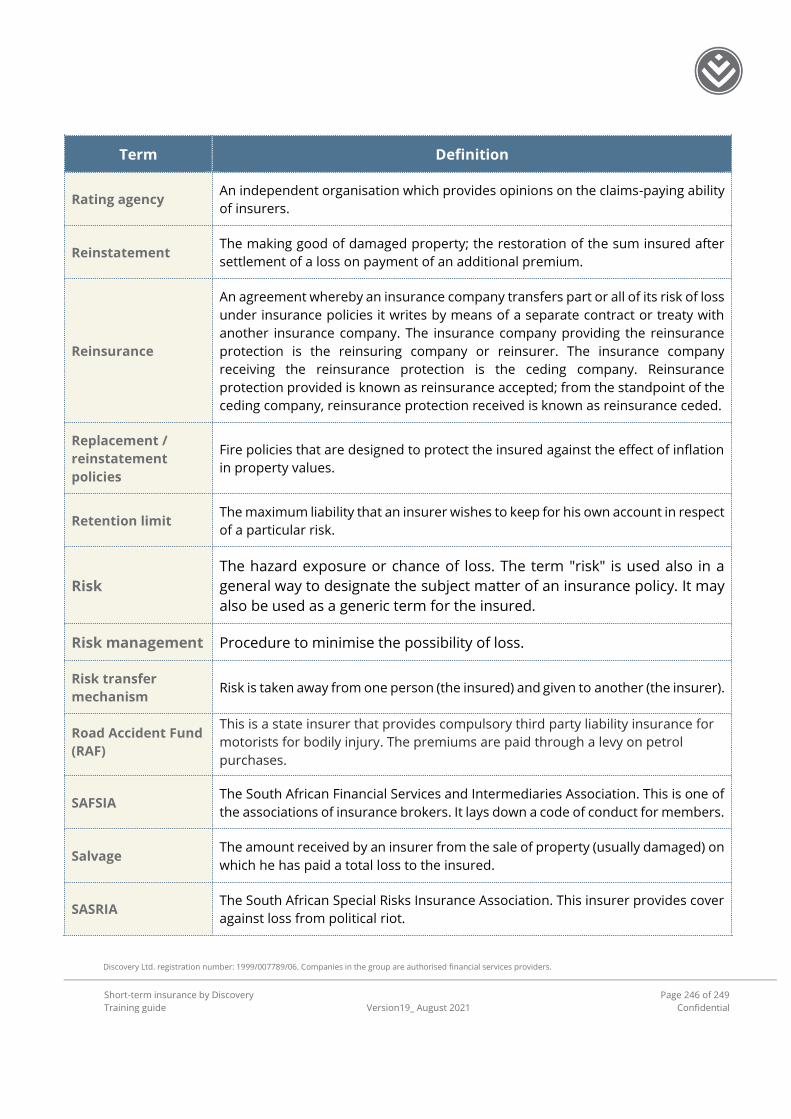

Important terms and glossary ................................................................................................................................... 234

References ................................................................................................................................................................. 249

Other documents used: ............................................................................................................................................. 249

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 9 of 249

Confidential

Key to the symbols used in this guide

Icons

Features of the product

Benefit to the client

Technical detail of the product

Did you know? (Additional information)

Word wealth (definition)

Note (important information to take note of)

Example

Tools

Reminder about important information

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 10 of 249

Confidential

Discovery Insure Plan suite

Discovery Insure provides comprehensive car and home insurance with unique rewards and safety features.

Clients can select one of four Plans depending on their needs.

Our entire Plan range offers comprehensive cover, safety features and rewards for good driving, while also

catering for different client profiles through innovative, optional benefit features to suit every need.

Our plan options are: ▪ Discovery Insure Classic Plan

▪ Discovery Insure Purple Plan

▪ Discovery Insure Essential Plan

The Classic Plan The Classic Plan is ideal for clients who are financially prudent and value the features, benefits and cover

limits provided. Clients can earn up to 50% of their fuel and Gautrain spend back in rewards every month for

driving well.

The Purple Plan The Purple Plan is ideal for more high-net worth clients who require insurance for assets amounting to more

than R5 million and value personalised service. Clients can earn up to 50% of their fuel and Gautrain spend

back in rewards every month for driving well. Other benefits include Multi Vehicle benefit, wider (all Risks)

cover and cellphone upgrades yearly.

The Essential Plan The Essential Plan is ideal for price-sensitive clients who require at least R250 000 in household contents

cover. Essential Plan clients who are good drivers, can earn up 25% of their fuel and Gautrain spend back in

rewards every month for driving well.

Different rewards programmes

What is a rewards programme? A rewards programme is a customised, strategically-aligned recognition and rewards system that helps

nurture a positive culture, and boosts client engagement, and ultimately, gives the financial adviser a

competitive advantage.

A rewards programme is designed to: ▪ Build a strategically focused, high-performance product through tailored client motivation solutions.

▪ Align clients to strategy, define goals, set targets, engage interest, recognise and reward achievements.

▪ Attract, retain and develop better clients.

The approach should be multi-dimensional, strategically aligned and measurable. This ensures that each

client is able to get the best results that are tailored to his unique requirements.

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 11 of 249

Confidential

Different rewards programmes available in the market There are a variety of rewards programmes out there, especially in the short-term insurance industry.

Here are a few examples:

▪ Santam: Multiplex

▪ Mutual and Federal: Allsure

▪ Alexander Forbes: Priceless

▪ CIB: Vertex

▪ Alexander Forbes: Envoy

▪ Echelon

▪ Momentum: Multiply

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 12 of 249

Confidential

Vitality Drive

Vitality Drive

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 13 of 249

Confidential

What is Vitality Drive? Vitality Drive is Discovery Insure’s unique driver behaviour programme that rewards clients for driving well. Vitality Drive uses the latest motor vehicle telematics technology to collect information about your clients’ driving behaviour, such as acceleration, braking, cornering, speed, night-time driving, distance driven and cellphone use. Clients have the option to join Vitality Drive when they take out comprehensive insurance on their motor vehicle or motorcycle. Vitality Drive is activated at plan level and costs R85 a month on the Purple and Classic Plans and R68 a month on the Essential Plan. Once a planholder selects the Vitality Drive programme, every primary driver on their plan will automatically be subscribed to Vitality Drive and the monthly fee is payable for each driver.

Vitality Drive reward options Vitality Drive has two reward options to choose from. Your clients will be able to join the Vitality Drive fuel cash back option and earn up to R800 fuel cash back each month and have access to other fuel-related benefits. Alternatively, they can join Vitality Drive through Drive your Discount and get an upfront and ongoing premium discount of up to 20%, based on how well they drive. Plans cannot have a combination of the Drive your Discount reward option and the fuel cash back reward option. One of the reward options would need to be chosen for all primary drivers on the plan. Both Vitality Drive reward options are available on all of our plans.

Vitality Drive status Clients can earn up to 1 600 Vitality Drive points a month. Clients earn Vitality Drive points by driving well, improving their driving behaviour, knowledge and awareness, and by making sure their vehicles are safe to drive. At the end of each month, clients will receive a Vitality Drive status based on their Vitality Drive points. The more Vitality Drive points they earn, the higher their Vitality Drive status and the more rewards they receive. We apply actuarial algorithms to the driving data to develop a scientific measure of drive. This provides an easy way for clients to understand how well they drive and how they can improve.

Vitality Drive status and Vitality Drive points needed Vitality Drive status Vitality Drive points needed Blue 0 to 299

Bronze 300 to 599

Silver 600 to 999

Gold 1 000 to 1 600

Diamond Earn a monthly average of 1 000 or more Vitality Drive points and remain claim free for 12 consecutive months.

Diamond Vitality Drive status Clients can achieve Diamond Vitality Drive status by earning a monthly average of 1 000 or more Vitality Drive points and remaining claim-free for 12 months. Each primary driver can achieve and maintain this status monthly.

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 14 of 249

Confidential

Technical details

▪ In the first year of their plan, clients can achieve Diamond status after their ninth month of cover, provided they are claims free since starting their plan, have an average monthly score of at least 1 000 Vitality Drive points, and at least seven months of driving behaviour data.

▪ If a client is a Diamond status driver and they claim, their status will change to Gold status in the following month. For the next 12 months, the highest status the client can achieve is Gold. As soon as the client is claim free for 12 months, they can qualify for Diamond status again, provided their 12-month rolling average Vitality Drive points is at least 1 000.

▪ If a client is a Diamond Vitality Drive status driver and remain claim free but they get less than a total of 12 000 Vitality Drive points for the 12-month period before the fuel cash back calculation date, their status will be changed to Gold or below, depending on their actual month-end Vitality Drive points. As soon as the client gets a total of 12 000 or more Vitality Drive points for the 12-month period before the fuel cash back calculation date, they will move to Diamond status again.

▪ The definition of ‘claims free’ follows the Vitality Drive points definition with regards to what is and what is not considered a claim. Therefore, vehicle glass and SOS claims do not affect a client’s claim-free years.

Clients can earn up to 1 600 Vitality Drive points every month Clients can earn up to 1 600 Vitality Drive points by improving their driving behaviour, completing knowledge and awareness activities and ensuring their vehicle is safe to drive. The better clients drive and the more point-earning activities they complete, the more Vitality Drive points they earn and the more rewards they get.

DRIVING BEHAVIOUR Up to 1 100 points

Driving Profile Up to 750 points Distance points Up to 100 points Night-time driving points Up to 150 points Claim-free years Up to 100 points

KNOWLEDGE AND AWARENESS Up to 350 points

Online driver assessment 50 points Driving courses 150 points EyeGym Up to 150 points

VEHICLE SAFETY Up to 150 points

Passing the Tiger Wheel & tyre Annual Multipoint check

100 points

Service history up to date 50 points

Clients can earn up to 1 100 Vitality Drive points a month for improving their

driving behaviour When clients join Vitality Drive, they must install a Vitality Drive telematics device so that we can measure their driving behaviour and reward them for driving well. Clients have the option of installing either the Vitality Drive Sensor or the Crowd Search Sensor in their vehicle. These devices are smartphone-enabled devices that are made up of a sensor, which is installed in the vehicle, and a smartphone app on Android or iOS phones. The smartphone must be compatible to the sensor to allow the app and the sensor to link to each other to measure client’s driving behaviour. If clients do not have a compatible smartphone to have the Vitality Drive Sensor or Crowd Search Sensor, they must install the standalone DQ-Track in their vehicle. If clients install the standalone DQ-Track, we will not be able to measure their cellphone use. This means that the maximum driving behaviour points they can earn each month

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 15 of 249

Confidential

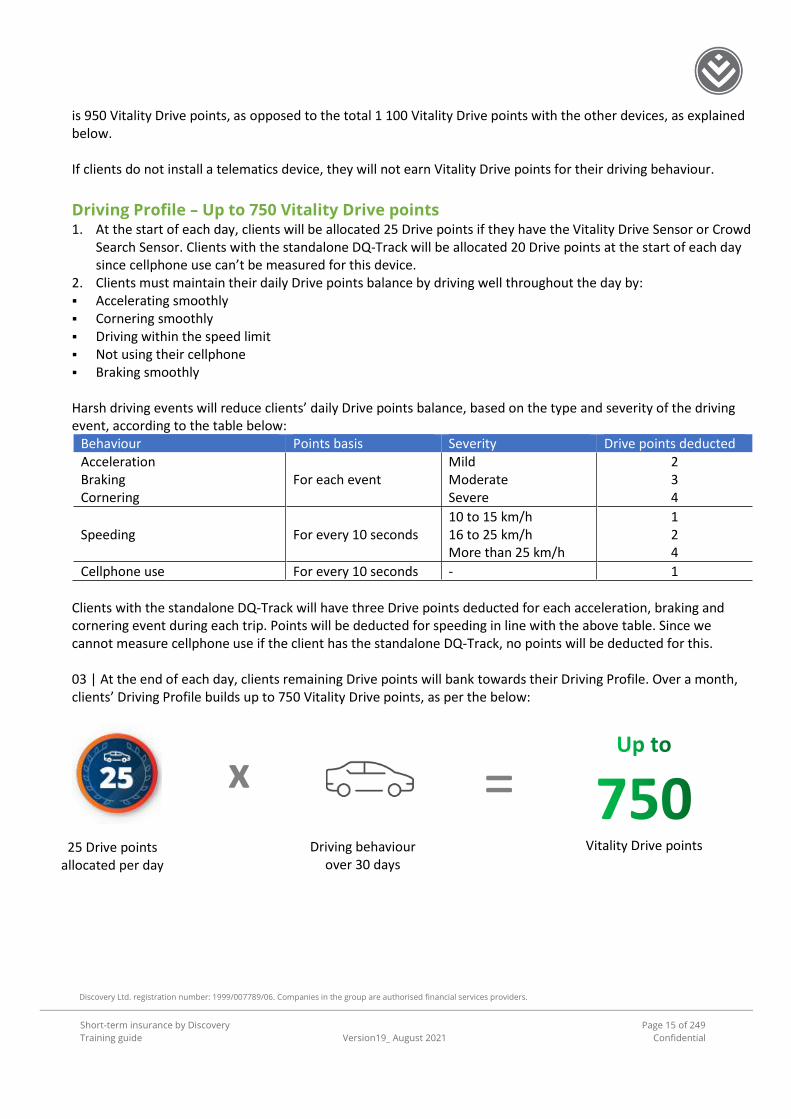

is 950 Vitality Drive points, as opposed to the total 1 100 Vitality Drive points with the other devices, as explained below. If clients do not install a telematics device, they will not earn Vitality Drive points for their driving behaviour.

Driving Profile – Up to 750 Vitality Drive points 1. At the start of each day, clients will be allocated 25 Drive points if they have the Vitality Drive Sensor or Crowd

Search Sensor. Clients with the standalone DQ-Track will be allocated 20 Drive points at the start of each day since cellphone use can’t be measured for this device.

2. Clients must maintain their daily Drive points balance by driving well throughout the day by: ▪ Accelerating smoothly ▪ Cornering smoothly ▪ Driving within the speed limit ▪ Not using their cellphone ▪ Braking smoothly Harsh driving events will reduce clients’ daily Drive points balance, based on the type and severity of the driving event, according to the table below:

Behaviour Points basis Severity Drive points deducted Acceleration Braking Cornering

For each event Mild Moderate Severe

2 3 4

Speeding For every 10 seconds 10 to 15 km/h 16 to 25 km/h More than 25 km/h

1 2 4

Cellphone use For every 10 seconds - 1

Clients with the standalone DQ-Track will have three Drive points deducted for each acceleration, braking and cornering event during each trip. Points will be deducted for speeding in line with the above table. Since we cannot measure cellphone use if the client has the standalone DQ-Track, no points will be deducted for this. 03 | At the end of each day, clients remaining Drive points will bank towards their Driving Profile. Over a month, clients’ Driving Profile builds up to 750 Vitality Drive points, as per the below:

x

25 Drive points allocated per day

Driving behaviour over 30 days

= Vitality Drive points

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 16 of 249

Confidential

Technical Details

▪ Since we cannot measure cellphone use for clients with the standalone DQ-Track, they will receive 20 daily Drive points a day. They can earn up to 600 Drive points from their daily driving behaviours towards their Driving Profile each month (20 Drive points x 30 days = 600 Vitality Drive points).

▪ The maximum Vitality Drive points clients with the standalone DQ-Track can earn each month is 1 450. This is because their Driving Profile builds up to a maximum of 600 Vitality Drive points. All other Vitality Drive point-earning activities are the same as the Vitality Drive Sensor.

▪ Clients’ minimum daily Drive points balance will be 0. Clients cannot have a negative Drive points balance, even if more than 25 (or 20, for standalone DQ-Track clients) Drive points are deducted for harsh driving events during the day.

▪ In months where there are 31 days, Drive points will contribute towards clients’ Driving Profile up to a maximum of 750 Vitality Drive points for clients with the Vitality Drive Sensor or 600 Vitality Drive points for clients with the standalone DQ-Track. Clients therefore have an extra day to maximise their Driving Profile.

▪ In February, we will allocate two bonus days of Drive points, equal to the client’s average daily Drive points over the past 30 days (or one bonus day when it is a leap year).

▪ If clients do not install a Vitality Drive telematics device in the beginning of the month, their Driving Profile will be pro-rated based on the remaining days of the month. For example, if the client gets their Vitality Drive Sensor mid-month, they will be able to earn a maximum of 375 Vitality Drive points (25 Drive points x 15 days) towards their Driving Profile.

▪ Where there is both a Vitality Drive Sensor and standalone DQ-Track in a single vehicle, all points will be based on the Vitality Drive Sensor only since this provides a more accurate measure of driving behaviour and awards clients with more Vitality Drive points for their cellphone use.

▪ Where the Vitality Drive Sensor is not working and the appropriate interventions have been logged to the Discovery Insure DQ-Track team, we will use the client’s standalone DQ-Track for scoring.

▪ Where a driver is listed as the primary driver of multiple vehicles the following rules will apply: ▪ Clients will receive a maximum of 25 Drive points each day if they have the Vitality Drive Sensor and

20 Drive points if they have the standalone DQ-Track. ▪ Driving events from all vehicles will be deducted from the daily Drive points allocation. This means

that if clients drive more than one vehicle on the same day Drive points will deducted based on their driving behaviour from all vehicles.

▪ Where multiple vehicles are driven at the same time, Drive points from all trips will be deducted from the clients daily Drive points allocation.

▪ Clients need to have a working device in all vehicles for which they are listed as a primary driver. ▪ Trips that are recorded and logged as passenger trips will be scored in the same way as other trips, with the

only difference being that clients will not be penalised for cellphone use for these trips. Note, we look at the number of times that clients select their trips as ‘Passenger trips’. If they do this excessively, their daily Drive points will be negatively affected because of cellphone use.

▪ Clients driving information will not be used in any way at claims stage other than to confirm the time and place of an incident. Clients may ask us to use the information to help prove that an insured third party was at fault.

▪ Client’s Driving Profile resets to zero at the beginning of every month.

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 17 of 249

Confidential

Clients will also be rewarded for no-drive days If clients do not drive for a full day, their Drive points balance for that day will be equivalent to the average of their daily Drive points balance over the past 30 days. This is an accurate predictor of what clients’ Drive points balance would have been, had they driven that day. Points for no-drive days will also bank towards clients’ Driving Profile.

Technical Details:

▪ Only the number of days in the past 30 days where driving behaviour was recorded will count when calculating clients 30-day average for no-drive days.

▪ Drivers who have less than seven days of driving data will receive a default score of 10 Drive points for no-drive days.

▪ Clients can earn an unlimited number of no-drive days if we are able to verify that they did not drive on that day:

▪ For the Vitality Drive Sensor or Crowd Search Sensor: the sensor and Discovery Insure app have synced and the client has uploaded trip information.

▪ For the standalone DQ-Track: the device is working. ▪ For no-drive days to count towards their monthly Driving Profile, clients must sync their Vitality Drive Sensor

to their Discovery Insure app and upload their trip information by the third day of the next month. For example, to get points for no-drive days for January’s cash back, clients must sync their Discovery Insure app with their Vitality Drive Sensor and upload their trip information by 3 February.

▪ However, for the Vitality Drive Sensor or Crowd Search Sensor, if clients do not sync their sensor and app or upload the trip information by the third day of the next month, then they will still receive points for no-drive days. These are considered unverified no-drive days as we don’t have trip information to verify if the client drove or not.

▪ We will only allocate a maximum of 30 unverified no-drive days within a six month rolling period. If clients have more than the maximum 30 days, they will not receive any Drive points for those days.

▪ If clients did drive on a day recorded as a no-drive day and their trips are not reflecting as a recorded trip, they must make sure that they upload their trip data. Clients may have selected to only upload their trip data when they are on Wi-Fi. If this is the case, clients must connect to Wi-Fi so that they can upload their latest trip information and we can record all of their trips. Please note that clients’ Drive points balance for the day may change to reflect the actual Drive points deducted during each trip and not an average of their Drive points balance that we have allocated to them for their no-drive day.

▪ If the client is the primary driver of more than one vehicle, to qualify for a no-drive day, none of their vehicles must have been driven on that day.

Points will also be deducted for uncovered trips An uncovered trip is when the Vitality Drive sensor or Crowd Search Sensor and the Discovery Insure app are not linked. Uncovered trips will reduce clients’ daily Drive points balance. Clients must make sure all the required settings are enabled and all permissions are accepted. Points will be deducted based on the length of the trip.

Length of trip Drive points deducted Less than 10 minutes 0

10 to 20 minutes 3

20 to 30 minutes 7

More than 30 minutes 10

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 18 of 249

Confidential

Monthly points – up to 250 Vitality Drive points

Distance points – up to 100 Vitality Drive points We look at the total number of kilometres driven over the past 30 days. The more time spent on the road, the higher the client’s risk of being involved in an accident. The less time clients spend driving, the higher their distance points.

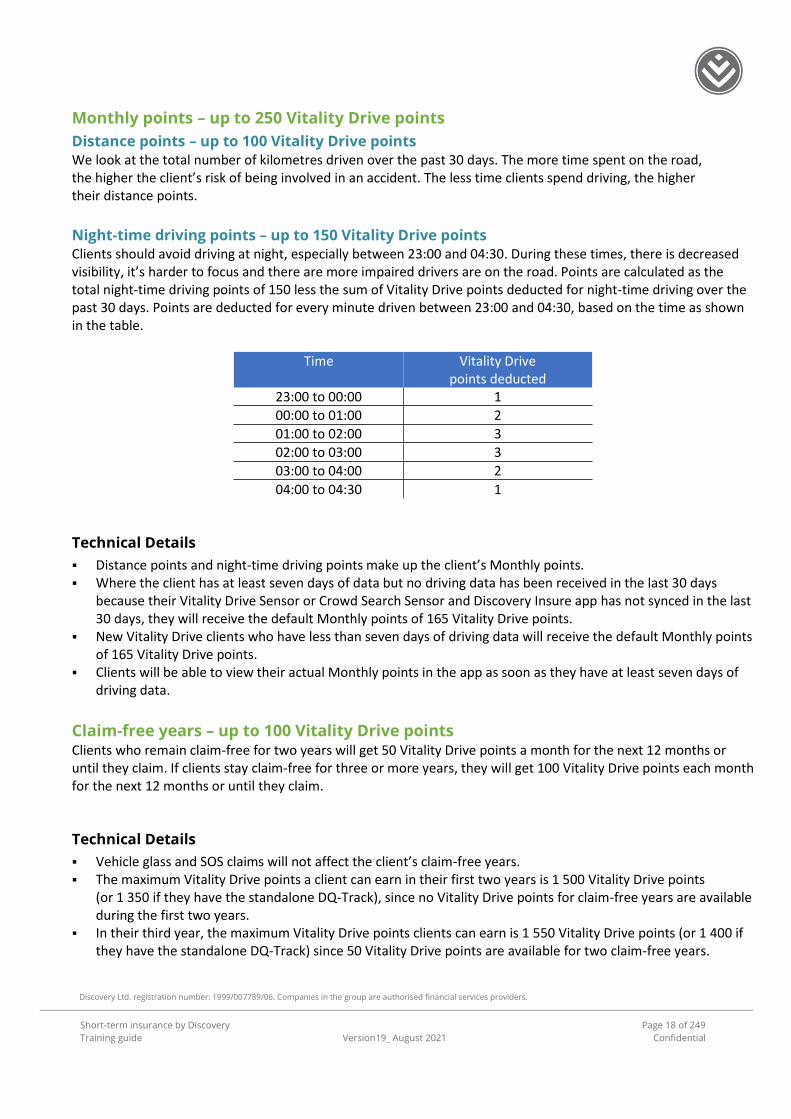

Night-time driving points – up to 150 Vitality Drive points Clients should avoid driving at night, especially between 23:00 and 04:30. During these times, there is decreased visibility, it’s harder to focus and there are more impaired drivers are on the road. Points are calculated as the total night-time driving points of 150 less the sum of Vitality Drive points deducted for night-time driving over the past 30 days. Points are deducted for every minute driven between 23:00 and 04:30, based on the time as shown in the table.

Time Vitality Drive points deducted

23:00 to 00:00 1

00:00 to 01:00 2

01:00 to 02:00 3

02:00 to 03:00 3

03:00 to 04:00 2

04:00 to 04:30 1

Technical Details

▪ Distance points and night-time driving points make up the client’s Monthly points. ▪ Where the client has at least seven days of data but no driving data has been received in the last 30 days

because their Vitality Drive Sensor or Crowd Search Sensor and Discovery Insure app has not synced in the last 30 days, they will receive the default Monthly points of 165 Vitality Drive points.

▪ New Vitality Drive clients who have less than seven days of driving data will receive the default Monthly points of 165 Vitality Drive points.

▪ Clients will be able to view their actual Monthly points in the app as soon as they have at least seven days of driving data.

Claim-free years – up to 100 Vitality Drive points Clients who remain claim-free for two years will get 50 Vitality Drive points a month for the next 12 months or until they claim. If clients stay claim-free for three or more years, they will get 100 Vitality Drive points each month for the next 12 months or until they claim.

Technical Details

▪ Vehicle glass and SOS claims will not affect the client’s claim-free years. ▪ The maximum Vitality Drive points a client can earn in their first two years is 1 500 Vitality Drive points

(or 1 350 if they have the standalone DQ-Track), since no Vitality Drive points for claim-free years are available during the first two years.

▪ In their third year, the maximum Vitality Drive points clients can earn is 1 550 Vitality Drive points (or 1 400 if they have the standalone DQ-Track) since 50 Vitality Drive points are available for two claim-free years.

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 19 of 249

Confidential

Clients earn up to 350 Vitality Drive points a month for improving their knowledge and awareness

Online driver assessment – 50 Vitality Drive points Clients can improve their driving knowledge and awareness with our Online driver assessment to earn 50 Vitality Drive points each month for 12 months. The assessment consists of a series of multiple-choice questions that test the clients knowledge of the rules of the road and their general road safety awareness. Clients can access the assessment in the Discovery app or by logging in to www.discovery.co.za.

Driving courses – up to 150 Vitality Drive points Clients can either complete the Online driver training from the comfort of their home to earn 150 Vitality Drive points a month for 12 months or complete an advanced driving course for 150 Vitality Drive points a month for 24 months or complete the Refresher simulator course at the Discovery Driving Academy simulator course and earn 150 Vitality Drive points every month for 12 months. Points for this category will be capped at 150 Vitality Drive points. Driving courses are designed to teach clients critical defensive driving techniques to help them drive better and be safer on the road. The Online driver training Clients can log in to www.discovery.co.za and watch a series of six short video clips. Each clip is followed by an assessment with a pass mark of 80%. Clients can watch each video and complete the assessments as many times as they like. However, Vitality Drive points will be capped at 150 points, which clients will receive every month for 12 months. Clients need to complete and pass all six assessments to qualify for their Vitality Drive points. Points for the Online driver training should reflect within 48 hours of completing the course. The advanced driving courses Clients can complete a driving course with Volkswagen Driving Academy, BMW Driving Experience or Jaguar Land Rover Experience and earn up to 150 Vitality Drive points a month, for 24 months after completing the course. Each course is provided at special discounted rates to Discovery Insure Vitality Drive clients. For more details on course locations and costs, visit www.discovery.co.za. Points will reflect within 14 days of completing the course.

Volkswagen Driving Academy The Discovery Insure Safety Driving course is a full-day course which includes the following sections in the course: Skidpan session, defensive driving and hijack prevention. Skidpan session

In-depth theory session on safe driving including different types of skids, weight transfer and safety systems in the vehicles, collision avoidance and slalom. Clients will also learn about ABS emergency lane changes, ESC emergency lane change and braking without ABS. Defensive driving

An in-depth lecture on defensive driving, recognising of hazards, following and stopping distances and general road rules. Clients will get an understanding of how to conduct an exterior vehicle inspection, interior vehicle inspection, correct seating position and a driving evaluation (clients will receive an evaluation sheet after completing the driving evaluation).

Hijack prevention

An informative theory session that will cover hijack prevention tips, hijacking statistics, types of hijacking and prevention techniques. Clients will see a hijack prevention demonstration and learn how to safely remove themselves and other passengers (including babies and children) from the vehicle during a hijack situation. The course will also provide detailed information on vehicle jamming, tracking device and what to do if the client is hijacked. The Safety Driving course is a full-day course. Clients will earn 150 Vitality Drive points for completing this course. This course is offered in Gauteng only.

BMW Driving Experience The Discovery Control Package covers a combination of the defensive driving and the collision avoidance and skid control courses. Module 1: Defensive driving

The Defensive driving course teaches clients to constantly evaluate the change in road conditions and to choose a course of action that enables them to minimise their risk. This course will give clients a greater awareness of the external factors that can influence situations on the road and teach them how to handle traffic problems safely. Clients can attend the morning or afternoon course. Clients will be tested during the course and if the instructors feel that the client needs to return, they will be notified when the course is complete. Although there is no additional cost involved to complete the test, clients will have to set aside the time to do it.

Module 2: Collision avoidance and skid control

This course is designed to improve the client’s skid control and collision-avoidance skills. BMW simulates several different types of skids on the wet skidpan and with practice, clients will begin to master the skills to deal with many emergency situations. On a steady gradient and under controlled conditions, the client’s growing confidence in handling the motor car will allow them to explore the limits of vehicle control. Clients will also learn hijack-prevention techniques and steps to follow in the event of the unexpected. Clients can attend a morning or afternoon course. This course is offered at the Zwartkops Raceway in Centurion.

Jaguar Land Rover Experience Jaguar Land Rover Experience teaches clients how to anticipate emergency situations on the road and negotiate them safely. Clients can also learn how to control their vehicle when they venture off-road. The Defensive driver training course An advanced driver is a person who drives to avoid accidents in spite of the actions of others or the presence of adverse conditions and who can take corrective measures to avoid an accident simply by searching, identifying, predicting, deciding, and executing their decisions before an incident occurs. This course includes practical on-road driving with an instructor carefully watching every manoeuvre. The Defensive driving training course will not only increase the client’s ability to anticipate emergency situations, it will teach them to handle these situations safely. Defensive driving principles include: vehicle orientation, potential hazards and threats, road hazards and vehicle positioning, road signs and legal actions, correct driving procedures and general on-road safety.

The Off-road introductory course This course is designed to introduce the participant to the world of 4x4 driving, covering basic four-wheel drive systems and the latest electronic aids fitted to four-wheel drive vehicles. A 45-minute theory session will also cover basic vehicle setup as well as handling vehicles when venturing into off-road conditions. The following driving elements will be covered in theory and during a three-hour practical drive: hill ascents and descents, traversing a side slope, driving through ditches and rutted tracks, and deep water wading. All major road surfaces will be discussed with general driving techniques.

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 21 of 249

Confidential

BMW Rider Academy The better equipped clients are to ride their motorcycle, the safer and more enjoyable their rides will be. BMW has developed special rider training courses which offer motorcyclists just what they need to improve their skills. The Refresher course

This course is perfect to equip riders who plan to purchase, or recently purchased a motorcycle with the correct riding skills and techniques to improve their safety. Riders who need to improve their confidence on the open road will also benefit from this course. The course consists of theory which covers safety aspects, defensive riding tips on various scenarios encountered on our roads and practical lessons. All training takes place in a controlled environment. This course is offered at the Zwartkops Raceway in Centurion.

The Novice course: Introduction to

motorcycling

This course is designed to help clients learn the essential elements every rider must know to #MakeLifeARide. First in theory then in practice, in a controlled environment, under the watchful eye of a coach. This course is suitable for new riders with limited or no riding experience. This intensive course provides theoretical and practical training, covering all the essential elements of riding that prepare new riders for the road. A BMW G 310 R training motorcycle, helmet and gloves can be provided. All practical training takes place in a controlled environment. No driving licence required and all attendees must be able to ride a bicycle before enrolling for the novice course.

Discovery Driving Academy Driving simulators place the driver in an artificial environment which is made to mimic an actual driving experience. The simulator itself mimics a real car and includes an accelerator, brake, clutch, gearbox, indicators and windscreen wipers. The simulators will teach new drivers the basics of driving in a safe environment with the Licence Prep course and will refresh the skills of experienced drivers with the Refresher course. The state-of-the-art driving simulators are in line with the Discovery Insure vision of creating a nation of better drivers. Discovery clients will get a 25% discount while Discovery Insure clients will get a 50% discount off simulator course fees. The Driving Academy can be found at 1 Discovery Place and is available to all members of the public. The Licence Prep course for first-time drivers

The Licence Prep course teaches first-time drivers the fundamentals of driving by providing them with real life driving experiences in a controlled environment. This allows new drivers to increase their confidence and helps to reduce their accident risk as they learn to anticipate, prepare for and handle unpredictable and hazardous driving conditions and react in a safe and controlled way, without putting themselves or others at risk. The

Licence Prep course consists of five lessons that are each 60 minutes long. Each lesson comprises of practical sessions and discussions with an instructor. First-time drivers get a 15% vehicle premium discount when they pass the Licence Prep simulator course and driver’s licence test and join Discovery Insure and Vitality Drive within two years. There are no Vitality Drive points earned for completing the Licence Prep course.

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 22 of 249

Confidential

The Refresher course for experienced drivers

This course is for those with a driver’s licence who wish to update their skills and learn defensive driving techniques. Vitality Drive clients who complete and pass the Refresher course will earn 150 Vitality Drive points every month for 12 months. The Refresher course consists of a 2-hour session that the driver can complete in one day. The course allows the driver to raise any concerns they may have in terms

of their driving skills. Defensive driving techniques and applications to everyday driving scenarios, including observation skills, ensuring the correct following and stopping distances as well as speed control. Driving in different traffic and weather conditions and on different road types is practised in order to apply the skills learned.

EyeGym – up to 150 Vitality Drive points When clients register for their EyeGym training on www.discovery.co.za, they will have immediate access to the Primary EyeGym course at no extra cost to them. Clients also get the Advanced EyeGym course at a discounted, once-off fee of R200. Clients can earn 150 Vitality Drive points by completing both the Primary course and the Advanced EyeGym course. Clients can even complete both courses at the same time if they want to. When a client logs in to the course for the first time, they will be prompted to do a series of short drills. This will assess their level of visual fitness. The time clients spend on these assessment drills does not form part of their daily EyeGym training time. Primary EyeGym course

Consists of four different drills, each made up of five grades. Across the five grades, there are 10 levels. Clients must pass the necessary levels for each drill to move to a higher grade.

▪ Clients will have access to the Primary EyeGym course for six months every year. For every 10 minutes of training that a client completes, they will earn 10 Vitality Drive points.

▪ Clients can earn a maximum of 50 points for their Primary EyeGym course. The maximum training time clients can do in a day is 10 minutes.

▪ If a client completes the five grades in the Primary course within less than 50 minutes, they will receive their 50 Vitality Drive points even sooner.

▪ If a client does not earn the maximum Vitality Drive points (50 points) within the six months free-access period, they can request to restart the course again for a fee of R85. When a client restarts the course, they then have another chance to earn the balance of their points to a maximum of 50 Vitality Drive points in a year.

The Advanced EyeGym course Consists of four new drills, each made up of five grades. Across the five grades, there are 15 levels in total. Clients can only progress to a higher grade when they have passed the necessary levels for each drill within that grade.

▪ Clients can access the Advanced course for a fee of R200 any time of year. This fee will give clients access to the course for 12 weeks.

▪ For every 10 minutes of training, a client completes in the Advanced course, they will earn 10 Vitality Drive points. Clients can earn up to a maximum of 100 Vitality Drive points.

▪ The maximum training time a client can do in a day is 10 minutes. ▪ If a client does not earn the maximum points within the 12-week access period, they can request to reactivate

the course again for a fee of R200. When a client reactivates the course, they can earn the balance of their points to a maximum of 100 Vitality Drive points in a year.

Discovery Ltd. registration number: 1999/007789/06. Companies in the group are authorised financial services providers.

Short-term insurance by Discovery

Training guide Version19_ August 2021

Page 23 of 249

Confidential

Clients can earn up to 150 Vitality Drive points a month for making sure their

vehicles are safe to drive

Tiger Wheel & Tyre Annual MultiPoint check – 100 Vitality Drive points Clients who pass the Tiger Wheel & Tyre Annual MultiPoint check will earn 100 Vitality Drive points each month for 12 months. The Tiger Wheel & Tyre Annual MultiPoint check is a set of tests done to assess the roadworthiness of the vehicle’s various safety functions and to check its service history. Included in the check are: ▪ Steering wheel ▪ Headlights ▪ Hooter ▪ Tyres

▪ Indicators ▪ Shocks ▪ Windscreen wipers ▪ Seat belts

Clients need to pay R95 for each check. In the event that a client’s vehicle fails the check and the client needs to complete the check again, the client needs to show the results of their previous check to Tiger Wheel & Tyre. If the previous check was done within the last 30 days, then no additional fee will be charged, otherwise another R95 will be payable.