temple bar investment trust plc report and accounts 2006

TRANSCRIPT

Temple Bar Investment Trust PLC

Report and Accounts 2006

Temple Bar Cover with spine:206262 Temple Bar Cover 23/2/07 19:12 Page 1

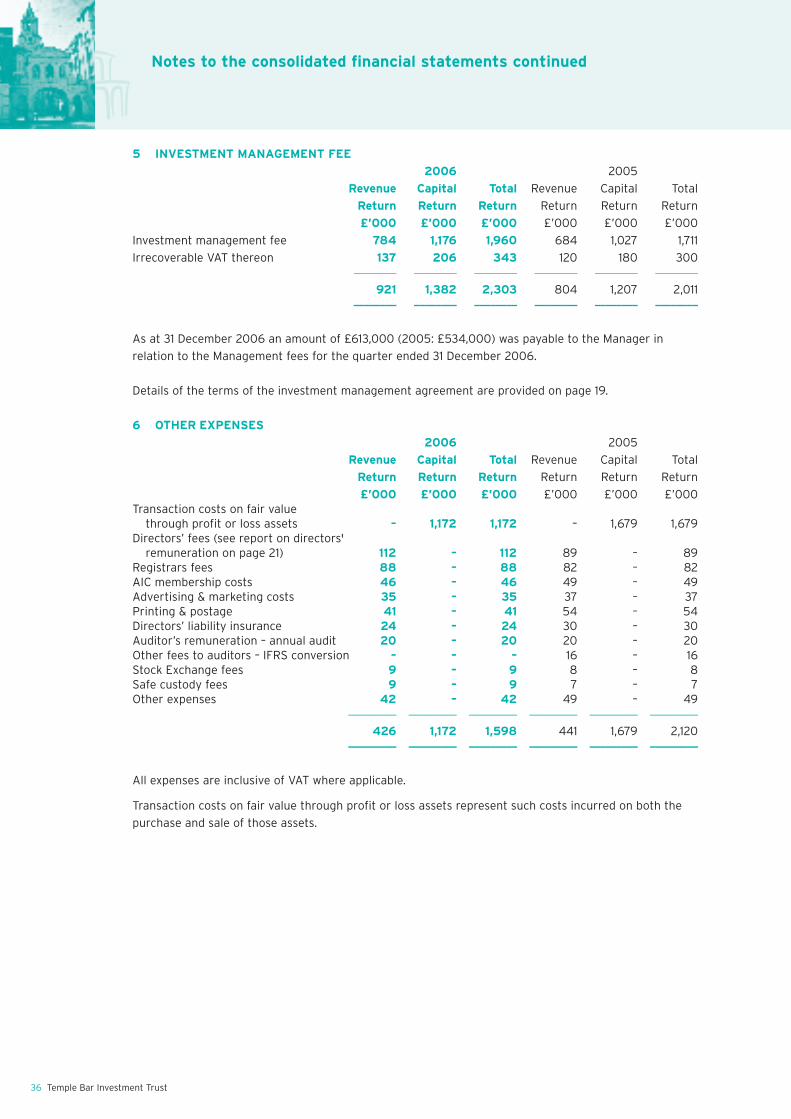

Group summary 1

Summary of results 2

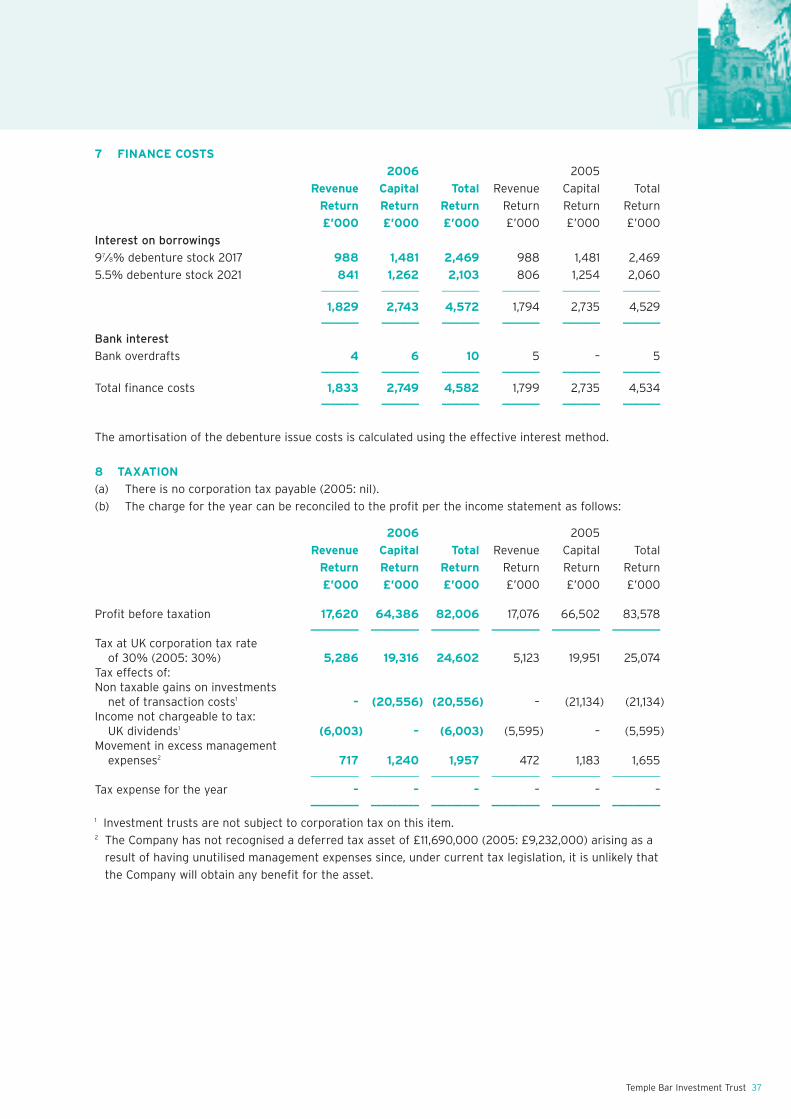

Ten year record 3

Comparative dividend growth 3

Five year summary 4

Directors 5

Management and administration 6

Chairman’s statement 7

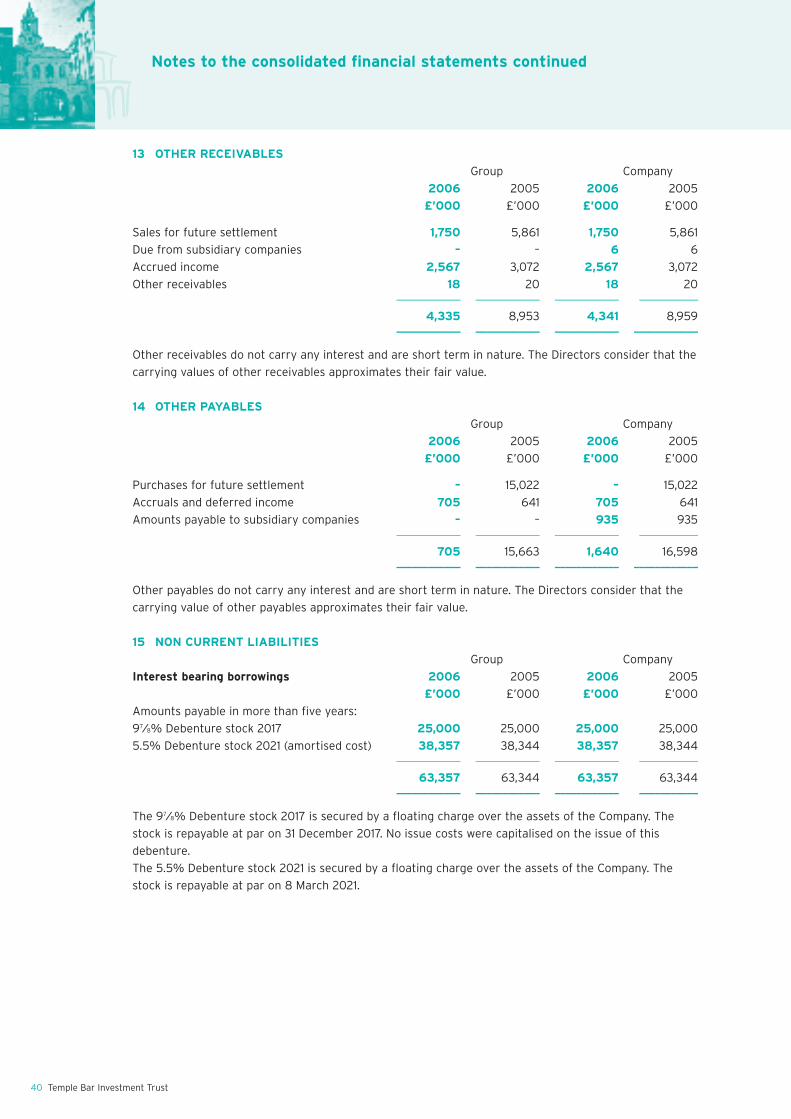

Twenty largest investments 9

Asset allocation 9

Manager’s report 10

Portfolio of investments 13

Report of the directors 16

Report on directors’ remuneration 21

Corporate governance 22

Independent auditors’ report 25

Statement of directors’ responsibilites 26

Consolidated income statement 27

Consolidated statement of changes in equity 28

Company statement of changes in equity 28

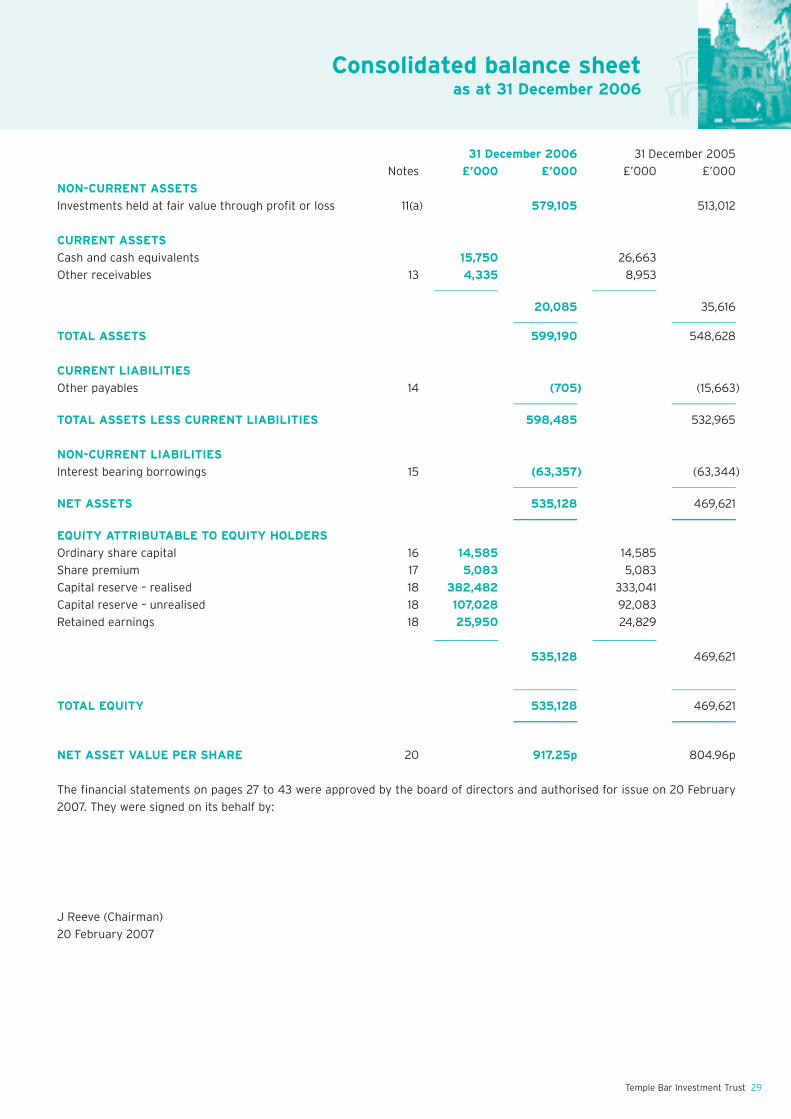

Consolidated balance sheet 29

Company balance sheet 30

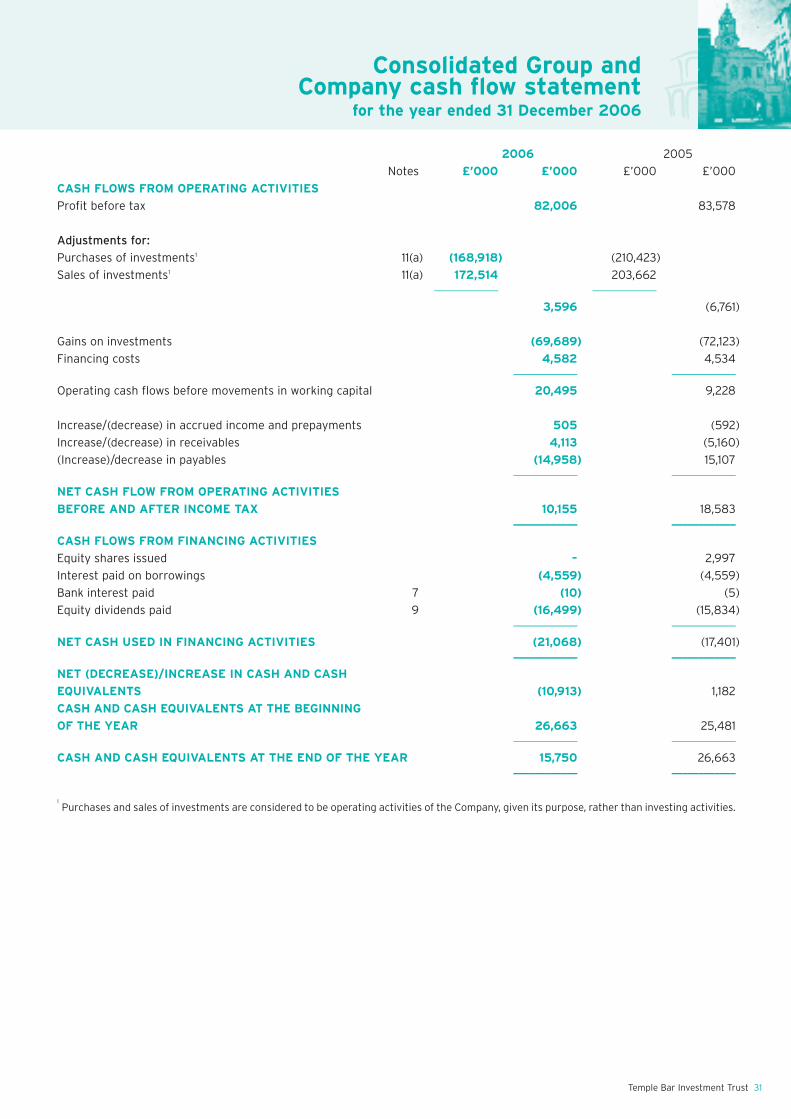

Consolidated group and company cash flow statement 31

Notes to the consolidated financial statements 32

Useful information for shareholders 44

Notice of meeting 45

Temple Bar Investment Trust Savings Scheme 47

Temple Bar Investment Trust

Contents

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page ii

Investment Objective The Company’s investment objective is to provide growth in income and capital to achieve a long term total return greater than the benchmark FTSE All-Share Index, through investment in UK securities. The Company’s policy is to invest in a broad spread of securities with typically the majority of the portfolio selected from the constituents of the FTSE 100 Index.

Benchmark Performance is measured against the FTSE All-Share Index.

Total Assets Less £598,485,000

Current Liabilities

Total Equity £535,128,000

Market Capitalisation £494,729,000

Capital Structure Ordinary shares 58,340,742 shares

5.5% Debenture Stock 2021 £38,000,000

9.875% Debenture Stock 2017 £25,000,000

Voting Structure Ordinary shares 100%.

Winding-Up Date None.

Managers’ Fees 0.35% per annum based on the value of the investments (including

cash) of the Company.

PEP/ISA Status The Company’s shares are capable of being held in an ISA and are a

qualifying investment under the Personal Equity Plan regulations.

AIC Member.

Website www.templebarinvestments.com

Group summary

Temple Bar Investment Trust 1

Group summary

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 1

2 Temple Bar Investment Trust

2006 2005 Percentage

change

ASSETS as at 31 December £’000 £’000––––––––– ––––––––– –––––––––

Consolidated net assets 535,128 469,621 13.95%––––––––– –––––––––

Ordinary shares

Net asset value per share 917.25p 804.96p 13.95%

Net asset value per share adjusted for market value of debt 901.35p 781.47p 15.34%

Market price 848.00p 779.50p 8.79%

Discount 7.5% 3.2%––––––––– –––––––––

2006 2005

REVENUE for the year ended 31 December £’000 £’000––––––––– –––––––––

Revenue return attributable to ordinary shareholders 17,620 17,076––––––––– –––––––––

Revenue return per ordinary share 30.20p 29.35p––––––––– –––––––––

Dividends per ordinary share-interim and proposed final 29.23p 27.83p 5.03%––––––––– –––––––––

2006 2005

CAPITAL for the year ended 31 December £’000 £’000––––––––– –––––––––

Capital return attributable to ordinary shareholders 64,386 66,502––––––––– –––––––––

Capital return attributable per ordinary share 110.36p 114.32p––––––––– –––––––––

2006 2005

TOTAL EXPENSE RATIO* 0.47% 0.46%

%TOTAL RETURNS for the year to 31 December 2006

Return on net assets 17.72

Return on gross assets 16.54

Return on share price 12.42

FTSE All-Share Index 16.75

FTSE 350 Higher Yield Index 14.92

Change in Retail Prices Index over year 4.43

DIVIDEND YIELDS (NET) as at 31 December 2006 %

Yield on ordinary share price (848.00p) 3.33

Yield on FTSE All-Share Index 2.86

Yield on FTSE 350 Higher Yield Index 3.79

*Management fees and all other operating expenses (including tax relief, where allowable, but excluding interest payments and

commissions) expressed as a percentage of average month end net assets over the year.

Summary of results

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 2

Temple Bar Investment Trust 3

Total Net assets Revenue

assets less Group per return to Revenue Dividends

Year current net ordinary ordinary return per share*

ended liabilities assets share shareholders per share (net)

£’000 £’000 p £’000 p p

1997 333,986 308,290 533.82 11,339 19.70 17.60

1998 360,520 335,064 579.56 11,089 19.24 19.36

1999 432,391 369,391 639.16 12,102 20.96 21.30

2000 451,917 388,917 672.95 13,428 23.24 23.43

2001 419,292 356,292 615.43 14,198 24.56 24.84

2002 341,066 278,066 480.24 14,674 25.34 25.59

20031 395,341 332,341 573.88 16,483 28.46 26.23

2004 462,254 398,880 688.78 15,851 27.37 27.02

20052 532,965 469,621 804.96 17,076 29.35 27.83

2006 598,485 535,128 917.25 17,620 30.20 29.23

NOTES

1. In 2003 there was a change of policy on the charging of finance expenses and management fees such that

60% of these (previously 50%) are now charged to capital. No prior years have been restated.

2. In 2005 the Company adopted International Financial Reporting Standards. As a result the 2004 data has been

restated but no prior years have been restated.

*Interim and proposed final for the year.

Comparative Dividend Growth

100

125

150

175

200

Ten year record

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 3

(Discount)/Premium to Net Asset Value

31-Dec-01

31-Mar-02

30-Jun-02

30-Sep-02

31-Dec-02

31-Mar-03

30-Jun-03

30-Sep-03

31-Dec-03

31-Mar-04

30-Jun-04

30-Sep-04

31-Dec-04

31-Mar-05

30-Jun-05

30-Sep-05

31-Dec-05

31-Mar-06

30-Jun-06

30-Sep-06

31-Dec-06

-9%-8%-7%-6%-5%-4%-3%-2%-1%0%1%2%3%4%5%6%

Share Price Total Return

TEMPLE BAR - TOTAL RETURNFTSE ALL SHARE - TOTAL RETURN Source: DATASTREAM

60

80

100

120

140

160

180

31-Dec-01

31-Mar-02

30-Jun-02

30-Sep-02

31-Dec-02

31-Mar-03

30-Jun-03

30-Sep-03

31-Dec-03

31-Mar-04

30-Jun-04

30-Sep-04

31-Dec-04

31-Mar-05

30-Jun-05

30-Sep-05

31-Dec-05

31-Mar-06

30-Jun-06

30-Sep-06

31-Dec-06

Net Asset Value Capital Return

TEMPLE BAR - SHARE PRICETEMPLE BAR - N.A.V. (PAR)FTSE ALL SHARE - PRICE RETURN

Source: DATASTREAM

60

70

80

90

100

110

120

130

140

150

160

31-Dec-01

31-Mar-02

30-Jun-02

30-Sep-02

31-Dec-02

31-Mar-03

30-Jun-03

30-Sep-03

31-Dec-03

31-Mar-04

30-Jun-04

30-Sep-04

31-Dec-04

31-Mar-05

30-Jun-05

30-Sep-05

31-Dec-05

31-Mar-06

30-Jun-06

30-Sep-06

31-Dec-06

Five year summary

4 Temple Bar Investment Trust

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 4

Directors

JOHN REEVE*, Chairman, aged 62, wasappointed a director in 1992. He was formerlyexecutive chairman of the Willis Group, groupmanaging director of Sun Life Assurance Societyand a member of the boards of the Association ofBritish Insurers and the International InsuranceSociety. He is currently Chairman of Alea GroupHoldings (Bermuda) Limited and a director of anumber of other companies.

GARY J ALLEN*†, aged 62, was appointed adirector in 2001. He has over 35 years’ experiencein engineering and is former chairman of IMI PLC.His other directorships include The London StockExchange and N V Bekaert SA.

RICHARD W JEWSON*, aged 62, was appointeda director in 2001. He first worked in the timberand building material supply industry, becomingmanaging director of Jewson the buildersmerchants for twelve years from 1974, and thenmanaging director and chairman of its parentcompany Meyer International PLC from which heretired in 1993. He is currently chairman of PFI Infrastructure PLC and Archant Limited, and anon-executive director of Grafton Group PLC andClean Energy Brazil PLC.

JUNE F de MOLLER*, aged 59, was appointed adirector in 2005. She is a non-executive directorof Derwent London PLC, Archant Limited and a

former managing director of CarltonCommunications PLC. She was previously a non-executive director of J Sainsbury PLC, CooksonGroup PLC and BT PLC.

MARTIN R RILEY*, aged 63, was appointed adirector in 2004. He has over 35 years’ experiencein stockbroking and fund management in the Cityand is a former director of Henderson CrosthwaiteLtd, Guinness Mahon & Co Ltd and Barlows PLC. Heis currently chairman of SR Europe InvestmentTrust PLC and Howard Investment Company Ltd anda director of Bonfield Asset Management Ltd andvarious private investment companies.

FIELD L J WALTON*, aged 66, was appointed adirector in 1983. He started his career inengineering management and moved to the Cityas an analyst with Cazenove in 1971. Subsequentlyhe held a number of positions in fundmanagement. He is currently a consultant toMacArthur & Co. Limited, a former chairman ofBiofuels Corporation PLC and a non-executivedirector of a number of engineering and trustcompanies. He is also a director of Harrods GroupTrustees Ltd.

*Independent non-executive director and member of the audit

committee and nomination committee.

†Chairman of the audit committee and Senior Independent

Director.

from left to right; June de Moller, Gary Allen, John Reeve, Martin Riley, Field Walton, Richard Jewson

Temple Bar Investment Trust 5

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 5

Investment ManagerInvestec Investment Management LimitedAuthorised and Regulated by the Financial Services Authority2 Gresham Street, London EC2V 7QPTelephone No. 020 7597 2000Facsimile No. 020 7597 1803

Registered Office2 Gresham Street, London EC2V 7QPSecretary: Investec Investment ManagementLimited, represented by M K Slade FCIS

Registered NumberRegistered in England No. 214601

RegistrarLloyds TSB Registrars, ScotlandPO Box 28506, Finance House, Orchard Brae, Edinburgh EH4 1XZTelephone No: 0870 6015366 (shareholder helpline)

0891 105366 (broker helpline)

Registered AuditorErnst & Young LLP1 More London Place, London SE1 2AF

Bankers and CustodianHSBC Bank plc, Poultry, London EC2P 2BX

StockbrokersJPMorgan Cazenove20 Moorgate, London EC2R 6DA

SolicitorsEversheds, Senator House, 85 Queen Victoria Street, London EC4V 4JL

from left to right; Peter Lowery, Jo Slater, David Lynch, Alastair Mundy, Martin Slade, Mark Wynne Jones, Celia Duncan

Management and administration

6 Temple Bar Investment Trust

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 6

The total return on thenet assets of TempleBar during 2006 was17.7%, which compareswith a total return forthe FTSE All-ShareIndex of 16.8%. Thereturn achieved is acombination ofunderlying portfolioperformance and theeffect of the capitalgearing of the Trust.

While it is always pleasant to report positively onshort-term performance, the Board is primarilyfocused on longer time periods. The five year trackrecord, over which the fund manager is principallyjudged, demonstrates sustained positiveperformance.

The Board is recommending a final dividend of 19.88p,to produce a total increase for the year of 5.0%. Thisdividend will be payable on 30 March 2007 toshareholders on the register as at 16 March 2007.This is the 23rd consecutive year that the dividendhas been increased. The revenue reserve, which, afteradjusting for the proposed final dividend for 2006,represents 84.2% of the 2006 dividend, shouldprovide shareholders with additional comfortregarding the security of the dividend.

Post-tax revenue earnings increased by 3.2%. Theproposed dividend was more than covered by netearnings generated on the portfolio during the year.The level of capital gearing, 11.9% at year end, againcontributed positively to performance during theperiod.

The price of Temple Bar shares traded at a smalldiscount to their underlying asset value throughoutthe year, once again supported by the steady demandcreated within the Company’s Savings Scheme. TheBoard has encouraged the Manager to maintain aregular dialogue with our larger shareholders andinvestment intermediaries.

StrategyAt the Board’s strategy review this year, inconjunction with the Manager, the strategy behind

the Temple Bar portfolio was assessed against boththe latest market developments and shareholders’expectations. Investment restrictions on theManager were also reviewed.

Overall, the conclusion of this discussion was thatmajor changes were not warranted but that therelaxation of selective constraints would provide theManager with greater flexibility and increase thepotential for out-performance of both ourbenchmark, the FTSE All-Share Index, and our peergroup, without a significant increase in long-termrisk. Inter alia, it was decided that the fund managershould have the authority to invest up to 50% ofthe portfolio in stocks outside the FTSE 100 (against30% previously) and that the Board would considerrequests to extend the non-FTSE 100 componentbeyond this point.

To reflect this greater flexibility, the Board hasagreed a new investment policy with the Manager,which is included on page 1 of these Report andAccounts.

The fund manager has no immediate plans to makeuse of this increased flexibility; as he details in hisreport, he currently sees greater value in the largeststocks in the market.

The Board also decided to ask the Manager tosecure an overdraft facility of £25m, to consider theuse of options as part of an overall hedgingstrategy, in particular market conditions, and to beaware of the potential for investing in ‘specialsituations’, such as high yield debt, in line with hiscontrarian principles. It was further felt that theManager should have greater flexibility with regardto balancing potential revenue and capital growthopportunities and it was agreed, therefore, that inany one year, up to 7.5% of the revenue reservecould be used to fund the dividend, if necessary.

OutlookThe bull market is now over four years old and overthat time some dramatic returns have beenachieved. The FTSE 100 has more than doubled(after reinvesting income) and the FTSE 250 (the250 largest stocks in the UK market after the

Chairman’s statement

Temple Bar Investment Trust 7

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 7

FTSE 100) has risen by over 200%. Corporateprofit margins are generally high, which manywould regard as unsustainable, and thevaluations of most companies are well above thelows they reached during the bear market.

The Manager believes that much of the valuethat remains in the market is to be foundamongst the largest companies as these offer animpressive combination of low valuations, strongbalance sheets, a greater security of earningsand better prospects for dividend growth. As aresult of this view, the portfolio is moreconcentrated than has been the normhistorically.

Any interruption to the earnings momentum thathas driven the market in the last few years islikely to increase volatility and thus provide anenhanced number of contrarian opportunities forour Manager to investigate. Currently, ourManager prefers to hold a portfolio more biasedtowards security than risk.

Annual General MeetingThe AGM will be held on Monday 26 March at theManagers’ office in London. In addition to theformal business of the meeting, the Managerswill make a presentation to shareholdersreviewing the past year and commenting on theoutlook. I look forward to welcoming as many ofyou as possible. Shareholders who are unable toattend the meeting are encouraged to use theirproxy votes.

John Reeve20 February 2007

Chairman’s statement continued

8 Temple Bar Investment Trust

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 8

UK Fixedinterest

Cash& other

Preferenceshares

Ordinaryshares

Twenty largest investmentsas at 31 December 2006

Total

Valuation Valuation assets

31 December Net purchases/ Appreciation/ 31 December less current

Company 2005 (sales) (depreciation) 2006 liabilities

£’000 £’000 £’000 £’000 %

Royal Dutch Shell 39,750 4,666 (1,523) 42,893 7.17

BP 24,322 21,873 (4,580) 41,615 6.95

HSBC 18,372 21,302 (394) 39,280 6.56

Vodafone 36,395 – (489) 35,906 6.00

GlaxoSmithKline 35,123 3,728 (3,088) 35,763 5.98

Royal Bank of Scotland 25,974 – 3,522 29,496 4.93

BT 15,686 – 5,545 21,231 3.55

AstraZeneca 13,721 6,640 (928) 19,433 3.25

Unilever 10,071 6,361 1,863 18,295 3.06

Signet – 14,356 2,234 16,590 2.77

HBOS 9,892 3,880 1,877 15,649 2.61

Prudential 16,299 (5,995) 4,448 14,752 2.46

Centrica 15,285 (5,908) 4,803 14,180 2.37

Legal & General 10,980 – 3,195 14,175 2.37

Amvescap 9,945 (562) 3,431 12,814 2.14

Kingfisher 8,897 2,230 202 11,329 1.89

Daily Mail & General Trust – 9,392 1,153 10,545 1.76

ITV 10,913 – (583) 10,330 1.73

HMV 2,711 9,748 (2,426) 10,033 1.68

Taylor Nelson Sofres 4,158 4,011 892 9,061 1.51–––––––––––– –––––––––––– –––––––––––– –––––––––––– –––––––

308,494 95,722 19,154 423,370 70.74–––––––––––– –––––––––––– –––––––––––– –––––––––––– –––––––

All securities in any one company are treated as one investment.

Asset allocation as at 31 December 2006BY CLASS (%) PORTFOLIO DISTRIBUTION (%)

%Ordinary shares 96.36UK Fixed interest 0.24Preference shares 0.16Cash & other 3.24

––––––100.00––––––

%Oil & Gas 14.59Basic Materials 0.59Industrials 3.67Consumer Goods 7.04Health Care 9.53Consumer Services 24.79

%Telecommunications 10.87Utilities 3.20Technology 0.64Financials 24.83UK Fixed Interest 0.25

––––––100.00––––––

Oil & GasBasic

Materials

Industrials

ConsumerGoods

Health Care

Consumer ServicesTelecommunications

Utilities

Technology

Financials

UK Fixed Interest

Temple Bar Investment Trust 9

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 9

In 2006, the UK equity market delivered

investors a fourth successive year of gains. The

prevalent themes of the last few years remained

in place: a belief that valuations were low, good

growth of profits and dividends and a high level

of merger and acquisition activity. Although

inflationary fears started to pick up, together

with the long-anticipated slowdown in US

economic growth, investor sentiment remained

positive.

The rise in the UK market from the low point of

March 2003 until the correction of Spring 2006

was the longest recorded uptrend without a 10%

pullback. Somewhat paradoxically the 10% fall in

the FTSE 100 was immediately labelled as

‘healthy’ and provided the bulls with the

justification for a strong recovery. They argued

that in late 2005 and early 2006 the market had

become less sensitive to risk and needed the

correction to remove the froth before it could

reach new highs. However, although the UK

market did hit these new highs later in the year,

it was not evident that the setback had

encouraged investors to become more risk

averse. In fact, it seemed that the exact opposite

had occurred – medium-sized equities continued

to outperform their larger peers; emerging

market equities recovered faster than developed

markets; spreads on high yield bonds relative to

government bond yields narrowed to multi-year

lows.

The performance of the portfolio over the year

may be viewed as two distinct parts: under-

performance relative to the market in the first

part being countered by out-performance in the

second part. In the first part, ending in April, the

market favoured stocks with a ‘story’: preferably

one stretching well into the future. In particular,

many investors continued to be attracted by

stories of a new paradigm in the commodity

markets. We thought the future in these areas

was less clear cut and that the expected

profitability and ratings attached to them by the

market were too high. The spring sell-off brought

a reversal in the Mining sector and, although the

overall market ended the year higher, the larger

miners such as Rio Tinto and BHP Billiton

recovered little of their lost ground over the

remainder of the year. Our nil exposure to this

sector contributed significantly to our improved

performance during the market fall.

10 Temple Bar Investment Trust

Manager’s report

The fall appeared to refocus investors on their

other target – ‘medium-sized’ equities, although

this description is not clear cut. Certainly, the

groupings used by most market commentators to

determine size: FTSE 100 (the largest 100

companies by market capitalization), FTSE 250

(the next 250 companies – hence mid caps) and

the FTSE Small Cap (the remaining 350 or so

companies in the FTSE All-Share Index) are too

rigid. Currently, instead, medium-sized seems to

be shorthand for the bid potential of any

company.

The shorthand may be simplistic, but it seems

justifiable when related to investor behaviour. A

number of ‘medium-sized’ companies have

received bids in the last few years, and the

pattern could well continue. With bidders often

motivated by the combination of potential cost

cutting opportunities, increased leverage and

fairly cheap funding, the potential for bids has

played on the twin emotions of fear and greed

that investors have always found hardest to

control. Their fear of missing out on a bid, having

held a stock for some time, and the greed for

receiving a bid, skewed supply and demand of

these stocks, leading, in our opinion, to a number

of them now trading at rich valuations.

PERFORMANCE ATTRIBUTION ANALYSIS

The following illustrates the factors that have

contributed to the Company’s performance in the

year to 31 December 2006:

Attribution Analysis %

Total return of FTSE All-Share Index 16.75

Relative return from the portfolio 0.30––––––––

Performance on total assets 17.05

Income distributed to shareholders* (3.33)

Expenses* (0.51)

Finance costs* (0.92)––––––––

12.29

Impact of gearing on portfolio 1.66––––––––

Change in net asset value

per ordinary share 13.95––––––––

* as percentage of opening NAV

High valuations, while not necessarily an

obstruction to higher prices, undoubtedly

increase the risk to an investor (assuming that

Annual report • Final copy:Temple Bar RA 23/2/07 19:20 Page 10

value of their Russian assets. The largest

pharmaceutical companies, GlaxoSmithKline and

AstraZeneca provided little encouragement

about the development of new drugs; and the

largest banks, HSBC and Royal Bank of Scotland,

suffered minor profit downgrades as the first

signs of a US consumer slowdown diminished the

quality of their loan books.

These stocks have now reached such low

valuations that we believe a great deal of

negative news is already included in their prices.

In fact, we can find few stocks elsewhere in the

market offering such a good combination of

secure earnings, balance sheet strength, dividend

growth and valuation support. Therefore, during

the year, we increased our holdings of all, except

Royal Bank of Scotland. These companies could

be involved in merger, and possibly de-merger,

activity in the future – and this is clearly not

discounted in their existing valuations. As a

result of these attractions, a significant part of

the portfolio is represented by a relatively small

number of holdings. While this might displease

advocates of investment diversification, we

believe that when building a portfolio it is of

primary importance to focus on finding cheap

stocks, rather than targeting a specific number of

holdings. While through the cycle we would

expect to have a greater number of holdings of

medium-sized companies, their valuations

currently preclude this and we are content with

an increased focus on the largest companies.

Another theme to note in the portfolio is the

sizeable position in the Media and General Retail

sectors. Many of these holdings have been

affected by rapid changes in consumer behaviour

that have occurred, or in some instances are

expected to occur, as a result of the increasing

usage of the internet. For example, HMV and

Woolworths have been affected by severe price

deflation in the CD and DVD market and Trinity

Mirror and ITV have suffered as advertising has

moved away from some traditional markets.

BSkyB and EMI have been volatile while investors

attempt to clarify whether they will retain their

large market positions, or whether customers will

find it easier and cheaper to access these

companies’ products in alternative ways.

However, we believe it is important to bear in

mind some positive prospects for these

the fundamentals of the company are

unchanged). Currently, investors appear happy to

accept the risk, believing that they are

underwritten by bidders, particularly private

equity buyers ready to pounce if prices fall. This

may be true to some extent but, historically,

private equity managers have avoided paying

high prices without good reason.

Given this background, it is no surprise that the

biggest contributors to the portfolio’s relative

performance during the year came mainly from

medium-sized companies: Cable & Wireless,

easyJet, N Brown, ICAP (all FTSE 250

constituents) and Centrica, Amvescap,

Legal & General and BT (FTSE 100 constituents

but still within biting distance of private equity).

As always, there were stocks whose performance

disappointed such as HMV, GlaxoSmithKline and

Royal Dutch Shell. However, in general, the

portfolio benefited from the absence of any

stocks which were significant negative

contributors to performance. It is important to

stress that this will not always be the case. As

contrarian investors, we are always seeking to

buy stocks that are significantly out of favour but

have the potential to exhibit strong share price

performance. With hindsight, we can see that

while some stocks are indeed out of favour but

cheap, others are out of favour but expensive.

History shows that the majority of stocks mean

revert, ie what goes down comes back up and

vice versa, in terms of both profitability and

share price, and our analysis aims to put the

odds on success further in our favour. However,

any portfolio will include some losers – those that

don’t mean revert in our holding period – and

sometimes no amount of analysis will protect a

fund from this.

Last year we highlighted the apparently

attractive valuations of many FTSE 100

companies which had clearly under-performed

the broader market for a number of years.

Generally, these companies, and in particular

many of the largest ones, disappointed again in

2006. As noted above, the market’s focus on

potential bid stocks offered little sustenance to

the market’s giants, and the newsflow from these

companies offered little to excite investors. In the

Oil sector, BP was affected by safety issues, and

Royal Dutch Shell and BP by concerns over the

Temple Bar Investment Trust 11

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 11

12 Temple Bar Investment Trust

and, particularly, the high quality customer

service associated with a familiar and well

regarded chain of physical high street stores.

Simultaneously, management promoted internet

sales to attract or retain price conscious

customers. Investors warmed to this strategy and

despite a disappointing Christmas trading

statement, the shares stand significantly higher

than the level at which we purchased them.

We purchased our holding in Jessops when the

shares were out of favour, and most

commentators believed the company to be in

structural decline. The market often exaggerates

a company’s problems, but we know that

outcomes are often far more positive than seem

likely when the panic is at its peak.

One possible reading of events in 2006 is that

investors took the Spring correction as a

warning, and subsequently increased the

protection element in their portfolios. However,

rather like driver self-confidence induced by seat

belts and air bags, it is possible that the

correction encouraged greater acceptance of

risk. Clearly, risk is reduced if protection is

precisely aligned with the constituent parts of

the portfolio. However, the science is undermined

by the capricious nature of asset markets, where

an imperfect hedge may provide far less

protection than expected in a severe market sell-

off, and could result in risky assets being

liquidated. In turbulent markets, this alone could

create downward momentum.

These factors of portfolio construction tend

currently to focus us on lowly rated liquid stocks

and strong balance sheets. Of course, if our

opinion hardens, we could easily increase the

level of liquidity on the portfolio, or buy some

protection. However, while market conditions

allow us to purchase a sufficient number of

stocks with the characteristics we desire, we are

happy to be almost fully invested.

Alastair Mundy

Investec Investment Management Limited

20 February 2007

companies. The swift take-up of broadband

internet has surprised many commentators, and

company managements have often been caught

without a strategic response. Although the

internet has encouraged new competition, much

of which did not exist even ten years ago, the

strengths of the incumbent companies should

not be under-stated.

In most cases, the incumbents are now

establishing, or have already established, equally

dominant positions on the internet. For example,

in the past few months, HMV’s Waterstone’s has

launched its own website, while most of the

largest UK recruitment websites are now owned

by traditional media companies, successfully

defending their positions.

It is always difficult to disentangle a structural

theme from a cyclical theme. The weakness of

sales in HMV and Woolworths may be as much a

reflection of poor music and indifferent film

releases – a cyclical effect – as of a structural

move to the internet.

Some of the changes may be faddish. For

example, companies may have been encouraged

to move their advertising away from traditional

media towards the internet; however, as the

power of internet advertising is untested, some

move back to the traditional formats is, at least,

possible.

Many incumbent companies have unassailable

content or brands. As a case in point EMI’s back

catalogue of music, and ITV’s archive of classic

programmes, are unique and, in fact, will

probably respond positively to new delivery

channels.

Finally, and perhaps most importantly, the

weakened share prices of these companies

already discount very unattractive scenarios.

Wider appreciation of any of the positives listed

above could significantly affect valuations.

Our holding in Jessops, the camera retailer,

provides a good case study. In 2005, investors

were concerned that a large percentage of

camera sales was likely to migrate from shops to

the internet; and, indeed, the company’s

operating performance suggested this was

already happening. As a result, the shares halved

from their peak. However, management quickly

assessed the gravity of the problem and

implemented a strategy utilising the advantages

Manager’s report continued

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 12

Temple Bar Investment Trust 13

Portfolio of investments

Valuation of FTSE All-holding as at Share Index31 December Percentage of 31 December

2006 Portfolio 2006£’000 % %

OIL & GAS

Oil & Gas 14.59 14.47BP 41,615Royal Dutch Shell (‘B’ shares) 42,893

––––––––––– –––––––––––14.59 14.47

––––––––––– –––––––––––

BASIC MATERIALS

Chemicals 0.59 0.58Scapa 397Yule Catto 3,026

Basic Resources – 6.67––––––––––– –––––––––––

0.59 7.25––––––––––– –––––––––––

INDUSTRIALS

Construction & Materials 0.93 0.67Heywood Williams 5,380

Industrial Goods & Services 2.74 6.78Alpha Airports 1,450Invensys 3,409Qinetiq 1,526St Ives 5,900TDG 3,567

––––––––––– –––––––––––3.67 7.45

––––––––––– –––––––––––

CONSUMER GOODS

Automobiles & Parts – 0.12Food & Beverage 5.21 4.82

Britvic 6,225Unilever 18,295UNIQ 5,638

Personal & Household Goods 1.83 4.71Alba 1,036British American Tobacco 5,879SSL International 3,697

––––––––––– –––––––––––7.04 9.65

––––––––––– –––––––––––

HEALTH CARE

Health Care 9.53 7.30AstraZeneca 19,433GlaxoSmithKline 35,763

––––––––––– –––––––––––9.53 7.30

––––––––––– –––––––––––

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 13

14 Temple Bar Investment Trust

Portfolio of investments continued

Valuation of FTSE All-holding as at Share Index31 December Percentage of 31 December

2006 Portfolio 2006£’000 % %

CONSUMER SERVICES

Retail 12.47 5.46Alexon 2,065Brown (N) 7,366Greggs 6,020HMV 10,033Jessops 5,305JJB Sports 5,970Kingfisher 11,329Mothercare 3,219Signet 16,590Woolworths 4,301

Media 10.21 3.32British Sky Broadcasting 7,960Daily Mail & General Trust 10,545EMI 2,848Future 5,386ITV 10,330Reuters 8,415SMG 544Taylor Nelson Sofres 9,061Trinity Mirror 4,038

Travel & Leisure 2.11 3.40Carnival 1,950Compass 3,551Easyjet 3,188Millennium & Copthorne 3,515

––––––––––– –––––––––––24.79 12.18

––––––––––– –––––––––––

TELECOMMUNICATIONS

Telecommunications 10.87 5.73BT 21,231Cable & Wireless 5,837Vodafone 35,906

––––––––––– –––––––––––10.87 5.73

––––––––––– –––––––––––

UTILITIES

Utilities 3.20 4.63Centrica 14,180Scottish Power 4,327

––––––––––– –––––––––––3.20 4.63

––––––––––– –––––––––––

TECHNOLOGY

Technology 0.64 0.99Alphameric 167Computacenter 3,182Spirent Communications 382

––––––––––– –––––––––––0.64 0.99

––––––––––– –––––––––––

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 14

Temple Bar Investment Trust 15

Valuation of FTSE All-holding as at Share Index31 December Percentage of 31 December

2006 Portfolio 2006£’000 % %

FINANCIALS

Banks 14.58 17.59HBOS 14,716HBOS (9.25% non cum pref shares) 933HSBC 39,280Royal Bank of Scotland 29,496

Insurance 7.08 4.80Friends Provident 4,837Highway Insurance 1,009Legal & General 14,175Prudential 14,752Resolution 508Standard Life 5,720

Financial Services 3.17 7.96Amvescap 12,814Framlington Innovative Growth Trust 1,556Wichford 3,969

––––––––––– –––––––––––24.83 30.35

––––––––––– –––––––––––

UK FIXED INTEREST

BAA 11.75% 2016 1,470 ––––––––––– ––––––––––– –––––––––––

TOTAL BONDS 1,470 0.25 –––––––––––– ––––––––––– –––––––––––

––––––––––– ––––––––––– –––––––––––TOTAL VALUATION OF PORTFOLIO 579,105 100.00 100.00

––––––––––– ––––––––––– –––––––––––

All investments are ordinary shares unless otherwise stated.

––––––––––– ––––––––––– –––––––––––TOTAL EQUITIES 577,635 99.75 100.00

––––––––––– ––––––––––– –––––––––––

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 15

16 Temple Bar Investment Trust

Report of the directors

The directors present their report and accountsfor the year ended 31 December 2006.

BUSINESS REVIEW

Introduction

This business review forms part of the Directors’Report. Its function is to provide a balanced andcomprehensive review of the Company’sperformance and development during the yearand its position at the year end. The review alsocovers the principal risks and uncertainties facedby the Company and sets out key performanceindicators used to measure, monitor and managethe Company’s business.

Business of the Company

The Company carries on business as aninvestment trust and was approved by HMRevenue & Customs as an investment trust inaccordance with Section 842 of the Income &Corporation Taxes Act 1988 for the year ended 31December 2005. In the opinion of the directorsthe Company has subsequently conducted itsaffairs so that it should continue to qualify.

The Company’s principal business activity ofinvestment management is sub-contracted toInvestec Investment Management Limited (‘IIM’)under the ultimate supervision of the board ofdirectors. The Company has one active whollyowned subsidiary company, whose principalactivity is investment dealing and one dormantsubsidiary.

A review of the business is given in theChairman’s statement and the Manager’s report.The results of the Group are shown on page 27.

Investment Objective and Policies

The Company’s investment objective is to providegrowth in income and capital to achieve a longterm total return greater than the benchmarkFTSE All-Share Index, through investment in UKsecurities. The Company’s policy is to invest in abroad spread of securities with typically themajority of the portfolio selected from theconstituents of the FTSE 100 Index.

Investment Approach

The investment approach of our Manager ispremised on a contrarian view on the timing ofbuy and sell decisions, buying the shares ofcompanies when sentiment towards them is at ornear its worst, and selling them as fundamentalprofit improvement and/or re-evaluation of theirlong-term prospects takes place.

The belief is that repeated investor behaviour in

driving down the prices of ‘out-of-favour’companies to below their fair value will offerinvestment opportunities provided a typicalemotional response to both good and bad newscan be avoided. This will allow the Company topurchase shares at significant discounts to theirfair value and sell them as they become morefully valued, principally as a result of predictablepatterns in human psychology.

The Manager’s process is designed to produce‘best ideas’ to drive active fund managementwithin a rigorous control framework. Theframework begins through narrowing down theuniverse of stocks by passing those companieswith a market capitalisation above £100mthrough a screening process which highlights the weakest performing stocks. This isolatesopportunities with attractive sentimentcharacteristics which are then in turn scrutinisedin greater detail to identify investmentopportunities.

The process is very much bottom-up, and canresult in large sector positions being taken ifenough stocks of sufficient interest are foundwithin one sector. However, top down riskanalysis is undertaken to identify potentialconcentration of risk and to factor thisawareness into portfolio construction. Theportfolio comprises stocks which have beenpurchased for different reasons and at differenttimes. In general, because of the bottom-upapproach to stockpicking, each of these reasonsis independent of the other and the portfolio,therefore, is not excessively vulnerable to longer-term macro trends. Cash is a residual of theprocess and normally will not exceed 5% of theportfolio value.

The approach to stock selection and portfolioconstruction is driven by four core beliefs:

1. Markets overreact to news on the upside and

the downside. The Manager aims to be

sceptical of the crowd and aware of investor

psychology, which often causes overvaluation

of those stocks that are deemed to have good

prospects and an undervaluation of those

which are out of favour.

2. There are few companies which sustain below

normal profits over the longer term. Weaker

companies tend to leave an industry, thus

improving the balance of supply and demand,

are bid for or management is changed.

Similarly, there are few companies which can

sustain supernormal profits over the longer

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 16

Temple Bar Investment Trust 17

term. Such profits tend to be competed or

regulated away.

3. Fundamental valuation is the key determinant

of stock prices over the long-term. In other

words ‘cheap’ stocks will outperform

‘expensive’ stocks.

4. Diversification is an important control.

Particular companies or sectors can be out of

favour for a considerable time.

Performance

In the year to 31 December 2006 the net asset

value total return of the Company increased by

17.72% compared with the total return by the

Company’s benchmark index of 16.75%. The

investment manager’s report on pages 10 to 12

includes a review of developments during the

year together with information on investment

activity within the Company’s portfolio.

Key Performance Indicators

The key performance indicators (‘KPIs’) used todetermine the progress and performance of theCompany over time and which are comparable tothose reported by other investment trusts are setout below:-

– Net asset value total return relative to the FTSE

All-Share Index

– Performance attribution

– Discount on net asset value

– Earnings and dividends per share

– Total expense ratio

While some elements of performance againstKPIs are beyond management control theyprovide measures of the Company’s absolute andrelative performance and are, therefore,monitored by the board on a regular basis.

Net Asset Value Total Return

In reviewing the performance of the assets of theCompany’s portfolio the Board monitors the netasset value in relation to the FTSE All-ShareIndex. During the year the net asset value totalreturn of the Company rose by 17.72% comparedwith a rise of 16.75% by the FTSE All-Share Index.

Performance Attribution

The purpose of performance attribution analysis

is to assess how the Company achieved its

performance relative to its benchmark index.

Details of the attribution analysis for the year

ended 31 December 2006 are given in the

investment manager’s report on page 10.

Discount on Net Asset Value

The Board monitors the premium/discount atwhich the Company’s shares trade in relation tothe assets. During the year the shares traded atan average discount to NAV of 3.5%. The Boardand Manager closely monitor both movements inthe Company’s share price and significantdealings in the shares. In order to avoidsubstantial overhangs or shortages of shares inthe market the Board asks shareholders toapprove resolutions each year which allow forthe buy back of shares and their issuance whichcan assist in the management of the discount.Regular demand generated by monthlyinvestment in the Savings Scheme and the use ofmarketing and promotional activity also assist inkeeping the discount at an acceptable level.

Earnings and Dividend Per Share

It remains the directors’ intention to distributeover time by way of dividends substantially all ofthe Company’s net revenue income afterexpenses and taxation. The Manager aims tomaximise total returns from the portfolio andattaches great importance to dividends inachieving total return. The portfolio will typicallyprovide a yield premium to the market. The finaldividend recommended for the year is 19.88p perordinary share which brings the total for the yearto 29.23p per ordinary share, an increase of5.03%. This increase exceeds the RPI inflation of4.43% by a comfortable margin and is the 23rdconsecutive year in which the Company hasincreased the overall level of its dividendpayment.

Total Expense Ratio (TER)

The TER is an expression of the Company’smanagement fees and all other operatingexpenses (including tax relief where allowablebut excluding interest payments) as a percentageof average month end net assets over the year.The TER for the year ended 31 December 2006was 0.47% (2005 0.46%). The Board reviewseach year a comparison of the Company’s TERwith those of its peers. At the present time theCompany has one of the lowest TERs in theincome and growth sector of investment trustcompanies.

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 17

18 Temple Bar Investment Trust

Report of the directors continued

Principal Risks and Uncertaintities

The principal risks facing the Company fall underthe general categories of strategy, operationaland management risks. With the assistance ofthe Manager the Board has drawn up a riskmatrix which identifies the key risks to theCompany under these broad headings. The Boardreviews and agrees policies, which have remainedunchanged since the beginning of the accountingperiod, for managing these risks as summarisedbelow.

Investment Strategy

An inappropriate investment strategy on matterssuch as asset allocation or the level of gearingmay lead to underperformance against theCompany’s benchmark index or peer companies,resulting in the Company’s shares trading on awider discount. The Board manages such risks bydiversification of investments through itsinvestment restrictions and guidelines, which aremonitored and reported on by the Manager. TheManager provides the directors with regular andaccurate management information includingabsolute and relative performance data,attribution analysis, revenue estimates, liquidityreports, risk profile and shareholder analysis. TheBoard monitors the implementation and resultsof the investment process with the investmentManager, who attends Board meetings.Periodically the Board holds a separate meetingdevoted to strategy.

Income Risk – Dividends

Generating the necessary level of income fromportfolio investments to meet the Company’sexpenses and to provide adequate reserves fromwhich to base a sustainable programme ofincreasing dividend payments to shareholders issubject to the risk that income generation frominvestments fails to meet the level required. TheBoard monitors this risk through the receipt ofdetailed income reports and forecasts which areconsidered at each meeting. As at 31 December2006 the Company had distributable revenuereserves of £25,071,000 before declaration ofthe final dividend for 2006.

Share Price Risk

The Company’s share price and discount to netasset value are monitored by the Manager and isconsidered by the Board at each meeting. Someshort term influences over the discount may beexercised by the use of share repurchases atacceptable prices; however, market sentiment is

beyond the absolute control of the managementand Board.

Accounting Legal & Regulatory

In order to qualify as an investment trust theCompany must comply with Section 842 of theIncome & Corporation Taxes Act 1988. Were theCompany to breach Section 842 it might loseinvestment trust status and, as a consequence,gains within the Company’s portfolio would besubject to capital gains tax. The Section 842qualification criteria are, therefore, monitored bythe Board at each meeting.

The Company must also comply with theprovisions of the Companies Acts and, since itsshares are listed on the London Stock Exchange,the UKLA Listing Rules. A breach of theCompanies Acts could result in the Companybeing fined or subject to criminal proceedings.Breach of the UKLA Listing Rules could result inthe Company’s shares being suspended fromListing which in turn would breach Section 842.The Board relies on the services of its companysecretary, Investec Investment ManagementLimited, and its professional advisers to ensurecompliance with the Companies Acts and theUKLA Listing Rules.

Corporate Governance and Shareholder

Relations

Details of the Company’s compliance withcorporate governance best practice includinginformation on relations with shareholders, areset out in the corporate governance report onpages 22 to 24.

Control Systems Risk

Disruption to, or failure of, IIM’s accounting,dealing or payments systems or the custodian’srecords could prevent accurate reporting andmonitoring of the Company’s financial position.Details of how the Board monitors the servicesprovided by IIM and its associates and the keyelements designed to provide effective internalcontrol are included within the internal controlsection of the corporate governance report onpages 22 to 24.

Other Risks

Other risks to which the Company is exposed andwhich form part of the market risks referred toabove are included in note 22 to the financialstatements together with summaries of thepolicies for managing these risks. Thesecomprise; market price risk, interest rate risk,liquidity risk and counterparty risk.

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 18

Temple Bar Investment Trust 19

The Board confirms that there is an ongoingprocess for identifying, evaluating and managingstrategic business and operational risks. Thisprocess is regularly reviewed by the Board inaccordance with the Turnbull guidance oninternal controls.

ORDINARY DIVIDENDS

An interim dividend of 9.35p per ordinary sharewas paid on 29 September 2006 (2005: 8.90p)and the directors are recommending a finaldividend of 19.88p per ordinary share (2005:18.93p), a total for the year of 29.23p (2005:27.83p). Subject to shareholders’ approval, thefinal dividend will be paid on 30 March 2007 toshareholders on the register on 16 March 2007.

PERSONAL EQUITY PLANS/ISAs

The Company has conducted its investment policy so

as to remain a qualifying investment trust under the

ISA and Personal Equity Plan regulations. It is the

intention of the Board to continue to satisfy these

regulations.

SHARE CAPITAL

There were no ordinary shares allotted during the

year.

DIRECTORS

The directors of the Company during the yearwere as stated below and their interests in theordinary share capital of the Company are asfollows. Each of the directors held officethroughout the year.

31 December 1 January

2006 2006

G J Allen 1,369 1,333

J F de Moller 1,211 –

R W Jewson 3,113 2,645

J Reeve 30,550 28,372

M R Riley 15,000 –

F L J Walton 6,724 6,724

All the above interests are beneficial. None of thedirectors had at any date any interest in either ofthe Company’s debenture stocks.

On 13 February 2007 Mr J Reeve acquired afurther 112 ordinary shares in the Companythrough his regular monthly saving in an ISA. On22 January 2007 Mr R W Jewson and Mrs J F deMoller acquired a further 29 and 58 ordinaryshares respectively in the Company through theirregular monthly savings in the Temple BarInvestment Trust Savings Scheme. No otherchanges in the interests shown above occurredbetween 31 December 2006 and 20 February2007.

No other person was a director during any partof the year.

The directors retiring by rotation and/or incompliance with the provisions of the AIC Codeare Mr J Reeve, Mr F L J Walton and Mr G JAllen. Each of these directors being eligible, theBoard recommends their re-election. In makingthese recommendations the Board has carefullyreviewed the composition of the Board as awhole and borne in mind the need for a properbalance of skills and experience. The Board doesnot believe that length of service per se detractsfrom the independence of a director, particularlyin relation to an investment trust, and on thatbasis considers that the directors standing for re-election are independent. It is confirmed that,following formal evaluation, the performance ofeach director continues to be effective and eachcontinues to demonstrate commitment to the role.

There were no contracts subsisting during or atthe end of the year in which a director of theCompany is or was interested and which are orwere significant in relation to the Company’sbusiness. No director has a service contract withthe Company.

PAYMENT OF SUPPLIERS

The Company’s policy is to obtain the bestpossible terms of payment from suppliers for allforms of business. All terms agreed withsuppliers have been complied with during theyear. There were no trade creditors at the yearend.

SUBSTANTIAL SHAREHOLDERS

As at 20 February 2007 the following companyhad indicated an interest in 3% or more of theissued ordinary shares of the Company.

%

Legal & General Group plc 3.41

MANAGEMENT CONTRACT

The Company has a management agreementwith Investec Investment Management Limited(‘IIM’) for the provision of investmentmanagement, secretarial, accounting andadministrative services to the Company and itssubsidiaries. The agreement is subject to oneyear’s notice of termination by either party.

IIM receives an investment management fee of0.35% per annum, payable quarterly, based onthe value of the investments (including cash) ofthe Company. Investments in funds managed bythe Investec Group are wholly excluded from thischarge. 60% (2005: 60%) of the investment

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 19

20 Temple Bar Investment Trust

Report of the directors continued

management fee payable to IIM is charged by theCompany to capital and the remaining 40%(2005: 40%) to the revenue account on the basisof the expected long term division of returns.

The investment management fee charged for theyear ended 31 December 2006 amounted to£1,960,000 (2005: £1,711,000) excluding valueadded tax.

IIM’s performance under the contract and thecontract terms are reviewed at least annually.This covers, inter alia, the performance of theManager, their management processes,investment style, resources and risk controls. Asnoted in the Chairman’s Statement, the recentperformance of the Company has been good,having outperformed its benchmark index over 5and 10 year periods. In the opinion of thedirectors the continued appointment of theinvestment Manager on the terms set out aboveis in the best interests of shareholders.

DONATIONS

No political or charitable donations were madeduring the year (2005: Nil).

DISCLOSURE OF INFORMATION TOAUDITORS

The directors are not aware of any relevantinformation of which the auditors are unawareand have taken all the steps that they ought tohave taken as directors in order to makethemselves aware of any relevant auditinformation and to establish that the Company’sauditors are aware of that information.

AUDITORS

A resolution to re-appoint Ernst & Young LLP as

auditors to the Company will be proposed at the

Annual General Meeting on 26 March 2007.

RENEWAL OF AUTHORITY TO ALLOTSHARES AND DISAPPLICATION OFPRE-EMPTION RIGHTS

It is proposed that the directors be authorised toallot up to £725,000 of relevant securities in theCompany (equivalent to 2,900,000 ordinaryshares of 25p each, representing 4.97% of itsordinary shares in issue).

When shares are to be allotted for cash, Section89(1) of the Companies Act 1985 requires suchnew shares to be offered first to existingshareholders in proportion to their existingholdings of ordinary shares. However, in certaincircumstances, it is beneficial to allot shares forcash otherwise than pro rata to existingshareholders and the ordinary shareholders canby special resolution waive their pre-emptionrights. Therefore, a special resolution will be

proposed at the Annual General Meeting which, ifpassed, will give the directors the power to allotfor cash equity securities up to an aggregatenominal amount of £725,000 (equivalent to2,900,000 ordinary shares of 25p each or 4.97%of the Company’s existing issued ordinary sharecapital), as if Section 89(1) does not apply.

The directors intend to use this authority to issuenew shares to participants in the Temple BarInvestment Trust Savings Scheme or to otherprospective purchasers whenever they believe itmay be advantageous to shareholders to do so.Any such issues would only be made at pricesgreater than net asset value, as adjusted for themarket value of the Company’s debt, and,therefore, would increase the assets underlyingeach share. The issue proceeds would be availablefor investment in line with the Company’sinvestment policy.

No issues of shares will be made which wouldalter the control of the Company without theprior approval of shareholders in generalmeeting.

The appropriate resolutions are set out in thenotice of meeting on page 45.

DIRECTORS’ AUTHORITY TO PURCHASETHE COMPANY’S OWN SHARES

The directors consider it desirable to give theCompany the opportunity to buy back shares incircumstances where the shares may be boughtfor a price which is below the net asset value pershare of the Company. The purchase of ordinaryshares is intended to reduce the discount atwhich ordinary shares trade in the marketthrough the Company becoming a new source ofdemand for ordinary shares. The rules of the UKListing Authority provide that the maximum pricewhich can be paid by the Company is 5% abovethe average of the market value of the ordinaryshares for the five business days before thepurchase is made.

The Company is not intending to make suchpurchases at present and will only exercise thepower after careful consideration and incircumstances where, in the light of prevailingmarket conditions, it is satisfied that it is in theinterests of the Company to do so. It is expectedthat any shares bought back pursuant to thisauthority will be cancelled rather than being heldin Treasury. The appropriate resolution is set outin the notice of meeting on page 45.

By order of the Board of DirectorsM K SladeFor Investec Investment Management LimitedSecretary20 February 2007

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 20

Temple Bar Investment Trust 21

Report on directors’ remuneration

This report is submitted in accordance with theDirectors’ Remuneration Report Regulations2002 in respect of the year ended 31 December2006. An ordinary resolution will be proposed atthe Annual General Meeting to approve thisreport, but the directors’ remuneration is notconditional upon the resolution being passed.

The Company does not have any executivedirectors and, as permitted under the ListingRules, has not, therefore, established aremuneration committee. Remuneration of non-executive directors is viewed as a decision of theBoard, subject to any shareholder approvalswhich may be necessary. In effect, therefore, theBoard as a whole fulfils the function of aremuneration committee. The Company’s Articlesof Association state that the Board shalldetermine the rate at which directors shall bepaid, provided that the aggregate of all such feesshall not exceed £150,000 per annum. This doesnot include any sums paid to directors that arenot classed as remuneration, e.g. expensereimbursements. The limit on the aggregateamount of directors’ fees paid is subject to theapproval of shareholders by an ordinaryresolution.

POLICY ON DIRECTORS’ REMUNERATION

The level of directors’ fees is determined withreference to a review of the remuneration paid tothe directors of a range of other investmenttrusts, comparable in terms of both size andinvestment characteristics. The Manager of theCompany compiles such analysis as part of themanagement and secretarial services provided tothe Company. No other external advice is takenin considering such fees. It is expected that thelevel of directors’ fees will continue to beassessed on this basis in forthcoming years.

Following the most recent review the Boardconcluded that the remuneration be increased to£25,750 p.a. for the Chairman and £17,500 p.a.for the other directors with effect from 1 January2007 to reflect the level of work andresponsibility involved. In addition, the Chairmanof the Audit Committee, currently Mr Allen, willreceive an annual remuneration of £19,500.

PERFORMANCE GRAPH

The directors consider that the most appropriatemeasure of the Company’s performance is itsshare price total return compared with the totalreturn on the FTSE All-Share Index. A graphillustrating this relative performance over a fiveyear period is shown below.

DIRECTORS’ EMOLUMENTS

The fee level for directors is shown below. Thereis no performance related fee. There is a formalletter of appointment for each director.

Directors are initially appointed until thefollowing Annual General Meeting when, underthe Company’s Articles of Association, it isrequired that they are offered for re-election byshareholders. Thereafter, a director’s continuingappointment is subject to re-election byshareholders on retirement by rotation or inaccordance with the AIC Code.

Audited

2006 2005

Director £ £

John Reeve 25,000 21,000

Gary Allen 19,000 14,000

June de Moller 17,000 8,500

John Hudson N/A 3,500

Richard Jewson 17,000 14,000

Martin Riley 17,000 14,000

Field Walton 17,000 14,000

Mr Walton’s remuneration is paid to FieldCorporate Services.

The fees disclosed above exclude employersnational insurance contributions and VAT whereapplicable.

No director received any pension contributions(2005: Nil).

By order of the Board of Directors

M K Slade

For Investec Investment Management Limited

Secretary

20 February 2007

Share Price Total Return

2002 2003 2004 2005 2006TEMPLE BAR - TOTAL RETURNFTSE ALL SHARE - TOTAL RETURN Source: DATASTREAM

60

80

100

120

140

160

180

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 21

22 Temple Bar Investment Trust

Corporate governance

APPLICATION OF AIC CODE PRINCIPLES

The Board attaches great importance to ensuring

that the Company operates to high ethical and

compliance standards. In addition, the Board

seeks to observe the principles set out in the AIC

Code of Corporate Governance, established

specifically for investment trust companies and

endorsed by the Financial Reporting Council in

February 2006. By following the Code, the

Company continues to meet its obligations in

relation to the FRC’s Combined Code on

Corporate Governance.

The Code provides a guide to best practice in

certain areas of governance where the specific

characteristics of investment trusts suggest that

alternative approaches to those set out in the

Combined Code may be preferable.

COMPLIANCE WITH THE PRINCIPLES OF THEAIC CODE OF CORPORATE GOVERNANCE

Operation of the Board

Each of the directors is independent of anyassociation with the management companywhich might interfere with the exercise ofindependent judgement. There is a formalschedule of matters to be specifically approvedby the Board and individual directors may seekindependent advice at the expense of theCompany within certain limits. The Board hasdelegated the investment management, withinclearly defined parameters and dealing limits,and the administration of the business toInvestec Investment Management Limited (‘IIM’).The Board makes all strategic decisions, reviewsthe performance of the Company at Boardmeetings and sets the objectives for theManagers. The directors have a range of businessand financial skills or experience relevant to thedirection of the Company. Mr G J Allen is theSenior Independent Director.

The Company Secretary is responsible to theBoard, inter alia, for ensuring that Boardprocedures are followed and for compliance withapplicable rules and regulations including the AICCode. Appointment or removal of the nominatedrepresentative of the Corporate CompanySecretary (‘the Company Secretary’) is a matterfor the Board as a whole.

The content and presentation of Board paperscirculated before each meeting contain sufficientinformation on the financial condition of theCompany. Key representatives of IIM attend eachBoard meeting enabling directors to probe on

matters of concern or seek clarification oncertain issues.

There were seven Board meetings, two auditcommittee meetings and two nominationcommittee meetings held during the year and theattendance by the directors was as follows:

Number of meetings attended

Audit Nomination

Board Committee Committee

John Reeve 7 2 2

Gary Allen 5 2 –

June de Moller 7 2 2

Richard Jewson 5 1 2

Martin Riley 7 2 2

Field Walton 7 2 2

Independence of the Directors

Each of the directors is independent of anyassociation with the management company andhas no other relationships or circumstanceswhich might be perceived to interfere with theexercise of independent judgement. Two of thesix directors (Mr Reeve and Mr Walton) haveserved on the Board for more than nine yearsfrom the date of their first election, but given thenature of the Company as an investment trustand the strongly independent mindset of theindividuals involved, the Board is firmly of theview that all of the directors can be consideredto be independent. In arriving at this conclusionthe Board makes a clear distinction between theactivities of an investment trust and aconventional trading company. An investmenttrust has no employees or executive directors,the only significant relationship being with themanagement company. In overseeing thisrelationship it is the view of the Board that longservice aids the understanding, judgement,objectivity and independence of the directorsand in no way detracts from any of thesequalities.

Re-election of directors

Directors are subject to re-election byshareholders at the first AGM following theirappointment and, thereafter, are subject toretirement by rotation at intervals of no morethan three years. In addition, the appointment ofeach director is reviewed by other members ofthe Board every year. Directors are not,therefore, subject to automatic reappointment.Non-executive directors are not appointed for

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 22

Temple Bar Investment Trust 23

specified terms. Because of the nature of aninvestment trust the Board believes that thecontribution and independence of a director isnot diminished by long service and, conversely,that a more detailed knowledge of the Companyand its business has a beneficial impact.

The directors due to stand for re-election at theforthcoming AGM are Mr Allen, Mr Reeve andMr Walton. The Board has carefully consideredthe position of each of these directors andbelieves it would be appropriate for them to beproposed for re-election. Each of the directorscontinues to be effective and to display anundiminished enthusiasm and commitment to therole.

Chairman

The Chairman has no relationships that maycreate a conflict of interest between his interestand those of shareholders. He has never been anemployee or an adviser to the Manager nor doeshe serve on the boards of other investmenttrusts managed by the same Manager.

He is also non-executive chairman of one otherquoted company and a director of a number ofother companies. He does not have a full timeexecutive role in any organisation and the Boardis satisfied that he has sufficient time availableto discharge fully his responsibility as Chairmanof the Company.

Audit Committee

The audit committee is a formally constitutedcommittee of the Board with defined terms ofreference which are available for inspection atthe AGM and can be inspected at the RegisteredOffice of the Company. It normally meets twiceyearly and among its specific responsibilities area review of the audit plan for the year, the reviewof the Company’s annual and half yearly results,together with associated documentation, and thereview of the internal and financial controlsapplicable to the management company. All ofthe directors are members of the auditcommittee and the Chairman is Mr Allen. Theauditors, who the Board has identified as beingindependent, are invited to attend the auditcommittee meeting at which the annual accountsare considered and any other meetings that thecommittee deem necessary.

Nomination Committee

A nomination committee has been established tooversee a formal review procedure governing theappointment of new directors and to evaluate the

overall composition of the Board from time totime, taking into account the existing balance ofskills and knowledge.

The committee is also responsible for assessingthe individual performance of directors and formaking recommendations as to whether theyshould remain in office. This committee is chairedby Mr Reeve.

Upon appointment to the Board each directorreceives relevant background information on theCompany together with a summary of the dutiesand responsibilities of directors. When a directoris appointed an induction meeting is arranged bythe Manager covering details about theCompany, its Manager, legal responsibilities,investment processes and investment trustindustry matters. Directors have also taken partin various training specific to non-executivedirectors, including courses and conferences runby the AIC.

Remuneration Committee

As all the directors are fully independent of themanagement company, the board as a wholefulfils the function of a remuneration committee.

Board/Audit Committee/Nomination

Committee/Director ongoing evaluation

On an annual basis the Board formally reviews itsperformance, together with that of the audit andnomination committees and the effectivenessand contribution of the individual directors,including the Chairman, within the context ofservice on those bodies. The review encompassesan assessment of how cohesively these bodieswork as a whole as well as the performance ofthe individuals within them. On the basis of thesereviews the Board has concluded that it has aproper balance of skills and is operatingeffectively.

Relations with Shareholders

Shareholder relations are given high priority byboth the Board and the Manager. The principalmedium by which the Company communicateswith shareholders is through the interim andannual reports. The information containedtherein is supplemented by regular NAVannouncements and by a monthly factsheetavailable on the Company’s website.

The Board largely delegates responsibility forcommunication with shareholders to themanagement company and, through feedback,expects to be able to develop an understanding

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 23

24 Temple Bar Investment Trust

Corporate governance continued

of their views. The current shareholdingconstituency of the Company is such that thereis only one major shareholder. All members ofthe Board are willing to meet with shareholdersat any time for the purpose of discussing mattersin relation to the operation and prospects of theCompany.

The Board welcomes investors to attend the AGMand encourages questions and discussion onissues of concern or areas of uncertainty. Inaddition, special arrangements have beenestablished to allow Temple Bar Savings Schemeinvestors to participate fully at Annual GeneralMeetings. A separate resolution will be proposedat the AGM in respect of each substantiallyseparate issue. Following the formal AGMproceedings the Manager makes a presentationto the meeting outlining the key investmentissues that face the Company.

Accountability, Internal Controls and Audit

The Board pays careful attention to ensuring thatall documents released by the Group and theCompany, including the Annual Report, present afair and accurate assessment of the Group andthe Company’s position and prospects.

After making enquiries, the directors have areasonable expectation that the Group and theCompany has adequate resources to continue inoperational existence for the foreseeable future,including recourse to a £25 million overdraftfacility with HSBC Bank. Accordingly, thedirectors continue to adopt the going concernbasis in preparing the accounts.

The directors are responsible for the Group andthe Company’s system of internal control and forreviewing its effectiveness. In order to facilitatethe control process the Board has requested theManagers to confirm annually that they haveconducted the Group and the Company’s affairsin compliance with the legal and regulatoryobligations which apply to the Group and theCompany and to report on the systems andprocedures within Investec which are applicableto the management of Temple Bar’s affairs. TheBoard meets on seven scheduled occasions ineach year and at each meeting receivessufficient financial and statistical information toenable it to monitor adequately the investmentperformance and status of the business.

The Board has also established a series ofinvestment parameters, which are reviewedannually, designed to limit the risk inherent inmanaging a portfolio of investments. Thesafeguarding of assets is entrusted to an

independent reputable custodian with whom theholdings are regularly reconciled.

The effectiveness of the overall system ofinternal control is reviewed on an annual basis bythe Board. Such a system can provide onlyreasonable and not absolute assurance againstmaterial misstatement or loss. The Boardbelieves that there is a robust framework ofinternal controls in place to meet therequirements of the AIC Code.

The Board receives reports from its advisers oninternal control matters and does not believethat there is scope or necessity for an internalaudit function in addition to that employed bythe Manager. This matter is subject to periodicreview. Based on the foregoing the Group andthe Company has a continuing process foridentifying, evaluating and managing the risks itfaces. This process has been in place for thereporting period and to the date of this reportand is regularly reviewed by the Board inaccordance with the requirements of the‘Internal Control Guidance for Directors on theCombined Code’ (the ‘Turnbull Guidance’) and theCombined Code.

Socially Responsible Investment

The Board believes that its primary duty is to actin the best financial interests of the Companyand its shareholders. While the Board takesaccount of the ethical stance of investeecompanies on matters such as the environmentor society as a whole, the ultimate objective is todeliver superior investment returns forshareholders.

Exercise of Voting Rights

The Managers have been instructed to vote onbehalf of the Company in accordance withrecommendations put forward by the NationalAssociation of Pension Funds (NAPF). Should theManagers wish to vote in a different way to therecommendation of the NAPF this requires thespecific approval of the Board.

Annual report • Final copy:Temple Bar RA 23/2/07 19:21 Page 24

Temple Bar Investment Trust 25

Independent Auditors’ Reportto the members of Temple Bar Investment Trust PLC

We have audited the group and company financialstatements (the ‘financial statements’) of Temple BarInvestment Trust PLC for the year ended 31 December 2006 which comprise the ConsolidatedIncome Statement, the Consolidated and CompanyBalance Sheets, the Consolidated and Company CashFlow Statement, the Consolidated and CompanyStatement of Changes in Shareholders’ Equity and therelated notes 1 to 22. These financial statements havebeen prepared under the accounting policies set outtherein. We have also audited the information in theDirectors’ Remuneration Report that is described ashaving been audited.

This report is made solely to the Company's members,as a body, in accordance with Section 235 of theCompanies Act 1985. Our audit work has beenundertaken so that we might state to the Company'smembers those matters we are required to state tothem in an auditors’ report and for no other purpose.To the fullest extent permitted by law, we do not acceptor assume responsibility to anyone other than theCompany and the Company's members as a body, forour audit work, for this report, or for the opinions wehave formed.

Respective responsibilities of directors and auditorsThe directors’ responsibilities for preparing the AnnualReport, the Directors’ Remuneration Report and thefinancial statements in accordance with applicableUnited Kingdom law and International FinancialReporting Standards (IFRS) as adopted by theEuropean Union are set out in the Statement ofDirectors’ Responsibilities.

Our responsibility is to audit the financial statementsand the part of the Directors’ Remuneration Report tobe audited in accordance with relevant legal andregulatory requirements and International Standardson Auditing (UK and Ireland).

We report to you our opinion as to whether thefinancial statements give a true and fair view andwhether the financial statements and the part of theDirectors’ Remuneration Report to be audited havebeen properly prepared in accordance with theCompanies Act 1985 and, as regards the group financialinformation, Article 4 of the IAS Regulation. We alsoreport to you whether in our opinion the informationgiven in the directors' report is consistent with thefinancial statements.

In addition we report to you if, in our opinion, thecompany has not kept proper accounting records, if wehave not received all the information and explanationswe require for our audit, or if information specified bylaw regarding directors’ remuneration and othertransactions are not disclosed.