telenet gs leveraged finance presentation

TRANSCRIPT

TelenetGoldman Sachs - European Leveraged Finance ConferenceConference

Renaat Berckmoes, Chief Financial Officer

L d S t b 6 2012London - September 6, 2012

Safe Harbor DisclaimerSafe Harbor Disclaimer

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995.

Various statements contained in this document constitute “forward-looking statements” as that term is definedunder the U.S. Private Securities Litigation Reform Act of 1995. Words like “believe,” “anticipate,” “should,”“intend,” “plan,” “will,” “expects,” “estimates,” “projects,” “positioned,” “strategy,” and similar expressionsidentify these forward-looking statements related to our financial and operational outlook, dividend policy andfuture growth prospects, which involve known and unknown risks, uncertainties and other factors that may causeg p p , , your actual results, performance or achievements or industry results to be materially different from thosecontemplated, projected, forecasted, estimated or budgeted whether expressed or implied, by these forward-looking statements. These factors include: potential adverse developments with respect to our liquidity or resultsof operations; potential adverse competitive, economic or regulatory developments; our significant debtpayments and other contractual commitments; our ability to fund and execute our business plan; our ability to

h ff d b d h fl h fgenerate cash sufficient to service our debt; interest rate and currency exchange rate fluctuations; the impact ofnew business opportunities requiring significant up-front investments; our ability to attract and retain customersand increase our overall market penetration; our ability to compete against other communications and contentdistribution businesses; our ability to maintain contracts that are critical to our operations; our ability to respondadequately to technological developments; our ability to develop and maintain back-up for our critical systems;our ability to continue to design networks install facilities obtain and maintain any required governmentalour ability to continue to design networks, install facilities, obtain and maintain any required governmentallicenses or approvals and finance construction and development, in a timely manner at reasonable costs and onsatisfactory terms and conditions; our ability to have an impact upon, or to respond effectively to, new ormodified laws or regulations, pending debt exchange transactions, our ability to make value-accretiveinvestments, and our ability to sustain or increase shareholder distributions in future periods. We assume noobligation to update these forward-looking statements contained herein to reflect actual results, changes ing p g , gassumptions or changes in factors affecting these statements.

Adjusted EBITDA and Free Cash Flow are non-GAAP measures as contemplated by the U.S. Securities andExchange Commission’s Regulation G. For related definitions and reconciliations, see the Investor Relationssection of the Liberty Global Inc website (http://www lgi com) Liberty Global Inc is our controlling

2

section of the Liberty Global, Inc. website (http://www.lgi.com). Liberty Global, Inc. is our controllingshareholder.

AgendaAgenda

Who we are1

Change to capital structure and shareholder 2 Change to capital structure and shareholder remuneration policy

2

Future growth drivers3

3

A cable company with a strong gtrack record...

F ll d d bi di ti l 600 MH t k Fully upgraded, bi-directional 600 MHz network Continuous stable level of investments Active node splitting to create next-gen network

Powerful networkPowerful network 1

EuroDocsis 3.0 powered broadband products Full interactive digital HDTV platform with true VOD Active beyond cable: WiFi and mobile

Product leadership

Product leadership 2

Customer Loyalty closely measured: management reward system based on customer satisfaction levels Leading service levels through efficiency

C ti l l l l f h l ti t

Service is keyService is key 3 Continuously low levels of churn relative to peers

Strong revenue growth and significant runway ahead Sustained focus on efficiency, disciplined cost control

V t j it f it l dit b dSolid financialsSolid financials

A strong brand

4 Vast majority of capital expenditures success-based Prudent, pro-active balance sheet management

Strong, diversified management team

4

4

Balance between long track record and outside experience Great company culture, promote from within

Our peopleOur people 5

...active in one of Europe’s most attractive cable markets...

Triple-play penetrationCable penetration per household

74%69%

(Q2 2012)(2011)

65%60%

52%48%

38%

47%

16%19%

BE UK DE PT NL TNET VMED KDG¹ ZON ZIGGO

(1) Excluding the effect of the TeleColumbus acquisition, as per March, 2012

Strong historical adoption of cable services

Substitution of basic cable TV by digital TV (cable, IPTV t llit DTT) till t d t ti l f

Triple‐play penetration of 38% at June 30, 2012

Significant potential to convert remaining 33% of i l l t t l di lti l l b dl

5

IPTV, satellite, DTT) ‐ still untapped potential for migration to higher ARPU digital TV platform

Legend: BE=Belgium, UK=United Kingdom, DE=Germany, PT=Portugal, NL=The NetherlandsSource: European Commission E-Communications Household Survey, Company data

single‐play customers to leading multiple‐play bundles

... in a region with national gcharacteristics

+ 1/3rd of Brussels

Legacy Telenet NetworkInterkabel Network = acquired Oct 1, 2008

Flanders is a cohesive footprint Our franchise area covers ~2.9 million Flanders is a cohesive footprint

… a focused, regional government

… a regional culture and language

Our franchise area covers 2.9 million households (61% of Belgium)

~2.8 million homes passed with cable = ~98% reach

… a regional media environment

… a strong and growing economy

… superior GDP per capita (23% above

98% reach

~2.2 million unique customers= ~75% cable penetration

In B2B we cover the whole of Belgium

6

p p p (EU average)

In B2B, we cover the whole of Belgium and Luxembourg

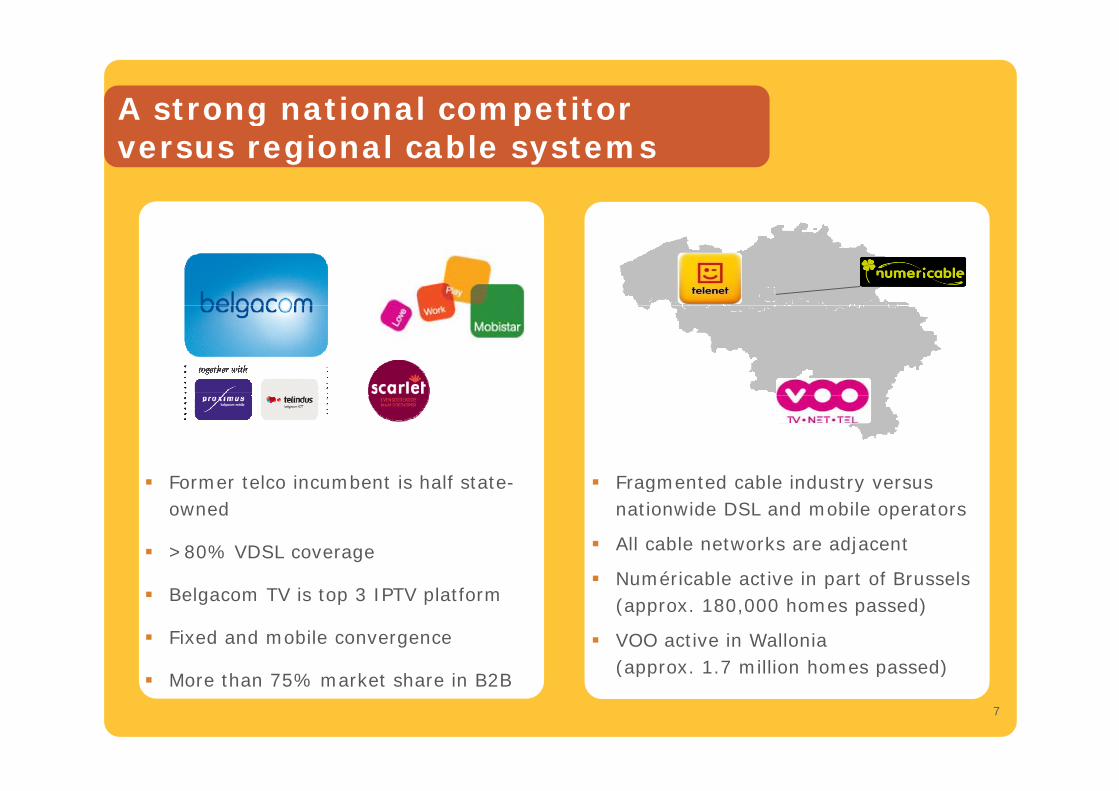

A strong national competitor gversus regional cable systems

Former telco incumbent is half state- Fragmented cable industry versus Former telco incumbent is half stateowned

>80% VDSL coverage

Fragmented cable industry versus nationwide DSL and mobile operators

All cable networks are adjacent

Numéricable active in part of Brussels Belgacom TV is top 3 IPTV platform

Fixed and mobile convergence

Numéricable active in part of Brussels (approx. 180,000 homes passed)

VOO active in Wallonia(approx 1 7 million homes passed)

More than 75% market share in B2B(approx. 1.7 million homes passed)

7

Leading the cable space in terms of g(multi-) product penetration

Digital TVDigital TV FixedTelephony

FixedTelephony

32% penetration

52% penetration

BroadbandInternet

BroadbandInternet Mobile

TelephonyMobile

Telephony47%

Basic Cable TV

Basic Cable TV

75% penetration

penetration

p

Penetration rates relate to total homes passed by the Telenet network 8

But still a challengerBut still a challenger

17%

€4.0 bn €3.8 bn €0.9 bnOthers

KPN/BASE 2%

7%17%KPN/BASE 2%

20%

24%

37%Mobistar

Telenet1% 56%

Belgacom 44%

1%

70%

19%

9

Mobile Fixed data & voice TV

Source: BIPT, 2011 – Market size and market shares are based on service revenues

Cable caters for unparalleled 1 Powerful networkpservice experience 1 Powerful network

Bandwidth shared over all services

Bandwidth shared over all services

Maximum download speed

# Product – April 2012

1 Telenet Fibernet 100

2 Telenet Fibernet 60

Dedicated bandwidth per

Maximum download speed up to 30 Mbps 3 Telenet Fibernet

4 VOO A La Folie

5 Telenet Comfortnetservice

Maximum download speedup to 120 Mbps

6 VOO Passionément

7 EDPnet Newer & Faster

8 Dommel CityConnecty

9 Belgacom Favorite

10 Belgacom Intense

Video and multiple devices will make high broadband speeds relevant

Added value of cable = simultaneous services into the house

10

New devices (tablet PCs) will require ample streaming capacitySource: www.ispmonitor.be

The ISP Monitor Speed Test is an independent source for bandwidth speed comparison. The results shown above are a summary of the test results gathered by the users of the ISP Monitor software.

Deeper fiberization to retain speed 1 Powerful network

leadership position

TODAY

1 Powerful network

Telenet Service Offering

~1,400homes/

node

Optical N d

Fiberloops

Node

2015

CMTSIP Backbone

~500homes/

nodeOptical Nodes

11FiberCoax HFC (Hybrid Fiber Coax Network)

Beyond our network…Beyond our network…

Focus on:

Our products Our service Our brand

12

Enhancing customer value 2 Product leadershipEnhancing customer value

Customer mix H1 2011 ARPU per customer Customer mix H1 2012

(in %) (in %) (in €/month)

2 Product leadership

39%34%

53.5

72.9profile

+61%33%

38%

27%

45.4 12.8

Q2'12 1P 2P 3P

29%

38%

Single-play Dual-play Triple-play

Q2 12 1P 2P 3P

(in 000) (in €/month)

Single-play Dual-play Triple-play

Triple-play subscribers

+9%

(in 000)ARPU per unique customer

+10%

(in €/month)

752819

41.045.1

13H1 2011 H1 2012 H1 2011 H1 2012

Constant innovation 2 Product leadershipConstant innovation 2 Product leadership

InternetInternet Fibernet – up to 120 Mbps

Digital TVDigital TV Sporting, Search & Recommend, GUI

Fixed TelephonyFixed Telephony FreePhone Mobile

MobileMobile Subsidies, Homespots, competitive and MobileMobileinnovative SIM-only rate plans

BusinessBusiness A-Desk14

Telenet internet starts where 2 Internetcompetition ends

Advertized download speeds (Mbps)Internet VDSL2

Up to 25 Mbps

2 Internet

Home Internet 12

Internet ADSLUp to 12 Mbps

€25.00

Up to 25 Mbps€35.00

Basic InternetUp to 30 Mbps

€24.95

Fibernet XLUp to 120 Mbps

€64.95Home Internet 12 Up to 12 Mbps

€40.000 1206030

//15

////// //

Internet BasicUp to 6 Mbps

€25.00I t t R l

FibernetUp to 60 Mbps

€44.95

StartUp to 30 Mbps

€24.95Internet RelaxUp to 16 Mbps

€30.00Home Internet 1

Up to 1 Mbps€25 00

ComfortUp to 30 Mbps

Internet MaxUp to 16 Mbps

€40.00

€25.00

Home Internet 4Up to 4 Mbps

Up to 30 Mbps€34.05

MaxiU t 30 Mb

15(*) Prices mentioned refer to stand-alone residential broadband internet products, in € (including 21% VAT) – temporary promotions have not been reflected – prices mentioned on company websites as per July 26, 2012

Up to 4 Mbps€30.00 Up to 30 Mbps

€44.94

Increased digitalization 2 Digital TVIncreased digitalization

Digitalization rate ARPU per customer Digitalization rate

(in %) (in %) (in €/month)

2 g

46%

Digitalization rate H1 2010 profile

32%

gH1 2012

x2

54%

46%

12 1Analog TV Digital TV

68%

Analog TV Digital TV

12.1

12.1

Analog TV Digital TV

Basic access VASAnalog TV Digital TV

(in 000) Accelerated digitalization fueled by Digital TV subscribers

+17%

g ysuccessful digital TV migration campaign;

116 700 net new subscribers to our

1,2621,473

116,700 net new subscribers to our higher ARPU interactive digital TV platform in H1 2012, of which 71,300 in Q2 2012;

16

H1 2011 H1 2012Q ;

68% of cable TV customers on digital.

Sporting Telenet 2 Digital TVSporting TelenetAddition of top Belgian football resulted in 48% increase in subscribers

2 Digital TV

~183,700subscribers~183,700

subscribers

Belgian football

3 top fixtures per week, exclusive and live in HD

The best sports now

€16.15 if 3-play

€21 55

+48%yoy

5 remaining fixtures on a non-exclusive basis

Top European footballsports nowexclusively

onSportingTelenet

€21.55 if 2-play

€26.95

p p

550 fixtures per season, live

Premier League, German, Italian, Dutch and French national leagues

Telenetif 1-play

NBA Basketball

NFL American Football

Also available onAll prices are retail prices per month and including 21% VAT

17

Golf

Fixed telephony remains a reliable 2 Fixed telephonyp ycheap voice solution

(in 000) i d l h k h (*)

2 Fixed telephony

880920

Fixed telephony subscribers(in 000) Fixed telephony market share(*)

Telenet Competition

455

548

629

741 815

71% 67% 64% 61%

364455

2005 2006 2007 2008 2009 2010 2011 H1 2012

29% 33% 36% 39%

2008 2009 2010 2011

(*) Adjusted for Telenet footprint only.Source: company data, adjusted based on own estimations.

Continued penetration(**) amongst our customer base, reaching 32.2% at the end of Q2 2012;

Net new subscriber growth driven by attractive flat-fee rate plans and multiple-play growth;Net new subscriber growth driven by attractive flat fee rate plans and multiple play growth;

Introduction of FreePhone Mobile in November 2011 is expected to drive incremental RGU growth;

Sustained market share gains despite mature and intensely competitive market;

(**) Penetration as a % of homes passed across the Combined Network. Combined Network includes both Telenet Network and Telenet Partner Network.

Reliability and cheap flat-fee plans remain key advantages over mobile.

18

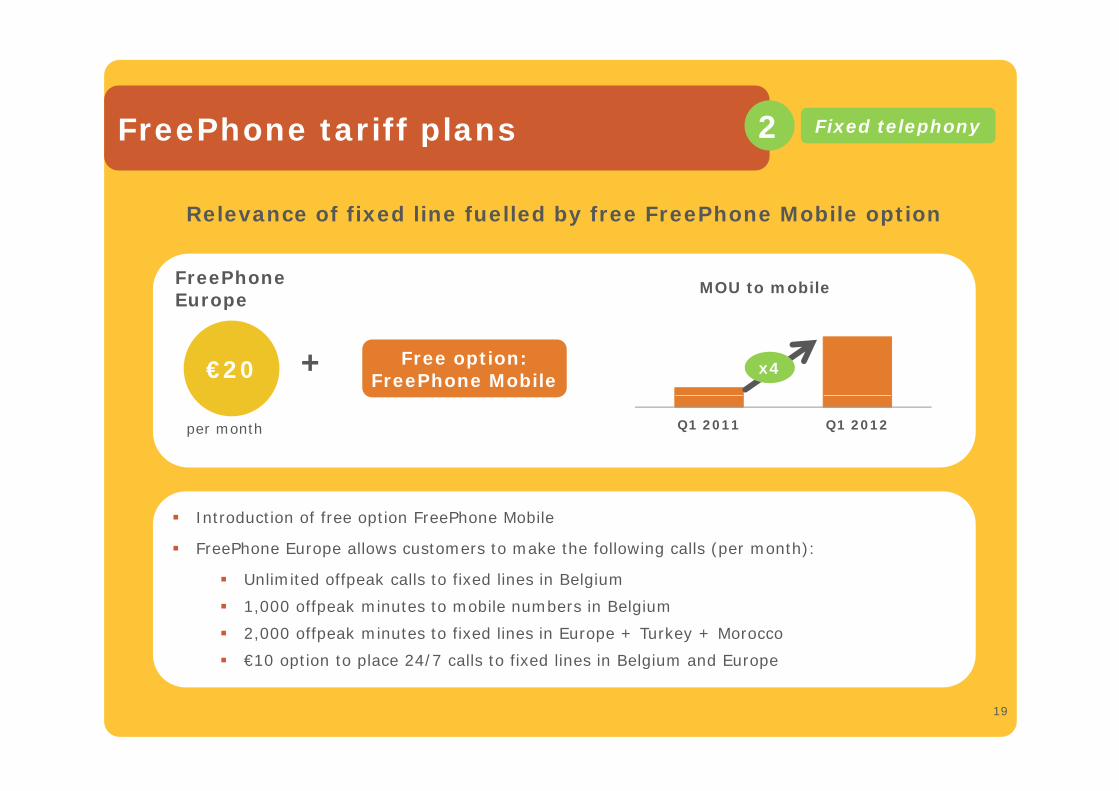

FreePhone tariff plans 2 Fixed telephonyFreePhone tariff plans 2 Fixed telephony

Relevance of fixed line fuelled by free FreePhone Mobile optionRelevance of fixed line fuelled by free FreePhone Mobile option

FreePhoneEurope

MOU to mobile

€20

Europe

+ Free option:FreePhone Mobile

x4

per month Q1 2011 Q1 2012

Introduction of free option FreePhone Mobile

FreePhone Europe allows customers to make the following calls (per month):

U li it d ff k ll t fi d li i B l i Unlimited offpeak calls to fixed lines in Belgium

1,000 offpeak minutes to mobile numbers in Belgium

2,000 offpeak minutes to fixed lines in Europe + Turkey + Morocco

€10 option to place 24/7 calls to fixed lines in Belgium and Europe

19

€10 option to place 24/7 calls to fixed lines in Belgium and Europe

The convergent future: 2 MobilegWiFi + mobile

2 Mobile

+ Telenet MobileTelenet MobileTelenet Hotspots / WiFi homezoneTelenet Hotspots / WiFi homezone

Telenet Hotspots: >1,200 locations (airports, train stations, hotels, highway parkings)

International coverage: >140,000 locations in 95 countries through iPass

Telenet WiFi homezone via home gatewayhome gateway

20

Launch of competitive SIM-only 2 Mobilep yrate plans

Ki KP

2 Mobile

150 minutes

King

2,000 minutes

Kong

€0.15 /min

Pay as you go

10,000 SMS

500 MB

10,000 SMS

1 GB

€0.10 /SMS

€0.10 /MB 500 MB 1 GB€0.10 /MB

€0 €70€20Stand-alone

€50 €15 For Telenetcustomers €0

Simple, transparent

No fixed contract durationNo fixed contract duration

85% of mobile consumers will be able to save money21

Telenet for Business 2 BusinessTelenet for Business 2 Business

Integration of VAS + connectivity and SmallBiz + enterprise segments create foundation for unique service portfolio

Security Solutions Security Consulting Managed ServicesValue Added Services

c-cure

segments create foundation for unique service portfolio

Integrated Hosting Housing Applications

Unified Collaboration Cloud

Carrier OfferConnectivity

hostbasketproduct portfolio

Data Internet Voice Multi-TV

Service Levels: Securitisation & Back-up Options

Fiber Coax Copper Mobile WirelessTransport

Client segment

22

targets

Delivering a superior service 3 Service is keyg

experience to our customers

A unique service experience

3 Service is key

360° Experience A unique service experiencefor our customers

TelevisionInternet

Speed leadershipthrough Fibernet

OTT market

TelevisionInternet

Platform

Richest experience & convergence

Bundles

Maximize ARPU perunique customer

23

Enhance customer loyalty 3 Service is keyEnhance customer loyalty

(in %) Continued low churn levels for all

3 Service is key

10.3%

Annualized churn(in %) Continued low churn levels for all

services compared to peers and other cable operators;

7.1%

7.1%

Q1'10 Q3'10 Q1'11 Q3'11 Q1'12

Reflects Telenet’s continued investments in customer care and focus on customer experience;

Basic cable TV Broadband internetFixed telephony

Management incentive schemes to enhance customer loyalty.

Maximum fixed

New Telecom Act

N fi d t t

Telenet

Maximum fixed contract term limited to six months as of

October 1, 2012

No fixed contract term for all major

services as of October 1, 2012

24

, October 1, 2012

And reward accordingly 3 Service is key

TOP-150

And reward accordingly 3 Service is key

Customer Loyalty

TOP 150

15%

Managerial

Operational

gskills43%

Operational and financial performance

44%

CC

2007-2009 As of 2010

Customer satisfactionCustomer

satisfactionCustomer loyaltyCustomer loyalty

25

Strong stable cash flows and 4 Solid financialssignificant operating leverage 4

% of revenue

Adjusted EBITDA(in €m)(in €m)

Revenue

Solid financials

669

7231,197 1,299 1,376

+9%

j

(*)

608

2009 2010 20112009 2010 2011

+7% CAGR

9% CAGR

2009 2010 20112009 2010 201152.6%51.5%50.7%

Free cash flow(in €m)

Accrued capital expenditures(in €m)

162

254 24231

160

+22% CAGR

Free cash flowAccrued capital expenditures

162

2009 2010 2011

318259

310

2009 2010 2011

+9% yoy

CAGR(**)

(**)

26

00 0 0 022.5%22.0%26.5% 17.6%19.6%13.5%

(*) Including approximately €8.0 million of revenue on certain premium voice and SMS content sevices, which were no longer recognized as of January 01, 2011 following a change in Belgian legislation.

(**) Excluding DTT license in 2010, 4th 3G mobile spectrum license and Belgian football rights in 2011.

(**)(**) (**)

Experienced management team 5 Our peoplep gwith long tenor across the industry

N J i d T l P i i

5 Our people

Name Joined Telenet Position

Duco Sickinghe 2001 Chief Executive Officer and Managing Director

Jan Vorstermans 2003 Chief Operating Officer

Patrick Vincent 2004 Chief Commercial Officer

Renaat Berckmoes 2001 Chief Financial Officer

Luc Machtelinckx 1999 Executive Vice President and General Counsel

Claudia Poels 2008 Senior Vice President Human Resources

Inge Smidts 2009 Senior Vice President Residential Marketing

Herbert Vanhove 2010 Senior Vice President Product Managementg

Martine Tempels 2009 Senior Vice President Telenet for Business

Ann Caluwaerts 2011 Senior Vice President Public Affairs & Media Management

Senior Vice President Strategy Investor Relations and CorporateVincent Bruyneel 2004

Senior Vice President Strategy, Investor Relations and Corporate Communications

Promoting an environment that supports a dynamic and innovative culture

27

Regulation: Timeline of wholesale

N lEuropean

of cable services

Not to scale (DD/MM/YY)

max 3

European Commission

notification RO and retail‐minus

Contract negotiationsContract

negotiations

max 3 weeks9 months (**)

Approval ofreference offer

6 months

Implementation

6 months

Preparation & submission draftreference offer

6/2013

negotiationsnegotiationsreference offer

4/9/201231/1/20121/08/2011 1/09/2011 1/5/2013 21/4/20131/11/2012

reference offer

Court of Appeal :introduction of

Launch date

Annual review by VRM

Possible suspension(*)

introduction of suspension and annulment

Possible annulment at the earliest

(*) In case suspension would not be granted to Telenet, Telenet could incur additional accrued expenditures related to preparatory IT investments for wholesale.

(**) Due to the delayed decision on the suspension, which was initially expected by April 26, 2012, the envisioned 4 month period for approval of the reference offer will be extended which subsequently affects the start of the 6 months implementation timing. 28

AgendaAgenda

Who we are1

Change to capital structure and shareholder 2 Change to capital structure and shareholder remuneration policy

2

Future growth drivers3

29

Policy changes to enhance returns to shareholders

Target range of 3 5 4 5x Net Total Debt to EBITDA(*) Target range of 3.5-4.5x Net Total Debt to EBITDA( )

maintained Objective to move to around 4.5x from c.3.5x

Higher net leverage supported by:

Net leverage to higher end of target range

1Higher net leverage supported by:

Strong cash flow generation

Stable business profile

Solid future growthSolid future growth

No significant acquisitions in the foreseeable future

Underpins future growth potentialFuture shareholder remuneration

mainly via share repurchases

2

Underpins future growth potential

Tax neutral for shareholders if in form of program (if in form of self-tender, for Belgian retail shareholders and other investors that cannot benefit from exemption or reduction, rate of the Belgian withholding tax is 21%)

Enhances flexibility for shareholder distributionsand increases FCF per share potential

Inc ease of o ne ship pe centage fo emaining

30

Increase of ownership percentage for remaining shareholders as repurchased shares will be cancelled

(*) Net leverage ratio is calculated as per the Senior Credit Facility definition, using net total debt, excluding subordinated shareholder loans, capitalized elements of indebtedness under the clientele and annuity fees and any other finance leases, divided by last two quarters’ annualized EBITDA.

Immediate actionsImmediate actions

O t i ti ti t i dditi l d bt fi i Opportunistic time to raise additional debt financing

Further improvement of long-term capital structure

Proceeds of any additional debt are intended to be used to fund a share buy-back

Incurrence of additional debt1

to fund a share buy-back

Telenet is targeting a Net Total Debt to EBITDA ratio of around 4.5x (*)

(*) Net leverage ratio is calculated as per Senior Credit Facility definition, using net total debt, excluding subordinated shareholder loans capitalized elements of indebtedness under the clientele excluding subordinated shareholder loans, capitalized elements of indebtedness under the clientele and annuity fees and any other finance leases, divided by last two quarters’ annualized EBITDA

Share buy-back of Voluntary conditional tender offer

Share buy back of €656.4 million via self-tender offer

2 20,673,043 shares or up to 18.2% of the share capital(**)

Offer price of €35.0 per share (***)

Majority shareholder LGI will not tender its shares Majority shareholder LGI will not tender its shares

Current €50.0 million Share Repurchase Program 2012, of which 91% has been executed, has been terminated

31

(**) Total number of shares issued by the Company including own shares currently held by the Company. These treasury shares represent 0.76% of the total number of shares.

(***) To be adjusted downwards by the gross amount of any distributions prior to the closing of the tender offer (including the €3.25 per share to be paid on August 31, 2012 pursuant to the capital decrease approved by the extraordinary shareholders’ meeting on April 25, 2012).

Details about share repurchase plan via self-tender offer

Share buy-back enhances flexibility for shareholder distributions and increases FCF per share potential

However, shareholders with focus on cash only returns can opt for voluntary tender offer

Purpose

for voluntary tender offer

Self-tender in accordance with the Belgian tender offer rules for a Form

Self tender in accordance with the Belgian tender offer rules for a maximum of 20,673,043 shares, or 18.2% of the share capital of TGH NV (*), at a price of €35.0 per share (to be adjusted downwards by the gross amount of any distributions prior to the closing of the tender offer, including the €3.25 per share capital return to be paid on August 31, 2012)

LGI, Telenet’s majority shareholder, would not tender any shares in the tender offer, but reserves its position concerning tendering in possible future repurchase programs. (**)

Each shareholder would be able to tender approximately Each shareholder would be able to tender approximately 37% of the shares it owns and tender additional shares by way of a pro ration mechanism (to the extent the tender offer is under-subscribed)

32(*) Total number of shares issued by the Company including own shares currently held by the Company. These treasury shares represent 0.76% of the

total number of shares. (**) If the maximum number of shares is tendered and subsequently cancelled, LGI’s shareholding in Telenet would increase from 50.04% to 61.18%

of the share capital of Telenet and to 61.75% if treasury shares are not counted.

Leverage to higher end of range while i t i i t d l itmaintaining strong deleverage capacity

Leverage ratio (1)Pro Forma Net Total Debt/EBITDA (*) Pro Forma deleverage capacity (**)

4

5

66.25x 6.0x

Leverage threshold 3.5-4.5x 4

5

6

CONCEPTUAL

0

1

2

3

Q1 09 Q3 09 Q1 10 Q3 10 Q1 11 Q3 11 Q1 12 Q3 120

1

2

3

2012 2013 2014 2015

-1.0x-1.5x

Q1 09 Q3 09 Q1 10 Q3 10 Q1 11 Q3 11 Q1 12 Q3 12

Senior Credit Facility EBITDA Covenant

Pro-forma2012 2013 2014 2015

Net Debt / L2QA EBITDA

Leverage ratio to increase to around 4.4x (pro-forma Q3’12) from 3.1x (Q2’12)

Reflects planned €3.25 per share capital reduction (€369.2 million in aggregate) and proposed €656.4 million share buy-back

Telenet maintains strong autonomous deleverage capacity Assuming all Free Cash Flow would be used for debt repayments, leverage would

decrease by ~1.0x by 2014 and by ~1.5x by 2015

33

(*) Calculated as per Senior Credit Facility definition, using net total debt, excluding subordinated shareholder loans, capitalized elements of indebtedness under the clientele and annuity fees and any other finance leases, divided by last two quarters’ annualized EBITDA.

(**) Conceptual, assuming that all FCF will be used to repay existing debt instruments. FCF based on Bloomberg consensus estimates as of Aug 7, 2012 that do not reflect management projections and are included for informational purposes. The Company takes no responsibility for the accuracy of such data.

Balanced debt profile remains unchangedBalanced debt profile remains unchanged

(in €m)Debt profile (committed)

(in €m)Pro-forma debt profile

(estimated amounts and maturities post transaction)

500

400799

500

400799

450500

100300

431175

158

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

TL M TL N TL O TL P TL Q TL R TL T Revolver

500

100300

431175

158 450250

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

TL M TL N TL O TL P TL Q TL R TL T Revolver New issuanceTL M TL N TL O TL P TL Q TL R TL T Revolver

New issuance of €700 million equivalent, of which €450 million 10Yr

Average maturity of ~7 years

No debt repayments before 2016 equivalent, of which €450 million 10Yr Senior Secured Notes at 6.25% and €250 million 12Yr Senior Secured Notes at 6.75%

Further extends average maturity

No debt repayments before 2016

34

Further extends average maturity

Enhanced shareholder return for 2012Enhanced shareholder return for 2012

Initial shareholder return 2012

€1 00 per share

Amended shareholder return 2012

€1 00 per shareRegular dividend

€1.00 per share

(paid May 10)

€1.00 per share

(paid May 10)

Capital reduction€3.25 per share

(to be paid Aug 31)

€3.25 per share

(paid on Aug 31)

Share buy back €50.0m in total €702.1m in total (*)

35

(*) Of which €45.7m under the Share Repurchase Program 2012 as announced on Feb 16, 2012 and terminated on August 11, 2012.

AgendaAgenda

Who we are1

Change to capital structure and shareholder 2 Change to capital structure and shareholder remuneration policy

2

Future growth drivers3

36

FY 2012 outlook reconfirmedFY 2012 outlook reconfirmedFY 2012 will be at least at top end of outlook

Revenue growth Top line and Adjusted EBITDA growth will

be higher in H1 relative to H2 2012; We will no longer benefit from favorable

5% – 6%

(~€1,445m – €1,459m)

Adjusted EBITDA growth

gimpact from price increases and launch of Sporting Telenet both happened in Q3 2011;

Strong continued underlying growth in H2 fueled by digital TV broadband and

( , , )

5% – 6%growth

Accrued

fueled by digital TV, broadband and mobile.

~76% success-based; Higher spending on set-top boxes and

(~€760m – €767m)

22% – 23%Accrued Capital Expenditures (1)

Higher spending on set top boxes and customer installations, in line with expected RGU growth, and Pulsar.

Solid and sustainable Free Cash Flow

(~€318m – €335m)

Free Cash Flow (2)

Solid and sustainable Free Cash Flowgeneration despite higher cash paymentsfor Belgian football rights and higher cash interest expenses,.

Stable

(1) Represents accrued capital expenditures. Accrued capital expenditures are defined as additions to property, equipment and intangible assets, including additions from capital leases and other financing arrangements, as reported in the Company’s statement of financial position on an accrued basis.

(2) Free Cash Flow is defined as net cash provided by the operating activities of Telenet’s continuing operations less (i) purchases of property and equipment and purchases of intangibles of its continuing operations, (ii) principal payments on vendor financing obligations, and (iii) principal payments on capital leases (exclusive of network-related leases), each as reported in the Company’s consolidated statement of cash flows. Free Cash Flow is an additional measure used by management to demonstrate the Company’s ability to service debt and fund new investment opportunities and should not replace the measures in accordance with EU GAAP as an indicator of the Company’s performance, but rather should be used in conjunction with the most directly comparable EU GAAP measure.

37

Future growth drivers

1 2Broadband penetration TV subscribers

Future growth drivers

Inter-Inter- Digital Digital 95%

Flanders

+19% 32%

TV subscribers

netnet TVTV80%

2011 2015 (Est)

68%

43

2011 2015 (Est)Digital Analog

Mobile SIMs per Business growth

B2BB2BM bilM bil

13%

Mobile SIMs per cable customer

Business growthopportunities

Legacy business SmallBizzB2BB2BMobileMobile

87%

Telenet Mobile Other mobile provider

HostingSecurity

Cloud Video services

Bizz

MLE

Telenet Mobile Other mobile provider

38

Strong fundamentals to deliver long-term h h ld l

Convert 62% of 1P and 2P Continued investments in

shareholder value

1 2customers to triple play

Repositioning in mobile and quadplay enhancing ARPU

Broadband market growth

Continued investments in fixed network (Pulsar node splitting project)

Maintain leadership position on broadband speed and Future

thFuture

th

Invest and maintain

Invest and maintain Broadband market growth

from c.80% now to c.95% by 2015

Convert 32% remaining analog TV base to digital

interactive digital TV platform

Strong focus on customer excellence and loyalty

growthgrowth leadership position

leadership position

Significant availability of Balanced revenue mix 43

Significant availability of cash at 4.5x leverage

Enhanced flexibility for long-term shareholder distributions

Balanced revenue mix underlines defensive characteristics

Solid EBITDA margins and Free Cash Flow generation

Strong share-Strong share-Sound

fi i l Sound

fi i l Stable leverage target of

~4.5x projects attractive and recurring shareholder distributions

Free Cash Flow generation

No debt maturities before 2016, average maturity around 7 years

Interest risks fully hedged

holder potential

holder potential

financial profile

financial profile

Interest risks fully hedged

39

And long-term strategy

L d hi

And long term strategy

Network Leading cable network

Fiber closer to the homes

Leadership

ff

Service Layer Aggregate services

All-IP

Differentiate

E ll

Customer Competitive, simple and rational

Top leadership commitment for

Excellence

40

ThankThankyouyou.

TelenetLiersesteenweg 42800 Mechelen Belgium

Vincent BruyneelSenior Vice President Strategy, Investor Relations and Corporate Communications

Rob GoyensDirector Investor Relationsand Strategic Planning2800 Mechelen, Belgium

investors.telenet.be

Relations and Corporate Communications + 32 (0)15 33 56 [email protected]

and Strategic Planning+ 32 (0)15 33 30 [email protected]