telefonicas profile

TRANSCRIPT

Telefónica’s Profile

Telefónica S.A.April 2014

DISCOVER, DISRUPT, DELIVER2

Telefónica is the result of more than 85 years of anticipation and transformation...

1990 - 1994 1995 - 19991924 - 1964 1965 - 1989

• CTNE is set up in Madrid; ITT is one of its initial shareholders (1924)

• The Spanish government takes 79.6% of CTNE shares (1945)

• Installs the phone 1 million (1953)

• CTNE becomes the #1 Spanish enterprise (1960)

Start of satellite communications (1967)

Begins operations of the 1st European Data Transmission Special Network (1971)

Installs the phone number 10 million (1978)

Lists on New York Stock Exchange (1987)

Enters in Chile (CTC) and in Argentina (TASA) (1990)

Launches MoviLine in Spain (1990), the analogue mobile service, reaching a geographic coverage of 98% in three years.

Enters in Peru (TdP) (1994)

Launches digital mobile telephony: Movistar (1994)

Commercial Internet is being born. Telefónica launches Infovía (1995)

Wins the tender for Telespin Brazil (1998)

Telefónica becomes fully public again (1999)

Launches fixed broadband access service ADSL (1999)

DISCOVER, DISRUPT, DELIVER3

...especially during the last decade

2009 - 2011 2012 - 20142000 - 2005 2006 - 2008

• Veronica Operation: Telefónica de Argentina; Telefónica del Perú; Telespand Tele Sudeste in Brazil (2000)

• Joint venture of Telefónicaand Portugal Telecom in Brazil: Vivo (2003)

• Launches Imagenio (2003)

• Acquisition of BellSouth's assets in Latin America (2004)

Acquisition of CeskyTelecom (2005)

Takes a 5% stake in China Netcom (2005)

Acquisition of the O2 assets in the UK, Germany and Ireland (2006)

Mobile license awarded in Slovakia (2006)

51% stake taken in Colombia Telecom (2006)

Industrial alliance with Telecom Italia (10.47% of the voting rights) (2007)

Acquisition of Telemig by Vivo in Brazil (2008)

Reaches a 5.38% participation in China Unicom after the CU-CNC merger (2008)

Strengthening of the strategic alliance with China Unicom (2009)

Acquisition of Hansenet in Germany, Jajah in Israeland Tuenti in Spain (2010)

Control of Vivo obtained by buying PT stake out of Brasilcel (2010)

Mobile license awarded in Costa Rica (2011)

T.Digital and TGR creation (2011)

Sale of 4.56% stake in China Unicom (2012)

IPO Telefónica Deutschland (2012)

Sale of Atento (2012)

Sale of 40% of Telefónica’sstake in Centroamérica(2013)

Sale of Telefónica Ireland (2013)*

Acquisition of E-Plus in Germany (2013)*

Capital increase in Telco (from 46,18% to 66%) (2013)

Sale of Telefónica Czech Republic (2014)**

New totally customer-centred organization

* The operations are subject to obtaining the relevant regulatory approval.** Telefónica holds a 4.9% stake in Telefónica Czech Republic.

DISCOVER, DISRUPT, DELIVER4

Since the beginning of internationalization, the company has experienced a significant growth

1989 2000 2013 1989 - 2013

Customers (Mn) 12 68 323 x27

Countries * 1 16 24 +23

Team (‘000) 71 149 130 x2

Revenues (Mn €) 4,273 28,482 57,061 x13

* Includes Ireland, Czech Republic and Slovakia. At the end of 2013, the sale of operations in these countries were pending regulatory approval.

DISCOVER, DISRUPT, DELIVER5

Telefónica is a reference in the Latin American Telco market...

Accesses December 2013 (Mn)

Brazil: 92.7

Argentina: 26.7

Mexico: 21.9

Peru: 20.9

Colombia: 14.8

Chile: 13.6

Central America: 11.8

Venezuela: 11.7

Ecuador: 5.2

Uruguay: 1.8

Total Accesses 222 Mn

Leading Contract

penetration*: 25%

Leading Smartphones

penetration*: 22%

Notes: Central America includes Guatemala, Panama, El Salvador, Nicaragua and Costa Rica. Total accesses figure includes Narrowband Internet accesses of Terra Brazil and Terra Colombia, and Broadband Internet accesses of Terra Brazil, Telefónica de Argentina, Terra Guatemala and Terra Mexico.* Penetration over mobile accesses.

DISCOVER, DISRUPT, DELIVER6

...and has a relevant scale in Europe

Total Accesses 102 Mn

Contract

penetration*: 61%

Smartphones

penetration*: 42%

Note: Accesses includes Ireland, Czech Republic and Slovakia. At the end of 2013, the sale of operations in these countries were pending regulatory approval.* Penetration over mobile accesses.

Accesses December 2013 (Mn)

Spain: 41.7

Germany: 25.2

United Kingdom: 23.9

Czech Republic: 7.8

Ireland: 1.6

Slovakia: 1.5

DISCOVER, DISRUPT, DELIVER7

Our scale is reinforced with global partnerships and collaboration agreements

+PARTNERS PROGRAM PARTNERS PROGRAM

~ 13 mn customers ~ 3 mn customers~ 148 mn customers ~ 70 mn customers

Strategic & Industrial Alliances

Stake 5.02%Stake 5.02% Stake 14.96%Stake 14.96%

million combinedcustomers *>1,000

* Telecom Italia doesn't include Brazil.

DISCOVER, DISRUPT, DELIVER8

Telefónica enjoys today a unique portfolio in the industry...

OIBDA by RegionRevenues by RegionAccesses by Region

Spain

Rest T-Europe

Brazil

Rest T-Latam

T-Latam 68%T-Europe 32% T-Latam 51%T-Europe 47% T-Latam 49%T-Europe 52%

Spain

Rest T-Europe

Brazil

Rest T-Latam

Spain

Rest T-Europe

Brazil

Rest T-Latam

23%

24%21%

30% 33%

19%21%

29%13%

19%

29%

40%

* Organic growth: Assumes constant exchange rates as of 2012 (average Fx in 2012), excludes hyperinflationary accounting in Venezuela and considers constant perimeter of consolidation.** Operating CF = OIBDA - CapEx (excluding spectrum).Note: Differences up to and over 100% are due to “Others & Eliminations”.

2013 (Mn €) % Var. Reported vs 2012

% Var. Organic vs 2012 *

Revenues 57,061 -8.5% +0.7%

OIBDA 19,077 -10.1% 0.0%

OIBDA Margin 33.4% -0.6 p.p. -0.2 p.p.

Operating CF ** 10,905 -11.8% -2.7%

DISCOVER, DISRUPT, DELIVER9

...both by its diversification...

% out of market of origin Accesses Revenues OIBDA

95.5% 85.7% (*) 89.4% (**)

87.1% 77.3% 66.8%

71.7% 64.9% 52.7%

69,9% 51.2% 44.7%

61.6% 62.7% 46.9%

54.9% 30.9% 18.8%

Operational data as of December 2013 and financial data as of January - December 2013.* Data calculated with Service Revenue.** Data as of April – September 2013.

DISCOVER, DISRUPT, DELIVER10

...as well as by customer base and revenues...

Top 10 worldwide...

Total accesses (as reported by companies) = Fixed Lines + Mobile Customers + Narrow and Broad Band Internet + Pay TV.* Vodafone’s Fixed Accesses as of Dec12.

Note: FY 2013 revenues as reported by companies.* Data as of FY 2012.

...by total accesses Million, December 2013)

... by revenues(Million Euros, FY 2013)

767.2

441.5

433.3

428.4

339.3

323.1

287.4

243.8

236.3

228.2

China Mobile

China Telecom

China Unicom

Vodafone *

América Móvil

Telefónica

Bharti-Airtel

Axiata

France Telecom

Vimpelcom

99,979

96,923

90,748

77,173

60,132

57,061

54,525

46,356

41,765

40,981

NTT *

at&t

Verizon

China Mobile

Deutsche Telekom

Telefónica

Vodafone *

América Móvil

NTT DoCoMo *

France Telecom

DISCOVER, DISRUPT, DELIVER11

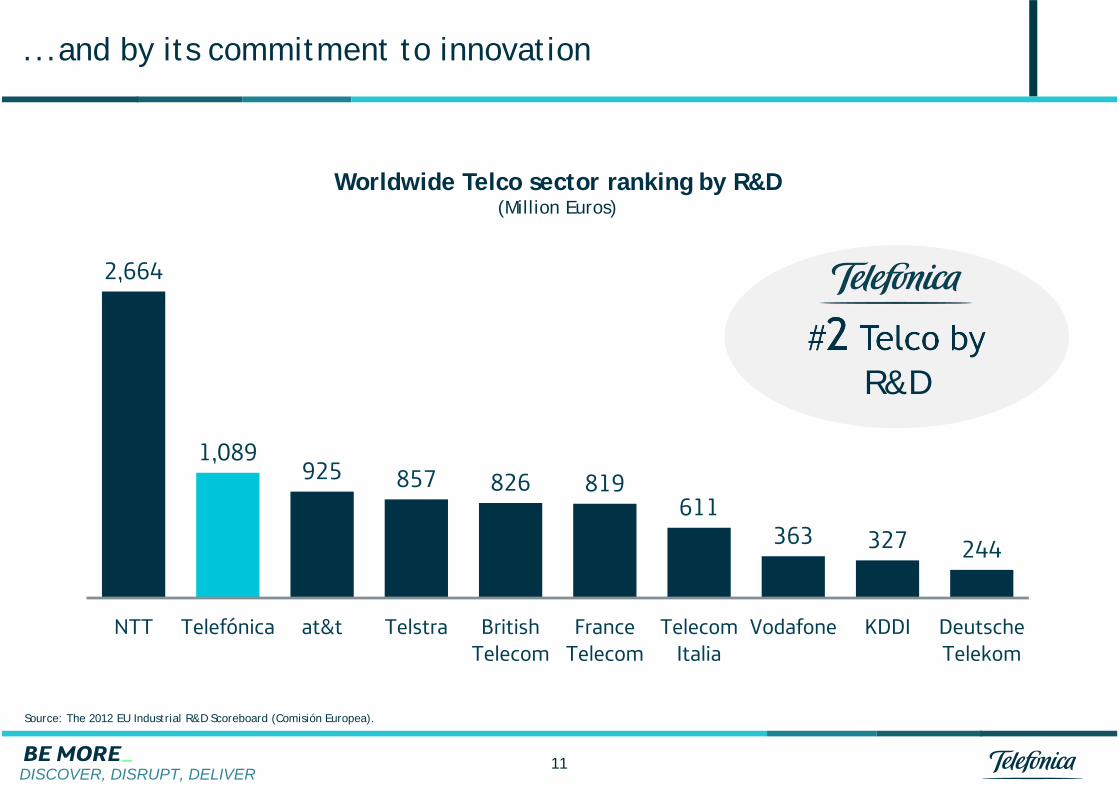

...and by its commitment to innovation

Source: The 2012 EU Industrial R&D Scoreboard (Comisión Europea).

2,664

1,089925 857 826 819

611363 327 244

NTT Telefónica at&t Telstra BritishTelecom

FranceTelecom

TelecomItalia

Vodafone KDDI DeutscheTelekom

Worldwide Telco sector ranking by R&D(Million Euros)

#2 Telco by R&D

DISCOVER, DISRUPT, DELIVER12

Telefónica among the Top 10 in the Telco sector worldwide

Worldwide Telco sector ranking by market cap (Million Euros)

Source: Bloomberg 03/31/2014.

143,040

134,023

132,591

70,551

65,976

52,346

52,269

50,777

50,062

44,996

Verizon

China Mobile

at&t

Vodafone

Softbank

Deutsche Telekom

Telefónica

América Móvil

NTT DoCoMo

NTT

DISCOVER, DISRUPT, DELIVER13

1Telefónica’s activity has a clear positive impact in the societies where

it is present

As an engine for economic sustainable development and innovation...

...and to help overcome social divides

DISCOVER, DISRUPT, DELIVER14

The ICT sector is key to improve productivity and for economic sustainable growth

Increase in GDP growth (pp) per each 10 ppincrease in penetration of Telco services

Broadband development

Direct BenefitsInfrastructure Investment

Consumer surplus

Contribution to GDP growth

Private IncomeTotal Factor Productivity

Household Penetration

Enterprise penetration

Developed countries Developing countries

ICT impact on the economyICT impact on the economy

0,0 0,3 0,6 0,9 1,2 1,5

Fixed-Line Phone

Mobile Phone

Dial-Up Internet

Broadband Internet

0.0 0.3 0.6 0.9 1.2 1.5

Source: World Bank; Qiang.

DISCOVER, DISRUPT, DELIVER

8,2288,928 8,871

8,172

13.5%14.2% 14.2% .14.3%

2010 2011 2012 2013

15

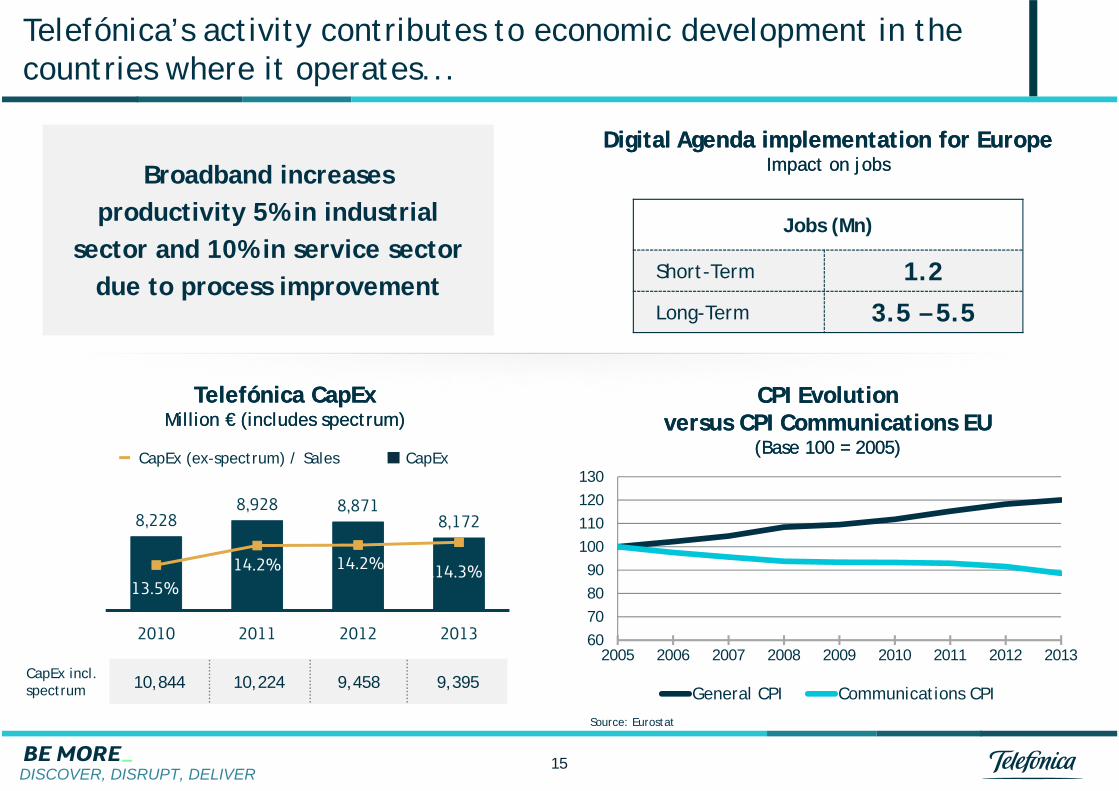

Telefónica’s activity contributes to economic development in the countries where it operates...

Digital Agenda implementation for EuropeImpact on jobs

Digital Agenda implementation for EuropeImpact on jobsBroadband increases

productivity 5% in industrial sector and 10% in service sector

due to process improvement

CPI Evolution versus CPI Communications EU

(Base 100 = 2005)

CPI Evolution versus CPI Communications EU

(Base 100 = 2005)

60708090

100110120130

2005 2006 2007 2008 2009 2010 2011 2012 2013

General CPI Communications CPI

Jobs (Mn)

Short-Term 1.2Long-Term 3.5 – 5.5

Telefónica CapExMillion € (includes spectrum)

Telefónica CapExMillion € (includes spectrum)

CapEx (ex-spectrum) / Sales CapEx

CapEx incl. spectrum 10,844 10,224 9,458 9,395

Source: Eurostat

DISCOVER, DISRUPT, DELIVER

THINK BIG

TALENTUM

CAMPUS PARTY

CROWDWORKING SPACES

WAYRA

AMÉRIGO

MARKET ACCESS

...with a clear commitment with innovation and entrepreneurship

16

INVE

STM

ENT

Crow

dfun

ding

-VA

’s-

VC’s

TALENTSELECTION &

QUALIFICATION

PARTNERSALLIANCES

TALENT EMPLOYMENT INVESTMENT

ACEL

ERAT

ION

Open Platform_

DISCOVER, DISRUPT, DELIVER17

Telefónica also promotes social cohesion through the development of social programs

• 716,641 children at risk of social exclusion have been attended in Latin America to fight against child labor

• 30,332 teachers have been trained

• More than 24,000 volunteers have taken part in solidarity initiatives

• 12,004 young people have been trained to support the development of 3,726 projects

Total beneficiaries of Telefónica Foundation 1,542,898

Education and learningArt and digital cultureCorporate Volunteering

Presence of FundaciónTelefónica in the world

Countries where Fundación Telefónica collaborates

12COUNTRIES

8COUNTRIES

DISCOVER, DISRUPT, DELIVER18

Different organizations have recognized our commitment with corporate sustainability

Telefónica in the top 5 sector

Carbon Disclosure Project: Signed by 551 institutional investors, with assets of US$71 trillion. CDP Global 500 Report examines the carbon reduction activities at the world’s largest public corporations

Included in FTSE4Good Index, an index that measure the performance of companies that meet globally recognized corporate responsibility standards

Member of DJSI World. Best practice in:• Risk & Crisis Management• Impact of Telecommunication services

The most admired Telco in Europe, and the second worldwide, according to the World’s Most Admired Companies Ranking in 2013

DISCOVER, DISRUPT, DELIVER19

Our brands, one of our main assets, are managed globally

Speaks to:• Institutions• Governments• Employees• Multinational Clients,• ...

Institutional Role

Speaks to Customers and Society

Commercial Role

Brand Architecture