telecom aw new - ibef telecom group of pricewaterhousecoopers in india ... and their stakeholders....

TRANSCRIPT

www.ibef.org

TELECOMMUNICATIONS

PricewaterhouseCoopers is one of the largest and most

reputed professional services network in the country.

The Telecom Group of PricewaterhouseCoopers in India

works with telecom service operators, lenders, policy making

authorities, infrastructure vendors, manufacturers and

associated services companies to provide industry focused

solutions. PricewaterhouseCoopers specialists from the tax

and advisory teams connect their thinking, experience and

solutions to build public trust and enhance value for clients

and their stakeholders.

For information, please contact:

Deepak Kapoor, Executive Director

PricewaterhouseCoopers Pvt. Ltd.

PwC Centre, Saidulajab, Opposite D-Block, Saket

Mehrauli Badarpur Road, New Delhi – 110 030

Tel: +91 11 5125 0000

E-mail: [email protected]

TELECOM IN INDIA

High on Opportunity 2

POLICY INITIATIVES 4

MARKET

Size, Players and Trends 8

OPPORTUNITIES 13

CONTACT FOR INFORMATION 16

TELECOMMUNICATIONS

High on Opportunity

India is currently

the fourth largest economy

in terms of Purchasing

Power Parity

India to emerge as

the third largest economy

in the world by 2050

Shift of focus to services

sector with its share

to increase to 60 per cent

of GDP by 2020; fuelled

by India becoming

the chosen destination

for BPO-ITES services

TELECOM IN INDIA

The Indian telecom market has been displaying sustained high

growth rates. Riding on expectations of overall high economic

growth and consequent rising income levels, it offers

an unprecedented opportunity for foreign investment.

A combination of factors is driving growth in the telecom

market, promising rich returns on investments.

Macro-economic impetus

Over the past 10 years, India has registered the fastest growth

among major democracies, having grown at over 7 per cent

in four years during the 1990s. It represents the fourth largest

economy in terms of “Purchasing Power Parity”.

According to a recent Goldman Sachs report, over the next

fifty years, Brazil, Russia, India and China - the BRIC economies

- could become a much larger force in the world economy.

“India could emerge as the world’s third largest economy

and of these four countries; India has the potential to show

the fastest growth over the next 30 to 50 years”. The report

also states that, “Rising incomes may also see these economies

move through the ‘sweet spot’ of growth for different kinds

of products, as local spending patterns change. This could be

an important determinant of demand and pricing patterns

for a range of commodities”.

The share of the services sector as a percentage of total GDP

is also predicted to rise from the current 46 per cent to

about 60 per cent by 2020. The boom in the services sector

is slated to come from India, emerging as a chosen destination

for software and other IT enabled services, tourism etc.

According to a Nasscom- McKinsey & Co. Study, by 2008,

the Indian IT software and services sector will account for

US$ 70-80 billion in revenues; employ 4 million people, and

account for 7 per cent of India’s GDP and 30 per cent

of India’s foreign exchange inflows.

T E L E C O M M U N I C A T I O N S

Demographic impetus

Population projections from the Planning Commission

of India suggest that the share of the working age population

(15-64 years) in total population will grow from the current

59 per cent to about 65 per cent, translating into 882 million

by year 2020.

According to the Vision 2020 document of the Planning

Commission of India, the country will witness continued

urbanisation. The urban population is expected to rise

from 28 per cent to 40 per cent of total population by 2020.

Future growth is likely to be concentrated in and around 60

to 70 large cities having a population of one million or more.

This profile of concentrated urban population will facilitate

customised telecom offerings from operators.

Over the years, spending power has steadily increased in India.

Between 1995 and 2002, nearly 100 million people became

part of the consuming and rich classes. Over the next five

years, 180 million people are expected to move into the

consuming and very rich classes. On an average, 30-40 million

people are joining the middle class every year, representing

huge consumption spending in terms of the demand for

mobile phones, televisions, scooters, cars, credit goods and

a consumption pattern associated with rising incomes.

Working age population

of India set to increase

to 882 million by 2020

India’s urban population

expected to rise

to 40 per cent from

the current 28 per cent

by 2020

30-40 million people joining

the middle class every year

with consumption spendings

associated with rising

incomes

PAGE 3

In 1999, the Government of India authored a very forward

looking National Telecom Policy 1999 (NTP-1999), which

acknowledged that access to telecommunications is of utmost

importance for the achievement of the country’s social

and economic goals. Availability of affordable and effective

communication for the citizens was the core vision and goal

of this telecom policy. Since the announcement of the Policy,

the Government has undertaken various concrete steps to

achieve the policy objectives.

“In our view,

the Government of India has

virtually deregulated every

segment of the Indian

Telecom industry over

the past two years”

- Morgan Stanley,

December 2003

Landmark National

Telecom Policy 1999

followed with concrete

steps to achieve

the stated objectives

POLICY INITIATIVES

The migration from a fixed to a revenue share licence regime

provided the desired relief to the private operators - earlier

burdened by huge debts that they had to service owing

to their licence fee commitments. This was the starting point

of the cellular revolution being witnessed in the country today,

wherein almost 2 million lines are getting added to the

network every month.

Impact of NTP-99 on mobile subscriber uptake

Source: COAI, PwC Analysis

in million

T E L E C O M M U N I C A T I O N S

Liberalisation of the national and international long distance

sector by the Government led to the setting up of private

companies in both service segments, and the consequent

competition that has emerged has led to reduction in tariffs,

which are lower than 80 per cent of the pre-liberalisation

days. The reduced tariffs are now almost at par with

world benchmarks.

Recognising the convergence of markets and technologies,

the Government, in December 2003, came out with the

Unified Access Licence allowing both basic and cellular

service providers to provide access, using any technology

in a specified service area. The Government also announced

the Interconnection Usage Charge (IUC) regime in January

2003, implemented from May 2003, to facilitate cost-oriented

interconnection in the Indian telecom market with multiple

operators - both public and private, with multiple

service offerings.

In tax related announcements made in January 2004,

the Government has further rationalised the customs

duty structure on imports related to telecom and specified

infrastructure equipment for basic/cellular/Internet, V-SAT,

radio paging and public mobile radio trunk services. Parts of

such equipment are being exempted from basic customs duty.

Later in the year, the Government announced reduction in

performance bank guarantees for Internet service providers,

national long distance providers and domestic call centres;

thus, reducing their cost of operations to enable them

to offer more affordable pricing.

In 2004, specified imports

related to telecom

infrastructure were

exempted from basic

customs duty and

performance bank

guarantees for certain

service providers

were reduced

In 2003, the Government

announced two significant

initiatives

Regulatory structure

* TDSAT: Telecom Disputes Settlement Appellate Tribunal

PAGE 5

Foreign Direct Investment (FDI) policy

in the telecom sector

Foreign Direct Investment (FDI) was permitted in the telecom

sector beginning with the telecom manufacturing segment in

1991 - when India embarked on economic liberalisation. FDI

is defined as investment made by non-residents in the equity

capital of a company. For the telecom sector, FDI includes

investment made by Non-Resident Indians (NRIs), Overseas

Corporate Bodies (OCBs), foreign entities, Foreign Institutional

Investors (FIIs), American Depository Receipts (ADRs)/Global

Depository Receipts (GDRs) etc.

Present FDI Policy for the Telecom sector:

• In Basic, Cellular Mobile, National Long Distance,

International Long Distance, Value Added Services and

Global Mobile Personal Communications by Satellite, FDI

is limited to 49 per cent (under automatic route) subject

to grant of licence from the Department of

Telecommunications and adherence by the companies

(who are investing and the companies in which investment

is being made) to the licence conditions for foreign equity

cap and lock-in period for transfer and addition of equity

and other licence provisions.

• Foreign Direct Investment up to 74 per cent permitted,

subject to licensing and security requirements for the

following:

- Internet Service (with gateways)

- Infrastructure Providers (Category II)

- Radio Paging Service

• FDI up to 100 per cent permitted in respect to

the following telecom services:

- ISPs not providing gateways

(both for satellite and submarine cables)

T E L E C O M M U N I C A T I O N S

- Infrastructure Providers providing dark fibre

(IP Category I)

- Electronic Mail

- Voice Mail

The above is subject to the following conditions:

- FDI up to 100 per cent is allowed subject to

the condition that such companies would divest

26 per cent of their equity in favour of Indian public

within 5 years, if these companies are listed

in other parts of the world.

- The above services would be subject to licensing and

security requirements, wherever required.

- Proposals for FDI beyond 49 per cent shall be

considered by Foreign Investment Promotion Board

(FIPB) on a case-to-case basis.

• In the manufacturing sector 100 per cent FDI is permitted

under the automatic route.

PAGE 7

Today, India has the eighth largest telecom network in the

world, which is growing at an overall rate of over 20 per cent.

As of May 2004, India had about 43 million fixed lines and

36 million wireless subscribers contributing to the total

tele-density of about 7 per cent.

MARKET

Size, Players and Trends

India currently has

43 million fixed lines

and 36 million wireless

connections

According to Morgan Stanley, the total revenue from

the Indian telecom market in financial year 2003 was estimated

to be about US$ 9.2 billion. Presently, wireline services

contribute about half of the total service revenues. Over

the next 5-8 years, however, their contribution is expected to

fall to about 30 per cent and wireless services are expected to

contribute half the industry revenue. Data revenue is expected

to increase from 2 per cent to 8 per cent of total revenues.

Tele-density & telephone subscribers in India

Source: Indian Telecommunications Statistics 2002, Ministry of Communications, Government of India

The Indian Telecommunication Industry Performance Indicators 2002-03, TRAI;

Statistics on Cellular Subscriber Numbers from COAI website

Telecom in India : way forward

Estimates for total wireless market in India

*E: Estimates for year ending March; Source: Cellular Operators Association of India

(COAI)

in

mill

ion

T E L E C O M M U N I C A T I O N S

Most of the telecom infrastructure till now has been deployed

in the urban areas, raising urban tele-density to about 18.2

per cent compared to a rural tele-density of about 1.5

per cent. According to the latest Telecommunication Industry

Performance Indicators issued by the Telecom Regulatory

Authority of India (TRAI), the equipped switching capacity

of the fixed network is about 60 million with the ownership

distribution as provided in the diagram above. There also

exists about 0.5 million route kms of optical fibre-based

and 0.15 million of microwave-based transmission network

infrastructure. The ownership pattern of the transmission

network infrastructure is as provided in the diagram, on

the following page.

% Contribution to telecom service revenue, f iscal year 2003

With urban tele-density

at 18.2 and rural tele-density

at less than 2, there is

enormous scope for addition

to telecom infrastructure

Equipped switching capacity

Source: Morgan Stanley estimates

*BSNL: Bharat Sanchar Nigam Limited; MTNL: Mahanagar Telephone Nigam Limited.

Both BSNL & MTNL are government controlled operators.

Source: TRAI Indian Telecom Service Performance Indicators, November 2003

PAGE 9

GSM service providers

No. Name of Total Sub % Market

Company Figures Share

1 Bharti 7,343,763 26.10 Integrated telco, with presence in all sectors - Cellular, Basic, National Long Distance (NLD) & International

Long Distance (ILD). Currently offering only GSM based cellular services. No CDMA based cellular services

being offered.

2 BSNL 5,549,285 19.70 Incumbent operator, virtual monopoly in the basic services. Very strong NLD operator; and, has been able

to quickly ramp up GSM subscribers due to nationwide network reach. Pan country presence in both basic

(except Mumbai and Delhi) and cellular services.

3 HUTCH 5,591,892 19.80 Pure play GSM mobility player offering cellular services in 11 circles. Has been working on a model of being

associated with the high ARPU subscribers.

4 IDEA 3,961,442 14.10 A 3 way GSM mobility joint venture between Tatas, Birlas and AT&T Wireless offering cellular services

in 8 circles. IDEA has recently taken over Escotel that was operating in 3 circles.

5 BPL 2,087,740 7.4 Pure play cellular operator along with Spice, Escotel and Aircel.

6 SPICE 1,270,904 4.5 Pure play GSM based mobility player offering services in 2 circles – Punjab and Karnataka.

7 AIRCEL 1,123,314 4.0 Recently acquired the contiguous metro circle of Chennai, while already operating

in the state circle of Tamil Nadu.

8 RELIANCE 850,831 3.0 Operating GSM wireless services in 6 circles and subsequently acquired Madhya Pradesh circle from RPG.

Reliance is currently focusing on rollout of CDMA based wireless services.

9 MTNL 396,281 1.4 Integrated incumbent operator also offering GSM based mobility in Delhi and Mumbai.

ALL INDIA 28,175,452

Players and Trends

Source: Cellular Operator Association of India, May 2004

The GSM subscriber base in India is expected to reach

about 35 million by the end of 2004. Indian GSM service

providers are presently operating in over 70 networks

covering almost 2000 cities and towns and thousands

of villages, serving over 26 million subscribers.

OFC (in RKms)

M/W Link (in RKms)

GSM in India -

a burgeoning market

Source: TRAI Indian Telecom Service Performance Indicators, November 2003

Source: TRAI Indian Telecom Service Performance Indicators, November 2003

T E L E C O M M U N I C A T I O N S

CDMA mobile has a subscriber base of 7 million in the

country. It is expected that the mobile-fixed crossover

in India will take place in 2004 itself. The global mobile

subscriber base is expected to cross 1.5 billion in 2004

and reach 2.3 billion by 2010, with India expected to

contribute significantly to the above growth.

Fixed service providers

Wireline WLL Tota l

BSNL 34,862,000 800,000 35,662,000

MTNL 4,475,000 130,000 4,605,000

Private Operators 1,113,197 1,109,986 2,223,183

Source: isourceupdates.com (as per media & other sources), March 2004

Trends

The Indian telecom market was liberalised in the 1990s

and the service licences were given on the basis

of services to be offered in specified areas of operation.

The country was demarcated into “circles” - categories

based on their economic potential, and these

demarcations were mostly contiguous with the states

of India. As a result, the Indian telecom market today

is characterised by the existence of various regional

players in the fixed and cellular segments.

With multiplying

opportunities, the number

of regional players

is growing

Tatas 652,735

Reliance 7,010,258

HFCL 34,114

Shyam 27,141

Tota l 7 , 7 2 4 , 2 4 8

Source: isourceupdates.com (as per media & other sources), May 2004

CDMA service providers

PAGE 11

Over the past few years, consolidation has been happening

in the industry, which has created about four large integrated

players who have a presence in all the segments like wireline,

wireless, national and international long distance and data

services. These four players are BSNL (incumbent), Bharti

Televentures, Reliance Infocomm and Tatas. Hutchison, another

significant player with more than five million subscribers, has

restricted itself to the mobile services space. The industry is

expecting to see more consolidation following issuance

of the Unified Access Licence by the Government

in December 2003 and clarity in intra-circle merger

and acquisition norms relating to both spectrum

and dominance issues.

Consolidation is underway

in the industry

T E L E C O M M U N I C A T I O N S

India offers an unprecedented opportunity for telecom service

operators, infrastructure vendors, manufacturers and associated

services companies. A host of factors are contributing to

enlarged opportunities for growth and investment in telecom:

• an expanding Indian economy with increased focus

on the services sector

• population mix moving favourably towards a younger

age profile

• urbanisation with increasing incomes

Investors can look to capture the gains of the Indian telecom

boom and diversify their operations outside developed

economies that are marked by saturated telecom markets

and lower GDP growth rates.

Till recently, the industry believed that while the hike in

Foreign Direct Investment (FDI) limits was necessary, it was

not a sufficient condition for growth of the telecom sector.

With most of the regulatory uncertainty getting over, there

is heightened interest in Indian telecom.

Further, at a time when global telecom majors are struggling

to cope with their losses and the rollout of 3G networks,

which has been a non-starter for close to a year now; India,

with its telecom success story, represents an attractive and

lucrative destination for investment.

Inflow of FDI into India’s telecom sector between 1991 and

2003 was about US$ 2 billion. Also, 20 per cent of the

approved FDI in the country is related to the telecom sector.

OPPORTUNITIES

Dynamism in the services

sector and changing

consumer profile

is enhancing growth

in telecom

India represents vast

untapped potential

for global telecom majors

PAGE 13

A comparison with countries in the Asian region indicates

that India still has some way to go, to reach the levels of

tele-density in these countries (data 2002), which brings

in its wake a host of opportunities for investment in

the Indian market.

Sectorwise inflow of telecom FDI (1991-2003)

Lower prevailing

tele-density levels

compared to Asian

economies indicate

a huge demand potential

Concrete steps taken by the Government of India are key

drivers facilitating investment in the sector. It is reported that

Department of Telecommunications is considering proposals

for reduction in Licence Fee (currently between 6 per cent

Government initiatives

facilitating…

Country/Market Total Tele-density %

India (Total) 5.2

India (Urban) 15

China 32

Malaysia 57

South Korea 116

Source: investindiatelecom.com

Source: Industry estimates

India and select markets 2002

T E L E C O M M U N I C A T I O N S

and 10 per cent) and Spectrum Charges (currently between

2 per cent and 4 per cent) for Basic and Cellular Operators

to make the services more affordable.

With the introduction of the Unified Access Licensing Regime,

operators can offer telecom access services to consumers

in a technology neutral manner, subject to fulfilling certain

conditions. Introduction of this regime has also broken

the legal/regulatory impasse between the cellular and basic

service providers.

Issuance of Intra-Circle Merger and Acquisition Guidelines

provide investors an opportunity to take stakes in existing

telecom operations.

Bharti Tele-Ventures, a large private telecom player offering

varied telecom services and the largest GSM cellular operator,

currently has foreign partners holding a combined stake of

47.3 per cent in the company; these include SingTel (with 28.5

per cent), Warburg Pincus, International Finance Corporation,

Asian Infrastructure Fund Group and New York Life Insurance.

Hutchison Whampoa has a 49 per cent stake in Hutchison

Telecom, the second largest GSM cellular operator in India.

Distacom has a 42 per cent stake in Spice Communications.

AT&T Wireless has a 33.3 per cent stake in Idea Cellular

while France Telecom holds a 26 per cent stake in BPL Mobile.

…expanding bouquet

of services to extended

to consumers…

...increasing opportunities

for investor stakes

PAGE 15

CONTACT FOR INFORMATION

The telecom market is regulated by the Telecom

Regulatory Authority of India, and the Department

of Telecommunications is the licensor. They can be

contacted at the following addresses:

Telecom Regulatory Authority of India

A-2/14 Safdarjung Enclave

New Delhi 110 029

India

Tel: + 91 11 2610 1934

Fax: + 91 11 2610 3294

Email: [email protected]

Website: www.trai.gov.in

Department of Telecommunications

Ministry of Communications

Sanchar Bhawan

20 Ashoka Road

New Delhi 110 001

India

Tel: + 91 11 2371 6666

Fax: + 91 11 2337 2323

Website: www.dotindia.com

Explore, invest and partner

with India to profit and

advantage

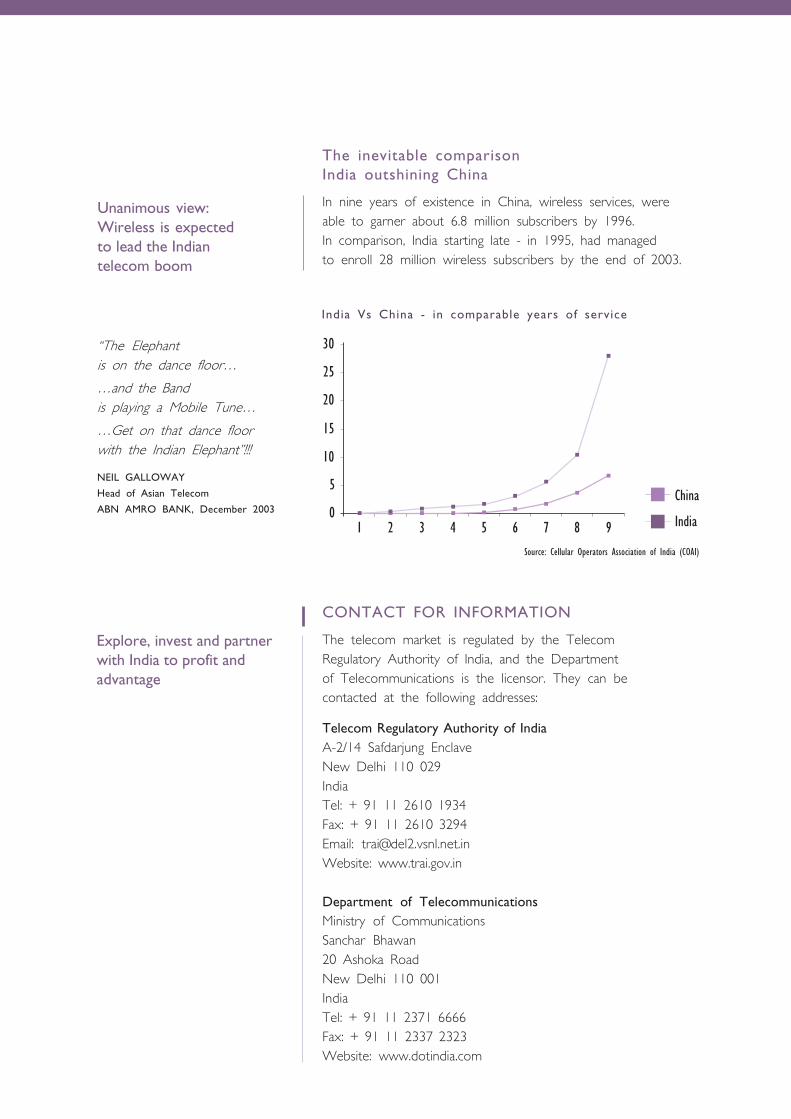

India Vs China - in comparable years of service

“The Elephant

is on the dance floor…

…and the Band

is playing a Mobile Tune…

…Get on that dance floor

with the Indian Elephant”!!!

NEIL GALLOWAY

Head of Asian Telecom

ABN AMRO BANK, December 2003

Unanimous view:

Wireless is expected

to lead the Indian

telecom boom

The inevitable comparison

India outshining China

In nine years of existence in China, wireless services, were

able to garner about 6.8 million subscribers by 1996.

In comparison, India starting late - in 1995, had managed

to enroll 28 million wireless subscribers by the end of 2003.

Source: Cellular Operators Association of India (COAI)

T E L E C O M M U N I C A T I O N S

DISCLAIMER

This publication has been prepared for the India Brand Equity Foundation

(“IBEF”).

All rights reserved. All copyright in this publication and related works is owned by

IBEF. The same may not be reproduced, wholly or in part in any material form

(including photocopying or storing it in any medium by electronic means and

whether or not transiently or incidentally to some other use of this publication),

modified or in any manner communicated to any third party except with the

written approval of IBEF.

This publication is for information purposes only. While due care has been taken

during the compilation of this publication to ensure that the information is

accurate to the best of IBEF’s knowledge and belief, the content is not to be

construed in any manner whatsoever as a substitute for professional advice.

IBEF neither recommends nor endorses any specific products or services that may

have been mentioned in this publication and nor does it assume any liability

or responsibility for the outcome of decisions taken as a result of any reliance

placed on this publication.

IBEF shall, in no way, be liable for any direct or indirect damages that may arise due

to any act or omission on the part of the user due to any reliance placed

or guidance taken from any portion of this publication.

The India Brand Equity Foundation is a public-private partnershipbetween the Ministry of Commerce, Government of India and

the Confederation of Indian Industry. The Foundation's primary objectiveis to build positive economic perceptions of India globally.

India Brand Equity Foundationc/o Confederation of Indian Industry

249-F Sector 18Udyog Vihar Phase IV

Gurgaon 122015 HaryanaINDIA

Tel +91 124 501 4087 Fax +91 124 501 3873E-mail [email protected]

Web www.ciionline.org

Knowledge Partner