tel_archives.ofca.gov.hktel_archives.ofca.gov.hk/en/report-paper-guide/paper/consultation/...a...

TRANSCRIPT

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

1

Joint Ownership of Hong Kong CSL Limited and New

World PCS Limited

Submission to the Office of the Telecommunications Authority

in support of a joint application for

prior consent under sections 7P(6) and (7) of the Telecommunications Ordinance

PUBLIC VERSION

25 January 2006

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

2

Contents

SSSeeeccctttiiiooonnn OOOnnneee Executive summary 3

SSSeeeccctttiiiooonnn TTTwwwooo Details of parties 7

SSSeeeccctttiiiooonnn TTThhhrrreeeeee Details of transaction 10

SSSeeeccctttiiiooonnn FFFooouuurrr Rationale and efficiencies 16

SSSeeeccctttiiiooonnn FFFiiivvveee Application of section 7P 18

SSSeeeccctttiiiooonnn SSSiiixxx Market definition 20

SSSeeeccctttiiiooonnn SSSeeevvveeennn Competitive overlap 26

SSSeeeccctttiiiooonnn EEEiiiggghhhttt Constraint from competitors 30

SSSeeeccctttiiiooonnn NNNiiinnneee Market concentration 40

SSSeeeccctttiiiooonnn TTTeeennn Scope for market entry 51

SSSeeeccctttiiiooonnn EEEllleeevvveeennn Competition analysis 54

SSSeeeccctttiiiooonnn TTTwwweeelllvvveee Public benefits 57

AAAttttttaaaccchhhmmmeeennntttsss 60

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

3

1 Executive Summary

1.1 Proposed common ownership of CSL and NWPCS

This submission has been prepared in support of a joint application to the Telecommunications Authority (“TA”) for prior consent under sections 7P(6) and (7) of the Telecommunications Ordinance (“Ordinance”). This submission is a joint submission by Hong Kong CSL Limited (“CSL”) and New World PCS Limited (“NWPCS”) as telecommunications licensees (“Applicants”).

The proposed transaction (“Transaction”) relevantly involves the injection and transfer by New World Mobile Holdings Limited (“NWM Listco”), a listed subsidiary of New World Development Company Limited (“NWD”, together with its subsidiaries, (the “NWPCS Group”) of all of NWM Listco’s interests in New World PCS Holdings Limited (“NWPCS Holdco”) to Telstra CSL Limited (to be renamed CSL New World Mobility Limited) (“JVCo”). NWM Listco will also make a cash payment of HK$244.024 million to JVCo. In consideration for which, JVCo has agreed to issue and allot to Upper Start Holdings Limited ("NWSPV"), a wholly-owned subsidiary of NWM Listco, new shares in JVCo.

The effect of the Transaction will be that JVCo will become the common owner of CSL and NWPCS. Upon completion, Telstra Corporation Limited (“Telstra”, together with its subsidiaries, the “Telstra Group”) will be the beneficial owner of 76.4% of the issued share capital of JVCo, while NWM Listco will become the beneficial owner of the remaining 23.6% of the issued share capital of JVCo.

The businesses of CSL and NWPCS will initially be retained in separate subsidiaries of JVCo, but progressive rationalisation will occur to realise efficiencies and synergies. Ancillary restraints will apply as between the Telstra Group and the NWPCS Group.

1.2 Commercial objectives

The primary commercial objectives of the Transaction are to:

• enhance CSL’s and NWPCS’ overall competitive and strategic position in the highly competitive Hong Kong mobile market by creating a commonly-owned business with strong brand recognition across the full spectrum of customer segments;

• more specifically, enable CSL and NWPCS to compete in the Hong Kong market from a position of greater efficiency;

The annual pre-tax operating cost savings arising from the realisable synergies and efficiencies of the Transaction are estimated at approximately HK$230 million. In addition, it is estimated that HK$215 million in savings will be derived from reductions in capital spending, predominately on network infrastructure and information technology platforms. [CONFIDENTIAL]; and

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

4

• reduce the need for duplicative capital expenditure by CSL and NWPCS, while enabling the efficient pooling of expenditure directed at service enhancement and innovation.

These commercial objectives are assisted by:

• NWPCS and CSL constituting the only mobile network operators in Hong Kong utilising Nokia core mobile network infrastructure and radio network infrastructure;

• NWPCS’ and CSL’s complementary brands and market strategies, resulting in minimal existing competitive overlap between NWPCS and CSL over the relevant market segments; and

• NWPCS’ desire to obtain optimal access to 3G spectrum so as to meet long-term 3G competition while minimising transaction costs.

1.3 Market definition

The relevant market in which the Transaction should be assessed is the Hong Kong market for the supply of mobile voice and data services. This market has a number of market segments as identified in Section 7 of this submission.

1.4 No substantial lessening of competition

The Transaction will not have, or be likely to have, the effect of substantially lessening competition in any telecommunications market for the following key reasons:

• High intensity of competition: The Hong Kong mobile market is widely recognised as one of the most competitive and least concentrated mobile markets in the world. Post-merger this situation remains. The high intensity of competition, in conjunction with the absence of any likely adverse impact of the Transaction on the intensity of that competition, should alone give OFTA sufficient comfort that no substantial lessening of competition is likely to occur.

• No additional market power: NWPCS and CSL will gain no additional market power from the Transaction. Post merger, there would still be:

• four strong, well-resourced, experienced and aggressive 3G/2G competitors (i.e., Hutchison, CSL-NWPCS, SmarTone-Vodafone and Sunday-PCCW);

• an experienced and aggressive competitor with a 2G licence (i.e., Peoples-China Mobile) with the potential ability to leverage roaming revenues and with access to 3G network capacity under the Mobile Virtual Network Operator (“MVNO”) open network access regime;

• seven licensed MVNO competitors with potential for significant further MVNO market entry; and

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

5

• numerous unlicensed Mobile Value-Added Resellers (“MVAR”) competitors with potential for significant further MVAR market entry.

• Continuing scope for fierce competition: Fierce competition will continue after the merger, particularly in light of recent market developments:

• Hutchison is currently the largest mobile operator in Hong Kong and has the ability to bundle mobile telephony with its fixed voice business while leveraging from its brand which is one of the largest 3G mobile businesses in the world.

• SmarTone through a Partner Network Agreement with Vodafone (the world’s largest mobile operator by revenue and the world’s second largest mobile operator by subscribers) can access Vodafone’s extensive global procurement pool, global and recognised brand, global expertise and extensive global mobile content.

• PCCW via Sunday can bundle and leverage PCCW’s fixed line business, brand, and significant overall market power.

• Following China Mobile’s proposed acquisition, Peoples will be aligned with the world’s largest mobile operator by subscribers and third largest mobile operator by revenue.

• High level of market contestability: The threat of further market entry is real and present, particularly by MVNO and MVAR competitors. 3G licensees are required under the mandatory open network access requirement of their licences to offer at least 30% of their 3G network capacity to non-affiliated MVNO operators, substantially reducing any barriers to entry associated with limited spectrum.

• No material competitive constraint on each other: NWPCS and CSL are not price leaders and have complementary brands that are generally targeted at different customer demographics, resulting in minimal existing competitive overlap between NWPCS and CSL over the different market segments. They do not exercise material competitive constraints on each other and the existing brands will be retained post-acquisition. Any impact of the Transaction on competition is therefore de minimus.

• Dynamic nature of mobile market: The market is dynamic and characterised by rapid innovation. 3G is currently viewed as the future of mobile competition. The industry move to 3G is generating further significant price and non-price competition.

[CONFIDENTIAL]

• Level of HHI concentration is acceptable: International precedent indicates that the proposed post-merger level of market concentration, illustrated by the HHI figures, will still result in a highly competitive market. Mergers resulting in significantly higher levels of HHI have been approved in a range of other jurisdictions and none have been rejected at the levels of post-merger HHI that will

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

6

occur in Hong Kong. Indeed, many commentators consider that market consolidation or exit among the mobile network operators in Hong Kong has been inevitable given the high number of mobile network operators relative to the size of the Hong Kong population and economy.

1.5 Significant potential public benefits

The Applicants do not consider that the Transaction will result in a substantial lessening of competition, but for completeness, should OFTA consider that a net public benefit analysis is necessary, the Applicants also submit that the Transaction is likely to result in material public benefits for the purposes of section 7P(7)(b)(iii) of the Ordinance.

• Greater cost efficiency: Network efficiencies, cost savings and economies of scale will provide scope for CSL and NWPCS to compete in the Hong Kong mobile market from a position of greater efficiency, to the ultimate benefit of Hong Kong consumers.

• New mobile technologies: The larger subscriber base of CSL and NWPCS will provide economies of scale in relation to the development and implementation of new mobile technologies (e.g., advanced data applications and technologies), potentially resulting in their earlier introduction to Hong Kong consumers and constraining the power of fixed line operators via fixed-mobile substitution.

• Enhanced intermodal competition as a constraint on fixed-line operators: As recognised by United States precedent, mergers of wireless carriers that lack a direct wireline affiliation are more likely to promote intermodal competition with fixed network operators. The Federal Communications Commission has viewed this as a public interest benefit.

• Higher quality services: The overall quality of both networks will be increased via progressive rationalisation around the best sites, technologies, and infrastructure, leading to increased quality of services to the benefit of Hong Kong consumers.

• Wider environmental benefits: Rationalisation will reduce unnecessary duplication of infrastructure, resulting in wider environmental benefits.

Please note: The words “[CONFIDENTIAL]” used in this submission designate instances where information has been included in the confidential version of the submission but not included in the public version of the submission.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

7

2 Details of Parties

2.1 Description of CSL business

CSL is a mobile telecommunications network operator and service provider in the Hong Kong market. CSL is a telecommunications licensee and the holder of a number of telecommunications licences, as identified in Attachment D of this submission.

• CSL’s background: Historically CSL (then Hong Kong Telecom CSL Limited) launched its mobile service in Hong Kong in 1993. A dualband GSM network was subsequently launched in 1998, integrating the GSM 900MHz network with a GSM 1800MHz (PCS) network acquired from Pacific Link Communications Limited. CSL was the first mobile operator in Hong Kong.

In late 2000, in the context of the takeover of Cable &Wireless HKT Limited by PCCW Limited (“PCWW”) and a subsequent joint venture with Telstra, Telstra acquired 60% of CSL and PCCW retained 40% through JVCo. Telstra subsequently acquired 100% ownership of CSL from PCCW in June 2002 by acquiring PCCW’s 40% holding in JVCo.

Telstra is Australia’s leading telecommunications and information services company. Telstra offers a full range of services and competes in telecommunications markets throughout Australia and in the Asia Pacific region.

• CSL’s networks: Today CSL operates an integrated 2G/3G world-class mobile network based on Nokia equipment.

[CONFIDENTIAL]

3G services were commercially launched in December 2004.

• CSL’s services: At the wholesale level CSL supplies mobile interconnect terminating services, MVNO services and MVAR resale services to a number of other market participants. At the retail level CSL supplies post-paid mobile services, international roaming services and pre-paid mobile services, as identified in Section 7 of this submission.

• CSL’s financial position: CSL’s financial position as at 30 June 2004 and 30 June 2005 is summarised in the following table based on the unaudited consolidated results of the Telstra CSL Group for each of the years ended 30 June 2005 and 30 June 2004: [CONFIDENTIAL]

The parties assume that OFTA is already highly familiar with CSL’s business. However, further information in relation to CSL can be found at the following URLs:

• http://www.hkcsl.com/main.html (English)

• http://www.hkcsl.com/main_c.html (Chinese)

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

8

2.2 Description of NWPCS business

NWPCS operates as a mobile telecommunications network operator and service provider in the Hong Kong market. NWPCS is a telecommunications licensee and the holder of a number of telecommunications licences, as identified in Attachment E of this submission.

• NWPCS’ background: Historically, NWPCS launched its first mobile service, a GSM 1800MHz (PCS) system in 1997. NWPCS was initially a subsidiary of New World Telephone Holdings Limited as part of the NWPCS Group. The principal activities of the NWPCS Group are property development, property investments, hotel and infrastructure investments, services and telecommunications and technology business, primarily in Hong Kong and mainland China.

In July 2004, NWPCS was sold to NWM Listco, a company incorporated in Hong Kong with limited liability and whose shares are listed on the Hong Kong Stock Exchange stock code “0862”. As a result of the sale, NWM Listco became and still remains a subsidiary of NWD.

NWPCS is currently a wholly-owned subsidiary of NWPCS Holdco which is in turn a wholly-owned subsidiary of NWM Listco. NWPCS trades under the name “New World Mobility”.

• NWPCS’ networks: Today NWPCS operates a world-class mobile network based on Nokia equipment, comprising a GSM network providing 2G voice and 2.5G mobile data services (i.e. GPRS and EDGE) over 1800MHz spectrum.

• NWPCS’ services: At the wholesale level NWPCS supplies mobile interconnect terminating services, MVNO services and MVAR resale services to a number of other market participants. At the retail level, NWPCS supplies post-paid mobile services, international roaming services and pre-paid mobile services.

• NWPCS Group’s financial position: NWPCS Group’s financial position as at 30 June 2004 and 30 June 2005 is summarised in the following table based on the audited consolidated results of the NWPCS Group for each of the years ended 30 June 2005 and 30 June 2004:

[CONFIDENTIAL]

The parties assume that OFTA is already highly familiar with NWPCS’ business. However, further information in relation to NWPCS can be found at the following URLs:

• http://www1.nwmobility.com/html/eng/default.jsp (English)

• http://www2.nwmobility.com/html/chi/default.jsp (Chinese)

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

9

2.3 Further correspondence

Further correspondence in relation to this joint application for prior consent should be directed to the following people.

Roger Featherston is nominated as the principal contact.

Roger Featherston Dr Martyn Taylor Partner Senior Associate Mallesons Stephen Jaques Mallesons Stephen Jaques Phone: +61 3 9643 4101 Phone: +61 2 9296 2309 Fax: +61 3 9643 5999 Fax: +61 2 9296 3999 Email: [email protected] Email: [email protected]

Copied to (for CSL):

Jillian Cordeiro Danny Kotlowitz General Counsel Lawyer Hong Kong CSL Limited Telstra Corporation Limited Phone: +852 2888 9146 Phone: +61 2 9206 0015 Fax: +852 2519 9933 Fax: +61 2 9261 2401 Email: [email protected] Email: [email protected]

Copied to (for NWPCS):

Dr Norman Wai Executive Director and CEO New World Mobility Phone: +852 2133 8365 Fax: +852 3111 9166 Email: [email protected]

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

10

3 Details of Transaction

3.1 Description of Transaction

The Transaction relevantly involves the injection and transfer by NWM Listco of all of NWM Listco’s interests in NWPCS Holdco to JVCo. NWM Listco will also make a cash payment of HK$244.024 million to JVCo. In consideration for which, JVCo will issue and allot to NWSPV new shares in JVCo, which will represent 23.6% of the enlarged issued share capital of JVCo upon completion.

The effect of the Transaction will be that JVCo will become the common owner of CSL and NWPCS. Upon completion, Telstra will be the beneficial owner of 76.4% of the share capital of JVCo, while NWM Listco will become the beneficial owner of the remaining 23.6% of the share capital of JVCo.

The businesses of CSL and NWPCS will initially be retained in separate subsidiaries of JVCo, but progressive rationalisation will occur to realise efficiencies and synergies.

Ancillary restraints will apply as between the Telstra Group and the NWPCS Group pursuant to a shareholders’ agreement.

The Transaction will not occur until completion, which is, in turn, conditional on:

• the TA’s prior consent under section 7P(7) of the Ordinance;

• approval by the shareholders of NWM Listco at an extraordinary general meeting;

• the Bermuda Monetary Authority giving its approval to the transactions to the extent such approval is required; and

• no material adverse change having occurred in relation to the respective groups between the execution of the merger agreement and completion.

3.2 Pre-Transaction structure of CSL

[CONFIDENTIAL]

• The operating company and telecommunications licensee is CSL.

• Telstra is the beneficial owner of 100% of the shares in CSL. Telstra is incorporated in Australia and is listed on the Australian and New York Stock Exchanges.

• As at the date of its annual report on 18 August 2005, Telstra was owned 51.8% by the Commonwealth of Australia and 48.2% by institutional and retail investors. The Telstra (Transition to Full Private Ownership) Act 2005 enables the Commonwealth of Australia to divest its remaining shareholding in Telstra.

• Telstra holds its interest in CSL via a chain of 4 intermediate holdings companies.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

11

[CONFIDENTIAL]

A simplified version of the CSL pre-Transaction structure is set out in Figure 1 below:

Figure 1 : Simplified CSL pre-Transaction structure

Telstra Corporation Limited (“Telstra”)

Telstra CSL Limited (“JVCo”)

Telstra Holdings Pty Limited (“TLS Holdco 1”)

100%

Telstra currently owns 100%

of CSL

Hong Kong CSL Limited and subsidiaries (“CSL”)

Bestclass Holdings Limited

100%

100%

100%

Holding

companies

Operating company and

licensee

Telstra Holdings (Bermuda) No.2 Limited (“TLS Holdco 2”)

100%

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

12

3.3 Pre-Transaction structure of NWPCS Group

[CONFIDENTIAL]

• The operating company and telecommunications licensee is NWPCS, trading under the name “New World Mobility”.

• NWM Listco is the beneficial owner of 100% of the shares in NWPCS. NWM Listco is incorporated in the Cayman Islands and its shares are listed on the Hong Kong Stock Exchange. NWM Listco holds its interest in NWPCS via two intermediate holding companies, as indicated by Figure 2 below.

• NWD is the indirect beneficial owner of 58.04% of the shares in NWM Listco. NWD is incorporated in Hong Kong and its shares are listed on the Hong Kong Stock Exchange.

A simplified version of the NWPCS pre-Transaction structure is set out in Figure 2 below:

Figure 2 : Simplified NWPCS Group pre-Transaction structure

NWD currently owns 58.04% of NWM Listco which in turn owns 100%

of NWPCS

New World Development Company Limited (“NWD”)

New World Mobile Holdings Limited (“NWM Listco”)

Intermediate holding companies

100%

58.04%

100%

Public 41.96%

Holding

companies

Operating company and

licensee

Listed

entity

100%

New World PCS Limited (“NWPCS”)

New World PCS Holdings Limited (“NWPCS Holdco”)

Listed

entity

Holding

companies

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

13

3.4 Ownership structure after the Transaction

The Transaction will relevantly involve the following key elements:

• NWM Listco will inject and transfer its 100% interest in NWPCS Holdco to JVCo;

• NWM Listco will make a cash payment of HK$244.024 million to JVCo; and

• JVCo will issue and allot to NWSPV new shares in JVCo which will represent 23.6% of the enlarged issued share capital of JVCo upon completion.

[CONFIDENTIAL]

A simplified version of the ownership structure after the Transaction is set out in Figure 3 below:

• JVCo is the point of common ownership of NWPCS and CSL. JVCo will have:

• beneficial ownership of 100% of the share capital of NWPCS, as operating company and licensee, via the holding company NWPCS HoldCo; and

• beneficial ownership of 100% of the share capital of CSL, as operating company and licensee, via the holding company CSL HoldCo.

• Telstra will be the beneficial owner of 76.4% of the shares in JVCo via a series of two wholly-owned intermediate holding companies, namely TLS Holdco 1 and TLS Holdco 2.

[CONFIDENTIAL]

• NWM Listco will be the beneficial owner of 23.6% of the shares in JVCo via a wholly-owned intermediate holding company, namely NWSPV.

• NWD will be the beneficial owner of 58.04% of the shares in NWM Listco via a series of intermediate holding companies.

[CONFIDENTIAL]

NWD, NWM Listco, NWSPV, Telstra, TLS Holdco 2 and JVCo have also entered into a shareholders’ agreement in respect of JVCo which will take effect as from completion of the Transaction (“Shareholders Agreement”). The Shareholders Agreement provides:

• based on the shareholding of TLS Holdco 2 and NWSPV after completion of the Transaction, the Shareholders Agreement relevantly gives TLS Holdco 2 the right to appoint 4 directors of JVCo, including the Chairman; NWSPV has the right to appoint 2 directors of JVCo;

[CONFIDENTIAL]

• Each of TLS Holdco 2 and NWSPV also have the right in mid 2008 to call for a listing of JVCo by way of an IPO in 2009 or subsequently.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

14

It is intended that Mr. Hubert Ng, the current CEO of CSL, will be the CEO of JVCo.

Figure 3 : Simplified post-Transaction structure

100%

Hong Kong CSL Limited and subsidiaries (“CSL”)

Telstra Holdings Pty Limited (“TLS Holdco 1”)

Telstra Corporation Limited (“Telstra”)

Bestclass Holdings Limited

100%

New World Development Company Limited (“NWD”)

New World Mobile Holdings Limited (“NWM Listco”)

Intermediate holding companies

100%

58.04%

New World PCS Holdings Limited (“NWPCS Holdco”)

100%

New World PCS Limited (“NWPCS”)

Telstra CSL Limited (“JVCo”) to be renamed as

CSL New World Mobility Limited

100% 100%

The existing, businesses will be retained, but with

progressive rationalisation and realisation of synergies

76.4% 23.6%

Upper Start Holdings Limited (“NWSPV”)

Telstra Holdings (Bermuda) No.2 Limited (“TLS Holdco 2”)

100%

100%

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

15

3.5 Timing of Transaction

The Transaction has two remaining phases:

• Phase 1 (Execution and announcement): The execution of formal Transaction documentation occurred on 8 December 2005 and was publicly announced on 9 December 2005 by Telstra and on 13 December 2005 by NWD and NWM Listco. As identified above, the documentation remains subject to various conditions precedent, including TA’s prior consent and an NWM Listco shareholder approval.

• Phase 2 (Completion and implementation): The Transaction completion target, as advised to the market by Telstra, is 31 March 2006. Following completion, JVCo will commence rationalising the businesses of CSL and NWPCS in order to realise efficiencies and synergies over an estimated 24 month period.

[CONFIDENTIAL]

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

16

4 Rationale and Efficiencies

4.1 Commercial rationale

The commercial rationale for the Transaction is as follows:

• Competitive and strategic positioning: The Transaction will enhance CSL’s and NWPCS’ competitive and strategic position in the highly competitive Hong Kong mobile market. The transaction will create an entity with strong brand recognition across the full spectrum of customer segments.

• Cost-savings and efficiencies: More specifically, the Transaction will enable CSL and NWPCS to compete in the Hong Kong market from a position of greater efficiency. NWPCS and CSL will jointly realise operating cost savings via economies of scale and rationalisation of assets and activities. The Transaction will reduce the need for duplicative capital expenditure.

The pre-tax operating cost savings arising from the realisable synergies and efficiencies of the Transaction are estimated at approximately HK$230 million with a further HK$215 million in savings arising from reductions in capital spending, predominately on network infrastructure and information technology platforms. [CONFIDENTIAL]

These commercial objectives are assisted by the following features of the Transaction:

• Complementary network technologies: NWPCS and CSL are the only network operators in Hong Kong utilising both Nokia core mobile network infrastructure and radio network infrastructure. In this manner, NWPCS and CSL have complementary network assets to enable network synergies to be progressively realised and maximised at minimal overall cost.

• Complementary brands and business strategies: NWPCS and CSL have complementary brands and focus their competitive activities on different customer segments, resulting in minimal existing competitive overlap, as identified in Section 7 of this submission.

• NWPCS’ need for 3G spectrum: NWPCS does not have a 3G licence but is facing intense and sustained 3G voice and data competition from other network operators. The merger provides NWPCS with optimal access to CSL’s 3G spectrum so as to meet long-term 3G competition while minimising transaction costs. In this manner, the Transaction facilitates NWPCS developing long-term 3G capability.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

17

4.2 Efficiencies and synergies from the Transaction

As identified above, the Transaction will enable NWPCS and CSL to jointly realise operating cost savings via economies of scale and rationalisation of assets and activities.

NWPCS and CSL intend to progressively achieve post-transaction operating cost savings, efficiencies and synergies in the following manner:

• Rationalisation of network assets: While the NWPCS and CSL networks will initially remain separate, a major benefit of the Transaction from a cost savings perspective arises from the ability to rationalise some of NWPCS radio access network and associated transmission over a 24 month period following completion.

In particular, cost savings are expected from:

• [CONFIDENTIAL]

• [CONFIDENTIAL]

• reduced repair and maintenance costs, as the overall size of the combined networks would be reduced for the same level of mobile coverage by the removal of wasteful duplication of infrastructure;

• [CONFIDENTIAL]

• [CONFIDENTIAL]

[CONFIDENTIAL]

• [CONFIDENTIAL]

• [CONFIDENTIAL]

• Realising economies of scale: Economies of scale could be realized in content, resulting in reduced content expenses. Economies of scale can also be realised in application development.

• Customer access to 3G spectrum: NWPCS has no 3G spectrum of its own so would otherwise need to establish a separate MVNO or MVAR business in order to supply 3G services to its customers.

[CONFIDENTIAL]

Essentially, the synergies and efficiencies arise from the rationalisation of the “back end” (network and operations) of the respective businesses of CSL and NWPCS while leaving the “front end” (sales and branding) relatively unchanged.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

18

5 Application of section 7P

5.1 Change in carrier licensee

Sections 7P(6) and (7) of the Ordinance enable a carrier licensee or any interested person to apply in writing to the TA for consent to any proposed change in relation to a carrier licensee.

The Transaction results in a change occurring in relation to two carrier licensees for the purposes of section 7P(16) of the Ordinance, namely NWPCS and CSL:

• a change occurs in relation to NWPCS because JVCo becomes the owner of 100% of the shares in NWPCS Holdco which, in turn, owns 100% of the shares in NWPCS as licensee;

• a change occurs in relation to both CSL and NWPCS because NWSPV will subscribe for new shares in JVCo which will represent 23.6% of the enlarged issued share capital of JVCo upon completion. JVCo is the indirect beneficial owner of 100% of the shares in CSL and NWPCS (via the simultaneous change identified above).

The relevant licences of CSL and NWPCS are listed in Attachments D and E of this submission respectively (“Relevant Licences”).

5.2 Overlapping provisions (para 1.22-1.24 of Guidelines)

The Telecommunications Authority’s Guidelines Mergers and Acquisitions in Hong Kong

Telecommunications Markets (“Guidelines”), at paragraphs 1.22-1.24, indicate that, in the interests of a clear and certain merger framework, the TA will rely primarily on the provisions of section 7P of the Ordinance when considering mergers and acquisitions, hence the TA will not apply:

• sections 7K and 7L of the Ordinance; or

• equivalent provisions to sections 7K and 7L in licences issues under the Ordinance prohibiting anti-competitive conduct and abuses of dominance.

The Applicants note that some of the Relevant Licences contain a number of relevant and overlapping provisions, in this category, some of which require express TA consent1.

The Applicants therefore seek consent to the Transaction under section 7P on the basis that the TA prior consent will also cover all other consents required from the TA for the Transaction under overlapping provisions in the Relevant Licences.

1 The Applicants note that the TA has waived the requirements under Special Conditions 21.1 of CSL’s 3G

licence.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

19

5.3 Ancillary restraint (para 1.25-1.26 of Guidelines)

Relevantly, the Transaction includes an ancillary restraint located within the Shareholders Agreement (“Ancillary Restraint’).

The Guidelines, at paragraphs 1.25 and 1.26, indicate that where the relevant restraints are directly related and necessary to the implementation of the merger agreement, they will be treated as ancillary restraints and will be assessed as part of the merger transaction under section 7P.

The Applicants consider that the Ancillary Restraint is directly related and necessary to the implementation of the Transaction for the reasons identified below. The Applicants therefore request the TA assess the Ancillary Restraint as part of the overall Transaction, consistent with the approach contemplated by the Guidelines.

[CONFIDENTIAL]

The remainder of this submission considers the overall competitive effect of the Transaction with the Ancillary Restraint included.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

20

6 Market Definition

6.1 Mobile market

The relevant market in which the Transaction should be assessed is the Hong Kong market for the supply of mobile voice and data services. The market encompasses both wholesale and retail supply of mobile services.

In the TA’s Report on the Competition Impact of the Acquisition of Shares in Sunday by PCCW (“Report”), the TA relevantly reached the following conclusions in relation to the appropriate mobile market definition of Hong Kong:

• While the TA considered a combined fixed-line and mobile telephony market in that case, this approach gave effect to the general principle that the TA should begin the assessment of competition factors using a market definition that most readily highlights potential competition concerns (para 6.6 of Report).

• The transaction in that case could also have been considered in the context of distinct fixed-line and mobile telephony markets (para 6.16 of Report).

• By the time BWA services become operational in Hong Kong, identification of separate mobile and fixed services markets may no longer be justified (para 6.25 of Report).

• OFTA also referred to a mobile market in a number of paragraphs throughout the Report, implicitly indicating that it viewed the mobile market as “national” (i.e., Hong Kong territory-wide) in scope and encompassing both wholesale and retail supply of mobile voice and data services.

6.2 International precedent on mobile market definition

International precedent indicates that 2G, 2.5G and 3G services are routinely considered to co-exist in the same product market, usually with voice and data co-existing in the same market (particularly given the relative infancy and small yet growing size of the mobile data market at this time). There is no precedent for defining separate pre-paid or post-paid markets. There is similarly no precedent for defining a market based on low, mid or high-level customer demographics. The geographic dimension is usually considered to be national in scope, particularly in a market the size of Hong Kong:

• Australia: The Australian Competition and Consumer Commission (“ACCC”) considered the appropriate market definition for mobile telephony in June 2004 in the context of its comprehensive Mobile Services Review and concluded that 2G, 2.5G, 3G and SMS services all co-exist within a national mobile market:2

“In determining the relevant product for the purposes of this inquiry, the Commission believes that, at the retail level, mobile operators sell a bundle of services to end-users that includes a range of subscription services and the ability to make outgoing calls.

2 ACCC, Mobile Services Review : Mobile Terminating Access Service, June 2004, Page 46,

http://www.accc.gov.au/content/item.phtml?itemId=708251&nodeId=file4327b89fad337&fn=Final%20report%20-%20mobile%20terminating%20access%20service%20(June%202004).pdf

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

21

Accordingly, the Commission believes it is appropriate to consider these retail services as being supplied within the same ‘cluster’ market.”

“Overall, therefore, the Commission’s view is the relevant market is that in which retail mobile services are supplied. This is a national market operating at a retail functional level. It includes retail mobile services provided on 2G, 2.5G and 3G networks and SMS services, but does not include fixed-line services.”

• United Kingdom: The Office of Communications (“OFCOM”) in the United Kingdom similarly concluded that 2G and 3G services exist in the same market in June 2004: 3

“The likelihood that there would be a common pricing constraint for 2G and 3G termination suggested that it would be appropriate to put these services in the same market ... OFCOM therefore considers that, on the basis of currently available information, it would not be appropriate to define separate markets.”

• European Union: The European Commission also concluded that different types of mobile platforms exist in the same market with national scope in July 2002:4

“As regards the provision of mobile communications services, the Commission has found that, from a demand-side point of view, mobile telephony services and fixed telephony services constitute separate markets. Within the mobile market, evidence gathered from the Commission has indicated that the market for mobile communications services encompasses both GSM 900 and GSM 1800 and possibly analogue platforms.”

“The fact that mobile operators can provide services only in the areas where they have been authorised to and the fact that a network architecture reflects the geographical dimension of the mobile licences explains why mobile markets are considered to be national in scope.”

• Netherlands: The Dutch Competition Authority (“Authority”) in its approval of the KPN/Telfort merger on 30 August 2005 discussed a number of issues relating to market definition in the context of a merger of two mobile operators, reducing the number of mobile network operators from 5 to 4. The Authority relevantly concluded for the purposes of its review that:5

• mobile voice and data exist in the same product market;

• business and consumer segments exist in the same product market; and

3 OFCOM, Statement on Wholesale Mobile Voice Call Termination, 1 June 2004, para 2.21,

http://www.ofcom.org.uk/consult/condocs/mobile_call_termination/wmvct/chapter2/?a=87101 4 European Commission, Commission guidelines on market analysis and the assessment of significant

market power under the Community regulatory framework for electronic communications networks and

services, (2002/C 165/03), 11 July 2002, para 66 and footnote 44, http://europa.eu.int/information_society/topics/telecoms/regulatory/maindocs/documents/c_16520020711en00060031.pdf 3G was not mentioned given the service had not been deployed in Europe at the time.

5 Decision of the Board of Directors of the Dutch Competition Authority as referred in article 37, first paragraph, of the Competition Law, Number 5104 /45, Regarding Case: 5104/KPN - Telfort, 30 August 2005, paras 14 to 19.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

22

• pre-paid and post-paid services exist in the same product market. The Authority relevantly commented, for example:6

“Given the low thresholds for switching and the similarities in product characteristics, it is plausible that a considerable proportion of end-users will change to post-paid in the case of an increase in the price of pre-paid and vice-versa. Besides, there are possibilities for supply-side substitution. Thus, for the current analysis, the retail market will not be subdivided further into post-paid and pre-paid services.”

• United States: For the purposes of its annual review of competitive market conditions in relation to commercial mobile services, the Federal Communications Commission (“FCC”) indicated on 30 September 2005 it was adopting a conservative market definition for the purposes of its report in which data and voice existed in separate product markets. However, the FCC commented that it may be inclined to adopt a view in which they both existed in the same product market in other contexts: 7

“The basic economic principle for defining the scope of the relevant product market is to include two mobile services in the same product market if they are essentially interchangeable from the perspective of most consumers – that is, if consumers view them as close substitutes. For the purposes of this report, relatively narrow product market definitions will be used, with a separate product market identified for each of the following services: interconnected mobile voice; interconnected mobile data; and mobile satellite service. However, the identification of separate markets for each service in the context of this report does not preclude the possibility that, in a different context, the Commission may find that two or more of these services belong in the same product market.”

The FCC’s approach of considering voice and data to exist in the same product market for the purposes of merger review decisions is illustrated by the Sprint-Nextel merger order. As indicated in the quote below, the FCC considered the competitive impact of a mobile industry merger within a mobile product market that comprised of both voice and data services:8

“As explained below, we find that there are separate relevant product markets for interconnected mobile voice services and mobile data services, and also for residential services and enterprise services. Nevertheless, we analyse all of these product markets under the combined market for mobile telephony. We believe, based upon consideration of factors including the nature of these services and their relationship with each other, that this approach will provide a reasonable assessment of any potential competitive harm to any of the markets as a result of the transaction….”

6 Ibid, para 16 : translated from Dutch by the Applicants. 7 Federal Communications Commission, 10th Annual Report and Analysis of Competitive Market

Conditions With Respect to Commercial Mobile Services, 30 September 2005, para 21, http://hraunfoss.fcc.gov/edocs_public/attachmatch/FCC-05-173A1.pdf

8 Ibid, para 38-42

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

23

• Canada: The Canadian Competition Bureau (“Bureau”) considered the acquisition of Microcell Telecommunications Inc. by Rogers Wireless Communications Inc. on 12 April 2005. The Bureau concluded that the relevant product market was mobile wireless (voice and data) telecommunications services.9

On the issue whether different product markets could be defined based on the underlying technological platform (i.e., CDMA as against GSM), the Bureau’s view was that the product market included both technological platforms.

6.3 Innovation and market evolution: 3G, WiMAX, and BWA

CSL and NWPCS note that the mobile market is dynamic and characterised by rapid innovation. 3G is viewed as the future of mobile competition and the industry move to 3G is already generating further significant price and non-price competition. In the near future, 3G will be supplemented by higher bandwidth BWA services such as WiMAX10, heralding the convergence of 3G, WiFi11 and local loop fixed-line services. The evolution of mobile technology is therefore likely to lead to increasingly greater substitutability between mobile and fixed line services, eroding the market power of fixed-line operators and possibly leading eventually to a converged fixed and mobile market.

In recognition of the dynamic nature of the Hong Kong mobile market, OFTA itself commented in its Report on the Competition Impact of the Acquisition of Shares in Sunday by PCCW (at para 6.25) that:

“By the time BWA becomes operational in Hong Kong for both fixed and mobile services (which is not expected within the next several years), identification of a narrow mobile services market (or a combined fixed-line/mobile services market) may not be justified. This is because technologies like BWA could hasten the convergence of a number of telecommunications services that are presently considered distinct, so that, for instance, the pricing of mobile services becomes closely related to the prices of fixed-line, broadband and other services that through substitution possibilities constrain the pricing and output discretion of mobile operators.”

Indeed, most competition regulators around the world have recognised the importance of innovation and market evolution to mobile markets. In the Canadian Competition Bureau's assessment of the Microcell Telecommunications Inc and Rogers Wireless Communications Inc. merger, for example, the Bureau commented: “Change and innovation will, in the Bureau's view, continue to play an important, positive role in the

future evolution of competition in this market.”12

9 Canadian Competition Bureau, Acquisition of Microcell Telecommunications Inc. by Rogers Wireless

Communications Inc., 12 April 2005. 10 WiMax stands for “Worldwide Interoperability for Microwave Access”, a system which is expected to

provide high bandwidth mobile access. A WiMax enabled device will be able to be connected over large areas much like existing mobile phones. A single WiMax antenna is expected to have a range of up to 65km with speeds of 70Mbit/s or more.

11 Wi-Fi stands for “Wireless Fidelity” and identifies a consortium which aims to guarantee the interoperability of hard and software for Wireless Local Area Networks.

12 See above, n 15.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

24

The Applicants submit that the impact of BWA and the speed at which BWA be rolled out in Hong Kong should not be understated.13 Subject to the formulation of regulatory policy and promulgation of relevant subordinate legislation, BWA is expected to be rolled out in Hong Kong in the near future in a comparable manner as similar services are being rolled out in other jurisdictions. International experience to date suggests that such services are likely to further intensify the level of competition in the mobile market, particularly in relation to wireless data services.

The potential for the rollout of BWA services in Hong Kong further increases the likelihood that competition in the Hong Kong mobile voice and data market is likely to intensify in the near future. Furthermore, the evolution of new technology means that greenfield operators could enter the market with networks capable of transmitting higher bandwidths at significantly lower cost than the networks of existing 2G, 2.5G and possibly 3G network operators (depending on the evolution of 3G technology).

Powerful global multinationals such as Intel Corporation are already positioning themselves to take advantage of new technologies like BWA to compete in the voice and data market. Intel comments in its current Investor fact sheet that, “We are focusing on growth through

platforms that run on powerful Intel® processors and incorporate the Ethernet, WiFi and

WiMAX technologies that users want”. For example, Intel recently acquired interests in “Clearwire” in the United States and “Unwired” in Australia. With Intel as the potential leading chipset producer for WiMax devices and as an investor in WiMax carriage providers, BWA will likely be a significant competitor to existing mobile services. Intel’s acquisitions reflect the industry view that BWA will, in the near future, compete with mobile voice and data services.

Commenting on the huge potential impact of WiMAX technology on mobile and fixed telecommunications operators, Richard Eccles recently commented in a July 2005 article:14

“Now a new technology, WIMAX (worldwide interoperability for microwave access), is just around the corner, and will enable wide area wireless communication via computers, in effect mobile or fixed access to broadband. It will also mobilise VoIP because VoIP works on any broadband connection, whether cable, DSL or wireless. WIMAX and VoIP combined will result in total convergence of internet, voice telephony, data and multimedia communication via a single device whether mobile or fixed – the ultimate convergence of communications technology and facilities.”

“The commercial availability of WiMAX will ultimately affect every part of the communications industry and once WiMAX networks have been rolled out and their usage has been established, the competitive structure of the sector will change. WiMAX will have an

impact on the following areas:

• Providers of DSL and cable modem broadband services will be affected as users take

up the mobile operation offered by WiMAX.

• Incumbents that have been slow to unbundle the fixed line local loop will find that any competitive leverage that they retain in this area will be reduced by the ability of WiMAX systems to bypass the copper local loop, accessing users directly from transmitter stations.

13 For example, on 18 October 2005 Nokia announced that it completed a call over its mobile WiMax

802.16e system. Nokia further announced it was now positioned to conduct WiMax trials during 2006. 14 R Eccles “The Mobile Broadband Revolution” Telecom Finance, Issue 16, 20 July 2005.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

25

• 3G data services (and also SMS services on 2G networks) will face the challenge of the same types and possibly a wider range of audio-visual content, including videos, being transmitted on equipment which may well be more user-friendly, for example, as regards to the sizes of the screens on WiMAX enabled computers.

• The introduction of VoIP on WiMAX systems will provide direct competition for voice telephony with 2G and 3G mobile services and increased competition to fixed-line services.”

“Also 3G operators will need to ensure that their charging structures for the provision of audio visual content are competitive in relation to WiMAX charges. All of this will take place before the 3G operators have even fully rolled out their services and recouped their investment.”

The Applicants are aware that the Hong Kong Government and OFTA are in the process of developing the spectrum and regulatory policy regarding the evolution and deployment of BWA services in Hong Kong. Accordingly, in the interests of brevity, the Applicants have not further identified the potential scope, impact and nature of BWA services in this submission. Rather, OFTA is assumed to be highly familiar with these issues.

These developments and their impact on market definition were well summarised by the TA at the recent Fixed-Mobile Convergence Forum:15

“With the advent of the Broadband Wireless Access (BWA) and other technologies, the access network can connect fixed customers or moving customers. It would be difficult to classify whether the core network connected to such an access network constitutes a fixed or a mobile network.”

“Once the restriction that a particular service can only serve fixed or moving customers is removed, there can be plenty of scope for designing the service around the actual communications needs of the users, who can be expected to be stationary at some times and moving at other times. The result is that new and innovative services will emerge, bringing convenience to users and generating value to operators.”

“Another important aspect is that not just one class of operators, fixed or mobile, can provide such converged services. Both the existing fixed and mobile operators will be able to participate in the provision of services that satisfy all the communications needs of their customers.”

15 http://www.ofta.gov.hk/en/speech-presentation/dg_20050922_speech.pdf

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

26

7 Competitive Overlap

7.1 Market segmentation

This Hong Kong market for the supply of mobile telephony services has a number of market segments which can be roughly plotted on a graph, indicating a consumer trade-off between price and quality, and between voice and data, as illustrated by Figure 4 below.

Figure 4: Mobile telephony market segmentation

The market segments identified in Figure 4 have the following key characteristics:

• Prepaid market segment: Most of the pre-paid market exists at the “value-focused” segment of the market. Consumers are largely focused on voice calls and SMS messaging as the main applications. Competition in the pre-paid market is characterised by intense price competition with less scope for product differentiation. However, network operators have successfully targeted different market niches, such as youth, teenagers, tourists, and foreign domestic workers.

• Postpaid “value-focused” consumer market segment: [CONFIDENTIAL] Consumers are highly price sensitive. Consumers prefer standard voice and SMS messaging applications to innovative data applications.

• Postpaid small-medium enterprise (“SME”) and “mid-tier” consumer market

segment: [CONFIDENTIAL] Consumers have a degree of price sensitivity, but also seek enhanced value-added services with innovative technology and some 2.5G/3G data applications.

• Postpaid corporate and “high-end” consumer market segment: [CONFIDENTIAL] Consumers are less price insensitive and more focused on

2G Voice / SMS Orientated 2.5G / 3G Data Orientated

Quality

Orientated

Price

Orientated

“Mid-tier” postpaid

market segment

“Value focussed” postpaid market

Corporate market segment

Prepaid market

segment

“High-end” postpaid market

segment

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

27

personalised service, advanced technologies and applications, quality and reliability. Consumers seek 2.5G and 3G services to support handheld mobile devices such as Blackberrys. Most large corporate consumers exist in this category as well as high usage consumers.

7.2 Business strategies and brands of CSL

[CONFIDENTIAL]

7.3 Business strategies and brands of NWPCS

[CONFIDENTIAL]

7.4 Complementary postpaid businesses of CSL and NWPCS

The above analysis of the brands and business strategies of CSL and NWPCS indicates that while they co-exist as competitors in the mobile telephony market, they target different postpaid customer segments:

• CSL’s general postpaid business strategy is to [CONFIDENTIAL]

• NWPCS’ general postpaid business strategy is to [CONFIDENTIAL]

In this manner, the postpaid brands of CSL and NWPCS exhibit a generally low degree of competitive overlap between market segments. Rather, the Transaction involves the amalgamation of two mobile operators with complementary post-paid brands and business strategies targeted at different customer demographics.

The complementary nature of the CSL and NWPCS postpaid brands evidences that any effect on competition arising from the Transaction is likely to be minimal.

In this regard, an important factor influencing the Authority’s assessment of the recent KPN/Telfort merger on 30 August 2005 was the complementary nature of the brands of the merged entities. The Authority reasoned:16

“In addition, it has been determined that the Telfort brand is complementary to the existing KPN brands because it is specifically aimed at a market segment in which KPN is traditionally not strongly present. Telfort is mainly active in the cost-aware segment of the market with high competitive prices and has relatively more pre-paid customers. The KPN Mobile brand predominantly aims at the ‘upper part’ of the market and the more conservative, traditional market segment.”

The Venn diagram in Figure 5 below illustrates, conceptually, the minimal nature of any competitive overlap between the postpaid brands of CSL and NWPCS given their focus on different customer demographics and market segments.

[CONFIDENTIAL]

16 Case: 5104/KPN-Telfort, at para 59.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

28

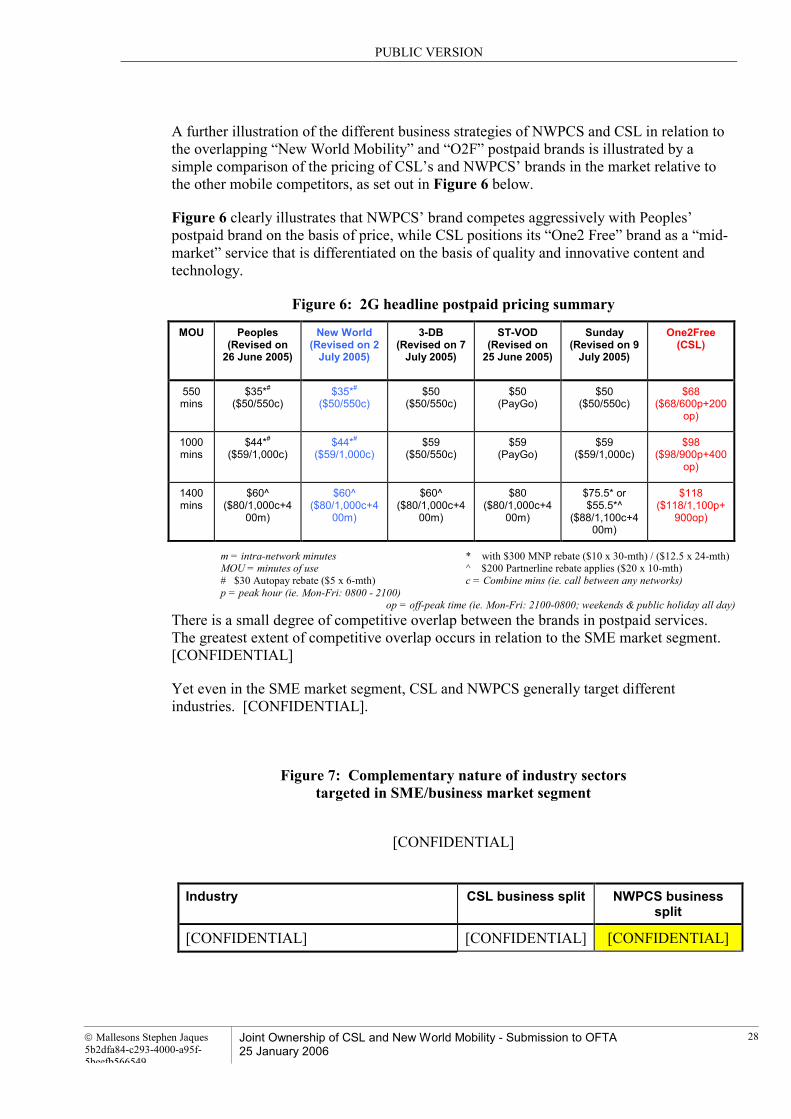

A further illustration of the different business strategies of NWPCS and CSL in relation to the overlapping “New World Mobility” and “O2F” postpaid brands is illustrated by a simple comparison of the pricing of CSL’s and NWPCS’ brands in the market relative to the other mobile competitors, as set out in Figure 6 below.

Figure 6 clearly illustrates that NWPCS’ brand competes aggressively with Peoples’ postpaid brand on the basis of price, while CSL positions its “One2 Free” brand as a “mid-market” service that is differentiated on the basis of quality and innovative content and technology.

Figure 6: 2G headline postpaid pricing summary

MOU Peoples (Revised on 26 June 2005)

New World (Revised on 2 July 2005)

3-DB (Revised on 7 July 2005)

ST-VOD (Revised on 25 June 2005)

Sunday (Revised on 9 July 2005)

One2Free (CSL)

550 mins

$35*# ($50/550c)

$35*# ($50/550c)

$50 ($50/550c)

$50 (PayGo)

$50 ($50/550c)

$68 ($68/600p+200

op)

1000 mins

$44*# ($59/1,000c)

$44*# ($59/1,000c)

$59 ($50/550c)

$59 (PayGo)

$59 ($59/1,000c)

$98 ($98/900p+400

op)

1400 mins

$60^ ($80/1,000c+4

00m)

$60^ ($80/1,000c+4

00m)

$60^ ($80/1,000c+4

00m)

$80 ($80/1,000c+4

00m)

$75.5* or $55.5*^

($88/1,100c+400m)

$118 ($118/1,100p+

900op)

m = intra-network minutes * with $300 MNP rebate ($10 x 30-mth) / ($12.5 x 24-mth) MOU = minutes of use ^ $200 Partnerline rebate applies ($20 x 10-mth) # $30 Autopay rebate ($5 x 6-mth) c = Combine mins (ie. call between any networks) p = peak hour (ie. Mon-Fri: 0800 - 2100)

op = off-peak time (ie. Mon-Fri: 2100-0800; weekends & public holiday all day)

There is a small degree of competitive overlap between the brands in postpaid services. The greatest extent of competitive overlap occurs in relation to the SME market segment. [CONFIDENTIAL]

Yet even in the SME market segment, CSL and NWPCS generally target different industries. [CONFIDENTIAL].

Figure 7: Complementary nature of industry sectors

targeted in SME/business market segment

[CONFIDENTIAL]

Industry CSL business split NWPCS business split

[CONFIDENTIAL] [CONFIDENTIAL] [CONFIDENTIAL]

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

29

Industry CSL business split NWPCS business split

[CONFIDENTIAL] [CONFIDENTIAL] [CONFIDENTIAL]

[CONFIDENTIAL] [CONFIDENTIAL] [CONFIDENTIAL]

[CONFIDENTIAL] [CONFIDENTIAL] [CONFIDENTIAL]

[CONFIDENTIAL] [CONFIDENTIAL] [CONFIDENTIAL]

[CONFIDENTIAL] [CONFIDENTIAL] [CONFIDENTIAL]

TOTALS 100% 100%

7.5 Minimal overlap of prepaid businesses of CSL and NWPCS

Given that the prepaid market segment is relatively homogeneous, there is a degree of competition between CSL and NWPCS in that market segment.

[CONFIDENTIAL]

Furthermore, CSL and NWPCS are not direct head-to-head competitors in the prepaid market segment, [CONFIDENTIAL]:

Figure 8: Complementary nature of operations in prepaid market

Feature NWPCS CSL

Price leadership [CONFIDENTIAL] [CONFIDENTIAL]

Business focus [CONFIDENTIAL] [CONFIDENTIAL]

Nature of operations [CONFIDENTIAL] [CONFIDENTIAL]

In this manner, [CONFIDENTIAL]. CSL’s business focus is largely on the postpaid, rather than prepaid market.

In contrast, [CONFIDENTIAL]. NWPCS has developed a number of products and services to assist it to gain market share, including products specifically targeted at youth end of the market.

7.6 Post Transaction brand strategy

[CONFIDENTIAL]

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

30

8 Constraint from Competitors

8.1 Recognised intensity of competition

The Hong Kong mobile telephony market is internationally recognised as one of the most competitive mobile telephony markets in the world. The Economist Intelligence Unit published a report on Hong Kong in October 2004 which included the following independent analysis of the level of competition:17

“Hong Kong’s mobile-telephone industry is already the world’s most competitive—with six operators fighting for a stake in a population of 7m... Price competition among the six mobile operators has been intense, and by June 2004 there were 7.6m mobile service subscribers, representing a penetration rate of 111.5%”

A recent Gartner report, titled Wireless Services and Service Providers in Hong Kong, dated 13 July 2005 confirms the intensity of competition. Gartner comments:18

“The Hong Kong mobile and wireless market, with a penetration of 120 percent (December 2004) and six mobile operators, is one of the most competitive markets in the region. This means every man, woman and child, in theory, has a mobile phone. In practice, the multiple use of prepaid subscriber identity module (SIM) cards and of prepaid replacement means that the figures are inflated, but the market is still virtually as penetrated as it can get ...”

“The Hong Kong operators have long engaged in a price war, which intensified after the launch of 3G services. With the entry of a fourth operator, it will continue. This price war has lead to an increase in churn, which declined from 2000 to 2003, climbed again in 2004 and will continue to climb during the next two years. Churn will remain a problem, given the inherent volatility in the market because of competitive pressures, price war promotions and handset subsidies.”

“Competition is expected to intensify as operators with 3G networks compete for customers.”

The TA himself has acknowledged the intensity of competition in the Hong Kong mobile market. In the TA’s Report on the Competition Impact of the Acquisition of Shares in Sunday by PCCW, the TA relevantly commented (at paragraph 6.23):

“Moreover, even if PCCW were able to have entered the mobile market using a newly created licence or as an MVNO and therefore increase the number of competitors by one, it is difficult to see how its entry could significantly improve the generally acknowledged intense competition between the 6 pre-existing mobile phone operators and 7 current MVNOs.”

The level of competition in the Hong Kong market is further intensified by the following salient market characteristics:

• Mobile number portability reduces barriers to churn: Mobile number portability (“MNP”) was introduced into the Hong Kong mobile market in March 1999, further intensifying the level of mobile competition. MNP removes barriers to

17 Economist Intelligence Unit Executive Briefing: Hong Kong, 1 October 2004,

http://eb.eiu.com/index.asp?layout=oneclick&country_id=1560000156 18 Gartner Wireless Services and Service Providers in Hong Kong, ID Number G00129225, 13 July 2005,

pp 4, 8 and 9.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

31

customers migrating between mobile operators associated with the inherent “stickiness” of telephone numbers. Churn is unusually high in the Hong Kong market relative to other markets. Furthermore, Hong Kong consumers tend to be more willing to adopt new technologies, respond to new consumer brands, and pro-actively take advantage of price differences.

By way of example, an estimated five million mobile customers in Hong Kong ported between March 1999 to January 2003, with the average number of ports per month being around 110,000.19

• Low barriers to entry for MVNOs and MVARs: This market characteristic is considered in greater detail in Section 10 of this submission.

• Advent of 3G services: 3G has shifted the dynamics of the market by strengthening the long-term competitive position of the operators with 3G licences (Hutchison, CSL, SmarTone-Vodafone, and Sunday-PCCW) as against those without 3G licences (NWPCS, Peoples-China Mobile). 3G services are also acting as an accelerant to mobile competition, boosting an already significantly overheated competitive market.

• Level of advertising: The significant rivalry among the mobile competitors is demonstrated by frequent media advertising blitzes and the high level of brand knowledge in the market. Consumers are keenly aware of alternative mobile operators and their ability to switch providers.

8.2 Competition from network competitors

As at December 2005, there are six network-based mobile telephony competitors in the Hong Kong market. The mobile networks are as follows:

• 2G networks: The six mobile operators hold a total of ten 2G licences. In 2004, the TA granted a “right of first refusal” that will give the licensees a further licence period of up to 15 years.20 Three operators hold both GSM 800MHz and GSM 1800MHz licences and supply dualband GSM services, namely Hutchison, CSL and SmarTone-Vodafone. NWPCS, Peoples-China Mobile and Sunday-PCCW operate GSM 1800MHz networks. There is also one CDMA 800MHz network operated by Hutchison.

• 2.5G networks: All six network operators have deployed 2.5G services.

• 3G networks: Hutchison, CSL, SmarTone-Vodafone and Sunday-PCCW each hold 3G licences. Hutchison launched Hong Kong's first 3G service in January 2004. CSL and SmarTone-Vodafone have also launched 3G services. Sunday-PCCW launched its 3G network with a data card service in June 2005. The 3G

19 Jackie Cooper and Marta Munoz Mendez-Villamil, The impact of MNP in Asia-Pacific, Ovum, June

2004. This trend continues with the average number of ports per month during the six months to October 2005 being 112,947 :http://222.ofta.gov.hk/en/mnp/mnp-statistics.html.

20 Statement of the Telecommunications Authority, “Licensing of Mobile Services on Expiry of Existing Licences for Second Generation Mobile Services”, 29 November 2004.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

32

market was predicted to exceed 500,000 subscribers by the end of 2005,21 but, according to statistics released by OFTA, the 3G market actually exceeded that figure in September 2005.22

8.3 Competition from Hutchison

Hutchison is currently the largest mobile operator in the Hong Kong telephony market with a market share estimated at 26.4%.23 Hutchison offers “3” brand mobile services over its dualband GSM/PCS and CDMA networks and over its 3G WCDMA network.

Hutchison is a particularly strong and spirited competitor in the mobile market at all levels. Of particular relevance:

• Multinational power and global scale of operations: As OFTA will also be aware, Hutchison Whampoa Limited is one of the largest companies listed on the Hong Kong Stock Exchange and, relevantly, it has a 70% shareholding in Hutchison Telecommunications International Limited. The company has interests in Hong Kong, Asia, Europe, Australasia, the Middle East and South America. Hutchison has the ability to leverage from its relationships in other markets to gain or retain business in Hong Kong.

• A major 3G mobile operator and economies of scope and scale: Specialising in mobile communications, Hutchison is one of the world’s largest 3G mobile operators. Hutchison has invested billions of dollars acquiring 3G licences and has built and operated 3G networks in Hong Kong, Europe, Australasia and Israel. Hutchison can use this association and learning to its advantage and can also draw from economies of scope and scale.

• Greatest number of retail outlets: Hutchinson operates the largest group of wholly-owned sales outlets in Hong Kong (equal to Peoples), giving it a strong distribution network.

• First-mover advantage and global procurement power: Given the scale of Hutchison’s global 3G operations and its extensive specialist international experience in 3G services, Hutchison is a strong competitor. Hutchison has been in a unique position to obtain a “first mover” advantage in relation to 3G content and handset arrangements, leveraging from its global procurement power.

• Aggressive 3G pricing to drive consumer take-up: Hutchison aggressively launched 3G services in the marketplace under its “3” brand in Hong Kong in January 2004. Since launch the service has been marked by heavily discounted introductory prices, very low tariffs and high handset subsidies. The 3G handsets are therefore price competitive with most 2G and 2.5G handsets, driving rapid take-up by consumers.

21 Ibid, para 4.6.2. 22 Key Statistics for Telecommunications in Hong Kong: Wireless Statistics (25 November 2005)

http:/www.ofta.gov.hk/en/datastat/eng_wireless.pdf 23 All Hong Kong mobiles market share estimates in this submission are calculated as at 30 June 2005 on

the basis identified in section 9 of this submission.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

33

• Distribution channel and scope for bundling: The Hutchison group owns many properties, providing a distribution channel to ensure easy access to customers. Hutchison also has considerable scope and ability to leverage from its other operations in property development and investment, ports and related services, retail and manufacturing, telecommunications, e-commerce, infrastructure and energy. Similarly, Hutchison also has the ability to bundle mobile telephony with its fixed-line communications, Internet and e-commerce services businesses.

Further information on Hutchison is set out at the following URL:

• http://www.htil.com.hk/eng/global/home.php (English)

8.4 Competition from Peoples Telephone Co and China Mobile

Peoples is currently the fourth largest mobile operator in the Hong Kong telephony market with a market share estimated at 14.4%. Peoples typically offers no-frills services with the simplest tariff structure with no monthly fee.

• Price leadership: Peoples is a very strong and aggressive competitor that competes largely on the basis of price and is often a price leader. Peoples is known for offering heavily discounted tariffs that undercut other pricing in the market in order to successfully win market share.

• Potential low cost 3G MVNO competitor: Peoples does not hold a 3G licence, so is a potential candidate to be the first MVNO offering 3G services in Hong Kong. By avoiding a costly investment in 3G infrastructure, Peoples may become a stronger and low cost competitor relative to the other 3G mobile operators. Peoples already has good cost control and a focused strategy in its 2G business.

• Greatest number of retail outlets: Peoples operates the largest group of wholly-owned sales outlets in Hong Kong (equivalent to Hutchison), giving it a strong distribution network.

• China Mobile entry: As OFTA is aware, on 20 October 2005, China Mobile (Hong Kong) Ltd (“CMHK”) and Peoples jointly announced that CMHK’s wholly-owned subsidiary, Fit Best Limited, will make voluntary conditional cash offers to acquire all the issued shares in the share capital of Peoples, and for the cancellation of outstanding employee share options of Peoples.

CMHK has indicated that should it receive acceptances of more than 90% of the disinterested shares in Peoples, CMHK would exercise its compulsory acquisition rights. CMHK’s acquisition will further increase the competitive tension in the Hong Kong mobile market.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

34

China Mobile is the world’s largest mobile operator by subscriber numbers and has an estimated market share of around 65.5% of the mainland Chinese mobile market, giving it an extremely powerful brand.24

The Applicants have not incorporated further information relating to Peoples into this submission given that OFTA is currently considering CMHK’s acquisition of Peoples, so will already have access to extensive information on Peoples’ current and future competitive strategies.

Further information on Peoples and China Mobile is set out at the following URLs:

• http://www.peoples.com.hk/ (English/Chinese)

• http://www.chinamobilehk.com/ (English/Chinese)

8.5 Competition from SmarTone-Vodafone

SmarTone-Vodafone is the fifth largest mobile operator in the Hong Kong telephony market with a market share estimated at 12.07%. In December 2004, SmarTone-Vodafone launched its commercial 3G service with a high-speed WCDMA/GPRS data card targeted at business executives and professionals.

• Alliance with Vodafone providing global power: SmarTone-Vodafone has formed an alliance with Vodafone, the world’s largest mobile operator by revenue. The alliance with Vodafone gives SmarTone-Vodafone a significant competitive edge in terms of offering international content to its subscribers via the powerful Vodafone Live brand and content. SmarTone-Vodafone also has access to Vodafone’s global handset procurement arrangements.

• Highly aggressive competitor and price leader: An example of the aggressiveness of SmarTone as a competitor is illustrated by SmarTone’s “we will match any offer” strategy in early 2003, triggering a large scale price war. SmarTone promised that it would match any new tariffs from its competitors under its PayGo call plan. As well as very low call plans, PayGo offered free intra-network SMS, free caller number display and free voicemail for 12 months. In a December 2003 press release, SmarTone said airtime usage had increased 40% due to the PayGo service.

More recently, in June 2005, SmarTone reduced prices at the value focussed of the market, taking the cost of 1000 minutes to $59.

• Innovative bundled 3G offering: SmarTone-Vodafone has rolled out 3G services with innovative bundled offerings. Vodafone has already rolled out numerous 3G networks throughout the world, enabling SmarTone-Vodafone to leverage from this existing experience.

Further information on SmarTone-Vodafone is set out at the following URLs:

24 XJ Wang, "China's 3G licence award: impact on the local market", Ovum 6, December 2005.

PUBLIC VERSION

Mallesons Stephen Jaques 5b2dfa84-c293-4000-a95f-5beefb566549

Joint Ownership of CSL and New World Mobility - Submission to OFTA 25 January 2006

35

• http://www.smartone-vodafone.com.hk/jsp/english/index.jsp (English)

• http://www.smartone-vodafone.com.hk/jsp/tchinese/index.jsp (Chinese)

8.6 Competition from Sunday and PCCW