tech insight: utility ownership of rooftop solar

TRANSCRIPT

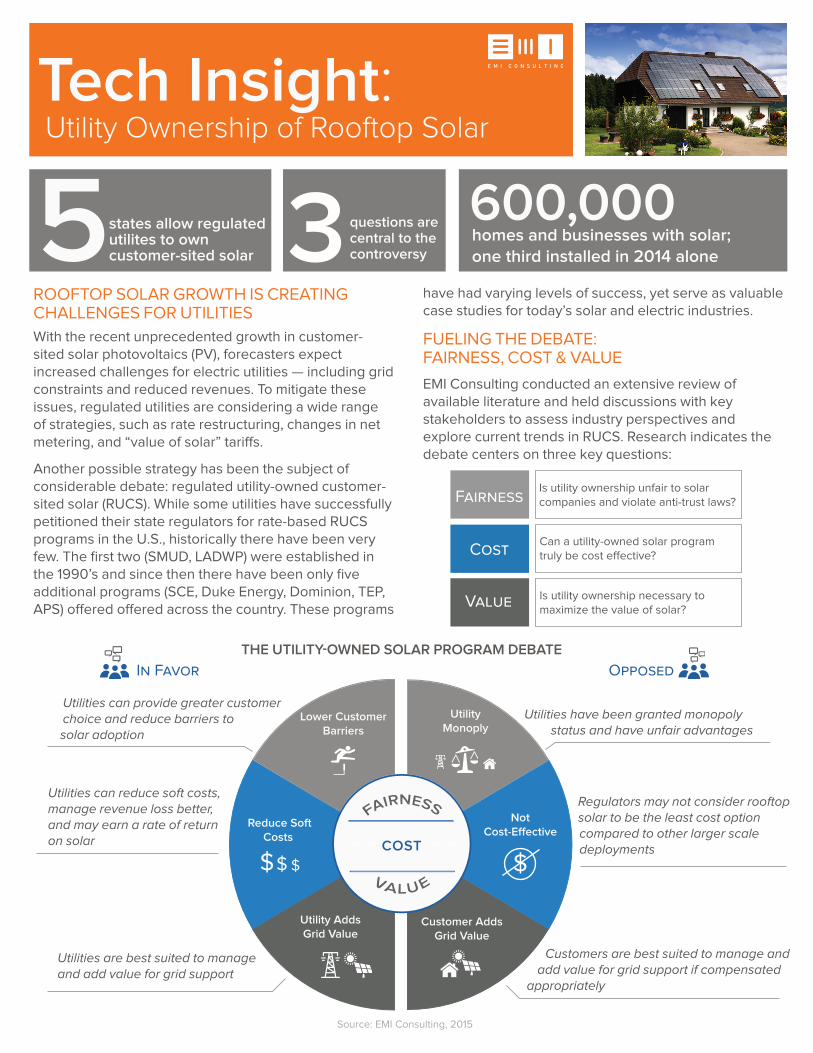

THE UTILITY-OWNED SOLAR PROGRAM DEBATE

Lower Customer Barriers

Utility Monoply

Not Cost-E�ective

Customer Adds Grid Value

Utility AddsGrid Value

Reduce Soft Costs

$$$ $

Utility-Owned Solar Program Debate

FAVOR OPPOSED

COST

FAIRNESSIs utility ownership unfair to solar companies and violate anti-trust laws?

COSTCan a utility-owned solar program truly be cost e�ective?

VALUE Is utility ownership necessary to maximize the value of solar?

ROOFTOP SOLAR GROWTH IS CREATING CHALLENGES FOR UTILITIES

With the recent unprecedented growth in customer-sited solar photovoltaics (PV), forecasters expect increased challenges for electric utilities — including grid constraints and reduced revenues. To mitigate these issues, regulated utilities are considering a wide range of strategies, such as rate restructuring, changes in net metering, and “value of solar” tari� s.

Another possible strategy has been the subject of considerable debate: regulated utility-owned customer-sited solar (RUCS). While some utilities have successfully petitioned their state regulators for rate-based RUCS programs in the U.S., historically there have been very few. The fi rst two (SMUD, LADWP) were established in the 1990’s and since then there have been only fi ve additional programs (SCE, Duke Energy, Dominion, TEP, APS) o� ered o� ered across the country. These programs

have had varying levels of success, yet serve as valuable case studies for today’s solar and electric industries.

FUELING THE DEBATE: FAIRNESS, COST & VALUE

EMI Consulting conducted an extensive review of available literature and held discussions with key stakeholders to assess industry perspectives and explore current trends in RUCS. Research indicates the debate centers on three key questions:

Utilities have been granted monopoly status and have unfair advantages

Utilities can provide greater customer choice and reduce barriers to solar adoption

Utilities can reduce soft costs, manage revenue loss better, and may earn a rate of return on solar

Regulators may not consider rooftop solar to be the least cost option compared to other larger scale deployments

Utilities are best suited to manage and add value for grid support

Customers are best suited to manage and add value for grid support if compensated

appropriately

OPPOSED IN FAVOR

Source: EMI Consulting, 2015

states allow regulated utilites to own customer-sited solar

homes and businesses with solar; one third installed in 2014 alone

questions are central to the controversy35

600,000

Tech Insight: Utility Ownership of Rooftop Solar

LIMITATIONS & LEGAL QUESTIONS

To date, regulators have limited the scope of RUCS programs to either serve low-income and less credit worthy customers or to provide electric grid benefi ts. In many states, neither state legislators nor public utility commissions have addressed the regulatory status of RUCS, and the legal status remains unknown or unspecifi ed.

States in which third-party owners participate in the solar market could potentially become regulatory battlegrounds. As more utilities consider this business model, it is likely that this topic will pervade regulatory proceedings.

HOW SHOULD UTITILITIES, REGULATORS & THE SOLAR INDUSTRY PROCEED?

As the number of distributed solar installations increases, so will the national conversation surrounding RUCS. There are valid points from both perspectives regarding regulated utilities developing customer-sited solar programs. EMI Consulting found there is limited information regarding the true costs and benefi ts of pursuing this business model.

Moving forward, utilities and policymakers alike will need to fully comprehend the implications on fairness, cost, and value resulting from the RUCS model. A better understanding of the regulatory, political, and market conditions of RUCS is critical to determine if ownership of rooftop solar is an economical and justifi able resource to explore.

For more information on how EMI Consulting can help bring clarity on this or other issues, please contact us.

*Refers to regulated utilities only. Some states have public or municipal utilities with utility-owned customer-sited solar programs.

CURRENT U.S. REGULATORY LANDSCAPE FOR UTILITY-OWNED SOLAR

Copyright © Free Vector Maps.com

Ownership Allowed

Ownership Not Allowed

Status Unknown/Unspecified*

Pending Legislation

TPO Allowed

TPO not Allowed

Source: EMI Consulting, 2015

www.emiconsulting.com (206) 621-1160 [email protected] 83 Columbia Street, Suite 400 Seattle, WA 98104

CREATIVELY ENGINEERING THE ENERGY FUTUREThe EMI Consulting Engineering Analysis and Technology Assessment team mission is to apply our unique engineering talents to help expand clients’ clean energy and e� ciency resources.

Michael Kerstin SeanErica Dave Andrea Jess