teachers' retirement system of the state of kentucky · teachers’ retirement system of the...

TRANSCRIPT

A Component Unit of the Commonwealth of KentuckyFiscal Years Ended June 30, 2017 and 2016

Teachers’ Retirement Systemof the State of Kentucky

479 Versailles RoadFrankfort, Kentucky 40601-3800

This report was prepared by theTeachers' Retirement System staff.

Teachers' Retirement Systemof the State of Kentucky

GARY L. HARBIN, CPAExecutive Secretary

The 77th ComprehensiveAnnual Financial Report

ii Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

TABLE OF CONTENTS

~ INTRODUCTORY SECTION ~

Chair’s Letter ............................................................................................................................. 2Letter of Transmittal ................................................................................................................. 3Board of Trustees ....................................................................................................................... 9Administrative Staff and Professional Consultants .......................................................... 10Organizational Chart .............................................................................................................. 11GFOA Certificate of Achievement ........................................................................................ 12PPCC Achievement Award .................................................................................................... 13

~ FINANCIAL SECTION ~Independent Auditor’s Report ............................................................................................... 16Management’s Discussion & Analysis ................................................................................. 18Basic Financial Statements

Statement of Fiduciary Net Position ................................................................................ 22Statement of Changes in Fiduciary Net Position .......................................................... 24Combining Statement of Fiduciary Net Position - Other Funds ................................ 26Combining Statement of Changes in Fiduciary Net Position - Other Funds ........... 27Notes to Financial Statements .......................................................................................... 29

Required Supplemental InformationSchedule of Changes in the Net Pension Liability ........................................................ 59Schedule of Net Pension Liability .................................................................................... 60Schedule of Employer Contributions ............................................................................... 60Schedule of Changes in the Net OPEB Liability – Medical Insurance Plan ............. 62Schedule of Net OPEB Liability – Medical Insurance Plan ......................................... 63Schedule of Employer Contributions – Medical Insurance Plan ............................... 63Schedule of Investment Returns – Health Insurance Trust ........................................ 64Schedule of Changes in the Net OPEB Liability – Life Insurance Plan ..................... 64Schedule of Net OPEB Liability – Life Insurance Plan ................................................. 65Schedule of Employer Contributions – Life Insurance Plan ....................................... 65Schedule of Investment Returns – Life Insurance Trust .............................................. 66

Additional Supporting SchedulesSchedule of Administrative Expenses ............................................................................... 67Schedule of Professional Services and Contracts ............................................................ 67Schedule of Contracted Investment Management Expenses ........................................ 68

~ INVESTMENT SECTION ~Report on Investment Activity ................................................................................................ 74Consultant Letter ........................................................................................................................ 75Retirement Annuity Trust Fund

Investment Policy Summary and Objectives ................................................................. 76Risk Controls ........................................................................................................................ 76Asset Allocation ................................................................................................................... 76Distribution of Investments .............................................................................................. 78Strategic Weightings by Asset Class ................................................................................ 79Portfolio Returns .................................................................................................................. 79Fixed Income Investments ................................................................................................. 81Equity Investments ............................................................................................................. 82Real Estate Investments ..................................................................................................... 85

TABLE OF CONTENTS

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 iii

TABLE OF CONTENTS

Alternative Assets ............................................................................................................... 86Portfolios Fair Values .......................................................................................................... 89Investment Summary ......................................................................................................... 90Contracted Investment Management Expenses ............................................................ 90Ten Largest Stock Holdings ............................................................................................... 92Top Ten Fixed Income Holdings ....................................................................................... 92Transaction Commissions .................................................................................................. 93Proxy Voting and Corporate Behavior ............................................................................ 95Security Lending .................................................................................................................. 95Kentucky Investments ........................................................................................................ 95Professional Service Providers .......................................................................................... 96

Health Insurance Trust FundInvestment Policy and Objectives .................................................................................... 97Risk Controls ........................................................................................................................ 97Asset Allocation ................................................................................................................... 98Distribution of Investments .............................................................................................. 98Portfolio Returns .................................................................................................................. 99Portfolios Fair Values ........................................................................................................ 100Investment Summary ....................................................................................................... 100Contracted Investment Management Expenses .......................................................... 101Schedule of Contracted and Administrative Investment Expenses .......................... 101Professional Service Providers ........................................................................................ 102

~ ACTUARIAL SECTIONS ~Actuarial Annual Valuation

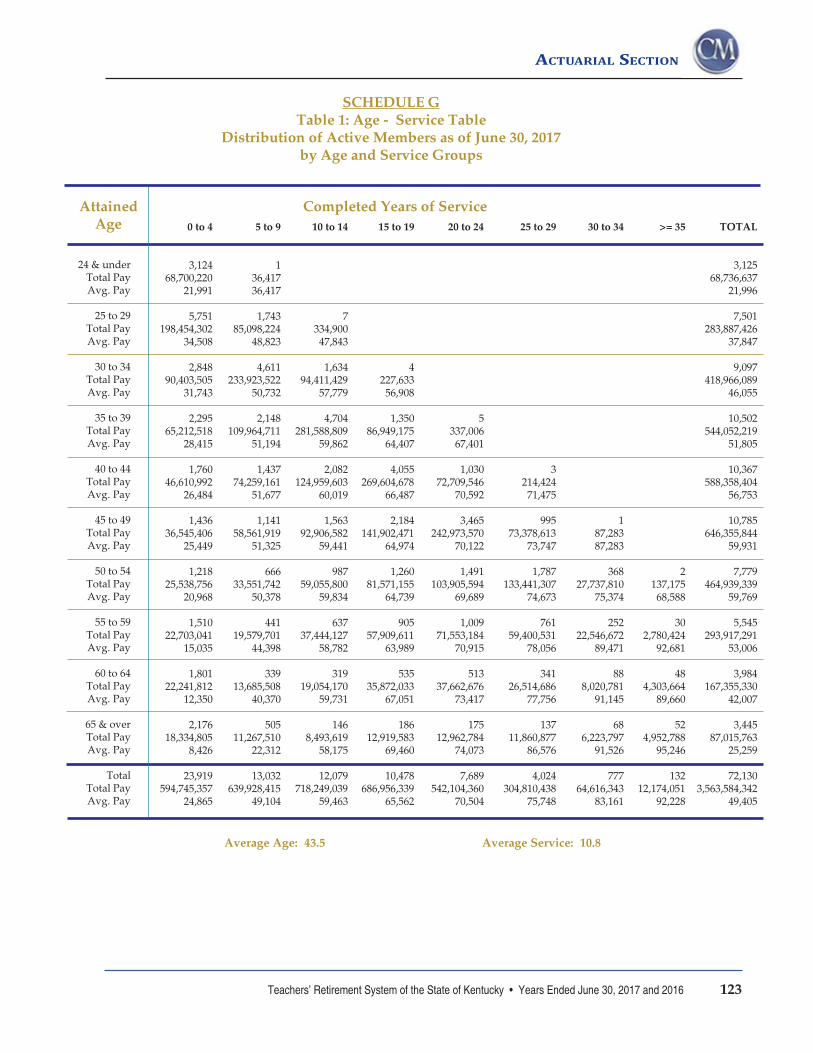

Actuary’s Certification Letter ......................................................................................... 104Summary of Principal Results ......................................................................................... 106Membership Data .............................................................................................................. 108Assets ................................................................................................................................... 109Comments on Valuation .................................................................................................. 109Contributions Payable Under the System ..................................................................... 109Comments on Level of Funding ...................................................................................... 111Analysis of Financial Experience .................................................................................... 113Accounting Information .................................................................................................. 113Valuation Balance Sheet .................................................................................................. 115Solvency Test ...................................................................................................................... 116Development of Actuarial Value of Assets .................................................................. 116Summary of Receipts and Disbursements ..................................................................... 117Outline of Actuarial Assumptions and Methods ......................................................... 118Actuarial Cost Method ...................................................................................................... 120Summary of Main System Provisions as Interpreted for Valuation Purposes ....... 120Table of Distribution of Active Members ...................................................................... 123

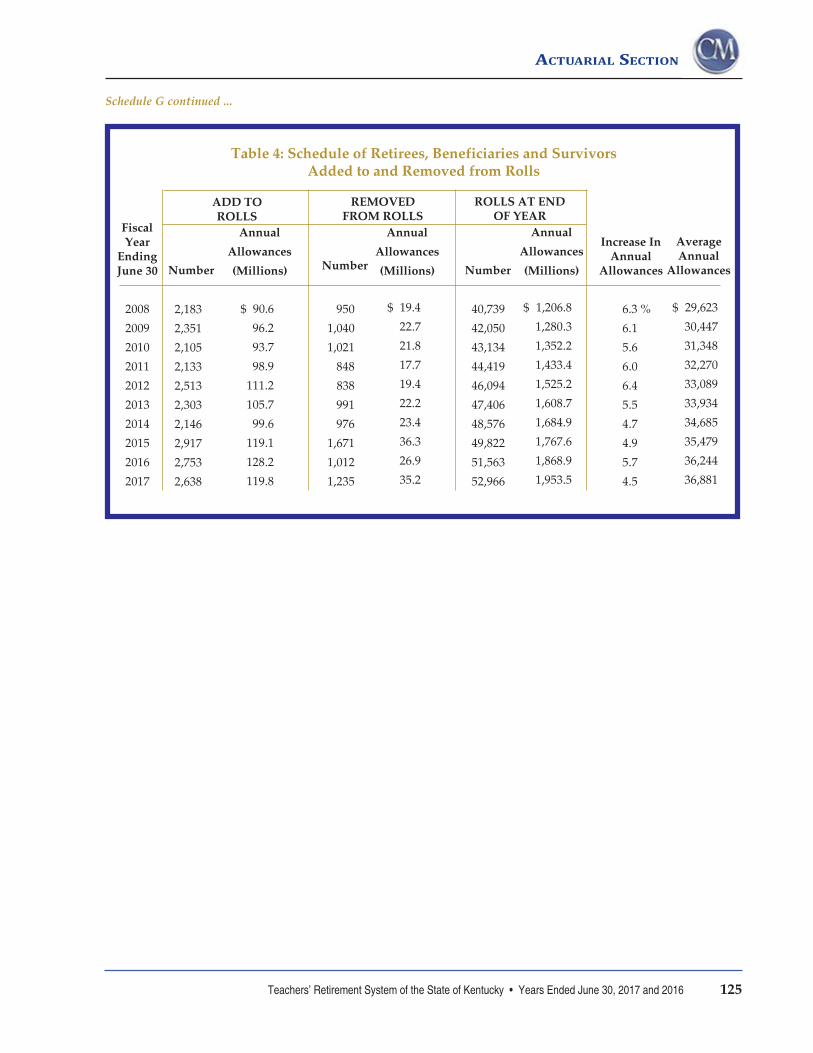

Table of Active Member Valuation Data ....................................................................... 124Table of Number of Retired Members, Beneficiaries and their Benefits by Age .... 124Table of Retirees, Beneficiaries, and Survivors Added to and Removed from Rolls ......................................................................... 125Board Funding Policy.......................................................................................................... 126Sensitivity Analysis ............................................................................................................. 127

iv Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

TABLE OF CONTENTS

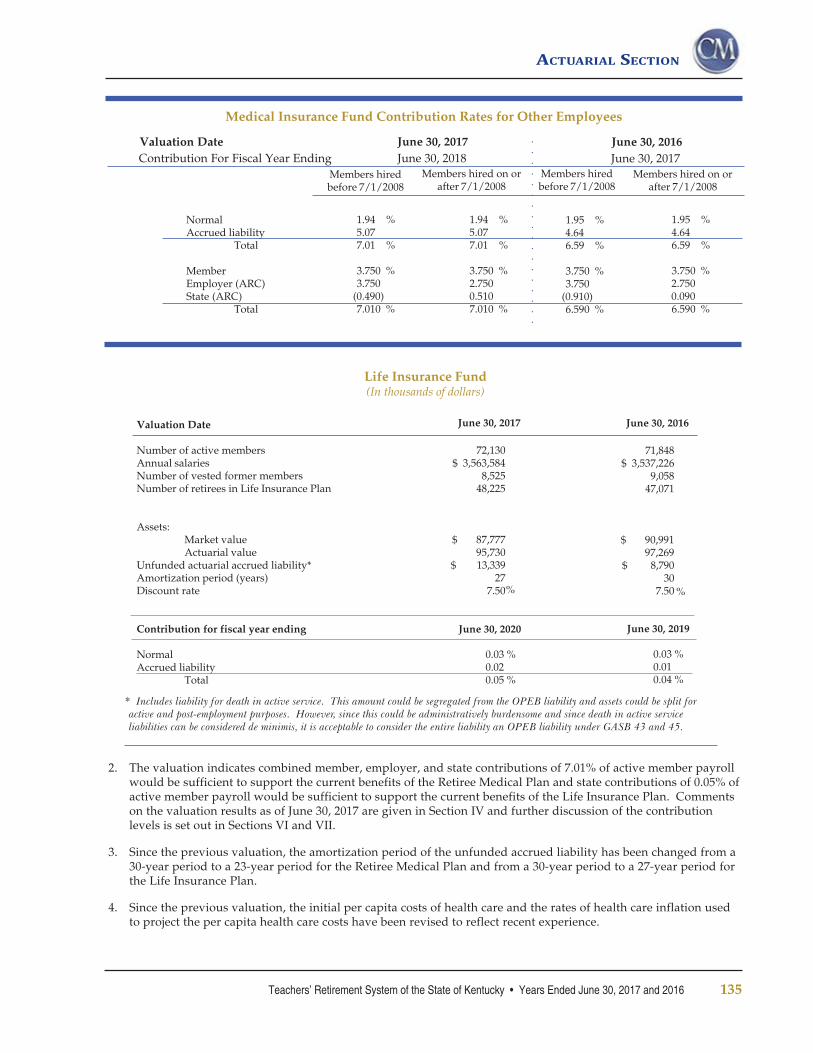

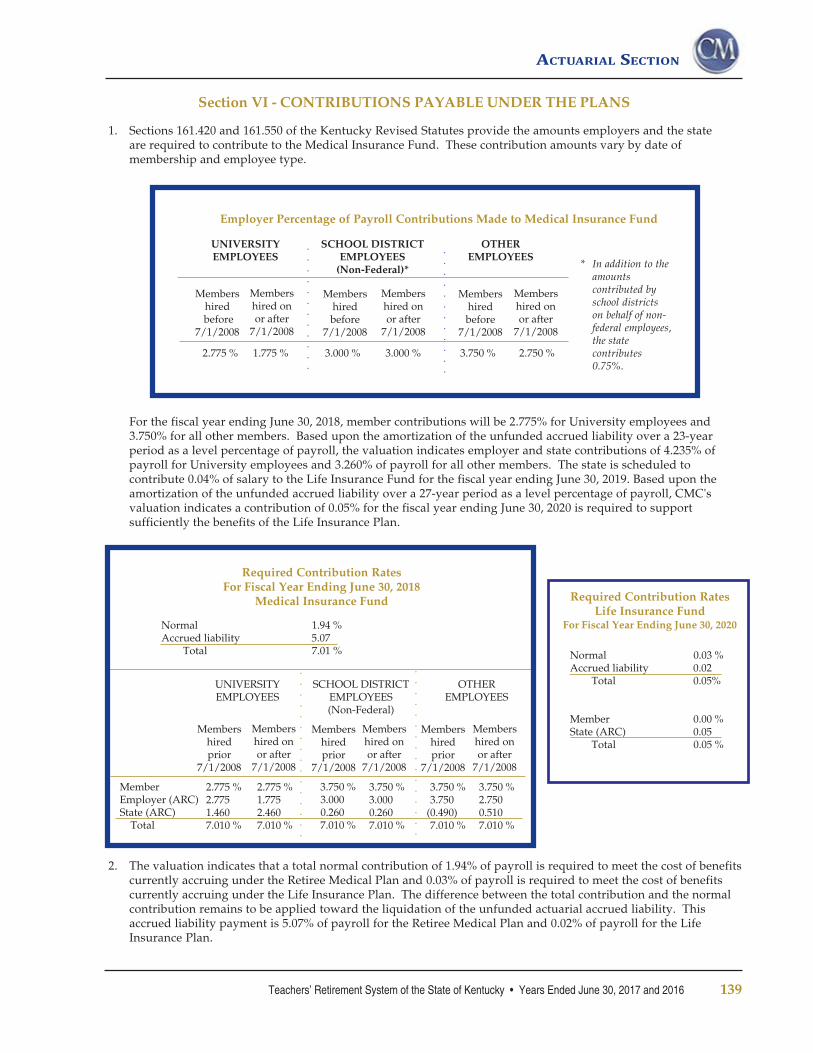

Actuarial Medical and Life Insurance ValuationActuary’s Certification Letter .......................................................................................... 132Summary of Principal Results .......................................................................................... 134Membership Data ............................................................................................................... 136Assets .................................................................................................................................... 137Comments on Valuation ................................................................................................... 137Derivation of Experience Gains and Losses .................................................................. 138Contributions Payable Under the Plans ......................................................................... 139Comments on Level of Funding ....................................................................................... 140Accounting Information ................................................................................................... 140Schedule of Funding Progress .......................................................................................... 141Schedule of Employer Contributions .............................................................................. 142Results of Valuation ........................................................................................................... 145Solvency Test ....................................................................................................................... 145Development of the Actuarial Value of Assets ............................................................ 146Summary of Receipts and Disbursements ..................................................................... 148Statement of Actuarial Assumptions and Methods .................................................... 149Summary of Main Plan Provisions as Interpreted for Valuation Purposes ............ 154Table of Distribution of Active Members ...................................................................... 158Table of Total Active Member Valuation Data ............................................................ 159Table of Eligible Deferred Vested Members .................................................................. 159All Retirees and Spouses Receiving Health Benefits ................................................... 160Table of Retirees, Beneficiaries, and Survivors

Added to and Removed from Rolls .......................................................................... 160Sensitivity Analysis – Medical Insurance Fund ............................................................ 161Sensitivity Analysis – Life Insurance Fund .................................................................... 164

~ STATISTICAL SECTION ~Defined Benefit Plan

Additions by Source ........................................................................................................... 169Deductions by Type ............................................................................................................ 169Changes in Plan Net Position ........................................................................................... 169

Medical Insurance PlanAdditions by Source ........................................................................................................... 170Deductions by Type ............................................................................................................ 170Changes in Plan Net Position ........................................................................................... 170

Life Insurance PlanAdditions by Source ........................................................................................................... 171Deductions by Type ............................................................................................................ 171Changes in Plan Net Position ........................................................................................... 171

Distribution of Active Contributing Members .................................................................. 171Principal Participating Employers ....................................................................................... 172TRS Schedule of Participating Employers .......................................................................... 172Geographical Distribution of Retirement and Medical Payments Worldwide .......... 174Geographical Distribution of Retirement and Medical Payments Statewide ............. 175Growth in Annuitants ............................................................................................................ 176Schedule of Annuitants by Type of Benefit ........................................................................ 176Schedule of Annuitants by Option Selected ....................................................................... 176Defined Benefit Plan Average Benefit Payments for the Past Ten Years ..................... 177Medical Insurance Plan Average Insurance Premium

Supplements for the Last Five Years .............................................................................. 178Summary of Retiree Sick Leave Payments ......................................................................... 179Funding of Additional Payments ......................................................................................... 179

2017

IntroductorySection

Teachers’ Retirement Systemof the State of Kentucky

2 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

INTRODUCTORY SECTION

BOARD OF TRUSTEES RON SANDERSChair, HodgenvilleALISON WRIGHTVice Chair, Georgetown

MARY ADAMSBrodheadJOHN BOARDMANLexington

FRANK COLLECCHIALouisvilleHOLLIS GRITTONUnion

BRENDA MCGOWNBowling GreenLAURA SCHNEIDERWaltonJOSH UNDERWOODTollesboro

ALLISON BALLState TreasurerSTEPHEN PRUITT, Ph.D.Education Commissioner_________________________

GARY L. HARBIN, CPAExecutive Secretary

Chair’s Letter

Teachers’ Retirement Systemof the State of Kentucky

December 18, 2017 Dear Members:On behalf of the Board of Trustees and staff, I am pleased to presentthis Comprehensive Annual Financial Report of the Teachers' RetirementSystem of the State of Kentucky for the year ending June 30, 2017, the 77thyear of operation of the system. The accompanying reports from theindependent auditor and the consulting actuary substantiate the financialintegrity and the actuarial soundness of the system.TRS closed the 2016-2017 fiscal year with $19.8 billion net assets. Theactive membership totaled 72,130 and the retired membership was 52,966with an annual annuity and medical insurance benefits of $2.1 billion.The Board of Trustees is totally committed to managing the retirementsystem funds in a prudent, professional manner. Every effort will be madeto ensure that the system continues to operate in a fiscally sound manner.Present and future members of the system deserve to be able to availthemselves of the best possible retirement as authorized by statute.We appreciate the support and cooperation extended by the governorand the legislature. This cooperation allows the system to not only meetcurrent challenges but to also make timely provisions for the future.The Board of Trustees pledges to continue to administer the affairs ofthe Teachers' Retirement System in the most competent and efficientmanner possible.

Sincerely,Ron SandersChairBoard of Trustees

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 3

INTRODUCTORY SECTION

Teachers’ Retirement Systemof the State of Kentucky

December 18, 2017

Honorable Matthew G. Bevin, GovernorCommonwealth of KentuckyCapitol BuildingFrankfort, Kentucky

Dear Governor Bevin:

It is my pleasure to submit the 77thComprehensive Annual Financial Report of theTeachers' Retirement System of the State ofKentucky (TRS), a component unit of theCommonwealth of Kentucky, for the fiscal yearended June 30, 2017. Allow me to begin again thistransmittal letter with an expression of my thanksfor your work and the work of the GeneralAssembly in approving a biennial budget for thecommonwealth that provides $973 million inadditional funding for TRS. The first year of thatfunding resulted in TRS receiving 99 percent of theactuarially determined employer contribution(ADEC) for the period - a dramatic increase overprior budgets that already is being invested to fulfillthe promise made by the state to teachers. Theimportance of the consistent full funding of theretirement plan for Kentucky's teachers cannot beoverstated.

TRS produced this annual report, which isrequired by state law and contains the annual auditand actuarial valuation of the retirement system,that provides you, the General Assembly and thepublic with information necessary to betterunderstand TRS, which is the largest financialinstitution in the commonwealth. Contained withinare numerous examples of how Kentucky teachers'future well-being is being provided for at a low costwith a great economic benefit for those educatorsand the state's businesses that receive many of theretirement dollars spent by the 89 percent ofretirees who live in Kentucky.

This report conforms with the principles ofgovernmental accounting and generally acceptedaccounting principles. Responsibility for both the

accuracy of the data and the completeness andfairness of the presentation, including alldisclosures, rests with TRS management. To thebest of management's knowledge and belief, theenclosed data is accurate in all material aspectsand reported in a manner designed to presentfairly the financial position and results ofoperations of TRS for the year ended June 30, 2017.Discussion and analysis of net assets and relatedadditions and deductions are presented inManagement's Discussion and Analysis in theFinancial Section of this report.

Management is responsible for maintaining asystem of internal controls to establish reasonableassurance that assets are safeguarded, transactionsare executed accurately and financial statementsare presented fairly. Limits are inherent in allsystems of internal control based on therecognition that the costs of such systems shouldbe related to the benefits to be derived.Management believes the system's controlsprovide this appropriate balance. The system ofinternal controls includes policies and proceduresand an internal audit department that reports tothe Board of Trustees.

Profile of TRS

TRS began operations on July 1, 1940, as a cost-sharing, multiple-employer defined benefit plan.The primary purpose of the plan is to provideretirement annuity plan coverage for local schooldistricts and other public educational agencies inthe state. TRS is a blended component unit of theCommonwealth of Kentucky. The plan is describedin the Notes to Financial Statements in theFinancial Section of this report. Also, the Summaryof Main System Provisions as Interpreted forValuation Purposes in the Actuarial Section, isuseful in understanding benefit and contributionprovisions. The number of TRS active and retiredmembers is contained in the preceding boardchair's letter.

An annual operating budget is prepared for theadministration of the retirement system andapproved by the Board of Trustees. Biennial budgetrequests also are submitted to the GeneralAssembly for adoption. TRS's investment earningspay for the agency's administrative expenses,which are among the lowest of its peers.

During fiscal year 2017, the enactment of SenateBill 2 (2017 RS) expanded the Board of Trustees

Letter of Transmittal

4 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

INTRODUCTORY SECTION

from its longstanding makeup of nine members to11; the additional two members are appointed bythe governor with the requirement that bothappointees have financial experience.

Major Initiatives

The system continually seeks better to serve itsmembership as the highest levels ofprofessionalism, integrity, performance andteamwork are required at all levels of theorganization. TRS is an organization that "does itright." As such, during the past year, TRS hascontinued work on several major initiativesconcerning funding and cost containment forretiree health care, the investment program andinformation technology.

Implementation of the "Shared Responsibility"Solution for Funding Retiree Health Care andCareful Management of Medical Insurance Costs

Kentucky continues to be a national leader inprefunding retiree health care benefits as a resultof the shared responsibility solution enacted in2010 through the collective efforts of the Board ofTrustees, the education community and electedofficials. The plan immediately eliminated $3.1billion in actuarial liability from the retiredteacher health care plan. Combined with othercost control measures, more than $5 billion inactuarial accrued liability has been eliminatedfrom the TRS Medical Insurance Fund. In onlyseven years, the medical insurance fund hasreached 26.7 percent funding compared to pay-as-you-go status before the law took effect. With thesix-year phase-in period having ended in 2016, themedical plan saw a one-year funding ratioincrease in 2017 of 4.8 percentage points. Thisremarkable improvement confirms that themedical insurance fund is on schedule to befunded fully in 23 years. The shared responsibilitysolution is truly a significant accomplishment forthe retirement security of current and futureretired teachers.

TRS is efficient, effective and always working toimprove the retirement security of Kentucky'steachers. The latest such initiative is the additionof a new personalized medicine pilot projectunder TRS's Medicare Eligible Health Plan.Personalized medicine uses DNA testing to help apatient's doctor make more effective treatmentdecisions for better health outcomes. This pilot,which has been months in development and

began in fall 2017, is focused on making sure thata retiree's medications are safe and will bebeneficial. Without this testing, medicines may beprescribed that won't work with a retiree'sindividual physiology (as shown through DNAtesting) and that, in some cases, may be fatal.Coriell Life Sciences, which has been providingclinical research services for more than 64 years,is TRS's partner in the pilot. Besides the healthbenefit to retirees, the pilot is expected to providesignificant cost savings to the plan by reducingadverse drug reactions and the trial-and-errorperiod that some patients see.

The Board of Trustees regularly reviews thehealth care plan to contain costs and maintain ameaningful benefit for retired teachers. The moveto Medicare Advantage, now in the 11th year,continues to be stable and financially feasible forour members and the TRS medical plan. The costof coverage for 2018 is a reduction from the 2017cost.

Some recent cost-saving initiatives includemoving the TRS-sponsored Medicare Part DEmployer Group Waiver drug plan from fullyinsured to a self-funded plan to achieve thegreatest federal subsidies. Additionally, TRS ispart of the Know Your Rx Coalition, which itjoined in 2012. Through the coalition, TRS savesmoney leveraging greater prescription purchasingpower, obtaining deeper drug discounts andincreasing the rate at which prescriptions arefilled with generic drugs from 73 percent to 88percent. Additionally, coalition pharmacists workwith retired teachers and their physicians tomaximize prescription dollars both for the retireeand the medical plan.

Implementation of Senate Bill 2

In June 2017, the board adopted an investmentprocurement policy, which built upon andcentralized existing TRS investing procurementpractices, to comply with the provisions of SB 2.TRS was the first of the state’s retirement systemsto have its policy certified by the secretary of theFinance and Administration Cabinet.Implementation of the other provisions of SB 2continues.

Investment Program

For the fiscal year ended June 30, 2017, themarket value of TRS's investment programincreased a net 15.0 percent for retirement and

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 5

INTRODUCTORY SECTION

14.4 percent for the medical insurance trust pushing total plan assets to a record of $19.9 billion. While a one-year period is not determinative for a long-term investor such as TRS, it should be noted that the gross return of 15.37 percent was among the top 8 percent of public plans with more than $1 billion under management. During the last 10 years, TRS's investment returns rank in the top 9 percent of those plans. Moreover, during the last 30 years, TRS investment returns of 8.18 percent have met the long-term assumed rate of return of 7.5 percent.

A multiyear program of diversifying theportfolio continued in line with TRS's focus onfundamental value and risk control. Theseongoing efforts are a continuation of a disciplinedinvestment process and long-term focus onretirement security. This focus has generatedexceptionally stable returns through the system'shistory, and we have every confidence that it willdo so in the future. TRS's investment programcontinues to be recognized as a leader in thepublic pension community for governancestructure, trustee education and cost effectiveness.

TRS regularly obtains independent reviews andalways is seeking to improve its investmentprogram and continue the tradition of adhering tobest governance practices that lead to soundinvestment returns. For example, with theadditional funding provided in the 2016-18biennial budget, TRS conducted an asset liabilitymodeling study and reviewed actuarialassumptions. The studies confirmed TRS'sapproach and the importance of the consistent fullfunding of the ADEC.

Information Technology

The Pathway information technology systemcontinues to be a success, allowing members toaccess account information online - availableanytime from anywhere. The member self-serviceportal in Pathway, its mobile device applicationand the TRS website continued to be updated. Asite index was added to the website. Staffcurrently is working with the KentuckyDepartment for Libraries and Archives to updateTRS's records retention schedule consistent withPathway's data and document storagecapabilities.

Communications

To reach members more easily, TRS continuedusing Facebook and Twitter accounts tocommunicate information about the system on amore timely basis. In less than two years, theFacebook account has received almost 2,100 likes,and posts often reach more than 1,000 users - ledby 33,239 users who saw a post on the system'sinvestment performance for fiscal year 2017.

Also, TRS revamped and added informationalseminar offerings for members. The new TRS OnThe Road takes place on Saturdays three times peryear in different parts of the state. Additionally,under the direction of the Member Servicesdivision, webinars of popular seminars are beingoffered and videos of popular informationalseminars began being posted to the TRS website.The Insurance division expanded the offerings ofits Turning 65 presentation for retirees about toenroll in the Medicare Eligible Health Plan.

Internal and External Reviews

TRS responds to legislative and administrationinquiries and mandates throughout the year. Inconnection with possible pension reform, TRSreceived - and responded to - numerous requestsfrom legislators, the executive branch, constituentgroups and others to provide accurateinformation about the experience of the system.

Economic Condition

The economic condition of the system is basedprimarily on investment earnings. The InvestmentSection of this report contains asset allocations,strategic target ranges for investments, discussionof the current year market environment andhistorical performance schedules, among others.

As of June 30, 2017, the retirement system'stotal funds reached $19.8 billion in market value.The retirement system's investment performancehas been strong in recent years relative to itspeers. As of June 30, 2017, TRS achieved one-yeargross returns of 15.37 percent with top 8 percentinvestment performance. The fiscal year wascharacterized by increasing global economicgrowth. This favorable environment producedstrong returns for domestic and internationalequities, the system's two largest asset classes.

TRS has beaten the independent investmentconsultant's public fund index in the one-, three-,

6 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

INTRODUCTORY SECTION

five- and 10-year periods, achieving top 9 percentperformance over the 10-year period. This recordvalidates policy changes adopted by the board andimplemented by the Investment Committee overthe last several years. TRS's commitment to bestpractices, stringent risk controls and fundamentalvalue philosophy in investing helps ensure long-term retirement security for Kentucky's teachers.

According to KRS 161.430, the TRS Board ofTrustees is responsible for investing the assets ofthe system. The Board of Trustees delegatesinvestment authority to the InvestmentCommittee. The Investment Committee worksclosely with experienced investment counselorsand the system's professional staff in evaluatingand selecting investment allocations.

The investment objectives of the Board ofTrustees are to ensure that funds shall be investedsolely in the interest of its members and theirbeneficiaries and that investment income shall beused for the exclusive purpose of providingbenefits to the members and their beneficiaries,while making payment of reasonable expenses inadministering the plan and its trust funds. Theinvestment program shall also provide areasonable rate of total return with majoremphasis being placed upon the protection of theinvested assets.

The investment portfolio experienced anincrease in value during the 2016-2017 fiscal yearas the market value went from $17,405,060,831 to$19,433,790,384. The increase in value of theportfolio was the result of favorable marketconditions, additional funding provided by thegovernor and General Assembly for the pensionfund. Interest income, dividends and employerand employee contributions also providedsignificant income to the portfolio.

Net investment income totaled $2,572,143,912for 2016-2017 compared to negative $249,661,104for 2015-2016. The major contributing factor of theincrease in return from the system's investmentportfolio resulted from the net appreciation in fairvalue of investments of $2,254,023,748 at June 30,2017 compared to net depreciation of $598,818,560at June 30, 2016.

As mentioned earlier, it should be noted thatTRS annuities bolster the Commonwealth ofKentucky's economy, as 89 percent of retiredteachers reside within the state. TRS paid morethan $2 billion in total benefits (retirement,medical, etc.) during the fiscal year.

Funding

The first benefits from the additional funding inthe 2016-18 state budget (2016 RS HB 303) wereseen as TRS received 99 percent of the ADEC in thebiennium's initial year.

Based on recommendations of the Board ofTrustees, the General Assembly establishes, bystatute, the contribution levels that are to be madeby members and employers to fund the liabilitiesof the system. Each year, an independent actuaryperforms a valuation to determine whether thecurrent levels of contribution will be sufficient tocover the cost of benefits earned by members.

Since fiscal year 2008, the state has not paid thefull recommended annual employer contributionnecessary to prefund the benefit requirements ofmembers of the retirement system as determinedby the actuary. Over this period, because of notmaking the additional appropriation beyondsalary-based contributions, the actuary says thestate's annual additionally required employercontributions have grown significantly from $60.5million (fiscal year 2009) to $538.3 million (fiscalyear 2020). The following schedule details thegrowth of the additional annual employercontributions payable by the state:

The board always has acted as required by statelaw and recommended annual employercontributions payable by the state that wouldensure that the state meets the contractualobligations to members.

The latest actuarial valuation was for the periodending June 30, 2017. This report reflects the

FiscalYear

200920102011201220132014201520162017201820192020

CumulativeIncreaseas a %

of Payroll

1.882.463.595.817.278.02

10.4212.9713.8013.4914.6114.10

CumulativeIncrease in Annual

Retirement AppropriationsPayable by the State

$ 60,499,80082,331,200

121,457,000208,649,000260,980,000299,420,000386,400,000487,400,000520,372,000512,883,000553,597,000538,253,000

(Source: TRS Report of the Actuary on the Annual ValuationPrepared as of June 30, 2017).

%

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 7

INTRODUCTORY SECTION

system's actuarial value of assets totaling $18.5billion and actuarially determined liabilitiestotaling $32.8 billion. The funded ratio of actuarialassets to liabilities is 56.4 percent, which is anincrease from the previous year and is dueprimarily to market appreciation of investmentsand smoothing of investment returns. The actuaryreports: "In our opinion, the system has not beenfunded on an actuarially sound basis since the fullactuarially determined contributions were notmade by the employer. However, an additionalappropriation of $498.5 million was made duringfiscal year 2017 and an additional appropriation of$474.7 million is expected to be made during fiscalyear 2018. If contributions by the employer to thesystem in subsequent fiscal years are less thanthose required, the assets are expected to becomeinsufficient to pay promised benefits. Assumingthat contributions to the system are made by theemployer from year to year in the future at ratesrecommended on the basis of the successiveactuarial valuations, the continued sufficiency ofthe assets to provide the benefits called for underthe System may be safely anticipated."

Annual required employer contributions for thedefined benefit plan are provided in the Scheduleof Employer Contributions in the RequiredSupplemental Information of the Financial Sectionof this report. Based on the 2017 valuation report,the actuary recommends a cumulative increase inemployer contributions of 14.10 percent of pay forthe 2019-2020 fiscal year as detailed in theContribution Rates tables in the Summary ofPrincipal Results in the Actuarial Section of thisreport.

TRS Medical Insurance Plan

The shared responsibility solution for fundingretiree health care, which went into effect on July1, 2010, provides a method of prefunding retireehealth care over the next 23 years. In only sevenyears, the medical insurance fund has reached 26.7percent funding compared to pay-as-you-go statusbefore the law took effect (with the most recentyear being a gain of 4.8 percentage points). Theresults confirm that the medical insurance fund ison schedule to be funded fully in 23 years and thatthe 2010 solution is working. The sharedresponsibility solution for funding retiree healthcare will help ensure the retirement security of thestate's teachers. An actuarial valuation of theMedical Insurance Plan for the fiscal year endedJune 30, 2017, indicated that the fund has an

unfunded liability of $2.71 billion. Annualrequired employer contributions for the MedicalInsurance Fund are provided in the Schedule ofEmployer Contributions in the RequiredSupplemental Information of the FinancialSection.

The actuary's opinion is: "… if the contributionsto the Medical Insurance Fund (MIF) continue atthe current statutorily required levels, the fundedratio of the Retiree Medical Plan will continue toincrease, and the ability of the MIF to fund thebenefits called for under the Retiree Medical Planwill improve."

Additionally, the system believes continuedsteps must be taken to realize true costcontainment through legislation on both the stateand national levels and TRS will continue takingadvantage of those measures.

Professional Services

Professional consultants are appointed by theBoard of Trustees to perform services that areessential to the effective and efficient operation ofTRS. Certifications from the board's externalauditor and independent actuary are enclosed inthis report. The system's consultants, which areappointed by the board, are listed in theAdditional Supporting Schedules of the FinancialSection and in the Investment Section'sProfessional Service Providers table and HealthInsurance Trust Professional Service Providerstable.

National Recognition

The System was honored by two nationalprofessional organizations in regard to theadministration of the retirement program.

GFOA Certificate of Achievement

The Government Finance Officers Associationof the United States and Canada (GFOA) awardeda Certificate of Achievement for Excellence inFinancial Reporting to the Teachers' RetirementSystem of the State of Kentucky for itsComprehensive Annual Financial Report (CAFR)for the fiscal year ended June 30, 2016. TheCertificate of Achievement is a prestigiousnational award recognizing conformance with thehighest standards for preparation of state andlocal government financial reports.

To be awarded a Certificate of Achievement, agovernment unit must publish an easily readable

8 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

INTRODUCTORY SECTION

and efficiently organized comprehensive annualfinancial report, whose contents conform toprogram standards. Such CAFRs must satisfy bothgenerally accepted accounting principles andapplicable legal requirements.

A Certificate of Achievement is valid for oneyear. TRS has received the Certificate ofAchievement for the last 29 consecutive years(fiscal years ended 1988-2016). TRS believes thecurrent report continues to conform to theCertificate of Achievement program requirements,and is being submitted to GFOA.

PPCC Achievement Award

The Public Pension Coordinating Council (PPCC)awarded a Certificate of Achievement to theTeachers' Retirement System of the State ofKentucky for 2017 for implementing andmaintaining high professional standards inadministering the affairs of the system. The awardis based on compliance with principles judged tounderlie exemplary retirement systemachievements in the areas of benefits, actuarialvaluation, financial reporting, investments anddisclosure. Those principles widely areacknowledged to be marks of excellence in thepublic pension industry.

The PPCC is a coalition of three nationalassociations that represent public retirementsystems and administrators. Combined, theseassociations serve retirement systems that providepension coverage for most of the nation's 16 millionemployees of state and local government. Theassociations that form the PPCC are the NationalAssociation of State Retirement Administrators; theNational Council on Teacher Retirement; and theNational Conference on Public EmployeeRetirement Systems.

NCTR Executive Committee

I am past-president of the National Council onTeacher Retirement (NCTR). NCTR is a national,nonprofit organization with a mission to promoteeffective governance and benefits administration instate and local public pension systems in order thatadequate and secure retirement benefits areprovided to educators and other plan participants.NCTR membership includes 69 state, territorial,local and university pension systems withcombined assets in excess of $2 trillion, servingmore than 18 million active and retired teachers,non-teaching personnel and other publicemployees.

Public Sector HealthCare Roundtable

Additionally, I serve on the Board of Directorsand as president of the Public Sector HealthCareRoundtable. The roundtable is a national coalitionof public sector health care purchasers that wasformed to ensure that the interests of the publicsector are represented properly during theformulation, debate and implementation of federalhealth care policies. Membership in the roundtableis open to any statewide, regional or localgovernmental unit that provides health carecoverage for public employees and retirees.

Acknowledgements

The preparation of this report reflects thecombined efforts of the TRS staff, under theleadership of the Board of Trustees. The report isintended to provide complete and reliableinformation that serves as a basis for makingmanagement decisions and for determiningcompliance with legal provisions. It also is used todetermine responsible stewardship of the assetscontributed by TRS members and their employers.

This report is located at the TRS web addresshttps://trs.ky.gov/financial-reports-information/#CAFR and is made available to all systememployer members, whose cooperation continuesto contribute significantly to TRS's success, andwho form the vital link between TRS and its activemembers.

TRS management and staff are committed to thecontinued operation of an actuarially sound andefficient retirement system. Again, thanks to youand the General Assembly for the additionalbudget funding that is ensuring retirement securityfor teachers. Your support is an essential part ofthis commitment, and we look forward to workingwith you.

Respectfully submitted,

Gary L. Harbin, CPAExecutive Secretary

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 9

INTRODUCTORY SECTION

BOARD OF TRUSTEES

Allison Ball Ex Officio Trustee

State Treasurer

Ron Sanders Chair

Lay Trustee Hodgenville

Alison Wright Vice Chair

Active Teacher Trustee Georgetown

Mary Adams Active Teacher Trustee

Brodhead

Hollis Gritton Lay Trustee

Union

Josh Underwood Active Teacher Trustee

Tollesboro

Stephen Pruitt, Ph.D. Ex Officio Trustee

Commissioner, Dept. of Education

John Boardman Appointed

Trustee Lexington

Frank Collecchia Appointed

Trustee Louisville

Brenda McGown Retired Teacher Trustee

Bowling Green

Laura Schneider Active Teacher Trustee

Walton

10 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

INTRODUCTORY SECTION

Teachers’ Retirement Systemof the State of Kentucky

479 Versailles RoadFrankfort, Kentucky 40601-3800

PROFESSIONAL CONSULTANTS

ACTUARY

Cavanaugh Macdonald Consulting, LLC3550 Busbee Parkway, Suite 250

Kennesaw, GA 30144

AUDITOR

Mountjoy Chilton Medley LLP462 South Fourth Street2600 Meidinger Tower

Louisville, Kentucky 40202

See the Schedules of Contracted Investment Management Expenses, TransactionCommissions and Professional Service Providers in the Investment Section for a list of

investment fees and external asset managers.

ADMINISTRATIVE STAFF

GARY L. HARBIN, CPAExecutive Secretary

ROBERT B. BARNES, JDGeneral Counsel and

Deputy Executive SecretaryOperations

J. ERIC WAMPLER, JDDeputy Executive SecretaryFinance & Administration

TOM SIDEREWICZ, CFAChief Investment Officer

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 11

INTRODUCTORY SECTION

Teachers’ Retirement SystemOrganizational Chart

Board of Trustees

TOM SIDEREWICZ

Chief InvestmentOfficer

Deputy Executive Secretaryof Finance & Administration

Executive Secretary

Chief FinancialOfficer

AdministrativeServices

MemberServices

InvestmentAccounting

Mark E.Whelan

Philip L.Webb

BeckyNiece

GARY L. HARBIN

• PortfolioManagement

• InvestmentTransactions

• PortfolioEvaluation

• AssistInvestmentCommittee

• InterestCollection

• SecuritySettlements

• CustodialServices

• RecordMaintenance

• FinancialReporting &Accounting

• BudgetPreparation &Analysis

• Tax Reporting• Cash Receipts/

Disbursements• Accounts

Payable/Receivable

• EmployerReporting

• Member &GroupCounseling

• Survivor &DeathBenefits

• Disability &ServiceRetirement

• RetirementWaivers & Re-Employment

• On SiteWorkshops

• InformationCenter

• Retiree Returnto WorkCounseling

• MemberAccountMaintenance

• BusinessAnalysis

• ApplicationDevelopment

• ApplicationSupport

• SecurityAdministration

• NetworkInfrastructure

• DatabaseAdministration

• Data Analysis

InformationTechnology

GlennTucker

• RetirementEducationthroughSeminars,Webinars,On-SiteCounseling

• Refunds &PersonalPayments

• Retiree Payroll• Record

Maintenance• Imaging

J. ERIC WAMPLER

Deputy ExecutiveSecretary of Operations

ROBERT B. BARNES

InvestmentManagement

• AdministrativeServices

• BuildingManagement

• Mailroom• Messenger

Services

NATHAN VAN SICKEL

Internal Auditor

ROBERT B. BARNES

General Counsel

RetireeHealth Care

JaneGilbert

MemberBenefits

DebiNewman

• RetireeInsurancePre andPostMedicare

• InsuranceCostContainmentand RiskManagement

• MonitorState andFederalInsuranceLegislation

12 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

INTRODUCTORY SECTION

The Government Finance Officers Association of theUnited States and Canada (GFOA) awarded a Certificate ofAchievement for Excellence in Financial Reporting to theTeachers' Retirement System of the State of Kentucky. TheTRS has received the Certificate of Achievement for the last29 consecutive years (fiscal years ended 1988-2016).

GOVERNMENT FINANCEOFFICERS ASSOCIATION (GFOA)

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 13

INTRODUCTORY SECTION

The Public Pension Coordinating Council awarded a Certificate of Achievementto the Teachers' Retirement System of the State of Kentucky for 2017 forimplementing and maintaining high professional standards in administering theaffairs of the System. The award is based on compliance with principles judged tounderlie exemplary retirement system achievements in the areas of benefits, actuarialvaluation, financial reporting, investments and disclosure and are acknowledgedwidely to be marks of excellence for retirement systems. It represents the higheststandards of excellence in the public pension industry.

PUBLIC PENSION COORDINATING COUNCILPUBLIC PENSION STANDARDS

Alan H. WinkleProgram Administrator

Public Pension Coordinating Council

Public Pension Standards2017 Award

Presented to

Teachers' Retirement Systemof the State of Kentucky

In recognition of meeting professional standardsfor plan design and administration as

set forth in the Public Pension Standards.

Presented by the Public Pension CoordinatingCouncil, a confederation of

National Association of State Retirement Administrators (NASRA)National Conference on Public Employee Retirement Systems (NCPERS)

National Council on Teacher Retirement (NCTR)

This page was intentionally left blank.

2017

FinancialSection

Teachers’ Retirement System

of the State of Kentucky

16 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

FINANCIAL SECTION

Independent Auditor’s Report

Board of TrusteesTeachers’ Retirement System of the State of KentuckyFrankfort, Kentucky

Report on the Financial Statements

We have audited the accompanying statements of fiduciary net position of the Teachers' Retirement System of the State ofKentucky as of June 30, 2017 and 2016, and the related statements of changes in fiduciary net position for the years then ended,and the related notes to the financial statements which collectively comprise the component unit financial statements of theTeachers' Retirement System of the State of Kentucky as listed in the table of contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accountingprinciples generally accepted in the United States of America; this includes the design, implementation, and maintenance ofinternal control relevant to the preparation and fair presentation of the financial statements that are free from materialmisstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits inaccordance with auditing standards generally accepted in the United States of America and the standards applicable to financialaudits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standardsrequire that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free ofmaterial misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements.The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of thefinancial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal controlrelevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that areappropriate in the circumstances, but not for the purpose of expressing an opinion of the effectiveness of the entity's internalcontrol. Accordingly we do not express such an opinion. An audit also includes evaluating the appropriateness of accountingpolicies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overallfinancial statement presentation.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the fiduciary net position of theTeachers' Retirement System of the State of Kentucky, a component unit of the Commonwealth of Kentucky, at June 30, 2017and 2016 and the respective changes in its fiduciary net position for the years then ended, in conformity with accountingprinciples generally accepted in the United States of America.

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 17

FINANCIAL SECTION

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management's discussion and analysison pages 18 through 21 and the Schedule of Changes in Net Pension Liability (page 59), Schedule of Net Pension Liability (page60), Schedule of Employer Contributions (page 60) Schedule of Investment Returns (page 61), Medical Insurance Plan Scheduleof Changes in Net OPEB Liability (page 62), Medical Insurance Plan Schedule of Net OPEB Liability (page 63), MedicalInsurance Plan Schedule of Employer Contributions (page 63), Schedule of Investment Returns (page 64), Life Insurance PlanSchedule of Changes in Net OPEB Liability (page 64), Life Insurance Plan Schedule of Net OPEB Liability (page 65), LifeInsurance Plan Schedule of Employer Contributions (page 65), and Schedule of Investment Returns (page 66) be presented tosupplement the basic financial statements. Such information, although not a part of the basic financial statements, is required bythe Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing thebasic financial statements in an appropriate operational, economic, or historical context. We have applied certain limitedprocedures to the required supplementary information in accordance with auditing standards generally accepted in the UnitedStates of America, which consisted of inquiries of management about the methods of preparing the information and comparingthe information for consistency with management's responses to our inquiries, the basic financial statements, and otherknowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assuranceon the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provideany assurance.

Other Supplementary Information

Our audits were conducted for the purpose of forming an opinion on the financial statements that collectively comprise theKentucky Teachers' Retirement System's basic financial statements. The additional supporting schedules (pages 67 through 69)are presented for purposes of additional analysis and are not a required part of the basic financial statements. The Schedule ofAdministrative Expenses, Schedule of Professional Services and Contracts, and Schedule of Contracted Investment ManagementExpenses are the responsibility of management and were derived from and relate directly to the underlying accounting and otherrecords used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied inthe audits of the basic financial statements and certain additional procedures, including comparing and reconciling suchinformation directly to the underlying accounting and other records used to prepare the basic financial statements or to the basicfinancial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in theUnited States of America. In our opinion, the Schedule of Administrative Expenses, Schedule of Professional Services andContracts, and Schedule of Contracted Investment Management Expenses are fairly stated, in all material respects, in relation tothe basic financial statements as a whole.

The introductory, investment, actuarial and statistical sections have not been subjected to auditing procedures applied in the auditof the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated November 14, 2017, on ourconsideration of the Teachers' Retirement System of the State of Kentucky's internal control over financial reporting and our testsof its compliance with certain provisions of laws, regulations, contracts and grant agreements and other matters. The purpose ofthat report is to describe the scope of our testing of internal control over financial reporting and compliance and the results ofthat testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integralpart of an audit performed in accordance with Government Auditing Standards in considering the Teachers' Retirement System ofthe State of Kentucky's internal control over financial reporting and compliance.

/s/ Mountjoy Chilton Medley LLP

Louisville, KentuckyNovember 14, 2017

Page 2Independent Auditor’s Report (continued)

18 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

FINANCIAL SECTION

$ 681.4 58.3

- 739.7

(5.9)$ 733.8

$ 609.7 29.1

- 638.8(11.8)

$ 627.0

$ 922.6 44.6

-967.2

(8.8)$ 958.4

$ 86.61.2

87.8

$ 87.8

$ 90.11.2

91.3(0.4)

$ 90.9

$ 88.61.1

89.7

$ 89.7

Summary of Fiduciary Net Position(In millions of dollars)

Cash & InvestmentsReceivablesCapital AssetsTotal AssetsTotal LiabilitiesNet Position

$ 16,707.7 119.5

17.0 16,844.2

(31.4)$ 16,812.8

$ 17,930.0295.5

14.918,240.4

(191.3)$ 18,049.1

Defined Benefit Plan 2017 2016 2015

Medical Insurance Plan 2017 2016 2015

Life Insurance Plan 2017 2016 2015

Categories

$ 18,649.0135.018.1

18,802.1(94.4)

$ 18,707.7

* Other Funds consisting of the 403(b) TaxShelter Plan, the Excess Benefit Fund andthe Losey Scholarship fund had a combinedfiduciary net position of $1.0 million foryears ended 2017, 2016 and 2015.

** Reflects revised amounts reported for both2016 and 2015 as described in Note 2

Cash & InvestmentsReceivablesCapital AssetsTotal AssetsTotal LiabilitiesNet Position

$ 17,479.2179.017.0

17,675.2(37.7)

$ 17,637.5

$ 18,628.3325.714.9

18,968.9(203.1)

$ 18,765.8

2017 2016** 2015***TOTALS

$ 19,658.2180.818.1

19,857.1(103.2)

$ 19,753.9

TEACHERS' RETIREMENT SYSTEM OF THE STATE OF KENTUCKYMANAGEMENT'S DISCUSSION AND ANALYSIS

This discussion and analysis of the Teachers' Retirement System of the State of Kentucky (TRS, System, or Plan) financialperformance provides an overview of the defined benefit and medical insurance plans' financial year ended June 30, 2017.Please read it in conjunction with the respective financial statements, which begin on page 22.

USING THIS FINANCIAL REPORTBecause of the long-term nature of the defined benefit retirement annuity plan, and the medical and life insurance

plans, financial statements alone cannot provide sufficient information to properly reflect the ongoing perspective ofthe System. The Statement of Fiduciary Net Position and Statement of Changes in Fiduciary Net Position (on pages22-25) provide information about the activities of the defined benefit retirement annuity plan, medical insurance plan,life insurance plan and the tax-sheltered annuity plan as a whole. The Teachers' Retirement System of the State ofKentucky is the fiduciary of funds held in trust for its members.

The Required Supplementary Information includes historical trend information about the funded status of thedefined benefit retirement annuity plan, the medical insurance plan and life insurance plan presented as required byaccounting standards. The Schedules of Employer Contributions present historical trend information about therequired contributions of employers and the contributions made by employers in relation to the requirement. Theseschedules provide information that contributes to understanding the changes over time in the funded status of theplans. Separate reports prepared by the actuary using board adopted funding methodology provide a long-term,ongoing plan perspective and the progress made in accumulating sufficient assets to pay benefits and insurancepremiums when due.

KENTUCKY TEACHERS' RETIREMENT SYSTEM AS A WHOLE

In the fiscal year ended June 30, 2017, the System's combined fiduciary net position increased by $2,116.3 million -from $17,638.5 million in 2016 to $19,754.8 million in 2017. In 2015, the combined net position totaled $18,766.8 million.The following summaries focus on the fiduciary net position and changes in fiduciary net position of the System'sdefined benefit retirement annuity plan, medical insurance plan, and life insurance plan.

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 19

FINANCIAL SECTION

$ 313.0565.5

(245.2 -

633.3

1,833.227.88.6

- 1,869.6

$ (1,236.3

$ 441.1745.1

(249.7

936.5

1,837.827.810.3

188.92,064.8

$ (1,128.3

ADDITIONSMember ContributionsEmployer ContributionsNet Investment Income/(Loss)

TOTAL ADDITIONS

DEDUCTIONSBenefit PaymentsRefundsAdministrative ExpenseInsurance ExpensesTOTAL DEDUCTIONSIncrease/(Decrease) in Net Position

*TOTALS

ADDITIONSMember ContributionsEmployer ContributionsNet Investment Income/(Loss)Other IncomeTOTAL ADDITIONS

DEDUCTIONSBenefit PaymentsRefundsAdministrative ExpenseInsurance ExpensesTOTAL DEDUCTIONSIncrease/(Decrease) in Net Position

$ 313.61,060.72,475.8 /-

3,850.1

1,918.626.310.3

-1,955.2

$ 1,894.9

$ 442.41,242.02,572.3

4,256.7

1,923.826.311.8

178.52,140.4

$ 2,116.3

The fiduciary net position of the defined benefit retirement annuity plan increased by 11.3 percent ($18,707.7million compared to $16,812.8 million) and in 2015, the fiduciary net position of the defined benefit plan totaled$18,049.1 million. The increase is primarily due to additional employer contributions from the state and improvementsin market conditions which resulted in a net investment income increase of $2.7 billion more than 2016. The 2016amount was $1.1 billion less than 2015. The defined benefit retirement annuity plan assets are restricted to providingmonthly retirement allowances to members and their beneficiaries.

The fiduciary net position of the medical insurance plan increased by 30.6 percent ($958.4 million compared to $733.8million) primarily due to contributions from members and employers exceeding insurance expenses due to legislationpassed in 2010. This compares to 2015 where fiduciary net position of the medical insurance fund totaled $627 million.Plan assets are restricted to providing hospital and medical insurance benefits to members and their spouses.

$ 128.8180.395.5

- 404.6

1.5 - 178.5

180.0

$ 224.6

$1.01.0

2.0

5.2

5.2

$ (3.2

$ 308.2559.6862.2

- 1,730.0

1,741.523.18.9

- 1,773.5

$ (43.5

$ 408.8 705.9871.6

1,986.3

1,745.623.110.5

160.7 1,939.9

$ 46.4

$ 128.1178.6

(9.3 -

297.4

1.7 - 188.9

190.6

$ 106.8

$ 100.6 145.3

7.4

253.3

- -

1.6160.7

162.3

$ 91.0

Defined Benefit Plan 2017 2016 2015

Medical Insurance Plan 2017 2016 2015

Life Insurance Plan 2017 2016 2015

Categories

$1.04.8

5.8

4.6

4.6

$ 1.2

Summary of Changes in Fiduciary Net Position(In millions of dollars)

$ -1.02.0

3.0

4.1

4.1

$ (1.1

2017 2016** 2015**

* Other Funds consisting of the 403(b) Tax ShelterPlan, the Excess Benefit Fund and the LoseyScholarship fund had a combined change in fiduciarynet position of $1.0 million for years ended 2017,2016 and 2015.

** Reflects revised amounts reported for both 2016 and2015 as described in Note 2.

DEFINED BENEFIT RETIREMENT ANNUITY PLAN ACTIVITIES

Retirement contributions are calculated by applying a percentage factor to salary and are paid monthly by eachmember. Members may also pay contributions to repurchase previously refunded service credit or to purchase varioustypes of elective service credit.

)

)

)

)

)

)

))

Management’s Discussion and Analysis (continued)

20 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

FINANCIAL SECTION

In 2017, Employer contributions totaled $1,060.7 million, a net increase of $495.2 million from the prior fiscal year.The increase was due to additional employer contributions paid by the state. In 2016, Employer contributions increased$5.9 million compared to the prior fiscal year.

In 2017, the defined benefit plan experienced an increase in net investment income compared to the previous year($2,475.8 million compared to negative $245.2 million). For 2015, net investment income totaled $862.2 million. Theincrease in net investment income is mainly due to favorable market conditions for the year ended June 30, 2017compared to 2016. Total deductions in 2017 increased $85.6 million. The increase was caused principally by anincrease of $86.0 million in defined benefit payments. Members who were drawing benefits as of June 2016 received anincrease of one and one-half percent to their retirement allowances in July 2016. Also, there was an increase of 1,403members and beneficiaries on the retired payroll as of June 30, 2017.

OTHER POSTEMPLOYMENT BENEFIT ACTIVITIES

During the 2017 fiscal year, the medical insurance plan member contributions increased $0.7 million and employercontributions increased $1.7 million from fiscal year 2016. The member, employer and state contributions increasedprimarily due to the implementation of the Shared Responsibility Plan beginning July 1, 2010 which includes increasedcontributions from active and retired members, employers and the state.

Net investment income for the medical insurance plan increased $104.8 million from negative $9.3 million in 2016 to$95.5 million in 2017. In 2015, net investment income totaled $7.4 million.

The life insurance plan has an actuarial valuation conducted independently from the defined benefit plan. Total lifeinsurance benefits paid for 2017, 2016 and 2015 were $5.2, $4.6 and $4.1 million respectively.

FUNDING

For the 2016-2018 biennium, the State budgeted $973 million of additional employer contributions for the unfundedliability of the System. The latest actuarial valuation was for the period ending June 30, 2017. This report reflects theSystem's actuarial value of assets totaling $18.5 billion and actuarial determined liabilities totaling $32.8 billion. Thefunded ratio of actuarial assets to liabilities is 56.4%. The additional funding provided in the budget resulted in 99% ofthe Actuarially Determined Employer Contribution being made for fiscal year 2017. Assuming that contributions to theSystem are made by the State from year to year in the future as recommended by the actuary, the System should havesufficient assets to provide the benefits defined by law.

The actuarial funding of the medical insurance and life insurance plans is provided in the Schedule of FundingProgress presented in the Required Supplementary Information. The asset value, stated in the Schedule of FundingProgress, is determined by the System's independent actuary. The actuarial accrued liability is calculated using theentry age cost method. Although the medical insurance plan continues to have a large unfunded actuarial liability, thecurrent obligations are being met by current funding. Effective July 1, 2010 the Shared Responsibility Plan for fundingretiree health benefits requires members, retirees, participating employers and the state to make contributions for pre-funding retiree medical benefits. Annual required contributions of the medical insurance plan are provided in theSchedule of Employer Contributions presented in the Required Supplementary Information.

HISTORICAL TRENDS

Accounting standards require that the Statement of Fiduciary Net Position present asset values at fair value andinclude only benefits and refunds due to plan members and beneficiaries and accrued investment and administrativeexpenses as of the reporting date. Detailed information regarding the funded status, including the key actuarialassumptions, target allocations and the sensitivity of the discount rate can be found in Note 4 of the financial statementsfor the defined benefit plan, Note 8 for the medical health plan, and Note 9 for the life insurance plan. The blendeddiscount rate mandated by accounting standards result in a lower funding level when compared to the actuariallydetermined funded levels reported in past years. The Schedule of Employer Contributions is provided in the RequiredSupplementary Information.

Management’s Discussion and Analysis (continued) . . .

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 21

FINANCIAL SECTION

The System's independent consulting actuaries are members of the American Academy of Actuaries andexperienced in performing valuations for public retirement systems. As mandated by state law, the valuations of theretirement annuity and health care plans are prepared in accordance with principles of practice prescribed by theActuarial Standards Board consistent with accepted actuarial procedures. Actuarial assumptions used in the valuationsare internally consistent and reasonable based on the actual experience of the plans. An actuarial audit was completedin 2015, which confirmed the accuracy of actuarial procedures and the reasonableness of assumptions. A five-yearexperience study was completed in 2016, which also confirmed the reasonableness of assumptions based upon theactual experience of the plans. The actuarial assumptions reflected in the results may be reasonably relied upon.However, projections using other assumptions may produce significantly different results.

The Finance and Administration Cabinet commissioned a study of the state's retirement systems, including theTeachers' Retirement System. The resulting report from this study was issued in August 2017 and is the basis forongoing discussions that may lead to legislative change to the System.

This financial report is designed to provide citizens, participating employers, plan members, and other users withan overview of the Kentucky Teachers' Retirement System's fiscal practices and responsibility. If you have questions orneed additional information, please contact Mark Whelan, Chief Financial Officer, Teachers' Retirement System at 479Versailles Road, Frankfort, Kentucky 40601.

Management’s Discussion and Analysis (continued) . . .

22 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

FINANCIAL SECTION

137,274,752 100,838

28,779,827 1,567,472

13,640,427 40,623,372 49,973,750

438,303

135,023,151

521,348,977 2,871,403,201

11,589,656,638 1,062,855,562 1,046,760,134 1,419,607,158

18,511,631,670

18,046,639

18,802,077,050

2,201,644

92,176,381

94,378,025

18,707,699,025

ASSETS

CashPrepaid Expenses

ReceivablesContributionsDue From Other Trust FundsState of KentuckyInvestment IncomeInvestment Sales ReceivableOther Receivables

Total Receivables

Investments at Fair Value (See Note 5)Short-Term InvestmentsBonds and MortgagesEquitiesAlternative InvestmentsReal EstateAdditional Categories

Total Investments

Capital Assets, at cost net of accumulated depreciation of $8,019,203 (See Note 2)

Total Assets

LIABILITIES

Accounts PayableDue to Other Trust FundsRevenues Collected in AdvanceInvestment Purchases Payable

Total Liabilities

Net Position - Restricted forPension and OtherPost-Employment Benefits

$

$

$

$

$

$

$

$

$

$

87,841,753

18,456,779

5,580,025 1,685,597

915,100 17,958,624

44,596,125

46,008,715 70,283,077

473,274,401 42,340,364 42,701,494

160,170,175

834,778,226

967,216,104

10,300 1,538,574 3,437,483 3,840,074

8,826,431

958,389,673

187,657

105,264

32,617 1,036,228

1,174,109

4,150,029 82,293,300

86,443,329

87,805,095

27,690

27,690

87,777,405

23,852

2,693

2,693

398,093 258,962 280,104

937,159

963,704

1,208

1,208

962,496

225,328,014 100,838

47,341,870 1,567,472

19,253,069 43,347,890 50,888,850 18,396,927

180,796,078

571,905,814 3,024,238,540

12,063,211,143 1,105,195,926 1,089,461,628 1,579,777,333

19,433,790,384

18,046,639

19,858,061,953

2,211,944 1,567,472 3,437,483

96,016,455

103,233,354

19,754,828,599

STATEMENT OF FIDUCIARY NET POSITIONAs of June 30, 2017

OtherFunds

LifeInsurance

Plan

MedicalInsurance

Plan

DefinedBenefit

Plan TOTAL

The “Combining Statement of Fiduciary Net Position - Other Funds” is presented on page 26.The accompanying notes are an integral part of these financial statements.

Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016 23

FINANCIAL SECTION

$

$

$

$

$

$

$

$

$

$

59,843,503

21,525,458

1,359,808 1,333,953

633,642 33,481,047

58,333,908

18,186,502 62,555,400

354,369,798 23,931,317 25,433,241

137,075,842

621,552,100

739,729,511

19,811 1,747,115 2,047,051 2,134,567

5,948,544

733,780,967

15,156,496 89,235

34,664,070 3,719,997

22,766,523 39,619,872 18,182,733

559,913

119,513,108

507,724,996 2,734,474,510

10,267,066,002 932,813,350 940,860,202

1,309,513,418

16,692,452,478

16,973,670

16,844,184,987

1,917,838 1,935,385

27,499,881

31,353,104

16,812,831,883

95,285

54,392 1,090,402

1,240,079

913,077 89,200,103

90,113,180

91,353,259

325,494 36,837

362,331

90,990,928

481

2,417

2,417

410,590 290,132 242,351

943,073

945,971

660

660

945,311

75,000,480 89,235

56,284,813 3,719,997

24,180,723 42,046,644 18,816,375 34,040,960

179,089,512

527,235,165 2,886,520,145

10,621,678,151 956,744,667 966,293,443

1,446,589,260

17,405,060,831

16,973,670

17,676,213,728

2,263,143 3,719,997 2,047,051

29,634,448

37,664,639

17,638,549,089`

ASSETS

CashPrepaid Expenses

ReceivablesContributionsDue From Other Trust FundsState of KentuckyInvestment IncomeInvestment Sales ReceivableOther Receivables

Total Receivables

Investments at Fair Value (See Note 5)Short-Term InvestmentsBonds and MortgagesEquitiesAlternative InvestmentsReal EstateAdditional Categories

Total Investments, at fair value

Capital Assets, at cost net of accumulated depreciation of $6,022,382 (See Note 2)

Total Assets

LIABILITIES

Accounts PayableDue to Other Trust FundsRevenues Collected in AdvanceInvestment Purchases Payable

Total Liabilities

Net Position - Restricted forPension and OtherPostemployment Benefits

STATEMENT OF FIDUCIARY NET POSITIONAs of June 30, 2016

OtherFunds

LifeInsurance

Plan

MedicalInsurance

Plan

DefinedBenefit

Plan TOTAL

The “Combining Statement of Fiduciary Net Position - Other Funds” is presented on page 26.The accompanying notes are an integral part of these financial statements.

24 Teachers’ Retirement System of the State of Kentucky • Years Ended June 30, 2017 and 2016

FINANCIAL SECTION

220,001

220,001

6,584 10,920 5,468

231 23,203

(114 (69

23,020 243,021

224,628

1,208 225,836

17,185

945,311

962,496

))

75,496,731 104,879,255 128,819,243

309,195,229

89,058,380 5,777,776 3,787,309

98,623,465

(3,170,868

95,452,597404,647,826

178,500,546 1,538,574

180,039,120

224,608,706

733,780,967

958,389,673

1,057,795,523 184,570,140 442,444,677

1,684,810,340

2,254,023,748 162,007,193 184,090,004 30,477,797 3,660,488

2,634,259,230

(61,017,510 (1,097,808

2,572,143,912 4,256,954,252

1,923,987,769 26,305,240

178,500,546 11,881,187

2,140,674,742

2,116,279,510

17,638,549,089

19,754,828,599

881,703 167,980

1,049,683

(2,087,797 3,011,187

3,692 927,082

(10,478 (1,107

915,497 1,965,180

5,151,013

27,690 5,178,703

(3,213,523

90,990,928

87,777,405

$

$

$

$

$

$

$

$

$

$

981,417,089 79,302,904

313,625,434

1,374,345,427