taxing natural resources - oecd semmingsen 231112 oecd.pdf · taxing natural resources basic...

TRANSCRIPT

Norwegian Ministry of Finance

Taxing Natural Resources

Basic Principles and Norwegian Experience

Deputy Director General Lone Semmingsen

2012 OECD Green Growth and Sustainable Development Forum, 23 November 2012, OECD Conference Centre, Paris

Norwegian Ministry of Finance 2

The Starting Point of Resource Rent Taxation

• Extraordinary profits due to limited resources

• Immobile resources A good tax base • Possible to tax the resource rent

without distorting incentives to invest

Taxing Natural Resources

Norwegian Ministry of Finance

Government Take Instruments

• Net profit taxation • Royalty - gross or net • Production sharing agreements • Government participation • Government owned oil companies • Auctions or signature bonuses Key issues when choosing: • Risk • Attracting profitable investments • Need of early income • Administrative issues

3 Taxing Natural Resources

Norwegian Ministry of Finance 4

The Norwegian Profit Tax Systems

Resource Rent: Potential for increased tax take

Extra allowance for ordinary returns Should not distort investment incentives

Ordinary income: • 28% on net income as in other industries • Neutrality between industries • Tax on ordinary returns and super-profit

Taxing Natural Resources

Norwegian Ministry of Finance 5

Petroleum Tax System

• Production from 1971 • Resource rent tax

introduced 1975 • Tax rate 50%,

total marginal tax rate 78%

• Profit based on a company basis

• Ring fenced against mainland activity

Taxing Natural Resources

Norwegian Ministry of Finance

Norwegian Government Net Revenue from Petroleum

6 Taxing Natural Resources

-10

10

30

50

70

90

110

-50

50

150

250

350

450

1971

19

72

1973

19

74

1975

19

76

1977

19

78

1979

19

80

1981

19

82

1983

19

84

1985

19

86

1987

19

88

1989

19

90

1991

19

92

1993

19

94

1995

19

96

1997

19

98

1999

20

00

2001

20

02

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

Oil

pric

e 20

13-U

SD

Reve

nues

Bill

. 201

3-N

OK

Taxes Environmental taxes SDFI Royalty and area fee Dividend Statoil Oil price (right axis)

Norwegian Ministry of Finance 7

State Direct Financial Interest (SDFI)

• Direct government interest in fields and pipelines

• Decided when licenses are awarded

• Varies between fields • The government pays its share

of investments and costs • ... and receives a corresponding

share of the gross income from the license.

• Established in 1985 • Similar to a cash flow tax

Taxing Natural Resources

Photo: Statoil

Norwegian Ministry of Finance 8

Hydro Power Taxation

• Production from about 1900 • Resource rent tax introduced

1997 • RRT tax rate 30 pct.

Total marginal tax rate 58 pct. • The RRT is neutral with regard

to investments

• Property tax • Concessional liabilities

Taxing Natural Resources

Norwegian Ministry of Finance 9

Hydro Power Generation Resource Rent Tax 1997-2011

0

1000

2000

3000

4000

5000

6000

7000

8000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Mill

. NO

K

Year

Hydropower - Resource rent tax 1997-2011

Taxing Natural Resources

Norwegian Ministry of Finance

Thank you!

Taxing Natural Resources 10

Norwegian Ministry of Finance 11

Tax Base - Petroleum on company basis – ring fenced against mainland

Companies without taxable income • Carry forward with interest - (risk free + 0,5%)*(1-0,28) • Tax refund (pay out) of exploration costs • Final losses can be sold or tax reimbursed from the state

Sales income (norm prices) - Operating costs - Capital depreciation (16,7 pct. over 6 years) - Financial costs - (Deficits from previous years) = Ordinary tax base liable to 28 pct. tax - Uplift (investment based extra depreciation, 7,5 pct. 4 years) - (Excess uplift from previous years) = Tax base liable to 50 pct. tax

Taxing Natural Resources

Norwegian Ministry of Finance 12

Tax Base – Hydro Power Generation

Negative resource rent will be entitled to a tax refund (pay out)

Sales income (market prices) - Operating costs - Concession fees - Property tax - Depreciation (linear: installations 1,5% equipment 2,5%) - Uplift (tax values * risk free rate) = Tax base liable to 30 pct. tax

Taxing Natural Resources

Norwegian Ministry of Finance 13

Return on fund investments

Fund Transfer to finance non-oil budget deficit

Revenues

Expenditures • consumption • investment • transfers

State Budget

The Fund Mechanism Integrated with Fiscal Policy

Fiscal policy guideline (over time spend real return of the fund,

approximately 4 pct.)

Petroleum revenues

Norwegian Ministry of Finance 14

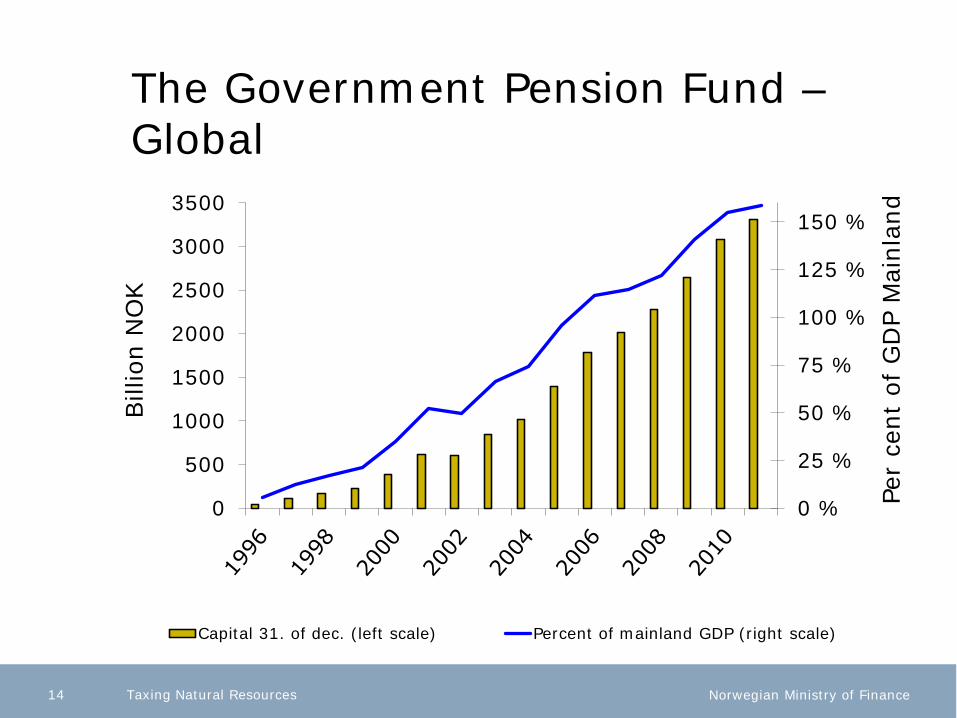

The Government Pension Fund – Global

0 %

25 %

50 %

75 %

100 %

125 %

150 %

0

500

1000

1500

2000

2500

3000

3500

Per

cent

of G

DP

Mai

nla

nd

Bill

ion N

OK

Capital 31. of dec. (left scale) Percent of mainland GDP (right scale)

Taxing Natural Resources