taxation of cross border dividend payments within eu 2012 clean

TRANSCRIPT

DG Taxation and Customs Union

TAXATION OF CROSS-BORDER DIVI-DEND PAYMENTS WITHIN THE EU IMPACTS OF SEVERAL POSSIBLE SOLUTIONS TO ALLEVIATE DOUBLE TAXATION | 22 JUNE 2012

Taxation of cross-border dividend payments within the EU

2

Disclaimer

This report has been produced by Copenhagen Economics following the commissioning of a

study by the European Commission, Directorate-General for Taxation and Customs Union.

It is the result of independent work carried out by Copenhagen Economics, and does not

necessarily reflect the opinions or position of the European Commission or of the experts or

stakeholders. Any errors are our own.

COLOPHON

Author: Partner Sigurd Næss-Schmidt (project manager), senior economist Eva Rytter

Sunesen (team leader), economist Martin Bo Hansen (team member) and analyst

Holger Nikolaj Jensen (team member)

Client: DG TAXUD

Date: 22 June 2012

Contact: SANKT ANNÆ PLADS 13, 2nd FLOOR | DK-1250 COPENHAGEN

PHONE: +45 2333 1810 | WWW.COPENHAGENECONOMICS.COM

Taxation of cross-border dividend payments within the EU

3

Preface 8

Executive summary....................................................................................................... 9

0.1 Dividend flows and their taxation .......................................................................... 9

0.2 Distortions to investment and the Internal Market .............................................. 11

0.3 Key impacts on Member States' budgets and possible welfare gains...................... 16

Chapter 1 Current cross-border equity investments and taxation of dividends ...... 18

1.1. Structuring of cross-border portfolio equity investments ...................................... 20

1.2. Current cross-border investments between member states .................................... 23

1.3. Current cross-border dividend flows between Member States .............................. 28

1.4. The current taxation of cross-border dividends .................................................... 31

Chapter 2 Option 1: Revenue effects from the current taxation of cross-

border dividends ........................................................................................................ 36

2.1. A preliminary assessment of the current tax regime .............................................. 36

2.2. Impacts on EU Member States of the current tax regime ..................................... 38

2.3. Impacts on investors of the current tax regime ..................................................... 44

2.4. Impacts on the Internal Market of the current tax regime .................................... 51

Chapter 3 The economic impacts of the proposed options ..................................... 56

3.1. Option 2: Abolition of WHT on cross-border dividends ..................................... 56

3.2. Option 3: Full credit for WHT levied on cross-border dividends ......................... 61

3.3. Option 4: Net rather than gross taxation in the source country ............................ 66

3.4. Option 5: General EU-wide reduced WHT rate with information exchange........ 68

3.5. Option 6: Limited taxation of dividend income and credit for corporate tax ........ 73

3.6. Option 7: No WHT and no income tax on cross-border dividends ..................... 78

3.7. Summing up the economic impacts of proposed options ..................................... 82

Chapter 4 The legal impacts of the proposed options ............................................ 87

4.1. Option 1: Maintaining the existing situation ....................................................... 87

4.2. Option 2: Abolition of WHT levied on cross-border dividends ........................... 94

4.3. Option 3: Full credit for WHT on cross-border dividends ................................... 95

4.4. Option 4: Net rather than gross taxation in the source country ............................ 96

4.5. Option 5: General EU-wide reduced WHT rate with information exchange........ 97

4.6. Option 6: Limited taxation of dividend income and credit for corporate tax ........ 99

4.7. Option 7: No WHT and no income tax on cross-border dividends ................... 100

4.8. Summing up the legal impacts of the proposed options ..................................... 101

Chapter 5 Cross-cutting issues related to the proposed options ........................... 102

5.1. Impacts of the proposed options on different investors ...................................... 102

5.2. Macroeconomic impacts of the reduced cost of capital ....................................... 103

5.3. Impacts on third countries ................................................................................. 107

TABLE OF CONTENTS

Taxation of cross-border dividend payments within the EU

4

5.4. Impacts on the Internal Market ......................................................................... 107

5.5. Interaction with the Parent Subsidiary Directive ................................................ 108

5.6. Sensitivity analysis ............................................................................................. 109

Taxation of cross-border dividend payments within the EU

5

Table 0.1 Impacts of the various options on compliance and administrative costs .............. 14

Table 0.2 Impacts of the various options on distortions to investment decision .................. 15

Table 0.3 Quantifiable costs to investors in the different options ...................................... 17

Table 1.1 Outbound portfolio equity investments ............................................................. 24

Table 1.2 Inbound portfolio equity investments ................................................................ 25

Table 1.3 Outbound portfolio equity investments as a share of total outbound equity

investments ....................................................................................................................... 26

Table 1.4 Inbound portfolio investments as a share of total inbound equity investments .... 27

Table 2.1 What is at stake for individual EU Member States? ............................................ 38

Table 2.2 Current tax revenues from WHT in EU Member States (Option 1) .................. 39

Table 2.3 Tax revenues from WHT compared with corporate income taxes ...................... 40

Table 2.4 Administration of the refund procedure in selected source countries .................. 44

Table 2.5 Current tax burden of investors in EU Member States (Option 1) ..................... 45

Table 2.6 Current tax burden of different investor types (Option 1) .................................. 46

Table 2.7 Summary of findings from two meta analysis ..................................................... 54

Table 3.1 Impact of Option 2 on tax revenues (compared to the current situation) ............ 58

Table 3.2 Tax burden of investors under Option 2 (compared to the current situation) ..... 59

Table 3.3 Tax burden by investor type under Option 2 (compared to current situation) .... 60

Table 3.4 Impact of Option 3 on tax revenues (compared to the current situation) ............ 63

Table 3.5 Tax burden of investors under Option 3 (compared to the current situation) ..... 64

Table 3.6 Tax burden by investor type, Option 3 (compared to the current situation) ....... 65

Table 3.7 Taxes faced by investors in source and residence countries.................................. 67

Table 3.8 Impact of Option 5 on tax revenues (compared to the current situation) ............ 70

Table 3.9 Tax burden of investors under Option 5 (compared to the current situation) ..... 71

Table 3.10 Tax burden by investor type, Option 5 (compared to the current situation) ..... 72

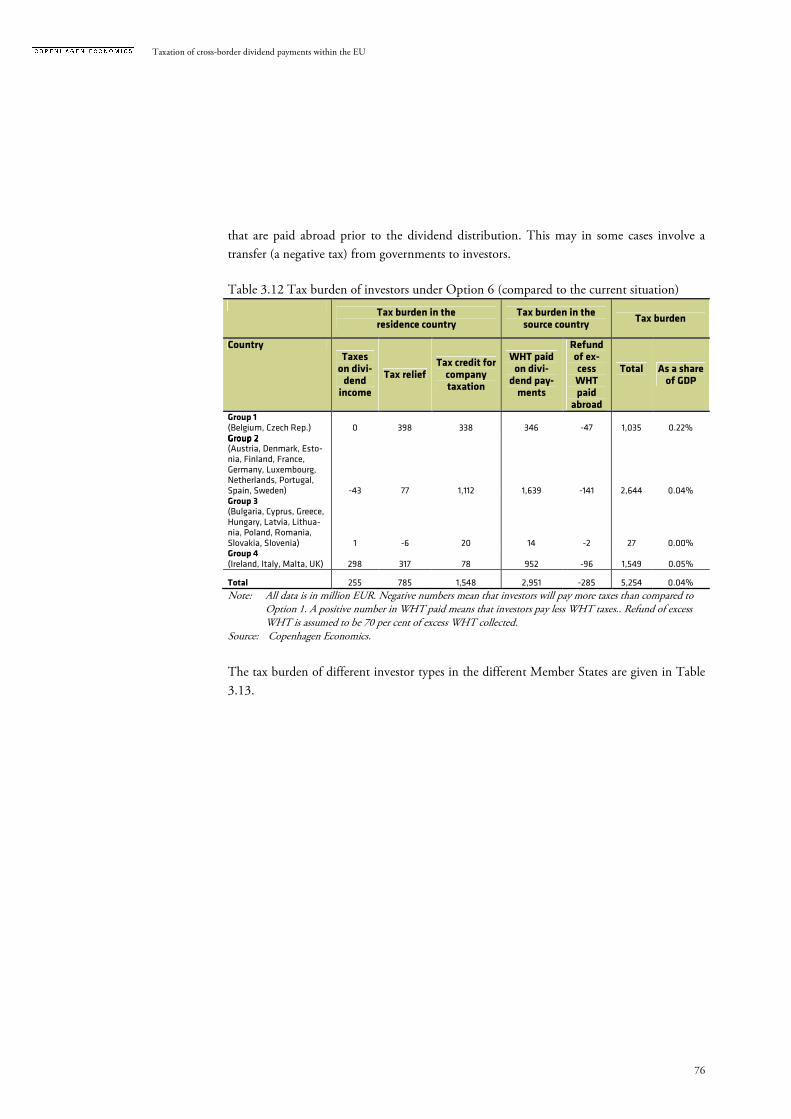

Table 3.11 Impact of Option 6 on tax revenues (compared to the current situation) .......... 75

Table 3.12 Tax burden of investors under Option 6 (compared to the current situation) ... 76

Table 3.13 Tax burden by investor type, Option 6 (compared to the current situation) ..... 77

Table 3.14 Impact of Option 7 on tax revenues (compared to the current situation) .......... 79

Table 3.15 Tax burden of investors under Option 7 (compared to the current situation) ... 80

Table 3.16 Tax burden by investor type, Option 7 (compared to the current situation) ..... 81

Table 3.17 Quantifying juridical double taxation............................................................... 83

Table 3.18 Foregone tax relief ........................................................................................... 83

Table 3.19 Impacts on compliance costs for investors and administration cost for Member

States ................................................................................................................................. 85

Table 3.20 Quantifiable impacts on compliance cost ........................................................ 86

Table 4.1 Domestic WHT rates on dividends paid to residents and non-residents ............. 88

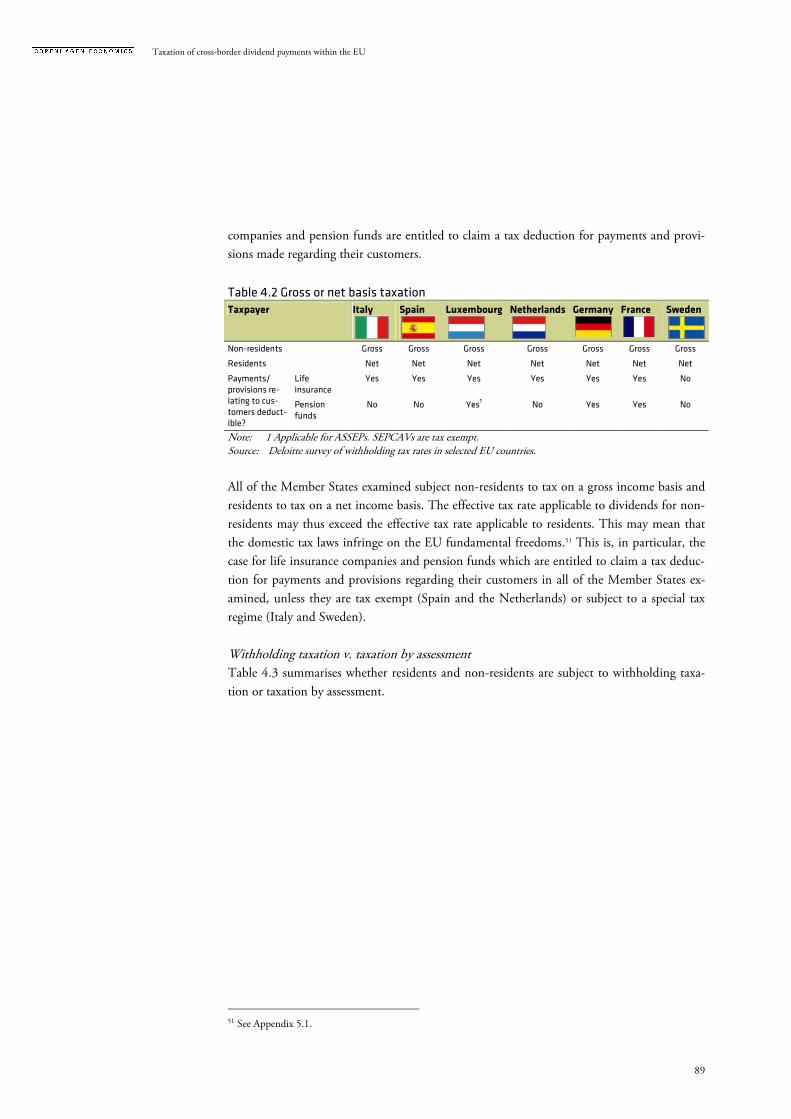

Table 4.2 Gross or net basis taxation ................................................................................. 89

Table 4.3 Withholding taxation vs. taxation by assessment ................................................ 90

Table 4.4 Relief at source or refund ................................................................................... 91

Table 4.5 Domestic taxation of dividends from resident and non-resident companies and

CIVs.................................................................................................................................. 92

Table 4.6 Method for relieving international juridical double taxation ............................... 93

LIST OF TABLES

Taxation of cross-border dividend payments within the EU

6

Table 4.7 Legal impacts of Option 2 ................................................................................. 95

Table 4.8 Legal impacts of Option 3 ................................................................................. 96

Table 4.9 Legal impacts of Option 4 ................................................................................. 97

Table 4.10 Legal impacts of Option 5 ............................................................................... 99

Table 4.11 Legal impacts of Option 6 ............................................................................. 100

Table 4.12 Legal impacts of Option 7 ............................................................................. 101

Table 4.13 Legal impacts of Options 2-7 ......................................................................... 101

Table 5.1 Change in tax burden of investors (compared to the current situation) ............. 103

Table 5.2 Impact on GDP from a reduction in cost of capital .......................................... 105

Table 5.3 Expected positive impact on the Internal Market of the proposed options ........ 108

Table 5.4 Sensitivity analysis on CIV’s treaty entitlements ............................................... 110

Taxation of cross-border dividend payments within the EU

7

Figure 0.1 EU taxation of portfolio and individuals' cross-border dividends ....................... 10

Figure 1.1 Individual investing in equity............................................................................ 21

Figure 1.2 Individuals investing in equity via domestic financial companies ....................... 22

Figure 1.3 Individuals investing in equity via foreign financial companies .......................... 23

Figure 1.4 Composition of intra-EU portfolio equity investments ..................................... 28

Figure 1.5 Total inbound portfolio dividends in Member States as a share of GDP ........... 29

Figure 1.6 Total outbound portfolio dividends in Member States as a share of GDP ......... 29

Figure 1.7 The potential distortions and other problems appear to be getting worse .......... 32

Figure 3.1 Change in tax revenue (compared to the current situation) ............................... 84

Figure 5.1 Distribution of current tax liabilities from cross border dividend flows on investor

type ................................................................................................................................. 102

Figure 5.2 Macroeconomic impacts of the reduced cost of capital .................................... 106

Figure 5.3 The organisational structure of EU firms ........................................................ 109

LIST OF FIGURES

Taxation of cross-border dividend payments within the EU

8

The European Commission has asked Copenhagen Economics to undertake a:

Study on the impact of several alternative solutions to the taxation problems that arise when

dividends are paid across borders to individual and portfolio investors within the EU.

The study relies on readily available information on legislation on domestic taxation of divi-

dends as well as withholding tax (WHT) rates in respect to dividends received by individuals

and companies. Information concerning the domestic taxation and WHT on dividends re-

ceived by collective investment vehicles (CIVs) is obtained by a survey of nine EU countries

carried out by Deloitte offices in the countries concerned.

The scope of the study has been narrowed in several ways:

� We exclude venture capital as returns from such investments are mostly in the form

of capital gains.

� We exclude equity investments in shares that are not listed since dividend taxation

in some resident States depends on whether the shares are listed or not.

� Issues related to dividend payments to portfolio investors/ individuals who are resi-

dent in non-EU Member States are out of scope of the study.

� The impact of all options on the revenue and cost factors for the Clearing and Set-

tlement Industry does not have to be looked into or reported on.

Finally, the following issues are outside the scope of the study because they are the subject of

separate Commission work:

� The tax issues related to Real Estate Investment Trusts (REITS) and open-ended

property investment funds.

� The tax issues related to UCITS IV recast1.

� The tax treatment of cross-border venture capital funds which was the subject of

discussions in a Commission expert group and on which a report2 was published in

2010.

� The functioning of the EU Savings Directive covering bond funds, which is being

dealt with in the discussions on the Commission's proposal to amend the Di-

rective.

� Interest and royalty payments.

1 Directive 2009/65/EC of the European Parliament and of the Council of 13 July 2009 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable se-curities (UCITS) (recast). 2 http://ec.europa.eu/taxation_customs/resources/documents/taxation/company_tax/initiatives_small_business/venture_capital/tax_obstacles_venture_capital_en.pdf.

PREFACE

Taxation of cross-border dividend payments within the EU

9

The basic premise for the discussion is that the present overall structure of taxation of cross-

border portfolio and individuals' equity investments creates distortions to investments in two

ways. First, it may lead to a higher overall taxation of dividends from non-domestic than

domestic equity investment and hence require a higher compensating pre-tax return. This

reduces the incentive to invest in other EU Member States and conflicts with the objective

of a common Internal Market for capital. Second, procedures to relieve such “over-taxation”

(e.g. the necessity to claim refund where relief at source is not available) may entail compli-

ance burdens that likewise reduce the incentive to undertake cross-border investments.

The European Commission has, on the basis of stakeholders’ suggestions, identified several

possible options on how to improve the current taxation of cross-border dividends. The eco-

nomic and legal impacts of the six options (in addition to the option to do nothing) have

been assessed in this report. The executive summary outlines the main results from the study

under three headlines:

� Dividend flows and their taxation

� Distortions to investment and the Internal Market

� Key impacts on Member States’ budgets and possible welfare gains

0.1 DIVIDEND FLOWS AND THEIR TAXATION In this section we recap the essential characteristics of the present tax regime in all its com-

plexity. The report only reviews portfolio investments (i.e. where the investor is a company

or individual which owns less than 10 per cent of the shares) as well as direct investments by

individuals. Investments by companies with shareholdings of more than 10 per cent are cov-

ered by the Parent-Subsidiary Directive and are outside the scope of this study.

In the simplest case, an individual in residence country A undertakes a portfolio equity in-

vestment in a company in source country B (see Figure 0.1) in the hope of receiving a return

on his investment for example in the form of dividends. Such a dividend stems from profits

which have initially been taxed at the company level. When it is paid to the individual as

dividends it will be subject to a withholding tax (WHT) in the source country generally

ranging between 5 to 30 per cent (some countries also levy no WHT). Tax treaties between

Member States normally reduce the WHT to 5-15 per cent. However, to benefit from the

reduced rate the investor will need to apply for a relief at source or a relief by refund of ex-

cess WHT, i.e. the difference between the non-treaty and the treaty rate. Then the investor

is also taxed in the country of residence. Recognising that the dividend has already been

taxed at source, the residence country usually relieves international juridical double taxation.

EXECUTIVE SUMMARY

Taxation of cross-border dividend payments within the EU

10

Figure 0.1 EU taxation of portfolio and individuals' cross-border dividends

Source: Copenhagen Economics.

However, most cross-border portfolio investments are carried out by institutional investors

(pension, mutual and insurance funds and companies etc.) that manage investments on be-

half of the ultimate investors. This also implies that the flow from such institutional inves-

tors to the ultimate investors may take many forms e.g. an annuity at retirement, an ongoing

dividend payment or a capital gain when selling out shares/units in a mutual fund.

In the most straightforward version, the ultimate investor invests in a foreign company

through an institutional investor resident in the same country as the ultimate investor. In

this case, taxation in the source country depends on how this country treats the institutional

investor in question. In some cases, institutional investors are not treated like separate enti-

ties for tax purposes (tax transparent), implying that source taxation depends on the charac-

teristics of the ultimate investors. In other situations, institutional investors are recognized as

separate entities for tax purposes and are taxed as other portfolio investors, including the

possibility of relief at source or relief by refund. In addition to this, taxation of the institu-

tional investor takes place in the residence country.

In the residence country, and at the level of the institutional investor, dividend income can

be tax exempt, subject to tax at relatively low tax rates or subject to a low effective taxation

because provisions made for obligations towards the ultimate investors are deductible. Con-

sequently, a foreign tax credit for the amount of WHT suffered in the source country may

not be obtained in the residence country. In this case, the WHT tax becomes a final tax un-

less the ultimate investors are entitled to claim a foreign tax credit for the WHT suffered by

the institutional investor. The most dominant result is that a foreign tax credit is not ob-

tained for full WHT amount paid by institutional investors.

Foreign/domestic financial company Foreign companyIndividual

Cross-border/domestic dividend payment

Portfolio equity investment Portfolio equity investment

Cross-borderdividend payment

Residencecountry� Tax on dividend income�Tax relief for WHT paidin source country

Intermediate country Source country� WHT on dividends� Refund of excessWHT (if applied WHT rate is higher than treaty rate)Direct equity investment

Cross-border dividend payment

Taxation of cross-border dividend payments within the EU

11

0.2 DISTORTIONS TO INVESTMENT AND THE INTERNAL MARKET Our assessment is that the current tax regime in many cases leads to compliance costs for in-

vestors, administrative cost for Members States, and distortions to investments linked to the

following outcomes:

� Compliance costs for investors:

o Liquidity costs that arise where relief is granted by refund (due to the long

time period investors have to wait to get a refund)

o Difficulties encountered when applying for relief by refund (i.e. docu-

mentation requirements and need to deal with foreign tax administra-

tions)

o Documentation requirements when applying for relief at source

o Foregone WHT relief in the State of Source when tax relief procedures

are too costly, burdensome and time-consuming

� Administrative costs for Member States:

o Administrating a relief at source system in the source country

o Administrating relief by refund claims (i.e. costs for handling refund

claims made by investors) in the source country

o Administrating tax credits to residents for foreign WHT

� Direct distortions to investment decisions:

o Created by economic double taxation, i.e. if the same profits are taxed in

the hands of two different taxpayers (e.g. at the company level and share-

holder level).

- distortions of investors’ incentive to carry out portfolio investments by

choosing debt rather than equity financing,

- related incentive to distribute profits in forms other than dividends

- distortion to the decision whether the profits shall be retained or dis-

tributed.

o Created by juridical double taxation, i.e. if the excessive withholding tax is

not fully credited in the residence country for the WHT paid abroad.

- distortions to incentives to invest abroad.

- distortions to the choice of investment location due to different degrees

of taxation and tax credit schemes

- distortions to the choice of the legal form and legal arrangements used

This is particularly important for CIV’s that are often unable to credit

withholding taxes in their residence country due to lack of taxable in-

come.

To deal with these potential distortions, the European Commission has on the basis of

stakeholders' suggestions identified several alternative solutions that might improve the cur-

rent situation:

Taxation of cross-border dividend payments within the EU

12

� Option 1: Keeping the existing situation unchanged

� Option 2: Abolition of withholding taxes on cross-border dividend payments to

portfolio/individual investors

� Option 3: The residence country grants full credit for the withholding taxes levied

in the source country

� Option 4: Net rather than gross taxation in the source country.

� Option 5: Application of a general EU-wide reduced rate of withholding tax with

information exchange (Neumark solution) if the taxpayer opts for information ex-

change

� Option 6: Limitation of both source and residence taxation of dividend income

and granting of limited underlying tax credit for foreign corporate taxation

� Option 7: No WHT in the source country and no taxation of foreign source divi-

dends in the residence country

In this study, we have reviewed the extent to which these options help address the distortions

created by the current system of taxing cross-border dividends.

Option 2 would eliminate discrimination of outbound and domestic dividends provided

that it would encompass all relevant entities including pension funds and CIVs with EU in-

vestors. Option 2 would eliminate juridical double taxation but would not in itself eliminate

economic double taxation. Option 2 will by definition remove the administrative costs asso-

ciated with refund of excess WHT and will considerably reduce compliance costs for inves-

tors associated with withholding tax relief procedures, although investors will still need to

document that they are entitled to be exempt from WHT. Moreover, the tax systems in

most source Member States will be simplified so that the cost of administrating withholding

tax relief procedures will be reduced. Furthermore the cost of administrating tax credits to

residents for foreign WHT is completely removed.

Option 3 will eliminate juridical double taxation of cross-border dividends when it is im-

plemented so that full credit of the withholding tax is provided independent of the taxes im-

posed in the residence state.3 This will therefore help deal with cases where domestic tax lia-

bilities of individual tax investors, for various reasons, is insufficient to allow full credits for

source taxes paid abroad. Option 3 however, will not remove discrimination of outbound

dividends in the source state and will not in itself eliminate economic double taxation. This

option is not expected to have a major impact on compliance costs for investors or adminis-

trative costs for Member States.

Whether Option 4 would eliminate juridical double taxation of cross-border dividends de-

pends, among other things, on how foreign tax credit is calculated in the residence state, the

level of expenses that may be allocated to the dividend income under the domestic tax laws

3 This would imply that governments in some cases would refund the surplus tax to the investors levy negative tax-es) if there were no sufficient tax liabilities to credit from. This assumption is based on the description in the Terms of Reference to this study

Taxation of cross-border dividend payments within the EU

13

of the source state and residence state and the level of the tax rates of the source state and

residence state. If the residence state calculates foreign tax credit on a gross income basis (Ita-

ly, the Netherlands, France, Ireland and the UK cf. Table 4.6) juridical double taxation

would normally be eliminated provided that sufficient taxes are imposed in the residence

state to accommodate an ordinary credit. If the residence state calculates foreign tax credit

on a net income basis (Germany, Luxembourg, Spain and Sweden), juridical double taxation

would normally be eliminated provided that the level of expenses allocated to the dividend is

almost identical in the source state and residence state and that the tax rate in the source

state does not exceed the tax rate in the residence state. Option 4 would not remove all dis-

crimination of cross-border dividends in the source state and residence state. In addition,

Option 4 would not of itself eliminate economic double taxation and seems to be difficult to

implement in practice.

Option 5 would in most cases reduce existing problems by reducing the level of WHT.

Whether juridical double taxation of cross-border dividends would be eliminated depends,

among other things, on how foreign tax credit is calculated in the residence state, the level of

expenses that may be allocated to the dividend income under the domestic tax laws of the

source state and residence state and the level of tax rates in the source state and residence

state. However, given that the withholding tax rate would be low, it is likely that this will

happen in most cases, besides those where there is no actual taxation at the CIV level. Op-

tion 5 would not remove all discrimination of cross-border dividends in the source state and

residence state. In addition, Option 5 would not of itself eliminate economic double taxa-

tion. By implementing an EU wide information exchange system, this option would provide

tax administrations with adequate safeguards and would justify the application of the re-

duced rate at source rather than by means of refund. It should also reduce the compliance

cost for investors of crediting WHT in the residence country since the residence state would

dispose of the necessary information.

Option 6 and 7 are far more far-reaching. Under Option 6, juridical double taxation of

cross-border dividends would normally be eliminated by requiring the residence state to pro-

vide a full credit relief. As in Option 3 this would imply that governments might refund sur-

plus tax. Option 6 would reduce economic double taxation to a very large degree by requir-

ing the residence state to grant ordinary credit relief for underlying corporate tax in the

source state. The solution will remove compliance costs for the tax payer of applying for re-

fund, but could also imply that the resident tax payer is allowed to credit foreign, but not

domestic, corporate tax rates when calculating the dividend tax burden. If Option 6 was to

be implemented, it should be accompanied by a proposal that credit for underlying corpo-

rate tax should also apply to domestic dividends in order to avoid a new distortion between

domestic and cross-border investments.

Option 7 would remove both juridical and economic double taxation of cross-border divi-

dends. Moreover, discrimination of cross-border dividends would be removed. Unless do-

mestic dividend income tax is also eliminated this option would introduce distortions be-

Taxation of cross-border dividend payments within the EU

14

tween dividends obtained domestically and abroad. As in Option 6, this option should also

be accompanied by an exemption for domestic dividends in order not to create new distor-

tions between domestic and cross-border investments.

The options from an economic perspective

The report touches upon the economic impacts of the current tax regime and the economic

impacts of the proposed options. In particular, the report discusses impacts on compliance

and administrative costs cf. Table 0.1, and impacts on current distortions, cf. Table 0.2. We

find that Option 2 eliminates almost all of the distortions, but it is only Option 6 or 7 that

reduce or eliminates economic double taxation. In addition, we find that Option 4 and 5 are

the only options that do not fully eliminate juridical double taxation.

Table 0.1 Impacts of the various options on compliance and administrative costs Option 2 Option 3 Option 4 Option 5* Option 6** Option 7

Compliance cost for inves-tors reduced

Liquidity costs reduced Full No No Full Full Full

Compliance costs for apply-ing for refund reduced

Full No No Full Partial Full

Compliance costs for relief at source reduced

Partial No No Partial No Partial

Less foregone tax relief Full No No Full Full Full

Compliance costs of docu-menting WHT payments in order to receive credit in res-idence country reduced

Full No No Partial No Full

Administrative costs for Member States reduced

Simplification of tax system in source country

Yes No No Yes No Yes

Simplification of tax system in residence country

Yes No No Partial No Yes

Improved information ex-change

No No No Yes No No

Note: * Under the assumption of full information exchange. ** Assuming that treaty rates are not below 7.5 per cent. In these (rather few) situations there will be compliance costs associated with refunding excess WHT and liquidity costs

Source: Copenhagen Economics, based on the analysis in Chapter 3.

Taxation of cross-border dividend payments within the EU

15

Table 0.2 Impacts of the various options on distortions to investment decision Distortion Option 2 Option 3 Option 4 Option 5* Option 6** Option 7

From economic double taxa-tion

No No No No Partial Full

Debt rather than equity fi-nancing

No No No No Partial Full

Incentive to distribute prof-its in forms other than divi-dends

Full Full No Partial Full Full

Distortion of individual in-vestors’ incentive to carry out portfolio equity invest-ments

Full Full Partial No Full Full

Distortion to the decision whether profits should be retained or distributed

Full Full Partial No Full Full

From juridical double taxa-tion

Full Full Partial Partial Full Full

Distortions to invest abroad Full Full Partial Partial Full Full

Distortions to different in-vestment locations

Full Full Full Full No Full

Distortions to the choice of the legal form and legal ar-rangements used

Full Full Partial No Full Full

CIV’s inability to credit WHT in residence country

Investing in non-zero WHT country

Full Full No No Full Full

Note: N.R means Not Relevant. * Under the assumption of full information exchange. ** Assuming that treaty rates are not below 7.5 per cent. In these (rather few) situations there will be compliance costs associated with refunding excess WHT and liquidity costs

Source: Copenhagen Economics, based on the analysis in Chapter 5.

The options from a legal perspective

We find that parts of the existing tax law in all Member States infringe internal market prin-

ciples from a legal perspective. So doing nothing would seem to be a non-acceptable route to

take. The six proposed possible options to change the taxation have been evaluated on six

criteria applied to dividend flows in 9 countries from a legal and compliance perspective as

outlined in Table 0.2.

Taxation of cross-border dividend payments within the EU

16

Table 0.2 Legal impacts of the options to change dividend taxation in 9 selected Mem-

ber States4.

Problem Option 2 Option 3 Option 4 Option 5 Option 6 Option 7

Simplification of MS’s tax systems

7 0 0 0 0 9

Practical diffi-culties and new administration

0 0 7 7 9 0

Conflict with principle of source-country entitlement to tax

9 0 9 0 0 9

Costs related to the intro-duction of au-tomatic ex-change of in-formation

0 0 0 7* 0 0

Need to amend domestic legis-lation

7 9 7 7 9 9

Need to amend Double Tax Conventions

0 0 0 0 0 0

Note: The table depicts how many countries in the survey (9 countries in total) that could answer “yes” to the ques-tion in column 1. Note that when 7 countries have answered “yes”, the two countries answering “no” is consistently UK and Ireland. * The Mutual Assistance Directive introduces automatic information exchange from 2015 of some income categories, however not dividend income. However, by having such a system in place already, the costs of introducing automatic exchange of information in dividend income will be reduced.

Source: Copenhagen Economics based on Deloitte survey of withholding tax rates in selected EU countries.

It can be noted that all options require all (or most) Member States to amend domestic legis-

lation. Moreover, only Option 2 and 7 (abolishing withholding taxes and abolishing all port-

folio dividend taxes respectively) are the only options simplifying Member States’ tax sys-

tems. Option 4, 5 and 6 may give rise to new administration and practical difficulties.

0.3 KEY IMPACTS ON MEMBER STATES' BUDGETS AND POSSIBLE WELFARE

GAINS Our study suggests that there are several welfare effects of the proposed options. Firstly, the

current situation leads to economic and juridical double taxation of portfolio/ individual in-

vestors. The different options will to varying degrees resolve this double taxation. Secondly,

the cost of investing in portfolio equity is reduced primarily due to a lower tax burden, but

also due to reduced compliance costs.

4 The survey includes Italy, Spain, Luxembourg, Netherlands, Germany, France, Sweden, Ireland and the UK. The-se 9 countries have been selected in order to cover as much of the dividend flows as possible. The group of countries receive 89 percent and 86 percent of ingoing dividends and outgoing dividends respectively.

Taxation of cross-border dividend payments within the EU

17

Our calculations suggest that the amount of juridical double taxation in the current situation

corresponds to €3.7 billion, cf. Table 3.17. This is fully reduced in Option 2, 6 and 7. In

Option 5, the double taxation is reduced to app. €2.0 billion, while in Option 3 juridical

double taxation is almost eliminated but totals to €0.1 billion. Moreover, some simple calcu-

lations suggest that the reduced cost of capital will increase the capital stock and lead to an

increase in EU's total GDP between 0.03-0.05 per cent (app. €3.0 – 6.4 billion) per year.

This is due to the growth effects of increasing the supply of capital.

Moreover, compliance costs for investors will be reduced in some of the options. We have

been able to quantify liquidity cost and compliance cost related to applying for refund re-

spectively, cf. Table 0.3. Since we have only quantified some of the compliance cost reduc-

tions, the total macroeconomic impacts can be expected to exceed these numbers. In addi-

tion, the capital stock may also increase since the reduced taxation of cross-border dividend

payments between EU countries will make such investments more attractive relative to in-

vesting in other locations (domestically or in a non-EU country) or relative to making other

types of investments.

Table 0.3 Quantifiable costs to investors in the different options Impacts Option 1 Option 2 Option 3 Option 5 Option 6 Option 7

Direct impact on investors 30 0 30 6 0 0

Liquidity costs 16 0 16 3 0 0

Compliance costs for applying for refund 14 0 14 3 0 0

Juridical double taxation 3,709 0 122 1,961 0 0

Note: All figures are in million EUR. Liquidity cost is found by considering the total amount excess collected WHT. Compliance cost for applying for refund is found by considering the refundable amount which is 70 per cent of the excess collected WHT.

Source: Copenhagen Economics.

All options will also lead to some direct reductions in tax revenues which vary across the dif-

ferent options from app. €1.7 billion in Option 5 to €8 billion in Option 7. The reduction

in tax revenue corresponds to the same amount as the reduction in investors’ tax burden.

The relevant question is thus whether the proposed options to reform is a good investment

compared to other uses of public revenue. This should also be seen in the perspective that a

vast amount of Member States’ current tax revenue from dividend taxation occurs through

double taxation and foregone tax relief, which investors are entitled to. Hence, by improving

the current situation, investors will receive a larger share of what they would have received

were it not for double taxation and foregone tax relief. We find that in most options – put

very crudely - the welfare gain from reducing the cost of capital outweighs the loss in tax rev-

enue as a per centage of GDP. Moreover, there are also legal reasons to improve the current

situation, since it may be infringing EU law.

Taxation of cross-border dividend payments within the EU

18

When a company is making profits it may choose to pay out dividends as a return to the eq-

uity investments made by its shareholders.

There is an inherent risk of double or multiple taxation of dividends when they are paid

across borders. In such cases there are generally three layers of taxation:

- Corporate income tax on the profits of the dividends distributing company in its

Member State of residence

- Withholding tax on the dividend payment to the non-resident investor in the

source Member State and

- Income tax in the investor's Member State of residence.

Dividend payments between Member States' associated companies are in principle exempt

from withholding tax under the Parent-Subsidiary Directive5 provided that certain share-

holding and other requirements are met. However, as these requirements are not met in the

case of individual shareholders and of companies with a mere portfolio shareholding, divi-

dend payments to such recipients are not covered by the Directive.

Withholding taxes play an important role in dividing taxing rights between a source state of

income and the state of residence of an investor. They also help to enforce taxation, thereby

preventing tax avoidance and evasion by taxpayers. Nevertheless, the fact that cross-border

dividend payments are subject to taxes in two Member States can lead to several problems.

Withholding taxes may give rise to juridical6 or economic7 double taxation, there may be dis-

crimination of non-resident investors and there may, consequently, be distortions of invest-

ment decisions (e.g. with regard to the type or location of the investment, etc) in the Inter-

nal Market.

Double Tax Conventions (DTCs) based on the OECD Model reduce juridical double taxa-

tion on dividends typically by limiting source State taxation on the dividends and by requir-

ing a State of residence of an investor to grant relief for source State taxation through a credit

or exemption mechanism. However, source State withholding taxes, even when reduced un-

der DTCs, may not be completely creditable in the State of residence.

5 Council Directive 90/435/EEC of 23 July 1990 on the common system of taxation application in the case of par-ent companies and subsidiaries of different Member States, amended by Council Directive 2003/123/EC of 22 De-cember 2003 6 "Juridical double taxation" occurs when the same income, such as a dividend, is taxed twice in the hands of the same person: first in the source Member State, when the dividend is distributed (normally by means of withholding tax), and then in the residence Member State, when it is taxed as a part of the same shareholder's taxable income. Juridical double taxation normally occurs in cross-border situations. 7 "Economic double taxation" occurs when the same profits are taxed in the hands of two different persons, such as dividends taxed first at the level of the company paying the dividends and then in the hands of the shareholders. Such taxation can take place both at a domestic level and at an international level.

Chapter 1 CURRENT CROSS-BORDER EQUITY INVESTMENTS AND

TAXATION OF DIVIDENDS

Taxation of cross-border dividend payments within the EU

19

The Court of Justice of the European Union (CJEU) has stated8 that in principle, juridical

double taxation is not in itself unlawful, as there is no obligation for Member States to adapt

their own tax systems to the different systems of tax of other Member States in order to

eliminate the double taxation arising from the exercise in parallel of their fiscal sovereignty.

Nevertheless, juridical double taxation represents an obstacle to cross-border activity and in-

vestment within the EU, thus distorting the effective functioning of the Internal Market.

Relief from economic double taxation (i.e. for underlying corporate taxes paid by the dis-

tributing company in States of source) is often available in purely domestic situations, but

not internationally. Thus, such relief is generally not addressed in Double Tax Conventions.

Member States are not per se required to relieve economic double taxation (except in the

cases covered by the Parent Subsidiary Directive). Nevertheless, the CJEU has found that

economic double taxation might be contrary to EU law if it reflects a difference in treatment

between domestic and cross-border situations, leading to discrimination. Removing discrim-

ination in the tax treatment of dividends paid to portfolio and individual investors is a basic

requirement of EU law and a Member State may treat cross-border situations differently

from domestic situations only if this is justified by a difference in the taxpayer’s circumstanc-

es. This CJEU ruling may reduce the scope for economic double taxation of dividends, at

the level of the source state, but does not address the problem of economic double taxation

by the country of residence.

Even when source State withholding taxes are reduced under Double Tax Conventions,

non-resident portfolio and individual investors may suffer interest costs and cash flow disad-

vantages if relief at the reduced DTC rate is not provided at source. Investors may even fore-

go the tax relief to which they are entitled under Double Tax Conventions if source States'

claim procedures are complicated, costly or time-consuming.

In this respect the Commission's Recommendation on withholding tax relief procedures of

19 October 2009 suggests solutions aimed at improving the existing procedures for the re-

duction of the withholding taxes levied by the source Member States to the lower Double

Tax Convention rates. It suggests that financial intermediaries could claim relief on behalf of

their investors at source rather than by refund in return for the financial intermediaries

agreeing to provide information to tax authorities on the investors on behalf of whom they

are claiming relief. This Recommendation would, if applied by Member States, ensure the

proper and timely implementation of solutions to the problem of juridical double taxation

to the extent that those solutions are provided for by Double Tax Conventions. However, it

would not resolve problems of juridical double taxation not addressed in Double Tax Con-

ventions, nor would it resolve the problem of economic double taxation.

8 See cases C-513/04, Kerckhaert and Morres, of 14 November 2006, C-67/08, Block, of 12 February 2009 and C- 128/08, Damseaux, of 16 July 2009.

Taxation of cross-border dividend payments within the EU

20

Finally, the reality that the majority of portfolio and individual investors hold their invest-

ments indirectly via collective investment vehicles (CIVs) rather than directly in companies,

creates additional layer of issues related to the tax treaty entitlement in the source state and

availability of foreign tax credit in the residence state of the portfolio/individual investor.

All these legal and economic problems arising when cross-border dividends are paid to port-

folio/individual investors result in numerous distortions presented in more detail above.

The purpose of this chapter is to review the current cross-border equity investments and the

taxation of cross-border dividends in the EU. In Section 1.1 we outline how portfolio inves-

tors may structure their equity investments. In Section 1.2 we provide an overview of the

current cross-border portfolio dividend flows between EU Member States to understand the

importance of such payments both for the EU as a whole and for different EU Member

States.

1.1. STRUCTURING OF CROSS-BORDER PORTFOLIO EQUITY INVESTMENTS There are many ways in which an investor in one country can make an equity investment in

another country and each alternative has different tax implications in the source and resi-

dence country. Below we will describe some of the mechanisms that are at play when inves-

tors make equity investment abroad. We will provide more details on the taxation of divi-

dends in Section 1.3.

When an individual buys shares in a foreign company it makes a direct equity investment

(shareholding>10%) or a portfolio equity investment (shareholding<10%). In most cases,

the source country charges a WHT on outbound dividends. Most countries have domestic

WHT rates (called non-treaty rates throughout the report) but these rates may be reduced

through a tax treaty between the source and the residence country (the treaty rate). When

there is relief at source and the investor is able to prove that he is eligible for the reduced rate

under the tax treaty, the WHT is automatically reduced to the treaty rate. When relief at

source is not granted, the investor will pay the non-treaty rate. The excess WHT (the differ-

ence between the non-treaty and the treaty rate) may be refunded if the investor applies for

this in the source country. Portfolio/ individual investors are also generally subject to tax on

the dividend income in the residence country. International juridical double taxation is in

most cases relieved in the residence country by way of a foreign tax credit.

The mechanisms at play in this type of investment are sketched in Figure 1.1. We note that

the same situation arises in cases where a non-financial company makes a portfolio equity

investment although the WHT rate on outbound dividends in the source country and the

tax on dividend income in the residence country are in many cases different for the two in-

vestor types.

Taxation of cross-border dividend payments within the EU

21

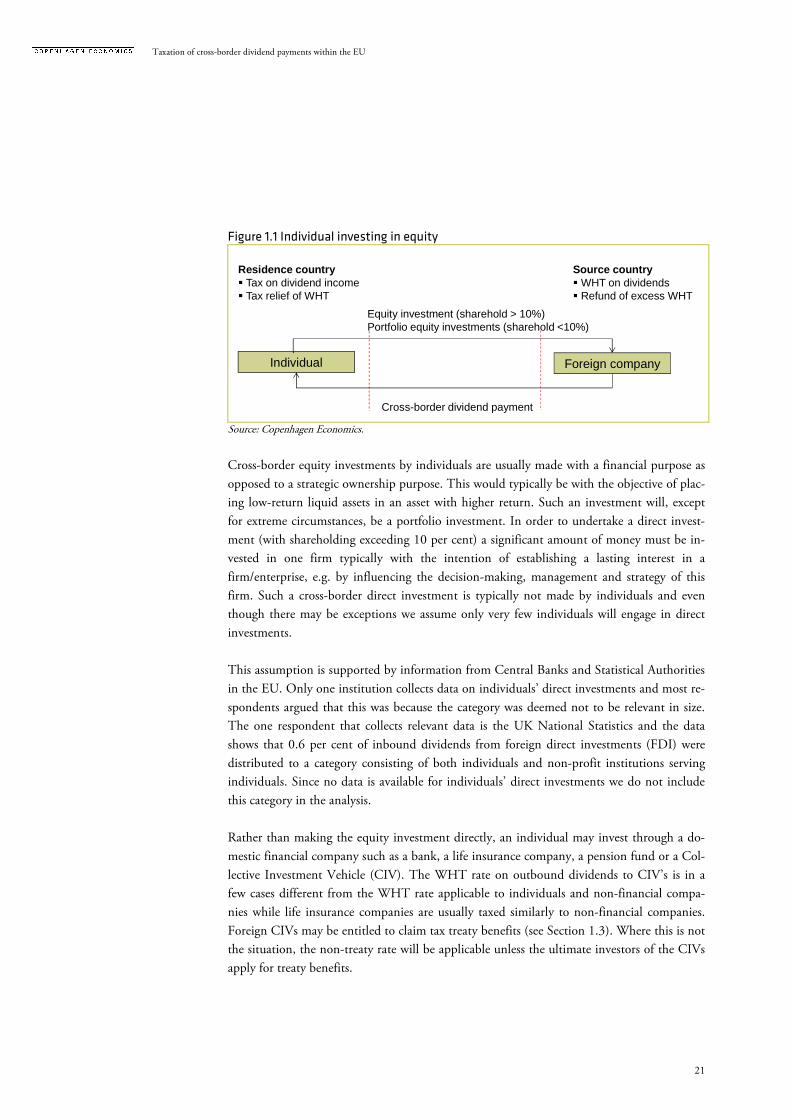

Figure 1.1 Individual investing in equity

Source: Copenhagen Economics.

Cross-border equity investments by individuals are usually made with a financial purpose as

opposed to a strategic ownership purpose. This would typically be with the objective of plac-

ing low-return liquid assets in an asset with higher return. Such an investment will, except

for extreme circumstances, be a portfolio investment. In order to undertake a direct invest-

ment (with shareholding exceeding 10 per cent) a significant amount of money must be in-

vested in one firm typically with the intention of establishing a lasting interest in a

firm/enterprise, e.g. by influencing the decision-making, management and strategy of this

firm. Such a cross-border direct investment is typically not made by individuals and even

though there may be exceptions we assume only very few individuals will engage in direct

investments.

This assumption is supported by information from Central Banks and Statistical Authorities

in the EU. Only one institution collects data on individuals’ direct investments and most re-

spondents argued that this was because the category was deemed not to be relevant in size.

The one respondent that collects relevant data is the UK National Statistics and the data

shows that 0.6 per cent of inbound dividends from foreign direct investments (FDI) were

distributed to a category consisting of both individuals and non-profit institutions serving

individuals. Since no data is available for individuals’ direct investments we do not include

this category in the analysis.

Rather than making the equity investment directly, an individual may invest through a do-

mestic financial company such as a bank, a life insurance company, a pension fund or a Col-

lective Investment Vehicle (CIV). The WHT rate on outbound dividends to CIV’s is in a

few cases different from the WHT rate applicable to individuals and non-financial compa-

nies while life insurance companies are usually taxed similarly to non-financial companies.

Foreign CIVs may be entitled to claim tax treaty benefits (see Section 1.3). Where this is not

the situation, the non-treaty rate will be applicable unless the ultimate investors of the CIVs

apply for treaty benefits.

Residence country� Tax on dividend income� Tax relief of WHT

Source country� WHT on dividends� Refund of excess WHT

Individual Foreign company

Equity investment (sharehold > 10%)Portfolio equity investments (sharehold <10%)

Cross-border dividend payment

Taxation of cross-border dividend payments within the EU

22

The residence country taxation of cross-border dividends of a domestic financial company

depends on the type of financial company. CIVs are often tax exempt on dividend income

(or are entitled to a tax deduction for provisions set up for obligations towards the ultimate

investors). However, an individual is typically taxed on its dividend income from a domestic

financial company. Other financial companies (such as life insurance companies and pension

funds) typically accumulate the dividend income with the individual investor being taxed

once the accumulated savings are paid out. The taxation may be either of a capital gain or

capital income character at this stage. If the original investment were tax deductible against

income, then their payout will typically also be taxable as income.

The residence country usually offers a foreign tax credit for WHT paid by a domestic finan-

cial company on inbound dividends. The mechanisms at play in this type of investment are

sketched in Figure 1.2.

Figure 1.2 Individuals investing in equity via domestic financial companies

Note: In official statistics an individual investment in a financial company will be classified as an equity invest-

ment even though the individual purchases an investment certificate and not equity per se. Moreover, “investments“ from individuals in pension funds and insurance companies are not considered

investments as such but pension contributions and insurance premiums. Consequently, returns from such vehicles are not dividends but other types of capital income such as pension and/or insurance disburse-ment.

Source: Copenhagen Economics.

The individual investor may also invest through a foreign financial company. When the for-

eign financial company makes an equity investment in a third country, there will be two

cross-border dividends: (i) the foreign company in the third country pays out dividends to

the financial company, and (ii) the financial company pays out dividends to the individual.

From a tax perspective, the consequence of such an intermediate country depends on wheth-

er the foreign financial company is eligible or non-eligible for tax treaty benefits. Here, it is

important to note that the tax status may be different in the three countries involved (cf.

Section 1.3).

When the financial company is non-eligible for tax treaty benefits in the source country, in-

formation on the ultimate investor (the individual) is often unknown to the source country

and the WHT rate charged will be the non-treaty rate which is often higher than the treaty

rate. When the financial company is eligible for tax treaty benefits in the source country, the

Domestic financial company Foreign companyIndividual

Dividend payment

Portfolio equity investment Portfolio equity investment

Cross-border dividend payment

Residencecountry� Tax on dividend income� Tax relief of WHT

Source country� WHT on dividends� Refund of excessWHT

Taxation of cross-border dividend payments within the EU

23

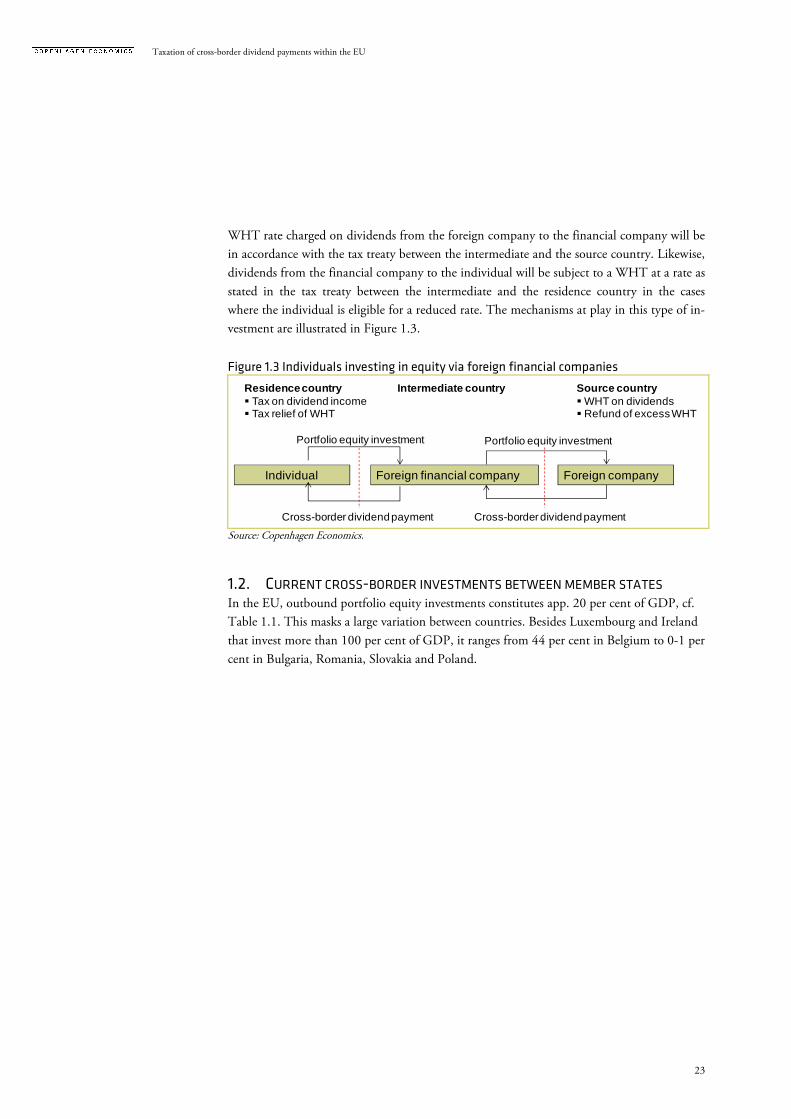

WHT rate charged on dividends from the foreign company to the financial company will be

in accordance with the tax treaty between the intermediate and the source country. Likewise,

dividends from the financial company to the individual will be subject to a WHT at a rate as

stated in the tax treaty between the intermediate and the residence country in the cases

where the individual is eligible for a reduced rate. The mechanisms at play in this type of in-

vestment are illustrated in Figure 1.3.

Figure 1.3 Individuals investing in equity via foreign financial companies

Source: Copenhagen Economics.

1.2. CURRENT CROSS-BORDER INVESTMENTS BETWEEN MEMBER STATES In the EU, outbound portfolio equity investments constitutes app. 20 per cent of GDP, cf.

Table 1.1. This masks a large variation between countries. Besides Luxembourg and Ireland

that invest more than 100 per cent of GDP, it ranges from 44 per cent in Belgium to 0-1 per

cent in Bulgaria, Romania, Slovakia and Poland.

Foreign financial company Foreign companyIndividual

Cross-border dividend payment

Portfolio equity investment Portfolio equity investment

Cross-borderdividend payment

Residencecountry� Tax on dividend income� Tax relief of WHT

Intermediate country Source country� WHT on dividends� Refund of excessWHT

Taxation of cross-border dividend payments within the EU

24

Table 1.1 Outbound portfolio equity investments

Country Total outgoing portfolio invest-

ments (EUR) Outgoing portfolio investments

as a share of GDP

Luxembourg 329.110 791%

Ireland 198.211 129%

Belgium 156.655 44%

Netherlands 177.618 30%

Sweden 103.825 30%

Finland 44.745 25%

Germany 425.209 17%

Italy 252.467 16%

Denmark 36.902 16%

France 285.815 15%

United Kingdom 237.686 14%

Austria 38.821 14%

Portugal 19.618 11%

Malta 632 10%

Estonia 888 6%

Spain 64.000 6%

Cyprus 1.034 6%

Hungary 5.346 5%

Greece 11.707 5%

Czech Republic 6.298 4%

Slovenia 1.291 4%

Lithuania 822 3%

Latvia 388 2%

Poland 3.613 1%

Bulgaria 271 1%

Slovak Republic 409 1%

Romania 394 0%

EU 27 2.403.775 20%

Note: Data from 2009. Source: Copenhagen Economics based on data from Coordinated Portfolio Investment Survey Database (CPIS)-

IMF (extract April 2012). GDP data is from Eurostat.

Inbound portfolio equity investments in EU similarly constitute 20 per cent of GDP (per

definition). Luxembourg’s inbound investments as share of GDP is a massive 2,000 per cent

while Ireland’s is 104 per cent, cf. Table 1.2. In addition to these two countries, Portugal has

a share of 26 per cent of GDP while Lithuania, Latvia, Romania, Slovenia, and Slovakia has

app. 1 per cent inbound portfolio investments as share of GDP.

Taxation of cross-border dividend payments within the EU

25

Table 1.2 Inbound portfolio equity investments

Country Total ingoing portfolio invest-

ments (EUR) Ingoing portfolio investments as

a share of GDP

Luxembourg 864.095 2077%

Ireland 160.625 104%

Portugal 44.979 26%

Finland 41.769 23%

Netherlands 110.004 19%

Cyprus 3.076 18%

United Kingdom 286.117 17%

France 273.123 14%

Belgium 44.275 13%

Sweden 43.451 13%

Germany 267.445 11%

Spain 103.221 10%

Malta 544 9%

Austria 19.439 7%

Denmark 14.888 6%

Italy 98.270 6%

Hungary 4.366 4%

Greece 9.035 4%

Poland 9.446 3%

Estonia 326 2%

Czech Republic 2.811 2%

Bulgaria 553 2%

Lithuania 355 1%

Latvia 152 1%

Romania 886 1%

Slovenia 192 1%

Slovak Republic 330 1%

EU 27 2.403.775 20%

Note: Data from 2009. Inbound portfolio investments corresponds to outbound investments from other EU Member States.

Source: Copenhagen Economics based on data from Coordinated Portfolio Investment Survey Database (CPIS)- IMF (extract April 2012). GDP data is from Eurostat.

The amount of outbound portfolio equity investments as a share of total outbound equity

investments (direct and portfolio investments) differ across countries, and varies from 16 per

cent in Slovakia to 82 per cent in Luxembourg, cf, Table 1.3. This picture naturally covers

large variety in the total size of investments. For the EU countries, the share of portfolio in-

vestments to direct investments is app. 34 per cent.

Taxation of cross-border dividend payments within the EU

26

Table 1.3 Outbound portfolio equity investments as a share of total outbound equity

investments

Country Outbound portfolio investments as a share of total

outbound investments

Luxembourg 82%

Ireland 68%

Romania 63%

Slovenia 62%

Malta 59%

Latvia 59%

Hungary 51%

Italy 50%

Lithuania 45%

CzechRepublic 41%

Germany 40%

Finland 40%

Denmark 40%

Greece 39%

France 39%

Sweden 39%

Austria 35%

Bulgaria 34%

United Kingdom 30%

Poland 28%

Estonia 24%

Spain 20%

Cyprus 20%

Slovakia 16%

Belgium N.A

Netherlands N.A

Portugal N.A

EU 27 47%

Note: Total equity investments equals: Foreign direct equity investments and portfolio equity investments abroad. Data is available in Table 4.5 in the Appendix. Data on direct investments were not available for the Netherlands, Belgium and Portugal. The data for FDI does not cover investments made by Special Purpose Entities which is only collected for an EU aggregate. Data is for 2009.

Source: IMF – Coordinated Portfolio Investment Survey Database (CPIS) for portfolio data (extract April 2012). Eurostat is used for data on direct equity investments.

Taxation of cross-border dividend payments within the EU

27

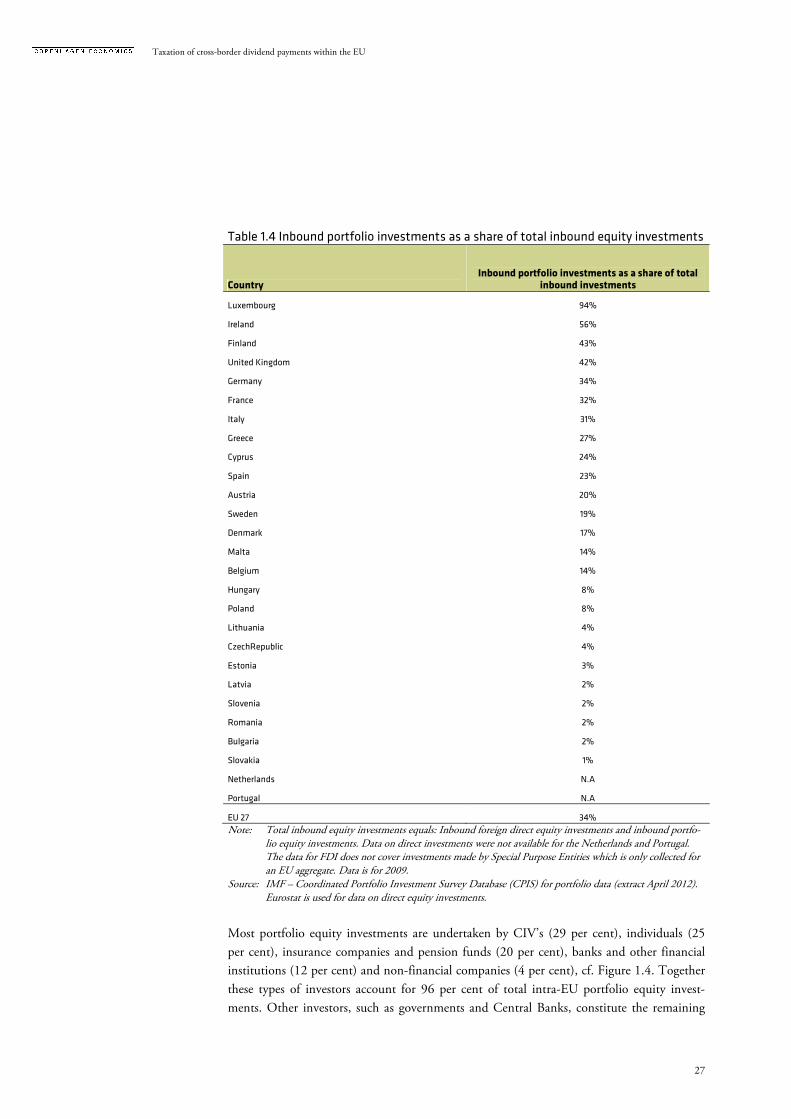

Table 1.4 Inbound portfolio investments as a share of total inbound equity investments

Country Inbound portfolio investments as a share of total

inbound investments

Luxembourg 94%

Ireland 56%

Finland 43%

United Kingdom 42%

Germany 34%

France 32%

Italy 31%

Greece 27%

Cyprus 24%

Spain 23%

Austria 20%

Sweden 19%

Denmark 17%

Malta 14%

Belgium 14%

Hungary 8%

Poland 8%

Lithuania 4%

CzechRepublic 4%

Estonia 3%

Latvia 2%

Slovenia 2%

Romania 2%

Bulgaria 2%

Slovakia 1%

Netherlands N.A

Portugal N.A

EU 27 34%

Note: Total inbound equity investments equals: Inbound foreign direct equity investments and inbound portfo-lio equity investments. Data on direct investments were not available for the Netherlands and Portugal. The data for FDI does not cover investments made by Special Purpose Entities which is only collected for an EU aggregate. Data is for 2009.

Source: IMF – Coordinated Portfolio Investment Survey Database (CPIS) for portfolio data (extract April 2012). Eurostat is used for data on direct equity investments.

Most portfolio equity investments are undertaken by CIV’s (29 per cent), individuals (25

per cent), insurance companies and pension funds (20 per cent), banks and other financial

institutions (12 per cent) and non-financial companies (4 per cent), cf. Figure 1.4. Together

these types of investors account for 96 per cent of total intra-EU portfolio equity invest-

ments. Other investors, such as governments and Central Banks, constitute the remaining

Taxation of cross-border dividend payments within the EU

28

four per cent. These investors are not included in the analysis since they are typically not

subject to taxation. Since they constitute a relatively small amount of total dividend flows

their exclusion will not have much impact on the results. It has not been possible to obtain

information on the number of investors engaging in portfolio equity investments.

Figure 1.4 Composition of intra-EU portfolio equity investments

Note: We label the investor group called mutual funds as CIV’s in the following. The data used is for the 17

countries shown in Figure 1.5. The large share of individual investors is driven mainly by Germany for which individual investors' share is on average 50%.

Source: IMF – Coordinated Portfolio Investment Survey Database (CPIS), extracted March 2012.

1.3. CURRENT CROSS-BORDER DIVIDEND FLOWS BETWEEN MEMBER STATES Total inbound portfolio dividend payments are very unevenly distributed across EU Mem-

ber States. Luxembourg is the main recipient of cross-border portfolio dividend payments

(when calculated as a share of GDP) followed by Ireland and Belgium, cf. Figure 1.5.

Individuals23%

Non-financial companies

4%

Insurance companies and pension funds

19%

CIV's31%

Banks and other financial

institutions19%

Other investors including

governments and central banks

4%

Taxation of cross-border dividend payments within the EU

29

Figure 1.5 Total inbound portfolio dividends in Member States as a share of GDP

Note: Data calculated as an average from 2004-2009. Dividend data is incomplete for Malta. For Belgium, Bul-

garia, Cyprus, Denmark, Finland, Germany, Latvia, Slovenia and UK data has been provided by Central Banks. For Portugal we have estimated the data based on investment data.

Source: Copenhagen Economics calculations based on Eurostat data supplemented with data from Central Banks. See Annex Table 4.9 for amounts in Euro.

Figure 1.6 Total outbound portfolio dividends in Member States as a share of GDP

Note: Data calculated as an average from 2004-2009. Dividend data is incomplete for Bulgaria and Malta. For Luxembourg, Portugal, Germany, UK and France dividends are combined from data provided from Cen-tral Bank data and through the CE estimation method.

Source: Copenhagen Economics calculations based on Eurostat data supplemented with data from Central Banks. See Annex Table 4.10 for amounts in Euro

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

5,0%

pct. of GDP

18 %

26 %

0,5%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%

Taxation of cross-border dividend payments within the EU

30

Bilateral dividend data is not available from official sources and has been collected/estimated

for the purposes of this report, cf. Box 1.1.

Box 1.1 Short description of how we obtain bilateral dividend data per investor type We are interested in obtaining data on dividends paid out as a return on portfolio equity investments be-tween all pairs of EU Member States and for each type of investor. How we obtain bilateral dividend data Portfolio dividend data is available for most EU countries on an aggregate level. Data on bilateral dividend payments between EU Member States is not available from official sources. To obtain this data we have followed a two step procedure:

1) We have enquired Central Banks (CBs) and Statistical Authorities (Stats) of the EU Members States for the availability of the relevant data. Through such direct enquiries we have received data for 16 countries9 (some available under confidentiality restrictions).

2) For the remaining countries we have estimated the data by using data on bilateral portfolio in-vestment relationships (see description underneath). This data was available for 10 additional countries.10

Our method to estimate data on bilateral dividends is illustrated in the following example with three coun-tries:

We have data on total dividend flows going into France (from Eurostat) which amount to approxi-mately €5.073 million.11 We assume that there are no systematic deviations in the returns obtained by French portfolio investments in other EU countries. We therefore assume that the share of France’s total dividends that comes from Belgium, for example, will be equal to the share of total French port-folio investments invested in Belgium. Data from the IMF CPIS database show that 5 per cent of total French portfolio investments are invested in Belgium and our estimate of dividend payments from Belgium to France will therefore be €332 million (5% of €5.073 million). By using the split of French portfolio investments across countries we can map out total inbound dividends from these countries. This method is repeated for the countries where we lack bilateral dividend data from Central Banks and Statistical Authorities.

By these two steps we are able to obtain data for 26 countries. For the one remaining country (Malta) no data is available from the CBs or from the CPIS database. The only data available stems from Central Banks or Statistical Authorities in other countries who have reported data on outbound dividends to Malta. In-bound dividends to Malta are therefore uncertain and incomplete and cannot be used conclusively. For the countries where we both have data from Central Banks and from our estimation method, it can be seen that the real data and the estimated data are indeed quite similar. See Appendix 2.1-2.3 for more on data requirements and availability. How we split bilateral dividend data per type of investor If all types of investors were taxed at the same rate then we could use data on bilateral dividends between EU countries to assess the economic impacts of the current situation in Chapter 2 and of the proposed op-tions in Chapter 3. However, different types of investors are in most cases taxed differently both in the source country and in the residence countries. In the source country, it is not always the case that all types of investors are entitled to treaty benefits (e.g. CIVs). In the residence countries, CIV’s are rarely taxed on their dividend income whereas other investors are taxed according to their respective income tax rates. We therefore need to attribute total dividends to each investor. In some cases the data on bilateral dividends provided by the Central Banks and Statistical Authorities is already split according to investor type. For the remaining countries we will obtain the split by a method il-lustrated in the following example:

We have data on France’s portfolio investments by each type of investor. We assume that the rate of return to all French portfolio investments in Belgium is the same irrespective of which type of investor

9 Belgium, Bulgaria, Cyprus, Denmark, Estonia, Finland, Germany, Greece, Ireland, Italy, Latvia, Poland, Slovak Republic, Slovenia, Sweden and UK. 10 Austria, Czech Republic, France, Hungary, Luxembourg, Netherlands, Portugal, Romania and Spain. It was not possible to obtain any data for Malta. 11 When taking an average from 2004-2009.

Taxation of cross-border dividend payments within the EU

31

makes the investment. For example, if five per cent of France’s investments in Belgium are made by individuals we assume that five per cent of the €332 millions dividends flowing from Belgium to France flow to individuals (equal to €16.6 millions). These dividends will then be taxed both in the source and in the residence country according to the investor type and nationality.

For Luxembourg and Ireland we applied a different method to assess the investor split since much dividend flow between two Member States pass through these countries’ (especially Luxembourg) CIV’s. The meth-od is based described in Box 2.1 in the Appendix. Using these three methods in combination we are able to obtain data for 26 countries. Results for Malta are not reported as we have not been able to obtain data for bilateral dividend or investment flows.

Source: Copenhagen Economics.

Luxembourg, and to a large extent also Ireland, are in many ways a special case. This is pri-

marily the case since the countries are home for a vast number of financial companies such as

investment funds and other collective investment vehicles. This implies that while income

derived by e.g. mutual funds in most countries is distributed to individuals in the same

country, Luxembourg acts as a transit country for dividend flows. We have been able to de-

rive data on cross border dividend flows to and from Luxembourg, which means that we will

catch both dividends going into Luxembourg based CIVs from other countries, and the div-

idends distributed from Luxembourg CIVs to shareholders in other countries. Due to the

special case of Luxembourg we have made the assumption, that Luxembourg does not earn

dividend tax income from the dividends being distributed from the CIVs. This is contrary to

our general assumption that dividend income earned by CIVs is taxed by the dividend in-

come tax rate for individuals. This assumption is made, since dividend income to CIVs in

general will – eventually – be distributed to individuals.

The fact that Luxembourg is a “transit” country for dividend flows is confirmed by the large

share of outbound dividends related to GDP (amounting to 26 per cent), cf. Figure 1.6. The

EU average outbound dividend flow is 0.5 per cent of GDP.

1.4. THE CURRENT TAXATION OF CROSS-BORDER DIVIDENDS WHT on cross-border portfolio dividends allows the taxing rights to be shared between the

source country and the residence country. WHT help to enforce taxation, thereby prevent-

ing tax avoidance and evasion. Dividend payments between associated companies are cov-

ered by the Parent-Subsidiary Directive and are therefore exempt from WHT. Cross-border

portfolio dividends and dividends received by individual investors regardless of their share-

holdings are not covered by the Directive.

The current system of different national WHT schemes creates distortions in intra-EU in-

vestment behaviour. Even though several bilateral double taxation treaties aim to treat WHT

in a common framework, large variations exist both with respect to the scope of WHT’s and

to the rate of WHT and domestic dividend income tax respectively. As discussed in the fol-

lowing chapter, this gives rise to juridical double taxation. Moreover, the current situation

also gives rise to economic double taxation, since dividend income tax is paid in the resi-

dence country on dividend income which has already been taxed via corporate tax at the

Taxation of cross-border dividend payments within the EU

32

firm level (see also the discussion in the following section). Such double taxation will distort

investments and reduce the overall amount of portfolio equity investments, since the cost of

investing is increased.

There is reason to believe that the distortions and other problems may get worse over time.

Except for the outbreak of the financial crisis in 2008, we find EU Member States tend to

receive an increasing amount of intra-EU cross border dividends from portfolio investments

for a number of countries, cf. Figure 1.7. From 2004 to 2008 dividends from portfolio equi-

ty investments increased from app. €12 billion to almost €45 billion. This suggests that the

current situation of double taxation should be expected to get worse over time.

Figure 1.7 The potential distortions and other problems appear to be getting worse

Note: Data is not available for a number of countries: Denmark, Germany, Spain, Italy, Malta, Portugal and UK. Source: Copenhagen Economics based on Eurostat [data series: bop_q_c] extracted February 2012

The taxation of cross-border portfolio dividends is determined by the taxation of outbound

dividends in the source country on the one hand and the taxation of inbound dividends in

the residence country on the other hand. We will discuss these two options in the following.

Taxation of outbound dividends in the source country

The domestic WHT on dividends in the source country (the non-treaty rate) varies accord-

ing to investor type. The domestic WHT rates on portfolio dividend income12 across coun-

tries and investor types can be found in Appendix 4, Table 4.1. WHT varies from 1.4 per

cent13 to 30 per cent14 in the countries that impose a WHT on outbound dividends. Cyprus,

12 That is, for shareholdings below 10 percent. 13 In Italy for e.g. non-financial investors. 14 In Sweden for e.g. individual investors.

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

2004 2005 2006 2007 2008 2009 2010

million EUR

Taxation of cross-border dividend payments within the EU

33

Ireland, Malta, Portugal, the Slovak Republic and the United Kingdom neither impose

WHT on outbound dividends to individuals nor corporate investors. Greece, Hungary, Lat-

via and Bulgaria do levy WHT on individual but not on corporate investors with sufficiently

low shareholding to be deemed portfolio investors. The non-treaty WHT rate can be re-

duced according to a tax treaty between the source country and the residence country (the

treaty rate). Treaty rates between EU Member States have large variations. However, in most

cases the treaty rate is significantly lower than the non-treaty rate. The general trend is that

the treaty rate is 15 per cent for portfolio dividends. This corresponds to the tax rate laid

down in Article 10(2)(b) of the OECD Model Income Tax Convention.15

Most countries in our survey grant tax treaty benefits to CIVs, cf. Annex 6, that meet two

requirements: (i) the CIV qualify as a “person” under the tax treaty, and (ii) the CIV quali-

fies as a “resident” under the tax treaty. The situation in most countries is that some foreign

CIVs are recognized under tax treaties whereas other CIVs are not eligible for tax treaty ben-