tax

TRANSCRIPT

Zakat And Ushr

Zohaib Ahmed

Zakat is one of the fundamental institutions in Islam. In importance, it is placed next to prayer. The commandment of Zakah is often coupled with the commandment of Salah in the Holy Quran. o ع� م� ك�ع�وا� ار� و� ك�اة� الز� � آت�وا و� ال�ة� الص� يم�وا� أ�ق� و�

اك�ع�ين -الر�

“And be steadfast in prayer; Practice regular charity; and bow down your heads with those who bow down (in worship).” Surah II Verse 4 ه��الل إ�ال� ت�ع�ب�د�ون� ال� ائ�يل� ر� إ�س� ب�ن�ي يث�اق� م� ذ�ن�ا أ�خ� �ذ� إ و�

ال�ي�ت�ام�ى و� ب�ى ر� ال�ق� و�ذ�ي انا4 س� إ�ح� ال�د�ي�ن� ب�ال�و� و� � وا يم� أ�ق� و� نا4 س� ح� ل�لن�اس� � ول�وا و�ق� اك�ين� ال�م�س� و�

نك�م� م; ل�يال4 ق� إ�ال� ل�ي�ت�م� ت�و� ث�م� ك�اة� الز� � آت�وا و� ال�ة� الص�ع�ر�ض�ون م; أ�نت�م Treat with kindness; your parents and kindred, and orphans“ �-و�

and those in need; speak fair to the people; be steadfast in prayer;” Surah II Verse 83

م;ن� ك�م س� أل�نف� د;م�وا� ت�ق� ا م� و� ك�اة� الز� � آت�وا و� ال�ة� الص� يم�وا� أ�ق� و�ا ب�م� الل�ه� إ�ن� الل�ه� ند� ع� د�وه� ت�ج� Cي�ر ير .خ� ب�ص� ل�ون� ت�ع�م�

“And be steadfast in prayer and regular in charity: And whatever good ye send forth for your souls before you, ye shall find it With God: for God sees Well all that ye do.” Surah II Verse 110

Literally, Zakah means purification, growth, righteousness and blessing. It is defined in Shariah as a specific amount due in the property of Muslims to be distributed to the deserving. The obligatory character of Zakah is spelled out in Surah Taubah (9) 103.

إ�ن� م� ع�ل�ي�ه� ل; و�ص� ا ب�ه� م ك;يه� ت�ز� و� ه�م� ر� ت�ط�ه; ة4 د�ق� ص� م� ال�ه� و� م�أ� م�ن� ذ� خ�

Iيع م� س� الل�ه� و� م� ل�ه� Iك�ن س� ال�ت�ك� ص�IIع�ل�يم

"Of their properties, take alms, so that you might purify and sanctify them.”

DEFINITIONS:

Administrator-General:

“Means the person appointed as such under section 13, and includes an officer authorized by him to exercise or perform any power or function of Administrator-General under this Ordinance.”

Annuity:

“Means the sum payable periodically, according to the annuity policy conditions, to an annuitant during his life-time, or for a fixed number of years’ as the case may be, and includes the scheme of postal annuities as notified by the Government.”

Assets:

“Means assets liable to Zakat as provided in this Ordinance.”

Atiyyat:“Means voluntary donations to the Zakat funds, otherwise than on account of Zakat or Ushr, and includes sadaqat-e-nafilohs.”

Means a person appointed as such under section 15, and includes an officer authorized by him to exercise or perform any power or function of Chief Administrator under this Ordinance.

Chief Administrator:

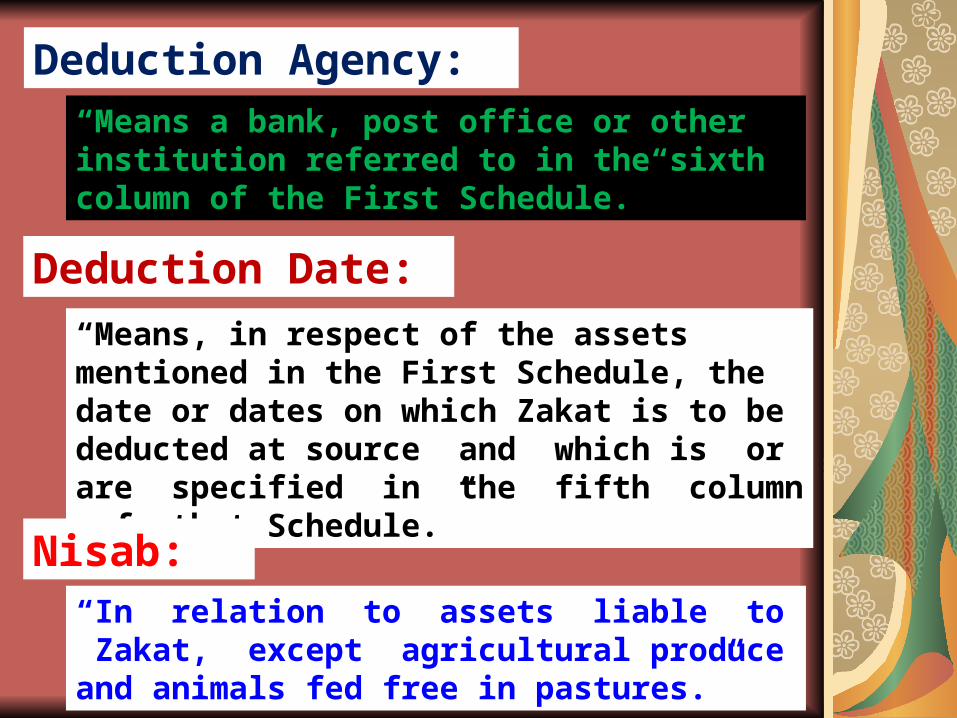

“Means a bank, post office or other institution referred to in the sixth column of the First Schedule.”

“Means, in respect of the assets mentioned in the First Schedule, the date or dates on which Zakat is to be deducted at source and which is or are specified in the fifth column of that Schedule.”

“In relation to assets liable to Zakat, except agricultural produce and animals fed free in pastures.”

Deduction Agency:

Deduction Date:

Nisab:

“Has the same meaning as in the Provident Funds Act, 1925.”

“Means a person who owns or possesses assets not less than nisaab, but does not include.”

Provident Fund:

Sahib-e-Nisab:

Zakat Year:

“Means year according to the Hijra calendar for which Zakat is chargeable, commencing on the first day of Ramadhan-ul-Mubarak and ending with the last day of the following Sha’ban-ul-Moazzam.

Charge and Collection of Zakat

Section 3 of the Zakat and Ushr Ordinance, 1980, deals with charge and collection of Ushr on the basis of some principle.

Principle of Zakat

Zakat is to be charged for each Zakat Year commencing on and from the first day of Ramadhan-ul-Mubarak.

Zakat is to charged on compulsory basis in respect of assets mentioned in the First Schedule from every sahib-e-nisab and who owns or possesses such assets on the Valuation Date and whole of the proceeding Zakat year.

Zakat is to be charged at the rate of 2.5% and in the manner specified in the First Schedule.

Note :Provided further that no Zakat shall be charged and collected from the assets

of a person who died on or before the Deduction Date.

Principle of Zakat

Deduction of Zakat

Primarily secured by that asset

Used for the creation of an asset on which Zakat is deductible at source .

Obtained from the Deducting Agency having custody of the asset securing the debt.

Exemption from Zakat Deduction

1:Assets of non Muslims

2:Person who is not a citizen of Pakistan

3:Person files a declaration on grounds of faith and fiqh.

4: Person excluded from the definition of sahib e nisaab.

5:Assets frozen under the order of

competent authority.

6:assets of a person decease on or

before the deduction date.

7:Assets acquired with or held in

foreign currency.

Exemption from Zakat Deduction

Zohaib Ahmed

CHARGES AND COLLECTION OF USHR

Section 5 of the Zakat and Ushr Ordinance, 1980, deals with charge and collection of Ushr on the basis of some principle.

Principle of Ushr

Ushr is to be charged on such date or dates as may be prescribed or as may be notified by the Administrator-General or by Chief Administrator with in his jurisdiction

Ushr is to be charged from every land owner,grantee,allottee,lease-holder or land holder in respect of his share of the produce as on the valuation date

The Ushr shall be the first charge on the produce.

The Ushr shall be collected in cash.

Where the produce consists of wheat, Ushr at the option of provincial council may be collected in kind.

Ushr is to be charged at the rates specified in the Schedule of the Zakat and Ushr Ordinance, 1980.

Principle of Ushr

He is eligible under shariah to receive Zakat.

The produce from his land is less than five wasqs (948 Kilograms) of wheat, or its equivalent in value in the case of other crops liable to Ushr.

Exempt from Ushr

Establishment of Zakat Fund

Central Zakat Fund

Provincial Zakat Fund

District Zakat Fund

Local Zakat Fund

Utilization of Zakat Funds

Assistance to the needy persons affected or rendered homeless due to natural calamities like floods and earthquakes and for their rehabilitation

Expenditure on the collection, disbursement and administration of Zakat and Ushr

Investment in any non-interest bearing instruments as is permitted under Shariah

Any other purpose permitted by Shariah.

ORGANIZATION AND ADMINISTRATION

Central Zakat Council

The Central Council shall consist of: A Chairman;

Four persons to be nominated by the president, of whom three shall be Ulema nominated in consultation with the Council of Islamic Ideology

One person from each Province, to be nominated by the President

Two women, who shall not be less than forty-five years of age, to be nominated by the President

The Chief Administrators

The Secretary to the Government of Pakistan in the Ministry of Finance.

The Secretary to the Government of Pakistan in the Ministry of Religious Affairs, Zakat and Ushr.

The Secretary to the Government of Pakistan in the Ministry of Health.

Central Zakat Council

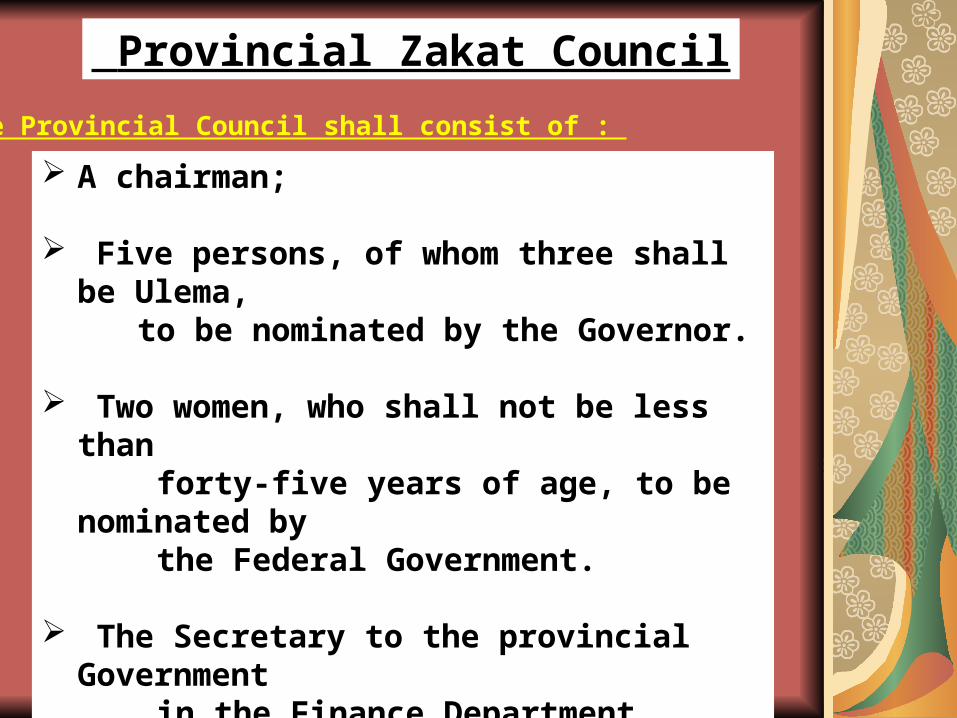

Provincial Zakat Council

The Provincial Council shall consist of :

A chairman;

Five persons, of whom three shall be Ulema,

to be nominated by the Governor.

Two women, who shall not be less than forty-five years of age, to be nominated by the Federal Government.

The Secretary to the provincial Government

in the Finance Department.

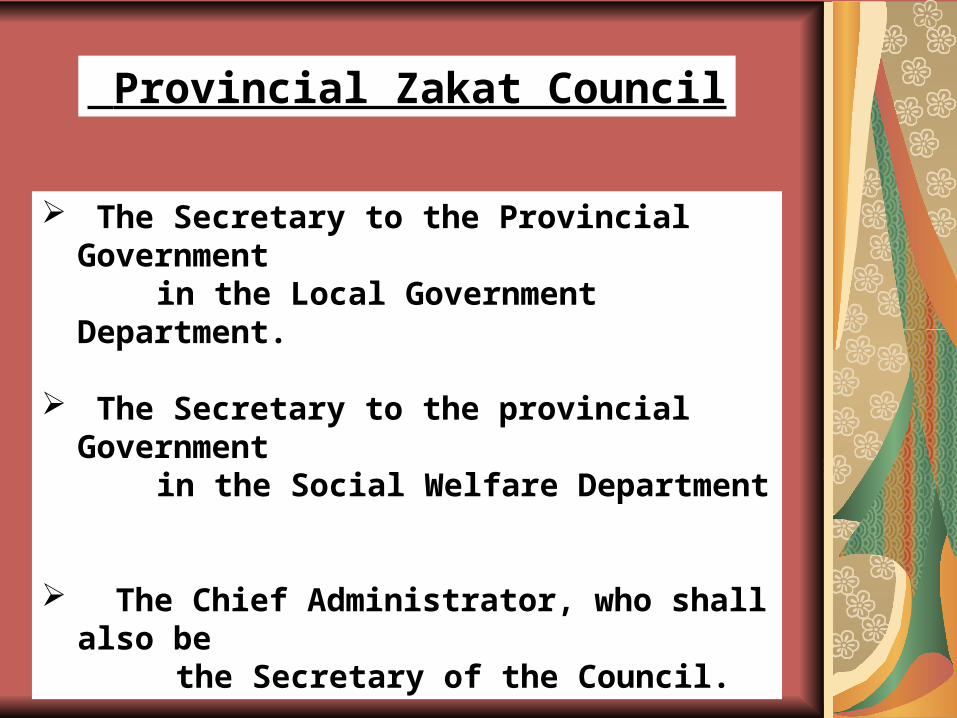

The Secretary to the Provincial Government in the Local Government Department.

The Secretary to the provincial Government in the Social Welfare Department

The Chief Administrator, who shall also be the Secretary of the Council.

Provincial Zakat Council

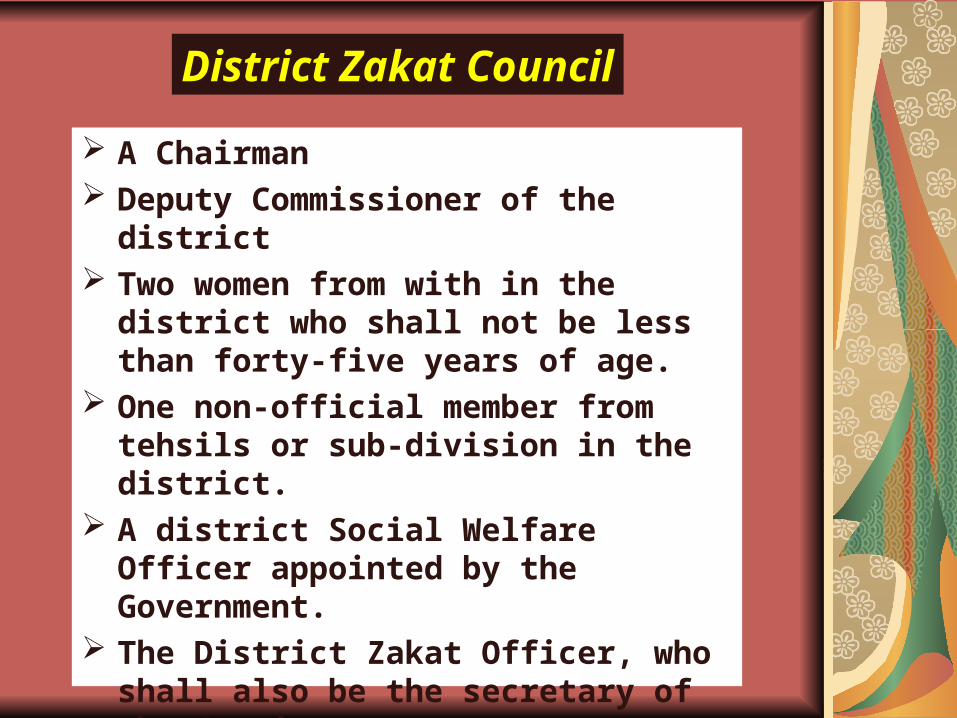

A Chairman Deputy Commissioner of the district Two women from with in the district

who shall not be less than forty-five years of age.

One non-official member from tehsils or sub-division in the district.

A district Social Welfare Officer appointed by the Government.

The District Zakat Officer, who shall also be the secretary of the Committee.

Where the number of tehsils or sub-division is less than five.

District Zakat Council

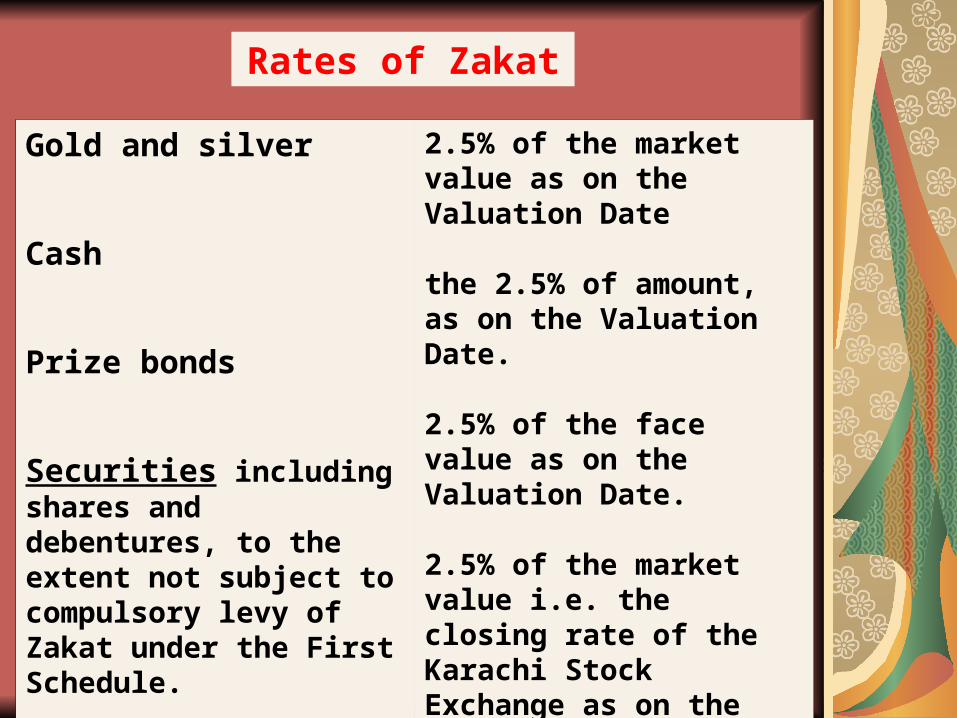

Rates of Zakat

Gold and silver

Cash

Prize bonds

Securities including shares and debentures, to the extent not subject to compulsory levy of Zakat under the First Schedule.

2.5% of the market value as on the Valuation Date

the 2.5% of amount, as on the Valuation Date.

2.5% of the face value as on the Valuation Date.

2.5% of the market value i.e. the closing rate of the Karachi Stock Exchange as on the Valuation Date.

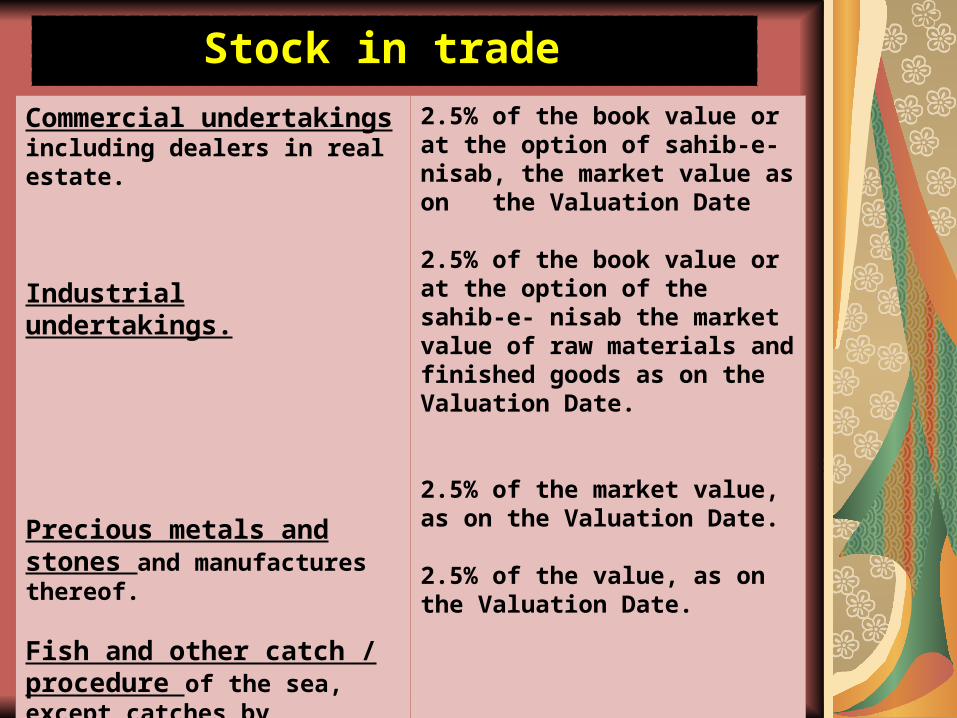

Commercial undertakings including dealers in real estate.

Industrial undertakings.

Precious metals and stones and manufactures thereof.

Fish and other catch / procedure of the sea, except catches by indigenous techniques.

2.5% of the book value or at the option of sahib-e-nisab, the market value as on the Valuation Date

2.5% of the book value or at the option of the sahib-e- nisab the market value of raw materials and finished goods as on the Valuation Date.

2.5% of the market value, as on the Valuation Date.

2.5% of the value, as on the Valuation Date.

Stock in trade

Tenant’s share.

Other than the tenant’s share.

10% of the produce, as on the Valuation Date.

5% over and above the compulsory 5% in the barani area, as on the Valuation Date.

Agricultural / including horticultural

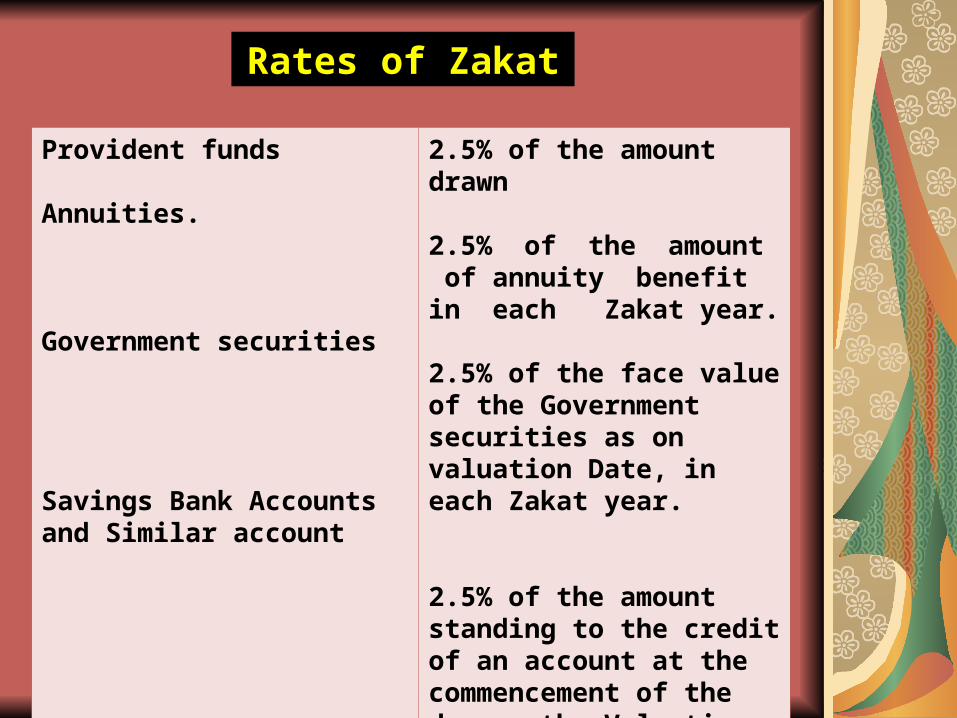

Provident funds

Annuities.

Government securities

Savings Bank Accounts and Similar account

2.5% of the amount drawn

2.5% of the amount of annuity benefit in each Zakat year.

2.5% of the face value of the Government securities as on valuation Date, in each Zakat year.

2.5% of the amount standing to the credit of an account at the commencement of the day on the Valuation Date.

Rates of Zakat

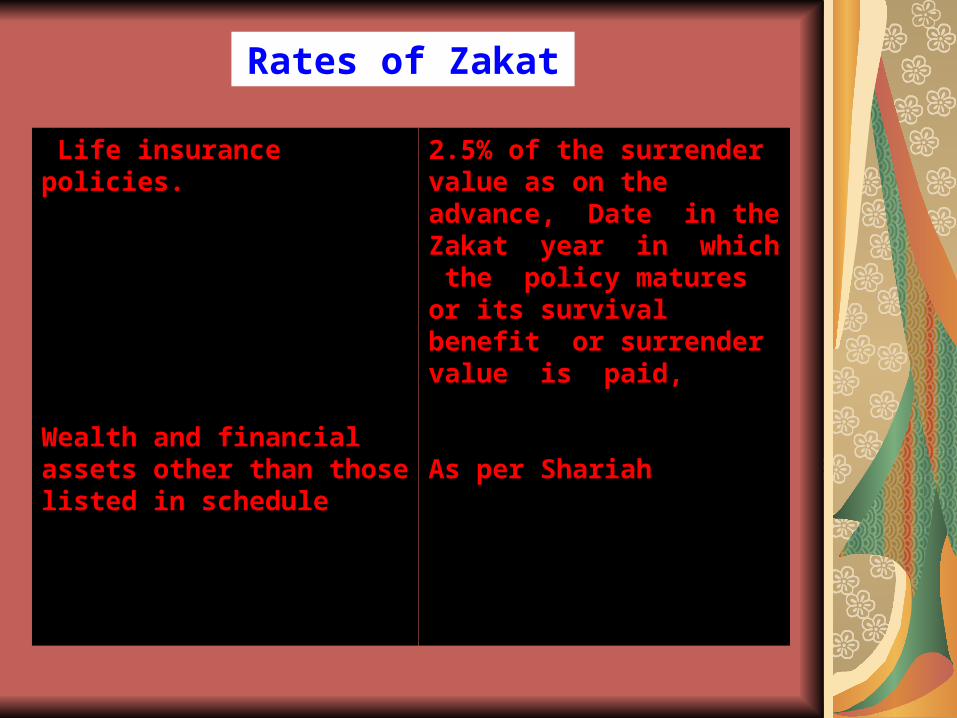

Life insurance policies.

Wealth and financial assets other than those listed in schedule

2.5% of the surrender value as on the advance, Date in the Zakat year in which the policy matures or its survival benefit or surrender value is paid,

As per Shariah

Rates of Zakat

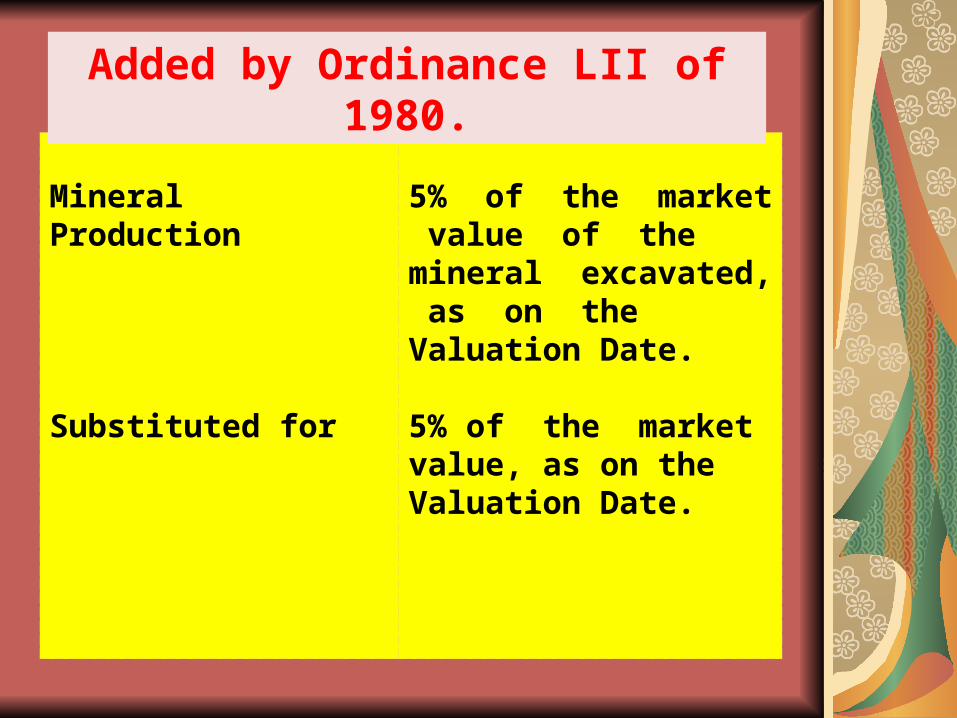

Mineral Production

Substituted for

5% of the market value of the mineral excavated, as on the Valuation Date.

5% of the market value, as on the Valuation Date.

Added by Ordinance LII of 1980.