tax provisions included in the path act of … · 1/12/2016 1 cpas & advisors tax provisions...

TRANSCRIPT

1/12/2016

1

CPAs & ADVISORS

TAX PROVISIONS INCLUDED IN THE PATH ACT OF 2015

January 12, 2016

TO RECEIVE CPE CREDIT

Participate in entire webinarAnswer polls when they are providedIf you are viewing this webinar in a group Complete group attendance form

All group attendance sheets must be submitted to [email protected] 24 hours of webinar

Answer polls when they are provided

If all eligibility requirements are met, each participant will be emailed their CPE certificate within 15 business days of live webinar

1/12/2016

2

Robert Conner, CPANational Tax Assistant [email protected]

Jesse Palmer, CPADirector of Tax Quality [email protected]

Damien Martin, CPANational Tax Assistant [email protected]

TODAY’S AGENDAIndividual Provisions

Business Provisions

Depreciation Changes

Other Provisions

Q&A

1/12/2016

3

PATH ACTProtecting Americans from Tax Hikes Act of 2015

$622 billion price tag

Enacted December 18, 2015, with bipartisan support Combined with $1.1 trillion omnibus spending package

Most were expecting temporary extension of various expired tax provisions…Received MUCH more!

Mostly taxpayer favorable

CPAs & ADVISORS

SELECT INDIVIDUAL PROVISIONS

1/12/2016

4

INDIVIDUAL PROVISIONSState & Local Sales Tax Deduction What is it? Election to claim an itemized deduction for state & local

general sales taxes in lieu of deducting state & local income taxes

Without PATH: Expired for tax years beginning after December 31, 2014

With PATH: Retroactively extended & made permanent

INDIVIDUAL PROVISIONSState & Local Sales Tax Deduction Example: The facts

• Jack & Jill are retired & live in Chicago, IL

• Received $250,000 in retirement distributions, paid $10,000 in real estate taxes & made $10,000 in charitable contributions in 2015

• Purchased a yacht in 2015 & paid $100,000 in state & local sales tax

1/12/2016

5

INDIVIDUAL PROVISIONSState & Local Sales Tax Deduction Example: The federal impact of PATH

Tax savings with the extension under PATH of $15,829

Without PATH With PATH

Adjusted gross income $500,000 $500,000

Itemized deductions 12,747 115,531

Exemptions - - - -

Taxable income 487,253 384,469

Tax liability 149,321 133,492

INDIVIDUAL PROVISIONSQualified Conservation Contributions What is it? Enhanced charitable deduction & carryforward period for

aggregate contributions of appreciated qualified real property to a qualified organization for conservation purposes

Without PATH: Expired for tax years beginning after December 31, 2014

With PATH: Retroactively extended & made permanent; modified to permit Alaska Native Corporations to deduct qualified contribution contributions up to 100% of taxable income

1/12/2016

6

INDIVIDUAL PROVISIONSCharitable Distributions from IRAs What is it? A taxpayer who is age 70 ½ & older can make tax-free

distributions from an Individual Retirement Account (IRA) to a qualified charitable organization up to $100,000 per tax year

Without PATH: Expired for tax years beginning after December 31, 2014

With PATH: Retroactively extended & made permanent

INDIVIDUAL PROVISIONSCharitable Distributions from IRAs Example: The facts

• Jack & Jill are retired & live in Chicago, IL.

• They both have required minimum distributions of $100,000 in 2015, & paid $10,000 in real estate taxes

• They would like to make charitable contributions of $200,000

1/12/2016

7

INDIVIDUAL PROVISIONSCharitable Distributions from IRAs Example: The federal impact of PATH

Tax savings with the extension under PATH of $12,094

Without PATH With PATH

Adjusted gross income $200,000 $ - -

Itemized deductions 110,000 12,600

Exemptions 8,000 8,000

Taxable income 82,000 - -

Tax liability 12,094 - -

INDIVIDUAL PROVISIONSExclusion of 100% of Gain on Certain Small Business Stock What is it? A noncorporate taxpayer may exclude all gain realized on

disposition of qualified small business stock held for more than five years subject to a per taxpayer limit. Excluded portion of gain is also excepted from treatment as an alternative minimum tax (AMT) preference item

Without PATH: Exclusion was to be limited to 50% of gain for stock acquired after December 31, 2014; 7% of excluded gain was to be an AMT preference

With PATH: Retroactively extended & 100% exclusion & exception from AMT preference treatment made permanent

1/12/2016

8

INDIVIDUAL PROVISIONSNonbusiness Energy Property Credit What is it? A taxpayer can claim a credit of 10% of qualifying expenses

for installing insulation, energy efficient exterior windows & doors & energy efficient heating & air conditioning services up to a $500 lifetime limit (with no more than $200 from windows & skylights)

Without PATH: Expired for tax years beginning after December 31, 2014

With PATH: Retroactively extended through 2016; modified to require exterior windows & doors meet Version 6.0 of Energy Star Program to qualify for credit for property placed in service after December 31, 2015

INDIVIDUAL PROVISIONSChanges to Section 529 Plan Distribution Rules Definition of qualified higher education expenses which qualify as

eligible, tax-preferred distributions from 529 accounts was expanded by PATH to include computer technology & equipment for tax years beginning after December 31, 2014

PATH modifies requirement to aggregate distributions from 529 accounts for distributions made after December 31, 2014

Tuition payments made with distributions from a 529 account & later refunded are treated as a qualified expense if refunded amount is recontributed to a 529 account within 60 days of receipt. This provision is effective for refunds received after 2014

1/12/2016

9

INDIVIDUAL PROVISIONSRollover Allowed From Retirement Plans to SIMPLE Accounts PATH allows a taxpayer to roll over amounts from an employer-

sponsored retirement plan to a SIMPLE IRA if plan existed for at least two years for contributions after December 18, 2015

CPAs & ADVISORS

SELECT BUSINESS PROVISIONS

1/12/2016

10

BUSINESS PROVISIONS – R&E CREDITResearch & Experimentation (R&E) Credit permanently extended, retroactive to 2015

Credit based on % of qualifying research expenses Wages

Supplies

Contract research

Regular credit vs. alternative simplified credit Compare methods for best result

Many states also provide R&E credits

BUSINESS PROVISIONS – R&E CREDITWhat qualifies? Products & processes

Process of experimentation required

PATH Act modifications Eligible small businesses claim credit against alternative minimum tax

for tax years beginning after December 31, 2015

Certain small start-up businesses can claim credit (up to $250K) against payroll tax liabilities for tax years beginning after December 31, 2015

1/12/2016

11

BUSINESS PROVISIONS – WOTC CREDITWork opportunity tax credit (WOTC) extended through 2019

Tax credit for employers hiring individuals from certain targeted groups, including Qualified veterans

Qualified ex-felons

Residents of designated communities

Qualified SSI recipients

Credit based on % of qualified wages paid Generally maximum credit of $2,400 per qualified employee

Certification rules apply

BUSINESS PROVISIONS – WOTC CREDITPATH Act adds new category of qualifying employee

Qualified long-term unemployment recipient Unemployed 27 weeks or more

Receiving unemployment compensation

Credit for this category effective for individuals who begin work after December 31, 2015

1/12/2016

12

BUSINESS PROVISIONS – ALTERNATIVE FUEL CREDIT50¢ per gallon tax credit for certain alternative fuels sold or used by taxpayer extended through 2016Refundable credit Claimed against fuel excise tax liability In some cases, a credit against income tax

Alternative fuels include Liquefied petroleum gas (propane) P Series fuels Compressed or liquefied natural gas Liquefied hydrogen

Does not include ethanol, methanol or biodiesel

BUSINESS PROVISIONS – ALTERNATIVE FUEL CREDITRequires certification with IRS before claiming credit

Often beneficial for businesses using propane forklifts

PATH Act includes revenue provision modifying credit amount for fuel sold or used after December 31, 2015 Liquefied natural gas - 50¢ per energy equivalent of diesel fuel vs. per

gallon (approximately 29¢ per gallon)

Liquefied petroleum gas - 50¢ per energy equivalent of gasoline vs. per gallon (approximately 36¢ per gallon)

1/12/2016

13

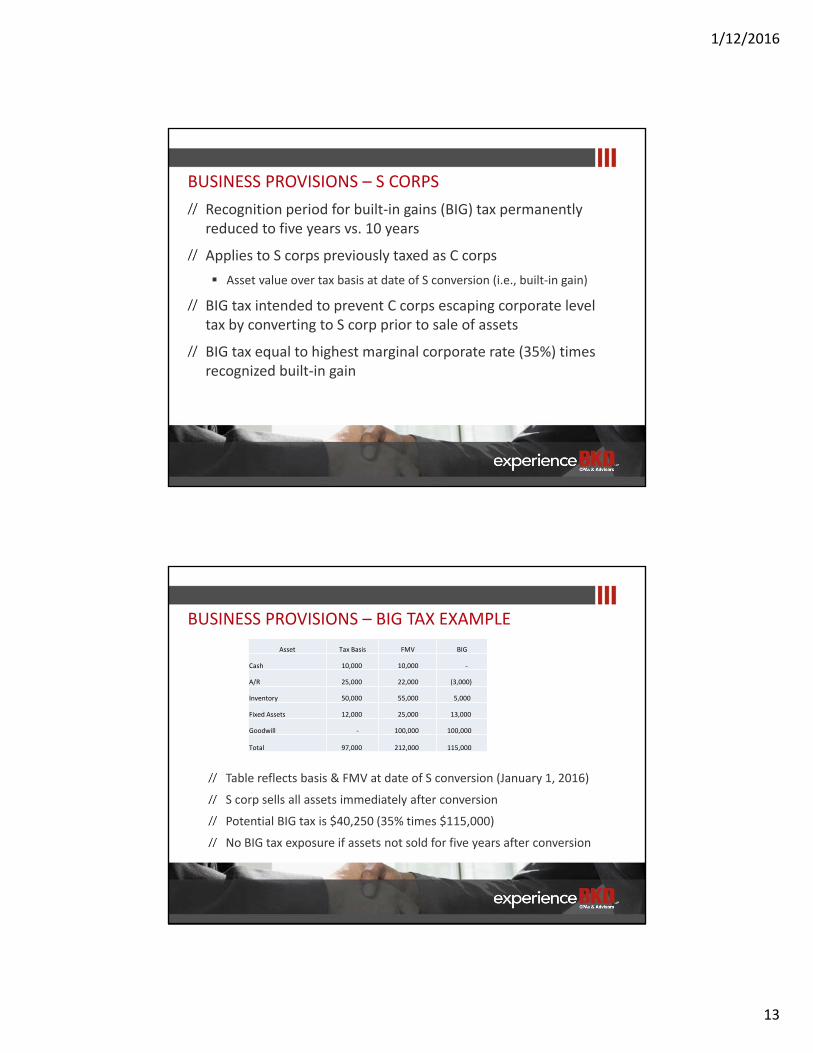

BUSINESS PROVISIONS – S CORPSRecognition period for built-in gains (BIG) tax permanently reduced to five years vs. 10 years

Applies to S corps previously taxed as C corps Asset value over tax basis at date of S conversion (i.e., built-in gain)

BIG tax intended to prevent C corps escaping corporate level tax by converting to S corp prior to sale of assets

BIG tax equal to highest marginal corporate rate (35%) times recognized built-in gain

BUSINESS PROVISIONS – BIG TAX EXAMPLE

Table reflects basis & FMV at date of S conversion (January 1, 2016)

S corp sells all assets immediately after conversion

Potential BIG tax is $40,250 (35% times $115,000)

No BIG tax exposure if assets not sold for five years after conversion

Asset Tax Basis FMV BIG

Cash 10,000 10,000 -

A/R 25,000 22,000 (3,000)

Inventory 50,000 55,000 5,000

Fixed Assets 12,000 25,000 13,000

Goodwill - 100,000 100,000

Total 97,000 212,000 115,000

1/12/2016

14

BUSINESS PROVISIONS – 1099 & W-2 CHANGESAccelerated due dates for W-2, W-3 & returns to report non-employee compensation (e.g., 1099-MISC) Must file with IRS by January 31 (same due date as employee & payee

statements)

No longer eligible for extended filing date for e-filed returns

Effective for returns & statements filed in 2017 for 2016 tax year

Extended ability to truncate social security numbers to W-2 forms SSN truncation previously only allowed on Forms 1099

Provisions intended to combat identity theft & fraudulent refund issues

BUSINESS PROVISIONS – CAPTIVE INSURANCE COMPANIES

Certain small insurance companies can elect to exclude receipt of premiums from taxable income Pre-PATH Act - $1.2 million

PATH Act increased to $2.2 million & indexed for inflation

PATH Act also added new diversification requirements to be eligible for premium exclusion election Risk diversification test

Relatedness test

Company must meet one of these tests

Annual reporting to IRS

1/12/2016

15

CPAs & ADVISORS

SELECT DEPRECIATION PROVISIONS

DEPRECIATION & EXPENSING PROVISIONSEnhanced Section 179 Expensing (Retroactively extended for 2015 & made permanent) $500,000 annual expensing limit ($25,000 under Pre-Act Law)

Phaseout threshold begins at $2 million ($200,000 under Pre-Act Law)

Eligible property computer software & qualified real property

Air conditioning & heating units are eligible after 2015

Eliminates $250,000 expensing cap for qualified real property after 2015

Indexes amounts for inflation

1/12/2016

16

DEPRECIATION & EXPENSING PROVISIONSQualified Leasehold, Restaurant & Retail Improvements(Retroactively extended for 2015 & made permanent) 15-year recovery period

(39 year under Pre-Act Law)

DEPRECIATION & EXPENSING PROVISIONSBonus First-Year Depreciation (Retroactively extended through 2019)

• 2015 - 2017 50% of basis of qualifying property

• 2018 40% of basis of qualifying property

• 2019 30% of basis of qualifying property

“Qualified Improvement Property” eligible for bonus depreciation after 2015

• Improvements to interior portion of real property if placed in service after building is placed in service

• Does not include building enlargements, elevator or escalators or internal structural framework

1/12/2016

17

DEPRECIATION & EXPENSING PROVISIONSBonus First-Year Depreciation Continued(Retroactively extended through 2019) After 2015, certain trees, vines & fruit-bearing plants are eligible

for bonus depreciation when planted or grafted

Corporations can elect to accelerate use of AMT credits in lieu of claiming bonus depreciation

After 2015, Act increases amount of unused AMT credits that may be claimed in lieu of bonus depreciation

DEPRECIATION & EXPENSING PROVISIONSEnhanced First-Year Depreciation Cap for Autos & Trucks(Retroactively extended through 2019) First year depreciation cap for qualifying autos & light trucks placed

in service during following years is increased

• 2015 - 2017 Additional $8,000

• 2018 Additional $6,400

• 2019 Additional $4,800

1/12/2016

18

DEPRECIATION & EXPENSING PROVISIONSSection 179D Energy Efficient Commercial Business Property (EECBP) Deduction(Retroactively extended through 2016) Immediate deductions provided for energy efficient improvements

to lighting, heating, cooling, ventilation & hot water systems of commercial buildings

Amount of deduction up to $1.80 per square foot for installation of EECBP in lieu of depreciating property, generally over a 39-year period

DEPRECIATION & EXPENSING PROVISIONSOther Depreciation & Expensing Provisions(Retroactively extended through 2016) Seven-year write-off for motorsport racing track facilities

Classification of certain race horses as three-year property

Accelerated depreciation for business property on an Indian reservation

1/12/2016

19

CPAs & ADVISORS

OTHER PATH ACT PROVISIONS

AFFORDABLE CARE ACT PROVISIONS

Moratorium on 2.3% medical device excise tax Won’t apply to sales in 2016 & 2017

Delay of “Cadillac” excise tax on high-cost employer-sponsored health coverage Now effective for tax years beginning after December 31, 2019

Payments will be deductible

One-year suspension (in 2017) of annual fee on health insurance providers

1/12/2016

20

OTHER PROVISIONS

Numerous other individual & business extenders

Real estate investment trust (REIT) provisions

Changes to tax court rules

IRS reforms IRS funded at $11.2 billion for 2016 ($290M increase)

Handful of revenue provisions

ADDITIONAL RESOURCES

BKD Alert at http://www.bkd.com/articles/2015/tax-extenders-for-2015-arrive-early-bearing-gifts.htm

Joint Committee on Taxation report JCX-144-15 (dated December 17, 2015) https://www.jct.gov/publications.html

1/12/2016

21

QUESTIONS

CONTINUING PROFESSIONAL EDUCATION (CPE) CREDITS

BKD, LLP is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.learningmarket.org

The information in BKD webinars is presented by BKD professionals, but applying specific information to your situation requires careful consideration of facts & circumstances. Consult your BKD advisor before acting on any matters covered in these webinars

1/12/2016

22

CPE CREDITThis presentation may be eligible for CPE credit upon verification of participant attendanceFor questions or comments regarding CPE credit, please email BKD Learning & Development Department at [email protected]

THANK YOU

FOR MORE INFORMATION // For a complete list of our offices and subsidiaries, visit bkd.com or contact:

Jesse Palmer, CPA // Director of Tax Quality [email protected] // 417.831.7283

Damien Martin, CPA // National Tax Assistant [email protected] // 417.831.7283

Robert W. Conner, CPA // National Tax Assistant [email protected] // 417.831.7283