tax planning 2014 29-30 october 2013 - pwc 14 15th annual conference maximise shareholder value...

TRANSCRIPT

15th AnnualConferenceMaximise

Recently emerging trend ofcustoms challenges and how toprepare for the challenges

Worldtrade Management Services

www.pwc.com/th

MaximiseShareholder Valuethrough EffectiveTAX Planning 2014

Worldtrade Management Services

29-30 October 2013

Agenda

I. Thai Customs Environment

II. Recent Challenges from CustomsII. Recent Challenges from Customs

A. Free Trade Agreements

B. Customs Valuation

C. Licensing

D. Customs Privileges

E. Classification

PwC

III. Other updates/development

IV. Conclusion

Slide 229-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Thai Customs Environment

PwC Slide 329-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

I. Thai Customs Environment

• Transition from revenue collector to facilitator

• Government revenue needs• Government revenue needs

• Falling duty rates

• Importance of trade

• Mindset shift

• Enhanced Post-Clearance Audit activities

• Penalties regimes

PwC

• Greater experience and therefore focus on key areas

• Closer coordination with Revenue Department and ExciseDepartment

Slide 429-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

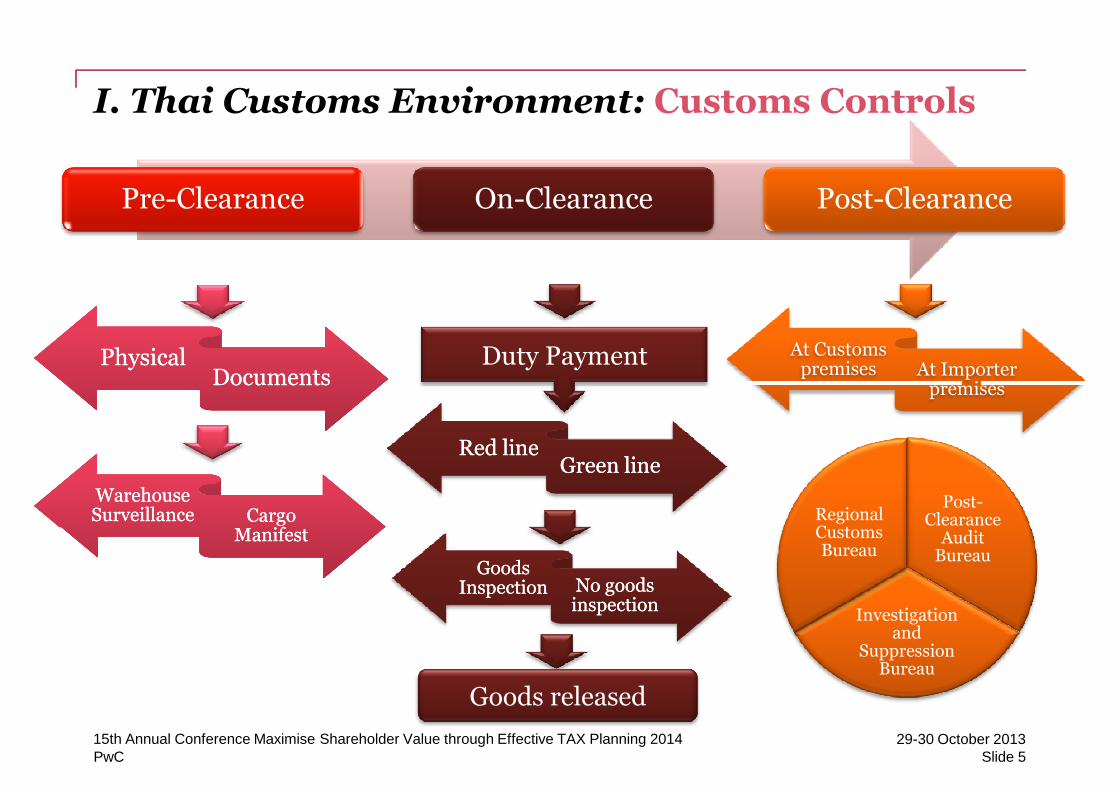

I. Thai Customs Environment: Customs Controls

Pre-Clearance On-Clearance Post-Clearance

PhysicalPhysicalDocumentsDocuments

At Customspremises At Importer

premises

Duty Payment

Red lineRed lineGreen lineGreen line

WarehouseSurveillanceWarehouseSurveillance Cargo

ManifestCargo

Manifest

Post-ClearanceRegional

Customs

PwC

ManifestManifest

GoodsInspection

GoodsInspection No goods

inspectionNo goodsinspection

Goods released

ClearanceAudit

Bureau

Investigationand

SuppressionBureau

CustomsBureau

Slide 529-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

I. Thai Customs Environment: Target Areas

Valuation

• Royalty• Assists• Adjustments• Proceeds• Management

fee, Technical

Classification

• Wrong tariffcode

• Wrong dutyrate

Formalities

• Prohibited/Restrictedgoods

• Ministry ofFinance(Section 12)

Privileges

• BOI• Section 19bis• Free Zone• Bonded

Warehouse• FTAs

PwC

• Managementfee, Technicalassistance

(Section 12)• Hand Carry• Courier

• FTAs

Slide 629-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

• Audit vs. Investigation

I. Thai Customs Environment

Audit approach

• Conflict between technical experts and audit officers

• High Penalties in case of non-compliance

• Current reward regime

- Up to 25% of penalties for Customs (No cap)

- Up to 30% of penalties for informers (No cap)

• Proposal for changing of penalties and reward regime (to be

PwC

• Proposal for changing of penalties and reward regime (to bediscussed in updates Section)

Slide 729-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

• SmugglingImporting/Exporting goods that have not duly passed through customs

I. Thai Customs Environment

Customs Offences

Importing/Exporting goods that have not duly passed through customs(i.e. no import/export entry)

• EvasionImporting/exporting goods that have duly passed through customs (i.e.with import/export entry) with false declaration (e.g. under-valuationof the goods) which results in duty deficiency.

• False Declaration

PwC

• False DeclarationEven without duty deficiency, the importer/exporter may still bedeemed as having committed a false declaration offence.

• Purchase/receipt of smuggled goodsKnowing at the time of purchase or receipt that the goods are smuggledor imported with duty evasion.

Slide 829-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

3 times of CIF + 3 times of duty + 2 times of VAT

I. Thai Customs Environment: Penalty Scheme(Case settlement at Customs level)

Smuggling(Section 27) 3 times of CIF + 3 times of duty + 2 times of VAT(Section 27)

3 times of duty + 2 times of VAT + 1.5% VAT surchargeEvasion

(Section 99+ 27)

1 time of CIF + 1 time of duty + 1 time of VATPurchasing

PwC

Note: If the importers loses the case at court level, currently the penalty shall be 4*CIF + 4*duty or

imprisonment for a term of not exceeding ten years, or both

1 time of CIF + 1 time of duty + 1 time of VAT(Section 27bis)

Slide 929-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Recent Challenges from Customs

PwC Slide 1029-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

A. Free Trade Agreements(“FTA”)

PwC Slide 1129-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs

Current FTAs for Thailand

Multilateral BilateralMultilateral Bilateral

ASEAN Thailand-Japan

ASEAN – China Thailand - Australia

ASEAN – Japan Thailand - New Zealand

ASEAN – Korea Thailand – India

ASEAN – India Thailand – Peru

PwC

ASEAN – Australia – New Zealand Thailand – Chile (not yet into force)

Slide 1229-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from CustomsFTA Compliance issues – indirect invoicing (3rd/4th party)

Companies may choose to structure their operations to optimize the cheaperlabor cost in ASEAN countries (Thailand) coupled with tax incentives inSingapore (HQ)

Japan

Thailand Contract

Goods

PwC

Thailand ContractManufacturer

SingaporeHQ

Contract

Arrangement Invoice

Slide 1329-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

3rd/4th party

II. Recent Challenges from Customs

FTA Compliance issues

P 3rd country invoicing concept:3rd/4th partyinvoicing

P 3 country invoicing concept:

• All Thai FTAs

• Latest FTA: Thai – Chile FTA

• No definition of 3rd country invoicing

O 4th country invoicing:

PwC

• Allowed Only for ATIGA

• Thai Customs authorities reject C/O from4th country invoicing

Slide 1429-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

On behalf of (“O/B”) or

II. Recent Challenges from Customs

FTA Compliance issues

• Exporter: Logistic Company O/B or C/O Manufacturing Company

Care of (“C/O”)

Discrepancies

• (Temporary) Flexibility for utilizing the duty privilege under theASEAN-China FTA. (1 January 2011 – 30 April 2011)

• Currently, Thai Customs authorities does not accept O/B or C/O onForm E

• Discrepancies between C/O and invoice: date, importer/exporter’sname and address

• Declaration of marks, number on packages, gross weight or otherquantity and value (FOB)

• Box ticking: Not ticking on

PwC

• Box ticking: Not ticking on

-Issued Retroactively-Exhibition-De Minimis-Third Country Invoicing

• Wrong application/ wrong Rules of Origin (RoO) in C/O

• Different C/O = different rules

Slide 1529-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs

FTA Compliance issues: Back-to-Back certificate of Origin (C/O)

• Restrictive interpretation by Thai Customs

- Bonded warehousing required in intermediate country

Exporter(ASEAN)

Singapore(Intermediate country)

Thailand100 pcs

1# Shipment 40 pcs

2# Shipment 30 pcs

3# Shipment 30 pcs

PwC

- Bonded warehousing required in intermediate country

- Back-to-Back C/O IS NOT ALLOWED for 3rd party invoicing transactions

Slide 1629-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs

PwC’s observation

• Moving responsibility from authorities to exporters• Moving responsibility from authorities to exporters

• Moving responsibility from exporter to importer

• Increased use of automated systems

• Different interpretations by exporting and importing FTA members

• Inconsistent interpretations among each FTAs by Thai Customs

• Increased post audit reviews by authorities on origin

PwC Slide 1729-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

B. Customs Valuation

PwC Slide 1829-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

Customs Valuation

Import price + Adjustments(either additions / deductions)

=

Price actually paid or payable

Invoice price

CustomsValuation

Proceeds

Commissions/ packing

Total

Royalty /License

fee

PwC

Invoice price

Invoiceprice

TotalpaymentAssists

Slide 1929-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

Customs Valuation

Considerations for dutiable royalties/license fees

Royalty/License fee

Incorporatethe IPR

Manufacturedby licensor’s

IP

Condition of Sales

PwC

Non-Dutiable Dutiable√

Slide 2029-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

Supreme Court Thailand

- 3rd party Royalty payment – dutiable?

- Customs value of goods $100 or $105?- Customs value of goods $100 or $105?

3rd party(Licensor)

Goods

Royalty 5

PwC

Manufacturer(Exporter)

Buyer(Importer)

Goods

100

Slide 2129-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

Advisory Opinion 4.15

Supply Agreement:

- Manufacturer to manufacture goods with Licensor’s Trade Mark under- Manufacturer to manufacture goods with Licensor’s Trade Mark underLicensor’s control

- Sell exclusively to buyer or others as Licensor determines

3rd party(Licensor)

Royalty 5

Manufactureunder

control/know-how

PwC

Manufacturer(Exporter)

Buyer(Importer)

Goods

100

Royalty 5

Slide 2229-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs: Comparison

3rd party(Licensor)

Royalty 5Supreme

Manufacturer(Exporter)

Buyer(Importer)

Goods

100

Royalty 5SupremeCourt

3rd party(Licensor)

Manufactureunder

control/know-how

PwC

Manufacturer(Exporter)

Buyer(Importer)

Goods

100

Royalty 5

how

AO 4.15

Slide 2329-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Advisory Opinion 4.15

PwC’s observation

• A more cautious approach for Customs’ consideration on royalty

• Customs would not only look into the royalty agreement, but also salessurrounding circumstances (other agreements in connection with royaltyagreement).

• Influence of licensor over manufacturer and buyer is also taken into account.

• Expect more challenges from Customs on 3rd party royalties.

PwC Slide 2429-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

C. Licensing

PwC Slide 2529-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

C. Licensing

• Are the goods prohibited from import?• Are the goods prohibited from import?

• Are the goods subject to import/ export license?

• Are the goods prohibited/ restricted under more than one relevant lawsand regulations?

• Is a Certificate of Free Sale considered as an import license?

• Could import license be issued retroactively?

PwC Slide 2629-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

C. Licensing

• Administrative Court ruling, dated 3 December 2012• Administrative Court ruling, dated 3 December 2012

• Repeal of Hazardous Substance Control List B.E. 2546 & HazardousSubstance Control List (No. 2) B.E. 2547

• Only reference to English names of the hazardous substances

• Omission of the names of hazardous substances in Thai

PwC Slide 2729-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

C. Licensing

• New Hazardous Substance Control List in effect on 28 September 2013

Key changes:

• Addition of Thai names for each substance with the English name in the parentheses;

• Each identification number refers to each substance;

• A categorization of the substances based on 6 responsible institutes / agencies ;

Department of Agriculture (DOA) Department of Livestock Development (DLD)

Department of Fisheries (DOF) Food and Drug Administration (FDA)

PwC

• An addition/ re-categorization of certain substances;

• An indication of restricted concentration (if any);

• Separate lists for groups of substances and products.

Department of Industrial Works (DIW) Department of Energy Business (DOEB)

Slide 2829-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

C. Licensing

Penalties under the Hazardous Substance Act B.E. 2535

Imprisonment Fine (THB) or Both

Type I: < 6 months < 50,000 /

Type II: < year < 100,000 /

Type III: < 2 years < 200,000 /

Type IV: < 10 years < 1 million /

Penalties under the Customs Act B.E. 2469

PwC

* Proposal for reduction of the penalty is recently raised.

Importing ofrestricted goodswithout importlicense.

- Surrender of the goodsOR- In lieu of goods surrendering, liable to value of the goods(CIF + Duty+ VAT)

Slide 2929-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

PwC’s observation

• Preparation for transition period on new Licensing Notification• Preparation for transition period on new Licensing Notification

• Expect more audits on licensing issue

• Keep an eye on updated regulation

PwC Slide 3029-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

D. Customs Privileges

PwC Slide 3129-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

D. Customs Privileges: Manufacturing BondedWarehouse (“MBW”)

Council of State’s opinion No. 247/2548 (2005)

Company AMBW

Vietnam

Form D

Company BThailand

Form D

Importer = A Importer = A

PwC

Customs Challenge √ Council of State

Slide 3229-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Potential

II. Recent Challenges from Customs:

D. Customs Privileges: Free Zone (“FZ”)

• Portion of local raw materialsPotential

Issues !

• Portion of local raw materials

• Manufacturing process under the FZ

• Clarification on the definition of Profit

o Acceptable threshold?

o Trading vs manufacturing profit

• Certificate issued by Independent institutes

PwC Slide 3329-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

D. Customs Privileges: Section 12 of Customs TariffDecree B.E.2530 (“Section 12”)

• Example of discrepancy

Customs ApprovalPart no. 1234

ImportedPart no. 1234A

PwC

Part no. 1234 Part no. 1234A

Slide 3429-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

D. Customs Privileges: Section 12 of Customs TariffDecree B.E.2530 (“Section 12”)

Challenges by Customs

• Could not enjoy the right for duty reductions/exemptions underSection 12,

• Liable to a fine of:

OffenceExposure

PwC

OffenceCase settlement at Customs Level

Evasion(Section 99+ 27)

(1) Fine 2*duty + 1*VAT

(2) Duty shortfall 1*duty + 1*VAT + 1.5% of VAT

Total 3*duty + 2*VAT + 1.5% of VAT

Slide 3529-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

D. Customs Privileges: Section 12 of Customs TariffDecree B.E.2530 (“Section 12”)

Key consideration

• Comply with the Ministry of Finance (“MOF”) Notification’srequirement

• Goods meet the rules and procedures specified under the MOF’sNotification

• Non-compliance with customs formality is a minor mistake?

PwC

• Non-compliance with customs formality is a minor mistake?

Slide 3629-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

D. Customs Privileges: PwC’s observation

• Bonded Warehouse and FTA benefits may continue (pending guidance• Bonded Warehouse and FTA benefits may continue (pending guidancefrom Customs)

• Free Zone continues to be focus area for Customs.

• Section 12 compliance more important given recent challenges fromCustoms.

PwC Slide 3729-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

E. Classification

PwC Slide 3829-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

E. Classification

• GRI 2 (a) and Section 6 of Customs Tariff Decree

ImportedCKD

CKD

CBU

?

PwC

• The CKD were imported with matching quantity (despite not the sameshipment)

Slide 3929-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

E. Classification: relevant laws

• General Rules of Interpretation 2 (a)• General Rules of Interpretation 2 (a)

“Any reference in a heading to an article shall be taken to include areference to that article incomplete or unfinished, provided that, as presented,the incomplete or unfinished article has the essential character of the completeor finished article. It shall also be taken to include a reference to that articlecomplete or finished (or failing to be classified as complete or finished byvirtue of this Rule), presented unassembled or disassembled.”

• Section 6 of Customs Tariff Decree

PwC

“Where it appears to the Director General of Customs that the dutychargeable upon any complete article is being evaded by means of importing,either simultaneously or otherwise, such article in separate parts, the dutychargeable upon such separate parts shall integrally be assessed at the rate forthe complete article.”

Slide 4029-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

II. Recent Challenges from Customs:

PwC’s observation

• Customs tends to apply rules to attract a higher rate• Customs tends to apply rules to attract a higher rate

• Placing deposit guarantee/ Reserve the right to argue onclassification issue upon importation

• Seeking for classification’s ruling?

PwC Slide 4129-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Other Updates/Developments

PwC Slide 4229-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Developments

FTA Under Negotiation

Thai – EU FTA

• Thailand will be delisted as “beneficiary country” under GSP by early 2015

• 2 rounds of negotiation done

• Next round in December 2013

• Controversial issues?

- Intellectual Property Right (“IPR”)

- Services

- Investor state disputes

PwC

- Investor state disputes

- Government procurement

- Duty drawback

• Time is ticking for Thailand ? (Singapore-EU FTA = Concluded, Vietnam-EU FTA andMalaysia-EU FTA = Advanced stage

Slide 4329-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Development

Future FTAs

Trans-Pacific Partnership (“TPP”)Trans-Pacific Partnership (“TPP”)

• High-Standard FTA

• Original: Brunei, Chile, New Zealand and Singapore (P4)

• Attempt to conclude by the end of 2013

• Under negotiations:

- Original signatories: Brunei, Chile, New Zealand and Singapore

- Negotiating members: Australia, Canada, Japan, Malaysia, Mexico,

PwC

- Negotiating members: Australia, Canada, Japan, Malaysia, Mexico,Peru, Vietnam and the United States

• Controversial issues?

• Where is Thailand?

Slide 4429-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Development

Future FTAs

Regional Comprehensive Economic Partnership (RCEP)

• ASEAN (10) + 6 (Australia, China, India, Japan, Korea, New Zealand)

• Intended to be the largest FTA globally

• ASEAN + 1 remain valid

• Attempt to be concluded by the end of 2015

PwC Slide 4529-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Developments

AEC

• Self- certification

• ASEAN• ASEAN

- 1st Pilot project on Self – Certification: Brunei, Malaysia,Singapore and Thailand participating. Myanmar indicatedintention to participate in the 1st Pilot Project. (extended till 31December 2015)

- 2nd Pilot project on Self – Certification: Indonesia, Laos PDR, thePhilippines and Vietnam participating. (Thailand possibleparticipant)

PwC

participant)

• The two projects will run in parallel until 2015. Developing a singlesystem is required by 2015

Slide 4629-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Developments

National Single Window (NSW)

• Integrate customs clearance process (e.g. import, export and transit)into a single system.into a single system.

• Exchange cargo clearance data electronically across ASEAN borders(as a part of ASEAN Single Window).

• Allow single submission of applications for licenses and permitsthrough relevant authorities e.g. Customs Department, ExciseDepartment and Board of Investment.

PwC Slide 4729-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Development

Authorized Economic Operator (AEO)

• The rise of terrorism during the past 12 years has raised concern onsecurity in global supply chain management.security in global supply chain management.

• WCO developed Framework of Standards to Secure and FacilitateGlobal Trade and AEO guideline

• Some countries may implement AEO program under different name;

- U.S.: Customs –Trade Partnership Against Terrorism (C-TPAT)

- New Zealand: Secure Export Scheme

- Singapore: Secure Trade Partnership

PwC

- Singapore: Secure Trade Partnership

- China: Classified Management of Enterprises

Slide 4829-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Development

Authorized Economic Operator (AEO)

• Thailand: AEO launched 1 January 2013

• Who can become an AEO?• Who can become an AEO?

- Importers – Exporters

- Customs Brokers

• But there are more parties involving…

- Manufacturers/Suppliers

- Warehouse Operators/Owners

PwC

- Warehouse Operators/Owners

- Port Operators

- Transport Operators

- Freight Operators

Slide 4929-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Other Updates/Development

Authorized Economic Operator (AEO)

• Responsibilities of an AEO

- Develop security system- Develop security system

- Perform security risk assessment

- Implement security measures as recommended by customs

- Develop document on security system to support application

• And why should you consider doing all of these?

- Privileges on customs clearance

PwC

- Privileges on customs clearance

- Privileges on duty refund

- Limit post clearance audit to 2 years

- Privileges on case settlement

• Future AEO Mutual Recognition Arrangement (“MRA”)

Slide 5029-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Other Updates/Development

Authorized Economic Operator (AEO)

PwC’s observationPwC’s observation

• Key criteria

o No smuggling offence;

o Continuous profitability/ Secure financial status

o Security compliance

• Obstacles

PwC

• Uptake low

• Gold Card / Licensed Broker expired at the end of September 2013

Slide 5129-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

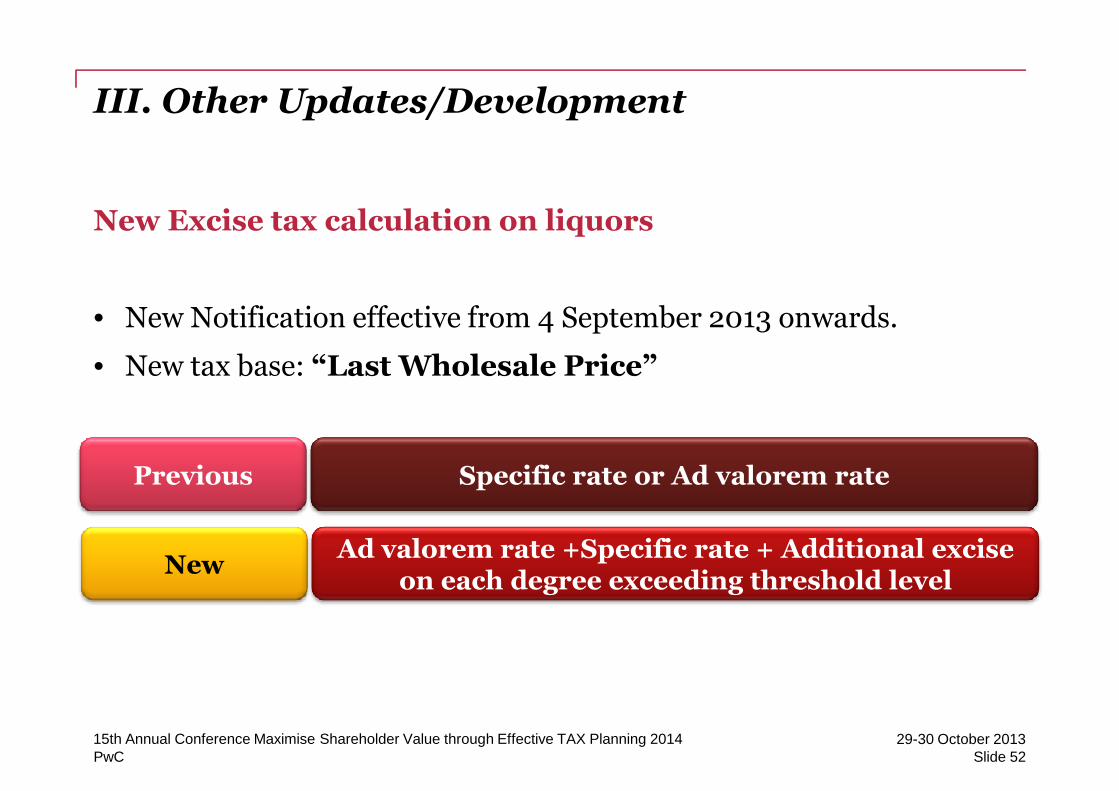

III. Other Updates/Development

New Excise tax calculation on liquors

• New Notification effective from 4 September 2013 onwards.

• New tax base: “Last Wholesale Price”

Specific rate or Ad valorem ratePrevious

PwC

Ad valorem rate +Specific rate + Additional exciseon each degree exceeding threshold level

New

Slide 5229-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Development

New Excise tax calculation on liquors: example

Excise tax / consumption tax payable = (1) + [(2) or (3)] + (4)

Ad

Wine and sparklingwine of grapes

Advalorem

Rate

Specific Rate(2) or (3) whichever is higher

Excise Rate in relation to productswith "exceeding degrees"

(1)*

(2) (3) (4)

THB/Litre/per100 Degree

THB/Litre ConditionTHB/Litre/

Exceeding Degree

1) the last wholesaleprice excluding VAT,not exceeding 600THB

0 1,000 225an alcoholic strengthby volume exceeding

15 degrees3

PwC

THB

2) the last wholesaleprice excluding VAT,exceeding 600 THB

36 1,000 225an alcoholic strengthby volume exceeding

15 degrees3

Slide 5329-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Development

Licensing

Potential reduction of penaltyPotential reduction of penalty

• Proposal by the Joint Standing Committee on Commerce, Industryand Banking

• To separate offences arising from technical mistakes from otheroffences under Section 27 e.g. import of restricted goods without license

• To specify appropriate penalty, not exceeding the penalty under themajor law

PwC

major law

• Cabinet resolution: assign Ministry of Finance for furtherconsideration

Slide 5429-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

III. Other Updates/Development

Customs Laws

• Penalty regime -Draft revision of Customs Act B.E.2469 (1926)• Penalty regime -Draft revision of Customs Act B.E.2469 (1926)

- Duty fine 0.5 to 4 times of the CIF value

- Customs audit period limited to 2 years

• Reward regime

- Up to 15% of penalties for Customs (capped at 5 million baht)

PwC

- Up to 15% of penalties for Customs (capped at 5 million baht)

- Up to 30% of penalties for informers (capped at 10 million baht)

Slide 5529-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Conclusion

PwC Slide 5629-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

IV. Conclusion: Key takeaway

2. Minimize your risks

a. Self assessment/ external expert

1. Hot issues

a. Royalty paid to 3rd party

b. Privilege utilizationa. Self assessment/ external expert

review => self disclosure

b. Training and development

c. Regulation updates

3. Defend yourself

a. Check legal precedents

b. Obtain ruling where possible

4. Maximize your opportunities

a. Sign up for trade facilitationmeasures

b. Privilege utilization

c. Licensing

d. FTA challenges

PwC

b. Obtain ruling where possible

c. Seek expert’s advice

d. Develop best practices

measures

b. Use duty incentive schemes

c. Stay on top on FTA opportunitiesand updates

Slide 5729-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Contact

Paul SumnerPartnerTel: +66 (0) 2344 1305Tel: +66 (0) 2344 [email protected]

Santi KrongsithidejDirectorTel: +66 (0) 2344 [email protected]

PwC

Nu To VanDirectorTel: +66 (0) 2344 [email protected]

Slide 5829-30 October 201315th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2014

Thank you

www.pwccustoms.com

© 2013 PricewaterhouseCoopers WMS Bangkok Ltd. All rights reserved.'PricewaterhouseCoopers' and/or 'PwC' refers to the individual members of thePricewaterhouseCoopers organisation in Thailand, each of which is a separate andindependent legal entity. Please see www.pwc.com/structure for further details.