tax highlights from your advisers · other business and non-business entities ... the definition of...

TRANSCRIPT

© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 0

Tax WhizTax highlights from your advisers

KPMG in Malaysia

15 April 2020

Special Tax Deduction for Rental Reduction on Business Premises Rented to Small and Medium Enterprises

© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 1

Tax Whiz 2020 | 15 April 2020

© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 1

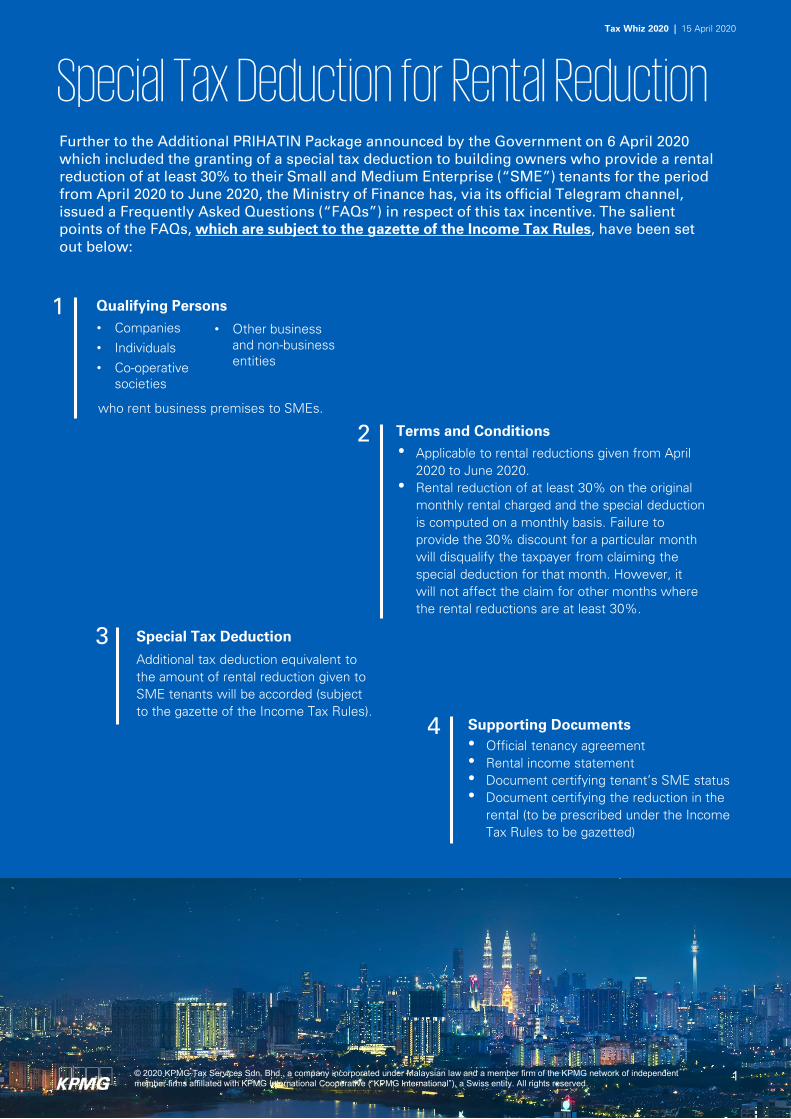

Additional tax deduction equivalent to the amount of rental reduction given to SME tenants will be accorded (subject to the gazette of the Income Tax Rules).

• Applicable to rental reductions given from April 2020 to June 2020.

• Rental reduction of at least 30% on the original monthly rental charged and the special deduction is computed on a monthly basis. Failure to provide the 30% discount for a particular month will disqualify the taxpayer from claiming the special deduction for that month. However, it will not affect the claim for other months where the rental reductions are at least 30%.

3

2

• Companies • Individuals• Co-operative

societies

1

• Official tenancy agreement• Rental income statement• Document certifying tenant’s SME status• Document certifying the reduction in the

rental (to be prescribed under the Income Tax Rules to be gazetted)

4

Special Tax Deduction for Rental ReductionFurther to the Additional PRIHATIN Package announced by the Government on 6 April 2020 which included the granting of a special tax deduction to building owners who provide a rental reduction of at least 30% to their Small and Medium Enterprise (“SME”) tenants for the period from April 2020 to June 2020, the Ministry of Finance has, via its official Telegram channel, issued a Frequently Asked Questions (“FAQs”) in respect of this tax incentive. The salient points of the FAQs, which are subject to the gazette of the Income Tax Rules, have been set out below:

Special Tax Deduction

Terms and Conditions

Qualifying Persons

Supporting Documents

who rent business premises to SMEs.

• Other business and non-business entities

© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 2

Tax Whiz 2020 | 15 April 2020

© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 2

The definition of “SME” for the purpose of the special tax deduction follows SME Corporation Malaysia’s definition. A business would have to fulfill either one of following two conditions to be regarded as an SME:

• Annual sales – based on the figure at the end of the basis period of the preceding Year of Assessment (“YA”); or

• Number of full time employees (“FTEs”) – based on numbers at the end of the basis period of the preceding YA or at 1 April 2020.

5 Definition of “SME”

* If a business fulfills either one condition across the different sizes of operation, then the smaller size will be applicable. For example, if a manufacturer’s annual sales is RM100 million but has 150 FTEs, it will be deemed to be an SME (not exceeding 200 FTEs).

For reference purposes, the FAQs provide a link to access the Guidelines for New SME Definition (“SME Guidelines”) issued by SME Corporation Malaysia (please click here for the link). It is noted that the SME definition in the SME Guidelines excludes subsidiaries of the following companies:

• Public listed companies in the main board; and• Large firms, multinational companies, Government-linked companies, companies owned by the

Minister of Finance (Incorporated) (Malaysia) and State-owned enterprises.

In addition, there are also additional criteria stated in the SME Guidelines which need to be met to be considered as an SME.

It remains unclear whether these exclusions and additional criteria will be applied to determine the eligibility of taxpayers for this special deduction.

Business Size

Sector Conditions (only one condition is required to be met)

Micro All sectors • Annual sales: Less than RM300,000• FTEs: Less than 5

Small Manufacturing • Annual sales: From RM300,000 but less than RM15 million• FTEs: From 5 to less than 75

Services and other sectors

• Annual sales: From RM300,000 but less than RM3 million• FTEs: From 5 to less than 30

Medium Manufacturing • Annual sales: From RM15 million but not exceeding RM50 million• FTEs: From 75 but not exceeding 200

Services and other sectors

• Annual sales: From RM3 million but not exceeding RM20 million• FTEs: From 30 but not exceeding 75

© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 3© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 3

Tai Lai KokExecutive Director –Head of Tax and Head of Corporate [email protected]+603 7721 7020

Long Yen PingExecutive Director –Head of Global Mobility [email protected]+603 7721 7018

Ng Sue LynnExecutive Director – Head of Indirect [email protected]+603 7721 7271

Soh Lian SengExecutive Director –Head of Tax Risk [email protected]+603 7721 7019

Bob KeeExecutive Director – Head of Transfer [email protected]+603 7721 7029

Kuching & Miri OfficesRegina LauExecutive Director – Kuching [email protected]+6082 268 308 (ext. 2188)

Penang OfficeEvelyn Lee Executive Director – Penang [email protected]+604 238 2288 (ext. 312)

Kota Kinabalu OfficeTitus TseuExecutive Director – Kota Kinabalu [email protected]+6088 363 020 (ext. 2822)

Johor Bahru OfficeNg Fie LihExecutive Director – Johor Bahru [email protected]+607 266 2213 (ext. 2514)

Petaling Jaya Office

Outstation Offices

Nicholas CristExecutive Director – Corporate [email protected]+ 603 7721 7022

Dato’ Leanne KohExecutive Director – Corporate [email protected]+603 7721 7026

Neoh Beng GuanExecutive Director – Corporate [email protected]+ 603 7721 7025

Ong Guan HengExecutive Director – Corporate Tax [email protected]+ 603 7721 7027

Chang Mei SeenExecutive Director – Transfer [email protected]+ 603 7721 7028

Ivan Goh Executive Director – Transfer [email protected]+ 603 7721 7012

Contact us

Ipoh OfficeCrystal Chuah Yoke ChinTax Manager – Ipoh [email protected]+605 253 1188 (ext. 320)

© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 4© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 4

Tax Whiz 2020 | Report Name

© 2020 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Petaling Jaya

Level 10, KPMG Tower, 8, First Avenue, Bandar Utama, 47800 Petaling Jaya, SelangorTel: +603 7721 3388Fax: +603 7721 3399Email: [email protected]

Penang

Level 18, Hunza Tower, 163E, Jalan Kelawei, 10250 PenangTel: +604 238 2288Fax: +604 238 2222Email: [email protected]

Kuching

Level 2, Lee Onn Building, Jalan Lapangan Terbang, 93250 Kuching, SarawakTel: +6082 268 308Fax: +6082 530 669 Email: [email protected]

Kota Kinabalu

Lot 3A.01 Level 3A, Plaza Shell, 29, Jalan Tunku Abdul Rahman, 88000 Kota Kinabalu, SabahTel: +6088 363 020Fax: +6088 363 022Email: [email protected]

Johor Bahru

Level 3, CIMB Leadership Academy, No. 3, Jalan Medini Utara 1, Medini Iskandar, 79200 Iskandar Puteri, JohorTel: +607 266 2213Fax: +607 266 2214Email: [email protected]

Ipoh

Level 17, Ipoh Tower, Jalan Dato’ Seri Ahmad Said, 30450 Ipoh, PerakTel: +605 253 1188Fax: +605 255 8818Email: [email protected]

Miri

1st Floor, Lot 2045, Jalan MS 1/2,Marina Square, Marina Parkcity,98000 Miri, SarawakTel: +6085 321 912Fax: +6085 321 962 Email: [email protected]

instagram.com/kpmgmalaysia

facebook.com/KPMGMalaysia

twitter.com/kpmg_malaysia

linkedin.com/company/kpmg-malaysia

kpmg.com/my

KPMG Offices