tax efficient investing - localinstitutes.cii.co.ukaid 6 • vcts / eiss / seiss subject to eu state...

TRANSCRIPT

Tax Efficient Investing

Leverage the past, present and future

UNDERSTAND THE RISKS

• Tax legislation can change and depends on

personal circumstances.

• EIS relief depends on companies retaining

their EIS qualifying status for 3 year period

post investment

• You should not invest if you are likely to

require the capital in the near term.

This summary has been approved by Enterprise Investment Partners LLP which is authorised and regulated by

the Financial Conduct Authority (FRN 604439). It is not an offer to invest in any of the offers mentioned.

Investment can only be made on the basis of the full Information Memorandums and examination of the risk

factors contained therein. We recommend you seek advice from an independent financial adviser authorised

under the Financial Services & Markets Act 2000 who specialises in investments of this type before investing.

• Past performance is not a reliable indicator of

future performance.

• Any stated returns are for illustrative purposes

only and no forecast (guaranteed or

otherwise) is implied or should be inferred.

• Your capital is at risk and you may not get

back the amount invested.

2

PROGRAMME

3

• Legitimate tax-efficient investing – forget the trial by media!

• A brief history

• What are the available structures?

• Recent Legislative Changes and their impact

• How to choose from the vast array of available products

OVERVIEW

4

Launch DateTotal funds

(Raised to date)Funds raised

(Most recent year)

VCT 1995 Nearly £6 billion £400 million Retail only

EIS 1994 £12.3 billion £1.5 billionIncl. retail and non

retail

SEIS 2012 £250 million £150 millionIncl. retail and non

retail

BPR 2004 £987 millionRetail only. Total market est. £1.8

billion

EIS INVESTMENT OVER THE YEARS

EU S

TATE

AID

6

• VCTs / EISs / SEISs subject to EU State Aid rules

• All government subsidies for companies subject to rules

• EU Competition Commission is in charge

• HMRC must get State Aid approval for all changes

• “Evidence-based” permissions – do schemes earn their keep?

New companies = employment = increased receipts from corporation tax / income tax / VAT

SUCCESS OF THE EIS

7

22,900 SME’s have received over £12.3bn of funding via

EIS

EIS

2,770 firms raised £1.5bn

in 2013/14

Firms raising funds for the

first time raised £840m

last year

WHAT QUALIFIES?

8

VCT / EIS / SEIS

Most trading businesses, excluding propertyand financial/professional businesses

Can be overseas, provided permanent UKestablishment

BPR

Most UK businesses which carry on a tradebut excluding investment businesses

* Watch out for connected party, joint venture and leasing rules* Watch out for gross assets test / employee test

VCT

9

• Fully quoted vehicle investing in qualifying unquoted companies

• AIM and all non RIEs count as unquoted

The Tax Reliefs - VCT

30% income tax relief

Tax-free dividends

CGT Free on exit

No IHT exemption

No Loss Relief

✔

X

✔

✔

X

VCT

• Generalist, AIM or sector specific

• New Fund or Top Up

• Can invest via equity or debt

• 5 year qualifying period

EIS

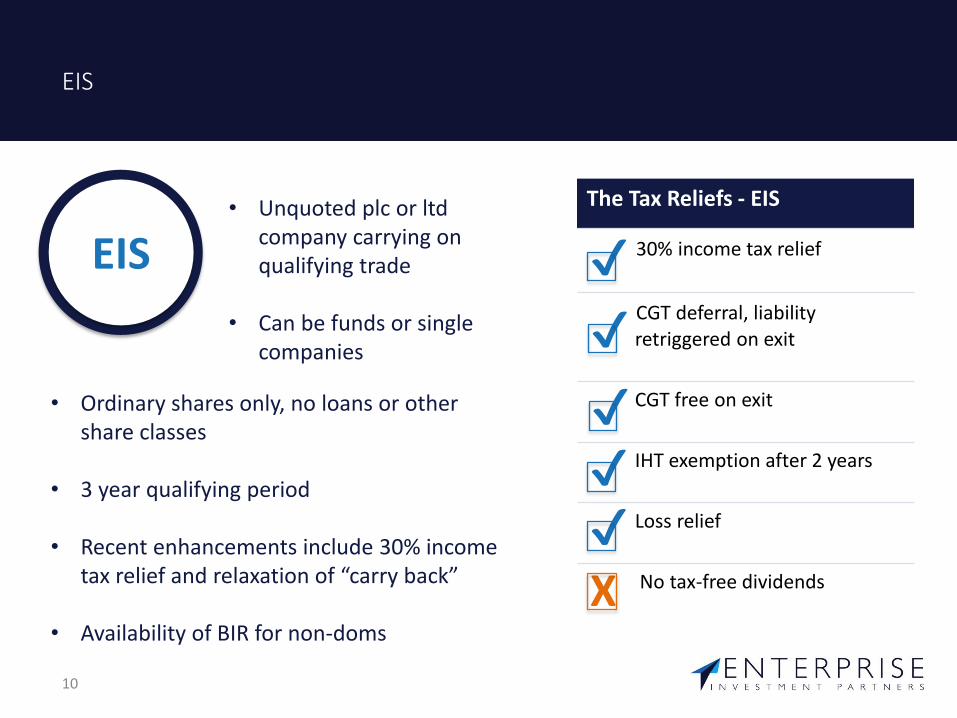

10

• Unquoted plc or ltd company carrying on qualifying trade

• Can be funds or single companies

The Tax Reliefs - EIS

30% income tax relief

CGT deferral, liability retriggered on exit

CGT free on exit

IHT exemption after 2 years

Loss relief

No tax-free dividends

✔

✔

✔

X

✔

✔

EIS

• Ordinary shares only, no loans or other share classes

• 3 year qualifying period

• Recent enhancements include 30% income tax relief and relaxation of “carry back”

• Availability of BIR for non-doms

SEIS

11

• ‘Son of EIS – Introduced in 2012 to stimulate start-up economy post-recession

• Maximum of £150,000 can be raised per company

The Tax Reliefs - SEIS

50% income tax relief

CGT write-off of 50%, reduces tax bill from 28% to 14%

CGT free on exit

IHT exemption after 2 years

Loss relief

No tax-free dividends

✔

✔

✔

X

✔

✔

SEIS

• SEIS/EIS funds can now be raised in parallel

• Best approached on fund basis due to higher risk of individual companies

• Not a big retail market, as sums involved are small!

BPR

12

• Business Property Relief originally introduced for Property only, subsequently extended to shares in unquoted companies

The Tax Reliefs - BPR

IHT exemption after 2 years

Can combine holding periods

On death, 5 year ‘look back’

✔

✔

✔

BPR

• Most normal UK companies qualify

• Must be trading and not investment companies

• Huge growth in BPR in recent years

COMPARISON OF TAX RELIEFS

13

Income Tax

CGT Deferral

No CGT on Exit

IHT Exempt

Tax Free Dividends

Loss Relief

VCT ✔ 30% X ✔ X ✔ X

EIS ✔ 30% ✔ ✔ ✔ X ✔

SEIS ✔ 50%✔

(Write-off)✔ ✔ X ✔

BPR X X X ✔ X X

THE PROCESS – HOW DO YOU GET YOUR TAX RELIEF? (EIS/SEIS)

14

“Advanced Assurance” application to HMRC

Clearance granted and tax certificates issued to investors via scheme arranger

Advance clearance granted based on the information disclosed

Raise Money

Commence trade (evidence required)

Submit full application to HMRC (after 4 months of trading)

RECENT CHANGES

15

July 2015 Budget introduced substantial changes to VCT/EIS:

• Lifetime cap of £12m per investee company

• All investments made with intention to “grow and develop” a business (not very clear!)

• Special concessions for “knowledge intensive” businesses

• New funds can not be used to acquire existing trades/shares (incl. Management buyouts for VCTs)

• Reserve power also disqualified (November 2015)

• Any remaining renewable energy schemes (incl. overseas) disqualified from 6 April 2016

EFFECT OF CHANGES

16

• No more renewable energy schemes

• No more schemes with “predictable income” viz reserve power

• Traditional pub EIS model now disqualified

• HMRC forcing focus onto genuine trading businesses

• HMRC also pointing rules towards new/startup businesses at the expense of mature businesses

• Ever lower pension cap driving business to EIS

WHAT TO LOOK FOR: VCT

17

If a new Fund

Track record of managerLook for “total return”, sum of tax relief,tax-free dividends and remaining NAV

If an existing Fund

Quality of portfolio including recent investee company performanceLikelihood of an early exit

If “second-hand” shares

Maturity of underlying businesses – how soon will they exit?No up-front tax relief, but tax-free dividends and CGT free on exit

✔

✔

✔

✔

✔

✔

VCT

WHAT TO LOOK FOR: EIS

18

Track record of manager: How many previous exits? Average return?

Capital preservation or growth? Trades with underlying freeholds?

Fair balance of risk and reward

Commitment of managers: have they invested?

Funds or spread portfolios rather than single companies

✔

✔

✔

✔

✔

EIS

WHAT TO LOOK FOR: SEIS

19

Track record of manager

Any exits yet?

A fund with portfolio spread rather than single company

Generalist or sector specialist?

Technology or non technology?

Capacity for follow on investment

✔

✔

✔

✔

✔

✔

SEIS

WHAT TO LOOK FOR: BPR

20

Balance of yield and security

Solid trades with predictable income streams

Asset-backed

Low fees!

✔

✔

✔

✔

BPR

FUND HIGHLIGHTS

21

TRACK RECORD

ASSET BACKED

NO UP-FRONT FEES

GROWING SECTOR

IMBIBAA Leisure EIS Fund from manager with outstanding track record – average of 35% IRR from 10 previous EIS exits. Most recent exit delivered a 5.7x cash return.

TITANA freehold storage EIS Fund offering capital preservation together with strong projected returns.

GUINNESSA BPR scheme investing in Solar projecting 5% return with no up-front fees.

FINTECH CIRCLEA specialist SEIS Fund investing in FinTech

CONCLUSION

22

“The government’s aim is to make Britain the best place in Europe to do business. The tax-advantaged venture capital schemes continue to be an important part of meeting this

aim, providing valuable support to small and growing businesses seeking finance to develop and grow.”

David GaukeFinancial Secretary

THE TREASURYJuly 2015

SOME USEFUL ADDRESSES

23

EIS Association: www.eisa.org.uk

HMRC: www.hmrc.gov.uk

Enterprise Investment Partners: www.enterprise-ip.com

Martin Sherwood: [email protected] 7843 0472