tax avoidance in multinationals: the case of debt … avoidance in multinationals: the case of debt...

TRANSCRIPT

CES Lecture Series

Tax Avoidance in Multinationals:

The Case of Debt Shifting

Dirk Schindler (Norwegian School of Economics)

Lecture 3: Regulation, Minority Ownership and Transfer Pricing

as Limiting Factors

Dirk Schindler

Potential (important) factors limiting debt shifting:

• Thin-capitalization rules (TC rules)

• Controlled-foreign-company rules (CFC rules)

• Minority ownership in affiliates

• Interplay with transfer pricing

CES Lecture: The Case of Debt Shifting 76 Lecture 3: Limiting Factors

Dirk Schindler

5 Thin-capitalization Rules and Controlled-

foreign-company Regulation

• Thin-capitalization rules

⋄ Few countries without TC rules, e.g., Cyprus, (still) Norway

⋄ Otherwise trend from TC rules in strict sense (safe harbor rules)

to non-specific TC rules (earnings-stripping rules / ‘Zinsschranke’)

• Controlled-foreign-company rules

⋄ Banned by European Court of Justice for EEA affiliates in 2006

⋄ Part of BEPS proposal by OECD (2013)

• Some overview on details in Ruf and Schindler (2012)

CES Lecture: The Case of Debt Shifting 77 Lecture 3: Limiting Factors

Dirk Schindler

5.1 Thin-Capitalization Rules

5.1.1 General Features of TC rules (in Strict Sense)

• Applicable for debt from shareholders with significant influence on ma-

nagement

• Threshold for influence mostly direct and indirect holding of at least

25% (or higher values) of shares / voting rights

• If applicable, no tax deductibility of interest expenses on (excess) inter-

nal debt

• Excess debt determined by fixed debt-to-equity ratio

• Safe harbor: no TC rules, if debt-to-equity ratio below threshold ratio

CES Lecture: The Case of Debt Shifting 78 Lecture 3: Limiting Factors

Dirk Schindler

• Average safe harbor in EU (2008): 3.4:1 debt-to-equity

• Usually exemption (or preferable rules) for financial institutions and

holding companies

• Often escape clause:

⋄ arm’s-length comparison: replacement of internal debt by external

debt at same conditions possible?

⋄ if proof provided, no application of TC rules

• For EU member states: no discrimination of non-residents from other

EU countries (Lankhorst-Hohorst ruling by ECJ)

⋄ no TC rules for EU-resident companies (e.g., Spain, Portugal)

⋄ TC rules for non-resident and for resident companies alikeCES Lecture: The Case of Debt Shifting 79 Lecture 3: Limiting Factors

Dirk Schindler

Example: German TC rules until 2007

• Introduction of (first) TC rule in 1994

• Only applicable for foreign investors (inbound investment)

• No tax-deduction of interest expenses on internal debt, if:

⋄ (direct and indirect) investor’s share in German affiliate ≥ 25%

⋄ internal-debt-to-equity ratio > 3:1 (from 2001: 1.5:1)

→ Concept of fixed debt-to-equity ratio with safe harbor

• Preference for holding companies: safe harbor of 9:1 (from 2001: 3:1)

CES Lecture: The Case of Debt Shifting 80 Lecture 3: Limiting Factors

Dirk Schindler

• Holding company, if

⋄ restriction to providing financial services only, or

⋄ ownership share in total assets ≥ 75%

• Escape clause:

→ no application of TC rules if arm’s-length comparison successful

• Due to Lankhorst-Hohorst ruling of ECJ from 2004 on:

⋄ TC rules applying to foreign and domestic investors alike

⋄ abolition of preference for holding companies

⋄ introduction of tax threshold:

→ no TC rules if interest expenses < 250.000 e

CES Lecture: The Case of Debt Shifting 81 Lecture 3: Limiting Factors

Dirk Schindler

5.1.2 Non-specific Thin-capitalization Rules: Earnings-stripping

• Disqualifying interest deductions from taxable income if equity is not

adequate from “commercial perspective” (Austria)

• Restricting interest deductions of both internal and external debt, if

interest payments exceed defined threshold (Germany, USA)

• Qualifying interest payments above certain percentage of profits /

EBIDTA as taxable profit / dividends

CES Lecture: The Case of Debt Shifting 82 Lecture 3: Limiting Factors

Dirk Schindler

Example: German earnings-stripping rules since 2008

• In place (with minor corrections) since 2008: §4h EStG, §8a KStG

• Restricting tax-deductibility of external and internal debt

• Net interest expenses deductible from tax base until 30% of EBIDTA

• EBIDTA = earnings before interest, depreciation, taxes + amortization

• No deductibility of net interest expenses exceeding 30% of EBITA, but

potential deductibility in following years (‘interest carry-forward’)

⇒ Attempt to protect tax base against any kind of debt shifting

CES Lecture: The Case of Debt Shifting 83 Lecture 3: Limiting Factors

Dirk Schindler

• Exceptions

⋄ tax threshold of 3 million euro (rules apply to full amount of inte-

rest expenses, when threshold exceeded)

⋄ trust clause

∗ no application of earnings-stripping rules, if firm not part of a

corporate group/trust

⋄ escape clause

∗ no application of earnings-stripping rules, if affiliate’s debt-to-

asset ratio is equal to or less than group-wide leverage

∗ exceeding of not more than 2 percentage points harmless

CES Lecture: The Case of Debt Shifting 84 Lecture 3: Limiting Factors

Dirk Schindler

• Aims

⋄ limit revenue losses from international debt shifting

⋄ exempt small enterprises

⋄ no distortion in investment + debt financing by domestic creditors

• Problem

⋄ rules can bite in and foster liquidity crises

CES Lecture: The Case of Debt Shifting 85 Lecture 3: Limiting Factors

Dirk Schindler

5.2 Economic Effects of Thin-Capitalization Rules

5.2.1 Effects on Debt-to-asset Ratio

• TC rules aimed to curb internal debt-shifting

• Two possibilities:

⋄ TC rules strictly binding at level b̄Ii

→ introduction of upper bound (ceiling) for internal leverage

⋄ some leeway in working around TC rules, but tax avoidance beco-

mes more expensive

→ flexible internal leverage bIi , but increased costs of internal debt

CES Lecture: The Case of Debt Shifting 86 Lecture 3: Limiting Factors

Dirk Schindler

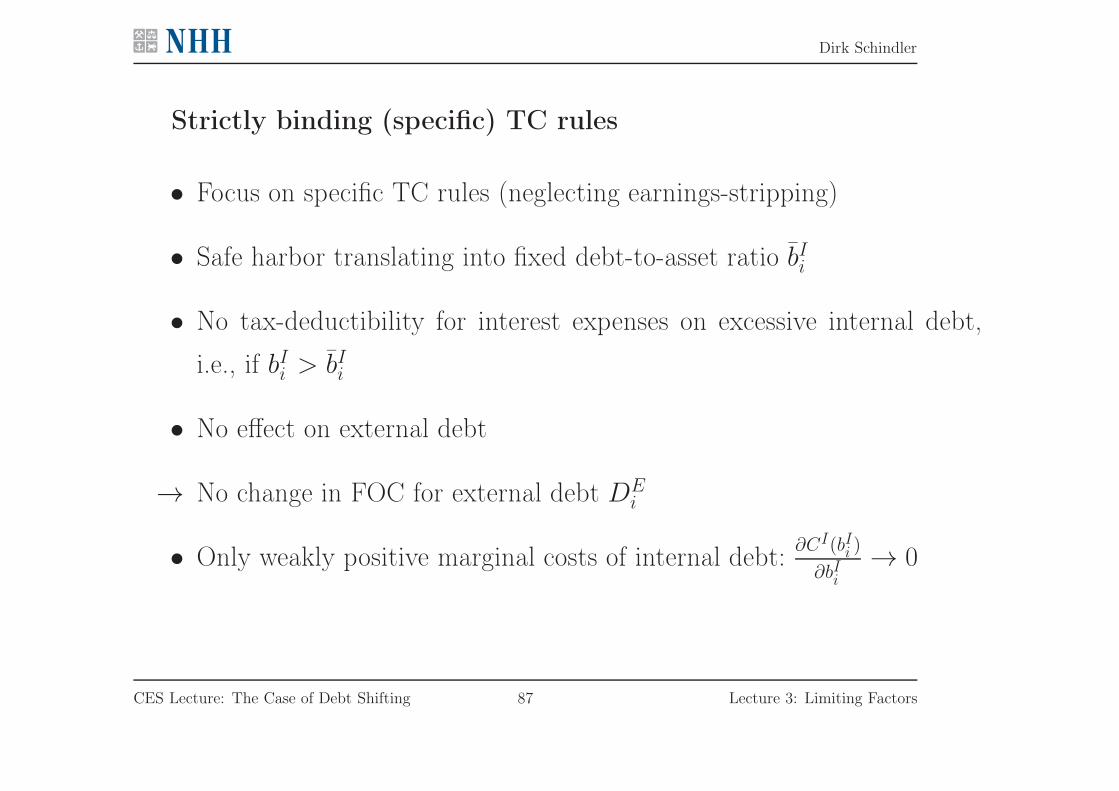

Strictly binding (specific) TC rules

• Focus on specific TC rules (neglecting earnings-stripping)

• Safe harbor translating into fixed debt-to-asset ratio b̄Ii

• No tax-deductibility for interest expenses on excessive internal debt,

i.e., if bIi > b̄Ii

• No effect on external debt

→ No change in FOC for external debt DEi

• Only weakly positive marginal costs of internal debt:∂CI(bIi )

∂bIi→ 0

CES Lecture: The Case of Debt Shifting 87 Lecture 3: Limiting Factors

Dirk Schindler

• Implications:

⋄ standard result carries over as long as optimal internal leverage

within safe harbor

⋄ if marginal costs of internal debt very low, corner solution:

positive debt tax shield drives internal leverage to threshold

⋄ no tax-deductibility above threshold turns tax shield negative:

no tax savings in affiliate, additional tax payments in internal bank

⇒ No internal debt beyond threshold b̄Ii

CES Lecture: The Case of Debt Shifting 88 Lecture 3: Limiting Factors

Dirk Schindler

Specific TC rules with leeway

• Definition of safe harbor, but leeway to work around TC rules

• Exceeding threshold b̄Ii possible, but costly

→ equivalent to positive shock on marginal costs of internal debt

• Define parameter αi as measure for tightness of TC rules in country i

• Redefine costs of internal debt as CI = CI(bIi , αi)

• Again: no effect on external debt (exception: earnings-stripping rules)

→ no change in FOC for external debt DEi

CES Lecture: The Case of Debt Shifting 89 Lecture 3: Limiting Factors

Dirk Schindler

• Adjusted FOC for internal debt:

(ti − λ) · r − (1− ti) ·∂CI(bIi , αi)

∂bIi= 0 ∀ i (5.1)

• From comparative-statics

∂bIi∂αi

= −∂2CI(bIi , αi)/(∂b

Ii∂αi)

∂2CI(bIi , αi)/(∂bIi )

2< 0, (5.2)

since∂2CI(bIi ,αi)

∂bIi ∂αi> 0 and

∂2CI(bIi ,αi)

(∂bIi )2 > 0

⇒ Tighter TC-rules reduce internal debt shifting

CES Lecture: The Case of Debt Shifting 90 Lecture 3: Limiting Factors

Dirk Schindler

• Implications

⋄ TC rules reduce optimal internal debt-to-asset ratio

⋄ no qualitative change in standard results

⋄ internal debt-to-asset ratio will exceed threshold b̄Ii

⋄ firms will incur higher tax-engineering costs

⋄ if∂2CI(bIi ,αi)

∂bIi ∂αi→ ∞ approach collapses to strictly binding TC rules

CES Lecture: The Case of Debt Shifting 91 Lecture 3: Limiting Factors

Dirk Schindler

5.2.2 Effects on Real Investment

• TC rules restrict tax savings from financial policy

• Reduced debt tax shields increase effective capital costs for MNCs:

r > r̃TCi = r − γTCi (ti)− ψTCi (ti, t1) > r̃i (5.3)

• Real capital investment less profitable (compare equation (3.17))

⇒ Effective TC rules reducing real investment in MNCs

CES Lecture: The Case of Debt Shifting 92 Lecture 3: Limiting Factors

Dirk Schindler

5.2.3 Effects on Tax Competition

• TC rules foster corporate tax competition (Haufler/Runkel, 2012)

• Weak TC rules alleviate effective tax burden on mobile capital (MNCs)

• Higher corporate taxation of immobile capital possible

• For harmonized corporate tax rates:

⋄ TC rules turn into main instrument for tax competition

⋄ lax TC regulation to attract MNCs and mobile capital

⋄ shift in tax competition efforts

⇒ Challenging sustainability of strict TC rules

→ at least, argument in favor of TC rules with some leeway

CES Lecture: The Case of Debt Shifting 93 Lecture 3: Limiting Factors

Dirk Schindler

5.3 Empirical Evidence on Thin-Capitalization Rules

• Mostly studies on German MNCs or on German rules (using Bundes-

bank MiDi data for both cases)

• (Almost) No studies of earnings-stripping rules since rules not opera-

tionalizable (and lack of data respectively)

• TC rules (rather) effective in reducing internal debt

• Effect on real investment ambiguous (not existing)

CES Lecture: The Case of Debt Shifting 94 Lecture 3: Limiting Factors

Dirk Schindler

5.3.1 German Inbound Foreign Direct Investment• Weichenrieder/Windischbauer (2008): MiDi data from 1996 to 2004

• Estimating effects of German TC rules on financing of German affiliates

of foreign MNCs

• Testing effect of reform in 2001: tightening TC rules

• Branches as control group: not affected by TC rules

→ controlling for time trend (and reductions in tax rates)

• Identification strategy:

⋄ split sample of corporations (branches) in affiliates with high/low

level of internal debt before 2001

⋄ compare effects between corporations and branches

CES Lecture: The Case of Debt Shifting 95 Lecture 3: Limiting Factors

Dirk Schindler

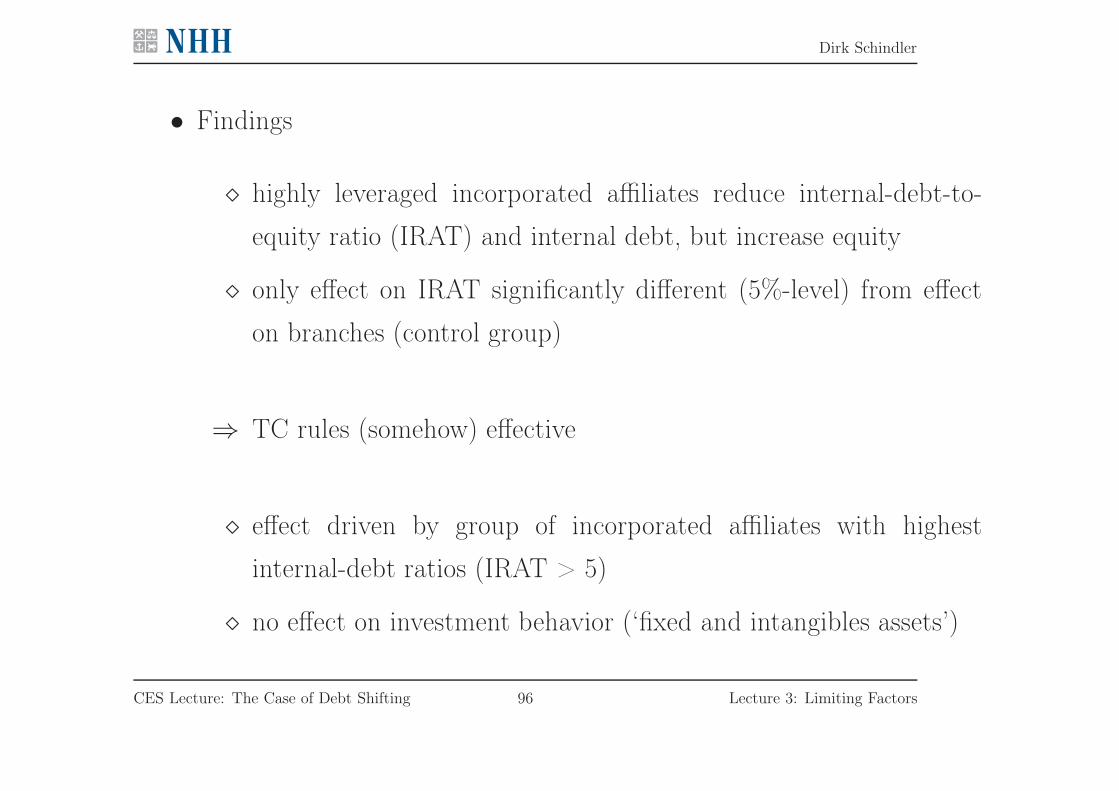

• Findings

⋄ highly leveraged incorporated affiliates reduce internal-debt-to-

equity ratio (IRAT) and internal debt, but increase equity

⋄ only effect on IRAT significantly different (5%-level) from effect

on branches (control group)

⇒ TC rules (somehow) effective

⋄ effect driven by group of incorporated affiliates with highest

internal-debt ratios (IRAT > 5)

⋄ no effect on investment behavior (‘fixed and intangibles assets’)

CES Lecture: The Case of Debt Shifting 96 Lecture 3: Limiting Factors

Dirk Schindler

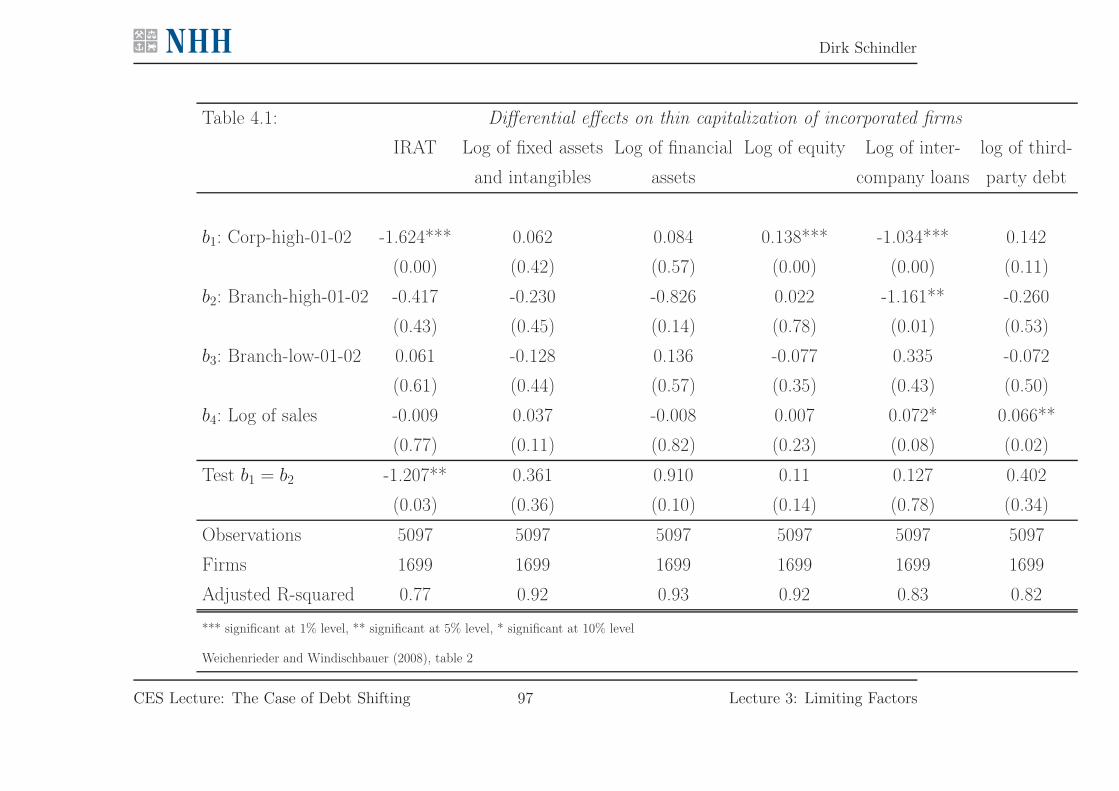

Table 4.1: Differential effects on thin capitalization of incorporated firms

IRAT Log of fixed assets Log of financial Log of equity Log of inter- log of third-

and intangibles assets company loans party debt

b1: Corp-high-01-02 -1.624*** 0.062 0.084 0.138*** -1.034*** 0.142

(0.00) (0.42) (0.57) (0.00) (0.00) (0.11)

b2: Branch-high-01-02 -0.417 -0.230 -0.826 0.022 -1.161** -0.260

(0.43) (0.45) (0.14) (0.78) (0.01) (0.53)

b3: Branch-low-01-02 0.061 -0.128 0.136 -0.077 0.335 -0.072

(0.61) (0.44) (0.57) (0.35) (0.43) (0.50)

b4: Log of sales -0.009 0.037 -0.008 0.007 0.072* 0.066**

(0.77) (0.11) (0.82) (0.23) (0.08) (0.02)

Test b1 = b2 -1.207** 0.361 0.910 0.11 0.127 0.402

(0.03) (0.36) (0.10) (0.14) (0.78) (0.34)

Observations 5097 5097 5097 5097 5097 5097

Firms 1699 1699 1699 1699 1699 1699

Adjusted R-squared 0.77 0.92 0.93 0.92 0.83 0.82

*** significant at 1% level, ** significant at 5% level, * significant at 10% level

Weichenrieder and Windischbauer (2008), table 2

CES Lecture: The Case of Debt Shifting 97 Lecture 3: Limiting Factors

Dirk Schindler

• Interpretation

⋄ Dourado/de la Feria (2008): TC rules effective at low costs since

no effect on real investment

⋄ alternative view: TC rules can be circumvented since no effect on

real investment

• Leeway: holding structure

⋄ evidence for holding structure and consolidation (‘Organschaft’)

⋄ holding facing higher safe harbor

⋄ evidence for increases of (holding) debt in groups with pronounced

leverage and binding TC rules

→ Avoiding TC rules on group level

CES Lecture: The Case of Debt Shifting 98 Lecture 3: Limiting Factors

Dirk Schindler

5.3.2 German Outbound Foreign Direct Investment

• Büttner et al. (2012): using Bundesbank MiDi data from 1996 to 2004

• Estimating effects of (foreign) TC rules on financing of foreign affiliates

of German MNCs

• Identification strategy:

⋄ cross-country and time variation in TC rules of 36 countries

⋄ dummy measuring effect of existence of TC rules on internal debt

⋄ estimating effect of tightness of TC rules by regressing on safe-

harbor threshold

⋄ splitting sample to analyze affiliates facing non-binding and bin-

ding TC rules separately

CES Lecture: The Case of Debt Shifting 99 Lecture 3: Limiting Factors

Dirk Schindler

• Findings (for interacted effects)

⋄ existence of TC rules (‘Rules’) reducing tax-rate effect on int. debt

⋄ lesser safe harbor (‘Tight’) diminishing tax sensitivity of int. debt

⋄ for threshold of 1.5:1 (‘Tight’ = 0.4) tax-rate effect reduced by

54% (i.e., −0.287·0.40.213

≈ 0.54)

⇒ TC rules (very) effective

⋄ however: using (affiliate-specific) fixed effects not allowing for crea-

ting new affiliates for holding purposes etc.

⋄ in WP-version (2008): strong negative effect on real investment

(‘fixed assets’)

CES Lecture: The Case of Debt Shifting 100 Lecture 3: Limiting Factors

Dirk Schindler

Table 4.2: Thin-capitalization Rules and Internal Debt

(1) (2) (3)

Statutory tax rate (STR) 0.214** 0.209** 0.213**

(0.095) (0.094) (0.093)

STR x Rule (TC rule exists) -0.049*

(0.028)

STR x Thight (safe harbor) -0.287**

(0.120)

R-squared 0.7643 0.7644 0.7645

Observations 42,950 42,950 42,950

Affiliate Fixed Effects yes yes yes

*** significant at 1% level, ** significant at 5% level, * significant at 10% level

Büttner et al. (2012), table 4

CES Lecture: The Case of Debt Shifting 101 Lecture 3: Limiting Factors

Dirk Schindler

• Interpretation

⋄ foreign TC rules more effective than German TC rules

⋄ potential problem: no information on loopholes and no possibility

to test for potential loopholes

⋄ binding TC rules costly: strong effect on investment behavior

→ confirmation of theoretical predictions

CES Lecture: The Case of Debt Shifting 102 Lecture 3: Limiting Factors

Dirk Schindler

5.4 Controlled-Foreign-Company Rules

5.4.1 General Features

• Affiliates in low-tax countries fostering tax avoidance

⋄ haven for valuable assets and internal debt

⋄ haven for license fees and patents

⋄ tax shelter for resulting passive incomes

• Controlled-foreign-company (CFC) rules to curb tax avoidance

⋄ denying low taxation in resident country of CFC

⋄ inclusion of passive income in tax base of parent on accrual basis

⇒ applying (higher) domestic tax rate on passive income (license fees,

patents, interest on internal debt) in foreign CFC

CES Lecture: The Case of Debt Shifting 103 Lecture 3: Limiting Factors

Dirk Schindler

• Problem: conflict with EU law

⋄ inclusion only in low-tax countries; imbalance to domestic or high-

tax affiliates

→ violation of freedom of establishment

(ECJ ruling 2006 on UK’s CFC rules in Schweppes-Cadbury case)

⋄ seeking tax advantage not sufficient for restricting freedom of esta-

blishment (‘no abuse’)

⋄ exception: ‘purely artificial structures’ (e.g., letterbox companies)

⋄ not yet tested: violation of freedom of movement of capital

⇒ Applicability of CFC rules (within EEA) legally rather impossible

CES Lecture: The Case of Debt Shifting 104 Lecture 3: Limiting Factors

Dirk Schindler

5.4.2 Example: German Controlled-foreign-company Rules

• Förster/Schmidtmann (2004); Ruf/Weichenrieder (2012); §§7-14 AStG

• German CFC rules biting, when following requirements fulfilled:

a) controlling ownership share

b) passive income

c) low taxation

a) Ownership share

⋄ ownership of 50% or more in shares or voting rights in foreign

corporation

⋄ no matter whether directly or indirectly held

CES Lecture: The Case of Debt Shifting 105 Lecture 3: Limiting Factors

Dirk Schindler

b) passive income

⋄ negative definition: whatever is not ‘qualified as active’

⋄ active income in particular income from production, agriculture

and dividends; but also banking, trade, services etc. as long as

main business partners are non-related third parties

⋄ capital income ‘active’ if proven that capital raised from unrelated

persons

c) low taxation

⋄ effective tax rate less than 25%

⋄ passive income calculated according to German tax law

→ effective tax burden decisive (tackling beneficial tax regimes)

CES Lecture: The Case of Debt Shifting 106 Lecture 3: Limiting Factors

Dirk Schindler

• Legal consequences

⋄ inclusion of passive income in tax base of German parent

⋄ no shelter from exemption principle or double tax treaties

⋄ tax exemption if passive income distributed as dividend later

⇒ Passive income (immediately) taxed at German tax rate

• German CFC rules and EU legislation

⋄ in principle, interfering with freedom of establishment and freedom

of movement of capital

⋄ conflict with EU law

→ CFC rules waived for affiliates residing in EEA countries

CES Lecture: The Case of Debt Shifting 107 Lecture 3: Limiting Factors

Dirk Schindler

5.4.3 Economic Effects of Controlled-foreign-company Rules

CFC rules with leeway

• CFC rules apply, but leeway to work around

• Increased (tax-engineering) costs of internal debt

→ equivalent to shock on marginal costs of internal debt (cf. TC rules)

• Define parameter γ as measure for CFC rule tightness (for parent p)

• Redefine costs of internal debt as CI = CI(bIi , γ)

• No effect on external debt

→ no change in FOC for external debt DEi

CES Lecture: The Case of Debt Shifting 108 Lecture 3: Limiting Factors

Dirk Schindler

• Adjusted FOC for internal debt:

(ti − λ) · r − (1− ti) ·∂CI(bIi , γ)

∂bIi= 0 ∀ i (5.4)

• From comparative-statics

∂bIi∂γ

= −∂2CI(bIi , γ)/(∂b

Ii∂γ)

∂2CI(bIi , γ)/(∂bIi )

2< 0, ∀ i (5.5)

since∂2CI(bIi ,γ)

∂bIi ∂γ> 0 and

∂2CI(bIi ,γ)

(∂bIi )2 > 0

⇒ Stricter CFC-rules reduce internal debt shifting

CES Lecture: The Case of Debt Shifting 109 Lecture 3: Limiting Factors

Dirk Schindler

• Implications

⋄ CFC rules reduce optimal internal debt-to-asset ratio

⋄ firms will incur higher tax-engineering costs

⋄ relevant for domestic MNCs only, but affecting financial policy in

all their affiliates worldwide (reduced internal tax savings)

⋄ no effect on domestic affiliates of foreign MNCs

⋄ less real investment in affected MNCs since higher capital costs

CES Lecture: The Case of Debt Shifting 110 Lecture 3: Limiting Factors

Dirk Schindler

Strictly binding CFC rules

• Define tp as tax rate of parent company

• CFC rules enforce tax rate tp in internal bank

⇒ Decrease of internal debt tax shield for all affiliates

⇒ Internal debt tax shield negative for affiliates with ti < tp

• No effect on external debt

→ no change in FOC for external debt DEi

• Additional constraint on internal debt: λ ≥ tp

CES Lecture: The Case of Debt Shifting 111 Lecture 3: Limiting Factors

Dirk Schindler

• Kuhn-Tucker problem for optimal capital structure (cf. equation (3.4))

maxDEi ,D

Ii

Πp =∑

i

{

(1− ti) · [F (Ki, Li)− wi · Li]− r ·Ki (5.6)

+ ti · r ·[

DEi +DI

i

]

− (1− ti)[

CE(bEi ) + CI(bIi )]

·Ki

}

− Cf(bf)

− λ∑

i

r ·DIi

− η (tp − λ)

s.t. bai =Dai

Ki, a = {E, I}, bf =

∑

iDEi

∑

iKi

CES Lecture: The Case of Debt Shifting 112 Lecture 3: Limiting Factors

Dirk Schindler

• FOC for internal debt DIi in country i:

∂Π

∂DIi

= (ti−λ) · r− (1− ti) ·∂CI(bIi )

∂bIi≤ 0 and λ ≥ tp ∀ i (5.7)

• Optimal to place internal bank in headquarters: mini λ = tp

• For affiliates with ti < tp: increased tax payments from internal debt

∂Π

∂DIi

< 0 ⇒ DIi = bIi = 0

• For ti ≥ tp: reduced internal debt tax shield

0 < bI∗i = CI(−1)(

ti − tp1− ti

· r

)

< CI(−1)(

ti − t11− ti

· r

)

⇒ Lower internal leverage in high-tax affiliates

CES Lecture: The Case of Debt Shifting 113 Lecture 3: Limiting Factors

Dirk Schindler

• Implications:

⋄ standard result collapsing for low-tax affiliates: bIi = 0 if ti ≤ tp

⋄ standard results qualitatively robust for affiliates with ti > tp

⋄ internal bank now located in headquarters

⇒ additional tax revenue for country p hosting MNC

CES Lecture: The Case of Debt Shifting 114 Lecture 3: Limiting Factors

Dirk Schindler

5.4.4 Empirical Evidence on Controlled-foreign-company Rules

• Ruf/Weichenrieder (2012): MiDi data from 1996 to 2006

• Estimating effects of German CFC rules on location of internal banks

of German MNCs

• Internal banks: conduit entities with positive net lending

• Testing effect of reform in 2003: tightening CFC rules for affiliates in

countries without activity clause in double tax treaty

• Control group: affiliates in countries with activity clause in tax treaty

• Hypotheses:

⋄ higher likelihood to host internal bank if no activity clause

⋄ effect vanishing after 2003

CES Lecture: The Case of Debt Shifting 115 Lecture 3: Limiting Factors

Dirk Schindler

• Findings for likelihood to own internal bank in country i

⋄ binding CFC rule (‘CFC-Dummy’) reducing likelihood by 45%

⋄ absence of activity clause (‘CFC-Dummy*NOACTI’) increasing

probability by 55%

⋄ activity-clause effect roughly nullified by reform in 2003

(‘CFC-Dummy*NOACTI*Post2003’)

⋄ caveat:

activity clause effects exclusively based on observations in Ireland

⇒ German CFC legislation effective in curbing tax avoidance

CES Lecture: The Case of Debt Shifting 116 Lecture 3: Limiting Factors

Dirk Schindler

Table 4.3: Locating Conduit Entities with Positive Net Lending

Panel logit OLS, linear probability

Corporate Tax Rate -1.664 -0.0527

(1.38) (0.055)

CFC-Dummy -0.659*** -0.0270***

(0.25) (0.0089)

CFC-Dummy*NOACTI 0.815** 0.0381***

(0.38) (0.014)

CFC-Dummy*NOACTI*Post2003 -1.066** -0.0577***

(0.52) (0.021)

Pseudo R-squared / R-squared 0.07 0.19

Observations 24,951 25,282

Affiliate Fixed Effects yes yes

Time Fixed Effects yes yes

*** significant at 1% level, ** significant at 5% level, * significant at 10% level

Ruf and Weichenrieder (2012), table 9

CES Lecture: The Case of Debt Shifting 117 Lecture 3: Limiting Factors

Dirk Schindler

Table 4.4: Conduit entities of German MNC with positive net lending by country (2006)

Country Lending to affiliated companies Number of conduit Statutory

less liabilites (in Mio. euro) entities tax rate

USA 53,824 58 0.4

UK 3,574 38 0.3

Switzerland 610 31 0.29

France 563 30 0.3333

The Netherlands 807 26 0.296

Belgium 2,607 12 0.3399

Austria 309 10 0.25

South Africa 82 9 0.396

Luxembourg 1,109 8 0.2963

Ireland 718 7 0.125

Spain 28 6 0.35

Sweden 71 6 0.28

Canada 405 5 0.361

Italy 226 5 0,3725

Cayman Islands 4,406 4 0

Malta 243 3 0.35

Sources: Ruf and Weichenrieder, 2012, table 6, MiDi database

CES Lecture: The Case of Debt Shifting 118 Lecture 3: Limiting Factors

Dirk Schindler

5.5 Comparison of Thin-capitalization and Controlled-

Foreign-Company Rules

• TC rules

⋄ restrict tax avoidance by (internal) debt shifting in country of

application

⋄ negatively affect domestic investment

⋄ affect domestic affiliates of both residing and foreign MNCs

⋄ low sustainability in tax-competition setting

CES Lecture: The Case of Debt Shifting 119 Lecture 3: Limiting Factors

Dirk Schindler

• CFC rules

⋄ restrict use of internal debt in all countries for domestic MNCs

⋄ affect only residing (domestic) MNCs / potentially reduced

competitiveness

⋄ negative effect on investment in all affiliates of domestic MNCs

⋄ potentially additional gains in tax revenue if internal bank located

in headquarters of MNC

⋄ sustainable under tax competition (!?)

CES Lecture: The Case of Debt Shifting 120 Lecture 3: Limiting Factors

Dirk Schindler

Result 5.1. Both thin-capitalization rules and controlled-foreign-company ru-

les are theoretically and empirically potential explanations for low tax sensi-

tivity of internal debt. Nevertheless, empirical studies provide evidence for

sufficient leeway to sustain all qualitative results on mechanisms of interna-

tional debt shifting.

CES Lecture: The Case of Debt Shifting 121 Lecture 3: Limiting Factors

Dirk Schindler

6 Other Limiting Factors

6.1 Minority Ownership

• Minority ownership: definition

⋄ joint ventures or diversified (minor) investors

⋄ MNC fully controlling its affiliates

→ total share of minority owners less than 50%

(cf., OECD-/IMF-definitions; Navaretti/Venables, 2004, ch. 1.1)

• Minority ownership in US-MNC (Desai et al., 2004, JFE)

⋄ wholly-owned affiliates amounting to 80.4% of all affiliates in 1997

⋄ share increased by 8.1 percentage points between 1982 and 1997

CES Lecture: The Case of Debt Shifting 122 Lecture 3: Limiting Factors

Dirk Schindler

• Minority ownership in German MNC (Hebous/Weichenrieder, 2010)

⋄ average share of partially-owned affiliates in number of all affiliates

in 2006: 20%

⋄ for emerging markets: decrease of partially-owned affiliates from

46% in 1996 to 30% in 2006

⋄ for OECD countries: decrease of partially-owned affiliates from

25% in 1996 to 18% in 2006

⋄ effects hold across all sectors

⇒ Strong and significant trend in reducing minority ownership in affiliates

CES Lecture: The Case of Debt Shifting 123 Lecture 3: Limiting Factors

Dirk Schindler

Tax-efficient capital structure

• Start out from model in chapter 3.1 (cf., Schindler/Schjelderup, 2012)

• For simplicity: no overall bankruptcy costs on parent level (Cf = 0)

→ no external debt-shifting

• Sum of minority shares in affiliate i given by Ji

• Cooperation on basis of cost savings CMi = CM

i (Ji) > 0

CES Lecture: The Case of Debt Shifting 124 Lecture 3: Limiting Factors

Dirk Schindler

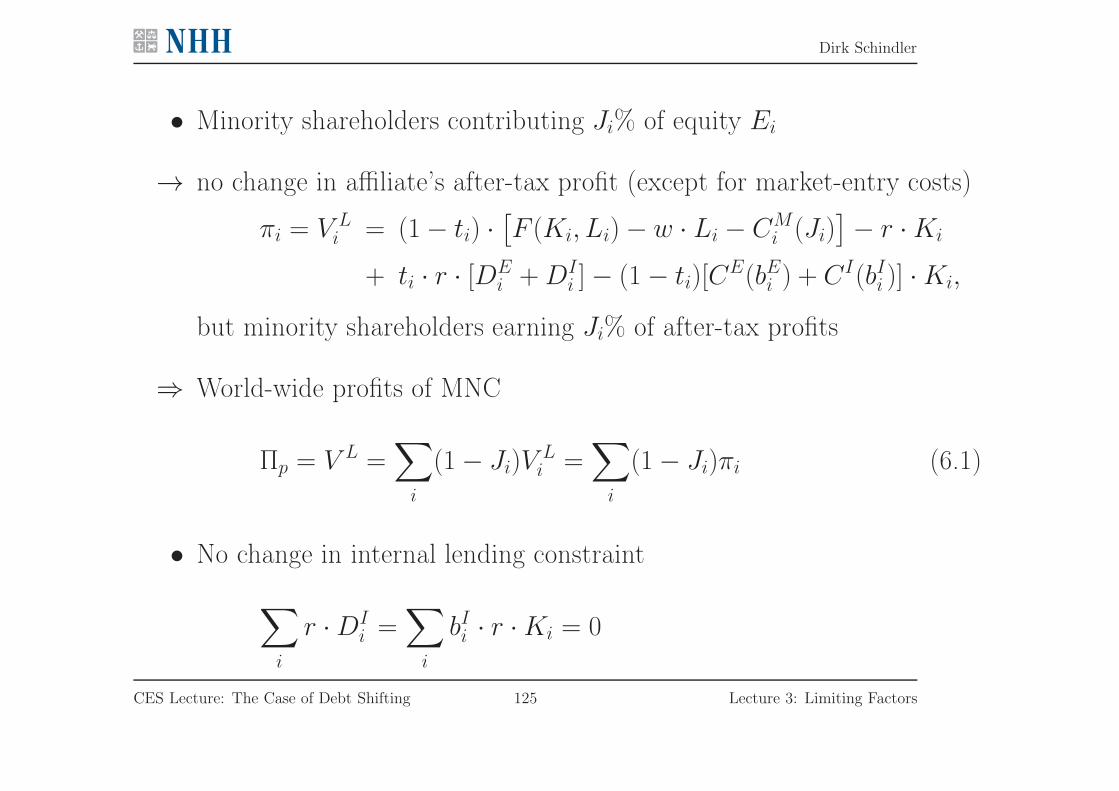

• Minority shareholders contributing Ji% of equity Ei

→ no change in affiliate’s after-tax profit (except for market-entry costs)

πi = V Li = (1− ti) ·

[

F (Ki, Li)− w · Li − CMi (Ji)

]

− r ·Ki

+ ti · r · [DEi +DI

i ]− (1− ti)[CE(bEi ) + CI(bIi )] ·Ki,

but minority shareholders earning Ji% of after-tax profits

⇒ World-wide profits of MNC

Πp = V L =∑

i

(1− Ji)VLi =

∑

i

(1− Ji)πi (6.1)

• No change in internal lending constraint

∑

i

r ·DIi =

∑

i

bIi · r ·Ki = 0

CES Lecture: The Case of Debt Shifting 125 Lecture 3: Limiting Factors

Dirk Schindler

• Optimal capital structure (for fixed inputs Ki, Li)

maxDEi ,D

Ii

Πp =∑

i

(1− Ji){

(1− ti)[

F (Ki, Li)− wi · Li − CMi (Ji)

]

− r ·Ki

+ ti · r ·[

DEi +DI

i

]

− (1− ti)[

CE(bEi ) + CI(bIi )]

·Ki

}

(6.2)

s.t.∑

i

r ·DIi = 0, (λ) and bai =

Dai

Ki, a = {E, I}

• Rearranging the FOC for external debt:

ti · r = (1− ti) ·∂CE(bEi )

∂bEi(6.3)

→ identical to basic model without minority shares

⇒ No influence on external debt decision (as long as Cf = 0)

CES Lecture: The Case of Debt Shifting 126 Lecture 3: Limiting Factors

Dirk Schindler

• Rearranged FOC for internal debt

∂CI(bIi )

∂bIi=

[(1− Ji) ti − λ] · r

(1− Ji)(1− ti)=ti −

λ1−Ji

1− ti≥ 0, ∀ i (6.4)

• Balancing marginal costs against effective internal debt tax shield

• Locate internal bank in affiliate with lowest effective tax rate

λ = mini(1− Ji)ti = te1 (by assumption, country 1)

→ not necessarily the lowest-taxed affiliate

CES Lecture: The Case of Debt Shifting 127 Lecture 3: Limiting Factors

Dirk Schindler

• Effect of minority ownership on level of internal debt

dbIidJi

= −te1 · r

CI ′′(bIi ) · (1− Ji)2 · (1− ti)< 0, i > 1 (6.5)

• Effect of minority ownership on tax sensitivity of internal debt

∂(

dbIidti

)

∂Ji= −

te1 · r

CI ′′(bIi ) · (1− Ji)2 · (1− ti)2< 0, i > 1 (6.6)

⇒ Internal debt less attractive for MNC

CES Lecture: The Case of Debt Shifting 128 Lecture 3: Limiting Factors

Dirk Schindler

• Intuition

⋄ minority shareholders fully profiting from tax savings in affiliate i

⋄ no sharing of tax payments on shifted interest in internal bank

→ cost externality benefitting minority shareholders

CES Lecture: The Case of Debt Shifting 129 Lecture 3: Limiting Factors

Dirk Schindler

• Opposite effect compared to transfer pricing (Kant, 1988, SEJ)

• Cost externality decreasing with effective tax rate te1 in internal bank

• Empirical evidence

⋄ effect of tax rate on internal debt 40% larger in wholly-owned affi-

liates compared to partially-owned ones (Büttner/Wamser, 2009)

⋄ significant reduction of tax sensitivity (e.g., Büttner/Wamser,

2009; Hebous/Weichenrieder, 2010; Desai et al., 2004, JFE)

→ not transfer-pricing conflicts, but cost externality should drive negative

effect (Schindler/Schjelderup, 2012)

CES Lecture: The Case of Debt Shifting 130 Lecture 3: Limiting Factors

Dirk Schindler

Result 6.1. Since they do not participate in the tax payments in the internal

bank, but profit from tax savings in borrowing affiliates, minority shareholders

cause a cost externality reducing the attractiveness of internal debt shifting for

MNCs. The resulting increase in effective capital costs constitutes an additio-

nal cost effect when determining the optimal ownership structure in affiliates.

CES Lecture: The Case of Debt Shifting 131 Lecture 3: Limiting Factors

Dirk Schindler

6.2 Combining Debt Shifting and Transfer Pricing

• Questions:

⋄ Interaction of transfer pricing and debt shifting?

⋄ Implications for tax sensitivity?

⋄ Effectivity of governmental regulation?

• Use standard model as in section 3.1

• Add interest-rate manipulation:

surcharge r̃i on internal debt, i.e., rIi ≡ r + r̃i

• See Schindler and Schjelderup (2013)

CES Lecture: The Case of Debt Shifting 132 Lecture 3: Limiting Factors

Dirk Schindler

• Internal lending constraint: total sum of internal loans zero

∑

i

r ·DIi =

∑

i

r · bIi ·Ki = 0

• Profit shifting in affiliate i: Pi = r̃i ·DIi = r̃i · b

Ii ·Ki

• Profit shifting constraint:

∑

i

Pi =∑

i

r̃i · bIi ·Ki = 0

• Specification and definition of concealment costs for internal debt and

transfer pricing crucial

CES Lecture: The Case of Debt Shifting 133 Lecture 3: Limiting Factors

Dirk Schindler

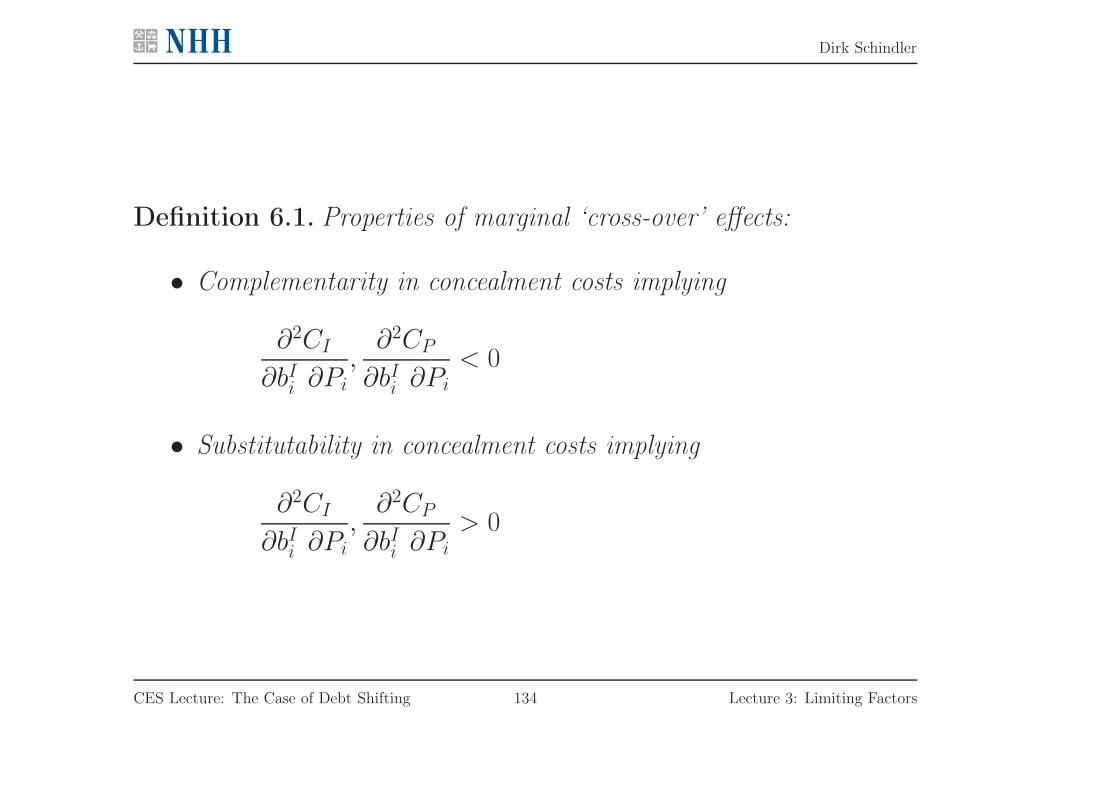

Definition 6.1. Properties of marginal ‘cross-over’ effects:

• Complementarity in concealment costs implying

∂2CI∂bIi ∂Pi

,∂2CP∂bIi ∂Pi

< 0

• Substitutability in concealment costs implying

∂2CI∂bIi ∂Pi

,∂2CP∂bIi ∂Pi

> 0

CES Lecture: The Case of Debt Shifting 134 Lecture 3: Limiting Factors

Dirk Schindler

Findings

• All interaction taking place via concealment cost functions

• Concealment cost complementarity ( ∂2CI∂bIi ∂Pi

< 0) increasing tax sen-

sitivity of both debt and profit shifting; that is dbIi/dti > 0 and

dPi/dti > 0.

• Concealment cost substitutability ( ∂2CI∂bIi ∂Pi

> 0) reducing tax sensitivity

of both debt and profit shifting and dbIi/dti ≷ 0 and dPi/dti ≷ 0.

CES Lecture: The Case of Debt Shifting 135 Lecture 3: Limiting Factors

Dirk Schindler

Intuition

• all else equal: higher tax rate increasing both internal debt and profit

shifting

• cost complementarity ( ∂2CI∂bIi ∂Pi

< 0): cost-mitigating ‘cross-over’ effect

⋄ economies of scale and scope reducing marginal costs of both tax-

engineering activities

• cost substitutab. ( ∂2CI∂bIi ∂Pi

> 0): additional costs from ‘cross-over’ effect

⋄ higher internal debt (profit shifting) increasing marginal costs of

profit shifting (internal debt)

CES Lecture: The Case of Debt Shifting 136 Lecture 3: Limiting Factors

Dirk Schindler

Effectiveness of Governmental Regulation

• Tightening TC rules or arm’s-length principle

⋄ win-win situation for cost complementarity: reducing debt shifting

and profit shifting

⋄ unintended effects for cost substitutability: either debt shifting or

profit shifting can increase

• Intuition

⋄ complement.: less debt shifting makes profit shift. more expensive

⋄ substitutab.: reducing one activity makes other strategy cheaper

CES Lecture: The Case of Debt Shifting 137 Lecture 3: Limiting Factors

Dirk Schindler

Result 6.2. The (main) interaction of debt shifting and transfer pricing is

driven by the concealment costs. Cost complementarity will amplify, cost sub-

stitutability will reduce the tax sensitivity of internal debt. On the other hand,

cost complementarity simplifies the regulation of profit shifting as a whole,

while cost substitutability can trigger unintended effects.

CES Lecture: The Case of Debt Shifting 138 Lecture 3: Limiting Factors

Dirk Schindler

6.3 A Step Back: Some Open Issues

• Very few theoretical literature on TC rules

→ maybe not promising enough (so, be careful)

• Empirical estimates of investment effects of TC rules

→ to date at most ambiguous or lacking

• Earnings-stripping rules

⋄ not really tested empirically / hard to get suitable data

⋄ some papers now coming: Blouin et al., Buslei/Simmler, Holzmann

CES Lecture: The Case of Debt Shifting 139 Lecture 3: Limiting Factors

Dirk Schindler

• CFC rules:

⋄ OECD proposal to foster CFC rules

⋄ theoretical literature dead silent about foundation/justification

• (Specific) Empirical test for externality result for minority ownership?

• Most interesting: shape of concealment cost functions

⋄ little theoretical work, no empirical evidence

⋄ obviously more knowledge relevant for policy design

⋄ could be helpful for interpreting (empirical) findings

CES Lecture: The Case of Debt Shifting 140 Lecture 3: Limiting Factors