tax avoidance and asymmetric cost behavior · asymmetric cost behavior (e.g., chen et al. 2012;...

TRANSCRIPT

Tax Avoidance and Asymmetric Cost Behavior

Shawn Xu

University of Wyoming

United States

Department of Accounting

Dept. 3275, 1000 E. University Ave.

Laramie, WY 82071-2000

United States

Phone: (307) 766-3919

Fax: (307) 766-4028

Kenneth Zheng

University of Wyoming

Department of Accounting

Dept. 3275, 1000 E. University Ave.

Laramie, WY 82071-2000

United States

Phone: (307) 766-3822

Fax: (307) 766-4028

June 2016

* We thank the research support provided by University of Wyoming College of Business.

Tax Avoidance and Asymmetric Cost Behavior

Abstract

This study examines the relationship between tax avoidance and asymmetric cost behavior. This

relationship arises due to direct economic benefits of cash savings from tax avoidance. On the one

hand, cash savings from tax avoidance may prompt managers to retain excess resources when

activity goes down. On the other hand, the cash savings may alleviate managers’ concerns about

adjustment costs due to expediting cost cuts in sales downturns. Using a large sample spanning the

1990-2013 period, we document a significantly negative relationship between tax avoidance,

proxied by cash effective tax rate, and sticky costs, suggesting tax avoidance is associated with

managers accelerating cost reductions in periods of declining activity. We also find that business

strategy plays a role in the relationship between tax avoidance and asymmetric cost behavior.

Specifically, relative to defenders, prospectors exhibit a more pronounced negative relation

between tax avoidance and cost stickiness. Further, we find that the negative relationship between

tax avoidance and asymmetric cost behavior is more pronounced for firms with more volatile cash

flows, consistent with cash savings from tax avoidance playing a more important role in managers’

cost reduction decisions for firms with more unpredictable cash flows. Our results are robust to

alternative tax avoidance measures, i.e., book-tax difference and permanent book-tax difference,

change in tax avoidance measures, or inclusion of main effects in the model. This study advances

the understanding of accounting researchers on the relationship between tax avoidance and

managers’ resource adjustment decisions.

Keywords: Tax avoidance, Asymmetric cost behavior, Resource adjustments, Business strategy.

1

Tax Avoidance and the Asymmetric Cost Behavior

1. Introduction

We examine the relation between tax avoidance and managers’ cost adjustment decisions.

Tax avoidance has a number of potential consequences. Extant studies have examined the relation

between tax avoidance and shareholder wealth (e.g., Desai and Dharmapala 2009; Kim et al. 2011).

Other studies have documented the impacts of a firm’s tax planning strategy and its related risk on

firm’s capital structure (e.g., Graham and Tucker 2006), cost of capital (e.g., Cook et al. 2015),

and cost of debt (e.g., Shevlin et al. 2013). Recent studies also find that aggressive tax planning

affects the transparency of a firm’s information environment (Balakrishnan et al. 2014) and is

related to aggressive financial reporting (Frank et al. 2009). While extant literature has primarily

focused on the impacts of tax avoidance on investors and creditors, this paper investigates whether

tax avoidance is associated with the firm’s resource allocation decisions, namely, asymmetric cost

behavior or “sticky costs.”

In their seminal work on cost behavior, Anderson, Banker and Janakiraman (2003)

(hereafter ABJ) find that on average costs increase more when activity rises than they decrease

when activity falls by an equivalent amount. They term this asymmetric cost behavior as “cost

stickiness,” which proposes an alternative view of cost behavior in contrast to the traditional

symmetric model where costs respond similarly to sales increases and sales decreases. The key to

understanding cost behavior resides in the fundamentals of cost behavior – resource adjustment

costs and deliberate managerial decisions (Banker and Byzalov 2014). When sales decrease,

managers must weigh the benefits from cutting unused resources against both current and future

resource adjustment costs, such as severance payments, disposal costs of capital equipment, and

2

subsequent hiring and training costs of new labor. Such adjustment costs will be particularly high

if the current sales downturn is temporary. Therefore, managers are less likely to cut unused

resources when the adjustment costs are high, giving rise to sticky costs.

ABJ and following studies have documented a variety of factors that affect asymmetric

cost behavior. For example, ABJ find that asset- and employee-intensive firms have a higher

degree of cost stickiness because these firms require more assets and employees to support their

operations. Recent studies have also documented that certain managerial incentives may influence

asymmetric cost behavior (e.g., Chen et al. 2012; Kama and Weiss 2013).

In this paper, we propose that tax avoidance is related to asymmetric cost behavior because

tax avoidance reduces a firm’s tax liability and improve its overall cash flow. On the one hand,

cash savings from tax avoidance may prompt managers to retain excess resources when activity

falls, leading to a higher degree of cost stickiness. On the other hand, the cash savings may alleviate

managers’ concerns about adjustment costs due to expediting cost cuts in sales downturns.

Consequently, managers may be more willing to bear the current and potential adjustment costs as

a result of cutting excess resources when activity falls, exhibiting a lower degree of cost stickiness.

To test our prediction, we follow prior literature (e.g., Frank et al. 2009; Cook et al. 2015)

and use cash effective tax rate (CETR) as our primary measure of tax avoidance. We adopt the

ABJ framework of asymmetric cost behavior and use SG&A costs to examine the cost behavior.

Controlling for known economic factors that affect cost stickiness, we find that when sales fall,

managers cut costs more aggressively if the firm engages in a higher level of tax avoidance. In

other words, tax avoidance reduces cost asymmetry.

We extend our analyses to investigate potential underlying factors that affect the negative

relation between tax avoidance and asymmetric cost behavior. First, we examine the role of a

3

firm’s business strategy in moderating the negative relation between tax avoidance and asymmetric

cost behavior. Recent literature has found that a firm’s strategic position plays a significant role in

determining both its tax avoidance strategy and its cost behavior. Higgins et al. (2015) document

that firms following an innovation strategy (i.e., prospectors) have higher levels of tax avoidance

than firms focusing on a cost leadership strategy (i.e., defenders) because relative to defenders,

prospectors possess more tax avoidance opportunities and are also more willing to tolerate the

risks associated with tax avoidance activities. Meanwhile, Banker, Flasher, and Zhang (2013) find

that prospectors exhibit a higher degree of cost stickiness because prospectors face higher

adjustment costs than defenders due to prospectors’ significant investments tailored to their

strategic needs. We find that the negative relation between tax avoidance and cost stickiness is

more pronounced for prospectors than for defenders, suggesting prospectors rely more heavily on

cash savings from tax avoidance in their resource reduction decisions.1

Second, we examine whether cash flow volatility influences the negative relationship

between tax avoidance and cost stickiness. The effect of cash savings from tax avoidance on

managers’ cost reduction decisions is likely more pronounced for firms with more unpredictable

cash flows from operations. For such firms, because operating cash flow is less reliable, managers

are likely to rely more on cash saving from tax avoidance to make resource allocation decisions.

Thus, tax savings from tax avoidance can better help managers achieve resource adjustment goals.

Therefore, we expect the relationship between tax avoidance and cost stickiness to be more

pronounced for firms with higher levels of cash flow volatility. We find that firms with higher cash

flow volatility exhibit a more negative relationship between tax avoidance and cost asymmetry.

1 Although seemingly different from the Banker, Flasher, and Zhang (2013) finding of generally stickier cost

behavior for prospector firms, our analysis and finding focus on the relationship between tax avoidance and cost

adjustment decisions and how business strategy affects this relation.

4

Further, we investigate two alternative explanations to our main finding. First, we examine

whether the negative relationship between CETR and cost stickiness is driven by managerial

financial reporting incentives. Prior studies find that when managers are faced with incentives to

avoid losses or earnings decreases, they will expedite resource cuts in order to increase earnings,

which diminishes sticky costs (Kama and Weiss 2013; Dierynck et al. 2012). In order to test

whether the negative relationship between tax avoidance (i.e., low levels of CETR) and cost

stickiness in our study is driven by firms meeting these earnings benchmarks, we partition our

sample based on whether incentives to avoid losses or earnings decreases exist. Results show that

our results are not concentrated in the subsample of firms with earnings targets incentives.

Next, we investigate whether the magnitude of the negative relationship between tax

avoidance and cost stickiness is affected by the severity of tax avoidance. We find that this negative

relationship becomes more significant as CETR increases. This evidence suggests that as tax

avoidance increases, financial uncertainty with future cash flows increases. Therefore, firms are

more likely to decrease sticky costs in order to improve their operational flexibility.

In robustness tests, we use book-tax difference (BTD) and permanent book-tax difference

(PERMDIFF) as alternative measures of tax avoidance. Results are qualitatively similar to those

in our main finding. Also, to alleviate endogeneity concerns, we replace tax avoidance level

measures with corresponding change measures and continue to find a negative relation between

change in tax avoidance and cost stickiness. Finally, our results are not sensitive to including main

effects of all interaction variables in the model to mitigate potential correlated omitted variables

problem.

This study makes several contributions to the literature. First, we provide direct evidence

of the role tax avoidance plays in shaping a real corporate decision, namely, asymmetric cost

5

behavior. Hanlon and Heitzman (2010) call for more research on the interactive effects of taxes

and financial accounting or managerial accounting on real corporate decisions. To our knowledge,

this is the first study to directly associate tax avoidance and corporate cost allocation decisions.

Our findings enrich the understanding of accounting researchers on how tax avoidance influences

firms’ cost allocation decisions.

Second, we add to the asymmetric cost behavior literature by documenting that tax

avoidance is negatively associated with cost stickiness. Prior literature has mainly focused on

explaining asymmetric cost behavior in the framework of adjustment costs or managerial

incentives (e.g., ABJ 2003; Banker, Byzalov, and Chen 2013; Chen et al. 2012; Dierynck et al.

2012; Kama and Weiss 2013). Our study extends this line of literature by demonstrating that

corporate tax avoidance may also play a significant role in shaping the firm’s cost behavior due to

cash savings generated through tax avoidance.

Finally, this study contributes to an emerging stream of research papers that integrates

research topics from different disciplines (e.g., Chen et al. 2012; Kama and Weiss 2013; Banker

et al. 2015; Chen et al. 2015; Higgins et al. 2015). Our findings advance our understanding on the

effect of tax avoidance on firms’ resource adjustment decisions.

The reminder of this paper is organized as follows. Section 2 reviews literature and

develops hypotheses. Section 3 describes our research design. Section 4 discusses our sample and

descriptive statistics. Section 5 presents empirical results and section 6 concludes.

2. Literature Review and Hypotheses Development

2.1 Consequences of tax avoidance

Following Hanlon and Heitzman (2010), we define tax avoidance broadly as “the reduction

of explicit taxes” (Hanlon and Heitzman 2010, p. 137). With respect to consequences of tax

6

avoidance, the literature has largely focused on its impacts on investors and creditors. Below, we

provide a brief review of this literature.

Traditionally, it is assumed that managers undertake tax avoidance activities to reduce

corporate tax obligations. Thus, from the investors’ perspective, tax avoidance is value enhancing,

and managers should be motivated to engage in such activities. In contrast, recent studies propose

alternative views suggesting that investors might perceive aggressive tax practices as value

decreasing due to the impact of tax aggressiveness on regulatory costs (Hanlon and Slemord 2009;

Cook et al. 2015; Goh et al. 2016), corporate transparency (e.g., Balakrishnan et al. 2014), and

agency conflicts (e.g., Desai and Dharmapala 2008). The two alternative perspectives on tax

avoidance have prompted several recent studies to investigate the stock market consequences of

tax avoidance activities. However, empirical findings so far are inconclusive (e.g., Desai and

Dharmapala 2009; Frank et al. 2009; Minnick et al. 2010; Koester 2011; Kim et al. 2011)

In addition, an emerging body of studies investigates the relation between tax avoidance

and cost of capital. Goh et al. (2013) find that less risky forms of tax avoidance are associated with

a lower cost of equity capital, consistent with their expectations that cash savings from tax

avoidance exceed the costs associated with increased information uncertainties. However, Cook

et al. (2015) document a nonlinear relation between tax avoidance and cost of capital. They find

that the relation becomes positive at higher levels of tax avoidance, implying an increased

uncertainty with the tax savings. Consistent with this argument, Hutchens and Rego (2012) find a

positive association between tax reserves, a riskier form of tax avoidance, and cost of equity capital.

This finding provides further evidence consistent with the notion that aggressive tax avoidance

increases a firm’s tax risk.

7

With respect to the impact of tax avoidance on firms’ capital structure and creditors, recent

studies have provided evidence in support of the traditional argument that tax avoidance and tax

sheltering are a substitute for interest deductions from debt financing (e.g., Graham and Tucker

2006; Richardson et al. 2014). Moreover, Shevlin et al. (2013) document that tax avoidance is

associated with higher bond offering yields due to the uncertainty of future cash flow and more

opaque reporting associated with higher levels of tax avoidance. Their argument regarding the

negative effect of tax avoidance is in line with Cook et al. (2015).

In addition to the literature on tax avoidance, another line of literature examines the effects

of taxes on various corporate decisions. Hanlon and Heitzman (2010) summarize three main areas

in their review of the literature – investment, capital structure, and organizational form. However,

few studies investigate the effects of taxes on corporate decisions other than those discussed above.

Hanlon and Heitzman (2010) call for more research to investigate the interactive effects of taxes

and financial accounting or managerial accounting on real corporate decisions. Our study fills the

gap by examining the impact of tax avoidance on corporate cost decisions.

2.2 Asymmetric cost behavior

Noreen and Soderstrom (1997) use data from hospitals located in the state of Washington

to investigate asymmetric cost behavior. Specifically, they find that costs respond to increases in

activity more rapidly than to decreases in activity. Using a large data set consisting of 7,629 firms

over 20 years, Anderson et al. (2003) document that on average selling, general, and administrative

(SG&A) costs increase by 0.55% for a 1% increase in sales but decrease by only 0.35% for a 1%

decrease in sales. They term this phenomenon “cost stickiness.” They argue that managers exercise

discretion and make deliberate cost adjustment decisions as to whether certain costs should be

retained or eliminated when demand falls.

8

ABJ’s cost stickiness is built on the rationale that firms must incur adjustments costs to

reduce committed resources during sales downturns and subsequently replace those resources

when demand is later restored. These adjustment costs include, but are not limited to, severance

pay for terminated employees, search and training costs for hiring employees in a later period, and

decreased employee morale. Cutting slack resources too rapidly when sales fall is likely to result

in higher adjustment costs if the decrease in demand is temporary. If these adjustment costs exceed

the costs of maintaining excess resources, then managers will likely keep the excess resources

instead of cutting them in periods of sales decreases.

Subsequent research extends this line of literature by building on ABJ’s fundamental

insight on asymmetric cost behavior. Studies have investigated cost asymmetry from the

adjustment cost perspective (Banker, Byzalov, and Chen 2013; Balakrishnan, Petersen, and

Soderstrom 2004), managerial expectations perspective (Banker, Byzalov, Ciftci, and Mashruwala

2014; Chen, Kama, and Lehavy 2015), agency problem perspective (Chen, Lu, and Sougiannis

2012), and economic incentives perspective (Kama and Weiss 2013; Dierynck, Landsman, and

Renders 2012). For example, Banker, Byzalov, and Chen (2013) use employment protection

legislation in different countries as a proxy for labor adjustment costs and find that the degree of

cost stickiness varies with the strictness of the country-level employment protection legislation

provisions.

Chen, Lu, and Sougiannia (2012) document that cost asymmetry increases in managers’

empire building incentives. Kama and Weiss (2013) find that managers expedite resource cuts in

periods of sales decreases in the presence of earnings targets in order to achieve cost reductions.

Similarly, Dierynck, Landman, and Renders (2012) document that managers of firms that report a

small profit conduct earnings management by firing employees who are relatively low cost to fire.

9

Because cost is a direct determinant of earnings, Banker and Byzalov (2014) call for research that

examines the implications of asymmetric cost behavior for topics at the intersection of both cost

and financial accounting.

2.3 Tax avoidance and asymmetric cost behavior

We propose that tax avoidance may play a significant role in asymmetric cost behavior due

to cash savings from tax avoidance. There is a countervailing effect of tax avoidance on firms’

cost allocation decisions. On the one hand, cash savings from tax avoidance may prompt managers

to retain excess resources when activity falls. ABJ find that on average firms tend to retain some

levels of excess resources in periods of sales decreases. In this scenario, cash savings from tax

avoidance will help the firm cover part of the costs of maintaining excess resources. If this is the

case, then we should observe a positive relationship between tax avoidance and cost stickiness.

On the other hand, cash savings from tax avoidance may alleviate managers’ concerns

about adjustment costs if they decide to cut unused resources when activity decreases. In this case,

the cash savings will help the firm cover part of the adjustment costs when demand is subsequently

restored. Thus, when activity falls, managers may choose to cut unutilized resources more rapidly

because of the financial flexibility resulting from tax avoidance, exhibiting in a negative relation

between tax avoidance and asymmetric cost behavior. Therefore, it is an empirical question as to

the direction of the relationship between tax avoidance and asymmetric cost behavior.2

Based on the above discussion, we state our main hypothesis in the null form:

H1: Tax avoidance is not related to asymmetric cost behavior.

2 We examine the association between tax avoidance and asymmetric cost behavior. We acknowledge that firms’

cost adjustment decisions may have an impact on the level of tax avoidance using CETR. Specifically, higher levels

of cost stickiness produce higher costs and lower operating income, potentially leading to lower income taxes (i.e.,

higher levels of tax avoidance). Thus, there is a mechanically positive association between cost stickiness and tax

avoidance.

10

H1 is built on the notion that both resource adjustment costs and economic benefits from

tax avoidance are significant. To support this argument, it is plausible to examine the effect of

resource adjustment costs and economic benefits from tax avoidance on the relationship between

tax avoidance and asymmetric cost behavior. If the adjustment cost concern is valid, then we

expect to find the magnitude of the association between tax avoidance and asymmetric cost

behavior to be different among firms faced with different levels of adjustment costs. If the

economic benefits from tax avoidance is valid, then we expect firms reaping more economic

benefits from tax avoidance to exhibit a more pronounced relationship between tax avoidance and

cost asymmetry. In order to further explore the effects of resource adjustment costs and economic

benefits from tax avoidance, we first look into a firm’s strategic environment. We then turn to the

impact of operating uncertainty on the main relationship.

2.3.1 Impact of business strategy on the relation between tax avoidance and sticky costs

A firm’s strategic position influences a broad range of its corporate decision making.

Recent literature has documented the impacts of business strategy on both tax avoidance and cost

behavior. Specifically, Higgins et al. (2015) find that firms following a cost leadership strategy

(i.e., defenders) exhibit lower level of tax avoidance than firms following an innovation strategy

(i.e., prospectors). They argue that prospectors have more tax-planning opportunities due to their

aggressive pursuit of new products and geographic markets. Moreover, the evidence is also

consistent with prospectors’ preference for risky projects relative to defenders as higher levels of

tax avoidance increase the uncertainty of future cash flow. Meanwhile, Banker, Flasher, and Zhang

(2013) argue that due to their pursuit of new products and technologies, prospectors3 invest heavily

in specialized resources, making it difficult to cut them when sales decrease (i.e., high potential

3 Banker, Flasher, and Zhang (2013) use “differentiator” for prospector and “cost leader” for defender. However, the

measurements are the same as those in Higgins et al. (2015).

11

adjustment costs). However, because defenders focus on operational excellence through efficient

operations, they are more flexible in cutting resources during downturns. Banker, Flasher, and

Zhang (2013) provide confirming evidence that prospectors exhibit greater cost stickiness than

defenders.

At first glance, the two studies cited above imply a positive relation between tax avoidance

and sticky costs for firms following an innovation strategy. However, to the extent that resource

adjustment costs play a role in determining cost stickiness for prospectors, engaging in high levels

of tax avoidance provides prospectors the financial leeway to adjust slack resources to a greater

extent. Further, prospectors likely operate with many specialized assets and have less flexibility to

adjust resources due to their operational structure. Thus, the adjustment cost concerns are likely

greater for prospectors. Consequently, if tax avoidance alleviates managers’ concerns about

adjustment costs, this effect will be more pronounced for prospectors. Accordingly, we propose

the following hypothesis:

H1a: The relation between tax avoidance and asymmetric cost behavior is more

pronounced for prospectors than for defenders.

2.3.2 Impact of cash flow uncertainty on the relation between tax avoidance and sticky costs

The other underlying assumption about the relationship between tax avoidance and sticky

costs is that the economic benefits of cash savings from tax avoidance are significant. For cash

savings from tax avoidance to play a more important role in managers’ cost adjustment decisions,

the company should have few other sources of cash to rely on. Therefore, we predict that cash

savings from tax avoidance becomes more significant in supporting managers’ resource cutting or

retention decisions if a firm faces more volatile cash flows from other sources. We propose the

following hypothesis:

12

H1b: The relation between tax avoidance and the asymmetric cost behavior is more

pronounced for firms with more volatile cash flows.

3. Research Design

3.1 Measures of tax avoidance

Our primary measure of tax avoidance is cash effective tax rate (CETR). Prior studies

indicate that CETR captures all tax activities that reduce cash tax paid during year (e.g., Dyreng et

al. 2008; Higgins et al. 2015). CETR is calculated as:

CETR = -1 × TXPD / (PI – SPI) (1)

where TXPD is cash tax paid; SPI is special items. We multiply the original rate by -1 so that tax

avoidance increases as the measure increases. We eliminate all observations with negative book

income and also restrict the value of this variable to fall between 0 and -1 (e.g., Higgins et al. 2015;

Cook et al. 2015).

3.2 Asymmetric cost behavior model

We extend the ABJ cost stickiness framework and investigate the impact of tax avoidance

on asymmetric cost behavior. A number of studies (Anderson et al. 2003; Chen et al. 2012; Banker

et al. 2014) examine cost asymmetry using a regression model with log change of SG&A costs as

the dependent variable and log change of sales as well as log change of sales multiplied by a

dummy variable for sales decrease as independent variables. Specifically, the estimated base

regression model in ABJ is

ΔlnSG&Ait = β0 + β1ΔlnSALEit + β2DECit × ΔlnSALEit + uit (2)

where ΔlnSG&Ait is the log change in SG&A costs, computed as log(SG&Ai,t/SG&Ai,t-1),

ΔlnSALEit is the log change in sales revenues, defined as log(SALEi,t/SALEi,t-1), and DECit is a

dummy variable which equals one if the firm experiences a sales decrease in year t and zero

13

otherwise. uit is an error term that has a zero mean and is independent of the explanatory variables.

In the base ABJ model (2), the coefficient β1 measures the percentage change in SG&A costs for

a 1% increase in sales, β2 measures the differential cost response to sales decrease relative to sales

increase, and the sum of β1 and β2 measures the percentage change in SG&A costs for a 1%

decrease in sales. A positive β1 and a negative β2 suggest that the decrease in SG&A costs in

response to sales decreases is less pronounced than the increase in SG&A costs in response to sales

increases, i.e., SG&A costs are sticky. Extant literature has focused on the sign of β2 to infer how

“sticky” or “anti-sticky” the cost is.

Following Banker, Byzalov, and Chen (2013), we augment the base ABJ model (2) by

using a hierarchical linear model in which the cost behavior derived from a level-1 model is defined

as a function of level-2 explanatory and control variables. Accordingly, we specify the slope

coefficients β1 and β2 in model (2) as

β1 = γ1 + γ2TAXAVOIDit + γ3ARETit + γ4EMPINTit + γ5ASINTit + ν1,i,t (2a)

β2 = γ6 + γ7TAXAVOIDit + γ8ARETit + γ9EMPINTit + γ10ASINTit + γ11SUC_DECit + ν2,i,t (2b)

where TAXAVOID is measured by CETR with a value between -1 and 0. ARET is the raw buy and

hold stock return in the year prior to the fiscal year end date. The effect of annual return ARET on

cost asymmetry is unclear. On the one hand, good stock performance may indicate that a decline

in demand is only temporary, thereby increasing managers’ expectation about future demand and

resulting in higher cost stickiness. On the other hand, firms with good stock performance may

expedite cost cuts in periods of sales decreases because they may be under greater pressure to

maintain the stock price run-up, hence reducing cost stickiness. EMPINT is computed as the

logarithm of the ratio of number of employees to sales revenue, ASINT is calculated as the

logarithm of the ratio of total assets to sales revenue, and SUC_DEC is a dummy variable that

14

captures whether there was a decrease in sales revenue in the previous year and takes the value of

one if revenue in year t-1 was less than that in year t-2, and zero otherwise. ν1,i,t and ν2,i,t are firm-

level random effects. The firm-level random effects capture the differences in cost behavior across

firms that are not accounted for by the explanatory variables in the model. By construction, ν1,i,t

and ν2,i,t have mean zero and are independent of the explanatory variables.

Combining equations (2) with (2a) and (2b), we obtain the following OLS regression model

to investigate the impact of tax avoidance on asymmetric cost behavior:

ΔlnSG&Ait = β0 + (γ1 + γ2TAXAVOIDit + γ3ARETit + γ4EMPINTit + γ5ASINTit) × ΔlnSALEit

+ (γ6 + γ7TAXAVOIDit + γ8ARETit + γ9EMPINTit + γ10ASINTit

+ γ11SUC_DECit) × DECit × ΔlnSALEit + uit (3)

where all variables are defined above. Hypothesis 1 in alternative form implies γ7 ≠ 0, i.e., tax

avoidance is associated with the degree of cost asymmetry. In our empirical analyses, all

continuous variables are mean-centered before they are included in regression analyses to mitigate

multicollinearity (Aiken and West 1991).

4. Sample and Descriptive Statistics

4.1 Sample selection

Our sample covers fiscal years 1990 – 2013 since 1990 is the earliest year used in the tax

avoidance literature. We first exclude firms in financial services and regulated industries with four-

digit SIC codes in 6000-6999 and 4900-4999 because their financial statement structure is

incompatible with those of other companies. Following Kama and Weiss (2013), we exclude firm-

year observations with nonpositive values for sales revenue, total assets, book value, and market

value. We also require share price at fiscal year-end to be greater than $1. We further remove

15

observations where sales revenue is smaller than SG&A costs or where requisite data for two

preceding years are missing.

Next, we obtain daily stock return data from CRSP and compute buy and hold annual stock

return with the daily return data over the 365 days preceding the fiscal year end date. We require

the number of trading days to be at least 250 in this 365-day period. Similar to other studies in the

asymmetric cost behavior literature, we trim all continuous variables at the 0.5% and 99.5%

percentiles to mitigate the effect of outliers. The sample size varies for each analysis due to the

specific measures used in each test.

4.2 Descriptive statistics

Table 1 displays the summary statistics of the main variables of interest for our sample.

Specifically, CETR has a mean (median) of -0.276 (-0.262) and a standard deviation of 0.215. The

firms in the sample has mean (median) annual sales of $2,289 million ($336 million) and mean

(median) SG&A costs of $449 million (66 million). A firm experiences a sales decrease in 20%

of all instances. The mean annual buy and hold return of the stocks in the sample is 22% percent

and the median firm achieves an annual return of 11%. Overall, the summary statistics in this study

are largely consistent with those documented in previous literature.

[Insert Table 1 about here]

5. Empirical Results

5.1 Effect of tax avoidance on asymmetric cost behavior

We estimate equation (3) to test the impact of tax avoidance on asymmetric cost behavior.

Table 2 presents the results. The coefficient on DECit×ΔlnSALEit×CETRit is 0.466 (t = 9.42),

suggesting all else equal, as the degree of tax avoidance increases, SG&A costs decrease more

rapidly relative to firms that engage in less tax avoidance. This result is consistent with the notion

16

that as a firm increases its tax avoidance activities, the increased cash savings from tax avoidance

reduces managers’ concerns regarding resources adjustment costs, allowing the firm to cut

unutilized resources more quickly in response to a sales decrease.

[Insert Table 2 about here]

The coefficients on control variables are largely consistent with those in prior studies (e.g.,

Chen et al. 2012). For instance, examining the coefficients on three-way interaction variables, the

coefficient on the interaction variable with ARET is positive, that on the interaction variable with

EMPINT is positive, and that on the interaction variable with ASINT is negative. The three-way

interaction variable with SUC_DEC is positive, consistent with the notion in ABJ that if a firm

experiences sales decreases in two years consecutively, then managers are more likely to expedite

the resource cost cuts because they are more likely to deem the decrease in demand permanent.

5.2 Effect of business strategy on the relation between tax avoidance and asymmetric cost

behavior

H1a predicts that the relation between tax avoidance and asymmetric cost behavior is more

pronounced for prospectors than for defenders. Following Miles and Snow (1978, 2003) and

Higgins et al. (2015), we categorize firms into three groups – defenders, analyzers, and prospectors

– based on a discrete STRATEGY composite measure computed using the following variables: (i)

the ratio of research and development to sales, (ii) the ratio of employees to sales, (iii) a historical

growth measure using one-year percentage change in sales, (iv) the ratio of marketing (SG&A) to

sales, (v) employee fluctuations (standard deviation of total employees), and (vi) capital intensity

calculated as net PP&E scaled by total assets. Each of the six measures is intended to capture

different elements of a firm’s business strategy.

17

All variables are computed using a rolling average of the corresponding ratio over the past

five years. We rank each of the six variables into quintiles within each industry-year. Observations

in the top quintile receive a score of 5, those in the 4th quintile receive a score of 4, and so on.

Observations in the bottom quintile receive a score of 1. Then, for each firm-year, we sum the

scores across the six variables to compute the STRATEGY score. Thus, the maximum STRATEGY

score a firm can receive in a year is 30 and the minimum is 6. If the STRATEGY score is between

24 and 30 (between 6 and 12), we consider the firm-year to be a prospector (defender) firm. Firm-

year observations with the STRATEGY score between 13 and 23 are analyzers and are regarded as

the control group.

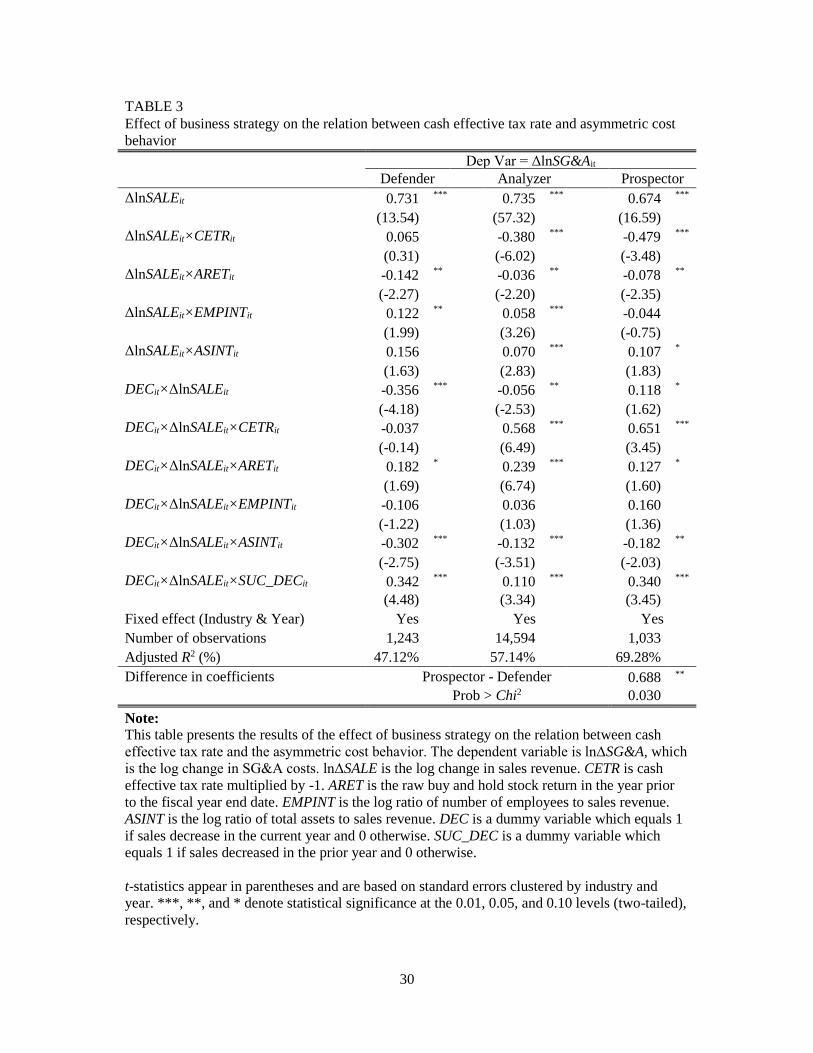

[Insert Table 3 about here]

We find evidence supporting the prediction that relative to defenders, prospectors exhibit

a stronger association between tax avoidance and asymmetric cost behavior. The results are

presented in table 3. Specifically, the coefficient on DEC×ΔlnSALE×CETR is -0.037 (t = 0.14) for

defenders, 0.568 (t = 6.49) for analyzers, and 0.651 (t = 3.45) for prospectors, suggesting that the

negative association between tax avoidance and cost asymmetry is more pronounced for

prospectors than for defenders. A test of difference in the coefficients between the prospector and

defender subsamples is statistically significant with a p-value of 0.03. Results support H1a that the

relation between tax avoidance and asymmetric cost behavior is more pronounced for prospectors

than for defenders.

5.3 Impact of cash flow volatility on the relation between tax avoidance and sticky costs

H1b predicts that the association between tax avoidance and asymmetric cost behavior is

stronger for firms with higher cash flow volatility. We measure cash flow volatility by standard

deviation of operating cash flow deflated by total assets over the past five-year period (e.g., Wasley

18

and Wu 2006). We then partition the sample into three groups and correspondingly name them as

based on the standard deviation measure.

[Insert Table 4 about here]

Table 4 presents the results. Comparing the low cash flow volatility group (low tercile)

with the high volatility group (high tercile), we find that the coefficient on DEC×ΔlnSALE×CETR

increases from 0.321 (t = 2.79) in the low volatility group to 0.735 (t = 9.53) in the high volatility

group. A test of difference in coefficients of this three-way interaction variable between the high

tercile and low tercile groups is significant at less than 1% level. This result is consistent with the

expectation that compared to firms with low cash flow volatility, firms with high cash flow

volatility exhibit a more pronounced relationship between tax avoidance and asymmetric cost

behavior, presumably because firms with high cash flow volatility rely more on cash savings from

tax avoidance in resource adjustments.

5.4 Additional analyses

5.4.1 Effect of incentives to avoid losses or earnings decreases on the relationship between tax

avoidance and asymmetric cost behavior

Recent studies have documented that managerial incentives to avoid losses or earnings

decreases diminishes cost stickiness (e.g., Dierynck, Landman, and Renders 2012; Kama and

Weiss 2013). For example, Kama and Weiss (2013) find that when managers face reporting

incentives to avoid losses or earnings decreases, they accelerate the downward adjustment of

unused resources when sales decrease in order to report higher income, resulting in a lower degree

of sticky costs. Because the raw CETR (i.e., before it is multiplied by -1) is a ratio of cash paid for

taxes to same-period pre-tax financial statement income, variations in the ratio can reflect either

tax avoidance activities through the numerator, or earnings management activities through the

19

denominator (Guenther, Krull and Williams 2014; Lev and Nissim 2004). In other words, a lower

level of the raw CETR (i.e., a higher level of tax avoidance) can be a result of more tax avoidance,

or a result of earnings inflation, or both. In fact, Guenther, Krull and Williams (2014) find that

CETRs are associated with both tax avoidance and earnings quality.

The above discussion suggests there exists a negative relation between tax avoidance and

cost stickiness due to managerial financial reporting incentives. On the one hand, managers reduce

costs aggressively as sales decrease to inflate earnings. On the other hand, the inflated earnings

drives down the raw CETR ratio (i.e., higher tax avoidance) even though the firm may not change

its tax avoidance activities at all. To the extent that firms that avoid losses or decreasing earnings

may manifest low CETRs, we test whether incentives to meet earnings targets drive our results.

Following Kama and Weiss (2012), we first partition our sample into two groups. The

“avoid loss” group contains all firms having annual earnings deflated by market value of equity at

prior year end being in the interval (0, 0.01). All other firms belong to the other group. We then

compare the coefficients on our interaction variable of interest between the two groups. If the

negative association between tax avoidance and asymmetric cost behavior in our study is driven

by managerial incentives to avoid losses, then we would observe the coefficient on

DEC×ΔlnSALE×CETR for the “avoid loss” group to be significantly higher in magnitude than the

coefficient for the benchmark group. Results presented in the first two columns of table 5 show

that the coefficient is 0.438 (0.474) for the “avoid loss” group (benchmark group), significant at

the 1% level. However, a test of difference between the two coefficient is not significant,

suggesting that the negative relationship between tax avoidance and asymmetric cost behavior is

not concentrated in the “avoid loss” group.

[Insert Table 5 about here]

20

Similarly, we test whether managers’ incentives to avoid earnings decreases drive out

results. Specifically, we classify a firm as having an incentive to avoid earnings decreases if the

change in annual earnings deflated by market value of equity at prior year end is in the interval (0,

0.01). We classify these firms in the “avoid earnings decrease” group and include all other firms

in the benchmark group. Results are shown in the last two columns of table 5. We find that the

coefficient on DEC×ΔlnSALE×CETR for the “avoid earnings decrease” group is negative and

insignificant, suggesting firms that have incentives to avoid earnings decreases exhibit no

association between tax avoidance and asymmetric cost behavior. In contrast, firms that do not

have incentives to avoid earnings decreases show a significantly positive coefficient on

DEC×ΔlnSALE×CETR. A test of difference in coefficients between the “avoid earnings decrease”

group and benchmark group is statistically significant, but in the wrong direction. Overall, the

empirical evidence does not support the possibility that the negative relationship between tax

avoidance and cost stickiness in our study is driven by managerial financial reporting incentives.

5.4.2 Tax avoidance, uncertainty, and asymmetric cost behavior

Cook et al. (2015) argue that investors’ perceptions of tax avoidance depend on the distance

between the observed level and the expected level of avoidance. As tax avoidance increases,

approaching the investors’ expected level, the cost of capital will decrease. However, incremental

tax avoidance beyond the optimal level may increase the uncertainty regarding future cash tax

savings due to the increased likelihood of a tax audit. Investors thus will perceive this uncertainty

unfavorable, increasing cost of capital. Accordingly, the authors find that tax avoidance decreases

cost of capital for low tax-avoidance firms. However, for firms with high levels of tax avoidance,

increasing tax avoidance increases cost of capital. Meanwhile, recent literature on cost structure

proposes that financial risk is a major factor that influences a firm’s cost structure choices. In

21

particular, Holzhacker et al. (2015) argue that firms with less elastic cost structures require higher

levels of sales to break even. Lower cost elasticity increases the likelihood of incurring losses.

Thus, it is more difficult for firms with lower cost elasticity to generate enough operating cash

flow to meet financial obligations. Higher financial risk (i.e., potential inability of the firm to meet

financial obligations) can intensify the situation due to its direct consequences, such as higher cost

of capital, and indirect consequences, such as loss of suppliers and customers. Therefore, firms

facing financial risk are more likely to explore options to increase the elasticity of their cost

structure.

The above discussion implies that as tax avoidance increases, financial uncertainty with

future cash flows increases. Therefore, firms are more likely to decrease sticky cost behavior in

order to improve their operational flexibility and increase the elasticity of their cost structure. To

explore this possibility, we first partition our sample into terciles according to our tax avoidance

measure. If the financial risk argument of tax avoidance is indeed valid, we would expect to

observe a stronger negative relation between tax avoidance and sticky costs as tax avoidance

increases.

[Insert Table 6 about here]

Table 6 shows that the negative impact of tax avoidance on cost stickiness becomes

stronger as the severity of tax avoidance increases. Specifically, from the lowest avoidance group

to the highest avoidance group, the coefficient increases from 0.328 (t = 3.80) for the low tax

avoidance tercile to 1.155 (t = 4.82) for the high tax avoidance tercile. The difference in

coefficients on the variable of interest is 0.827, significant at the 1% level. This result is consistent

with the above discussion that financial uncertainty associated with high levels of tax avoidance

22

makes firms more likely to decrease sticky cost behavior in order to improve their operational

flexibility and increase the elasticity of their cost structure.

5.5 Robustness tests

We conduct robustness tests to verify whether our results are sensitive to alternative

measures of tax avoidance, change in tax avoidance, or including main effects in an expanded

model. We run these robustness tests to ensure our results are not dependent on the choice of the

tax avoidance measure as well as to mitigate endogeneity issue and correlated omitted variables

problem.

First, we use two other measures of tax avoidance as proposed in the related literature (e.g.,

Desai and Dharmapala 2008; Frank et al. 2009; Goh et al. 2013) to test our main hypothesis. The

measures we adopt are book-tax difference (BTD) and permanent book-tax difference

(PERMDIFF). BTD is defined as the total difference between book and taxable income. It is

calculated as BTD = PI – (TXFED + TXFO)/STR, where PI is pretax income, TXFED is current

federal tax expense, TXFO is current foreign tax expense, and STR is the statutory tax rate.

Following Frank et al. (2009), PERMDIFF is defined as total book-tax differences less temporary

book-tax differences. As discussed in Frank et al. (2009), total book-tax differences contain

temporary book tax differences which may reflect earnings management through pre-tax accruals.

High levels of BTD may be driven by earnings management, rather than tax avoidance activities.

Therefore, permanent book-tax differences are better in capturing tax avoidance activities.

PERMDIFF is calculated as PERMDIFF = BTD – (TXDI/STR), where TXDI is total deferred tax

expense. Both the raw values of BTD and PERMDIFF are scaled by beginning-of-year total assets.

[Insert Table 7 about here]

23

Regression results using these alternative measures of tax avoidance are presented in table

7. We find that the coefficients on DEC×ΔlnSALE×TAXAVOID remain significantly positive when

the tax avoidance measure is BTD or PERMDIFF, suggesting our results are robust to the choice

of tax avoidance measure.

To the extent that a firm’s tax avoidance strategies and SG&A cost decisions may be

adopted by a firm endogenously, we repeat our analyses using change in the three tax avoidance

measures in place of the level measures. Results are presented in table 8. The coefficient on

DEC×ΔlnSALE×ΔTAXAVOID is positive and significant for all three change measures. To some

degree, these results mitigate the concern of endogeneity in our main findings.

[Insert Table 8 about here]

Finally, we include the main effects and two-way interactions with sales decrease dummy

in our main regression. To the extent that there may be a correlated omitted variables problem, the

model may be misspecified. The regression output, reported in table 9, still shows a significant

and positive coefficient on DEC×ΔlnSALE×CETR after the main effects and other two-way

interaction variables are included in the model. Overall, our findings are not sensitive to these

robustness tests.

[Insert Table 9 about here]

6. Conclusion

The study examines the association between tax avoidance and asymmetric cost behavior.

Prior studies (e.g., ABJ; Banker and Byzalov 2014) demonstrate that asymmetric cost behavior is

a phenomenon resulting from the deliberate managerial decision to retain unused resources when

there is a sales decrease, and this decision is influenced by resource adjustment costs associated

24

with downsizing. We propose that cash savings from tax avoidance may affect managers’ resource

adjustment decisions.

Using cash effective tax rate as our main measure of tax avoidance and adopting the ABJ

framework on asymmetric cost behavior, we document a significantly negative relationship

between tax avoidance and sticky costs. This result suggests that cash savings from tax avoidance

helps to alleviate mangers’ resource adjustment cost concerns in periods of sales decreases. Further

analyses reveal that a firm’s strategic position and operating cash flow volatility have a significant

influence on this main relationship. We do not find that managerial incentives to avoid losses or

earnings decreases drive the negative relationship between CETR and cost stickiness. However,

we do find evidence supporting the argument that the uncertainty of future cash flows associated

with more severe tax avoidance may exacerbate the negative relation between tax avoidance and

asymmetric cost behavior.

This study contributes to both the tax avoidance and sticky cost literatures. First, with

respect to the consequences of tax avoidance, the literature has largely focused on the impact of

tax avoidance on investors and creditors (Desai and Dharmapala 2009; Kim et al. 2011; Shevlin et

al. 2013; Cook et al. 2015). Second, our paper extends the literature on cost stickiness. This

literature has documented that certain economic factors and managerial characteristics can drive

asymmetric cost behavior. To our knowledge, this is the first study to examine the association

between a firm’s tax strategy and cost management – a real corporate decision. Finally, this paper

is among a handful of studies that endeavor to bring together research topics from different

disciplines (e.g., Chen et al. 2012; Kama and Weiss 2013).

25

References

Aiken, L. S., and West, S. G. 1991. Multiple regression: Testing and interpreting interactions.

Newbury Park, CA: Sage.

Anderson, M., Banker, R., and Janakiraman, S. 2003. Are selling, general, and administrative costs

“sticky”? Journal of Accounting Research 41(1): 47–63.

Balakrishnan, K., Blouin, J., and Guay, W. 2014. Does Tax Aggressiveness Reduce Corporate

Transparency? Working paper, University of Pennsylvania.

Balakrishnan, R., Petersen, M., and Soderstrom, N. 2004. Does capacity utilization affect the

“stickiness” of cost? Journal of Accounting, Auditing, and Finance 19(3): 283–299.

Banker, R., and Byzalov, D. 2014. Asymmetric cost behavior. Journal of Management Accounting

Research 26(2): 43–79.

Banker, R., Byzalov, D., and Chen, L. 2013. Employment protection legislation, adjustment costs

and cross-country differences in cost behavior. Journal of Accounting and Economics 55:

111–127.

Banker, R., Byzalov, D., Ciftci, M., and Mashruwala, R. 2014. The moderating effect of prior sales

changes on asymmetric cost behavior. Journal of Management Accounting Research 26(2):

221–242.

Banker, R., Flasher, R., and Zhang, D. 2013. Strategic positioning and asymmetric cost behavior.

Working Paper, Temple University, Pennsylvania State University, and Temple University.

Chen, J., Kama, I., and Lehavy, R. 2015. Management expectations and asymmetric cost behavior.

Working Paper, University of Illinois at Chicago, Tel Aviv University, and University of

Michigan.

Chen, C., Lu, H., and Sougiannis, T. 2012. The agency problem, corporate governance, and the

asymmetric behavior of selling, general, and administrative costs. Contemporary

Accounting Research 29(1): 252–282.

Cook, K. A., Moser, W. J., and Omer, T. 2015. Tax avoidance and ex ante cost of capital. Working

paper, Miami University of Ohio.

Demerjian, P., Lev, B., and McVay, S. 2012. Quantifying managerial ability: A new measure and

validity tests. Management Science 58(7): 1229–1248.

Demerjian, P., Lev, B., Lewis, M., and McVay, S. 2013. Managerial ability and Earnings Quality.

The Accounting Review 88(2): 463–498.

Desai, M. A., and Dharmapala, D. 2008. Tax and corporate governance: An economic approach.

MPI Studies on Intellectual Property, Competition and Tax Law 3: 13–30.

26

Desai, M. A., and Dharmapala, D. 2009. Corporate tax avoidance and firm value. Review of

Economics and Statistics 9(3): 537–546.

Dierynck, B., Landsman, W., and Renders, A. 2012. Do managerial incentives drive cost behavior?

Evidence about the role of zero earnings benchmarks for labor cost behavior in private

Belgian firm. The Accounting Review 87(4): 1219–1246.

Francis, B., Sun, X., and Wu, Q. 2013. Managerial ability and tax avoidance. Working paper,

Rensselaer Polytechnic Institute.

Frank, M., Lynch, L., and Rego, S. 2009. Tax reporting aggressiveness and its relation to

aggressive financial reporting. The Accounting Review 84: 467– 496.

Frank, M. M., Lynch, L., Rego, S., and Zhao, R. 2011. Are aggressive reporting practices

indicative of an aggressive corporate culture? Working paper, Indiana University.

Goh, B. W., Lee, J., Lim, C. Y., and Shevlin, T. 2013. The effect of corporate tax avoidance on

the cost of equity. Working paper, Singapore Management University.

Graham, J., and Tucker A. 2006. Tax shelters and corporate debt policy. Journal of Financial

Economics 81: 563–594.

Guenther, D., Krull, L., and Williams, B. 2014. Are “tax aggressive” firms just inflating earnings?

Working paper, University of Oregon.

Hanlon, M., and Slemrod, J. 2009. What does tax aggressiveness signal? Evidence from stock

price reactions to news about tax shelter involvement. Journal of Public Economics 93:

126–41.

Hanlon, M., Heitzman, S. 2010. A review of tax research. Journal of Accounting and Economics

50: 127–178.

Higgins, D., Omer, T., and Phillips, J. 2015. The influence of a firm’s business strategy on its tax

aggressiveness. Contemporary Accounting Research 32(2): 674–702.

Holzhacker, M., Krishnan, R., and Mahlendorf, M. 2015. The impact of changes in regulation on

cost behavior. Contemporary Accounting Research, forthcoming.

Hutchen, M. and Rego, S. 2015. Does greater tax risk lead to increased firm risk. Working paper,

Indiana University.

Kama, I., and Weiss, D. 2013. Do earnings targets and managerial incentives affect sticky costs?

Journal of Accounting Research 51(1): 201–224.

Kim, J. B., Li, Y., and Zhang, L. 2011. Corporate tax avoidance and stock price crash risk: Firm-

level analysis. Journal of Financial Economics 100: 639–662.

27

Koester, A. 2011. Investor value of tax avoidance through uncertain tax positions. Working paper,

Georgetown University.

Lev, B., Nissim, D. 2004. Taxable income, future earnings, and equity values. The Accounting

Review 79, 1039-1074.

Miles, R., and Snow, C. 1978. Organizational strategy, structure and process. New York:

McGraw-Hill.

Miles, R., and Snow, C. 2003. Organizational strategy, structure, and process. Stanford, CA:

Stanford University Press.

Minnick, K., and Noga, T. 2010. Do corporate governance characteristics influence tax

management? Journal of Corporate Finance 16: 703–718.

Noreen, E., and Soderstrom, N. 1997. The accuracy of proportional cost models: Evidence from

hospital service departments. Review of Accounting Studies 2: 89–114.

Rego, S., and Wilson R. 2012. Equity risk incentives and corporate tax aggressiveness. Journal of

Accounting Research 50(3): 775–810.

Richardson, G., Lanis, R., and Leung, S. 2014. Corporate tax aggressiveness, outside directors,

and debt policy: An empirical analysis. Journal of Corporate Finance 25: 107–121.

Shevlin, T., Urcan, O., and Vasvari, F. 2013. Corporate tax avoidance and public debt costs.

Working paper, University of California.

Wasley, C. E., and Wu J. S. 2006. Why do managers voluntarily issue cash flow forecasts? Journal

of Accounting Research 44(2): 389–429.

Wilson, R. 2009. An examination of corporate tax shelter participants. The Accounting Review 84:

969–999.

28

TABLE 1

Descriptive statistics

Mean Median Std. dev.

CETR -0.276 -0.262 0.215

SALE ($ million) 2289 336 9781

SG&A ($ million) 449 66 1886

DEC 0.20 0.00 0.40

ARET 0.22 0.11 0.63

EMPINT -5.26 -5.21 0.79

ASINT -0.13 -0.16 0.56

SUC_DEC 0.22 0.00 0.42

Note: This table presents the mean, median, and standard deviation of the main

variables used in the empirical analyses. CETR is cash effective tax rate

multiplied by -1. SALE is sales revenue. SG&A is selling, general, and

administrative costs. DEC is a dummy variable that equals 1 if sales

revenue in year t is smaller than that in year t–1 and 0 otherwise. ARET is

annual buy and hold return. EMPINT is the logarithm of the ratio of

number of employees to sales revenue. ASINT is the logarithm of the ratio

of total assets to sales revenue. Finally, SUC_DEC is a dummy variable

that equals 1 if sales revenue in year t–1 is less than that in year t–2 and 0

otherwise.

29

TABLE 2

Effect of cash effective tax rate on asymmetric cost behavior

Dep Var = ΔlnSG&Ait

ΔlnSALEit 0.763 ***

(95.03)

ΔlnSALEit×CETRit -0.282 ***

(-7.29)

ΔlnSALEit×ARETit -0.045 ***

(-5.10)

ΔlnSALEit×EMPINTit 0.052 ***

(5.19)

ΔlnSALEit×ASINTit -0.004

(-0.25)

DECit×ΔlnSALEit -0.109 ***

(-7.85)

DECit×ΔlnSALEit×CETRit 0.466 ***

(9.42)

DECit×ΔlnSALEit×ARETit 0.174 ***

(8.92)

DECit×ΔlnSALEit×EMPINTit 0.052 ***

(3.14)

DECit×ΔlnSALEit×ASINTit -0.127 ***

(-5.97)

DECit×ΔlnSALEit×SUC_DECit 0.142 ***

(7.82)

Fixed effect (Industry & Year) Yes

Number of observations 34,977

Adjusted R2 (%) 55.01%

Note:

This table presents the results of the effect of cash effective tax rate on cost stickiness. The

dependent variable is lnΔSG&A, which is the log change in SG&A costs. lnΔSALE is the log

change in sales revenue. CETR is cash effective tax rate multiplied by -1. ARET is the raw buy

and hold stock return in the year prior to the fiscal year end date. EMPINT is the log ratio of

number of employees to sales revenue. ASINT is the log ratio of total assets to sales revenue.

DEC is a dummy variable which equals 1 if sales decrease in the current year and 0 otherwise.

SUC_DEC is a dummy variable which equals 1 if sales decreased in the prior year and 0

otherwise.

t-statistics appear in parentheses and are based on standard errors clustered by industry and year.

***, **, and * denote statistical significance at the 0.01, 0.05, and 0.10 levels (two-tailed),

respectively.

30

TABLE 3

Effect of business strategy on the relation between cash effective tax rate and asymmetric cost

behavior

Dep Var = ΔlnSG&Ait

Defender Analyzer Prospector

ΔlnSALEit 0.731 *** 0.735 *** 0.674 ***

(13.54) (57.32) (16.59)

ΔlnSALEit×CETRit 0.065 -0.380 *** -0.479 ***

(0.31) (-6.02) (-3.48)

ΔlnSALEit×ARETit -0.142 ** -0.036 ** -0.078 **

(-2.27) (-2.20) (-2.35)

ΔlnSALEit×EMPINTit 0.122 ** 0.058 *** -0.044

(1.99) (3.26) (-0.75)

ΔlnSALEit×ASINTit 0.156 0.070 *** 0.107 *

(1.63) (2.83) (1.83)

DECit×ΔlnSALEit -0.356 *** -0.056 ** 0.118 *

(-4.18) (-2.53) (1.62)

DECit×ΔlnSALEit×CETRit -0.037 0.568 *** 0.651 ***

(-0.14) (6.49) (3.45)

DECit×ΔlnSALEit×ARETit 0.182 * 0.239 *** 0.127 *

(1.69) (6.74) (1.60)

DECit×ΔlnSALEit×EMPINTit -0.106 0.036 0.160

(-1.22) (1.03) (1.36)

DECit×ΔlnSALEit×ASINTit -0.302 *** -0.132 *** -0.182 **

(-2.75) (-3.51) (-2.03)

DECit×ΔlnSALEit×SUC_DECit 0.342 *** 0.110 *** 0.340 ***

(4.48) (3.34) (3.45)

Fixed effect (Industry & Year) Yes Yes Yes

Number of observations 1,243 14,594 1,033

Adjusted R2 (%) 47.12% 57.14% 69.28%

Difference in coefficients Prospector - Defender 0.688 **

Prob > Chi2 0.030

Note:

This table presents the results of the effect of business strategy on the relation between cash

effective tax rate and the asymmetric cost behavior. The dependent variable is lnΔSG&A, which

is the log change in SG&A costs. lnΔSALE is the log change in sales revenue. CETR is cash

effective tax rate multiplied by -1. ARET is the raw buy and hold stock return in the year prior

to the fiscal year end date. EMPINT is the log ratio of number of employees to sales revenue.

ASINT is the log ratio of total assets to sales revenue. DEC is a dummy variable which equals 1

if sales decrease in the current year and 0 otherwise. SUC_DEC is a dummy variable which

equals 1 if sales decreased in the prior year and 0 otherwise.

t-statistics appear in parentheses and are based on standard errors clustered by industry and

year. ***, **, and * denote statistical significance at the 0.01, 0.05, and 0.10 levels (two-tailed),

respectively.

31

TABLE 4

Effect of cash flow volitility on the relation between cash effective tax rate and asymmetric

cost behavior

Dep Var = ΔlnSG&Ait

Low Tercile Middle

Tercile High Tercile

ΔlnSALEit 0.778 *** 0.746 *** 0.699 ***

(52.28) (46.41) (44.58)

ΔlnSALEit×CETRit -0.149 * -0.196 ** -0.470 ***

(-1.68) (-2.36) (-7.79)

ΔlnSALEit×ARETit -0.063 ** -0.043 ** -0.068 ***

(-2.53) (-2.32) (-4.97)

ΔlnSALEit×EMPINTit 0.100 *** 0.067 *** 0.035 **

(4.77) (3.68) (2.13)

ΔlnSALEit×ASINTit -0.006 -0.060 ** 0.057 **

(-0.20) (-2.06) (2.39)

DECit×ΔlnSALEit -0.042 -0.099 *** -0.137 ***

(-1.37) (-3.58) (-4.84)

DECit×ΔlnSALEit×CETRit 0.321 *** 0.285 ** 0.735 ***

(2.79) (2.54) (9.53)

DECit×ΔlnSALEit×ARETit 0.163 *** 0.297 *** 0.181 ***

(2.91) (6.76) (5.62)

DECit×ΔlnSALEit×EMPINTit 0.016 0.071 ** 0.074 ***

(0.43) (2.06) (2.64)

DECit×ΔlnSALEit×ASINTit -0.101 ** -0.015 -0.197 ***

(-2.08) (-0.33) (-5.32)

DECit×ΔlnSALEit×SUC_DECit 0.066 * 0.102 ** 0.218 ***

(1.75) (2.53) (6.47)

Fixed effect (Industry & Year) Yes Yes Yes

Number of observations 8,552 9,369 9,567

Adjusted R2 (%) 57.04% 51.66% 50.76%

Difference in coefficients High Tercile - Low Tercile 0.414 ***

Prob > Chi2 0.002

Note:

This table presents the results of the effect of cash flow volatility on the relation between cash

effective tax rate and asymmetric cost behavior. The dependent variable is lnΔSG&A, which

is the log change in SG&A costs. lnΔSALE is the log change in sales revenue. CETR is cash

effective tax rate multiplied by -1. ARET is the raw buy and hold stock return in the year prior

to the fiscal year end date. EMPINT is the log ratio of number of employees to sales revenue.

ASINT is the log ratio of total assets to sales revenue. DEC is a dummy variable which equals

1 if sales decrease in the current year and 0 otherwise. SUC_DEC is a dummy variable which

equals 1 if sales decreased in the prior year and 0 otherwise.

t-statistics appear in parentheses and are based on standard errors clustered by industry and

year. ***, **, and * denote statistical significance at the 0.01, 0.05, and 0.10 levels (two-

tailed), respectively.

32

TABLE 5

Effect of incentives to meet earnings targets on the relation between cash effective tax rate and

asymmetric cost behavior

Dep Var = ΔlnSG&Ait

Avoid Loss Avoid Earnings Decrease

Yes No Yes No

ΔlnSALEit 0.701 *** 0.767 *** 0.846 *** 0.756 ***

(14.82) (95.63) (45.47) (88.56)

ΔlnSALEit×CETRit -0.129 -0.315 *** 0.186 -0.327 ***

(-1.43) (-7.72) (1.57) (-8.20)

ΔlnSALEit×ARETit 0.020 -0.056 *** -0.041 -0.038 ***

(0.65) (-5.66) (-1.21) (-4.17)

ΔlnSALEit×EMPINTit 0.092 * 0.048 *** 0.035 0.052 ***

(1.90) (4.82) (1.56) (4.99)

ΔlnSALEit×ASINTit 0.066 -0.011 0.012 -0.011

(1.23) (-0.73) (0.33) (-0.73)

DECit×ΔlnSALEit -0.029 -0.112 *** -0.108 ** -0.111 ***

(-0.38) (-7.94) (-2.16) (-7.54)

DECit×ΔlnSALEit×CETRit 0.438 *** 0.474 *** -0.300 0.520 ***

(3.30) (9.18) (-1.17) (10.33)

DECit×ΔlnSALEit×ARETit 0.089 0.189 *** 0.309 ** 0.163 ***

(1.31) (9.14) (2.13) (8.31)

DECit×ΔlnSALEit×EMPINTit -0.178 ** 0.063 *** 0.060 0.050 ***

(-2.02) (3.68) (0.69) (2.95)

DECit×ΔlnSALEit×ASINTit -0.314 *** -0.115 *** -0.138 -0.121 ***

(-3.79) (-5.16) (-1.25) (-5.47)

DECit×ΔlnSALEit×SUC_DECit 0.056 0.146 *** 0.068 0.147 ***

(0.73) (7.83) (0.81) (7.88)

Fixed effect (Industry & Year) Yes Yes Yes Yes

Number of observations 1,389 33,588 5,503 29,474

Adjusted R2 (%) 56.68% 55.20% 62.68% 54.54%

Difference in coefficients

Avoid - Not Avoid -0.036 -0.820 ***

Prob > Chi2 0.796 0.002

Note:

This table presents the results of an additional test that examines whether the relation between cash

effective tax rate and cost stickiness is driven by managerial incentives to meet earnings earnings targets.

The dependent variable is lnΔSG&A, which is the log change in SG&A costs. lnΔSALE is the log change

in sales revenue. CETR is cash effective tax rate multiplied by -1. ARET is the raw buy and hold stock

return in the year prior to the fiscal year end date. EMPINT is the log ratio of number of employees to

sales revenue. ASINT is the log ratio of total assets to sales revenue. DEC is a dummy variable which

equals 1 if sales decrease in the current year and 0 otherwise. SUC_DEC is a dummy variable which

equals 1 if sales decreased in the prior year and 0 otherwise.

t-statistics appear in parentheses and are based on standard errors clustered by industry and year. ***, **,

and * denote statistical significance at the 0.01, 0.05, and 0.10 levels (two-tailed), respectively.

33

TABLE 6

Effect of tax avoidance severity on the relation between cash effective tax rate and asymmetric

cost behavior

Dep Var = ΔlnSG&Ait

Low Tercile Middle Tercile High Tercile

ΔlnSALEit 0.746 *** 0.805 *** 0.899 ***

(39.38) (62.59) (28.04)

ΔlnSALEit×CETRit -0.165 ** -0.907 *** -0.864 ***

(-2.49) (-5.77) (-5.31)

ΔlnSALEit×ARETit -0.050 *** -0.039 ** -0.041 ***

(-2.63) (-2.19) (-3.41)

ΔlnSALEit×EMPINTit 0.069 *** 0.045 *** 0.044 ***

(3.74) (3.04) (2.61)

ΔlnSALEit×ASINTit -0.020 0.008 0.037

(-0.80) (0.32) (1.61)

DECit×ΔlnSALEit -0.050 -0.184 *** -0.291 ***

(-1.61) (-7.04) (-5.68)

DECit×ΔlnSALEit×CETRit 0.328 *** 0.515 ** 1.155 ***

(3.80) (2.27) (4.82)

DECit×ΔlnSALEit×ARETit 0.214 *** 0.157 *** 0.150 ***

(5.82) (3.49) (5.49)

DECit×ΔlnSALEit×EMPINTit 0.040 0.071 ** 0.040

(1.40) (2.36) (1.39)

DECit×ΔlnSALEit×ASINTit -0.112 *** -0.099 *** -0.175 ***

(-3.14) (-2.58) (-4.54)

DECit×ΔlnSALEit×SUC_DECit 0.122 *** 0.161 *** 0.132 ***

(4.04) (4.45) (4.30)

Fixed effect (Industry & Year) Yes Yes Yes

Number of observations 11,241 12,127 11,609

Adjusted R2 (%) 57.19% 56.96% 53.84%

Difference in coefficients High Tercile - Low Tercile 0.827 ***

Prob > Chi2 0.001

Note:

This table presents the results of the effect of cash flow volatility on the relation between cash effective

tax rate and asymmetric cost behavior. The dependent variable is lnΔSG&A, which is the log change in

SG&A costs. lnΔSALE is the log change in sales revenue. CETR is cash effective tax rate multiplied by -

1. ARET is the raw buy and hold stock return in the year prior to the fiscal year end date. EMPINT is the

log ratio of number of employees to sales revenue. ASINT is the log ratio of total assets to sales revenue.

DEC is a dummy variable which equals 1 if sales decrease in the current year and 0 otherwise.

SUC_DEC is a dummy variable which equals 1 if sales decreased in the prior year and 0 otherwise.

t-statistics appear in parentheses and are based on standard errors clustered by industry and year. ***,

**, and * denote statistical significance at the 0.01, 0.05, and 0.10 levels (two-tailed), respectively.

34

TABLE 7

Effect of tax avoidance on asymmetric cost behavior: Robustness test with alternative tax

avoidance measures

Dep Var = ΔlnSG&Ait

BTD PERMDIFF

ΔlnSALEit 0.733 *** 0.736 ***

(87.04) (86.90)

ΔlnSALEit×TAXAVOIDit -0.442 *** -0.288 ***

(-7.00) (-4.12)

ΔlnSALEit×ARETit -0.047 *** -0.047 ***

(-5.83) (-5.78)

ΔlnSALEit×EMPINTit 0.038 *** 0.042 ***

(3.82) (4.23)

ΔlnSALEit×ASINTit -0.026 ** -0.024 **

(-2.19) (-1.96)

DECit×ΔlnSALEit -0.180 *** -0.196 ***

(-12.73) (-13.89)

DECit×ΔlnSALEit×TAXAVOIDit 1.065 *** 0.761 ***

(11.57) (7.68)

DECit×ΔlnSALEit×ARETit 0.148 *** 0.150 ***

(9.23) (9.08)

DECit×ΔlnSALEit×EMPINTit 0.023 0.016

(1.56) (1.11)

DECit×ΔlnSALEit×ASINTit -0.163 *** -0.168 ***

(-9.50) (-9.68)

DECit×ΔlnSALEit×SUC_DECit 0.162 *** 0.164 ***

(10.72) (10.75)

Fixed effect (Industry & Year) Yes Yes

Number of observations 43,805 43,478

Adjusted R2 (%) 50.14% 49.98%

Note:

This table presents the results of the effect of tax avoidance on cost stickiness using alternative tax

avoidance measures. The dependent variable is lnΔSG&A, which is the log change in SG&A costs.

lnΔSALE is the log change in sales revenue. TAXAVOID is BTD or PERMDIFF, respectively. ARET is the

raw buy and hold stock return in the year prior to the fiscal year end date. EMPINT is the log ratio of

number of employees to sales revenue. ASINT is the log ratio of total assets to sales revenue. DEC is a

dummy variable which equals 1 if sales decrease in the current year and 0 otherwise. SUC_DEC is a

dummy variable which equals 1 if sales decreased in the prior year and 0 otherwise.

t-statistics appear in parentheses and are based on standard errors clustered by industry and year. ***, **,

and * denote statistical significance at the 0.01, 0.05, and 0.10 levels (two-tailed), respectively.

35

TABLE 8

Effect of tax avoidance on asymmetric cost behavior: Robustness test with change in tax

avoidance

Dep Var = ΔlnSG&Ait

ΔCETR ΔBTD ΔPERMDIFF

ΔlnSALEit 0.766 *** 0.741 *** 0.744 ***

(92.87) (89.77) (90.41)

ΔlnSALEit×ΔTAXAVOIDit -0.198 *** -0.766 *** -0.769 ***

(-5.57) (-12.59) (-13.11)

ΔlnSALEit×ARETit -0.053 *** -0.033 *** -0.035 ***

(-5.32) (-4.06) (-4.19)

ΔlnSALEit×EMPINTit 0.052 *** 0.025 ** 0.029 ***

(5.19) (2.55) (3.06)

ΔlnSALEit×ASINTit -0.008 -0.018 -0.019

(-0.56) (-1.55) (-1.61)

DECit×ΔlnSALEit -0.117 *** -0.194 *** -0.214 ***

(-8.06) (-13.66) (-15.02)

DECit×ΔlnSALEit×ΔTAXAVOIDit 0.402 *** 1.781 *** 1.570 ***

(8.72) (20.36) (17.50)

DECit×ΔlnSALEit×ARETit 0.182 *** 0.103 *** 0.107 ***

(8.02) (6.32) (6.30)

DECit×ΔlnSALEit×EMPINTit 0.048 *** 0.040 *** 0.032 **

(2.82) (2.75) (2.22)

DECit×ΔlnSALEit×ASINTit -0.098 *** -0.166 *** -0.168 ***

(-4.46) (-9.40) (-9.44)

DECit×ΔlnSALEit×SUC_DECit 0.127 *** 0.126 *** 0.141 ***

(6.61) (8.21) (9.10)

Fixed effect (Industry & Year) Yes Yes Yes

Number of observations 32,439 41,138 40,761

Adjusted R2 (%) 55.99% 51.83% 51.41%

Note:

This table presents the results of the effect of tax avoidance on cost stickiness. The dependent variable is

lnΔSG&A, which is the log change in SG&A costs. lnΔSALE is the log change in sales revenue.

ΔTAXAVOID is ΔCETR, ΔBTD, ΔPERMDIFF, or, respectively. ARET is the raw buy and hold stock

return in the year prior to the fiscal year end date. EMPINT is the log ratio of number of employees to sales

revenue. ASINT is the log ratio of total assets to sales revenue. DEC is a dummy variable which equals 1 if

sales decrease in the current year and 0 otherwise. SUC_DEC is a dummy variable which equals 1 if sales

decreased in the prior year and 0 otherwise.

t-statistics appear in parentheses and are based on standard errors clustered by industry and year. ***, **,

and * denote statistical significance at the 0.01, 0.05, and 0.10 levels (two-tailed), respectively.

36

TABLE 9

Effect of cash effective tax rate on asymmetric cost behavior - expanded model

with main effects

Dep Var = ΔlnSG&Ait

ΔlnSALEit 0.809 ***

(98.72)

ΔlnSALEit×CETRit -0.154 ***

(-4.20)

ΔlnSALEit×ARETit 0.006

(0.61)

ΔlnSALEit×EMPINTit 0.048 ***

(4.82)

ΔlnSALEit×ASINTit -0.030 **

(-2.19)

ΔlnSALEit×SUC_DECit -0.243 ***

(-12.09)

DECit×ΔlnSALEit -0.150 ***

(-6.32)

DECit×ΔlnSALEit×CETRit 0.247 ***

(3.27)

DECit×ΔlnSALEit×ARETit 0.081 **

(2.41)

DECit×ΔlnSALEit×EMPINTit 0.097 ***

(3.46)

DECit×ΔlnSALEit×ASINTit -0.066 *

(-1.85)

DECit×ΔlnSALEit×SUC_DECit 0.315 ***

(7.13)

DECit×CETRit 0.030 *

(1.95)

DECit×ARETit 0.009

(1.24)

DECit×EMPINTit 0.012 **

(2.33)

DECit×ASINTit -0.003

(-0.45)

DECit×SUC_DECit 0.015 **

(2.01)

DECit -0.005

(-0.97)

CETRit -0.059 ***

(-14.72)

ARETit -0.021 ***

(-12.72)

37

EMPINTit 0.000

(-0.22)

ASINTit 0.015 ***

(8.37)

SUC_DECit -0.036 ***

(-18.20)

Fixed effect (Industry & Year) Yes

Number of observations 34,977

Adjusted R2 (%) 57.13%

Note:

This table presents the results of the robustness test on the effect of tax

avoidance on cost stickiness by including in the model the main effects as well

as all two-way interactions. The dependent variable is lnΔSG&A, which is the

log change in SG&A costs. lnΔSALE is the log change in sales revenue. CETR

is cash effective tax rate multiplied by -1. ARET is the raw buy and hold stock

return in the year prior to the fiscal year end date. EMPINT is the log ratio of

number of employees to sales revenue. ASINT is the log ratio of total assets to

sales revenue. DEC is a dummy variable which equals 1 if sales decrease in the

current year and 0 otherwise. SUC_DEC is a dummy variable which equals 1 if

sales decreased in the prior year and 0 otherwise.

t-statistics appear in parentheses and are based on standard errors clustered by

industry and year. ***, **, and * denote statistical significance at the 0.01,

0.05, and 0.10 levels (two-tailed), respectively.